GOLD: $1233.55 UP $3.65 (COMEX TO COMEX CLOSINGS)

Silver: $14.69 UP 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1233.50

silver: $14.69

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 10 NOTICE(S) FOR 1000 OZ

Total number of notices filed so far for OCT: 1824 for 182,400 OZ (5.6734 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 502 for 2,510,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6550: up $23

Bitcoin: FINAL EVENING TRADE: $6540 up 13

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUGE 3755 CONTRACTS FROM 200,743 UP TO 204,498 DESPITE YESTERDAY’S 7 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 1631 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1631 CONTRACTS. WITH THE TRANSFER OF 474 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1631 EFP CONTRACTS TRANSLATES INTO 8.155 MILLION OZ ACCOMPANYING:

1.THE 7 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 2,520,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

38,981 CONTRACTS (FOR 20 TRADING DAYS TOTAL 38,981 CONTRACTS) OR 194.90 MILLION OZ: (AVERAGE PER DAY: 1949 CONTRACTS OR 9.745 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 194.90 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 27.84% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,414.3 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A STRONG INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3755 DESPITE THE 7 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1631 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 5486 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1631 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3855 OI COMEX CONTRACTS. AND ALL OF DEMAND HAPPENED WITH A 7 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.63 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.022 BILLION OZ TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER: 2,520,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 9604 CONTRACTS UP TO 485,222 DESPITE THE SMALL GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $1.15).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5874 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 5874 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 485,222. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,078 CONTRACTS: 9,604 OI CONTRACTS INCREASED AT THE COMEX AND 5874 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 15,478 CONTRACTS OR 1,547,800 OZ = 48.14 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A SMALL RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.15??.

YESTERDAY, WE HAD 5636 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 151,897 CONTRACTS OR 15,189,700 OZ OR 472.46 TONNES (20 TRADING DAYS AND THUS AVERAGING: 7594 EFP CONTRACTS PER TRADING DAY OR 759,400 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 472.46 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 472.46/2550 x 100% TONNES = 18.52% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,140.05* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 9,604 DESPITE THE SMALL GAIN IN PRICING ($1.15) THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5874 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5874 EFP CONTRACTS ISSUED, WE HAD AN HUGE GAIN OF 15,078 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5874 CONTRACTS MOVE TO LONDON AND 9,604 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 48.14 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH A TINY GAIN OF $1.15 IN YESTERDAY’S TRADING AT THE COMEX.??

we had: 10 notice(s) filed upon for 1000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.65 TODAY: /

NO CHANGES IN GOLD INVENTORY TODAY

/GLD INVENTORY 749.64 TONNES

Inventory rests tonight: 749.64 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 7 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 330.375 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 3755 CONTRACTS from 200,743 UP TO 204,498 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

1631 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1631 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3855 CONTRACTS TO THE 1631 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE NET GAIN OF 5486 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE STRONG GAIN ON THE TWO EXCHANGES: 27.43 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A HUGE INCREASE IN SILVER OI AT THE COMEX DESPITE THE 7 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A SMALL SIZED 1631 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 4.95 POINTS OR 0.19% //Hang Sang CLOSED DOWN 276.83 POINTS OR 1.11% //The Nikkei closed DOWN 84.13 OR 0.40%/ Australia’s all ordinaires CLOSED DOWN 0.01% /Chinese yuan (ONSHORE) closed DOWN at 6.9457 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 66.31 dollars per barrel for WTI and 76.06 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9457 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9619: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

iii)This is a death blow to the USA: China produces most of the world’s rare earths which is used in the manufacture of many items

4/EUROPEAN AFFAIRS

i)Germany/USA/Russia

A must read: Luongo explains why Germany is putting a small LNG unit in Germany to appease Trump. However Germany admits it will need much more gas from Russia than even the Nordstream 2 will supply. They need a Nordstream 3

( Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

the bond king has spoken: Gundlach tells investors to get out of corporate bonds..now!!

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)It seems that Turkey has skirted USA sanctions against Venezuela by buying their gold(Robinson,MedillNews Service/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)Today we received first estimate of Q3 GDP and it came in at 3.5% due to soaring inventories. But investments tumbled. I would be surprised if the final number is north of 3%

( zerohedge)

b)University of Michigan sentiment drops as home, auto spending outlook slides

( zerohedge)

b)Now Mulvaney is critical of the Fed( zerohedge)

iv)SWAMP STORIES

I guess we should have expected this from NBC: they sat on information that would have discredited Kavanaugh accusers

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a LOSS of 31 contracts to stand at 2 contracts. We had 32 notices filed YESTERDAY so we gained 1 contract or AN ADDITIONAL 5,000 oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus . Somebody was after badly needed physical silver.

After October, is the non active delivery month of November and here we lost 32 contracts DOWN to 1264 contracts. After November, we have a December contract and here we GAINED 1990 contracts up to 160,693

AND NOW COMPARISON FOR OCTOBER:

Gold Gains Nearly 1% On Week As Global Stock Markets Fall Sharply

Golden Nuggets: Key Gold and Precious Metals News, Commentary and Charts This Week

Here is our Friday digest of the important news, commentary, charts and videos we were informed of this week.

The old Wall Street adage is that they “never ring a bell at the top” but there was a real sense this week that we may have seen a turning point. U.S. stocks including both the NASDAQ and the S&P 500 have seen sharp falls already this week of 4% and nearly 5% respectively.

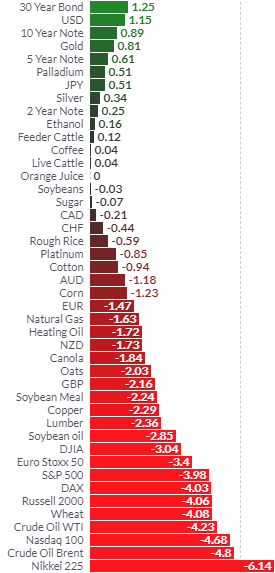

Weekly Relative Performance (Source: Finviz.com)

Asian and European markets did not fare much better with the Euro Stoxx 50 down 3.4% and Nikkei down 6.1% for the week.

This resulted in a rotation out of risk assets and into safe haven assets which saw certain government bonds, the dollar, gold and silver catch a bid.

Gold is 0.8% higher for the week and 3.5% higher month to date. Safe haven gold is again acting as a hedge and safe haven asset, exactly when investors need one.

Much of the news flow and price action this week was bearish for risk assets and quiet bullish for the precious metals. The world’s central banks, already the biggest holders of gold, are again looking at gold as a safer reserve asset than the U.S. dollar. Hungary increased its gold reserves by a massive 1,000% due to increasing “safety concerns.”

Large banks such BofAML and Goldman Sachs are again recommending gold to their clients as a diversification. This week BofAML (Bank of America Merrill Lynch) recommended as an “asset hedge” and “value play.”

Property markets around the world are seeing price falls – some sharply. This is being seen in London, Sydney, Vancouver and in other overvalued housing markets.

Prudent investors are positioning themselves in physical gold due to the increasing risks of sharp market corrections or indeed a crashes.

The ‘market bells’ rang a little bit louder this week …

Market Updates this Week

Dublin Housing Boom Set To Bust?

Palladium Surges To All Time Record High On Russian Supply Concerns

End Of The World As We Know It?

Key News this Week

Central Banks to Increase Gold Buying

Gold at 3-Month Highs; Flirts With $1,250 as Stocks Tumble

Gold Shorts Suffer Biggest Squeeze Since 1999 As Specs Abandon VIX-Selling Spree

Gold Recommended As Asset Hedge and “Value Play” By BofAML

Charts this Week

Charts via Bloomberg

News and Commentary

House prices ‘falling by over $1,000 a week’ in Sydney and Melbourne – Deloitte (ABC.net.au)

Asia stumbles again despite Wall St. bounce amid growth, earnings fears (Reuters.com)

Pending home sales snap back in September after 4-month losing streak (MarketWatch.com)

U.S. business spending on equipment slowing; goods trade deficit rises (Reuters.com)

Treasury official points finger at Turkey over Venezuelan gold trade (UPI.com)

Rare gold hoard unearthed in Donegal goes on display (Breakingnews.ie)

Source: PA & Breakingnews.ie

Paul Volcker, at 91, Sees ‘a Hell of a Mess in Every Direction’ (CNBC.com)

Wall Street analyst who called tstock-market rout sees another nasty drop (MarketWatch.com)

Here Comes The Housing Bust “Reverse Wealth Effect” (DollarCollapse.com)

Ted Butler: Why the frantic movement of silver at the Comex? (Gata.org)

Trouble In Arkansas: This Cycle’s Countrywide Financial Just Imploded (ZeroHedge.com)

Wary of crypto, UK government blocks Royal Mint’s digital gold (Reuters.com)

Learn More and Watch Direct Access Gold Video Here

Gold Prices (LBMA AM)

25 Oct: USD 1,232.15, GBP 954.67 & EUR 1,079.36 per ounce

24 Oct: USD 1,231.65, GBP 952.80 & EUR 1,078.68 per ounce

23 Oct: USD 1,235.60, GBP 950.67 & EUR 1,076.45 per ounce

22 Oct: USD 1,222.90, GBP 938.09 & EUR 1,062.21 per ounce

19 Oct: USD 1,228.25, GBP 942.44 & EUR 1,073.12 per ounce

18 Oct: USD 1,224.60, GBP 933.76 & EUR 1,062.83 per ounce

17 Oct: USD 1,226.75, GBP 933.68 & EUR 1,061.38 per ounce

Silver Prices (LBMA)

25 Oct: USD 14.74, GBP 11.43 & EUR 12.92 per ounce

24 Oct: USD 14.75, GBP 11.42 & EUR 12.92 per ounce

23 Oct: USD 14.71, GBP 11.33 & EUR 12.83 per ounce

22 Oct: USD 14.63, GBP 11.23 & EUR 12.72 per ounce

19 Oct: USD 14.61, GBP 11.21 & EUR 12.75 per ounce

18 Oct: USD 14.52, GBP 11.06 & EUR 12.60 per ounce

17 Oct: USD 14.65, GBP 11.16 & EUR 12.69 per ounce

Recent Market Updates

– Dublin Housing Boom Set To Bust?

– Palladium Surges To All Time Record High On Russian Supply Concerns

– Happy Birthday GoldCore

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

– End Of The Financial World?

– Gold Reserves Surge 1,000% In Hungary As It Joins Poland, Russia, China and Other Central Banks Buying Gold

– How Do You Sell Your Digital Gold When the Internet Goes Down?

– IMF Issues Dire Warning – ‘Great Depression’ Ahead?

– Poland Raises Gold Holdings to Record High in September – IMF

Ted Butler: Why the frantic movement of silver at the Comex?

Submitted by cpowell on Thu, 2018-10-25 17:08. Section: Daily Dispatches

1:12p ET Thursday, October 25, 2018

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler today marvels at the frantic movement of huge amounts of silver among the vaults of the New York Commodity Exchange, and wonders why it is happening and why it gets no notice from other market analysts.

Butler speculates that the cause is physical demand by JPMorganChase, which seems to have become the master of the silver and gold markets in the United States.

…

Butler concludes: “This is just but another example of unanswered mysteries surrounding silver. Others include the fact that JPMorgan has never taken a loss when adding new Comex short positions in silver (or gold) over the past 10 years, only profits. And that JPMorgan has remained the largest paper Comex short while at the same time accumulating massive amounts of physical silver and gold.

“The real mystery, of course, is why the U.S. Commodity Futures Trading Commission or JPMorgan won’t even address these concerns. One thing that’s not a mystery is that JPMorgan is positioning itself for a monster move up in price and so should you.”

Butler invites other explanations or elaborations, so here is some speculation:

1) Maybe the former head of JPMorganChase’s commodity desk, Blythe Masters, was telling the truth to CNBC in April 2012 when she maintained that the bank had no position of its own in the monetary metals markets and traded them only for clients:

https://www.youtube.com/watch?v=gc9Me4qFZYo

2) Maybe those clients include the U.S. government. After all, the filings of CME Group, operator of the major U.S. futures exchanges, reveal that its clients include governments and central banks —

http://www.gata.org/node/14411

— and CME Group’s own internet site describes the discounts it provides to governments and central banks for their secret trading of all major futures contracts in the United States:

http://www.gata.org/node/17976

3) If JPMorganChase is trading the silver market for the U.S. government or for another government with the U.S. government’s approval, that would explain the CFTC’s indifference to market rigging conducted by the bank as the government’s broker, since the Gold Reserve Act of 1934, as amended in the 1970s, establishing the Exchange Stabilization Fund in the U.S. Treasury Department, plainly authorizes the government to trade secretly in and manipulate any market in the world:

https://home.treasury.gov/policy-issues/international/exchange-stabiliza…

At a hearing in U.S. District Court in Boston in 2001 in GATA’s market-manipulation lawsuit against the Bank for International Settlements, the U.S. Federal Reserve, the Treasury Department, JPMorganChase, and other investment banks, an assistant U.S. attorney stated that the U.S. government claimed the legal power to secretly rig the markets exactly as GATA was charging:

4) Signing the Coinage Act of 1965, which demonetized silver, President Lyndon B. Johnson proclaimed that the U.S. government would dishoard as much silver as necessary from its metal stockpile to prevent the metal’s price from rising. Johnson said: “If anybody has any idea of hoarding our silver coins, let me say this. Treasury has a lot of silver on hand, and it can be and it will be used to keep the price of silver in line with its value”:

http://www.gata.org/files/JohnsonSigningStatementCoinageAct1965.pdf

That silver stockpile was exhausted years ago. So maybe, in its need to control monetary metals prices to protect the U.S. dollar and government bond prices and to control interest rates, the U.S. government has been using JPMorganChase as its broker in rebuilding a silver stockpile through manipulating the silver futures market and acquiring metal at a discount to fair-market value.

Months ago GATA formally asked JPMorganChase to elaborate on Blythe Masters’ assertion that the bank trades the monetary metals only for clients. That is, GATA asked the question CNBC failed to ask: Do those clients include the U.S. government or other governments and central banks? Of course GATA got no response.

But if JPMorganChase is acting as the U.S. government’s broker in the gold and silver futures markets, the bank may not be planning to run prices up but rather only to execute government trading orders, dishoarding and reacquiring metal as necessary to control the price.

In that case the gold and silver price suppression policy, longstanding as it has been, may still have a long way to go.

Butler’s commentary is headlined “Mysterious Metal Movement” and is posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/mysterious-metal-movement-17457

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-mysterious-metal-movemen…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

END

It seems that Turkey has skirted USA sanctions against Venezuela by buying their gold

(Robinson,MedillNews Service/GATA)

Treasury official points finger at Turkey over Venezuelan gold trade

Submitted by cpowell on Thu, 2018-10-25 22:35. Section: Daily Dispatches

By Lucas Robinson

Medill News Service

Wednesday, October 24, 2018

WASHINGTON — The United States should publicize Turkey’s involvement in the Venezuelan gold industry, a Treasury Department official said today.

Marshall Billingslea, assistant secretary for terrorist financing at Treasury, said at a Brookings Institution event that the Turkish government has skirted international sanctions by purchasing tons of Venezuelan gold in recent months.

…

“These are not your typical gold mines,” Billingslea said. “We’re approaching a similar kind of ‘blood diamond’ situation here with the gold in Venezuela.”

Billingslea criticized the government for driving out private mining companies and said the country’s mines operate outside of environmental and customs regulation. The mines, according to Billingslea, are a “wholesale” environmental disaster, leading to deforestation as well as disease through mercury contamination of water supplies. …

… For the remainder of the report:

https://www.upi.com/Treasury-official-points-finger-at-Turkey-over-Venez.

end

LAWRIE WILLIAMS: Gold in almost any other currency…

My colleague (boss) Ross Norman has published an article on this site looking at the precious metal’s performance in many other currencies than the U.S. dollar in which the gold price is almost universally quoted (see: The Stealth Gold Bull Market). Ross points to a couple of examples in major currencies – the UK pound and the Euro. Since 2014 the gold price in U.S. dollars is pretty much unchanged but in the British pound it has risen from £748 to £955 – a 30% rise. In the Euro it has similarly risen from €888 to €1,080 a gain of around 27%.

Ross also notes that in Chinese Yuan gold is up 15% in the same period; in the Russian ruble it is up a massive 94%; in the Indian rupee up 18% and in the Turkish Lira up an enormous 156%. Even in Swiss Francs, Ross notes, gold is up13% since 2014.

As can be seen from the Russian and Turkish examples where sanctions and geopolitical issues have affected the domestic currencies adversely I don’t think Ross has gone far enough in making his point. In Argentina for example the gold price has advanced around 467% in the domestic currency and in Venezuela, where hyperinflation is still raging, the rise has been astronomical.- up almost 3.6 million% in the local currency.

Most currencies have been slipping against the mighty dollar, at leastsince April this year, and as a consequence there are few, if any, currencies, in which gold has not advanced over the past four to five years.. As noted above even what might be considered a pretty stable currency like the Euro and the Swiss Franc have seen what might be considered significant gains. Even the Japanese yen has seen a 4.75 increase in the local gold price over the past five years.

But it is, in particular, worth looking at gold price rises in the principal gold producing nations which may be why global production is not falling to the extent anticipated in the various peak gold scenarios so beloved of gold analysts. A couple of the world’s major gold producers – China and Russia – are among the nations which have seen the gold price appreciate in their local currencies over the past five years. See Table below for the top 10 gold producing nations giving the five year price rises in local currencies(Anomalies with figures in text above due to slightly different timescales involved.)

Table: Top 10 2017 Gold producers

|

Rank |

Country |

2017 gold production (tonnes) |

5 year price rise over USDin local currency |

|

1 |

China |

429 |

+3.75% |

|

2 |

Australia |

287 |

+22.8% |

|

3 |

Russia |

272 |

+86.6% |

|

4 |

USA |

244 |

-9.0% |

|

5 |

Canada |

171 |

+13.8% |

|

6 |

Peru |

167 |

+10.1% |

|

7 |

South Africa |

157 |

+34.4% |

|

8 |

Ghana |

130 |

+100.5% |

|

9 |

Mexico |

122 |

+36.9% |

|

10. |

Indonesia |

114 |

+ 25.1% |

Source: lawrieongold.com, Goldprice.org

As can be seen in the table in a number of cases the gold price rises in local currencies have been sufficient to stimulate increased gold exploration and consequent production rises. This has been particularly important for gold miners and explorers in Australia and Russia – the number 2 and 3 global gold producers, both of which have seen decent gold output increases in the past couple of years, and has been significant too in staving off more closures in South Africa’s deep, and high cost, gold mines. In the world’s No.1 producer, China, the price rise has been insufficient to counter environmental pressures at some of the country’s mines which have led to closures.

26 Oct 2018

-END-

_________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9457/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9619 /shanghai bourse CLOSED DOWN 4.95 POINTS OR 0.19%

. HANG SANG CLOSED DOWN 276.83 POINTS OR 1.11%

2. Nikkei closed DOWN 84.13 POINTS OR 0.40%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 96.81/Euro FALLS TO 1.1345

3b Japan 10 year bond yield: FALLS TO. +.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.98/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.31 and Brent: 76.06

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.35%/Italian 10 yr bond yield UP to 3.52% /SPAIN 10 YR BOND YIELD UP TO 1.58%

3j Greek 10 year bond yield RISES TO : 4.30

3k Gold at $1235.60 silver at:14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 31/100 in roubles/dollar) 65.93

3m oil into the 66 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.98DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0010 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1358 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.35%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.08% early this morning. Thirty year rate at 3.31%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6174

“Tech-Wrecked”: Global Stocks, US Futures

Plunge As Panic Selling Returns

“The good news is: It’s Friday. The bad news is: everything else.”

For traders, Bloomberg’s summary of today’s early morning action couldn’t be more spot on. On the last day of a turbulent week, global market turmoil is back with a vengeance and traders in the US are greeted by another sea of red as stocks in Europe renewed their plunge along with Asian shares and U.S. futures as the tech-wreck returns after poor earnings from tech giants Amazon and Google slammed sentiment one day after a torrid dead cat bounce.

Disappointing Amazon and Alphabet results reignited investors’ anxieties about the overwhelming dominance of tech stocks – priced for seemingly unstoppable growth – in this market cycle, as well as peak earnings with e-commerce revenue growth now clearly rolling over. “There’s a huge amount of hot money in the FANG stocks,” said Christopher Peel, chief investment officer at Tavistock Wealth, and now it’s clearly going out.

The rosy picture of U.S. indexes finally ending their 6-day losing streak faded very quickly with Asian equities falling again, and after yesterday’s solid bounce, S&P futures were trading below the Wednesday session lows with the Nasdaq once again inside correction territory, down over 10% from its September highs.

The MSCI All-Country World Index was down 0.3% after trading began in Europe. It was set for its fifth straight week of losses, its worst losing streak since May 2013. “Expectations for US company earnings are quite high, so whenever they are not being met, the reactions are quite severe,” said Miraji Othman, credit strategist at BayernLB. “We have grown used to solid numbers, 18 percent revenue growth, 25 percent revenue growth and so on. The valuations have become quite ambitious.”

“You’re going to see a lot more volatility,” Con Michalakis, chief investment officer at Statewide Super, told Bloomberg TV in Sydney. “It’s going to be a feature of this environment.”

In Europe, Thursday’s rebound proved a brief respite as the Stoxx Europe 600 Index headed for the biggest monthly decline since the US downgrade in August 2011, with all sectors in the red and tracking a decline in U.S. futures after tech stocks Alphabet and Amazon missed results expectations, further sapping risk appetite as European earnings also disappointed with Valeo harshly punished.

The Stoxx Europe 600 fell 1.6% with Germany’s DAX down 1.7% and France’s CAC 40 down 2%. Overall the third-quarter earnings season has been marred by rolling sell-offs across global markets and sharp downgrades to earnings estimates.

Three main issues were plaguing European companies overall: rising costs from raw materials and wages, new trade tariffs, and a slowdown in China. Wary analysts were downgrading their earnings estimates for MSCI Europe at their fastest pace since Feb 2016.

Shares in French auto parts maker Valeo sank a record 20% percent after its second profit warning in three months, flagging disruption from tougher European emissions tests and a sharp sales downturn in China. Peer Faurecia also tumbled 7.7% after it announced an agreement to buy Japanese car navigation system maker Clarion from Hitachi. The autos & parts sector index fell 2.3%, the worst performer.

In other disappointing results, Europe’s biggest appliance maker, Electrolux fell 7.3% after it trimmed its market demand expectations and forecast higher costs due to increasing raw material prices and tariffs. Shares in French household appliances maker SEB also fell 9.4 percent, their worst day since 2012, after it cut its revenue guidance due to a “difficult environment” with FX and raw material costs rising. “If on one side the valuation is interesting and the top-line momentum is strong, we… need more visibility on the operating leverage in a more competitive market context,” wrote Equita analysts.

Results from banks were more mixed after more encouraging results from UBS had boosted it in the previous session. Spain’s Banco Sabadell topped the IBEX with a 4.3 percent gain after its third-quarter profit beat expectations. Britain’s RBS meanwhile tumbled 4.5 percent after it warned of economic uncertainty and its profit lagged forecasts

Earlier in the session, Asian shares sank deeper into a bear market, with Japanese stocks sliding more than 5% this week. MSCI’s index of Asia-Pacific shares outside Japan dropped 0.9%, erasing gains made in the opening hour and hitting its lowest level since February 2017. The MSCI Asia index has been bruised by a sell-off in the past several days, and is on course for its fifth weekly loss – its longest losing streak since 2015. It has fallen more than 4% this week amid concerns the global tech bubble has burst.

Over in China, shares were pulled lower and the yuan fell past 6.96 to the dollar, touching its weakest level against the dollar since December 2016, before the National Team stepped in, however despite a solid last hour push, it failed to bring the Shanghai Composite to the green….

… while the tumbling Chinese Yuan suddenly reversed its losses abruptly to trade stronger when at least one big China bank sold the greenback in the afternoon. The big lender’s selling triggered stop-loss by short-sellers of the yuan according to Bloomberg.

Elsewhere, on Hong Kong, the Hang Seng index was 1.1 percent lower, with tech shares dropping 3.13 percent. Tech firms also fell in South Korea, where the broader market slid 1.75 percent. The Kospi had earlier touched its lowest level since December 2016. Australian shares ended flat. Japan’s Nikkei stock index closed 0.4 percent lower, ending the week down 5.98 percent.

Markets remain on edge after more than $6.7 trillion was lost from global equities’ value since late September, as lofty expectations for earnings were tested amid heightened trade tensions and tightening financial conditions. The focus now turns to U.S. GDP, consumer-price and consumption data later Friday amid debate about the Federal Reserve’s policy path.

Emerging markets have suffered the worst monthly losses since May 2012 as increased volatility in the run-up to U.S. midterm elections ended a nascent rebound from a $5.5 trillion sell-off. Currencies were poised for a weekly drop and bond-risk premiums rose. The MSCI Emerging Markets Index declined for the 15th time in 20 trading days this month. Asian emerging markets were the worst performers and were on course for the worst year since the financial crisis. The Thai baht and South Africa’s rand led Friday’s losses among currencies, while Indonesian bonds trailed peers in the local debt markets. October has seen global assets fall in step, a departure from the first nine months of the year when much of the pain was felt in emerging markets amid concerns over the U.S.-China trade war and Federal Reserve tightening. World equities have erased $15 trillion, or 17 percent, of their value since January, with China alone losing $3 trillion

* * *

In currency markets, the euro fell after ECB President Mario Draghi said the bank’s 2.6 trillion-euro ($2.96 trillion) asset purchase program would end this year and interest rates might rise after next summer, despite fears about the monetary union’s economic and political future. The single currency was 0.2% lower at $1.1351.

Stock rout and PBOC comments over restrictions on using support tools for bond financing in some sectors with overcapacity kept the Antipodean and commodities currencies under pressure. The Aussie slipped to a two-year low and the dollar touched its strongest level since June 2017.

Meanwhile, the dollar extended its rally, staying at the highest since June 2017 as risk appetite remained under pressure. The Bloomberg Dollar Spot Index touched a higher high for an eighth day, the first time in six months; the gauge rose 0.2% to take gains for the week to 0.8%, its best performance since August.

Traders expect a strong reading of U.S. gross domestic product data on Friday, which could see the dollar strengthen.”Today’s robust U.S. GDP will illustrate to the market the deep division between the U.S. and the euro zone when it comes to growth performance,” said Commerzbank analyst Thu Lan Nguyen.”

Antipodean currencies lead losses in G-10 currencies as sentiment was dented with stocks in the red and after China’s central bank said financing support for some companies will be limited.

The British pound was near seven-week lows against the dollar on Friday and three-week lows against the euro, as doubt grew about whether the UK and the European Union can clinch a Brexit deal. Bloomberg, citing people familiar with the matter, reported on Friday that Brexit talks were on hold because Prime Minister Theresa May’s cabinet was not close enough to agreement on how to proceed.

U.S. Treasury yields fell as equity markets plunged. The 10-year yield fell to 3.0774% percent compared with its U.S. close of 3.136 percent on Thursday. Core European bonds gained and gold rose to a three-month high as the risk-off mood spread.

Oil prices headed for a third weekly loss after Saudi Arabia warned of oversupply and the slump in stock markets and concern about trade clouded the outlook for fuel demand. U.S. crude dipped 1 percent to $66.68 a barrel. Brent crude fell 0.73 percent to $76.33 per barrel.

Expected data include GDP and University of Michigan Consumer Sentiment Index. Aon, Colgate-Palmolive, Phillips 66, Moody’s and Ventas are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 1.1% to 2,658.25

- MXAP down 0.4% to 146.26

- MXAPJ down 0.9% to 461.97

- Nikkei down 0.4% to 21,184.60

- Topix down 0.3% to 1,596.01

- Hang Seng Index down 1.1% to 24,717.63

- Shanghai Composite down 0.2% to 2,598.85

- Sensex down 0.3% to 33,584.39

- Australia S&P/ASX 200 up 0.02% to 5,665.16

- Kospi down 1.8% to 2,027.15

- STOXX Europe 600 down 1.2% to 350.76

- German 10Y yield fell 2.8 bps to 0.37%

- Euro unchanged at $1.1375

- Italian 10Y yield fell 11.0 bps to 3.12%

- Spanish 10Y yield fell 0.5 bps to 1.582%

- Brent futures down 0.6% to $76.40/bbl

- Gold spot up 0.4% to $1,236.88

- U.S. Dollar Index down 0.1% to 96.62

Top Overnight News from Bloomberg

- U.K. Prime Minister Theresa May’s Cabinet is not close enough to agreeing a way forward for top level Brexit negotiations to resume, even as time is running short to reach a deal, according to people familiar with the matter. There will almost certainly be no new plan put forward by the British side before next Monday’s budget

- A no-deal Brexit would mean a difference of 1.6 percentage points to U.K. growth next year

- Some Bank of Japan officials are comfortable with yields on 10-year government bonds fluctuating further above their zero percent target than the 0.2 percent assumed by many investors, according to people familiar with the matter

- If Britain leaves the EU without an agreement, reverting to WTO’s most-favored-nation status rules, gross domestic product would increase only 0.3% in 2019, according to the National Institute of Economic and Social Research said

- The Italian government could use about EU15b of funds allocated but not spent by previous administration to aid banks if they’re at risk due to holdings of Italian state debt, La Stampa reports, without saying where it got the information

- Two Federal Reserve officials who vote on rates this year downplayed the effects on the economy of the rough October for U.S. stocks, saying the market turbulence would have to be sustained to alter their outlook for growth

- China’s forex reserves and stable fundamentals will keep yuan stable, Market News reports, citing Pan Gongsheng, head of State Administration of Foreign Exchange, as saying

- Australia is on track to ratify a new Pacific trade deal by Nov. 1, the country’s trade minister said, a move that would trigger the first tariff cuts this year in an 11-nation accord that survived an exit by President Donald Trump

- China’s government has told at least two of its state oil companies to avoid purchasing Iranian oil as the U.S. prepares to impose sanctions on the Persian Gulf state, according to people with knowledge of the matter

Asian stocks were broadly negative as early attempts to nurse the prior day’s sell-off and replicate the rebound seen on Wall St, were thwarted amid Amazon revenue disappointment which weighed across equity futures. ASX 200 (Unch) traded choppy but managed to pare back losses towards the end of the session and Nikkei 225 (-0.4%) failed to hold on to opening gains as the Japanese benchmark gradually deteriorated with earnings dominating news flow. Elsewhere, Shanghai Comp. (-0.2%) and Hang Seng (-1.1%) both conformed to downbeat tone, although the mainland briefly outperformed after this week’s substantial liquidity injection and with China also said to be considering additional tax and fee reductions including a VAT adjustment. Finally, 10yr JGBs eventually traded higher amid the widespread risk-averse tone in the region and with BoJ’s present in the market for JPY 1.1tln in 1yr-10yr JGBs.

Top Asian News

- Chinese $640 Billion Share-Pledge Risk Looms on Banks, Brokers

- Dealmaker to Tech Stars Has Record Flop After Hong Kong IPO

- The 1% Mark on Japan Yields Isn’t Enough to Sway Dai-Ichi

- Some at BOJ Are Said to See 10-Year Yield Limit Higher Than 0.2%

- Hong Kong’s Bad Run Continues as Tencent Drags for Fourth Day

European stocks are negative across the board in a continuation of the sell-off experienced in Asia overnight and on Wall St. yesterday. Almost 80% of the Stoxx 600 companies are in the red, while Eurostoxx 50 (-2.0%) flirts around levels last seen in November 2016, with the biggest losers consisting of German and French heavyweights such as Deutsche Bank (-4.5%), Airbus (- 3.9%) and Total (-3.5%) France’s CAC 40 (-2.3%) underperforms its peers with the index pressured by Valeo (-21.1%) after the company cut revenue guidance for FY 18. Over in Germany, the DAX (-2.0%) is weighed on by index heavyweight BASF (-2.2%) after the company forecasts adjusted EBIT guidance to the lower end of their previously guided range, while Covestro (-5.4%) rests at the foot of the index amid a downgrade at Berenberg. Sectors are experiencing broad-based losses with energy names pressured by price action in the complex and IT names uninspired following a revenue-miss reported by Alphabet (-5.9% pre-market). On the flip side, gainers in the Stoxx 600 are fuelled by earnings with Neste (+7.0%), Fingerprint Cards (+7.0%) and Banco de Sabadell (+4.5%) all higher following their numbers

Top European News

- Norway Wealth Fund Delivers $21 Billion Return on U.S. Stocks

- U.K. Bank Regulators Ask EU for Cooperation in Brexit Plans

- Surging Spreads Prompt More Italy Questions for ECB’s Draghi

- Draghi Faces Seven-Week ECB Confidence Test on Euro Economy

- RBS Drops After Making Provision for Brexit-Related Uncertainty

In FX, the DXY trades marginally firmer, extending on gains seen yesterday which pushed the index back above 96.50. Subsequently, EUR/USD remains on a 1.13 handle and below support at 1.1358 with relatively upbeat tones from Draghi yesterday unable to support the multi-bloc currency. Focus today for the EUR (absent of any negative Italian headlines), could well fall upon the slew of option activity with a slew of option expiries due to roll-off at the NY cut; 1.1350 (1.3bln), 1.1375 (1.3bln), 1.1400 (918mln), 1.1450-55 (1.1mln). From a tech perspective, if EUR/USD makes a break of 1.1350 to the downside, focus will turn to the August 16th low at 1.1336. GBP/USD has breached yesterday’s lows in recent trade alongside the aforementioned USD strength, with the latest Brexit-related commentary also bringing markets back to reality. Sources suggest that Brexit talks are on hold as UK PM May’s team cannot agree a way forward on how to proceed with negotiations and as such Cable is back below 1.2800. A sustained break below this level could open a test of YTD lows around 1.2660, particularly so, with November’s emergency EU leaders summit far from confirmed. Once again, focus during Asia-Pac trade continued to focus on the CNY after the PBoC opted to set the fix beyond 6.9500 for the first time since early January 2017. This subsequently prompted selling in high-beta currencies with AUD and NZD feeling the brunt with AUD/USD knocked below Feb 2016 lows of 0.7023. However, prices eventually bottomed out amid comments from the PBoC Vice Governor said the central bank will take necessary and target measures to deal with those who short the CNY; USD/CNY subsequently retreated from 6.9500 to 6.9350. Looking ahead, EM focus could be guided by events in Russia with the CBR due to come to market with their latest policy announcement. After the CBR unexpectedly raised rates by 25bps at its previous policy meeting, the consensus expects the central bank to maintain its one-week auction rate at 7.50%. Analysts at Barclays suggest that September’s rate hike has probably done enough to contain the pressure in the RUB and given the still below target inflation and a weak economy.

In commodities, gold is on target to notch a fourth week in the green, marking the yellow metal’s longest set of weekly gains since January; spurred on by ongoing economic constraints and concern over US corporate earnings. Prices continue to extend north of USD 1230/oz, while printing fresh session highs. Copper prices have retreated overnight as the red metal was weighed on by the market’s negative tone, eroding Thursday’s gains from a drop-in inventory. WTI and Brent are both extending losses in excess of a percent with the latter losing the USD 76.00/bbl level, in-fitting with the risk sentiment and signs that global trade is slowing with both container and bulk freight rates dropping, while yesterday’s comments of an upcoming oversupply by Saudi Arabia’s OPEC governor Al-Aama also weighing on prices. Additionally, markets are waiting for today’s Baker Hughes rig count which showed an increase of four operational oil rigs last week.

The key highlights for today are the advance Q3 GDP release for the US and the outcome of S&P’s sovereign ratings review for Italy. On the data front, in Europe, we get the ECB’s survey of professional forecasters along with France’s September PPI and October consumer confidence. In the US, we get the final University of Michigan October survey results as well as advance Q3 personal consumption, GDP price index and core PCE. Away from data, the ECB’s Draghi and Coeure will be speaking at different times. In addition, Total will release its earnings.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 3.3%, prior 4.2%

- Personal Consumption, est. 3.3%, prior 3.8%

- Core PCE QoQ, est. 1.8%, prior 2.1%

- 10am: U. of Mich. Sentiment, est. 99, prior 99; Current Conditions, prior 114.4; Expectations, prior 89.1

DB’s Jim Reid concludes the overnight wrap

If you joined the financial market as a graduate around about the third week of September you may have been shocked by yesterday’s trading session. Yes US equities can actually go up as well as just down. After 19 down days out of 24 since September 21st for the S&P500, yesterday saw a strong rally in the US as well as in Europe. Before you think it’s safe to come out of hiding though, after the close tepid earnings from Amazon and Google helped erase around half of the gains and that negative momentum has driven the Asian session. The Nikkei (-1.11%), Hang Seng (-1.44%), Shanghai Comp (-0.58%) and Kospi (-2.52%) are all lower along with most Asian markets. Elsewhere futures on S&P 500 (-0.95%) are pointing towards disappointing start.

Before this, the S&P 500, DOW, and NASDAQ ended +1.87%, +1.63%, and +3.35%, respectively. They are all now back into positive territory for the year, but failed to fully retrace their losses from Wednesday’s selloff. The FANG index gained +5.77% – its largest gain since the NYSE started tracking them in 2014 – and are now higher over the last two days, as strong earnings from Twitter boosted sentiment during the New York session.

European bourses also closed higher yesterday to eclipse their Wednesday losses, with the STOXX 600 up +0.51% and the DAX gaining +1.03%. On both sides of the Atlantic, cyclical (tech, materials, consumer discretionary) sectors outperformed safe haven sectors (utilities, consumer staples). The VIX fell -2.2pts but remains somewhat elevated compared to the recent past at 23.1 (24.2 in Asian trading), while Treasuries resumed their selloff. Ten-year yields rose +1.5bps (again reversed overnight though), while the dollar gained +0.19% to close within 0.15pp of its recent high from August.

Corporate earnings were strong yesterday morning, before Google and Amazon both disappointed after hours. First the good news. Twitter reported earnings beating estimates with revenues up +29% yoy (Q3 revenues at $758mn vs. $703mn expected) and earnings beating expectations by +50% (21c vs. 14c expected), despite monthly users falling by 9mn. Twitter shares climbed +15.47%. Freight shipping firm Union Pacific beat expectations, signalling robust US economic activity, while Comcast, Altria, and ConocoPhillips all posted positive results as well. After US markets closed, Amazon and Google both beat profit expectations, with Amazon posting earnings per share of $5.75 versus consensus expectations for $3.11 (a whopping +85% beat) and Google reporting EPS of $13.06 versus expected $10.45 (a +25% beat). Both stocks reported softer-than-expected revenue growth though, missing consensus expectations by -0.9% for Amazon (first back to back miss for 4 years) and -0.4% for Google, and traded down -7.14% and -3.75%, respectively after hours. Another instance of companies being brutally punished for even marginal top-line misses this earnings season.

The market gyrations this week somewhat overshadowed the ECB meeting yesterday, and even with the excitement of recent days and the ongoing Italian saga, Mr Draghi still managed to successfully turn the ECB meeting and press conference into a dull affair. As Mark Wall described it (see report here ), it was a classic “buying time” performance from Mario Draghi – the ECB was treading water at this press conference. They did acknowledged recent weaker-than-expected data, but the full conclusions and ramifications were left until the new forecasts are available in December. Mark still thinks that, based on the data and communications, the hurdle to extend QE is very high, even though they’ve given themselves until the last minute in December to make a final decision.

Reinvestments were not discussed by the ECB Governing Council, but Draghi added during the presser that he would be surprised if the ECB were to use a different concept than the capital key for carrying out reinvestments. On Italy, Mr. Draghi expressed confidence that the EU and Italian government will reach an agreement on the budget. He also quoted the EC Vice President Dombrovskis, who was present at the ECB meeting, saying that we have to respect fiscal rules but the EU is seeking a dialogue with the Italian government.

Continuing with Italy, Italy’s finance ministry denied the Thursday morning report from Italian daily Il Messaggero that Finance Minister Tria is looking at possible budget adjustments for pensions and if needed, adjustments to citizen’s income following the EU’s rejection of the budget plan. Elsewhere, Italian Deputy Premier Di Maio said that the widening of Italian BTP spreads to record levels was on account of concern that the country might leave Euro and was not a reaction to the Italian budget plan. He expects the spreads to narrow over the next few weeks as the Italian government discusses budget plan with the EU officials. Yields on 10y BTPs fell by -11.3bp yesterday.

Later today, we have the result of the S&P rating deliberations on Italy. With Moody’s downgrading the country to the lowest notch of IG (Baa3) but deciding on a stable outlook, it’s tempting to suggest that S&P (BBB currently) will do the same. However there are differences. S&P upgraded Italy only a year ago and, unlike Moody’s, hasn’t recently had a negative outlook. So although the most likely outcome is a downgrade – and justifiable given the recent developments – they may simply change the outlook to negative and wait to see what happens over the coming weeks.

Staying with Europe, our equity strategist Sebastian Raedler has turned tactically positive on European equities. He highlights that after the 10% correction since late July European equities are priced for a sharp growth slowdown. However, he thinks the slowdown is unlikely to materialize, given that: (a) Euro area PMIs are likely to have troughed, as the lagged impact of EUR strength and the roll-over in the inventory cycle start to fade and (b) China PMIs should have upside over the coming months, as the growth boost from the recent monetary easing and RMB weakness outweighs the drag from US tariffs. These macro projections are consistent with a Stoxx 600 fair-value range of 370 to 385 until mid-Q1 next year, 4% to 8% above current levels. His favourite trades are overweight banks, mining & airlines and underweight pharma and real estate.

Elsewhere, on trade, the WSJ reported, citing officials on both sides, that the US is refusing to resume trade negotiations with China until they comes up with a concrete proposal to address US complaints about forced technology transfers and other economic issues. The Chinese Yuan has been pressured this year amid the trade fracas, and drew some attention yesterday when it touched its weakest level of the year at 6.9669. The Yuan has depreciated all year as Chinese monetary policy diverges from the US, and data released yesterday indicated that, in September, Chinese banks bought dollars at the highest pace since June 2017. This could signal a shift in expectations by onshore investors, who want to move ahead of further currency weakness.

In central bank speak, Fed Vice Chair Richard Clardia and Cleveland Fed President Loretta Mester both downplayed the impact of the recent drop in equity prices on the Fed Policy with Vice Chair Clardia saying that that the fundamentals of the economy are “very, very solid” and Fed’s Mester saying, “while a deeper and more persistent drop in equity markets could dash confidence and lead to a significant pullback in risk-taking and spending, we are far from this scenario.”. Mester also added that she judges growthto be 3% this year and 2.75%-3% in 2019 while highlighting that firms in the Cleveland district are increasingly limited by labor shortages, and she expects unemployment to fall slightly below 3.5% by end-2019. On inflation, she said, “with appropriate adjustments in monetary policy, my outlook is that inflation will remain near 2%.” Both are voting members of the FOMC this year.

US data releases were somewhat soft yesterday, but didn’t change our economists’ expectation for a 3.3% Q3 GDP print today. with preliminary September durable goods orders printing at +0.8% mom (vs. -1.5% mom expected) but excluding transport they came in at +0.1% mom (vs. +0.4% expected). Capital goods orders stood at -0.1% mom (vs. +0.5% mom expected). The latest weekly initial jobless claims came in line with consensus at 215k expected while continuing claims stood at 1,636k (vs. 1,644k expected). September pending home sales came in at +0.5% mom (vs. 0.0% expected) – the first rise in 3 months which helped S&P homebuilders climb +3.71% after a -26.3% fall from the August local peak and the -39.6% fall since the all-time highs in January. Finally the October Kansas City Fed manufacturing index printed at 8 (vs. 14 expected), its weakest print since December 2016.

Other data releases from yesterday included Germany’s October IFO business confidence, which came in at 102.8 (vs. 103.2 expected). This was a slightly less steep drop compared to yesterday’s PMIs, with the expectations index standing at 99.8 (vs. 100.4 expected) and current conditions at 105.9 (vs. 106.0 expected). Spain’s September PPI came at +0.7% mom (vs. revised +0.4% mom in last month). France’s Q3 total jobseekers stood at 3.46mn (vs. 3.44mn in last quarter).

The key highlights for today are the advance Q3 GDP release for the US and the outcome of S&P’s sovereign ratings review for Italy. On the data front, in Europe, we get the ECB’s survey of professional forecasters along with France’s September PPI and October consumer confidence. In the US, we get the final University of Michigan October survey results as well as advance Q3 personal consumption, GDP price index and core PCE. Away from data, the ECB’s Draghi and Coeure will be speaking at different times. In addition, Total will release its earnings.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 4.95 POINTS OR 0.19% //Hang Sang CLOSED DOWN 276.83 POINTS OR 1.11% //The Nikkei closed DOWN 84.13 OR 0.40%/ Australia’s all ordinaires CLOSED DOWN 0.01% /Chinese yuan (ONSHORE) closed DOWN at 6.9457 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 66.31 dollars per barrel for WTI and 76.06 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9457 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9619: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

“The Central Bank Will Intervene”: PBOC Said To Sell Reserves If Yuan Drops Below 7.00

According to the latest data from China’s SAFE, net FX outflows from China picked up to US$21BN in September (vs. US$11BN in August) and the highest since mid-2017 with Goldman noting that “outflow might have increased moderately further in October, but has unlikely reached the level seen in late 2015/early 2016 in our view.”

It may not have reached the furious outflows from the peak of the post-depreciation period, but as Goldman concedes, this risk will rise over time if the authorities continue to resist interest rate differential-driven depreciation pressure.

And, to counter the risk of a return to China’s dramatic outflow phase, Reuters writes this morning that China is likely to resume selling some of its vast $3 trillion currency reserves to stop any precipitous fall through the psychologically important level of 7 yuan per dollar “as it could risk triggering speculation and heavy capital outflows.”

Indeed, as noted in our morning wrap, on Friday the yuan hit a fresh 22-month low of 6.9641 against the dollar. Additionally, earlier in the session the offshore Yuan tumbled as low as 6.9769 after the PBOC fixed the onshore Yuan north of 6.95 and weaker than consensus expected, at which point however Beijing intervened, when at least one big China bank sold the US dollar in the afternoon, prompting the yuan to reverse loss, and triggering stop-loss orders by short-sellers of the yuan.

And with the Yuan just inches away from the key level of 7.00 vs the dollar, dropping 6% against the dollar so far this year, reflecting its slowing economy as well as pressure on exports due to an ongoing tariff war with the United States, Beijing is starting to sweat.

According to Reuters, to counter any potential spike in outflows, “a defense of the yuan at 7 per dollar would be mounted to show investors that the authorities wouldn’t allow a runaway market.”

“If the yuan falls through 7, there could be a rapid depreciation of the exchange rate”, said one policy insider. “In order to avoid such a passive situation, the authorities are likely to step in the market to stabilise the yuan.”

And, according to a second Reuters source, should the Yuan hit 7.00 against the dollar, the PBOC would make a stand, rather than allow any sudden break through a psychologically important level to feed pessimism among investors.

“The central bank will intervene – intervene directly or indirectly. It’s necessary. The central bank has many policy tools. We cannot let the yuan fall past 7, as it would have a psychological impact on people,” the second source said.

That said, China is now juggling two opposing tasks, with Beijing’s priority now to ward off a sharper slowdown in the economy, which grew only 6.5% in the third-quarter, while at the same time it is worried about the impact of the weaker currency on capital outflows.

To address the slowing economy, the central bank has cut reserve requirements for lenders four times this year, and is expected to ease monetary policy further, while on the fiscal side the government has pledged more tax cuts next year to support growth. Those actions, however, have caused the yuan to weaken to just shy of a decade low.

Should the PBOC loosen monetary policy further to depreciate the yuan more in order to bolster sagging economic growth, policymakers will be on guard against spooking markets as the exchange rate nears 7 per dollar, a third Reuters source said.

“We need to loosen monetary policy and should allow the yuan to depreciate to help expand exports, otherwise it will be more difficult,” the source said. “But they (the authorities) will pay special attention to the psychological effect of breaking the 7 per dollar level.”

The good news is that if China does revert to its currency defense posture from 2015/2016, when it burned through $1 trillion in reserves to halt outflows, it still has a sizable cushion, even if as noted last week, they have started to decline again: as a result, traders are closely watching to see if China’s foreign currency reserves fall below $3 trillion, having slipped to $3.087 trillion last month.

Specifically, reserves fell $52.9 billion in the first nine months of 2018 – with 43% of the drawdown happening in September, but the scale of the decline is dwarfed by a record annual drop of $512.7 billion in 2015, showing the authorities have been far less interventionist.

Meanwhile, and as one would expect, capital outflows have picked up as the yuan moves closer to the key 7 per dollar level, with net foreign exchanges sales by China’s commercial banks rose to $17.6 billion in September, the highest in 15 months.

That number will only rise as the Yuan weakens further, sparking the same dynamic that was observed in the months ahead of the Shanghai Accord in early 2016.

Meanwhile, so far this year, Chinese policymakers have been less interventionist on the yuan than they were in 2015, as a weaker currency helps cushion a slowing economy and take some of the sting out of higher U.S. tariffs, even though Beijing has rejected talk that it’s deliberately pushing down the yuan to spur exports.

The good news is that should China engage in a full-blown defense of the Yuan, Trump will be happy as it will mean his crusade to stop Beijing’s “devaluation” of the Yuan will have succeeded. The US president may not be so happy however, if the selling of hundreds of billions of USD-denominated assets leads to an acceleration in the global market rout, in a repeat of what happened in early 2016 when global market tumbled sharply and only coordinated intervention from the world’s central bankers prevented a global bear market.

Trump will most certainly not be happy if a sudden dump of US Treasurys by Beijing results in a sharp spike higher in US interest rates.

And now that China has set an intervention “trigger” bogey, FX traders will quickly test just how serious Beijing truly is. Expect the USDCNH to hit 7.00 in days, if not hours. What happens after could set the tone for risk returns for a long time.

“Drop Everything Else” Saxo Warns It’s Only About CNY 7.00

Authored by John Hardy via Saxo Bank,

Summary: FX Traders sole focus for the moment should be whether the renminbi stands or falls through its floor and USDCNY trades significantly above the 7.00 line in the sand. Already overnight, a very marginal new high in the rate above 6.95 saw widespread unease, but this is only a warm-up for the vicious volatility potential if China allows the CNY to float here…

FX market action remains rather muted relative to the tremors in the equity market of late, but that shouldn’t lead us to believe that conditions in the FX market will remain quiet if this storm continues. That’s particularly because the recent USD strength is pushing very hard on the USDCNY exchange rate and the CNY, or renminbi floor that has been established by China ahead of the 7.00 level is suppressing volatility in currencies as the world watches and waits whether the world’s most important exchange rate will remain contained.

The pressure on this level to give way is enormous as the Chinese currency remains overvalued on a real effective basis and as the country has moved to ease monetary policy to support its deleveraging efforts in recent months. This at a time when the Fed has continued to tighten policy via rate hikes and quantitative tightening (reducing its balance sheet), tightening USD liquidity the world over.

There have been similar if still different situations to the current one in the past: for example, the Swiss National Bank’s franc ceiling vs. the EUR that was abandoned in January of 2015 as the European Central Bank was set to launch its massive QE programme. An earlier example is Japan’s defense of the 115.00 area in USDJPY back in 2003. The franc situation was the worst one for market participants as the exchange rate was completely quiet and provided no inkling of what was about to unfold until an explosion of unprecedented force when the SNB stepped away from defending the franc ceiling. The 2003 JPY episode saw speculative attacks of hundreds of billions of dollars from market participants and nervous price action before Japan’s ministry of finance finally stepped away and allowed USDJPY to fall. Because the market had moved so aggressively and wanted to take profit, the price move after that episode was far smaller and slower.

Chart: USDCNH

The onshore USDCNY rate is the more important anchor here, but the USDCNH is the only way to trade the Chinese currency offshore, and drifts a bit from the USDCNY rate. Still, it is clear that the 7.00 level is the crucial one for whether we are set for a new wave of cross-market volatility if China “devalues” or even simply allows the renminbi to float and for the exchange rate to drift above this level on its own accord due to market pressures.

USDCNH chart.

What happens if the renminbi devalues?

Part of the answer depends on how the price action develops. A chaotic, gap-like move of more than a couple of percent with a continued slide in the wake of the initial move would prove the most disruptive and would up-end risk appetite the world over, kicking weak asset markets when they are already down in what could be a worse version of the August 2015 renminbi devaluation announcement and the ensuing deflationary fears that washed over global markets – especially emerging markets – until early 2016 when the Fed raised the red flag on the USD strength and China stepped into staunch the CNY weakness. The idea is that a weak CNY is deflationary and turns the inflation risk narrative on its head. Global commodity prices would be hit hard as would risky asset prices in general.

What would do well? The general rule in events is that only the most liquid instruments do well – so the US dollar and US Treasuries would likely spike. The weakest currencies in this scenario would likely be the most China-linked exporters like Singapore (SGD), South Korea (KRW), Thailand (THB), Indonesia (IDR), Malaysia (MYR), etc. and even AUD and NZD. But in general, any smaller currency would likely perform poorly. Elsewhere, it is uncertainty whether the JPY would outperform even the USD – positioning would suggest that the JPY could be an even bigger mover than the USD to the upside as Japanese savings sloshing around the world look to deleverage and as the market is still rather short of JPY.

A less severe move in the CNY to the downside could still see a lower volatility version of the above.

Beware of the volatility acceleration

Just overnight we got a sense of how sensitive other markets are to a CNY move. The USDCNY rate was allowed to drift to new highs for the cycle and for the last decade, but still less than 0.18% above the previous day’s highs. This was enough to push AUDUSD almost a full percent lower to new lows for the cycle after the pair had traded in a narrow range in previous days.

This small example would likely be multiplied many times over on a real move in the CNY exchange rate of a mere full percentage point lower or more as the market won’t have a feel immediately for how the exchange rate might be allowed to go. The rising volatility in all asset classes triggers the classic deleveraging that sees correlations across markets rapidly heading to one, aggravating the search for safe havens.