GOLD: $1342.70 UP $19.50 (COMEX TO COMEX CLOSINGS)

Silver: $16.67 UP 34 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $134150

silver: $16605

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1335.22 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1327.20

PREMIUM FIRST FIX: $8.02

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1335.22

NY GOLD PRICE AT THE EXACT SAME TIME: 1329.04

PREMIUM SECOND FIX /NY:$6.10

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $xxx

NY PRICING AT THE EXACT SAME TIME: $xxx

LONDON SECOND GOLD FIX 10 AM: $xxx

NY PRICING AT THE EXACT SAME TIME. $xxx

end

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:399 NOTICE(S) FOR 39,900 OZ.

TOTAL NOTICES SO FAR 551 FOR 55100 OZ (1.713 tonnes)

For silver:

APRIL

8 NOTICE(S) FILED TODAY FOR

40,000 OZ/

Total number of notices filed so far this month: 19 for 90,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $054/OFFER $7154: UP $260(morning)

Bitcoin: BID/ $6889/offer $6989: UP $95 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A GOOD SIZED 1901 contracts from 227,230 RISING TO 229,131 DESPITE THURSDAY’S SMALL 6 CENT RISE IN SILVER PRICING. AGAIN, WE HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2261 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2261 CONTRACTS. WITH THE TRANSFER OF 2261 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2261 CONTRACTS TRANSLATES INTO 11.30 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

2261 CONTRACTS (FOR 1 TRADING DAY TOTAL 2261 CONTRACTS) OR 11.30 MILLION OZ: AVERAGE PER DAY: 2261 CONTRACTS OR 11.30 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 11.30 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.61% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 729.795 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A STRONG SIZED GAIN IN COMEX OI SILVER COMEX OF 1901 WITH THE 6 CENT RISE IN SILVER PRICE. HOWEVER, WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 2261 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2261 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A VERY STRONG 4162 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 2261 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 1901 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 6 CENTS AND A CLOSING PRICE OF $16.33 WITH RESPECT TO THURSDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.136 BILLION TO BE EXACT or 164% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 8 NOTICE(S) FOR 40,000 OZ OF SILVER

IN SILVER, WE ARE NOW 5,000 CONTRACTS AWAY FROM RECORD LEVELS AND YET THE SILVER PRICE IS EXTREMELY LOW

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 227,200 CONTRACTS (OR 1.136 BILLION OZ/

- HUGE EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOWER PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT JPMORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

In gold, the open interest FELL BY AN EXTREMELY LARGE SIZED 8602 CONTRACTS DOWN TO 499,565 ACCOMPANYING THE FAIR SIZED FALL IN PRICE IN THURSDAY TRADING ( LOSS OF $3.20). AS WE ENTER THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 14,769 CONTRACTS : JUNE SAW THE ISSUANCE OF 14,769 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 499,565. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 6167 OI CONTRACTS DECREASED AT THE COMEX AND A VERY STRONG SIZED 14,769 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 6167 CONTRACTS OR 616700 OZ =19.18 TONNES

THURSDAY, WE HAD 24,732 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 14,769 CONTRACTS OR 1,476,900 OZ OR 45.937 TONNES (1 TRADING DAYS AND THUS AVERAGING: 14,769 EFP CONTRACTS PER TRADING DAY OR 1,476,900 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 1 TRADING DAY IN TONNES: 45.937 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 45.937/2550 x 100% TONNES = 1.80% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2090.5 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX WITH THE FAIR SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($3.20 LOSS). WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,769 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,769 EFP CONTRACTS ISSUED, WE HAD A GOOD NET GAIN IN OPEN INTEREST OF 6721 contracts ON THE TWO EXCHANGES:

14,769 CONTRACTS MOVE TO LONDON AND 8602 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 20.91 TONNES).

we had: 152 notice(s) filed upon for 15,200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $19.50 : WE HAD A BIG CHANGE IN GOLD TONNAGE AT THE GLD/ A DEPOSIT OF 6.19 TONNES

Inventory rests tonight: 852.31 tonnes.

SLV/

WITH SILVER UP 34 CENTS TODAY: NO CHANGE

/INVENTORY RESTS AT 319.012 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE BY A STRONG 1901 contracts from 227,230 UP TO 229,131 (AND now A LOT CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787. THE PRICE OF SILVER ON THAT DAY: $17.89) WITH THE SMALL SIZED RISE IN PRICE OF SILVER (6 CENTS// THURSDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2261 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2022 CONTRACTS TO THE 2261 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN ASTRONG GAIN OF 4162 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 20.81 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE SMALL RISE IN SILVER PRICING THURSDAY (6 CENT RISE IN PRICE) . BUT WE ALSO HAD ANOTHER VERY STRONG SIZED 2261 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 5.71 POINTS OR 0.18% /Hang Sang CLOSED / The Nikkei closed DOWN 65.72/Australia’s all ordinaires CLOSED /Chinese yuan (ONSHORE) closed UP at 6.2831/Oil UP to 65.25 dollars per barrel for WTI and 69.73 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2830 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2650 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY GOOD CHINESE MARKETS/CHINA RETALIATES WITH TARIFFS/

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

Friday: Japan experiencing problems as this big exporting nation sees its industrial production slow down. CPI drops which is something that Japan does not want. Also unemployment jumps..another sign that their economy might be in trouble

( zerohedge)

3 c CHINA

i)Fresh from it’s successful introduction of a yuan denominated crude oil futures, now China is orchestrating paying for oil imports directly with yuan instead of dollars

( zerohedge)

ii)China imposes tariffs on more than 125 USA imports including fruit, pork and wine as fears of a trade war grow

two commentaries Mirror and zero hedge

(courtesy Mirror.coUK/zerohedge)

4. EUROPEAN AFFAIRS

i)France/Turkey/Syria

This is becoming a real mess: Now France is sending military forces to North west Syria in a move to help the Kurds, knowing that Trump has announced that he will withdraw his troops “shortly”

( zerohedge)

ii)FRANCE, TURKEY AND SYRIA

Immediately French troops are deployed at 5 military bases in Northern Syria and these forces are being used to fortify the American backed SDF. These forces are helping the Syrian Kurds which is forcing Erodgan into a temper tantrum as he wants to oust the Kurds

( South Front)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Friday: Israeli stealth fighters fly over Iran and they were not detected..speculation of an imminent war is tensifying

( zerohedge)

Israel announces that it will respond by going inside the Gaza Strip if organized terrorist operations continue

( zerohedge)

iii)Friday

( zerohedge)

iv)Russia/USA

Trump warns Putin of a arms race in a phone call over the weekend

( zerohedge)

This is going to hurt Russia a bit: Theresa May is considering a ban on issuance of Russian sovereign debt in London and clearing of Russian debt. Russia will need the assistance of China on this matter.

vi)Turkey/NATO/Russia

Interesting: Turkey breaks with NATO as they refuse to expel Russians. We know that Turkey is playing with fire as they antagonize the EU over Syria . Although Turkey condemned the alleged poisoning of Skripal, they refuse to expel any diplomats. It is also interesting that Israel has refused to expel any Russians as they may deem the attack to be a false flag

( Jim Carey/Geopolitics.Alert com)

vii)MONDAY/RUSSIA

(courtesy zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

i)Two important commentaries re the new Petro yuan scheme. In the first commentary, Pepe Escobar is of the opinion that China is taking the long road to solve the dominance of the USA dollar. It believe it is shorter than what he thinks

two commentaries

( Asia Times/Pepe Escobar)

ii)The following is a very important commentary on the subject of the Petro Yuan scheme.

This is a must read as Macleod outlines the details on the new contract of which the first deliveries will be in September. Already conditions are being laid for gold to be delivered to holders if they do not want to hold yuan. This will ultimately be the death knell of the uSA dollar as excess dollars will now float around the world with no home except the US

a must read.

( Alasdair Macleod)

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)Another essential commentary from Nicholas as he describes the complete opaqueness of the LBMA( Nicholas Biezanek)

iii)Bitcoin breaks below 6800/Sunday

( zerohedge)

iv)Wishful thinking: Monetary reform would rebalance trade..a good history lesson

( Sean Rushton/GATA)

v)In the 4th quarter, the USA dollar share of currency reserves has hit a 4 yr low

( Reuters)

vi)China is now planning to crackdown on all virtual currencies

( GATA/Reuters)

10. USA stories which will influence the price of gold/silver

I would not pay too much attention to soft data Markit PMI which soared again despite the fact that the same soft data ISM mfg index went the other way. However in both reports, the new tariffs and the decline in the dollar is causing commodity prices to rise and this is causing manufacturing input costs to soar. Looks to me like we have stagflation which is the enemy of the Fed.

( zerohedge)

ib)Early morning trading

ii)The Donald continues with his attack on Amazon and the deal Amazon has with the post office. Citibank has calculated that the USPS is losing 1.50 for every package sent(courtesy zerohedge)

iii)Donald Stockman explains the truth behind the real earnings of the SP 500 and the truth behind Amazon

( Donald Stockman)

iv Looks like we are getting a mutiny on the bounty at McDonald’s especially in California as the company renegs on wage hikes.

( zerohedge)

v)Let us close out tonight with this very important interview of Rob Kirby by Greg hunter

(COURTESY GREG HUNTER)

vi)SWAMP STORIES

a)This does not look promising: Jeff Sessions (and probable a Deep State) hires Prosecutor Huber, an Obama appointee to investigate the FBI and he will join Horowitz in a joint effort.

it keeps the investigation under the dept of Justice.

( zerohedge)

( zerohedge)

( zerohedge)

d)First there was Stormy Daniels, then Karen McDougall, and now a third woman, Jessica Denson that wants to lift NDA’s signed with the Trump administration so they would not disclose affairs with the Donald.

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:112,749 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 265,530 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A STRONG 1901 CONTRACTS FROM 227,230 UP TO 229,131 DESPITE OUR TINY 6 CENT RISE IN SILVER PRICING/ THURSDAY). ALSO,WE WERE ALSO INFORMED THAT WE HAD A VERY STRONG 2261 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2261. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE AGAIN SURPRISINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A VERY STRONG SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 4161 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1901 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2261 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:4162 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 11 contracts FALLING TO 350 contracts. We had 11 notices filed upon (CME correction last Thursday night) so in essence we lost 0 contracts or NIL additional ounces of silver will stand for delivery in this non active delivery month of April.

The next big active delivery month for silver will be May and here the OI LOST 1421 contracts DOWN to 153,449. June saw its first gain of one contract to stand at one. The next big delivery month for silver is July and here the OI rose by 2435 contracts up to 40,007.

We had 8 notice(s) filed for 40,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 2/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

399 notice(s)

39,900 OZ

|

| No of oz to be served (notices) |

2230 contracts

(223,000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

551 notices

55100 OZ

1.7130 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 41 notices were issued from their client or customer account. The total of all issuance by all participants equates to 399 contract(s) of which 151 notices were stopped (received) by j.P. Morgan dealer and 32 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (551) x 100 oz or 55100 oz, to which we add the difference between the open interest for the front month of APRIL. (2629 contracts) minus the number of notices served upon today (399 x 100 oz per contract) equals 278,100 oz, the number of ounces standing in this active month of APRIL (8.650 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (551 x 100 oz or ounces + {(2629)OI for the front month minus the number of notices served upon today (399 x 100 oz )which equals 278,100 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST A MONSTROUS 3616 CONTRACTS OR 361600 OZ OF GOLD AND THESE GUYS WILL MORPH INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

201,355.220

oz

SCOTIA

DELAWARE

BRINKS

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,798,168.304 oz

CNT

JPMorgan

SCOTIA

|

| No of oz served today (contracts) |

8

CONTRACT(S

(40,000 OZ)

|

| No of oz to be served (notices) |

342 contracts

(1,710,000 oz)

|

| Total monthly oz silver served (contracts) | 19 contracts

(95,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 3 deposits into the customer account

i) Into JPMorgan: 597,413.790 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) into CNT: 600,489.604 oz

iii) into Scotia: 660,264.910 oz

total deposits today: 1,798.168.304 oz

we had 3 withdrawals from the customer account;

i) Scotia; 161,516.220 oz

ii) Out of Delaware: 5932.65 oz

iii) Out of CNT: 600,429.240 oz

iii) our od Brinks: 33,905.95 oz

total withdrawals; 201,355.220 oz

we had 0 adjustment

total dealer silver: 58.8561 million

total dealer + customer silver: 262.106 million oz

The total number of notices filed today for the APRIL. contract month is represented by 8 contract(s) FOR 40,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 19 x 5,000 oz = 95,000 oz to which we add the difference between the open interest for the front month of April. (350) and the number of notices served upon today (8 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 19(notices served so far)x 5000 oz + OI for front month of April(350) -number of notices served upon today (8)x 5000 oz equals 1,805,000 oz of silver standing for the April contract month

WE NEITHER GAINED NOR LOST ANY SILVER OUNCES STANDING IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 33,834 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 88,190 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 88,190 CONTRACTS EQUATES TO 440 MILLION OZ OR 62.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.45% (APRIL 2/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.70% to NAV (APRIL 2/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.45%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.70%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.50%: NAV 13.81/TRADING 13.47//DISCOUNT 2.50.

END

And now the Gold inventory at the GLD/

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 2/2018/ Inventory rests tonight at 846.12 tonnes

*IN LAST 353 TRADING DAYS: 88.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 303 TRADING DAYS: A NET 67.57 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 2/2018: NO CHANGES IN SILVER INVENTORY:

Inventory 319.012 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.44

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.97%

libor 2.44 FOR 6 MONTHS/

GOLD LENDING RATE: .47%

XXXXXXXX

12 Month MM GOFO

+ 2.43%

LIBOR FOR 12 MONTH DURATION: 2.66

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.23

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Brexit, Stagflation Pressures UK High Street

– UK high street and wider consumer market feeling effects of financial crisis, Brexit and inflation

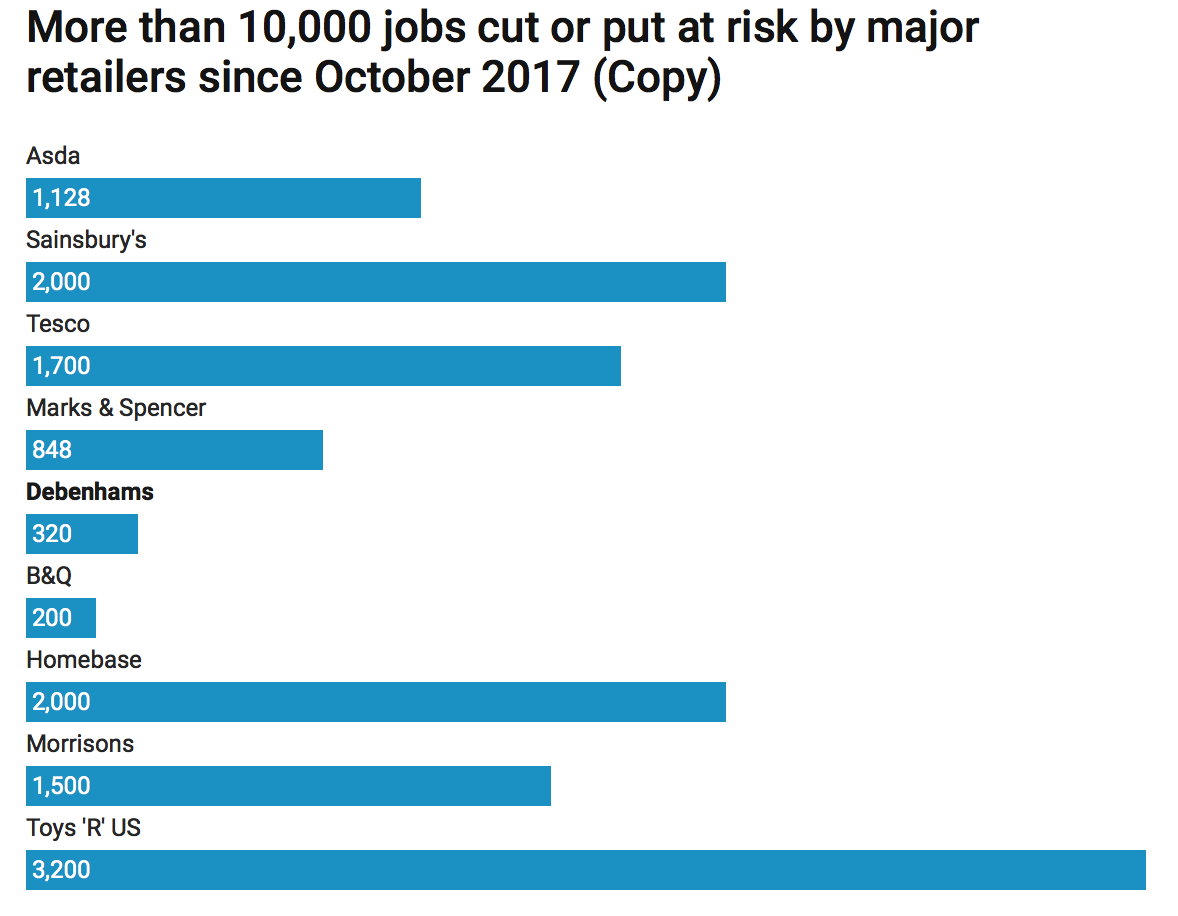

– 350,000 retails jobs expected to disappear between 2016 and 2020

– Centre for Retail Research predicts 9,500 shops to close this year and 10,200 in 2019

– UK is ‘worst performing’ European market for new car registrations – Moody’s

– UK’s growth outlook is the ‘worst in the G20’ – Institute of Fiscal Studies

– Consumer spending grow just 1.3% in 2018, a seven-year low

– Spending growth dropped by 2.6% since 2016 contributing to UK high street bankruptcies

The eponymous British High Street is on the verge of its biggest crisis since 2008. According to The Centre for Retail Research up to 200,000 retail jobs could be gone by 2020, this is in addition to the 150,000 that have disappeared since 2016. Many household chains are scrambling to negotiate with creditors in order to avoid collapse and total wipeout.

In 2018 alone eleven high street retailers have gone into administration, Professor Joshua Bamfield of the Centre for Retail Research has warned that 1 in 10 shops could disappear in the next two years. Whilst the government has been called on to help this isn’t something that is easily resolved.

Chancellor Philip Hammond is being lobbied to reduce business rates, however this is just one problem amongst many. In all likelihood it is the only problem which can be directly resolved by the government. Larger (more potent) problems such as Brexit uncertainty, inflation and reduced household spending are out of anyone’s control. With Brexit now less than one year away many are asking if this is something that can ever be resolved.

The cause of the problem is a mixture of the aftermath of an unresolved financial crisis and the economic effects of Brexit. The uncertainty following the referendum and the resulting currency-driven inflation has without doubt reduced shoppers’ keenness to let loose on high street, but this outcome was inevitable given the real lack of progress following the financial crisis.

It is estimated that one pound in five is spent online. Not only are retailers having to compete with the countless reams of websites that now offer a more engaged shopping experience but they are facing a market that is heavily indebted, losing jobs, stagnant wages and facing unknown changes in the coming months and years.

Like dominoes

At the end of February two major high street fixtures, Maplins and Toys R Us, announced their collapses within two hours of one another. Each are thought to be responsible for up to 3,000 members of staff losing their jobs.

This is not surprising reading. Last month Visa said the British high street had had its worst start to the year since 2012. Inflation-adjusted consumer spending in February was 1.1% lower than in 2017, after a 1.2% decline in January.

“As we look ahead into March, consumer spending is at risk of posting one of the worst Q1 results on record,” Visa’s chief commercial officer, Mark Antipof, said.

The collapse of the UK high street has been ongoing for nearly a decade. In 2008 Woolworths went under, with 30,000 employees out of work. Since then the likes of MFI, Borders, Comet (one of many white goods firms to go bust) and JJB sports have lost out to the struggling economy.

The most recent victim on the British High Street is department store House of Fraser. It is responsible for the jobs of 5,000 direct employees and 12,500 concession stand staff. Last Friday the owners announced EY had been called in to try and help with a dire financial situation. The company is desperately trying to renegotiate rental arrangements whilst navigate its way around hundreds of millions of pounds of debt, £350m of which is a publicly traded bond.

In the background Carpetright is due to close stores (2,700 employees), stark profit warnings have come from Moss Bros (1,350 employees), B&Q’s owners are in trouble (25,000 employees) and Mothercare (5,200 employees) are in ongoing talks with creditors.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

With the economic situation as it is and changing shopping behaviours there seems to be little let-up for the high street retailer. Whilst this makes stark reading now, it will have profound long-term consequences on an economy which is increasingly finding itself with several thousand retail workers without anywhere to turn to.

Inflation and wage squeeze leads to high street stagflation

Despite what the government might tell you inflation really is biting at the heels of households. If one considers that it is mainly appearing in food, transport and housing costs then you have accounted for around (at least) 50% of a household’s spending. This is non-discretionary, so what will suffer? Shops.

What is discretionary is purchases of non-essential items. Households that are feeling the pinch through wage stagnation, inflation and the impact of Brexit are unlikely to just buy on a whim anymore.

Inflation has been rising at a faster pace than wages for some time now. Officially the government has only just noticed this since the Brexit vote which has resulted in imported currency-related inflation. But, in truth it has been around along-time, evidenced by shrinkflation and increasing levels of consumer debt.

Conversely, spending is climbing in one area – online shopping. Consumers feeling the pinch are more willing to spend online where they can hunt out bargains, save money on transport to the shops and reduce the chances of overspending whilst shopping. At the moment one in every five pounds is spent online, this is likely to increase as habits evolve.

No hot wheels here

It’s not just on the UK high street where consumers have decided to rein in their spending. The new car market is also feeling the impact of the economic downturn.

According to Ratings agency Moody, new car registrations are likely to fall 5.5% this year, making the UK the ‘worst performing’ market in Europe. This will make the second year in a row that car registrations are down, bringing the fall to 10%.

“The UK market will be the worst performer compared to all other major economies in Europe, and, even worse, the only one that is declining.” Matthias Hellstern, Moody’s

In stark contrast to the UK, Spain and Germany Spain and Germany will see new registrations climb by 4.7% and 4% respectively in 2018.

The UK motor market is just one example of problems outside of the UK retail sector. Consider the reduction in bank branches, post offices and other public service outlets.

Light at the end of the tunnel?

In his Spring statement Chancellor Philip Hammond tried to give a rosy picture of the future of the UK economy. He assured the House of Commons that not only would growth be at 1.5% for 2018 but that debt would represent a smaller proportion of GDP by the end of the year.

This was a lot of political rose-tinting though. Paul Johnson, director of the Institute of Fiscal Studies told the BBC that none of this meant very much, ‘The UK economy was now 14% smaller than would have been expected, based on pre-crisis trends, while median earnings remained below their 2008 level.

“The reality of the economic and fiscal challenges facing us ought to be at the very top of the news agenda,” Mr Johnson said. “And I mean the reality, not the spin and bluster of politicians on all sides pretending there are easy solutions.”‘

An Ernst & Young report released at the beginning of the month reported that the ‘the U.K. consumer will be hit by new issues which will impact their spending power…Our prediction of a ‘so-so’ consumer sector over the next few years points to a ‘so-so’ economy, growing at an unspectacular rate compared with past standards.”

How will this reduction in consumer spending really impact the UK economy? Clearly no-one really knows but you can gain a fair idea when you consider that domestic consumer spending makes up the largest part of British economic demand.

With over 200,000 people losing their jobs that’s a significant number of people now dependent on the UK government. This is not only for unemployment benefit but also for long-term support such as their pensions.

The Toys R Us defined benefit pension fund, which has an estimated £37m deficit, is one such whole the government will have to plug. Other high street retailers collapsing also have very red pension funds. The British tax payer will no doubt end up propping those who now face a retirement without a pension.

Protect yourself from further Brexit blow-ups

Sadly much about the above situations were unavoidable. After years of rapid debt-fuelled expansion, rising inequality and growing nationalism across Europe it was inevitable that we would step out to find our high streets in such a state.

There is also something inevitable about how this will end. But, what happens to your wealth, investments and savings is not a given. At the moment savers are still able to use what is the calm before the storm to reallocate their portfolios so they are well-balanced and protected against the aftermath of easy monetary policy and political fallout.

Investments such as gold and silver by their very nature are immune to the effects of inflation, stagflation and the dangerous ideas and experiments of central banks. Gold has just completed its most successful three quarterly run since 2011. This should offer two key signals – the first that safe haven demand is on the up as buyers become increasingly wary of the outcome of political and economic decisions and, secondly, that now is an ideal time to prepare your portfolio against even more upset in the marketplace.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related reading

UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

World is $233 Trillion In Debt: UK Personal Debt At New Record

UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

News and Commentary

Gold rises on softer dollar, fresh trade worries (Reuters.com)

Asian Stocks Rise Led by Korea; Treasuries Slip (Bloomberg.com)

Data, earnings set to wrest stock market’s attention from Facebook and trade (MarketWatch.com)

Steel, cocoa among first-quarter gainers, but coal, sugar take biggest hits (MarketWatch.com)

Bitcoin Breaches $7,000 in Downbeat End to Dismal Quarter (Bloomberg.com)

ECB’s Knot Urges QE End to Help Wean World Economy Off Stimulus (Bloomberg.com)

BofA: This Is “The Last QE Trade” (ZeroHedge.com)

The rebel bank, printing its own notes and buying back people’s debts (TheGuardian.com)

Gold Prices (LBMA AM)

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

21 Mar: USD 1,316.35, GBP 935.53 & EUR 1,071.64 per ounce

Silver Prices (LBMA)

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

21 Mar: USD 16.25, GBP 11.56 & EUR 13.23 per ounce

Recent Market Updates

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Crock Of Gold Hidden In Ireland? Happy Saint Patrick’s Day

– Buy Silver And Sell Gold Now

– Stephen Hawking – Doomsday Prophet’s Top Five Predictions

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

The following exchange from Nicholas Biezanek to me is an essential read. In essence the banks are hiding the huge number of EFP’s through what is called a serial sub 14 day forward obligation. Anything less than 14 day forwards do not have to be included for monitoring by the Office of the Comptroller, Great Britain. I will endeavour to find out if this is exactly true. If so, then this is nothing but a criminal conspiracy to defraud by the bankers. Also note that all physical bars delivered upon at 2018 markings..nothing from the past..obviously bars are disappearing faster than a speeding bullet.

Nicholas to me:

|

10:03 AM (2 minutes ago) |

|

||

|

||||

Bill,Harvey,

I don’t know whether you have listened to Andrew Maguire’s interview with Greg Hunter but ,if not, then here are some key points.This interview is just to important to miss:

- Whilst the volume of gold EFPs for the 1st quarter ,ending tonight,will almost certainly exceed 2 000 tonnes,Andrew believes that these delivery obligations are rolled into serial forward contract obligations for nominal delivery in less than 14 days ,and hence avoid inclusion in the reports required by the Office of the Comptroller that seeks to monitor any liquidity squeeze on the ‘too big to fail’ banks .The logic for excluding obligations due in less than two weeks is not immediately obvious.Perhaps this delusional Comptroller believes that these criminals will at least have the integrity and risk management systems in place to accommodate all such short term and therefore,unavoidable, commitments.

- All physical gold deliveries out of the LBMA recently bear 2018 markings only-presumably all gold bars refined prior to this date are now ‘AWOL’

- The actual gold market fractional reserving ratio may be as high as 1000/1

- Whilst every time Andrew Maguire goes on air, the paper price of gold is trashed, correlation is not to be confused with causation. At 15.00 on the last Friday of every month (perhaps today as tomorrow is Good Friday), the BIS tries to window dress its trillion USD underwater derivatives book for reporting purposes.Therefore the paper gold price action of the last 24 hours was caste in stone.

- The bad news for the BIS, Cartel and LBMA is that the whole world is now waiting for this end of month market action and seeks to capitalize upon these waterfall paper gold price declines as unmissable windows of opportunity for physical gold acquisition.

- Many astute investors are also loading up on physical gold in order to ‘front run’ the imminent seriously large physical gold purchases for the ‘alternative currency’ -kinesis.com-that will go live in October 2018. If you are in paper gold only (including unallocated gold holdings) you will simply be ostracized from this ‘party to end all parties’ (If you haven’t listened to this interview at least twice, then you are not really serious about the gold market)

- Denis Gartman believes that as soon as the Venezuelan Central Bank has completed its disposal of (184?) tons of gold,an orderly gold market will return.Andrew also believes that it will be ‘business as usual’, but only until the impossible,unsustainable strain and tightness in the physical gold market causes a massive price ‘reset’,probably over a weekend, and it may be soon. (Harvey: I strongly believe that all of the Venezuelan gold has been sold long time ago as soon as Maduro got in trouble)

Whilst I have been immersed in GATA’s attempts to unravel the corruption,and manipulation of the physical gold market for a decade, I still find it difficult to get my mind around the magnitude of this imminent unraveling..

Regards

Nicholas

end

Another essential commentary from Nicholas as he describes the complete opaqueness of the LBMA

(courtesy Nicholas Biezanek)

What exactly is the LBMA?

The Comex warehouses contain a total of about 12 tons of registered gold and yet the entire price setting mechanism for physical gold is dictated in the paper markets based on the premise that, if demanded, physical delivery of Comex gold paper contracts is available at the contract price because of this truly microscopic amount of physical gold backing a gargantuan open interest of 508,000 contracts (as at 29/03/2018.)

Recently, however, thanks to Harvey Organ, it has been revealed, that Exchange for Physical (EFP) contracts have been heavily utilized as a mechanism for transferring physical delivery obligations over to LBMA market participants. Although almost certainly predating Harvey’s first unravelling in Nov of 2017, this EFP manipulative technique has allowed the COMEX to prevent a catastrophic delivery failure and almost certain consequent closure. In just the three months to 29th March 2018, the volume of these EFP transfers over to the LBMA is computed at 2,044 tons.(Impossible)

Let us have a closer look at the LBMA, now that it has assumed this role of being the mechanism to which the corrupt COMEX paper Ponzi scheme owes its continuing existence. The best place to look is the LBMA’s own Annual Review, published for the first time ever in 2017. In is a ‘glossy’ of only 20 pages, and at least half the content relates to pictures. The ‘war cries’ of integrity and transparency abound, but let us unpack the fine words to seek out anything more substantial.

At the end of the report is a brief financial summary. Income=3.546 million ponds and expenditure=3.378 million pounds=operating surplus of 167 thousand pounds only. The LBMA is therefore demonstrably a midget organization so maybe expectations should be commensurately tailored.

The LBMA takes great pride in its harmonization of physical delivery standards, but as the Sino bloc rejects the LBMA finesse standard of .995 to the extent of demanding re refining to a .9999 finesse standard, perhaps the LBMA is not doing a very good job.

The LBMA takes great pride in seeking to harmonize the contractual framework relating to transactions under its umbrella, but as the Holter/Sinclair collaboration keeps reminding us- “what is the value of a contract that cannot perform?” Nonperformance of physical gold delivery obligations out of loco London seems to be a recurring and pervasive theme. (Many weeks delay to receive gold bars refined in 2018 etc.)

The LBMA has now put delivery of its reporting project to bring transparency to the opaque world of OTC transactions on hold. Same day reporting of the London gold fixes has now been discontinued for reasons that don’t appear to be compelling, and consequently all that is sighted in the West are these manipulated paper prices sourced from the COMEX platform that would have lost its right and ability to exist but for the aforementioned co-mingling of physical delivery contracts into the opaqueness of the LBMA vortex.

Even in Nigeria, all the bankers stay behind every trading day in order to balance the day’s trading and consequent cash balances etc. The LBMA takes great pride in the fact that total loco London gold hoardings are now reported. This reporting, however, is 90 days in arrears, whereas based on Nigerian standards it should be after an elapse of 24 hours maximum.(Surely all physical verification is on a perpetual basis?) The biggest farce of all, however is that these (historic) reports of loco London gold hoardings are complete disinformation. It is an insult to our intelligence to provide this historic information without disclosure of all corresponding liabilities of the LBMA members in respect of claims on this gold. Maybe there are indeed 7,800 tons of loco London gold, but if 78,000 tons of gold are required to satisfy all corresponding obligations, that would better contextualize this abomination.

But then I return to the financial information in respect of the LBMA. Less than $5 million total revenue. Ruth Crowell, the CE of the LBMA, has all the authority and budget of a part time meter maid armed with a feather duster. She probably has no idea of what is coming down the road or else she would get out, just like Rothschild, Credit Suisse, Deutsche Bank and Barclays On the other hand, here is the 2018 budget request from the CFTC acting Commissioner:‘ In order for the CFTC to fulfill its duty to oversee these vital markets in FY2018, I am requesting $281.5 million and 739 fulltime equivalents (FTE). This is an increase of $31.5 million and 36 FTE over the FY 2017 continuing resolution (CR) level.’

As we all know only too well, despite all these abundant resources, the CFTC has never intervened, not once, in the grotesque concentration and manipulative heavy trading volumes at the most illiquid trading periods in respect of COMEX precious metal trading. ‘Nothing to see here’ is the eternal war cry. The CFTC and COMEX must be pleased that the Achilles heel of the COMEX, (its inability to deliver physical metal when required) has, for the time being at any rate, been transferred to the opaque, unregulated LBMA and is currently out of sight. For how long? The LBMA does not have the physical metal to satisfy all these EFP transfers from the COMEX. Not at all. The combined authority of both the LBMA and COMEX are probably unaware of the imminent eruption and are clueless about the enormity of the crisis. In the words of Don Rumsfeld, the current situation can be summed up as:

‘There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.

end

Friday night: Bitcoin below 7,000.

(courtesy zerohedge)

Crypto Carnage Continues – Bitcoin Back Below $7,000, Ether Under $400

Despite a brief bounce overnight, cryptos are sliding once again with Bitcoin below $7,000; Ethereum below $400; and Ripple back below 50c.

“It’s a sea of red,” said one seasoned crypto-trader, adding after a stoic pause, “again!”

Amid the worst month for tech stocks in years, cryptos are in freefall…

Bitcoin is back below $7,000…

Heading towards its early Feb lows…

As CoinTelegraph notes, the overall market slump could be attribued to both Twitter’s recent announcment that would ban crypto-related ads, following on the heels of similar announcements from Google and Facebook, or Mailchimp’s apparent closure of crypto-related accounts.

In response to the social media ad bans, crypto and Blockchain associations in Russia, South Korea, and China have created a joint assocation in order to sue the social media giants, including Yandex, referring to the bans as “market manipulation” by “monolopies.”

Regulatory crackdowns on crypto could also be compounding the market’s downward trend, as two Japanese exhanges this week have decided to close instead of working with regulators for compliance.

end

Bitcoin breaks below 6800/Sunday

(courtesy zerohedge)

Cryptogeddon – Bitcoin Breaks Below $7,000; Ether Down 75% From Highs

As if the last few weeks were not bad enough, cryptocurrencies are re-tumbling since Friday’s close.

Once again there is no clear catalyst but headlines from crypto world include South Korean and Thai regulators preparing to unveil their crypto-tax proposals (and notably the maze of details surrounding US tax requirements for cryptos may also be forcing some unwinds to cover unforeseen ‘costs’).

The Kazakh National Bank has banned crypto-mining and The FBI has issued a warning regarding fraud and cryptos.

Bitcoin is now below $7,000 – a level it first hit in October 2017 – down 67% from its record high in December.

Ethereum is worse – down 75% from its highs and back below $400, this is the lowest level for the second largest crypto by market cap since November 2017.

While this collapse is very reminiscent of the dotcom debacle, CoinTelegraph’s Nikolai Kuznetsov sees innovation and sustainability.

While it is only prudent and smart for anyone entering the crypto space to proceed with caution especially when it comes to trading and investing in crypto assets, it would be unfair to be totally dismissive of what the Blockchain technology has brought about. The parallels with the dotcom bubble should serve as lessons to stakeholders.

One must remember that the aftermath of the dotcom bubble also affirmed that truly innovative organizations and technologies could weather the storm. Companies such as Amazon and eBay proved that pairing novel ideas with good business acumen can lead to success. Surely, the situation today with crypto and the environment of dotcoms from nearly twenty years ago would have their differences. Ventures must be able to navigate these nuances in order to make the best possible decisions moving forward.

Whether or not crypto ventures will share a similar fate to dotcoms remains to be seen. At least for now, crypto stakeholders have a chance to write a different story.

end

Wishful thinking: Monetary reform would rebalance trade..a good history lesson

(courtesy Sean Rushton/GATA)

Sean Rushton: Monetary reform would rebalance trade

Submitted by cpowell on Thu, 2018-03-29 15:00. Section: Daily Dispatches

By Sean Rushton

The Wall Street Journal

Wednesday, March 28, 2018

https://www.wsj.com/articles/monetary-reform-would-rebalance-trade-15222…

Contrary to claims coming from some trade hawks, America’s large and persistent trade deficit is not caused primarily by bad trade deals.

The U.S. dollar’s status as the global reserve currency is at least as responsible as any free-trade agreement or unfair practices. High demand for dollars has tilted the playing field against American exporters and workers. Those arguing against tariffs — including Republicans courting blue-collar voters in the industrial Midwest — should be leading the charge for international monetary reform.

Before World War I the international gold standard amounted to an independent, relatively stable and universally accepted global currency. That system broke down during the interwar years. Then, at the Bretton Woods conference after World War II, the victorious Allies decided that the U.S. dollar, backed by gold, would be the international reserve currency to which exchange rates would be fixed. But this “gold exchange standard” was fatally flawed: The world’s need for dollar reserves soon outstripped America’s gold supply.

In the 1950s and ’60s, the U.S. ran big trade deficits with its Cold War allies Japan and Germany, as they rebuilt their manufacturing bases and stockpiled dollars. By the early 1970s, American policy makers were fed up. They severed the dollar’s link to gold and allowed the greenback’s value to float relative to other currencies, in the hope that it would depreciate and smoothly reduce the trade deficit.

The opposite happened. No longer bound by fixed exchange rates and dollar convertibility, the U.S. government’s fiscal discipline broke down. Federal debt as a percentage of gross domestic product, which had been falling since the end of World War II, soon began rising steadily. As a matter of national income accounting, Johns Hopkins economist Steve Hanke has explained, a rising fiscal deficit means a rising trade deficit.

In the bedlam of floating exchange rates, demand for dollars soared. Many nations abhorred having their currencies—and thus their economies—jerked up and down because of decisions made by central bankers in the U.S. and other large economies. To defend against crises, especially at times of major U.S. monetary easing or depreciation, foreign governments stockpiled dollars. In 1973 the world held $500 billion in foreign-exchange reserves (in 2017 dollars); last year it was $11 trillion, a 22-fold increase. About two-thirds of total reserves are now denominated in dollars. Because of high global demand, the dollar’s international position is always stronger and U.S. interest rates are lower than they would be otherwise. This, in turn, means that America’s budget and trade deficits swell in tandem, while U.S. exports are costlier and imports are cheaper, regardless of trade practices.

Such a dynamic has made it difficult for American companies to add manufacturing jobs inside the U.S. Meantime, the finance industry—driven by profits from trading currencies and hedging the associated risk—has grown from about 2% of GDP to more than 9%.

Leveling the playing field will require reducing global demand for dollars, first by stabilizing the dollar and other major currencies, then by establishing a new international reserve currency. Here’s how to do that:

First, to guide monetary policy, Federal Reserve appointees should commit to targeting the real-time prices of an index of commodities, plus foreign currencies and bonds. Such an approach would have prevented the Fed’s biggest recent errors. Easy money in the 1970s and 2000s led to large increases in world dollar holdings, price bubbles and crashes.

Second, the U.S. should invite other major currencies — starting with the second-largest, the euro — to stay steady with the dollar. A dollar-euro stability pact, later including Japan and other democracies, would stabilize demand for dollars. A recent International Monetary Fund communique expressed positive sentiments on this front: “We recognize that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations, and will not target our exchange rates for competitive purposes.”

Third and most controversial, the U.S. and other leading economies should establish a new international currency for pricing global commodities and settling trade accounts. Nations would keep their own currencies for domestic use, exchanging them for the international currency at fixed rates.

The Nobel laureate Robert Mundell suggested such an international currency, to be backed 50% by gold and 50% by the world’s five leading currencies. Rep. Jack Kemp once proposed solving the “reserve currency curse” with a return to the full international gold standard. Other ideas, such as expanded use of the IMF’s reserve asset, the Special Drawing Right, are also worth considering.

If the U.S. has reached the end of its rope and is unwilling to feed the world’s demand for dollars through its trade deficit, then international monetary reform is the answer. It would put U.S. trade on a more level playing field, enforce fiscal discipline in Washington, and help millions of American workers.

—–

Mr. Rushton is director of the Project on Exchange Rates and the Dollar at the Jack Kemp Foundation.

end

Eric states the obvious: with the world sporting a rising indebted world economy, he doubts that any economy could withstand any substantial increases in interest rates.

(courtesy Eric Sprott/Criag Hemke)

Sprott doubts that world can stand rising rates

Submitted by cpowell on Fri, 2018-03-30 02:22. Section: Daily Dispatches

9:22a ICT Friday, March 29, 2018

Dear Friend of GATA and Gold:

Sprott Asset Management’s Eric Sprott, interviewed for Sprott Money by the TF Metals Report’s Craig Hemke, doubts that a spectacularly indebted world economy can stand substantial increases in interest rates. They also discuss the positioning of commercial traders that has become favorable to silver. Sprott argues that gold has been in a bull market for more than two years. The interview is 14 minutes long and can be heard at Sprott Money here:

https://www.sprottmoney.com/Blog/weve-been-in-a-bull-market-for-two-year…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

In the 4th quarter, the USA dollar share of currency reserves has hit a 4 yr low

(courtesy Reuters)

U.S. dollar share of currency reserves hits 4-year low, IMF says

Submitted by cpowell on Sat, 2018-03-31 05:06. Section: Daily Dispatches

From Reuters

via Malay Mail, Kuala Lumpur

Saturday, March 31, 2018

NEW YORK — The U.S. dollar’s share of currency reserves reported to the International Monetary Fund declined in the final quarter of 2017 to a four-year low, as other currencies’ shares of reserves grew, data released yesterday showed.

The share of dollar reserves has declined for four straight quarters as the greenback weakened in 2017 due to faster growth outside the United States and bets that other major central banks would consider reducing stimulus. Still, the dollar has remained the biggest reserve currency by far.

Global reserves are assets of central banks held in different currencies, mainly used to support their liabilities. Central banks sometimes have used reserves to help support their respective currencies.

“Reserve managers in Q4 liked yen and ‘other currencies,'” Steven Englander, head of research and strategy with Rafiki Capital Management, wrote in a research note. “The limited U.S. dollar buying is not surprising. Reserve managers buy dollars when they have to. They rarely want to buy.” …

… For the remainder of the report:

http://www.themalaymailonline.com/money/article/us-dollar-share-of-globa…

end

China is now planning to crackdown on all virtual currencies

(courtesy GATA/Reuters)

China’s central bank plans crackdown on virtual currencies

Submitted by cpowell on Mon, 2018-04-02 08:52. Section: Daily Dispatches

From Reuters

Thursday, March 29, 2018

https://www.reuters.com/article/us-china-finance-digital-currency/china-…

BEIJING — China’s central bank will launch a crackdown on all types of virtual currencies this year, a vice governor of the central bank said Thursday.

The central bank will also push forward the research and development of its own digital currency this year, Fan Yifei said in a statement posted on the website of the People’s Bank of China.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2830 /shanghai bourse CLOSED DOWN 5.71 POINTS OR 0.18% / HANG SANG CLOSED

2. Nikkei closed DOWN 65.72 POINTS OR 0.31% /USA: YEN RISES TO 106.27/

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 89.89/Euro RISES TO 1.2332

3b Japan 10 year bond yield: RISES TO . +.045/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.27/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.25 and Brent: 69.73

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.497%/Italian 10 yr bond yield DOWN to 1.786% /SPAIN 10 YR BOND YIELD DOWN TO 1.164%

3j Greek 10 year bond yield FALLS TO : 4.317?????????????????

3k Gold at $1333.40 silver at:16.52 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 57.39

3m oil into the 65 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.27 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9528 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1755 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.497%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.7530% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 32.985% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Slide With Most Markets On Holiday As China Strikes Back In Trade Wars

Global markets started the new week and quarter with very muted trading in Asia as most key markets including Australia, New Zealand , Hong Kong, Canada, UK and most parts of Europe remain closed for Easter holidays. US stock futures are lower…

…and equities in Asia have given up the gains seen early in the session amid fears of escalating trade wars, while European markets remain offline.

As a reminder, overnight China announced that that starting Monday it would impose tariffs on U.S. products including frozen pork, wine and certain fruits and nuts in response to U.S. duties on imports of aluminum and steel.

MSCI’s world equity index ended up 1.2% last week, but it lost about 1.5% in the first quarter, pushed away from record highs as tensions over global trade escalated, turmoil in the White House deepened and market-leading technology firms wobbled on fears of regulation and other issues. Still, so far the S&P 500 has tested and held the 200d MA twice and has again begun to bounce / stabilize, as all eyes remain on this key technical support level.

“We expect strong and broad-based growth to continue globally,” wrote strategists at Barclays who warned that there were looming risks: “Trade protectionism, U.S. economic policy uncertainty, concerns about higher cross-market volatility and risk premium in core rates markets call for a more tactical approach to risk assets.”

With FX markets on a standstill (more below), the key focus of note today will be China’s new tariffs on 128 US products which officially start today, as well as softer manufacturing PMI data from many countries in Asia.

The main themes remain the same: trade tensions, a dovish start to life under Powell at the Fed, soggy wages and potentially further changes to the Trump administration, Brexit headline risks, rate hike outlooks being pushed forward in the antipodeans, uncertainty around ECB, JPY’s volatility and political risks in EM and for Oil.

What Asian markets were open saw aggressive profit-taking into the close: Chinese stocks erased gains to end Monday at session lows, following their worst quarter in two years. Brokers bucked broad market declines after the central government announced a trial program for Chinese Depositary Receipts. The Shanghai Composite closed down 0.2%, wiping out an earlier advance of 0.7%.

Similarly in Japan, the Topix closes down 0.4%, erasing gain of as much as 0.4%, with volume 20% below 30-day average. Banks were the biggest drag on benchmark, outweighing gain in “other products” gauge. The Nikkei also slumped 0.3% after wiping out a 0.7% rise. Ovenright we got the latest Japan Tankan data: large manufacturers tankan came at 24 (expected 25), with the Japan Tankan manufacturing outlook disappointing at 20 (vs expected 22). The budget rate for USDJPY was lowered a bit from 110.67 to 109.66 during FY2018. CitiFX Strategist Osamu Takashima says, “I believe most of manufacturing companies have lowered it further toward 105 more recently.”

Asian manufacturing PMI for March have mainly disappointed today and while this is not having an impact on the immediate price action, it is something to keep an eye on. Of note, China’s March Caixin manufacturing PMI data came lower than expected at 51.0 versus exp. 51.7.

It has been a quiet start to the FX week as well, with the Bloomberg Dollar Spot Index falling 0.1%, extending the three-day slide to 0.4% although staying within a tight range, amid muted trading due to the Easter holiday. The pound led gains among G-10 currencies at the start of a week flooded with tier-one data releases out of the U.S, while the yen was marginally weaker after Tankan survey slips.

Of note: for Monday, the The People’s Bank of China raised the daily reference rate for the yuan to strongest since Aug. 11, 2015, aka the “day of the devaluation”, as the dollar weakened: PBOC raised the yuan reference rate by 0.19% to 6.2764 per dollar. The fixing was in line with expectations: average estimate in Bloomberg survey of 17 traders and analysts was 6.2762. Some of the other notable FX moves, from Bloomberg:

- The Bloomberg Dollar Spot Index falls 0.1%; the measure declined for a fifth straight quarter, ended March 30, its worst run since March 2008

- The pound is the biggest mover amid thin trading as some markets in Asia and Europe remained shut for Easter holidays

- Sterling rises for the first time in five days versus the dollar, climbing 0.4% to $1.4064; rises 0.3% to 87.67 pence against the euro

- The Japanese yen is little changed during London hours after weakening slightly in Asia; analysts project it will weaken against all its G-10 peers this quarter; USD/JPY is forecast to climb to 108 by the end of June, from the current level of 106.35, the median estimate in a Bloomberg survey shows

- U.S. 10-year Treasury yield climbs 2bps to 2.76% after its third straight quarterly advance in the period through March 30

Crude oil prices extended gains, lifted by a drop in U.S. drilling activity as well as by expectations that the United States could re-introduce sanctions against Iran. U.S. drillers cut seven oil rigs in the week to March 29, bringing the total count down to 797. It was the first time in three weeks that the rig-count fell. U.S. crude futures rose 0.3 percent to $65.14 a barrel and Brent advanced 0.5 percent to $69.67 a barrel.