GOLD: $1187.60 UP $2.65 (COMEX TO COMEX CLOSINGS)

Silver: $14.32 DOWN 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1194.50

silver: $14.32

FOR THE NEXT TWO WEEKS, MY COMMENTARIES WILL BE DELIVERED BUT NOT AT MY USUAL TIME. I WILL GET IT DONE BUT IT IS INCREASINGLY MORE DIFFICULT TO WRITE

SO TRY AND CLICK ON AFTER 6:30 PM

THANKS

H

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: `1 NOTICE(S) FOR 100 OZ

Total number of notices filed so far for OCT: 851 for 85100 OZ (2.649 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 296 for 1,480,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6597: DOWN $53

Bitcoin: FINAL EVENING TRADE: $6631 DOWN 15

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 795 CONTRACTS FROM 200,648 DOWN TO 199,853 DESPITE YESTERDAY’S HUGE 33 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED A FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR OCT. 1733 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1733 CONTRACTS. WITH THE TRANSFER OF 1733 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1733 EFP CONTRACTS TRANSLATES INTO 8.665 MILLION OZ ACCOMPANYING:

1.THE 9 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 1,590,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

18,652 CONTRACTS (FOR 8 TRADING DAYS TOTAL 18,652 CONTRACTS) OR 93.26 MILLION OZ: (AVERAGE PER DAY: 2331 CONTRACTS OR 11.657 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 93.26 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.31% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,312.78 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 795 DESPITE THE 9 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2166 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED:938 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1733 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 795 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 9 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.39 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.999 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER:1,590,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 5281 CONTRACTS DOWN TO 465.253 DESPITE THE RISE IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A GAIN IN PRICE OF $2.00.THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY GOOD SIZED 5416 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 5416 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 465,253. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY TINY SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 135 CONTRACTS: 5281 OI CONTRACTS DECREASED AT THE COMEX AND 5416 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 135 CONTRACTS OR 135000 OZ = 0.419 TONNES. AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.00??? GO FIGURE!!

YESTERDAY, WE HAD 12092 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 63,316 CONTRACTS OR 6,331,600 OZ OR 198.90 TONNES (8 TRADING DAYS AND THUS AVERAGING: 7915 EFP CONTRACTS PER TRADING DAY OR 827,100 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 198.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 198.09/2550 x 100% TONNES = 7.76% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,864.46* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 5281 DESPITE THE GAIN IN PRICING ($2.00 THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD AN STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5416 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5416 EFP CONTRACTS ISSUED, WE HAD A TINY GAIN OF 135 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5416 CONTRACTS MOVE TO LONDON AND 35281 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 0.419 TONNES). ..AND ALL OF LACK OF DEMAND OCCURRED WITH A GAIN OF $2.00 IN YESTERDAY’S TRADING AT THE COMEX.???

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.65 TODAY: /

NO CHANGE IN INVENTORY

/GLD INVENTORY 730.17 TONNES

Inventory rests tonight: 730.17 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 7 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 332.912 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 795 CONTRACTS from 200,648 DOWN TO 199,853 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1733 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1733 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 795 CONTRACTS TO THE 1733 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 938 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 4.69 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW 1.590 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1733 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

) WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 4.82 POINTS OR 0.14% //Hang Sang CLOSED UP 20.16 POINTS OR 0.05% //The Nikkei closed UP 36.65 OR .16%/ Australia’s all ordinaires CLOSED up 0.14% /Chinese yuan (ONSHORE) closed WELL DOWN at 6.9253 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 74.79 dollars per barrel for WTI and 84.62 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9253 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9321: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Saudi Arabia/Turkey

The Washington Post now publishes images of the Saudi journalist (dissident) walking into the Istanbul consulate but he never leaves as we was killed and dismembered

( zerohedge)

ii)Unbelievable!! The USA knew of the Saudi plan and went along with it. Turkey releases footage of the “hit team”

( zerohedge)

6. GLOBAL ISSUES

Your most important paper. Goldman delves into the latest BIS report and they have sounded the alarm bell on a derivate volcano blowing up; the big reason: Europeans plus Japanese can no longer get swaps in order to buy USA bonds. The cost of acquiring the swaps exceeds the yields.

Now the big question: who will buy the huge 1.8 trillion of USA bonds that need to be funded this year

(David Goldman/Asia Times)

7. OIL ISSUES

Oil slumps sto 2 week lows after a huge crude build

( zerohedge)

8 EMERGING MARKET ISSUES

i)ARGENTINA

9. PHYSICAL MARKETS

i)Craig Hemke is stating the obvious; the banks are not on our side

( Craig Hemke)

ii)USA gold’s October letter fears a stock market crash and talks about Italy’s threat to Eurozone unity.

( USA Gold/GATA)

iii)gold demand from Chinese citizens faltered a bit last month; nothing to worry about

(courtesy Lawrie Williams)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

Both wholesale inventories and wholesale sales were very strong in the 4th quarter and that will help Trump dramatically in the 4th quarter GDP numbers which may except 45

( zerohedge)

b)Trump will finally get his wall as a 23 billion funding will be introduced this week

( zerohedge

e)Trump after being informed that the Dow was down 1000 points and the Nasdaq down over 5% states that the Fed has gone crazy. He just threw Powell under the bus…

iv)SWAMP STORIES

a)Wray states that the Kavanaugh background probe was consistent with the Kavanaugh probes

( zerohedge)

b) the King report/

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a gain of 0 contracts to stand at 5 contracts. We had 0 notices filed YESTERDAY so we gained 0 contracts or NIL oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we lost 9 contracts up to 466 contracts. After November, we have a December contract and here we lost 1764 contracts down to 163,663

AND NOW COMPARISON FOR OCTOBER:

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

“Gold Is On The Cusp” Of An “Explosion Higher” As Stock and Tech “Crash Is Coming”

“The Crash Is Coming” As “Money-Printing Never Works” Warns Hickey

by Christoph Gisiger via FUW.ch

Few investors have a deeper understanding of the tech sector than Fred Hickey.

The renowned editor of the popular investment newsletter «The High-Tech Strategist» draws alarming parallels to the bursting of the dotcom bubble in the year 2000 and spots high risks in stock market darlings like Amazon and Apple.

For the industry veteran, one important reason to be concerned are rich valuations. He also sees troubles ahead with respect to the rise in interest rates and the growing mountain of debt around the world.

Against this background, the outspoken contrarian sees bright opportunities in gold and in attractively priced mining stocks.

About Fred Hickey

For many investors around the world, Fred Hickey’s monthly newsletter is a must read. It’s a unique treasure of deep knowledge that goes way beyond the tech sector. Having grown up in Lowell, Massachusetts, in the heartland of the computing cluster around Route 128, Mr. Hickey has been fascinated by technology since his youth. After graduating from the University of Notre Dame, he started working for the former telecom giant General Telephone & Electronics. In 1987, he began writing his newsletter for his friends and family. After just five years it went so well that he could make a living out of his investing tips. Today, Mr. Hickey who likes to take long walks in his rare spare time, lives far away from Wall Street in Nashua, New Hampshire, and in sunny Costa Rica.

Mr. Hickey, despite raising interest rates, global trade tensions and turmoil in the emerging markets the stock market in the United States is chasing one record after record. How long will this go well?

Today’s situation reminds me of the fall 2000 which was a very difficult time for me as a contrarian investor. The internet bubble had broken in March when the Nasdaq peaked at 5132 and all those crazy valued dotcom stocks had crashed. In the three weeks after the Nasdaq had peaked it looked like the whole stock market had broken. But it hadn’t because investors rotated into what they perceived to be safer big cap tech names. So, they piled into stocks like Intel, Cisco, Microsoft, Nortel, EMC and Sun Microsystems. And that’s what we’re seeing today in a similar way with stocks like Amazon, Apple and, again, Microsoft.

What happened next?

Once we got into September and October, the market started to roll over. Back then, I was short via puts a number of tech stocks. My biggest short position was Intel and the stock first went higher and higher. In August 2000, Intel rose 20% in just one month and pushed into a new high of almost 76 $ a share. For me, these were some of my toughest days trying to fight the mania. The maniacs were piling into the stock and had no clue. They were only chasing momentum – just as they’re doing it today.

But as soon as Labor Day rolled around, Intel’s shares started to fall because fundamentally the business was deteriorating. Intel had to lower its outlook and the stock crashed 45% in one month. Think about it: At that time, Intel was the second largest company in the world. It’s the equivalent of Amazon today which means that Amazon’s market cap would go from around $1 trillion to $550 billion in just one month. That’s a shocking thing. But the difference is that Intel’s P/E ratio was 55 back then. Amazon’s is 155 today.

Then again, there are also important differences. In 2000, the Fed Funds Rate was 6,5%. Today it’s hardly more than 2%. Shouldn’t that provide some kind of safety net for stocks?

The bulls argue that interest rates are very low. Therefore, they think the coast is clear. But here’s the problem: By dropping rates to zero percent or even lower central banks have encouraged the whole world to take on an enormous amount of debt. Global world debt amounts to $245 trillion and it’s up 40% since the credit crisis. They have tried to correct a debt crisis with much more debt. Just consider the US, for instance: We have more than doubled our debt up to $21.2 trillion and we added $1.4 trillion of debt in the last twelve months. So even though interest rates for US treasuries are historically still very low at this point, we are heading into severe troubles. Even with rates staying where they are today the interest expense for the US government is going to be skyrocketing in the next years just like the price of bitcoin before it broke at the end of 2017.

Why is this a problem for stocks?

This huge amount of debt is causing all kinds of other problems. With rates around the world now rising we’re probably looking at another emerging market crisis. There are some twenty countries now whose currencies have fallen by double digits against the dollar. And in the US, it’s not just the government that borrowed heavily. Consumers have borrowed a record amount of debt as well as corporations. This means that higher interest expenses will more than offsets or at least equalize the positive effects from Trump’s tax cuts – and these tax cuts are going to increase the deficit even more. Yet, the people who funded the US deficits are dropping their treasury holdings. Japan, China, Russia and Mexico have all sold a lot of treasuries. The only ones remaining who are now funding the US in a big way are the Europeans because they still have negative rates. But as rates in Europe eventually are going to rise this support could go away, too. Investors who are piling into these big-name tech stocks are not thinking about that.

You have been bearish for some time. When will judgement day come?

No one knows exactly when. In March 2000, I didn’t know that the Nasdaq would break, nor did I know that S&P 500 would break a number of months later. But today, I know that the most elusive objects of speculation, the cryptocurrencies, have broken. Also , the situation in the emerging markets is getting worse, interest rates are rising, the Federal Reserve is scaling down its balance sheet and consumers are in trouble. We’re already seeing indications of weakness in the housing market as well as in auto sales. So, it’s just a matter of time and each time the Fed raises rates further it’s a adding a straw to the camel’s back. The Fed knows that this is an extremely difficult situation even though they never admit it. Almost every time we had interest rate hike campaigns by the Fed it led to a recession and a bear market. I don’t know if history will repeat exactly. But I know it does rhyme and we’re kind of in the same situation today as we were in the fall of 2000.

But weren’t equity valuations significantly higher at that time?

True, the P/E ratios don’t look as high as they were in 2000. But other indicators do. For instance, the median price to sales ratio for the S&P 5000 is two times higher than it was in 2000. What’s more, the median price to book value is just as high as it was back then. This shows that this bubble is much broader than it was in 2000. And think about all the methods that corporations have taken in order to pump up their earnings which includes the record number of corporate buybacks and non-GAAP- earnings numbers. They do everything they can to make earnings look better than they are. If you were to take all those gimmicks out, you probably have P/E ratios just as crazy as you did in 2000. That’s how dangerous this bubble is. But there is no recognition in the market just as there was no recognition in 2000 of the danger that was ahead.

So, which of today’s mega-cap tech stock is the most vulnerable?

Some of them have already started to break. Facebook has broken. The stock is down quite a bit and, the company is under great pressure. There are regulatory issues and they are losing customers. Netflix has broken, too. But if you look at the biggest names, the ones that are still holding up, Apple looks like the most vulnerable.

Why?

Apple is a smartphone maker. But even though it has the largest market valuation in the world, it’s not the number one smartphone maker. Until recently, Apple was number two after Samsung but now it dropped to number three because Huawei, a Chinese smartphone maker, surpassed it. Also, Xiaomi which is right behind Apple is growing dramatically faster and will soon take out the number three spot.

Agreed, but Apple has successfully positioned itself as a premium brand in the smartphone market. Also, their service business shows robust growth.

But keep in mind that a lot of these services are games for smartphones. If you are losing market share and you are not selling much more smartphones you are not going to be able to sell services. A year ago, Apple announced their tenth anniversary iPhone X. It was supposed to kick off a new super-cycle like the iPhone 6 Plus did in 2014. But sales aren’t that great, and inventories rose significantly. Now, they’ve launched a series of new products like the iPhone XS Max. But these new products don’t have many new features. And right now, the Chinese makers have really good products at one third less of the price. This is what happened in the PC market, this is how people lose market share. So how the heck can you be valuing Apple at $1.1 trillion? They’re losing market share and they’re trying to raise prices in a saturated mature market. Nevertheless, the share price keeps rising which makes the stock highly vulnerable.

Which is the strongest big-cap tech stock?

I’d say Google has a better longer-term position. But let me tell you what happened in 2000 to all those big cap names: Intel’s stock, even though it was the second largest company globally, fell 80% until it bottomed. Cisco’s stock fell 90% and that was the third largest company. Nortel fell 99%, and EMC and Sun Microsystems fell 96%. So, if you’re asking which one of today’s big cap tech stocks is going to do better I would refer to Intel after the dotcom crash: It did better than the other stocks with “only” 80% decline. That’s what the future looks like today and there will be no place to hide.

So how are positioned as an investor?

Since this is a bubble I’m doing exactly what I was doing in 2000: I’m not long any tech stocks because I’m expecting a crash. When I’m bullish I like to be in stocks which generate lots of cash flow, have high margins and these are oftentimes software companies. But when I’m bearish, I want to be short – through put-options – stocks where the cash just flies out the door and where the cycles are so extreme that we get the biggest booms to busts. That’s in the semiconductor world and that’s where my focus is. The semiconductor market has topped, and some memory makers are getting hit hard already. Western Digital has gone from over $100 late last year to around $50. Micron Technology is getting hammered as well. I also have put options on Intel and Nvidia . The semiconductor equipment manufacturers are starting to get hit, too. Lam Research went from around $220 to $150 and Applied Materials is getting hit, too.

How bad will it really get? In the past decades, investors could always count on the Fed to step in when things get dicey.

There is going to be a lot of pain unless the Fed comes in and prints a heck of a lot more money. With interest rates still at these low levels, they are not going to be able to lower rates much more. In fact, when they tried to lower rates in 2007/08 it didn’t have any impact. The markets kept plunging so they had to launch quantitative easing. So, this time it’s going to be another round of quantitative easing which will hopefully indicate to the people that the central banks are never going to be able to get us out of this. Money printing never works. If it worked, everybody would have been doing it for 5000 years. A lot of governments have tried it and every time it has failed. All you get is malinvestments, overcapacities, asset bubbles and all these evil things.

So, what should investors do?

Up to the 2000 bubble I was a 100% in tech names. That worked out great because I benefited from the great bull market in the 80s and 90s. But I sold my last tech stock in late 1998 when I realized that this was a bubble. I also realized that the Fed and the other central banks were out of control. I didn’t know how out of control they would get. I don’t think anyone could have imagined that there would be trillions of dollars around the world with negative rates because this never happened before in human history. Also, I would never have imagined of $15 trillion printed around the world. All I knew for sure was that monetary policy was out of control. So, I looked around and asked myself what will do well when the central banks are going crazy? How can I protect my wealth if they are debasing the currencies in order to continue with these bubbles? And of course, historically the best way to protect your money is precious metal.

Gold and especially gold mining stocks had an amazing run in that last decade. But since 2011 gold’s glimmer seems to have faded.

Two factors were responsible for this: growing production and shrinking demand from financial investors. But now, I think the gold market bottomed in December of 2015.

Gold production is going down because many mining companies have slashed their exploration and development. There are no new major mines that have been found and there aren’t many which are being developed. That means supply has started to shrink and it will continue to shrink. On the other side, we had a great disinvestment in gold by US investors who have poured all their money into stocks. But when the stock market declines, as I expect, they are going to do what they usually do: They are going back into gold and demand will increase at the same time as supply is decreasing.

How will this impact the stocks of gold miners?

In the last gold bull market which started in 2001, gold was up 650% but the gold miners were up 17 times. Also, in the first phase of what I consider the new gold bull market which began in 2016, gold went up 30% but mining stocks went up 160%. So, you can see the leverage, especially when these stocks are depressed like today. For me as a contrarian, this is an amazing moment. On one hand, it’s a demoralizing moment like it was in 2000. But at the same time, it’s the most exciting moment since gold is on the cusp of an explosion higher.

All you have to do is to be willing to wait and to be patient for it to happen, but most people are not.

Avoid Digital & ETF Gold – Key Gold Storage Must Haves

News and Commentary

Gold inches up as retreat of bond yields weigh on dollar (Reuters.com)

Rising yields suggests ‘conflicting factors’ over U.S. growth: Fed’s Kaplan (Reuters.com)

Small-business sentiment retreats from 45-year high, NFIB says (MarketWatch.com)

Tech rebound props up Wall Street, but global growth concerns weigh (Reuters.com)

IMF cuts world economic growth forecasts on tariff war, emerging market strains (Reuters.com)

Source: Bloomberg

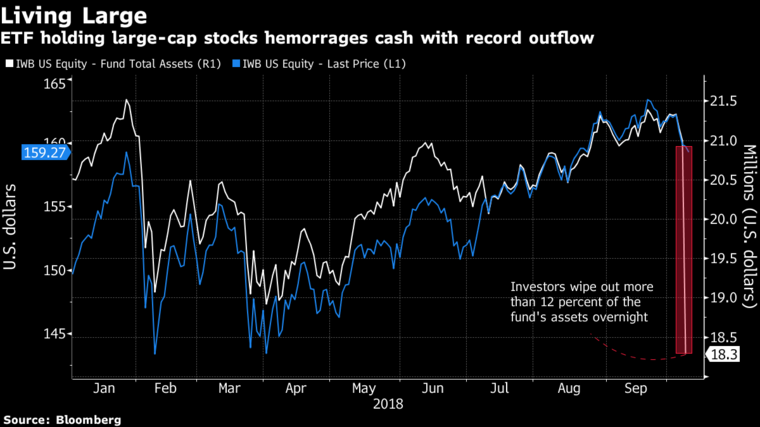

Investors Yank Record Cash Out of Stock, Real Estate, and Muni ETFs (BloombergQuint.com)

Italy’s bond yields fall after Tria makes Draghi-style pledge (Reuters.com)

Think You’re Prepared For The Next Crisis? Think Again. (PeakProsperity.com)

Blockchain Tech Coming to Commodity Markets, Blythe Masters Says (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

09 Oct: USD 1,187.40, GBP 910.26 & EUR 1,036.01 per ounce

08 Oct: USD 1,194.80, GBP 914.86 & EUR 1,040.67 per ounce

05 Oct: USD 1,201.10, GBP 921.48 & EUR 1,045.08 per ounce

04 Oct: USD 1,199.45, GBP 925.02 & EUR 1,043.28 per ounce

03 Oct: USD 1,203.50, GBP 925.73 & EUR 1,040.55 per ounce

02 Oct: USD 1,192.65, GBP 919.77 & EUR 1,035.46 per ounce

Silver Prices (LBMA)

09 Oct: USD 14.33, GBP 10.98 & EUR 12.51 per ounce

08 Oct: USD 14.47, GBP 11.10 & EUR 12.61 per ounce

05 Oct: USD 14.64, GBP 11.23 & EUR 12.73 per ounce

04 Oct: USD 14.63, GBP 11.27 & EUR 12.72 per ounce

03 Oct: USD 14.74, GBP 11.36 & EUR 12.75 per ounce

02 Oct: USD 14.51, GBP 11.20 & EUR 12.59 per ounce

Recent Market Updates

– Gold Bottoms As Gold Industry Consolidates and Weak Hands Capitulate

– 60 Charts For The (Last Few Remaining) Gold Bulls

– Poland and Australia Buy Gold As Global Property Bubble Bursts – This Week’s Golden Nuggets

– Brexit To Burst Dublin and London Property Bubbles? GoldCore Video

– Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

– “I’m Favouring Equities and Gold Over Bonds” – Stepek

– Poland Buys Gold For First Time In 20 years

– This Week’s Golden Nuggets – Central Banks, Goldman, Bank of America Positive On Undervalued Gold

– Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

– Europe Unveils “Special Purpose Vehicle” With Russia and China To Bypass SWIFT, Jeopardizing Dollar’s Reserve Status

– Gold Set to Soar Above $1,300 – Goldman and Bank of America

– Goldnomics Podcast: Silver Guru – David Morgan – Silver and Gold Will Protect in the Coming Currency Collapse

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke is stating the obvious; the banks are not on our side

(courtesy Craig Hemke)

Craig Hemke at Sprott Money: The banks are not on your side

Submitted by cpowell on Wed, 2018-10-10 00:48. Section: Daily Dispatches

8:48p ET Tuesday, October 9, 2018

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing at Sprott Money, argues tonight that futures trader positioning data does not suggest that the bullion banks are planning to profit from a short squeeze. Rather, Hemke says, the banks are letting off easy the traders who are now short, so as to maintain the old charade of a market in the monetary metals.

Hemke’s analysis is headlined “The Banks Are Not on Your Side” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-banks-are-not-on-your-side.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

USA gold’s October letter fears a stock market crash and talks about Italy’s threat to Eurozone unity.

(courtesy USA Gold/GATA)

USAGold’s October letter with market and metal commentary

Submitted by cpowell on Wed, 2018-10-10 01:00. Section: Daily Dispatches

9p ET Tuesday, October 9, 2018

Dear Friend of GATA and Gold:

USAGold’s October newsletter has been posted, with commentary about fears of a stock market crash, the spurt in sales of U.S. silver eagles, concerns about inflation, Italy’s threat to Eurozone unity, China’s acquisition of a big mine in Argentina, and more. It’s available in the clear at USAGold here:

http://www.usagold.com/publications/NewsViewsOCTober2018.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

gold demand from Chinese citizens faltered a bit last month; nothing to worry about

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: China gold demand may be faltering

Chinese gold demand, as represented by gold withdrawal figures from the Shanghai Gold Exchange (SGE), slipped in September from the same month a year earlier, but remained above the corresponding 2016 figure. The cumulative figure for the year to date remains higher than that of a year ago after nine months, but only by just over 3%. (See table below:)

Table: SGE Monthly Gold Withdrawals (Tonnes)

| Month | 2018 | 2017 | 2016 | % change 2017-2018 | % change 2016- 2018 |

| January | 223.58 | 184.41 | 225.08 | +21.2% | -0.7% |

| February* | 118.42 | 148.24 | 107.60 | -20.1% | +10.7% |

| March | 192.61 | 192.25 | 183.24 | +0.2% | +5.1% |

| April | 212.64 | 165.78 | 171.40 | +28.3% | +24.1% |

| May | 150.58 | 138.08 | 147.28 | +9.1% | +2.2% |

| June | 140.59 | 155.51 | 138.51 | -9.6% | +1.5% |

| July | 137.41 | 144.71 | 117.58 | -5.0% | +16.9% |

| August | 190.59 | 161.41 | 144.44 | +18.1% | +32.0% |

| September | 188.12 | 214.24 | 170.90 | -12.2% | +10.1% |

| October* | 151.54 | 153.25 | |||

| November | 189.10 | 214.72 | |||

| December | 185.21 | 196.37 | |||

| Year to date | 1,554.55 | 1504.70 | 1406.03 | + 3.3% | +10.6% |

| Full Year | 2,030.48 | 1,970.37 |

Source: Shanghai Gold Exchange. Lawrieongold.com

* Months include week long New Year and Golden Week holiday periods

Perhaps this is not too surprising as latest reports out of China, as reported by Bloomberg, in an independently produced PMI type survey, suggest that Chinese business confidence has dropped to the lowest level in its seven-year history in September. This is presumably a factor as the U.S. and Chinese governments imposed new rounds of tariffs on each other’s exports, escalating the Trump Administration initiated trade war.

The report highlights the latest results of an ongoing indicator from Beijing-based Cheung Kong Graduate School of Business which has dropped to its lowest level in the seven years since the graduate school started compiling these figures.

Bloomberg notes that the index is based on a survey of CKGSB students and graduates who are executives at companies operating in China. The respondents represent around 300 privately-owned small and mid-sized enterprises across several sectors of the economy. Over the last seven years, Bloomberg comments, the CKGSB index has shown bigger swings than the official PMI gauges produced by China’s National Bureau of Statistics.

What is perhaps most alarming in the report is the final commentary by the economics professor who oversees the survey. “Most surveyed companies are now experiencing unprecedented difficulties and have become increasingly pessimistic about business prospects for the next six months. For most, business has never been worse.” he says.

All this is an indicator that the ‘trade war’ is indeed beginning to bite. One suspects though that this Chinese experience may also be repeated elsewhere – even in the U.S. where the tariff impositions on Chinese imports are likely to filter through to the domestic economy in terms of price rises. The U.S high tech industry, for example, is hugely dependent on imports of Chinese-manufactured components which can not be replaced in the short’ or even the medium, term by U.S product and if the U.S. industry does gear up to raise supplies these are likely to be at a higher cost to the consumer. The Fed may be looking to a rise in inflation to help mitigate the country’s enormous debt position but this may well happen due to factors outside its control. We don’t necessarily think there will be U.S. hyper-inflation, as some commentators have been suggesting, but there certainly could be price rises across the board ahead.

But what of the latest SGE figure for September gold withdrawals? It’s probably too early to tell if this suggests the start of an ongoing downturn in gold demand – we will need to see another few months’ figures yet to be sure. The September figure was still around 10% up on the 2016 amount and the nine months cumulative total is still up on a year ago, but the lower September withdrawals could be a sign that Chinese gold demand is beginning to turn down with the economy. Only time will tell.

-END-

______________________________________________________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9253/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9321 /shanghai bourse CLOSED UP 4.82 POINTS OR 0.14%

. HANG SANG CLOSED UP 20.16 POINTS OR 0.05%

2. Nikkei closed UP 36.65 POINTS OR 0.16%

3. Europe stocks OPENED IN THE RED

/USA dollar index FALLS TO 95.74/Euro RISES TO 1.1493

3b Japan 10 year bond yield: RISES AT. +.16/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.38/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 74.79 and Brent: 84.62

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.57%/Italian 10 yr bond yield UP to 3.50% /SPAIN 10 YR BOND YIELD UP TO 1.62%

3j Greek 10 year bond yield RISES TO : 4.46

3k Gold at $1187.10 silver at:14.37 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 7/100 in roubles/dollar) 66.31

3m oil into the 74 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.25DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9930 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1415 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.57%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.23% early this morning. Thirty year rate at 3.40%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0648

Global Stocks Spooked As US Treasury Yields Resume

Their Ascent

Global markets entered Wednesday in tentative fashion as US Treasury yields resumed their upward march after dropping the day before ahead of a closely watched US CPI report and as the US Treasury prepared to sell more debt to fund the soaring US deficit.

The mood in stocks soured, and European equities turned lower with American futures as Asian peers erased an advance while world stocks inched off eight-week lows; market gains were checked by fears for global economic growth, greater US decoupling, escalating trade war and the possibility of an Italy-EU clash over budget spending. The result was generally a sea of red among global capital markets in early trading.

The equity rout that resulted from the global bond selloff that took bond yields to seven-year highs this week were exacerbated by continued growth concerns arising from trade conflicts and $80-per-barrel oil, with the IMF cutting its world GDP forecasts for the first time in two years.

The yield on 10-year Treasurys resumed its ascent to 3.23% from 3.20%, after falling for the first time in a week on Tuesday, putting a lid on early trader optimism.

“We are at some sort of critical moment, a crossroads, for bond and equity markets,” Marie Owens Thomsen, global head of economic research at Indosuez Wealth Management, said noting that while U.S. 10-year yields at 2% unequivocally favored equity investment, this was not so above 3%. “This January we took out the 2 percent (yield) handle and now we are wondering if we are permanently taking out the 3 percent handle as well. That makes the climate for equities much more challenging.”

The MSCI world equity index rose 0.14% after four days in the red. However, while Japan’s Nikkei and MSCI’s Asia-Pacific index outside Japan rose 0.2-0.3 percent, European shares slipped 0.2 percent, undermined by more bellicose rhetoric from Italian politicians.

The Stoxx Europe 600 Index dropped as most sectors turned lower. The European basic resources index (SXPP) – which was one of the best-performing sectors since the end of August – fell as much as 2.2%, one of Wednesday’s main sector laggards, as investors rotated toward defensive sub-groups including telecoms and health care. Milan-listed stocks traded between gains and losses, rising off 18-month lows hit earlier in the week.

Europe’s weakness followed a modest recovery of bullish sentiment in Asia, as shares in Japan rose after four days of losses, South Korean equities slumped as trading resumed after a holiday while those in China closed 0.2% higher after fluctuating between gains and losses before edging barely up after early gains slipped with lithium-related stocks tumbling, while Tencent suffered a record ninth day of declines in Hong Kong.

The retreat in emerging markets took a pause on Wednesday after Donald Trump said the Fed is moving too fast on rate hikes and as traders awaited U.S. inflation data before taking a stance on riskier assets. Equities slowed their drop and currencies eked out their first gain this week, led by India’s rupee

The yuan slipped against the dollar for the fifth session out of the past six to approach four-year lows hit in August, unresponsive to Mnuchin’s warning on devaluation. The focus is on next week’s semi-annual U.S. report on currencies amid Treasury officials’ comments that recent yuan depreciation has raised concerns in Washington.

The backdrop to global markets is still dominated by deepening U.S.-China tensions and a surge in volatility for stock and bond markets. While the Treasury rout has eased, a glut of new U.S. debt is coming to the market this week. American producer and consumer price data is also due in the next two days, and may determine where yields go from here.

“After President Trump once again criticized the Fed for raising rates too fast and he reiterated his preference for low borrowing costs, U.S. bond yields fell from their recent highs,” Rabobank strategist Piotr Matys wrote in a note. “This in turn provided the emerging-market currencies with respite. However, looking from the perspective of technical analysis the price action implies that U.S. 10-year Treasuries have entered a period of consolidation.”

Italian bonds initially dropped and bear flattened beyond the belly after Deputy PMs Salvini and Di Maio said the budget plan won’t change and there’s no going back, suggesting an unwillingness to compromise. Italy’s 10y spread to Germany blew out to 305bps, after Di Maio said that “our objective is not the spread, but the citizen… We expect that the economic growth rate will be higher” with measures included in the next year’s budget plan.

However the initial weakness reversed in a repeat of Tuesday’s action after Finance Minister Giovanni Tria, speaking before the parliament’s joint budget committee, pledged action to restore calm should market turbulence escalate into financial crisis. Yields slipped further after Tria said he expected “collaboration” with the EU on the budget issue, and added that “the rise in government bond yields recorded in the last few days is certainly a reason for concern, but I want to reiterate that it was an excessive reaction which is not justified by the fundamentals of Italy’s economy and public finances.”

That said, markets’ pressure has not dissuaded the government from a bigger-than-expected budget deficit as ministers’ comments indicated they are prepared to defy European Union critics. The developments have raised risks of a credit ratings downgrade for the country, with a knock-on effect for Italian banks which are big holders of government bonds. However the banks’ shares received a boost after an EU official told Reuters regulators were “intensely” monitoring Italian banks’ liquidity levels but there was no cause for alarm.

“I am not saying Italy is managing the situation in an ideal fashion but at the current junction I don’t think they are anywhere near a position where they can provoke another crisis in Europe,” Owens Thomsen said.

In currencies, the dollar reversed an early decline, rising to session highs, tracking Treasury yields, while another drop in Italian bonds kept the euro under pressure. The Bloomberg Dollar Spot Index heads for its third straight weekly advance as Treasury 10-year yields hold close to cycle highs and the euro meets selling interest on rallies above 1.15.

Politics were also in focus in Britain where reports of progress between the UK and the EU in negotiating a Brexit deal pushed the pound to 3-1/2-month highs against the dollar. Analysts at Eurizon SLJ Capital said parliamentary approval looked likely for Prime Minister Theresa May’s Brexit deal. The Times newspaper reported 30-40 opposition Labour MPs would back the agreement. “Already significantly undervalued, sterling has upside risks, especially against the euro,” Eurizon SLJ told clients, arguing that $1.55 was “fair value” for the currency.

The krone led gains in G-10 on stronger Norwegian inflation. Sterling hits its strongest level in two weeks on hopes officials will reach a compromise Brexit deal that could see the U.K. remain temporarily in the EU’s customs regime; wider than forecast trade deficit data helps push the pound back toward its opening level. The South African rand dropped following Tuesday’s rally.

In geopolitics, US President Trump said a summit with North Korean leader Kim Jung Un will be after US midterm elections on November 6th. In related news, US Secretary of State Pompeo noted real progress on his trip to North Korea and sees a full path to denuclearization.

In the latest Brexit news, ITV reported that UK PM May’s negotiator Robbins has made meaningful progress in talks with EU’s Chief Negotiator Barnier on the Irish border backstop. The article stated, “The most important development would be that the EU seems close to agreeing that the backstop would apply to the whole UK and not just to Northern Ireland, as it originally demanded – or at least it would apply to the whole UK for customs.” (ITV) In related news, UK Brexit Minister Raab said the UK will not sign up to an indefinite customs union with the backstop and negotiations with the EU have intensified, some differences on the withdrawal agreement.

In commodities, WTI slipped but was still near $75 a barrel as Hurricane Michael curtailed offshore oil production and the IEA issued a warning to the global market.

Expected data include mortgage applications, PPIs, and wholesale inventories. Fastenal is among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 2,885.25

- STOXX Europe 600 down 0.3% to 371.92

- MXAP up 0.02% to 157.41

- MXAPJ down 0.05% to 492.53

- Nikkei up 0.2% to 23,506.04

- Topix up 0.2% to 1,763.86

- Hang Seng Index up 0.08% to 26,193.07

- Shanghai Composite up 0.2% to 2,725.84

- Sensex up 1.3% to 34,758.76

- Australia S&P/ASX 200 up 0.1% to 6,049.81

- Kospi down 1.1% to 2,228.61

- German 10Y yield rose 0.2 bps to 0.551%

- Euro down 0.01% to $1.1490

- Italian 10Y yield fell 9.0 bps to 3.104%

- Spanish 10Y yield rose 1.1 bps to 1.611%

- Brent futures down 0.2% to $84.82/bbl

- Gold spot down 0.2% to $1,187.48

- U.S. Dollar Index up 0.1% to 95.76

Top Overnight News from Bloomberg

- Republican groups have been pulling back in more than a half dozen tough House races to focus their resources in districts where they see a better chance to defend against a building midterm surge by Democrats

- China plans to increase the number of companies it deems systemically important financial institutions, people familiar with the matter said, a sign that policy makers are stepping up crisis-prevention efforts as the nation’s debt burden swells to unprecedented levels

- Mnuchin warns China on competitive currency devaluations; Treasury has monitored currency issues “very carefully”; notes yuan has “depreciated significantly” during the year: FT

- Italy: Finance Minister Tria says budget watchdog approved govt economic forecast, however had different view on growth targets; rise in BTP yields are an excessive reaction

- BOE’s Haldane: risks to domestic prices are now broadly balanced; U.K. wage growth is likely to be limited and gradual

- Brexit: a group of 30-40 Labour MPs are prepared to back Chequers deal, according to people familiar: Times

- ECB’s Mersch: tightening labor market should support core inflation; reiterates ECB will be data dependent

- British and European Union officials are locked in talks in Brussels over a compromise Brexit deal that could see the U.K. remain temporarily in the EU’s customs regime, people familiar with the negotiations said

- There are growing signs China’s yuan may weaken past 7 per dollar, a key psychological level it hasn’t breached in a decade. The latest came in a China Securities Journal commentary

- The U.S. is threatening to block the U.K. from a 46- nation public procurement agreement, a move that would deny British companies from accessing a near $2 trillion-dollar marketplace after leaving the European Union, according to two officials with knowledge of the situation

- Federal Reserve Chairman Jerome Powell is pinning his hopes of stopping the U.S. economy from overheating on a variable that a former colleague called “the most significant unobservable of all:” inflation expectations

- Hurricane Michael’s winds rose to Category 4 strength of 130 miles an hour as it careened toward Florida

Asia-Pacific equities traded mixed as the region mimicked the lead from Wall St. where the S&P notched its fourth day of losses while the Nasdaq snapped its three-day losing streak. The Dow closed in the red as the major indices swung between positive and negative territory throughout the day. ASX 200 (+0.3%) was supported by strength in the healthcare and consumer discretionary sectors, while Nikkei 225 (Unch) was pressured by machinery names along with Softbank after reports emerged that the company discussed investing between USD 15bln-20bln for a majority stake in WeWork, while a firmer currency only subdued the index further. Elsewhere, mixed trade in China with Hang Seng (+0.5%) supported by oil names, while Shanghai Comp. (-0.3%) gave up initial gains to trade with no firm direction for most of the session before stabilising in the red.

Top Asian News

- China’s Banking Showdown Pits WeChat vs. 3 Million Bank Tellers

- Rocket Scientist’s Veggie Startup Is Said Valued at $7 Billion

- Hong Kong Bans E-Cigarettes in Latest Blow for Big Tobacco

- SoftBank Is Said to Consider Taking a Majority Stake in WeWork

- Luxury Shoppers in China Still Buy Bags, But Not BMWs

- Singapore Central Banker Strikes Upbeat Tone Amid Trade Risk

Major European indices (ex-SMI) trade lower (Eurostoxx 50 -0.4%) as Italian budgetary concerns remain a key focus; SMI. The CAC 40 (-0.7%) lags its peers after being weighed on by the Luxury names after the sector was downgraded to underweight by Morgan Stanley with the US bank citing concerns about a slowdown in Chinese activity. The move by MS took the shine of LVMH’s latest sales update with other Luxury names such as Kering and Burberry trading lower in sympathy. Sectors are mixed with telecom stocks leading their peers amid broad support for the sector today. Energy names are firmer by 0.7% following oil supply concerns from Hurricane Michael. Consumer discretionary is down by over 1.5% due to the aforementioned poor performance of luxury brands. Dixons is up by 3.5% after being upgraded to buy at HSBC; whilst Sage are up by 2.4% following being upgraded to Hold at Deutsche Bank.

Top European News

- U.K. Economy Set for Best Quarter Since 2016 Despite Flat August

- Patisserie Valerie Owner Suspends CFO Amid Accounting Probe

In FX, the Greenback has regained some composure overall after Tuesday’s rather sharp and abrupt sell-off on a degree of US Treasury yield retracement, and to a lesser extent another expression of dissent about the rate of Fed tightening from President Trump. To recap, the broad Dollar and DXY recoiled from best levels in relatively quick order, with the index down to 95.500 vs 96.000+ and circa 95.750 now, as rival currencies also derived bullish momentum on independent factors. The JPY is back below 113.00 vs the Usd and still unable to really test a key Fib level at 112.73, but perhaps drawn towards decent option interest from the big figure to 113.05 (1.2 bn) if the headline pair fails to break above 113.25. Some retracement from peaks for the Zar after a broadly positive reaction to the new SA Finance Minister appointment, while in contrast the Try has pared losses following initial disappointment over the Turkish Government’s inflation-fighting measures.

In commodities, both WTI and Brent are down just under 0.5%, trading just under USD 75/bbl and USD 85/bbl following further supply shortages from Hurricane Michael with 40% of Gulf of Mexico production now suspended in preparation. Note, APIs will be released otnight at 2130BST due to the Columbus Day holiday on Monday. Iron ore futures are up by over 0.6% following comments from Australia’s Port Hedland that Iron ore shipments to China to rise to 37.4mln tonnes. Gold is uneventful once again trading within a thin USD 5/oz range. Zinc hit a 4-month high in Shanghai overnight amid tightening supplies.

Looking ahead, in the US, focus will be on the September PPI report ahead of Thursday’s CPI, as well as August wholesale inventories data. Brexit negotiations will remain in focus, the BoE’s Chief Economist Haldane will speak in London, and regional Fed Presidents Bostic and Evans will speak on the economic outlook later in the evening.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 0.0%

- 8:30am: PPI Final Demand MoM, est. 0.2%, prior -0.1%;

- PPI Ex Food and Energy MoM, est. 0.2%, prior -0.1%

- PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.1%

- PPI Final Demand YoY, est. 2.7%, prior 2.8%

- PPI Ex Food and Energy YoY, est. 2.5%, prior 2.3%

- PPI Ex Food, Energy, Trade YoY, prior 2.9%

- 10am: Wholesale Inventories MoM, est. 0.8%, prior 0.8%; Wholesale Trade Sales MoM, est. 0.5%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

It was another day to wear your seatbelts if you were trading BTPs yesterday. By late morning London time 10yr yields had climbed another 14bps to 3.711%. However by the close we were almost 10bps tighter on the day at 3.476%. An impressive turnaround. Yields seemed to start to fall at the same time as the following headlines came through from Tria’s parliamentary hearing. He said that the “Government would act in case of an unexpected rise in bond spreads,” and that Italy’s current government bond yield spread is “unacceptable” and hopes to bring it down by explaining the budget measures. To be fair, this was all very vague and it’s not clear what the government could do other than reduce the budget deficit – which he hasn’t had much power over in the first place. Nevertheless the rally had started and seemed to get a further leg when headlines came through that “Conte, Tria, Salvini and Di Maio to meet at 8pm over budget.” We haven’t seen any follow through on this but Tria will address parliament at 10AM local time today.

If BTP trading required a seatbelt yesterday, Treasury and Bund markets required a small dose of motion sickness pills as 10yrs traded to both sides of a 6bp and 4bps range respectively. Given the risk off of the last few days and the weak global day for risk across the US bond market holiday on Monday, it was a bit of a surprise to see US Treasuries sell off 3bps in the morning to nearly 3.26%. However, we closed 3.0bps lower at 3.203% (3.208% in Asia). Bunds closed largely unchanged.

US equities were mixed again, though the recent underperformers bounced, with the NYFANG index up +0.63% and the NASDAQ eking out a +0.03% gain after 3 sessions of losses over which time it had shed -3.60%. The S&P 500 and DOW fell -0.14% and -0.21% respectively, while the VIX index rose as much as 1.8pts, but fell throughout the evening to close only 0.26pts higher at 15.95. That’s still a 3-month high.

This morning in Asia markets are continuing to trade mixed with the Hang Seng (+0.43%) up while the Shanghai Comp (-0.18%), Nikkei (-0.09%) and Kospi (-1.10%) are all down. Elsewhere, futures on S&P 500 (-0.15%) are pointing to a slightly softer start while EM FX is generally stronger against the greenback. On oil, IEA Executive Director Fatih Birol made a direct appeal to OPEC and other major oil producers to boost output, warning that high prices are inflicting damage on the global economy at a time when global economy is already losing growth momentum.

The pound rallied 0.41% versus the dollar yesterday on positive-sounding headlines, with Dow Jones reporting that the EU and UK will agree to a solution on the Northern Ireland issue at next week’s EU Council meeting. Separately, Brexit Secretary Raab told Parliament that the backstop for Northern Ireland will be temporary and limited. It’s hard to see how this will satisfy the EU but the headlines over the last 24 hours suggest we getting closer to a deal. The DUP’s Arlene Foster reiterated that on the Northern Ireland border issue they are trying to find a deal that works for everyone which sounded a little more dovish while the Government’s spokesman James Slack said that the UK’s new proposal for how to prevent a hard border with Ireland is coming “in due course,” signaling that the government expects the EU to flesh out how it sees UK’s future ties with the EU. In the meantime, The Times reported that the UK PM Theresa May is planning to have an extended discussion on Brexit at next Tuesday’s cabinet meeting in hopes of outlining a compromise deal on the Irish border. Overall, our strategists remain cautious, since the actual agreement of the deal will not be the key stumbling block; the real issue is if a deal can pass through Parliament. Positive movement from Labour MPs or from “hard” Brexiteers would be a more bullish catalyst for the pound. Interestingly the FT reports this morning that up to 30 Labour MPs are assessing whether they would vote against the government if it meant a no-deal.

In terms of central bank speak, the Fed’s Kaplan said on inflation that the cyclical inflation pressures are building and didn’t think that inflation is going to “run away from us” On rates he reiterated his previous view that he is comfortable hiking rates three more times till June while adding that higher productivity could lift neutral interest rates. He also added that I “don’t know the answer yet” on whether the U.S. central bank should lift interest rates past the neutral level that neither spurs nor slows growth, or “sit tight for a while.” Philadelphia Fed President Harker continued his recent hawkish shift by describing the labour market as having “very little slack left.” Overnight the Fed’s John Williams said that he expects the US economy to grow by c.3% in 2018 and 2.5% in 2019 while adding that the above trend growth should lead to decline in unemployment levels to slightly below 3.5% in 2019. On inflation he said he expects it to move a bit above 2% but doesn’t see any signs of greater inflationary pressures on the horizon.

Emerging market currencies gained 0.32% yesterday, amid positive news in Turkey and South Africa. Turkey’s treasury and finance minister Berat Albayrak announced a new plan to cut inflation, including price controls/cuts and lower bank loan rates. The Turkish lira erased morning declines to close 0.26% stronger. In South Africa, Finance Minister Nene resigned after a corruption scandal and was replaced by Tito Mboweni, a former central bank governor. Mboweni has a strong reputation as an orthodox inflation hawk, and the markets greeted the new appointment with the Rand rallying 1.88% versus the dollar. The Brazilian Real also outperformed, gaining 1.74% for its 7th consecutive day of gains. It has now appreciated every day in October, as investors anticipate a victory by rightwing candidate Bolsonaro in the October 28 runoff Presidential election.

In Europe, Germany’s August trade balance came in at €17.2bn (vs. €16.2bn expected) while the current account balance stood at €15.3bn (vs. €16.2bn expected). German exports declined -0.1% mom (vs. +0.4% mom expected) for the second month in a row, however the decline in imports was more accentuated at -2.7% mom (vs. -0.1% mom expected). In the US, the NFIB small business confidence fell modestly from its all-time high of 108.8 in August, printing at 107.9 versus expectations for 108.3.

Looking ahead to today, August industrial production will print in the UK and France. After a soft reading in Germany, the stakes are marginally higher than normal. The UK will also have its monthly GDP reading and trade balance report. In the US, focus will be on the September PPI report ahead of Thursday’s CPI, as well as August wholesale inventories data. Brexit negotiations will remain in focus, the BoE’s Chief Economist Haldane will speak in London, and regional Fed Presidents Bostic and Evans will speak on the economic outlook later in the evening.

|

ReplyForward

|

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT: