GOLD: $1323.20 DOWN $3.20 (COMEX TO COMEX CLOSINGS)

Silver: $16.33 UP 6 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1325.10

silver: $16.35

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1323.90

NY PRICING AT THE EXACT SAME TIME: $1324.10

LONDON SECOND GOLD FIX 10 AM: $1323.85

NY PRICING AT THE EXACT SAME TIME. $1323.10

end

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:152 NOTICE(S) FOR 15,200 OZ.

TOTAL NOTICES SO FAR 152 FOR 15200 OZ

For silver:

APRIL

10 NOTICE(S) FILED TODAY FOR

50,000 OZ/

Total number of notices filed so far this month: 10 for 50,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7884/OFFER $7954: down $47(morning)

Bitcoin: BID/ $7261/offer $7326: DOWN $623 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUMONGOUS SIZED 7712 contracts from 219,518 RISING TO 227,230 DESPITE YESTERDAY’S CONSIDERABLE 27 CENT DROP IN SILVER PRICING. SURPRISINGLY WE HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GIGANTIC SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2933 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2933 CONTRACTS. WITH THE TRANSFER OF 2933 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2933 CONTRACTS TRANSLATES INTO 14.665 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

47,334 CONTRACTS (FOR 21 TRADING DAYS TOTAL 47.334 CONTRACTS) OR 236.670 MILLION OZ: AVERAGE PER DAY: 2254 CONTRACTS OR 11.270 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 236.670 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 33.85% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 718.495 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED GAIN IN COMEX OI SILVER COMEX OF 7712 WITH THE 27 CENT FALL IN SILVER PRICE. HOWEVER, WE ALSO HAD ANOTHER HUGE SIZED EFP ISSUANCE OF 2933 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2933 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED AN ATMOSPHERIC 10,645 OI CONTRACTS i.e. 2933 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 7712 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 27 CENTS AND A CLOSING PRICE OF $16.27 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR THE NEXT APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.136 BILLION TO BE EXACT or 162% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 10 NOTICE(S) FOR 50,000 OZ OF SILVER

ANNOUNCEMENT: THE CME MADE AN ERROR AND INCORRECTLY STATED THAT THE EFP ISSUANCE WAS 1214. THE CORRECT TOTALS CAME AT 5 PM AND I WILL RECALCULATE

In gold, the open interest FELL BY A HUMONGOUS SIZED 21,523 CONTRACTS DOWN TO 508,167 ACCOMPANYING THE FAIR SIZED FALL IN PRICE IN YESTERDAY TRADING ( LOSS OF $16.30). AS WE ENTER THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN HUMONGOUS SIZED 24,732 CONTRACTS : APRIL SAW THE ISSUANCE OF 1552 CONTRACTS, JUNE SAW THE ISSUANCE OF 23,180 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 508,167. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS: 21,523 OI CONTRACTS DECREASED AT THE COMEX AND A HUMONGOUS SIZED 24,732 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 3,209 CONTRACTS OR 320,900 OZ =9.98 TONNES

YESTERDAY, WE HAD 16,331 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 238,518 CONTRACTS OR 23,851,800 OZ OR 741.89 TONNES (21 TRADING DAYS AND THUS AVERAGING: 11,358 EFP CONTRACTS PER TRADING DAY OR 1,135,800 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 21 TRADING DAYS IN TONNES: 741.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 741.89/2550 x 100% TONNES = 29.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2044.56 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX WITH THE CONSIDERABLE SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($16.30 LOSS). WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 24,732 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 24,732 EFP CONTRACTS ISSUED, WE HAD A GOOD NET GAIN IN OPEN INTEREST OF 3209 contracts ON THE TWO EXCHANGES:

24,732 CONTRACTS MOVE TO LONDON AND 21,523 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 9.98 TONNES).

we had: 152 notice(s) filed upon for 15,200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $3.20 : AND OUR USUAL RAID ON OPTIONS EXPIRY WEEK FINISHED: WE HAD NO CHANGE IN GOLD TONNAGE AT THE GLD

Inventory rests tonight: 846.12 tonnes.

SLV/

WITH SILVER UP 6 CENTS TODAY: OUR HEROES DECIDED TO ADD SOME SILVER: 943,000 OZ

/INVENTORY RESTS AT 319.012 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE BY A HUMONGOUS 7712 contracts from 219,7677 UP TO 227,230 (AND now A LOT CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787. THE PRICE OF SILVER ON THAT DAY: $17.89) DESPITE THE GOOD SIZED FALL IN PRICE OF SILVER (27 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2933 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 7712 CONTRACTS TO THE 2933 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 10,645 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 53.225 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE CONSIDERABLE FALL IN SILVER PRICING YESTERDAY (27 CENT FALL IN PRICE) . BUT WE ALSO HAD ANOTHER VERY STRONG SIZED 2933 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 38.24 POINTS OR 1.22% /Hang Sang CLOSED UP 70.85 POINTS OR 0.24% / The Nikkei closed UP 127.77/Australia’s all ordinaires CLOSED DOWN 0.51%/Chinese yuan (ONSHORE) closed UP at 6.2877/Oil DOWN to 64.29 dollars per barrel for WTI and 68.27 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2877 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2755 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY GOOD CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED STRONGER GLOBAL MARKETS/STRONGER CURRENCY )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

Meeting between the North and South is April 27.

( zerohedge)

the truth behind the deal: no gain to the uSA

( Global Macro Monitor)

b) REPORT ON JAPAN

3 c CHINA

i)Wilbur Ross confirms that the USA will initiate Chinese tariffs despite China warning that the USA will open Pandora’s Box. Maybe China will want to repatriate all the silver lent by them back to China

( zerohedge)

ii)China is advancing fast in technology. Now they have “skynet” which can compare 3 billion faces per second

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia expels 60 USA diplomats and orders the uSA to close the consulate in St Petersburg: exactly tit for tat

( zerohedge)

end

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

Humour story for you today:

VENEZUELA

Venezuela is trying to pay their Russian debt with the new cryptocurrency introduced by Venezuela

(courtesy Paraskova./OilPrice.com)

9. PHYSICAL MARKETS

i)A good commentary for you today: Ronan Manly states categorically that central banks do care about the gold price and enough to manipulate it constantly

( Ronan Manly/Bullionstar)

ii)Our good friend and ally Koos Jansen writes the the USA gold reserve audits lack credibility

(courtesy Koos Jansen/Bullionstar)

10. USA stories which will influence the price of gold/silver

i)USA DATA THIS MORNING

The following is a very important data point. Today the Bureau released real personal spending and it advanced by 0% over last month. In the last two months real personal spending is down .2% and thus by definition the savings rate rises. This does not bode well for the economy and will be a subtraction to GDP

( zerohedge)

ii)The following is the most important data entry points for the Fed. They are counting on inflation boiling over to cause wages and salaries to rise. It just is not happening

iii)Trump realizes that Amazon is paying little or no taxes and yet are putting thousands of retailers out of business. He must formulate a new tax policy to take care of this but it is a little too late( zerohedge)

iv)Soft data, Chicago PMI plunges to one year low. However inflation is surgin

( zerohedge)

v)Soft data U. of Michigan confidence at a 14 year high

( zerohedge)

vi)Barclay’s agrees to only a $2 billion dollar settlement on the RMBS case. The USA wanted more and Barclay’s refused to pay anything greater than 2 billion dollars

( zerohedge)

vii)SWAMP STORIES

a)Next on the firing line is David Shulkin. Trump fires him and nominates his personal physician, Dr Ronny Jackson

( zerohedge)

b)The Inspector General of the USA confirms that he will open a probe on the the FBI’s criminal warrant abuse that was used to spy on Trump

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:232,0745 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 466,085 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A STRONG 7712 CONTRACTS FROM 219,518 UP TO 227,230 DESPITE OUR 27 CENT FALL IN SILVER PRICING/ YESTERDAY’). ALSO,WE WERE ALSO INFORMED THAT WE HAD A VERY STRONG 2933 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2933. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE SURPRISINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 10,645 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 7712 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2933 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:10,645 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 1 contract FALLING TO 361 contracts.

Thus by definition, the amount of silver standing in this very poor non active delivery month of April is as follows:

361 contracts x 5000 oz per contract = 1,805,000 oz which is huge!!

The next big active delivery month for silver will be May and here the OI GAINED 5658 contracts UP to 154,870. The next big delivery month for silver is July and here the OI rose by 1203 contracts up to 37,572.

We had 10 notice(s) filed for 50,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for APRIL/GOLD

MARCH 29/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

152 notice(s)

15200 OZ

|

| No of oz to be served (notices) |

6237 contracts

(623,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

152 notices

15200 OZ

.4727 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 80 notices were issued from their client or customer account. The total of all issuance by all participants equates to 152 contract(s) of which 37 notices were stopped (received) by j.P. Morgan dealer and 28 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (152) x 100 oz or 15200 oz, to which we add the difference between the open interest for the front month of APRIL. (6397 contracts) minus the number of notices served upon today (152 x 100 oz per contract) equals 639,700 oz, the number of ounces standing in this active month of APRIL (19.897 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (152 x 100 oz or ounces + {(6397)OI for the front month minus the number of notices served upon today (152 x 100 oz )which equals 639,700 oz standing in this nonactive delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

728,793.532

oz

SCOTIA

DELAWARE

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,203,694.100 oz

HSBC

JPMorgan

|

| No of oz served today (contracts) |

10

CONTRACT(S

(50,000 OZ)

|

| No of oz to be served (notices) |

351 contracts

(1,755,000 oz)

|

| Total monthly oz silver served (contracts) | 10 contracts

(50,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: 604,132.000 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) into HSBC: 599,562.100 oz

total deposits today: 1,203,694.100 oz

we had 3 withdrawals from the customer account;

i) Scotia; 101,382.110 oz

ii) Out of Delaware: 16982.182 oz

iii) Out of CNT: 600,429.240 oz

total withdrawals; 728,793.532 oz

we had 1 adjustment

i) out of CNT: 531,519.850 oz was adjusted out of the dealer and this landed into the customer account and this will be used for settlement

total dealer silver: 58.8561 million

total dealer + customer silver: 260.510 million oz

The total number of notices filed today for the APRIL. contract month is represented by 10 contract(s) FOR 50,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 10 x 5,000 oz = 50,000 oz to which we add the difference between the open interest for the front month of April. (361) and the number of notices served upon today (10 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 10(notices served so far)x 5000 oz + OI for front month of April(361) -number of notices served upon today (10)x 5000 oz equals 1,805,000 oz of silver standing for the April contract month.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 79,958 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 104,018 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 104,018 CONTRACTS EQUATES TO 520 MILLION OZ OR 74.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.24% (MARCH 29/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.74% to NAV (March 29/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.24%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.74%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.13%: NAV 13.64/TRADING 13.22//DISCOUNT 3.13.

END

And now the Gold inventory at the GLD/

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 28/2018/ Inventory rests tonight at 846/12 tonnes

*IN LAST 352 TRADING DAYS: 94.92 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 302 TRADING DAYS: A NET 61.38 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 29/2018: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 943,000 OZ

Inventory 319.012 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.44

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.07%

libor 2.44 FOR 6 MONTHS/

GOLD LENDING RATE: .37%

XXXXXXXX

12 Month MM GOFO

+ 2.44%

LIBOR FOR 12 MONTH DURATION: 2.66

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.22

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

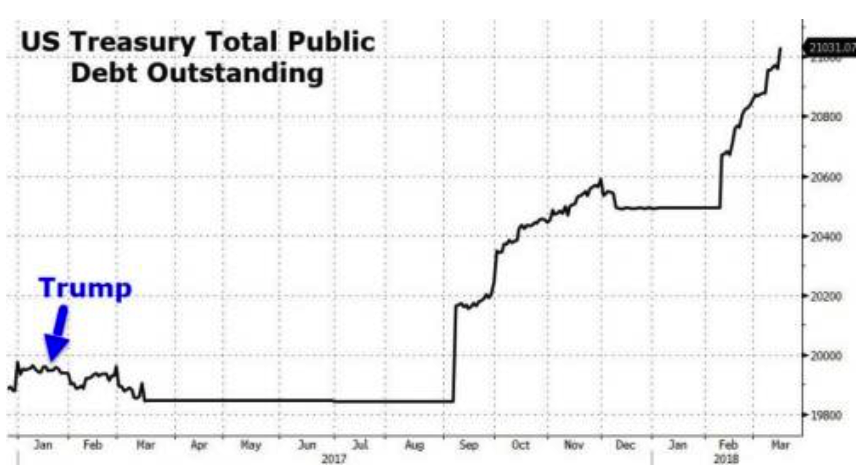

Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– US needs to borrow almost $300 billion this week alone

– This is the largest debt issuance since 2008 financial crisis

– Trump threatens trade war with its biggest creditor – China

– Bond auctions have seen weak demand due to large supply and trade war concerns

– $20 trillion mark reached in early September 2017; $1 trillion added in just 6 months

– US total national debt level now exceeds $21.05 trillion and is accelerating higher

– U.S. debt and dollar crisis coming which will propel gold higher (see chart)

This week the US has gone cap in hand to the bond markets to sell nearly $300 billion of US debt while at the same time threatening a trade war with its largest creditor China. This is despite it being the largest debt issuance since the 2008 financial crisis.

Trump has added $1 trillion in new debt in just over six months. This trillion dollar increase has only happened once before – at the height of the 2009 global financial crisis.

To give a sense of perspective of how huge $300bn issuance in one week is, it is the total amount of US debt when JFK was President. The U.S. national debt appears to be increasing parabolically and yet much of the media remains silent on the real risks this poses to the dollar, financial markets and the U.S. and global economy.

The U.S. government is in need of another $300 billion this week due to Trump’s grand tax and spend policies. The recent cut in taxes means there is reduced federal revenue and therefore the government must borrow more in order to make ends meet. The money will be used to refinance the current maturing debts and to finance new.

The sale will include $109 billion of coupon-bearing paper (debt featuring a maturity of more than a year) and $185 billion of bills.

Will Trump’s creditor China be interested?

Asking the market for $300bn when you’re picking a fight with some of the world’s biggest economic powers is bad timing to say the least. This is particularly the case when one of those economic powers is China, by far the largest holder of Treasuries.

Currently around 46% of US debt is owned by foreign entities, China’s holding accounts to $1.18 trillion of this. In light of Trump’s recent trade tariff placed on the Asian superpower, markets are unsure if US debt’s biggest fan will be coming to the debt waterhole for more.

When trade tariffs and wars were first mentioned China said it would respond to any measures by fighting a trade war ‘to the end’. China’s ambassador to the United States told Bloomberg ‘we are looking at all options’ when asked if the country would scale back purchases of US debt.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

This isn’t news that China may be losing interest in propping up the US economy. In early January Bloomberg reported that, ‘Senior government officials in Beijing reviewing the nation’s foreign-exchange holdings have recommended slowing or halting purchases of U.S. Treasuries.’

Given how heavily invested China is in just one class of US debt, it would not be surprising for the country to consider rebalancing their portfolio. Strategically now might be considered a wise time to do so.

Even if China doesn’t make an active decision to slow down its US debt purchases, it might be inevitable. Should the US be successful in reducing its trade deficit with the country then China will automatically have fewer dollars with which to purchase US Treasuries. Trump’s promises to ‘Make America Great Again’ may well lead to bond market panic and rising borrowing costs.

This sounds as though China holds the US by its private parts when it comes to debt. In many ways it does, but it could prove to be a zero sum game. It would not work in China’s interests to decide to suddenly sell US debt in large tranches as it would reduce the value of China’s dollar denominated assets.

More likely is that they greatly reduce purchases of U.S. debt and stop buying and instead buy the debt of sovereigns with a more sustainable debt profile such as Switzerland, Singapore, Norway and other creditor nations. They may also favour the debt and assets of nations that they have good trade, economic and foreign policy relations such as Russia.

Gold will become even more attractive to China and the People’s Bank of China (PBOC) and the Chinese accumulation of gold is likely to accelerate.

Is the market saturated with US debt?

Demand for US debt has certainly been lacklustre this week. A large part of this may be due to timing. The recent sabre-rattling from Trump in regard to trade war talk will have certainly put a dampener on demand.

However, the average-demand auctions have seen the 10-year yield curve flatten to a seven week low. Since February, the 10-year Treasury note yield has traveled in a tight trading range of 2.80% to 2.90%.

Treasury rates have been supported this year by concerns of the gap between US revenue and spending. The issuance of new debt this week will not be a one off, last week President Trump signed a $1.3 trillion spending bill that will increase spending requirements at a time when federal revenues are falling.

Bond buyers will likely demand a much higher interest rate to compensate for the increased sovereign risk in the U.S. and the country’s lack of desire and ability to rein in its debt-fuelled decisions.

The Committee for a Responsible Federal Budget (a fiscal watchdog group) warned yesterday the interest payments on US debt alone may quadruple to $1.05 billion by 2028 if current policies are not discontinued.

In February the country ran its biggest deficit in six years, of $215 billion. By as early as next year the annual budget deficit will exceed $1 trillion, according to the Committee for a Responsible Federal Budget.

The issuance of new debt will likely see inflation rise, which may hamper the Federal Reserve’s stated plans to step away from its carefully crafted timeline and force them to revert increase interest rates at a faster pace than scheduled.

Will this give the US a false sense of hope?

The danger with successful auctions (no matter where or how strong the demand was) is that it gives the seller the confidence that this is a good way to raise funding.

The US, like many western economies, has become a debt addict. It is completely unaware as to how it can grow and maintain its super power status without an economic model that is based on debt. It assumes it must grow by spending and consumption, rather than saving and production – two very different models.

In the words of Sovereign Man Simon Black, ‘Countries whose economic models are based on debt and consumption will suffer’.

When the US does suffer it will not be a contained event, the whole world will feel the pinch as we are so intertwined and dependent on the U.S., their policies and the dollar.

Trump has bankrupted many of his companies over the years and he appears to be accelerating the slow motion bankruptcy of the U.S. At the very least, he is set to create a U.S. debt and a dollar crisis which will again propel gold higher.

This risk underlines the importance of owning physical gold to protect against geo-political risks, stock and bond market bubbles and the continuing devaluation of the dollar and all fiat currencies.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related reading

Dow 20K, US Debt $20 Trillion, Trump and Gold

“Forgive Us Our Debts” – Debt Forgiveness Only Way To Prevent Global Depression

News and Commentary

Gold prices edge up from one-week low after steep fall (Reuters.com )

Asian Stocks Mixed; Japan Gains Ease as Yen Rises (Bloomberg.com)

Tech, Once Again, Weighs on Stocks as Dollar Jumps (Bloomberg.com)

U.S. pending home sales rise in February (Reuters.com)

U.S. Economic Growth Revised Higher on Spending, Inventories (Bloomberg.com)

Source: ZeroHedge.com

Will Brexit Trigger an Exodus of Banks From London? (Bloomberg.com)

U.K. Economic Confidence Drops to the Lowest Since 2016 (Bloomberg.com)

Trendline Broken: Similarities to 1929, 1987 and the Nikkei in 1990 Continue (Acting-Man.com)

Who Needs Wall Street When You Can Have A Monetary Unicorn? (DavidStockMansContraCorner.com)

Is The Fed Panicking: Yield Curve Tumbles To Fresh 11-Year Lows (ZeroHedge.com)

Gold Prices (LBMA AM)

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

21 Mar: USD 1,316.35, GBP 935.53 & EUR 1,071.64 per ounce

Silver Prices (LBMA)

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

21 Mar: USD 16.25, GBP 11.56 & EUR 13.23 per ounce

Recent Market Updates

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Crock Of Gold Hidden In Ireland? Happy Saint Patrick’s Day

– Buy Silver And Sell Gold Now

– Stephen Hawking – Doomsday Prophet’s Top Five Predictions

– Gold Cup At Cheltenham – Gold Is For Winners, Not For the Gamblers

– Hungary’s Gold Repatriation Adds To Growing Protest Against US Dollar Hegemony

– Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

The following exchange from Nicholas Biezanek to me is an essential read. In essence the banks are hiding the huge number of EFP’s through what is called a serial sub 14 day forward obligation. Anything less than 14 day forwards do not have to be included for monitoring by the Office of the Comptroller, Great Britain. I will endeavour to find out if this is exactly true. If so, then this is nothing but a criminal conspiracy to defraud by the bankers. Also note that all physical bars delivered upon at 2018 markings..nothing from the past..obviously bars are disappearing faster than a speeding bullet.

Nicholas to me:

|

10:03 AM (2 minutes ago) |

|

||

|

||||

Bill,Harvey,

I don’t know whether you have listened to Andrew Maguire’s interview with Greg Hunter but ,if not, then here are some key points.This interview is just to important to miss:

- Whilst the volume of gold EFPs for the 1st quarter ,ending tonight,will almost certainly exceed 2 000 tonnes,Andrew believes that these delivery obligations are rolled into serial forward contract obligations for nominal delivery in less than 14 days ,and hence avoid inclusion in the reports required by the Office of the Comptroller that seeks to monitor any liquidity squeeze on the ‘too big to fail’ banks .The logic for excluding obligations due in less than two weeks is not immediately obvious.Perhaps this delusional Comptroller believes that these criminals will at least have the integrity and risk management systems in place to accommodate all such short term and therefore,unavoidable, commitments.

- All physical gold deliveries out of the LBMA recently bear 2018 markings only-presumably all gold bars refined prior to this date are now ‘AWOL’

- The actual gold market fractional reserving ratio may be as high as 1000/1

- Whilst every time Andrew Maguire goes on air, the paper price of gold is trashed, correlation is not to be confused with causation. At 15.00 on the last Friday of every month (perhaps today as tomorrow is Good Friday), the BIS tries to window dress its trillion USD underwater derivatives book for reporting purposes.Therefore the paper gold price action of the last 24 hours was caste in stone.

- The bad news for the BIS, Cartel and LBMA is that the whole world is now waiting for this end of month market action and seeks to capitalize upon these waterfall paper gold price declines as unmissable windows of opportunity for physical gold acquisition.

- Many astute investors are also loading up on physical gold in order to ‘front run’ the imminent seriously large physical gold purchases for the ‘alternative currency’ -kinesis.com-that will go live in October 2018. If you are in paper gold only (including unallocated gold holdings) you will simply be ostracized from this ‘party to end all parties’ (If you haven’t listened to this interview at least twice, then you are not really serious about the gold market)

- Denis Gartman believes that as soon as the Venezuelan Central Bank has completed its disposal of (184?) tons of gold,an orderly gold market will return.Andrew also believes that it will be ‘business as usual’, but only until the impossible,unsustainable strain and tightness in the physical gold market causes a massive price ‘reset’,probably over a weekend, and it may be soon. (Harvey: I strongly believe that all of the Venezuelan gold has been sold long time ago as soon as Maduro got in trouble)

Whilst I have been immersed in GATA’s attempts to unravel the corruption,and manipulation of the physical gold market for a decade, I still find it difficult to get my mind around the magnitude of this imminent unraveling..

Regards

Nicholas

A good commentary for you today: Ronan Manly states categorically that central banks do care about the gold price and enough to manipulate it constantly

(courtesy Ronan Manly/Bullionstar)

Ronan Manly: Central banks care about the gold price enough to manipulate it

Submitted by cpowell on Wed, 2018-03-28 15:33. Section: Daily Dispatches

11:35p SSR Wednesday, March 28, 2018

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly today reviews some of the history of the longstanding policy of Western central banks to control the price of gold to protect their own currencies against competition from a free market in money. Manly’s analysis is headlined “Central Banks Care About the Gold Price Enough to Manipulate It” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/central-banks-care-gold-pr…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Our good friend and ally Koos Jansen writes the the USA gold reserve audits lack credibility

(courtesy Koos Jansen/Bullionstar)

Koos Jansen: U.S. gold reserve audits lack credibility

Submitted by cpowell on Thu, 2018-03-29 00:25. Section: Daily Dispatches

8:30a SST Thursday, March 29, 2018

Dear Friend of GATA and Gold:

Bullion Star’s Koos Jansen today details serious problems with what the U.S. government purports to be audits of the U.S. gold reserve. His analysis is headlined “Audits of U.S. Monetary Gold Severely Lack Credibility” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/audits-of-us-monetary-gold…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Barrick founder, Peter Munk dies at the age of 90

(courtesy Canadian Press/GATA)

Barrick Gold founder and philanthropist Peter Munk dies at 90

Submitted by cpowell on Thu, 2018-03-29 00:37. Section: Daily Dispatches

By Ian Bickis

Canadian Press

via The Globe and Mail, Toronto

Wednesday, March 28, 2018

Barrick Gold Corp.’s visionary founder Peter Munk, a man of lofty global ambitions who fulfilled them like few others, died Wednesday at the age of 90.

He racked up an impressive series of accomplishments in everything from custom stereos to tropical resorts, and established himself as one of Canada’s great entrepreneurs.

Mr. Munk will always be most renowned, however, as the founder and builder of one of the world’s largest gold mining empires while at the helm of Barrick Gold. It was there where he most displayed his willingness to take risks, spot overlooked opportunities, and challenge the status quo. …

… For the remainder of the report:

https://www.theglobeandmail.com/business/industry-news/energy-and-resour…

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2877 /shanghai bourse CLOSED UP 38.24 POINTS OR 1.22% / HANG SANG CLOSED UP 70.85 POINTS OR 0.24%

2. Nikkei closed UP 127.77 POINTS OR 0.61% /USA: YEN FALLS TO 106.51/

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 89.99/Euro RISES TO 1.2327

3b Japan 10 year bond yield: RISES TO . +.040/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.29 and Brent: 68.27

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.506%/Italian 10 yr bond yield DOWN to 1.821% /SPAIN 10 YR BOND YIELD DOWN TO 1.186%

3j Greek 10 year bond yield FALLS TO : 4.376?????????????????

3k Gold at $1325.50 silver at:16.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 57.56

3m oil into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.51 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9562 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1787 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.506%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.7680% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.003% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Whiplashed Global Stocks, US Futures Limp Higher Ahead Of Long Weekend

After three days of violent moves and sharp intraday reversals, in a week that feels far longer than just 4 days in, even equities appear exhausted today, and have entered the slow drift into the Easter break with volatility and volume far more subdued than earlier in the week courtesy of a slowdown in the newsflow, and as a result risk is once again bid, as it has been in the early part of most days this week… the question is will we get another late-day selloff.

Commenting on the recent risk moves, Deutsche Bank notes that markets seem to have spent the last 24 hours packing their bags and jetting off for the long weekend after an eventful last few weeks.

Aside from digesting a few more tech related stories, the lack of any material newsflow – the first time we can say that in a while – certainly seems to have helped. Indeed, by the end of trading last night the S&P 500 and Dow closed -0.29% and -0.04% respectively. The lack of any real direction throughout the session is best summed up by the fact that the S&P 500 passed between gains and losses by 37 times.

For some investors, especially the bulls, the coming holiday will be a relief following a roller coaster quarter in which stellar global equity gains gave way to a volatility blow up in February and a tech wreck. “We’ve done some damage with the correction and it’s going to take some time to repair,” Bob Doll, portfolio manager and chief equity strategist at Nuveen Asset Management, told Bloomberg TV. “Expect choppy, sideways volatility.”

The MSCI All-World Index of global stocks is set to end a 7-quarter winning streak – its longest such stretch of gains since 1997 – while global bonds are set for their first decline in currency neutral terms since 2016. The “melt-up” that sent the MSCI’s world share index up 8% in January has melted away, and now the Dow Jones, S&P 500, FTSE Nikkei and scores of other big markets are all down for the year.

“We have got to make sure (the market selloff) …is not too prolonged because the longer this goes the higher the chance it will start to affect the man on street,” said Head of Equities at London & Capital Roger Jones.

So heading into Easter weekend, European stocks are higher on Thursday after a mixed, if mostly higher session in Asia, as equity markets staggered toward the end of the most tumultuous quarter in years.

For the third consecutive day, S&P futures support at the 2,600 level, and we trading at session highs, 10 points higher than Wednesday’s close, around 2,618, while the VIX edged lower in early trading. “I think most of these markets are staring at the 200-day moving average on the S&P 500 to see if it breaks,” said Societe Generale’s Kit Juckes. As a reminder, the S&P 200DMA is at 2,588, so around 30 points lower.

Europe’s Stoxx 600 Index headed for a 3rd day of gains as most major country bourses traded quietly in the green. Automakers led the move higher after Renault and Nissan Motor were reported to be in talks to merge. Defensive sectors were in the red with focus on utilities and healthcare whilst broad gains are seen across all the other sectors. Sodexo (-14.1%) was the laggard this morning after reporting its earnings, dragging down Elior (-1.0%) and Compass (-3.6%) in the UK food catering segment. SwissRE (+2.9%) is leading the SMI after Softbank is said to be interested in building a 25% stake in the Co. for a USD 9.6bln deal. TomTom suffered losses of 6.3% after approaching Deutsche Bank for a potential sale of the whole firm or minority stake, but then denied calling for an adviser to seek potential buyers. Understandably, volumes were subdued, with many traders wrapping up ahead of a long weekend.

To be sure, the overnight quiet has been the exception lately, with the Stoxx 600 making gains or losses of more than 1% 16 times in the current quarter.

Earlier in Asia, equity markets traded indecisive as bourses failed to completely shrug-off the lacklustre lead from Wall Street. Helping the mood were media reports that Japan had sounded out North Korea’s government about a bilateral summit, and that Pyongyang had also discussed the possibility of a broader meeting with other global leaders. As a result, Japanese shares closed higher even as the yen retraced some of Wednesday’s slump, while stocks in China and Korea gained. ASX 200 (-0.5%) and Nikkei 225 (+0.6%) were mixed with Australia dragged lower by tech as well as recent weakness across commodities, while the Japanese benchmark was propped up for most the day by a softer currency. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+1.2%) were choppy in the midst of earnings season and with initial gains seen following reports of VAT reductions, although continued liquidity inaction by the PBoC and ongoing trade tensions with the US eventually weighed.

In overnight trade and tariff news, the China Ministry of Commerce said it hopes US drops unilateralism and protectionism, while it also hopes US takes steps and resolves conflict with China through dialogue. Furthermore, Mofcom added that US action on trade is like opening a Pandora’s box and that it sees spillover effects.

It was initially reported that US and are China in talks to shield soybeans from trade war, but this was later followed by conflicting overnight comments from the US Soybean Export Council that said China is still contemplating import curbs on US soybeans.

In FX, the dollar found support around fixing times, and after sliding earlier in the session is back to unchanged levels.

In a rather lackluster session, G-10 currencies remained confined to relatively tight ranges as traders await direction from tier-one data out of the U.S. due later Thursday. The USD/JPY holds close to 106.50 as yesterdays strong USD was unwound during Asian hours. A small pickup in activity into the Tokyo fix also saw EUR/USD and GBP/USD forced to session lows with most G-10 pairs then remaining in tight ranges.

Here are the overnight FX highlights from Bloomberg:

- EUR/USD was little changed, trading in a tight range, while the U.S. yield curve continued to bull-flatten

- The pound weakened amid continued month- and quarter-end flows

- USD/JPY declined as the pair’s surge Wednesday prompted investors to book profits ahead of the Easter holiday outside Japan

- Aussie recovered after dropping to a fresh year-to-date low of 0.7643 against the dollar, supported by gains in the price of iron ore

Treasuries also rose, if modestly, paced by core government bonds in Europe, with EGBs particularly quiet, showing a small outperformance of the European periphery, while benchmark yields on German government bonds crept back above 0.5% having been on a sharp slide for most of the month. Spanish yields meanwhile saw their biggest monthly fall since mid-2016. The 10-year U.S. Treasury yield was at 2.7662 percent after touching a near two-month low of 2.743 percent overnight amid the strains on Wall Street.

In commodities, WTI was poised to end its longest losing streak in almost a month, even as U.S. crude stockpiles resumed their expansion. Gold nudged lower, extending Wednesday’s plunge, while cryptos continued to slide overnight.

Bulletin Headline Summary from RanSquawk

- European bourses drifting higher heading into the long Easter weekend

- DXY stable around the 90.00 level

- Looking ahead, highlights include national German CPI, US personal income, PCE, Canadian GDP, Fed’s Harker

Market Snapshot

- S&P 500 futures up 0.4% to 2,618.50

- STOXX Europe 600 up 0.1% to 369.63

- MXAP up 0.02% to 171.83

- MXAPJ up 0.1% to 562.21

- Nikkei up 0.6% to 21,159.08

- Topix up 0.3% to 1,704.00

- Hang Seng Index up 0.2% to 30,093.38

- Shanghai Composite up 1.2% to 3,160.53

- Sensex down 0.6% to 32,968.68

- Australia S&P/ASX 200 down 0.5% to 5,759.37

- Kospi up 0.7% to 2,436.37

- German 10Y yield fell 0.3 bps to 0.5%

- Euro up 0.02% to $1.2310

- Italian 10Y yield fell 3.3 bps to 1.586%

- Spanish 10Y yield fell 1.0 bps to 1.203%

- Brent futures down 0.1% to $69.43/bbl

- Gold spot little changed at $1,324.33

- U.S. Dollar Index little changed at 90.11

Top Overnight News from Bloomberg

- North Korean leader Kim Jong Un and South Korean President Moon Jae-in will hold a summit on April 27, according to a South Korean Unification Ministry official. China’s commerce ministry said the nation is open to talks with the U.S. and it won’t submit to unilaterally coerced negotiations

- Japan will not get dragged into bilateral negotiations with the U.S. over steel and aluminum import tariffs, Finance Minister Taro Aso says in parliament Thursday

- Officials from the two Koreas are meeting Thursday on their heavily militarized border to discuss details of an upcoming summit between Kim Jong Un and South Korean President Moon Jae- in. The talks at Panmunjom could set the stage for a similar meeting between Kim and U.S. President Donald Trump

- Robert Lighthizer, the U.S. Trade Representative ,said Wednesday he’s “hopeful’’ of reaching a deal “in the next little bit” with Canada and Mexico to update the North American Free Trade Agreement. Canada’s chief negotiator,Steve Verheul, said he didn’t know what an “in principle’’ deal would look like and “significant gaps” remain

- Treasury 7-Year auction got a cool reception as it came after a rally cut benchmark 7Y yields from Tuesday high of 2.78%. The 2.34 bid-to-cover ratio, lowest since February 2016, compared with 2.54 average for previous six auctions

- President Donald Trump is hailing the revised U.S. free trade agreement with South Korea as a “great deal” yet the revamped U.S.-South Korea accord unveiled earlier this week isn’t much different from the existing pact that Trump often condemned as “disastrous.” White House ‘win’ on South Korea gets mixed marks

- SoftBank Group Corp. is edging closer to a deal to buy a stake in Swiss Re AG that would value the reinsurer at as much as 37 billion Swiss francs ($39 billion), according to people with knowledge of the matter

- Carry trades are set for a fourth straight quarter of losses despite the relative calm of foreign-exchange rates over the past three months

Asian equity markets traded indecisive as bourses failed to completely shrug-off the lacklustre lead from Wall St. where the major indices were subdued amid month-end flows and continued tech losses. ASX 200 (-0.5%) and Nikkei 225 (+0.6%) were mixed with Australia dragged lower by tech as well as recent weakness across commodities, while the Japanese benchmark was propped up for most the day by a softer currency. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+1.2%) were choppy in the midst of earnings season and with initial gains seen following reports of VAT reductions, although continued liquidity inaction by the PBoC and ongoing trade tensions with the US eventually weighed. Finally, 10yr JGBs were weaker as Japanese yields rose across the curve, with demand for paper sapped by initial outperformance in Japanese stocks and after an uninspiring 2yr auction in which the amount sold, b/c and accepted prices all declined from prior. PBoC skipped open market operations for a net daily drain of CNY 40bln. PBoC sets CNY mid-point at 6.3046 (Prev. 6.2785)

Top Asian News

- Japan Watchdog Says Deutsche Bank, BofA Colluded on Bond Trade

- Ping An Is Said to Start Work on $3 Billion OneConnect IPO

- Hyundai Motor’s Chung Overhauls Group as Succession Looms

- Two Koreas Set April 27 for Kim Jong Un’s Historic Walk South

European equities (Eurostoxx +1.2%) are back into positive territory, improving on the mixed tone seen in Asia overnight and shrugging-off the losses on Wall Street. Defensive sectors are in the red with focus on utilities and healthcare whilst broad gains are seen across all the other sectors. Sodexo (-14.1%) was the laggard this morning after reporting its earnings, dragging down Elior (-1.0%) and Compass (-3.6%) in the UK food catering segment. SwissRE (+2.9%) is leading the SMI after Softbank is said to be interested in building a 25% stake in the Co. for a USD 9.6bln deal. TomTom suffered losses of 6.3% after approaching Deutsche Bank for a potential sale of the whole firm or minority stake, but then denied calling for an adviser to seek potential buyers. Finally, as a reminder, Melrose’s GBP 8bln hostile bid for GKN is due to expire today at 1300 BST.

Top European News

- German Joblessness Hits Record Low as Firms Push Capacity Limits

- Wary U.K. Consumers Keep House Prices Subdued Year Before Brexit

- Bulgaria Reluctant to Seek ECB Scrutiny Before Euro Entry

In FX, the Greenback is showing little sign of losing its month, quarter and Japanese FY end bid, although the DXY is only tentatively above the 90.000 handle and the Dollar is somewhat mixed against its G10 rivals. Usd/Jpy is hovering just above 106.50 having touched 107.00 overnight after the biggest 1 day jump this year so far and with near term support seen at the 30 DMA (106.35). Aud/Usd has recovered some poise after hitting a fresh 2018 low around 0.7644 overnight but looks capped ahead of macro supply seen at 0.7680 vs major support at 0.7600 where hefty option expiry interest also resides (1.2 bn). Usd/Cad remains close to 1.2900 amidst less positive NAFTA vibes (long way to go to reach a deal and US demands on food not palatable), and with the Loonie now looking towards Canadian GDP data for some independent direction. Eur/Usd looks anchored around 1.2300 with strong support and resistance not far from the round number at 1.2286 and 1.2329 (latter representing the 30 DMA) and little to offer impetus via German jobs or inflation data given outcomes relatively close to consensus. Cable is clinging to 1.4050 (just) having lost grip of 1.4200 and 1.4100 handles on the run in to the end of March and long Easter weekend amidst decent expiries at the latter level and 1.4000, while techs are also wary of a fib at 1.4041. Nzd/Usd sits near 0.7200 and Usd/Chf is just above 0.9550

In commodities, WTI (+0.3%) and Brent Crude (+0.1%) are trading in close proximity to yesterday’s post-DoE levels. Prices have also been supported by yesterday’s comments from OPEC stating the producer cartel and other suppliers are looking to continue withholding the output cut for the rest of the year and potentially 2019. Moving on to metals, Gold is trading close to the prior session’s lows where the yellow metal posted its biggest 1-day percentage fall in almost 9 months as it continues to move inversely to the dollar. Base metals have seen a rebound in prices on the London Metal Exchange with Nickel (+2.0%) leading the advance and copper (+1.0%) higher following recent declines.

Looking at the day ahead, it’s a reasonably busy day for data highlighted by that February PCE data in the US, and personal income and spending reports. The latest weekly initial jobless claims reading, March Chicago PMI and final revisions to the March University of Michigan consumer sentiment reading are also due. Away from the data, in the early evening the Fed’s Harker is due to speak.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 230,000, prior 229,000; Continuing Claims, est. 1.87m, prior 1.83m

- 8:30am: Personal Income, est. 0.4%, prior 0.4%; Personal Spending, est. 0.2%, prior 0.2%; Real Personal Spending, est. 0.1%, prior -0.1%

- 8:30am: PCE Deflator MoM, est. 0.2%, prior 0.4%; PCE Deflator YoY, est. 1.7%, prior 1.7%

- 8:30am: PCE Core MoM, est. 0.2%, prior 0.3%; PCE Core YoY, est. 1.59%, prior 1.5%

- 9:45am: Chicago Purchasing Manager, est. 62, prior 61.9

- 9:45am: Bloomberg Consumer Comfort, prior 56.8

- 10am: U. of Mich. Sentiment, est. 102, prior 102; Current Conditions, prior 122.8; Expectations, prior 88.6

DB’s Craig Nicol concludes the overnight wrap

Markets seem to have spent the last 24 hours packing their bags and jetting off for the long weekend after an eventful last few weeks. Aside from digesting a few more tech related stories, the lack of any material newsflow – the first time we can say that in a while – certainly seems to have helped. Indeed, by the end of trading last night the S&P 500 and Dow closed -0.29% and -0.04% respectively. The lack of any real direction throughout the session is best summed up by the fact that the S&P 500 passed between gains and losses by 37 times.

The Nasdaq (-0.85%) did lag behind but at least that was the first sub-2% move in either direction for that index since this time last week. That performance looks even more solid when you look at the fall for the NYSE FANG index (-2.40%), which is now down -13.15% in the last 8 sessions. The tech equivalent of the VIX did however rise to 30.19 and is not far off the recent high of 33.89. In fact, the spread of the VXN over the VIX at one stage touched the highest in 13 years yesterday. Meanwhile, Europe spent much of the day scrambling back from a big leg lower at the open, sparked by that selloff in the US the night before. The Stoxx 600 clambered to a +0.46% gain after being down as much as -1.33% at one stage.

In bond land 10y Treasuries consolidated below 2.80% after yields closed at 2.782%, although touched 2.7425% intraday which is the lowest since early February. That was despite a bigger than expected upward revision to Q4 GDP (more on that below). The curve flattened once more though with 2s10s down 1.3bps to a fresh 10-year low while 5s30s also fell 3.4bps. In Europe yields were broadly speaking a couple of basis points lower yesterday.

So, as it’s the last day before markets shut down for the long weekend, it should be a fairly quiet end to the week although we say that slightly tentatively given what markets have done over the last few weeks. In any case we do have some important data to consider as we’ll get the US PCE report for February this afternoon. Both our US economists and the market expect a +0.2% mom print for the core, while the headline deflator is also expected to come in at +0.2% mom. The data takes on a little bit more significance in light of the Fed last week raising its inflation forecast above 2% in 2019. Our economists note that a print in line with their expectation would keep the year-over-year reading roughly steady at +1.5% yoy, however the 6m and 3m annualized rates should jump to +2.1% and +2.4% respectively, and so putting a bit of daylight between the run rate and the Fed’s target. Our colleagues also make the point that this is the last inflation data before the wireless services price drop is annualized in the March report, which will boost core CPI and core PCE by about 20bps and 10bps, respectively. Anyway, today’s data is due out at 1.30pm BST.

Ahead of it, markets in Asia are trading mixed this morning with the Nikkei (+0.40%) and Kospi (+0.27%) modestly up while the Hang Seng (-0.27%) and ASX 200 (-0.37%) are slightly lower. Bourses in China are flat having recovered from an early fall. Futures in Europe and the US are down about -0.10%.

Back to the subject of tech, yesterday Luke Templeman in our team published a timely and topical note as part of his Accounting Lifeguard series called ‘Europe’s digital tax’. Luke highlights that the ‘interim’ three percent tax on digital revenues is likely to be the mere opening salvo in negotiations between European states about the design of a new tax system and companies outside the technology sector should not be complacent. The EU’s digital tax may merely represent the first change to move taxation from being a domicile-based system to one based on value-creation. Given the decades-long rise of multinational firms, their taxation has become an increasingly sensitive topic. Digital firms are now the test subjects. You can find a link to Luke’s report here.

Rounding back to the US GDP print which we mentioned at the top, Q4 growth was revised up four-tenths and more than expected to +2.9% yoy annualized (vs. +2.7% expected) at the final reading. A 20bp uplift from personal consumption was the main driver. The data also included the latest corporate profits numbers, however it was a bit of a disappointment. Profits fell -0.1% qoq following two straight quarters of growth, although it appeared to be driven by financials predominantly with non-financial corporate profits still fairly solid.

In terms of the other macro data from yesterday, the February advanced goods trade deficit in the US was slightly wider at -$75.4bn (vs. -$74.4bn expected), while February wholesale inventories (+1.1% mom vs. +0.5% expected) and pending home sales (+3.1% mom vs. +2.0% expected) were both above expectations. In Europe, Germany’s April GfK consumer confidence index was slightly above consensus at 10.9 (vs. 10.7 expected) while France’s March consumer confidence was in line at 100. In the UK, March CBI retailing reported sales was below market at -8 (vs. 7 expected), partly impacted by the harsh weather during the month, although we should note that the data can be particularly volatile.

Away from the data, there were also some Brexit headlines to digest yesterday. The BOE noted that it’s “reasonable” for UK based firms “to plan that they will be able to continue undertaking activities during the (Brexit) implementation period in much the same way as now”. Chancellor Hammond also echoed similar sentiments and said that the BOE’s statement and the transition deal “will provide further confidence to financial services firms that there will be a smooth exit”. Notably, the FCA did caution that the transition agreements are not binding until they’re ratified as part of the withdrawal agreement.

Before we look at the day ahead, the Fed’s Bostic has reiterated that staying on a gradual path of rate hikes would be appropriate. He added that “unemployment is very close to full employment position and inflation our 2% target. If things are close to where we hope that they’ll be, then our policy doesn’t need to be super accommodative”. Elsewhere, the Bundesbank’s Wuermeling noted that “the upbeat economy and the inflation forecast would justify bringing (QE) to a rapid end, if the economic recovery in the Euro area continues as expected”.

Looking at the day ahead, it’s a reasonably busy day for data highlighted by that February PCE data in the US, and personal income and spending reports. The latest weekly initial jobless claims reading, March Chicago PMI and final revisions to the March University of Michigan consumer sentiment reading are also due. In Europe, the main highlight will likely be the flash March CPI report in Germany. Money and credit aggregates data in the UK along with the final Q4 GDP revision is also due. Away from the data, in the early evening the Fed’s Harker is due to speak.

Before we wrap up, a quick mention that on Easter Friday most major markets will be shut for the long weekend holiday. Industrial production and housing starts data is due in Japan for February while in Europe we’ll get the flash March CPI reports in France and Italy. Finally, on Saturday, China’s official PMIs for March will be released.

end

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 38.24 POINTS OR 1.22% /Hang Sang CLOSED UP 70.85 POINTS OR 0.24% / The Nikkei closed UP 127.77/Australia’s all ordinaires CLOSED DOWN 0.51%/Chinese yuan (ONSHORE) closed UP at 6.2877/Oil DOWN to 64.29 dollars per barrel for WTI and 68.27 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2877 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2755 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY GOOD CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED STRONGER GLOBAL MARKETS/STRONGER CURRENCY )

3 a NORTH KOREA/USA

North Korea/South Korea

Meeting between the North and South is April 27.

(courtesy zerohedge)

North, South Korea Set April 27 As Date For Historic Summit

The date for the first meeting between a North Korean and South Korean leader in a decade has been set for April 27, South Korean officials told US media. For the first time since the Korean War broke out in 1948, a North Korean leader will cross the DMZ to attend the meetings, which are set to be held in South Korea.

After Kim Jong Un promised that he would consider denuclearization of the peninsula during talks with Chinese President Xi Jinping this week, it appears that the multiple rounds of sanctions imposed by the UN and the US are having their desired effect.

According to Bloomberg, the last inter-Korean summit was held in October 2007 between then President Roh Moo-hyun and Kim Jong Il, the father of Kim Jong Un. The pair signed a peace declaration calling to end the armistice with a permanent treaty, but progress stalled and the two sides remain in a stalemate. While the two countries allowed for some family reunions, relations later soured under a more conservative administration in the South.

President Trump, who has repeatedly threatened the North with nuclear annihilation, cheered Kim’s decision to seek a detente with the West and a meeting with the US.

Donald J. Trump

✔@realDonaldTrump

Received message last night from XI JINPING of China that his meeting with KIM JONG UN went very well and that KIM looks forward to his meeting with me. In the meantime, and unfortunately, maximum sanctions and pressure must be maintained at all cost!

A government spokesman said South Koreans were encouraged to be “united in making a groundbreaking turning point for peace.”

“As the date for the inter-Korean summit is finalized now, we will do our best to be fully prepared for it during the given time,” Moon’s spokesman, Kim Eui-kyeom, said in a text message. “We hope all South Koreans will be united in making a groundbreaking turning point for peace settlement on the Korean Peninsula at the summit.”

The subject of the talks will be improving inter-Korean relations and de-nuclearization, according to Reuters.

The two Koreas had agreed to hold the summit at the border truce village of Panmunjom when South Korean President Moon Jae-in sent a delegation to Pyongyang this month to meet North Korean leader Kim Jong Un.

According to a statement, the two sides will hold a working-level meeting on April 4 to discuss details of the summit, such as staffing support, security and news releases.

Meanwhile, Bloomberg reported that the North has also expressed a desire to meet with the Japanese government.

Japanese Foreign Minister Taro Kono told parliament that his nation would consider holding talks with North Korea in the context of the other summits taking place. The Asahi newspaper said earlier that Kim Jong Un’s administration was seeking a summit with Prime Minister Shinzo Abe. The yen weakened to a two-week low against the dollar after the report.

As a reminder, talks between the US and the North, which are tentatively expected to be held at the DMZ, are set for May.

end

South Korea/USA

the truth behind the deal: no gain to the uSA

(courtesy Global Macro Monitor)

Potemkin Trade Deals Exposed

What a farce.

South Korea, meanwhile, negotiated a permanent steel-tariff exemption in exchange for allowing additional U.S. auto imports.