GOLD: $1322.40 DOWN $ 14.00 (COMEX TO COMEX CLOSINGS)

Silver: $16.64 DOWN 50 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1324.70

silver: $16.66

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR 673 FOR 67300 OZ (2.0933 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 461 for 2,305,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8860/OFFER $8960: up $377(morning)

Bitcoin: BID/ $8877/offer 8976: UP $343 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1341.50

NY price at the same time: 1334.50

PREMIUM TO NY SPOT: $7.00

ss

Second gold fix early this morning: 1338.36

USA gold at the exact same time: 1333.80

PREMIUM TO NY SPOT: $4.56

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A SMALL 410 CONTRACTS FROM 221,913 FALLING TO 221,503 ACCOMPANYING FRIDAY’S SMALL 11 CENT LOSS IN SILVER PRICING. AFTER A STRING OF 4 CONSECUTIVE OI GAINS, WE FINALLY REGISTER A SMALL DROP. WE WERE AGAIN NOTIFIED THAT WE HAD AN HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP :120 EFP CONTRACTS FOR APRIL, 3354 EFP’S FOR MAY , 149 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 3623 CONTRACTS. WITH THE TRANSFER OF 3623 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3623 EFP CONTRACTS TRANSLATES INTO 18.115 MILLION OZ ACCOMPANYING 1.THE FALL IN SILVER PRICE (11 CENTS) AT THE COMEX AND 2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

56,764 CONTRACTS (FOR 16 TRADING DAYS TOTAL 56,764 CONTRACTS) OR 283.82 MILLION OZ: AVERAGE PER DAY: 3,547 CONTRACTS OR 17.738 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 283.82 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 40.54% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1.001.95 BILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A TINY SIZED FALL IN COMEX OI SILVER COMEX OF 410 ACCOMPANYING THE SMALL 11 CENT LOSS IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD AN HUMONGOUS SIZED EFP ISSUANCE OF 3623 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 120 CONTRACTS WERE ISSUED FOR APRIL, 3354 EFP’S WERE ISSUED FOR THE MONTH OF MAY, AND 149 EFP CONTRACTS FOR JULY, FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 3623). WE GAINED A STRONG 3213 OI CONTRACTS ON THE TWO EXCHANGES: i.e. 3623 open interest contracts headed for London (EFP’s) TOGETHER WITH AN DECREASE OF 410 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE SMALL FALL IN PRICE OF SILVER OF 11 CENTS AND A CLOSING PRICE OF $17.14 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by WELL OVER 1 BILLION oz i.e. 1.107 BILLION TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 5 NOTICE(S) FOR 25,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY 4601 CONTRACTS DOWN TO 514,852 ACCOMPANYING THE FALL IN PRICE/FRIDAY’S TRADING ( DROP OF $10.20). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 11,451 CONTRACTS : JUNE SAW THE ISSUANCE OF 11,451 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 514,852. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A LARGE SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 4601 OI CONTRACTS DECREASED AT THE COMEX AND AN GIGANTIC SIZED 11,451 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 6850 CONTRACTS OR 685,000 OZ = 21.30 TONNES.

FRIDAY, WE HAD 15,381 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 175,887 CONTRACTS OR 17,588,700 OZ OR 547.70 TONNES (16 TRADING DAYS AND THUS AVERAGING: 10,992 EFP CONTRACTS PER TRADING DAY OR 1,099,200 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 16 TRADING DAYS IN TONNES: 547.7 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 547.70/2550 x 100% TONNES = 21.47% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,592.50 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN DECREASE IN OI AT THE COMEX OF 4610 WITH THE FALL IN PRICE // GOLD TRADING FRIDAY ($10.20 DROP). WE ALSO HAD A GIGANTIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,451 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,451 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED NET GAIN OF 6850 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,451 CONTRACTS MOVE TO LONDON AND 4601 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 21.30 TONNES).

we had:198 notice(s) filed upon for 19800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $14.00 : WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 865.89 tonnes.

SLV/

WITH SILVER DOWN 50 CENTS TODAY: ANOTHER HUGE CHANGE/ A WITHDRAWAL OF 1.413 MILLION OZ/

/INVENTORY RESTS AT 315.298 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY 410 CONTRACTS from 221,913 UP TO 221,503 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AFTER WE HAVE HAD FOUR CONSECUTIVE OI GAINS WE FINALLY HAVE A DROP. OUR BANKERS ALSO USED THEIR EMERGENCY PROCEDURE TO ISSUE: 120 EFP CONTRACTS FOR APRIL, 3354 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 149 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 3623 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 26 CONTRACTS TO THE 3623 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 3213 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.065 MILLION OZ!!! AND THIS OCCURRED WITH A SMALL FALL IN PRICE OF 11 CENTS. THE BANKERS ORCHESTRATED THEIR RAID TODAY AS THEY DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE FALL IN SILVER PRICING / FRIDAY (11 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 3623 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 3.53 POINTS OR 0.11% /Hang Sang CLOSED DOWN 163.93 POINTS OR 0.54% / The Nikkei closed DOWN 74.20 POINTS OR 0.33%/Australia’s all ordinaires CLOSED DOWN .19% /Chinese yuan (ONSHORE) closed DOWN at 6.3079/Oil DOWN to 68,13 dollars per barrel for WTI and 73.98 for Brent. Stocks in Europe OPENED RED. ONSHORE YUAN CLOSED DOWN AT 6.3079 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3020/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/

Kim seeks peace and will abandon nuke testing:

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

CHINA

Sorghum which arrived in China was immediately turned away after the huge 200% tariff imposed on it

( zerohedge)

4. EUROPEAN AFFAIRS

What an absolute joke: the ECB refuses to tackle their huge Non Performing Loan debacle:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

The rhetoric between Iran and Israel intensifies

( zerohedge)

ii)Iran

Iran warns the rest of the world that there is no plan B. They must encourage Trump to endorse it. If not then the Iran deal is shredded.

( zerohedge)

iii)Iran is having great difficulty obtaining dollars..so they now switch to Euros. Do not know how this will help them

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Movement of earmarked gold and no doubt that the gold is heading to Turkey

(Harvey)

ii)Officially Venezuela has only 5 million oz left but they have also done major swaps with Citibank so all of their gold has been technically sold for needed dollars

iii)The New York Fed nominee Williams does not think that bitcoin has the qualities for currency.( Cox/CNBC)

iv)Seems Russia is probably the only sane nation out there other than China as they keep all of its gold reserves at home

(Russia Today/Moscow/GATA)

v)Gold Money concludes that we have had relentless selling pressure in the futures market. He notes that huge suppression in silver prices but he also opinion that silver is on the verge of a breakout. As far as I am concerned, the breakout will only occur when London runs out of metal.

( GoldMoney/GATA)

vi)Eric Sprott talking to Craig Hemke and wonders if we are closer to a short squeeze in both gold and silver

( Sprott Money/Craig Hemke)

10. USA stories which will influence the price of gold/silver

A)Trading this morning:

shorts are crushed!!

i)Every month we see two soft data PMI reports, the ISM and Markit. Markit is always bullish . Today was no exception as the Markit PMI showed a Q2 rebound totally opposite to the iSM

( zerohedge)

ii)The Mexican Peso hits one month lows as Trump may tie immigration crackdown to NAFTA

( zerohedge)

iii)Existing home sales rebound from last month, but on a yearly basis it is still registering downward

( zerohedge)

iv)SWAMP STORIES

a)Sessions threatens to quit if Trump fires Rosenstein. Sessions is deep state (even though Republican)

( zerohedge)

b)The fun continues as now Wikileaks counter sues the Democrats. Now everything will be on the table: discovery is going to be a dandy!

c)Assange twitter account returns as the campaign for funds commences:

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:278,909 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 302,056 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY 410 CONTRACTS FROM 221,659 UP TO 221,503 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 11 CENT FALL IN SILVER PRICING. WE ALSO WERE ALSO INFORMED THAT WE HAD A 120 EFP CONTRACTS ISSUED FOR APRIL, 3354 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS, AND 149 EFP CONTRACTS ISSUED FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 3623. ON A NET BASIS WE GAINED 3213 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 410 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 3623 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 3213 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month GAINED 124 contracts RISING TO 146 contracts. We had 1 notices filed upon so in essence we GAINED 125 contracts or 625,000 additional ounces of silver will stand for delivery in this non active delivery month of April .

The next big active delivery month for silver will be May and here the OI LOST 9760 contracts DOWN to 85,100. June saw a LOSS of 185 contracts to stand at 174. The next big delivery month for silver is July and here the OI ROSE by 8204 contracts UP to 96,612.

We had 5 notice(s) filed for 25,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 23/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

128.604 OZ

Brinks

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

198 notice(s)

19800 OZ

|

| No of oz to be served (notices) |

629 contracts

(62,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

871 notices

87100 OZ

2.709 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 198 contract(s) of which 193 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (871) x 100 oz or 67300 oz, to which we add the difference between the open interest for the front month of APRIL. (827 contracts) minus the number of notices served upon today (198 x 100 oz per contract) equals 150,100 oz, the number of ounces standing in this active month of APRIL (4.668 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (871 x 100 oz or ounces + {(827)OI for the front month minus the number of notices served upon today (198 x 100 oz )which equals 150,100 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 1 COMEX OI CONTRACTS OR 100 OZ OF GOLD WILL STAND

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

4,882.910 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

58,262.700 oz

CNT

|

| No of oz served today (contracts) |

5

CONTRACT(S)

(25,000 OZ)

|

| No of oz to be served (notices) |

139 contracts

(695,000 oz)

|

| Total monthly oz silver served (contracts) | 466 contracts

(2,330,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) INTO CNT: 58,262.700 OZ

total deposits today: 58,262.700 oz

we had 2 withdrawals from the customer account;

i) out of Brinks: 964.810 oz

ii) Out of Delaware: 3918.100 oz

total withdrawals; 4,882.910 oz

we had 0 adjustment

i

total dealer silver: 62.576 million

total dealer + customer silver: 261.751 million oz

The total number of notices filed today for the APRIL. contract month is represented by 5 contract(s) FOR 25,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 466 x 5,000 oz = 2,330,000 oz to which we add the difference between the open interest for the front month of April. (146) and the number of notices served upon today (5 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 466(notices served so far)x 5000 oz + OI for front month of April(146) -number of notices served upon today (146)x 5000 oz equals 3,025,000 oz of silver standing for the April contract month

WE GAINED 125 SILVER CONTRACT OR 625,000 ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

CRIMINALS!!

ESTIMATED VOLUME FOR TODAY: 188,092 CONTRACTS (WOW) 940 MILLION OZ OR 134% OF ANNUAL PRODUCTION.

CONFIRMED VOLUME FOR YESTERDAY: 130,388 CONTRACTS (my goodness)

YESTERDAY’S CONFIRMED VOLUME OF 130,388 CONTRACTS EQUATES TO 651 MILLION OZ OR 93.13% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.77% (APRIL 23/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (APRIL 23/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.77%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.10%: NAV 13.71/TRADING 13.41//DISCOUNT 2.10.

END

And now the Gold inventory at the GLD/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 23/2018/ Inventory rests tonight at 865.89 tonnes

*IN LAST 366 TRADING DAYS: 75.15 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 316 TRADING DAYS: A NET 81.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 23/2018: A BIG CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ

Inventory 315.298 million oz

end

6 Month MM GOFO 2.04/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.04%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .47%

XXXXXXXX

12 Month MM GOFO

+ 2.76%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.26

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

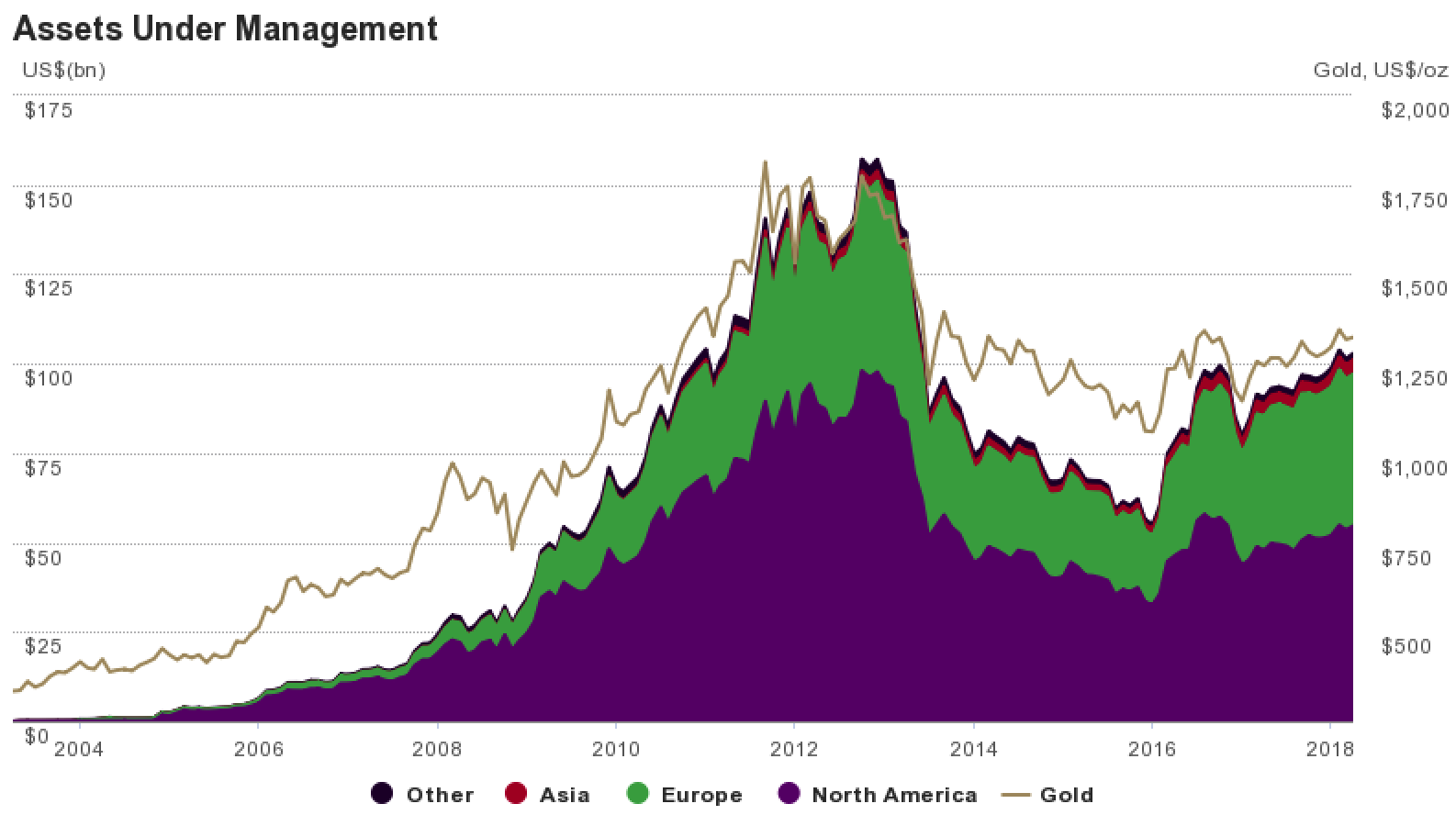

Family Offices and HNWs Invest In Gold Again

Family Offices and HNWs Are Investing In Gold Again

– Rising interest by family offices and high-net-worth (HNW) into gold bullion investments

– Gold ETF assets have reached almost $100 billion due to HNWs and pension funds’ increased demand

– Volatility in equities, concerns over trade wars, Trump’s Presidency and other economic worries are spurring demand for gold coins and bars

– Prudent money ‘trickle’ back into gold as investors are reminded of gold’s insurance qualities

– Gold investment ‘indemnifications’? Gold should not be overcomplicated

– Family offices and high net worth (HNWs) should hold gold for wealth preservation and protection during downturns

Editor: Mark O’Byrne

Gold exchange traded funds (ETFs) have seen assets increase to £100 billion as investors, including family offices and high net worth (HNWs) investors look to the precious metal to preserve wealth in the face of volatile markets and heightened economic geopolitical tensions and uncertainty.

Family offices and high net worth (HNWs) investors are again looking to protect their wealth by diversifying into gold ETFs and physical gold bullion after many exited the safe haven asset after gold’s unexpectedly poor performance from 2013 to 2015.

Gold ETFs famously held about $150 billion in assets in 2012 following the bull market in gold. Since then such investments have fallen out of favour as family offices and HNWs have looked elsewhere for returns.

In contrast to the period leading up to 2012, we are not seeing a sudden rush back into gold ETFs, but what can best be described as a slow but steady and rising trickle as asset levels return to around $100 billion. Similarly with gold bullion, leading specialists such as GoldCore who cater to HNW and family offices, are seeing a rising tide of interest from this important niche sector.

Uncertainty from every angle

This steady trickle comes courtesy of multiple geopolitical situations which have caused a significant amount of uncertainty and volatility in financial markets. This uncertainty is likely to continue as there are uncertainties on both the long and short-term horizon which will continue to make investors, retail and HNW, nervous.

Since the start of the year each of the major regions have seen an increase in gold ETF holdings. This is because of gold’s recent strong price performance and courtesy of Trump, Brexit and heightened geo-political risk which will affect UK, U.S. and investors internationally.

Short-term issues such as Trump’s trade announcements, Brexit updates and the global reaction to events in Syria and the Middle East are leading more risk investors to seek out safe-havens.

Longer-term concerns over global inflation, interest rates, pension deficits and the ‘next’ subprime crisis or wider debt crisis will be playing on the back of some investors’ mind, uncertain how such events will unfold and their likely impact on risk assets – stocks and bonds.

Europe and North America are seeing strong demand and hold similar levels of gold holdings – 90% of the total gold ETFs. Such gold products have not proven to be as successful in the likes of Middle Eastern and Asian countries where holding gold is seen as something which must be done directly and without counter party risk. This makes physical gold coins and bars much more popular in the majority of the world – especially China and India.

Given gold’s role as a wealth preserver for the last 2,000 years or more it is obvious why those looking to protect their wealth would return to this traditional asset class. What is perhaps less clear is why many western investors would choose to invest in what is really a very simple asset via a complicated investment product structure, such as an exchange traded fund (ETF).

Gold investment indemnifications? Gold should not be overcomplicated

There are a number of different options when it comes to gold investment. When looking at how to invest in gold one needs to consider the safe haven asset’s security and liquidity.

As we explain in our Essential Family Office Guide to Investing in Gold, exchange traded funds may or may not be backed by physical gold holdings and some of those that do hold gold contain complex stipulations on convertibility of ETF shares into bullion and very high levels of indemnification. This includes indemnification from many of the key risks that many gold investors own gold in order to hedge against – such as theft, custodian risk, bank risk and systemic risk.

Investors looking for wealth protection will be better served, if they invest in gold with an independent gold provider that enables them to store and access their gold directly through specialist third party storage providers. Gold storage should be in a non bank facility, with insurance and in the stablest and safest jurisdictions.

By managing their gold investment this way investors are ensuring that they have full title to their gold bars, which can be sold at any time and to any gold broker internationally. This ensures liquidity and competive pricing and removes dependence one single gold broker and their staff, IT, servers, website platforms etc.

The decision to invest in gold is one that is based on the investor looking to benefit from the qualities offered by tangible physical gold, as well as performance and returns. Given that owning physical bullion and opting for allocated and segregated storage is only marginally more expensive than getting exposure in the ETF, it behooves all family offices and HNWs to consider ownership of physical gold rather than ETFs. Indeed, financial and pension advisers and brokers who believe in a fiduciary duty should give serious consideration to the benefits of outright ownership of gold bars.

With an ETF, one gets exposure to the gold price, with gold bars in allocated and segregated storage you are guaranteed (even in worst case scenarios) that, but more importantly you also have actual financial insurance, a valuable hedge and an essential wealth preservation asset that will protect and grow wealth in the coming years.

Read our popular Family Office Guide to Investing in Gold.

Related reading

Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube above

News and Commentary

Dollar edges higher, bolstered by rising U.S. yields (Ruters.com)

Asia Stocks Trade Mixed; Yen Slips as Bonds Slide (Bloomberg.com)

Fed’s Williams sees more rate hikes, not worried on yield curve (Reuters.com)

Global Yield Surge Defies Skepticism on Inflation’s Momentum (Bloomberg.com)

Image source Visual Capitalist

Gold Has A High Probability Of Hitting $1500 This Year: Holmes (Bloomberg.com)

Venezuela’s Gold Liquidation Accelerates; Will Be Out Of Gold In One Year (ZeroHedge.com)

Citi: “2018 Is Not Going To Plan” (ZeroHedge.com)

The Pension Time Bomb: $400 Trillion by 2050 (VisualCapitalist.com)

Why Countries Pull Out Their Bullion From the US (SputnikNews.com)

Gold Prices (LBMA AM)

20 Apr: USD 1,340.15, GBP 953.52 & EUR 1,089.14 per ounce

19 Apr: USD 1,347.90, GBP 950.54 & EUR 1,090.59 per ounce

18 Apr: USD 1,346.55, GBP 949.59 & EUR 1,088.95 per ounce

17 Apr: USD 1,342.95, GBP 937.24 & EUR 1,084.57 per ounce

16 Apr: USD 1,344.40, GBP 941.21 & EUR 1,087.62 per ounce

13 Apr: USD 1,340.75, GBP 938.93 & EUR 1,087.35 per ounce

12 Apr: USD 1,345.90, GBP 951.01 & EUR 1,090.99 per ounce

Silver Prices (LBMA)

20 Apr: USD 17.11, GBP 12.15 & EUR 13.91 per ounce

19 Apr: USD 17.20, GBP 12.09 & EUR 13.91 per ounce

18 Apr: USD 16.95, GBP 11.93 & EUR 13.70 per ounce

17 Apr: USD 16.63, GBP 11.60 & EUR 13.44 per ounce

16 Apr: USD 16.60, GBP 11.61 & EUR 13.42 per ounce

13 Apr: USD 16.51, GBP 11.57 & EUR 13.40 per ounce

12 Apr: USD 16.66, GBP 11.74 & EUR 13.50 per ounce

Recent Market Updates

– New All Time Record Highs For Gold In 2019

– Palladium Bullion Surges 17% In 9 Days On Russian Supply Concerns

– Silver Bullion Remains Good Value On Positive Supply And Demand Factors

– London House Prices See Fastest Quarterly Fall Since 2009 Crisis

– Global Debt Bubble Hits New All Time High – One Quadrillion Reasons To Buy Gold

– Oil Surges Over 8%, Gold and Silver Marginally Higher, Stocks Gain In Volatile Week

– EU and Euro Exposed To Risks Including Trade Wars and War With Russia In Middle East

– Trump Tweets Russia “Get Ready” For Missiles In Syria – Gold, Oil Rise and Stocks Fall

– Private: EU and Euro Exposed To Trade Wars, Energy Dependence, Anti-EU and Anti-Euro Movements

– Trump Making ‘Major Decisions’ on Syria, Iran and Russia Response ‘Very Quickly’

– Gold Out Performs Stocks In 2018 and This Century By Ratio Of Two To One

– Jamie Dimon Warns Of Potential ‘Market Panic’

– Silver Bullion: Should We Be Worried About Silver?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Movement of earmarked gold and no doubt that the gold is heading to Turkey

(Harvey)

Federal reserve bank of NY earmarked gold departures:

Venezuela’s Gold Liquidation Accelerates; Will Be Out Of Gold In One Year

On Friday, Turkey unveiled its latest unorthodox financial surprise, when a local newspaper reported that Ankara will repatriate all of its gold held at the NY Fed. The stated reason: an attempt to circumvent the dollar. “Why do we make all loans in dollars? Let’s use another currency” said Turkey’s president Recep Tayyip Erdogan during a speech at the Global Entrepreneurship Congress in Istanbul on April 16, according to Hurriyet. “I suggest that the loans should be made based on gold.”

In what some saw an appeal for a gold standard by the Turkish president and a bid to sever ties with the US Dollar, Erdogan added that “with the dollar the world is always under exchange rate pressure. We should save states and nations from this exchange rate pressure. Gold has never been a tool of oppression throughout history.”

While Erdogan may have had honest, and even noble, intentions (yes, one can smirk here) it is worth noting that Turkey is hardly the first country to demand its gold back from western nations, having been preceded in recent years by Germany, Austria and the Netherlands.

But the most notable, and ominous for the people of Turkey, example of gold repatriation is also the first one in the post-crisis period, when Venezuela’s then-leader Hugo Chavez demanded all Venezuela gold located in offshore central banks be returned to the motherland. At the time, Chavez said he did it for the people, and since he died shortly after, there was no way to gauge what his real intentions were.

The problem is what happened later.

Conveniently, last week Russ Dallen of Caracas Capital wrote inform his clients what Venezuela has been doing over the course of the past several years regarding is repatriated, and now swiftly dwindling gold reserves.

In September 2011, Venezuela had $21.269 billion in gold reserves. After a rash of selling gold in Switzerland to pay bonds maturities and coupons in early 2016 (which we tracked assiduously and reported on in these reports), Venezuela’s gold reserves had fallen to $7.7 billion where they held steady until November 2017. But as we reported in October of 2017, there were loans backed by gold that Venezuela had taken out that were coming due. As we reported last month, in the last two months of 2017, Venezuela had lost $1.1 billion in gold and reported that they held $6.6 billion in gold on December 31. In January, Venezuela’s gold reserves fell another $500 million.

As of January 31, Venezuela had just $6.1 billion in gold reserves, down another half billion from the $6.6 billion Venezuela reported a month earlier on December 31. In short, Venezuela burned through $1.6 billion of its gold reserves in 3 months, and it is important to note that this fall in gold reserves is without Venezuela paying its bond debts.

Here is a chart of the recent declines in Venezuela’s gold…

… and the dramatic plunge in the past 2 years in context.

As Dennis Gartman summarized in his Friday letter to clients, “at the current pace of sales, Venezuela will effectively be out of gold by May or June of next year. Having fallen from $21.3 billion seven years ago, it’s now down to $6.6 billion as of the end of January and we suspect that it’s sold another billion since then.” His conclusion:

“The trend is clear; “The Seller” is almost sated.”

He certainly is, and soon the world’s poorest socialist paradise will also have no gold left unleashing the final stage of Venezuela’s social collapse. Still, one wonders who is on the other side of the trade, and is so eagerly buying all the gold Venezuela has to sell.

Meanwhile, we hope Venezuela’s tragic experience with its soon-to-be-vaporized physical gold which was converted to paper money so Venezuela could repay the country’s debts to the west will be a lesson to the people of Turkey: keep a close eye on what Erdogan is about to do with the people’s gold. If the “president for life” follows in Maduro’s footsteps, Turkey’s gold will soon be gone, all 591 tonnes of it.

end

The New York Fed nominee Williams does not think that bitcoin has the qualities for currency.

(courtesy Cox/CNBC)

NY Fed nominee faults bitcoin for lacking elasticity and central bank sponsorship

Submitted by cpowell on Sat, 2018-04-21 12:57. Section: Daily Dispatches

But isn’t that the point of cryptocurrency — and gold?

* * *

Likely New York Fed President Says Bitcoin ‘Doesn’t Pass the Basic Test’ for a Currency

By Jeff Cox

CNBC, New York

Friday, April 20, 2018

The central banker expected to be the next head of the New York Fed doesn’t think much of bitcoin and other cryptocurrencies.

“Cryptocurrency doesn’t pass the basic test of what a currency should be,” John Williams, currently the head of the San Francisco Fed but the nominee for the top slot in New York, said during a speech today

Eric Sprott talking to Craig Hemke and wonders if we are closer to a short squeeze in both gold and silver

(courtesy Sprott Money/Craig Hemke)

Eric Sprott’s weekly review: Closer to a short squeeze in metals?

Submitted by cpowell on Sat, 2018-04-21 13:06. Section: Daily Dispatches

9:06a ET Saturday, April 21, 2018

Dear Friend of GATA and Gold:

Reviewing this week’s market action, mining entrepreneur Eric Sprott and Craig Hemke of Sprott Money News discuss the seemingly growing possibility of a short squeeze in the monetary metals. Their discussion is 13 minutes long and can be heard at Sprott Money here:

https://www.sprottmoney.com/Blog/if-your-systems-going-to-crash-you-want…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Seems Russia is probably the only sane nation out there other than China as they keep all of its gold reserves at home

(Russia Today/Moscow/GATA)

Russia says it keeps all its gold reserves at home

Submitted by cpowell on Sat, 2018-04-21 13:11. Section: Daily Dispatches

Russia Entrusts Its Gold to No One, has Zero Bullion in U.S.

From Russia Today, Moscow

Saturday, April 21, 2018

The Central Bank of Russia keeps all its bullion at home, since only in Russia can its gold be completely safe, according to Anatoly Aksakov, the chairman of the State Duma Committee on Financial Markets.

Answering a question about Turkey’s decision to repatriate its gold from the U.S. Federal Reserve, Aksakov said: “We do not have a gold reserve in the United States. We have only foreign exchange reserves abroad. No one can lay hands on our gold.” …

… For the remainder of the report:

END

Gold Money concludes that we have had relentless selling pressure in the futures market. He notes that huge suppression in silver prices but he also opinion that silver is on the verge of a breakout. As far as I am concerned, the breakout will only occur when London runs out of metal.

(courtesy GoldMoney/GATA)

Amid ‘relentless’ futures selling, silver nears breakout, GoldMoney says

Submitted by cpowell on Sat, 2018-04-21 13:27. Section: Daily Dispatches

9:29a ET Saturday, April 21, 2018

Dear Friend of GATA and Gold:

A research report by GoldMoney’s Stefan Wieler concludes that “relentless selling pressure in the futures market” has been suppressing silver prices but that the market is on the verge of a breakout. The report is headlined “Silver on the Verge of a Breakout” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/silver-on-the-verg…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Russia adds 300,000 oz of gold or 9.33 tonnes to its official reserves

(courtesy Lawrie Williams)

LAWRIE WILLIAMS:

Russia adds to gold reserves again in March

China may continue to be telling the world that it has added zero to its gold reserves since October 2016, but Russia is still increasing its gold hoard on a monthly basis. Its official total gold reserve holding as reported to the IMF surpassed that of China a couple of months ago and continues to rise further with the central bank reporting another 300,000 ounces (9.33 tonne) increase in March bringing its official gold holding to around 1,890 tonnes, now getting on for nearly 50 tonnes more than China’s ‘official’ total of 1,842.6 tonnes.

There is speculation that, given the badwill between the two nations, Russia may dispose of some of the U.S.- denominated assets in its substantial Forex holdings replacing them with some other currency (the Chinese yuan for example) and gold (It may already have started this process). This would be a move that if followed by some other nations (notably China with its enormous forex reserves) could start to destabilise the U.S. economy which is very reliant on the global acceptance of the U.S. dollar as the world’s principal reserve currency..

According to a recent report by Russian news agency, Pravda (www.pravda.ru), The Bank of Russia holds a third of its currency assets in the U.S. but all its physical gold holdings are thought to be held in depositories in Moscow, St Petersburg and Yekaterinburg. Formally, the USA can not impose sanctions on the Bank of Russia, even though earlier, US authorities froze the assets of the National Fund of Kazakhstan. The move clearly indicated that Russian assets in the USA could be frozen as well. If the USA freezes Russian gold and foreign currency assets, such an act would be equal to the declaration of war, economist and publicist Mikhail Khazin earlier told Pravda.Ru.

Gold offers Russia independence from the dollar amid financial sanctions from the U.S. and its allies, notes Bloomberg in a recent article. The initial sanctions were imposed in 2014 as punishment for Russia’s involvement in Ukraine and annexation of Crimea and have just been tightened following alleged Russian state involvement in the Skripal poisoning in the U.K. and an alleged chemical weapons attack by the Syrian Regime in Douma. (The Syrian Government is supported militarily by the Russians). Russia denies any involvement and, indeed claims the alleged Douma chemical attack is fiction!

Much of Russia’s gold purchases come from local production — Russia is the world’s third-largest miner of the metal behind China and Australia, according to research firm Metals Focus although Russia’s Finance Ministry’s own figures suggest it may actually be in second place having overtaken Australia last year with output of more than 300 tonnes. On the Metals Focus reckoning Russia produced around 270 tonnes of gold while its central bank added over 200 tonnes to its reserves. (See: World Top 20 Gold producing nations in 2017 – not peak gold yet!).

Russia’s gold reserves had been run down under Mikhail Gorbachev to as little as 290 tonnes, but President Vladimir Putin is a strong believer in the power of gold and forex reserves as a guarantor of Russian financial independence and is believed to have been the leading instigator of the reserve increase

21 Apr 2018

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3079 /shanghai bourse CLOSED DOWN 3.53 POINTS OR 0.11% / HANG SANG CLOSED DOWN 163.93 POINTS OR 0.54%

2. Nikkei closed DOWN 74.20 POINTS OR 0.33%/ /USA: YEN RISES TO 108.26/

3. Europe stocks OPENED RED /USA dollar index RISES TO 90.73/Euro FALLS TO 1.2226

3b Japan 10 year bond yield: RISES TO . +.067/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.26/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.13 and Brent: 73.98

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.625%/Italian 10 yr bond yield DOWN to 1.778% /SPAIN 10 YR BOND YIELD UP TO 1.291%

3j Greek 10 year bond yield FALLS TO : 4.0351?????????????????

3k Gold at $1327.70 silver at:16.95 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 73/100 in roubles/dollar) 62.10

3m oil into the 68 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.26 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9759 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1934 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.625%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.9808% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1658% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Stumble As 10Y Hits 2.996%; Dollar Squeeze Accelerates

Global stocks stumbled on Monday ahead of an avalanche of earnings in this season’s busiest reporting week but the big story overnight was the spike in 10Y Yield which climbed as high as 2.9957%, the highest level since January 2014, and nearing the psychological 3% level which has triggered market spasms and more than one tantrum in the past. The move was catalyzed by Treasury Secretary Steven Mnuchin saying over the weekend that he is planning a trip to China, an indication the US is considering a truce in its trade war with China.

Citi’s technical team repeats the key highlights, pointing out that we’re 1bp away from the psychological 3% level in the Treasury 10y yield. “The benchmark is trading at levels not seen since 2014, and we are continuing to make fresh YTD highs. The 10s now trade at 2.99% while the 2s10s trades on the 51 mark.”

If we break 3%, major levels come in here that extend up to 3.05%: this is the level where we have the 2014 high which is also the long term double bottom neckline and the long term channel top:

Not everyone is convinced that the 10Y will soar once it blows through 3% (especially not in a world which both the IMF and IIF said has record debt): “Ultimately it’s hard to see a move sustained above 3 percent on the U.S. 10-year,” Mitul Kotecha, a strategist at TD Securities, told Bloomberg TV from Singapore. “Some of the dialing down in tensions, in risk aversion, may be having some impact there as well as expectations of continued strong growth in the U.S.”

Meanwhile, rising yields are capping other risk assets and the recent sell off in Treasuries is being closely eyed by other markets, and supporting a pretty aggressive USD bid and VIX is rallying.

Mostly as a result of rising yields and a stronger dollar, S&P 500 Index futures turned lower, tracking moves in the Stoxx Europe 600 Index which failed to capitalize on an unexpected beat in the April PMI prints, while earlier the MSCI Asia Pacific Index also started off the week in the red.

In global stocks, MSCI’s world index fell 0.25% after Asia shed 0.5% overnight and Europe then slipped 0.2% as results from Switzerland’s biggest bank, UBS, disappointed. S&P futures also pointed to a modestly lower open.

Meanwhile, traders are on edge because in addition to earnings – more than 180 companies in the S&P 500 are due to report results this week, including Amazon, Alphabet, Facebook, Microsoft, Boeing and Chevron– traders also received the latest round of advance economic surveys that should show in the coming days if economic softness in the first quarter was just a passing phase linked to wintery weather and the Lunar New Year holidays in Asia. Readings from Japan, France and Germany were all relatively reassuring. Japan’s PMI data firmed as output and domestic demand picked up, France got help from its services sector, while Germany came in above forecast despite weaker new orders numbers.

- EU Markit Manufacturing Flash PMI (Apr) 56.0 vs. Exp. 56.6 (Prev. 56.6)

- EU Markit Services Flash PMI (Apr) 55.0 vs. Exp. 54.8 (Prev. 54.9)

- EU Markit Comp Flash PMI (Apr) 55.2 vs. Exp. 54.9 (Prev. 55.2)

“It’s a good reading, it’s still encouraging,” said Chris Williamson, chief business economist at IHS Markit, of the combined euro zone numbers, which he said pointed to quarterly GDP growth of 0.6 percent.

Helping the spike in yields is the recent sharp reversal/short squeeze in the dollar as the dollar; the BBDXY index gained a fifth day, rising 0.5% on Monday to the highest level since March 1, and is now up by 1.4% since Wednesday’s close, the most on a three-day basis since December 2016. In addition to the squeeze of near record dollar shorts, a “Europe-based trader” quoted by Bloomberg says dollar bids represent both unwinding of medium-term trailing stops and fresh positions, while another trader said that interbank names are seen selling the euro and the yen.

Elsewhere in FX, the EUR/USD slipped for a third day, down to a two-week low of 1.2226 while GBP/USD reversed an earlier gain to drop below 1.4000 handle as chances that the BOE may not move in May, together with renewed concerns over the Brexit front, weighed on pound sentiment. USD/JPY rose to trade above 108.00 for the first time since mid-February: option-related offers below that level capped for a while, before stops above the figure were filled. As Citi notes, some big levels have been broken in FX today:

- EURUSD is through Friday’s low at 1.2256 and is less than 30 pips away from the 100d MA at 1.2206.

- USDJPY has broken the 108 handle and now through 108.13. The reverse head and shoulders target of 109.36 looks feasible according to CitiFX Technicals.

- AUDUSD trendline comes in here at 0.7634 as we find fresh YTD lows.

- NZDUSD testing the 200d MA at 0.7185. From here, there are a few levels to eye with 0.71500 and 0.7111.

- USDCAD levels in 1.2720-80 including the 55d MA at 1.2767 seem to have been broken. Through 1.2800, there are plenty of levels from the March rally.

- USDNOK MTD highs are at 7.8990, and the 100d MA at 7.9284. EURNOK looks more mixed, with the 100d MA not until 9.6721.

- GBPUSD: The pair has broken through the 1.40 handle and looks like we could test the 100d MA at 1.3850. However GBP may stabilize against EUR here, with all the notable MA levels converging ahead.

It was a busy weekend in geopolitical news, with North Korea surprising the world on Saturday stating that it would immediately suspend nuclear and missile tests, scrap its nuclear test site and instead pursue peace and economic growth, a development which Trump quickly latched on to as evidence of yet another mission (nearly) accomplished. Additionally, talk of a trip by the U.S. Treasury Secretary to China also fueled hopes that the recent trade tensions between the world’s two biggest economies may be thawing.

In overnight central banks news, the Nikkei reported that the Bank of Japan has shown signs it is tapering its ETF purchases in order to trim what it sees as an outsize profile in the equity market. Meanwhile, BoJ Governor Kuroda said the Bank of Japan must continue very strong accommodative monetary policy for some time in order to

reach 2% inflation. However, he may not have the choice, as dark clouds continue to gather over the head of this boss and over the weekend, the approval of Japanese Prime Minister Shinzo Abe’s cabinet dropped in polls conducted by the Yomiuri and Mainichi newspapers to the lowest level since 2012.

Oil prices edged down in the cross-currents but were not far from their highest since late 2014. The market had wobbled on Friday when Trump tweeted criticism of OPEC’s role in pushing up global prices, but quickly steadied. Oil prices dipped in Monday trade with WTI down 0.6% at USD 68/bbl. In addition to echoes from Trump’s anti-OPEC tweet, the modest weakness followed Baker Hughes reporting an increased rig count on Friday, which is now at its highest level since March 2015. The strengthening dollar is also weighing on gold with the yellow metal down 0.5% on the day. Some OPEC specific news coming from the Azerbaijani energy minister who says the country joining OPEC is not on the agenda.

It’s a busy week (full preview to follow), with some of the key events as follows:

- French President Emmanuel Macron begins a three-day visit to the U.S. Monday

- U.S. manufacturing and services sector PMIs. Later this week: GDP and jobless claims.

- Earnings season continues. Among those reporting: Alphabet/Google, Amazon.com, Samsung and Credit Suisse.

- The European Central Bank has a rate decision on Thursday. Investors will watch for any sign that officials are preparing a shift in stimulus plans for their June meeting.

- Bank of Japan announces its latest policy decision Friday and releases a quarterly outlook report.

Bulletin Headline Summary from RanSquawk

- US 10 year treasury ticking towards 3.00% yield

- Upward pressure on the USD pushing down commodities

- Looking ahead, highlights include US existing homes sales, ECB’s Coeure and BoC’s Poloz

Market Snapshot

- S&P 500 futures down 0.2% to 2,667.25

- STOXX Europe 600 down 0.2% to 380.98

- MSCI Asia Pacific down 0.4% to 173.19

- MSCI Asia Pacific ex Japan down 0.5% to 564.10

- Nikkei down 0.3% to 22,088.04

- Topix down 0.02% to 1,750.79

- Hang Seng Index down 0.5% to 30,254.40

- Shanghai Composite down 0.1% to 3,068.01

- Sensex up 0.5% to 34,579.62

- Australia S&P/ASX 200 up 0.3% to 5,886.01

- Kospi down 0.09% to 2,474.11

- German 10Y yield rose 4.1 bps to 0.631%

- Euro down 0.3% to $1.2254

- Italian 10Y yield fell 0.3 bps to 1.524%

- Spanish 10Y yield rose 1.9 bps to 1.301%

- Brent futures down 0.5% to $73.66/bbl

- Gold spot down 0.7% to $1,327.23

- U.S. Dollar Index up 0.4% to 90.66

Top Overnight News from Bloomberg

- U.S. Treasury Secretary Steven Mnuchin said he’s considering a trip to China amid a trade dispute with Beijing that finance chiefs warn could derail the global economic upswing. Mnuchin said he’s “cautiously optimistic” of reaching an agreement with China

- President Trump tempered his optimism on North Korea on Sunday, saying that “only time will tell” how things turn out. U.S. lawmakers sounded skeptical about promises made by Pyongyang ahead of possible historic talks between the countries leaders

- North Korea will freeze nuclear and intercontinental ballistic missile launch tests from April 21, state-run media Korean Central News Agency said Saturday; The leaders of the two Koreas are set to hold their first summit since 2007 on Friday

- Approval of Japanese Prime Minister Shinzo Abe’s cabinet dropped in polls conducted by the Yomiuri and Mainichi newspapers over the weekend.

- French President Emmanuel Macron’s arrival in the U.S. kicks off a crucial week for European leaders in an uphill battle to convince Donald Trump to stay in the Iran nuclear deal

- “If conflict increases, there will be less growth, more inflation,” says Federal Reserve Bank of San Francisco President John Williams in an interview with El Pais published in Spanish

- Has an invisible hand stepped in to support the Indian sovereign bond market? Traders are abuzz with speculation over the identity of the buyer or buyers behind the $862 million of purchases Friday

- U.K. PM Theresa May’s inner circle thinks she could be forced to accept staying in the EU’s customs union because Parliament will reject her plan to withdraw from it when the issue comes to a vote in the House of Commons, according to one official. Such a move could trigger a challenge to May’s leadership from Brexit campaigners in the Conservative Party

- U.K. Chancellor of the Exchequer Philip Hammond has indicated a willingness to look abroad when he begins his search for a successor to Bank of England Governor Mark Carney

- Eurozone April Flash composite PMI 55.2 versus estimate 54.8

Asia equity markets began the week lacklustre after last Friday’s losses on Wall St where all majors declined on continued tech weakness and losses in Apple amid concerns regarding iPhone demand. However, overnight pressure was contained in the AsiaPac region amid a further improvement of the geopolitical climate in the Korean peninsula after North Korea announced it will stop nuclear and ICBM testing, as well as begin dismantling a nuclear test site in the north of the country. ASX 200 (+0.3%) and Nikkei 225 (-0.3%) were mixed with weakness in Japan the result of last week’s flows into JPY. Elsewhere, Shanghai Comp. (-0.1%) and Hang Seng (-0.5%) were choppy amid a lack of drivers and a neutral position by the PBoC which injected CNY 80bln via reverse repos to match maturing operations, although underperformance was observed in Hong Kong names. Finally, 10yr JGBs were lower amid spill over selling from USTs and as yields tracked the upside in their US counterparts, in which the US 10yr yield printed its highest since January 2014. PBoC injected CNY 80bln via 7-day reverse repos for a daily net neutral position.

Top Asian News

- Sudden Modi-Xi Meet Signals Diplomatic Thaw Between Neighbors

- Bond Traders in India Hope Mystery Buyer Is the Central Bank

- Ping An Good Doctor Aims to Raise as Much as HK$8.8b in IPO

- Noble Group Board Becomes Battleground as Goldilocks Fights

- New Hong Kong Tech Darling Hawks IPO With Rare Valuation Metric

European equities opened on the back foot this morning (Eurostoxx 50 -0.2%) following the dampened tone from Asia. Switzerland’s SMI is underperforming as index heavyweight UBS (-3.1%) lags following earnings. Sector wise, consumer staples underperform while Reckitt Benckiser (-2.2%) are at the bottom of the FTSE 100 following a downgrade at Raymond James and a target price cut at JP Morgan. In terms of stocks specifics, Fresenius (+0.6%) shares are higher following the terminations of the Akorn merger amid data breaches. Fresenius Medical (-3.6%) is at the foot of the DAX 30 following a revenue target cut for this year. Capita (+10.1%) is the best performing in the Stoxx 600 following earnings and reports the company is to raise GBP 701mln in a 3 for 2 rights issue entirely underwritten by Citigroup and Goldman Sachs.

Top European News

- May Is Said to Face Cabinet Pressure Over Brexit Customs Union

- Poland Shatters Fragile Peace With Its Jews After Holocaust Law

- Euro-Area Economy Stays in Lower Gear as Order Growth Weakens; German Growth Momentum Rebounds After First-Quarter Slowdown

- How China Bought Up A Swath of Europe When Nobody Was Looking

In FX, firmer US rates are certainly fuelling the latest Dollar revival and the Greenback’s broad gains, but latest conciliatory noises from NK on the nuclear front are also undermining the traditional safe-haven currencies. The index is now comfortably above 90.500 and 90.600 resistance, looking at 90.750 next. JPY/EUR: Both on the brink of breaking out of recent ranges, with Usd/Jpy up through 108.00 offers, a big barrier and resistance extending to 108.20, but capped just ahead of stops reportedly lying between 108.25-30, while Eur/Usd has breached last Friday’s 1.2250 low having failed to reach 1.2300 in wake of better than forecast Eurozone flash PMIs, and is now also below the next downside technical support level at 1.2235, eyeing 1.2200. CAD: Usd/Cad looks is revisiting 1.2800+ on the aforementioned supportive Greenback narrative and contrasting Loonie weights in the form of last Friday’s CPI data and a still cautious BoC, although latest NAFTA reports indicate a deal could be reached in early May. The range has been 1.2750-1.2805, and the recent peak is circa 1.2820 (February 9). GBP: Losing traction around the 1.4000 level after last week’s heavy losses on a mixture of UK data misses and dovish or less hawkish BoE policy guidance from Governor Carney. Looking to test chart support around 1.3960 while Eur/Gbp is nudging up towards the high of a 0.8745-75 range.

In commodities, oil prices dipping in Monday trade with WTI down 0.6% at USD 68/bbl. This follows Baker Hughes reporting an increased rig count on Friday, which is now at its highest level since March 2015, suggesting increased US production putting downward pressure on the fossil fuel, as well as tweets from the US President suggesting oil is “artificially high” due to OPEC. The strengthening dollar is also weighing on gold with the yellow metal down 0.5% on the day. Some OPEC specific news coming from the Azerbaijani energy minister who says the country joining OPEC is not on the agenda.

Kicking off the week today will be the flash April PMIs due to be released in Europe and the US. Other data worth flagging is US existing home sales data for March. Away from that French President Macron is due to begin a three-day visit to the US, while the ECB’s Coeure is scheduled to speak in the afternoon. UBS and Google are the earnings release highlights.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0.3, prior 0.9

- 9:45am: Markit US Manufacturing PMI, est. 55.2, prior 55.6

- Markit US Services PMI, est. 54.1, prior 54

- Markit US Composite PMI, prior 54.2

- 10am: Existing Home Sales, est. 5.55m, prior 5.54m; MoM, est. 0.18%, prior 3.0%

We wonder whether this week will finally host the 10 year Treasuries at 3% party? The sell off continued on Friday with yields closing at the highs for the session at 2.96% (+5bps) – the highest since January 2014. This was in spite of a Trump tweet bomb where he accused OPEC of artificially driving up prices. This morning in Asia, yields have crept up another c1.5bp and edging us closer to this landmark. Elsewhere equities are trading mixed with the ASX200 up 0.42% while the Nikkei (-0.30%), Kospi (-0.19%) and Hang Seng (-0.36%) are down as we type. Datawise, Japan’s April Nikkei manufacturing PMI firmed 0.2pts mom to 53.3.

Back to yields, in terms of what might attract us or repel us to the 3% mark we have a busy week with the ECB and BoJ holding policy meetings and the latest flash PMIs out around the globe today as well as a first look at Q1 GDP in the US. European PMIs in particular will be closely watched given the recent sharp deceleration.

With regards to the two big central bank meetings this week the ECB (Thursday) is the more interesting. While no change in policy is expected all eyes will be any hints or signs that officials are preparing the ground for an announcement in June that stimulus is to come to an end by the end of the year. Weaker data of late and some slightly dovish ECB commentary perhaps means that risks are tilted to the downside so the market will likely be on the watch in Draghi’s press conference. Ahead of this today sees the flash PMIs. In Europe the consensus is for a continued moderation with the manufacturing print expected to nudge down another 0.5pts to 56.1 (which would be the lowest since February 2017) and the services a more modest 0.3pt decline to 54.6. European data surprises have been hovering at multi-year lows of late so Europe could do with some stabilisation soon to avoid stoking fears of a sharper downturn. It’s possible that the easing trade war tensions and healthier sentiment in the last week or so won’t yet be in these numbers though.

In terms of earnings this week, 181 S&P 500 companies are scheduled to report including some of the big tech heavy hitters like Google (today), Facebook / eBay / Twitter (Wednesday), Microsoft / Amazon / Intel (Thursday). Also worth highlighting are earnings reports from Verizon, Caterpillar and Coca-Cola on Tuesday, AT&T and Boeing on Wednesday and Exxon Mobil and Chevron on Friday. Earnings season also picks up in Europe with 121 Stoxx 600 companies reporting including the likes of UBS today, Credit Suisse on Wednesday and Volkswagen, Total and Royal Dutch Shell on Thursday.

Last but by no means least, the big political event this week is likely to be the summit held between South Korea President Moon Jae-in and North Korea Leader Kim Jong Un in the demilitarized zone between the two countries on Friday. Over the weekend, President Trump seemed to have softened his expectations as he tweeted “we’re a long way from conclusion on North Korea….only time will tell”. Away from that, French President Macron is due to travel to the US on Monday for three days and is scheduled to meet US President Trump on Tuesday. German Chancellor Merkel is also due to meet Trump on Friday.

Turning to trade, tensions appeared to have eased further over the weekend as the US Treasury Secretary Mnuchin said he’s “cautiously optimistic” on reaching a trade agreement with China and that “a trip (to China) is under consideration”, but declined to comment on potential timing. On the other side, China’s Ministry of Commerce said it would welcome such a visit. Elsewhere, the PBOC’s Governor Yi reiterated that the recently announced measures to open up China’s financial sector will be “implemented either in the next few months or by the end of this year”. Finally, the Russian Finance Minister Siluanov has met with Secretary Mnuchin and sought “clarifications” on the US sanctions, without elaborating more.

Now recapping other markets performance from Friday. US bourses weakened further, weighted down by tech and consumer staples stocks (S&P -0.85%; Dow -0.82%; Nasdaq -1.27%). The VIX rose for the third straight day to 16.88 (+5.8%) while the Stoxx 600 was marginally lower. In FX, the USD index gained for the fourth consecutive day (+0.42%) while the Euro and Sterling fell -0.46% and -0.62% respectively. WTI oil edged up 0.10% to $68.40/bbl on Friday.

Elsewhere, European government bonds firmed and partly reversed Thursday’s losses with yields on 10y Bunds and OATs both down c1bp while Gilts outperformed (-4.1bp), partly due to BOE Governor Carney’s dovish talk on a potential rate hike in May. Notably, the Bloomberg implied odds of a May rate hike in the UK fell 31ppt to 46% on Friday.

Moving onto central bankers speak. The Fed’s Williams reiterated that it makes sense to keep raising rates through next year given an improving economy and noted that if growth slows, the USD could get “dramatically stronger”. In Europe, the ECB’s Villeroy said the greatest medium term risk is “incontestably protectionism”. He added that if tariffs increased by 10% and became the norm, then “global GDP could decrease by at least 2%”. Elsewhere, Bloomberg cited unnamed sources which noted the ECB see scope to wait until their July meeting to announce their plans on ending QE, in part to allow more time to judge the impacts of the recent economic slowdown.