GOLD: $1331.30 UP $ 9.90 (COMEX TO COMEX CLOSINGS)

Silver: $16.72 UP 8 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1331.00

silver: $16.70

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:96 NOTICE(S) FOR 9600 OZ.

TOTAL NOTICES SO FAR 967 FOR 696700 OZ (3.007 tonnes)

ACTUALLY THERE WERE TWO LOTS FILED; LATE THIS AFTERNOON: 198 AND LATE TONIGHT: 96

THE COMEX IS OUT OF GOLD

For silver:

APRIL

11 NOTICE(S) FILED TODAY FOR

55,000 OZ/

Total number of notices filed so far this month: 477 for 2,385,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9301/OFFER $9401: up $390(morning)

Bitcoin: BID/ $9409/offer 9509: UP $502 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1334.58

NY price at the same time: 1326.80

PREMIUM TO NY SPOT: $7.00

ss

Second gold fix early this morning: 1334.46

USA gold at the exact same time: 1327.20

PREMIUM TO NY SPOT: $7.26

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE 6923 CONTRACTS FROM 221,503 FALLING TO 214,580 ACCOMPANYING YESTERDAY’S HUGE 50 CENT LOSS IN SILVER PRICING. AFTER A STRING OF 4 CONSECUTIVE OI GAINS, WE FINALLY REGISTER TWO CONSECUTIVE DROPS IN OI. HOWEVER WE WERE AGAIN NOTIFIED THAT WE HAD AN HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 0 EFP CONTRACTS FOR APRIL, 5220 EFP’S FOR MAY , 193 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 5413 CONTRACTS. WITH THE TRANSFER OF 5413 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 5413 EFP CONTRACTS TRANSLATES INTO 27.065 MILLION OZ ACCOMPANYING 1.THE FALL IN SILVER PRICE (50 CENTS) AT THE COMEX AND 2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

62,177 CONTRACTS (FOR 17 TRADING DAYS TOTAL 62,177 CONTRACTS) OR 310.885 MILLION OZ: AVERAGE PER DAY: 3,657 CONTRACTS OR 18.287 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 310.885 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 44.41% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1.028950 BILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED FALL IN COMEX OI SILVER COMEX OF 6923 ACCOMPANYING THE LARGE 50 CENT LOSS IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD AN HUMONGOUS SIZED EFP ISSUANCE OF 5413 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 0 CONTRACTS WERE ISSUED FOR APRIL, 5220 EFP’S WERE ISSUED FOR THE MONTH OF MAY, AND 193 EFP CONTRACTS FOR JULY, FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 5413). SURPRISINGLY WITH THE HUGE WHACK YESTERDAY WE LOST ONLY 1510 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 5413 open interest contracts headed for London (EFP’s) TOGETHER WITH AN DECREASE OF 6923 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 50 CENTS AND A CLOSING PRICE OF $16.64 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.073 BILLION TO BE EXACT or 155% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 11 NOTICE(S) FOR 55,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 310.885 MILLION OZ/ (SO FAR)

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY 4629 CONTRACTS DOWN TO 510,233 ACCOMPANYING THE FALL IN PRICE/YESTERDAY’S TRADING ( DROP OF $14.00). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 15,916 CONTRACTS : JUNE SAW THE ISSUANCE OF 15,851 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 65 CONTRACTS (REPORTED LATE YESTERDAY) WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 510,233. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A LARGE SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 4629 OI CONTRACTS DECREASED AT THE COMEX AND AN GIGANTIC SIZED 15,916 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 11,287 CONTRACTS OR 1,128,700 OZ = 35.107 TONNES.

YESTERDAY, WE HAD 11,451 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 191,803 CONTRACTS OR 191,80,300 OZ OR 596.58 TONNES (17 TRADING DAYS AND THUS AVERAGING: 11,282 EFP CONTRACTS PER TRADING DAY OR 1,128,200 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 17 TRADING DAYS IN TONNES: 596.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 596.58/2550 x 100% TONNES = 23.39% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,642.005* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN DECREASE IN OI AT THE COMEX OF 4629 WITH THE FALL IN PRICE // GOLD TRADING YESTERDAY ($14.00 DROP). WE ALSO HAD A GIGANTIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,916 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,451 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED NET GAIN OF 12,757 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15,916 CONTRACTS MOVE TO LONDON AND 4619 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 35.107 TONNES).

we had:96 notice(s) filed upon for 9600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $9.90 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER UP 8 CENTS TODAY: ANOTHER HUGE CHANGE/SOMETHING SPOOKED THE CROOKS: A DEPOSIT OF 1.601 MILLION OZ

/INVENTORY RESTS AT 316.899 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE 6923 CONTRACTS from 221,503 UP TO 214,580 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AFTER WE HAVE HAD FOUR CONSECUTIVE OI GAINS WE FINALLY HAVE TWO CONSECUTIVE OI DROPS. HOWEVER OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE: 0 EFP CONTRACTS FOR APRIL, 5220 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 193 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 5413 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 6923 CONTRACTS TO THE 5413 OI TRANSFERRED TO LONDON THROUGH EFP’S, SURPRISINGLY WE OBTAIN A LOSS OF 1510 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.55 MILLION OZ!!! AND THIS OCCURRED DESPITE A HUGE FALL IN PRICE OF 50 CENTS. THE BANKERS ORCHESTRATED THEIR RAID YESTERDAY TO DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL: ON A NET BASIS NOBODY LET THE SILVER ARENA.

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX ACCOMPANYING THE FALL IN SILVER PRICING / YESTERDAY (50 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 5413 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 60.92 POINTS OR 1.99% /Hang Sang CLOSED UP 381.94 POINTS OR 1.26% / The Nikkei closed UP 190.08 POINTS OR 0.86%/Australia’s all ordinaires CLOSED UP .56% /Chinese yuan (ONSHORE) closed UP at 6.3070/Oil UP to 69,07 dollars per barrel for WTI and 74.73 for Brent. Stocks in Europe OPENED MIXED. ONSHORE YUAN CLOSED UP AT 6.3070 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3068/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

GERMANY

A must read if you want to understand what is going on in Europe. As i have pointed out the key is the Nord Stream 2 project and that will bring Germany closer to Russia than the USA.

a very important commentary

( Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

ii)TURKEY/USA/SYRIA

Turkey is upset with the USA in that they are providing 5,000 trucks loaded with weapons to the Kurds in Northern Syria and yet the USA refuses to supply defensive weapons to Turkey. No wonder Turkey wants to repatriate its gold from the Federal Reserve Bank of New York (FRBNY)

( zerohedge)

iii)IRAN/EUROPE/USA

Iran again threatens trouble for the west if Trump leaves the Nonproliferation treaty

( zerohedge)

France/Iran/USAiii b)Macron could not break Trump as he states that the Iran deal is insane:

( zerohedge)

6 .GLOBAL ISSUES

( zerohedge)

ii)Bellwether Caterpillar, a good indicator of global growth had good earnings but stunned the market as the basically stated that the economy turned on a dime

( zerohedge)

7. OIL ISSUES

Oil drops on Macron’s proposal of a new Iranian deal

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)The rise in the price of oil is helping save global asset prices according to these two reporters at Bloomberg( Bloomberg/GATA)

iii) FRBNY earmarked gold report

(Harvey)

10. USA stories which will influence the price of gold/silver

ic)AFTERNOON TRADING: THINGS GET UGLY

ii)This morning’s data reports:

b)Soft data Richmond Fed sinks to a 25 yr lows: it does not look good for the USA economy(courtesy zerohedge)

iii)SWAMP STORIES

a)A deep state operative and friend of Rosenstein will not recuse himself from the Trump Cohen probe

(courtesy zerohedge)

b)This is interesting: a former Obama DOJ made a dramatic call to McCabe to quash the Clinton probe

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:266,471 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 312,630 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE 6923 CONTRACTS FROM 221,503 DOWN TO 214,580 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 50 CENT FALL IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A 0 EFP CONTRACTS ISSUED FOR APRIL, 5220 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS, AND 193 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 5413. ON A NET BASIS WE LOST 1510 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 6923 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 5,413 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 1510 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 115 contracts FALLING TO 31 contracts. We had 5 notices filed upon so in essence we LOST 120 contracts or 600,000 additional ounces of silver will NOT stand for delivery in this non active delivery month of April .

The next big active delivery month for silver will be May and here the OI LOST 17,874 contracts DOWN to 67,226. June saw a GAIN of 208 contracts to stand at 382. The next big delivery month for silver is July and here the OI ROSE by 7396 contracts UP to 104,008.

We had 11 notice(s) filed for 55,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 24/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

96 notice(s)

9600 OZ

|

| No of oz to be served (notices) |

530 contracts

(53,000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

967 notices

96700 OZ

3.007 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 96 contract(s) of which 95 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (967) x 100 oz or 96700 oz, to which we add the difference between the open interest for the front month of APRIL. (626 contracts) minus the number of notices served upon today (96 x 100 oz per contract) equals 149,700 oz, the number of ounces standing in this active month of APRIL (4.656 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (967 x 100 oz or ounces + {(626)OI for the front month minus the number of notices served upon today (96 x 100 oz )which equals 149,700 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 3 COMEX OI CONTRACTS OR 300 OZ OF GOLD WILL STAND

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

703,334.924 oz

Brinks

Delaware

CNT

HSBC

SCOTIA

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

11

CONTRACT(S)

(55,000 OZ)

|

| No of oz to be served (notices) |

20 contracts

(100,000 oz)

|

| Total monthly oz silver served (contracts) | 477 contracts

(2,385,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) everybody else: OZ

total deposits today: nil oz

we had 5 withdrawals from the customer account;

i) out of Brinks: 2000.35 oz

ii) Out of Delaware: 1001.00 oz

iii) Out of CNT 615,084.157 oz

iv) Out of HSBC: 20,014.380

v) Out of Scotia: 65,235.037 oz

total withdrawals; 703,334.924 oz

we had 0 adjustment

total dealer silver: 62.576 million

total dealer + customer silver: 261.751 million oz

The total number of notices filed today for the APRIL. contract month is represented by 11 contract(s) FOR 55,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 477 x 5,000 oz = 2,385,000 oz to which we add the difference between the open interest for the front month of April. (31) and the number of notices served upon today (11 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 477(notices served so far)x 5000 oz + OI for front month of April(31) -number of notices served upon today (11)x 5000 oz equals 2,485,000 oz of silver standing for the April contract month

WE LOST 120 SILVER CONTRACT OR 600,000 ADDITIONAL OUNCES WILL NOT STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AND THESE GUYS GAVE UP AT THE COMEX AND TRAVELED TO LONDON IN AN ATTEMPT TO OBTAIN METAL.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

CRIMINALS!!

ESTIMATED VOLUME FOR TODAY: 163,430 CONTRACTS (WOW) 817 MILLION OZ OR 116% OF ANNUAL PRODUCTION.

CONFIRMED VOLUME FOR YESTERDAY: 206,603 CONTRACTS (my goodness)

YESTERDAY’S CONFIRMED VOLUME OF 206,603 CONTRACTS EQUATES TO 1,033 MILLION OZ (1.033 billion oz) OR 148% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.22% (APRIL 24/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.51% to NAV (APRIL 24/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.22%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.51%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.12%: NAV 13.77/TRADING 13.47//DISCOUNT 2.12.

END

And now the Gold inventory at the GLD/

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 24/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 368 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 318 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 24/2018: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.601 MILLION OZ

Inventory 316.899 million oz

end

6 Month MM GOFO 2.01/ and libor 6 month duration 2.52

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.01%

libor 2.52 FOR 6 MONTHS/

GOLD LENDING RATE: .51%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.48

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.29

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

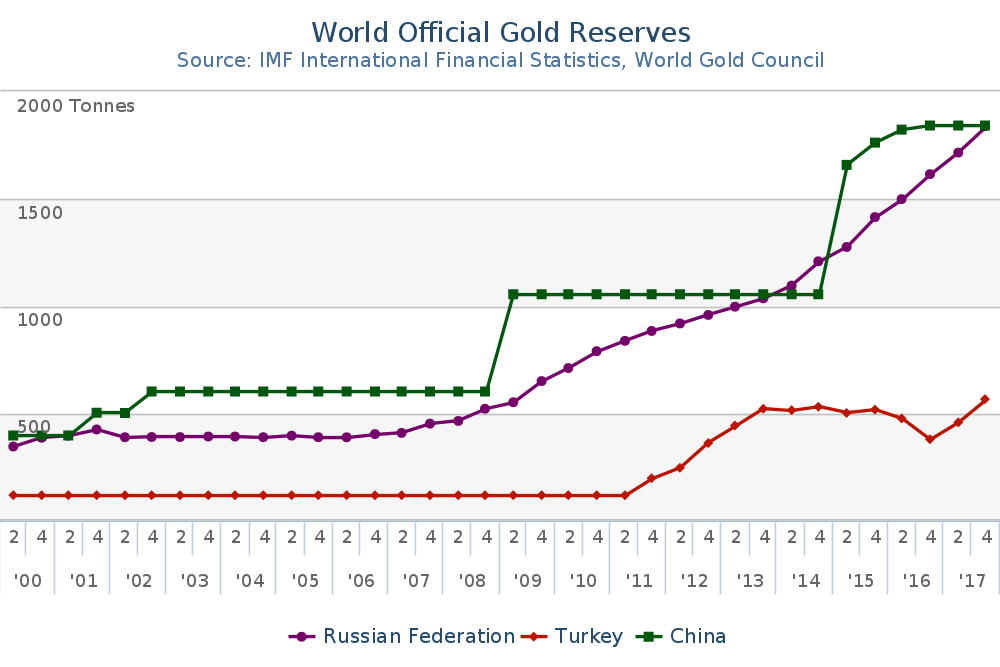

Russia Buys 300,000 Ounces Of Gold In March – Nears 2,000 Tons In Gold Reserves

– Russia buys 300,000 ounces of gold in March and nears 2,000t in gold reserves

– Russia now holds just over 1,861 tonnes, more than officially reported by China at 1,842t

– Both Russia and China have the power to destabilise US dollar by dumping dollar-denominated assets

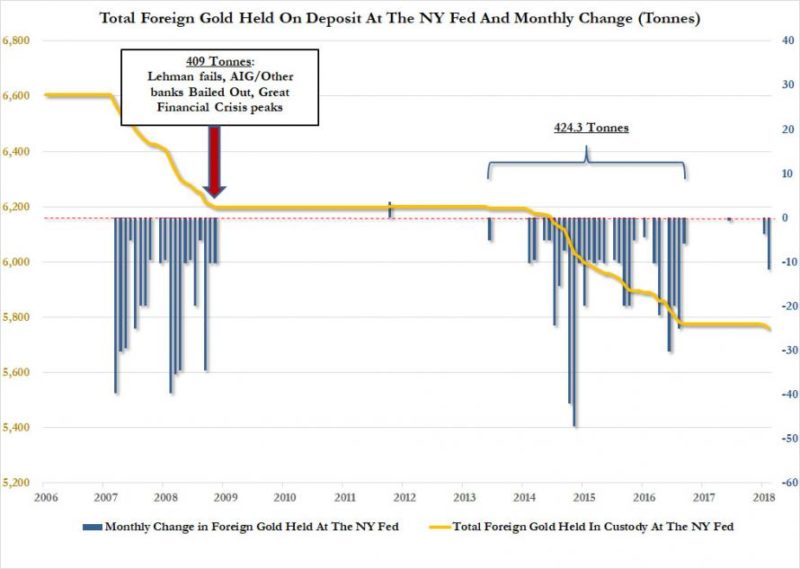

– Turkey has removed all gold held in the U.S. opting for Bank of England and BIS

– Turkey follows trend set by both Germany, Netherlands and others to remove gold reserves stored in the United States

– Central bank decisions regarding gold reserves are examples of countries becoming nervous about the outlook for the dollar under the Trump administration

Russia bought another 300,000 troy ounces of gold in March bringing Russia’s total gold reserves to 1,861 tonnes or 60.8 million troy ounces as of the start of April, the central bank announced loudly at the weekend.

The continuing robust and steady accumulation of gold reserves continues and it was notable how Russian media channels loudly (more loudly than usual it seemed with many outlets covering) pronounced the continuing diversification into gold bullion by the Russian central bank. It suggests that gold is being used as a bulwark to protect Russia from the stealth financial, trade and currency wars which appear to be deepening.

Russia is not the only country diversifying into gold and many other countries are doing so as they seek to protect themselves from the coming devaluation of the US dollar and U.S. dollar hegemony. This is evidenced both by gold purchases and also in many strategic decisions regarding the storage of national gold reserves.

While Russia was adding to its gold reserves, taking it above China’s holdings, Russia’s new ally Turkey was busy removing all gold bullion reserves held in the United States.

Both are clear moves against US dollar hegemony. Gold reserve changes combined with the news that Russia and China have agreed to settle some trades in ruble and yuan is a clear step that the world’s super powers are looking to reduce dependence on the US dollar and the increasing move away from the US dollar as global reserve currency.

Whilst it can be difficult to look past the Western media rhetoric regarding the likes of Russia, Turkey and China, there are lessons to be learnt by the everyday investor and saver.

These moves have also been seen by western nations such as the Netherlands and Germany who recently made the decision to bring some (if not all) of their reserves back to Europe.

The Gold Mission

Putin has long been on a mission to build up the country’s gold reserves after previous Russian governments ran the country’s reserves down to less than 300 tonnes.

The current president has made it clear that the country should be holding gold, rather than US dollars. For many years, the Russian central bank has consistently bought gold, driven by Putin’s believe in the financial sovereignty offered by gold and its protection against geopolitical and economic risks.

“Under the instruction by President Putin, the Bank of Russia has been implementing the program of increasing the absolute share of gold in the gold and currency reserves of Russia for many years.”

First Deputy Chairman of the Russian regulator Sergey Shvetsov

Putin first came to power in 2000 and since then the country has had more months than not, when it has purchased gold bullion. A large jump in reserves was seen in 2014 after Western sanctions were imposed and Russia has been the world’s largest gold buyer ever since. It is now the fifth largest gold holder after the United States, Germany, Italy, and France.

Russia is also the third largest producer of the precious metal. As a result, the majority of its purchases are locally sourced, giving the country an additional edge when it comes to protecting its finances. This is something that China is also wise to. It does not allow the export of any gold mined in the country, further evidence of the desire to protect the country’s financial system and economy and position the yuan as an alternative to the dollar in the long term.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

The golden noose?

The build-up of gold reserves by non-Western countries is something which could end up tipping the scales of the global order.

Many believe that should bad relations continue between the US and these nations then US-denominated assets currently held in forex holdings by the relevant central banks, could be dumped for alternatives. Nations may opt to diversify into the Chinese yuan (in the case of Russia) but also gold. Most likely it would just take either Russia or China to do this, before many others followed suit.

We know from recent comments by the likes of Erdogan and Putin that this is a possibility not far from their minds:

“With the dollar the world is always under exchange rate pressure. We should save states and nations from this exchange rate pressure. Gold has never been a tool of oppression throughout history.” Turkish PM Erdogan, April 2018

At the same conference Erdogan explained how he was pushing for international loans to no longer be made in dollars, but instead gold:

“I made a suggestion at a G20 meeting. I asked: Why do we make all loans in dollars? Let’s use another currency. I suggest that the loans should be made based on gold.”

When loans are made in dollars, the debtor is instantly taken hostage by the issuing central banks’ policies. The central bank determines the price of dollar through monetary policy and it’s value thanks to currency printing. Were loans to be issued in gold these huge counter party pressures would no longer be a feature of the largely dollar based debt-system.

Hands off our gold

China for many years has made it clear that gold purchased in China is to stay in China. Russia and Turkey are of the same belief.

The news broke last month that Erdogan’s central bank had decided to call back its gold reserves held in the United States. There were reportedly 220 tonnes stored in the country. The move was followed by the country’s largest private banks also moving their gold from the country. One example was Halk Bankasi bank which transferred 29 tons of gold back to Turkey

The decision followed Erdogan’s call to “to get rid of exchange rate’s pressure and to use gold against the dollar.”

Speaking to RT about Turkey’s decision to repatriate its gold from the US Federal Reserve, Anatoly Aksakov (chairman of the State Duma Committee on Financial Markets) said: “We do not have a gold reserve in the US, we have only Forex (foreign exchange) reserves abroad. No one can lay hands on our gold.“

By removing gold from one jurisdiction to another you are making one very loud and political statement – we can look after our gold and we don’t want you anywhere near it.

Decisions by both western and non western countries to repatriate their gold tells the US that they will no longer have power over their foreign reserves and that they do not trust them to look after them.

Conclusion – Be your own central bank and take delivery or own in safest vaults, in safest jurisdictions in the world

Russia and increasingly Turkey and China are countries that are increasingly seen as threats to the West, in one form or another. As a result various measures have been taken against them to make international trade and negotiations very difficult.

Whether through sanctions or trade tariffs countries are beginning to really feel the weight of the US and its allies’ powers. As a result, they are using gold to protect themselves and to protect their foreign exchange reserves and hard earned national savings.

Investors can learn something here. Fiat currencies will always have a counterparty that is far more powerful than the saver or pension holder. There is rarely little interest by the fiat issuer to take note of how it’s currency management is affecting the individual’s savings and investments.

Gold removes this risk. Central banks are unable to impact the supply or holding of physical gold that an investor holds legal title to and stores in a safe jurisdiction.

The likes of Russia, Turkey and China recognise the financial independence holding gold bullion can bring, they also understand the importance of storing it at a location that cannot be compromised by western sanctions, central bank screw-ups, political targeting and nationalisation of gold assets and gold companies.

Investors should follow suit and act as their own central bank. Prepare financially by having a sensible allocation to physical gold so that it is protected from central banks massive monetary experiment that risks destroying all hard earned wealth.

Gold also serves to protect in times of heightened geopolitical risk, terrorism and war. Follow the same steps as these aforementioned countries – own physical gold, store in a safe jurisdiction and ensure you have legal title to your bullion through allocated and segregated bullion ownership.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Recommended reading

Gold Bullion Is “100% Guarantee from Legal and Political Risks” – Russia

Turkey, Gold and the End of US Dollar Hegemony

China, Russia Alliance Deepens Against American Overstretch

News and Commentary

Gold steady but buoyant dollar, Treasury yields weigh (Reuters.com)

U.S. existing home sales rise; inventory remains tight (Reuters.com)

Trade war negative for economy says Fed’s Williams: El Pais (Reuters.com)

After Weeks of Chaos, U.S. Throws Aluminum Industry Lifeline (Bloomberg.com)

Deutsche Bank’s Bad News Gets Worse With $35 Billion Flub (Bloomberg.com)

Image source: US Investors

Trump Stress-Tests the World Economy (Bloomberg.com)

Oil Rises on Flaring Geopolitical Risks and Shrinking Stockpiles (Bloomberg.com)

The Pension Crisis Gets A Catchy Name: “Silver Tsunami” (DollarCollapse.com)

SWOT Analysis: Hindu Celebration Could Push Gold Price Higher By 10 Percent (GoldSeek.com)

ECB Capitulates On Defusing Eurozone’s “$1 Trillion Ticking Time Bomb” (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

23 Apr: USD 1,328.00, GBP 950.45 & EUR 1,085.64 per ounce

20 Apr: USD 1,340.15, GBP 953.52 & EUR 1,089.14 per ounce

19 Apr: USD 1,347.90, GBP 950.54 & EUR 1,090.59 per ounce

18 Apr: USD 1,346.55, GBP 949.59 & EUR 1,088.95 per ounce

17 Apr: USD 1,342.95, GBP 937.24 & EUR 1,084.57 per ounce

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

Silver Prices (LBMA)

23 Apr: USD 16.94, GBP 12.14 & EUR 13.85 per ounce

20 Apr: USD 17.11, GBP 12.15 & EUR 13.91 per ounce

19 Apr: USD 17.20, GBP 12.09 & EUR 13.91 per ounce

18 Apr: USD 16.95, GBP 11.93 & EUR 13.70 per ounce

17 Apr: USD 16.63, GBP 11.60 & EUR 13.44 per ounce

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

Recent Market Updates

– Family Offices and HNWs Invest In Gold Again

– New All Time Record Highs For Gold In 2019

– Palladium Bullion Surges 17% In 9 Days On Russian Supply Concerns

– Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Movement of earmarked gold and no doubt that the gold is heading to Turkey

(Harvey)

Federal reserve bank of NY earmarked gold departures:

Ted Butler: In interview, CFTC chairman avoids the obvious

Submitted by cpowell on Mon, 2018-04-23 23:58. Section: Daily Dispatches

8p ET Monday, April 23, 2018

Dear Friend of GATA and Gold:

Silver market analyst and manipulation exposer Ted Butler today disparages a self-congratulatory interview done by the chairman of the U.S. Commodity Futures Trading Commission that acknowledges the many complaints about manipulation of the monetary metals markets but never addresses the key issues, like JPMorganChase’s domination of the silver market. Also not addressed is the surreptitious involvement of the U.S. government in these markets, which may explain the CFTC’s uselessness.

Butler’s comments are headlined “Avoiding the Obvious” and are posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/avoiding-obvious-17229

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-avoiding-the-obvious.asp…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Avoiding the Obvious

|

April 23, 2018 – 1:57pm

A new interview by James McDonald, Director of Enforcement for the U.S. Commodity Future Trading Commission (CFTC), on Friday makes it clear that neither he nor the Commission has any intent to address the obvious manipulation of the silver market, conducted principally by JPMorgan. As a reminder, preventing manipulation is the primary mission of the CFTC.

https://www.cftc.gov/ click on podcast April 20, 2018

What you’ll hear is a self-congratulatory review of what a great job the agency is doing in terms of market manipulation in precious metals and how the agency welcomes and takes very serious and always follows up on all allegations to the fullest extent; even offering multi-million dollar rewards under its whistleblower program.

McDonald acknowledged that the agency has received more public complaints on precious metals manipulation (silver specifically) than on any other market and wished to assure the public that the CFTC was diligently protecting it from the evils of price manipulation. It’s true the agency has brought many more cases involving spoofing and other fraudulent acts and for that both McDonald and the Commission should be commended. But both are avoiding the 800 pound gorilla of silver manipulation and JPMorgan standing right in front of them.

So rather than a public interview offering the general assurance that everything is on the up and up in COMEX silver, why not just address the specific issues that have caused so many to believe otherwise? Those issues include excessive speculation on the COMEX, JPMorgan’s perfect trading record and its massive accumulation of physical silver. Why not just pick up the phone and explain to me why I am wrong in my allegations? Or just hit “reply” to any of my more than 100 emails explaining the COMEX scam? That would seem to be the most expedient course of action.

The truth is that no one from the agency has ever inquired, followed up on or challenged any of my allegations. That’s because all my allegations are based upon the agency’s own public data. One would think that this presented a perfect opportunity for the CFTC to prove me wrong and end the allegations of manipulation in silver which, clearly, aren’t going away. Should you choose to encourage the agency to resolve this issue once and for all, I’ve enclosed a letter from Jim Cook, president of IRI, Inc., that he has allowed me to offer as a template.

Ted Butler

April 23, 2018

James McDonald jmcdonald@cftc.gov

Chairman Giancarlo cgiancarlo@cftc.gov

Commissioner Quintenz bquintenz@cftc.gov

Commissioner Behnam rbehnam@cftc.gov

Dear Director McDonald,

I listened to your recent interview on the CFTC podcast. You claim to always respond to questions. This seems disingenuous. You have never responded to claims that JPMorgan has suppressed the price of silver in the futures market while accumulating a large amount of physical silver. Nor have you ever tried to explain how JPMorgan has never taken a loss in silver futures trading but always enjoyed large profits, something that’s impossible in a free market.

Surely you are aware of the enormous increase in commentary on these subjects on the Internet and elsewhere. This groundswell is based on your own CFTC data. You, of course, know that Mr. Butler has written to your agency for years raising the above issues and others regarding the silver market. Why can’t you address these issues? Why does JPMorgan appear to have carte blanche freedom to do whatever it chooses?

It would be a tremendous relief to many thousands of silver producers and silver investors to have you respond to these issues. You are highly regarded and have a reputation for unblemished integrity. Consequently, I am asking you to respond to these questions which are the central issue in the silver market.

Sincerely,

James R. Cook

President

Investment Rarities Inc.

end

Lots of metals market rigging described in federal trial

Submitted by cpowell on Tue, 2018-04-24 17:19. Section: Daily Dispatches

1:20p ET Tuesday, April 24, 2018

Dear Friend of GATA and Gold:

The federal trial of monetary metals market rigging defendant Andre Flotron, financial journalist Allan Flynn reports today, is producing a lot of testimony about market rigging, if not anything yet incriminating Flotron himself. Flynn’s report is headlined “UBS and Deutsche Bank Gold and Silver Traders: ‘We Are ——– Gambling Addicts” and it’s posted at “Comex, We Have a Problem” here:

http://comexwehaveaproblem.blogspot.com.au/2018/04/ubs-and-deutsche-bank…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The trial of the Legend..what a crook!!!

(courtesy Allen Flynn)

You might have guessed precious metals bank trader Kar-Hoe “Mike” Chan, on transfer from the US after completing initial training, had landed in some far flung colonial outpost rather than a bustling Asian financial center.

Under cross examination in court last week at the gold and silver spoofing trial of UBS FX precious metals team manager Andre Flotron, Chan affirmed, as he had told the FBI three years ago, how lonely he had felt after arriving in Singapore in April, 2009.

Early on though, as chance would have it, “at a bar” one evening the banker met Deutsche Bank’s David Liew, coincidentally also a new precious metals trader. Amazingly his new friend’s employer also happened to share the same address as Chan’s, but in a different tower; 1 Raffles Quay in the port city. Presumably, neither had any idea the direction the relationship would take.

The two new friends from the Swiss and German global banking competitors went on to rig gold and silver markets in Singapore with such cooperation, they even imagined amalgamating operations in a “secret agreement” calling themselves “DB-UBS Capital.”

Under cross examination on day two in the spoofing trial of UBS trader Andre Flotron in New Haven Connecticut last week, Flotron’s understudy for two months, Chan, conceded that he and Deutsche Bank trader David Liew, got into “some bad things.”

Taking encouragement from his Singapore regional manager “to talk to other banks,” Chan’s brazen collaboration with Liew didnt care for standard rules of business conduct.

Explaining twice under oath that he was only joking with Liew in chat about working for him, Chan finally agreed with Flotron’s attorney Marc Mukasey that the joke was funny, only because as the banks were competitors, he was “not supposed to be working with him.”

The scenario emerged before the court that Chan had told Liew once in chat “I’m bored,” and that when they next met in the cafeteria he would tell him some “super evil tricks.”

Between quizzing from Mukasey and Perry, it became apparent the witness and Liew had used at least five different methods to defraud the precious metals, including spoofing, front running, “high and low prices,” (collusion in spreads), trading to print, and squeezing shorts. Chan’s leading, in responses that the activities were “common practice” in the industry, were all stuck down by the Court. The accused, Chan’s mentor Flotron, for one reason or another stands trial on only one crime; spoofing.

|

|

US District Courthouse, New Haven,

Connecticut – Wikipedia Image

|

In February, the US District Court Judge, Jeffrey Alker Meyer dismissed six out of seven of Andre Flotron’s superseding charges in favor of maintaining the court’s April schedule. Standing trial on a single charge of spoofing only, it’s unlikely that the 12-strong jury will hear of his wider involvement in the scandal bringing the “overarching conspiracy,” as Judge Meyer put it then, in gold and silver to come into view.

In a pre-trial ruling, the court ordered that evidence of Flotron’s front running would be disallowed with one proviso. Only if defense attorney probed a witness on front running, could the trigger, permitting prosecution to question the defendant on emails between Flotron and Chan about it, be pulled.

Chan and Liew are recorded, in CFTC UBS and Deutsche Bank orders, coordinating front running on numerous occasions in chat. The illegal practice refers to a form of insider trading where privileged client information on pending orders is traded on, for illicit profit.

With court confessions such as; “whenever we had a chance to make money together we would do it,” and multiple chat self-references of, “bandits” normally associated with organized crime, the evidence coming out of Chan’s questioning last week, adds a new dimension to understanding of the slowly emerging big bank scandal in precious metals.

As the duo’s chat, similarly to their trading, showed no regard for discretion; some dark truths surfaced.

Chan’s troubling testimony after the first three days corroborate, with accounts in recent CFTC Orders against UBS, that three others at the bank, were involved in precious metals manipulation. Of the four members of the precious metals foreign exchange team under and including Flotron, located in Singapore, Connecticut and Zurich, three he had either seen or discussed spoofing markets with, giving the traders and their bank the upper hand in round-the-clock trading in gold, silver, platinum and palladium.

In addition the junior trader, who undertook some fourex trading for the bank, named four FX traders previously unmentioned in relation to the global benchmark scandal, with which he had either seen, doing, or discussed currency spoofing at UBS.

Ralf Klonowoski in Zurich, and regional manager Lai Yuk-Nyen, minors trader Francis Koh and pound sterling trader William Ishmael in Singapore, had all at some stage Chan said, worked closely to him at the desk as he moved from Stamford to Singapore in 2009, via Zurich for a week. Two other names were also mentioned in the trial, one in passing, for the first time in relation to the scandal.

Pointing to Chan’s FBI interview notes from April 27, 2015, “right before it says Julius Baer,” Flotron’s lawyer repeatedly asked Chan if he coordinated trading with traders from the Japanese bank, Mitsui. After three questions had fallen flat, Makusey pressed, asking if Chan denied during “the entire two years” he was in Singapore having colluded with traders at Mitsui about “strategy to reach agreements to trade in concert in order to drive market price momentum.” Chan’s flat response was: “I don’t deny it happened; I just don’t recall.” Both, private Swiss bank Julius Baer, and Mitsui have offices in Singapore.

|

| Historic Mitsui Banking Building Tokyo – Wikipedia Image |

The court also heard, on the first day of trial, from expert data analyst Lisa Pinheiro and FBI Special Agent Jonathon Luca, a former precious metals trader at Morgan Stanley who worked on Flotron’s case as they were questioned by defense counsel and attorney for the prosecution.

Warning the jury they would hear a lot about cancellation of orders during the trial, Marc Mukasey for Flotron¸ artfully compared the act of a trader cancelling an order, the final critical step in spoofing, with a customer changing their mind when buying a coke at the store, and putting it back on the shelf.

Appealing again to simple culture, the white collar defense counsel touched on his client’s employment record and the inanimate nature of his supposed spoofing victims. “Andy is not guilty and this trial is a 24 carat mistake,” Mukasey declared, “the only job he ever had was trading gold and silver for UBS bank,” and he traded with “heart,” “feel,” and “curiosity” not against “mom-and-pop investors” but “supercomputers.”

Prosecuting attorney Avi Perry said of Flotron in opening however that he “ripped off other gold and silver traders hundreds of times. And it cost those victims hundreds of thousands of dollars. He wanted a low price, so he forced the market down and he got what he wanted, easy money for him.”

In spoofing, after a real order is placed, a much larger trick order is then put on the other side of the market. Once the real order is filled, the trick order having fooled the market, is quickly withdrawn. Summarizing the four stages of a spoof, of which the defendant is accused, the prosecuting attorney left the jury the catchy mantra;“bid, trick, fill, kill.”

Given the court-placed limits on charges, Chan’s evidence against his mentor Flotron, paled in shock value and scope compared to his own admissions regarding his and his chief cohort’s mischief.

The junior trader described sitting at his mentor’s desk for two months observation and training in precious metals trading at Stamford, Connecticut in 2008, taking handwritten notes and transcribing them diligently onto his laptop at night.

Although the ex-trainee admitted that Flotron had never used the word “spoof” with him, his Swiss trainer and manager, had told him to “trick” rather and, led in spoofing by example. It was, he said, only on his arrival in Singapore that he heard “spoof” being used, as it was, “a lot” at the UBS trading desk there.

A key piece of evidence offered from Chan’s training notes from the start of his training, June 1, 2008 reads according to their author, as Flotron’s guide containing three of four parts of a spoof:

The missing portion of the script,“…” meaning, the junior trader explained, the “dodgy” part of the trade.

After deliberation, the words were deemed admissible by Judge Meyer as a transcription of what Chan wrote after listening to Flotron, rather than truth or verbatim quote from the defendant’s lips.

The slow emergence of facts regarding a gold and silver scandal involving the worlds biggest banks goes back to June, 2013, when Bloomberg news reported that currency traders had been front running client orders and manipulating currency benchmarks. In large banks, precious metals trading is usually conducted alongside FX trading.

After a court break on Wednesday, and Mike Chan’s concluding of evidence on Thursday last week, Andre Flotron’s spoofing trial resumes this week in New Haven, Connecticut.

(courtesy Bloomberg/GATA)

Here come the petrodollars, back to save global asset prices

Submitted by cpowell on Tue, 2018-04-24 12:14. Section: Daily Dispatches

By Tracy Alloway and Sid Verma

Bloomberg News

Tuesday, April 24, 2018

The recent surge in oil prices is poised to boost global assets as crude-producing states deploy replenished stashes of petrodollars, according to a growing chorus of analysts.

It’s the potential reversal of part of the global “quantitative tightening” that was said to have occurred as oil prices dropped precipitously, and could amount to an extra shot of liquidity at a time when central banks are beginning to normalize monetary policy.

“The increase in oil prices is generating a shift in flows and incomes across the world, effectively reversing the previous big shift seen between 2014 and 2016,” wrote JPMorgan Chase & Co. analysts led by Nikolaos Panigirtzoglou. They estimate that energy producers stretching from the Middle East to Norway saw their oil-related revenues plunge from $1.6 trillion in 2014 — when crude reached $115 a barrel — to less than $800 billion in 2016, when it fell to $27.

The drop in oil-related proceeds roiled global markets by cutting off producers’ demand for imported goods and curtailing the ability of big sovereign wealth funds and central banks to buy foreign assets. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-04-24/here-come-the-petrodo..

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3070 /shanghai bourse CLOSED DOWN 60.92 POINTS OR 1.99% / HANG SANG CLOSED UP 381.84 POINTS OR 1.26%

2. Nikkei closed UP 190.08 POINTS OR 0.86%/ /USA: YEN RISES TO 108.81/

3. Europe stocks OPENED RED/MIXED /USA dollar index FALLS TO 90.88/Euro RISES TO 1.2213

3b Japan 10 year bond yield: FALLS TO . +.058/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.81/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.03 and Brent: 74.73

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.631%/Italian 10 yr bond yield UP to 1.801% /SPAIN 10 YR BOND YIELD UP TO 1.3181%

3j Greek 10 year bond yield FALLS TO : 4.006?????????????????

3k Gold at $1326.05 silver at:16.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 61/66

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.81 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9777 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1943 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.625%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.9677% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1344% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Jump As Treasuries Rebound; China Surges On PBOC Easing Rumors

If the big story yesterday was the surge in 10Y TSY yields to just shy of 3.00% (2.996% to be precise), then it is only reasonable that the failure of the 10Y yield to rise above 3.00% overnight is today’s “big story”, and indeed as shown in the chart below, US benchmark treasuries edged higher, leading most European government bonds, as traders hit pause on the rates selloff amid extremely oversold conditions.

“The U.S. yield spike story has been a theme for the last 24 hours but we don’t expect a sharp surge as the U.S. continues to be in a late economic cycle,” said Danske Bank FX strategist Christin Tuxen.

Recall that just as investors are curious what happens once yields breach 3.00%, so they want to know how low they could drop if the 10Y fails to penetrate the key level for the 2nd time in 2 months, a question which Morgan Stanley yesterday answered, saying the next stop could be a reversal back to 2.70%. And while we wait to see what happens next, the Treasury curve flattened slightly as the 2-year sector underperformed ahead of today’s supply.

Traders have been weighing the implications of climbing bond yields that were in part spurred by higher commodity prices and concern surrounding their inflationary impact on the wider economy. But, as noted yesterday, so far the volatility in interest-rate markets remains low and equity price swings are well off the highs seen earlier this year, indicating investors believe rising borrowing costs may not be enough to cause outsized pain to equities, for now.

“For us it’s more the reasons why we’re seeing the move: better growth outlook, a little bit more inflation and faster rate hikes being priced in by the market,” Kerry Craig, a JPM Asset Mgmt strategist told Bloomberg TV. “It should be reaffirming the fact that we see a global economy that’s looking relatively healthy.”

The bid for bonds, together with strong earnings from Google overnight, helped restore risk sentiment, and global equity markets steadied overnight, with European stocks climbing following gains for most Asian markets as the earnings season picked up steam while Chinese equities soared (Shanghai Comp +2%) following an overnight report from the China Securities Journal that liquidity tensions in China may ease while fiscal spending will increase this week; speculation of further easing from Beijing re-emerged with subsequent similar reports of RRR cuts follow in European morning.

After hugging the flatline, US equity futures enjoyed a burst of buying as Europe came online, sending the E-Mini to session highs, up 0.6%, or 16.00 points, to 2,687, and above yesterday’s highs.

Meanwhile, WTI oil, which according to many has been a key driver behind the move in both bonds and FX, continued grinding higher, rising above $69 overnight, the highest price since late 2014. Still, keep in mind that just as the oil surge propelled risk, and inflation sentiment, so a sharp spike in oil from here could lead to renewed market volatility according to Deutsche Bank.

“It is this move higher in crude oil prices, along with the rise in demand, that is helping fuel the recent rise in yields as well as the positive tone for equity markets,” said Michael Hewson, chief market analyst at CMC Markets in London. “However if it continues too far we could start to see it act as a drag on equity markets, if prices along with yields start to move even higher.”

After yesterday’s furious short squeeze which sent the dollar soaring the most since the election, the USD steadied in the last few hours as traders focused on whether take-profit interest will emerge after the latest gains or macro bids are enough to support the rally. As a result, the dollar was little changed at about its highest level since January.

Meanwhile, the yen decline continued, helping spur Japan’s Topix index to the highest in almost two months; similarly in Europe, the EUR dropped below the 1.22 handle as positioning ahead of the ECB meeting favors downside exposure, while the pound briefly slipped to a fresh one-month low. Australia’s dollar was sold in a knee-jerk reaction to a headline inflation miss before erasing declines as investors were encouraged by the improvement in the core measure, while the New Zealand dollar fell against all Group-of-10 peers after leveraged funds liquidated long positions. Still, don’t read too much into today’s moves as volumes are below Monday already depressed levels in the FX market.

Looking at equity markets, European stocks opened broadly higher with blue-chip stock markets in London and Frankfurt 0.3 percent higher. Markets brushed off further signs that Europe’s biggest economy Germany is losing some of its momentum, with the Ifo business climate index falling in April to 102.1 from 114.7, missing estimates of 102.6. SAP, Europe’s largest tech company by stock market valuation, announced upbeat results in the seasonally tough first quarter. However, Chipmaker AMS reported first-quarter sales towards the lower end of its guidance range on Monday and warned of a downturn owing to weaker orders from one of its main customers.

Earlier, Chinese stocks lead Asian indexes higher after Monday’s Politburo meeting and state-backed newspaper commentary signaled liquidity conditions will improve; Shanghai Composite rose 2%, with H shares 1.9% higher. As noted above, China roared higher amid press reports that China has further room to cut RRR and is likely to ease liquidity tension this week.

The MSCI Asia Pacific index advanced 0.4%, with Rusal shares rising by around 30% in Hong Kong on hopes of sanction relief, while the blue-chip energy and property names led the upside in the Hang Seng. Still, there remained pressure on technology shares in Asia after a slew of companies reported disappointing earnings. The Philadelphia Semiconductor Index is down more than 7 percent over the past four days.

In commodities, aluminum extended its biggest slump since 2005 after slumping 7% on Monday when the U.S. Treasury Department signaled it may lift United Co. Rusal sanctions if Oleg Deripaska divests control of the company. Three-month aluminum on the London Metal Exchange CMAL3 last stood at $2,255 per tonne. Rusal shares in Hong Kong posted their biggest-ever gain. AS noted above, West Texas oil rose above $69 a barrel amid flaring geopolitical tensions in the Middle East and expectations for a decline in U.S. crude stockpiles.

On today’s calendar, we have data on new home sales, Case Shiller home prices, and Conference Board consumer confidence index. Amgen, Biogen, Caterpillar, Coca-Cola, Eli Lilly, Lockheed Martin, NextEra Energy, and Verizon are reporting earnings

Bulletin Headline Summary from RanSquawk

- European equities opened on the backfoot, but have seen more choppy trade since (Eurostoxx 50 flat) amid relatively light newsflow thus far

- DXY has cleared another key upside technical level amidst more widespread Dollar gains and has also eclipsed 91.000.

- Looking ahead, highlights include, US consumer confidence, housing data, APIs, and a slew of speakers

Market Snapshot

- S&P 500 futures up 0.6% to 2,687.00

- STOXX Europe 600 up 0.2% to 383.94

- MSCI Asia up 0.4% to 173.37

- MSCI Asia ex Japan up 0.2% to 563.99

- Nikkei up 0.9% to 22,278.12

- Topix up 1.1% to 1,769.75

- Hang Seng Index up 1.3% to 30,636.24

- Shanghai Composite up 2% to 3,128.93

- Sensex up 0.4% to 34,591.49

- Australia S&P/ASX 200 up 0.6% to 5,921.55

- Kospi down 0.4% to 2,464.14

- German 10Y yield fell 2.1 bps to 0.615%

- Euro down 0.1% to $1.2197

- Italian 10Y yield rose 1.6 bps to 1.54%

- Spanish 10Y yield fell 0.9 bps to 1.304%

- Brent futures up 0.2% to $74.87/bbl

- Gold spot up 0.2% to $1,327.60

- U.S. Dollar Index little changed at 90.95

Top Overnight News

- German Chancellor Angela Merkel is traveling to the U.S. this week to meet President Donald Trump in an effort to prevent trade war

- German business confidence continued to slide in April as companies’ qualms over a potential trade war coincided with economic data signaling the country’s growth momentum may have peaked

- U.S. Treasury threw a potential lifeline to United Company Rusal by making clear it’s not pushing for the company’s collapse. Treasury Secretary Mnuchin said it was considering a request to lift the sanctions against the company

- Australia’s consumer prices rose less than forecast in the first quarter, suggesting the central bank will keep rates on hold

- Oil extended gains toward $69 a barrel as tensions in the Middle East flared up and U.S. crude stockpiles were seen falling a second week. Saudi Arabia intercepted ballistic missiles fired by Iran-backed Houthis in Yemen

- Germany wants to help U.K. banks get access to the European market after Brexit, but would need Britain to make concessions, according to a person familiar with the German government’s position

- Pound’s resurgence in recent months may affect the Bank of England’s outlook for price gains in next month’s Inflation Report, complicating the case for an immediate rate hike

- Britain was in surplus on its day-to-day budget for the first full fiscal year since the early 2000s, a milestone that is almost certain to revive calls for an end to austerity

- An unprecedented downgrade of Poland’s investment growth is forcing a reassessment of the European Union’s largest eastern economy, with the amended data showing last year actually ended on a slight slowdown

- Takeda Pharmaceutical Co. is nearing a preliminary agreement to acquire Shire Plc after the Japanese drugmaker sweetened its roughly $60 billion bid for the biotechnology behemoth, according to people with knowledge of the matter

Asia-Pac stock markets were mostly in the green with an improvement in tone seen in comparison to the lacklustre performance on Wall St where rising yields and declines in basic materials dampened sentiment. ASX 200 (+0.6%) and Nikkei 225 (+0.9%) traded positive with Australia supported by gains in financials and energy names, while Japanese exporters benefited from a weaker JPY. Elsewhere, Shanghai Comp. (+0.9%) and Hang Seng (+1.3%) outperformed after a mild net liquidity injection by the PBoC, as well as press reports that China has further room to cut RRR and is likely to ease liquidity tension this week. Furthermore, Rusal shares rose by around 30% in Hong Kong on hopes of sanction relief, while the blue-chip energy and property names led the upside in the Hang Seng. Finally, 10yr JGBs were relatively uneventful with demand subdued amid the improvement in risk appetite, although downside was also limited as USTs nursed losses and following a relatively uneventful 2yr auction. China has additional room to reduce RRR and repay maturing Medium-term Lending Facility loans, while it is also likely to ease liquidity tension during the week, according to reports. (China Securities Journal)

Top Asian News

- Singapore’s Shelved IPOs Pile Up as Summit, Qualitas Struggle

- China Concerned Trade and Debt Risk May Curb Economic Growth

- Saudis Said to Delay Bourse IPO on Hope MSCI Will Lift Valuation

- Hong Kong Approves Dual-Class Shares, Paving Way for Tech Titans

European equities opened on the backfoot, but have seen rebounded in the green amid relatively light newsflow thus far. Looking at the sectors, energy names are outperforming amid the rise in oil prices. Telecom names lag behind with Telenor (-2.5%) weighing on the sector following weak earnings. In terms of stock specifics, William Hill (-14.0%) are at the foot of the Stoxx 600 after reports that UK Chancellor Hammond has accepted the proposal for GBP 2 fixed-odd betting terminals limit. Semi-conductor names took a hit following earnings from AMS (-9.0%) with Dialog Semiconductors (-6.0%) and STMicroelectronics (-1.6%) lower in sympathy. On the flip side SAP (+3.2%) shares are higher post-earnings while BP (+1.4%) shares are fuelled by an upgrade at Goldman Sachs.

Top European News

- Stronger Pound May Give BOE Hawks Further Pause for Thought

- German Business Confidence Extends Drop as Economic Data Weakens

- U.K. Balances Day-to-Day Budget for First Time Since 2001-02

- Mercedes Tests Billionaires’ Appetite for Maybach With Crossover