I AM GLAD TO BE BACK

GOLD: $1229.90 UP $1.15 (COMEX TO COMEX CLOSINGS)

Silver: $14.62 DOWN 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1232.00

silver: $14.64

I love this one from James McShirley:

Three scenarios for silver:

*If the silver price control is part of a mutually agreed contractual obligation the buyers of physical are getting the deal of a lifetime.

*If the silver price control isn’t mutually agreed upon the buyers of physical are still getting the deal of a lifetime, however under hostile circumstances.

*If the silver price control is because of the cartel’s total terror of silver getting away from them, and hence gold too then somebody is still getting the deal of a lifetime.

The only question is, WHOSE lifetime? At what point does a massive buyer of silver make their move, and clean up the BILLIONS currently there for the taking? In a short squeeze there’s no earthly reason why silver couldn’t be priced closer to platinum, or even palladium. Daily moves of $10 or more would be more probable that these 1 cent daily comas.

All manipulations eventually end badly, for the manipulators. Either way all comas eventually end as well. Once the silver patient is removed from this induced coma it will make up for lost time in spade

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 30 NOTICE(S) FOR 3000 OZ

Total number of notices filed so far for OCT: 1814 for 181,400 OZ (5.6432 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

32 NOTICE(S) FILED TODAY FOR

160,000 OZ/

Total number of notices filed so far this month: 502 for 2,510,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6550: DOWN $15

Bitcoin: FINAL EVENING TRADE: $6545 DOWN 19

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY 997 CONTRACTS FROM 199,746 UP TO 200,743 DESPITE YESTERDAY’S 9 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 474 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 474 CONTRACTS. WITH THE TRANSFER OF 474 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2673 EFP CONTRACTS TRANSLATES INTO 2.37 MILLION OZ ACCOMPANYING:

1.THE 9 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 2,510,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

37,350 CONTRACTS (FOR 19 TRADING DAYS TOTAL 37.350 CONTRACTS) OR 186.75 MILLION OZ: (AVERAGE PER DAY: 1965 CONTRACTS OR 9.828 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 186.75 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 26.67% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,406.1 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 997 DESPITE THE 9 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMAL SIZED EFP ISSUANCE OF 474 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1471 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 474 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 997 OI COMEX CONTRACTS. AND ALL OF DEMAND HAPPENED WITH A 9 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.69 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.004 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 32 NOTICE(S) FOR 160,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER: 2,510,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2214 CONTRACTS DOWN TO 475.618 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $4.90).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5836 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 5836 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 475,618. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3622 CONTRACTS: 2214 OI CONTRACTS DECREASED AT THE COMEX AND 5836 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 3622 CONTRACTS OR 362,200 OZ = 11.26 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.90.

YESTERDAY, WE HAD 9054 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 146,023 CONTRACTS OR 14,602,300 OZ OR 454.19 TONNES (19 TRADING DAYS AND THUS AVERAGING: 7685 EFP CONTRACTS PER TRADING DAY OR 778,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 454.19 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 454.19/2550 x 100% TONNES = 17.81% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,121.78* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 2214 WITH THE LOSS IN PRICING ($4.90) THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5836 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5836 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 3622 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5836 CONTRACTS MOVE TO LONDON AND 2214 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 11.26 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH A LOSS OF $4.90 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 30 notice(s) filed upon for 3000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.15 TODAY: /

A BIG CHANGES IN GOLD INVENTORY TODAY

A DEPOSIT OF 1.76 TONNES OF GOLD INTO THE GLD INVENTORY.

/GLD INVENTORY 749.64 TONNES

Inventory rests tonight: 749.64 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 7 CENTS TODAY

SURPRISINGLY A HUGE WITHDRAWAL OF 1.316 MILLION OZ OF SILVER FROM SLV INVENTORY

/INVENTORY RESTS AT 330.375 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 997 CONTRACTS from 199,746 UP TO 200,743 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

474 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 474 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 997 CONTRACTS TO THE 474 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 1471 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE STRONG GAIN ON THE TWO EXCHANGES: 4.375 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A SMALL SIZED 474 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 0.51 POINTS OR 0.02% //Hang Sang CLOSED DOWN 255.32 POINTS OR 1.01% //The Nikkei closed DOWN 822.45.49 OR 3.72%/ Australia’s all ordinaires CLOSED DOWN 2.82% /Chinese yuan (ONSHORE) closed DOWN at 6.9440 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 67.10 dollars per barrel for WTI and 76.56 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9440 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9489: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

Albert Edwards is joining Kyle Bass in explaining that China will undergo a hard landing. He cites as does Bass, the fact that China has its first and probable permanent current account deficit and they may not have the appetite to continue to inflate their way out of their mess

( zerohedge)

4/EUROPEAN AFFAIRS

i)Some wanted the language stronger but Draghi did not oblige. He stated that the ECB will end QE in December 2018 and keep long term interest rates at present levels until the summer of 2019. Nothing changed from previous statements

( zerohedge)

ii)The street wanted Draghi more dovish on his statement and that caused the Euro to rise, the 10 yr bund yields to rise..

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

ii)The Saudi’s now change their story again: the Khashoggi killing was a premeditated act…and 15 Saudi members that entered the embassy have been charged..he just do not know who ordered the hit..

(courtesy zerohedge)

iii)IRAN

This is a major surprise and a big concession..Trump will allow Iran to remain connected to SWIFT

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

Ted Butler…

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)So much for the tariffs helping the USA: they recorded another record high good trade deficit of 76 billion dollars.

( zerohedge)

b)Core durable goods stagnate but the war machine saves the day

( zerohedge)

c)Housing continues to disappoint: this time it is pending home sales that slumps for the 5th straight month

(courtesy zerohedge)

iv)SWAMP STORIES

a)What took them so long: Both Avenatti and Swetnick have been referred to the DOJ for criminal investigation over false statements on Kavanaugh

( zerohedge)

b)It now looks like we have two challenges to Mueller with respect to a witness, Miller, (Roger Stone case) and a grand jury witness who is challenging the issuing of that subpoena to undergo his/her duty.

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a GAIN of 30 contracts to stand at 33 contracts. We had 2 notices filed YESTERDAY so we gained 32 contracts or AN ADDITIONAL 160,000 oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus . Somebody was after badly needed physical silver.

After October, is the non active delivery month of November and here we lost 4 contracts DOWN to 1296 contracts. After November, we have a December contract and here we GAINED 722 contracts up to 158,937

AND NOW COMPARISON FOR OCTOBER:

i) into the dealer Brinks: 602,084.450 oz

Dublin Housing Boom Set To Bust?

– Is Dublin’s property market heading for a soft landing?

– Increasing fears the latest housing boom could foreshadow another slump as reported in the Financial Times

– 68 per cent of prime properties in Dublin 4 and 6 have cut prices

– “I doubt it will be ‘soft’ … My suspicion is that it’ll hurt like hell…” warned Karl Deeter of Irish Mortgage Brokers

Over the past five years Ireland has been on something of a tear.

The economy is the fastest growing in Europe, unemployment has fallen below the EU average and house prices rose 11.9 per cent last year, on top of 8.6 per cent growth in 2016, according to rating agency Standard & Poor’s.

In some corners, the devastation wrought by the 2008 financial crash — when house prices dropped 55 per cent — feels a distant memory. But there are fears the latest housing boom could foreshadow another slump — especially among Dublin’s wealthy enclaves.

Since the property market started to recover in May 2013, Ireland’s residential house prices have ballooned by 69.9 per cent, according to the country’s Central Statistics Office. S&P foresees the runaway growth slowing, but its forecast still has Irish house prices rising 9.5 per cent this year, 8 per cent next year and 7 per cent in 2020.

If the agency’s predictions are borne out, house prices will have increased 127.9 per cent between 2013 and 2021.

“There could be a situation where [developers] start to bail into the sector and you eventually reach hyper-supply, and when that becomes apparent you get a reversal in the market,” says Karl Deeter, compliance manager at Irish Mortgage Brokers.

“I doubt it will be ‘soft’, ” he says. “My suspicion is that it’ll hurt like hell.”

In Dublin, there are already signs the prime market is faltering.

In the upmarket areas of Dublin 4 and Dublin 6, high-priced homes are struggling to sell. A report by property portal MyHome.ie shows that 68 per cent of prime properties in Dublin 4 — the most expensive area in the country with an average price of €775,973 — and Dublin 6 have cut their prices.

“For quite a few properties that are on the market for more than €1m, the asking prices are being pushed down,” says Stephen Day, residential director at Lisney estate agents.Day has recently reduced a five-bedroom property in Ranelagh from €2.25m to €1.995m.

“To be blunt,” he says, “agents are putting houses on for too high a price, and so they have been sitting on the market.”

Full article from FT here

Editors Note: The Dublin housing market looks vulnerable to a severe correction and, in the event of a global financial crisis, another crash.

The question that needs to be asked is how far prices will fall and will this be a relatively mild correction, a sharp correction or indeed another property crash?

We have long contended that London house prices would fall sharply and there are increasing signs that this is happening in not just in London (see News today below) but in Sydney, Melbourne, Vancouver and other cities which have seen massive appreciation in their house prices in the last two decades.

A crash in property prices in these major cities will have obvious ramifications for other property markets.

Psychology is a powerful thing and falling prices in leading financial capitals around the world will likely curb property investors enthusiasm for other over valued and frothy property markets including Toronto, Perth, San Francisco, Los Angeles, Amsterdam, Frankfurt, Paris, Dublin and others.

Property investors should consider diversifying into safe haven gold which will again hedge and protect investors in a sharp correction or a crash.

Related Content

News and Commentary

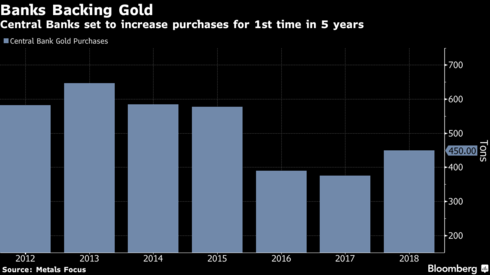

Central Banks to Increase Gold Buying for First Time Since 2013 (Bloomberg.com)

Gold hovers near 3-month peak as equities plunge (Reuters.com)

US official: Maduro ‘looting’ Venezuela’s gold amid crisis (KSL.com)

Dow erases gains for year, tumbles over 600 points and extends October swoon (CNBC.com)

Property asking prices slashed by £26,000 as UK housing market slows down (Independent.co.uk)

U.S. New-Home Sales Tumble to Lowest in Almost Two Years (Bloomberg.com)

Source: Bloomberg

Gold Is Becoming Cool Again (Gold-Eagle.com)

Sri Lanka calls for global coalition to tackle rising dollar (ArabNews.com)

Why the Information Revolution Failed (BonnerAndPartners.com)

Watching Palladium Make New All-Time Highs (ZeroHedge.com)

Gold prices on the move; pushing prices towards 1235.60 (FXStreet.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

24 Oct: USD 1,231.65, GBP 952.80 & EUR 1,078.68 per ounce

23 Oct: USD 1,235.60, GBP 950.67 & EUR 1,076.45 per ounce

22 Oct: USD 1,222.90, GBP 938.09 & EUR 1,062.21 per ounce

19 Oct: USD 1,228.25, GBP 942.44 & EUR 1,073.12 per ounce

18 Oct: USD 1,224.60, GBP 933.76 & EUR 1,062.83 per ounce

17 Oct: USD 1,226.75, GBP 933.68 & EUR 1,061.38 per ounce

Silver Prices (LBMA)

24 Oct: USD 14.75, GBP 11.42 & EUR 12.92 per ounce

23 Oct: USD 14.71, GBP 11.33 & EUR 12.83 per ounce

22 Oct: USD 14.63, GBP 11.23 & EUR 12.72 per ounce

19 Oct: USD 14.61, GBP 11.21 & EUR 12.75 per ounce

18 Oct: USD 14.52, GBP 11.06 & EUR 12.60 per ounce

17 Oct: USD 14.65, GBP 11.16 & EUR 12.69 per ounce

Recent Market Updates

– Palladium Surges To All Time Record High On Russian Supply Concerns

– Happy Birthday GoldCore

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

– End Of The Financial World?

– Gold Reserves Surge 1,000% In Hungary As It Joins Poland, Russia, China and Other Central Banks Buying Gold

– How Do You Sell Your Digital Gold When the Internet Goes Down?

– IMF Issues Dire Warning – ‘Great Depression’ Ahead?

– Poland Raises Gold Holdings to Record High in September – IMF

– Why It’s Worth Holding Gold Bullion in Your Portfolio

* * *

END

Mysterious Metal Movement

Theodore Butler | October 25, 2018 – 9:17am

The hit movie from 1996, “A Time to Kill”, based upon the novel by John Grisham, had an all-star cast, including Matthew McConaughey, Samuel Jackson, Sandra Bullock, Kevin Spacey and Donald and Kiefer Sutherland among others. It concerned the rape and beating of a young black girl in the racially-divided rural Deep South, the subsequent killing by her father of the two white rapists and the trial that followed the father’s killing of the rapists.

The film’s highlight was the moment during the trial when the father’s lawyer asked the jury to close their eyes and imagine the suffering of the young girl while he described the depravity in lurid detail. Just when the images reached what had to be a climax, the lawyer suddenly shocked everyone by then asking them how they would have felt had the little girl been white and not black. That was the turning point in the trial that ended with the father being found not guilty.

I invoke that scene today to revisit an issue I have written endlessly about since first uncovering it more than seven and a half years ago in April 2011. That was when an unprecedented physical silver movement commenced in the COMEX-approved warehouses which has continued to this day and very recently has accelerated to absolutely astounding levels – an average weekly physical movement of more than 9 million ounces over the past five weeks, or more than 475 million ounces on an annualized basis. That’s fully 60% of total world annual production, basically being physically moved in and out of 6 warehouses in and around the New York City area. To be sure, this is purely physical silver movement and is not to be confused with paper trading.

Over the past seven and a half years, more than 200 million ounces of physical silver has been moved annually in and out of the COMEX warehouse system, as reported in daily COMEX warehouse releases. In total, more than 1.5 billion silver ounces have been so moved over this time, roughly corresponding to the world’s entire total inventory of silver in the form of 1000 oz bars. I’ve recounted this highly unusual physical movement weekly since it began in April 2011, all the while noting that was when silver ran to $50 and then collapsed and how that was when JPMorgan first opened its COMEX silver warehouse and began to accumulate physical silver – all while remaining the leading short seller in COMEX silver futures. Starting from zero back then, today JPMorgan holds more than 147 million ounces of silver in its own COMEX warehouse, more than 50% of the total 291 million oz of silver ounces held in the world’s second largest visible depository of silver (the big silver ETF, SLV, holds the most visible silver in the world, some 330 million ounces and not coincidentally, JPMorgan is the custodian for that metal). As I have contended for ten years, JPMorgan is the kingpin of the silver (and gold) market in every way possible.

So what the heck does the frantic and unprecedented physical metal movement in and out of the COMEX silver warehouses have to do with a hit movie from twenty years ago? Just this – close your eyes and imagine for a moment that what has been occurring in the COMEX silver warehouses had been happening in gold instead. I’ve heard more cockamamie stories about gold to last a couple of lifetimes; stories about eligible vs. registered COMEX holdings and the ratio to paper open interest, wacky EFP theories about delivery obligations being transferred to London and about pending COMEX delivery defaults prior to every first delivery day for years.

I’m firmly convinced that people’s heads would explode if what had been happening in silver had been instead occurring in gold. If the same type of physical movement had been occurring in the COMEX gold warehouses as has occurred in silver over the past nearly eight years, it would dominate the conversation – little else would be discussed. And even more would be made of the issue if the frantic movement were occurring solely in gold and not in any other commodity, as has been the case with silver. Please remember, the COMEX silver physical movement is available on a daily basis (for free) and I know it is being viewed by many – since total COMEX inventories are referenced regularly.

So why is the frantic COMEX silver warehouse physical turnover not a subject of widespread attention (where it would be impossible to avoid were it gold)? I think it has to do with it being very difficult to explain exactly why it is occurring. There is no question it is occurring (as the thought that it is some type of intentional misreporting is too absurd to contemplate), but there are no easy answers as to why the unprecedented physical silver movement is occurring. Unfortunately, the documented frantic physical silver turnover doesn’t come with an explanation manual. We can easily see it is occurring, just not why. That’s a combination that demands analytical attention.

Aside from it being absurd to conclude that the silver movement is not occurring and being deliberately misreported, it’s also absurd to think it is some type of “make work” project, solely intended to employ truck drivers and warehousemen. For sure, there is a reason for the physical movement, as well as a reason for why it exists only in silver. While I am open to any and every alternative explanation, I can’t help but think that the movement is the result of extraordinary physical demand.

COMEX silver is being moved because it is demanded. Further, given the timing for when the movement started (April 2011) and the myriad clues around that date for silver and JPMorgan, I am convinced that the demand prompting the unprecedented turnover is due to demand from JPMorgan. Specifically, I believe JPMorgan, in addition to the 147 million oz it has accumulated in its own COMEX warehouse, has skimmed off hundreds of millions of ounces more, held either in or out of this country.

Unfortunately, I seem to be operating in an echo chamber, as I am aware of hardly any other commentator willing to acknowledge the easily documented COMEX silver turnover, no less attempt to explain it. When it comes to silver and particularly gold, there is never a shortage of explanations for just about everything under the sun. But in the matter of the unprecedented physical metal movement in the COMEX silver warehouses, there’s not even the chirping of crickets. Go figure. Please feel free to inquire of any commentator you have access to and pass along any responses to me.

And this is just but another example of unanswered mysteries surrounding silver. Others include the fact that JPMorgan has never taken a loss when adding new COMEX short positions in silver (or gold) over the past ten years, only profits. And that JPMorgan has remained the largest paper COMEX short while at the same time accumulating massive amounts of physical silver and gold. The real mystery, of course, is why the CFTC or JPMorgan won’t even address these concerns. One thing that’s not a mystery is that JPMorgan is positioning itself for a monster move up in price and so should you.

Ted Butler

October 25, 2018

www.butlerresearch.com

_________________________________________________________________________________________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9440/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9489 /shanghai bourse CLOSED UP 0.51 POINTS OR 0.02%

. HANG SANG CLOSED DOWN 255.32 POINTS OR 1.01%

2. Nikkei closed DOWN 822.45 POINTS OR 3.72%

3. Europe stocks OPENED MIXED

/USA dollar index RISES TO 96.33/Euro RISES TO 1.1409

3b Japan 10 year bond yield: FALLS TO. +.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.38/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.10 and Brent: 76.56

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.40%/Italian 10 yr bond yield UP to 3.50% /SPAIN 10 YR BOND YIELD DOWN TO 1.57%

3j Greek 10 year bond yield FALLS TO : 4.23

3k Gold at $1232.80 silver at:14.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 3/100 in roubles/dollar) 65.66

3m oil into the 67 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.38DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9957 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1407 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.40%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.13% early this morning. Thirty year rate at 3.36%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6475

US Futures Surge, Europe Rebounds As Market

Rout Fades After $7 Trillion Wiped Out

Is it finally safe to buy the dip?

One day after Wall Street’s worst day since 2011 which sent US stock markets into the red for the year, and after Asian markets suffered heavy losses putting global stocks on course for their worst month since the financial crisis, the global rout has eased and S&P 500 futures gained as much as 1%, signaling a bounce on Wall Street and wiping out much of Wednesday’s last hour losses…

… while Nasdaq 100 futures are 1.8% higher with Tesla gaining 11% in pre-market after smashing expectations and helping to brighten the mood, following a similar rebound in Europe which initially fell 1% in early trade, but has since rebounded and the Stoxx Europe 600 was up 0.3% with Italian and Spanish stocks leading the European recovery, the FTSE MIB up as much as 1.4% and the IBEX up 1.3%, helped by a rebound in the beaten-down tech and auto sectors following reassuring results from Peugeot.

After hitting 26 yesterday, the VIX fell over 2 points to 23.16 and suddenly the market looks to be turning the corner on yesterday’s brutal selloff.

Earlier in the session, Asia-Pac bourses saw hefty selling as the stock market bloodbath rolled over from the US, with the MSCI Asia Pac sliding into a bear market overnight.

Australia’s ASX 200 (-2.8%) and Japan’s Nikkei 225 (-3.7%) slumped from the open amid heavy pressure in tech and with losses in Japan magnified by a firmer currency, sending Japan’s Topix index to the lowest in more than a year while corporate updates failed to provide any reprieve as Sharp shares slumped following a cut in its revenue forecasts. Asia’s overnight woes have seen the global wipeout on the MSCI World since January near $7 trillion. Pan Asia-Pacific shares skidded more than 2% while Japan’s Nikkei tumbled as much as 4% to a six-month low.

However an early sign that a rebound was in the offing came from China’s Shanghai Composite, which pared losses of as much as 2.8% as the National Team made its usual late-day appearance, helping stocks close just barely in the green and providing a base for sentiment.

While China’s rebound was certainly helped by Beijing, an odd hiccup was observed in the offshore Yuan, which suddenly tumbled after the European open, then cratered to the lowest level in years as the USDCNH spiked as high as 6.9669 before retracing most of the bizarre move. There was no news to explain the spike or subsequent fade.

So is this the bottom at last? To be sure, all signs are positive for the time being, but there’s the case of North American trading to navigate, and another barrage of earnings; we could very well get a deja vu repeat of Wednesday’s session, when heading into yesterday’s session risk sentiment recovered as well but that quickly faded later on and US stocks endured a bloodbath instead. That said, US stocks are now more oversold than they were at the trough of the February crash.

Additionally, investors remain apprehensive as a flood of earnings, while mostly stellar, have come with warnings about the future impact of tariffs and rising costs. Central banks are also in the spotlight, with investors speculating what if any impact the market uncertainty will have on policy decisions.

Currency dealers were also cautiously reversing out of Swiss franc and Japanese yen safety trades and Italian and Spanish bonds made ground as traders waited to see what message the ECB delivers at its meeting later.

“The markets have been acting like classic flight-to-safety markets,” said London & Capital’s head of fixed income Sanjay Joshi, pointing to the slump in stocks and rally in safer bonds and currencies. “The worst thing the ECB could do would be to come out with a hawkish statement considering the situation we have at the moment.”

Most economists expect ECB President Mario Draghi to say the bank will stick to plans to end stimulus this year. But it will be the signal he sends about market volatility and concerns around Italy, his homeland, that could be most crucial. Ahead of the ECB meeting – where as previewed last night the outlook for the euro-zone economy will be scrutinized – US Treasuries declined and European bonds were mixed; the German yield curve meanders around unchanged levels ahead of the ECB with 10Y yields steady ~0.40%. Importantly, the Bund/BTP spread is 7bp tighter, as BTP futures rise despite official denials of possible budget adjustments. Other peripheral spreads similarly tighter, semi-core yields little changed.

It wasn’t just the ECB that was being closely watched either. Turkey, which has been stabilizing in recent weeks having been at the center of emerging market troubles was also holding a central bank meeting. The consensus is that having almost doubled its interest rates already this year to 24 percent, it might be brave enough to hold still this month.

Looking at FX, major currencies traded in relatively tight ranges as stocks rebounded in Europe with the ECB press conference looming.

The Bloomberg Dollar Spot Index consolidated after reaching the highest level in 16 months yesterday while the overnight risk rally put the yen and the Swiss franc on the back foot. Bank of Canada’s hawkish stance supported the loonie another day, as the Canadian dollar tested 55-DMA resistance versus the greenback, and oil consolidated recent losses. Norway’s central bank retained its careful approach in raising rates and the krone met modest support. Emerging-market currencies stayed under pressure while euro-area bonds advanced and Treasuries edged lower together with the yuan. In G-10, NZD is the worst performer after New Zealand trade deficit hit a record. WTI stages a small bounce off Asian lows back up to $66.70. Base metals little changed.

Over in the oil complex, WTI (+0.1%) and Brent (+0.4%) are both in the green, with prices eyeing USD 67.00/bbl and USD

76.50/bbl to the upside respectively, with traders mindful of increases in US crude stocks as countries are importing less from Iran

and storing most of what they import ahead of Iranian sanctions coming into effect at the start of November. Additionally, Saudi

Arabia and Russia have agreed to extend their agreement to preserve oil market stability. Elsewhere, Sinopec and CNPC have not

placed a November oil order from Iran due to concerns over how the sanctions will impact their global operation.

Looking ahead, it’s going to be a big day for earnings with American Airlines, CME Group, Comcast, Conoco, Merck & Co., Twitter, Union Pacific, Alphabet, Amazon, Intel and Snap are among many companies due to report earnings. Expected data include wholesale inventories, durable goods orders, and jobless claims.

Market Snapshot

- S&P 500 futures up 0.9% to 2,688.75

- MXAP down 2% to 146.75

- MXAPJ down 1.5% to 464.76

- Nikkei down 3.7% to 21,268.73

- Topix down 3.1% to 1,600.92

- Hang Seng Index down 1% to 24,994.46

- Shanghai Composite up 0.02% to 2,603.80

- Sensex down 0.9% to 33,730.86

- Australia S&P/ASX 200 down 2.8% to 5,664.07

- Kospi down 1.6% to 2,063.30

- STOXX Europe 600 down 0.1% to 352.80

- German 10Y yield fell 0.3 bps to 0.393%

- Euro up 0.1% to $1.1407

- Italian 10Y yield rose 1.2 bps to 3.23%

- Spanish 10Y yield fell 1.1 bps to 1.614%

- Brent futures up 0.1% to $76.28/bbl

- Gold spot down 0.1% to $1,232.96

- U.S. Dollar Index down 0.1% to 96.32

Top Overnight News

- President Donald Trump will be briefed by CIA Director Gina Haspel today, following a report in the Washington Post that she heard an audio tape allegedly made of Khashoggi’s interrogation and killing at the consulate on Oct. 2

- The U.K.’s financial watchdog is examining whether secret relationships between polling companies and hedge funds, especially the sale of market-moving exit polls and voter-opinion data, could violate market-abuse prohibitions

- More money is flowing into the world’s largest exchange-traded fund tracking Chinese stocks than at any time since the boom-and-bust in 2015, as state investors were said to have been stepping in to stem a market rout

- Norway’s central bank kept its key interest rate unchanged and reiterated its intention to tighten again early next year as policy makers proceed cautiously in unwinding the record stimulus unleashed over the past years

- Italian Treasury spokeswoman Adriana Cerretelli denies report that Finance Minister Giovanni Tria offered to quit after Moody’s downgraded Italy’s credit rating on Friday

- Italy spread will start narrowing over the next few weeks, helped by govt talks with EU officials to clarify its budget plan for next year, Deputy Premier Luigi Di Maio says

- Putin says he has ‘no qualms’ about buying Italian debt

- ECB’s Nowotny says next euro-area enlargement is a few years away

Asia-Pac bourses saw hefty selling as the stock market bloodbath rolled over from US where the S&P 500 and DJIA turned negative YTD, while the Nasdaq posted its worst performance since 2011 and slipped into correction territory amid an aggressive sell-off in tech. As such, ASX 200 (-2.8%) and Nikkei 225 (-3.7%) slumped from the open amid heavy pressure in tech and with losses in Japan magnified by a firmer currency, while corporate updates failed to provide any reprieve as Sharp shares slumped following a cut in its revenue forecasts. Shanghai Comp. (Unch) closed little changed and Hang Seng (-1.2%) saw firm losses with Cathay Pacific shares descending on reports of a data breach that could affect around 9.4mln passengers, although losses in the mainland were to a somewhat lesser extent amid further liquidity efforts by the PBoC and continued supportive rhetoric by Chinese agencies. Finally, 10yr JGBs were higher as they tracked upside in T-notes and with demand underpinned as the stock sell-off spurred a flight to quality.

Top Asian News

- China’s Xiaomi Aims its Priciest Phone at Huawei and Apple

- Asian Stocks Lose $5 Trillion This Year With No End in Sight

- It’s Time to Consider SoftBank’s Future Without Saudi Money

- Japanese Stocks Slump as Topix Heads for Worst Month Since 2008

European equities mostly higher despite the mass sell-off experienced overnight in Asia after the soured sentiment from US spilled over onto the region. Eurostoxx 50 (+0.9%) resurfaced after opening in the red while the SMI (-0.4%) failed to take advantage of the rebound as the index is pressured by shares in ABB (-3.0%) and Lonza (-1.7%) amid weak earnings. On the flip side, CAC (+1.4%) is buoyed as 75% of the index is in the green (with the top gainers fuelled by earnings), and Spain’s IBEX (+1.3%) is lifted by banking names after Bankinter (+1.5%) reported inspiring earnings. In terms of sectors, telecom names lag along with healthcare while consumer discretionary and materials outperform. Moving onto individual movers, WPP (-18.0%) rests at the foot of the Stoxx 600 after cutting guidance, dragging Publicis (-5.0%) shares lower in sympathy, while AB InBev (-9.0%) shares are also trading with hefty losses amid disappointing earnings across all metrics.

Top European News

- Best Hope for Italian Bonds May Be Populist Coalition’s Collapse

- WPP Slumps After New CEO Outlines Painful Turnaround Effort

- Debenhams to Close Up to 50 Stores, Take $660 Million Charge

- Nokia to Cut Jobs as Profit Improves Less Than Expected

FX markets have begun the session on a relatively tentative footing with most majors relatively unchanged thus far alongside a

broadly flat DXY which remains contained by its recent 96.00 to 96.50 range. European markets await updates from the ECB with EUR/USD contained by offers around 1.1420-25 with analysts also flagging 1.1bln in option expiries for the pair between 1.1420-30. Focus for the ECB release today will likely centre around the Bank’s view on risks to the Eurozone’s economic outlook and whether risks will continue to be viewed as ‘balanced’ or ‘tilted to the downside’; expectations for any material adjustments to the ECB’s forward guidance are relatively low. Elsewhere, GBP has seen little in the way of material price action as GBP/USD straddles the 1.2900 handle (note, 627mln expiry Friday) as political jitters keep any potential moves to the upside contained for now with Lloyds touting the possibility that daily momentum suggest the pair could extend recent losses towards 1.2800. May appears to have survived any potential catastrophic fallout from yesterday’s 1922 Committee meeting but intra-party tensions remain a threat to the Brexit process. Focus during Asia-Pac trade continues to focus on the seemingly one-way moves in USD/CNY with CNY posting its weakest close vs. USD since Jan 3rd 2017. Commentary continuing to speculate over what action (if any the PBoC) will take against defending the 7.00 barrier with this week’s measures taken by policymakers unable to reassure markets against the threat of trade conflict from the US. Elsewhere for Asia-Pac currencies, USD/JPY managed to reclaim 112.00 to the upside overnight with some suggestions of selling fatigue, that said, the current stock market rout could lead any optimism to be relatively short-lived; UBS recommends selling rallies between 112.25-35. Notable option expiries for USD/JPY includes 1.3bln at 112.00-10, 815mln at 111.75-85 and 1.7bln at 112.50-60.

In commodities, gold is trading flat just above USD 1230/oz, following the overnight equity sell off in Asia, where the yellow metal rose to session highs of as investor sought a safe haven, but has since come off highs. Copper prices have again fallen for the third day in a row, reaching a two-week low as the red metal tracked overnight sentiment. Over in the oil complex, WTI (+0.1%) and Brent (+0.4%) are both in the green, with prices eyeing USD 67.00/bbl and USD 76.50/bbl to the upside respectively, with traders mindful of increases in US crude stocks as countries are importing less from Iran and storing most of what they import ahead of Iranian sanctions coming into effect at the start of November. Additionally, Saudi Arabia and Russia have agreed to extend their agreement to preserve oil market stability. Elsewhere, Sinopec and CNPC have not placed a November oil order from Iran due to concerns over how the sanctions will impact their global operation. Iraq Oil Minister Ghadhban said Iraq will help maintain a fair price for producers and consumers, adding that Iraq will cooperate with OPEC members to stabilize oil market.

The highlight today will be the ECB’s monetary policy meeting and press conference. On the data front, we get Spain’s September PPI, Germany’s October IFO business survey, and France’s 3Q total jobseekers data. In the US, it’s a busy day with: preliminary September wholesale inventories, durable goods, and capital goods orders; October’s Kansas City Fed manufacturing activity index; the latest weekly jobless claims; and September’s pending home sales, advance goods trade balance, and retail inventories. Away from data, UBS, Daimler, Twitter, Alphabet, Amazon, and Intel will release their earnings.

US Event Calendar

- 8:30am: Advance Goods Trade Balance, est. $75.1b deficit, prior $75.8b deficit, revised $75.5b deficit

- 8:30am: Wholesale Inventories MoM, est. 0.5%, prior 1.0%; Retail Inventories MoM, prior 0.7%, revised 0.7%

- 8:30am: Durable Goods Orders, est. -1.5%, prior 4.4%; Durables Ex Transportation, est. 0.4%, prior 0.0%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.5%, prior -0.9%; Cap Goods Ship Nondef Ex Air, est. 0.4%, prior -0.2%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 210,000; Continuing Claims, est. 1.64m, prior 1.64m

- 9:45am: Bloomberg Consumer Comfort, prior 60.8

- 10am: Pending Home Sales MoM, est. 0.0%, prior -1.8%; YoY, est. -2.6%, prior -2.5%

- 11am: Kansas City Fed Manf. Activity, est. 13.5, prior 13

DB’s Jim Reid concludes the overnight wrap

Yet another chastening 24 hours for markets with many global equities closing at multi-month, YTD, or multi-quarter lows. The S&P 500 dropped -3.08% to its lowest level since May, and is now down -0.65% on the year. For context, it’s the fourth time that the S&P 500 has moved by +/-3% this year, after only four other instances in the preceding six years (2012-2017). Quite a remarkable stat. The NASDAQ fell -4.63%, for its second move +/-4% this year, after only two other instances over the preceding six years. We’ll see if earnings today from Google and Amazon make much difference. The DOW fell -2.41% yesterday, also undoing its gains for the year, while US banks are now down over 10% YTD after their -2.68% drop.

In Europe, the STOXX 600 closed down -0.22%, though selling on futures accelerated during the US session and point to a notably lower open today. Safe havens rallied, with yields on 10-year Treasuries and Bunds falling -6.0bps and -1.3bps. The dollar, the yen, and gold all rallied, by +0.41%, +0.25%, and +0.17%, respectively. The VIX closed back above 25 up around 4.5 points.

Mixed earnings were blamed for the risk-off as was weaker US housing data. Fears over the global economy were also heightened by the softer European flash PMIs earlier. The US equivalent held up a bit better but still slightly missed. More on this later but it’s worth highlighting that Asian markets are following the lead from Wall Street with the Nikkei (-3.32%), Hang Seng (-1.80%), Shanghai Comp (-1.42%) and Kospi (-1.55%) all down along with most Asian markets. In the process, the Kospi entered bear market territory today down -20.84% from its January highs as we type while the MSCI Asia Pacific index entered it yesterday – down -20.32% from its January highs.

The main focus today will be on the ECB policy meeting and President Draghi’s press conference. We don’t expect any major announcements or changes to the policy stance, but expect it to be interesting nonetheless, given the recent softening in macro data and political developments in Italy. On the former point, as discussed above, PMIs yesterday in Europe softened more than expected and present downside risks to growth. Indeed, it’s possible that Mr. Draghi may reframe the risk outlook towards “to the downside” rather than “balanced.” The preliminary October composite PMI for Europe printed at 52.7 versus expectations for 53.9, down -1.4pts from September. This is the lowest print since September 2016, and indicates that some of the slowdown over the summer may not have been completely transitory. Full recap of the data follows later.

On the Italy question, tensions continue to swirl between the national and European authorities. For the third consecutive session, BTPs traded strongly in the morning before retracing during the afternoon as New York awoke. Again, the rhetoric was mixed throughout the day, with European Commissioner Moscovici saying the Italian growth projections were “optimistic” and that “public debt may not come down in the next two years.” Italian Cabinet Undersecretary Giorgetti cautioned that a further sell-off in BTPs would have negative implications for Italian banks’ capital situations, and an index of Italian banks traded down -3.31% yesterday to its lowest level since November 2016. Deputy Prime Minister Salvini was not evidently sensitive the sell-off saying that “Brussels can send Italy 12 little letters from now until Dec. 25 when Santa Claus is at the door, but we will say in a respectful and polite way that the Italians come first.” Ten-year BTPs ultimately retraced gains of as much as -7.4bps to close +1.3bps higher.

So between the softer data and the Italy situation, we expect Mr. Draghi to sound dovish today, but to sound firm on Italy. He will probably defer a decision on the end of QE until the December meeting, at which point the Governing Council is likely to endorse the end of QE for year-end. However, given the latest data and the ongoing Italy stress, our FX strategists have revised down their end-2018 forecast for the euro. Rather than 1.17 versus the dollar, they now expect it to trade down to 1.13. They don’t see steeper downside risk as the ECB is already priced very dovishly and the flow outlook still looks positive. Full ECB preview and updated euro call can be found here and here .

Back to yesterday and trying to dissect the mixed earnings. Tesla and Boeing were the standout positive performers, but didn’t outweighing tepid reports from the likes of Visa, AT&T, and UPS. Tesla posted its highest-ever quarterly revenue and only its third-ever profit, and shares rose over +8% in after-hours trading. Boeing generated a robust free cash flow and raised its profit forecasts. It provided the biggest boost to the DOW yesterday – one the only five companies to gain out of the index’s 30 members. AT&T and UPS both missed on profits and traded down -8.12% and -5.53%, respectively. After markets closed, Visa and AMD both reported. Visa missed on revenues while AMD – which had been the best-performing stock in the S&P 500 year-to-date – lowered its fourth quarter guidance and traded as much as -24% lower overnight, giving up around $5.5bn of its year-to-date market cap gain of $12.2bn. Pretty brutal reactions to earnings disappointments.

The biggest data release yesterday were the flash PMIs in Europe. The euro area-wide composite index printed at 52.7 (versus expectations for 53.9), manufacturing at 52.1 (versus 53.0), and services at 53.3 (versus 54.5). For Germany, the composite index printed at 52.7 (versus 54.8), manufacturing at 52.3 (versus 53.4), and services at 53.6 (versus 55.5). In France, the composite index printed at 54.3 (versus 53.9), manufacturing at 51.2 (versus 52.4), and services at 55.6 (versus 54.7). So overall, weaker than expected, with German manufacturing new orders dipping to 48.2- its first reading below the 50-level since November 2014. Certainly not a positive signal for global demand.

In the US, the composite flash PMIs showed continued expansion at 54.8 from 53.9. However the manufacturing and services numbers both slightly missed expectations even if they increased mom. Qualitatively, the report indicated strong growth and robust price pressures, with some concerns over tariffs. Separately, new home sales were down a sharp -5.5% mom in September, far exceeding expectations for -0.6%. The prior three months were all revised lower as well. The ratio of current inventory to sales, a popular metric of the housing market, rose to 7.1, its highest level since 2011, signaling a supply overhang and/or tepid demand. Our economists have been highlighting the trends weighing on US housing all year, and they don’t expect sectoral weakness to derail the broader macro strength.

The highlight today will be the ECB’s monetary policy meeting and press conference. On the data front, we get Spain’s September PPI, Germany’s October IFO business survey, and France’s 3Q total jobseekers data. In the US, it’s a busy day with: preliminary September wholesale inventories, durable goods, and capital goods orders; October’s Kansas City Fed manufacturing activity index; the latest weekly jobless claims; and September’s pending home sales, advance goods trade balance, and retail inventories. Away from data, UBS, Daimler, Twitter, Alphabet, Amazon, and Intel will release their earnings

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 0.51 POINTS OR 0.02% //Hang Sang CLOSED DOWN 255.32 POINTS OR 1.01% //The Nikkei closed DOWN 822.45.49 OR 3.72%/ Australia’s all ordinaires CLOSED DOWN 2.82% /Chinese yuan (ONSHORE) closed DOWN at 6.9440 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 67.10 dollars per barrel for WTI and 76.56 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9440 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9489: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

Albert Edwards is joining Kyle Bass in explaining that China will undergo a hard landing. He cites as does Bass, the fact that China has its first and probable permanent current account deficit and they may not have the appetite to continue to inflate their way out of their mess

(courtesy zerohedge)

“Their Luck Is Running Out”: Why Albert Edwards Expects A Chinese Hard-Landing

Albert Edwards remembers the 1987 equity crash “as if it were yesterday.”

As the SocGen strategist reminisces in his latest note to clients, “one key feature was investors’ surprise that the already frothy Japanese equity market and economy just sailed through the crisis more untouched than most. This was mistakenly attributed to sound policy and an unsinkable economy. As a result, confidence that Japanese policymakers could deftly manage and avert any potential crisis saw investors pour money into Japanese assets. Risk appetite inflated to previously unseen levels, and then……”

Albert brings up this particular diversion from the real risks facing traders on that October morning in 1987 because it represents a lesson “that when policymakers have a ‘good’ crisis, investors then become over-complacent and fail to price risk correctly.”

It wasn’t just Black Monday: as Edwards notes, in 2001, in the immediate aftermath of the Nasdaq crash and with the expected deep recession averted, investors made the mistake of anointing Alan Greenspan with semi-supernatural powers of policy management “whereas in fact he might have just been lucky.” He was.

Alan Greenspan and the Fed were seen by investors to have had a good crisis, and together with Greenspan’s mythical equity market put, investors became overcomplacent. The bust, when it came, was worse, precisely because over-confidence in policymakers’ ability to control events led to excessive risk and debt being taken on.

Fast forward to today when Edwards claims that with the world suddenly focused on the US, the real trouble continues to brew enearly half a world away: namely “China is currently another place where there is over-complacency.” Investors, who long ago decided to stop paying attention to the Kyle Basses of the world who repeatedly have warned about the risks posed by China’s economy…

Kyle Bass

✔@Jkylebass

Watch how China has fooled the world into believing their economy is strong by printing RMB. GDP on top, money printing in middle.#facade

… are virtually certain that China’s economy will not hard-land, mainly because the policymakers have proved the naysayers wrong time and time again. But, as in the case of 1987 and 2001, “is luck now running out?” Edwards asks, this time for Beijing.

Edwards’ argument revolves around the claim with China’s policymakers having had a very ‘good’ crisis in 2008 (which was papered over only thanks to trillions in new debt, as Kyle Bass’ tweet above shows), “since then, naysayers, such as myself, have been consistently wrong in projecting that policymakers would lose control and that a grotesque credit bubble would burst and lay the economy low.”

And yet, just like in late 2015, with the sharp swoon that followed China’s devaluation and the bursting of its stock bubble, once again fears are growing about the Chinese economy slowing rapidly, even if few fear a bust. Instead, Edwards contends that as President Trump exerts mounting pressure on the Chinese economy via tariffs, “the worry is that a Chinese policy response will send the global markets into a tailspin, just as the August 2015 devaluation did.”

Which, in turn, reminds the SocGen strategist that, as we reported back in August, China just unveiled its first ever current account deficit, marking a seachange in the direction of China’s capital flows, and making China’s policymakers’ job even harder, once again bringing up the question: “Is luck running out?”

Of course, the current account is just a symptom of an greater malady affecting China: namely a rapid slowdown in Chinese growth. Referencing the recent work of SocGen China economist Wei Yao, Edwards notes that the swing into current account deficit shown above is likely to be permanent. The result will be increased fragility in the renminbi “at a time when economic growth is slowing sharply, led by the industrial (secondary) sector (see left-hand chart below). And with export growth to the US only temporarily buoyed to avoid tariff hikes, this slowdown is likely to intensify.”

Even more troubling than China’s brand new current account deficit is that as Yao highlights, the Chinese economy has slowed to the point that employment has begun to fall, most visibly in the slump in the latest employment component of the PMIs (both official and Caixin). And while the decline in manufacturing jobs has been apparent for a few years now (ie sub 50), but it is also the services sector that is now also shedding labor, making China’s economic slowdown a “really serious” issue for policymakers.

Meanwhile, the traditional response Beijing has activated in such situations – namely blowing a massive credit bubble, no longer appears to be an option as Chinese policy seems “to swing from feast to famine as policymakers grapple with the increasing instability of the credit bubble they have created.”

The main reason cited by the SocGen economists for the policymakers’ reluctance to blow yet another bubble is concerns about how it will affect China housing market, where the issue is that Beijing’s credit policy swings about so violently it destabilizes a housing market that is constantly prone to bubble tendencies (see chart below). This, Edwards believes, is due to few alternative investment opportunities – especially after the 2015 H2 equity market collapse.

And here Edwards makes a bold assumption: “after the aggressively expansive monetary and fiscal policy of 2015/16, the authorities remain determined not to reignite the credit bubble.” Perhaps, or perhaps Beijing simply has not had a reason to pull out all the debt stops just yet in the past 3 years, ever since the Shanghai Accord of early 2016 unleashed another debt tsunami across China, whose aftereffects have kept the economy afloat.

Still, one can argue that Edwards is correct, especially when one looks at the overall public sector deficit which is already at 2009 crisis levels of 11% of GDP, as creation of China’s shadow credit – the deus ex machina for the past decade – continues to be “strangled.”

As a result of these trends, the SocGen strategists describe Chinese policy easing in the face of the current sharp slowdown as only “half-hearted” and demanding for more stimulus from Beijing to avoid a sharp economic contraction.

Which in turn brings us back to the start of this post, and the lesson from 1987, because whereas everyone is focusing on an entirely different set of problems, Edwards cautions that “no one expects a [Chinese] hard-landing” and asks “Why not?”

If he, and Kyle Bass are right, we’ll get the answer to this question very soon.

4.EUROPEAN AFFAIRS

Some wanted the language stronger but Draghi did not oblige. He stated that the ECB will end QE in December 2018 and keep long term interest rates at present levels until the summer of 2019. Nothing changed from previous statements

(courtesy zerohedge)

ECB To End QE In December, Will Keep Rates

Unchanged “As Long As Necessary”

In a statement that was a virtual replica from September, the ECB announced it was keeping its three key rates unchanged (main refinancing operations: 0.00%, marginal lending facility: 0.25%; deposit facility: -0.40%), that it will end its LSAP QE program at the end of December however “subject to incoming data confirming the medium-term inflation outlook”, that it will reinvest the principal payments from maturing securities purchased “for an extended period of time” and that in keeping with its prior forward guidance, “rates will remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.”

In short, no surprises, even though as Bloomberg notes, the ECB still says it “anticipates” to end new QE purchases in December, while some analysts had suggested the Governing Council might tweak the language to make the commitment stronger. Not yet.

Full statement below:

At today’s meeting the Governing Council of the European Central Bank (ECB) decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the new monthly pace of €15 billion until the end of December 2018. The Governing Council anticipates that, subject to incoming data confirming the medium-term inflation outlook, net purchases will then end. The Governing Council intends to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Bunds Drop, Euro Rises As Draghi “Not Dovish

Enough”

Ahead of Draghi’s press conference, some traders had hoped that Draghi would acknowledge the sharp slowdown in the European economy in recent weeks, as shown by the latest drop in the Citi Eurozone surprise index, the ongoing political turmoil in Italy and the UK, and general economic slowdown due to the ongoing trade war, perhaps going so far as hinting at an extension of the ECB’s QE.

And while the ECB president did acknowledge a “somewhat weaker moment”, citing Brexit, trade and Italy as the key risks, offsetting this was the assessment that risks to growth are still “broadly balanced” while noting that there still is a broad-based expansion and remarking that the ECB has “no reason to doubt our confidence in inflation” has rendered Draghi’s commentary “not dovish enough”

Furthermore, as Bloomberg notes, the key to the Draghi’s thinking is that the slowdown is due to ‘country-specific factors’ “idiosyncratic reasons” as he mentions the German auto sector as well as trade and political uncertainties (Italy/Brexit).

The fact that the ECB sees these as temporary factors means that there’s no plans – for now – to reverse on QE’s December end-date.

And so, despite the reference to weaker-than-expected incoming data, as a result of Draghi’s hawkish tone and the denial to even hint at an end to QE, the EURUSD has jumped to session highs…

… alongside Bund yields which are also several basis points higher.

end

Brexit Talks On Hold As “May’s Team Can’t

Agree”, Cable Slides

The neverending Brexit saga, replete with endless trial balloons and head fake headlines, took its latest detour into the unknown, and sent cable sliding, after the latest report from Bloomberg that U.K. Prime Minister Theresa May’s Cabinet is not close enough to agreeing a way forward for top level Brexit negotiations to resume, even as time to reach a deal is running short.

According to Bloomberg sources, “there will almost certainly be no new plan put forward by the British side before next Monday’s budget, the annual statement setting out the government’s tax and spending plans for the next year.”

The latest disappointing, if expected, assessment followed a “stormy meeting” of May’s cabinet on Tuesday, when two factions battled each other over the question of how to avoid customs checks at the Irish border without tying the U.K. into the European Union’s trade regime forever. Two days later, a meeting that was called to discuss the issue on Thursday was canceled because agreement within May’s team is still out of reach, according to a report in the Evening Standard newspaper.

Divisions within the U.K. negotiating team meant a draft agreement was vetoed by May’s ministers, notably Brexit Secretary Dominic Raab, the people said. At the summit in Brussels, May offered further compromises, pledging to consider extending the transition period and to drop her demand for a strict end-date to the so-called backstop arrangement for the Irish border.

Predictably, the pound dipped on the news, and is now trading well below its 50 and 100-DMA, although much of its losses have been a function of the stronger dollar.

That said, with kneejerk reactions such as this one it would be difficult to claim that a hard Brexit is fully baked into the cake.

end

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

CIA Director To Brief Trump Thursday On ‘Fact

Finding’ Trip To Turkey

As his willingness to give Crown Prince Mohammad bin Salman any benefit of the doubt continues to fade, President Trump is set to be briefed by CIA Director Gina Haspel on Thursday about what she learned on her ‘fact-finding’ mission to Turkey earlier this week, where she reportedly heard the audio of Khashoggi’s brutal slaying recorded by Turkish spies (though the CIA has refused to confirm these reports).

According to CNN, Haspel traveled to Turkey on Monday, apparently to analyze information the Turks had collected on Khashoggi’s Oct. 2 murder inside the Saudi consulate in Istanbul at the hands of a 15-man hit squad reportedly sent to the embassy to either interrogate or kill Khashoggi (depending on whom you believe). Trump also said that the US has sent officials to Saudi Arabia to get more information on the killing, which has sparked a global diplomatic crisis, with Western countries weighing whether to cut off ties to the kingdom as Saudi’s regional allies line up in support of the kingdom.

The briefing will take place after Trump told WSJ that he suspects MbS knew about Khashoggi’s killing – or at least that he was more likely to have known about the killing than his father, King Salman. Trump on Tuesday called the killing and coverup “one of the worst in the history of coverups.”

“The prince is running things over there more so at this stage,” Trump said when asked about bin Salman’s involvement. “He’s running things and so if anybody were going to be, it would be him.”

Trump told reporters on Monday that “we have top intelligence people in Turkey. We’re going to see what we have.” Meanwhile, as Bloomberg reminds us, Trump is facing increasing pressure to do something – anything – to hold the Kingdom, a key US ally and buyer of US arms, accountable for its actions, with lawmakers in both parties pushing bills that would halt weapons sales to the kingdom – a possibility that Trump has already said he would prefer to avoid, per BBG.

The briefing also follows comments from the Saudi Attorney General who again shifted the narrative on Thursday by saying that the killing was “premeditated” by those who carried it out (who are now all, presumably, in custody in Saudi Arabia).

end

The Saudi’s now change their story again: the Khashoggi killing was a premeditated act…and 15 Saudi members that entered the embassy have been charged..he just do not know who ordered the hit..

(courtesy zerohedge)

Saudi Arabia Says Khashoggi Killing Was

“Premeditated Act”

Nearly a week after Saudi Arabia’s public prosecutor admitted that journalist Jamal Khashoggi had indeed been murdered inside the kingdom’s Istanbul consulate in what he described as a “botched interrogation”, the kingdom has apparently changed its story once again.

According to AFP, the public prosecutor is now saying that Khashoggi’s killing was a premeditated act presumably orchestrated by the 15 members of the Saudi hit squad that met and detained Khashoggi inside the consulate on Oct. 2.

AFP news agency

✔@AFP

#BREAKING: Saudi Arabia’s public prosecutor says the murder of #JamalKhashoggi in Istanbul was “premeditated” based on information supplied by Turkey

The news immediately preceded a report in the Kingdom’s Al-Arabiya news station that Crown Prince Mohammad bin Saman, who decried Khashoggi’s killing as a “heinous crime” and promised on Wednesday to punish anyone found to be responsible, had chaired his first meeting of the committee to restructure the Saudi intelligence service. The kingdom fired 5 intelligence officials and arrested 18 Saudi nationals for their involvement in the killing.

Al Arabiya English

✔@AlArabiya_Eng

BREAKING: #SaudiArabia: Committee to restructure the kingdom’s intelligence agency has discussed a reform plan and is assessing the current situation. https://english.alarabiya.net/en/News/gulf/2018/10/25/Saudi-Crown-Prince-chairs-first-meeting-to-restructure-intelligence-agency.html …

Saudi Attorney General Shaikh Suood bin Abdullah Al Mo’jab said are being “interrogated” using the information handed over by the Turks, per CNN.

“The public prosecution received information from the Turkish side through the Joint Working Group between the Kingdom of Saudi Arabia and the Turkish Republic, indicating that the suspects in Khashoggi’s case premeditated their crime,” Attorney General Shaikh Suood bin Abdullah Al Mo’jab said.