GOLD: $1257.25 UP $5.15(COMEX TO COMEX CLOSINGS)

Silver: $16.06 UP 6 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1257.75

silver: $16.06

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT:16 NOTICE(S) FOR 1600 OZ

TOTAL NOTICES SO FAR 53 FOR 5300 OZ (0.1648 tonnes)

For silver:

JUNE

310 NOTICE(S) FILED TODAY FOR

1,550,000 OZ/

Total number of notices filed so far this month: 4487 for 22,435,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6590/OFFER $6675: UP $45(morning)

Bitcoin: BID/ $6450/offer $6536: DOWN $94 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1259.25

NY price at the same time: 1255.95

PREMIUM TO NY SPOT: $12.06

Second gold fix early this morning: 1258.05

USA gold at the exact same time:1254.95

PREMIUM TO NY SPOT: $3.10

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE 2552 CONTRACTS FROM 209,151 DOWN TO 205,622 DESPITE TUESDAY’S GOOD 17 CENT RISE IN SILVER PRICING. WE HAVE HAD SUCH CONSIDERABLE COMEX LIQUIDATION THESE PAST SEVERAL DAYS BUT IT HAS NOT MANIFESTED ITSELF INTO LOWER DEMAND FOR PHYSICAL SILVER..JUST THE OPPOSITE. WE ARE STILL WITNESSING A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(OVER 28 MILLION OZ) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED TUESDAY NIGHT, THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 1909 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1909 CONTRACTS. WITH THE TRANSFER OF 1909 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1909 EFP CONTRACTS TRANSLATES INTO 9.545 MILLION OZ ACCOMPANYING:

1.THE 17 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) AND NOW JULY/ 2018 WITH 28.210 MILLION OZ INITIALLY STANDING FOR DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

7369 CONTRACTS (FOR 3 TRADING DAYS TOTAL 7369 CONTRACTS) OR 36.84 MILLION OZ: (AVERAGE PER DAY: 2456 CONTRACTS OR 12.281 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 36.84 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.26% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* LAST MONTH’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,696.58 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX OF 2552 DESPITE THE GOOD 17 CENT GAIN IN SILVER PRICE. NOT ONLY THAT BUT THE CME NOTIFIED US THAT IN FACT WE HAD A FAIR SIZED EFP ISSUANCE OF 1909 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 1909 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1909). TODAY WE LOST A TINY: 643 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.1909 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 2552 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 17 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.00 WITH RESPECT TO TUESDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE JULY DELIVERY MONTH OF MORE THAN 28 MILLION OZ. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.029 MILLION OZ TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 310 NOTICE(S) FOR 1,550,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ / JUNE/2018 (5.420 MILLION OZ) AND NOW JULY 2018 AMOUNT INITIALLY STANDING: 28.210 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A CONSIDERABLE 3354 CONTRACTS UP TO 494,164 WITH THE GOOD RISE IN THE GOLD PRICE/YESTERDAY’S TRADING (A GAIN IN PRICE OF $11.30). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JULY. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 12,875 CONTRACTS : AUGUST SAW THE ISSUANCE OF: 11,875 CONTRACTS, DECEMBER HAD AN ISSUANCE OF 100 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 494,164. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 3354 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 12,875 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: AN ATMOSPHERIC 16,229 CONTRACTS OR 1,722,900 OZ = 50.43 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH ONLY A FAIR RISE IN THE PRICE OF GOLD ON TUESDAY TO THE TUNE OF $11.30???

TUESDAY, WE HAD 9758 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 24,631 CONTRACTS OR 2,463,100 OZ OR 76.612 TONNES (3 TRADING DAYS AND THUS AVERAGING: 8,210 EFP CONTRACTS PER TRADING DAY OR 821,000 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 76.612 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 76.612/2550 x 100% TONNES = 3.00% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,179.52* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3354 WITH THE $11.30 RISE IN PRICING GOLD UNDER TOOK YESTERDAY // . WE ALSO HAD A GIGANTIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,875 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,875 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC NET GAIN OF 16,229 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,875 CONTRACTS MOVE TO LONDON AND 3354 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 50.43 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED WITH ONLY A FAIR SIZED GAIN OF $11.30 IN TRADING. AT THE COMEX!!!. THE COMEX IS AN OUTRIGHT FRAUD

we had: 16 notice(s) filed upon for 1600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP ANOTHER $5.15 TODAY: / A BIG CHANGE IN GOLD INVENTORY AT THE GLD/THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF A 5.89TONNES OF GOLD WITHDRAWAL

/GLD INVENTORY 803.42 TONNES

Inventory rests tonight: 803.42 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 6 CENTS: A GOOD CHANGE IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 470,000 OZ OF SILVER.

/INVENTORY RESTS AT 324.305 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2552 CONTRACTS from 208,174 DOWN TO 205,622 (AND FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2209 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2209CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2552 CONTRACTS TO THE 1909 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET LOSS OF 643 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 3.215 MILLION OZ!!! AND YET WE HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESS AN INITIAL STANDING OF OVER 28 MILLION OZ AND YET ALL OF THIS DEMAND OCCURRED DESPITE A RELATIVELY SMALL 17 CENT GAIN IN PRICE??? .

IT SURE LOOKS LIKE WE ARE GETTING SOME COVERING FROM THE BANKERS SIDE ESPECIALLY WHEN YOU SEE A GOOD GAIN IN PRICE AND THEN A FALL IN COMEX OI AND A SMALLER THAN EXPECTED EFP ISSUANCE.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 17 CENT RISE THAT SILVER UNDERTOOK IN PRICING ON TUESDAY. BUT WE ALSO HAD ANOTHER FAIR SIZED 1909 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 25.24 POINTS OR 0.91% /Hang Sang CLOSED DOWN 59.58 POINTS OR 0.21%/ / The Nikkei closed DOWN 170.05 POINTS OR 0.78% /Australia’s all ordinaires CLOSED UP 0.47% /Chinese yuan (ONSHORE) closed UP at 6.6384 AS POBC STOPS ITS HUGE DEVALUATION /Oil DOWN to 74,52 dollars per barrel for WTI and 78.23 for Brent. Stocks in Europe OPENED IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.6384 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6480 :HUGE DEVALUATION/PAST SEVERAL DAYS HALTED//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

Tuesday night:

Semantics: China does not want to the first to initiate tariffs so they will delay until after the US begins their tariffs at 12:01 July 6. Friday.

( zerohedge)

ii)China is trying to isolate the uSA. It sought a grand alliance with Europe against the USA but the EU just do not trust China

( zerohedge)

iii)China rejects the USA “blackmail” on the eve of trade war ready to commence. It is fascinating that Europe refused to go along with China and isolate the USA, The reason given behind the scenes is that Trump is correct on China and also the fact that Europe does not trust China will impliment its proposals

4. EUROPEAN AFFAIRS

i)Wednesday/ECB

The Euro spikes higher as ECB banking members are very uneasy with the market’s dovish view on rate hikes

( zerohedge)

ii)Mish exposes Merkel’s “common goal” as shear hypocrisy. The deal is still not final and they still have to deal with the SPD. Austria is also in on the plan because migrants must be sent back through Austria and onto African camps. No African nation has approved any of this!!

iii)We now have a 3 way deal reached in Germany but what about Austria? How could they as well as Hungary agree to this(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran

Iran threatens the USA that it will block the Straits of Hormuz and if they do so the USA will bomb Iran

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

india

Meet another emerging nation with troubles. India has a huge 11.1% of total loans being non performing. In other words, their total loans are 1.7 trillion dollars equivalent and a gigantic 210 billion of that is non performing. India has high external debts and must also import huge amounts of crude oil, the higher price is certainly not helping them. The Rupee is now at an all time low similar to most emerging nations

This will no doubt be a huge crisis for the world as this will set of contagion like we have never seen

( zerohedge)

9. PHYSICAL MARKETS

i)Hemke believes that banks have reduced short interest at the Comex (but not their huge obligations with respect to EFP’s) and that might spark a rally in NY pricing of gold/silver

( Craig Hemke/GATA/Sprott)

ii)This fellow, Kiener, comes to the same conclusion as myself. With huge payments to hedge funds holding Exchange for Physical, gold is essentially in backwardation at the Comex in New York

( Kiener/GATA)

iii)This was to be expected: cryptocurrency exchange theft has surged in the first half of 2018

( zerohedge)

iv)I guess this was to be expected: Iranian cops are cracking down on “gold hoarders”. This one guy bought a massive 250,000 of Iranian gold coins. No wonder gold coins are disappearing faster than a speeding bullet everywhere

( zerohedge)

10. USA stories which will influence the price of gold/silver)

I)MARKET TRADING/EARLY MORNING

This is alarming stock enthusiasts: the yield curve is inverting faster than expected and no doubt that one more rate hike will cause the curve to be completely inverted which signals a recession 9 out of 10 times

(courtesy zerohedge)

ib)FOMC minutes:

the FOBC minutes show a hawkish fed eying a very strong economy (which is false). The big fear is that the yield curve is collapsing and another rate hike will invert the curve giving us a 90% surety of a severe recession.

(courtesy zerohedge0

Terribly biased ADP private employment report now disappoints for the 4th consecutive month; In past times there would be a good correlation with Friday’s job report and the ADP but not know.

(courtesy zerohedge/ADP)

iv)SWAMP STORIES

a)Strzok, after getting cold feet on testifying, is now slapped with a subpoena to testify in public

( zerohedge)

b)Strzok may attend but not answer any questions and basically plead the 5th. This would set a constitutional challenge because he has already testified and has waived his 5th amendment rights

( zerohedge)

c)Mueller probe expands despite Trey Gowdy’s plea “to finish it..the hell up!!”

( zerohedge)

d)And the next to go: Scott Pruitt at the EPA

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 402,770 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 327,983 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE SIZED 2552 CONTRACTS FROM 208,174 DOWN TO 205,622 (AND A LITTLE FURTHER FROM THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE GOOD 17 CENT GAIN IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE A FAIR SIZED 1909 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1909. ON A NET BASIS WE LOST 643 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2552 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1909 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 643 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of JULY and here the front month fell by 571 contacts to stand at 1465 contracts. We had 706 notices filed yesterday so we continue where we left off last month as guys refuse to take any more silver ETF’s and instead seek physical delivery at the comex. We gained 135 contracts or an additional 675,000 oz of silver will stand at the comex.

The next delivery month, after July is the non active delivery month of August and here we LOST 166 contracts to stand at 1018. The next active delivery month after August for silver is September and here the OI FELL by 2051 contracts DOWN to 160,096

We had 310 notice(s) filed for 1,550,000 OZ for the JULY 2018 COMEX contract for silver

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 SILVER COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY. SO WITH TODAY’S NUMBERS WE SURPASSED LAST YEAR’S LEVEL BY A WIDE MARGIN.

INITIAL standings for JULY/GOLD

JULY 5/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

16 notice(s)

1600 OZ

|

| No of oz to be served (notices) |

161 contracts

(16,100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

53 notices

5300 OZ

.1648TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JULY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY. contract month, we take the total number of notices filed so far for the month (53) x 100 oz or 2900 oz, to which we add the difference between the open interest for the front month of JULY. (188 contracts) minus the number of notices served upon today (16 x 100 oz per contract) equals 21,400 oz,(.6656 tonnes) the number of ounces standing in this non active month of JULY

Thus the INITIAL standings for gold for the JULY contract month:

No of notices served (53 x 100 oz) + {(199)OI for the front month minus the number of notices served upon today (16 x 100 oz )which equals 21,400 oz standing in this NON – active delivery month of JULY .

We LOST 3 contracts or an additional 300 oz will NOT stand for delivery and these guys morphed into London based forwards and received a good fiat sweetener on top of their forwards for their efforts

THERE ARE ONLY 7.4208 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 0.6656 TONNES STANDING FOR JULY

IN THE LAST 18 MONTHS 82 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JULY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

311,998.180 oz

HSBC

Malca

|

| Deposits to the Dealer Inventory |

597,526.300

oz

CNT

|

| Deposits to the Customer Inventory |

nil

|

| No of oz served today (contracts) |

310

CONTRACT(S)

(1,550,000 OZ)

|

| No of oz to be served (notices) |

1155 contracts

(5,775,000 oz)

|

| Total monthly oz silver served (contracts) | 4487 contracts

(22,435,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

i) Into dealer CNT: 597,526.300 oz

total dealer deposits: 597,426.300 oz

we had 0 deposits into the customer account

i) Into JPMorgan: NIL oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) Into everybody else; zero oz

total customer deposits today: zero oz

we had 2 withdrawals from the customer account;

i) out of HSBC: 287,000.460 oz

ii) Out of Malca: 24,997.720

total withdrawals: 311,887,189 oz

we had 0 adjustments/

total dealer silver: 75.717 million

total dealer + customer silver: 276.988 million oz

The total number of notices filed today for the JULY. contract month is represented by 310 contract(s) FOR 1,550,000 oz. To calculate the number of silver ounces that will stand for delivery in JULY., we take the total number of notices filed for the month so far at 4487 x 5,000 oz = 22,435,000 oz to which we add the difference between the open interest for the front month of JULY. (1465) and the number of notices served upon today (310 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2018 contract month: 4487(notices served so far)x 5000 oz + OI for front month of JULY(1465) -number of notices served upon today (310)x 5000 oz equals 28,210,000 oz of silver standing for the JULY contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

THE INITIAL STANDING FOR SILVER AT THE COMEX JULY 2017: 12.115 MILLION OZ ALTHOUGH AT MONTH’S END: 16.435 MILLION OZ. THIS COMPARES WITH TODAY’S INITIAL STANDING FOR SILVER OF 28.210 MILLION OZ.

As I stated on Tuesday:

“WHEN WE WITNESS THE AMOUNT OF PHYSICAL INCREASE IN THE AMOUNT STANDING AT THE COMEX AND ESPECIALLY COMMENCING ON DAY 2 OF THE DELIVERY CYCLE, YOU CAN BET THE FARM THAT THIS AMOUNT WILL INCREASE FROM THIS DAY FORTH UNTIL THE CONCLUSION OF THE MONTH OF JULY. THIS IS KNOWN AS QUEUE JUMPING AND THIS PHENOMENON HAS BEEN FRONT AND CENTRE OF OPERATIONS IN SILVER FOR NOW OVER 14 MONTHS. SILVER IS BEING SOUGHT BY COMMERCIALS OVER ON THIS SIDE OF THE POND AS DWINDLING SUPPLIES VACATE THE GLOBAL ARENA.”

queue jumping continues to intensify to the highest degree in silver as dealers scrounge around for dwindling supplies.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 88,843 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 77,412 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 77,412 CONTRACTS EQUATES TO 387 million OZ OR 55.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -3.08% (JULY 3/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.43% to NAV (JULY 3/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -3.08%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.07/TRADING 12.57//DISCOUNT 3.78.

END

And now the Gold inventory at the GLD/

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 5/2018/ Inventory rests tonight at 803.42 tonnes

*IN LAST 406 TRADING DAYS: 123,17 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 356 TRADING DAYS: A NET 33.15 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

JULY 5/2018:

Inventory 324.305 MILLION OZ

6 Month MM GOFO 2.11/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.11%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .40%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.26

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Irish Gold Money Rings Found – Mystery Surrounds What May Be Ancient, Pre-Historic Currency

– Irish gold artefacts form pre-history discovered in field in Ireland

– “Very significant” find by farmer of “arm sized” rings in Donegal

– Irish gold artefacts akin to bracelets may be some sort of currency or money says Museum curator

(Photo: Caroline Carr, Donegal County Museum)

An Irish farmer from County Donegal has discovered gold artefacts believed to be an ancient currency or money thousands of years old and from pre-history.

Norman Witherow uncovered the gold objects on Saturday when he was digging a drain in a field

The artefacts remained in his kitchen and car boot until Tuesday when his friend, who is a jeweller, told him that it needed to be reported.

Initial observations by staff from the National Museum of Ireland date the gold from at least the Bronze Age (c. 3200–600 BC) or even earlier.

Experts from the Donegal County Museum believe that the artefacts were used as some sort of currency during the Bronze Age.

The beautiful round gold objects, which are over four inches in diameter, are too big to be rings and too small to be bracelets and hence the view that they may be a form of ancient currency or money.

Museum staff were shocked and astounded by the discovery of the gold artefacts.

“This is a once in a lifetime find for our county and we are absolutely delighted,” said assistant curator of the Donegal County Museum Caroline Carr.

The Goldnomics Podcast – Listen and subscribe on YouTube, ITunes, Soundcloud or Blubrry

News and Commentary

Gold steady near $1,255.00 as Dollar treads water ahead of Thursday’s FOMC minutes (FXStreet.com)

Gold Prices Hold Steady Ahead of Fed Minutes (Investing.com)

U.S. ‘opening fire’ on world with tariff threats – China (Reuters.com)

Gold range-bound as attention turns to Fed minutes (BusinessLive.co.za)

Trump Pressed Aides About Invading Venezuela (Bloomberg.com)

Things Are Lining Up Nicely For Gold And Silver (DollarCollapse.com)

Platinum has been a terrible investment – but I’m sticking with it (MoneyWeek.com)

China, EU and U.S.: Arch Stanton’s Grave (TrueEconomics)

China Set for Record Defaults, and Downgrades Tip More Pain (Bloomberg.com)

Want to Win the Trade War? Long the Dollar … For Now (Bloomberg.com)

The Dollar Is a Source of Global Instability – Rickards (DailyReckoning.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

04 Jul: USD 1,256.90, GBP 951.47 & EUR 1,079.80 per ounce

03 Jul: USD 1,245.85, GBP 944.85 & EUR 1,068.81 per ounce

02 Jul: USD 1,249.00, GBP 948.87 & EUR 1,072.39 per ounce

29 Jun: USD 1,250.55, GBP 950.29 & EUR 1,073.85 per ounce

28 Jun: USD 1,250.50, GBP 955.26 & EUR 1,081.68 per ounce

27 Jun: USD 1,256.80, GBP 951.40 & EUR 1,079.97 per ounce

Silver Prices (LBMA)

04 Jul: USD 16.05, GBP 12.15 & EUR 13.78 per ounce

03 Jul: USD 15.93, GBP 12.08 & EUR 13.68 per ounce

02 Jul: USD 15.98, GBP 12.14 & EUR 13.73 per ounce

29 Jun: USD 16.03, GBP 12.20 & EUR 13.77 per ounce

28 Jun: USD 16.11, GBP 12.30 & EUR 13.90 per ounce

27 Jun: USD 16.21, GBP 12.27 & EUR 13.93 per ounce

Recent Market Updates

– Gold $10,000 In Currency Reset? Russia, China Gold Demand To Overwhelm Gold Futures Manipulation (GOLDCORE VIDEO)

– Italian Debt – A Financial Disaster Waiting To Happen

– As The Currency Reset Begins – Get Gold As It Is “Where The Whole World Is Heading”

– Buy Gold Or Bitcoin As The “Liquidity Party” Is Ending?

– Why Russia and Turkey Diversifying Into Gold May Signal A Bigger Global Shift

– London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– Gold Exports To London From U.S. Surge 152% In 2018

– Manipulation of Gold & Silver by Bullion Banks Is “Undeniable”

– “Perfect Environment For Gold” As Fed Will Weaken Dollar and Create Inflation – Rickards

– Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

– In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

– Bitcoin Price To $0 Or $1 Million In One Year? MoneyConf 2018 Poll

– Cashless Society – Good or Bad? MoneyConf 2018 Video

– Do We Still Need Banks In The Age Of Fintech?

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

This fellow, Kiener, comes to the same conclusion as myself. With huge payments to hedge funds holding Exchange for Physical, gold is essentially in backwardation at the Comex in New York

(courtesy Kiener/GATA)

Comex doesn’t reflect physical gold market,

Swiss Asia Capital’s Kiener says

Submitted by cpowell on Tue, 2018-07-03 18:00. Section: Daily Dispatches

2p ET Tuesday, July 3, 2018

Dear Friend of GATA and Gold:

Juerg Kiener, managing director of Swiss Asia Capital in Singapore, today calls the attention of Bloomberg News television to the transfer to London and presumably the resulting cash settlement of gold futures contracts from the New York Commodities Exchange. Using the “exchange for physicals” mechanism for settling gold contracts, Kiener says, the Comex fails to reflect the structure of the physical gold market, which is in backwardation.

The interview with Kiener is three minutes long and can be viewed at Bloomberg here:

https://www.bloomberg.com/news/videos/2018-07-03/swiss-asia-capital-s-ci…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Hemke believes that banks have reduced short interest at the Comex (but not their huge obligations with respect to EFP’s) and that might spark a rally in NY pricing of gold/silver

(courtesy Craig Hemke/GATA/Sprott)

Craig Hemke at Sprott Money: Finally time for Comex gold to rally?

Submitted by cpowell on Tue, 2018-07-03 18:38. Section: Daily Dispatches

2:39p ET Tuesday, July 3, 2018

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing for Sprott Money, today reviews futures trader positioning data and concludes that the bullion banks have reduced their shorts enough to spark a summer rally.

Hemke’s analysis is headlined “Is It Finally Time for Comex Gold to Rally?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/is-it-finally-time-for-comex-gold-to-ra…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This was to be expected: cryptocurrency exchange theft has surged in the first half of 2018

(courtesy zerohedge)

Cryptocurrency exchange theft surges in first

half of 2018, report says

Submitted by cpowell on Wed, 2018-07-04 00:10. Section: Daily Dispatches

By Gertrude Chavez-Dreyfus

Reuters

Tuesday, July 3, 2018

NEW YORK — Theft of cryptocurrencies from exchanges soared in the first half of this year to three times the level seen for the whole of 2017, leading to a three-fold increase in associated money laundering, according to a report from U.S.-based cybersecurity firm CipherTrace released today.

The report, which looks at the global anti-money laundering market, showed that in the first six months of the year a total of $761 million was stolen from digital currency exchanges, compared with about $266 million for the whole of 2017.

The losses could rise to $1.5 billion this year, estimated CipherTrace, which is launching a software to help exchanges and hedge funds that use or trade cryptocurrencies comply with anti-money laundering laws. …

… For the remainder of the report:

https://www.reuters.com/article/us-crypto-currencies-ciphertrace/cryptoc…

end

I guess this was to be expected: Iranian cops are cracking down on “gold hoarders”. This one guy bought a massive 250,000 of Iranian gold coins. No wonder gold coins are disappearing faster than a speeding bullet everywhere. To gold coin collectors out there: the coin depicted is a coin minted in 1991, it is one azadi and has a weight of gold equal to .2358 oz

(courtesy zerohedge)

‘Confiscation Is Coming’ As Iranian Cops

Crackdown On “Gold Hoarder” Who Collected

250,000 Coins

As the collapse of the Iranian rial has led to soaring inflation, leading to protests and civil unrest, authorities are beginning to crack down on “gold hoarders” as Iranians scramble to preserve their wealth by swapping rials for gold, which has the added effect of exacerbating the already troubled currency’s decline.

In a move that will send a message to others who’ve buying up large quantities of gold, Iranian police have arrested a man they accused of hoarding two tonnes of gold coins with the intention of manipulating the local market. Tehran Police Chief Gen Hossein Rahimi said the unnamed 58-year-old had collected an estimated 250,000 coins over the past 10 months, working in concert with several accomplices. Police dubbed him “Sultan of Coins.”

The rial has bounced off its all-time lows to trade at roughly 81,000 to the dollar on unofficial currency markets on Wednesday, according to the BBC.

In a scene that mirrored the protests that rocked Tehran in early January, merchants from Tehran’s sprawling Grand Bazaar shuttered their stores in what state media described as “a protest against rising prices and a weakened currency.” During times of unrest, authorities often try to redirect public anger away from the government by creating a scapegoat – like “hoarders” – and blaming them for the country’s economic ills… and – after seeing the chart below, is a full declaration of gold confiscation coming?

But with protests continuing in the capital, we’ll see if that approach works, or if police will need to fall back on their initial plan: Tear gasing everybody.

end

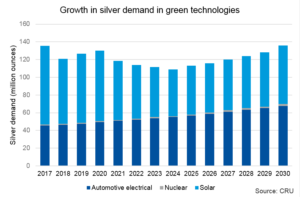

from the silver institute:

OVER 1.5 BILLION OUNCES OF SILVER FORECAST TO BE CONSUMED IN CRUCIAL GREEN TECHNOLOGIES THROUGH 2030

(Washington, D.C. – July 5, 2018) The ongoing revolution in green technologies, driven by the exponential growth of new energy vehicles (NEVs) and continued investment in solar photovoltaic energy, should further boost global industrial demand for silver over the next decade and beyond. These sectors, along with silver demand in nuclear power, are explored in a new report, The Role of Silver in the Green Revolution, released today by the Silver Institute.

The cost of installing and providing solar photovoltaic (PV) systems has fallen rapidly relative to other electrical energy sources over the past two decades. This is expected to continue over the medium-term, leading to an ever-increasing share in renewable energy generation and investment for PV, led by both macroeconomic/cost considerations and public policy. Silver’s importance to solar energy is well documented and the metal will continue to play a substantial role in this technology. It is estimated that roughly 820 million ounces (Moz) of silver will be utilized by global solar energy applications through 2030.

Recognizing an opportunity to curb pollution in urban areas, governments across the globe have provided financial incentives, as well as new regulations, that favor the development of electric and hybrid vehicles into their broader strategies to tackle climate change. China, the largest car market in the world, is gradually moving from incentivizing consumers to buy electric vehicles to penalizing manufacturers who fail to offer NEV models. Other nations have also made longer-term commitments to EVs, including Norway, Germany, India, the Netherlands, the U.K, France, and seven U.S states.

Spurred on by this policy support, as well as falling costs, new energy vehicles such as battery electric vehicles and plug-in hybrids will account for an ever-increasing proportion of global vehicle sales. A potential game changer for transportation is the use of inductively coupled power transfer technology to wirelessly charge vehicles using silver-plated induction coils. Though current market penetration remains low, improvements in performance and cost can open significant opportunities for wireless charger adoption in the coming years. When combined, these efforts are projected to account for approximately 725 Moz of total silver demand through 2030.

An often-overlooked application for silver is nuclear power, where silver is used in combination with other metals to produce the reactors’ control rods. The rod cluster control assemblies are inserted into the reactor to control the rate of fission, and as such must be made of a material that is capable of absorbing neutrons without undergoing nuclear fission itself, has a high mechanical strength, and is resistant to corrosion. One of the most common materials used is an alloy that is 80% silver, 15% indium and 5% cadmium. Though small in terms of expected offtake at 19 Moz of total silver demand through 2030, demand for silver in this area could rise with future growth of nuclear reactors globally.

The report was authored by CRU, a global commodities consultancy. Detailed analysis behind the projections are presented in the publication, which can be downloaded for free at this link: The Role of Silver in the Green Revolution.

The Silver Institute is a non-profit international industry association headquartered in Washington, D.C. Established in 1971, the Institute’s members include leading silver producers, prominent silver refiners, manufacturers and dealers. The Institute serves as the industry’s voice in increasing public understanding of the value and the many uses of silver. For more information on the Silver Institute, silver’s important uses in industry, or silver in general, please visit: www.silverinstitute.org.

For more information on this report, please contact either:

Michael DiRienzo

The Silver Institute

Tel: +1 202-495-4030

e-mail: Mdirienzo@silverinstitute.org

Alex Laugharne

CRU Consulting

Tel: +1 646-628-2515

e -mail: Alex.Laugharne@crugroup.com

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.6384/HUGE DEVALUATION FOR THE PAST TWO WEEKS HALTED/ /shanghai bourse CLOSED DOWN 25.24 POINTS OR 0.91% AFTER FALLING 3.3% ON WEDNESDAY// HANG SANG CLOSED DOWN 59.58 POINTS OR 0.21%

2. Nikkei closed DOWN 170.05 POINTS OR .12% / /USA: YEN FALLS TO 110.61/

3. Europe stocks OPENED DEEPLY IN THE GREEN / /USA dollar index FALLS TO 94.31/Euro RISES TO 1.1983

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.61/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 74.52 and Brent: 78.234

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.32%/Italian 10 yr bond yield UP to 2.67% /SPAIN 10 YR BOND YIELD UP TO 1.32%

3j Greek 10 year bond yield RISES TO : 4.02

3k Gold at $1253.70 silver at:15.99 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 20/100 in roubles/dollar) 63.31-

3m oil into the 74 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.61 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9918 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1608 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.32%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.86% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.98%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

With Trade War Looming, Futures Spike On

Report Of US-EU Auto Tariff Talks

Bulletin Headline Summary from RanSquawk

- European equities positive as auto names drive gains, on suggestions that US is ready to give car tariffs a break

- UK markets react to an upbeat Carney after the BoE chief suggests Q1 softness was largely due to weather

- Looking ahead, highlights include, US ADP, ISM non-MFG, DOEs, FOMC minutes, and ECB’s Weidmann and Mersch

With trade war between the US and China set to begin at midnight on Friday, the market is taking on a surprisingly relaxed attitude, and after S&P futures rose yesterday even as human traders were out on vacation, this morning S&P futures have continued their ascent and are back to where they were before the waterfall drop just before Tuesday’s close when China announced it would prohibit Micron from temporarily selling chips in China.

In advance of the grand trade war start, on Wednesday China Mofcom said China will respond if US implements tariffs, while Customs states that tariffs on US goods will immediately take effect after US tariffs on China are in place; however as China has said just this many times before, the market took the news in stride and largely ignored the latest threat.

It wasn’t just the US that was in a better mood this morning, but most European markets as well, if only for the time being.

The Stoxx Europe 600 was lifted by carmakers which rebounded on hopes of a cross-Atlantic tariff deal, after Handelsblatt reported the U.S. Ambassador to Germany told the country’s automakers he was asked by Washington to reach a solution between Berlin and Brussels on car tariffs. Specifically, Washington would support lowering car tariffs to zero for U.S. and European carmakers; the report added that the bosses of Volkswagen, Daimler and BMW as well as the head of parts maker Continental were in attendance. While it was unclear if Germany would accept such a broad zero-tariff regime, the market took the news as an indication of a softening in Trump’s stance, even though this is a verbatim replica of what Trump has already floated previously.

Elsewhere, recently battered Glencore Plc rose over 3% after announcing it’ll buy back as much as $1 billion of its shares, following the report earlier this week that it was being the target of a DOJ money-laundering probe.

Meanwhile, after the PBOC intervened verbally (and physically) in the yuan market on Tuesday, the Chinese currency barely budged – at least in the context of Tuesday’s gargantuan, 1200 pip intraday move, and despite a sharply higher fixing in the onshore Yuan, one which was once again stronger than the Wall Street consensus, the freely traded offshore Yuan went nowhere as the currency appears to have flatlined for the time being.

The return of stability to the Yuan did not help Chinese stocks, however, where the equity bear market deepened, with the Shanghai declining again, its 15 drop in the past 20 days, and the index closing at its lowest level since March 2016. The index is now 23.2% off its January highs.

China’s weakness dragged the MSCI Asia ex-Pac index lower by another 0.5% to 162.58, and pushed Japan’s Nikkei down 0.8% to 21,546.99, Hong Kong’s Hang Seng Index down 0.2%, and S. Korea’s Kospi 0.4% lower to 2,257.55. Still, the losses was relatively more manageable than in the sharp rout seen in recent days.

Elsewhere in FX, the Bloomberg Dollar Spot Index headed for its third day of declines, having touched a three-week low, and has now wiped out half its gains following the ECB’s unexpectedly dovish QE-taper-but-will-keep-rates-lower-for-longer announcement from mid-June.

The euro rose above $1.17 following hawkish rhetoric from ECB policymakers with Bloomberg reporting on Wednesday that some ECB policy makers are uneasy that investors aren’t betting on an interest-rate hike until December 2019, suggesting a move in September or October next year could be on the cards. The common currency was further boosted by Germany’s factory orders for the month of May surging 2.6% m/m, well above a forecast of 1.1% gain.

The pound held steady as U.K. Prime Minster Theresa May continues to seek backing for her vision of Brexit and after BOE’s Carney said tighter policy will be needed. The biggest gain versus the dollar was seen in the Swedish krona, boosted this week by hawkish central bank rhetoric according to which Sweden may hike rates before the end of the year.

In rates, U.S. Treasuries slipped alongside European counterparts. 10Y yields were 3bps higher at 2.86%, pushed the 2s10s spread from the flattest since 2007 after it hit 30bps on Tuesday. The yield on 10Y Germany bunds also rose three basis points to 0.34%, the highest in more than a week on the biggest increase in more than three weeks.

Brent crude fell as traders weigh tightening U.S. supplies against a pledge from Saudi Arabia to expand output. Emerging-market shares dropped for the eighth time in nine days, and developing-nation currencies nudged lower. Commodities, heavily exposed to international trade, fell. Iron ore futures in Singapore hit the lowest since May.

In the latest news surrounding the neverending Brexit saga, Theresa May is said to have asked Chancellor Hammond and Business Secretary Clarke to warn colleagues of the dangers in pressing for a hard Brexit at the meeting on Friday at Chequers. Elsewhere, there were also reports that ministers warned PM May not to sidestep controversial Brexit issues at the meeting amid concern focus on customs may neglect issues such as services sector and freedom of movement.

In the biggest central bank news overnight, Bloomberg reported that some ECB policymakers are said to be concerned regarding some investors’ expectations for a hike in end-2019 as they view this as too late, according to sources which also suggested that the door is open for possible rate move in September or October next year. The news sent the EUR higher and repriced rate hike expectations. Elsewhere, ECB’s Praet says the uncertainty about the inflation outlook has been declining significantly, and the risk of deflation has vanished, there are grounds to be confident that the sustained convergence of inflation will continue in the period ahead. Added that the expectation is that policy rates will remain at their present levels at least through the summer of 2019 and, in any case, for as long as necessary

Also overnight BoE Governor Carney said data gives him confidence that the soft UK economy in Q1 was largely due to weather and not economic climate; reiterating tighter monetary policy will be needed. Added that pay and domestic cost growth have continued to firm broadly as expected, widespread evidence that slack is largely used up. Meanwhile, BoJ Board Member Masai said it may take some time to reach to reach 2% price goal and that it is appropriate to continue with strong monetary easing in a persistent and sustainable manner. Furthermore, Masai also suggested that structural problems in the banking industry should be discussed independently from monetary easing.

Today’s economic data include initial jobless claims, Markit PMI readings, but all attention will fall on the FOMC minutes, with traders scanning for hints of a dovish relent by the Fed after the recent repricing of a total of 4 rate hikes in 2018.

Market Snapshot

- S&P 500 futures up 0.4% to 2,724.00

- STOXX Europe 600 up 0.4% to 381.50

- MXAP down 0.5% to 162.58

- MXAPJ down 0.2% to 529.85

- Nikkei down 0.8% to 21,546.99

- Topix down 1% to 1,676.20

- Hang Seng Index down 0.2% to 28,182.09

- Shanghai Composite down 0.9% to 2,733.88

- Sensex down 0.05% to 35,626.24

- Australia S&P/ASX 200 up 0.5% to 6,215.52

- Kospi down 0.4% to 2,257.55

- German 10Y yield rose 2.9 bps to 0.334%

- Euro up 0.3% to $1.1687

- Brent Futures down 0.5% to $77.86/bbl

- Italian 10Y yield rose 1.8 bps to 2.388%

- Spanish 10Y yield rose 3.5 bps to 1.334%

- Brent Futures down 0.5% to $77.86/bbl

- Gold spot down 0.04% to $1,254.48

- U.S. Dollar Index down 0.1% to 94.40

Top Overnight News

- The U.S. imposition of tariffs on $34 billion of China’s exports will not only hurt China, but the U.S. itself and the rest of the world. That’s because $20 billion of those goods are produced by foreign companies, including American companies, Gao Feng, China’s Commerce Ministry spokesman said Thursday

- China’s proposed additional tariffs on U.S. goods will become effective “immediately” after the U.S. imposes its levies, according to a statement on General Administration of Customs Thursday

- U.K. Prime Minister Theresa May is fighting to win Cabinet backing for her Brexit plan as a compromise proposal that aimed to unite warring ministers was rejected by her chief negotiator — Brexit Secretary David Davis

- Oil traded near $74 a barrel as investors weighed tightening U.S. supplies against a pledge from Saudi Arabia to expand output. Meanwhile, President Donald Trump lashed out at OPEC

- Investors from Japan have plowed record amounts into U.S. stocks, corporate bonds and agency-backed securities, pushing investments in those assets past $1 trillion for the first time ever this year. That’s a stark contrast to the big pullback from Treasuries, which has cut Japan’s holdings to a seven-year low

- Italy’s new government will have both tax cuts and a universal basic income in its very first budget to show financial markets the coalition isn’t backing down from its agenda, Finance Minister Giovanni Tria said. The sweeping economic program is aimed at proving to investors that the populist administration is serious about its mission

- Friday July 6 is the date when the world’s two largest economies are due to slide deeper into a trade conflict that’s roiled markets and cast a shadow over the global growth outlook.

- Some European Central Bank policy makers are uneasy that investors aren’t betting on an interest-rate hike until December 2019, according to people familiar with the matter. A move in September or October next year is in the cards, the people said, even though the decision will be data dependent

- German factory orders surged in May, ending a string of declines and suggesting a much- awaited pick-up in growth momentum in Europe’s largest economy

Asian equity markets were cautious from the open ahead of this week’s key risk events and following the US holiday closure, with sentiment later deteriorating as focus turned to the looming July 6th tariffs. Nikkei 225 (-0.8%) initially struggled for direction and remained at the whim of the currency before trade war fears eventually took its toll, while ASX 200 (+0.5%) bucked the trend with upside led by strength in telecoms and the heavily-weighted financials sector. Elsewhere, Hang Seng (-0.2%) and Shanghai Comp. (-0.9%) began choppy after the PBoC skipped open market operations for a net liquidity drain of CNY 140bln which coincided with its previously announced targeted RRR cut taking effect, before trade concerns and fears of a full-blown trade war proved to be the deciding factor. Finally, 10yr JGBs saw mild gains and approached closer to the 151.00 level, with the late support seen as risk sentiment soured on tariff fears and which also followed firmer demand in the 30yr auction. PBoC skipped open market operations for a net daily drain of CNY 140bln, although its previously announced targeted RRR cut took effect from today, which is said to release CNY 700bln of funds. PBoC set CNY mid-point at 6.6180 (Prev. 6.6595)

Top Asian News

- Top Manager Sticks With Samsung Before Results, Defying Analysts

- Philippines CPI Smashes Forecasts in ‘Setback’ for Espenilla

- Beauty Turns Ugly: Cosmetic Stock Implodes After Leading World

- China Says U.S. ’Fully’ Understands its Stance over Trade

Automotive names are driving European stocks higher after reports of compromises being close on auto tariffs, with a reduction in tariffs being touted. As such the DAX is outperforming on the back of strength in index heavy-weights Daimler (+3.9%), Volkswagen (+4.3%), BMW (+5.2%) and Continental (+2.8%), with traders eyeing the 100DMA of 12,515 on the upside, currently trading at 12,454. Peugeot (+3.3%) and Michelin (+3.0%) are also driving the CAC, with the bourse breaking through its 100DMA and approaching its 200DMA of 5,374. Further support is offered to the French index after Sodexo (+6.7%) reported positive sales figures. Associated British Foods (-4.6%) reported uninspiring earnings, and have increased concerns over their sugar business not meeting profit targets. This is pressuring consumer staples (-0.5%) which is currently the worst performing sector. The materials sector is outperforming on the back of mining names (FTSE 350 mining index +1.9%) moving in sympathy with Glencore (+3.3%) post announcement of a USD 1bln share repurchase. Linde (+1.3%) have said that a sale of Praxair’s European gas businesses will allow for a merger clearance by the European Commission. Praxair have agreed to sell their assets to Taiyo Nippon Sanso

Top European News

- Italy to Start Sweeping Economic Program With Upcoming Budget

- Euro-Area Bonds Decline on Conviction ECB May Raise Rates Sooner

- SBM Slumps as Brazil Decision Keeps Company From Largest Market

- Primark Sticks to Cautious U.S. Expansion Plans as Sales Gain

In FX, The EUR currency has extended gains vs the Usd through the 1.1700 handle and first heavy expiry option hedges at the strike (2.3 bn today, and a further 1.7 bn on Friday), albeit briefly, in wake of latest ECB sources claiming market expectations for an end 2019 rate hike would be too late, and with perhaps some added momentum from upbeat German data (industrial orders). Eur/Jpy also boosted by M&A-related flows, but capped around 129.50 and just ahead of its 55 DMA (129.54). GBP/CAD/CHF/JPY – All relative stable vs the Greenback, with Cable building a firmer base above 1.3200, but not able to clear 1.3250 and its 21 DMA just above ahead of a speech from BoE Governor Carney and the next big Brexit event (Chequers on Friday). In the event the MPC head was positive on growth and the inflation outlook, lifting near term rate hike expectations and the Gbp through the aforementioned psychological and technical resistance levels albeit briefly. The Loonie is essentially stuck around 1.3150, Franc equally tight within 0.9940-10 bounds and hardly responding to in line Swiss CPI data (albeit weaker vs the Eur circa 1.1600), while the Jpy hugs 110.50 eyeing decent expiries between there and 110.60 (1 bn). SEK – Onward and upward for the Krona, and latest catalyst comes in the form of strong Swedish data (industrial output), with further gains vs the Eur that is strong in its own right, as mentioned earlier – Eur/Sek inching close towards 10.2000.

In commodities, Oil prices were down with WTI languishing around the USD 74 level after US President Trump reiterated his position on Twitter overnight vs. OPEC of prices being too high. This was reversed in later trade however, with WTI positive and Brent negative on the day as traders look ahead to today’s holiday-delayed DoE inventory report. In the metals scope Gold is pulling back after hitting a one week high in yesterdays trade of USD 1,261/oz, currently at USD 1,253/oz. Base metals are slipping as the threat of a trade war looms, with zinc and nickel sulking around one-year lows. Copper is also being hit by these worries, with the bellwether metal down 2.8% in Shanghai.

Looking at the day ahead, the main focus will likely be the release of the FOMC meeting minutes for the June 13th policy meeting. We algo get the final June services and composite PMIs due along with the June ISM non-manufacturing, and June ADP employment change reading. The latest weekly initial jobless claims data will also be due. Away from that, BoE Governor Mark Carney is due to speak at an event in Newcastle while the ECB’s Mersch and Nowotny along with Bundesbank President Jens Weidmann will also be speaking at different times at the Central Bank of Austria’s annual conference.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -4.8%

- 8:15am: ADP Employment Change, est. 190,000, prior 178,000

- 8:30am: Initial Jobless Claims, est. 225,000, prior 227,000; Continuing Claims, est. 1.72m, prior 1.71m

- 9:45am: Bloomberg Consumer Comfort, prior 57.3

- 9:45am: Markit US Services PMI, est. 56.5, prior 56.5; Composite PMI, prior 56

- 10am: ISM Non-Manf. Composite, est. 58.3, prior 58.6

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Just as you thought it was safe to leave the office in Europe last night and relax knowing that nothing was going to happen in the US due to the holiday, along comes a Bloomberg news story after 6pm in Frankfurt suggesting that “some ECB policy makers are uneasy that investors aren’t betting on an interest-rate hike until December 2019”. It was a big headline but as DB’s Mark Wall pointed out the article really only hinted that September and October were thought to be mis-priced. DB’s George Saravelos also made the point that markets had probably gone too far the other way in terms of not pricing the first 20bps hike until March 2020. He also made the valid point that we were reaching the limits of divergence between ECB and Fed policy expectations. If the ECB market pricing is right, it’s probably because the world is struggling (e.g. major Italy problems or a full trade war) and the Fed will have to pause. If the Fed is correct, the ECB will likely have to move earlier or more than currently priced. Overall Mark Wall still thinks the first 20bp deposit rate hike/25bp refi rate hike will be in September 2019. The Euro jumped 25c on the story but it happened too late to impact bond yields.