GOLD: $1332.70 UP $7.50 (COMEX TO COMEX CLOSINGS)

Silver: $16.40 UP 4 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1333.70

silver: $16.40

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:60 NOTICE(S) FOR 6000 OZ.

TOTAL NOTICES SO FAR 655 FOR 65500 OZ (2.0373 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 19 for 90,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6571/OFFER $6671: DOWN $144(morning)

Bitcoin: BID/ $6552/offer $6652: DOWN $163 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE AGAIN BY 1760 contracts from 241,135 RISING TO 242,895 WITH YESTERDAY’S TINY 6 CENT RISE IN SILVER PRICING. TODAY WE SET ANOTHER NEW ALL TIME RECORD FOR SILVER OPEN INTEREST . OBVIOUSLY, WE AGAIN HAD ZERO COMEX LIQUIDATION. ALSO WE WITNESSED ZERO COMEX SHORT COVERING AS THE RAID FAILED TRYING TO SHAKE SOME OF THE SILVER LEAVES FROM THE SILVER TREE. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2261 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2261 CONTRACTS. WITH THE TRANSFER OF 2261 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2261 CONTRACTS TRANSLATES INTO 11.309 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

11,255 CONTRACTS (FOR 5 TRADING DAYS TOTAL 11,255 CONTRACTS) OR 56.28 MILLION OZ: AVERAGE PER DAY: 2251 CONTRACTS OR 11.255 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 56.28 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.04% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 774.77 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED GAIN IN COMEX OI SILVER COMEX OF 4511 DESPITE THE tiny 6 CENT RISE IN SILVER PRICE. WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 2261 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2261 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A STRONG 4021 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 2261 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 1760 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE TINY RISE IN PRICE OF SILVER OF 6 CENTS AND A CLOSING PRICE OF $16.36 WITH RESPECT TO THURSDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.215 BILLION TO BE EXACT or 173% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 242,895 AND AGAIN THIS HAS BEEN SET WITH A LOWE PRICE. THE PREVIOUS RECORD WAS YESTERDAY AT 241,135 CONTRACTS WITH A SILVER PRICE CLOSING OF $16.36.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 242,895 CONTRACTS (OR 1.217 BILLION OZ/

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOWE PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

In gold, the open interest FELL BY A CONSIDERABLE SIZED 6393 CONTRACTS DOWN TO 493,317 ACCOMPANYING THE GOOD SIZED FALL IN PRICE/YESTERDAY’S TRADING ( LOSS OF $8.20). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A RATHER LARGE SIZED 11,895 CONTRACTS : JUNE SAW THE ISSUANCE OF 11,895 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 493,317. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 6393 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 11,895 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 5502 CONTRACTS OR 550,200 OZ =17.113 TONNES

YESTERDAY, WE HAD 12098 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 51,625 CONTRACTS OR 5,162,500 OZ OR 160.57 TONNES (5 TRADING DAYS AND THUS AVERAGING: 10,325 EFP CONTRACTS PER TRADING DAY OR 1,032,500 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 5 TRADING DAYS IN TONNES: 160.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 160.57/2550 x 100% TONNES = 6.29% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2205.06 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A LARGE SIZED DECREASE IN OI AT THE COMEX WITH THE GOOD SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($8.20 LOSS). WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,895 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11895 EFP CONTRACTS ISSUED, WE HAD A GOOD NET GAIN IN OPEN INTEREST OF 5502 contracts ON THE TWO EXCHANGES:

11,895 CONTRACTS MOVE TO LONDON AND 6393 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 17.113 TONNES).

we had: 60 notice(s) filed upon for 6000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $7.50 : WE HAD A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES

Inventory rests tonight: 859.99 tonnes.

SLV/

WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE/ A MASSIVE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 320.196 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY AN STRONG 1760 CONTRACTS from 241,135 UP TO 242,895 (AND A NEW COMEX RECORD SET TODAY/APRIL 6/2017. THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED YESTERDAY WAS 234,787 SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89). THIS ALL OCCURRED SURPRISINGLY WITH THE TINY RISE IN PRICE OF SILVER (6 CENTS// YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2261 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 1760 CONTRACTS TO THE 2261 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN GIGANTIC GAIN OF 4021 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 20.105 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY RISE IN SILVER PRICING / YESTERDAY (6 CENTS) . BUT WE ALSO HAD ANOTHER VERY GOOD SIZED 2261 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed HOLIDAY /Hang Sang CLOSED HOLIDAY / The Nikkei closed DOWN 77,90 POINTS OR 0.36%/Australia’s all ordinaires CLOSED DOWN .02% /Chinese yuan (ONSHORE) closed UP at 6.3033/Oil DOWN to 63.09 dollars per barrel for WTI and 67.83 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AT 6.3033 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3198 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR CHINA ON HOLIDAY TODAY/CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

i)LAST NIGHT 6 PM

the markets do not like this: Trump orders consideration of new 100 billion in Chinese tariffs as he intensifies the tariffs wars

( zerohedge)

ii)THIS MORNING 2 AM

China vows to attack the Trump tariffs at any cost. China urges the EU to join in the fight against the USA. The real problem: there is just not enough USA goods entering China that could be subject to tariffs:

( zerohedge)

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

( Alex Christoforou/The Duran.com)

6 .GLOBAL ISSUES

( BILL BLAIN/MINTPARTNERS)

7. OIL ISSUES

With the loans given by China to Venezuela, it looks like China will be the new operators of those oil assets. They are orchestrating this in order than their loans are repaid. Venezuela has another 9 billion on bond payments due this year and if they default here, then the nation will be under tremendous chaos

( Nick Cunningham/OilPrice.com

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)It seems that China is now using Singapore as a source of gold supply as well as Switzerland as London is drying up. Actually again China through its international operation exported 11 tonnes of gold to London

Gold demand according to Koos is around 2,000 tonnes, made up of approximately 430 tonnes of Chinese mining, 1100 tonnes of net SGE withdrawals and the rest scrap.

a must read…

( Koos Jansen)

ii)India’s central bank shuts down crypto currencies

(Times of India/GATA)

ii b)And now Japan orders 2 unlicensed crypto exchanges to halt operations

( zerohedge)

iii)Very important, Aussie Allan Flynn writes a blog called, “Comex, We have a Problem”. He highlights how easy it is to spoof the gold/silver markets something that I have highlighted to you several times a year. Allan is planning to attend the hearing of one of traders caught spoofing and he is collecting funds to help him with his expedititon

( GATA/Allan Flynn)

iv)Alasdair explains why the dollar collapse is inevitable..as the dollar falls so does all other currencies linked to it

( Alasdair Macleod/GATA)

v)Ambrose Evans Pritchard explains why this latest trade disputes with China is very dangerous as each seek to become the dominant power

( Ambrose Evans Pritchard/GATA)

10. USA stories which will influence the price of gold/silver

i. Jobs report

A huge miss/first the general report of only 103,000 jobs added but the hourly earnings rose to .3%. The miss was a Sigma 3 miss.

( zerohedge)

ii)Of the job growth, it mainly occurred in the high end. The minimum wage sector saw a drop

( zerohedge)

( zerohedge)

v)This morning’s trading

Stocks tumble as China urges American citizens to rise up against an unscrupulous President Trump

( zerohedge)

v b)Afternoon trading/

v d) At :315 with 3/4 hr to go: S and P below its 200 day moving averag(zerohedge)

vi)Not good: Trump warns that “we may take a hit” and prepare for “pain” in the markets with the trade wars

( zerohedge)

viii)Nine West is now preparing for bankruptcy protection

( zerohedge)

ix)We knew that this would become inevitable: the tapped out USA consumer has hit a brick wall as total consumer credit plunged to one of its lowest readings in 3 years. Student loans and auto loans however did pick up again and their total is record 2.836 trillion dollars. The consumer is 70% of GDP and this will be a huge negative to first quarter GDP and then onto 2nd quarter.

( zerohedge)

( zerohedge)

b)oh OH! this is going to be interesting!! It seems that Mueller has evidence that Erik Prince and brother of Education Sec. Betsy De Voes has “lied” about meeting a Russian sovereign wealth fund head at the Seychelles. The meeting was held a few days before Trump was inaugurated. It is perfectly legal for him to has these meetings and if legal no reason to lie!

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:353,217 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 289,042 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY AN STRONG 1760 CONTRACTS FROM 241,135 UP TO 242,895 AND A NEW RECORD OI FOR SILVER, WITH OUR 6 CENT RISE IN SILVER PRICING/ YESTERDAY). ALSO,WE WERE ALSO INFORMED THAT WE HAD A STRONG 2261 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2261. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE SURPRISINGLY AND SHOCKINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION. WE ALSO HAVE A GIGANTIC SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 4021 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2250 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2261 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:4021 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 1 contract LOWERING TO 336 contracts. We had 0 notices filed upon (CME correction last Thursday night) so in essence we lost 1 contract or 5,000 additional ounces of silver will NOT stand for delivery in this non active delivery month of April.(AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS)

The next big active delivery month for silver will be May and here the OI LOST 1510 contracts DOWN to 151,047. June saw a loss of 1 contract to stand at 42. The next big delivery month for silver is July and here the OI rose by 1936 contracts up to 54,207.

We had 0 notice(s) filed for NIL OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 6/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

60 notice(s)

6000 OZ

|

| No of oz to be served (notices) |

1575 contracts

(157,500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

655 notices

65,500 OZ

2.0373 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 59 notices were issued from their client or customer account. The total of all issuance by all participants equates to 60 contract(s) of which 31 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (655) x 100 oz or 65,500 oz, to which we add the difference between the open interest for the front month of APRIL. (1635 contracts) minus the number of notices served upon today (60 x 100 oz per contract) equals 223,000 oz, the number of ounces standing in this active month of APRIL (6.936 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (655 x 100 oz or ounces + {(1635)OI for the front month minus the number of notices served upon today (60 x 100 oz )which equals 223,000 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 72 COMEX OI CONTRACTS OR 7200 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

633,255.380

oz

Scotia

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

669,516.53oz

JPMorgan

Scotia

|

| No of oz served today (contracts) |

0

CONTRACT(S

NIL OZ)

|

| No of oz to be served (notices) |

336 contracts

(1,680,000 oz)

|

| Total monthly oz silver served (contracts) | 19 contracts

(95,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: 605,295.100 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan deposited into its warehouses (official) today.

ii) Into Scotia: 64,221.430 oz

total deposits today: 669,516.53 oz

we had 1 withdrawals from the customer account;

i) Out of Scotia: 633,255.380 oz

total withdrawals; 633,255.380 oz

we had 0 adjustment

total dealer silver: 58.8561 million

total dealer + customer silver: 263.369 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 19 x 5,000 oz = 95,000 oz to which we add the difference between the open interest for the front month of April. (336) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 19(notices served so far)x 5000 oz + OI for front month of April(336) -number of notices served upon today (0)x 5000 oz equals 1,775,000 oz of silver standing for the April contract month

WE LOST 1 SILVER CONTRACTS OR 5,000 ADDITIONAL OUNCES WILL NOT STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 88,023 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 85,557 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 85,557 CONTRACTS EQUATES TO 427 MILLION OZ OR 61.12% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.48% (APRIL 6/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.78% to NAV (APRIL 6/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.48%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.78%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.48%: NAV 13.70/TRADING 13.29//DISCOUNT 2.48.

END

And now the Gold inventory at the GLD/

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 6/2018/ Inventory rests tonight at 859.99 tonnes

*IN LAST 357 TRADING DAYS: 81.05 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 307 TRADING DAYS: A NET 75.25 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 6/2018: A HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.319 MILLION OZ.

Inventory 320.196 million oz

end

6 Month MM GOFO 1.96/ and libor 6 month duration 2.47

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.96%

libor 2.47 FOR 6 MONTHS/

GOLD LENDING RATE: .51%

XXXXXXXX

12 Month MM GOFO

+ 2.70%

LIBOR FOR 12 MONTH DURATION: 2.45

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.35

IT COSTS MORE TO LEND GOLD OUT.

end

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 234,677 | 68,088 | 52,011 | 162,608 | 351,473 | 449,296 | 471,572 |

| Change from Prior Reporting Period | ||||||

| -24,355 | 12,410 | -11,385 | 5,165 | -32,330 | -30,575 | -31,305 |

| Traders | ||||||

| 180 | 68 | 73 | 47 | 57 | 261 | 168 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 43,845 | 21,569 | 493,141 | ||||

| -5,974 | -5,244 | -36,549 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, April 3, 2018 | |||||

At 3:30 pm we receive a totally useless report, the COT which gives position levels of our major players. If the use of a huge number of EFP’s every day, I for life of me see any value in them. However for completeness I will provide it for you

OUR LARGE SPECULATORS

those large specs that have been long in gold pitched (transferred through EFP) 24,355 contracts

those large specs that have been short in gold added a net 12,410 contracts to their short side

OUR COMMERICALS

those commercials that have been long in gold added 5165 contracts to their long side

those commercials that have been short in gold transferred (covered) a huge 32,330 contracts from their short side. my guess is that all of these obligations transferred to London.

OUR SMALL SPECULATORS.

those small specs that have been long in gold pitched (transferred through EFP) 5,974 contracts from their long side.

those small specs that have been short in gold covered (transferred) through EFP their obligation to London or just covered probably the former.

Conclusion

there is only one word to describe the above: FRAUD

AND NOW SILVER COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 65,969 | 82,934 | 47,964 | 86,416 | 89,053 | |

| 5,183 | 8,491 | 5,509 | 4,329 | -386 | |

| Traders | |||||

| 112 | 62 | 51 | 46 | 34 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 232,682 | Long | Short | |

| 32,333 | 12,731 | 200,349 | 219,951 | ||

| -1,857 | -450 | 13,164 | 15,021 | 13,614 | |

| non reportable positions | Positions as of: | 185 | |||

INTERESTING!

OUR LARGE SPECULATORS

those large specs that have been long in silver added 5183 contracts on a net basis to their long side

those large specs that have been short in silver added 8491 contracts to their short side.

OUR COMMERCIALS

those commercials that have been long in silver added a net 4329 contracts to their long side

those commercials that have been short in silver covered (transferred) a net 386 contracts from their short side.

OUR SMALL SPECULATORS.

those small specs that have been long in silver added 5063 contracts to their long side

those small specs that have been short in silver added a huge 8259 contracts to their short side??

Conclusions:

same as gold.

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Jamie Dimon Warns Of Potential ‘Market Panic’

Jamie Dimon Warns Of Potential ‘Market Panic’

– JPMorgan Chase CEO Jamie Dimon sees ‘chance of market panic’

– In annual letter to shareholders Dimon warns of increased inflation and interest rates

– Concerned QE unwinding could cause chaos as ‘markets will get more volatile’

– Hard to look at the last 20 years in America “and not think that it has been getting increasingly worse.”

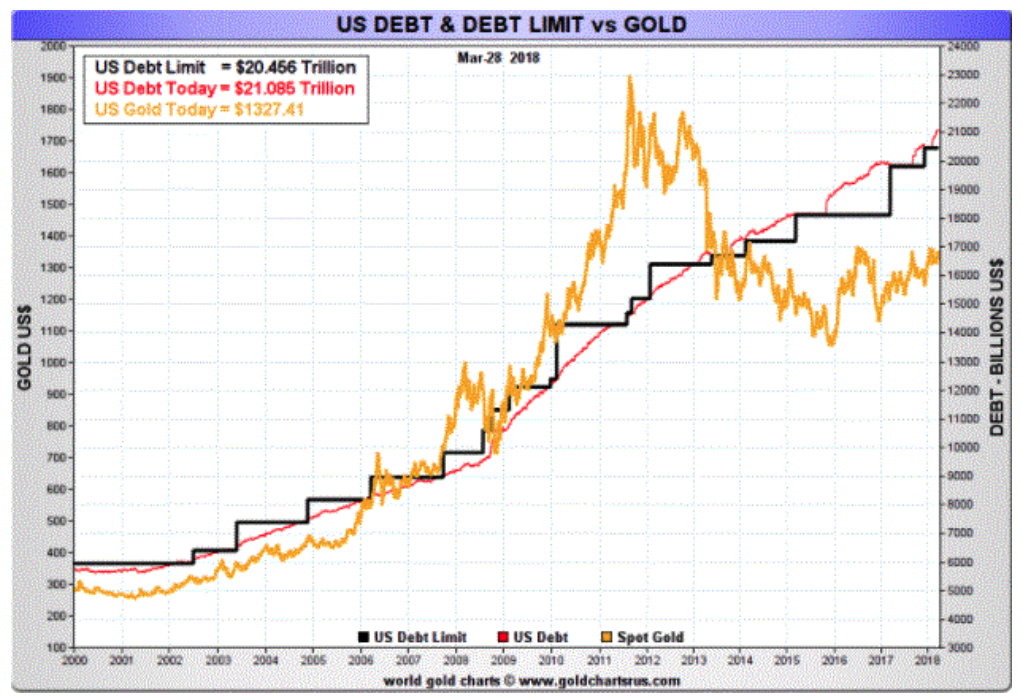

– Positive about US economy over next year, but ignores record levels of world and government debt

– Believes major buyers of US debt (e.g. China) could reduce their purchases of US government debt

– Investors can protect portfolios with gold and silver bullion

– U.S. debt and dollar crisis coming which will propel gold higher (see chart)

The following has been taken from Simon Black’s SovereignMan.com.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

The above was taken from Simon Black’s SovereignMan.com.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Concluding comments

In the words of Sovereign Man Simon Black, ‘Countries whose economic models are based on debt and consumption will suffer’.

When the US does suffer (as Dimon clearly believes it will) it will not be a contained event, the whole world will feel the pinch as we are so intertwined with U.S., their policies and currency.

Another crisis may well be in the pipeline, so bad it is that banks whose models run on debt are giving out warnings. Dimon’s warnings could be a strong signal for investors to allocate a part of their portfolios to gold and silver. These assets have historically held their value in times of economic contraction.

This risk underlines the importance of owning physical gold to protect against geo-political risks, stock and bond market bubbles and the continuing devaluation of the dollar and all fiat currencies.

Recommended reading

Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

Gold A Store Of Value – Protect From $217 Trillion Global Debt Bubble

News and Commentary

Gold settles lower as trade-war tensions cool, dollar strengthens (MarketWatch.com)

Gold prices drop as U.S.-China trade tensions ease (Reuters.com)

U.S. trade deficit sticks to nearly 10-year high (MarketWatch.com)

ASIA GOLD-India demand up ahead of festival, subdued buying elsewhere (Reuters.com)

N. American gold ETF inflows up in March; Europe saw outflows for second month -WGC (Reuters.com)

Euro-Area Data Maze Leaves Economists Puzzled Over Way Out (Bloomberg.com)

Silver Finally Starts To Catch Up With Gold (SilverSeek.com)

Gold Price Seen ‘Moving North’ as World Fails to Replace Output (Bloomberg.com)

Two Mines Supply Half Of U.S. Silver Production & The Real Cost To Produce Silver (ZeroHedge.com)

Gold Prices (LBMA AM)

05 Apr: USD 1,327.05, GBP 943.67 & EUR 1,080.75 per ounce

04 Apr: USD 1,343.15, GBP 955.52 & EUR 1,092.79 per ounce

03 Apr: USD 1,336.60, GBP 949.65 & EUR 1,085.99 per ounce

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

Silver Prices (LBMA)

05 Apr: USD 16.31, GBP 11.59 & EUR 13.28 per ounce

04 Apr: USD 16.46, GBP 11.72 & EUR 13.40 per ounce

03 Apr: USD 16.52, GBP 11.78 & EUR 13.44 per ounce

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

Recent Market Updates

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

India’s central bank shuts down crypto currencies

(Times of India/GATA)

India’s central bank shuts down crypto-currencies

Submitted by cpowell on Thu, 2018-04-05 15:28. Section: Daily Dispatches

Your Bank Will Not Allow You to Buy Bitcoins Anymore

By Preeli Motiani

The Times of India, Mumbai

Thursday, April 5, 2018

You will not be able to buy cryptocurrency via banks or e-wallets etc. in India anymore as the Reserve Bank of India has banned them with immediate effect from “dealing with or providing services to any individuals or business entities dealing with or settling virtual currencies.”

At it its first bi-monthly monetary policy meeting, the RBI has announced that any entity regulated by the central bank such as banks, wallets, etc., shall not deal with or provide services to any individual or business entities for buying or selling of cryptocurrency such as bitcoins. If banks, e-wallets, and any other entities regulated by the RBI are not allowed to facilitate sale or purchase of cryptocurrencies, obviously individuals will not be able to transfer money from their bank accounts to their crypto-trading wallets. …

… For the remainder of the report:

https://economictimes.indiatimes.com/wealth/personal-finance-news/your-b…

END

And now Japan orders 2 unlicensed crypto exchanges to halt operations

(courtesy zerohedge)

Japan Orders 2 Unlicensed Crypto Exchanges To Temporarily Halt Operations

In a sign that Japan’s crackdown on crypto firms might be coming to an end, the Financial Services Agency announced penalties against three unlicensed exchanges that will force two of them to suspend operations.

According to Bloomberg, the FSA issued a “business improvement order” against FSHO, Eternal Link and LastRoots. FSHO and Eternal Link were also ordered to suspend operations, with FSHO ordered to shut down between April 8 and June 7, and Eternal Link from April 6 to June 7.

The exchanges were ordered to make improvements in bookkeeping, systems risk management and anti-money laundering and terrorism controls. Inspections into the country’s 16 unlicensed crypto exchanges are ongoing.

Japan launched its probe after CoinCheck, one of the country’s largest unlicensed crypto exchanges, was attacked by hackers, who stole more than $500 million worth of NEM tokens in what has been described as the largest crypto heist of all time. The FSA had earlier ordered CoinCheck to firm up its consumer protection and money laundering controls.

On Thursday, Japanese online brokerage firm Monex Group announced it would buy Coincheck Inc. for 3.6 billion yen ($33.6 million) after assuring the FSA that it would implement the improvements mandated by the agency as it plans for an eventual IPO of CoinCheck – what could be the first IPO of a crypto exchange, per Reuters.

Cryptocurrency prices have continued to slide in April after notching their worst quarterly performance ever during Q1.

It seems that China is now using Singapore as a source of gold supply as well as Switzerland as London is drying up. Actually again China through its international operation exported 11 tonnes of gold to London

Gold demand according to Koos is around 2,000 tonnes, made up of approximately 430 tonnes of Chinese mining, 1100 tonnes of net SGE withdrawals and the rest scrap.

a must read…

(courtesy Koos Jansen)

Koos Jansen: China’s secret gold supplier is Singapore

Submitted by cpowell on Fri, 2018-04-06 01:42. Section: Daily Dispatches

9:40a HKT Friday, April 6, 2018

Dear Friend of GATA and Gold:

Singapore, Bullion Star gold researcher Koos Jansen writes today, has become a major source of gold supply for China since 2013 and those exports are increasing. Jansen writes: “Singapore net-exported 102 tonnes to China in 2017, a record year and up 177 percent from 2016.” Jansen’s analysis is headlined “China’s Secret Gold Supplier Is Singapore” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/chinas-secret-gold-supplie…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Very important, Aussie Allan Flynn writes a blog called, “Comex, We have a Problem”. He highlights how easy it is to spoof the gold/silver markets something that I have highlighted to you several times a year. Allan is planning to attend the hearing of one of traders caught spoofing and he is collecting funds to help him with his expedititon

(courtesy GATA/Allan Flynn)

Allan Flynn: Gold and silver futures were easy targets for spoofers

Submitted by cpowell on Fri, 2018-04-06 03:53. Section: Daily Dispatches

11:55a HKT Friday, April 6, 2018

Dear Friend of GATA and Gold:

Allan Flynn, who runs the “Comex, We Have a Problem” blog, this week posted a fascinating review of the traders who are the major targets of the recent investigation by the U.S. Justice Department and Commodity Futures Trading Commission of “spoofing” in the monetary metals futures markets.

Two details that may be of special interest:

1) The traders seemed to find “spoofing” exceedingly easy. So one may wonder how much easier market manipulation may be for governments with access to infinite money and more advanced technology and programming — especially since U.S. law fully authorizes the U.S. government to rig surreptitiously any market in the world.

2) The government’s first investigation of manipulation of the monetary metals markets failed to identify the evidence developed by the class-action anti-trust lawsuits brought against bullion banks in federal court in New York. The government’s second investigation has caused a long delay in those lawsuits.

Flynn’s report is headlined “U.S. Gold and Silver Futures Markets: ‘Easy’ Targets” and it’s posted at “Comex, We Have a Problem” here:

http://comexwehaveaproblem.blogspot.hk/2018/04/us-gold-silver-futures-ma…

Flynn, an Australian, is hoping to attend and report about the upcoming trial of one of the traders charged, which will be held in Connecticut soon, and is seeking to raise money for his expedition at GoFundMe here:

https://www.gofundme.com/Gold-Spoofing-Trial

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ambrose Evans Pritchard explains why this latest trade disputes with China is very dangerous as each seek to become the dominant power

(courtesy Ambrose Evans Pritchard/UKTelegraph/GATA)

Ambrose Evans-Pritchard: Trump’s power struggle with China isn’t about trade

Submitted by cpowell on Fri, 2018-04-06 04:23. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

via Gulf News, Dubai

Friday, April 6, 2018

U.S. Dresident Donald Trump’s declaration of tariff warfare against China has little to do with trade. It is about raw power, a struggle over which of the two sparring hegemons will dominate technology and run the world in the 21st century.

The pretense of cordial coexistence has all but ended in the Hobbesian era of Trumpism. The latest U.S. national security strategy report for the first time names China as a strategic rival that seeks to “challenge American power, influence, and interests, attempting to erode American security and prosperity.” It is the poisonous-diplomatic context that makes this week’s trade skirmish so dangerous.

A Wall Street crash is perhaps the only deterrent that Trump really fears as the mid-term elections approach and Democrats threaten to gain control of impeachment powers on Capitol Hill. China could — if it chose — trigger this with large sales of its $1.2 trillion holding of U.S. Treasuries. Yet it is a perilous game for China as well. …

… For the remainder of the commentary:

http://gulfnews.com/opinion/thinkers/trump-s-power-struggle-with-china-i…

END

Alasdair explains why the dollar collapse is inevitable..as the dollar falls so does all other currencies linked to it

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod: Why a dollar collapse is inevitable

Submitted by cpowell on Fri, 2018-04-06 02:30. Section: Daily Dispatches

10:30a HKT Friday, April 5, 2018

Dear Friend of GATA and Gold:

The export of so many U.S. dollars around the world makes another collapse of the currency inevitable, GoldMoney research director Alasdair Macleod argues in his new commentary.

Macleod concludes: “When the overvaluation of the dollar is corrected, the downside of a dollar collapse is far greater than it was in the early 1930s or the early 1970s. All other fiat currencies take their value from the dollar, not gold. So the destabilizing forces on the dollar, the other unexpected side of Triffin’s dilemma, could take down the whole fiat complex as well.”

Macleod’s commentary is headlined “Why a Dollar Collapse Is Inevitable” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/why-a-dollar-colla…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

ALASDAIR MACLEOD……

_

Why A Dollar Collapse Is Inevitable

“Naturally, the smooth termination of the gold-exchange standard, the restoration of the gold standard, and supplemental and interim measures that might be called for, in particular with a view to organizing international credit on this new basis, will have to be deliberately agreed upon between countries, in particular those on which there devolves special responsibility by virtue of their economic and financial capabilities.”

General Charles de Gaulle, February 1965

We have been here before – twice. The first time was in the late 1920s, which led to the dollar’s devaluation in 1934. And the second was 1966-68, which led to the collapse of the Bretton Woods System. Even though gold is now officially excluded from the monetary system, it does not save the dollar from a third collapse and will still be its yardstick.

This article explains why another collapse is due for the dollar. It describes the errors that led to the two previous episodes, and the lessons from them relevant to understanding the position today. And just because gold is no longer officially money, it will not stop the collapse of the dollar, measured in gold, again.

General de Gaulle made himself very unpopular with the international monetary establishment by holding the press conference from which the opening quote was taken. Yet, his prophecy, that the gold exchange standard of Bretton Woods would end in tears unless its shortcomings were addressed by a return to a gold standard, turned out to be correct shortly after. What the establishment did not like was the bald implication that it was wrong, and that the correct thing to do was to reinstate the gold standard. Plus ça change, as he might say if he was still with us.

Those of us who argue the case for a new gold standard, and not some sort of half-way house such as a gold exchange standard to address the obvious failings of the current monetary system, are in a similar position today. The first task is that which faced General de Gaulle and Jacques Rueff, his economic advisor, which is to explain the difference between the two.[i] It is now forty-seven years since all forms of monetary gold were banished by the monetary authorities, and today few people in finance understand its virtues.

Furthermore, in the main, historians educated as Keynesians and monetarists do not understand the economic history of money, let alone the difference between a gold standard and a gold-exchange standard. These similar sounding monetary systems must be defined and the differences between them noted, for anyone to have the slimmest chance of understanding this vital subject, and its relevance to the situation today.

Defining the role of gold

To modern financial commentators, there is little or no significant difference between a gold standard and a gold exchange standard. Keynes’s famous quip, that the gold standard was a barbarous relic, was made in his Tract on Monetary Reform, published in 1923, before the gold exchange standard really got going, yet it is quoted as often as not indiscriminately in the context of the latter.

Yet, they are as different as chalk and cheese. The gold exchange standard evolved in the 1920s as America and Britain went to the aid of European countries, struggling in the wake of the Great War. It allowed the expansion of national currencies under the guise of them being as good as gold. It was not. In modern terms, it was as different as paper gold futures are to the possession of physical gold today.

A gold standard is commodity money, where gold is money, and monetary units are defined as a certain fixed fineness and weight of gold. The monetary authority is obliged by law to exchange without restriction gold against monetary units and vice-versa, and there are no restrictions on the ownership and movement of gold.

Under a gold exchange standard, the only holder of monetary gold is the issuer of the domestic monetary unit as a substitute for gold. The monetary authority undertakes to maintain the relationship between the substitute and gold at a fixed rate. Only money substitutes (bank notes and token coins – gold being the money) circulate in the domestic economy. The monetary authority exchanges all imports of monetary gold and foreign currency into money substitutes for domestic circulation at the fixed gold exchange rate. The monetary authority holds any foreign exchange which is also convertible into gold on a gold exchange standard at a fixed parity, and treats it to all extents and purposes as if it is gold.

The essential difference between a gold standard and a gold exchange standard is that with the latter, the monetary authority has added flexibility to expand the quantity of money substitutes in circulation without having to buy gold. A gold standard may start, for example, with 50% gold and 50% government bonds backing for money units, but all further issues of monetary units will require the monetary authority to purchase gold to fully cover them. This was the monetary regime in Britain and many other countries before the First World War.

As stated above, gold exchange standards evolved after the First World War, in the early 1920s.[ii] It was the taking in of foreign currencies, also on gold exchange standards themselves, and booking them as if they were the equivalent of gold, that allowed central banks to expand the quantity of monetary units domestically. To understand how this operated in practice requires us to work through an example between two countries on gold exchange standards. We will take the entirely hypothetical example of two countries, America and Italy, both of which have monetary gold in their reserves and operate on a gold exchange standard.

America lends Italy dollars by crediting its central bank’s account at the Fed with the dollars loaned. But while ownership has changed to Italy, dollars never leave America. And dollars, when drawn down by the Banca d’Italia are recycled into America’s banking system.

The economic sacrifice to America of lending money to Italy is therefore zero. America has simply created a loan out of its own currency, and in the process increased the quantity of dollars in circulation. And because in practice Italy does not encash dollars for gold, America expects to preserve its gold reserves.

Meanwhile, The Banca d’Italia has expanded its balance sheet by the inclusion of America’s dollar loan to it as a liability, and the dollars themselves as an asset regarded as the equivalent of gold. Because dollars are not permitted to circulate in Italy’s domestic economy, they can be used by Banca d’Italia, either to settle other foreign obligations, or as a gold substitute to back the issue of further lira. Meanwhile, the Banca d’Italia’s dollars are reinvested in US Treasuries, which give a yield. Banca d’Italia has little incentive to exchange its dollars for physical gold, because gold yields nothing and is costs to store.

If Banca d’Italia uses dollars to discharge a foreign obligation with another country, that third party will also end up investing the dollars gained in US Treasuries, assuming it also prefers yielding assets to physical gold. Alternatively, if the dollars are used by the Banca d’Italia to back an increase in the quantity of lira or to subscribe for government debt, the effect in the domestic Italian economy is an inflation of prices.

Therefore, the effect of a gold exchange standard is the opposite of a gold standard. A gold standard puts the requirements for the quantity of money in circulation entirely in the hands of the market, to which the central bank mechanically responds. A gold exchange standard allows a lending central bank to inflate its money supply through inward investment, and a borrowing central bank to inflate its money supply on the presumption the monetary substitutes borrowed to back it are monetary units of gold.

The gold exchange standard in the 1920s

After the First World War, both sterling and dollars were made available under the Dawes Plan of 1924, which provided non-domestic capital for Germany after her hyperinflation. France suffered a currency crisis in July 1926, which was successfully dealt with by the Poincaré government through raising taxes. The Bank of France was then enabled to borrow dollars and sterling and to issue francs and subscribe for government debt.

To summarise, these loans bolstered the balance sheets of the Reichsbank and the Bank of France, which invested the sterling and dollars borrowed in gilts and Treasuries respectively. If instead France and Germany had taken gold under the gold exchange provisions, they would have had an asset with no yield, though France did opt increasingly for some gold towards the end of the decade and beyond – by December 1932 she had accumulated 3,257 tonnes. So, by lending their monetary units, the creditor nations achieved finance for their own governments, as well as providing capital for foreign central banks. It was seen to be a win-win for all the central banks involved.

The accumulation of dollars in foreign hands from 1922 onwards accompanied and fuelled bank credit expansion in the US. This gave the roaring twenties an inflationary impetus, dramatically reflected in its stock market bubble. However, the increasing quantity of dollars in foreign ownership became an accident waiting to happen. There had been a mild thirteen-month recession from October 1926 to November 1927, after which the stock market boomed. The Fed was compelled to reverse earlier interest rate cuts and increased the discount rate from 3 ½% to 5% by July 1928.

French investors began to repatriate capital en masse, and the Bank of France’s gold reserves rocketed from 711 tonnes in 1926 to 2,099 tonnes by 1930.[iii]The gold exchange standard had spectacularly failed, and redemption of dollars for gold, being deflationary, exacerbated the Wall Street Crash. It certainly rhymed with Robert Triffin’s dilemma: the export of dollars into foreign ownership was monetary magic, until it reversed at the first sign of trouble.

The gold exchange standard of Bretton Woods

In 1944, the monetary panjandrums of the day, led by Harry Dexter-White for the US and Lord Keynes for the UK, designed the post-war gold exchange standard of Bretton Woods. No doubt, Dexter-White fully understood the advantage to the US of forcing all countries to accept dollars with a yield, or gold with none. When American payments abroad exceeded receipts, the difference was generally reflected in dollars issued to foreign central banks, kept on deposit in New York, or invested in US Treasuries.

Throughout the ‘fifties, America recorded a surplus on goods and services, which declined as European manufacturing recovered. But other factors, such as investment abroad and the Korean war resulted in an overall balance of payments deficit totalling $21.41bn, the equivalent of 19,024 tonnes of gold at $35 per ounce. However, US gold reserves declined only 4,457 tonnes between 1950 and 1960, which tells us that the balance was indeed invested in US bank deposits and US Government notes and bonds.[iv]

The respective figures for the 1960s were total payment deficits of $32bn, the equivalent of 28,437 tonnes of gold, and an actual decline in gold reserves of 5,283 tonnes.[v]

The accelerating increase of foreign ownership of dollars over these two decades meant the world, ex-America, was awash with dollars by the mid-1960s. By the end of that decade, America’s gold reserves had declined from 20,279.3 tonnes in 1950, two-thirds of the world’s monetary gold, to 10,538.7 tonnes, 29% of the world’s monetary gold in 1970.

The effect was to remove trade settlement disciplines on net importing nations, and to cause inflation in net exporting nations, the opposite of the disciplines of a pre-WW1 gold standard on global trade. It was this effect that was central to the second Triffin dilemma, whereby dollars became wildly over-valued in gold terms through their excessive issuance.

In the mid-sixties, Washington became increasingly alarmed that foreigners weren’t playing by the assumed rule that they should take dollars and not redeem them for gold. By then, France and Germany between them had increased their gold holdings from 487.1 tonnes in 1948 to 7,089 tonnes at the time of de Gaulle’s press conference. General de Gaulle’s press conference, from which this article’s opening quote is taken, had touched some very raw nerves.

It was clear that the dollar, with the overhang of foreign ownership, had become horribly overvalued, and so should have been devalued, perhaps to over $50 or $60 per ounce, for a gold peg to stick. A devaluation of this magnitude might have been sufficient at that time to stem the outflow of gold.

Both Washington and American public opinion were set strongly against any devaluation. Instead, the London gold pool, designed to ensure the major central banks supported the Bretton Woods System, collapsed in 1968, when France withdrew from it. A dollar devaluation to $42.2222 shortly after was simply not enough, and in 1971 President Nixon suspended the Bretton Woods System, and the new regime of floating exchange rates that is still with us to this day began.

The situation today

Following the Nixon shock, official monetary policy towards gold was to ignore it, and to persuade other central banks and financial markets it was irrelevant to the modern monetary system. To this day, the Fed still books the gold note from the Treasury at $42.2222 per ounce, even though the price has risen to over $1300.

We can simplistically value the dollar in terms of gold, which is certainly a valid, perhaps the most valid approach. But to merely conclude that the dollar has collapsed since 1971, while true, side-steps an analysis that points to the risk that even today’s value may still be too high. Furthermore, with the dollar acting as the world’s reserve currency, all other fiat currencies, which are priced with reference to it rather than gold, are to a greater or lesser extent in the same boat.

Taking a cue from our analysis of the workings of cross-border monetary flows, which allows America to have its privilege of foreigners financing its deficits, we can estimate the approximate extent of the accumulated imbalances that could lead to the dollar’s collapse.

We know that the US balance of payments deteriorated from 1992 onwards, though those figures did not include military spending abroad, which has been a significant and unrecorded addition to dollars both in cash circulation outside America, and also to estimates of the balance of payments.[vi] Official balance of payments figures are therefore understated and have been for at least a quarter of a century.

More recently, from September 2008 the Fed began expanding its balance sheet by policies designed to increase commercial bank reserves, as a response to the financial crisis. That August, they were $10.5bn, increased to $67.5bn the following month, and peaked at $2,786.9bn in August 2014, since when there has been a modest decline. From our analysis of the run-ups to the two previous dollar crises, we know we should try to estimate how much of the increase was effectively funded from abroad. Treasury TIC Data gives us a fairly good steer to what extent this has happened. We find that between those dates, (August 2008 – August 4014) foreign ownership of dollars increased by $6,237.7bn, over twice as much as the increase in the Fed’s record of commercial bank reserves.[vii]

This is Triffin at its most fast and furious. Since then, foreign ownership of dollars has increased a further $2,142.4bn to a record $18,694.1, even though bank reserves declined by $572bn.[viii] In other words, the accumulation of dollars in foreign hands now stands at over 95% of US GDP.

Another way of looking at it is to assess the market values of US securities held by foreigners and relate that to GDP, though this information is less timely,. This is shown in the following chart.

The build-up of foreign investment in America, in large measure the counterpart of dollar loans to foreigners, has been remarkable. At the time of the dot-com bubble, it had jumped to 35% of GDP, from less than 20% in the nineties and considerably less before. At over 90% of GDP in recent years, there can be no doubt that the next financial event, whether it be derived from a rise in interest rates or a general weakness in the dollar, can be expected to trigger a substantial flight out of the dollar.

The pricing of financial assets, and today’s extraordinarily low interest rates indicate that a flight from the dollar is the last thing expected in financial markets. If they were still alive, de Gaulle and his economic advisor, Jacques Rueff, would be instructing the ECB, as successor to the Bank of France, to dump all dollars for gold immediately. And probably to dump all other foreign fiat currencies for gold as well. However, today, it is likely that other actors will blow the whistle on the dollar, such as the Chinese, and the Russians.

For it is clear that when the over-valuation of the dollar is corrected, the downside of a dollar collapse is far greater than it was in the early-thirties or the early-seventies. All other fiat currencies take their value from the dollar, not gold. So, the destabilising forces on the dollar, the other unexpected side of Triffin’s dilemma, could take down the whole fiat complex as well.

[i] This article draws upon Rueff’s account of the issues that led to the dollar crisis between 1968-71, in his book The Monetary Sin of the West, translated by Roger Glémet (Macmillan, NY)

[ii] A gold exchange standard existed in a number of European countries between 1922 and 1930, as the basis of loans to them in US dollars, when the dollar was convertible into gold. The system recommenced in 1945 and formed the basis of the Bretton Woods Agreement.

[iii] See The International Gold Standard and US Monetary Policy from World War I to the New Deal, by Leland Crabbe, of the Division of Research and Statistics at the Fed, 1962.

[iv] See St Louis Fed’s Review, Vol 43 No 3 March 1961 Table 2 Column (3). Gold reserve figures supplied by the World Gold Council.

[v] See US Balance of Payments Problems and Policies in 1971, by Christopher Bach, Table IV (Published by St Louis Fed.)

[vi] See sub-heading “Imports by military agencies”, page A-4 at https://www.census.gov/foreign-trade/Press-Release/current_press_release/explain.pdf

[vii] Derived from TIC data: https://www.treasury.go/resource-center/data-chart-center/tic/Pages/ticpress.aspx

[viii] Ibid. Reserves held at the Fed correct at January 2018.

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3033 /shanghai bourse CLOSED / HANG SANG CLOSED

2. Nikkei closed DOWN 77.90 POINTS OR 0.36%/ /USA: YEN RISES TO 107.34/

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index RISES TO 90.25/Euro FALLS TO 1.2263

3b Japan 10 year bond yield: RISES TO . +.046/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.08/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.09 and Brent: 67.83

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.516%/Italian 10 yr bond yield UP to 1.800% /SPAIN 10 YR BOND YIELD UP TO 1.247%

3j Greek 10 year bond yield RISES TO : 4.012?????????????????

3k Gold at $1322.85 silver at:16.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 57.89

3m oil into the 63 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.34 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9638 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1796 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.521%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.821% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0633% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Tumble Amid Tariff, Payrolls, Powell Chaos

When summarizing yesterday’s market action, which saw the market surge for the third consecutive day and culminated with Europe’s best day since June 2016, we said that it all boiled down to one question: “Trade war or no trade war?”

Until 6pm, the answer was the latter, however with one announcement Trump flipped everything on its head, and just as the president called for an additional $100 billion in Chinese tariffs, futures tumbled, with Dow futs plunging over 400 points as escalating trade war with China was back front and center.

China promptly responded, with the Chinese state-run tabloid Global Times said the new tariff threat reflects arrogance on issues to China and that Trump’s administration is totally wrong about the nature of current US-China trade relations, while China’ official press agency Xinhua stated the US proposal of USD 100bln tariffs violates international trade regulations and that China keeps the door open regarding trade discussions with the US.

Meanwhile there is today’s main event: March payrolls, where consensus is pegged for a 185k print (following that bumper 313k print in February). Still, as DB notes, March has been a tricky month for employment forecasters as the median consensus estimate has overestimated the initial March nonfarm payrolls print in four of the last five years by an average of 62k. Interestingly, the consensus has underestimated nonfarm payrolls by an average of 66k over the past two months.

Fed Chair Powell will also be speaking at 1:30pm ET. Consensus expects Powell to reiterate the upbeat outlook he presented at the March 21 FOMC meeting. However, since Powell will not be speaking on behalf of the Committee, we will be looking to get a sense of his own take on the latest data. There is Q&A so that will be closely watched.

And so, with both payrolls and Powell looming big on today’s event calendar, the market is once again obsessed with the ongoing trade war between the US and China, and stoically waiting for China’s retaliation, which is 100% assured and which will be a tit-for-tat increase in the amount of US imports subject to tariffs rising to $150 billion or… all of them, as the US exports just under $150 in goods and services to China, suggesting China will have to do “something else” to fully match the US response, with choices including devaluing the Yuan, selling Treasurys, blocking US oil exports, and others.

Or perhaps this is just more negotiating bluster, and neither the US nor China will do anything. To be sure, this is the theory preferred by the market, and is also why once again global stocks and US futures have recouped much of the overnight losses.

The ECB’s Coeure also felt the need to chime in and claimed that the ECB’s studies show US tariffs would be significantly negative for the economy globally. He also said drop in equity prices and uncertainty over tariffs retaliation already show adverse impact on economy, which of course is great news for central banks as it means they don’t have to hike rates.

Still, despite the rebound from the lows, both Asian and European shares fell alongside the U.S. futures dump Trump’s latest threat to target Chinese imports. Predictably, Treasuries rose and commodities, especially China-heavy industrials, fell. Also helping risk sentiment is today’s payrolls report (which Trump hinted could be “fantastic”), and Powell’s speech at 1:30pm in which the question – of course – will be “three or four.”

Digging through the carnage – at least until some 17 year old hedge fund manager decides that if $50BN in tariffs was good for 1000 Dow Points higher, then $150BN should be enough for 3,000 – carmakers and miners were the biggest losers in Europe’s Stoxx 600 Index. Almost all European sectors are in the red with the exception of utilities. Material names are underperforming amid the weakness in base metals. In terms of individual stocks, DAX heavyweight Daimler (-5.7%) shares are seen lower following company going ex-dividend. On the flip side, UK-based

Shire (+1.6%) is again at the top of the FTSE 100 after continued speculation in UK press that the Co. could be subject to a takeover attempt by Japanese Takeda Pharmaceuticals.

While China was closed for the day, the offshore yuan slid, with the USDCNH rising 250pips amid rising concerns China may retaliate by devaluing the currency…

zerohedge@zerohedgeCNY puts looking real cheap right about now

… after Beijing said it would counter U.S. protectionism “to the end, and at any cost.”

And yet despite the new trade war – and tape – bomb, Asian equities traded indecisive. Pressure in ASX 200 (unch) was contained and later reversed amid commodity sector strength in Australia and JPY weakness. KOSPI (-0.3%) was lower with index heavyweight Samsung Electronics failing to benefit from better than expected prelim. Q1 operating profit, as it also missed on revenue while some cited participants selling on the news and booking profits after the prior day’s rally.

Meanwhile for those who are about to lose track of everything that is going on, here is a handy recap courtesy of Bloomberg:

- The war of words on trade is escalating, with China saying it would counter U.S. protectionism “to the end, and at any cost.” The statement from Beijing came after Trump ordered his administration to consider tariffs on an additional $100 billion in Chinese goods on Thursday, sending U.S. stock futures tumbling. Meanwhile, China has signaled what could be next on its own tariff target list after American farmers: the U.S. shale industry

- With investors around the world are getting tired of the tit-for-tat in trade, U.S. Fed Chair Jerome Powell is facing off with U.S. payrolls as the days’ biggest potential headline- maker. Payrolls-wise, an increase of 185,000 new jobs is forecast, with hourly earnings also expected to show a slight pick-up. Five hours later, Powell to due give speech on the economic outlook during a visit to Chicago