GOLD: $1333.40 UP $2.90 (COMEX TO COMEX CLOSINGS)

Silver: $16.30 DOWN 11 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1333.30

silver: $16.32

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR 595 FOR 59500 OZ (1.8506 tonnes)

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 19 for 90,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7035/OFFER $7135: DOWN $331(morning)

Bitcoin: BID/ $6845/offer $6945: DOWN $570 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE BY 4457 contracts from 229131 RISING TO 232,682 DESPITE YESTERDAY’S STRONG 26 CENT FALL IN SILVER PRICING. OBVIOUSLY, WE HAD ZERO COMEX LIQUIDATION. HOWEVER WE ALSO WITNESSED ZERO COMEX SHORT COVERING. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1220 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 5677 CONTRACTS. WITH THE TRANSFER OF 1220 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1220 CONTRACTS TRANSLATES INTO 6.10 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

5032 CONTRACTS (FOR 3 TRADING DAYS TOTAL 5032 CONTRACTS) OR 25.16 MILLION OZ: AVERAGE PER DAY: 1677 CONTRACTS OR 8.386 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 25.16 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.59% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 743.65 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED GAIN IN COMEX OI SILVER COMEX OF 4457 DESPITE THE 26 CENT FALL IN SILVER PRICE. HOWEVER, WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 1220 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1220 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 5677 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 1220 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 4457 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 26 CENTS AND A CLOSING PRICE OF $16.41 WITH RESPECT TO TUESDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.1635 BILLION TO BE EXACT or 166% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER, WE ARE NOW 2,000 CONTRACTS AWAY FROM RECORD LEVELS AND YET THE SILVER PRICE IS EXTREMELY LOW

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 232,600 CONTRACTS (OR 1.163 BILLION OZ/

- HUGE EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOWER PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT JPMORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

In gold, the open interest FELL BY GOOD SIZED 8274 CONTRACTS DOWN TO 494,141 ACCOMPANYING THE STRONG SIZED FALL IN PRICE/YESTERDAY’S TRADING ( LOSS OF $9.30). AS WE ENTER THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A RATHER LARGE SIZED 9691 CONTRACTS : JUNE SAW THE ISSUANCE OF 9291 CONTRACTS AND SURPRISINGLY APRIL AT 400 CONTRACTS (SOMEBODY IN URGENT NEED OF GOLD) THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 493,141. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 8274 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 9691 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 1417 CONTRACTS OR 141700 OZ =4.407 TONNES

YESTERDAY, WE HAD 3180 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 27,640 CONTRACTS OR 27,64,000 OZ OR 85.972 TONNES (3 TRADING DAYS AND THUS AVERAGING: 9213 EFP CONTRACTS PER TRADING DAY OR 921,300 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 2 TRADING DAYS IN TONNES: 85.972 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 85.972/2550 x 100% TONNES = 3.337% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2130.44 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED DECREASE IN OI AT THE COMEX WITH THE STRONG SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($9.30 LOSS). WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9691 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9691 EFP CONTRACTS ISSUED, WE HAD A GOOD NET GAIN IN OPEN INTEREST OF 1417 contracts ON THE TWO EXCHANGES:

9691 CONTRACTS MOVE TO LONDON AND 8274 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 4.407 TONNES).

we had: 8 notice(s) filed upon for 800 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $2.90 : WE HAD NO CHANGES IN GOLD TONNAGE AT THE GLD/

Inventory rests tonight: 852.31 tonnes.

SLV/

WITH SILVER DOWN 11 CENTS TODAY: A SMALL CHANGE/ A WITHDRAWAL OF 135,000 OZ TO PAY FOR FEES.

/INVENTORY RESTS AT 318.877 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 4457 contracts from 229,131 UP TO 232,682 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787. THE PRICE OF SILVER ON THAT DAY: $17.89) DESPITE THE STRONG SIZED FALL IN PRICE OF SILVER (26 CENTS// YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1220 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 4457 CONTRACTS TO THE 1220 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 5677 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 28.38 MILLION OZ!!!

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE GOOD SIZED FALL IN SILVER PRICING / YESTERDAY (26 CENTS) . BUT WE ALSO HAD ANOTHER VERY GOOD SIZED 1220 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 5.52 POINTS OR 0.18% /Hang Sang CLOSED DOWN 661.41 POINTS OR 2.19% / The Nikkei closed UP 27.26 POINTS OR .13%/Australia’s all ordinaires CLOSED UP .08% /Chinese yuan (ONSHORE) closed DOWN at 6.3077/Oil DOWN to 62.36 dollars per barrel for WTI and 66.86 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.3077 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3094 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY POOR CHINESE MARKETS/CHINA RETALIATES WITH TARIFFS/LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

i)This will develop into a full scale trade war as the USA just released their list targeting 1300 products. This has the makings of a full scale trade war which will inevitably cause all markets to crash. We now await China’s response!!

( zerohedge)

ii)China responds with a vengeance!! They are striking back with a strong 25% tariffs on 50 billion dollars worth of USA imports.

( zerohedge)

iii)Your most important read this year…why China’s soybean tariffs will change everything. The USA exports a huge 12 billion USA dollars of soybeans to the Chinese who use the beans for their feedstock (pigs) as their plantings will only suffice for human consumption. China consumes 60% of all soybean global production. This will hurt not only the USA exporters but also the Chinese as it will drive up inflation and global costs for livestock and just about everything. The risk to the globe is runaway inflation.

( zerohedge)

iv)Trump’s dilemma: the stock market or a trade war..he picked a trade war as “this is a long term thing…”

( zerohedge)

4. EUROPEAN AFFAIRS

Strange: the UK foreign office now denies it is claiming Russian is responsible for the nerve agent poisoning as it deletes tweets on the subject

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

a must read..

(courtesy Bill Blain/Mint Partners)

(courtesy Mac Slavo/SHFTPlan.com)

iii)Your list of winners and loser and we have mostly losers from the trade war:

(courtesy zerohedge

iv)Canada and Mexico get a little break as the White House caves in on a small NAFTA demand

( zerohedge)

7. OIL ISSUES

Oil prices and gasoline rebound after a surprise crude draw

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Essential reading: Chris Powell’s correct interpretation of why London is backward in gold

( Chris Powell/Bron Suchecki)

ii)Craig Hemke at Sprott outlines that gold is no longer pairing with the Japanese yen but pairs only with the dollar or the Euro. Supply and demand no longer enter the equation for gold pricing and the movement of gold/silver is determined by the high frequency trading.

( Craig Hemke/Sprott)

10. USA stories which will influence the price of gold/silver

i)Trading this morning

Dow opens down 400 points:

( zerohedge)

ii)One complete joke!! stocks stage a comeback after the bozo, Larry Kudlow urged the market not to overreact

( zerohedge)

iii)Market data this morning

Expectations was for an ugly USA service sector slump but the numbers were not as bad. However this soft data report signals tariff turmoil straight ahead;

( zerohedge)

iv)Trump had dinner with the Co CEO of Oracle who is Amazon’s competitor in the cloud based computing contracts which are huge. Amazon makes all of its money on the cloud services and this funds his distribution business. Trump is angry that Amazon pays little taxes and uses the USPS despite the fact that the USA mail has lost money every single year. The markets will tank on this and on the Chinese implementation of tariffs on soybeans.

( zerohedge)

v)The Amazon effect: mall vacancies are now at a 6 year high.

( zerohedge)

vi)We have pointed out to you that the primary reason for the continual rise in Lobor -OIS or stress in the banking sector was due to the repatriation of dollars from Europe back into the USA. Matt King states that there is another likely candidate for the rise: the Fed’s roll off on bonds which this month commences with the roll off of 30 billion usa. No question: both are contributing to the rise.

(courtesy zerohedge)

a)A new ploy by Mueller as he tells Trump’s lawyers that the President is not a criminal target but remains a “subject”. His goal is to get him for an interview and then possibly charged for perjury

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:328875 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 298,381 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE 4457 CONTRACTS FROM 228,225 UP TO 232,682 DESPITE OUR STRONG 26 CENT FALL IN SILVER PRICING/ YESTERDAY). ALSO,WE WERE ALSO INFORMED THAT WE HAD A FAIR 1220 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1220. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE SURPRISINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION BUT THAT WAS SHORT COVERING, AND WE ALSO HAVE A VERY GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 5677 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 4457 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1220 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:5677 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 0 contracts REMAINING AT 342 contracts. We had 0 notices filed upon (CME correction last Thursday night) so in essence we lost 0 contracts or NIL additional ounces of silver will stand for delivery in this non active delivery month of April.

The next big active delivery month for silver will be May and here the OI LOST 572 contracts DOWN to 149,180. June saw its THIRD gain of 1 contract to stand at 10. The next big delivery month for silver is July and here the OI rose by 4867 contracts up to 47,894.

We had 0 notice(s) filed for NIL OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 4/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

3215.000 oz

100 kilobars

Scotia

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

8 notice(s)

800 OZ

|

| No of oz to be served (notices) |

1993 contracts

(199300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

595 notices

59500 OZ

1.8506 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 14 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (595) x 100 oz or 59500 oz, to which we add the difference between the open interest for the front month of APRIL. (2001 contracts) minus the number of notices served upon today (8 x 100 oz per contract) equals 258,800 oz, the number of ounces standing in this active month of APRIL (8.049 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (595 x 100 oz or ounces + {(2001)OI for the front month minus the number of notices served upon today (8 x 100 oz )which equals 258,800 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 166 COMEX OI CONTRACTS OR 16600 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil

oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

638,049.590 oz

Delaware

HSBC

|

| No of oz served today (contracts) |

0

CONTRACT(S

NIL OZ)

|

| No of oz to be served (notices) |

342 contracts

(1,710,000 oz)

|

| Total monthly oz silver served (contracts) | 19 contracts

(95,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) Into Delaware: 34,882.690 ox

iii) Into HSBC: 603,166.900 oz

total deposits today: 638,049.590 oz

we had 0 withdrawals from the customer account;

total withdrawals; nil oz

we had 0 adjustment

total dealer silver: 58.8561 million

total dealer + customer silver: 262.106 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 19 x 5,000 oz = 95,000 oz to which we add the difference between the open interest for the front month of April. (342) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 19(notices served so far)x 5000 oz + OI for front month of April(342) -number of notices served upon today (0)x 5000 oz equals 1,805,000 oz of silver standing for the April contract month

WE NEITHER GAINED NOR LOST ANY SILVER OUNCES STANDING IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 106,114 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 106768 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 106,768 CONTRACTS EQUATES TO 533 MILLION OZ OR 76.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.17% (APRIL 2/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.66% to NAV (APRIL 2/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.17%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.66%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.90%: NAV 13.67/TRADING 13.30//DISCOUNT 2.90.

END

And now the Gold inventory at the GLD/

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 4/2018/ Inventory rests tonight at 852.31 tonnes

*IN LAST 355 TRADING DAYS: 88.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 305 TRADING DAYS: A NET 67.57 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 4/2018: NO CHANGES IN SILVER INVENTORY:

Inventory 318.877 million oz

end

6 Month MM GOFO 2.01/ and libor 6 month duration 2.45

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.01%

libor 2.45 FOR 6 MONTHS/

GOLD LENDING RATE: .44%

XXXXXXXX

12 Month MM GOFO

+ 2.45%

LIBOR FOR 12 MONTH DURATION: 2.67

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.22

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

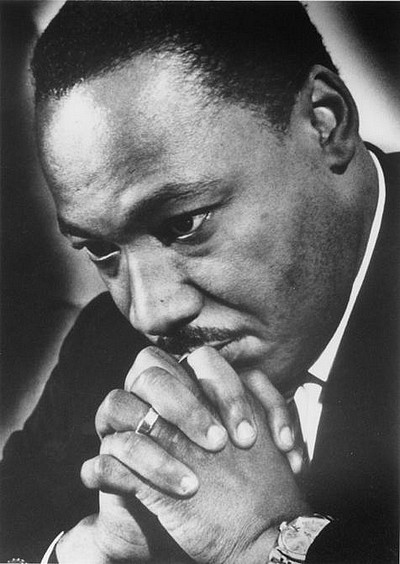

Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Civil rights leader Martin Luther King Jr. assassinated 50 years ago today

– An anti-war campaigner, protesting against the damage inflicted by military operations

– King was almost prophetic in his vision that wars would drive a bigger wedge between rich and poor

– Foresaw the damage that would come to US in terms of costs to society and the economy

– Fifty years on Western nations can learn from King’s words when it comes to considering costs of war

– War is financed by debt bringing significant financial burdens on investors, savers and future generations

Today is the fiftieth anniversary of the assassination of civil rights leader Martin Luther King. He not only fought for the rights of minorities but he spoke out against inequality and the damage done by war.

In the fifty years passed we have perhaps not had a year full of such political, emotional and economical upset as we have in the last twelve months or so.

In this time we have had a convergence of major political shifts, civil rights campaigns, saber-rattling between nuclear powers and the rise of populism. This is something that has arguably not been seen at this level for many years previous.

This convergence has lead to a world that seems fraught on many levels and on the precipice of change. What kind of change is up for debate by many sides. Sadly attempts at change can be followed by violence and war, from all parties. Whether it’s civil rights movements such as Black Lives Matter, gun control demonstrations or more global efforts such as Trump’s attempts to affect the Middle East in some way, North Korea’s desire to gain respect around the globe or Russia’s keenness to demonstrate its strength against the West – each may end in violence and military action.

Martin Luther King was known for many things – an equal rights campaigner, a economic campaigner and a peace campaigner. All qualities that are appreciated today as much as they were fifty years ago. He fought to highlight the dramatic costs to society and the economy when it came to war – whether civil or otherwise.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Campaigner for peace and non-violent demonstration for change

King’s words resonate as strongly today as they did fifty years ago, less than a week before his death:

I want to say one other challenge that we face is simply that we must find an alternative to war and bloodshed. Anyone who feels, and there are still a lot of people who feel that way, that war can solve the social problems facing mankind is sleeping through a great revolution. President Kennedy said on one occasion, “Mankind must put an end to war or war will put an end to mankind.” The world must hear this. I pray to God that America will hear this before it is too late, because today we’re fighting a war. Martin Luther King, Jr., Remaining Awake Through a Great Revolution, 31 March 1968

King was openly critical of the US government and their military policies, referring to them as “the greatest purveyor of violence in the world today.” He was prophetic in his declarations as to the damage military operations could do to the US at it pursued military activities both at home and abroad.

Exactly one year before his death, on April 4th 1967, King gave a speech in protest of the war in Vietnam. Of the US he said: “a nation that continues year after year to spend more money on military defense than on programs of social uplift is approaching spiritual death.”

He warned of the widening gap between rich and poor at home whilst spending on military operations abroad increased disproportionately. This is more glaringly obvious today than it was fifty years ago. Western countries are entangled in military exercises around the world, with no means with which to pay for them. Countries on both sides of the field are driven further into debt, with far lasting consequences for their citizens.

The true cost of war

The 2017 Global Peace Index found that violence cost 12.6% of global GDP. This means that the economic impact of violence on the global economy in 2016 was $14.3 trillion in purchasing power parity (PPP) terms, the equivalent of $5.40 per person, per day.

This gives no indication to the direct financial cost of war. By way of example a report from Brown University’s Watson Institute for International and Public Affairs finds that finds that an average American taxpayer has spent $23,386 on post-9/11 wars. The report estimates that by the end of this year the overall U.S. spending on wars in Iraq, Syria and Afghanistan could reach $5.6 trillion.

This is just direct spend. Study author Neta Crawford explained that ‘future interest payments on borrowing for the wars will likely add more than $7.9 trillion to the [US] national debt…Thus, even if military spending plateaus, interest costs will far surpass total war costs unless Congress devises another plan to pay for the wars, for instance by selling war bonds or increasing taxes’

In the modern Western world wars are financed by borrowing. Borrowing is a debt on future generations and a cost to society from day one. It is the opportunity cost of money going towards domestic projects such as healthcare, education, social mobility and infrastructure.

The Watson Institute Cost of War project reminds us of the following:

- The human and economic costs of these wars will continue for decades with some costs, such as the financial costs of US veterans’ care, not peaking until mid-century.

- US government funding of reconstruction efforts in Iraq and Afghanistan has totaled over $170 billion. Most of those funds have gone towards arming security forces in both countries. Much of the money allocated to humanitarian relief and rebuilding civil society has been lost to fraud, waste, and abuse.

- War spending created fewer jobs than similar spending investment in clean energy, public education, and health care.

- Federal investment in military assets during the wars made for a lost opportunity to significantly boost capital improvements in core infrastructure such as roads and public transit.

- War spending financed entirely by debt has contributed to higher interest rates charged to borrowers such as new homeowners.

The final point regarding interest rates is key for investors to pay attention. Whilst higher interest rates may seem like an excellent reason to hold interest-bearing assets, in truth the wider impact they can have on an heavily indebted economy can be devastating.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Who will end up paying for the abandonment of King’s dream?

An indebted economy means an indebted people which inevitably leads to major financial upset. It wouldn’t come as a surprise to find ourselves in yet another situation where investors exposed to the financial system are being called upon (read: told) to support the economy and banking system. Hard-earned assets would not be safe should the government perceive a better use for them.

There are many side-effects of wartime, one of the most long-lasting is the financial impact on individuals’ savings. Nowadays ‘war’ does not just means guns and tanks, it can be trade wars or currency wars. Sadly, they’re not exclusive of one another.

Trade wars frequently turn to currency wars. These decimate the capital of companies and the wealth of people and nations. It can also result in stocks and shares losing value sharply and crashing. Governments in any kind of war can be ‘forced’ to devalue people’s savings and in the next crisis, bail-ins will likely see savers’ accounts plundered … all for the public good.

This is where gold bullion comes into its own. Throughout history it has acted as a safe haven during times of protectionism and economic war. This was seen most recently in the 1970s.

The world was already a very uncertain financial and economic place with a lot of clouds on the horizon. Trump’s reckless actions have made this outlook even more uncertain. This bodes well for the gold price in the coming months and years.

Safe haven gold bullion will come into its own as these real risks become manifest.

News and Commentary

Gold steady as China-U.S. trade tensions escalate (Reuters.com)

Stocks in Asia Trade Mixed; Treasuries Steady (Bloomberg.com)

BlackRock’s $1.3 Billion Gold Fund Feels Pain of Miners (Bloomberg.com)

Sberbank to increase gold sales to India and China in 2018 (Reuters.com)

The Gold Price Driver (GoldSeek.com)

And The Fastest Growing Bank Asset in 2017 Was… Subprime (ZeroHedge.com)

Why April Showers the Pound With Good Fortune (Bloomberg.com)

Trade Tensions Are Already Hitting Industrial-Metal Prices (Bloomberg.com)

MARKET MELTDOWN CONTINUES: Gold And Silver Prices Begin To Disconnect (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

03 Apr: USD 1,336.60, GBP 949.65 & EUR 1,085.99 per ounce

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

Silver Prices (LBMA)

03 Apr: USD 16.52, GBP 11.78 & EUR 13.44 per ounce

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

Recent Market Updates

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Crock Of Gold Hidden In Ireland? Happy Saint Patrick’s Day

– Buy Silver And Sell Gold Now

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Essential reading: Chris Powell’s correct interpretation of why London is backward in gold

(courtesy Chris Powell/Bron Suchecki)

Intervention may best explain anomalies in the gold market

Submitted by cpowell on Tue, 2018-04-03 12:15. Section: Daily Dispatches

8:23p HKT Tuesday, April 3, 2018

Dear Friend of GATA and Gold:

In an essay at the Monetary Metals blog headlined “Backwardation, the Bank of England, and Falling Prices” ––

https://monetary-metals.com/backwardation-the-bank-of-england-and-fallin…

— the firm’s vice president of operations, Bron Suchecki, offers an explanation of one of the anomalies of the gold market, backwardation (when prices for immediate or spot delivery are higher than prices for future delivery) happening while prices generally are falling. For backwardation usually indicates supply shortages, difficulty meeting demand.

Suchecki writes: “However, in the case of gold, the fact that the stock of gold above ground is equal to over 60 years’ worth of mine production means that gold is not a typical commodity and cannot really ever be in shortage.”

Of course Suchecki is right that gold, unlike other commodities, like oil and wheat, is hoarded rather than consumed. But what if unbacked paper claims equal to a thousand years of gold production have been issued and demands for delivery of those unbacked claims suddenly increase?

Of the smash of the gold price in April 2013, Suchecki writes: “The falling forward (basis) rate indicated that it was futures prices which were falling faster than spot, closing the gap, until futures fell below spot, giving us negative Monetary Metals GOFO. The driver for this behavior is the leverage inherent in futures contracts: Futures traders are under more pressure to liquidate positions, once they move against them, than those holding fully paid physical (spot) gold.”

But what if in April 2013 futures positions were not being liquidated by ordinary traders at all but, instead, governments and central banks were using their power of infinite money creation to dump many more unbacked paper claims on the gold market to frighten non-official-sector holders of gold into selling both their futures and physical positions, whereupon central banks could cover their short positions at a profit or at least knock down physical demand, thereby protecting their currencies and government bonds?

Central bank and government archives are full of official plans and speculation about selling gold to suppress prices or spook the market. Further, the records of the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission and CME Group, operator of the major U.S. futures exchanges, show that in recent years central banks and governments have been secretly trading all commodity and financial futures contracts in the United States:

GATA long has argued these points:

1) Formulas and charts about monetary metals prices and indeed all commodity and financial futures prices are of limited value without knowledge of what central banks and governments are doing in the markets.

2) If central banks and governments, creators and allocators of infinite money, are secretly trading markets, there really are no markets at all, just interventions.

3) The gold market analysis business suffers an amazing lack of curiosity about what governments and central banks are doing in the market.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Craig Hemke at Sprott outlines that gold is no longer pairing with the Japanese yen but pairs only with the dollar or the Euro. Supply and demand no longer enter the equation for gold pricing and the movement of gold/silver is determined by the high frequency trading.

(courtesy Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Gold price driver isn’t dollar/yen pairing anymore

Submitted by cpowell on Wed, 2018-04-04 00:12. Section: Daily Dispatches

8:14a HKT Wednesday, April 3, 2018

Dear Friend of GATA and Gold:

The driver of the gold price, the TF Metals Report’s Craig Hemke writes at Sprott Money today, no longer seems to be its correlation with the Japanese yen’s pairing with the U.S. dollar but rather with the dollar itself or the euro. In any case, Hemke asserts, the gold price long ago lost any correlation with physical supply and demand and now is determined largely by algorithm-based high-frequency trading.

Who is doing that HFT trading? Hemke doesn’t say. But if gold market analysts who deny that the market is comprehensively manipulated by central banks ever worked up the curiosity and initiative to visit the Federal Reserve Bank of New York or the Bank for International Settlements in Basle, Switzerland, during market hours and asked for a tour of the trading room, they might receive a powerful hint when the slammed door struck them in the face.

Hemke’s analysis is headlined “The Gold Price Driver” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-gold-price-driver-craig-hemke-03-04…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

John Embry at Kingworldnews claims correctly that the volatility is scaring central banks to death.

(courtesy John Embry/Kingworldnews)

(GATA) Stock market volatility scares central banks, Embry tells KWN

Submitted by cpowell on 02:40PM ET Wednesday, April 4, 2018. Section: Daily Dispatches

10:40p HKT Wednesday, April 4, 2018

Dear Friend of GATA and Gold:

Central banks are terrified by the new volatility in the U.S. stock market, Sprott Asset Management’s John Embry tells King World News today, as that sort of thing ordinarily signals a change in trend. Embry expects that the future holds either a depression or hyperinflation. His comments are excerpted at KWN here:

https://kingworldnews.com/look-who-just-said-he-hasnt- seen-anything-like-this-in-55-years/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3077 /shanghai bourse CLOSED DOWN 5.52 POINTS OR 0.18% / HANG SANG CLOSED DOWN 661.41 POINTS OR 2.19%

2. Nikkei closed UP 27.26 POINTS OR .13%/ /USA: YEN FALLS TO 106.15/

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index FALLS TO 90.14/Euro RISES TO 1.2280

3b Japan 10 year bond yield: RISES TO . +.033/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.15/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.36 and Brent: 66.86

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.485%/Italian 10 yr bond yield DOWN to 1.744% /SPAIN 10 YR BOND YIELD DOWN TO 1.168%

3j Greek 10 year bond yield FALLS TO : 4.147?????????????????

3k Gold at $1343.60 silver at:16.48 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 26/100 in roubles/dollar) 57.86

3m oil into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.15 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9587 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1773 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.485%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.753% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.997% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dow Plunges 600, Global Markets Tank After China Retaliates In All-Out Trade War

So much for yesterday’s Amazon bounce.

Just before 4AM EDT, a Bloomberg headline hit which has not only unleashed a furious global selling wave, sending the S&P lower by nearly 2% and the Dow 600 lower, but may have changed the course of history: that’s when China announced it was striking back in the ever faster and more furious trade war between the US and China:

While we detailed the response earlier, for those who missed it, China announced it would launch reciprocal tariffs on 106 US products worth $50bln in bilateral trade, setting a new tariff rate of 25% on soybean, autos and chemicals. While the Chinese response was expected, the inclusion of soybeans was not, and will likely infuriate Navarro/Trump and lead to another round of US tariffs. China Ministry of Commerce also said it would adjust tariffs on ethylene glycol and diethylene glycol sold by firms including Dow Chemical (DOW), Ineos and BASF (BAS GY) among others.

And in an ominous warning that more is coming, China said that while its door to the US remains open for negotiations, if the US wants to keep fighting, China will hold onto the last, according to the Chinese Vice Commerce Minister.

The result was a freefall in both S&P futures, which were down nearly 50 points from Tuesday’s close…

… but also in the Dow Jones, which plunged as much as 600 points…

… and, of course, Emerging Markets, with the MSCI EM stock index heading for its lowest close in two months with EM currencies a sea of red across the board.

And speaking of sea of red, this is what global cash markets and futures look like right now.

And while we previously discussed China’s response, which for now includes a 25% tariffs on 106 items with a trade value of $50 billion, traders are already thinking about what happens next, should Trump proceed to a third round of measures. Commenting on this, Alicia Garcia Herrero, chief Asia-Pacific economist at Natixis, said that “China will probably reduce its net purchases of U.S. Treasuries, as it has done from the beginning of the year, but more rapidly. This should push up longer-term yields in the U.S. but also widen spreads of investment grade U.S. credit.” There is also the FX angle: “There is a chance (although I doubt it will be immediate) that the PBOC engineers a staggered depreciation of the renminbi against the dollar.”

For now, however, keep an eye on the plunge in Boeing which is down 6% this morning, and soybeans, the most important US food import into China…

… whose price is plunging this morning as a result of China’s unexpected announcement the commodity would make the list.

Amusingly, China picked a good time to retaliate, with its own markets closed for the rest of the week, even if industrial metals were hammered overnight as one would expect.

To be sure (as the charts above reveal) the return of trade wars front and center dominated traders’ attention, as global markets reacted in traditional risk-off fashion: the USD/JPY slumped, with 106 so far proving support; AUD was weaker across the board given correlation to China demand and commodities, while the yuan weakened into North American crossover. The euro filled stops above $1.23 as short-term accounts were caught short.

Mining and tech sectors lead European equity markets lower, while risk-off assets such as USTs and bunds, rallied. The Treasury curve steepened and credit spreads edge wider.

Oil was trading at session lows in response to China’s retaliation; oil prices continued to slip further after yesterday’s APIs, which showed a surprise drawdown of 3.3mln for headline crude, but a build in the other product components. Gold climbed higher as risk-aversion spreads across the market and flows move into safe-havens. Base metals also suffered losses after more tariffs were imposed on steel and as trade war fear continues to dictate global sentiment with copper futures -2%, and soybeans, as noted previously, tumbled -5%

Market Snapshot

- S&P 500 futures down 1.5% to 2,576.25

- STOXX Europe 600 down 0.8% to 365.98

- MSCI Asia Pac down 0.6% to 171.05

- MSCI Asia Pac ex Japan down 1.2% to 556.76

- Nikkei up 0.1% to 21,319.55

- Topix up 0.1% to 1,706.13

- Hang Seng Index down 2.2% to 29,518.69

- Shanghai Composite down 0.2% to 3,131.11

- Sensex down 1% to 33,044.75

- Australia S&P/ASX 200 up 0.2% to 5,761.35

- Kospi down 1.4% to 2,408.06

- German 10Y yield fell 0.5 bps to 0.496%

- Euro up 0.2% to $1.2300

- Italian 10Y yield rose 0.7 bps to 1.539%

- Spanish 10Y yield fell 0.6 bps to 1.184%

- Brent futures down 1.8% to $66.93/bbl

- Gold spot up 0.8% to $1,343.23

- U.S. Dollar Index down 0.2% to 90.06

Top Overnight News

- China said it would levy 25 percent tariffs on imports of 106 U.S. products including soybeans, automobiles, chemicals and aircraft, in a tit-for-tat response to proposed American duties on its high-tech goods

- The Ministry of Commerce in Beijing said the charges will apply to around $50 billion of U.S. imports, a step that ratchets up tension in a brewing trade war between the world’s two largest trading nations

- Chinese companies scrambled to assess the impact of proposed U.S. tariffs on 1,300 products after President Donald Trump’s scattergun approach hits a wide- ranging list of products

- China’s State Administration of Foreign Exchange will give higher priority on preventing and curbing risks from foreign-exchange market and cross-border capital flows, according to a statement

- Euro-area inflation accelerated last month, buttressing the arguments of policy makers keen to phase out unprecedented stimulus

- The Bank of Japan’s record purchases of local stocks helped a market deserted by foreign investors. The BOJ spent 833 billion yen ($7.8 billion) on exchange-traded funds tracking the country’s shares last month, the biggest amount in data stretching back to late 2010

- Four U.S. pipeline companies have reported their electronic systems for communicating with customers were shut down over the last few days, with three confirming it resulted from a cyberattack

- Trump’s shrinking legal team has opened a gap in criminal law expertise that could expose him to legal risk if he agrees to be interviewed by Special Counsel Robert Mueller

Asia traded somewhat indecisive as the region failed to take full impetus from the rebound on Wall St, where all major indices recovered lost ground and reprieve for tech stocks pushed the Nasdaq back into the green YTD. ASX 200 (+0.1%) and Nikkei 225 (+0.1%) initially caught a tail wind from the momentum stateside and both opened higher, but then failed to hold on to the gains as trade concerns lingered after the US announced its proposed China tariff list. This was met by condemnation from China which is also said to be planning reciprocal tariffs of equal scale and strength. Conversely, Hang Seng (-2.2%) was choppy and Shanghai Comp. (+0.2%) shrugged-off the trade tensions and disappointing Caixin PMI data, to trade with a positive tone ahead of the extended weekend for the mainland and following reports of a USD 9.7bln bailout for Chinese conglomerate Anbang Insurance. Finally, 10yr JGBs were uneventful amid the indecisive risk tone in the region and as JGBs took a breather from yesterday’s gains which saw the 20yr yield drop to its lowest since late 2016. The BoJ were also present in the market under its bond buying program for 1yr-10yr JGBs, although it maintained the purchase amounts in line with the prior. Chinese Caixin Services PMI (Mar) 52.3 vs. Exp. 54.5 (Prev. 54.2). Chinese Caixin Composite PMI (Mar) 51.8

Top Asian News

- Hong Kong Stocks Erase 2018 Gain as China Bites Back at U.S.

- Meituan Is Said to Buy Bike Startup in $3.4 Billion Deal

- China Injects $9.7 Billion Into Anbang After Fraud Alleged

- Toshiba’s New CEO Says Chip Sale Will Proceed Even With Hurdles

Markets have been shaken up amid China’s most recent tit-for-tat tariff announcement on 106 US products. As a result, European equities have slipped firmly into the red (Eurostoxx 50 -1.3%). The tech sector opened softer following US President Trump proposing a tariff list on China consisting mostly of tech products. Industrials and materials have edged lower amid fears of a lag in global growth as trade disputes escalate. Energy and utilities are the only sectors in the green. Elsewhere, in terms of stocks specifics, WPP (-1.8%) is lower as CEO Martin Sorrell is under investigation for misconduct claims. Swiss Re (-3.4%) shares are lower following reports the company is in talks with Softbank over a minority stake of no more than 10%.

Top European News

- U.K. Construction, Hit by March Snow, Shrinks Most Since 2016

- Italian Unemployment Falls in Key Signal for Government Talks

- Euro-Area Inflation Ticks Up as ECB Prepares to Unwind Stimulus

- Putin’s Stealth Economic Weapon Loses Punch as Recovery Falters

In currencies, the Dollar index is clinging to 90.000+ levels amidst more US vs China import tariff measures and countermeasures as the trade war ratchets up a few more notches. JPY was one of the more volatile majors again, but this time on broader risk sentiment factors rather than BoJ policy statements and misperceptions. Usd/Jpy hit highs near 106.70 overnight, but is now retreating through modest bids at 106.40 to a circa 106.00 low as China backs up strong words with action via 25% taxes on 106 US products totalling Usd50 bn (ie equal and opposite to the US). EUR/CHF was firmer vs the retreating Greenback and revisiting recent peaks (around 1.2300+ and 0.9550 respectively) as aversion and safe-haven positioning resurfaces. EUR was largely unphased by the latest Eurozone CPI data with the headline printing in-line with expectations. Sterling was undermined by a much weaker than expected UK Construction PMI (47.0 vs. consensus 50.9), with cable down below 1.4050 vs almost 1.4100 at best and Eur/Gbp close to 0.8750 from near 0.8715. Loonie lost some NAFTA-related gains and the headline pair back over 1.2800 vs 1.2775 earlier, with the global trade rift threatening to undermine if not neutralise any positives from a tri-party agreement between Canada, the US and Mexico. USD/CNY was up sharply on the latest US-Chinese protectionism offensives to around 6.3000 vs the PBOC’s 6.2926 mid-point fix.

In commodities, oil is trading at session lows after China responded with extensive retaliatory measures against the US. Oil prices continue to slip further after yesterday’s APIs, which showed a surprise drawdown of 3.3mln for headline crude, but a build in the other product components. Looking at the metal complex, gold climbs higher as risk-aversion spreads across the market and flows move into safe-havens. Base metals also suffered losses after more tariffs were imposed on steel and as trade war fear continues to dictate global sentiment.

Looking at the day ahead, we’ll get the March ADP employment print, final PMI revisions for March (services and composite), ISM non-manufacturing for March, factory orders data for February and final durable and capital goods orders revisions for February. The Fed’s Bullard and Mester are also scheduled to speak.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 4.8%

- 8:15am: ADP Employment Change, est. 210,000, prior 235,000

- 9:45am: Markit US Services PMI, est. 54.2, prior 54.1; Composite PMI, prior 54.3

- 9:45am: Fed’s Bullard Speaks on U.S. Economy and Monetary Policy

- 10am: ISM Non-Manf. Composite, est. 59, prior 59.5

- 10am: Factory Orders, est. 1.7%, prior -1.4%; Ex Trans, prior 0.4%

- 10am: Durable Goods Orders, prior 3.1%; Durables Ex Transportation, prior 1.2%

- 10am: Cap Goods Orders Nondef Ex Air, prior 1.8%; Cap Goods Ship Nondef Ex Air, prior 1.4%

- 11am: Fed’s Mester Speaks on Diversity in Economics

DB’s Jim Reid concludes the overnight wrap

A few days of quiet evening markets and well behaved babies wouldn’t go amiss as tonight Liverpool are back in the Champions League quarter finals for the first time since 2009 and tomorrow sees the start of the Masters at Augusta – possibly the most perfect event to get televisually lost in. However the reality will probably be that I’ll be scrambling to work out why the S&P 500 dived 2% into the close for the EMR and why the twins have decided to wake up in tandem and cry uncontrollably. Regardless of this I’m backing a Liverpool / Mcllroy / stronger average hourly earnings treble this week.

On my return from holidays I spent yesterday trying to work out where next for markets. On reflection I would say there are five things negatively impacting markets at the moment. 2 were very predictable, one less so and 2 have come more from left-field. Higher US inflation and tighter monetary policy/less QE were very predictable at the start of the year. The speed of the loss of momentum in growth has been less easy to predict though. The two curve balls are the sudden move towards tariffs/protectionism, and the tech sector woes although the former was always the direction of travel but the scale and speed of Mr Trump’s actions would have been difficult to predict at the start of the year. The problem going forward is that the first two are going to continue to be an issue this year. The growth outlook is more uncertain than it was but we think it likely holds up and the recent loss of momentum stabilises soon. However the final two will remain curveballs. If you can second guess how far and fast Mr Trump pushes protectionism then please let me know. As for the tech sector, again much depends of how far the authorities want to increase regulation and maybe taxes. It feels like it’s on the up but it’s very difficult to analyse. Overall we continue to believe the low vol world is over (as we felt in our 2018 Outlook) but where the higher vol regime settles is probably down to whether global growth holds up from here.

Last night saw a recovery in US markets (S&P 500 +1.26%) as one of the five factors above – namely tech – seemingly got a reprieve as Bloomberg reported that the White House isn’t planning to follow through on Mr Trump’s attacks on Twitter on Amazon. Staying with tech, Tesla’s shares rallied +6.0% after the company said it did not need to raise capital this year and announced better than expected Model 3 production numbers. This all helped the S&P rise back above its 200 day moving average (that it breached on Monday for the first time since the Brexit vote) with all sectors up and gains led by the energy, health care and financials sectors. The Dow (+1.65%) and Nasdaq (+1.04%) also recovered around half of Monday’s losses, while the VIX fell 10.7% to 21.10. In Europe, bourses pared back losses and the Stoxx 600 (-0.49%), DAX (-0.78%) and FTSE (-0.37%) ended modestly down.

Overnight the US trade representative office (USTR) has proposed imposing 25% tariffs on c$50bn worth of Chinese made imports. The list of 1,300 products include high tech items that “benefit from Chinese industrial policies, including (the) Made in China 2025 (strategy)” such as semi-conductors as well as products ranging from TV sets, motor vehicles, dishwashers and even flamethrowers! Looking ahead, there is a 60 day consultation period where the public can provide feedback and the government will hold hearings on the tariffs on 15th May. On the other side, the Chinese Ministry of Commerce indicated “China plans to bring relevant US practice to the dispute settlement body of the WTO and is ready to take counter measures on US products with the same intensity and scale that will be published in the coming days”.

This morning in Asia, markets are trading little changed in part awaiting to see whether trade tensions escalate from here. The Nikkei (+0.14%) and Shanghai Comp. (+0.80%) are up while the Hang Seng (-0.08%) and Kospi (-1.24%) are modestly down as we type. Datawise, China’s March Caixin composite PMI (51.8 vs. 53.3 previous) and Japan’s Nikkei composite PMI (51.3 vs. 52.2 previous) both slowed from the prior month.

Now recapping other markets performance from yesterday. In government bonds, core European 10y bonds yields were slightly higher (Bunds +0.5bp; Gilts +0.9bp) while UST 10y rose 4.5bp to 2.776% partly driven by the risk on tone in equities and tech shares. In FX, the US dollar index and Sterling gained 0.16% and 0.09% respectively while the Euro fell -0.26%. Elsewhere, WTI oil was up 0.79% to $63.51/bbl while precious metals weakened and partly reversed Monday’s gains (Gold -0.64%; Silver -1.06%).

Moving on, with the March monthly manufacturing PMI/ISM data now in, we have updated our usual charts showing the data regressed against the YoY change in equity markets over the last 20 years. Previously, equity markets looked very cheap relative to the very elevated level of PMIs across the globe. Something had to give. However while the data has softened from recent highs, the plunge in equity markets in recent weeks means that this argument still holds true. This is particularly true in Europe where the data suggests that the current level of the Stoxx is about 21% cheap. Indeed the equity PMI implied level for the Stoxx is 50.0 compared to the actual reading of 56.6. The export-heavy DAX, which has fallen sharply in recent weeks, is 28% cheap while the CAC is 11% cheap and IBEX 23% cheap. The FTSE MIB, however, is just 2% cheap with the index largely outperforming other bourses in recent weeks, and Italy’s PMI seeing a pullback in the last two months. That said, when we again re-benchmark to take into account currency moves the gaps are less exaggerated given the 15% appreciation in the Euro over the last 12 months. Indeed the Stoxx is just 6% cheap when we do this, while the DAX and IBEX are 15% and 10% cheap. The CAC and FTSE MIB are actually 5% and 14% expensive, respectively.

Meanwhile, for the US the S&P 500 is up 9% over the last twelve months however the ISM implied level (given it remains elevated) is 24% implying a performance gap of 15%. For the UK the FTSE 100 is similar (14% cheap) however when we again dollar adjust the data the gap shrinks to being just 4% cheap. Finally in Asia the Nikkei is 2% cheap in local currency terms and 5% expensive in dollar terms, while China’s Shanghai Comp is 18% and 11% cheap, respectively. See the tables and charts in the PDF for more info. We’ve included both local currency and dollar adjusted numbers. As we always say we use this as a rough guide to valuations and try to concentrate on the general cheapness/expensiveness of global markets rather than individual ones where distortions can occur, especially for indices where the constituents are more/less exposed to their domestic markets.

Now turning to the various Fed speak yesterday. The Fed’s Brainard reiterated that US fiscal stimulus and other economic tailwinds creates a backdrop that “warrant continual gradual increases in rates”. She added that while these stimulus “should boost the economy” when we are close to full employment, but “it’s hard to know with precision how the economy is likely to respond”. On asset valuations, she noted “valuations in a broad set of markets appear elevated… even after taking into account recent movements”. Elsewhere, the Fed’s Kashkari reiterated his dovish views and noted “we’re probably pretty close to the neutral (rates) right now” and that while US tax cuts have clearly lifted enthusiasm among businesses but it’s still unclear if the cuts are “actually going to lead to more investments”. Finally, the San Francisco Fed president John Williams has been confirmed to replace William Dudley as the next head of the NY Fed. Following on, our US economists have taken a closer look at the degree of slack in the US labour market. Their analysis reinforces their previous assessment that there is little, if any, remaining slack in the labour market. This conclusion is based on two findings: i) most groups within the marginally attached workers (those that want a job but not currently in the labour force) are either near pre-crisis levels or are not particularly sensitive to the business cycle and ii) data on labour market flows indicate that the probability of this group entering the labour force has fallen to near record low levels. Hence, they continue to expect the unemployment rate to fall to 3.4% this year and to 3.2% by end-2019, which would be the lowest level since 1953. Refer to their note for more details.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the March total vehicle sales were above market at 17.4m (vs. 16.9m expected) and the highest for YTD CY18. In Europe, the final reading on the Euro area’s March manufacturing PMI was confirmed at 56.6, which is -2pt mom and -4pt from the 20 year high in last December. Across the region, Germany was revised down by -0.2pt to 58.2 while France was revised up by 0.1pt to 53.7. For flash manufacturing PMIs, Italy was below market at 55.1 (55.5) while the UK was above expectations at 55.1 (vs. 54.7), although the new orders measures expanded the least since June. Elsewhere, Germany’s February retail sales was below expectations at -0.7% mom (vs. 0.7%) and fell for the third consecutive month, thus lowering annual growth to 1.3% yoy.

Looking at the day ahead, the most significant release is likely to be the March CPI report for the Euro area, while February unemployment data is also due. In the afternoon in the US we’ll get the March ADP employment change print, final PMI revisions for March (services and composite), ISM non-manufacturing for March, factory orders data for February and final durable and capital goods orders revisions for February. The Fed’s Bullard and Mester are also scheduled to speak.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 5.52 POINTS OR 0.18% /Hang Sang CLOSED DOWN 661.41 POINTS OR 2.19% / The Nikkei closed UP 27.26 POINTS OR .13%/Australia’s all ordinaires CLOSED UP .08% /Chinese yuan (ONSHORE) closed DOWN at 6.3077/Oil DOWN to 62.36 dollars per barrel for WTI and 66.86 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.3077 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3094 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY POOR CHINESE MARKETS/CHINA RETALIATES WITH TARIFFS/LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

This will develop into a full scale trade war as the USA just released their list targeting 1300 products. This has the makings of a full scale trade war which will inevitably cause all markets to crash. We now await China’s response!!

(courtesy zerohedge)

Trade War Round 2: US Releases China Tariff List Targeting 1,300 Products

Assuring that a second retaliation by China in the escalating trade war is just a matter of days if not hours, moments ago the US Trade Representative released a list of Chinese product subject to 25% tariffs as part of Trump’s Section 301 crackdown on Beijing Intellectual Property abuses, focusing on high tech products.

The list covers about 1,300 tariff lines, or 44 pages, the USTR said, referring to a system of codes used to categorize products. It added that the value of the list is approximately $50 billion in terms of estimated annual trade value for calendar year 2018, a level which is “appropriate both in light of the estimated harm to the U.S. economy, and to obtain elimination of China’s harmful acts, policies, and practices.”

Some example of are shown below:

The list of products included in the USTR list, lines up with technologies China identified in its “Made in China 2025” strategy, White House trade adviser Peter Navarro told Bloomberg Television on March 28.

“China, in my view, brazenly has released this China 2025 plan that basically told the rest of the world, ‘We’re going to dominate every single emerging industry of the future, and therefore your economies aren’t going to have a future,”’ Navarro said. “It’s artificial intelligence, robotics, quantum computing.”

As a reminder, “Made in China 2025” was announced in 2015, and highlighted 10 sectors for support on the way to China becoming an advanced manufacturing power: Information technology, high-end machinery and robotics, aerospace, marine equipment and ships, advanced rail transport, new-energy vehicles, electric power, agricultural machinery, new materials, and bio-medical. China alsohas a separate development strategy for artificial intelligence, published in 2017.

While both investors and businesses have been awaiting details of Trump’s plan to place tariffs on $50 billion in Chinese goods, nobody was looking forward to the list more than China itself. As we reported this morning, China’s US Ambassador said that Beijing is preparing aggressive counter-measures of the “same proportion, scale and intensity” once the Trump administration imposes further tariffs on Chinese goods.

USTR Robert Lighthizer had until April 6 to publish a list of proposed products. There’s now a 60-day period when the public can provide feedback and the government holds hearings on the tariffs.

Back on March 22, Trump said that the tariffs were aimed at penalizing Beijing for what the U.S. alleges to be theft of American companies’ intellectual property.

While China already imposed tariffs in response to Trump’s actions on metal imports (under Section 232), it has repeatedly threatened additional retaliation if Trump unveils the list of Section 301 tariffs, something the Administration did on Tuesday afternoon.