GOLD: $1338.95 DOWN $17.40 (COMEX TO COMEX CLOSINGS)

Silver: $16.50 DOWN 27 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1335.20

silver: $16.46

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 660 FOR 66000 OZ (2.053 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 144 for 720,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7445/OFFER $7579: up $586(morning)

Bitcoin: BID/ $7642/offer 7742: up $752 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL AGAIN BY A CONSIDERABLE 2989 contracts from 227,175 FALLING TO 224,186 DESPITE YESTERDAY’S 16 CENT RISE IN SILVER PRICING. . WE AGAIN HAD CONSIDERABLE COMEX LIQUIDATION. BUT DUE TO THE RISE IN PRICE, WE MUST HAVE AGAIN WITNESSED CONSIDERABLE COMEX SHORT COVERING BY OUR BANKERS AS THEY HAVE NOW CAPITULATED AND WE SHOULD START TO SEE SILVER MOVE ON A HUGE NORTHERLY TRAJECTORY. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUMONGOUS SIZED (ATMOSPHERIC?) NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 8408 EFP’S FOR MAY AND 153 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 8561 CONTRACTS. WITH THE TRANSFER OF 8561 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 8561 CONTRACTS TRANSLATES INTO 42.80 MILLION OZ ACCOMPANYING THE FALL IN OPEN INTEREST IN SILVER AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

28,301 CONTRACTS (FOR 9 TRADING DAYS TOTAL 28301 CONTRACTS) OR 141.505 MILLION OZ: AVERAGE PER DAY: 3,144 CONTRACTS OR 15.722 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 141.505 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.21% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 859.99 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED LOSS IN COMEX OI SILVER COMEX OF 2989 DESPITE THE 16 CENT RISE IN SILVER PRICE. WE MUST HAVE HAD A LOT MORE SHORTCOVERING BY THE BANKERS. WE ALSO HAD ANOTHER STRONG SIZED EFP ISSUANCE OF 8561 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 8408 EFP’S FOR THE MONTH OF MAY AND 153 EFP CONTRACTS FOR JULY, WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A CONSIDERABLE 5572 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 8561 open interest contracts headed for London (EFP’s) TOGETHER WITH AN DECREASE OF 2989 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 16 CENTS AND A CLOSING PRICE OF $16.77 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.120 BILLION TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 WITH TRADING ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY AN ATMOSPHERIC SIZED 32,161 CONTRACTS UP TO 531,749 WITH THE GOOD SIZED GAIN IN PRICE/YESTERDAY’S TRADING ( GAIN OF $13.85). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN UNBELIEVABLY SIZED 21,936 CONTRACTS : JUNE SAW THE ISSUANCE OF 21,786 CONTRACTS , MAY SAW THE ISSUANCE OF 150 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 533,931. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A FAIRY TALE OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 32,161 OI CONTRACTS INCREASED AT THE COMEX AND AN ATMOSPHERIC SIZED 21,936 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 54,097 CONTRACTS OR 5,409,700 OZ =168.26 TONNES

YESTERDAY, WE HAD 5003 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 94,115 CONTRACTS OR 9,411,500 OZ OR 292.73 TONNES (9 TRADING DAYS AND THUS AVERAGING: 10,457 EFP CONTRACTS PER TRADING DAY OR 10,45,700 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 9 TRADING DAYS IN TONNES: 292.73 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 292.73/2550 x 100% TONNES = 11.47% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,337.21 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN UNBELIEVABLY SIZED INCREASE IN OI AT THE COMEX WITH THE GAIN IN PRICE // GOLD TRADING YESTERDAY ($13.85 GAIN). WE HAD A FAIRY TALE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 21,936 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 21,936 EFP CONTRACTS ISSUED, WE PROBABLY HAD THE LARGEST NET GAIN IN RECORDED HISTORY OF TOTAL OPEN INTEREST OF 54,097 contracts ON THE TWO EXCHANGES:

21,936 CONTRACTS MOVE TO LONDON AND 32,161 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 168.26 TONNES).

we had: 0 notice(s) filed upon for nil oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $17.40 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 859.99 tonnes.

SLV/

WITH SILVER DOWN 27 CENTS TODAY: NO CHANGES/

/INVENTORY RESTS AT 320.196 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A CONSIDERABLE 2989 CONTRACTS from 227,175 DOWN TO 224,186 (AND AWAY FROM THE NEW COMEX RECORD SET YESTERDAY/APRIL 9/2017). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

TODAY’S TRADING WITH THE RATHER LARGE COMEX LOSS OF CONTRACTS, SURPRISINGLY OCCURRED AGAIN WITH THE RISE IN PRICE OF SILVER (16 CENTS//). THUS FOR THREE STRAIGHT DAYS WE MUST HAVE HAD SOME CONSIDERABLE BANKER SHORT COVERING AT THE COMEX. OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 8408 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 153 EFP’S FOR JULY AND ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD AGAIN ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 2989 CONTRACTS TO THE 8561 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN 5577 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN APRIL (SEE BELOW). THE NET GAIN IN OI TODAY IN OZ ON THE TWO EXCHANGES: 27.860 MILLION OZ!!!

RESULT: A LARGE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE RISE IN SILVER PRICING / YESTERDAY (16 CENTS/BANKER SHORTCOVERING) . BUT WE ALSO HAD ANOTHER VERY FAIRY TALE SIZED 8561 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 27.92 POINTS OR 0.87% /Hang Sang CLOSED DOWN 66.43 POINTS OR 0.43% / The Nikkei closed DOWN 26.82 POINTS OR 0.12%/Australia’s all ordinaires CLOSED DOWN .24% /Chinese yuan (ONSHORE) closed UP at 6.2844/Oil UP to 66.71 dollars per barrel for WTI and 71.83 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2844 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2786 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

i)HONG KONG

The extremely high libor in the uSA is causing havoc to the Hong kong dollar as investors borrow heavily against a low HIBOR and buying higher yielding assets like the uSA dollar

( zerohedge)

( zerohedge)

4. EUROPEAN AFFAIRS

i)GREAT BRITAIN/ GERMANY, ITALY/FRANCE

Smart move on the part of Germany and Italy as they will not join the Syrian airstrikes as the do not want to confront Russia that supplies a major portion of their heating natural gas

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

ii)Good reason to whack gold today: Russia cannot exclude the possibility of war with the USA

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The Bundesbank is going to showcase German gold and prove that it is real. The problem is that only half is real…the other half at the FRBNY is nothing but paper obligations

( Bloomberg/Look/GATA)

ii)Bullion star interviews Chris Powell of GATA

( Chris Powell/GATA)

iii)We brought you this story yesterday: Iran is desperately searching for dollar.

(courtesy/GATA/AP.)

10. USA stories which will influence the price of gold/silver

unexpectedly dovish and that sent the Euro down/gold down.

( zerohedge)

ii)the markets both in Europe and the USA became green on Trump’s tweet: the Syrian attack “could take place very soon or not at all”

iv)Luongo emphasizes how the Deep State have placed their tentacles on Trump”

( Tom Luongo)

This is not good for the USA as already in this fiscal yr 2108, their USA budgetary deficit rises to 600 billion and the spending has not yet been implemented. Not only that but the interest payments already are north of 525 billion rising from last yr’s 424 billion. The interest payments are also set to climb so the uSA will surely surpass the 1.2 trillion deficit projection for the upcoming fiscal year 2019 starting in Oct

( zerohedge)

vi)SWAMP STORIES

a)After months of continual stalling at the last second Rosenstein hands the memo over that kick started the Russian probe. House Intelligence Committee Chairman Nunes received the mostly unredacted communication document.

( zerohedge)

( zerohedge)

c)Bannon urges Trump to fire Rosenstein to cripple the Mueller witchhunt

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:377,297 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 517,871 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL AGAIN BY A TOTALLY UNEXPECTED 2989 CONTRACTS FROM 227,175 DOWN TO 224,186 (AND AWAY FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018) DESPITE ANOTHER 16 CENT RISE IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A STRONG 8408 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS, 150 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 8561. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE SURPRISINGLY AND SHOCKINGLY HAD CONTINUAL LONG COMEX SILVER LIQUIDATION WITH OUR HIGH SILVER OPEN INTEREST . AS A RESULT WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE OF APRIL AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 6047 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2989 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 8561 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:5572 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 4 contracts LOWERING TO 217 contracts. We had 4 notices filed upon so in essence we GAINED 0 contracts or NIL additional ounces of silver will stand for delivery in this non active delivery month of April.

The next big active delivery month for silver will be May and here the OI LOST 8885 contracts DOWN to 118,807. June saw a GAIN of 6 contracts to stand at 54. The next big delivery month for silver is July and here the OI ROSE by 5213 contracts UP to 68497.

We had 0 notice(s) filed for nil OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 12/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

nil OZ

|

| No of oz to be served (notices) |

1348 contracts

(134,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

660 notices

66,000 OZ

2.053 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (660) x 100 oz or 66000 oz, to which we add the difference between the open interest for the front month of APRIL. (1348 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 200,800 oz, the number of ounces standing in this active month of APRIL (6.245 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (660 x 100 oz or ounces + {(1348)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 200,800 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 39 COMEX OI CONTRACTS OR 3900 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

995.098

oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0

CONTRACT(S

nil OZ)

|

| No of oz to be served (notices) |

217 contracts

(1,085,000 oz)

|

| Total monthly oz silver served (contracts) | 144 contracts

(720,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) into Delaware:995.098 oz

total deposits today: 995.098 oz

we had 0 withdrawals from the customer account;

total withdrawals; nil oz

we had 0 adjustment

total dealer silver: 59.452 million

total dealer + customer silver: 263.567 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR nil oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 144 x 5,000 oz = 720,000 oz to which we add the difference between the open interest for the front month of April. (217) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 140(notices served so far)x 5000 oz + OI for front month of April(217) -number of notices served upon today (0)x 5000 oz equals 1,805,000 oz of silver standing for the April contract month

WE GAINED 0 SILVER CONTRACT OR NIL ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 116,933 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 169,344 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 169,344 CONTRACTS EQUATES TO 846 MILLION OZ OR 120.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.96% (APRIL 12/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.67% to NAV (APRIL 12/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.96%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.67%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.27%: NAV 13.73/TRADING 13.42//DISCOUNT 2.27.

END

And now the Gold inventory at the GLD/

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 12/2018/ Inventory rests tonight at 859.99 tonnes

*IN LAST 361 TRADING DAYS: 81.05 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 311 TRADING DAYS: A NET 75.25 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 12/2018: A NO CHANGES IN SILVER INVENTORY:

Inventory 320.196 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.49

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.07%

libor 2.49 FOR 6 MONTHS/

GOLD LENDING RATE: .42%

XXXXXXXX

12 Month MM GOFO

+ 2.71%

LIBOR FOR 12 MONTH DURATION: 2.47

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Dow set to drop 300 points at open after Trump tweet today

– Stocks see sell off and gold pops to test resistance at $1,350/oz

– US stock futures suggest over 1% losses at New York open

– Oil surged to a two-week high and has surged nearly 7% this week

– U.S. bombing Syria may provoke escalation of conflict with Russia and wider conflict in volatile Middle East

President Donald Trump warned Russia in the last hour to “get ready” as U.S. missiles would soon be sent into Syria in response to a suspected chemical weapons attack.

Donald J. Trump

✔@realDonaldTrump

Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia, because they will be coming, nice and new and “smart!” You shouldn’t be partners with a Gas Killing Animal who kills his people and enjoys it!

Oil prices surged and extended gains after touching their highest levels in more than three years as geopolitical concerns and concerns of war in the Middle East rose.

Brent crude, the international benchmark, was up 1 per cent to over $71.68 per barrel. West Texas Intermediate, the US benchmark, was 1.3 per cent lower to $66.37.

Spot gold was up 0.8 per cent to $1,349.60 an ounce. Spot silver rose just 0.2% to $16.67/oz. Platinum and palladium were both 0.4% higher.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related Content

Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

News and Commentary

Gold up a third session to settle at 1-week high (MarketWatch.com)

Gold up on a softer dollar; U.S. CPI, Fed minutes in focus (Reuters.com)

Stocks Rally Amid U.S., China Conciliatory Remarks (Bloomberg.com)

Sterling basks at 2-week highs but risks grow (Reuters.com)

Global Debt Hits Record $237 Trillion, Up $21TN In 2017 (Bloomberg.com)

Gold’s Dot Plot Is Positive for Gold (Tocqueville.com)

US Congressman Pushes Bill To Reinstate Gold Standard (ZeroHedge.com)

Trump Is About To Make Us Gold Bugs Very Wealthy Again (ZeroHedge.com)

Is Silver Setting Up to Outshine Gold in the Near-Term? (Bloomberg.com)

Gold Prices (LBMA AM)

10 Apr: USD 1,335.95, GBP 942.25 & EUR 1,083.46 per ounce

09 Apr: USD 1,328.50, GBP 941.91 & EUR 1,082.33 per ounce

06 Apr: USD 1,325.60, GBP 946.08 & EUR 1,082.75 per ounce

05 Apr: USD 1,327.05, GBP 943.67 & EUR 1,080.75 per ounce

04 Apr: USD 1,343.15, GBP 955.52 & EUR 1,092.79 per ounce

03 Apr: USD 1,336.60, GBP 949.65 & EUR 1,085.99 per ounce

Silver Prices (LBMA)

10 Apr: USD 16.49, GBP 11.65 & EUR 13.38 per ounce

09 Apr: USD 16.34, GBP 11.59 & EUR 13.32 per ounce

06 Apr: USD 16.28, GBP 11.61 & EUR 13.30 per ounce

05 Apr: USD 16.31, GBP 11.59 & EUR 13.28 per ounce

04 Apr: USD 16.46, GBP 11.72 & EUR 13.40 per ounce

03 Apr: USD 16.52, GBP 11.78 & EUR 13.44 per ounce

Recent Market Updates

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

– “Stars Are Slowly Aligning For Gold” – Frisby

– Uncle Sam Issuing $300 Billion In New Debt This Week Alone

– Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

end

April 12/Goldcore

EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– EU and euro face growing risks including trade wars, energy independence and war with Russia in Middle East

– Middle East war involving Russia may badly impact energy dependent & fragile EU

– Trade and actual wars on European doorstep show the strategic weakness of the EU

– Toxic combination due to growing anti-EU and anti-Euro sentiment in many EU nations

– Investors should diversify to hedge investment, currency and systemic risk

Source: Bloomberg

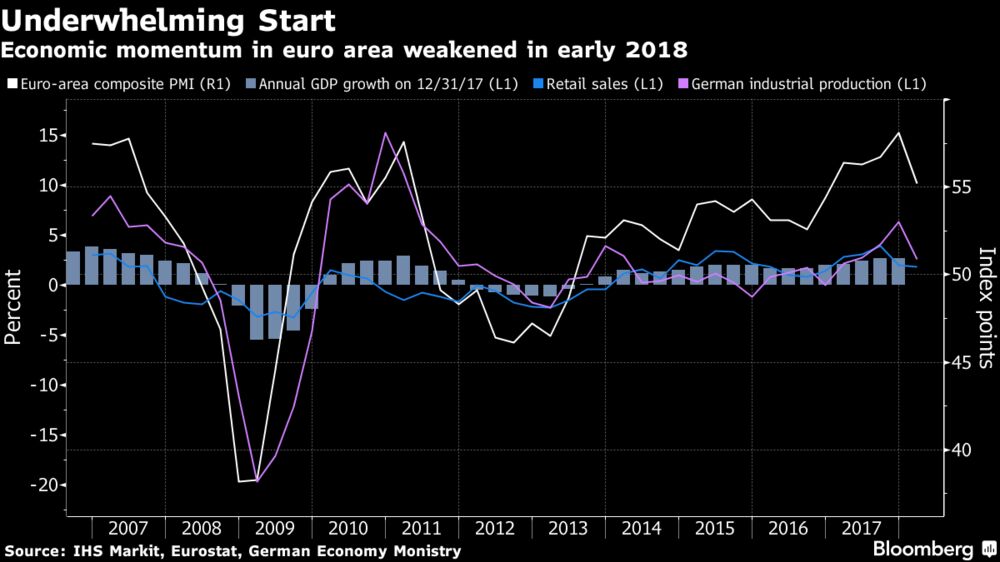

Recent economic data in the Eurozone has pointed to slowing economies. Retail sales and industrial production is down in many nations (see Bloomberg chart above – source). Germany, the prime driver of growth in the region has seen exports plunge due to the euro strengthening against the dollar and due to the risk of tariffs and a potential global trade war on the horizon.

Brexit has disappeared from the headlines, debt crises are yesterday’s news and frequent terrorist attacks in different EU nations seem to be taken in their stride. So one might think that things are on the up for the European Union.

This could not be further from the truth. The single-economic area has a major flaw: it is in a permanent state of dependence. Whether on democratically elected national leaders to tow the EU line, governments not to overspend, the rest of the world to tolerate the EU’s current account surpluses, Russia to supply energy and the powder keg that is the Middle East not to explode into a major conflagration and war.

Not to mention many chronically indebted nations with still fragile banks and banking systems. Contrary to perceptions, systemic risk has not gone away.

Many events going on both within and around the EU have exposed these major cracks in what is supposed to be the answer for peace and economic prosperity in Europe. The dangers to the union right now are manifold and look soon to manifest.

Going to war with our energy supplier

In recent days, we have covered the tragic state of affairs that is Syria, Trump tweets and the risks that a ‘Franz Ferdinand’ moment leads to a wider world war involving many nations who appear gung ho to eschew diplomacy and adopt military options.

Many western governments, media and indeed social media such as Facebook are keen to finger blame on Russia for literally everything they don’t like right now – whether a chemical attack on civilians or meddling in national elections on Facebook and Twitter.

One problem the EU in particular has with adopting a very aggressive U.S. military stance with Russia in Syria is that it is the EU’s largest supplier of gas. There is also the risk from the fact that Turkey appears to be breaking away from the EU and this could result in war at the borders of the EU. War, terrorism and new immigrant crisis on a scale of what was seen in recent years would be very destabilising.

Russia supplies of gas have been growing each year. 2017 was a stellar year for Gazprom who delivered record stocks of gas to the EU, with Germany and Austria responsible for record sales. This is despite sanctions.

The EU is much more dependent on Russia then is realised in this regard. For all the talk by France’s and the UK’s foreign secretaries of coming down hard on Russia’s involvement in Syria, Putin knows they can only go so far given the gas tap is in his backyard.

Politico reminds us:

Of far greater concern should be the fact that Slovakia, the Czech Republic and even Hungary, are nearly wholly reliant on Russian gas imports to fuel their economies — an arguably far greater risk to their economies and to their security.

Trade surplus and wars are a danger to the EU

Last week European stocks tanked as China and the US traded angry words with one another regarding tariffs. Europe is firmly caught in the crossfire. The threat is twofold – firstly we are hugely exposed to any trade war between the world’s biggest economies but secondly Trump may decide to impose his own sanctions on the EU too.

Jack Ewing in the New York Times explains the dilemma currently facing the single-market:

One is a good customer, a military ally and an old friend, although lately its behavior has been erratic.

The other is also a good customer, and despite a few spats and some lingering mistrust, it’s getting to be a more lucrative and dependable business partner all the time.

A spiralling war of tariffs and counter-tariffs would interfere with the global flow of raw materials and components for manufactured goods, disrupting the European economy. And some European companies, like the German carmaker BMW, manufacture in the United States and export to China. Such companies would see their sales suffer if China were to slap tariffs on American goods.

The EU cannot afford to have its trading relationships screwed up by Trump or Xi Jinping. The recovery, post-crisis, is now losing momentum and industrial production figures are slowing down. There is a danger that countries within the EU will be forced to negotiate separately with both China and the US, rather than collectively, as each fights to protect their economy.

As a collective the EU will have to work hard to persuade trading partners that it should not face trade tariffs. But this will be tricky given its trade surplus and Germany’s trade surplus in particular, which (until now) countries have put up with.

The macroeconomic dependency is more subtle, but it shows up in trade policy. The eurozone had a current account surplus of 3.5 per cent of GDP in 2017 — almost €400bn — a sum that needs to be absorbed by offsetting deficits in the rest of the world. The trade surplus explains why the EU is not keen to impose counter-sanctions to the US steel and aluminium tariffs once the temporary exemption ends on May 1. Wolfgang Munchau, FT.

Collective action with singular mindsets

The fault with the EU (and one that so many in Brussels are keen to ignore) is that the model only works if based on a singular mindset. However, how can this work when it is formed of so many small countries with their own singular mindsets and national interests?

When the Dutch far-right party failed to win the election in 2017, many Eurocrats decided this signalled that populism and the anti- establishment movement were in decline. In fact, this couldn’t be further from the truth

Take, for example, Victor Orban in Hungary. His eight-year rule has established him as the role-model for the anti-establishment movement that is sweeping across Europe, from Poland to Serbia to France.

The two-thirds parliamentary majority secured on Sunday by Orban is something the EU would like to make go away, so polar opposite to its own values is the Fidesz party.

But some politicians of the EU are not so sure. Following the victory French National Front leader Marine Le Pen said Orban’s win was rejection of “the change of values and the mass immigration extolled by the EU.”

Even in Germany there was some support from on high as reported by Bloomberg:

“I’m pleased with the election victory, it’s once again a very clear win for Viktor Orban,” Horst Seehofer, German federal interior minister, told reporters in Munich. He fired a volley at the EU to stop lecturing the Hungarian government over its shift to the right, adding: “I’ve always thought that this policy of arrogance and paternalism with respect to other member states is wrong.”

Italy is another example. And an extreme one. It is a country that has a serious tug-of-war with its own mindset and that of the EU. The tug-of-war that is the country’s current coalition government is made up of various parties, elected because of discontent regarding pretty much everything that is going on in Italy.

The same can be said in Hungary and Poland.

Poland has been at loggerheads with the EU establishment for over two years now over Polish national interests. Like Orban’s party, the ruling Law and Justice Party (PiS) has capitalized on the frustration with the post- communist transition. They are fed up with what they view as unequal economic paths and a lack of progress in catching up with the advances of the West.

In Italy they are tired of falling behind. The March 4 vote saw the anti- establishment 5-Star Movement take the most votes for a single party, but it wasn’t enough to secure leadership. Meanwhile a rightist alliance, including the League, Brothers of Italy and Berlusconi’s Forza Italia (Go Italy!) group won the biggest bloc of seats.

Coalitions have been formed but egos are now firmly in the way, in both the Italian parliament and in Brussels which is determined to prevent the 5 Star Movement from having any power, at all.

The problem is that no one comes close to the 5-Star Movement’s 26-30% majority. But this doesn’t seem to matter to the ivory tower residents in Brussels, who are deaf to the cries of the unemployed and economically fed up and blind to see the irony with which they bang on about democracy while ignoring the wishes of the citizens of the member states.

Even if the rightist alliance does manage to secure power, the major flaw is that Berlusconi and the League’s Salvini do not see eye to eye on much at all. Not the euro, taxes or immigration…

Salvini is an admirer of Orban. Following Sunday’s victory the party leader tweeted: “Hungary voted with the heart and with the head, ignoring the threats of Brussels and Soros’s billions…”

For all of the EU’s dismissal of these parties, they fail to miss one vital point – they keep winning elections and gaining in popularity.

We’re forgetting one important risk …the Euro

A few years ago we were considering how the euro itself might be the downfall of the Eurozone. It still might well be. Amongst the rising populism, outside threats and trade wars, the risks posed by the single currency will also challenge the EU in the coming months and years. As Sebastian Mallaby recently wrote in the Washington Post:

“The economic obstacles, including the reality that a single currency and a single interest rate are unlikely to serve a territory as large and varied as Europe. The monetary policy that suits Germany at any given time probably won’t be the one that happens also to suit Italy or Ireland. To manage this problem, you need large budgetary transfers from booming areas to depressed ones. You also need central insurance against banking crises in weak countries.”

The EU has economists, policy wonks and many and varied proposals as to how best to protect the euro. The problem is they all rely on everyone agreeing.

Why would the wealthier economies such as Germany allow their currency to continue to be debased in order to keep a dysfunctional monetary union intact?

The EU and indeed the monetary union in its current state is totally unsustainable. The political uprisings across the Union are one of the results of the single currency union itself, the union of political rule and the union of values – none of which have worked.

This weakness now leaves Europe hugely exposed to wider global events such as trade wars and actual wars on our doorstep in the Middle East.

This is the absolute opposite of the initial goals and vision of those who dreamt up this economic ‘solution’ post World Wars.

It is now not difficult to see the looming threats to the stability of the European financial and political systems.

Protect yourself from EU banking and euro risk

Investors and savers in the EU should be aware that these risks have not gone away and are merely dormant.

They should focus their energies on diversifying and protecting themselves from banks in the EU, the ongoing debasement of the euro and the not inconsequential risk of European monetary dis-union.

European banks, including Deutsche bank in Germany, remain vulnerable and the risk of bail-ins and the confiscation of deposits from savings account remains real.

Two years ago, the ECB approved the bail-in tool. In simple terms it gave them the right to bail out banks using the cash of unsecured creditors including individuals’ and companies.

Besides banking and currency risk, there is also the risk of national stock markets, bond markets and property markets under performing as they did during the financial crisis.

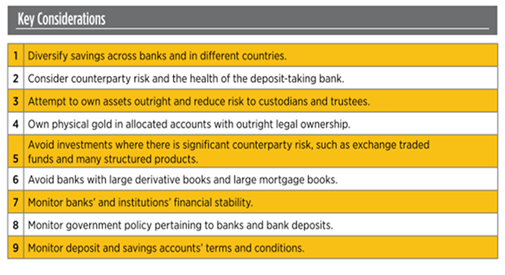

Savers need to consider counter party risk and diversify accordingly. Gold and silver bullion, if owned in the safest manner, remain one of the best options in this regard as if owned in the safest ways, it is very difficult indeed to confiscate them.

Physical, allocated and segregated bullion coin and bars ownership ensures all important liquidity, gives outright legal ownership and protection from counter party risk.

There is no dependency on single company websites and platforms and there are no counter parties who can claim it is legally theirs or legislation that rules that deposits can be confiscated to bail out failing banks.

Gold and silver bullion are important hedges and financial insurance against bail-ins, political mismanagement, and overreaching government and financial institutions.

-END-

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

The Bundesbank is going to showcase German gold and prove that it is real. The problem is that only half is real…the other half at the FRBNY is nothing but paper obligations

(courtesy Bloomberg/Look/GATA)

Bundesbank strives to show Germans that their gold is real

Submitted by cpowell on Wed, 2018-04-11 12:54. Section: Daily Dispatches

By Carolynn Look

Bloomberg News

Tuesday, April 10, 2018

If Germans have any doubts about the authenticity of their gold — and some of them really do — their central bank is doing all it can to qualm their concerns.

Germany’s Bundesbank this week launches a nearly six-month exhibition on gold, which will showcase the most interesting gold bars and coins in the central bank’s collection. That follows its release earlier this month of a book on “The Gold of the Germans,” which “for the first time shows readers the gold bars in such a way as if they were held in their own hands,” according to board member Carl-Ludwig Thiele.

The subject of the country’s reserves became particularly heated during the years of the sovereign debt crisis, when lawmakers and members of the public began to wonder why it had taken so long to repatriate the Bundesbank’s gold amassed during the post-war boom. Since then, the central bank has made an expedited effort to bring them back home, and it also made a short documentary on the subject. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-04-10/bundesbank-pulls-all-…

END

Bullion star interviews Chris Powell of GATA

(courtesy Chris Powell/GATA)

Bullion Star interviews GATA secretary in Singapore

Submitted by cpowell on Wed, 2018-04-11 13:04. Section: Daily Dispatches

9:05a ET Wednesday, April 11, 2018

Dear Friend of GATA and Gold:

Visiting Singapore two weeks ago to speak at the Mining Investment Asia conference, your secretary/treasurer was interviewed by Bullion Star Chief Operating Officer Luke Chua about GATA’s work and plans and the most recent surreptitious interventions in the monetary metals markets by central banks. The interview is a little longer than a half hour and can be viewed at You Tube here:

https://www.youtube.com/watch?v=Yb4BJN_BEJE&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

We brought you this story yesterday: Iran is desperately searching for dollar.

(courtesy/GATA/AP.)

So much for Iran’s trying to get away from the dollar

Submitted by cpowell on Wed, 2018-04-11 15:41. Section: Daily Dispatches

Iran Seeks to Pin Rial to the Dollar as It Hits Record Low

By Nasser Karimi

Associated Press

via ABC News, New York

Tuesday, April 10, 2018

Iran moved on Tuesday to enforce a single exchange rate to the dollar, banning all unregulated trading after the rial hit an all-time low.

The country’s senior vice president, Eshaq Jahangiri, was quoted by state TV as saying that the official rate will be 42,000 rials to the dollar as of Tuesday. He said that trading at any other price was forbidden and would be considered “smuggling.

The decision came late Monday after a two-day hike in prices of foreign currencies that saw the rial trading at 62,000 to the dollar — an 18 percent drop since Saturday.

In downtown Tehran, people lined up to buy hard currency outside an exchange office at the new, fixed rate but many complained there were not enough dollars available. Some exchange offices turned off their currency display boards. …

… For the remainder of the report:

http://abcnews.go.com/International/wireStory/iran-sets-rials-exchange-r…

* * *

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2844 /shanghai bourse CLOSED UP 27.92 POINTS OR 0.87% / HANG SANG CLOSED DOWN 66.43 POINTS OR 0.43%

2. Nikkei closed DOWN 26.82 POINTS OR 0.12%/ /USA: YEN RISES TO 107.11/

3. Europe stocks OPENED IN THE GREEN /USA dollar index RISES TO 89.74/Euro FALLS TO 1.2348

3b Japan 10 year bond yield: RISES TO . +.037/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.71 and Brent: 71.83

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.491%/Italian 10 yr bond yield UP to 1.784% /SPAIN 10 YR BOND YIELD UP TO 1.260%

3j Greek 10 year bond yield FALLS TO : 4.031?????????????????

3k Gold at $1346.90 silver at:16.65 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 109/100 in roubles/dollar) 61.63

3m oil into the 66 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.11 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9622 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1882 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.512%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.7936% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0102% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Jump, Global Stocks Extend Advance After Trump Tweet

It was a relatively subdued trading session, with markets treading water amid modest volumes awaiting news of action in Syria, until just after 6am ET when as we reported previously, Trump reversed on his Wednesday morning tweet, and in his latest tweetstorm, said that he “Never said when an attack on Syria would take place. Could be very soon or not so soon at all!”

Well, that certainly is one way to try and regain the “element of surprise”, even if it makes the whole fiasco even worse.

While implicitly Trump’s tweet makes the market confusion about Syria even worse, as instead of the original timetable of “72 hours before a strike”, this leaves the now-certain Syrian strike as open-ended, delaying the risk of a global selloff once Trump does launch, so far world stock markets, and US index futures, are loving what they see as a sign of de-escalation, and following Trump’s tweet, stocks in Europe and the UK, along with U.S. stock futures have jumped…

… after Trump’s tweet:

- Stoxx Europe 600 Index gains as much as 0.3%

- In London, the FTSE 100 gains as much as to 0.1%

- E-Mini futures on S&P and Dow Jones up 0.4%

That said, the situation in Syria is still problematic, and overnight we got reports that the US-led coalition was asking all Middle East flight companies to change itinerary for next 48 hours amid possible strike, according to Kurdistan24. Additionally, French President Macron says chemical weapons were used in Syria and that a reaction is coming in days. All Syria military bases are said to be on high alert as a US attack is expected, according to sources.

Trump’s Tweet was more than sufficient to make markets forget that, as China explained overnight, the reason for the torrid Tuesday rally was – as we said – wrong after Beijing warned that Xi speech wasn’t a concession to US and added it was ready to hit back at any escalation. Of course, that was Tuesday’s fake news, and who cares if it catalyzed a huge surge in the stock market.

Meanwhile European stocks got an extra lift earlier in the session after the Euro weakened to session lows after industrial output unexpectedly declined for a third consecutive month. In other news, bad news is good again, as the world’s “global coordinated recovery and reflation” phase slowly but surely ends. European equities began the day trading slightly lower with the risk-on sentiment seen in yesterday’s trade not being echoed early on, as market sentiment was largely being guided by increased tensions in Syria amid potentially imminent – or not so imminent now – military action by the US. European equity sector performance has largely been driven by company specific news with Deutsche Telekom (+4%) driving the telecoms sector higher (+0.7%) as T-Mobile, a company in which they own 64% of shares, has restarted deal talks with Sprint.

In Asia, Australia’s ASX 200 (-0.4%) failed to sustain mild opening gains as softer Australian consumer sentiment data and weaker than expected Chinese inflation figures clouded the upside seen in commodity related sectors. Nikkei 225 (-0.5%) was also lacklustre with J Front the worst off among the retailers on expectations of weaker profits this year, while SoftBank outperformed on M&A hopes after reports its unit Sprint and T-Mobile renewed merger talks. The Hang Seng (+0.5%) and Shanghai Comp. (+0.5%) were initially choppy as participants digested the miss on Chinese CPI and PPI data, although stocks gradually found some comfort from efforts by PBoC Governor Yi Gang to build upon the momentum from President Xi at the Boao forum in which the PBoC Governor talked about opening up and announced to increase stock connect quotas.

Meanwhile, geopolitical fears are not only stressing stocks, but oil too, although rising to the highest price in over 3 years, West Texas crude turned modestly lower overnight following recent big gains. As Bloomberg notes, oil has been advancing on growing concerns that the U.S. will take military action in the Middle East, and after Saudi Arabia intercepted a ballistic missile and shot down drones.

While that pushed down most of the main stock benchmarks in the region, it gave a break to oil-rich Russia, where the ruble bounced back from the lowest level in 15 months.

Elsewhere, markets were additionally pressured by Wednesday’s Fed hawkish minutes which showed officials leaned toward a slightly faster pace of policy tightening at their March meeting, even as they saw clear “downside risks” for the biggest economy from retaliatory trade duties, in other words, all Trump needs to avoid more rate hikes is escalate the trade war with China to nuclear.

Overnight, RBA Governor Lowe said his board does not see a strong case for raising interest rates in the near term; more likely next move in cash rate will be up rather than down. While some central banks are hiking rates, Australian circumstances are different. Serious escalation of trade tensions would risk health of the economy. Meanwhile, in Japan, BoJ Governor Kuroda says BoJ will continue powerful QE to meet inflation target, adds that there are expectations for consumer prices to keep rising.

Today’s data include jobless claims and earnings from BlackRock, Delta Air Lines, and Rite Aid. The U.S. won’t tolerate Russian aggression any more, Secretary of State nominee Mike Pompeo will say at his confirmation hearing Thursday, according to prepared remarks. He’ll make it a “personal priority” to work with allies to see if it’s possible to fix the Iran nuclear deal.

Market Snapshot

- S&P 500 futures up 0.4% to 2,656.00

- STOXX Europe 600 up 0.1% to 376.5

- MXAP down 0.4% to 173.84

- MXAPJ down 0.3% to 570.91

- Nikkei down 0.1% to 21,660.28

- Topix down 0.4% to 1,718.52

- Hang Seng Index down 0.2% to 30,831.28

- Shanghai Composite down 0.9% to 3,180.16

- Sensex up 0.5% to 34,123.36

- Australia S&P/ASX 200 down 0.2% to 5,815.53

- Kospi down 0.06% to 2,442.71

- German 10Y yield fell 0.2 bps to 0.497%

- Euro unchanged at $1.2367

- Italian 10Y yield rose 0.7 bps to 1.548%

- Spanish 10Y yield fell 0.4 bps to 1.268%

- Brent futures down 0.1% to $71.99/bbl

- Gold spot down 0.5% to $1,346.01

- U.S. Dollar Index up 0.2% to 89.77

Top Overnight News

- Congressional Republicans moved to head off any attempt by President Trump to fire special counsel Robert Mueller as the president continued to attack the Russia investigation and the Justice Department.

- China will “unquestionably” retaliate if the U.S. further escalates trade tension, and authorities have prepared a detailed, comprehensive counter-punch plan

- Federal Reserve officials leaned toward a slightly faster pace of policy tightening at their March meeting as their growth outlook and confidence in hitting their inflation target strengthened, according to minutes of the gathering released Wednesday

- Germany is leading a drive within the European Central Bank’s oversight arm for tough action this year to deal with nearly $1 trillion of bad loans on banks’ books, according to people with knowledge of the discussions

- President Donald Trump is still weighing options for U.S. military action against Syria as Western powers rallied against Syrian President Bashar al- Assad over an apparent chemical weapons attack near Damascus

- Theresa May’s officials could be lining up to keep the U.K. in the European customs union after Brexit, according to a new analysis that chimes with the views of parts of the British government

- Saudi Arabia said it intercepted a ballistic missile over Riyadh and shot down two drones in another part of the country on Wednesday

Asian equity markets traded mixed as sentiment settled down from the bullishness seen from President Xi Jinping’s conciliatory tone on Tuesday which resulted to a solid performance on Wall St, while attention turned to the geopolitical climate with a possible announcement on Syria said to be imminent. ASX 200 (-0.4%) failed to sustain mild opening gains as softer Australian consumer sentiment data and weaker than expected Chinese inflation figures clouded the upside seen in commodity related sectors. Nikkei 225 (-0.5%) was also lacklustre with J Front the worst off amongst the retailers on expectations of weaker profits this year, while SoftBank outperformed on M&A hopes after reports its unit Sprint and T-Mobile renewed merger talks. Hang Seng (+0.5%) and Shanghai Comp. (+0.5%) were initially choppy as participants digested the miss on Chinese CPI and PPI data, although stocks gradually found some comfort from efforts by PBoC Governor Yi Gang to build upon the momentum from President Xi at the Boao forum in which the PBoC Governor talked about opening up and announced to increase stock connect quotas. Finally, 10yr JGBs were flat as prices lacked direction amid an indecisive risk tone in the region, while the BoJ also kept the amounts of its Rinban announcement unchanged at just over JPY 1tln of JGBs in 1yr-10yr maturities.

Top Asian News

- IMF Aims to Nudge Xi’s Silk Road Plan Away From Spending Splurge

- Hong Kong Dollar Touches Weak End of Band, First Time Since 2005

- SoftBank in $25-Billion Plan to Reshape World Soccer, FT Reports

- IHH Said to Propose Up to $1.3 Billion Fortis Bid to Top TPG

European Equities began the day trading slightly lower (Stoxx 600 -0.2%) with the risk-on sentiment seen in yesterday’s trade not being echoed early on. This comes to fruition despite the revelations from Chinese president Xi mentioning a preference to implement auto tariff cuts as soon as possible (this relating to a possible reduction on import taxes on autos by half from 25% currently). Market sentiment is largely being guided by increased tensions in Syria amid potentially imminent military action by the US. This follows on from overnight news of increased air traffic over Syrian airspace and condemnation from the international community. EU equity sector performance has largely been driven by company specific news with Deutsche Telekom (+4%) driving the telecoms sector higher (+0.7%) as T-Mobile, a company in which they own 64% of shares, has restarted deal talks with Sprint. Elsewhere, Tesco are seen higher (+6.2%) amid encouraging earnings, whilst Hammerson shares are seen lower (-1.9%) post the rejection of a revised proposal from Klepierre for GBP 3.65/share and finally CHR Hansen also lag their peers (-4%) amid a miss on earnings.

Top European News

- Core Inflation Shows Riksbank Will Have a Hard Time Tightening

- Euro-Area Output Slump Adds to Concerns Over Economic Prospects

- Avast’s $1 Billion Listing to Be One of U.K.’s Largest Tech IPOs

- Sulzer Rebounds as Vekselberg’s Stake Cut Eases U.S. Sanctions

In currenices, remains narrowly mixed against G10 peers, but the Index looks prone to another downturn and test of near term chart support ahead of 89.000, with the late March low around 89.250 an obvious target. Optimism surrounding US-China trade negotiations have been somewhat neutralised or even negated by the Syrian situation. However, the Dollar could receive a reprieve from upcoming headline inflation data and or FOMC minutes. Several factors appear to have lifted GBP ahead of data with market observers still noting the bullish April seasonal element (even though the weather is still far from favourable), and of course Tuesday’s promptings from BoE hawk McCafferty. Reports suggesting an olive branch offered by chief EU Brexit negotiator Barnier may also be impacting as Cable climbed above 1.4200 and tested the next tech resistance zone 1.4215-25 (above the 10 DMA). Note, contacts reported selling in EUR/GBP from 0.8710 down to 0.8703 in the run up to the 9.30BST releases but in the event buyers were thwarted by weak output numbers vs an encouraging smaller trade shortfall. Renowned safe-havens have diverged yet again, as USD/JPY continues to hug 107.00 amidst option expiry interest at the strike, but with a more offered tone on the aforementioned geopolitical jitters. Conversely, USD/CHF is back up near 0.9600 vs circa 0.9550 at one stage, while EUR/CHF has rallied to fresh post-SNB floor removal highs around 1.1880, with M&A related flows perhaps impacting alongside more official activity, according to others. EUR is edging more gains towards 1.2400, but hampered by offers ahead of the next big figure and also wary of decent expiries between 1.2345-60 (1.8bn). ECB minutes and speeches may provide more independent direction after hawkish comments from Nowotny on Tuesday were confirmed as personal rather than a collective policy view

In commodities, WTI and Brent crude futures trade relatively flat following yesterday’s circa 3.7% gains. Downside was initially seen in the wake of last night’s unexpected build in the API inventories (+1.758mln vs. Exp. -0.200mln) with comments from the Iranian oil minster stating that USD 60/bbl is a good price for oil given current conditions with USD 70/bbl too high a level. Note, the comments appear to be at odds with reports yesterday suggesting that Saudi are to seek an oil price of around USD 80/bbl. However, losses were short-lived with traders mindful of any geopolitical developments with US military officials saying that the US is ready to attack Syria upon orders from President Trump which could come at any time. In metals markets, spot gold has benefitted from the modest risk aversion seen in markets thus far with the slightly softer USD also giving prices a helping hand. Elsewhere, copper was initially firmer overnight alongside early gains in Chinese metals amid restocking demand and expectations of increased construction activity in the upcoming month before staging a retreat. Finally, iron ore prices were seen lower overnight amid concerns over steel margins, whilst aluminium is once again seen higher in London trade as the fallout from Russian sanctions continues to guide price action.

Looking at the day ahead, France’s March CPI and the February industrial production print for the Euro area are due. The BoE’s credit conditions and bank liabilities survey will also be out. In the US, data includes the latest weekly initial jobless claims print, and March import price index reading. In the evening the Bundesbank’s Weidmann and Fed’s Kashkari are due to speak at separate events. The ECB’s Coeure is also due to speak in Paris.

US event calendar

- 8:30am: Initial Jobless Claims, est. 230,000, prior 242,000; Continuing Claims, est. 1.84m, prior 1.81m

- 8:30am: Import Price Index MoM, est. 0.1%, prior 0.4%; Export Price Index MoM, est. 0.15%, prior 0.2%

- 9:45am: Bloomberg Consumer Comfort, prior 57.2

DB’s Jim Reid concludes the overnight wrap

As we await the almost inevitable response from the US and others in the West to the Syrian situation, markets are moving from the relief that the trade war rhetoric has stepped back for now to a realisation that the Middle East rhetoric is stepping up. Mr Trump fired off two somewhat conflicting tweets aimed at Russia yesterday. The first very provocative, the second more conciliatory and quite profound! Firstly he said “Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia because they will be coming, nice and new and smart. You shouldn’t be partners with a gas killing animal who kills his people and enjoys it”. Secondly, “Our relationship with Russia is worse now than it has ever been, and that includes the Cold War. There is no reason for this. Russia needs us to help with their economy, something that would be very easy to do, and we need all nations to work together”.

Anyway, the short-term geo-political fear has been the dominant theme over the last 24 hours, overshadowing an in line US CPI print and a slightly hawkish set of Fed minutes. The risk off tone saw the Stoxx 600 fall for the first time in three days (-0.59%) while losses in the S&P accelerated during the day following the slightly hawkish FOMC minutes before eventually closing at -0.55%. Safe haven assets were in vogue with gold up +1.03%, bonds firming (UST 10y yields -2bp; Bunds -1.6bp), while WTI oil jumped to the highest in c3 years (+2.0% to $66.82/bbl). The latter partly helped by news that Yemen rebels have fired a ballistic missile at Saudi Arabia’s capital before being intercepted.

Back to Syria, sources told Bloomberg that President Trump is still weighing options while White House spokeswoman Sanders noted “…we have a number of options and all those options are still on the table” and when asked whether military actions were possible, she said “final decisions haven’t been made yet on that front”. In the UK, the Daily Telegraph has cited unnamed sources that PM May has ordered submarines to move within missile range of Syria while the BBC reported earlier that the PM is ready to join military actions in Syria without seeking parliamentary consent first.

Moving onto the FOMC minutes now. They indicated that “all participants agreed that the outlook for the economy beyond the current quarter had strengthened in recent months” and that “all participants expected inflation on a 12-month basis to move up in coming months”, which should not be too surprising given prior commentaries, but then the minutes also added that “a number of participants indicated….the appropriate path for the federal funds rate over the next few years would likely be slightly steeper than they had previously expected”.

Notably, the minutes also indicated that participants discussed the possibility of revising the statement’s language “at some point” to acknowledge that monetary policy “would gradually move from an accommodative stance to being a neutral or restraining factor for economic activity”. Elsewhere on trade, “participants did not see the steel tariffs, by themselves….as likely to have a significant effect on the national economic outlook….but a strong majority of participants viewed the prospects of retaliatory trade actions by other countries as a downside risk”.

This morning in Asia, markets are mixed with the Kospi (+0.22%) slightly up while the Nikkei (-0.20%), Hang Seng (-0.23%) and Shanghai Comp. (-0.60%) are down as we type. In Japan, BOJ Governor Kuroda noted”…we expect inflation to accelerate as a trend and head towards 2%” while the BOJ will maintain its stimulus program “until needed to stably and sustainably achieve” its target.

Now recapping other markets performance from yesterday. US bourses weakened (Dow -0.90%; Nasdaq -0.36%) and within the S&P, only the energy and real estate sectors were up while losses were led by telcos, financials and healthcare stocks. In tech, the Congressional hearings involving Facebook’s CEO seemed to be gone relatively well with little consensus on potential regulations.

Facebook’s shares rose +0.78% yesterday while the Nasdaq 100 index dipped -0.49%. Across Europe, markets were also modestly lower with the DAX (-0.83%) and FTSE (-0.13%) both down while Russia’s MOEX rose for the second consecutive day (+0.85%). The VIX traded within a c2pt range before closing -1.1% lower to 20.24.

Over in government bonds, the curve has flattened further with the 2s10s and 5s30s down -2bp and -1.4bp respectively and back near its 10 year low. Elsewhere, Italian BTPs slightly underperformed as Bloomberg reported the Italian President may give a preliminary mandate to League Party leader Salvini to form the next government if no progress in coalition talks is made by early next week (10y yields +0.7bp). In FX, the US dollar index weakened for the fourth consecutive day (-0.02%) while the Euro and Sterling were marginally higher. In commodities, LME aluminium prices rose for the sixth consecutive day and are now at the highest since early January (+13.8% on a cumulative basis), in part due to the potential disruption of Russian supply.

Turning now to Draghi’s latest comments on trade and inflation. He reiterated that the direct impact from announced protectionist measures are not big, but “we’ve be especially mindful of another more subtle channel which can affect the economy (ie: the potential hit to confidence)”, which “can be very important in the coming months”. Elsewhere, he has broadly stuck to script and is confident wages will pick up and inflation will eventually move towards the ECB goal as the economy improves. Finally, the ECB’s Hansson noted the ECB should move ahead with policy normalisation “maybe with a little bit more courage, but I think that all these changes need to be gradual”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the March core CPI was in line at 0.2% mom. As last year’s big decline in mobile services prices dropped out of the calculation, the annual core CPI rose to a 13 month high of 2.1% yoy – also in line with expectations. Notably, on a 3 and 6 month annualised basis, inflation momentum is stronger at 2.9% yoy and 2.6% yoy respectively. Elsewhere, the NY Fed’s underlying inflation gauge was steady in March with the prices index up 2.2% yoy while the Cleveland Fed reported a 2.5% yoy rise in the weighted median. Our US economists viewed this month’s CPI as consistent with their forecast that core CPI will rise to 2.3% yoy this year. Finally, the March monthly budget deficit was wider than expected at -$209bln (vs. -$186bln expected).

The UK’s February IP was below market at 0.1% mom (vs. 0.4% expected), leading to annual growth of 2.2% yoy, while manufacturing output fell for the first time in 11 months (-0.2% mom vs. 0.2% expected). The February trade deficit was narrower than expected at -£1.0bln (vs. -£2.6bln) as growth in exports outpaced imports. Italy’s February retail sales was slightly above market at 0.4% mom (vs. 0.3%) while the Bank of France’s March industrial sentiment index was 103 (vs. 104 expected).

Looking at the day ahead, France’s March CPI and the February industrial production print for the Euro area are due. The BoE’s credit conditions and bank liabilities survey will also be out. In the US, data includes the latest weekly initial jobless claims print, and March import price index reading. In the evening the Bundesbank’s Weidmann and Fed’s Kashkari are due to speak at separate events. The ECB’s Coeure is also due to speak in Paris.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 27.92 POINTS OR 0.87% /Hang Sang CLOSED DOWN 66.43 POINTS OR 0.43% / The Nikkei closed DOWN 26.82 POINTS OR 0.12%/Australia’s all ordinaires CLOSED DOWN .24% /Chinese yuan (ONSHORE) closed UP at 6.2844/Oil UP to 66.71 dollars per barrel for WTI and 71.83 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2844 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2786 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

HONG KONG