GOLD: $1336.75 UP $4.05 (COMEX TO COMEX CLOSINGS)

Silver: $16.53 UP 12 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1336.50

silver: $16.50

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:2 NOTICE(S) FOR 200 OZ.

TOTAL NOTICES SO FAR 657 FOR 65700 OZ (2.043 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 19 for 90,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6684/OFFER $6784: UP $135(morning)

Bitcoin: BID/ $6616/offer $6716: up $67 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE AGAIN BUT BY A SMALLER THAN EXPECTED 516 contracts from 242,895 RISING TO 243,411 WITH FRIDAY’S TINY 4 CENT RISE IN SILVER PRICING. TODAY WE SET ANOTHER NEW ALL TIME RECORD FOR SILVER OPEN INTEREST . OBVIOUSLY, WE AGAIN HAD ZERO COMEX LIQUIDATION. BUT WE MUST HAVE WITNESSED SOME COMEX SHORT COVERING AS THE BANKERS ARE QUITE CONCERNED WITH SILVER’S DIZZYING OPEN INTEREST HEIGHT. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1470 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1470 CONTRACTS. WITH THE TRANSFER OF 1470 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1470 CONTRACTS TRANSLATES INTO 7.35 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

12,725 CONTRACTS (FOR 6 TRADING DAYS TOTAL 12,725 CONTRACTS) OR 63.625 MILLION OZ: AVERAGE PER DAY: 2120 CONTRACTS OR 10.604 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 63.625 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.08% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 782.12 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A SMALL SIZED GAIN IN COMEX OI SILVER COMEX OF 516 WITH THE TINY 4 CENT RISE IN SILVER PRICE. WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 516 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 516 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A STRONG 1986 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 1470 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 516 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE TINY RISE IN PRICE OF SILVER OF 4 CENTS AND A CLOSING PRICE OF $16.40 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.217 BILLION TO BE EXACT or 174% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOWE PRICE. THE PREVIOUS RECORD WAS YESTERDAY AT 242,895 CONTRACTS WITH A SILVER PRICE CLOSING OF $16.40.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOWE PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

In gold, the open interest ROSE BY A SMALL SIZED 1765 CONTRACTS UP TO 495,082 ACCOMPANYING THE GOOD SIZED GAIN IN PRICE/FRIDAY’S TRADING ( GAIN OF $7.50). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A RATHER LARGE SIZED 9917 CONTRACTS : JUNE SAW THE ISSUANCE OF 9917 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 495,082. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 1765 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 9917 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 11,682 CONTRACTS OR 1,168,200 OZ =36.33 TONNES

FRIDAY, WE HAD 11895 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 61,542 CONTRACTS OR 6,154,200 OZ OR 191.42 TONNES (6 TRADING DAYS AND THUS AVERAGING: 10,257 EFP CONTRACTS PER TRADING DAY OR 1,025,700 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 6 TRADING DAYS IN TONNES: 191.42 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 191.42/2550 x 100% TONNES = 7.50% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2235.90 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A LARGE SIZED INCREASE IN OI AT THE COMEX WITH THE SMALL SIZED GAIN IN PRICE IN GOLD TRADING FRIDAY ($7.50 GAIN). WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9917 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9917 EFP CONTRACTS ISSUED, WE HAD A GOOD NET GAIN IN OPEN INTEREST OF 11,682 contracts ON THE TWO EXCHANGES:

9917 CONTRACTS MOVE TO LONDON AND 1765 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 36.33 TONNES).

we had: 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $4.50 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 859.99 tonnes.

SLV/

WITH SILVER UP 12 CENTS TODAY: NO CHANGES/

/INVENTORY RESTS AT 320.196 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A SMALLER THAN EXPECTED 516 CONTRACTS from 242,895 UP TO 243,411 (AND A NEW COMEX RECORD SET TODAY/APRIL 9/2017. THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED FRIDAY. THE PREVIOUS RECORD WAS: 234,787 SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89).

FRIDAY’S TRADING OCCURRED SURPRISINGLY WITH THE TINY RISE IN PRICE OF SILVER (4 CENTS//). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1470 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 516 CONTRACTS TO THE 1470 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1986 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 9.93 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE TINY RISE IN SILVER PRICING / FRIDAY (4 CENTS) . BUT WE ALSO HAD ANOTHER VERY GOOD SIZED 1470 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed UP 7.18 POINTS OR .23% /Hang Sang CLOSED UP 384.64 POINTS OR 1.29% / The Nikkei closed UP 110.74 POINTS OR 0.51%/Australia’s all ordinaires CLOSED UP .30% /Chinese yuan (ONSHORE) closed DOWN at 6.3153/Oil DOWN to 62.25 dollars per barrel for WTI and 67.59 for Brent. Stocks in Europe OPENED IN THE GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3153 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3161 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

i))China/ SOUTH CHINA SEAS

China wishes to show her muscle as they deploy 3 carrier battle groups in the South China Sea

( zerohedge)

ii)It seems that instead of dumping its USA treasuries, China is thinking about the devaluation of the yuan and that would put tremendous pressure around the world

iii)This seems like a logical step for the Chinese. They do not want to send the nuclear button to the USA. A good alternative is for them to just stop buying USA treasuries. It will hurt the USA as their deficit is already at 1.2 trillion dollars and then on top of that the Fed will roll off 600 billion. If the Chinese stop buying the Fed will be called upon to purchase Bonds and QT will end.

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

i)GREAT BRITAIN

Tom Luongo discusses what happens next with the Theresa May Government post Skripal

( Tom Luongo)

( zerohedge)

iii)ITALY

Tom Luongo discusses the foolishness of the League party

( Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Oh no!! not again…Trump threatens Putin again over Saturday night’s purported “chemical attack”. Russia warns of a grave response if the USA launches a strike in retaliation to this “event”

( zerohedge)

ii)Last night explosions heard above Syria/Pentagon denies it was responsible

( zerohedge)

iii)ISRAEL/RUSSIA/SYRIA

Russia blames Israel for the above attack last night

(courtesy zerohedge)

iv)Israel told USA officials of last night’s raid in Syria and now the big question: what will be the Russian response?

( zerohedge)

v)Israel also strikes Hamas in the Gaza Strip knocking out military compounds

(courtesy zerohedge)

vi)The USA has no evidence that Assad was behind the chemical attack on Friday night but says that they will retaliate regardless of the UN decision

( zerohedge)

The Turkish Lira falls badly to 4.07 to the dollar and over 5 Turkish Lira/Euro

(courtesy zerohedge)

viii)TRUMP TO MAKE A MAJOR DECISION BY THE END OF TODAY ON SYRIA. HE IS EXTREMELY ANGRY AT THE CHEMICAL ATTACK ON FRIDAY BUT HE DOES NOT HAVE PROOF IT WAS ASSAD

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)This is just a small part in the criminal actions by the banks in manipulating gold and silver. As we get more canaries talking, it will get more intense

( Alan Flynn/Comex We have a Problem blog)

ii)Chris Powell comments on the above story

iii)A commentary on why silver should explode in price

(courtesy Gijsbert G)

iv)Ambrose Evans Pritchard explains why China will not benefit at all with they dump with USA treasuries as the USA Fed can easily soak up all of this debt.

( Ambrose Evans Pritchard/UKTelegraph)

v)Chinese foreign exchange reserves rise slightly as the USA dollar weakens

( GATA/Reuters)

vi)Cryptos crash on the weekend due to the Russian sanctions

( zerohedge)

vii)The sanctions against Russian aluminum company RUSAL is causing fears that they may collapse

( zerohedge)

10. USA stories which will influence the price of gold/silver

(courtesy zerohedge)

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:219,194 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 383,966 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A SMALLER THAN EXPECTED 516 CONTRACTS FROM 242,895 UP TO 243,411 AND A NEW RECORD OI FOR SILVER, WITH OUR 4 CENT RISE IN SILVER PRICING/ FRIDAY). ALSO,WE WERE ALSO INFORMED THAT WE HAD A STRONG 1470 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1470. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE AGAIN SURPRISINGLY AND SHOCKINGLY HAD ZERO LONG COMEX SILVER LIQUIDATION WITH OUR RECORD SILVER OPEN INTEREST. WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1986 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 516 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1470 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:1986 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month GAINED 1 contract RISING TO 337 contracts. We had 0 notices filed upon so in essence we GAINED 1 contract or 5,000 additional ounces of silver will stand for delivery in this non active delivery month of April.(AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS)

The next big active delivery month for silver will be May and here the OI LOST 3385 contracts DOWN to 147,662. June saw a loss of 4 contracts to stand at 38. The next big delivery month for silver is July and here the OI rose by 3532 contracts up to 57,739.

We had 0 notice(s) filed for NIL OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 9/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

1497 contracts

(149,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

657 notices

65,700 OZ

2.043 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 2 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (657) x 100 oz or 65,700 oz, to which we add the difference between the open interest for the front month of APRIL. (1499 contracts) minus the number of notices served upon today (2 x 100 oz per contract) equals 223,000 oz, the number of ounces standing in this active month of APRIL (6.699 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (657 x 100 oz or ounces + {(1499)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 223,000 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 76 COMEX OI CONTRACTS OR 7600 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

679,863.510

oz

Scotia

|

| Deposits to the Dealer Inventory |

601,255.440

oz

Brinks

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0

CONTRACT(S

NIL OZ)

|

| No of oz to be served (notices) |

337 contracts

(1,685,000 oz)

|

| Total monthly oz silver served (contracts) | 19 contracts

(95,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

i) Into Brinks: 601,255.440 oz

total dealer deposits: 601,255.440 oz

we had 0 deposits into the customer account

i) Into JPMorgan: zero oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

total deposits today: nil oz

we had 1 withdrawals from the customer account;

i) Out of Scotia: 679,863.510 oz

total withdrawals; 679,863.510 oz

we had 0 adjustment

total dealer silver: 59.452 million

total dealer + customer silver: 263.290 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 19 x 5,000 oz = 95,000 oz to which we add the difference between the open interest for the front month of April. (336) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 19(notices served so far)x 5000 oz + OI for front month of April(337) -number of notices served upon today (0)x 5000 oz equals 1,780,000 oz of silver standing for the April contract month

WE GAINED 1 SILVER CONTRACTS OR 5,000 ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 84,135 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 96,963 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 96,963 CONTRACTS EQUATES TO 484 MILLION OZ OR 69.22% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.14% (APRIL 9/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.52% to NAV (APRIL 9/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.14%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.52%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.14%: NAV 13.75/TRADING 13.41//DISCOUNT 2.14.

END

And now the Gold inventory at the GLD/

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 9/2018/ Inventory rests tonight at 859.99 tonnes

*IN LAST 358 TRADING DAYS: 81.05 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 308 TRADING DAYS: A NET 75.25 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 9/2018: A NO CHANGES IN SILVER INVENTORY:

Inventory 320.196 million oz

end

6 Month MM GOFO 1.90/ and libor 6 month duration 2.47

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.90%

libor 2.47 FOR 6 MONTHS/

GOLD LENDING RATE: .57%

XXXXXXXX

12 Month MM GOFO

+ 2.71%

LIBOR FOR 12 MONTH DURATION: 2.47

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

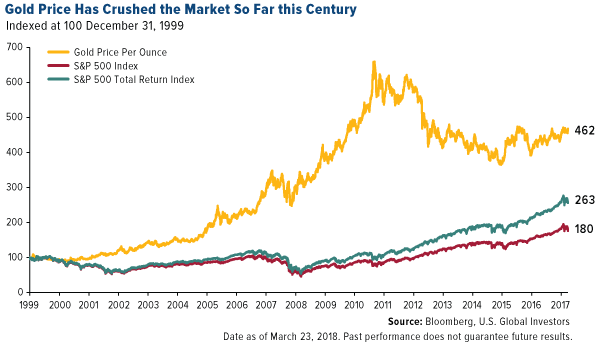

Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Gold outperforming stocks in 2018 and this century (see chart)

– Gold up close to 2% in 2018 while S&P 500 is down 2%

– Trump trade wars and Kudlow as Trump chief economic advisor is gold bullish

– Given gold’s performance, Kudlow’s dismissal of gold as “end of the world insurance” is “irrational”

– Market volatility could drive gold to $1,500/oz in 2018 – Holmes

Editor: Mark O’Byrne

Authored by Frank Holmes of US Funds

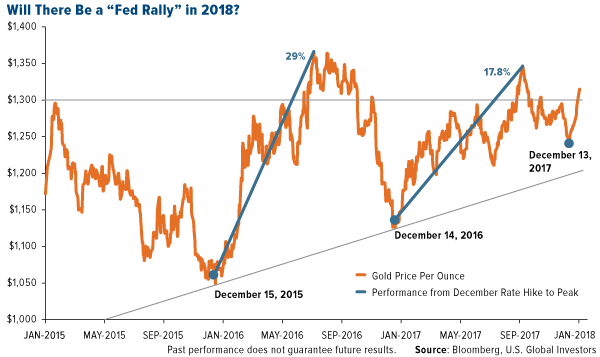

In a January post, I showed how the price of gold rallied in the months following the 2015 and 2016 December interest rate hikes—as much as 29 percent in the former cycle, 17.8 percent in the latter. Gold ended 2017 up double digits, despite pressure from skyrocketing stocks and massive cryptocurrency speculation.

I forecast then that we could see another “Fed rally” this year following the rate hike in December 2017. Hypothetically, if gold took a similar trajectory as the past two cycles, its price could climb as high as $1,500 this year.

As I told Kitco News’ Daniela Cambone last week, I stand by the $1,500 forecast. Before last week, investors might have been slightly disappointed by gold’s mostly sideways performance so far this year. But now, in response to a number of factors, it’s up close to 3 percent in 2018, compared to the S&P 500 Index, down 2.4 percent.

Living with Volatility

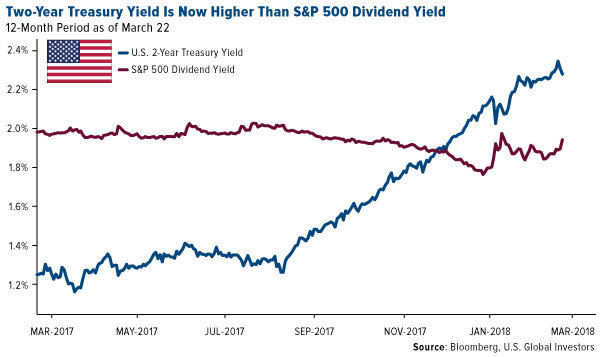

While I’m on the topic of equities, the S&P 500 dividend yield, for the first time in nearly a decade, is now below the yield on the two-year Treasury. Historically, the economy has slowed around six months after dividends stopped paying as much as short-dated government paper.

This could spur some stock investors to trim their exposure and rotate into other asset classes, including not just bonds but also precious metals, which I believe might help gold revisit resistance from its 2016 high of $1,374 an ounce.

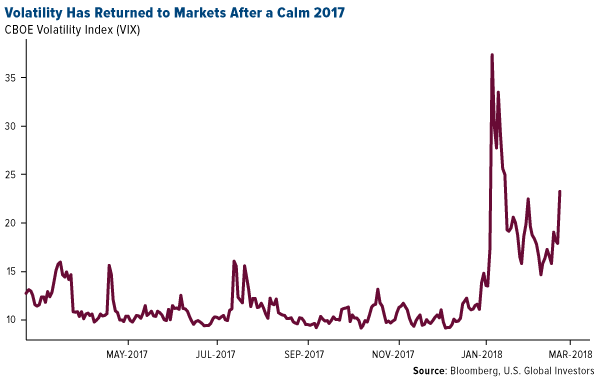

Volatility has also crept back into markets. It began with the positive wage growth report in February, implying the possibility of faster inflation. More recently, the CBOE Volatility Index (VIX), or “fear gauge,” has surged on the departures of Gary Cohn as chief economic advisor and Rex Tillerson as secretary of state, as well as the application of tariffs on steel and aluminum imports.

Last week, President Donald Trump ordered tariffs on at least $50 billion of Chinese goods, stoking new fears of a U.S.-China trade war. In response, the Asian giant proposed fresh duties on as much as $3 billion of U.S. products, including wine, fruits, nuts, ethanol and steel pipes.

As I see it, there could be other contributing factors pushing up the price of gold. A good place to start is with Trump’s recent appointment of former CNBC star Larry Kudlow as White House chief economic advisor.

Kudlow’s Kerfuffle Over Gold

Between 2001 and 2007, I appeared on Kudlow’s various CNBC shows a number of times, and though he always struck me as highly intelligent, informed and accomplished—he served as Bear Stearns’ chief economist and even advised President Ronald Reagan—it was clear he had a strong bias against gold. This was the case even as the price of the yellow metal was on a tear, rising from $270 in 2001 to more than $830 an ounce by the end of 2007.

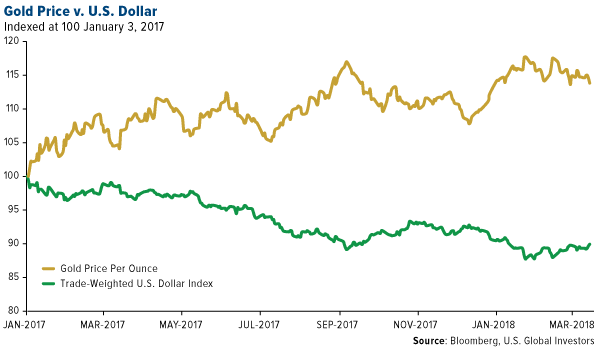

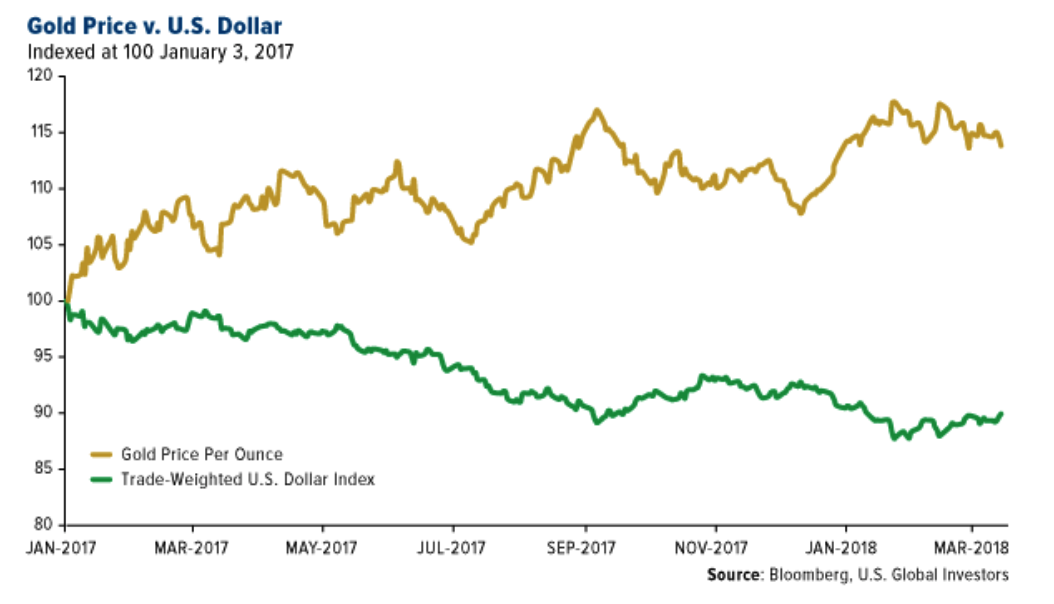

Kudlow showed his true colors toward gold as recently as this month, telling viewers: I would buy King Dollar and I would sell gold. As you can see below, this has’t been a prudent trade for more than a year now.

Earlier this month, Kudlow wrote that falling gold is good, as it “bodes well for the future economy.” He said he agreed with a friend, who called the metal an “end-of-the-world insurance contract.”

While there are those who would agree with him, it’s important to remember that gold is used for much more than as a portfolio diversifier, and its price is driven by a number of factors. These include Fear Trade factors, from inflation to negative real interest rates, and Love Trade factors such as gift-giving during cultural and religious festivals. The precious metal has important industrial applications as well.

And since I first went on Kudlow’s program, gold has outperformed the S&P 500’s price action nearly two-to-one, as I showed you back in December. Even with dividends reinvested, the market is still trailing the yellow metal.

So it’s fine if gold isn’t your favorite asset, but to dismiss it wholesale as Kudlow has again and again is, with all due respect, irrational.

It’s Not About Steel, It’s About Stealing

Kudlow isn’t just anti-gold, however.

He’s also anti-China, and even though he’s traditionally opposed tariffs in general, he supports Trump’s efforts to levy taxes on Chinese imports. Specifically, the duties are designed to offset the cost of intellectual property allegedly stolen by the Chinese over the past several years.

China’s J-31 fighter jet, for example, is believed to be a knockoff of Lockheed Martin’s F-35, the most expensive piece of U.S. military equipment. It’s for this reason that Lockheed’s CEO, Marillyn Hewson, was present when Trump signed the authorization to impose new tariffs.

Our intellectual property is hugely important to the U.S. economy. As important as steel and aluminum are, they account for only 2 percent of world trade, and in the U.S., it’s even less than a percent of gross domestic product (GDP). Technology exports, on the other hand, represent about 17 percent of U.S. GDP.

That said, the implications of a trade war with the world’s second-largest economy certainly have many investors concerned—all the more reason to consider adding to your gold allocation at this time. As always, I recommend a 10 percent weighting, with 5 percent in gold bullion, 5 percent in high-quality gold mining stocks and ETFs.

Is Trump Betting on the Wrong Guy?

On a final note, we were pleased to have an old friend visit our office last week. Michael Ding, a veteran of the U.S. Global investments team, joined us to share some laughs and his thoughts on what’s happening in Asian markets right now.

Specifically, Michael said that Ray Dalio, founder of mammoth investment firm Bridgewater Associates, which manages around $160 billion, has become something of an economic guru for members of the Chinese ruling party’s highest-ranking members, including Premier Li Keqiang.

Dalio—whose most recent book, Principles, nowtops China’s bestseller list—is reportedly advising the country’s top bankers and economists on how to deleverage safely without triggering a so-called “hard landing.”

A trade war between the U.S. and China, Ray Dalio said recently, would be a “tragedy.”

So to put it in perspective: Whereas Trump has just now brought on Kudlow, the Chinese are leaning on a fellow American, Dalio, one of the smartest, most gifted money managers in the world—not just of our time but of all time.

Did Trump make the right call? Which player would you want on your team: Kudlow or Dalio? For my money, I would pick Dalio.

This post was originally posted here

Recommended reading

Gold Outperforms Stocks In Q1, 2018

“Stars Are Slowly Aligning For Gold” – Frisby

Uncle Sam Issuing $300 Billion In New Debt This Week Alone

Gold and Silver Bullion – News and Commentary

Gold slips as dollar firms, but trade war fears persist (Reuters.com)

Soft NFP and trade tensions underpin gold ahead of CPI next week (FXStreet.com)

As U.S. and China trade tariff barbs, others scoop up U.S. soybeans (Reuters.com)

China’s Foreign Reserves Rise on Yuan Gains, Capital Curbs (Bloomberg.com)

Kashkari Says Fed Watching U.S.-China Spat as Markets Shudder (Bloomberg.com)

Source: US Global Investors

Another Superb COT Report For Silver (GoldSeek.com)

The Stars Be Aligned for $1,500 Gold (IRIS.xyz)

China has the ‘financial arsenic’ to ruin the US – but will it use it? (SMH.com)

India, Pakistan central banks clamp down on crypto-currencies (Reuters.com)

Chinese Investors Rush to Gold ETF as Trade Angst Adds to Risk (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices

09 Apr: USD 1,328.69, GBP 941.61 & EUR 1,082.29 per ounce

06 Apr: USD 1,325.60, GBP 946.08 & EUR 1,082.75 per ounce

05 Apr: USD 1,327.05, GBP 943.67 & EUR 1,080.75 per ounce

04 Apr: USD 1,343.15, GBP 955.52 & EUR 1,092.79 per ounce

03 Apr: USD 1,336.60, GBP 949.65 & EUR 1,085.99 per ounce

29 Mar: USD 1,323.90, GBP 941.69 & EUR 1,075.80 per ounce

Silver Prices

09 Apr: USD 16.37, GBP 11.60 & EUR 13.33 per ounce

06 Apr: USD 16.28, GBP 11.61 & EUR 13.30 per ounce

05 Apr: USD 16.31, GBP 11.59 & EUR 13.28 per ounce

04 Apr: USD 16.46, GBP 11.72 & EUR 13.40 per ounce

03 Apr: USD 16.52, GBP 11.78 & EUR 13.44 per ounce

29 Mar: USD 16.28, GBP 11.58 & EUR 13.21 per ounce

Recent Market Updates

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

This is just a small part in the criminal actions by the banks in manipulating gold and silver. As we get more canaries talking, it will get more intense

(courtesy Alan Flynn/Comex We have a Problem blog)

“I F**k The [Precious Metals] Market Around A Lot” – Spoofer Admits “I Was A Tyrant”

Authored by Alan Flynn via COMEX We Have A Problem blog,

Following news coverage of the charging of five precious metals traders and three banks in January, Commodities Futures Trading Commission and Department of Justice documents reveal a global criminal cabal of 16 traders operating in at least four major financial institutions between 2008 and 2015 to defraud COMEX gold and silver futures markets.

Of the many examples published, one reveals a UBS AG precious metals trader known as “The Legend,” spoofed sell orders to push down the price of gold futures on September 6, 2011, the day the gold market attained, and commenced a lengthy retreat, from its historic peak of US $1,923.70.

Jury trials are sought for Cedric Chanu and James Vorley of Deutsche Bank, Edward Bases and John Pacilio of Merrill Lynch Pierce Fenner & Smith, and Andre Flotron of UBS AG. The traders are indicted with multiple offences including spoofing, manipulation and attempted manipulation of the precious metals futures market. FBI investigations found many of the traders had placed “thousands” of fake orders over “hundreds” of occasions during the relevant period. Some even more.

Enforcement orders totaling $46.6 million were issued to Deutsche Bank, UBS AG and HSBC. Bank of America Merrill Lynch, parent company of Merrill Lynch Pierce Fenner & Smith, although implicated by the alleged actions of its subsidiaries traders, has not been sanctioned.

The agencies said traders placing genuine orders to buy or sell and concurrently huge opposite spoof orders to present a false picture of supply or demand. Other traders were thus tricked into accepting the genuine orders at prices favourable to the manipulators. The spoof orders being placed far enough away from the current price to safeguard against their actual execution were then swiftly cancelled. The traders had the ability using spoofing to move prices up or down.

By correlating details among multiple court documents and public sources it has been possible, with a high degree of certainty, to match the sample chats provided with the indicted traders, and banks they worked for.

“THE LEGEND”

Deutche Bank trader and Informant David Liew thought so highly of senior cabal member and co-conspirator, Trader F, according to Bloomberg’s disclosure of a sealed indictment, that he called him “The Legend.”

Trader F, as CFTC UBS Orders name, dominated the world of precious metals spoofing at UBS, appearing in nine of 12 manipulation samples listed in the CFTC UBS AG Orders, seven of which involve David Liew, Deutsche Bank informant. While the regulators describe four UBS traders as involved in the scandal, they currently seek a jury trial for only one.

Andre Flotron – LinkedIn image

Veteran UBS precious metals specialist Andre Flotron’s term at the trading desk predates the bank itself.

His LinkedIn timeline says he began trading gold and silver in 1982 with the Swiss Banking Corporation, Zurich. While still at the SBC precious metals desk, the corporation amalgamated with the Union Bank of Switzerland becoming UBS AG in 1999.

In over 15 years at UBS, the 55 year old worked two stints each in Zurich and Stamford. In addition to trading, he held also managerial and training responsibilities until January, 2014, when placed on leave from Zurich following an internal investigation.

An FBI affidavit describes how from July, 2008, Flotron mentored a new UBS employee in the art of spoofing. Trader#1 sat with Flotron for 2 months at his trading desk in Stamford, Connecticut “shadowing and observing” him with the aim of then transferring to the UBS precious metals desk in Singapore. The unnamed Trader#1 is now assisting the FBI investigation in return for immunity from prosecution.

In a teaching moment with a colleague about best practice for spoofing, on April 30, 2010, The Legend instructed:

“u gotta be quick with spoofs cause everyone else knows the trick too … except for smaller shops … and algos of course.”

Then contrasting the ease at which spoofing could be pulled off in years past:

“u know i use[d] to do that is Stamford so i can get filled … i’d be short 10k, show a bid for 35 lots … mkt chases it … i shift it lower … and lower.”

As the FBI investigators found, a hallmark of Flotron’s operation became placing spoof orders in quantities such as 22, 33, 44, 55, or 99 contracts by “automated trading software which had the ability to … place, modify, and cancel multiple orders nearly simultaneously.”

In one example allegedly aiming to manipulate the market down to his favourable purchase orders on October 17, 2013, Flotron placed and then withdrew three large fake sell orders for futures worth $30.5 million in gold over a 2.5 minute period.

The largest of his fake orders was placed, a parcel of 99 lots worth $13 million in gold, immediately doubled the volume of sell orders compared to buy orders, while “never intending” it to be executed, the indictment says. The multi-million dollar spoof order was sufficient to immediately bring sellers down from $1319.30 to $1,319.20 filling several of the trader’s partially concealed 1-contract bids totalling $1.5 million gold value.

Sometimes the traders could move COMEX much more.

On January 28, 2009, Deutsche Bank’s Edward Bases allegedly shifted the gold futures price two dollars in one attack alone by placing and quickly cancelling a number of large bids in order to “help” his then colleague Cedric Chanu’s resting orders fill.

As a post-spoof chat shows, the technique and camaraderie bore a strong semblance to computer gaming.

Bases: “so glad i could help…got that up 2 bucks…hahahahah.”

“that does show u how easy it is to manipulate so[me]times.”

Chanu: “yeah yeah of course.”

Bases: “that was alot of clicking”

Chanu: “basically you tricked alkll [sic] the algorythm”

Bases: “good man. Correct.i know how to “game” this stuff…”

Chanu: “THAT IS BRILLIANT.”

Bases: “I just dotn have the time to do it.. but i do it a lot in the aftermakete.

i f..k the m[ar]k[e]t around a lot…not alot of people…had it figgied

out…thats [sic] why i love electronic trading.”Bases: “im just glad we got you out…”

Besides helping each other achieve better than market prices, the Deutsche Bank traders helped UBS traders and traders from another global financial institution, Bank of America Merrill Lynch. One of the traders worked directly for two of the banks.

THE “TYRANT”

Edward Bases – Facebook image

Edward Bases was a metals tough guy. A 25-year career trading gold and silver in New York for the world’s largest banks, including a couple of years at Bear Sterns, gave him some trading bristle.

The era of floor trading in commodities and stocks was coming to an end when Bases departed Deutsche Bank for Bank of America Merrill Lynch in June, 2010. There, as he reminisced with a UBS trader in 2015, he was already a formidable spoofer in the pits long before he clicked his way to wealth at Deutsche Bank.

UBS Trader #2: “when you were a younger man where you also this angry?”

Bases: “In a different way”

“I was a tyrant”

“Different world”

“U called out dealersla”

“Sppoofed the mkt”

“Lined people up”

“It was very physcial and emotional”

“I was very good”

“At it”

At the trading desk as on the floor, when extra muscle was required to move prices Bases strong-armed it.

Paraphrasing the indictment: on January 28, 2009, his then colleague Cedric Chanu placed an iceberg order to sell 170 contracts with only one visible lot at $892.50. Five minutes later to help him out, Bases placed a spoof order to buy 250 contracts at $890.80, worth $22 million in gold, which he cancelled two seconds later. Straight away Bases placed a 240 lot spoof order to buy at various prices between $890.80 and $892.40, and all 170 of Chanu’s primary orders became filled.

The spoofing methods and amounts could be tweaked depending which market participants were being targeted.

THE TACTICIAN

John Pacilio – Facebook image

Hailing from the neighbouring affluent townships of New Caanan and Southport, Connecticut, 50 miles from New York, Bases, 56, and John Pacilio, 54, share an indictment of five charges in connection with Title 7 and 18 spoofing, manipulation, conspiring and fraud involving a commodity for future delivery.

While trading precious metals at Bank of America Merrill Lynch, New York, John Pacilio is alleged to have spoofed solo and in tandem with his colleagues including Bases, and other banks between January, 2010, and April, 2011. Pacilio’s published trades include the largest of spoofing examples by the six traders.

On February 4, 2011, Pacilio placed and cancelled within the space of less than a minute, spoof orders to sell the equivalent of $74.1 million worth of gold in futures contracts.

His spoofing victims weren’t always human and rational as the trader advised seven others at BOAML including Bases on November 16, 2010.

“guys the algos are really geared up in here. if you spoof this it really moves. thats where alot of this noise is coming from.”

According to court filings, 20 seconds later Pacilio placed an iceberg Primary Order to sell 10 silver futures contracts at $25.48. After 29 seconds he then placed a succession of Opposite Orders totalling 250 lots to buy silver futures at between $25.455 and 25.47, which were cancelled as soon as his Primary Orders were filled.

THE SPOKESMAN

Cedric Chanu – Twitter image

Three years after commencing with Deutsche Bank precious metals desk London, Chanu was promoted to Director, Precious Metals Trading Singapore, in 2011, where called on, in between weekend recreations, to promote and represent the German bank in its Asian precious metals business.

When interviewed by the Wall St Journal in September, 2012, Chanu, perhaps alluding to a growing disdain for spoofable forms of gold, noted “a dramatic increase in customers wanting to move out of paper, that is over-the-counter gold, and into physical.”

The trader had a brief stint trading for the Swiss company Gunvor after leaving Deutsche Bank at the end of 2013. The conglomerate got out of precious metals trading however, according to Bloomberg in December 2014, when “executives decided to abandon the precious metals trading business partly because of difficulties in finding steady supplies of gold where the origin could be well documented.” Gunvor, it appears, couldn’t locate unspoofable gold bullion at the same price and volume at which gold futures and unallocated gold investments were trading.

Part owned by Russian billionaire Gennady Timchenko until March, 2014, Gunvor ceased precious metals operations only one month after Deutsche Bank announced it was pulling out of precious metals trading in November, 2014.

Cedric Chanu’s indictment details nine examples out of “hundreds” of precious metals manipulations while at Deutsche Bank between December, 2008, and June, 2013.

A shared indictment for Chanu, 37, and his Deutsche Bank colleague James Vorley, 38, residents of the UAE and the UK respectively, was filed in an Illinois Court on January, 19. A Status Conference for the related civil case titled: CFTC vs Vorley and Chanu is scheduled for May, 7.

“THE MASTER”

London precious metals desk Deutsche Bank trader James Vorley cast himself in the theatre of chat as the quintessential English gent with a strong sense of fair play.

He even told a trader at another firm in October, 2007, of his repulsion at a third firms manipulation of either futures or another precious metals instrument:

“this spofi.ng [sic] is annoying / its illegal for a start…”its just not cricket.”

It was all a bad joke as FBI Special Agent Nevens found, seven months later from at least May, 2008, Vorley was running a “self enrichment scheme” to defraud the COMEX precious metals futures market and spoof training a new employee. His collaborators: Chanu and other Deutsche Bank traders, and those at another bank.

According to the indictment, the FBI uncovered over “a thousand” instances of Vorley trading in a pattern consistent with spoofing, “placing over ten thousand Opposite Orders,” presumably withdrawn, and coordinating in spoofing with his Deutsche Bank colleague Cedric Chanu “over one hundred times” up to March, 2015.

Included, an episode on March 16, 2011, when Vorley is recorded chatting to his colleague about “spoofing it up / ahem ahem” in relation to simultaneous platinum and gold futures trades.

Deutsche Bank co-conspirator turned informant David Liew whom Vorley trained in spoofing, testifies that Vorley preferred the term “jam it” when referring to the illegal act.

After one operation assisting Liew getting an order filled on November 3, 2010, Vorley “submitted and cancelled 29 buy orders at 10 contracts each”, and celebrated after:

“was cladssic [sic] / jam it / woooooooooooo…bif [sic] it up.”

As a sign of gratitude, his understudy Liew responded glowingly:

“tricks from the…master.” (Emphasis supplied.)

Not one to readily admit to wrongdoing, when queried in March, 2015, by Deutsche Bank compliance and employee relations, Vorley told them the term spoofing had been used “to describe more innocent and everyday occurrences.” He went on to defend the reason for his “inopportune use of the word spoof ” as “a bad example of market banter masquerading as sarcasm.”

A study by West Australian University Prof. Andrew Caminschi published September, 2013, observed gold and silver futures, and the GLD ETF, were “significantly impacted” by downward pricing anomalies from the London Gold and Silver PM Fixings leaking, prior to the publishing of the Fixing auction results.

A previously unreported crack through which the Fix prices may have bled from London to Chicago and elsewhere can be found in one of the six futures trader’s connection to the London Gold and Silver Fixings.

At the same time Deutsche Bank’s James Vorley is alleged by the CFTC and FBI to have manipulated COMEX precious metals futures, at least from May, 2008, to March, 2015, he was also a director of London Silver Market Fixing Limited and the London Gold Market Fixing Limited auctions.

The London Gold and Silver Fixings set the world benchmark prices for the precious metals twice daily. Vorley’s tenure on the Fix lasted between September 2009 and May, 2014, for the Gold Fixing, and October, 2015, for the Silver Fixing.

Three short weeks after Caminschci’s paper was published, UBS AG self-reported to global authorities that an internal investigation had uncovered “possible signs of manipulation, collusion and other market abusive conduct in foreign exchange trading” between the bank and other financial institutions. The Precious Metals Desk at UBS was a sub-unit of their Foreign Exchange Desk.

As precious metals class action lawsuits flooded US courts in the following three years, Vorley’s employer Deutsche Bank, failing to find a buyer for its seat, dropped out of the London Gold and Silver Fixings, disbanded their precious metals trading unit, payed $98 million to settle class action lawsuits alleging collusion in the London Gold and Silver Fixings, and supplied antitrust plaintiffs with significant evidence against co-defendants.

Short of an innocent sounding explanation as to how the precious metals pricing got so quickly from Fix-to-Futures, “ahem ahem,” it remains to be explored what Fixing information Vorley had prior to its publishing and what use, if any, he made of it in futures trading.

THE INFORMANT

After joining Deutsche Bank as a fresh graduate in 2009, David Liew was assigned, at completion of a short orientation and training period, to the Singapore Deutsche Bank precious metals desk. He was supervised and trained in manual spoofing by Vorley and Chanu, among others in Singapore and the UK, with whom he shared a “common electronic trading platform screen.” Here his trading could be monitored and he in turn could observe his mentor’s spoofing activities on his monitor.

David Liew – Google Plus image

CFTC findings stressed that by allowing the traders to observe each other’s orders, Deutsche Bank facilitated their spoofing activities. The bank’s traders also communicated across the globe via electronic chat rooms and video teleconferencing.

The 31 year old who participated in, solo and coordinated spoofing with other traders “hundreds of times,” and stop loss manipulation coordinated with Trader F at UBS, apparently Andre Flotron, pleaded guilty in a Chicago court on June 1, 2017. Stop loss manipulations were also undertaken with others at Deutsche Bank in relation to information about a large metals trade for a bank customer.

The penalty handed down by the CFTC for Liew included a lifetime ban from commodity trading, while a monetary fine was not imposed “based upon his cooperation in a Commission investigation and related proceedings.” The DOJ prosecutes his criminal trial where he is expected to receive reduced sentencing in return for cooperation as a witness.

According to the sealed FBI affidavit cited by Bloomberg, after Liew was taught to spoof by Vorley and Chanu at Deutsche Bank he went on to train others in the “tricks.”

Since leaving the bank, Liew has continued to use his business and training skills, as he told the Court in June last year.

“I’ve set up my own businesses. So, I — a co-owner of a restaurant. I own a online toy store for children. And most recently I’ve also started teaching programming to kids.”

Presently up to four Deutsche Bank, two Merrill Lynch and UBS AG traders associated with the alleged manipulations are absent from indictments. Similarly an HSBC trader who allegedly spoofed alone remains at large.

The only US financial organisation implicated, Bank of America Merrill Lynch and its indicted traders, Edward Bases and John Pacilio are absent from CFTC Orders and Complaints.

The first public proceedings for the six traders is to begin in couple of weeks with Flotron’s jury selection scheduled for April, 6. His trial under Judge Jeffrey A. Meyer in Newhaven, Connecticut, is set to commence on April, 9.

“BEYOND SPOOFING”

Even with the first trial about to start, four years since the last of the allegations, the precious metals probes continue.

The Department of Justice Fraud and Antitrust Divisions opened their precious metals investigations into financial institutions in 2015, but the criminal antitrust probe was closed in January, 2016. The US Government agencies were not the only parties investigating banks precious metals trading though.

The banks, defending also civil antitrust precious metals class action lawsuits, received an extraordinary boost in the form of letter/s from the DOJ announcing closure of the investigations. Predictably the letter was used by defendants straight away in an attempt to convince the Courts to dismiss the lawsuits.

The Court: “You all love this letter, don’t you?”

Defense Attorney: “They are not that easy to get, your Honor.”

The Court: “That’s true. You should have gold bars around it.”

Raising the spectre that the DOJ had botched the antitrust probe, in October the Court denied Motions to Dismiss against all the banks except UBS, the only non-Fixing bank defendant.

Challenging the Courts decision to dismiss civil complaints against UBS, only a short month later in November, the antitrust plaintiffs submitted damning new evidence.

Frank chat messages between traders in different banks, including UBS, about manipulating the Gold and Silver Fixes had been provided to plaintiffs by Deutsche Bank in their settlement cooperation materials. Surprisingly the DOJ had for 13 months sifted the same evidence without finding criminal evidence of antitrust conspiracy.

At the request of the DOJ the Court then placed the civil antitrust lawsuits on a partial stay of discovery for 12 months until December, 2017, doubtless to protect their ongoing precious metals fraud investigation.

To be fair to the DOJ, as Judge Valerie Caproni, former FBI General Counsel, had warned at the April, 2016, arguments, mistakes are not uncommon in government investigations.

“Just because a government investigation is closed…doesn’t mean everybody is innocent.”

Another reason for delays in criminal prosecution of the cartel, concerns international treaties. Andre Flotron’s indictment and arrest on US soil in September last year was a stroke of luck for investigators and prosecutors who understand that extradition between countries with different laws can be problematic.

For example in May, 2015, the CFTC brought spoofing charges in gold and silver futures against UAE traders Heet Khara and Nasim Salim for manipulation between February and April, 2015. In 2016 a Federal New York court ordered the duo to pay $1.38 and $1.31 million in civil monetary penalties, but the pair are yet to be indicted in the US.

The FBI is yet to declare if the futures traders were also manipulating the underlying commodity such as the Gold and Silver Fix and spot markets, not to mention other products such as ETF’s.

At Andre Flotron’s pre-trial Status Conference December 4, 2017, DOJ Fraud Section Attorney Micheal Rinaldi hinted at a bigger picture:

“The larger conspiracy includes this much larger universe where Mr. Flotron is spoofing on a regular basis.”

The Swiss trader, was all but named by a Swiss regulator in 2014 who said they had, “seen clear attempts to manipulate fixes in the precious metals markets,” at the UBS precious metals desk in Zurich. FINMA went on to ban two UBS precious metals traders for one year, evidently Flotron, principal trader at the desk since 2010, and another uncharged.

Answering the judge’s question at the October 5, 2017, Status Conference about Flotron’s witness statement and the possibility of new evidence emerging, Assistant U.S. Attorney Jonathon Francis said:

“if we have communications, his chats, his e-mails, something like that, here’s no reason not to give them to them now. It’s when we get into the sort of the everything else. And I’ll tell you, the everything else goes beyond spoofing. Because this investigation dealt with trading more broadly and many banks.”

Allan Flynn: Gold and silver futures were easy targets for spoofers

Submitted by cpowell on Fri, 2018-04-06 03:53. Section: Daily Dispatches

11:55a HKT Friday, April 6, 2018

Dear Friend of GATA and Gold:

Allan Flynn, who runs the “Comex, We Have a Problem” blog, this week posted a fascinating review of the traders who are the major targets of the recent investigation by the U.S. Justice Department and Commodity Futures Trading Commission of “spoofing” in the monetary metals futures markets.

Two details that may be of special interest:

1) The traders seemed to find “spoofing” exceedingly easy. So one may wonder how much easier market manipulation may be for governments with access to infinite money and more advanced technology and programming — especially since U.S. law fully authorizes the U.S. government to rig surreptitiously any market in the world.

2) The government’s first investigation of manipulation of the monetary metals markets failed to identify the evidence developed by the class-action anti-trust lawsuits brought against bullion banks in federal court in New York. The government’s second investigation has caused a long delay in those lawsuits.

Flynn’s report is headlined “U.S. Gold and Silver Futures Markets: ‘Easy’ Targets” and it’s posted at “Comex, We Have a Problem” here:

http://comexwehaveaproblem.blogspot.hk/2018/04/us-gold-silver-futures-ma…

Flynn, an Australian, is hoping to attend and report about the upcoming trial of one of the traders charged, which will be held in Connecticut soon, and is seeking to raise money for his expedition at GoFundMe here:

https://www.gofundme.com/Gold-Spoofing-Trial

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A commentary on why silver should explode in price

(courtesy Gijsbert G)

Explaining why the silver price should be at new highs! — My latest article on silver. All the facts show a huge breakout is nigh. Best Gijsbert

Explaining why the silver price should be at new highs:

(courtesy Gijsbert Groenewegen

end

Ambrose Evans Pritchard explains why China will not benefit at all with they dump with USA treasuries as the USA Fed can easily soak up all of this debt.

(courtesy Ambrose Evans Pritchard/UKTelegraph)

Ambrose Evans-Pritchard: China’s dumping Treasuries won’t win the trade war

Submitted by cpowell on Sat, 2018-04-07 13:34. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

via The Sydney Morning Herald

Saturday, April 7, 2018

https://www.smh.com.au/business/investments/china-has-the-financial-arse…

China’s leaders must be sorely tempted to activate the “nuclear option” and punish the capitalist running dog, the tango dancer in the White House.

They could at any time start to liquidate their $US1.2 trillion ($1.5 trillion) holdings of US Treasury debt, switching the proceeds into euro, sterling, krona, Aussie, or peso debt to stop the yuan exchange rate soaring.

Even a small dose of this financial arsenic would — in the minds of Beijing’s ultra-nationalist faction — set off a salutary panic. It would crater the US bond market at the very moment when Donald Trump’s fiscal depravity is driving the US budget deficit to a stratospheric $US1 trillion.

The contagion would spread instantly through US mortgages and consumer credit, and would detonate a Wall Street equity crash — the “Trump crash” in blood and gore.

Timed astutely, it might decide the midterm elections and deliver a Democratic Congress, one with control over the impeachment machinery. The demise of Trumpism would then be in sight, either because the Mueller inquiry establishes collusion with the Kremlin or because the president commits perjury in one of sundry lawsuits ensnaring him.

China need say nothing. Action would speak loud enough. If pressed to explain, it could state, with some justification, that US fiscal policy is out of control and that the Trump administration is not a fit custodian of any country’s wealth.

This drastic possibility is on the radar screen after China’s commerce ministry upped the ante with talk of “comprehensive measures,” which appear to go beyond trade. President Xi Jinping cannot retaliate symmetrically to Mr Trump’s new threat to impose tariffs on another $US100 billion of Chinese exports. China does not buy enough imports from the US to match it.

The Communist Party leadership will not kowtow to Mr Trump. The “opium century of humiliation” at Western hands is too fresh in the collective Chinese psyche to yield to such crude intimidation. Beijing said that the nation is “willing to make any sacrifice” to uphold its dignity.

The hardline tabloid Global Times has been writing daily editorials proclaiming that China is a coequal superpower with an arsenal of reserves and limitless tolerance for pain, so make our day. “To take China down would mean an unimaginably cruel battle for the US,” it said.

Yet the nuclear option is in reality almost useless. “The US Federal Reserve could counter it easily with emergency open market operations,” said Geoffrey Yu from UBS.

If the Fed can buy more than $US3 trillion of US Treasuries and mortgage bonds under its quantitative easing programme, it can equally soak up China’s entire holdings if necessary. A stroke of the electronic pen would do the job. Jeffrey Gundlach from DoubleLine Capital said China cannot fruitfully deploy its weapon. “It is more effective as a threat. If they sell, it would only eliminate their leverage,” he said.

Let us suppose as a Gedanken experiment that Xi Jinping did succeed in triggering a US financial crisis by this method. The consequences would be deeply destructive for China itself. The ensuing rout would engulf “risk assets” across the world, as the Chinese central bank has patiently explained to fire-breathers on the State Council. “It is just not worth the risk,” said Mr Wu.

The global mayhem would violate China’s solemn pledge to “protect the multilateral framework” and would drive away the very allies that it is so systematically cultivating. It would undermine the grand plan to steal the mantle of world leadership from the US, a fallen Trumpian dystopia that is abandoning the international system that Americans built and ran with such high statecraft for 70 years.

The Chinese equity and bond markets would crash, triggering a rerun of the capital flight crisis in early 2016, but this time with greater intensity. Mark Ostwald from ADM said it would lead to a worldwide scramble for US dollars, the reflex default in times of trouble for an international financial system that is leveraged to the hilt on dollar credit. The dollar would go through the roof. Never forget that it spiked 53 per cent against the euro as the Lehman crisis unfolded.

The Bank for International Settlements says offshore dollar debt has ballooned to $US25 trillion in direct loans and equivalent derivatives. At least $US1.7 trillion is debt owed by Chinese companies, often circumventing credit curbs at home. Any serious stress in the world financial system quickly turns into a vast dollar “margin call.” Woe betide any debtor who had to roll over three-month funding.

The financial “carry trade” would seize up across Asia, now the epicentre of global financial risk. Nomura said the region is a flashing map of red alerts under the bank’s predictive model of future financial blow-ups. East Asia is vulnerable to any external upset. The world’s biggest “credit gap” is in Hong Kong, where the overshoot above trend is 45 per cent of GDP. It is an accident waiting to happen.

China is of course a command economy with a state-controlled banking system. It can bathe the economy with stimulus and order lenders to refinance bad debts. It has adequate foreign reserve cover to bail out its foreign currency debtors. But it is also dangerously stretched, with an “augmented fiscal deficit” above 12 per cent of GDP.

It is grappling with the aftermath of an immense credit bubble that has pushed its debt-to-GDP ratio from 130 per cent to 270 per cent in 11 years, and it has reached credit saturation. Each yuan of new debt creates barely 0.3 yuan of extra GDP. The model is exhausted.

China has little to gain and much to lose from irate and impulsive gestures. Its deep interests are better served by seeking out the high ground — hoping the world will quietly forgive two decades of technology piracy — and biding its time as Mr Trump destroys American credibility in Asia.

The US president is a strategic gift if handled carefully. He is so ignorant and fundamentally shallow that he might even be induced to hand over Taiwan in exchange for a face-saving frippery on trade.

That truly would be the “art of the deal” — for China.

end

Chinese foreign exchange reserves rise slightly as the USA dollar weakens

(courtesy GATA/Reuters)

China’s forex reserves rise slightly as U.S. dollar weakness continues

Submitted by cpowell on Sun, 2018-04-08 04:50. Section: Daily Dispatches

From Reuters

Saturday, April 7, 2018

BEIJING — China’s foreign exchange reserves rose slightly in March as broad U.S. dollar weakness continued and escalating trade tensions between the world’s two largest economies bolstered expectations of a firmer Chinese currency.

Reserves rose $9 billion in March to $3.143 trillion, compared with a drop of $27 billion in February, central bank data showed on Sunday.

Economists polled by Reuters had expected reserves to increase by around $6 billion in March to $3.14 trillion. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-economy-forex-reserves/china-fo…

end

Cryptos crash on the weekend due to the Russian sanctions

(courtesy zerohedge)

Cryptos Crash As Russian Sanctions Ripple Through Markets

Despite news that more ultra-elite family wealth (Rockefellers) is being aimed at cryptocurrencies, it seems the US sanctions against Russian oligarchs has created some anxiety in the space with Ethereum and Bitcoin plunging.

For now the broad crypto space remains higher from Friday’s close…

But Bitcoin is back below $7,000 on heavy volume…

Catalysts for the move are unclear but some have suggested Oligarch’s pulling virtual currency to source dollars while others have suggested this is pre-emptive selling ahead of possible crackdowns to further pressure the oligarchs.

END

The sanctions against Russian aluminum company RUSAL is causing fears that they may collapse

(courtesy zerohedge)

Aluminum Soars On “Panic Buying” Amid Fears Of Imminent Rusal Collapse

While Russia’s currency and capital markets are tumbling in a delayed response to Friday’s US sanctions against a handful of Kremlin-friendly billionaires, one vital metal used across the globe in aircraft manufacturing and the auto industries is soaring today as a consequence to sanctions against Russia.

Aluminum prices have soared, first on Friday and then again on Monday, amid growing fears that sanctions on a Russian metal producer will prevent it from supplying the global commodity market, and could threaten a significant part of the global supply chain.

On Friday, the Treasury sanctioned Russian individuals, officials, state-owned firms and companies, including Rusal, the world’s second largest marker of aluminum, under provisions of a law Congress passed last year to retaliate against Moscow for meddling in the 2016 U.S. presidential election. The action actions target Russian oligarchs whose companies have wide-ranging involvement in international capital markets.

Of these, Rusal may be the most important one as it accounts for about 17% of supply outside of China, according to Harbor Intelligence, whose managing director, Jorge Vazquez said that sanctions are “going to create chaos in the short term.”

“This does warrant a little bit of panic buying by traders – the risk is large enough and real enough to buy on the back of insecurity of supply,” said Daniel Hynes, senior commodities strategist at Australia & New Zealand Banking Group Ltd.

And panic buying there is: aluminum for delivery in three months soared as much as 4% to $2,124 a metric ton on the London Metal Exchange, extending a 1.6% gain in the previous session, heading for the biggest jump in more than 2 years.

At the same time, the stock of Rusal tumbled a whopping 50% today alone amid fears that US sanctions – which have been designed to make it impossible for Deripaska’s commodity giant to do business in U.S. dollars – would terminally cripple the company, forcing an imminent bankruptcy and collapse for the company that is owned by one of President Vladimir Putin’s closest allies.

Adding fuel to the fire, the company warned that the sanctions may result in technical defaults on some credit obligations and be “materially adverse to the business and prospects of the group,” Rusal said in a statement Monday, adding its annual report may also be delayed. “The company’s primary focus remains its business and, most importantly, all of its global customers, investors and partners.”