GOLD: $1346.90 DOWN $ 1.00 (COMEX TO COMEX CLOSINGS)

Silver: $16.78 UP 10 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1347.50

silver: $16.78

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 663 FOR 66300 OZ (2.062 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

115 NOTICE(S) FILED TODAY FOR

575,000 OZ/

Total number of notices filed so far this month: 379 for 1,895,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8039/OFFER $8139: up $32(morning)

Bitcoin: BID/ $7862/offer 7962: DOWN $146 (CLOSING/5 PM)

end

I will be reporting on the Shanghai gold fix as I can now attest to it’s accuracy:

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

TOMORROW I WILL PROVIDE BOTH FIXES.

Second gold fix early this morning:1353.83

USA gold at the exact same time: 1346.60

PREMIUM TO NY SPOT: $7.23

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST SURPRISINGLY FELL AGAIN BY A CONSIDERABLE 3817 CONTRACTS FROM 217,817 FALLING TO 214,000 DESPITE YESTERDAY’S 7 CENT RISE IN SILVER PRICING. WE AGAIN HAD CONSIDERABLE COMEX LIQUIDATION AND FOR SURE BANK SHORTCOVERING AT THE COMEX. WE WERE AGAIN NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 555 EFP’S FOR MAY AND 207 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 762 CONTRACTS. WITH THE TRANSFER OF 762 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 768 EFP CONTRACTS TRANSLATES INTO 3.810 MILLION OZ ACCOMPANYING THE RISE IN SILVER PRICE AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

33,744 CONTRACTS (FOR 12 TRADING DAYS TOTAL 33,744 CONTRACTS) OR 168.720 MILLION OZ: AVERAGE PER DAY: 2,812 CONTRACTS OR 14.060 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 168.720 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.10% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 887.205 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED LOSS IN COMEX OI SILVER COMEX OF 3817 DESPITE THE 7 CENT GAIN IN SILVER PRICE. WE MUST HAVE HAD SOME SHORTCOVERING BY THE BANKERS AS A SMALL AMOUNT OF THE LOST COMEX OPEN INTEREST LANDED IN LONDON AS FORWARDS. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 762 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA 535 EFP’S FOR THE MONTH OF MAY AND 207 EFP CONTRACTS FOR JULY, WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE LOST 3055 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 762 open interest contracts headed for London (EFP’s) TOGETHER WITH AN DECREASE OF 3817 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 7 CENTS AND A CLOSING PRICE OF $16.68 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.070 BILLION TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 115 NOTICE(S) FOR 575,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY AN FAIR SIZED 2699 CONTRACTS UP TO 509,128 WITH THE SMALL GAIN IN PRICE/YESTERDAY’S TRADING ( RISE OF $2.80). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9736 CONTRACTS : JUNE SAW THE ISSUANCE OF 9736 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 509,823. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES 2699 OI CONTRACTS INCREASED AT THE COMEX AND AN STRONG SIZED 9736 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 12,435 CONTRACTS OR 1,243,500 OZ = 38.678 TONNES.

YESTERDAY, WE HAD 10,403 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 130,927 CONTRACTS OR 13,092,700 OZ OR 407.23 TONNES (12 TRADING DAYS AND THUS AVERAGING: 10,910 EFP CONTRACTS PER TRADING DAY OR 1,091,000 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 12 TRADING DAYS IN TONNES: 407.23 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 407.23/2550 x 100% TONNES = 15.96% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,451.17 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 2699 WITH THE RISE IN PRICE // GOLD TRADING YESTERDAY ($2.80 GAIN). HOWEVER, WE HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9736 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9736 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED NET GAIN OF 12,435 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9736 CONTRACTS MOVE TO LONDON AND 2699 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 40.83 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $1.00 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER UP 10 CENTS TODAY: NO CHANGES/

/INVENTORY RESTS AT 320.196 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE 3817 CONTRACTS from 217,817 DOWN TO 214,000 (AND AWAY FROM THE NEW COMEX RECORD SET YESTERDAY/APRIL 9/2017). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE RATHER LARGE COMEX LOSS OF 3817 CONTRACTS, OCCURRED DESPITE THE RISE IN PRICE OF SILVER (7 CENTS//). THE COMEX OPEN INTEREST HAS FALLEN FOR 6 CONSECUTIVE DAYS. HOWEVER OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 555 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 207 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 762 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3817 CONTRACTS TO THE 762 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL NET LOSS 3055 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 15.275 MILLION OZ!!! AND THIS OCCURRED WITH A RISE IN PRICE OF 7 CENTS. THE BANKERS ARE CAPITULATING AS THEY DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT.

RESULT: A LARGE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE RISE IN SILVER PRICING / YESTERDAY (7 CENTS/) . BUT WE ALSO HAD ANOTHER SMALL SIZED 762 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed DOWN 43.85 POINTS OR 1.41% /Hang Sang CLOSED DOWN 252.84 POINTS OR 0.83% / The Nikkei closed UP 12.06 POINTS OR 0.06%/Australia’s all ordinaires CLOSED UP .02% /Chinese yuan (ONSHORE) closed UP at 6.2834/Oil DOWN to 66.69 dollars per barrel for WTI and 71.81 for Brent. Stocks in Europe OPENED IN THE RED . ONSHORE YUAN CLOSED UP AT 6.2834 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2773 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

3 c CHINA

i)USA is now planning a 3rd front into its attack on China. China does not allow USA firms to compete in China unless they find a joint venture partner of Chinese origin. Basically Chinese high technology is off limits to the USA and Trump is planning to remedy this:

(courtesy zerohedge)

ii)Two major points this morning:

- Chinese Macro data huge disappoints which sends their stocks markets into a tailspin

- China is now threatening retaliation for the ban of high tech equipment from the uSA to China’s big telecom company ZTE. It seems that these guys were selling their chips to Iran.

(courtesy zerohedge)

( zerohedge)

iv)China, true to form and carrying on its trade war with the USA announces a huge 179% tariff on USA Sorghum used in animal feed.

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Now we know what happened last week when we were informed of a massive explosion last Monday inside the T4 air base. At the time nobody claimed responsibility. Once the Americans categorically stated that they had nothing to do with the hit, all eyes turned on Israel..and sure enough they admitted the attack today.

The question was why they targeted an Iranian drone base. Israel now state that Iran sent over a drone into Israeli soil carrying explosives and this drone was shot down. This is the very first confrontation between Iran and Israel directly and no through proxies.

thus the reason for the attack on live Iranian targets inside Syria..this will escalate!

( zerohedge)

ii)This is big: Robert Fisk, famed war reporter for the UK Independent now reached his conclusion after visiting the Syrian chemical gas attack that the Syrians inside East Ghouta were not gassed.

(courtesy zerohedge)

iii)This is interesting: The Russians find a chemical weapons lab right inside the rebel held section of Douma. The USA side states that the Russians have somehow hid this…do not make this up

(courtesy zerohedge)

6 .GLOBAL ISSUES

The IMF warns of huge risks to the system:

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Surprising China increases its USA treasuries despite trade tensions due to the tariff war

(Wigglesworth/London’s Financial times)

ii)We knew that this would happen: Venezuela’s oil workers are now requesting payment in dollars for their wages

(courtesy Bloomberg)

iii)Mac Slavo reports why Eastern Central banks and one major bullion bank (JPMorgan) is stockpiling physical gold and silver

( Mac Slavo SHTFPlan.com)

10. USA stories which will influence the price of gold/silver

Although housing starts and permits rebound in March the general 2018 housing scene is not very promising;

( zerohedge)

iv)David Stockman talks about the failed Empire first American policy:

iii)SWAMP STORIES

b)Trump is very worried about what is seized in the Cohen raid

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:265,609 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 277,452 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL AGAIN BY 3817 CONTRACTS FROM 217,817 DOWN TO 214,000 (AND AWAY FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018) DESPITE THE 7 CENT RISE IN SILVER PRICING. HOWEVER, WE ALSO WERE ALSO INFORMED THAT WE HAD A SMALL 693 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS: 75 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 762. WE SURPRISINGLY AND SHOCKINGLY AGAIN HAD CONTINUAL LONG COMEX SILVER LIQUIDATION. ON A NET BASIS WE LOST 3055 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 3817 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 762 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES:3055 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 5 contracts FALLING TO 211 contracts. We had 120 notices filed upon so in essence we GAINED 115 contracts or 575,000 additional ounces of silver will stand for delivery in this non active delivery month of April AS SOMEBODY WAS IN URGENT NEED OF SILVER.

The next big active delivery month for silver will be May and here the OI LOST 6690 contracts DOWN to 98,037. June saw a LOSS of 4 contracts to stand at 95. The next big delivery month for silver is July and here the OI ROSE by 3057 contracts UP to 78,855.

We had 115 notice(s) filed for 575,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 17/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1288 contracts

(128,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

663 notices

66,300 OZ

2.062 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (663) x 100 oz or 66300 oz, to which we add the difference between the open interest for the front month of APRIL. (1288 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 195,100 oz, the number of ounces standing in this active month of APRIL (6.068 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (660 x 100 oz or ounces + {(1288)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 195,100 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 13 COMEX OI CONTRACTS OR 1300 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

605,295.100

JPMORGAN

oz

|

| Deposits to the Dealer Inventory |

NIL

oz

|

| Deposits to the Customer Inventory |

NIL oz

|

| No of oz served today (contracts) |

115

CONTRACT(S

575,000 OZ)

|

| No of oz to be served (notices) |

96 contracts

(480,000 oz)

|

| Total monthly oz silver served (contracts) | 379 contracts

(1,895,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) INTO EVERYBODY ELSE: ZERO OZ

total deposits today: ZERO oz

we had 1 withdrawals from the customer account;

i) out of JPMorgan; 605,295.100 oz

total withdrawals; 605,295.100 oz

we had 0 adjustment

total dealer silver: 61.363 million

total dealer + customer silver: 263.191 million oz

The total number of notices filed today for the APRIL. contract month is represented by 115 contract(s) FOR 575,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 379 x 5,000 oz = 1,895,000 oz to which we add the difference between the open interest for the front month of April. (211) and the number of notices served upon today (115 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 379(notices served so far)x 5000 oz + OI for front month of April(211) -number of notices served upon today (115)x 5000 oz equals 2,275,000 oz of silver standing for the April contract month

WE GAINED 115 SILVER CONTRACT OR 575,000 ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AS SOMEBODY WAS IN URGENT NEED OF PHYSICAL SILVER.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 96,979 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 92,910 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 92,910 CONTRACTS EQUATES TO 464 MILLION OZ OR 66.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.92% (APRIL 17/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.51% to NAV (APRIL 17/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.92%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.51%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.40%: NAV 13.90/TRADING 13.58//DISCOUNT 2.42.

END

And now the Gold inventory at the GLD/

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 17/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 363 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 313 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 17/2018: A NO CHANGES IN SILVER INVENTORY:

Inventory 320.196 million oz

end

6 Month MM GOFO 2.04/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.04%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .46%

XXXXXXXX

12 Month MM GOFO

+ 2.75%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

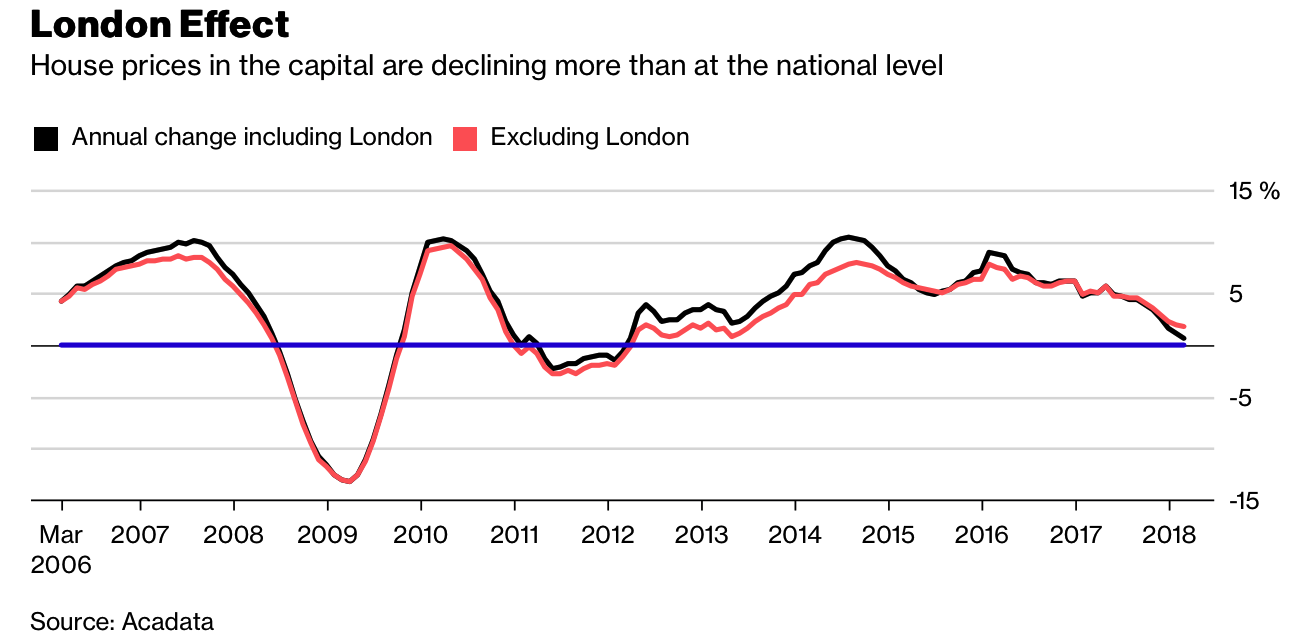

London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– London house prices fell by 3.2% in the first quarter – Halifax

– Brexit, financial and geo-political uncertainty lead to falls

– Excluding sale of seven £10m-plus houses in London, prices were down 3.4% in the year

– UK house prices climb by just 0.4% in April, the slowest increase since 2008 for same period

– Sales transactions fall by 19% and asking versus selling prices show turning into buyers’ market

– Homeowner or not, buy physical gold to hedge falls in physical property

Editor: Mark O’Byrne

London house prices declined at the sharpest pace in nine years during the first quarter of 2018, the latest data from Halifax shows.

London house prices fell by 3.2% in the first three months of the year according to the Halifax House Price Index. This was the fastest rate of decline since the UK and global financial crisis in 2009.

The average London house price fell to £430,759, its lowest since the end of 2015.

Average prices of London property continued to drop this month with house prices in the capital down by 0.6%, contributing to an overall fall of 2% for the year.

The UK property market has remained more resilient so far. The national average asking price for properties appearing for the first time was up by 0.4%. Six of the eleven major UK regions reached individual property price highs.

In London sellers are no longer achieving the asking price. The days of buyers outbidding one another seem long gone.

Anecdotally, a friend selling a 2-bed flat in West London’s Putney has had to lower the price from £595,000 to £545,000. A couple of years ago there would have been a queue around the block filled with potential buyers, armed with mortgage offers and desperation to pay ‘whatever it takes’.

My friend’s experience is worse than the data suggests. Research from Rightmove finds that sellers are achieving 95.6% of the asking price, with an average loss of £27,442 based on the average London asking price of £628,039. The difference reflects the ‘cloud 9’ approach of sellers who are yet to come to terms with the fact that buyers can no longer afford to pay any asking price.

By way of comparison the national average loss is £10,000, or 96.7 per cent of the final asking price. A difference of 1.1% between the two groups (London versus national) is not that dramatic and perhaps suggests than London is the siren call for the rest of the UK.

The fall in the London boroughs appears to be concentrated in the central areas of the city and outer boroughs are yet to feel the tightening. This is most likely due to the ripple effect.

The worries surrounding Brexit, stamp duty and interest rates will eventually be felt everywhere. This is regardless of how and when inflation really begins to bite.

Ongoing house price climbs are unsustainable

The strong performance by the rest of the UK may be seen as something to celebrate by those angry about the north-south divide. In reality history and data suggests this is not a sustainable situation for the long-term.

As we have already seen in London, home buyers will becoming increasingly stretched as prices climb. Wages are certainly not increasing but interest rates are.

The 0.4% increase in house prices was down significantly from the 1.5% climb seen in the previous period, perhaps a reflection of a changing and pushed market.

The property correction, and potentially crash, has started closest to the centre of the capital first. Soon a ripple effect will likely play out.

Many of the factors felt by central Londoners will also be experienced by the rest of the UK. Brexit, interest rate climbs or stamp duty rises make this likely. Brexit may be felt more keenly in the capital but this will set the tone for the rest of the country.

Banks are feeling financial pressures and the jobs market is certainly not suggesting to anyone that wages are on their way up. None of these are London-exclusive problems.

Throw in Brexit and you’ve just served up uncertainty on a platter for the entire UK.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Pressured first-time buyers support the market

In the short-term it may well remain a sellers’ market. There are still some property shortages across the country. Brits remain instilled with the psyche that it is better to own a home than to rent one. Earlier this year first-time buyers reached 10-year highs, ‘thanks’ to help-to-buy and shared ownership schemes. With interest rates set to climb further and stamp duty here to stay we may see a surge from first time buyers keen to jump on the housing ladder before it becomes even more unaffordable.

Rightmove and propertywire, explain the key differences between the property prices, lead by first-tme buyers:

The index also shows that typical first time buyer properties with two bedrooms or fewer are up by 2.2% average year on year, while the sector favoured by second steppers, mainly comprising three bedroom properties, rose by 2.7% rise.

In contrast, the more expensive top of the ladder category, typically detached with four bedrooms or more, has a more muted annual rate of increase of 0.9% and is still behind its peak set in October 2017 of £542,347.

‘In the more popular locations and for the property with the right specifications, buyer demand is helping to push prices higher. A lack of choice is nudging prices up to test the ceiling of what the market will pay,’ Shipside pointed out.

An abundance of houses or not, if they are unaffordable then there won’t be much demand for them.

Whilst the government is apparently working to increase the number of new homes, it may be too little too late. A housing shortage was not the driver of the housing boom. It was easy money and easy lending and those days are rapidly coming to an end and there are consequences to the age of frivolity by mortgage lenders and over-stretched buyers.

No property? You’re still vulnerable

London should not be seen as the outlier when it comes to property prices. It just feels change more acutely than the rest of the UK. Investors and analysts should see it as an only partially effective shock-absorber or airbag.

A crash appears likely. As ever, those who are diversified and own gold will weather the storm better than those who do not.

It’s easy to think that you are immune from a housing market crash if you are not a property owner. Sadly there are few who will be unaffected by a fall in property prices. So ingrained is the debt-fuelled housing market in our economy that all investors, savers and consumers are exposed.

Whilst the crash in house prices looks inevitable, it may not be imminent. The slow collapse in the London housing market has been ongoing since before the Brexit referendum, as buyers face the reality of reduced real wages and increased interest rates.

Investors and savers should hedge themselves by allocating a sensible proportion of their portfolio to the only real counter-party free asset – gold and silver bullion coins and bars.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Recommended reading

London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

Brexit Risks Increase – London Property Market and Pound Vulnerable

London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

News and Commentary

Gold ends higher as Trump comments put pressure on the dollar (MarketWatch.com)

Gold inches up as dollar slides, but risk premium fades (Reuters.com)

U.S. Homebuilder Sentiment Declined in April for a Fourth Month (Bloomberg.com)

U.S. retail sales spring back 0.6% in March after three straight declines (MarketWatch.com)

Source: Bloomberg

Barclays: Geopolitical Risk Is Back To Cold War Highs (ZeroHedge.com)

Greece Back in the Spotlight (Bloomberg.com)

U.S. Libor Replacement, Two Weeks After Debut, Has Some Issues (Bloomberg.com)

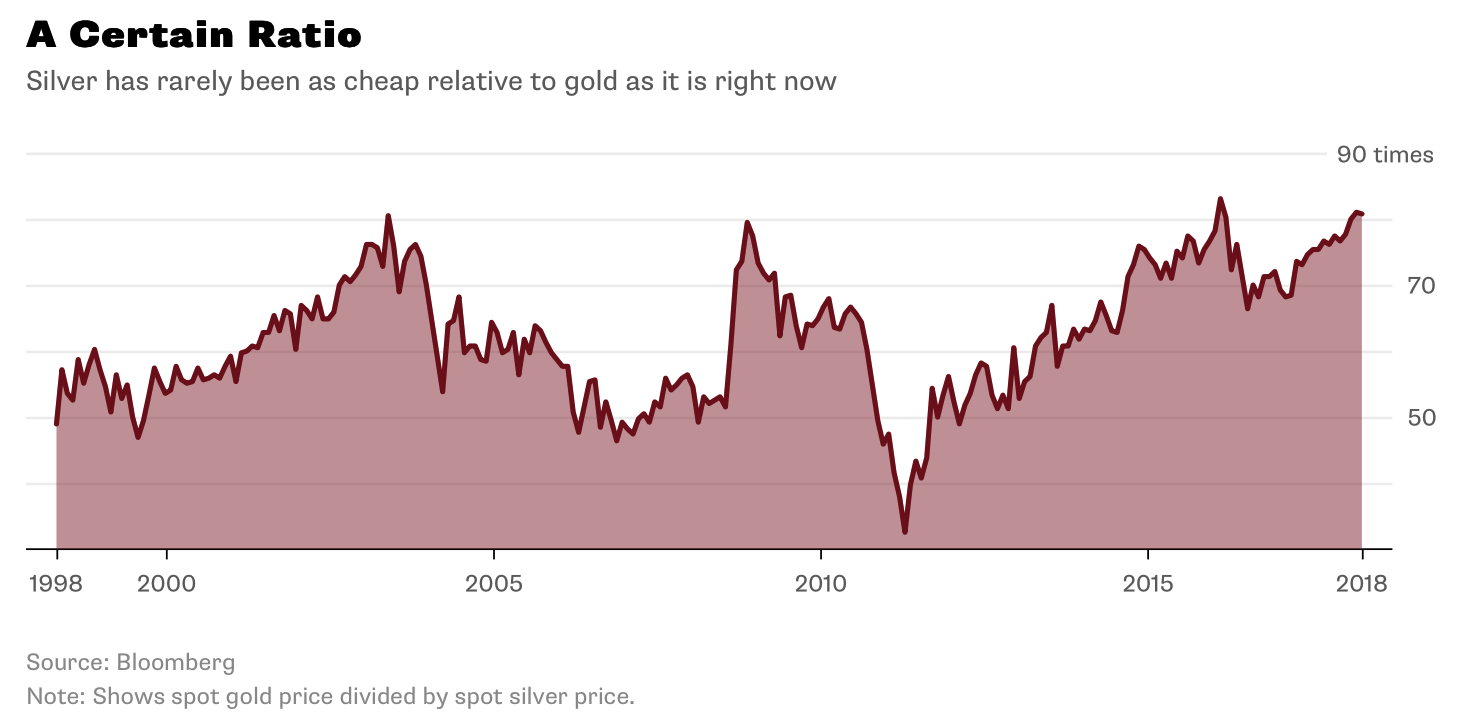

Silver’s Bullet (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

13 Apr: USD 1,340.75, GBP 938.93 & EUR 1,087.35 per ounce

12 Apr: USD 1,345.90, GBP 951.01 & EUR 1,090.99 per ounce

11 Apr: USD 1,345.20, GBP 947.96 & EUR 1,087.86 per ounce

10 Apr: USD 1,335.95, GBP 942.25 & EUR 1,083.46 per ounce

09 Apr: USD 1,328.50, GBP 941.91 & EUR 1,082.33 per ounce

Silver Prices (LBMA)

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

13 Apr: USD 16.51, GBP 11.57 & EUR 13.40 per ounce

12 Apr: USD 16.66, GBP 11.74 & EUR 13.50 per ounce

11 Apr: USD 16.57, GBP 11.67 & EUR 13.39 per ounce

10 Apr: USD 16.49, GBP 11.65 & EUR 13.38 per ounce

09 Apr: USD 16.34, GBP 11.59 & EUR 13.32 per ounce

Recent Market Updates

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

– Gold Is Money While Currencies Today Are “IOU Nothings”

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

An email from Nicholas to me:

and yes we will be watching that inventory closey:

Nicholas…

What will be interesting will be to continue to monitor LBMA gold holdings from 31st January 2018 onward to see if the Jan 2018 EFP contracts of 653 tonnes make any impact on loco London total gold holdings. The LBMA gold holdings are promulgated three months in arrears. If we reach (say) 31st July 2018 and the LBMA reported gold holdings as at 30th April 2018 show no response to the YTD April 2018 EFP transfers (presumably +2,500 tonnes), then that will be proof that these EFP transfers are merely corrupt spoofs to keep the paper gold ponzi scheme afloat.

Regards

Nicholas

Surprising China increases its USA treasuries despite trade tensions due to the tariff war

(Wigglesworth/London’s Financial times)

China increases U.S. Treasuries holdings despite trade tension

Submitted by cpowell on Tue, 2018-04-17 11:36. Section: Daily Dispatches

By Joe Rennison and Robin Wigglesworth

Financial Times, London

Monday, April 16, 2018

China expanded its U.S. Treasury holdings in February despite escalating trade tension between Beijing and Washington at the time, helping damp concerns the country could shed U.S. assets to hit back at the Trump administration.

China, the single biggest foreign holder of U.S. government debt, added $8.5 billion to its Treasury holdings in February, taking its total to $1.18 trillion, according to data released by the U.S. Treasury on Monday. …

… For the remainder of the report:

https://www.ft.com/content/93e1dcda-41ca-11e8-93cf-67ac3a6482fd

END

We knew that this would happen: Venezuela’s oil workers are now requesting payment in dollars for their wages

(courtesy Bloomberg)

Venezuela’s ‘suffocating’ oil workers request dollar payments

Submitted by cpowell on Tue, 2018-04-17 11:42. Section: Daily Dispatches

By Fabiola Zerpa

Bloomberg News

Monday, April 16, 2018

A group of workers at Venezuela’s state-owned oil company is requesting wages in dollars as well as meal plans and better health insurance to make up for what they called “suffocating” economic conditions.

“We expect receptivity to these requests that will grant dignity to workers and allow us to reach an environment of productivity and efficiency,” according to an April 2 letter to the managers of Petropiar, a PDVSA joint venture with Chevron Corp., seen by Bloomberg News. School tuition and recreational plans were also part of the requests.

In the letter employees said that an oil worker’s basic monthly wage stands at about 8.8 million bolivars. That’s around $14 at today’s black market average rate of about 650,000 bolivars per dollar. The Petropiar JV cut production earlier this year after falling short of its 2017 goal. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-04-16/venezuela-s-suffocati…

* * *

END

Mac Slavo reports why Eastern Central banks and one major bullion bank (JPMorgan) is stockpiling physical gold and silver

(courtesy Mac Slavo SHTFPlan.com)

“They Know What’s Going To Happen” – Governments, Big Banks Are Stockpiling Gold

Authored by Mac Slavo via SHTFplan.com,

The writing is on the wall and major financial institutions across the world are warning about the economic disaster to come. Unabated money printing, tariff trade wars, rising interest rates and retail slowdowns point to one result, and it’s going to be brutal.

Big banks and governments know what’s coming and they are preparing for this eventuality by stockpiling huge amounts of “real money” ahead of the crisis.

According to Keith Neumeyer, the CEO of the world’s top primary silver producer First Majestic Silver and chairman of First Mining Gold, the cartels he’s previously reported to the CFTC have continued to manipulate the prices of precious metals while loading up their own vaults with gold and silver. The answer to why they’re doing it is simple, as Neumeyer highlights in a recent interview with SGT Report:

The verdict is still out on whether we’re going into a dis-inflationary or inflationary environment… gold can do well in both environments… the fact of the matter is governments are printing extraordinary amounts of fiat currencies and that is not going to change…

The stage is set for higher gold prices due to the amount of money being printed… I am of the belief a major reset is coming where the governments of the world will need to get rid of their debt by fixing everything to the price of gold… and that’s why governments like China and Russia and other governments around the world are accumulating gold… it’s because they know what’s going to happen over the next several years…

If it is true [that JP Morgan has acquired the largest position of physical silver in the world] then it’s pretty amazing… Any bank wanting a long position like that is doing it for a reason…

Banks like JP Morgan… they haven’t had a losing trade in multiple years… if they’re long something that’s probably what you want to be buying.

Neumeyer explains that not only are there monetary factors at play, but also supply issues, as production, especially in silver, has dropped markedly over the last several years.

All of this bodes well for rising precious metals prices going forward, with reasonable estimates for future growth far exceeding the all-time highs we saw in recent years:

Metals are in an extremely tight trading range… This base the metals are building right now is three years in the making… and when the metals finally take off this year it’s going to be astounding to watch.

… We lived through it in 2010 and 2011… a good mining stock will far exceed the movement of the metal itself… a stock like First Mining would absolutely explode in an environment like that… it’s hard to predict the exact prices that stocks would do but it would be quite different than it is today…

I think $2000 or $3000 gold… these are reasonable numbers that we will experience in the not too distant future.

Financial analysts and large institutions have generally avoided gold and silver for nearly a decade. But the tide appears to be changing.

As prices remain suppressed, government are acquiring, big banks are acquiring and even Morgan Stanley recently noted that gold can be used as a “very good proxy of the true value of a dollar over long periods of time.”

We know economic collapse on a massive scale is approaching.

To get an idea of where one should be diversifying their assets in the event this worst-case scenario plays out, one need only ask the following question: What is money when the system collapses?

5,000 years of history for the single most reliable monetary asset class of last resort has already given us the answer.

Prepare accordingly.

END

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2834 /shanghai bourse CLOSED DOWN 43.85 POINTS OR 1.41% / HANG SANG CLOSED DOWN 252.84 POINTS OR 0.83%

2. Nikkei closed UP 12.06 POINTS OR 0.06%/ /USA: YEN RISES TO 107.07/

3. Europe stocks OPENED IN THE GREEN /USA dollar index RISES TO 89.45/Euro FALLS TO 1.2374

3b Japan 10 year bond yield: FALLS TO . +.045/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.25 and Brent: 71.39

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.525%/Italian 10 yr bond yield DOWN to 1.771% /SPAIN 10 YR BOND YIELD DOWN TO 1.231%

3j Greek 10 year bond yield RISES TO : 4.027?????????????????

3k Gold at $1342.40 silver at:16.65 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 43/100 in roubles/dollar) 61.56

3m oil into the 66 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.07 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9619 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1906 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.541%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8359% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0350% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Surge; Confused Dollar Stumbles Then Spikes Higher

US equity futures continued their Monday ramp, rising 0.5% alongside advancing stocks in Europe after investor focus shifted to earnings and the economic outlook, and away from fading geopolitical and trade war risks. The result is another sea of green in our futures screen this morning.

US Futures shrugged off weakness in Asia to point to a higher U.S. open as traders awaited results from companies including Goldman Sachs, while Europe’s Stoxx 600 Index rebounded from Monday’s drop.

The dollar initially flirted with the lowest level in two months in the wake of President Donald Trump’s latest verbal foray into exchange rates, before U.K. wage growth including bonuses missed estimates and a survey showed German investor confidence tumbling. The pound and euro edged lower (after another notable ZEW miss, see below) as the dollar rebounded sharply.

Stocks were encouraged by the limited fallout from a U.S.-led strike on Syria over the weekend – except for the occasional daily Israeli airstrike on Syria – while the U.S. government’s announcement it has not decided on additional sanctions on Russia suggested tensions between Moscow and DC are easing.

Meanwhile, investors are counting on Q1 earnings, expected to post the biggest Y/Y earnings increase since 2011 thanks to Trump’s tax reform – to fuel a recovery in equities and are looking for hints on the monetary-policy outlook from Federal Reserve officials due to speak this week, including incoming New York Fed President John Williams.

As Bloomberg adds, corporate earnings should offer some distraction for investors after a torrid period for stocks, but there remain no shortage of other catalysts waiting in the wings to roil markets. Trump’s latest intervention in currencies comes at a time of already elevated geopolitical tension, and ongoing fears of a lurch toward global protectionism.

Meanwhile, the macroeconomic backdrop leave quite a bit to desired as overnight China’s Q1 GDP print just met estimates (on a Y/Y basis and missed Q/Q) while industrial production in March came in below forecasts.

- China Q1 GDP YoY MEET at 6.8%, versus +6.8% exp. and +6.8% prior.

- China Retail Sales YoY BEAT at 10.1%, versus +9.7% exp. and +9.4% prior.

- China Industrial Production YoY MISS at 6.0%, versus +6.3% exp. and +6.2% prior.

- China Fixed Asset Investment YoY MISS at 7.5%, versus +7.7% exp. and +7.9% prior.

However, Q1 GDP QoQ disappointed, rising only 1.4% QoQ (versus expectations of a 1.5% QoQ jump

To be sure, trade war rumbling remain: earlier in the session tech shares slumped on the MSCI Asia Pacific Index after China’s ZTE Corp. was blocked from buying crucial American technology and its suppliers fell.

The dollar fell in U.S. trading after President Donald Trump took to Twitter to accuse China and Russia of “playing the Currency Devaluation game” as the U.S. raises interest rates. GBP/USD rises to 1.4354 in Asian trading, highest since Brexit, as purchases from leveraged accounts takes out sell orders from ex- Asia funds above 1.4340. Aussie dollar declines on macro selling after mixed China data while kiwi falls as it tries to consolidate under resistance around 0.7400.

The Bloomberg Dollar Spot Index came under intense pressure during Asia hours, touching its lowest level since Feb. 16; however it rapidly pared its drop after London stepped in, before erasing its entire move lower as German ZEW data missed estimates.

This also sent the euro to session lows at 1.2365 as of 6:30am ET, versus a three-week high of 1.2414 reached earlier. While the days German ZEW data moved the currency market seem long gone, investors took notice this time around as investor confidence tumbled to its lowest level since late 2012 due to mounting risks to global trade.

Until the European open, the yen advanced to session high against the dollar on concern currency issues will surface at a meeting between U.S. President Trump and Japanese Prime Minister Abe that starts Tuesday. However, as the dollar rebound picked up steam, the Yen slumped and was trading largely unchanged at last check. The pound erased early gains as U.K. labor data failed to provide fresh stimulus to bulls who opted to take profit on part of their exposure.

In other overnight geopol and trade news:

- China is prepared and ready to start trade countermeasures; according to China Foreign Ministry spokeswoman.

- US is said to be considering ways to retaliate against Chinese restrictions on US tech firms

- Mexico Economy Minister Guajardo says 10 NAFTA chapters are already concluded or close to conclusion adds they are exploring a possible meeting with USTR Lighthizer on Thursday but is not expecting a major announcement regarding NAFTA on Thursday.

- China diplomat warns that UK trade discussions with China would face significant uncertainties if UK fails to strike a Brexit deal with the EU.

- Syrian TV reports that air defenses are responding to missiles over Syria’s Homs and that there is an unidentified aircraft over Damascus.

- North Korea and South Korea are reported to discuss announcing a permanent end to military conflict, according to press reports.

In rates, the U.S. yield curve slightly steepens in Asia with 10-yr yields edging up 1bp to 2.83% while 2-yr yield is little changed at 2.37%. The 5s30s curve broke below 35bps in U.S. session to touch its flattest level since August 2007.

Oil steadied at $66.57 a barrel for U.S. crude and $71.66 a barrel for Brent having tumbled nearly 1.8 percent overnight as concerns over Middle East tensions eased. Gold (-0.4%) prices have dipped lower, closer to the bottom of the range but losses are modest at best. Chinese iron ore futures extended losses and hit a 10-month low on concerns of a supply glut. On the flip side, London aluminium futures extend their rally to the highest level in almost seven years, buoyed by growing concerns that the aftermath of the US sanctions on major Russian producer Rusal will result in tighter supply conditions.

Bulletin Headline Summary from RanSquawk

- EU equities firmer on an improved risk sentiment

- Cable falls on weaker than expected wage data

- Looking ahead, highlights include, US Building Permits, Housing Starts, Industrial Production, APIs, Fed’s Williams, Bostic,Quarles, Harker and Evans

Market Snapshot

- S&P 500 futures up 0.4% to 2,692.25

- STOXX Europe 600 up 0.2% to 378.66

- MSCI Asia Pacific down 0.3% to 173.11

- MSCI Asia Pacific ex Japan down 0.5% to 564.81

- Nikkei up 0.06% to 21,847.59

- Topix down 0.4% to 1,729.98

- Hang Seng Index down 0.8% to 30,062.75

- Shanghai Composite down 1.4% to 3,066.80

- Sensex up 0.2% to 34,380.72

- Australia S&P/ASX 200 unchanged at 5,841.55

- Kospi down 0.2% to 2,453.77

- German 10Y yield rose 0.4 bps to 0.529%

- Euro up 0.2% to $1.2400

- Italian 10Y yield rose 0.5 bps to 1.547%

- Spanish 10Y yield unchanged at 1.244%

- Brent futures up 0.2% to $71.56/bbl

- Gold spot down 0.2% to $1,343.10

- U.S. Dollar Index little changed at 89.41

Top Overnight News from BBG

- China’s economic expansion held up amid robust consumer spending, underpinning global growth and giving authorities more room to purge excessive borrowing, while the industrial sector showed signs of modest slowdown.

- U.S. Libor replacement runs into issues just two weeks after debut. The Federal Reserve Bank of New York said Monday it had mistakenly included certain repo transactions in the settings for April 2 to April 12 for the new benchmark, SOFR

- Trump suffered a setback as a federal judge rejected his initial request to keep prosecutors from immediately reviewing evidence seized by the FBI from his longtime personal lawyer, Michael Cohen

- U.K. wages are rising at their fastest pace in almost three years, raising the prospect of an end to the squeeze on living standards, according to Office for National Statistics data. The unemployment rate fell but headline earnings growth figure missed estimates and weighed on sterling

- German investor confidence tumbled to its lowest level since late 2012 on mounting risks to global trade and signs of a domestic economic slowdown

- Bank of England staff are close to finding out who will help the next governor settle in after Mark Carney steps down

- Trump announced his intention to nominate Richard Clarida, a respected monetary economist and Pacific Investment Management Co. global strategic adviser, as vice chairman of the Federal Reserve

- Russia is using compromised computer-network equipment to attack U.S. and British companies and government agencies, the two countries warned in an unprecedented joint alert

- China plans to remove foreign ownership limits for auto ventures within the next four years, giving a boost to global companies seeking better access to the world’s biggest vehicle market

- U.K. PM Theresa May will face a second debate in as many days on Britain’s role in bombing Syria on Tuesday after she stayed late the night before listening to lawmakers’ views in the House of Commons

- Aluminum surged to a six-year high as the impact of U.S. sanctions against United Co. Rusal continued to reverberate through the global market. Some forecast the price may hit $3,000 a metric ton

Asia equity markets traded with a somewhat indecisive tone after the positive momentum from Wall St waned as the region digested mixed tier-1 data releases from China including GDP. ASX 200 (+0.2%) saw mild gains amid a slew of corporate updates, while Nikkei 225 (Unch) was flat with price action contained by a firm JPY. Hang Seng (-0.83%) and Shanghai Comp. (-1.4%) were choppy in reaction to the mixed data figures in which GDP Y/Y printed inline with estimates at 6.8% which surpasses the official target for 2018, while Q/Q printed slightly below estimates at 1.4% vs. Exp. 1.5%. Furthermore, Industrial Production also disappointed but was counterbalanced by solid growth in Retail Sales. Finally, 10yr JGBs were relatively flat amid a similar picture seen in riskier assets in Japan, while a 5yr JGB auction also failed to spur price action despite slightly firmer demand and higher prices, as this was in tandem with a lower amount sold.

Top Asia News

- China Slaps Anti-Dumping Duties on $957 Million U.S. Grain Trade

- Kaisa Group Is Said to Discuss Dollar-Bond Sale With Banks

- Chinese Stocks Sink Below Key Level as Investor Concerns Mount

- Asia IPO Bankers Continue Game of Musical Chairs With BofA Moves

- Commonwealth Bank to Spin Off Global Asset Management Arm in IPO

European equities have shown strength (Eurostoxx +0.3%) on the back of improved risk sentiment with Syrian tensions continuing to abate. This is most noted in the materials and IT sectors, with both leading their peers. Negativity is noted in consumer discretionary, led by Reckitt Benckiser (-2.6%) on a broker downgrade by Credit Suisse. Elsewhere, Chinese permission for foreign auto companies to set up more than two ventures has led to auto names strengthening with Daimler rising from EUR 65.24 to EUR 65.44 and BMW up from EUR 90.47 to EUR 91.10. GKN (2.2%) have been supported with Melrose expecting an offer to become unconditional by April 19th, AB food (+2.6%) are higher amid an earnings beat and Bayer (2.0%) have been lifted by the news that the co. has agreed to sell 3.6% of new shares to Singaporean state investment company Temasek for EUR 3bln; this comes as the company plans for a USD 62.5bln takeover of Monsanto.

Top European News

- Airlines Have to Pay EU Passengers for Some Strikes

- U.K. Wages Rise Most Since 2015 as End to Consumer Squeeze Nears

- Russia Looks to Dodge Crossfire of Sanctions as Eurobond Beckons

- Sabadell Is Said to Focus on U.K. as Probable Target for M&A

- Telefonica Is Said to Hire Banks for Argentine Share Sale

In currencies, the USD remains under pressure, and the index slipped through chart support in the 89.355-325 area that houses a recent April low and rising channel, to expose 89.250 ahead of 89.000 and another major downside technical level around 88.942 (end of March base), before regaining a foothold on disappointing EU data. EUR/GBP: Still vying for top spot within the G10, as the cross remains in a broad 0.8650-00 range amidst decent buying interest between 0.8625-30, but both making further headway against the Greenback. Eur/Usd finally absorbed offers ahead of 1.2400 to trade above on stops (briefly), while Eur/Chf climbed to a fresh post-SNB floor removal peak just over 1.1900 as Usd/Chf hovers around 0.9600. Cable has also notched up a landmark after setting a new post-Brexit vote best around 1.4375 and now eyeing 1.4400 barrier resistance assuming no major set-back in wake of broadly softer than expected UK labour and earnings data – 1.4300 is holding in thus far. JPY: Retreating from recent 107.00+ highs and pivoting around the big figure with daily chart support around 106.89 underpinning the pair vs hefty 1.5 bn option expiry interest at 107.20 that appears to be capping the upside

In commodities, taking a look at the commodities complex, oil prices consolidated from the overnight gains with WTI (-0.1%) and Brent Crude (- 0.1%) modestly lower on the day as concerns of supply disruptions in the Middle East temporarily fade, whilst rising US shale outputs is on traders’ minds ahead of the API weekly inventories later today. Moving onto the metals bloc, gold (-0.4%) prices have dipped lower, closer to the bottom of the range but losses are modest at best. Overnight, Chinese GDP printed in line at 6.8%, above the government’s target of around 6.5%. However, industrial output came short of the expected 6.3%, whilst daily steel output in March climbed to the highest level since September. In turn, Chinese iron ore futures extended losses and hit a 10-month low on concerns of a supply glut. On the flip side, London aluminium futures extend their rally to the highest level in almost seven years, buoyed by growing concerns that the aftermath of the US sanctions on major Russian producer Rusal will result in tighter supply conditions.

Looking at the day ahead, in Europe the most significant releases are UK employment stats for February and March, and Germany’s April ZEW survey which as noted above tumbled to the lowest since 2012. In the US we’ll get March housing starts and building permits as well as March industrial and manufacturing production. Today is a busy day for Fedspeak with Williams, Quarles, Harker, Evans and Bostic all slated to speak. Meanwhile, President Trump is due to welcome Japan PM Abe, while the IMF and World Bank Annual Spring Meetings will commence, concluding April 22nd. Goldman Sachs is the earnings highlight along with IBM and Johnson & Johnson.

US Event Calendar

- 8:30am: Housing Starts, est. 1.27m, prior 1.24m; MoM, est. 2.51%, prior -7.0%

- 8:30am: Building Permits, est. 1.32m, prior 1.3m; MoM, est. 0.0%, prior -5.7%

- 9:15am: Industrial Production MoM, est. 0.3%, prior 1.1%; Manufacturing (SIC) Production, est. 0.1%, prior 1.2%

DB’s Jim Reid concludes the overnight wrap

Markets were generally passported back to better times yesterday as they breathed a collective sigh of relief after there was no ramp up in rhetoric or escalation to the Syrian missile strikes over the weekend. Indeed, even another fairly controversial Trump tweet (more on that below) did little to dampen the generally upbeat start for risk as the S&P 500 (+0.81%) moved back into positive territory for 2018 for the first time since mid-March. The ViX (16.56) also hit its lowest since mid-March and is down 33.4% from its recent high. The Dow (+0.87%) and Nasdaq (+0.70%) also finished higher although prior to this European markets did actually fade at the close to finish slightly lower. The Stoxx 600 in particular ended -0.39%. Treasuries on the other hand were a bit weaker but the reality is that they continue to just ebb and flow in this fairly tight range at present. 10y Treasuries ended last night unchanged at 2.828% (a high of 2.86% and threatening to break out though) which means that they’ve stayed in a slightly greater than 20bp range since the start of February even though they climbed 30bps during January. Bunds continue to bump along the bottom of their recent yield range and it is worth noting that the 2y Treasury-Bund spread closed at 296bps, marking a fresh high since the reunification of Germany. Elsewhere, WTI oil fell for the first time in six days to $66.22/bbl (-1.74%) while LME aluminium jumped 4.99% yesterday to the highest since September 2011.

Overnight the main focus has been on China where we’ve received the Q1 GDP print which was in line at 6.8% yoy and steady since last September. In addition to that we’ve also had the March activity data, with retail sales above market (10.1% yoy vs. 9.7% expected) while the March IP eased 0.2ppt mom to 6.0% yoy (vs. 6.3% expected). After the bell in the US, Netflix’s share price jumped c5% after reporting better than expected growth in subscribers. This morning in Asia, markets are mixed and little changed with the Hang Seng and Nikkei broadly flat, the ASX 200 is up +0.25% while the Shanghai Comp. is down -0.35%. Back to yesterday, the tweet that we referred to at the top from President Trump which attracted the usual attention was: “Russia and China are playing the currency devaluation game as the US keeps raising interest rates. Not acceptable!”. The USD was weaker in response but in reality was already declining before the President tweeted. Still, this was the first reference to FX policy by the President in some time however it perhaps says something that the Predata Trump Presidential Volatility Index – which measures fluctuations in online discussions about the multiple political controversies surrounding the administration of Trump (similar to PVIX) – is still below the highest levels in January, February and March this year, and indeed most of last year, suggesting a bit of fatigue perhaps in Trump’s social media comments.

In other news, US banks actually lagged a bit yesterday despite the move higher for bond yields and also slightly better than expected results for BofA. On the latter, the Bank reported EPS of 62c for Q1 which was ahead of the 59c consensus following cost cuts, while revenues also marginally beat expectations. That continues what has been a generally solid set of results for US banks so far with all 4 banks having beaten earnings expectations and 3 of 4 beating on revenues (1 in line). As a reminder, today we’ll get Goldman Sachs’ results.

Now moving onto the four Fed speakers on rates and inflation. The Fed’s Dudley noted that “as long as inflation is relatively low, the Fed is going to be gradual (on rate hikes)”, but “if inflation were to go above 2% by an appreciable margin, then I think the gradual path might have to be altered”. Following on, Mr Kaplan expects the Fed to hike rates two more times this year and more next year. He added that “I don’t have a problem with being restrictive” on rates, provided rates do not rise above the 2.5%-2.75% range that he estimates as their “neutral” level. Further, rate hikes should not move up so fast or far which leads to an inverted yield curve. Conversely, Mr Kashkari noted “there are now indications that inflation is gradually starting to move toward our 2% target”, but “I don’t see signs of any sudden acceleration in inflation or overheating”. Hence, “its’ hard to say when the Fed should raise rates again”, in part as he “prefers not to make such predictions because (he) wants the data to guide us rather than some promise that we’ve made”. Finally, Mr Bostic noted the Fed has not seen much movement in wage growth while “we’re having a conversation why we have struggled to reach” the Fed’s 2% inflation target.

Back in Europe, the ECB’s Praet noted “the growth outlook confirms our confidence that inflation will converge toward our aim of close to 2% over the medium term” but reiterated that inflation developments “remain subdued” and ample degree of stimulus remains necessary. He also played down the recent softening in Euro area economic data, as it followed “several quarters of very strong growth”. Elsewhere, the ECB’s Visco noted Italian banks have improved but there are ‘still some weakness” and banks overall must take advantage of the current favourable conditions to improve their balance sheets and profitability. Turning to the some of the other headlines in the US, the White House has confirmed that President Trump intends to nominate Richard Clarida as the next Fed Vice-Chair and Kanas State Bank Commissioner Michelle Bowman to fill one of the vacant Fed Governor positions. Mr Clarida is a Columbia University professor and an MD at Pimco. On the nominations, the Fed’s Kaplan said he has known “Rich for many years” and “thinks extremely highly of him”. Overall, he “don’t know (if the new nominees) will change the dynamic around the table”.

Elsewhere, the White House has noted the new sanctions on Russian firms as flagged by the US ambassador to the UN are not imminent, in part as the Washington Post noted President Trump is not comfortable with the additional measures yet. Moving on, the US Treasury noted China’s holding of US debt increased $8.5bn mom to $1.18trn in February, marking the largest monthly increase in six months. Finally, the US Commerce Department has imposed a 7 year ban on the Chinese telco. company ZTE Corp. from buying sensitive technology from US suppliers, as it alleged that the company engaged in illegal conduct and making false statements to US authorities. As we type, the ZTE shares are in trading halt in HK.

Away from the micro, there was a bit of US data to also digest yesterday with the March retail sales report. There were no great surprises in the data however with both ex auto sales (+0.2% mom) and control group sales (+0.4% mom) printing in line with expectations. Headline sales (+0.6% mom vs. +0.4% expected) did surprise to the upside. It’s also worth noting the April empire manufacturing print which came in at a much softer than expected 15.8 (vs. 18.4 expected) and down nearly 7pts from March. Of most significance was the fall in the outlook component with the index for future business conditions falling 26pts to 18.3 and to the lowest in a bit over 2 years. It was also the biggest monthly decline since September 2001. So signs that the heightened protectionist measures in recent weeks are weighing on the outlook for businesses in the sector. Elsewhere, the February business inventories was in line at 0.2% mom. Factoring in the above, the latest Atlanta Fed’s estimate of real PCE and GDP growth are 0.9% saar and 1.9% saar respectively.

Looking at the day ahead, in Europe the most significant releases are UK employment stats for February and March, and Germany’s April ZEW survey. In the afternoon in the US we’ll get March housing starts and building permits as well as March industrial and manufacturing production. Today is a busy day for Fedspeak with Williams, Quarles, Harker, Evans and Bostic all slated to speak. Meanwhile, President Trump is due to welcome Japan PM Abe, while the IMF and World Bank Annual Spring Meetings will commence, concluding April 22nd. Goldman Sachs is the earnings highlight along with IBM and Johnson & Johnson.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed DOWN 43.85 POINTS OR 1.41% /Hang Sang CLOSED DOWN 252.84 POINTS OR 0.83% / The Nikkei closed UP 12.06 POINTS OR 0.06%/Australia’s all ordinaires CLOSED UP .02% /Chinese yuan (ONSHORE) closed UP at 6.2834/Oil DOWN to 66.69 dollars per barrel for WTI and 71.81 for Brent. Stocks in Europe OPENED IN THE RED . ONSHORE YUAN CLOSED UP AT 6.2834 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2773 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

USA is now planning a 3rd front into its attack on China. China does not allow USA firms to compete in China unless they find a joint venture partner of Chinese origin. Basically Chinese high technology is off limits to the USA and Trump is planning to remedy this:

(courtesy zerohedge)

US Planning To Open “Third Front” In China Trade Spat

In news that broke (conveniently, we should add) shortly after the market closed on Monday, the Wall Street Journal is reporting that the White House is gearing up for what would be the third front in its nascent trade spat with China.

As the paper points out, Trade Representative Robert Lighthizer is preparing a fresh trade complaint – again under Section 301 of the Trade Act of 1974 – the same section of the trade act under which the US filed its complaint about China’s intellectual property abuses, aka the first salvo in the US’s trade war.

This time, Lighthizer is aiming at China’s unfair restrictions on US companies trying to establish a foothold in China in high-tech industries like cloud computing. As a general rule, China requires foreign firms to partner with a domestic firm in a “revenue-sharing agreement” before they can gain entry to the Chinese market. By comparison, the US allows Chinese firms like Alibaba to function almost totally unfettered.

To be sure, Lighthizer has yet to decide whether to go ahead with the complaint, leaving the tariffs on steel and aluminum and the investigation into IP abuses as the only concrete actions that the White House has taken to hold China accountable for what Trump has described as decades of abuses on trade (threatening to impose tariffs on $150 billion in goods doesn’t count).

The trade representative has yet to decide whether to go ahead with the complaint, the individuals said, which would be in addition to recent moves to ratchet up pressure on China, including the imposition of tariffs on a total of $150 billion in Chinese imports. But USTR, which has taken the lead in the China trade fight, views China’s restrictions on cloud computing as providing a clear-cut example that might garner public support.