GOLD: $1177.05 DOWN $1.05 (COMEX TO COMEX CLOSINGS)

Silver: $14.69 UP 14 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1174.50

silver: $14.68

GOLD AND SILVER LAST NIGHT WERE HEADED TO THE CLEANERS AS THE BANKERS WERE SETTING UP A CAPITULATION DAY. AFTER SUPPLYING A CONSIDERABLE SHORT POSITION AT 8:30 PM TO INITIATE THE HUGE RAID, THE CROOKS WERE ROBBED AFTER CHINA ANNOUNCED THAT THEY WERE COMING TO WASHINGTON FOR TRADE TALKS. THAT REVERSED GOLD/SILVER THE DOLLAR AND THAT SET THE STAGE FOR TODAY.

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 119 NOTICE(S) FOR 11,900

TOTAL NOTICES SO FAR 2197 FOR 219,700 OZ (6.8335 tonnes)

For silver:

AUGUST

273 NOTICE(S) FILED TODAY FOR

1,365,000 OZ/

Total number of notices filed so far this month: 1053 for 5,265,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6378/OFFER $6463: UP $78(morning)

Bitcoin: BID/ $6307/offer $6391: UP $7 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1178.22

NY price at the same time:$1172.20

PREMIUM TO NY SPOT: $6.02

XX

Second gold fix early this morning: $ 1180.43

USA gold at the exact same time:$1176.05

PREMIUM TO NY SPOT: $6.02

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY ONLY 3740 CONTRACTS FROM 240,621 DOWN TO 236,298 DESPITE YESTERDAY’S HUGE 56 CENT LOSS IN SILVER PRICING AT THE COMEX. WE HAVE GENERALLY BEEN WITNESSING A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS BUT THAT STOPPED ABRUPTLY WITH THE RAID. HOWEVER, WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 4 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

4355 EFP’S FOR SEPT. , 378 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 4733 CONTRACTS. WITH THE TRANSFER OF 4733 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4733 EFP CONTRACTS TRANSLATES INTO 23.665MILLION OZ AND ACCOMPANYING:

1.THE 56 CENT FALL IN SILVER PRICEAT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, AND NOW 5.375 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

17,570 CONTRACTS (FOR 12 TRADING DAYS TOTAL 17,570 CONTRACTS) OR 87.850 MILLION OZ: (AVERAGE PER DAY: 1464 CONTRACTS OR 7.320 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 87.850 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.54% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,917.51 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3740WITH THE HUGE 56 CENT LOSS GAIN IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 4733 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 993 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4733 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 3740 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 56 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.50 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 5.375 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL IN SILVER.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.184 MILLION OZ TO BE EXACT or 169% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 273 NOTICE(S) FOR =1,365,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 5.375 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 3230 CONTRACTS UP TO 479,969 DESPITE THE HUGE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $15.15). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 11,399 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 0 CONTRACTS, OCTOBER HAD 0EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 11,399 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 479,969. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,629 CONTRACTS: 3230OI CONTRACTS INCREASED AT THE COMEX AND 11,399 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 14,629 CONTRACTS OR 1,462,900 OZ = 45.50 TONNES. AND ALL OF THIS HUMONGOUS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $15.15.???..THIS IS A TOTAL FRAUD

YESTERDAY, WE HAD 8678 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 90,171 CONTRACTS OR 9,017,100 OZ OR 280.46 TONNES (12 TRADING DAYS AND THUS AVERAGING: 7514 EFP CONTRACTS PER TRADING DAY OR 751,400 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 280.46 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 280.46/2550 x 100% TONNES = 9.70% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,999.10* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3230 DESPITE THE HUGE LOSS IN PRICING ($15.15 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A VERY STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,399 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,399 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC GAIN OF 14,629 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,399 CONTRACTS MOVE TO LONDON AND 3230 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 45.50 TONNES). ..AND THIS HUGE DEMAND OCCURRED DESPITE A HUGE LOSS OF $15.15 IN YESTERDAY’S TRADING AT THE COMEX!!!. ????

we had: 119 notice(s) filed upon for 11900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.05 TODAY: /

LATE LAST NIGHT:

A BIG CHANGES IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 2.06 TONNES AND THIS GOLD WAS USED IN THE RAID/AND ATTEMPTED RAID LAST NIGHT.

TONIGHT: ANOTHER BIG CHANGE IN INVENTORY: 1.18 TONNES OF GOLD WAS REMOVED FROM INVENTORY/

.

/GLD INVENTORY 773.41 TONNES

Inventory rests tonight: 773.41 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 14 CENTS TODAY

A BIG CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.881 MILLION “PAPER’ OZ/

/INVENTORY RISES AT 329.104 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 3230 CONTRACTS from 240,038 DOWN TO 236,298 (BUT STILL WITHIN SPITTING DISTANCE TO A NEW COMEX RECORD. THE LAST RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD TO THAT WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..VERY STRANGE INDEED AND IT WILL COME TO FRUITION AGAIN VERY SHORTLY

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR AUGUST., 4355EFP CONTRACTS FOR SEPTEMBER, 378 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4733CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3108 CONTRACTS TO THE 4733 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 993 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 8.125MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 5.375 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE PHYSICAL DEMAND OCCURRED DESPITE A HUGE 56 CENT PRICING LOSS AT THE SILVER COMEX!!!!????.

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE HUGE 56 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 4733EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 18.07 POINTS OR 0.66% /Hang Sang CLOSED DOWN 222.53 POINTS OR 0.82%/ / The Nikkei closed DOWN 12.18 POINTS OR 0.05%/Australia’s all ordinaires CLOSED DOWN 0.05% /Chinese yuan (ONSHORE) closed UP HUGELY at 6.8877 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 64.95 dollars per barrel for WTI and 70.84 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8973: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

3 c CHINA

i)Last night, we were scheduled to have a massive downdraft in gold/silver. however that was negated by a report that a Chinese delegation is coming to the USA to discuss trade talks. The spec shorts were caught off-guard.

( zerohedge)

ii)A super commentary from James Rickards on the Chinese plan re the currency/trade war with the USA

China will sacrifice the stock market for “people stability”

a must read…

( James Rickards)

iii)China did what Turkey did yesterday: making it very costly to short the yuan

( zerohedge)

4. EUROPEAN AFFAIRS

i)Italy

Italy’s investment in infrastructure is alarmingly low and a good reason why the Genoa bridge collapsed due to poor maintanence

( zerohedge)

ii)The EU fears that British spies have bugged the secret Brexit talks

( zerohedge)

iii) Italy

(courtesy zerohedge)

iv)Greece/Turkey

An up to date story on the two Greek soldiers who have been finally returned to Greek soil after being held in detention after wandering onto Turkish territory. The Turkish Supreme Court has rejected Pastor Brunson’s appeal for release..

( Raul Meijer)

v)Italy

A bomb detonates at the Italian Headquarters of Salvini’s league Party just outside of Turino. An anarchist party is claiming responsibility

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

Early morning trading: gold up/dollar down, rouble up

(zerohedge)

Philly Fed manufacturing crashes to pre election lows

(courtesy zero hedge)

b)I think we can prepare to sit shiva for JCPenny as they are about to default

( zerohedge)

iv)SWAMP STORIES

a)King pin of the Russian collusion scandal,Brennan goes nuclear after losing his security clearance/

writes an Op -edin the New York Times and then he proceeds to his safety net at CNN

( zerohedge)

b)There was a frantic email to Bruce Ohr from Christopher Steele hoping that there would be ‘firewalls” in place. This occurred in March 2017 two days before Comey was to testify!! Are the firewalls..the insurance policy

Let us head over to the comex:

FOR THOSE THAT WISH TO FOLLOW TODAY’S SILVER OI VS LAST YR

AUGUST 16.2017: 98,418 OPEN INTEREST CONTACTS STILL OPEN FOR THE UPCOMING SEPT ACTIVE CONTRACT MONTH VS TODAY AUG 15.2018: 133,128 CONTRACTS.(DEMAND REMAINS EXTREMELY STRONG DESPITE THE LOWER PRICE)

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

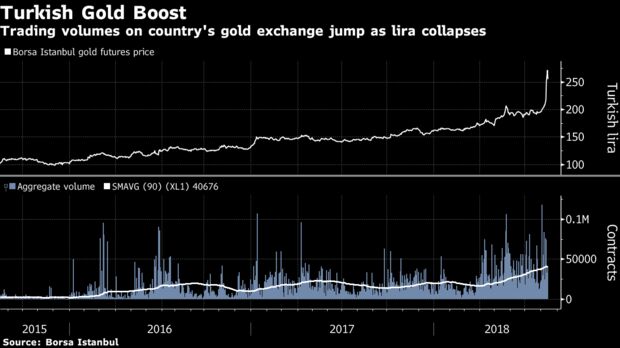

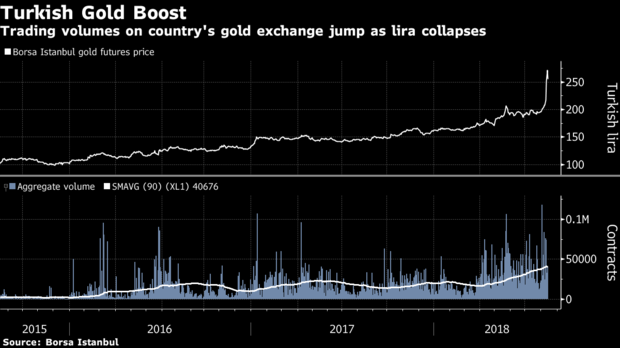

Gold And Silver Prices Fall Sharply To Near 2 Year Lows Despite Strong Demand In Turkey

Gold and silver prices fell sharply again yesterday and were down 1.6% and 4.3% respectively to multi-month lows.

Gold drifted lower all day and ended near its late session low of $1173.20/oz, its lowest since January 2017, for a loss of 1.6%. Gold in euros has been more robust of late and it fell to about €1036/oz.

Silver saw another bout of intense selling on the futures market and was pushed as low as $14.37/oz. There was no economic news or silver related developments that would account for the deepening sell-off.

It is again a purely futures-related price action with no refineries, mints or dealers reporting a sudden selling of silver bullion. Quite the opposite, contrarian gold and silver buyers are again accumulating coins and bars on the dip.

Demand for gold jewellery and gold bars is strong in Turkey due to the currency crisis. Gold trading volumes on the Turkish Gold Exchange (Borsa Istanbul) have more than doubled and gold prices in Turkish lira have surged by more than a third since March as reported by Bloomberg. Or rather the Turkish lira has collapsed in value by a third versus gold.

The sharp falls in the precious metals is being attributed to dollar strength. The U.S. dollar is holding steady near a recent peak for now, despite the increasingly precarious fiscal outlook as Trump’s reckless government spending has seen the national debt surge to $21.35 trillion – an increase of $1.45 trillion since Trump, the “King of Debt”, took office.

The precious metals are now near their lowest in nearly 2 years despite the very favourable backdrop of heightened geo-political and economic risks due to trade wars and concerns that the financial crisis in Turkey could lead to a wider global financial crisis.

Concerns about the financial crisis in Turkey, and its impact on the EU in particular, and China and the global economy’s health are badly impacting emerging market currencies. This has led to safe-haven demand for gold, but this is not resulting in gold, or silver, being bought in the futures market.

Counter-intuitively, the opposite is happening again and this has led some analysts to again believe that the gold and silver prices are being manipulated lower on futures markets. This could be done purely for profit motives by hedge funds and banks and or due to official intervention in order to curtail safe-haven demand, depress sentiment towards the precious metals and maintain confidence in risk assets and the wider markets (see GATA.org and Gold & Silver Being Hit Like In 2008 To Cover-Up Impending Global Financial Crisis).

As ever, it remains prudent to take a long-term view. Contrarian investors, value investors and bullion buyers, while rightly frustrated will either simply sit out the latest bout of contrived price weakness or accumulate gold and silver again at these depressed prices (see It’s Time for Contrarians to Get Bullish on Gold).

News and Commentary

Gold prices sink to 19-month low amid strong dollar (Reuters.com)

Gold Refuses to Shine for Investors in Search of a Haven (Bloomberg.com)

Dow just registered its longest stint in correction territory in nearly 60 years (MarketWatch.com)

Home builder sentiment hits 11-month low as trade war takes a hit (MarketWatch.com)

U.S. household debt rises to $13.3 trillion in second quarter (Reuters.com)

Source: Bloomberg

Gold And Silver Manipulated Lower As Was Case In 2008 (InvestmentResearchDynamics.com)

Gold Trading Volumes Double in Turkey Amid Currency Crisis (Bloomberg.com)

UK housing stagnation rather than collapse seems more likely scenario for now (MoneyWeek.com)

Cashout: FBI Warns Of Imminent Global ATM Hack (Independent.co.uk)

Africa Rising: US may be a powerful country, but it is on the decline (DavidMCWilliams.ie)

Gold Prices (LBMA AM)

15 Aug: USD 1,186.70, GBP 933.10 & EUR 1,047.74 per ounce

14 Aug: USD 1,195.30, GBP 935.32 & EUR 1,049.11 per ounce

13 Aug: USD 1,204.40, GBP 944.85 & EUR 1,058.19 per ounce

10 Aug: USD 1,211.65, GBP 947.87 & EUR 1,056.44 per ounce

09 Aug: USD 1,215.50, GBP 944.08 & EUR 1,048.13 per ounce

08 Aug: USD 1,212.35, GBP 939.57 & EUR 1,045.17 per ounce

Silver Prices (LBMA)

15 Aug: USD 14.83, GBP 11.66 & EUR 13.10 per ounce

14 Aug: USD 15.04, GBP 11.77 & EUR 13.18 per ounce

13 Aug: USD 15.18, GBP 11.91 & EUR 13.35 per ounce

10 Aug: USD 15.37, GBP 12.04 & EUR 13.41 per ounce

09 Aug: USD 15.48, GBP 12.01 & EUR 13.35 per ounce

08 Aug: USD 15.35, GBP 11.93 & EUR 13.24 per ounce

Recent Market Updates

– London House Prices Fall At Fastest Annual Rate Since Height Of Financial Crisis

– Jim Rogers on Gold, Silver, Bitcoin and Blockchain’s “Spectacular Future”

– This Week’s Golden Nuggets

– The Stock Market is Stretched to Double Tech-Bubble Extremes

– Jim Rogers and the World’s New Reserve Currency

– Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed

– Jim Rogers – Making China Great Again! (Video)

– This Week’s Golden Nuggets

– Gold to Enter New Bull Market – Charles Nenner

– Here’s Where the Next Crisis Starts

– House prices aren’t just slipping in the UK – this is global

– Russia Sells 80% Of Its US Treasuries

– Are China’s Gold Reserves Slowly Rising?

– Gold Outlook In H2 2018

– Gold Production In South Africa Continues To Collapse – Plummets 85% From Peak In 1970 (VIDEO)

– Physical Gold Is The “Best Defence” Against “Escalating Currency Wars”

– Trump and War With China? Goldnomics Podcast

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8827/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS //OFFSHORE YUAN: 6.8977 /shanghai bourse CLOSED DOWN 18.07 POINTS OR 0.66% /HANG SANG CLOSED DOWN 222.53 POINTS OR 0.82%

2. Nikkei closed DOWN 12.18 POINTS OR 0.05%/USA: YEN RISES TO 110.87/

3. Europe stocks OPENED ALL GREEN

//USA dollar index FALLS TO 96.59/Euro RISES TO 1.1376

3b Japan 10 year bond yield: FALLS TO . +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.95 and Brent: 70.84

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.320%/Italian 10 yr bond yield UP to 3.12% /SPAIN 10 YR BOND YIELD UP TO 1.43%

3j Greek 10 year bond yield RISES TO : 4.30

3k Gold at $1181.25silver at:14.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 27 /100 in roubles/dollar) 67.03

3m oil into the 64 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.87 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9933 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1300 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.32%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.05%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Relief rally in the Turkish lira…no developments at all…

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Surge, Yuan Jumps And Dollar Drops

As China-US To Resume Trade Talks

Heading into Thursday trading, global stocks were set for another downbeat session when China’s Ministry of Commerce broke news broke that – at the invitation of the US – China would send its Vice Commerce Minister, Wang Shouwen, to the U.S. for low-level trade talks in late August, the first official exchanges since earlier negotiations broke down two months ago. The Chinese delegation would meet with an American group led by David Malpass, under secretary for international affairs at the Treasury.

The news – which the market immediately interpreted as an opportunity for an end in the trade war between the US and China – sparked a furious risk-on rally, which sent US futures, the offshore Yuan, and other risk assets surging, while the dollar and Treasuries slumped.

Maybe the market got ahead of itself again because the upcoming talks will be at a relatively low level: “This will be ‘talks about trade talks,’” said Gai Xinzhe, an analyst at the Bank of China’s Institute of International Finance in Beijing. “Lower-level officials will meet and haggle and see if there is a possibility for higher-level talks.” Yet for some reason, despite several rounds of failed talks to date, the market reaction clearly shows that investors are hopeful for successful negotiations.

And while Asian stocks had to catch up to US selling of tech stocks in the aftermath of the Tencent earnings debacle, both Europe (with the exception of Italy, whose stocks slumped after Atlantia shares crashed the most since 1987 following the Genoa bridge tragedy) and US futures have held on to gains and the result is yet another (mostly) sea of green this morning as yesterday’s drop has been faded.

Still, as Gai Xinzhe, a Bank of China’s analyst noted, “Even if the senior officials reach a deal, things could still change, as President Trump can easily flip-flop. We have been there”, he said quoted by Bloomberg.

Others agreed: “The news (of the China-U.S. trade talks) triggered short-covering but I think fundamentally it is of limited significance,” said Yasuo Sakuma, chief investment officer at Libra Investments.

One thing that could make China more amenable is that Beijing is – for now – a loser in the currency war. China’s equity market has suffered declines and the yuan has been on a losing streak for more than a month. Chinese authorities, bracing for economic fallout, have introduced measures to support growth ranging from shifting toward a more accommodative monetary policy to boosting fiscal spending.

Which however begs the question why the US would invite China, especially if Trump is winning, if only for the time being.

In any case, the market decided to buy, and ask questions later, and it certainly did that with the Chinese Yuan, which gained the most in three weeks, rising as much as 1.1% earlier, and currently trading at 6.8955 per dollar from around 6.9400 earlier…

… not only on the upcoming trade talks between China and the U.S. and stronger-than-expected fixing, but also a surge in the 12 month forward points, the latest attempt by China to force buy the Yuan, as currency bears were violently squeezed as the cost to short surged the most since 2016 (more on that shortly).

And as US equity futures and the Yuan rebounded on fresh hopes of easing trade tensions, so did European stocks while the dollar fell for the first time in 6 days and Treasuries dipped.

After dipping into a bear market yesterday, the Stoxx Europe 600 Index rose, with most sectors in the green, however there was one outlier: Italian stocks declined as infrastructure company Atlantia SpA’s shares fell by almost one-fifth in the wake of a deadly bridge collapse. UK Retail Sales for July smashed expectations, rising 0.7% vs. Exp. 0.2%. ONS said that clothing sales possibly boosted by extended discounting, world cup and sunshine supported food sales.

Earlier, Asian equities had hit one-year lows overnight as they tracked Wednesday’s global falls and Tencent results disappointed, though pared declines after the Chinese news of possible de-escalation in the trade war. Chinese stocks pare losses, with both Shanghai Composite Index and Hong Kong’s Hang Seng index each down 0.8%. Earlier in the day, Shanghai was down as much as 1.9 percent while Hong Kong was off 1.7 percent. Japan’s Nikkei average closed 0.1% lower in choppy trade, with the benchmark falling as much as 1.5% before a brief swing into positive territory on China news.

Meanwhile, the crash across Emerging Markets halted, as EM currencies fought to regain their footing on Thursday, while the story of earlier this week, the Turkish Lira collapse, seeming ever more like a distant memory as the Turkish currency rose again, the USDTRY sliding from 6.00 to below 5.80, an increase in the value of the Lira of over 16% since Monday, its best three-day run since 1994.

A drop in the dollar and the sight of the lira striding back above 6 per dollar, coupled with a sharply higher Chinese yuan also steadied emerging market currencies like South Africa’s rand, Russia’s ruble and Mexico’s peso. And while EM stocks nudged lower again though after they entered a bear market on Wednesday, metals markets clawed higher, however, after copper had also entered ‘bear’ territory.

Summarizing the latest state of global chaos, SocGen’s FX strategist Kit Juckes said “the Chinese are heading to Washington and yuan bounced, the Qataris are heading to Ankara and the lira bounced and has left everything else floating around really.” He added that it was still too early to sound the all clear around Turkey – its new finance minister and son-in-law of President Tayyip Erdogan will hold a global conference call later – and that the broader worries were still around the extent of China’s economic slowdown.

Meanwhile, markets were still shaken by the weak earnings from Tencent: the Chinese tech giant which holds a 40 percent stake in the U.S. firm that makes cult game Fortnite reported its first quarterly profit fall in nearly 13 years on weak gaming revenue. That knocked other Asian tech firms with South Korea’s Samsung Electronics, Asia’s third largest firm by market cap, down to a one-year low, although the trade news quickly llifted market sentiment.

The tentative recovery in risk appetite also saw bond benchmark German Bund and U.S. Treasury yields, which move inverse to the bond’s price, nudge up.

In FX, the Bloomberg Dollar Spot Index slips from the highest level in more than a year as some dollar bulls take profits following confirmation that the U.S. and China would resume trade talks. Broad improvement in risk sentiment also weighed on the greenback as Treasuries slipped and European stocks edged higher. The Turkish lira headed for its best three-day run since 1994 while the pound advanced, snapping a two-day decline, after U.K. retail sales beat estimates.

The Australian dollar led Group-of-10 gains as news China and the U.S. are resuming trade talks outweighed earlier short- selling spurred by a miss in the employment change; the euro rebounded to touch 1.1398 day high while the yen was the worst performer among G-10 currencies amid improved risk appetite. The Norwegian krone was little changed against the euro after the central bank confirmed what was already expected by markets, namely that a hike most likely will come in September.

In other news, the Norwegian Key Policy Rate remained unchanged at 0.50% as expected. The Norges Bank said the outlook and balance of risks don’t appear to have changed substantially since the June report and the outlook and balance of risks suggested that the key policy rate would most likely be raised in Sept. 2018. The upturn in the Norwegian economy is continuing broadly in line with expectations set out in June and Underlying inflation is below target, but driving forces indicate it will rise further out.

President Trump stated tariffs will rescue the US steel industry, while he also stated he is considering interview with Special Counsel Mueller. In addition, there were separate reports that US President Trump’s team is preparing to oppose a potential subpoena from Special Counsel Mueller.

Elsewhere, metals rebounded after a hammering on Wednesday. Gold turned higher after touching a 19-month low. In Hong Kong, currency interventions continued after the currency fell to the weak end of its trading band.

And though metals strengthened, oil prices were left flat after data showed a surprise weekly increase in U.S. crude stockpiles, compounding worries about a weaker global economic growth. Brent was at just over $70 a barrel and U.S. crude oil CLc1 last stood at $65.12 per barrel, having fallen to two-month lows of $64.42 per barrel, following Wednesday’s 3.2 percent fall.

Expected data include jobless claims and housing starts. JD.com, Madison Square Garden, Applied Materials, and Nvidia are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.3% to 2,829.50

- STOXX Europe 600 up 0.3% to 380.74

- MXAP down 0.5% to 161.00

- MXAPJ down 0.4% to 519.08

- Nikkei down 0.05% to 22,192.04

- Topix down 0.6% to 1,687.15

- Hang Seng Index down 0.8% to 27,100.06

- Shanghai Composite down 0.7% to 2,705.19

- Sensex down 0.3% to 37,754.35

- Australia S&P/ASX 200 down 0.01% to 6,328.29

- Kospi down 0.8% to 2,240.80

- German 10Y yield rose 1.4 bps to 0.318%

- Euro up 0.3% to $1.1384

- Italian 10Y yield rose 13.7 bps to 2.895%

- Spanish 10Y yield fell 1.4 bps to 1.436%

- Brent futures little changed at $70.74/bbl

- Gold spot up 0.4% to $1,179.83

- U.S. Dollar Index down 0.1% to 96.57

Top Overnight News

- Turkey President Recep Tayyip Erdogan moved to shore up alliances in Europe and the Middle East, easing pressure on the battered lira, as the standoff between Turkey and the U.S. deepened

- Russian officials are hoping the U.S. president may yet be able to deliver on his promises of improving relations — or at least head off pressure growing in Congress for even more draconian sanctions, according to officials and others close to the leadership

- U.K. retail sales bounced back strongly in July amid warmer weather and extended discounts at stores. Sales gained 0.7 percent from June, compared with a median estimate of a 0.2 percent gain in a Bloomberg survey.

- Deutsche Bank fixed- income traders generated a $35 million profit in two weeks as economic turmoil in Turkey triggered a slump in assets across emerging markets, according to people with knowledge of the matter

- The Bank of Japan may allow long-term interest rates to rise to around 0.4% under the new guidance introduced last month, Reuters reports, citing an interview with former BOJ executive Hideo Hayakawa

- Italy’s fatal bridge collapse has further hit returns in the euro area’s worst-performing major corporate-bond market this year

Asian equity markets traded lower across the board on spill over selling from Wall Street where all majors declined amid a tech and energy rout, although the announcement of US-China trade talks provided some glimmer of hope. ASX 200 (-0.1%) and Nikkei 225 (-0.1%) were negative from the open as Australia was weighed by a slump across commodities including the 3% drop in oil and with hefty opening losses in Japan as exporters bore the brunt of a firmer JPY. Elsewhere, Hang Seng (-0.8%) conformed to the negative tone after index heavyweight Tencent sparked off the global tech rout, and ended Asia-Pac -3%, due to its first profit decline in 13 years and the Shanghai Comp. (-0.6%) slipped to a 2½-year low alongside the broad weakness which had earlier dragged the MSCI EM Index into bear market territory. However, sentiment then improved and some of the regional majors nearly pared all their losses after reconciliation hopes were spurred by news that China’s Vice Commerce Minister is to visit US for trade discussions later this month. Finally, 10yr JGBs head into the European morning flat although price action was choppy overnight alongside the tumultuous tone in riskier assets, while today’s 5yr auction failed to spur demand as the b/c and accepted prices

declined from prior

Top Asian News

- China’s Tumbling Equities Now Look Very Attractive, to Some

- China’s Yuan Surges Most Since January, Rebounding From 2017 Low

- Yuan Bears Squeezed as Cost to Short Surges the Most Since 2016

- China Pork Producer WH Group Plunges on Swine Fever Concern

European stocks have started the day higher (ex-Italy) amid an improved risk tone, as China and the US are to have renewed trade talks, and Qatar are said to invest USD15bln into Turkey. The DAX has bounced from 6 week lows seen on Wednesday and is back in positive territory with the DAX’s gains led by SAP (+2.5%). The FTSE is the outperforming bourse and is up ~0.4%. Both these bourses are being driven by tailwinds from positive Cisco earnings yesterday, and improved US-Sino relations, lifting the IT sector into outperformance. The FTSE MIB is the marked underperformer after Atlantia (-15%) shares failed to open for just under an hour, and eventually started the day down 23%. This comes after both playing catch-up after yesterday’s index closure, and news that the Italian Government is seeking reparations after the Genoa Bridge disaster on Tuesday

Top European News

- Henkel Slumps After Higher Chemical Prices Force Outlook Cut

- Norway Keeps Rates Unchanged on Path to Tightening Next Month

- U.K. Retail Sales Rebound in July on Warm Weather, Discounts

- Wages Jack Up Czech Factory Prices to Boost Case for Rate-Hikes

In FX, EMs saw risk revival emanating from the region after reports that Turkey will get a much needed financial boost from Qatar ($15 bn) ahead of the Finance Minister’s investor call that could tempt others to follow suit. Meanwhile, plans are afoot for China and the US to engage in trade talks before the next scheduled exchange of import tariffs come into effect, and collectively this has given the Lira more recovery momentum (Usd/Try back down and more convincingly below 6.0000), alongside the Yuan (Usd/Cnh sub-6.9000 vs almost 6.9500 at one stage, and even though the PBoC pushed up the Usd/Cny mid-point again, to 6.8946 from 6.8856 on Wednesday) and other contagious EM currencies. DXY – The index has duly retraced further amidst the broad improvement in sentiment having stopped a fraction short of 97.000 yesterday and is currently pivoting around 96.500. AUD/NZD/EUR – The biggest beneficiaries from latest Chinese and Turkish-related news having borne the brunt in the G10 sphere when aversion was more prominent. Aud/Usd has bounced firmly from near 0.7200 lows above 0.7250, but looks capped ahead of a hefty 1 bn option expiry at 0.7300 and somewhat undermined by mixed Aussie jobs data overnight. The Kiwi has also pared recent losses to just south of 0.6550, though like its antipodean counterpart seems top heavy approaching the next big figure, as does the single currency at 1.1400 vs its circa 1.1300 base. However, the failure to break barriers at that level and trip stops below reportedly caught several shorts cold and forced a squeeze when Eur/Usd rebounded to and through 1.1350. NOK – No real reaction to the Norges Bank, as the accompanying statement merely confirmed previous guidance that flags a 1/4 point hike at the next policy meet on September 20. Eur/Nok relatively rangy between 9.5750-6130.

In commodities, WTI and Brent are essentially flat, with WTI and Brent languishing around the USD 71.00/BBL & USD 65.00/BBL levels respectively. Gold is modestly benefitting from a USD that is set for its first fall in over a week, with the yellow metal up ~0.5% on the day, and testing the USD 1180/OZ level to the upside after breaking through its 50 DMA in the early morning. Base metals have recovered after yesterday’s sell-off, with all of lead (+4%), zinc (+3.4%) and copper (+1.9%) rising off the back of an improved risk tone owed to mending US-Sino trade relations.

Looking ahead to today, we get the August Philadelphia Fed PMI along with July building permits and housing starts data. Walmart, Gap, and Nordstrom will also report earnings.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 215,000, prior 213,000; Continuing Claims, est. 1.74m, prior 1.76m

- 8:30am: Philadelphia Fed Business Outlook, est. 22, prior 25.7

- 8:30am: Housing Starts, est. 1.26m, prior 1.17m; Housing Starts MoM, est. 7.42%, prior -12.3%

- 8:30am: Building Permits, est. 1.31m, prior 1.27m; Building Permits MoM, est. 1.39%, prior -2.2%

- 9:45am: Bloomberg Economic Expectations, prior 53.5; Bloomberg Consumer Comfort, prior 59.3

DB’s Jim Reid concludes the overnight wrap

The proverbial hole in the wall for markets this last week has been Turkey. However there were quite contrasting moves yesterday as Turkey rallied but the rest of the risk complex started to see a delayed reaction. The Turkish lira rose +6.36% (17.4% from intra-day lows on Monday) firstly because of early morning moves by the Banking Regulation and Supervision Agency to limit funds’ access to lira liquidity in the offshore swap market and later in the day on headlines (per FT) that Qatar plans to invest $15bn into the Turkish economy. The former now makes it harder for investors to borrow the currency from local lenders and short it. The latter news seemed to help wider markets recover from the lows as we’ll see below. Also a quick mention that DB’s Oliver Harvey and team have taken a closer look at who’s lent money to Turkey across its external debt, portfolio assets and FX loans

The irony is that whilst Turkey has had a good 36 hours, the rest of global markets seem to be suffering from a delayed contagion reaction yesterday. Although there was risk off across the board, the highlight was Italy where 10 year yields climbed 13.7bp and edging above levels seen at the end of May (and to 4-year highs) when there was a constitutional crisis and 70 basis points higher than the recent lows of 2.47% back on July 18. Meanwhile, the spread to 10-year Bunds (now at +286 bps) is within 4 basis points of their May wides. Two-year Italian yields rose 12bps but remain 140 bps lower than the end-May highs, reflecting that this episode is not indicative of an immediate crisis of confidence but rather a re-rating of risk. Nevertheless, the moves were impressive given that yesterday was a public holiday in Italy. Perhaps that was part of the problems in that there was no local money to stand in the way of the international risk off.

Risk is stabilising a bit overnight as it looks like high level trade talks between the US and China will be back on. This morning, Bloomberg noted that at the invitation of the US Department of Treasury, a Chinese delegation led by Vice Commerce Minister Wang will travel to Washington later this month for more talks. Following on, equities in Asia have recovered from session lows to trade modestly lower. The Hang Seng (-0.61%), Kospi (-1.03%), Nikkei (-0.21%) and Shanghai Comp. (-0.87%) are all down. Meanwhile futures on the S&P are pointing to a firmer start and the Yuan is stronger while the Lira is down c0.9%. Datawise, Japan’s July trade deficit was wider than expected at -231bn Yen (vs. -41bn Yen expected), in part as exports grew at a slower than expected rate of 3.9% yoy. After the bell in the US, Cisco also jumped +6% after guiding to higher than expected sales growth for the current quarter. Meanwhile on Turkey, the White House spokeswoman Ms Sanders noted that “the tariffs that are in place on steel (by the US) won’t be removed with the release of Pastor Brunson” while German Chancellor Merkel seems to be signalling some support as she noted “no one has an interest in the economic destabilisation of Turkey”.

Now turning to equity volatility. After moving back towards the cyclical lows this time last week, we’ve spiked back up this week, especially in Europe. At 18.48 the V2X is all of a sudden at the highest level since the Italian led spike at the end of May and has now only been higher for two days since early April when it was still adjusting lower after the February vol spike. The VIX rose +1.3pt to 14.64 after an intra-day spike to 16.82 late morning US time.

That spike in vol coincided with the lows of the day for the S&P 500 (-1.32%) but the market stabilised and rallied around the time of the Turkey/Qatar headlines and closed -0.76% lower. Losses were concentrated in energy and materials stocks, with those two sectors down 3.53% and 1.55%, as the commodity complex sold off broadly. Brent crude oil shed 2.35% to $70.76 per barrel, its lowest level in over 4 months. This is partially a result of the strong dollar, which, despite trading flat yesterday, remains within a few basis points of its highest level in over a year. Sentiment in the sector was not helped by US Department of Energy data at 3:30pm London time, which showed US crude oil inventories increased by 6.8 million barrels last week. That’s the biggest inventory build since March 2017, and was contrary to consensus expectations which had called for a 2.9 million barrel draw down. This increase in oil stockpiles is against the typical seasonal pattern where consumers increase their consumption amid summer driving trips, and the risk is it could signal softer demand moving forward. Other commodities also dropped yesterday, with LME copper futures falling 4.02% to their lowest level in over a year, while Zinc and Lead also tumbled -6.28% and -7.09% respectively.

Sentiment was further depressed by poor earnings from Chinese internet giant Tencent, announced around 11:00am London time. Revenue and profit both fell short of expectations, with the latter actually declining yoy. Exuberance around the tech sector accordingly cooled somewhat, as investor concerns about valuations and growth deceleration resurfaced. The NASDAQ index lagged other major indices in the US, falling -1.23% and the NYFANG index of the biggest tech companies shed -1.62%. Separately, Macy’s posted solid earnings in the US, with sales and profits exceeding consensus, but the stock still traded -16.0% lower, impacted by investors’ concerns on higher than expected cost growth and discounting of goods (YTD share price +39.5%). Elsewhere Sears (-13.1%) and JC Penney (-8.7%) also dropped in sympathy.

Developments in foreign exchange markets also weighed on equity markets yesterday. The Chinese yuan which had rallied a bit this morning broke above the closely-watched 6.90 level yesterday, and the weakening continued throughout the US trading session to touch an intraday level of over 6.95. This is the yuan’s weakest level versus the dollar since last January, though the Chinese currency has remained stable over the last week against the authorities’ tradeweighted basket. Asian currencies continued their recent outperformance versus other EM currencies thanks to this stability, but equity markets will probably remain attentive to the yuan’s continued slide against the dollar, as it has had a strong negative relationship with US equities this year (i.e. higher/weaker dollar-yuan exchange rate is associated with weaker stocks). So far, the weaker yuan has not reflected capital outflow pressures like in 2015-2016, but it could signal underlying weakness in the Chinese economy. Further weakness also raises the odds of further, market-unfriendly rhetoric and policies from the US administration. Having said all this, our China economists published a piece this week where they pointed to a loosening of financial conditions, which are expected to have some stimulative effect on growth by 1H 2019. Meanwhile they believe the Yuan will be under further depreciation pressure and expect USDCNY to reach 6.95 by end-2018 and 7.40 by end-2019.

Back to yesterday, in fixed income Treasuries rallied along with German bunds. The 10-year Treasury closed at 2.86% and near the bottom of its recent range. The 2-year 10-year curve flattened back to 25 basis points, one basis points off of its recent low reached in mid-July. Bank stocks, which tend to perform better amid higher yields and a steeper curve, completely retraced yesterday’s gains, though their bonds held up well. The CDX IG and HY indexes widened 1.3 and 5.7 basis points, respectively, and on a single-name basis, energy firms again underperformed.

Looking ahead to today, the euro area trade balance will print at 10:00am London time, followed by the August Philadelphia Fed PMI along with July building permits and housing starts data. Walmart, Gap, and Nordstrom will also report earnings.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 18.07 POINTS OR 0.66% /Hang Sang CLOSED DOWN 222.53 POINTS OR 0.82%/ / The Nikkei closed DOWN 12.18 POINTS OR 0.05%/Australia’s all ordinaires CLOSED DOWN 0.05% /Chinese yuan (ONSHORE) closed UP HUGELY at 6.8877 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 64.95 dollars per barrel for WTI and 70.84 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8973: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

Last night, we were scheduled to have a massive downdraft in gold/silver. however that was negated by a report that a Chinese delegation is coming to the USA to discuss trade talks. The spec shorts were caught off-guard.

(courtesy zerohedge)

Yuan, Futures Jump On Report China Delegation Coming To US To Discuss Trade

The Yuan is surging, alongside S&P futures, while the Japanese Yen has erased its gains and US Treasury futures are slumping on a Bloomberg report that China’s Vice Commerce Minister, Wang Shouwen, will lead a delegation to the U.S. in late August, the Ministry of Commerce says on website, adding that the visit comes at the invitation of the US.

Additionally, China reiterates that it opposes unilateralism and trade protectionism, and won’t accept any unilateral trade restriction measures. It also “welcomes communications and dialogue on the basis of equality and integrity.”

The news is quickly being interpreted by the market as a possible thaw in the trade war tit-for-tat, and has sent H-shares sharply higher, while S&P futures jumped 10 points:

And as the dollar index slides…

… the USDJPY popped back in the green…

… while 10Y yields spiked to 2.875% and the USDCNH tumbled by 200 pips, from 6.9420 to just over 6.920.

In the general risk-on wave oil, which tumbled earlier on the massive DOE inventory build, has also caught a bid.

The news may explain why the PBOC fixed the onshore far stronger than the offshore yuan suggested, because as some desks have suggested, the last thing China will want when it comes to the US is a plunging Yuan.

So is this the end of the trade war? Hardly: after all, a Chinese delegation visited the US not that long ago, and just before Trump announced even more tariffs. Furthermore, why would Trump seek to end the “trade war” when the US is clearly winning based on the US vs Chinese stock market, and the divergence in economic growth.

For the time being, however, the market mood is clearly risk on.

end

A super commentary from James Rickards on the Chinese plan re the currency/trade war with the USA

China will sacrifice the stock market for “people stability”

a must read…

(courtesy James Rickards)

Rickards On China’s Plan To Tank Its Own Stock Market

Authored by James Rickards via The Daily Reckoning,

When I say the fix is in for FXI that’s not meant to be mysterious. FXI is the ticker symbol for a U.S. exchange-traded fund (ETF) composed of the largest Chinese stocks.

The phrase “the fix is in” simply refers to government-backed manipulation. When you combine the two into a government plan to tank their own stock market, at least to a point, you’re as close to a sure thing as stock market indexes allow these days. That’s exactly what’s going on in China right now.

A currency devaluation will likely lead to a stock market collapse, but it’s a trade-off China is willing to accept because a cheaper currency will stimulate exports and support jobs.

China’s motives in market manipulation are about social stability more than profit and loss. Of course, the Chinese have nothing against making money; they’re good at it. But China is controlled by a Communist Party dictatorship that is most concerned about its self-perpetuation.

That self-perpetuation can involve prison camps, thought control and torture if needed, but on a day-to-day basis it’s more likely to involve avoidance of inflation, unemployment and market panics (versus slow, steady declines).

Investors with vague or no recollection of the 1989 Tiananmen Square protest and massacre in Beijing have been taught to recall the event as a “pro-democracy” student rally complete with a 33-foot-tall papier-mâché statue called the Goddess of Democracythat was destroyed as the military cleared the square. That’s a highly selective and misleading portrait of the overall protest.

It’s true that student demonstrators placed demands for more freedom of the press and freedom of speech in their petitions. Yet the origins of the protest were economic. Rapid economic growth in the 1980s had resulted in large gains for some but had marginalized and disgruntled many others.

Inflation was a real tax on those with limited resources and an easily avoided inconvenience for the rich. It was these economic grievances — inequality and inflation — that gave rise to the protests. The pro-democracy aspects were tacked on in the later stages as the crowds grew.

Initially the Communist Party leadership was divided between moderates, like Zhao Ziyang, who favored some dialogue with the protesters, and hard-liners, like de facto leader Deng Xiaoping, who favored a forced breakup of the protest and the arrest of its leaders.

In the end, the hard-liners got the upper hand and the result was a violent military attack on the demonstration. Death estimates vary widely and cannot be verified but range from 1,000 to 10,000 dead protesters. Communist Party leadership itself was thrown into chaos in the aftermath of Tiananmen with Zhao Ziyang being purged and Jiang Zemin being installed as the new hard-line party leader.

This statue, located at the University of British Columbia in Vancouver, is a replica of the Goddess of Democracy first displayed during the Beijing Tiananmen Square protests in April–June 1989.

The ghosts of Tiananmen still haunt the Communist Party leadership almost 30 years later. Economic warfare between China and its trading counterparties is not mainly about economics. It’s mainly about social stability in China, which means avoidance of new mass protests and suppression of widely voiced political dissent.

This econo-political history brings us to the ongoing trade war between China and the U.S. A superficial account of the trade war says it was started by President Trump last winter with his imposition of tariffs on Chinese (and other) goods imported into the U.S. including steel, aluminum and certain appliances.

China retaliated with tariffs on U.S. imports. Trump doubled down with U.S. tariffs on a much longer list of Chinese goods and imposed penalties for Chinese theft of U.S. intellectual property.

China retaliated again, and Trump doubled down again. These tit-for-tat tariffs were rising in $10 billion bumps. Suddenly the happy talk about posturing and empty threats was swept aside. A full-scale, red-hot trade war was underway.

This recent outline is accurate as far as it goes. Yet it leaves out a much longer and more complicated backstory. On Dec. 11, 2001, China was formally admitted to the World Trade Organization, WTO, the legal successor to the General Agreement on Tariffs and Trade, GATT, one of the original Bretton Woods institutions from 1944.

China’s admission to the WTO was the result of years of negotiations and substantive concessions on the part of China. Despite those perceived concessions, China secretly pursued the same policy it has used at the U.N. Security Council, the IMF and other multilateral organizations it has joined in recent years.

Here’s an easy metaphor that captures Chinese behavior: Imagine you’re on the admissions committee at an exclusive club. Your club has a strict dress code that involves jackets, ties and leather shoes even on casual occasions.

A new potential member has applied. They go through the interview process, bring recommendations are informed about the dress code and agree to strict adherence. The new member is admitted. The next day the new member shows up at the bar in cutoffs, flip-flops and a T-shirt.

Your club has a problem.

China’s the same way. They go through rigorous vetting. The organization rules and procedures are carefully explained. China agrees to play by the rules and is formally admitted. The next day, China proceeds to break every rule in the book and, in effect, dares the leadership to sanction them. The sanctions never arrive.

The group has a problem.

From this perspective, the trade war did not begin in 2018; it began in 2001. It was not started by President Trump; it was started by China through rule breaking, theft of intellectual property, export dumping and slow-rolling open markets.

When China joined the WTO, its trade surplus with the U.S. was about $100 billion per year. Today China’s trade surplus with the U.S. is about $400 billion per year and rising. This surplus is in addition to the theft of over $600 billion of intellectual property. The 17-year wealth transfer from the U.S. to China now exceeds $3 trillion.

Viewed this way, Trump’s 2018 tariffs on China were not the start of a trade war. They were a desperate effort to stop one before the U.S. is looted further by the Chinese.

In the short run, China has been able to see Trump’s ante every time Trump increases tariffs. Yet China is crucially weak on this front. The U.S. imports about $500 billion per year in goods from China and exports about $100 billion to China. The difference is the $400 billion per year trade deficit the U.S. runs with China.

China is getting close to tariffs on 100% of U.S. imports. The U.S. can still impose tariffs on another $400 billion of Chinese imports. This is what Trump referred to when he said the U.S. cannot lose the trade war with China because “we already lost.”

Trump’s hope is that China will see it’s playing a losing hand, meet Trump for negotiations and settle on lower tariffs all around. This could expand bilateral trade and be a boost to the global economy.

So far, China has not sought reconciliation. Instead it has injected a currency war tactic into the trade wars to give it more leverage than would otherwise exist. Here’s a chart that shows the radical devaluation of the Chinese yuan, CNY, against the dollar, USD, in the past four months:

Chart 1

In the past four months, the Chinese yuan (CNY) has collapsed 8.5% against the U.S. dollar (USD). From 6.28 to 6.88 per dollar. This is a greater collapse than the August 2015 3% “shock” devaluation that triggered an 11% U.S. stock market collapse. This new devaluation will continue as part of China’s play in the trade wars. This time a Chinese stock collapse is a more likely result.

This currency devaluation is China’s reply to Trump. If the yuan dropped 20% against the dollar, Chinese export costs would drop by about the same amount because yuan unit labor costs are a huge part of Chinese manufacturing costs.

If Chinese export costs are $100 per unit, a 20% devaluation will lower those costs to $80 per unit. A 25% U.S. tariff on the new $80 baseline will raise the export cost to $100 — exactly where it started.

China has discovered that devaluation is a near-perfect offset to tariffs. The devaluation tactic not only lowers Chinese export costs; it increases U.S. export costs, as shown in Chart 2 below.

Chart 2

With the trade wars and currency wars now commingled, what are my predictive analytic models telling us about the prospects for Chinese stocks in particular and China more broadly?

Right now, they’re telling us that China is not backing down from its aggressive response to Trump’s tariffs. The Trump team shows no inclination to back down either. The result will be constricted bilateral trade and slower growth at the margin for both countries.

A declining Chinese stock market, as reflected in the FXI price, will be collateral damage in this escalating struggle. It’s not a result that China wants, but it’s a price they will pay in order to keep Chinese citizens employed and assembly lines humming.

Lower unit labor costs combined with higher U.S. tariffs will shift wealth from Chinese enterprises to U.S. importers, but there should be little change in the local currency earnings and job security of Chinese workers. That’s the line in the sand the Communists will defend.

The combined trade and currency wars are like a perfect storm aimed at FXI. Wall Street is misreading these developments, but you don’t have to.

end

China did what Turkey did yesterday: making it very costly to short the yuan

(courtesy zerohedge)

China Crushes Yuan Bears As Cost To Short Yuan Soars Most Since 2016

One day after Turkey unleashed measures to crush Turkish Lira shorts, China did the same and on Thursday, the offshore Yuan tumbled by 0.7% from as low as 6.94 to 6.8825 – the biggest drop since July 25 – after the offshore Yuan’s 12 month forward points soared from 350 bps to 830bps, the biggest one-day move since January 2016 – sending the cost of short bets against the Yuan soaring, with the spike in CNH forward points making it riskier, and more expensive, to short the Yuan.

Separately, CNH tomorrow-next forward points soared as much as 15.7 to 15, before paring the increase to 3 in an attempt to force stops by Yuan shorts.

“Two reasons are supporting the yuan today: the restart of China-U.S. trade talks, and the widespread market rumor that some banks at Shanghai free-trade zone are not allowed to lend the yuan to offshore banks,” a move that could squeeze liquidity, said Scotiabank’s Gao Qi. “The yuan may stabilize at the current level or even strengthen in the near term, as sentiment improves on the trade front. Its fate in the longer-term hinges on the trade talks and Turkey.”

A Reuters report confirmed the move was driven by China limiting CNH liquidity to increase cost of shorting CNH, similar to what Erdogan did to Lira shorts earlier this week. Specifically, China banned banks in its free trade zones from certain lending activities to ease pressure on the yuan currency in offshore markets.

The restrictions, announced by the Shanghai branch of the PBOC on Thursday morning, closed off channels used to deposit and lend yuan offshore through the trade zones as the currency plumbs 15-month lows. They prevent commercial banks from using some interbank accounts to deposit or lend yuan offshore through free trade zone schemes. And while the restriction on offshore yuan deposits and lending applies to some Free Trade Accounting Unit (FTU) businesses, it is not meant to affect cross-border capital flows that reflect real demand, according to the notice.

The yuan surged on the news, adding to earlier gains that were fueled by a stronger-than-expected daily fixing from the central bank and a report that Chinese and U.S. officials will engage in low-level trade talks later this month.

“Many offshore investors unwound their short yuan positions today,” said Zhou Hao, senior emerging markets economist at Commerzbank AG in Singapore.

As Bloomberg notes, Chinese authorities have been trying to limit bets against the yuan after the currency depreciated more than 9% since March, approaching the closely watched level of 7 per dollar. While a weaker exchange rate has helped Chinese exporters weather the impact of U.S. President Donald Trump’s tariffs, policy makers worry that a disorderly drop could trigger capital outflows and threaten China’s financial stability; it could also lead to further anger among the Trump administration and accusations of devaluation, just as a Chinese trade delegation is set to come to Washington.

As the yuan’s slump has accelerated in recent weeks, the People’s Bank of China has taken several steps to slow its drop. Two weeks ago, the central bank made it costlier to place short bets against the currency with forwards. And last week, the monetary authority urged big banks to avoid bearish momentum trades.

To be sure, the PBOC’s response has been well rehearsed: during a similar selloff in the Yuan in 2015 and 2016, Chinese authorities squeezed yuan bears by lifting offshore funding costs dramatically. They also spent billions in foreign-exchange reserves to buy the currency and clamped down on capital outflows.

While the government’s response this time around has been much less extreme, policy makers have sent a clear message that they want to avoid disorderly swings in the exchange rate, according to Carie Li, an economist at OCBC Wing Hang Bank in Hong Kong.

“PBOC’s bottom line is to prevent one-way yuan depreciation,” Li said. “Investors probably have unwound short-yuan positions amid fear of further intervention.”