GOLD: $xxx UP $xx (COMEX TO COMEX CLOSINGS)

Silver: $14.68 DOWN xxx CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : xxx

silver: $xxx

I will not be able to complete my commentary for today. However my morning data is accurate along with the comex data except inventory levels. Disregard all data from 1 pm on as the data is yesterdays.

I am not sure if I can deliver to you a commentary for Thursday.

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 30 NOTICE(S) FOR 3000 OZ

Total number of notices filed so far for OCT: 944 for 944400 OZ (2.9362 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 340 for 1,700,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6700: UP $64

Bitcoin: FINAL EVENING TRADE: $xxx UP xx

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY 232 CONTRACTS FROM 199,166 UP TO 199,398 DESPITE YESTERDAY’S 2 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

205 EFP’S FOR NOV. 1196 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1401 CONTRACTS. WITH THE TRANSFER OF 1717 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1401 EFP CONTRACTS TRANSLATES INTO 7.001 MILLION OZ ACCOMPANYING:

1.THE 2 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 2,050,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

27,035 CONTRACTS (FOR 13 TRADING DAYS TOTAL 27,035 CONTRACTS) OR 135.18 MILLION OZ: (AVERAGE PER DAY: 2429 CONTRACTS OR 12.145 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 135.18 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.33% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,354.69 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 299 DESPITE THE 2 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1401 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1700 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1401 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 232 OI COMEX CONTRACTS. AND ALL OF DEMAND HAPPENED WITH A 2 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.68 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 69 NOTICE(S) FOR 345,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER: 2,050,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 6670 CONTRACTS DOWN TO 474,418 DESPITE THE RISE IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A GAIN IN PRICE OF $1.00).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY GOOD SIZED 7549 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7549 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 474,418. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 879 CONTRACTS: 6670 OI CONTRACTS DECREASED AT THE COMEX AND 7549 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 879 CONTRACTS OR 87,900 OZ = 2.73 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.00.

YESTERDAY, WE HAD 7534 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 114,502 CONTRACTS OR 11,450,200 OZ OR 356.14 TONNES (13 TRADING DAYS AND THUS AVERAGING: 8.807 EFP CONTRACTS PER TRADING DAY OR 880,700 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 356.14 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 356/14/2550 x 100% TONNES = 13.96% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,031.96* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED inCREASE IN OI AT THE COMEX OF 6670 DESPITE THE GAIN IN PRICING ($1.00) THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7549 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7549 EFP CONTRACTS ISSUED, WE HAD A FAIR GAIN OF 2,826 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7549 CONTRACTS MOVE TO LONDON AND 6670 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 2.73 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A GAIN OF $1.00 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 87 notice(s) filed upon for 8700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.00 TODAY: /

ANOTHER BIG CHANGE IN INVENTORY

ANOTHER BIG DEPOSIT OF: 4.12 TONNES (NO DOUBT THAT THIS IS A PAPER GOLD ENTRY)

(THIS IS A GREAT SIGN THAT THE CROOKS ARE HAVING DIFFICULTY CONTAINING GOLD)

/GLD INVENTORY 748.76 TONNES

Inventory rests tonight: 748.76 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 332.912 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 232 CONTRACTS from 199,166 UP TO 199,398 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 205 EFP’s for November… and

1196 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1401 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 238 CONTRACTS TO THE 1401 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 1633 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 8.1650 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A INCREASE IN SILVER OI AT THE COMEX DESPITE THE 2 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1401 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

) WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 15.28 POINTS OR 0.60% //Hang Sang CLOSED //The Nikkei closed UP 271.12 OR 1.29%/ Australia’s all ordinaires CLOSED UP 1.16% /Chinese yuan (ONSHORE) closed DOWN at 6.9290 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 71.56 dollars per barrel for WTI and 81.22 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON//. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9290 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9251: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)ITALY

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a GAIN of 48 contracts to stand at 70 contracts. We had 1 notice filed YESTERDAY so we gained 49 contracts or AN ADDITIONAL 245,000 oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we GAINED 96 contracts up to 921 contracts. After November, we have a December contract and here we LOST 347 contracts down to 159.245

AND NOW COMPARISON FOR OCTOBER:

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

IMF Issues Dire Warning – ‘Great Depression’ Ahead?

IMF Issues Dire Warning – ‘Great Depression’ Ahead?

– “Large challenges loom for the global economy to prevent a second Great Depression” warn IMF

– Massive government debts and eroded fiscal buffers since 2008 suggest global dominos await a single market crash

– 2008 crisis measures cast long, dark “terrifying” shadow

by William Pesek via Asia Times

Is another “Great Depression” on the horizon?

It would be easier to dismiss these words from Nouriel Roubini, Marc Faber or other doom-and-gloom prognosticators. Coming from Christine Lagarde’s team, though, they take on a new dimension of scary.

The International Monetary Fund head isn’t known for breathlessness on the world stage. And yet the IMF sounded downright alarmist in its latest Global Financial Stability report, stating that “large challenges loom for the global economy to prevent a second Great Depression.”

Even some market bears were taken aback. “Why,” asks Michael Snyder of The Economic Collapse Blog would the IMF use this phrase “in a report that they know the entire world will read?”

Perhaps because, unfortunately, the findings of other referees of global risks – including the Bank for International Settlements – hint at similar dislocations.

Ten years after the Lehman Brothers crisis, these worrisome warnings that will be explored in depth at this week’s annual IMF meeting in Bali. The tranquil setting, though, will offer few respites from cracks appearing in markets everywhere – from Italy to China to Southeast Asia, where currencies are cratering like it’s 1998 again.

Source: Wikipedia

Source: Wikipedia

Potential flashpoints and a long line of dominos

Italy is the current flashpoint – and the latest target of “domino effect” chatter in frothy world markets. China’s shadow-banking bubble, and the extreme opacity and regulations that enable it, also came in for criticism. And, of course, the 800-pound beast in any room where global investors gather these days: Donald Trump’s assault on world trade.

But the real worry is the health of foundations underpinning these and other risks.

As the BIS warned on Sept. 23, the global economy faces a potential “relapse” of the “Lehman shock” of 2008. “Things look rather fragile,” says BIS chief economist Claudio Borio. Equally worrying, he adds: “There’s little left in the medicine chest to nurse the patient back to health or care for him in case of a relapse.”

A similar connection of dangerous dots runs through the IMF’s latest report. The big problem, says Malhar Nabar, deputy chief of IMF research, is the one that investors tend to ignore or explain away: how much of the Lehman fallout is still with us.

“There are many countries, even today, that are operating below pre-crisis trends,” Nabar says. “And what’s interesting is not just countries that suffered banking crises in 2007-2008 but also other countries outside of that epicenter that were affected through trade links or through financial links.”

Increased inequality is one troubling side-effect. Yet Nabar highlights, “possible long-lasting effects of the crisis on potential growth” that might seem tangential to Wall Street’s crash – lower birth rates, lower fertility and even “some evidence of slower technology adoption.” All this, he says, “can affect productivity growth and potential growth going forward.”

There is no doubt that many of the official policy actions taken since 2008 “seemed to have helped limit the harm.” But the costs of those efforts are only beginning to get calculated.

2008 crisis measures cast long, dark shadow

Excessively loose monetary policies have exacerbated the widening inequality trends unfolding pre-Lehman crackup. At the same time, there’s been, in the words of the IMF, a “large accumulation of public debt and the erosion of fiscal buffers in many economies following the crisis point to the urgency of rebuilding defenses to prepare for the next downturn.”

Yet all the diplomatic speak in the world can’t sugarcoat the roughly $250 trillion crisis unfolding in slow motion. That’s the level to which the world’s debt burden ballooned since the Lehman crash. That’s 18 times China’s annual gross domestic product.

And with official rates from Washington to Tokyo still at ultra-low levels historically, there’s little ammunition to battle the next reckoning.

Italy’s debt woes are an obvious weak link. One reason: just as with US officials after 2008, Europe did more to treat the symptoms of its woes than address underlying causes.

So is China’s unbalanced economy, one being trolled by US President Donald Trump’s tariffs arms race. This year’s 6.4% drop in the yuan is raising eyebrows for good reason. For one thing, it coincides with a marked slowdown in exports, industrial production, fixed-asset investment and an 18% plunge in Shanghai stocks this year. For another, it raised the specter of sizable defaults on dollar debt, which would reverberate through the global economy.

And therein lies Asia’s problem.

Asia’s exposure

In general, the region has journeyed a long way since the darkest days of 1997 and 1998. Financial systems are stronger and governments are more transparent. Currencies are more flexible. Foreign-exchange reserves have been rebuilt. That leaves advanced economies from South Korea to Singapore reasonably well equipped to withstand fresh turmoil.

But there are cracks in the region’s developing markets, as the ferocity of currency plunges in India, Indonesia and the Philippines show. Investors may argue they’ve learned from past misstates, but still fall prey to herd mentalities.

It’s an urgent wakeup call for India’s Narendra Modi, Indonesia’s Joko Widodo and Rodrigo Duterte of the Philippines to narrow current-account and budget deficits. Leaders also need to devise macroprudential firewalls against global contagion.

The problem for Asia: contagion could come as much from the West and its own backyard.

Trump’s fiscal incompetence – including a $1.5 trillion tax cut America didn’t need – could roil global rates and the dollar. A recent spike in 10-year yields to 3.2%, the highest in seven years, could be a bad omen. Trump, too, is publicly dueling with his hand-picked Federal Reserve chairman. And given Trump’s legal woes, the odds of new tariffs or even military action to distract voters can’t be ruled out.

Any new assault on China could devastate Japan’s reflation effort. True, epic Bank of Japan easing and a weaker yen boosted exports. It pushed Nikkei 225 index stocks to 27-year highs. Yet Asia’s No. 2 economy is in harm’s way if the US-China brawl trumps the region’s key growth engine.

Even before most policymakers and financiers arrive in Bali this week, the IMF is signaling that global growth has plateaued. It downgraded output to 3.7% from 3.9%.

That not the end of the world, per se. But with trade battles intensifying and dormant old devils re-emerging, all bets could soon be off.

That is a lot more than depressing: it’s terrifying.

IMF Global Financial Stability Report (2018) can be accessed here

Avoid Digital & ETF Gold – Key Gold Storage Must Haves

News and Commentary

Gold prices hold steady as investors wait for Fed minutes (Reuters.com)

Asian markets jump following Wall Street’s big gains (MarketWatch.com)

U.S. industrial output rises, but momentum slowing (Reuters.com)

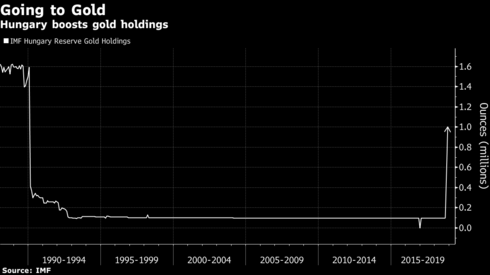

Hungary Boosts Gold Reserves 10-Fold, Citing Safety Concerns (Bloomberg.com)

Hungary raises gold reserves tenfold on safety concerns (RT.com)

Source: Bloomberg

Art mania and tech stocks – The financial canary’s desperate last gasp (MoneyWeek.com)

China May Have $5.8 Trillion in Hidden Debt With ‘Titanic’ Risks (Bloomberg.com)

S&P Reveals $5.8 Trillion In “Hidden” Chinese Debt With “Titanic Credit Risks” (ZeroHedge.com)

Your shout: how gold could bring stability to volatile crypto markets (WhatInvestment.co.uk)

October Doesn’t Disappoint: Volatility Is Back After a Tranquil Third Quarter (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

16 Oct: USD 1,228.85, GBP 931.35 & EUR 1,061.73 per ounce

15 Oct: USD 1,233.00, GBP 937.70 & EUR 1,064.45 per ounce

12 Oct: USD 1,218.75, GBP 922.11 & EUR 1,052.15 per ounce

11 Oct: USD 1,201.10, GBP 910.31 & EUR 1,040.27 per ounce

10 Oct: USD 1,186.40, GBP 902.02 & EUR 1,033.00 per ounce

09 Oct: USD 1,187.40, GBP 910.26 & EUR 1,036.01 per ounce

Silver Prices (LBMA)

16 Oct: USD 14.76, GBP 11.16 & EUR 12.74 per ounce

15 Oct: USD 14.74, GBP 11.19 & EUR 12.71 per ounce

12 Oct: USD 14.60, GBP 11.04 & EUR 12.60 per ounce

11 Oct: USD 14.40, GBP 10.90 & EUR 12.45 per ounce

10 Oct: USD 14.38, GBP 10.92 & EUR 12.50 per ounce

09 Oct: USD 14.33, GBP 10.98 & EUR 12.51 per ounce

Recent Market Updates

– Poland Raises Gold Holdings to Record High in September – IMF

– Why It’s Worth Holding Gold Bullion in Your Portfolio

– Gold’s Best Day In 2 Years Sees 2.5 Percent Gain As Global Stocks Sell Off – This Week’s Golden Nuggets

– Gold Up 2.5 Percent As Global Stock Rout Spreads To Europe

– “Gold Is On The Cusp” Of An “Explosion Higher” As Stock and Tech “Crash Is Coming”

– Gold Bottoms As Gold Industry Consolidates and Weak Hands Capitulate

– 60 Charts For The (Last Few Remaining) Gold Bulls

– Poland and Australia Buy Gold As Global Property Bubble Bursts – This Week’s Golden Nuggets

– Brexit To Burst Dublin and London Property Bubbles? GoldCore Video

– Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

– “I’m Favouring Equities and Gold Over Bonds” – Stepek

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold,silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke at Sprott Money: Golden implications of

total U.S. deficits, debt, and debt service

8:54p ET Tuesday, October 16, 2018

Dear Friend of GATA and Gold:

Writing at Sprott Money tonight, the TF Metals Report’s Craig Hemke explains how the U.S. government’s budget deficit is far greater than generally understood. Hemke adds that if the price of gold returns to its normal relationship with total U.S. government debt, the price will be far higher than it is today.

Hemke’s analysis is headlined “The Golden Implications of Total U.S. Deficits, Debt, and Debt Service” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-golden-implications-of-total-us-def…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

_________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9290/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9250 /shanghai bourse CLOSED UP 15.28 POINTS OR 0.60%

. HANG SANG CLOSED

2. Nikkei closed UP 271.12 POINTS OR 1.29%

3. Europe stocks OPENED IN THE RED EXCEPT LONDON FTSE

/USA dollar index RISES TO 95.13/Euro FALLS TO 1.1537

3b Japan 10 year bond yield: RISES TO. +.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.56 and Brent: 81.22

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.46%/Italian 10 yr bond yield UP to 3.49% /SPAIN 10 YR BOND YIELD DOWN TO 1.63%

3j Greek 10 year bond yield FALLS TO : 4.26

3k Gold at $1226.35 silver at:14.69 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 25/100 in roubles/dollar) 65.60

3m oil into the 71 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.28DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9832 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1457 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.46%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.16% early this morning. Thirty year rate at 3.33%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6976

US Futures Slide To Session Lows As Global Stock

Rebound Fizzle Loses Steam

S&P 500 futures fell to session lows, down 0.3% following yesterday’s torrid rally, while Nasdaq 100 futures also turned red despite Netflix’ 12% surge. The global rally fizzled as European shares pared earlier gains and turned flat in morning trade, after the Stoxx Europe 600 gained 1.6% on Tuesday. The dollar rebounded, trading at session highs and Treasuries were unchanged at 3.17%.

Europe was dragged lower by auto stocks after data showed car sales in the region plunged in September and Goldman warned 3Q was a “challenging” quarter for industry, with potential for downward earnings revisions by suppliers. The drop outweighed a gain for technology companies in the wake of solid results from chip maker ASML Holding NV.

Europe’s slide reversed an upbeat mood earlier in Asia where MSCI’s ex-Japan share index added 0.6% while Japan’s Nikkei jumped 1.3%; South Korean and Australian shares also posted strong gains, while even the Shanghai Composite rose 0.6% after dipping in early trading.

The gains followed a scintillating New York session where the three major indexes saw their biggest one-day percentage gains since March, rising more than 2% each.

In the currency market, the pound dropped after U.K. inflation slowed more than expected, while the euro edged down as consumer price numbers came in as expected.

While investors are skeptical the recent volatility is over, they also hope another strong quarter of corporate profits will calm nerves jangled by trade tensions and rising bond yields. Third-quarter earnings for S&P 500 companies are seen growing 22% according to consensus.

“There are negative risks in the short term, but on the positive side we have good earnings and data from the United States,” said Christoph Barraud, an economist at Paris-based brokerage Market Securities. “Last week’s correction was extreme, a lot of people became short (the market) so this is a bit of normalization.”

The latest gains in the S&P were triggered by Netflix, which soared 12% after the close as its subscriber numbers blew away expectations. That sent shares of Alphabet Inc, Facebook Inc and Amazon.com Inc up about 1 percent in extended trade

Banking giants Goldman Sachs and Morgan Stanley also posted better-than-expected quarterly profits. And on the data front, U.S. industrial production rose for a fourth straight month in September, soothing fears the economy may be running out of steam. As a result, Barraud said the out-performance of U.S. equities was likely to continue: “People want to put money where there is best visibility … In the U.S., you have growth visibility, strong earnings (as well as) buybacks and dividends … So the U.S. is still attractive compared to peers.”

To be sure, it’s still early in the earnings season but the better-than-expected numbers are welcome amid a risk-heavy global picture, which features periodic Brexit headlines, a divisive Italian budget, a lingering trade spat between the U.S. and China, concern surrounding the disappearance of a Saudi journalist and President Donald Trump’s criticism of the Federal Reserve

The upbeat mood also favored EM currencies and took some steam out of the safe-haven yen. Turkey’s lira traded just off 2 1/2-month highs, having rallied 10% over the past week as the release of an imprisoned U.S. pastor fueled hopes of a rapprochement with Washington. Ankara said investors had put in $6 billion in bids for $2 billion of bonds it sold on Tuesday, though it had to pay a substantial new-issue premium.

Sterling was the worst performing G-10 currency as UK Sept. headline CPI printed lower than expected. Brexit discussions remain in focus, with PM May set to meet Tusk, Juncker and Varadkar before this evening’s summit.

The Bloomberg Dollar Spot Index edged higher while the greenback stayed in tight ranges versus most of its major peers before the Federal Reserve releases its September meeting minutes and as markets continue to wait on the U.S. semi-annual currencies report. The dollar rose 0.15 percent against a basket of currencies after being undermined on Tuesday fresh criticism of the U.S. Federal Reserve from Trump. He told Fox Business Network: “My biggest threat is the Fed.”

“While such name calling shouldn’t mean anything in terms of what the Fed actually does, it is a factor which somewhat undermines sentiment toward the dollar,” Ray Attrill, head of currency strategy at National Australia Bank, said.

In rates, French bonds pulled EGBs higher, with BTPs continuing to benefit from improving sentiment and lack of headlines following the Italian draft budget being submitted to the European Union. Germany 30y sale technically covered, though demand slips compared with prior; bonds stay higher. Core bonds pushed higher from the open, with France leading gains and German 10y yields dipping further below 0.5%. BTPs rallied for a third day, led by the front end, following Monday’s budget submission; still, the news flow is likely to be negatively skewed in the coming weeks with the European Commission expected to provide its initial response to proposals within a week, and ratings reviews from Moody’s and S&P due before the end of the month.

Elsewhere, oil traded in the red and in close proximity to recent lows with WTI approaching USD 71.50/bbl to the downside while Brent edges further below USD 82.00/bbl following a surprise draw on yesterday’s API crude data. OPEC Secretary General Barkindo emerged stating that OPEC+ have decided to sustain market balance and are cautiously optimistic the oil market will remain well supplied, while Saudi are to ensure there is no shortage in the oil market. Traders will be eying the weekly DoE crude inventory data release along with any developments surrounding journalist Khashogghi who went missing at the Saudi Consulate in Istanbul. Elsewhere, metals are mixed with gold mirroring dollar action while copper came off lows.

Minutes of the last Fed meeting are due out later Wednesday and should show it committed to further tightening. Expected data include mortgage applications and housing starts. Abbott, U.S. Bancorp, Alcoa, Crown Castle, and Northern Trust are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.2% to 2,813.25

- STOXX Europe 600 up 0.2% to 365.54

- MXAP up 0.9% to 154.72

- MXAPJ up 0.5% to 485.19

- Nikkei up 1.3% to 22,841.12

- Topix up 1.5% to 1,713.87

- Hang Seng Index up 0.07% to 25,462.26

- Shanghai Composite up 0.6% to 2,561.61

- Sensex down 0.2% to 35,079.00

- Australia S&P/ASX 200 up 1.2% to 5,939.10

- Kospi up 1% to 2,167.51

- German 10Y yield fell 1.6 bps to 0.475%

- Euro down 0.06% to $1.1567

- Italian 10Y yield fell 9.1 bps to 3.081%

- Spanish 10Y yield fell 0.6 bps to 1.637%

- Brent futures up 0.1% to $81.50/bbl

- Gold spot up 0.2% to $1,227.30

- U.S. Dollar Index up 0.2% to 95.231

Top Overnight News

- Saudi Arabia understands the need to conclude its investigation into the disappearance of government critic Jamal Khashoggi in a timely and rapid fashion, U.S. Secretary of State Mike Pompeo said

- Federal Reserve meeting minutes set for release at 2 p.m. Wednesday in Washington could flesh out what factors are informing policymaker debate on the location of the neutral rate — a highly-uncertain dividing line between easy and tight money — and whether they should go above it. It is also likely Trump’s trade war was also discussed at September meeting.

- China’s holdings of U.S. Treasuries fell for a third consecutive month in August as the Asian nation struggles to prevent the yuan from weakening amid trade tensions with America.

- Theresa May was told the latest Brexit proposals would be thrown out by Parliament in a stark reminder of the constraints on the U.K. prime minister as she heads into a summit to try to break the deadlock. According to three people familiar with the matter, government Chief Whip Julian Smith told her top ministers that the current guarantee to avoid a policed border with Ireland doesn’t have enough votes to pass.

- Three British traders accused of conspiring to manipulate the $5.1-trillion-a-day currency market were actually playing “fix poker” — bluffing each other to make money, not cooperating to rig the system, according to a lawyer for one of the men

- A senior Treasury department official warned that a hard Brexit could hurt global financial stability and said the U.S. is working with officials in the U.K. and EU to limit risks of Britain’s withdrawal from the bloc

- In her first remarks as a monetary policy maker, Federal Reserve Bank of San Francisco President Mary Daly said that she favors continued gradual interest-rate increases as the labor market overshoots full employment and inflation comes in near-goal

- President Donald Trump called the Federal Reserve his “biggest threat,” again criticizing the central bank for endangering economic growth through interest-rate hikes

- Australia’s jobless rate might need to decline further than in the past in order to generate faster wage growth, the central bank’s No. 2 official Guy Debelle said

- China’s holdings of U.S. Treasuries fell for a third consecutive month in August as the Asian nation struggles to prevent the yuan from weakening amid trade tensions with America

Asia-Pac equity markets were higher across the board as the region got a tailwind from the earnings-fuelled momentum in the US, where all majors gained over 2% and the tech sector led the advances after strong earnings including Netflix which beat on EPS and subscriber additions. ASX 200 (+1.1%) gained from the open with the tech sector mimicking the outperformance of its counterpart stateside, although miners underperformed as BHP suffered from weak quarterly output figures. Elsewhere, Nikkei 225 (+1.2%) benefitted from the broad optimism and edged closer towards the 23k level, while Hang Seng was closed for holiday and Shanghai Comp. (+0.1%) was higher amid some quasi-measures including a relaxation of FX related regulations to promote trade and facilitate investment.

Top Asian News

- China Stock Rout Puts $613 Billion of Share Pledges at Risk

- China Moves to Boost Bond Trading With Tri-Party Repo Launch

- Billionaire Family’s Energy-Drink Firm Surges 20% in Debut

- Indonesia Bonds Rally After FinMin Flags Lower Budget Deficit

Most major European bourses are mixed with Germany’s DAX underperforming as the index is weighed on by Fresenius Medical (-15.0%) amid a profit warning, while auto names are also pressure the benchmark following downbeat new car registrations, subsequently pushing the European auto sector lower by over a percent, with some attributing the weakness to Goldman’s downbeat view on Q3 Stoxx 600. On the flip side, the tech sector outperforms following optimistic earnings from ASML (+4.0%) which in turn lifted the likes of STMicroelectionics (+3.0%) and Infineon (+1.0%) in sympathy. Elsewhere, Fresenius SE (-11.9%) rests at near the foot of the DAX after the company cut guidance, while Crest Nicholson (-4.7%) is firmly in the red amid a profit warning.

Top European News

- Nordea Money Flows Questioned as Browder Seeks Nordic Probes

- Falcon Edge’s Gerson Said to Field, Reject Russia Fund’s Advance

- U.K. Inflation Slows More Than Expected on Food, Transport

In FX, focus was on the GBP which was boosted by above average earnings yesterday, but softer than forecast UK CPI undermined Sterling in the run up to Wednesday’s EU summit on Brexit and pre-dinner speech by PM May. Cable is now down around one full point from 1.3200+ peaks as a result, while Eur/Gbp is retesting 0.8800. Note, bids are said to be waiting at 1.3100 and 1.3080 if the low so far circa 1.3130 is breached. AUD/JPY/NZD: Marginal outperformance against the Greenback, but again very confined ahead of FOMC minutes, with the Aud benefiting from a short squeeze overnight and climbing above 0.7150, but now drifting back down and perhaps wary about a hefty 1.1 bn option expiry at the 0.7125 strike. Meanwhile, the Jpy has recovered from 112.40 lows as heavy supply up to 112.50 continues to provide support and the Kiwi has retested 0.6600, but remains capped near the big figure.

Oil traded in the red and in close proximity to recent lows with WTI approaching USD 71.50/bbl to the downside while Brent edges further below USD 82.00/bbl following a surprise draw on yesterday’s API crude data. OPEC Secretary General Barkindo emerged stating that OPEC+ have decided to sustain market balance and are cautiously optimistic the oil market will remain well supplied, while Saudi are to ensure there is no shortage in the oil market. Traders will be eying the weekly DoE crude inventory data release along with any developments surrounding journalist Khashogghi who went missing at the Saudi Consulate in Istanbul. Elsewhere, metals are mixed with gold mirroring dollar action while copper came off lows. Separately, mining giant BHP has reported a 8% increase in Q1 iron ore production on the back of strong Chinese demand.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -1.7%

- 8:30am: Housing Starts, est. 1.21m, prior 1.28m; MoM, est. -5.62%, prior 9.2%

- 8:30am: Building Permits, est. 1.27m, prior 1.23m; MoM, est. 2.04%, prior -5.7%

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

The big question after yesterday’s move is whether US earnings season is coming to the rescue of markets. Risk assets rallied hard yesterday, with the S&P 500 posting its best daily gains since March, rallying +2.15%. The rally was very broad, with 92.6% of S&P 500 companies gaining on the day, the third highest rate of the year. As earnings season accelerates into its busiest portion of the calendar, the reports out yesterday boosted sentiment, with positive news from the healthcare, financial, tech, and transport sectors. The DOW, NASDAQ and NYFANG performed similarly well, gaining +2.17%, +2.89% and +3.63%, respectively. The tech sector may have been boosted by bullish talk of a potential Uber IPO, with the Wall Street Journal reporting that investment banks have proposed valuing the ride-hailing firm at $120bn, far above its prior valuation of around $70bn. Tech outperformed in Europe too, with the Stoxx IT index gaining +3.30% versus the broad Stoxx 600’s +1.58% gain. The DAX and CAC gained +1.40% and +1.53%. Ten-year Bund yields rallied -1.2bps, while Treasuries and the dollar were little changed. EM equities gained +2.51% while EM FX gained +0.58%, led by gains in the Turkish Lira (more below).

Several major US companies reported strong third quarter earnings yesterday, highlighted by UnitedHealthcare, Morgan Stanley, Goldman Sachs, Netflix, and the transport firm CSX. UnitedHealthcare beat consensus earnings estimates and boosted its full-year outlook, with investors relieved to hear the company talk down concerns over rising costs. Morgan Stanley and Goldman Sachs both beat consensus estimates as well, with investment banking revenues up strongly. Both saw mixed trading activity, with FICC up and equities down. Netflix gained around 12% after US markets closed last night, as it beat expectations on revenue, earnings, and – most importantly – subscribers. The railway firm CSX beat expectations as well, and in an encouraging signal for the macroeconomy, reported a robust increase in freight volumes on the quarter. Blackrock and IBM both underperformed after their earnings reports, but they were overshadowed by the slew of positive news.

This morning in Asia markets are up largely tracking the strong session on Wall Street. The Nikkei (+1.50%), Shanghai Comp (+0.10%), Kospi (+1.20%) and ASX (+1.18%) are all up. Markets in Hong Kong are closed for a holiday. Elsewhere, Futures on S&P 500 (-0.06%) are largely unchanged.

Elsewhere, our economists continue to think that Italy is squarely on a collision course with the European Commission, whose President Juncker said yesterday that there would be a “violent reaction” from other euro area countries if the Italian budget were to be approved. The Commission has two weeks to decide on whether to ask for budget revisions. Nevertheless, Italian assets gained yesterday in the first trading session since the government finalised the budget plan. The FTSE-MIB gained +2.23%, pacing gains in Europe, and 10- year BTPs rallied -9.3bps. Partially this reflected the broader risk-on sentiment yesterday, but it may also have been a reaction to a new poll showing Five Star + Northern League support at 58.6%, still a majority but at its lowest level in over six weeks.

Also in European politics, Prime Minister May navigated her cabinet meeting without major controversy, while European Council President Tusk reportedly briefed national euro area leaders that a Brexit deal is not likely to be completed until December. Later in the session, FAZ reported that the EU will offer the UK the option to stay in the EU beyond December 2020 to allow more time for everything to be in place that needs to be. However, it’s not clear how that would help Mrs May with the Brexiteers in her party. The pound gained around +0.25% on the session, though it was also buoyed by strong data (more below). Mrs May goes to Brussels today for the EU leaders Brexit summit. Expect lots of headlines but little progress yet.

Back to markets and Brent crude oil gained 0.97% as the diplomatic spat between Turkey, Saudi Arabia, and the US over the disappearance of the dissident journalist Khashoggi continued to fester. Senator Lindsey Graham described Mohammed bin Salman as “toxic,” but President Trump said he had a productive call with the Crown Prince, which defused tensions. Forwards on the South African Riyal retraced some of Monday’s big moves, and the Tadawul index – the country’s benchmark index – gained +0.99%. The Tadawul has outperformed most other equity indexes this year, up +6.10%. Separately, the Turkish Lira gained +2.07% for its eighth consecutive daily gain, the longest streak since 2014, as the country continues to benefit from defused tensions with the US and better sentiment.

On the economic data front, the official UK unemployment rate for August printed at +4.0% as expected, matching its cyclical low. August average weekly earnings ex-bonuses rose +3.1% 3m/3m, its fastest pace since January 2009. In Germany, the ZEW survey of financial market experts showed a modest slide, with the assessment of the current situation sliding 5.9pts to 70.1 (versus expectations for 74.4) and the forward-looking expectations down to -24.6 (versus -12), tying the lowest level since 2012. In the US, September industrial production rose +0.3% mom versus expectations for a +0.2% gain. The Fed noted that Hurricane Florence likely depressed the print by 0.1pp, so the trend was even more positive. On the other hand, capacity utilisation missed expectations by 0.1pp at 78.1%, which partially balanced out the IP print. Finally, the JOLTS job data showed a new all-time high number of job openings at 7,136,000, equivalent to 115 for every 100 unemployed workers. That’s a big improvement from the recession lows of 15 openings for every 100 unemployed workers. The quits rate also stayed at its postcrisis high, which has been a good leading indicator of wages.

Looking ahead to today’s data, the highlight will be the release of the latest FOMC policy meeting minutes at 19:00 BST. In Europe, we get the September EU27 new car registrations, and the euro area’s August construction output and final September CPI. It’s a busy day in the UK, with September CPI, RPI, PPI input, PPI output and the August house price index all due, along with minutes of the BoE’s Oct Financial Policy Committee meeting. In the US, we get September housing starts and building permits along with latest weekly MBA mortgage applications. Away from data, the EU leaders will start to discuss the next steps for Brexit in Brussels while separately, ECB Chief Economist Peter Praet will be speaking at an event in Madrid. Alcoa, Kinder Morgan, Northern Trust, and US Bancorp will report their earnings.

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 15.28 POINTS OR 0.60% //Hang Sang CLOSED //The Nikkei closed UP 271.12 OR 1.29%/ Australia’s all ordinaires CLOSED UP 1.16% /Chinese yuan (ONSHORE) closed DOWN at 6.9290 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 71.56 dollars per barrel for WTI and 81.22 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON//. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9290 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9251: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

S and P reveals that China has an extra 5.8 trillion dollars of hidden debt with titanic credit risks. The new Chinese debt to GDP total is now 340%. GDP is 11 trillion dollars so total USA dollar debt outstanding: 38 trillion dollars.

S&P Reveals $5.8 Trillion In “Hidden” Chinese Debt With “Titanic Credit Risks”

When it comes to estimating China’s total outstanding debt, there has long been confusion about the real number with most putting the debt/GDP at around 250%, while the IIF last year calculated China’s debt load as high as 300% of GDP.

Now, China watchers can one add another ~40% of debt/GDP to the total because according to S&P, China’s local governments have accumulated 40 trillion yuan ($5.8 trillion) – or even more – in off-balance sheet debt, suggesting the already record surge in defaults is set to accelerate further.

“The potential amount of debt is an iceberg with titanic credit risks,” S&P credit analysts wrote in a report Tuesday, Bloomberg reported, with much of the build-up related to local government financing vehicles, which don’t necessarily have the full financial backing of local governments themselves.

LGFV debt has emerged as a growing risk for China’s economy, because with the national economy slowing, and as a result of a crackdown on shadow lending and a Beijing quota for issuance of local-government bonds not enough to fund infrastructure projects to support regional growth, authorities across the country have resorted to LGFVs to raise financing, according to S&P.

That’s left LGFVs “walking a tightrope” between deleveraging and transforming their businesses into more typical state-owned enterprises, S&P warned.

Meanwhile, debt vulnerabilities continue to rise as a result of the previously reported record surge in Chinese corporate defaults this year, as Beijing seeks to roll back a decades-old practice of implicit guarantees for debt.

And while so far LGFV debt has avoided an event of default, several issues have come close, with local government bailouts taking place only in the last minute, adding to concerns about LGFVs vulnerabilities. Meanwhile, according to S&P the riskiest LGFVs include the following:

- Those tied to weaker prefectural, city or district-level governments with lax supervision over state-owned enterprises.

- Those focused on commercial activities – thus having diminishing importance to local governments.

- Those with significant refinancing risks thanks to large short-term debt or reliance on borrowing from the shadow-banking sector.

As Bloomberg notes, the focus on funding to sustain growth at the local level echoes a broader shift in the central government, which last year was focused on reducing leverage in the financial system. That phase is essentially over, thanks in part to an escalating trade war with the U.S., according to Citi. The result has been a sharp slowdown in China’s debt-reliant economy.

“The markets are right, in our view, to feel more concerned about the sustainability of China’s debt and the increased financial risks,” said Citi’s chief China economist Liu Li-Gang, who also saw “renewed pressure” on the yuan as the currency continues to creep ever lower to the PBOC “redline” of 7.00.

Meanwhile, despite China’s recently renewed shift toward fiscal stimulus, S&P said that Beijing remains determined to “bring discipline to the financing practices of local governments and their LGFVs.” That may mean local authorities aren’t fully able to keep LGFVs afloat, however, and the bottom line is “the default risk of LGFVs is increasing.” That said, the first LGFV default has yet to hit; how it will impact the broader market as yet another hub of moral hazard is wiped out remains to be seen.

end

Trump abandons a 144 yr old shipping treaty which allows small pkgs to be delivered into the USA at a huge discount

(courtesy zerohedge)

Trump Goes Postal – Abandons 144-Year-Old ‘Unfair’ Shipping Treaty With China

“Something has to be done…How can my government be subsidizing China and driving me out of business?”

Those are the words of Jayme Smaldone, who runs a 12-employee housewares company in Rahway, N.J., who first became aware of the problem when he noticed websites selling Chinese knockoffs of his “Mighty Mug,” a desktop coffee cup he designed with an anti-topple base.

And it appears President Trump has listened to Jayme among many others, as The New York Times reports that he plans to withdraw from a 144-year-old postal treaty that has allowed Chinese companies to ship small packages to the United States at a steeply discounted rate, undercutting American competitors and flooding the market with cheap consumer goods.

Peter Navarro, Mr. Trump’s hard-line trade adviser, wrote in a Financial Times op-ed last month.

“These disparities have introduced a massive distortion in the eCommerce market.

It is often possible for a Chinese company to sell ‘knockoff’ products through online vendors, such as Amazon or Alibaba, to U.S. consumers for less than it costs for American mailers to ship authentic goods. Moreover, while USPS loses an estimated $1 on every small package that arrives from China, outbound mail of American exporters is charged at well above cost.”

As The New York Times details, a 2015 report from the Inspector General of the United States Postal Service found that the treaty, which was created to ease the flow of mail and small parcels between 192 countries, had not been overhauled to reflect the new realities of eCommerce and China’s aggressive undercutting of international competitors.

The price of shipping a 4.4 pound package, the largest parcel covered by the treaty, from China to the United States is about $5, according to United States estimates, according to post office estimates culled by Mr. Navarro’s staff.

American companies can pay two to four times that amount to ship a similar package from Los Angeles to New York, and much more for packages sent to China.

The “system creates winners and losers,” the report’s author’s concluded, especially China’s national postal service and “Chinese online retailers in the lightweight, low-value package segment at the expense of the U.S. PostalService and American retailers.”

It is not clear how much the disparity costs American taxpayers and retailers, in part because the Postal Service does not release detailed country-by-country shipping breakdowns. A 2014 study, cited in a Postal Service analysis of the issue, estimated that discounted shipping cost industrialized nations as much as $2.1 billion a year in aggregate.

The losses to retailers and manufacturers could be much more, as online commerce expands further.

Presumably, President Obama decide to ignore the 2015 report.

What is most odd about this decision by President Trump is no one is against it, no one is complaining at Trump “breaking norms” or “isolationism” or “being racist” – politicians and industry groups are all in agreement that it was unfair and needed to stop…

Even industry groups that have questioned the president’s tariffs on Chinese imports, applauded the move as proportional and targeted.

“This outdated arrangement contributes significantly to the flood of counterfeit goods and dangerous drugs that enter the country from China,” said Jay Timmons, chief executive of the National Association of Manufacturers, a trade group.

“Manufacturers and manufacturing workers in the United States will greatly benefit from a modernized and far more fair arrangement with China.”

“Manufacturers are pleased to see that this issue has been elevated to the very highest levels in the Trump Administration.”

Patrick Hedren, National Association of Manufacturers vice president for labor, legal and regulatory policy, said in an emailed statement:

“Manufacturers have struggled in recent years with the rapid growth of counterfeit goods pouring in to the country through the U.S. postal system from countries like China. This problem is fueled by heavily subsidized shipping rates and it displaces American innovators from online marketplaces,”

The announcement was welcome news to Sen. Bill Cassidy, R-La., who has been pushing legislation on the issue.

“I’ve been working with the administration for months on addressing this terrible deal, because American companies are being run out of business by foreign competitors making cheap knockoff products they can ship to Louisiana for less than it costs an American company to mail the genuine product,” he said in a statement.

“President Trump is standing up for American workers and companies who are being hurt by this outdated, unfair international agreement on shipping rates.”

A new front has been opened in the trade war with China – the question is: how will China respond to this one?

4.EUROPEAN AFFAIRS

Italian Bonds Slide After Official Warns Credit Rating Downgrade Possible

After starting off strong, Italian 10Y Yields have leaked wider all morning after a senior government official said on Wednesday that Italy’s 2019 budget may be rejected by the European Commission and a credit rating downgrade is also possible.

“Let’s say that the premise is there” for the commission to start an infraction process over the budget, Stefano Buffagni, cabinet undersecretary for regional affairs, said in an interview with Radio Capital cited by Reuters.

“Premier (Giuseppe) Conte is going to the EU to explain the motivations” behind the budget, he added.

With Moody’s and Standard & Poor’s due to review Italy’s credit rating this month, Buffagni said a downgrade “can’t be excluded and we must be ready” in case it happens. He added, however, that he did not think a downgrade would be justified because “Italy has very solid economic fundamentals”.

Meanwhile, Deutsche Bank economists said they think that Italy is squarely on a collision course with the European Commission, whose President Juncker said yesterday that there would be a “violent reaction” from other euro area countries if the Italian budget were to be approved.

The Commission has two weeks to decide on whether to ask for budget revisions. Nevertheless, Italian assets gained yesterday in the first trading session since the government finalized the budget plan amid the broad market euphoria. The FTSE-MIB gained +2.23%, pacing gains in Europe, and 10- year BTPs rallied -9.3bps, however much of this move is being reversed on Wednesday. Partially this reflected the broader risk-on sentiment yesterday, but it may also have been a reaction to a new poll showing Five Star + Northern League support at 58.6%, still a majority but at its lowest level in over six weeks.

EU Commission To Reject Italian 2019 Budget Plan

Earlier this morning, we reported that according to Deutsche Bank economists – and virtually everyone else except for those who were apparently waving in BTPs yesterday – Italy was squarely on a collision course with the European Commission, whose President Juncker said yesterday that there would be a “violent reaction” from other euro area countries if the Italian budget were to be approved.

Moments ago, Spiegel confirmed this when it reported that the “dispute between the EU Commission and Italy’s populist government is entering the next round” after EU Commissioner Guenther Oettinger said that the EU Commission would reject Italy’s 2019 budget plan, which is not compatible with EU rules.

“It has been confirmed that Italy’s budget for 2019 is not compatible with the commitments that exist in the EU,” Oettinger said. The official rejection of Italy’s budget in the form of a letter from Economic and Financial Commissioner Pierre Moscovici is due to arrive in Rome on Thursday or Friday.

EU Economic and Financial Affairs Commissioner Pierre MoscoviciItaly submitted its budget draft at the last minute on Monday night, giving the Commission two weeks to respond, but it appears it won’t need that long. Moscovici will reportedly not to submit any counterproposals to the Italian budget, but merely point out the breach of the agreed framework data.

EU Economic and Financial Affairs Commissioner Pierre MoscoviciItaly submitted its budget draft at the last minute on Monday night, giving the Commission two weeks to respond, but it appears it won’t need that long. Moscovici will reportedly not to submit any counterproposals to the Italian budget, but merely point out the breach of the agreed framework data.

As a reminder, Italy’s coalition of a nationalist and populist forces plans to increase the country’s deficit to 2.4% GDP next year to finance its expensive campaign pledges. This is three times more than the 0.8% that the Italian previous government had agreed with the European Commission, and it could become even more, as the 2.4% forecast is based on the Italian government’s highly optimistic assumptions about economic growth.

Still, many have accused the EU of hypocrisy in cracking down on Italy while letting other, just as egregious budgets slide in recent years.

Commenting on the Italian budget, in an overnight note Goldman said that Italy is not the only country to deviate from the EU’s country-specific recommendations and be in breach of the fiscal rules, with the bank noting that France is also non-compliant with the public debt rule. “That said, the French budget does not breach the expenditure benchmark rule; moreover, France can justify its deviation from the structural adjustment path on the basis of the structural reforms it is implementing.”

There is one mitigating factor according to Goldman: “it could be argued that France’s deviations from the structural adjustment path reflect the current government’s aim to boost potential growth, in particular through an increase in capital stock and labour participation, it is more difficult to make the same case for Italy, where the reforms to the pension system imply a deterioration in the medium-term sustainability of public finances.”

Goldman concludes that while it does not expect the EC to initiate a formal procedure vis-à-vis France, the EC will likely send a formal warning to Italy to initiate a significant deviation procedure. Although any such procedure is unlikely to end with the application of fines, it would likely generate further tensions between Italy and the EC, and increased volatility in the Italian sovereign bond market. A different stance vis-à-vis France could also lead to further criticism from the Italian government of the European Union and its rules.

Meanwhile, the earlier news of a warning about a potential sovereign credit rating downgrade and the Spiegel news have pushed Italian 10Y yield 7bps higher, back over 3.50%, erasing most of yesterday’s gains.

European Car Sales Plunge 23%, Dragging Market Lower

The global carmageddon wave is spreading: just two weeks after the US reported its worst auto sales in years – now ex dealer incentives, and just days after the latest Chinese data showed passenger-car purchases by dealerships plunged 12% from a year earlier to just over 2 million units in September, the biggest drop on record…

… the auto weakness has hit Europe, where passenger car registrations in Europe slumped 23% during September after new emissions test rules took hold, reversing August gains when automakers were hurrying vehicles out the door to beat the deadline.

Europe’s tougher testing methods are designed to produce results more in line with real-world conditions, and come as the industry struggles to regain credibility after it emerged in recent years that virtually every German carmaker was gaming emissions tests.

The new emission test methods in Europe are having an adverse effect on companies like (surprise) Volkswagen and Daimler AG. Both companies have stated that they are going to struggle to meet delivery targets this year because of the new rules, which are designed to produce emission results more in-line with real world conditions. VW hopes to have these emission struggles behind them by the fourth quarter. While BMW hasn’t seen trouble from these emission tests, it issued a profit warning last month regardless. The company blamed pricing pressure from competitors as a headwind.

And while there is the temptation to assume the September slide is a one-time event, Bloomberg Intelligence warned that the emissions tests and tough annual comparisons would add further pressure in 4Q, while diesel and emission compliance continues to squeeze automakers’ margins.

Meanwhile, as Bloomberg notes, other headwinds remain:

BMW cited trade tensions in last month’s profit forecast cut. The European car lobby is warning on Brexit. And don’t forget the parts makers – Goldman sees a “challenging” 3Q for European automotive industry, with potential for downward earnings revisions by suppliers. A spate of positive 3Q results starting next week could help throw sinking valuations in reverse, but trade worries are going to take longer. Sentiment remains negative and investors more inclined to push the sell than buy button for now.

In reaction to these numbers, the STOXX 600 Automobiles and Parts Index is down about 1.8% in trading in Frankfurt…

… with Europe’s automakers the worst sector today…