GOLD: $1350.65 UP $ 3.65 (COMEX TO COMEX CLOSINGS)

Silver: $17.22 UP 44 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1349.50

silver: $17.19

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:2 NOTICE(S) FOR 200 OZ.

TOTAL NOTICES SO FAR 665 FOR 66500 OZ (2.068 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 379 for 1,895,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8039/OFFER $8139: up $32(morning)

Bitcoin: BID/ $8129/offer 8229: UP $287 (CLOSING/5 PM)

end

I will be reporting on the Shanghai gold fix as I can now attest to it’s accuracy:

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First fix gold: 10 pm est: 1352.20

NY price at the same time: 1344.40

PREMIUM TO NY SPOT: $7.80

Second gold fix early this morning:1352.20

USA gold at the exact same time: 1344.80

PREMIUM TO NY SPOT: $7.40

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST SURPRISINGLY ROSE BY A SMALL 297 CONTRACTS FROM 214,000 RISING TO 214,297 WITH YESTERDAY’S 10 CENT GAIN IN SILVER PRICING. THIS BROKE THE STRING OF 6 CONSECUTIVE DAYS OF DROPS IN OPEN INTEREST. WE FINALLY HAD ZERO COMEX LIQUIDATION. WE WERE AGAIN NOTIFIED THAT WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 4963 EFP’S FOR MAY , 114 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 5077 CONTRACTS. WITH THE TRANSFER OF 5077 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 5077 EFP CONTRACTS TRANSLATES INTO 25.03 MILLION OZ ACCOMPANYING THE RISE IN SILVER PRICE AT THE COMEX AND THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

38,821 CONTRACTS (FOR 13 TRADING DAYS TOTAL 38,821 CONTRACTS) OR 194.105 MILLION OZ: AVERAGE PER DAY: 2,986 CONTRACTS OR 14.931 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 194.105 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 27.72% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 912.235 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A SMALL SIZED GAIN IN COMEX OI SILVER COMEX OF 297 WITH THE 10 CENT GAIN IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE OF 5077 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA 4963 EFP’S FOR THE MONTH OF MAY AND 114 EFP CONTRACTS FOR JULY, WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 5374 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 5077 open interest contracts headed for London (EFP’s) TOGETHER WITH AN INCREASE OF 297 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 10 CENTS AND A CLOSING PRICE OF $16.78 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.071 BILLION TO BE EXACT or 153% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY AN SMALL SIZED 1101 CONTRACTS DOWN TO 510,229 WITH THE DROP IN PRICE/YESTERDAY’S TRADING ( FALL OF $1.00). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7535 CONTRACTS : JUNE SAW THE ISSUANCE OF 7535 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 510,229. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES 1101 OI CONTRACTS DECREASED AT THE COMEX AND AN STRONG SIZED 7535 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 6434 CONTRACTS OR 643,400 OZ = 20.01 TONNES.

YESTERDAY, WE HAD 9736 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 138,280 CONTRACTS OR 13,828,000 OZ OR 430.108 TONNES (13 TRADING DAYS AND THUS AVERAGING: 10,636 EFP CONTRACTS PER TRADING DAY OR 1,063,600 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 13 TRADING DAYS IN TONNES: 430.108 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 430.108/2550 x 100% TONNES = 16.86% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,474.60 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 1101 DESPITE THE DROP IN PRICE // GOLD TRADING YESTERDAY ($1.00 FALL). HOWEVER, WE HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7535 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7535 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED NET GAIN OF 6434 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7535 CONTRACTS MOVE TO LONDON AND 1101 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 20.01 TONNES).

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $3.65 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER UP 44 CENTS TODAY: NO CHANGES/

/INVENTORY RESTS AT 320.196 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY 297 CONTRACTS from 214,000 UP TO 214,297 (AND AWAY FROM THE NEW COMEX RECORD SET YESTERDAY/APRIL 9/2017). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.WE FINALLY HAD AN OPEN INTEREST GAIN AFTER 6 CONSECUTIVE DAYS OF LOSSES. THE GAIN OCCURRED WITH THE SHARP RISE IN PRICE YESTERDAY. HOWEVER OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 4963 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 114 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 5077 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 297 CONTRACTS TO THE 5077 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 5374 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 26.87 MILLION OZ!!! AND THIS OCCURRED WITH A RISE IN PRICE OF 10 CENTS. THE BANKERS ARE CAPITULATING AS THEY DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE RISE IN SILVER PRICING / YESTERDAY (10 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 5077 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed UP 24.60 POINTS OR 0.80% /Hang Sang CLOSED UP 221.50 POINTS OR 0.74% / The Nikkei closed UP 310.61 POINTS OR 1.42%/Australia’s all ordinaires CLOSED UP .37% /Chinese yuan (ONSHORE) closed UP at 6.2829/Oil UP to 67.43 dollars per barrel for WTI and 72.35 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2829 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2768 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING A LITTLE STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

Japan

Unusual: the tariffs initiated by Trump has caused the price of Aluminium to skyrocket. Now Japan has asked Rusal to stop aluminum shipments to them as the prices are just too high. Traders also risk being a USA target if they do purchase Rusal aluminium. This may force Rusal into bankruptcy. The big winner in the aluminium space; China has they have gained huge market share at Rusal’s expense. If Trump hits nickel next, then Norlisk is at risk

( zerohedge)

3 c CHINA

i)Hong Kong

With Libor much higher than Hibor, it was a lucrative trade for investors: shorting the Hong Kong dollar and buying USA dollars/treasuries/bonds. Hong Kong securities have a tiny yield but the uSA stuff has a much higher yield and thus the reason for loss in value of the Hong Kong dollar.

( zerohedge)

ii)China/USA

Another probe: this time an anti dumping probe into steel wheels imported form China

( zerohedge)

iii)The trade war escalates as China prepares an “emergency response plan”

( zerohedge)

4. EUROPEAN AFFAIRS

Greece/Turkey

This is just what the world needed; Turkey flying into Greece airspace harasses the helicopter of Greek Prime Minister Tsipras

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

ii)Mac Slavo outlines why there was no chemical bombing in Eastern Damascus

( Mac Slavo/SHTFPlan.com)

( zerohedge)

iv)Badly wounded Russia tries to fight back and now threatens the halt the key rocket engine exports to the USA. Believe it or not the uSA uses Russian rockets to propel low orbiting satellites.

( zerohedge)

6 .GLOBAL ISSUES

( zerohedge)

7. OIL ISSUES

Oil and gasoline surge after a huge across the board inventory draw down

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)A super commentary by Ronan Manly describing the criminal activity of the bankers as to how they have manipulated the fixes, how they blasted gold/silver on many occasions with impunity right under the watchful eyes of regulators.

( Ronan Manly)

ii)GATA is an exempt non profit organization and as such must show it’s return. So here it is:

( GATA

( Craig Hemke/Sprott Money/GATA)

iv)An excellent commentary from Lawrie Williams. I would not take the GFMS’s calculations on silver demand as they are always on the low side. However they do note that silver supply is down 4%, identical to the calculations of Steve St Angelo.

Please note that all of silver’s demand components (other than hoarding) are well up:

Photovoltaics, jewellry, the auto sector and also silver’s use in electrical components. The killer blow to the banking cartel is the lower silver supply from the mines

( Lawrie Williams/Sharp Pixley)

10. USA stories which will influence the price of gold/silver

iii)The Fed’s Beige Book for April has been released and it seems that all 12 Fed districts are concerned with the tariffs. Also wage growth is not forthcoming as they would have liked( zerohedge)

iv)SWAMP STORIES

b)Each side has selected choices that we would be good candidates for “Special Master” although the Government would not like to have a Master but a Government filter agent.

c)The fun begins; 11 GOP members of Congress have written a letter to Attorney General Jeff Sessions asking them to investigate Comey , Clinton, Lynch, Strzok and Page under the criminal code.

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:171,580 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 288,272 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY 297 CONTRACTS FROM 214,000 UP TO 214,297 (AND AWAY FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018) WITH THE 10 CENT RISE IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A HUMONGOUS 4963 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS: 114 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 5077. ON A NET BASIS WE GAINED 5374 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 297 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 5077 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 65374 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 115 contracts FALLING TO 96 contracts. We had 115 notices filed upon so in essence we GAINED 0 contracts or ZERO additional ounces of silver will stand for delivery in this non active delivery month of April

The next big active delivery month for silver will be May and here the OI LOST 2044 contracts DOWN to 95,993. June saw a GAIN of 1 contract to stand at 96. The next big delivery month for silver is July and here the OI ROSE by 2160 contracts UP to 81,105.

We had 0 notice(s) filed for NIL OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 18/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

803.75 OZ

Manfra

(25 kilobars)

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

938 contracts

(93,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

665 notices

66,500 OZ

2.068 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (665) x 100 oz or 66500 oz, to which we add the difference between the open interest for the front month of APRIL. (940 contracts) minus the number of notices served upon today (2 x 100 oz per contract) equals 160,300 oz, the number of ounces standing in this active month of APRIL (4.9860 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (665 x 100 oz or ounces + {(940)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 160,300 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 348 COMEX OI CONTRACTS OR 34800 OZ OF GOLD WILL NOT STAND BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,267,370.360 oz

JPMORGAN

Scotia

|

| Deposits to the Dealer Inventory |

NIL

oz

|

| Deposits to the Customer Inventory |

2039.89 oz

Brinks

|

| No of oz served today (contracts) |

0

CONTRACT(S

(NIL OZ)

|

| No of oz to be served (notices) |

96 contracts

(480,000 oz)

|

| Total monthly oz silver served (contracts) | 379 contracts

(1,895,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) INTO EVERYBODY ELSE: ZERO OZ

total deposits today: ZERO oz

we had 2 withdrawals from the customer account;

i) out of JPMorgan; 605,295.100 oz

ii) Out of Scotia: 60,641.660

total withdrawals; 1,267,370.360 oz

accumulation in last two days for JPMorgan silver withdrawal:1,812,023.0 oz

why is JPMorgan withdrawing so much silver?

we had 0 adjustment

total dealer silver: 61.363 million

total dealer + customer silver: 261.925 million oz

The total number of notices filed today for the APRIL. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 379 x 5,000 oz = 1,895,000 oz to which we add the difference between the open interest for the front month of April. (96) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 379(notices served so far)x 5000 oz + OI for front month of April(96) -number of notices served upon today (115)x 5000 oz equals 2,375,000 oz of silver standing for the April contract month

WE GAINED 0 SILVER CONTRACT OR NIL ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 97,131 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 108,999 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 108,999 CONTRACTS EQUATES TO 544 MILLION OZ OR 77.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.79% (APRIL 18/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (APRIL 18/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.79%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.04%: NAV 14.04/TRADING 13.75//DISCOUNT 2.04.

END

And now the Gold inventory at the GLD/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 18/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 364 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 314 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 17/2018: A NO CHANGES IN SILVER INVENTORY:

Inventory 320.196 million oz

end

6 Month MM GOFO 2.03/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.03%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .47%

XXXXXXXX

12 Month MM GOFO

+ 2.75%

LIBOR FOR 12 MONTH DURATION: 2.50

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.25

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– Silver bullion remains good value on positive supply and demand factors

– Industrial demand set to continue to climb from 2017, into 2018 and beyond

– Speculators are bearish on silver as net short positions in silver futures reach record

– Investment demand sees silver ETF holdings at eight-month high of 665.4 million ozs

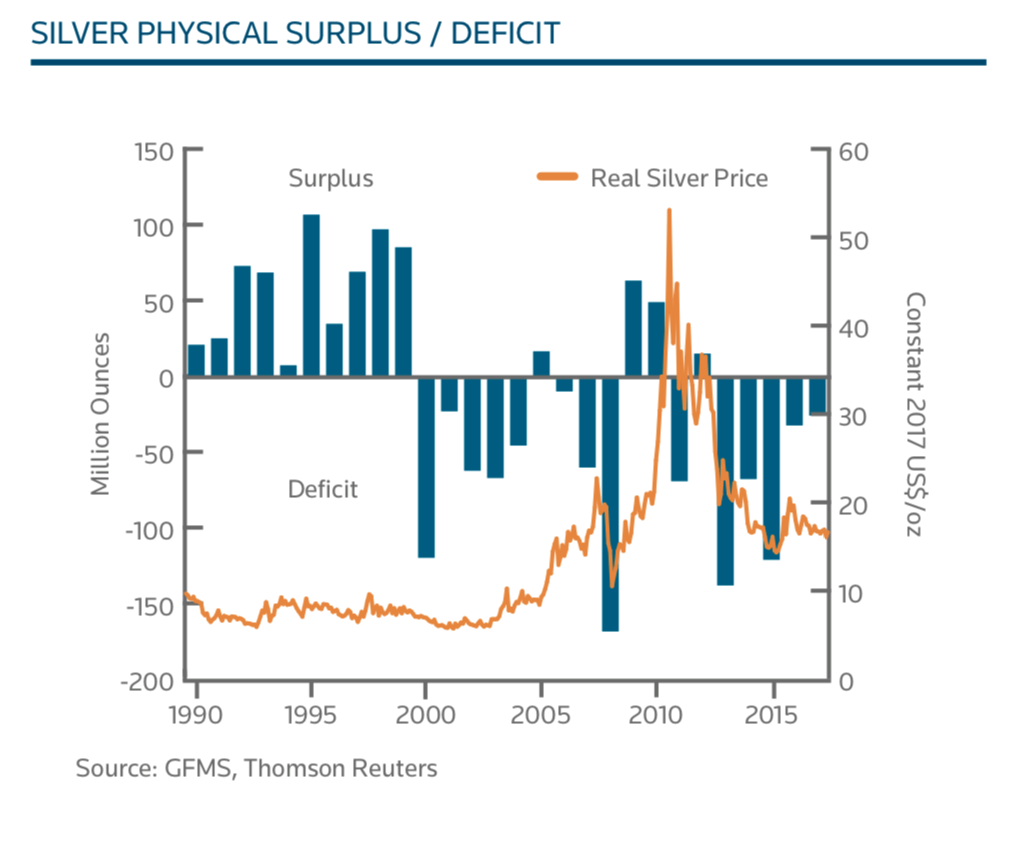

– 2017 saw fifth consecutive annual physical deficit in scrap silver, of 26 moz

– Global silver mine production fell 4% last year, 2nd consecutive year of decline

– Fundamentals and speculative positions suggest silver may soon see strong gains

Editor: Mark O’Byrne

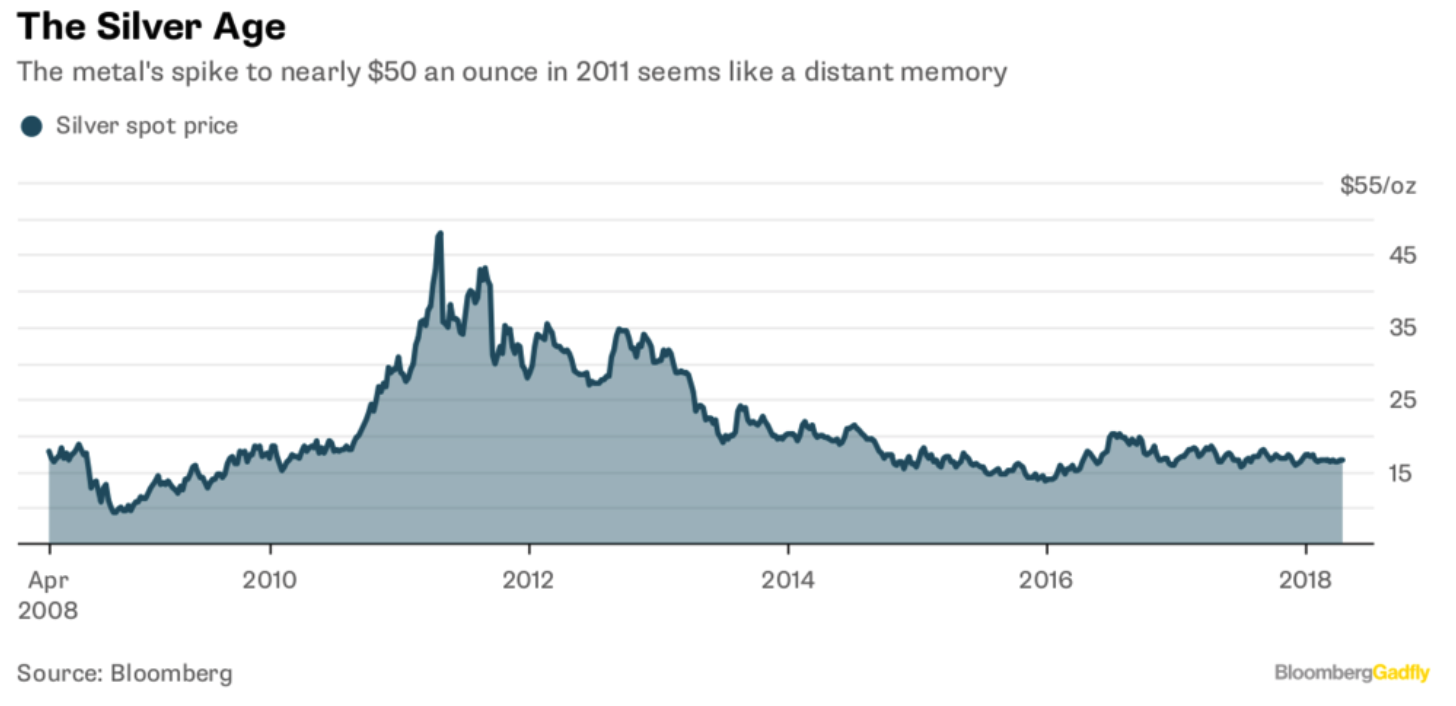

It’s been tough going for many silver bullion investors who look back fondly on silver’s surge to nearly $50/oz in 2011. But things are set for a turnaround judging by recent COT reports, investment demand as seen in ETF holdings and non-investment metrics such as strong industrial demand and falling mine supply.

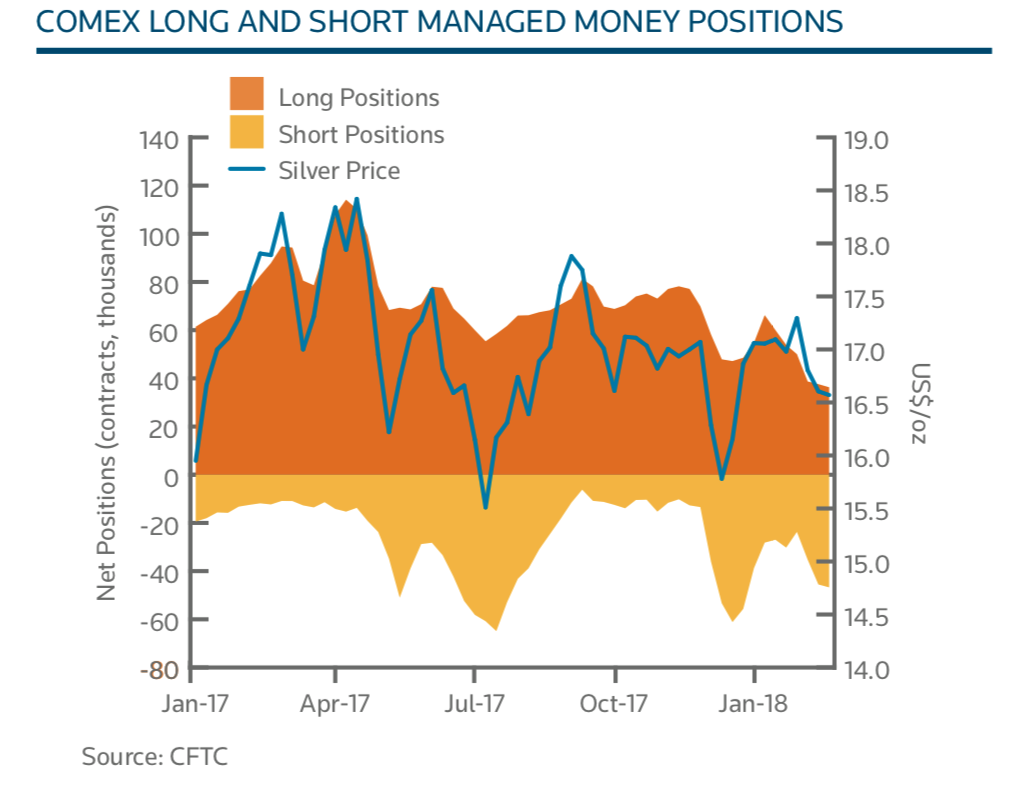

Earlier this month you could be forgiven for thinking that silver’s future certainly contained no shiny lining of any kind. There were a record 39,604 contracts (equivalent to five-and-a-half metric tons) of net short positions in silver futures held by money managers. Some would see this as bearish but the record shows that such positioning is generally bullish from a contrarian perspective and frequently presages sharp reversals higher in the price of silver.

On the arguably more important long term side of the market is investment demand. Total silver ETF holdings reached an eight-month high of 665.4 million troy ounces last week. Investors increasingly like the medium and long term fundamentals of the silver market. Not so bearish after all.

On the all important physical, non-investment part of the silver market, life is looking even shinier. Industrial demand currently makes up about 60% of the silver market and is set to climb. A recent report from Thomson Reuters’ GFMS and the Silver Institute has found that demand for silver in the non-investment space climbed in 2017 and is expected to continue to do so this year and beyond.

These figures – speculative bets on a lower silver price on one hand but strong investment and industrial demand on another – look counter intuitive to the uninformed observer.

They likely show that silver remains undervalued versus gold and indeed versus very overvalued stock, bond and indeed most property markets.

The Bearish Managed Money Positions Are A Good Sign

We look at money managed positions in silver futures as they serve as a good proxy for for investor and speculative activity on the COMEX. Currently (and pretty much since August 2017) speculators are more short than they are long, with a lot of cash betting that silver is set for further fall in price.

As of last week the managed money positions made it 9 consecutive weeks of bearish sentiment. According to several market analysts the metal is now “oversold” and “vulnerable” to a hop up the price scale. Interestingly, despite the air of negativity, silver has remained resilient – falling by just 2% in the last two months or so.

We saw a similar situation last year, despite a wave of bearish speculators silver bullion managed to finish the year up 6%.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Some analysts believe the current negativity surrounding silver could signal a turnaround. Bloomberg’s David Fickling wrote an astute article which is well worth a read on Monday:

‘As the stunning reversal of aluminum’s three-month decline last week demonstrated, commodity markets can go wild when bearish investors are caught short.’

SocGen’s own analysts are inclined to agree, when studying last week’s CFTC data they concluded that the industrial precious metal is now “oversold [and] generally vulnerable to short-covering.”

It’s clear that the weakness in the price is coming from negative speculation rather than the fundamentals – all of which point to a bullish future.

Industrial demand says industrious

Source: GFMS Thomson Reuters

Source: GFMS Thomson Reuters

The newly released 2017 Silver Survey makes for some interesting reading and is something that should perhaps be handed over to all those bearish money managers. Whilst investment demand in the form of silver bullion coins and bars did fall last year (mainly thanks to lower demand in the US and Canada) all other physical metrics point to an extremely bullish market.

Industrial demand, jewellery demand and supply restrictions all point to a much tighter market than the likes of COT and even some ETF holding reports would have you believe.

Thanks to photovoltaic growth (up 19%) industrial demand grew for the first time last year, since 2013. Whilst jewellery and silverware demand increased by 2% and 12% respectively.

These numbers mean little if you don’t know the juicy numbers – the huge tightening in supply.

Global mine production fell by more than 4% last year, this was the second annual decline. As with any industrial market, the industry doesn’t just rely on fresh metal from the ground – scrap is a major factor. But this is in an even worse state, falling to 138.1 Moz in 2017 – its sixth successive annual decline.

Silver Institute: Silver Will Outperform Gold

Generally silver likes to move in line with gold, if at a much lower price. However, this year it has not been able to match up to it’s own strong performance in early 2017 or gold’s performance this year. Currently the gold price is reacting nicely to global events whilst silver has lagged behind.

The ratio is back up above 80, something which has only been seen 3 times in the past. The World Silver Institute believe we should look at this as the market trying to tell us something:

The gold:silver ratio can rally in the face of a crisis, although the nature of such a crisis would dictate how the ratio develops. If circumstances suggest that market instability increases then investors would favor gold over silver. A good example

was during the 2008 global nancial crisis, when the ratio surged above 80. Meanwhile, a high ratio in the early 1990s was in response to the Gulf War. It is arguable that in anticipation of a crisis the market could see 80 or beyond. At the end of 2017, the gold:silver ratio was at 77 (though the full year average was just a moderate year-on-year increase to 73.9), a high level that perhaps suggests that the market is trying to tell us something. We suspect the high gold:silver ratio indicated that the market had been expecting another major crisis could be looming, or at the least that it was about time for equities correction, and therefore investors had been accumulating physical gold in the market.

Interestingly, the World Silver Institute Report’s own Johann Wiebe believes this high figure of 80 won’t be here to stay:

Wiebe believes that silver prices will rise and that the white metal will outperform gold in 2018 “purely based on the ratio argument.”

He continued, “[if] you look at the ratio it is at 82, and every time it pops above 80 … it reverses back because it is simply too cheap vs. gold. So in that sense, yes, I support that argument [that] silver will upsell gold.”

Whilst gold is probably the safest way to hedge against global crises, a falling dollar and increased monetary inflation, silver is by far the most profitable.

Consider that during gold’s last big rally in 2011, it reach $1,900 an ounce. At the same time silver was at $50/oz. Around 200% higher than silver’s current $16.75 price. And, a much lower ratio to gold.

Investors are likely to see this as they watch the gold price slowly tick upwards in response to ongoing, uncertain events. There will no doubt be many who turn to silver as a cheaper and more likely profitable complementary hedging asset. Indeed, we see them every week with very strong demand for silver coins (VAT free) from our UK/Irish and EU clients in recent weeks.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Silver Deserves An Allocation In Investment and Pension Portfolios

It can be very easy to dismiss something on first glance. In this case it is the price and speculators that are “painting” silver in a bad light. If anything, this should be the selling point. It is very likely that silver is in the early stages of a bull run. Its current price should not be dismissed by investors instead the fundamentals should be the focus of anyone deciding how best to allocate their portfolio.

Some analysts of late have suggested owning silver over gold. We would not advocate this as we believe that both merit a place in a well-balanced and diversified portfolio. We believe silver will outperform gold and offer opportunities for silver buyers to rebalance into gold after seeing gains in silver.

We fully expect both precious metals to outperform stocks, bonds, currencies and most other assets in the near future.

Recommended Reading

Silver bullion will likely outperform gold bullion going forward

News and Commentary

Gold up as investors hold onto positions; but risk appetite remains (Reuters.com)

Gold settles slightly lower as stocks rise, dollar drifts higher (MarketWatch.com)

Earnings Spur Stocks as Trade Woes Take Back Seat (Bloomberg.com)

Dow up over 200 points as investors cheer earnings (MarketWatch.com)

Factory Output in U.S. Cools After Surging in Previous Month (Bloomberg.com)

IMF Spots Trouble Ahead for the Global Economy After 2020 (Bloomberg.com)

U.K. Consumers Stay Under Pressure Even as Pay Squeeze Nears End (Bloomberg.com)

Majority Of Investors Starting To Cash Out, Convinced Market Peaks In Second Half (ZeroHedge.com)

How Libor’s Surge Will Help Pop The Global Bubble (RealInvestmentAdvice.com)

Turkey withdrew gold from Fed amid crisis (AhvalNews.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

17 Apr: USD 1,342.95, GBP 937.24 & EUR 1,084.57 per ounce

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

13 Apr: USD 1,340.75, GBP 938.93 & EUR 1,087.35 per ounce

12 Apr: USD 1,345.90, GBP 951.01 & EUR 1,090.99 per ounce

11 Apr: USD 1,345.20, GBP 947.96 & EUR 1,087.86 per ounce

10 Apr: USD 1,335.95, GBP 942.25 & EUR 1,083.46 per ounce

09 Apr: USD 1,328.50, GBP 941.91 & EUR 1,082.33 per ounce

Silver Prices (LBMA)

17 Apr: USD 16.63, GBP 11.60 & EUR 13.44 per ounce

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

13 Apr: USD 16.51, GBP 11.57 & EUR 13.40 per ounce

12 Apr: USD 16.66, GBP 11.74 & EUR 13.50 per ounce

11 Apr: USD 16.57, GBP 11.67 & EUR 13.39 per ounce

10 Apr: USD 16.49, GBP 11.65 & EUR 13.38 per ounce

09 Apr: USD 16.34, GBP 11.59 & EUR 13.32 per ounce

Recent Market Updates

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

– Martin Luther King Jr. Anniversary: Reminds Us Of Costs Of War To Society and Financial System

– Gold Outperforms Stocks In Q1, 2018

– Brexit, Stagflation Pressures UK High Street

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

A super commentary by Ronan Manly describing the criminal activity of the bankers as to how they have manipulated the fixes, how they blasted gold/silver on many occasions with impunity right under the watchful eyes of regulators.

(courtesy Ronan Manly)

Gold Manipulation, Spoofing Futures And Banging Fixes: Same Banks, Same Trading Desks

Submitted by Ronan Manly of Bullionstar

On 29 January 2018, the Commodity Futures Trading Commission (CFTC) Division of Enforcement together with the Criminal Division of the US Department of Justice and the FBI announced criminal and civil enforcement actions against 3 global investment banks and 5 traders for involvement in trade spoofing in precious metals futures contracts on the US-based Commodity Exchange (COMEX). COMEX is by far the largest and most active futures exchange in the world for trading precious metals futures including gold futures contracts and silver futures contracts.

The CFTC is bringing the charges under what it calls “commodities fraud and spoofing schemes“. Spoofing of orders is illegal under the US Commodity Exchange Act. The 3 banks in question are Deutsche Bank, UBS, andHSBC. As part of the CFTC’s prosecution, Deutsche Bank is being fined US$ 30 million, UBS US$ 15 million, and HSBC US$ 1.6 million.

The CFTC’s Order against the banks maintains that from at least February 2008 to at least September 2014, Deutsche Bank traders were involved in a scheme to manipulate precious metals futures prices by spoofing orders for those futures contracts, and also by extension that this spoofing triggered customer stop-loss orders.

Similarly, the CFTC Order says that UBS traders on the UBS precious metals spot trading desk were involved in spoofing orders in gold futures and silver futures contracts from January 2008 to at least December 2013, and likewise triggering customer stop-loss orders.

In the case of HSBC, the CFTC says that HSBC, through its New York office, spoofed orders in gold futures and other precious metals. However, the CFTC Order does not specify the period under which HSBC is accused of engaging in such spoofing. This may be because, according to the CFTC, HSBC cooperated during the CFTC’s investigation and offered to settle. But overall, the spoofing by one or more of the named banks was said to have run from January 2008 to at least September 2014.

As part of the process, the CFTC also announced civil enforcement actions against precious metals traders Andre Flotron formerly of UBS, and James Vorley and Cedric Chanu formerly of Deutsche Bank for what the CFTC describes as “spoofing and engaging in a manipulative and deceptive scheme in the precious metals futures market“.

According to the Department of Justice (DoJ) press release on the matter, Vorley (a UK citizen) and Chanu (a French citizen) are being charged in a criminal complaint in the Northern District of Illinois court with “conspiracy, wire fraud, commodities fraud, and spoofing offenses in connection with executing a scheme to defraud involving both solo and coordinated spoofing on the COMEX“. During that time, Vorley was based in London with Deutsche bank and Chanu was based in London and Singapore with Deutsche Bank.

Flotron is charged in an indictment in the District of Connecticut for “conspiracy to commit spoofing, wire fraud, and commodities fraud” during the time when he worked at UBS as a precious metals trader on the UBS trading desks in Zürich, Switzerland, and Stamford, Connecticut USA.

The DoJ statement also names Edward Bases and John Pacilio, and says that Bases and Pacilio are charged in a criminal complaint with “commodities fraud in connection with an alleged scheme to engage in both solo and coordinated spoofing on the COMEX“. Bases was at Deutsche Bank until June 2010 at which point he moved to a unit of Merrill Lynch. Pacilio worked for a unit of Merrill Lynch during 2010 and 2011 when some of his trade spoofing is alleged to have taken place.

Note that according to the DoJ “a complaint, information, or indictment is merely an allegation, and all defendants are presumed innocent until proven guilty beyond a reasonable doubt in a court of law“.

For an excellent explanation of some of the spoofing activities that these traders are accused of have engaged in, please see the recent article ‘US Gold & Silver Futures Markets: “Easy” Targets‘ by specialist researcher Allan Flynn posted on the BullionStar website and on his own ‘COMEX We have a Problem’ website here.

Spot, Fixes and Futures in the Gold and Silver Markets

While gold and silver futures trading is one side of the wholesale precious metals markets, it is not the full picture, because as well as COMEX, the over-the-counter (OTC) London Gold and Silver Markets are key gold and silver trading venues for these same investment banks, as well as key components of gold and silver price determination. And central to the London Gold Market and London Silver Market are the daily fixing auctions for gold and silver.

The investment bank precious metals traders who trade gold and silver in the wholesale market do so not just through exchange traded futures contracts or OTC contracts, but both. And they constantly trade across the London and COMEX ‘venues’ at the same time. In both gold and silver, predominant price discovery for the international gold price and for the international silver price occurs in the London OTC Market and on COMEX.

Price movements in one location, for example on COMEX futures, get instantly reflected in the London OTC spot quotes, and vice versa. Therefore price quotes in the London market, including opening prices and round prices for the London daily Fixings can be influenced by moving the futures prices. For example, if there is collusion among traders to push the futures prices lower so as to benefit other traders who have positions based on Fixing levels, this can be done by the trader from one bank pushing the futures price lower, while a trader at a second bank benefits from this movement in terms of his exposure to the Fixing price which has also moved lower. Such price movements are documented in the ‘Final Notice’ that the UK Financial Conduct Authority (FCA) levied against Barclays Bank and one of its precious metals traders in May 2014 (See below for details).

As highlighted below, the majority of the banks mentioned in the CFTC fines were also central to these gold and silver fixings, and astoundingly one of the traders mentioned above and subject to the CFTC and DoJ actions, James Vorley, was even a director of both of the private companies that oversaw the London Gold and Silver Fixings.

With the CFTC / DoJ fines, complaints and indictments against the banks and their traders for manipulating gold and silver futures prices now in the public arena, the question of manipulation of the London Gold and Silver fixing auctions now comes back in focus, and the question now needs to be asked – where are the regulators in investigating (and perhaps prosecuting) banks and traders for gold and silver fixings manipulation?

Because even a superficial look at the banks and traders, the trading desks and their operations, the trader chat room transcripts, and the connections between the futures and fixings at the time of the fixings should give even the most dullard regulators and prosecutors pause for thought.

Deutsche Bank and HSBC – New York Futures and London Fixings

As a reminder, the London Silver Fixings were a daily auction of (paper) silver at midday in London that operated up until August 2014 when they were replaced by the LBMA Silver Price auction. The London Gold Fixings were a twice daily auction of (paper) gold at 10:30 am and 3:00 pm in London that operated up until March 2015 when they were replaced by the LBMA Gold Price auction.

The London Silver Fixings were administered by a private company called London Silver Market Fixing Ltd (LSMFL) whose three members were Deutsche Bank, HSBC and the Bank of Nova Scotia. Deutsche Bank, HSBC and Bank of Nova Scotia were also the only 3 entities allowed to take directly participate in the silver fixings, and each had become a member of the silver fixings by acquiring one of the 3 traditional companies that had run the fixings – ScotiaBank acquired Mocatta in 1997, Deutsche acquired the old Sharps Pixley in 1993, and HSBC had acquired Samuel Montagu and rebranded as HSBC during its 1990s reorganisation.

The London Gold Fixings were administered by a private company called London Gold Market Fixing Ltd (LSMFL)which had 5 members, namely Deutsche Bank, HSBC, Bank of Nova Scotia, Barclays, and Societe Generale (SocGen). Only these 5 banks were allowed to directly participate in the gold fixings. These 5 banks were also the only banks in the gold fixings from 2004 all the way to 2014.

So from “January 2008 to at least September 2014“, the period stipulated by the CFTC that covers manipulation of gold and silver futures, the same banks, i.e. Deutsche Bank and HSBC, were at all times active members of the daily gold and silver fixings in London.

Even more amazingly, James Vorley, the Deutsche Bank trader who is the subject of the CFTC / DoJ accusation of “conspiracy, wire fraud, commodities fraud, and spoofing offenses” on COMEX was a Director of both London Silver Market Fixing Ltd and London Gold Market Fixing Ltd from September 2009 until May 2014 , which is all the way through the period of ‘at least February 2008 to at least September 2014’, when Deutsche Bank precious metals traders were involved in a scheme to manipulate precious metals futures prices by spoofing orders for those futures contracts. You couldn’t make this up!

Vorley, along with Deutsche’s Kevin Rodgers resigned from the London Gold and Silver Market fixing companies in May 2014, when Deutsche Bank dropped out of the daily gold and silver fixing auctions. Matthew Keen of Deutsche Bank had previously resigned as a director of the gold and silver fixing companies in January 2014 when he left the bank and was replaced by Rodgers who was Global Head of Foreign Exchange at Deutsche Bank at that time. But curiously, Rodgers also left Deutsche at the end of April 2014.

For a full rundown of all the directors of London Gold Market Fixing Ltd, and a timeline of the Keen – Rodgers – Vorley – Deutsche departures, see the excellent article on ZeroHedge from May 2015 titled ‘From Rothschild To Koch Industries: Meet The People Who “Fix” The Price Of Gold’.

There is plenty written elsewhere on how the LBMA maintained its stranglehold over the London gold and Silver reference price benchmarks when the old tarnished fixings were no longer viable and the bullion banks running those fixings had to quickly pretend to distance themselves from the fixing while at the same time maintaining total control over the new versions of the auctions. But in summary, in August 2014, when the new LBMA Silver Price auction was launched by the LBMA with just 3 bank members, HSBC and Bank of Nova Scotia continued as 2 of these members. When the LBMA Gold Price auction was launched in March 2015, the existing incumbents of the old Gold Fixings namely Barclays, HSBC, Bank of Nova Scotia and SocGen, rejoined the new auction along with its new members, UBS and Goldman Sachs.

Barclays Mini-Puke: Gaming the Gold Fixing

In May 2014, the UK Financial Conduct Authority (FCA) fined Barclays Bank £26 million for systems and controls failings and conflicts of interests in relation to the London Gold Fixing auctions of which it was one of the 5 bullion bank participants. According to the FCA, these failings persisted from 2004 (when Barclays joined the fixings) until 2013. The year 2004 was also when the gold and silver fixings stopped being conducted in a room in Rothschilds offices and began to be conducted remotely.

As part of the May 2014 fines of Barclays, the FCA also fined Daniel Plunkett, one of the Barclays London-based precious metals traders, £95,000. While the fine for Plunkett was specifically to penalise his placement and cancellation of orders which were intended to manipulate prices within the rounds of the fixing, the commentary supplied by the FCA on the case is interesting in that it shows how gold futures price movements external to the fixings also very much influenced the fixing round prices during the auction that the FCA penalised Plunkett for.

At the start of the 28 June 2012 Gold Fixing at 3:00 p.m., the Chairman proposed an opening price of USD1,562.00. However, the proposed price quickly droppedto USD1,556.00, following a drop in the price of August COMEX Gold Futures (which was caused by significant selling in the August COMEX Gold Futures market, independent of Barclays and Mr Plunkett).

You can see here the interactions and influences that the COMEX gold futures prices movements had on the opening price that the Gold Fixing Chairman proposed to the begin the auction with. And now that we know there was collusion between the various precious metals traders across the bullion banks, it is not difficult to accept that the traders from one bank could be moving the futures lower to not only help themselves but as a favour to precious metals traders at other cartel banks that were also involved in the collusion schemes.

Banging the Fixes – Chat Room Transcripts from Class Action Suits

But there is also direct evidence of trader collusion to manipulate prices in the London gold and silver fixings in the form of trader chat room transcripts. This is not speculation, it is fact. Facts that have been documented in class action proceedings in the New York courts brought by plaintiffs against the bank member of the London Gold and Silver Market Fixing companies.

Again we turn to Allan Flynn, who was probably first to call attention to the manipulation of the silver market by these same banks with his extensive and succinct coverage of the evidence from the New York class action suits in his 8 December 2016 article ‘How to Trigger a Silver Avalanche by a Pebble: “Smash(ed) it Good”‘ posted on the BullionStar website and on Allan’s website here, and in his follow-up article from 14 December 2016 titled “When Gold Pops 1430 We Whack It“, posted on his website and on the ZeroHedge website here.

In the silver class action suit against Deutsche Bank, HSBC, the Bank of Nova Scotia, and UBS, Deutsche agreed in April 2016 to settle with the plaintiffs and to produce “instant messages, and other electronic communications”as part of the settlement. See BullionStar article ‘Deutsche Bank agrees to settle with Plaintiffs in London Silver Fixing litigation‘ for full details of the April 2016 announcement.

Attorneys for the plaintiffs subsequently, as Allan Flynn documented “submitted samples of dozens of chat room messages between UBS and Deutsche Bank“, indicating “many efforts to artificially suppress gold prices, and to manipulate gold prices at the time of the Fixing.”

“One chat see’s a Deutsche Bank trader confirming with a UBS trader his trading had indeed influenced the Gold Fix: ‘u just said u sold on fix.‘ The UBS traded replied ‘yeah,’ ‘we smashed it good.‘

Another transcript example contained the following exchange:

“During a trading day which had been less successful the Deutsche Bank trader assured his opposite trader from Bank of Nova Scotia that ‘at least the fix will be fun . . . make it all back there!!!!!!‘”

So here we have precious metals traders actually colluding to artificially move the price levels on the fixings.

Technology Facilitated the Manipulation of the Fixes since 2004

In June 2015, I wrote an article on the BullionStar website titled “The pre-2015 London Gold Fixings – More technologically advanced than reported” in which I set out substantial evidence that the former Gold Fixings up until March 2015 were not some archaic dial-in telephone based auction using paper and pencils to set the price as the mainstream financial media choose to believe, but that the auctions since 2004 in both gold and silver employed sophisticated web-based technology apps, trading software, messaging apps and chat apps, all of which could also facilitate collusion and price manipulation across multiple trading desks in ‘rival’ banks.

When Rothschild pulled out of the Gold Fixings in 2004, Barclays took Rothschild’s place and the fixings moved to a remote model where traders from each of the 5 members banks of the Gold Fixing coordinated remotely instead of meeting twice a day face to face. At the same time, the fixing members introduced this new communication technology to assist their twice daily fixes.

In November 2014, the Swiss financial regulator FINMA announced that an investigation of UBS had found manipulation and attempted manipulation of by UBS Zurich employees of forex and precious metals benchmarks. At the time, Mark Branson, FINMA’s CEO said that “we have [also] seen clear attempts to manipulate fixes in the precious metals markets.”

According to FINMA, it found that chat groups between traders at multiple banks were central to how the manipulation was coordinated:

“In the improper business conduct in foreign exchange and precious metals trading, electronic communication platforms played a key role. The abusive practices were evidenced in the information exchanged between traders in chat groups. FINMA examined thousands of suspicious chat group conversations between traders at multiple banks.“

The introduction of new technology and chat apps from 2004 is also highly correlated with academic research findings showing “a decade of manipulation” of the gold fixing from 2004 until 2013. As highlighted in the Bloomberg article “Gold Fix Study Shows Signs of Decade of Bank Manipulation”

“Abrantes-Metz and Metz screened intraday trading in the spot gold market from 2001 to 2013 for sudden, unexplained moves that may indicate illegal behavior. From 2004, they observed frequent spikes in spot gold prices during the afternoon call. The moves weren’t replicated during the morning call and hadn’t happened before 2004, they found.

Large price moves during the afternoon call were also overwhelmingly in the same direction: down.

On days when the authors identified large price moves during the fix, they were downwards at least two-thirds of the time in six different years between 2004 and 2013. In 2010, large moves during the fix were negative 92 percent of the time, the authors found.

There’s no obvious explanation as to why the patterns began in 2004, why they were more prevalent in the afternoon fixing, and why price moves tended to be downwards, Abrantes-Metz said in a telephone interview this week.”

Well, there is an obvious explanation. The downward price movements identified by Abrantes-Metz and Metz started in 2004 because that’s when the London gold fixings went to a remote model and technology including chat apps was introduced. The suspicious price movements were more prevalent in the London afternoon because that was also the New York morning where COMEX gold futures were more active and where New York based traders could force the futures down causing a corresponding drop in the opening prices and round prices in the fixing auctions.

Conclusion

Prosecuting banks and traders for price manipulation on COMEX futures while ignoring the far larger London market and its gold and silver fixings looks like a job half done. Trading desks and their traders are agnostic to trading venues and with interlinked markets, the COMEX and the London Fixings are two sides of the same coin.

With blatant evidence that the same banks and traders were involved in both markets, and with actual chat room transcripts now confirming that precious metals traders across multiple banks were colluding in fixing price manipulation, then why are their no active regulatory investigations of trader manipulation of the London Gold and Silver Fixings?

Is it because of lack of jurisdictional authority or are the regulators and criminal enforcement agencies such as the FCA, DoJ, FINMA and the German BAFIN too terrified of opening a can of worms into the huge liabilities that would arise from proving a decade long criminal manipulation of the London Gold and Silver price benchmarks and that were used throughout the world the value everything from ISDA contracts to institutional precious metals products, to ETFs.

END

GATA is an exempt non profit organization and as such must show it’s return. So here it is:

(courtesy GATA)

Dear Friend of GATA and Gold:

Today is the federal tax filing deadline for most taxpayers in the United States, and since GATA, as a federally tax-exempt educational and civil rights organization, is obliged by law to disclose its tax return to all who ask to see it, a tax returns section has been created at our internet site, containing copies of the organization’s tax returns for 2017, 2016, and 2015.

This seems to be the most efficient mechanism of transparency.

The tax returns can be found here:

http://www.gata.org/taxonomy/term/24

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke talking with Sprott Money outlines the fraud behind the “Exchange for Physical” contracts that I highlight to you every trading day.

(courtesy Craig Hemke/Sprott Money/GATA)

Craig Hemke at Sprott Money: The Comex ‘exchanges for physical’ fraud

Submitted by cpowell on Tue, 2018-04-17 23:33. Section: Daily Dispatches

7:35p ET Tuesday, April 17, 2018

Dear Friend of GATA and Gold:

The sudden rise in settlement of Comex gold and silver futures contracts through the formerly obscure off-exchange mechanism of “exchange for physicals” is likely just increasing the supply of imaginary metal, the TF Metals Report’s Craig Hemke writes today for Sprott Money

Hemke writes: “The escalating abuse of this process has brought the sham and fraud of the digital derivative pricing scheme into greater focus. Mainly, how in the world does a swapping of derivative contracts, where there’s obviously zero physical metal involved, equitably determine the true price and value of underlying physical asset?

“Additionally, what does the increasing volume of EFPs say about the state of the physical market and the availability in size of physical gold on demand? If the Comex/LBMA is simply increasing the amount of leverage in the system, one must wonder how stretched and stressed the pricing scheme has become.”

Hemke’s analysis is headlined “Comex Exchanges for Physical” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/comex-exchanges-for-physical-craig-hemk…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

An excellent commentary from Lawrie Williams. I would not take the GFMS’s calculations on silver demand as they are always on the low side. However they do note that silver supply is down 4%, identical to the calculations of Steve St Angelo.

Please note that all of silver’s demand components (other than hoarding) are well up:

Photovoltaics, jewellry, the auto sector and also silver’s use in electrical components. The killer blow to the banking cartel is the lower silver supply from the mines

(courtesy Lawrie Williams/Sharp Pixley)

LAWRIE WILLIAMS: Silver market in deficit for fifth year – GFMS

London-based metals analysis consultancy GFMS has just released its latest annual Silver Survey on behalf of the Washington DC-based Silver Institute and it would appear to provide ammunition for those who believe silver is currently underpriced vis-à-vis gold. Perhaps it is coincidental, but the Gold:Silver ratio (GSR) fell below 80 this morning for the first time in weeks. We have several times put forward the view that the recent high level of the GSR, which recently reached close to 82, provided a strong buying opportunity for silver and that a level of 70 or lower might be more realistic.

The GFMS analysis found that in 2017, for the fifth year in a row, the silver market recorded another deficit – this time of some 26 million ounces (810 tonnes).

One of the principal factors was that mine supply is adjudged as having fallen for the second consecutive year – by 4% in 2017 This follows on from 13 consecutive annual increases prior to 2016. The fall in mined output is partly attributed to years of Capex reductions in combination with supply disruptions, particularly in the Americas. GFMS also reckoned that scrap supply contracted by 1% and, in combination with net-hedging of 1.4 million ounces (44 tonnes), total silver supply was seen as falling by 2% to just under one billion ounces.

Physical demand, though, is also seen as contracting in 2017 – by 2%. This was largely attributed to a 27% drop in coin and bar demand for investment. The fall was the second significant decline in a row and the consultancy sees that as mainly driven by robust equity performances across various exchanges globally, and also the perhaps temporary attraction of investment in bitcoin which surged hugely in 2017, but seems to have come to an abrupt halt in the current year as cryptocurrencies plunged by as much as 60% over a very short period of time. Investors are also adjudged to have opted for used coins as opposed to new ones which hindered new coin sales. However, on the positive demand side, silver used in jewellery, silverware and industrial fabrication are all estimated at recording increases last year, rising by 2%, 12% and 4% respectively.

In particular, silver demand used in photovoltaics (mostly solar panels) recorded another strong year, rising by 19%, driven in particular by strong uptake from Chinese households. Following various years of increased thrifting and substitution pressure, silver used in electrical components, brazing & alloys and other applications also recorded a positive performance last year. Demand from the automotive sector was reportedly strong.

Other factors pointed to in the GFMS analysis were that in spite of lower retail demand, silver ETP investors continued to add a net total of 2.4 million ounces (74 tonnes) to the total outstanding silver ETP stock across the various funds, with silver stored in Switzerland and the U.S. in particular benefiting from the annual rise. On balance, though, total global exchange stocks are seen as rising by 6.8 million ounces (210 tonnes) which was largely a function of lower physical demand in major consuming regions.

Combined, the silver net-balance is seen as a deficit of 35.2 million ounces(1,094 tonnes) representing on average 3% of total annual demand, the lowest since 2005.

There’s enough nervousness in the air to see gold climb through the $1,360 level again although it probably needs to hit $1,365 or higher to call the latest rise a true breakout. But if it does do so the principal beneficiary may well be silver which has been seriously underperforming its sibling precious metal of late. Could this be the start of what silver buffs have been predicting in terms of a restting of the price balance with gold?

Of the other main investment options, bitcoin has tanked, and could yet fall further as more and more opposition from governments and central banks to crypto- currencies materializes; equities and bonds are no longer the sure route to investment growth they have been over the past several years, while gold stocks continue to underperform given management’s failings to control costs and debt – although this may be beginning to come right, but perhaps too little too late for the investment community.

What may have gone unnoticed is that gold in particular has outperformed equities so far this year – and where gold goes silver tends to follow. So far this year the Dow is down and the S&P 500 alos and both are looking potentially vulnerable to further falls. By contrast the gold price is up around 2% year to date, while silver is still lagging – down 3.5% but perhaps at last beginning to play catch-up. Gold stocks, as represented by the HUI index, are down a massive 10.8% which shows how strongly out of favour they have become so far this year. (We do anticipate a recovery but this may only be in the medium to long term as the gold stocks in general have a fair way to go in restoring investor confidence.)

But as far as the silver price is concerned the level of the gold price has to be particularly relevant too as the two principal precious metals have usually moved together, with silver tending to outperform gold when the latter is rising and vice versa. As we see gold continuing to rise this year that colours our views on the likely progress of the GSR (see above).

Re, gold there is also a considerable amount of geopolitical anxiety as the world awaits the outcome of proposed tit-for-tat tariff barriers between the U.S. and China in particular being raised in response to President Trump’s initiatives, as well as serious concerns about an escalation of conflict in Syria, which could pit the U.S. in direct military conflict with Russia. Both sides might be willing to trial their latest weaponry against each other in a limited-area conflict to see who might come out on top in a bigger military confrontation.

President Trump no doubt had the support of his new more hawkish National Security Advisor, John Bolton, in the pre-emptive military action following the disputed alleged chemical weapons attack against the former Syrian rebel stronghold of Douma. Latest reports coming out of Douma, now that independent reporters are able to access the area, may even suggest that the alleged chemical weapons attack may never have happened at all and that the images of children gasping for breath may have been due to oxygen deprivation as a result of conventional bombing. Not, perhaps an acceptable situation in its own right, but in the eyes of the world not as heinous as chemicals weapons deployment. It is difficult to see what the hugely maligned President Assad could have gained through the use of chemical weapons apart from universal condemnation! Even if this latest reported evidence gains credence it seems unlikely that the U.S., U.K. and France will ever admit this.

Both Russia and Iran appear to be lined up in support of Syria’s President Assad – and all of these seem to be among the U.S. Administration’s list of hostile military powers deserving of a bloody nose – but it might not stop there which is somewhat unnerving and could all be beneficial for gold should matters escalate further. Modern warfare seems to be as much a matter of propaganda as actual military action but the former can easily degenerate into the latter.

So the latest analysis from GFMS does seem to support the potential advantages of silver as an investment over gold through the remainder of the current year, and perhaps beyond. Supply/demand fundamentals look positive and the price ratio with gold looks due to come down, while we see the latter’s potential for price growth still looks positive.

18 Apr 2018

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2829 /shanghai bourse CLOSED UP 24.60 POINTS OR 0.80% / HANG SANG CLOSED UP 221.50 POINTS OR 0.74%

2. Nikkei closed UP 310,61 POINTS OR 1.42%/ /USA: YEN RISES TO 107.17/

3. Europe stocks OPENED IN THE GREEN /USA dollar index RISES TO 89.56/Euro RISES TO 1.2384

3b Japan 10 year bond yield: FALLS TO . +.038/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.17/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.43 and Brent: 72.36

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.519%/Italian 10 yr bond yield DOWN to 1.7271% /SPAIN 10 YR BOND YIELD DOWN TO 1.220%

3j Greek 10 year bond yield FALLS TO : 4.012?????????????????

3k Gold at $1350.25 silver at:16.98 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 7/100 in roubles/dollar) 61.59

3m oil into the 67 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.17 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9677 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1984 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.519%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.