i

GOLD: $1228.75 DOWN $4.90 (COMEX TO COMEX CLOSINGS)

Silver: $14.69 DOWN 9 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1234.80

silver: $14.69

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 32 NOTICE(S) FOR 3200 OZ

Total number of notices filed so far for OCT: 1784 for 178,400 OZ (5.5489 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2 NOTICE(S) FILED TODAY FOR

10,000 OZ/

Total number of notices filed so far this month: 470 for 2,350,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6613: UP $65

Bitcoin: FINAL EVENING TRADE: $6550 UP 29

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY 202 CONTRACTS FROM 199,544 UP TO 199,746 WITH YESTERDAY’S 22 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

50 EFP’S FOR NOV. 2623 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2673 CONTRACTS. WITH THE TRANSFER OF 2673 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2673 EFP CONTRACTS TRANSLATES INTO 13.37 MILLION OZ ACCOMPANYING:

1.THE 22 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 2,355,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

36,876 CONTRACTS (FOR 18 TRADING DAYS TOTAL 36.876 CONTRACTS) OR 184.38 MILLION OZ: (AVERAGE PER DAY: 2046 CONTRACTS OR 10.243 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 184.38 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 26.70% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,403.7 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 202 WITH THE 22 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2673 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2875 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2673 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 202 OI COMEX CONTRACTS. AND ALL OF DEMAND HAPPENED WITH A 22 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.78 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER: 2,355,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 5,000 CONTRACTS UP TO 477,832 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $11.85).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9054 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 9054 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 477,832. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,054 CONTRACTS: 5000 OI CONTRACTS INCREASED AT THE COMEX AND 9054 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 14,054 CONTRACTS OR 1,405,400 OZ = 43.71 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $11.85.

YESTERDAY, WE HAD 5793 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 140,187 CONTRACTS OR 14,018,700 OZ OR 436.04 TONNES (18 TRADING DAYS AND THUS AVERAGING: 7788 EFP CONTRACTS PER TRADING DAY OR 778,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 436.04 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 436.04/2550 x 100% TONNES = 17.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,103.63* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 5000 WITH THE GAIN IN PRICING ($11.85) THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9054 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9054 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 14.054 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9054 CONTRACTS MOVE TO LONDON AND 5000 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 43.71 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH A GOOD GAIN OF $11.85 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 32 notice(s) filed upon for 3200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $11.85 TODAY: /

NO CHANGES IN GOLD INVENTORY TODAY

/GLD INVENTORY 747.88 TONNES

Inventory rests tonight: 747.88 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 22 CENTS TODAY

SURPRISINGLY A HUGE WITHDRAWAL OF 2.819 MILLION OZ OF SILVER FROM SLV INVENTORY

/INVENTORY RESTS AT 331.690 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 202 CONTRACTS from 199,544 UP TO 199,746 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 50 EFP’s for November… and

2623 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2673 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 388 CONTRACTS TO THE 2673 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 2875 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE STRONG GAIN ON THE TWO EXCHANGES: 14.38 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A INCREASE IN SILVER OI AT THE COMEX DESPITE THE 22 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A HUGE SIZED 2673 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 8.47 POINTS OR 0.33% //Hang Sang CLOSED DOWN 96.77 POINTS OR 0.38% //The Nikkei closed UP 80.49 OR 0.37%/ Australia’s all ordinaires CLOSED DOWN 0.31% /Chinese yuan (ONSHORE) closed DOWN at 6.9427 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 66/82 dollars per barrel for WTI and 76.60 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9427 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9482: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

ii)I still feel that Kyle Bass is one smart cookie as he tries to dissect what is going on with respect to the shady finances inside China. After suffering two years of losses due to the rise in the yuan, he has now gained 10% this year and he believes that the Chinese yuan is going to falter badly and their debt to implode

a must read..

( Kyle Bass/zero hedge)

4/EUROPEAN AFFAIRS

i)Deutsche bank again in trouble as their net income plunges by 65%. They are the largest derivative player on earth and their losses in this arena are killing them

(courtesy zerohedge)

ii)ITALY/EU

We now know the red line in the sand: it is the spread between German rates and Italian rates. In other words if the spread hits 400 basis points, then the banks need recapitalization or in other words a bail in. Watch for Italians to continue moving money into Switzerland.

( zerohedge

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Israel has no choice but to invade Gaza as rockets fired by Hamas has come very close to TelAviv

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

We continue to point out the crashing of the housing sector in the USA. Today it is new home sales as supply soars

( zerohedge)

a)Trump surely knows what is going on as he again attacks Powell on his raising interest rates. He is probably ready to throw the Fed under the bus

( zerohedge)

b)

iv)SWAMP STORIES

The following is the genesis of how the Russian collusion story was fabribated

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a LOSS of 57 contracts to stand at 3 contracts. We had 59 notices filed YESTERDAY so we gained 2 contracts or AN ADDITIONAL 10,000 oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus . Somebody was after badly needed physical silver.

After October, is the non active delivery month of November and here we gained 40 contracts up to 1300 contracts. After November, we have a December contract and here we LOST 71 contracts up to 158,215

AND NOW COMPARISON FOR OCTOBER:

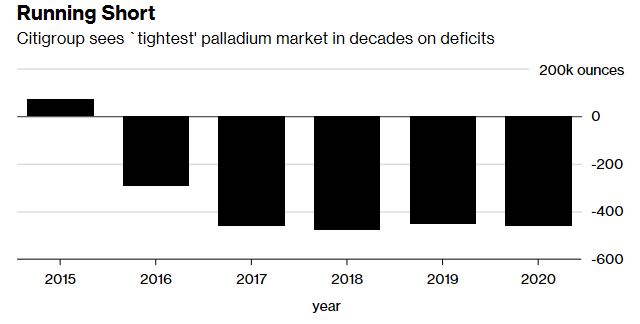

Palladium Surges To All Time Record High On Russian Supply Concerns

– Palladium prices surge to an all-time nominal high over $1,150/oz

– Russia is one of the top producers and growing tensions with the U.S. may result in a “supply crunch”

– Palladium is widely used in the automotive industry and is experiencing significant demand and a “supply crunch”

– Deep supply deficits in palladium are predicted by Citigroup and other analysts (see Bloomberg table)

– Gold and silver to follow due to similar strong supply and demand fundamentals

via Bloomberg

Palladium, a precious metal widely used in the automotive industry, has hit an all-time high.

The rally has been fueled by concern over shortages and speculators piling in to bet on even higher prices. The majority of palladium is used to make catalytic converters in gasoline automobiles, and there’s increased demand for the metal as consumers increasingly choose gasoline vehicles over diesel.

In a year that’s seen losses for most other commodities, the rally in palladium has been exceptional. It’s the one major metal that’s at an all-time high and prices have almost doubled in the past two years. On Tuesday, the metal advanced 1.8 percent to settle at $1,144.20 an ounce at 5 p.m. in New York. It earlier climbed as much as 2.5 percent to $1,152.54.

The rally has accelerated in recent days due to growing political tensions between the U.S. and Russia, one of the top producers, and stimulus measures in China, a key consumer.

“Supplies were already predicted to be in deficit this year,” and any future supply issues with Russia may exacerbate the problem, said David Govett, head of precious metals at Marex Spectron Group Ltd. “Forward rates are tightening and there is good physical offtake from the market.”

Here’s what you need to know about the rally:

Supply Crunch

The plunge in palladium holdings of exchange-traded funds is the biggest indicator that there’s a scramble for supply.

Holdings have dwindled in recent years, but it’s not a bearish signal. Rather, it’s an indication that there’s a lucrative business of lending palladium, where borrowers pay ETF holders a premium to use the metal.

Market Deficit

The market has remained in deficit as consumers turn toward gasoline cars, which tend to use more palladium in autocatalysts, instead of diesel. Shortages will probably persist though 2020, leading to the “tightest” market in two decades, according to Citigroup Inc.

Running Short

Citigroup sees `tightest’ palladium market in decades on deficits

Citigroup and Bloomberg

Citigroup and Bloomberg

Substituting Metal?

The rally raises the risk that the auto industry, the biggest user of palladium, will look to reduce consumption and instead use more platinum in catalytic converters. It’s been 17 years since palladium was last this expensive relative to platinum.

Both metals are used in varying amounts in different engine types, depending on efficiency and price. While it can take years to design autocatalysts, sizable switching has happened before. The car industry cut palladium usage by almost 50 percent in two years through 2002 after prices spiked, and increased platinum purchases by 37 percent.

Too Fast?

Prices appear to have moved ahead of fundamentals in the short term, according to Georgette Boele, an analyst at ABN Amro Bank NV. The metal’s 14-day relative-strength index is at about 77, above the level of 70 that suggests to some chart watchers that palladium may have become overbought.

News and Commentary

Gold edges higher as political, economic concerns lend support (Reuters.com)

Trump calls Khashoggi murder ‘worst cover-up in history’ (BBC.com)

Miner Fresnillo trims silver output guidance (Reuters.com)

Euro zone businesses hit the brakes as trade war stalls growth (Reuters.com)

U.S. Stock Futures Decline as Europe Bucks Selloff (Bloomberg.com)

U.K. Cabinet at War Over Theresa May’s Brexit Plan (Bloomberg.com)

China will ‘compel’ Saudi Arabia to trade oil in yuan (CNBC.com)

Source: Bloomberg

Brexit Bulletin: May Faces Open Conflict (Bloomberg.com)

Financial Extremes, The Everything Bubble and Gold (Gata.org)

Stock market faces ‘unlimited downside risk,’ warns veteran trader (Marketwatch.com)

We Have Far More Control Than They Want Us To Believe

(Sovereignman.com)

Trump says Fed Chairman Powell ‘almost looks like he’s happy raising interest rates’ (Zerohedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

23 Oct: USD 1,235.60, GBP 950.67 & EUR 1,076.45 per ounce

22 Oct: USD 1,222.90, GBP 938.09 & EUR 1,062.21 per ounce

19 Oct: USD 1,228.25, GBP 942.44 & EUR 1,073.12 per ounce

18 Oct: USD 1,224.60, GBP 933.76 & EUR 1,062.83 per ounce

17 Oct: USD 1,226.75, GBP 933.68 & EUR 1,061.38 per ounce

16 Oct: USD 1,228.85, GBP 931.35 & EUR 1,061.73 per ounce

15 Oct: USD 1,233.00, GBP 937.70 & EUR 1,064.45 per ounce

Silver Prices (LBMA)

23 Oct: USD 14.71, GBP 11.33 & EUR 12.83 per ounce

22 Oct: USD 14.63, GBP 11.23 & EUR 12.72 per ounce

19 Oct: USD 14.61, GBP 11.21 & EUR 12.75 per ounce

18 Oct: USD 14.52, GBP 11.06 & EUR 12.60 per ounce

17 Oct: USD 14.65, GBP 11.16 & EUR 12.69 per ounce

16 Oct: USD 14.76, GBP 11.16 & EUR 12.74 per ounce

15 Oct: USD 14.74, GBP 11.19 & EUR 12.71 per ounce

Recent Market Updates

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

– End Of The Financial World?

– Gold Reserves Surge 1,000% In Hungary As It Joins Poland, Russia, China and Other Central Banks Buying Gold

– How Do You Sell Your Digital Gold When the Internet Goes Down?

– IMF Issues Dire Warning – ‘Great Depression’ Ahead?

– Poland Raises Gold Holdings to Record High in September – IMF

– Why It’s Worth Holding Gold Bullion in Your Portfolio

– Gold’s Best Day In 2 Years Sees 2.5 Percent Gain As Global Stocks Sell Off – This Week’s Golden Nuggets

– Gold Up 2.5 Percent As Global Stock Rout Spreads To Europe

Looks like China will yield to U.S. sanctions on Iran

Submitted by cpowell on Tue, 2018-10-23 13:44. Section: Daily Dispatches

Exclusive: As U.S. Sanctions Loom, China’s Bank of Kunlun to Stop Receiving Iran Payments, Sources Say

By Chen Aizhu and Shu Zhang

Reuters

Tuesday, October 23, 2018

BEIJING — Bank of Kunlun Co., the key Chinese conduit for transactions with Iran, is set to halt handling payments from the Islamic Republic under pressure of imminent U.S. sanctions against the country, four sources familiar with the matter told Reuters.

Kunlun, the main official channel for money flows between China and Iran, has informed clients that it will stop accepting yuan-denominated Iranian payments to China from Nov. 1, said the sources, who include external loan agents and business officials who trade with Iran.

The bank, controlled by the financial arm of Chinese state energy group CNPC, had already quietly suspended euro-denominated payments from Iran in late August, the four sources said, declining to be named due to the sensitivity of the matter. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-iran-banking-kunlun-exclusive/e…

END

Craig Hemke at Sprott Money: Russia may not save price suppression in palladium this time

Submitted by cpowell on Wed, 2018-10-24 01:03. Section: Daily Dispatches

9p ET Tuesday, October 23, 2018

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money, today raises the possibility that Western governments and their bullion bank agents are in danger of losing control of the palladium market, since the last time palladium broke out, Russia came to the rescue with large physical supplies. Russia, Hemke writes, does not seem likely to help the West again with palladium.

Hemke’s analysis is headlined “Watching Palladium Make New All-Time Highs” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/watching-palladium-make-new-all-time-hi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Central banks to increase gold buying for first time since 2013

Submitted by cpowell on Wed, 2018-10-24 13:50. Section: Daily Dispatches

By Rupert Rowling

Bloomberg News

Wednesday, October 24, 2018

Central banks are set to increase their purchases of gold in 2018 for the first time in five years as eastern European and Asian countries seek to diversify their reserves.

Net purchases of gold by central banks are forecast to rise to 450 metric tons this year, up from 375 tons in 2017, according to consultancy Metals Focus Ltd. That will be the first increase since 2013, when banks boosted their holdings by 646 tons, the most for several decades.

With just over two months of the year left, it’s more likely that the projection will be raised than lowered because central banks generally seem interested in purchases, according to Junlu Liang, a senior analyst at London-based Metals Focus. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-10-24/central-banks-to-incr..

END

Sri Lanka calls for global coalition to tackle rising dollar

Submitted by cpowell on Wed, 2018-10-24 13:58. Section: Daily Dispatches

From Agence France-Presse

via Arab News, Riyadh, Saudi Arabia

Tuesday, October 23, 2018

COLOMBO, Sri Lanka — Sri Lanka on Tuesday called for a “coalition of the willing” to help stabilize free-falling emerging market currencies around the globe, as the beleaguered rupee slumped to fresh lows.

The island’s currency bottomed out at a record-low 174.12 rupees to the dollar, resisting a slew of measures by policymakers to arrest its steady decline.

The rupee has shed more than 12 percent of its value this year and Sri Lanka fears it could slide further as U.S. sanctions squeeze Iran, the island’s chief source of oil.

A stronger dollar has made it difficult for emerging markets to repay debts and battered global currencies from Turkey to India and Argentina.

Finance Minister Mangala Samaraweera invited those nations experiencing currency crises to visit Colombo and hash out a strategy. …

… For the remainder of the report:

END

_________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9427/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9482 /shanghai bourse CLOSED UP 8.47 POINTS OR 0.33%

. HANG SANG CLOSED DOWN 96.77 POINTS OR 0.38%

2. Nikkei closed UP 80.49 POINTS OR 0.37%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 96/77/Euro FALLS TO 1.1404

3b Japan 10 year bond yield: FALLS TO. +.14/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.54/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.82 and Brent: 76.60

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.39%/Italian 10 yr bond yield UP to 3.59% /SPAIN 10 YR BOND YIELD DOWN TO 1.62%

3j Greek 10 year bond yield FALLS TO : 4.30

3k Gold at $1230.50 silver at:14.72 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 9/100 in roubles/dollar) 65.60

3m oil into the 66 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.54DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9957 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1412 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.43%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.12% early this morning. Thirty year rate at 3.34%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7053

“Tremendous Wall Of Worry” Sends US Futures

Lower As China, Europe Rebound

One day after US equity futures plunged in early morning trading on a combination of fears about China slowing, Italy’s standoff with the EU, corporate profits, Fed tightening, escalating trade war and Saudi tensions, sentiment this morning appears somewhat more stable, even if S&P futures are near session lows and set for their 6th of losses, having faded an earlier bounce after Chinese stocks posted modest gains.

The global picture was mixed, with Asian shares extending their decline on Wednesday, as the MSCI Asia Pac index (MXAP) dropped another 0.3%, and is now down 19.6% from its January high, just shy of a bear market despite a modest rebound in the Shanghai Composite as nervous investors were unwilling to buy the dip after the latest bout of market volatility.

Meanwhile, European stocks bucked the Asian decline and brushed off weaker flash PMIs which underscored the growing impact of trade wars and tariffs, with most bourses in the green.

Confirming that Europe’s economy is slowing down, IHS Markit reported that the Eurozone’s manufacturing PMI dropped further in October, sliding from 53.2 to 52.1, sharply lower from the 58.0 reported a year ago and missing estimates of 53.0. Meanwhile, the New Orders subindex posted a contraction, sliding to 49.8 vs 51.5 in September, its lowest reading since Nov. 2014

IHS Markit PMI™@IHSMarkitPMIFlash Eurozone Composite Output Index drops to 52.7 (54.1 – Sep), lowest in just over 2 yrs. Both services and manufacturing sector growth slows notably (2-yr and 46-month low respectively). More here: http://ihsmark.it/3YUT30mlTW7

IHS Markit PMI™@IHSMarkitPMIGerman business activity growth slows to near 3-and-a-half yr low (Flash Composite Output PMI at 52.7 vs. 55.0 in Sep). Evidence that manufacturing slowdown seen YTD is starting to spill over into the services economy. More here: http://ihsmark.it/MKNl30mlUbY pic.twitter.com/BsyXQLuGGx

European basic resources and tech names underperformed, with auto names idle despite more negative China-related news for the sector after Volkswagen slashed its outlook on Chinese sales. Italy’s FTSE MIB lagged peers as the Italian banking sector sheds 1%, however with BTPs steady and the Bund/BTP spread holding around 315bp, fears over Italy remains contained.

The European tech index SX8P also declined, extending Tuesday’s sell-off and trailing a broader market rebound; chip stocks tumbled further as AMS slid for a second day with downgrades rolling in while STMicro results fail to boost sentiment. Software stocks limit losses with Dassault Systemes +0.6% after raising EPS forecast.

Retailers were the biggest winners in the Stoxx Europe 600, while Barclays climbed on earnings and Deutsche Bank fell after cutting its revenue outlook. The pound weakened on Brexit worries, and European bonds followed Treasuries higher. While stocks generally ignored the disappointing manufacturing data, the Euro dropped, dipping under 1.14 to the lowest level since mid-August.

Trader sentiment remained fragile as global shares set for the worst month in more than three years. The cautious mood was further damped by renewed worries over the impact of tariffs after industrial bellwether Caterpillar warned about rising costs due to higher steel prices. European politics is also in focus, with Italian Prime Minister Giuseppe Conte doubling down on his government’s budget and U.K. Prime Minister Theresa May’s cabinet descending into conflict.

In rates, German and U.S. curves are bull steeper, after the German 10Y breached 0.40% before the move is faded. Meanwhile, gilt yields dropped as GBPUSD breaches yesterday’s lows ahead of Prime Minister’s Questions and PM May’s appearance before the 1922 committee. US 10Y yields dropped modestly to 3.145% as the Bloomberg Dollar Spot Index stood just 0.2% short of its year-to-date high. The Canadian loonie was steady ahead of Bank of Canada’s rate decision, when it is forecast to raise rates. The Swedish krona swung between losses and gains as the Riksbank maintained expectations for a December hike.

Emerging-market assets halted their declines as currencies clawed back gains after Tuesday’s slump and stocks traded little changed. The Turkish lira, South African rand and Indian rupee led the advance, while the currencies of eastern Europe traded weaker as the dollar climbed against the euro. Lower U.S. Treasury yields and a relatively stable yuan eased concern over potential outflows from the Asian region. Investors are hurting as developing-nation stocks head for their worst year since 2011, fanned by concerns the U.S.-China trade war will hurt economic expansion. Still, there’s a possibility that weaker U.S. data in the fourth quarter could trigger a tactical rally for emerging markets as the pressure from higher U.S. rates eases, according to UBS Group AG.

“We’ve come up upon a tremendous wall of worry for U.S. stocks and stocks around the world,” said David Kudla, CEO of Mainstay Capital Management. “Concern among investors is the deceleration in earnings growth.”

In commodities, WTI resumed its sell-off touching the lowest in almost two-months on a pledge by Saudi Arabia to meet any shortfall that materializes from Iranian sanctions, with Brent dropping below its 50-DMA, flipping the Dec-Jan spread into contango for the first time since August.

Expected data include mortgage applications, PMIs, and new home sales. AT&T, Boeing, UPS, Ford, Microsoft, Tesla, and Visa are among companies reporting earnings. Texas Instruments drops in pre-market trading after slashing guidance.

Market Snapshot

- S&P 500 futures down 0.8% to 2,725.00

- STOXX Europe 600 up 0.4% to 355.48

- MXAP down 0.3% to 150.05

- MXAPJ down 0.2% to 473.38

- Nikkei up 0.4% to 22,091.18

- Topix up 0.08% to 1,652.07

- Hang Seng Index down 0.4% to 25,249.78

- Shanghai Composite up 0.3% to 2,603.30

- Sensex down 0.2% to 33,780.07

- Australia S&P/ASX 200 down 0.2% to 5,829.03

- Kospi down 0.4% to 2,097.58

- German 10Y yield fell 0.8 bps to 0.401%

- Euro down 0.5% to $1.1417

- Italian 10Y yield rose 9.9 bps to 3.217%

- Spanish 10Y yield fell 2.7 bps to 1.636%

- Brent futures down 0.9% to $75.75/bbl

- Gold spot little changed at $1,230.89

- U.S. Dollar Index up 0.3% to 96.28

Top Overnight News

- U.S. President Donald Trump stepped up his attacks on Federal Reserve Chairman Jerome Powell, saying he “maybe” regrets appointing him to the post and demurring when asked under what circumstances he would fire the central bank chief. Trump told the Wall Street Journal that he was intentionally sending a direct message to Powell that he wanted lower interest rates

- President Donald Trump said he is passing responsibility to Congress for responding to the killing of Jamal Khashoggi at a Saudi consulate in Istanbul

- Almost three weeks after the death of Jamal Khashoggi in Istanbul, Saudi Arabia and Turkey have finally laid out competing versions of the journalist’s fate. For the U.S., now comes the hard part; deciding which of the conflicting story lines to endorse, or whether to just wait for more evidence and accusations to emerge

- Crown Prince Mohammed bin Salman has “blood on his hands” in the killing of Khashoggi, a top aide to Turkey’s president said, in the country’s first direct accusation against the power behind the Saudi throne

- Italian Deputy Premier Matteo Salvini said government budget program will not change. Separately, EU economics chief Pierre Moscovici said Italy’s 2019 economic growth target of 1.5% is “optimistic” in an interview with the newspaper la Repubblica

- Italy won’t change its budget plans, according to Prime Minister Giuseppe Conte, who said he’s keeping a close eye on the 10-year spread between Italian and German bond yields

- U.K. Prime Minister Theresa May is facing another bruising showdown with her own Conservative Party over her Brexit plans Wednesday, after a cabinet meeting descended into open conflict. Seven senior pro-Brexit ministers spoke out against a proposal to allow the U.K. to stay inside the European Union’s tariff regime indefinitely, according to people familiar with the matter

- U.K. employers’ economic confidence is weakening as the nation prepares to leave the European Union. The net balance of employers with a positive outlook for the economy fell to the lowest level since February, the Recruitment and Employment Confederation said Wednesday

- Expectations for a one-on-one meeting between President Donald Trump and China’s Xi Jinping are already being lowered with officials from both sides increasingly pessimistic about prospects for a resolution to the deepening trade war

- The chairman of the House tax-writing committee said if Republicans retain the House and the Senate they’ll advance a 10 percent tax cut aimed at middle-income earners

- Oil in New York slid more than 5 percent in Tuesday’s session as Saudi Arabia pledged to meet any supply shortfalls, and as a risk-off sentiment spread throughout global markets

Asian equity markets eventually traded mostly higher on what was a turbulent session, following the dramatic rebound on Wall St where all majors finished negative albeit well off worst levels. ASX 200 (-0.2%) and Nikkei 225 (+0.4%) opened higher on early bargain hunting following their recent declines and as the aggressive recovery stateside reverberated in the region. However, both indices failed to sustain their gains as commodity-related sectors dragged on Australia with energy the underperforner after a near-5% slip in oil prices, while the Japanese benchmark was temperamental and made several attempts on the 22000 level to the downside. Elsewhere, Shanghai Comp. (+0.3%) and Hang Seng (-0.4%) conformed to the volatile tone and swung between gains and losses amid indecisiveness due to on-going trade concerns and further efforts by Chinese authorities including a respectable liquidity injection by the PBoC. Finally, 10yr JGBs were marginally higher as prices benefitted from the overnight volatility and with today’s BoJ Rinban operation heavily focused on the belly.

Top Asian News

- China Said to Halt Special Approval Process for New Games

- Even a Gain in China Can’t Get Asia’s Stock-Market Bulls Going

- Chinese Stocks Continue Wild Ways as Earlier Gains Evaporate

- State Street Says Put Money in Cash as Volatility Increases

Major European indices are mostly higher, albeit off highs seen at the cash open as positive sentiment slowly fades away and US equity futures extended losses. The SMI (+0.5%) outperforms with Nestle (+1.0%) and Swiss Re (+0.8) lifting the index. The IT sector is under further pressure after yesterday’s slump, amid uninspiring earnings from STMicroelectronics (-8.8%), which in turn is weighing on chip makers across the continent. On the flip side, luxury names are lifted the on back of Kering (+7.5%) after reporting a beat on earnings aided significantly by Gucci sales, with other names such as LVMH (+1.3%) and Hermes (+2.0%) move in sympathy. Furthermore, Vinci (+3.5%) are higher following a 7% beat on their revenue growth, while Deutsche Bank (-3.7%) are in the red after cutting revenue guidance.

Top European News

- Trade Woes Set Up Euro-Area Economy for Disappointing Year- End

- Handelsbanken Plans 1,600 Job Cuts as CEO Announces His Exit

- Heineken’s Asian Shipments Weaken as Growth Engine Stutters

- ECB Grappling Italy, Inflation to Give Traders Food for Thought

In FX, DXY – The broad Dollar and index are benefiting from the demise of most major rivals, as overall risk sentiment wobbles again after signs of a revival on Tuesday and overnight. The DXY is just off 96.341 highs, and finally breached a key level around 96.150 that has been capping rallies, with bulls now eyeing 96.402. EUR/GBP – Propping up the G10 pile, but for different reasons as the single currency breached technical support around 1.1430 vs the Usd and tripped stops below 1.1425 in wake of prelim Eurozone PMIs that fell short of expectations, and with the pan manufacturing survey particularly weak given sub-50 new orders. Meanwhile, Cable retreated further from 1.3000+ highs to trigger some chart-related offers around 1.2937 ahead of UK PM May’s 1922 showdown and ongoing Brexit uncertainty, which is keeping the Eur/Gbp cross above 0.8800. SEK – Clawing back lost ground, largely due to the aforementioned Eur weakness, having weakened to circa 10.3900 and not far from heavy supply/resistance at 10.4000 following the latest Riksbank policy meeting, as guidance was maintained for a hike either in December or February next year. This, despite recent Swedish inflation data surprising to the upside and 2 hawkish dissenters calling for a 25 bp rise in the repo. However, the consensus remains for gradual normalisation and an expansionary stance to continue for an extended period even after the 1st tightening for years is delivered. Hence, Eur/Sek back down to 10.3300, or just under, and Eur/Nok following suit (sub-9.5000). AUD/NZD – The antipodean Dollars have both slipped back from overnight peaks, as the Yuans weaken and the aforementioned Chinese-led global stock market recovery wanes. Aud/Usd is back under 0.7100 and Nzd/Usd pivoting 0.6550, with the Kiwi now looking towards NZ trade data for some independent impetus.

In commodities, gold is moving sideways, off yesterday’s highs as the yellow metal detaches itself from USD action to moves in lockstep with risk sentiment, as markets are focused on the Italian budget, trade tensions and concerns over US earnings. Copper prices fell slightly (-0.2%), which could be related to doubts from investors regarding China’s plans to invigorate their economy.

The oil market is mixed with WTI (Unch) little changed and Brent (-0.8%) in the red, as the upcoming Iranian sanctions move back into focus after Saudi Arabia reassured markets that oil supply will meet demand yesterday. Furthermore, the weekly API’s printed

a larger-than-expected build of 9.88mln barrels against an expected 3.70mln barrels, which provided further pressure to the complex. Traders will be keeping an eye on the weekly DoE crude inventory numbers released later today with focus on US oil production.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -7.1%

- 9am: FHFA House Price Index MoM, est. 0.3%, prior 0.2%

- 9:45am: Markit US Manufacturing PMI, est. 55.3, prior 55.6; Services PMI, est. 54, prior 53.5; Composite PMI, prior 53.9

- 10am: New Home Sales, est. 625,000, prior 629,000; New Home Sales MoM, est. -0.64%, prior 3.5%

- 2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

Hopefully someone reading this is $1.6bn richer after last night’s mega US lottery draw. My builder and the global equity markets both need you. To put this mind boggling sum in some context though the Bloomberg global equity index lost $637 billion in market cap yesterday. So we’ll need a few lottery winners to fill the gap at the moment.

Even with a near 2% rally from the lows of the session US equities fell last night to cap another troubled day for risk across the globe. The S&P 500 did pare losses of as much as -2.34% to close only -0.55% lower (nearly got back to flat at one stage late in the session).

The moves were similar for the DOW and NASDAQ, which retraced from down -2.17% and -2.79% respectively to close down -0.50% and -0.32%. The FANGs opened down -2.92% in New York, but ultimately closed +0.45% higher. Investors were initially spooked by some cautious commentary from earnings reports (more below), but the concerns faded through the US session. Still, the S&P 500 is on track for its worst month since August 2015, and most global equities are down for the year. North America is still the best performing region with 67% of the six countries having benchmark equities trading higher on the year in US dollar terms. In EMEA, only 23% of countries are up, and only 6% of countries in the European Union (in USD). In South American (6 countries) and Asia (18), not a single country has a positive return in USD terms this year. The recent selloff has taken a steep toll. The UK’s FTSE (-1.24%) briefly touched levels yesterday that it first breached in 1999, while across the continent, indexes hit multi-year lows. The STOXX 600 fell -1.58% to its lowest level since Dec 2016. The DAX (-2.17%) and IBEX (-0.91%) also closed at their lowest levels since 2016. European banks (-1.27%) are at their lowest levels since October 2016 just ahead of an important Q3 reporting season. Its almost as if the calm and positive 2017 never happened now for many indices. Indeed the VIX and V2X both closed above 20 again – levels the former didn’t cross in 2017 and the latter only crossed around the French elections.

Away from equities, other risk assets also traded lower yesterday, with the index of US HY CDS rising +8bps to hit fresh highs since 2016. The cash US HY market has held in much better but is finally starting to respond to the external environment widening 13bps yesterday and over 50bps from the recent tights. We’ve long seen it as the most expensive RV part of the credit spectrum. Safe havens rallied yesterday, with 10-year Treasury and Bund yields falling -3.0bps and -3.9bps respectively. Gold advanced +0.70% to a 3-month high, and the yen rallied +0.35% versus the dollar.

This morning in Asia, markets are trading mixed with the Nikkei (-0.12%) down while the Hang Seng (+1.08%), Shanghai Comp (+1.29%) and Kospi (+0.34%) are up. However, at one point the Shanghai Comp and Hang Seng were down as much as -0.65% and -0.60%, respectively before paring back the losses. In the meantime, China continues its drip feed of stimulus for the stumbling markets with the PBOC announcing yesterday that it plans to give CNY 10bn to China Bond Insurance Co. to provide credit support for debt sales by private enterprises.

Elsewhere, MSCI Asia Pacific index was down -19.97% from its January high after yesterday’s close and is flirting with bear market territory. So one to keep an eye on over the next few sessions.

In other news, US President Trump ramped up his criticism of Fed Chair Powell. In an interview with the WSJ he said that Powell “almost looks like he’s happy raising interest rates” and that it is “too early to tell, but maybe” he regrets appointing him. Trump also said that he was intentionally sending a direct message to Powell that he wanted lower interest rates, even as he acknowledged that the central bank is an independent entity.

Back to yesterday and earnings reports dominated market attention with a series of negative releases weighing on the market in early afternoon trading. Caterpillar, the machinery manufacturer seen as a global macro bellwether, reported strong earnings but expressed caution about the outlook. The company reported that manufacturing costs were higher due to increased material and freight costs, and cited tariffs as a headwind. 3M, another diversified industrial firm, revised down its earnings guidance, citing the strong dollar as a headwind. Those two firms traded -7.56% and -4.38% lower, respectively. In Europe, automaker Renault reported a drop in revenues, saying “the situation in emerging markets is hurting pretty bad” and the “underlying market in the UK is not good.” Chipmaker “ams” lowered its profit guidance, and IT services firm Atos cited a “more uncertain and challenging” global environment.” There were some bright spots from Lockheed Martin, McDonalds, United Technologies, and Verizon, but they didn’t fully outweigh the cautious tone.

With the renewed focus on tariffs and the stronger dollar from some corporate earnings reports, markets were especially sensitive to the relevant rhetoric from US policymakers. Comments yesterday from White House economic adviser Larry Kudlow did not ease concerns, as he said that Presidents Trump and Xi will meet at next month’s G-20 summit but downplayed the likelihood of a deal that would defuse tensions. Kudlow said that “I’d love to see them [China] respond” to the administration’s requests, but “thus far, they haven’t.” The yuan briefly eclipsed its weakest closing level of the year (6.947) during yesterday’s trading, before closing within 0.06% of that level. Our economists continue to expect China to ease policy to combat trade tensions, weakening the yuan to 7.40 next year.

Italian BTPs rallied as much as -7.3bps in the morning before reversing gear, and ultimately closing +10.2bps higher. Initially, sentiment improved on optimistic rhetoric from Eurogroup Chair Mario Centeno, who said that talks with Italy have been “very positive” and that he was optimistic that the European Commission would reach a compromise with the country authorities. Press reports in Il Messaggero said that the Italian government was readying a “plan B” to address the Commission’s concerns by moderating the pace of planned expenditures. Later in the session, however, Prime Minister Conte directly refuted the reports, saying there is no “plan B.” The Commission formally rejected Italy’s budget and their rhetoric was not especially constructive. Commission Vice President Dombrovskis said that “the Italian government is openly and consciously going against commitments made.” So tensions continue to escalate on this front and we expect the trend to continue.

Sterling also saw steep intraday moves, gaining as much as +0.62% versus the dollar before trading lower to close only +0.17% higher. Initially, investors were encouraged by reports that the EU will offer Prime Minister May a UK-wide customs union arrangement in an effort to resolve their outstanding issues. Our economists do not think that such an arrangement will be easy to get through parliament. If it covers the entire UK and is open-ended, the hard Brexiteer flank of the Conservative party will not be satisfied; if it is temporary and separates the UK and Northern Ireland in some way, the DUP will not be satisfied; and the EU is unlikely to support a deal that resolves these differences. Later in the evening, a cabinet meeting at Downing Street reportedly (per Bloomberg) erupted in intra-party conflict as PM May tried to navigate all these differences. Separately, The Times political editor tweeted late yesterday that the Brexit transition will last for years under PM May’s latest plan where Plan A is to involve Northern Ireland in a separate VAT area. The Times further reported that the Brexit transition period will be on a “rolling” basis with an annual “decision point” where any transition extension is reviewed.

The geopolitical dispute between Turkey and Saudi Arabia continued to escalate yesterday, with Turkish President Erdogan describing the disappearance of journalist Jamal Khashoggi as “a political murder.” He endorsed the “sincerity of King Salman” but pointedly stopped short of mentioning Crown Prince Mohammed bin Salman. The tensions did not drive market action, but will continue to receive outsized attention as Turkey continues to makes its influence count (Bloomberg).

Separately, Brent crude oil dropped -4.32% for its worst day in over three months. Saudi Energy Minister said that OPEC is in “’produce as much as you can’ mode” and that he is confident that the cartel “will meet any demand that materializes.” Increased supply could balance out disruptions in Iran and Venezuela, which have underpinned the rally in oil prices this year. Additionally, investors anticipate the Department of Energy will tomorrow announce a fifth consecutive weekly build in US crude oil inventories, the longest such stretch since the first quarter of 2017.

The data front was relatively quiet yesterday. German PPI printed at +0.5% mom and +3.2% yoy, beating expectations for +0.3% and +3.0%, though the upside was driven by higher energy costs rather than underlying pressures. In the UK, the Confederation of British Industry reported the October manufacturing new orders index at -6, missing expectations for a reading of +2 and the lowest print since 2016. Finally, in the US, the Richmond Fed manufacturing index came in at 15 versus expectations for 24, a miss but the 25th consecutive month of expansion, the longest stretch since 1995.

Data releases will be in focus today, with preliminary October PMIs across the globe. France, Germany, and the euro area will report their manufacturing services, and composite PMIs in the morning followed by the US in the afternoon. We will also get France’s October business confidence, manufacturing confidence, production outlook indicator, and business survey overall demand. The ECB will release September’s M3 money supply, and the British Bankers’ Association will publish its September finance loans for housing in the UK. In the US, we get latest weekly MBA mortgage applications, August’s FHFA house price index, September’s new home sales, and the Fed’s latest Beige Book. Away from data, the Fed’s Bostic, Bullard, and Mester will be speaking at different times. European Council President Donald Tusk and the European Commission President Jean-Claude Juncker will present conclusions from the October 18-19 summit to the EU Parliament. Besides this, Barclays, Microsoft, AT&T, Boeing, and Ford will report their earnings.

.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 8.47 POINTS OR 0.33% //Hang Sang CLOSED DOWN 96.77 POINTS OR 0.38% //The Nikkei closed UP 80.49 OR 0.37%/ Australia’s all ordinaires CLOSED DOWN 0.31% /Chinese yuan (ONSHORE) closed DOWN at 6.9427 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 66/82 dollars per barrel for WTI and 76.60 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9427 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9482: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

“Prospect Of U.S.-China War Rising” After US Warships Sail Through Taiwan Strait

Just after U.S. warships again made a provocative passage through the Taiwan Strait on Monday, further making already strained tensions between the Washington and Beijing — currently in the midst of a trade war — even hotter, Steve LeVine at Axios poses the question long on the Western public’s mind: what are the chances of a US-China war?

LeVine recently crossed paths with Graham Allison, who published his explosive “Destined For War: Can America And China Escape Thucydides Trap?” a year ago which detailed the reasons for a coming major war being all but inevitable, sparking a global debate about the Harvard professor’s controversial thesis. LeVine followed up with Allison in relation to the recent uptick in tensions in the region of the South China Sea:

He said, if history holds, the U.S. and China appeared headed toward war.

Over the weekend, I asked him for an update — specifically whether the danger of the two going to war seems to have risen.

“Yes,” he responded. The chance of war is still less than 50%, but “is real — and much more likely than is generally recognized.”

LeVine comments of Graham Allison’s central thesis, “Glued to a 2,400-year-old script, the U.S. and China seem to be on the same war-bound path that great powers have taken since Sparta fought upstart Athens.”

LA Times: On Monday the ships sailed from the south to the north through the Taiwan Strait and were shadowed by multiple Chinese navy vessels. (U.S. Navy)The reference is to the History of the Peloponnesian War, in which ancient Greek historian Thucydides told us the tale of a dominant regional power (Sparta) that felt threatened by the rise of a competing power (Athens). Sparta felt so threatened, in fact, that all the moves they made to keep the Athenian rise in check eventually escalated the power struggle into an all out war.

LA Times: On Monday the ships sailed from the south to the north through the Taiwan Strait and were shadowed by multiple Chinese navy vessels. (U.S. Navy)The reference is to the History of the Peloponnesian War, in which ancient Greek historian Thucydides told us the tale of a dominant regional power (Sparta) that felt threatened by the rise of a competing power (Athens). Sparta felt so threatened, in fact, that all the moves they made to keep the Athenian rise in check eventually escalated the power struggle into an all out war.

The idea is that when, out of fear, a dominant power takes certain steps to keep its competitor at bay, these actions ultimately lead to war between the two, or what modern political scientists call the Thucydides Trap.

“If Thucydides were watching, he’d likely say all parties almost seem to be competing to show who can best exemplify the role as rising power, ruling power, and provocateur.”

— Graham Allison

LeVine summarizes, based on Allison’s latest comments, that now more than ever the two great powers are inching toward that trap in their brinkmanship based on an “inexorable, invisible force prodding them to almost inevitable war”. Per the Axios report:

The U.S. has slapped increasing tariffs on Beijing, cordoned off U.S. tech, and jailed a Chinese spy, while Beijing has continued to build its military footprint in the disputed South China Sea, demanded tech secrets from Western companies, and more.

But would the current trade war alone or even wide scale tech theft and a few encounters on the open seas be enough to trigger escalation and actual war?

Likely not, says Allison, but instead a WWI type scenario of an unintended domino effect of one-upmanship in which, for example, the simple assassination of Archduke Franz Ferdinand triggered massive escalation leading to world war. By a similar scenario, writes LeVine of Allison’s comments, “the two countries will be pulled into conflict by miscalculation involving a third party, such as Taiwan.”

Says Professor Graham Allison:

“What happens is that a third-party provocation, an accident, becomes a trigger to which one of the two feels obliged to respond. and they find themselves in a war that neither wanted.”

We saw precisely this almost happen between the US and Russia over Syria on multiple occasions over the past two years — especially with the September accidental downing of the Russian IL-20 surveillance plane with 15 crew members on board after US ally Israel launched a wide scale missile assault on Syrian government facilities.

Currently, what the Pentagon called a “routine” operation as two US Navy vessels sailed through the Taiwan Strait has sparked fury with Beijing, with the Chinese Foreign Ministry on Tuesday saying it’s expressed “deep concern” to the United States over the action, which was the second such operation this year.

Foreign ministry spokeswoman Hua Chunying said in reaction to the incident at a press briefing on Tuesday, “The Taiwan issue concerns China’s sovereignty and territory, and is the most important, most sensitive issue in China-U.S. relations.”

The Pentagon, for its part, repeated its position of a “U.S. commitment to a free and open Indo-Pacific,” per Commander Nate Christensen, deputy spokesman for U.S. Pacific Fleet, via Reuters. “The U.S. Navy will continue to fly, sail and operate anywhere international law allows,” he added.

Meanwhile, a crucial piece in the South Morning China Post entitled, Taiwan’s cosying up to Trump could spark a China-US war, takes us down memory lane, and outlines precisely – based on recent history – how easily the world could be on the brink of an all-out US-China war per Graham Allison’s thesis:

This is not the first time Taiwan has become a central issue in US-China relations. In the 1960 US presidential debate, John Kennedy and Richard Nixon traded barbs over whether America should launch a nuclear war against China to protect the tiny islands of Matsu and Quemoy, or Kinmen, in the event of a communist invasion.

Trump might now see Taiwan as an increasingly valuable point of leverage over China, but Beijing will make no compromise on this politically most sensitive issue as it considers Taiwan a “core interest”.

As the US and China drift dangerously towards direct conflict, Taiwan should be cautious. The narrow Taiwan Strait could be the flashpoint that sparks war between the world’s most powerful nations.

Indeed the “Thucydides trap” might be right there in this seemingly remote strait that could very well be the flashpoint that takes us past the brink.

end

I still feel that Kyle Bass is one smart cookie as he tries to dissect what is going on with respect to the shady finances inside China. After suffering two years of losses due to the rise in the yuan, he has now gained 10% this year and he believes that the Chinese yuan is going to falter badly and their debt to implode

a must read..

(courtesy Kyle Bass/zero hedge)

Kyle Bass: Trump Has “Strongest Negotiating Position We’ve Ever Had” Against China

After spending two years in the dog house, Hayman Capital Management and its founder, Kyle Bass, are finally seeing some positive returns on the fund’s signature short-Chinese-yuan play, which has returned more than 10% since the beginning of 2018 after the fund recorded a 20% loss last year. Since he first went public with the short in 2016, Bass has stood by his view that a looming capital outflow crisis would eventually cause the Chinese yuan to shed 30% of its value vs. the dollar. And luckily for him, Trump showed up and decided to expedite this process by waging his economically disruptive trade war.

So during an interview with CNBC, Bass said that China is facing its “worst financial situation” since the financial crisis after that 6.5% yoy GDP print, which has only given Trump more leverage to press his trade advantage. In making his case, Bass pointed to first-quarter data that showed for the first time in 17 years China ran a current account deficit, meaning it imported more goods and services than it exported, even as it continued to run a massive trade surplus with the US, even as it ran a massive trade surplus with the US. While this is consistent with China’s goal of transitioning into a service-reliant economy, the shortage of foreign capital will create serious economic headwinds in the short term.

“And so, the US is in a very particularly interesting negotiating position today. We are in the strongest negotiating position we’ve ever had against China. They’ve kind of leveled the playing field a little bit more with their, let’s say, subversion of WTO rules, their intellectual property theft and basically everything they’ve done to take advantage of the US over the past 15, 17 years.”

The Trump administration needs to level the playing field on trade, Bass said, and “it looks like they are doing so.” And it certainly helps that Trump’s trade push, while initially reviled by globalists in both parties, has since won the reluctant support of both Democrats and Republicans as the US economy has largely escaped any serious repercussions so far. But ultimately, the arbiter of government money and influence over the domestic economy is the yuan-dollar exchange rate. And as the yuan sinks, foreign ownership of Chinese assets is falling as the PBOC runs “a structural and more permanent” current-account deficit with the rest of the world as the US continues to institute trade barriers.

“So they can change a lot of things domestically, but their – the arbiter of the Chinese plan is their cross rate or their exchange rate with the rest of the world. China Inc.’s working capital account is now going South because they’re running what we believe to be a structural and more permanent deficit on the current account. And so, ie, their working capital, their dollar balance whether it’s dollars, euros, yen or pounds, it’s mostly dollars.”

All of this instability risks toppling the mountain of bad debt upon which China’s economic growth in recent years has depended. Already, corporate defaults have surged in 2018 to the highest level on record.

With all of these factors at play, China is running what Bass described as “the largest financial experiment the world has ever seen.”

“And they’ve got, you know, $40 trillion worth of credit, somewhere between 40 and 50, no one knows, in a system with only a couple trillion dollars’ worth of equity.And so China is running the largest financial experiment the world has ever seen. And the economic tides have turned negative for them. If you notice the narrative amongst the United States, it’s actually a bipartisan narrative whereby you’re seeing both sides of the aisle pushing back on China taking advantage of the US.”

And with the yuan poised to break below the key technical level of 7 to the dollar, Bass and Hayman might finally be able to make up for the losses on their yuan short, as a break below 7 would likely invite a speculative attack.

Watch the full video below:

Watch CNBC’s full interview with Hayman Capital’s Kyle Bass from CNBC.

4.EUROPEAN AFFAIRS

Deutsche bank again in trouble as their net income plunges by 65%. They are the largest derivative player on earth and their losses in this arena are killing them

(courtesy zerohedge)

Deutsche Bank Shares Tumble After Net Income

Plunges 65% On Lowest Revenue In 8 Years

There was some good, but mostly bad news in Deutsche Bank’s Q3 earnings report.

The good news is that after years of turmoil, the biggest German bank is showing signs of stabilization under new CEO Christian Sewing after a bitter boardroom battle. The bad news is that the bank missed across all key revenue metrics as Sewing scrambles with a looming problem: how to boost revenue after firing thousands of banks in a multi-year long cost-cutting campaign.

The German bank reported net income of €229 million on Wednesday, above the €160 million expected but 65% below the €649 million reported a year ago. Profit before tax also tumbled by nearly half, dropping from €933 million to €506 million.

Investors were closely watching the bank’s costs: the new management team, which was appointed last April, promised to deliver further cost-cutting to revamp the balance sheet. In the third quarter of 2018, the bank said that adjusted costs dropped 1% from a year ago to 5.5 billion euros, with the aim for the full year to bring adjusted costs down to €23 billion and €22 billion in 2019. A core part of the new “restructuring” effort have been mass layoffs as the number of workers is set to come down to 93,000 by the end of 2018, and 90,000 one year later.

But while costs and the bottom line beat were a modest positive surprise, the same could not be said for the bank’s revenue which disappointed across the board: total revenue of €6.17BN missed expectations of €6.34BN and guided lower, now predicting a slight decline for full year revenue after earlier guiding for a flat result; trading income in the key FICC division tumbled 15% from a year earlier, while equities trading, a sector where Wall Street banks generally posted gains, also dropped at the same pace as these two key businesses have been hardest-hit by executives departures recently.

More Q3 revenue details:

- FICC revenue: €1.32BN vs €1.545BN in Q3 2017, and missing expectations of €1.365BN

- Equities trading revenue: €466BN vs €548BN in Q3 2017, and missing expectations of Exp. €473BN

- Total sales and trading revenue: €1.79BN, missing expectations of €1.84BN

- Total revenue: €6.17BN, missing expectations of €6.34BN

In total, Deutsche reported its lowest third-quarter revenue since 2010 and now expects a slight decline for the full year, after earlier guiding for a flat result according to Bloomberg.

The silver lining is that while revenue was a disappointment, costs also shrank which should allow the bank to post its first annual profit in four years according to Sewing who added that the focus now has to be on growing the top line without compromising controls: “With profit before tax of 506 million euros, this result is another milestone on our way to becoming a sustainably profitable bank. We have our costs under control and sufficient capital to grow. We are on track to be profitable in 2018, for the first time since 2014.”

Of course, being profitable by butting into the muscle is hardly what shareholders expected, and the CEO admitted as much writing in a memo to employees that while “we made headway on our cost reductions,” he admitted that “we have not yet achieved a turnaround in terms of revenues.”

As Bloomberg notes, for investors who have been through the bank’s previous turnaround plans, “it’s a familiar pattern.” John Cryan, Sewing’s predecessor, had vowed to restore “controlled growth” last year after raising fresh funding, but failed to deliver. Sure enough, the stock was promptly punished for this latest disappointment, with Deutsche Bank shares falling 3.5%, having lost 44% of its value this year and trades near its record low.

Sellside reactions were mixed, with JPM analyst Kian Abouhossein writing that Deutsche Bank “has done an excellent job under Sewing” on cost reductions and improving the bank’s capital strength, however “we remain concerned about DB’s inability to turn around” the investment bank division.”

On the other hand, Goldman analyst Jernej Omahen was more critical, writing that the third quarter results were “weak” from an operational perspective, noting underperformance relative to U.S. peers in investment bank revenue progression, as well as the underlying pretax profit miss. The silver lining: capital was better-then-expected, as was bottom line, due to lower burden of non-operating items.

But the one recurring theme was the lack of top-line growth: “Costs are in line with targets,” said Daniel Regli, an analyst with MainFirst who has a hold recommendation on the stock. “But there is continued weakness in investment bank revenue. That needs to be fixed.”

* * *

Sewing had staked his restructuring effort, and Deutsche’s fourth in three years, on boosting profitability by trimming costs and refocusing on fewer, core activities. Yet the continued contraction in the top line risks undermining investor confidence in the strategy and may fuel speculation that the lender needs to combine with a rival in the long run, BBG adds.

The new CEO has vowed the investment banks will remain a core business for Deutsche Bank, with at least half of the revenue coming from the unit. And yet, he’s cutting at least 7,000 jobs and retrenching in areas such as prime finance, U.S. rates and corporate finance in the U.S. and Asia. The bank cut another 700 positions in the third quarter after eliminating about 1,700 jobs in the three months through June; it said it remains on track to hit its job target of well below 90,000 by end of 2019.

The bank’s steady exodus of employees has left the business stuck in what CFO James von Moltke called a “vicious circle” of declining revenue, “sticky” expenses, a lowered credit rating and rising funding costs. Additionally, the bank on Wednesday highlighted higher funding costs and geopolitical events among the headwinds for the securities unit.

Meanwhile, as the one-time financial titan continues to shrink, all management can do is try to boost morale: Garth Ritchie, head of the bank’s securities unit urged employees in a memo to “focus resolutely on rebuilding revenue momentum” in the final quarter; surely a preferable alternative to being fired. Von Moltke said on a conference call that the bank wants to redeploy excess cash to return to growth, as restructuring expenses are likely to be lower than previously expected. He said rating companies would be comfortable with such use of capital.

“We need to end the year on a strong note,” Sewing wrote in his memo. “We’ll stay disciplined on costs, and we’ll turn around revenues.”

Indeed…

END

We now know the red line in the sand: it is the spread between German rates and Italian rates. In other words if the spread hits 400 basis points, then the banks need recapitalization or in other words a bail in. Watch for Italians to continue moving money into Switzerland.

(courtesy zerohedge

“400 bps”: Italy Inadvertently Sets The Red Line

For Coming Bank Runs

In what may prove to be a painful admission in retrospect and an inadvertent green light for future bank runs, on Wednesday morning Italy’s Cabinet Undersecretary Giancarlo Giorgetti said in an interview on Italy’s RAI that Italian banks would need a “recapitalization” if the spread with German bonds continues to rise toward 400 basis points, from the current level of 314bps which is just shy of the widest level it has been going back to early 2013.

The last time “lo spread” hit 400 bps was in late 2012, around the time of Mario Draghi’s legendary “whatever it takes” speech.

According to the Italian official, who is Deputy Prime Minister Matteo Salvini’s closest aide, bank assets would “automatically” suffer if the spread neared the 400-level and so as a consequence recapitalization would be needed. And since a recap for Italy’s capital starved banks would likely entail balance sheet restructurings, accompanied by bail-ins of creditors and/or depositors, the closer “lo spread” got to the critical red line, the more likely Italian bank runs will become.

Said otherwise, the Italian population will now be even more focused on the spread of Italian bonds, and the higher it grows, the less comfort Italians will have with keeping their savings in local banks, and the more likely bank jogs (and then runs) will become.

Having thus set the bogey, Giorgetti then tried to assure the population that such a move would not be needed, as the government would be ready to intervene “immediately” if needed and “won’t wait months as Matteo Renzi’s government did with Monte dei Paschi” although as Berlusconi so fondly remembers, any attempts at intervention will ultimately end up futile if not backstopped by the ECB and/or Brussels.