GOLD: $1222.80 UP $35.20 (COMEX TO COMEX CLOSINGS)

Silver: $14.57 UP 25 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1224.00

silver: $14.60

Expect many margin calls as the world wakes up to the fact that global growth has dissipated. The number one problem in the world is foreign exchange swaps and their cost is higher than the uSA interest rate spread and the negative Japan and European rates. This means that nobody can finance USA citizens purchase of foreign goods. Thus nobody was finance the huge $1.8 trillion of debt funding facing USA government today.

FOR THE NEXT TWO WEEKS, MY COMMENTARIES WILL BE DELIVERED BUT NOT AT MY USUAL TIME. I WILL GET IT DONE BUT IT IS INCREASINGLY MORE DIFFICULT TO WRITE

SO TRY AND CLICK ON AFTER 6:30 PM

THANKS

H

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: `1 NOTICE(S) FOR 100 OZ

Total number of notices filed so far for OCT: 852 for 85200 OZ (2.6500 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 316 for 1,580,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6198: DOWN $338

Bitcoin: FINAL EVENING TRADE: $6164 DOWN 363

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A GOOD SIZED 1176 CONTRACTS FROM 199,853 DOWN TO 201,029 DESPITE YESTERDAY’S 7 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR OCT. 1526 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1526 CONTRACTS. WITH THE TRANSFER OF 1526 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1733 EFP CONTRACTS TRANSLATES INTO 7.630 MILLION OZ ACCOMPANYING:

1.THE 7 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 1,590,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

20,178 CONTRACTS (FOR 9 TRADING DAYS TOTAL 20,178 CONTRACTS) OR 100.89 MILLION OZ: (AVERAGE PER DAY: 2242 CONTRACTS OR 11.210 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 100.89 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.41% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,320.41 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1176 DESPITE THE 7 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1526 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 2702 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1526 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1176 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 7 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.32 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.005 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER:1,590,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 6646 CONTRACTS DOWN TO 458,607 DESPITE THE RISE IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A GAIN IN PRICE OF $2.65.THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY GOOD SIZED 4446 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 4446 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 458,607. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY FAIR SIZED OI LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2201 CONTRACTS: 6646 OI CONTRACTS DECREASED AT THE COMEX AND 4446 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 2200 CONTRACTS OR 220,000 OZ = 6.842 TONNES. AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.65??? GO FIGURE!!

YESTERDAY, WE HAD 5416 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 67,762 CONTRACTS OR 6,776,200 OZ OR 210,76 TONNES (9 TRADING DAYS AND THUS AVERAGING: 7529 EFP CONTRACTS PER TRADING DAY OR 752,900 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 210.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 210.76/2550 x 100% TONNES = 8.26% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,886.69* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 6646 DESPITE THE GAIN IN PRICING ($2.65 THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD AN STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4446 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4446 EFP CONTRACTS ISSUED, WE HAD A FAIR OF 1889 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4446 CONTRACTS MOVE TO LONDON AND 6646 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 6.842 TONNES). ..AND ALL OF LACK OF DEMAND OCCURRED WITH A GAIN OF $2.65 IN YESTERDAY’S TRADING AT THE COMEX.???

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $35.20 TODAY: /

A HUGE CHANGE IN INVENTORY

A PROBABLE PAPER GOLD DEPOSIT OF: 8.82 TONNES

/GLD INVENTORY 738.99 TONNES

Inventory rests tonight: 738.99 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 25 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 332.912 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A FAIR SIZED 1176 CONTRACTS from 199853 UP TO 201,029 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1526 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1526 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1176 CONTRACTS TO THE 1526 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 2702 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 13.56 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW 1.590 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 7 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1526 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 142.38 POINTS OR 5.22% //Hang Sang CLOSED DOWN 926.70 POINTS OR 3.54% //The Nikkei closed DOWN 915.18 OR 3.89%/ Australia’s all ordinaires CLOSED DOWN 2.76% /Chinese yuan (ONSHORE) closed UP at 6.9146 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 74.79 dollars per barrel for WTI and 84.62 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED SLIGHTLY UP AT 6.9146 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY UP ON THE DOLLAR AT 6.9111: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

Asian markets crushed last night as the liquidation crisis smashes into Asia

( zerohedge)

4/EUROPEAN AFFAIRS

A good look at what is going on in Italy and the huge popularity of the Lega (Northern ) party

a must read..

(courtesy Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

Oil continues to lose ground falling below 72 dollars after two big builds:

in crude inventory and at Cushing OK

( zerohedge)

8 EMERGING MARKET ISSUES

i)ARGENTINA

9. PHYSICAL MARKETS

( Reuters/GATA)

ii)Gold spikes above 1200 dollars and breaks a key resistance level. Silver still in prison( zerohedge)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

i)Last night:

forced liquidations coming as the world deleverages

( zerohedge)

ii)This morning: 8 am

(zerohedge)

iii)This morning 10 am..a temporary reprieve

iv)Trading late in the afternoon/both bonds and bullion skyrocket. Dow collapses again and VIX at 25

(courtesy zerohedge)

b)Wow!! this is middle class erosion on steroids: 33 million Americans will not travel because they cannot afford to take a holiday

(courtesy Michael Snyder/ Economic Collapse Blog)

c)In a late night interview Trump again blasts the Fed for raising rates. The problem is the Fed must raise rates to keep the flow of funds coming into the USA. However we learned from the BIS and the Goldman paper that the costs to hedge in order to buy USA treasuries is greater than the yield. I do not think Trump understands this

iv)SWAMP STORIES

a)Rosenstein will not appear in front of the House Judiciary Committee and thus this committee will issue a subpoena forcing him to appear.

( zerohedge)

b) the King report/SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a LOSS of 1 contract to stand at 4 contracts. We had 1 notices filed YESTERDAY so we gained 0 contracts or NIL oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we GAINED 21 contracts up to 487 contracts. After November, we have a December contract and here we GAINED 446 contracts down to 164,109

AND NOW COMPARISON FOR OCTOBER:

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

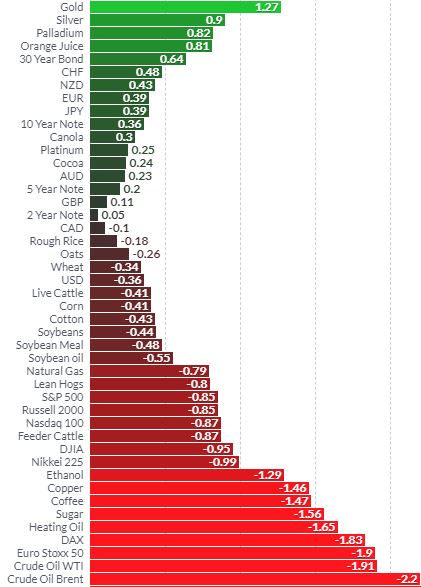

Gold Is Best Performing Asset In Global Stock Rout

Gold Up 1.2 Percent As Global Stock Rout Spreads To Europe

– Gold gains 1.27% as stock markets fall globally

– EuroStoxx -2%, FTSE -1.9%, Nikkei -4%, Shanghai -5.3%

– Gold, silver outperform all assets in stock market rout

– Trump accuses Fed of going “crazy” by continuing to raise rates

– Huge spike in VIX and volatility on deepening concerns of market correction or crash

1 Day Relative Performance (Finviz)

1 Day Relative Performance (Finviz)

Gold has gained 1.2% today on safe-haven demand as sharp declines on Wall Street spread throughout Asia and Europe.

Stocks in Europe have slumped to a more than 18-month low after sharp losses on Wall Street, centered on tech stocks and the Nasdaq.

The worst losses in eight months triggered a significant sell-off in stocks in Asia. China’s main stock indexes slumped over 5 percent and MSCI’s broadest index of Asian shares not including Japan ended down 3.6 percent, having struck its lowest level since March 2017.

It meant MSCI’s 24-country emerging market index had its worst day since early 2016, after Wall Street’s swoon had given the 47-country world index equivalent its worst day since February.

The losses were not helped by President Donald Trump accusing the Federal Reserve of going “crazy and “loco” as trade wars appear to be intensifying.

The VIX or Cboe Volatility Index has more than doubled in the last week. The huge spike in volatility comes as there are deepening concerns of a major market correction – particularly in the U.S.

Gold and silver, the traditional havens in times of volatility, are again displaying their lack of correlation and frequent inverse correlation (over the long term) with risk assets. The precious metals’ hedging benefits to investors portfolios are being seen as they again benefit from a safe haven bid exactly when investors need it.

Avoid Digital & ETF Gold – Key Gold Storage Must Haves

News and Commentary

Stock Rout Spreads as Bonds, Currencies Stay Calm for Now (Bloomberg.com)

Gold prices edge higher as global stocks sag, U.S. dollar slips (Reuters.com)

India’s Sept gold imports drop 14 pct on weak rupee-GFMS (Reuters.com)

Dow plunges more than 800 points in worst drop since February (CNBC.com)

U.S. bond yields near seven-year high stymie world stocks’ recovery (Reuters.com)

Source: Bloomberg

Trump says the Federal Reserve has ‘gone crazy’ by continuing to raise interest rates (CNBC.com)

Major Event Looms As Italy’s Lega Popularity Rises With Each EU Confrontation (ZeroHedge.com)

US-Russia tensions threaten nuclear arms race and tensions (FT.com)

Crypto theft hits nearly $1 billion in first nine months, report says (Reuters.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

10 Oct: USD 1,186.40, GBP 902.02 & EUR 1,033.00 per ounce

09 Oct: USD 1,187.40, GBP 910.26 & EUR 1,036.01 per ounce

08 Oct: USD 1,194.80, GBP 914.86 & EUR 1,040.67 per ounce

05 Oct: USD 1,201.10, GBP 921.48 & EUR 1,045.08 per ounce

04 Oct: USD 1,199.45, GBP 925.02 & EUR 1,043.28 per ounce

03 Oct: USD 1,203.50, GBP 925.73 & EUR 1,040.55 per ounce

Silver Prices (LBMA)

10 Oct: USD 14.38, GBP 10.92 & EUR 12.50 per ounce

09 Oct: USD 14.33, GBP 10.98 & EUR 12.51 per ounce

08 Oct: USD 14.47, GBP 11.10 & EUR 12.61 per ounce

05 Oct: USD 14.64, GBP 11.23 & EUR 12.73 per ounce

04 Oct: USD 14.63, GBP 11.27 & EUR 12.72 per ounce

03 Oct: USD 14.74, GBP 11.36 & EUR 12.75 per ounce

Recent Market Updates

– “Gold Is On The Cusp” Of An “Explosion Higher” As Stock and Tech “Crash Is Coming”

– Gold Bottoms As Gold Industry Consolidates and Weak Hands Capitulate

– 60 Charts For The (Last Few Remaining) Gold Bulls

– Poland and Australia Buy Gold As Global Property Bubble Bursts – This Week’s Golden Nuggets

– Brexit To Burst Dublin and London Property Bubbles? GoldCore Video

– Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

– “I’m Favouring Equities and Gold Over Bonds” – Stepek

– Poland Buys Gold For First Time In 20 years

– This Week’s Golden Nuggets – Central Banks, Goldman, Bank of America Positive On Undervalued Gold

– Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

– Europe Unveils “Special Purpose Vehicle” With Russia and China To Bypass SWIFT, Jeopardizing Dollar’s Reserve Status

– Gold Set to Soar Above $1,300 – Goldman and Bank of America

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on gold,

silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Crypto thefts hit nearly $1 billion in the first nine months of the year.

(courtesy Reuters/GATA)

Crypto theft hits nearly $1 billion in first nine months,

report says

Submitted by cpowell on Wed, 2018-10-10 14:55. Section: Daily Dispatches

By Gertrude Chavez-Dreyfuss

Reuters

Wednesday, October 10, 2018

NEW YORK — Theft of cryptocurrencies through hacking of exchanges and trading platforms soared to $927 million in the first nine months of the year, up nearly 250 percent from the level seen in 2017, according to a report from U.S.-based cyber security firm CipherTrace released today.

The report, which looks at criminal activity and money laundering in the digital currency market, also showed a steadily growing number of smaller thefts in the $20-60 million range, totaling $173 million in the third quarter.

Digital currencies stolen from exchanges in 2017 totaled just $266 million, according to a previous report from CipherTrace. …

… For the remainder of the report:

https://www.reuters.com/article/us-crypto-currency-crime/cryptocurrency-..

END

Gold spikes above 1200 dollars and breaks a key resistance level. Silver still in prison

(courtesy zerohedge)

Gold Spikes Above $1200, Breaks Key Technical

Resistance On Heavy ‘Safe-Haven’ Flows

end

A massive 8.5 tonnes were added into the GLD (probably paper gold). I have my doubts that this was real physical

It has been difficult to get any physical in London so to acquire 8.5 tonnes in one day is very suspect

(courtesy Lawrie on Gold)

Is this the turning point for gold and silver?

October 11, 2018lawrieongold

We wrote here recently about the short term headwinds facing gold and the longer term positives, but some of the short term negatives seemed as if they fell away at a single swoop yesterday! Could the 800 point fall in the Dow be the start of the much predicted equities collapse? Indeed the Dow and the S&P 500 were both down around 3% on the day and the NASDAQ down a massive 4%. These falls have been mirrored by big falls in general equities in Asia and Australia, and this morning in Europe. The equities sell-off has continued today, but not, so far, as severely as yesterday.

As perhaps another indicator, yesterday a massive 273,851 ounces of gold were added to the SPDR Gold Shares ETF (GLD) – that’s over 8.5 tonnes and is the first positive movement of gold into GLD for nearly 3 months, and a very sizeable amount to boot. We have stated here before that one should watch GLD additions or withdrawals as a guide to institutional sentiment towards gold and since April we have mostly seen withdrawals – an enormous 141 tonnes of gold had been taken out from GLD from end- April until yesterday. Again could this be a turning point for gold? One day’s figures are perhaps not a sufficient indicator of what’s to come, but are a and it is essential to monitor this indicator as a guide to precious metals sentiment.

Today we have seen a big rally in the gold price which has hit its highest level since the beginning of August, up over 2% at its intra day peak so far today. Silver has seen a slightly stronger increase too, but not enough yet to see it break out from its correlation with the gold price. But investor interest has been strong as witness the high level of silver Eagle sales out of the U.S. Mint. It has the potential to outperform gold should the rallies in both metals continue.

As always commentators’ views are mixed on the likely effect of yesterday’s falls in equities valuations. Some see them as a buying opportunity in an ongoing bull market pointing to a similar fall in February from which the major indexes made a fairly rapid recovery. All eyes will be on the Dow and the S&P over the next few days to see if the falls will continue, or if there will be a bounce back.

We are entering a time where Fed tightening by raising interest rates may well be making markets nervous. President Trump has been quick to lay the blame for yesterday’s fall on the Fed’s policy of raising interest rates thus leading to a stronger dollar (which has adversely affected the gold price in dollars if not in some other currencies). This fall in other currencies against the dollar has had a counter-effect on some of the Administration’s tariff impositions. Yet even so some U.S. manufacturers are already warning that the tariffs on Chinese goods in particular will have a negative impact on input and consumer prices.

So, we are likely going to see a steady increase in U.S. inflation, and unless there is a slew of positive data on job creation, wages and in PMI forecasts, we could see sentiment turning down which could further impact U.S. equities markets. If equities are seen as likely to fall further this could see an increased move towards safe haven assets like gold and silver.

Although be warned, if equities markets really do tank as some are predicting, then precious metals prices could suffer too as individuals and funds/institutions struggle to maintain liquidity and are forced to sell off good assets with the bad. We saw this happen in the 2008 market crash, although it should be noted that gold, in particular, was far quicker to recover than equities and climbed back to pre-crash levels while equities were still falling.

And what of silver? This has had a pretty torrid time of late as represented by a gold:silver ratio (GSR) at around its highest level for around 20 or more years. When the GSR has been this high in the past it has tended to precede either an economic crisis or a big stock market turndown, or both. Is that what we are now experiencing? We have often said we don’t anticipate a return to the supposed old average GSR of around 15 as the out and out silver bulls will suggest, but a return to the 70 level, or even 60, could be on the cards with a huge positive impact on the price of silver. vis-a-vis that of gold

This morning, gold has already regained the $1,200 level which had previously seen major resistance to an increase coming in. And once U.S. markets opened the price shot up another $20. If this level is sustained through the end of the week and equities continue to fall, then we could see a big surge in precious metals prices in the days and weeks ahead. Chart followers had been pointing to a gold close above $1,215 as being the significant level from which gold might continue to appreciate and, as I update this article gold is sitting comfortably higher than this level. it obviously remains to be seen whether it will stay there, but we think there is a good chance of it so doing and then move on to get some of its lustre back.

Bitcoin too has been stuttering with BTC down around 5% and the smaller cryptos, like ETH, mostly down more than 10%. We have long warned that we have no confidence in the stability of a bitcoin investment and this kind of volatility perhaps makes the point for us. Some observers reckon that BTC will fall to around $2,000 by the year end, or even lower, and some of the lesser cryptos to close to zero. We wouldn’t be surprised if this were to come about!

https://lawrieongold.com/2018/10/11/is-this-the- turning-point-for-gold-and-silver/

______________________________________________________________________________________________________________________________________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9146/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9321 /shanghai bourse CLOSED DOWN 142.38 POINTS OR 5.22%

. HANG SANG CLOSED DOWN 926.70 POINTS OR 3.54%

2. Nikkei closed DOWN 915.18 POINTS OR 3.89%

3. Europe stocks OPENED IN THE RED

/USA dollar index FALLS TO 95.17/Euro RISES TO 1.1573

3b Japan 10 year bond yield: RISES AT. +.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.26/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.93 and Brent: 81.50

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.52%/Italian 10 yr bond yield UP to 3.58% /SPAIN 10 YR BOND YIELD UP TO 1.63%

3j Greek 10 year bond yield RISES TO : 4.51

3k Gold at $1203.60 silver at:14.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 39/100 in roubles/dollar) 66.44

3m oil into the 72 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.26DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9816 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1429 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.52%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.18% early this morning. Thirty year rate at 3.37%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9768

“It’s Just Beginning”: US Futures Plunge As Global Rout

Hammers Asia, Europe

It is a sea of blood red this October morning as the biggest market rout since February and the longest selloff of the Trump administration triggered a surge of global selling from the U.S. through Asia and spreading to Europe on Thursday, with markets from Tokyo to London slumping amid fresh fears the decade-old bull market may be coming to an end.

“Equity markets are locked in a sharp sell-off, with concern around how far yields will rise, warnings from the IMF about financial stability risks and continued trade tension all driving uncertainty,” summed up analysts at ANZ.

The sell-off that started in the U.S. ripped across Asian stock markets Thursday, with indexes in Japan, Hong Kong and China all tumbling.

All but one stock listed on Japan’s Nikkei 225 Stock Average retreated, while the country’s Topix index posted its steepest decline since March losing around $207 billion in market value, falling 3.5%. China’s Shanghai Composite sank 5.2%, its biggest drop since February 2016 to close at its lowest since November 2014, while the Hang Seng Index lost 3.5%. Taiwan’s Taiex index led the rout with a 6.3% slump.

The MSCI Asia Pacific Index had its worst day since June 2016, when the U.K. voted to leave the EU, with the index plunging 3.5% and closing in on entering a bear market.

Turbulence spiked in Asian markets as the Nikkei Stock Average Volatility Index surged 44%. The MSCI Asia Pacific Index ex Japan closed down 3.6%, hitting its lowest level since March 2017. China’s main indexes had slumped over 5 percent

The Asian regional benchmark gauge has slumped 13 percent this year as uncertainties such as the U.S.-China trade war weigh on investor sentiment. The Shanghai Composite Index has lost 22 percent in 2018, while Japan’s Topix is down 6.4 percent.

“It’s just a beginning,” said Banny Lam, head of research at CEB International Investment. “The U.S. tech bubble may take a while to burst and we are facing many external uncertainties – trade wars, risks in emerging markets currencies and oil price. And people should also watch yuan closely.”

“Asia is like a leveraged play on the U.S. market and the global trade situation right now, that’s not going to change until a deal is reached between the two largest economies in the world,” said Olivier d’Assier, head of applied research for the Asia-Pacific region at Axioma. For emerging markets, “the trifecta of a falling U.S. market, higher U.S. interest rates, and a stronger dollar is a deadly combination so they are likely to remain under pressure.”

The Asian rout then spread to Europe, where stocks slumped to a more than an 18-month low. Losses in London, Paris and Milan were already climbing toward 2% in early trading, although the selloff wasn’t quite as dramatic as the overnight session in Asia. Italian equities entered a bear market, however, on ongoing budget concerns and LeasePlan Group NV pulled a planned IPO.

As a result of the global rout, MSCI’s 24-country emerging market index was having its worst day since early 2016, after Wall Street’s swoon had given the 47-country world index equivalent its worst day since February.

Meanwhile, in a surprising reversal from previous routs, US futures failed to rebound as dip buyers stayed away from the E-Mini. S&P futures extended losses from Wednesday, when the Nasdaq 100 Index plunged more than 4% for its worst day in seven years.

The futures drop took place after the S&P500’s sharpest one-day fall since February wiped out around $850 billion of wealth as technology shares tumbled on fears of slowing demand. The S&P 500 ended Wednesday with down 3.29%, wiping out nearly half the year’s gains in one session; the Nasdaq Composite plunged 4.08% and the Dow 2.2%.

“The latest drop is reminiscent of February’s selling, which saw its recovery assisted by positive earnings results,” said Jingyi Pan, a market strategist at IG Asia Pte. “As for the upcoming earnings season commencing with major U.S. banks on Friday, the outlook is rather mixed thus adding to the uncertainty. It will be one worth watching for aid to the market given the proximity and it will be difficult to rule out further decline in the market absent positive factors.”

Investors seeking to isolate the cause of the current rout in equities have no shortage of culprits: U.S companies are increasingly fretting the impact of the burgeoning trade war, while the same concern prompted the IMF to dial down global growth expectations for the first time in 2 years. In the tech sector, which was a key driver of the rally that pushed American equities to a record just a month ago, expensive-looking companies have been roiled by a hacking scandal.

At the same time, the Federal Reserve has been trimming its balance sheet and raising interest rates which as “well below” the neutral rate of interest according to Powell, which in turn provoked the ire of President Donald Trump and helping force a repricing of riskier assets. Trump, who has claimed credit for record U.S. stock levels, said after the market closed on Wednesday that the Fed is “loco”, that it is making a “mistake” and “has gone crazy.”

Commenting on the recent move, Saxo Capital strategist Eleanor Creagh said that “the sharp rise in U.S. 10-year yields has caused investors to suddenly reprice the impact of moving from post-crisis low yields to a rising rate environment. We have the global growth engines, price of energy rising, price of money rising and quantity of money falling combined with the ongoing trend of de-globalization which has started to impact markets and the cracks are showing.”

Curiously, Treasuries which helped trigger the stock selloff when 10-year yields hit the highest since 2011, nudged higher after jumping on Wednesday as bonds have once again become a safe haven. It meant that as equities were caught in a global carnage, US Treasurys were oddly calm, with the 10Y generally unchanged overnight.

“The rise in Treasury yields has been the primary catalyst for the sell-off in equities, since higher yields suggest a lower present value of future dividend streams, assuming an unchanged economic outlook,” said Steven Friedman, senior economist at BNP Paribas Asset Management. “It is also possible that equity investors are growing concerned that the Federal Reserve’s projected rate path will choke off the expansion.”

Meanwhile, Italian bonds sold off again as Deputy Premier Matteo Salvini once again said the populist government will stick with its budget plan and that rating agencies “won’t make us change our minds”, though the country successfully sold new debt. Asked about possible downgrade by ratings agencies and concerns about spread with German bunds, Salvini said “we’ve already seen this movie in the past, it’s forced Italians to make incredible sacrifices, to have cuts on schools and reforms on health and pensions which impoverished,” adds “we will do exactly the opposite.”

“It remains to be seen whether the accelerating equity plunge is a healthy correction or the tip of the iceberg,” Commerzbank analysts said in a note. “For sure it creates a more challenging environment for today’s (Italian) auctions.”

Meanwhile, bunds and gilts led advances amid the broader risk-off mood.

The shift in yields is also sucking funds out of emerging markets, putting particular pressure on the Chinese yuan as Beijing fights a protracted trade battle with the United States. China’s central bank has been allowing the yuan to gradually decline, breaking the 6.9000 barrier and allowing traders to push the dollar up to 6.9431.

China’s move has forced other emerging-market currencies to weaken to stay competitive and drawn the ire of the United States, which sees it as an unfair devaluation. “The yuan has already weakened significantly, to offset the tariffs announced so far,” said Alan Ruskin, Deutsche’s global head of G10 FX strategy. “Further weakness could exacerbate concerns of a self-fulfilling flight of capital and a loss of control.”

Still, there was little sign of panic in currencies, where the euro gained and dollar weakened versus most of its major counterparts. The Swedish krona was the standout gainer, jumping after inflation data. The Turkish lira and rand rallied, but emerging currencies overall edged lower. The euro was at $1.1550 up from a low of $1.1429 early in the week. The dollar lapsed to 112.14 yen, a retreat from last week’s 114.54 peak. That left the dollar at 95.263 against a basket of currencies

Sinking global shares have raised the stakes for U.S. inflation figures due later on Thursday. High inflation would only stoke speculation of more aggressive rate hikes from the Federal Reserve.

In commodity markets, gold struggled to get any safety bid and edged down to $1,192.77. Oil prices skidded in line with U.S. equity markets, even though energy traders worried about shrinking Iranian supply from U.S. sanctions and kept an eye on Hurricane Michael, which shut down some U.S. Gulf of Mexico oil output. Brent crude fell 1.6 percent to $81.75 a barrel. U.S. crude dropped 1.5 percent to $72.07. A Bloomberg index of cryptocurrencies dropped as much as 11%.

Scheduled earnings include Walgreens and Delta Air Lines. CPI figures, jobless claims are among economic data due.

Finally, one wonders just what is it about October, when half of the biggest US market crashes have taken place.

Market Snapshot

- &P 500 futures down 1% to 2,753.75

- STOXX Europe 600 down 1.4% to 361.75

- MXAP down 3.5% to 151.91

- MXAPJ down 3.7% to 473.27

- Nikkei down 3.9% to 22,590.86

- Topix down 3.5% to 1,701.86

- Hang Seng Index down 3.5% to 25,266.37

- Shanghai Composite down 5.2% to 2,583.46

- Sensex down 1.6% to 34,218.05

- Australia S&P/ASX 200 down 2.7% to 5,883.76

- Kospi down 4.4% to 2,129.67

- German 10Y yield fell 3.9 bps to 0.513%

- Euro up 0.2% to $1.1547

- Brent Futures down 1.1% to $82.16/bbl

- Italian 10Y yield rose 2.9 bps to 3.133%

- Spanish 10Y yield rose 1.2 bps to 1.625%

- Brent Futures down 1.1% to $82.16/bbl

- Gold spot up 0.2% to $1,197.28

- U.S. Dollar Index down 0.2% to 95.33

Top Overnight News from Bloomberg

- The biggest stock sell-off since February rolled from the U.S. through Asia on Thursday, with benchmarks from Tokyo to Hong Kong seeing declines in excess of 3 percent. Some emerging- market currencies also came under pressure, with the won hitting a one-year low

- A sell off in Hong Kong and Chinese shares deepened following a slump in U.S. equities amid concerns about a trade war

- President Donald Trump slammed the Federal Reserve as “going loco” for its interest-rate increases this year. His latest criticism of the Fed began earlier Wednesday. “They’re so tight. I think the Fed has gone crazy,” the president said

- Wall Street is bracing for the prospect that the U.S. uses this month’s semiannual foreign-exchange report to label China a currency manipulator. IMF Managing Director Christine Lagarde says yuan weakness has a lot to do with dollar strength

- Brexit negotiators are edging toward a compromise on the thorniest issue in talks. The main sticking point is how to keep the Irish border open after Brexit

- Oil extended losses as U.S. stocks tumbled on a concern over a trade war with China and Hurricane Michael threatened to slash demand in America’s southeastern fuel markets

- Global finance chiefs including U.S. Treasury Secretary Steven Mnuchin played down the economic risks posed by the biggest U.S. stock sell-off since February, with many describing the decline as a long-awaited correction

- Convergence to sustainable price stability in the euro area “requires significant monetary stimulus” and this calls for “prudence and for a gradual approach to monetary policy normalization,” ECB Governing Council member and Bank of Finland Governor Olli Rehn says in remarks at panel in Bali, Indonesia

- A former UBS Group AG banker is set to testify as soon as Thursday as the U.S. government’s star witness against three British traders accused of conspiring to rig the foreign-exchange market

Asian stocks drowned in a sea of red following the battered lead from Wall St. amid a sell-off in tech stocks where the sector posted its worst day since 2011. Dow and S&P notched their biggest one-day drop since early February, while Nasdaq fell below its 200 DMA to experience its largest single-day decline since June 2016. ASX 200 (-2.5%) was dragged lower by the tech sector, closely followed by the energy names, while Nikkei 225 (-4.0%) plumbed the depths amid weakness in mining and energy names alongside currency effects. Elsewhere, Hang Seng (-3.7%) and Shanghai Comp. (-4.3%) dived deeper into bear-market territory in a continuation of the tech sell-off, with the former hitting lows last seen in February while the latter tumbled to 4-year lows.

Top Asian News

- India’s Sensex on Verge of Losing Yearly Gain Amid Global Rout

- Wave of Reforms Coming as Indonesia Confronts Weak Currency

- China Urges U.S. to Address Trade Differences by Talks

- IMF Says Pakistan Has Formally Requested Financial Assistance

Major European indices are all in the red due to the global market turmoil which began on Wednesday in U.S markets (Euro Stoxx 50: -1.3%), the cause has been quoted as a multitude of factors not limited to; US-China trade tensions, the current yield environment, the Italian political situation and suggestions that the markets were overdue a correction. However, it is yet to be seen whether this is part of a broader economic downturn as we enter into U.S earning season with a relatively solid U.S economic backdrop. All sectors are down with energy firms down by over 2% in fitting with price action in the complex. Healthcare and consumer staples are the best performing sectors as more defensive investments are sought in the risk-off environment, but are both in the red by just under 1% Dialog Semiconductor is vastly outperforming, up over 23%, following a EUR 600mln deal with Apple, which has led to the company updating their revenue outlook for the next 4 years. Ingenico are also up over 12% after confirmation that Natixis (-4.5%) are in the early stages of take over discussions. Hays Plc are at the bottom of the Stoxx 600, down by 12% after reporting a slower quarterly growth rate.

Top European News

- London Housing Is Taking a Beating From From Brexit Uncertainty

- Russia Targets 25% Global Energy Market Share: La Stampa

- Merlin Says Report on El Corte Ingles Talks ‘Unfounded’

- Semis Are Worst Hit as Tech Stock Sell-off Extends in Europe

- Italy’s FTSE MIB Is Set to Enter Bear Market on Budget Concerns

In FX, the EUR is firmly back above 1.1500 vs the Usd and pivoting 1.1550 within a higher range flanked by hefty option expiry interest (1.8 bn at the 1.1500 strike and 2.3 bn from 1.1600-20), while also facing chart resistance in the 1.1572-91 region that houses a daily top, 55 DMA and Fib. Fundamentally, not much to glean from latest ECB comments, but the minutes may provide something to trade off. In EM, the Lira stands out amidst broad rebounds vs the Dollar across the region as Usd/Try crosses the 6.0000 handle to the downside on a combination of more concerted efforts to get runaway Turkish inflation back down towards target and a wider than forecast current account surplus. Elsewhere, the Rand and Real also have data to digest in the form of SA manufacturing production and Brazilian retail sales that might deflect some attention away from domestic politics, for a while at least. SEK – Hot on the heels of its Scandi peer, the Sek has seized pole position on the G10 grid and extended gains on the back of relatively hawkish Riksbank rhetoric, as Swedish CPI and CPIF readings also topped market expectations. In response, December rate hike odds have narrowed to better than evens, while Eur/Sek is testing psychological support circa 10.4000 ahead of the nearest downside tech level around 10.3725 (early October low)

In commodities, both WTI and Brent are down by 2% at just under USD 72/bbl and USD 82/bbl respectively with prices hampered by the risk-off environment as investors are concerned following global growth uncertainty and ongoing trade disputes. This comes alongside API’s reporting a larger than expected headline build of +9.75mln offering pressure on the fossil fuel. Supply concerns from Hurricane Michael are also easing as oil assets were likely spared significant damage from the storm. Gold is up 0.3% as investors seek safe havens from the current global dip, gold has subsequently breached USD 1200/oz to the upside. Base metals also fell again amidst the broader global risk sentiment with underperformance seen in copper.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.2%, prior 0.2%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- 8:30am: US CPI YoY, est. 2.4%, prior 2.7%; CPI Ex Food and Energy YoY, est. 2.3%, prior 2.2%

- 8:30am: Real Avg Weekly Earnings YoY, prior 0.52%; Real Avg Hourly Earning YoY, prior 0.2%

- 8:30am: Initial Jobless Claims, est. 206,500, prior 207,000; Continuing Claims, est. 1.66m, prior 1.65m

- 9:45am: Bloomberg Consumer Comfort, prior 61.6

DB’s Jim Reid concludes the overnight wrap

Days like yesterday, although brutal, restore one’s belief that at this stage of the rate cycle things should start to get more difficult and more volatile even if the center (the US economy) is still likely to hold for now. In fact it’s been our thesis that the US economy at risk of overheating is partly what’s going to drive volatility up. So with that in mind today’s US CPI comes at a fascinating point.

Before reviewing that let’s review the wreckage from yesterday. The S&P 500 (-3.28%) and DOW (-3.15%) both had their worst days since the February market correction and the NASDAQ (-4.08%) shed the most since June 2016. The S&P 500 has now traded lower for 5 consecutive sessions, shedding -4.77% over that period, its longest such stretch since March.

Every S&P 500 sub-sector traded lower amid generalised risk-off sentiment, but the FANGs (-5.60%) continued to underperform, saw their worst day since March and are now down -17.86% from their June peak. Volatility spiked, with the VIX index up 7.01pts and closing at its highs around 22.96, a six-month high. Using another measure of vol, this year we’ve now had 6 days with the S&P 500 falling more than 2% – the most since 2011. 2017 had none. Perhaps tellingly, Treasuries yields were higher all day until a mini plunge started with 10 minutes left of US equity trading. They traded around -4.3bps lower for the day at 3.164% at the close. In Asia overnight they are at 3.147% as we type. US HY had been the most expensive part of the credit spectrum in our view and was at 9 month tights 2 weeks ago but has been selling off of late. CDX HY widened 18.1bps yesterday and is now around 46.7bps wider than the late September tights and back nearer the top end of the YTD range.

On the equity sell off the big names in the US administration had their say. US Treasury Secretary Steven Mnuchin said, “the fundamentals of the U.S. economy continue to be extremely strong, I think that’s why the stock market has performed as well as it has. The fact that there’s somewhat of a correction given how much the market has gone up is not particularly surprising” while President Trump also said that the stocks decline was “a correction that we’ve been waiting for for a long time.” However, Trump stepped up his rhetoric on Fed saying that it is making a “mistake” by raising rates and “has gone crazy” while adding that yesterday’s market plunge wasn’t because of the US trade war with China.

This morning in Asia, the risk off sentiment has continued from Wall Street with all equity indices trading in sea of red and bumping around the lows for the session as we type. The Nikkei (-4.28%), Hang Seng (-3.74%), Shanghai Comp (-4.34%), ASX (-2.40%) and Kospi (-3.61%) are all down but in these fast markets things might have changed again by the time you read this. In other markets, Taiwan’s Taiex (-6.23%), India’s Nifty (-2.78%) and Indonesia’s Jakarta Comp (-1.67%) are all heading lower. Elsewhere, futures on S&P 500 are down another -0.66%. Overnight, BoJ board member Makoto Sakurai called for the central bank to assess the sustainability of its easing policy from a much wider perspective indicating that the policy tweaks in July haven’t put to bed concerns over side effects. She said that the BoJ needed to keep in mind the risk of distortions building up in the economy and the financial sector if the easing policy is prolonged in a favorable economic environment with demand exceeding supply.

Today will be a key test for markets with US CPI set to dominate attention. The consensus doesn’t expect much to happen, but then again it rarely has for this data print over the last few years. The consensus forecast is again at +0.2% mom for the core for the 36th successive month. DB is at +0.25% mom so we think it could round up to 0.3%. Before the recent risk-off, I would have automatically said that the downside risks to the market from an upside inflation print were much larger than the upside market risks from a downside surprise. However, given the recent risk sell-off, you’d have to say that there is scope for a decent relief rally on a softer number. Medium-term though, signs of higher inflation would be much worse for risk than softer inflation would be positive.

Back to yesterday and in Europe a number of markets hit YTD lows with the DAX (-2.21%) at the lowest since February 2017 and experiencing the 5th worst day of the year. The Stoxx 600 (-1.61%) was at the lowest since March. The FTSEMIB (-1.71%) actually held in well relative to the market, though it did reach a fresh 20-month low. 10yr BTPs only rose 3.0bps and only slightly widened to Bunds (+0.5bps). The S&P fell -1.82% after Europe closed so there should be some additional catch up this morning.

On Italy, Moody’s chief economist, Mark Zandi said that it is logical that the market concerns about Italy will be reflected in ratings agencies’ upcoming reviews of the country. He added that the Italian government’s fiscal plan can be compared to gambling with the long-term fiscal and economic health of Italy. Elsewhere, Italian Deputy Premier Matteo Salvini said that he won’t go back on pension reform and tax cuts in budget plan while adding he is “absolutely sure” that the BTPs-bunds spread won’t reach 400bps. It’s hard to know how he can control for both of these. In the meantime Finance Minister Tria reiterated more of same at his parliament hearing saying “the rise in government bond yields recorded in the last few days is certainly a reason for concern, but I want to reiterate that it was an excessive reaction which is not justified by the fundamentals of Italy’s economy and public finances.”

On Brexit it was another eventful day. Media reports highlighted that the UK and EU officials engaged in talks indicated that the UK government is likely to back down on opposition to new regulatory checks on some items moving between the British mainland and Northern Ireland while, in exchange, the UK is seeking the EU to compromise and allow the whole of the UK, not just Northern Ireland, to stay in the bloc’s customs regime until a future trade deal is eventually drawn up between the two sides. The officials indicated that the discussions over the next few days could lead to provisional agreement between the EU and the UK over the issue of the Irish backstop on Monday. The chief EU negotiator Michel Barnier confirmed this positive movement, saying “a deal is within reach.” Elsewhere, the UK Prime Minister Theresa May’s de-facto deputy, David Lidington, said in an interveiw that “we’ve got a fair way to go still. There are still differences between our position and that of the European Commission, but we’re working very hard to overcome them.”

Looking at the data releases from yesterday. In US, September PPI and core PPI both printed in line with consensus at +0.2% mom, rising for the first time in 3 months largely on the back of higher airfares (+5.5% mom; highest since 2009) and rail-transportation costs (+1.4% mom; highest since 2012). Overall, services prices increased +0.3% mom while the cost of goods fell -0.1% mom, reflecting declines in both food and energy. The core-core PPI stood at +0.4% mom (vs. +0.2% mom expected).

Across the pond in Europe, France’s August industrial production came in at +0.3% mom (vs. +0.1% mom expected) while the previous months was revised upwards to +0.8% mom from +0.7% mom and manufacturing production came in at +0.6% mom (vs. +0.1% mom expected). Industrial production also rose in Italy (+1.7% mom), Spain (+0.7%), and the Netherlands (+1.7%). These prints are likely distorted due to new regulations, but the trend signals healthy IP growth of around 1% for the euro area overall. In the UK, the August three month GDP change came in at +0.7% 3m/3m (vs. +0.6% 3m/3m expected) with August GDP remaining flat as against consensus of +0.1% mom. The UK’s August visible trade balance stood at -£11.2bn (vs.-£10.9bn expected) while the trade balance came in at -£1.3bn (vs. -£1.2bn expected). UK’s August industrial production came in at +0.2% mom (vs. +0.1% mom expected), manufacturing production at -0.2% mom (vs. +0.1% mom expected) and construction output at -0.7% mom (vs. -0.5% mom expected).

Before the US CPI print today, we’ll get CPI revisions in France and Spain. Later this morning, the Bank of England will publish its latest credit conditions and bank liabilities survey. The ECB will publish the minutes of its September policy meeting this afternoon, while BoE Governor Carney will speak on a panel alongside Banque de France Governor Villeroy. Concurrent with the US CPI, the latest weekly jobless claims will print.

3. ASIAN AFFAIRS

i) THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 142.38 POINTS OR 5.22% //Hang Sang CLOSED DOWN 926.70 POINTS OR 3.54% //The Nikkei closed DOWN 915.18 OR 3.89%/ Australia’s all ordinaires CLOSED DOWN 2.76% /Chinese yuan (ONSHORE) closed UP at 6.9146 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 74.79 dollars per barrel for WTI and 84.62 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED SLIGHTLY UP AT 6.9146 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY UP ON THE DOLLAR AT 6.9111: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

Asian markets crushed last night as the liquidation crisis smashes into Asia

(courtesy zerohedge)

Asian Markets Crushed By Capitulation Carnage

No “National Team”… No “Plunge Protection Team”… No RRR Cuts… and not a word from Powell. The US equity market massacre is extending overnight as the liquidation crisis smashes into Asia…

The initial red box is the after-hours drop and the second drop is as Asian cash markets opened…

From yesterday’s cash close at 26,449, Dow futures are now down almost 1300 points…

AsiaPac markets are a sea of red…

MSCI AsiaPac is plunging almost 4% to its lowest since May 2017…

Taiwan is getting monkey-hammered…

China is opening in freefall…

And it’s not just equity markets.

Currencies are tumbling…led by the Won and Taiwanese Dollar…

Yuan is back near cycle lows…

And cryptocurrencies are crashing too…

There is some green in the world, however…

US Treasuries are bid with 10Y now down 12bps from Tuesday’s highs…

It’s going to be a long night.

end

4.EUROPEAN AFFAIRS

A good look at what is going on in Italy and the huge popularity of the Lega (Northern ) party

a must read..

(courtesy Mish Shedlock/Mishtalk)

“Major Event” Looms As Italy’s Lega Popularity Rises With Each EU Confrontation

Authored by Mike Shedlock via MishTalk,

The EU conspiracy to oust Berlusconi succeeded because his popularity was on the skids. Lega is a far different story…

Eurointelligence has an interesting take on rising Italian yields, Italy’s budget deficit, and the inability of the EU and ECB to do any thing about it.

One of the lessons of 2012 is that rising spreads in the eurozone can create a self-fulfilling dynamic once they breach a certain (unknown) level. For Italy, we don’t think spreads have reached that point at the current levels of just above 300bp. But another 50bp or 100bp could trigger a crisis. A rating downgrade is certain, but the markets are watching whether the downgrade will come with a stable or negative outlook. If it is negative, Italian bonds would be on the brink of losing their investment-grade status.

The nervousness is fuelled by defiant comments from Italian ministers. Paolo Savona said that, if the EU opts to reject the Italian budget, it will be up to the people of Italy to decide what to do next. This is where the situation today is so different from that of 2011 when an Italian president colluded with the ECB to remove Silvio Berlusconi. By then, Berlusconi had lost his majority in the chamber of deputies – and the support of the public at large. The Lega, by contrast, is currently seeing its support rise. And this continues with every row with the EU. It is therefore far from clear that a financial crisis would necessarily play into the hands of the EU and produce a more compliant Italian government, or at least a more compliant budget. The opposite might be the case. As of now, we see no signs of the Italian government backing down.

There are good reasons to expect that the situation will come to a head at some point. Italy remains one of the eurozone’s slowest-growing economies. The IMF sees eurozone growth at around 2% this year, and a fraction less next year – while Italy’s growth is a little over half of that. The Italian government’s forecast of a falling deficit was premised on the idea of a fiscal boost generating higher growth. If that is not the case (it won’t be), the deficit is likely to rise above 2.4%. So we are looking at a return of the near-3% deficit and inevitable increases in the debt-to-GDP ratio. This is clearly not sustainable.

We note a comment in Il Sole 24 Ore by Carlo Bastasin, who writes that Italy’s failure to achieve public-sector debt reduction during the short periods of relatively-strong economic growth means that the country is even worse equipped to deal with the next financial crisis than it was in 2008.

Great Pretenders

- The League and M5S pretend growth will be far bigger than realistic.

- The EU is willing to pretend as well because it does not want a confrontation with Italy on top of Brexit and confrontations with Poland over its judicial reforms and Hungary over immigration.

Meanwhile, Lega continues to strengthen. This will come to a head sooner or later, sooner if yields blow out and later once Brexit is worked out by March.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7 OIL ISSUES

Oil continues to lose ground falling below 72 dollars after two big builds:

in crude inventory and at Cushing OK

(courtesy zerohedge)

WTI Extends Losses Below $72 After Big Crude,

Cushing Build

WTI is extending losses after DOE reported a bigger than expected crude (and Cushing) inventory build, after API reported the biggest crude build since Feb 2017 and OPEC cut its global demand estimates.

Of course, OPEC was careful to play down its demand downgrade:

“There is no cause for alarm,” Barkindo said at the Oil and Money conference in London. OPEC and its allies “are ready and willing to continue to make sure that the market remains well supplied.”

“We are now gradually but steadily seeing the brighter path ahead, [That’s] despite some of the bumps, despite some of the occasional clouds that have gathered.”

As Bloomberg Intelligence Senior Energy Analyst Vince Piazza notes, a mix of U.S.-China trade tensions and elevated crude prices pose a near-term risk to the oil market. With WTI above $75 a barrel, we believe crude has moved too far, too fast. Saudi Arabia seems comfortable with Brent below the current $85. At current prices, we expect increased hedging by U.S. producers and an extension of robust output, fostering a negative feedback loop.

But, despite OPEC and the storm shut-ins, all eyes were on inventories (at least in the short term)

API

- Crude +9.75mm (+2.5mm exp) – biggest build since Feb 2017

- Cushing +2.3mm (+800k exp) – biggest build since March 2018

- Gasoline +3.4mm – biggest build since June 2018

- Distillates -3.5mm – biggest draw since May 2018

Keep in mind that the API reported a build of about 1 million barrels last week. The EIA then came out and said there was a build of nearly 8 million. So part of this big number by the API could be a catch-up for last week.

DOE

- Crude +5.987mm (+2.5mm exp)

- Cushing +2.359mm (+800k exp)

- Gasoline +951k

- Distillates -2.666mm

After a massive reported crude build by API, traders were apprehensive ahead of the official DOE data – especially after last week’s big crude draw – and DOE reported a big crude draw of 5.987mm barrels (less than API but still big). Additionally, as Bloomberg notes, we’ve swung from fears of tank bottoms at the Cushing storage hub to concerns about how quickly it’ll grow…

WTI sunk below $72 ahead of the DOE data, heading for the biggest 2-day drop since July, and held those losses on the crude build…

“The oil market can not shield itself from the rout in equity markets,” said Norbert Ruecker, head of macro and commodity research at Julius Baer Group Ltd. in Zurich.

Meanwhile, WCS settled at $26.17/bbl, lowest at close since August 2016, pushing Western Canada Select’s discount to West Texas Intermediate crude to $52 a barrel on Tuesday, the widest on record…

The plunge in Canadian crude prices may dent exploration budgets and shrink the nation’s rig fleet, according to the chief executive officer of a major drilling contractor. The discount on Canadian crude will hammer cash flow, Precision Drilling Corp. CEO Kevin Neveu said at an event in Calgary.

With Canada’s debt and equity markets “almost closed” to energy producers, cash is the sole source of funding for drilling, he said.

“If cash flows get crimped back on a quarterly basis or a daily basis by the widening differential, they would adjust their rig counts sometimes even weekly,” Neveu said.

However, there is a silver lining as The National Post reports, Chinese oil buyers are making a beeline for a bargain across the Pacific.