GOLD: $1236.80 UP $23.85 (COMEX TO COMEX CLOSINGS)

Silver: $14.80 UP 52 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1233.25

silver: $14.73

Today was the last day for options expiry for London based/LBMA gold and silver options. The crooks always raid during this week in order to make options on precious metals underwritten by the banks worthless.

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT: 32 NOTICE(S) FOR 3200

Total number of notices filed so far for NOV: 148 for 14,800 OZ (0.4603 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

467 NOTICE(S) FILED TODAY FOR

2,335,000 OZ/

Total number of notices filed so far this month: 926 for 4,630,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6357: down $14

Bitcoin: FINAL EVENING TRADE: $6380 up 8

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HEALTHY 2870 CONTRACTS FROM 208,976 UP TO 211,846 DESPITE YESTERDAY’S 18 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 2384 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2384 CONTRACTS. WITH THE TRANSFER OF 2384 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2384 EFP CONTRACTS TRANSLATES INTO 11.920 MILLION OZ ACCOMPANYING:

1.THE 18 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 6,610,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV:

2384 CONTRACTS (FOR 1 TRADING DAYS TOTAL 2384 CONTRACTS) OR 11.92MILLION OZ: (AVERAGE PER DAY: 2384 CONTRACTS OR 11.92 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 11.92MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.70% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,441.65 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A HUGE INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2903 DESPITE THE HUGE 18 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 2384 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUMONGOUS SIZED: 5257 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2384 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2870 OI COMEX CONTRACTS. AND ALL OF THUS HUGE DEMAND HAPPENED WITH A 18 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.29 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW OVER 6 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 467 NOTICE(S) FOR 2,335,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT OVER 6 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS AND CRIMINAL SIZED 16,570 CONTRACTS UP TO 491,511 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A DROP IN PRICE OF $10.35).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 8996 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 8966 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 491,511. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC RISE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 25,566 CONTRACTS: 16,570 OI CONTRACTS INCREASED AT THE COMEX AND 8996 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 25566 CONTRACTS OR 2,556,000 OZ =79.52TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $10.35.???

YESTERDAY, WE HAD 5311 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 8996 CONTRACTS OR 899,600 OZ OR 27.98 TONNES (1 TRADING DAY AND THUS AVERAGING: 8996 EFP CONTRACTS PER TRADING DAY OR 899,600 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY IN TONNES: 27.98 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 27.98/2550 x 100% TONNES = 1.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,239.49* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 16,570 DESPITE THE LOSS IN PRICING ($10.35) THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8996 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8966 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC RISE OF 25,566 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8966 CONTRACTS MOVE TO LONDON AND 16,570 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 79.52 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A LOSS OF $10.35 IN YESTERDAY’S TRADING AT THE COMEX.??

we had: 32 notice(s) filed upon for 3200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $23.85 TODAY: /

2 TRANSTRACTIONS TODAY

I)A WITHDRAWAL OF .80 TONNES AND THIS WOULD BE TO PAY FOR FEES AND INSURANCE AND STORAGE FEES FOR OCTOBER.

II) A deposit of 6.76 tonnes of gold into the GLD

/GLD INVENTORY 760,82 TONNES

Inventory rests tonight: 760.82 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 54 CENTS TODAY

STRANGE: A BIG CHANGES IN SILVER INVENTORY AT THE SLV:

A WITHDRAWAL OF 1.033 MILLION OZ FROM THE SLV…MAKES SENSE.

/INVENTORY RESTS AT 327.463 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 2870 CONTRACTS from 208,976 UP TO 211,846 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

2903 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2603 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2870 CONTRACTS TO THE 2384 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 5257 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 26.27 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW OVER 6 MILLION OZ STANDING IN NOVEMBER.

RESULT: A STRONG INCREASE IN SILVER OI AT THE COMEX DESPITE THE 18 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZED 2384 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 2.94 POINTS OR 0.13% //Hang Sang CLOSED UP 232.81 POINTS OR 1.06% //The Nikkei closed DOWN 232.81 OR 1.06%/ Australia’s all ordinaires CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed UP at 6.9421 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 65.01 dollars per barrel for WTI and 74.63 for Brent. Stocks in Europe OPENED MIXED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9421 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9386: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Early last night: the yuan tumbles to new lows amid signs of capital outflows. The yuan broke the 6.98 barrier before recovering with huge Chinese central bank intervention

( zerohedge)

ii)This will certainly get on the nerves of Trump: China boosts its Antarctic presence with a planned permanent airbase as they cite strategic needs.

4/EUROPEAN AFFAIRS

i)Our resident expert on German and European affairs comments on what will happen next with respect to Merkel. She is a lame duck and will probably seek the presidency of the European Parliament replacing Juncker. Germany has faced Russia trying to solve the Syrian problem..They want a Syria where the migrants return home to their country.

a must read..

( Tom Luongo)

ii)UK

iii)Cable and British bonds are basically unimpressed as the Bank of England warns of Brexit. The bank England thinks that the economy will heat up in 2019

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SAUDI ARABIA/TURKEY

This is rather gruesome: did the Saudi hitmen dissolve Khashoggi’s body in acid and throwing it down a well on their property at the embassy?

( zerohedge)

ib)Washington Post claims that MbS tells Kushner that Khashoggi was a “dangerous islamist’

ii)RUSSIA

Russia warns that it will act if either the Ukraine or Georgia joins NATO

( Mac Slavo/SHFTPlan.com)

iii)CYPRUS/TURKEY/GREECE/ISRAEL

As we have outline to you on many occasions, the conflict with the huge gas discovery off the Israeli-Cyprus coast is intensifying. Turkey does not recognize Nicosia and they are intent on interceding in the production/discovery of natural gas.

a must read

( GEFIRA)

6. GLOBAL ISSUES

Seems that the Chinese have ditched Vancouver and instead has sought out Singapore to purchase homes. Singapore home prices rise 13% while Vancouver prices drop 11%

( zero hedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

INDIA/RUSSIA

We highlighted this to you yesterday: India has called Trump’s bluff and will pay for Russian S 400 in roubles

( zerohedge)

9. PHYSICAL MARKETS

ii)India is trying to limit its currency loss in dollars by trading in yuan. They are allowing some imports from China to be settled in yuan( Bloomberg/GATA)

iii)I am so glad Craig Hemke notes that the bullions banks switched from long to short at the comex and thus they will continue to the end of time manipulating gold and silver. So please do not pay attention to the “pundits” that our precious metals will explode when the commercials are short. Gold/silver will explode when they run out of physical.

(courtesy Craig Hemke/Sprott Money/GATA

iv)This is interesting: Trump signs an executive order targeting Venezuela’s gold exports to Turkey. Trump realizes that this is the only way that Maduro is getting money into his country

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)Even though the results are a bit disappointing, USA productivity reported its best back to back quarters in over 3 years despite the slowing

( zerohedge)

b)USA manufacturing slumps and the key prices component jumps. Also on the negative side is export orders which slowed dramatically as financial conditions tightened.

( zerohedge)

b)The red hot San Diego house market collapses with its lowest level in 11 years

c)Do not pay much attention to what Trump says. I doubt very much if Xi will relent. Trump is just anxious to see the stock market higher as they enter into the elections

( zerohedge)

iv)SWAMP STORIES

a)Gillum, in a race for the governor’s office in Florida (against Republican DeSantis), project vertitas catches a staffer in racist slur: “it is not for them to know”

(zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 863 notices standing for a loss of 452 contacts. We had 459 notices served upon yesterday so we again gained 7 contracts or an additional 35,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accept a fiat bonus. QUEUE JUMPING IS NOW THE NAME OF THE GAME IN BOTH GOLD AND SILVER AS BOTH METALS ARE SCARCE ON THIS SIDE OF THE POND.

After November, we have a December contract and here we gained 1157 contracts up to 161,161. January saw a gain of 111 contracts up to 1053 contracts. March, the next big delivery month after December saw a gain of 1790 contracts up to 38,791.

i) into CNT: 1,801,914.300 oz

Alarm Bells Ring and Gold Rises In October As Stocks and Property Fall Globally

In our latest video update, we consider the performance of markets in a volatile October. Stock markets globally fell sharply while gold acted as a hedge in all currencies, rising 1.7% in dollars, 4.4% in euro terms and 4.2% in sterling terms.

Stocks Fall Sharply in October

The S&P 500 is just short of a 10% decline from its record September high and remains on pace for the worst month since 2009. It has fallen from a record high of 2930 to 2640. In October alone, the S&P is down 7.3%.

Asian shares as represented by the MSCI Asia Pacific Index have entered a bear market. Many Asian stock indices, including China, fell into a bear market last week amid the global sell-off and China is down a large 30%. Japan and Australia are down nearly 15% from recent peaks

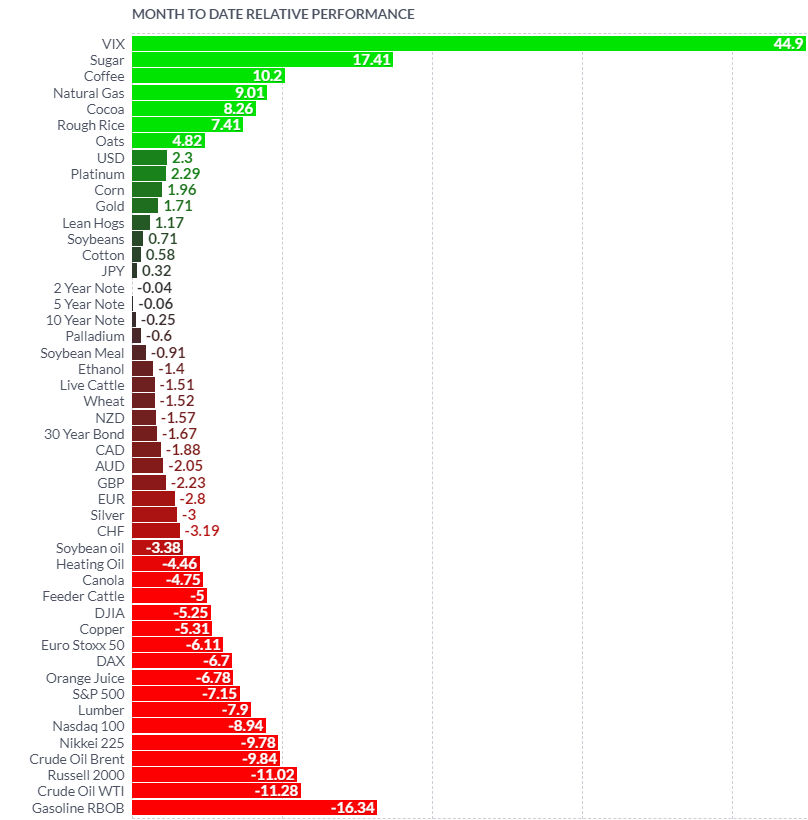

October Market Performance (Finviz.com)

From their 52-week highs, the big tech stocks, the FANGs are down sharply: FB -33.9% AMZN -23.8% NFLX -32.8% GOOGL -18.0% and the FANG index is now in bear market territory.

Is this a correction or the start of a bear market or crash? We are not betting people at GoldCore but if we had to bet, our money is on one of the latter two – a bear market or a crash in the coming months.

Property Falls Continue

House prices in over valued markets continue to fall with Australia being at the vanguard in this regard. House prices are ‘falling by over $1,000 a week’ in Sydney and Melbourne according to Deloitte.

In the UK, the housing market, particularly in London, continues to slow down. UK house asking prices have been slashed and asking prices of almost two-in-five properties for sale in Britain has been reduced by an average of more than £26,000.

In London, 39.5 per cent of property listings have been reduced in price. Kensington and Chelsea registered the biggest drop in cash terms with an average discount of £127,394.

In Ireland, the Dublin housing boom looks vulnerable and weakness has crept into the higher end of the prime Dublin housing market as Brexit jitters deepen.

Conclusion

Many political, economic and financial risks have been ‘bubbling’ away under the surface and were being ignored as risk assets, especially U.S. stocks, kept marching higher.

As financial markets fell in October, these risks came to the fore and became harder for the media to ignore.

Yet still very few have “joined the dots” and considered how the confluence of these many risks will likely create another global financial crisis…

Watch Video Update With Charts Here

News and Commentary

Gold prices recover from 3-week low on softer US dollar (EconomicTimes)

U.S. Mint American Eagle gold coin sales rise 7.3 pct in October (Reuters.com)

Cost of Dublin luxury homes falls for first time since recovery (IrishTimes.com)

How Gold Outshone Bitcoin In October (Forbes.com)

One ominous sign that another recession is looming (MarketWatch.com)

The Same Old COMEX Gold Games (GoldSeek.com)

Ireland in danger of turning boom to bust again (IrishTimes.com)

From the GoldCore Vault (Sept 2018): Gold Largest One Day Price Rise in History (GoldCore.com)

Gold Prices (LBMA AM)

31 Oct: USD 1,217.70, GBP 955.77 & EUR 1,074.25 per ounce

30 Oct: USD 1,220.00, GBP 956.36 & EUR 1,074.33 per ounce

29 Oct: USD 1,230.75, GBP 958.88 & EUR 1,078.38 per ounce

26 Oct: USD 1,236.05, GBP 964.98 & EUR 1,087.23 per ounce

25 Oct: USD 1,232.15, GBP 954.67 & EUR 1,079.36 per ounce

24 Oct: USD 1,231.65, GBP 952.80 & EUR 1,078.68 per ounce

Silver Prices (LBMA)

31 Oct: USD 14.34, GBP 11.23 & EUR 12.64 per ounce

30 Oct: USD 14.43, GBP 11.32 & EUR 12.71 per ounce

29 Oct: USD 14.65, GBP 11.42 & EUR 12.86 per ounce

26 Oct: USD 14.69, GBP 11.48 & EUR 12.94 per ounce

25 Oct: USD 14.74, GBP 11.43 & EUR 12.92 per ounce

24 Oct: USD 14.75, GBP 11.42 & EUR 12.92 per ounce

Recent Market Updates

– Gold Analysts At LBMA See 25% Return To $1,532/oz In 12 months

– Gold Improves Investment, Pension and Central Bank Portfolio’s Risk-Adjusted Returns

– Gold Gains Nearly 1% On Week As Global Stock Markets Fall Sharply

– Dublin Housing Boom Set To Bust?

– Palladium Surges To All Time Record High On Russian Supply Concerns

– Happy Birthday GoldCore

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

– End Of The Financial World?

– Gold Reserves Surge 1,000% In Hungary As It Joins Poland, Russia, China and Other Central Banks Buying Gold

– How Do You Sell Your Digital Gold When the Internet Goes Down?

Dollars declined as India plans to pay in rubles for Russian air-defense system

Submitted by cpowell on Wed, 2018-10-31 14:38. Section: Daily Dispatches

From Russia Today, Moscow

Wednesday, October 31, 2018

The contract between Moscow and New Delhi on supplies of Russian S-400 air defense systems will be settled in rubles, according to Russian Deputy Prime Minister Yuri Borisov.

The move comes as Moscow intensifies recent efforts to make de-dollarization of the Russian economy one of the main pillars of its policy. The Kremlin is looking for an alternative to the U.S. dollar in mutual settlements with international partners. The key point of the plan is to make it more profitable for Russian exporters and importers to use rubles instead of dollars. …

… For the remainder of the report:

https://www.rt.com/business/442716-india-s-400-ruble-settlement/

END

*

India is trying to limit its currency loss in dollars by trading in yuan. They are allowing some imports from China to be settled in yuan

(courtesy Bloomberg/GATA)_

Slump in rupee pushes India to seek trade settlement in yuan

Submitted by cpowell on Wed, 2018-10-31 17:05. Section: Daily Dispatches

By Archana Chaudhary

Bloomberg News

Monday, October 29, 2018

India is considering allowing some imports from China to be settled in yuan, people familiar with the proposal said, as the South Asian nation moves to limit its currency’s loss against the dollar.

The plan would enable direct convertibility between the rupee and yuan and would help cut transaction and hedging costs, the people said, asking not to be identified. The proposal would allow Indian exports of pharmaceuticals, oilseeds, and sugar to China to be settled in rupees, while keeping out trade in high-volume products such as electronics, they said.

India-China trade is mainly settled in U.S. dollars since currencies between the two nations aren’t directly convertible. By allowing Indian importers to pay for Chinese goods in yuan, India would be able to save on dollars to pay for escalating oil import costs in the face of higher crude prices and the rupee’s slump to a record low. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-10-29/rupee-slump-is-said-t.

end

I am so glad Craig Hemke notes that the bullions banks switched from long to short at the comex and thus they will continue to the end of time manipulating gold and silver. So please do not pay attention to the “pundits” that our precious metals will explode when the commercials are short. Gold/silver will explode when they run out of physical.

(courtesy Craig Hemke/Sprott Money/GATA)

Craig Hemke at Sprott Money: Bullion banks want market rigging, not higher prices

Submitted by cpowell on Wed, 2018-10-31 14:59. Section: Daily Dispatches

9:50a CT Wednesday, October 31, 2018

Dear Friend of GATA and Gold:

Writing at Sprott Money, the TF Metals Report’s Craig Hemke notes today that the big commercial traders in the monetary metals futures markets, the bullion banks, have flipped from long to short again on what was only a small move up in prices. This, Hemke argues, shows that the banks envision forever making their money through market manipulation on behalf of central banks rather than through accumulating metal and someday driving prices up.

Hemke concludes: “So, please: The next time you hear someone state that ‘the banks are getting long’ and that price is thus ‘set to explode,’ think otherwise. The banks that operate on the Comex are not your friend, they are not your ally, and they are not interested in profiting on the long side. Instead, their goal is to manipulate and manage price to their own benefit and to the benefit of their central bank masters.

“This has been the case since precious metals futures contracts came into existence in 1975, and it will be the case until this system finally implodes under the sheer weight of its inherent corruption, deception, and fraud.”

Hemke’s analysis is headlined “The Same Old Comex Games” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-same-old-comex-games-craig-hemke-31…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Trump Signs Executive Orders Targeting Venezuela Gold Exports

In the latest move to pressure Venezuela’s president Nicolas Maduro, Donald Trump signed an executive order enabling new sanctions on Venezuela’s gold sector, in a bid to disrupt trade with Turkey which U.S. officials believe is undermining efforts to cripple Venezuela’s economy and force Maduro and members of his government out of office.

“I hereby report that I have issued an Executive Order with respect to Venezuela that takes additional steps with respect to the national emergency declared in Executive Order 13692 of March 8, 2015,” Trump wrote in his letter to the leaders of the House of Representatives and Senate.

According to Bloomberg, the order which was signed by Trump on Wednesday and will be announced at a speech Thursday by National Security Adviser John Bolton, targets those “operating corruptly within the gold sector” and will have a “fairly significant” effect on the country’s economy.

Steve Herman

✔@W7VOA

Executive order signed by @POTUS imposing new sanctions on #Venezuela.

Steve Herman

✔@W7VOA

New US sanctions on #Venezuela target gold exports. pic.twitter.com/U0OsKGYgBU

“The new sanctions will target networks operating within corrupt Venezuelan economic sectors and deny them access to stolen wealth,” Bolton will say, according to an advanced copy of his speech seen by Bloomberg. “Most immediately, the new sanctions will prevent U.S. persons from engaging with actors and networks complicit in corrupt or deceptive transactions in the Venezuelan gold.”

While it was not initially clear what form the sanctions will take, the Treasury Department is will announce details of how the latest sanctions will be implemented later on Thursday. And while the initial effort will focus on Venezuela’s gold sector, whose exports Venezuela allegedly uses to circumvent financial sanctions, Trump’s order gives the State and Treasury departments authority to target additional industries in the future.

Bolton, speaking at Freedom Tower, the symbolic building where the federal government received many refugees fleeing Fidel Castro’s Cuba, framed the plans as part of a broader effort by the U.S. to promote democracy in the Americas.

Venezuela’s gold reserves have declined sharply in the past four years, and according to the IMF were just above 5MM troy oz most recently, down from a recent peak just below 12 million. Much of this decline is due to what some have speculated has been payment for imports in gold, and is what the US is hoping to curb going forward.

The sanctions are likely to have a particular effect on trade with Turkey, with tons of gold sent there annually for refinement and processing. Officials have also voiced concern that some of the gold may be making its way to Iran in violation of sanctions on the Islamic Republic.

Venezuela’s gold industry has been under scrutiny by U.S. officials in recent weeks, with the Treasury Department noting that many mines are run by criminal gangs.

Separately, Bolton will also suggest that the U.S. is preparing sanctions against the government of Nicaragua after the violent political crisis sparked earlier this year by President Daniel Ortega’s announced changes to the country’s social security program. The U.S. wants free and fair elections in the country, the Trump administration official said.

“This Troika of Tyranny, this triangle of terror stretching from Havana to Caracas to Managua, is the cause of immense human suffering, the impetus of enormous regional instability, and the genesis of a sordid cradle of communism in the Western Hemisphere,” Bolton will say. “Under President Trump, the United States is taking direct action against all three regimes to defend the rule of law, liberty, and basic human decency in our region.”

As Bloomberg adds, Bolton’s Thursday speech in Miami is not expected to announce any changes in the U.S. posture toward Central American countries that have recently drawn the ire of Trump after the formation of a pair of migrant caravans joined by thousands of individuals who say they are traveling to seek refugee status in the U.S.

While Trump has repeatedly threatened to cut aid to the caravan’s origin countries – Guatemala, Honduras, and El Salvador – the official said the U.S. has had a productive dialogue with those governments since the formation of the migrant groups.

_________________________________________________________________________________________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9421/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9386 /shanghai bourse CLOSED UP 2.94 POINTS OR 0.13%

. HANG SANG CLOSED UP 436.31 POINTS OR 1.75%

2. Nikkei closed DOWN 232.81 POINTS OR 1.06%

3. Europe stocks OPENED ALL MIXED

/USA dollar index FALLS TO 96/43/Euro RISES TO 1.1403

3b Japan 10 year bond yield: FALLS TO. +.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.79/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65/01 and Brent: 74.65

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.41%/Italian 10 yr bond yield DOWN to 3.35% /SPAIN 10 YR BOND YIELD DOWN TO 1.54%

3j Greek 10 year bond yield FALLS TO : 4.22

3k Gold at $1230.50 silver at:14.58 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 30/100 in roubles/dollar) 65.68

3m oil into the 65 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.79DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0022 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1431 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.41%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.17% early this morning. Thirty year rate at 3.41%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5523

US Futures Jump, Global Markets Rise As Dollar

Tumbles

After a torrid rally in the last two days of a brutal October helped offset some of the losses in the worst month for global equities in more than six years, world markets started off November in a sea of green with gains in Asian and European markets, and S&P futures pointed to a higher open buoyed by upbeat earnings and hope that today’s Apple earnings will ease more “growth” and tech stock concerns, while sterling rallied on reports that Britain and the European Union are close to a post-Brexit deal on financial services, even though a government official has since denied the report.

After October’s drubbing which saw global markets drop 7.5%, their worst month since May 2012, as shares took a battering on a number of factors ranging from trade wars to concerns about the global economy and higher U.S. interest rates, the MSCI All-Country World Index was up 0.3% on the first day of November. The recent rally has helped the S&P rise above its long-term uptrend.

Futures on the S&P 500 jumped after the European open, having traded mixed for much of the overnight session, and rising 0.6% as of 7am ET.

European markets followed a strong start in Asia, with robust company earnings helping the pan-European STOXX 600 index hit a two-week high with miners and carmakers leading the way higher. And while strong results from the likes of ING Groep helped push European banking shares higher, not all the news was positive, with Royal Dutch Shell falling after profit fell short of expectations. At the same time, Britain’s FTSE 100 fell 0.1% as the pound strengthened on a report – since denied – that Britain and the EU are close to a deal that would give financial services firms in the UK continued access to European markets once Brexit happens.

Earlier in the session, Asian shares also posted advances with MSCI’s index of Asia-Pacific shares outside Japan rising 0.7%, adding to modest gains the previous day. The index had fallen 10.2% in October, its worst monthly performance since August 2015.

Earlier in Asia, markets enjoyed Wall Street’s improved mood, and rose for a second day on Wednesday as strong company results and bargain hunting of beaten-down technology and internet favorites lifted spirits, despite an air pocket late in the session which cut the Dow’s 400 point gain in half in a manner of minutes. Hong Kong’s Hang Seng rose 1.5 percent on Thursday and the Shanghai Composite Index climbed 0.2%, closing barely green after stronger gains earlier in the session.

China’s yuan rallied from the weakest level in a decade as the country’s leadership signaled that further stimulus measures are being planned.

Japan’s Nikkei bucked the trend and slipped 1% following two days of big gains.

“What we are seeing is the equity markets trying to rebound after bottoming out. Corporate earnings in the U.S. and Japanese markets have been relatively strong on the whole, which means there are plenty of bargain hunting opportunities,” said Soichiro Monji, senior economist at Daiwa SB Investments in Tokyo.

The big currency mover overnight was the pound, which surged after reports that U.K. and European negotiators have reached a tentative agreement to give U.K. financial services companies access to European markets, however, on Thursday morning this report was denied by a government official, paring some of the gains.

Sterling’s rally nudged the dollar off its recent peak, with the DXY index sliding 0.6% to 96.539. The index had spiked to a 16-month high of 97.20 overnight after the ADP report showed U.S. private sector payrolls increased by the most in eight months in October. The Bloomberg Dollar Spot Index headed for its biggest loss in nearly three weeks as profit taking was the name of the game, given multiple signals the latest move was overdone versus other Group-of-10 currencies.

The Australian dollar and the Kiwi dollar were also sharply higher, rising 1.2% and 1.4% respectively after strong domestic trade data helped offset some of the concerns about slowing growth in China – Australia’s biggest trading partner. “We’ve got a reasonably risk-friendly market, and with the new month we have some dollar selling,” said Kit Juckes, a strategist at Societe Generale.

The Scandinavian currencies – the Norwegian crown and Swedish crown – a proxy for overall risk, also rallied as did the euro, which rose over half a percent to $1.1376 after retreating to $1.1302 on Wednesday, its lowest since mid-August. The single currency has been weighed by less-than-stellar economic news from the euro zone.

In commodities, WTI futures were down 0.86 percent at $64.75 per barrel after its worst month in more than two years, and Brent crude lost 1.13 percent to $74.19 per barrel. The two benchmarks remained on the back foot after falling more than $10 from a four-year peak reached early in October as broader market ructions were seen hurting demand for fuel.

The focus now turns to Apple earnings Thursday, then to the monthly U.S. jobs report Friday. Other expected data highlights include initial jobless claims and manufacturing PMI readings from Markit and ISM. In addition to Apple, DowDuPont and Starbucks are among companies set to report earnings.

Market Snapshot

- S&P 500 futures up 0.2% to 2,717.00

- STOXX Europe 600 up 0.4% to 363.15

- MXAP up 0.2% to 149.84

- MXAPJ up 1% to 476.56

- Nikkei down 1.1% to 21,687.65

- Topix down 0.9% to 1,632.05

- Hang Seng Index up 1.8% to 25,416.00

- Shanghai Composite up 0.1% to 2,606.24

- Sensex up 0.2% to 34,505.43

- Australia S&P/ASX 200 up 0.2% to 5,840.80

- Kospi down 0.3% to 2,024.46

- German 10Y yield rose 1.2 bps to 0.397%

- Euro up 0.5% to $1.1372

- Brent Futures down 0.5% to $74.68/bbl

- Italian 10Y yield fell 4.7 bps to 3.056%

- Spanish 10Y yield fell 0.7 bps to 1.541%

- Brent Futures down 0.5% to $74.68/bbl

- Gold spot up 0.9% to $1,225.61

- U.S. Dollar Index down 0.5% to 96.61

Top Headline News from Bloomberg

Asia equity markets traded mostly higher as the region sustained the momentum from Wall St where stocks continued to pare back some of the losses from its worst monthly performance in 7 years, helped on the day by month-end rebalancing and with sentiment also underpinned by strong jobs data as well as a rally across FAANG stocks post-Facebook earnings beat. ASX 200 (+0.2%) was lifted by early outperformance in the mining sector as BHP shares gained on the announcement of a USD 10.4bln shareholder return program, although upside was capped by indecisiveness across financials amid less than inspiring NAB results and M&A hopes with Macquarie said to be mulling an offer for AMP Capital. Elsewhere, Nikkei 225 (-1.0%) was pressured by the recent currency strength and with much of the focus on earnings, while Shanghai Comp. (+0.6%) and Hang Seng (+1.8%) outperformed following the better than expected Chinese Caixin Manufacturing PMI data and continued supportive efforts by Chinese authorities. Finally, 10yr JGBs were lower with yields higher across the curve after the BoJ tweaked its monthly bond purchases in which it cut the number of occasions it will buy 1-3yr and 3-5yr JGBs to just 4 times from 5 times per month, although firmer demand at the 10yr auction helped stem losses.

Top Asian News

- China’s Yuan Jumps Most in Three Weeks as USD Bulls Take Profit

- Daiwa Finds Partner to Set Up Majority-Owned China Venture

- Hong Kong Reveals Crypto Rules in Push to Tame Wild Market

- Japan Victory Over Mobile Carriers Triggers $34 Billion Rout

- Keyence Boosts Full Year Dividend Forecast, Beats Estimates

European equities trade mostly higher (Eurostoxx 50 +0.8%) after erasing initial losses as sentiment from Asian and Wall Street translated onto the region. The pan-European Stoxx 600 (+0.7%) is fuelled by earnings with the likes of BT (+10.2%), ASM (+15.0%) and Smith & Nephew (+7.0%) all near the top of the index. In terms of sectors, energy names are lagging, in-fitting with the price action in the complex, while telecom names outperform after BT raised their EBITDA guidance. In terms of US earnings on the docket, traders will be keeping an eye on tech-giant Apple who are due to report after market.

Top European News

- BT’s Brighter Profit Outlook Smooths Path for New CEO Jansen

- BOE Rate-Hike Plans Hamstrung by Brexit: Decision Day Guide

- Emirates and FlyDubai Evolve From Odd Couple to Best Buddies

- Novo Slashes 1,300 Jobs as CEO Jorgensen Reshapes Drugmaker

- Abu Dhabi Said in Talks to Form 2 Banks in Three-Way Merger

In FX, all change for the USD and index just a day after month end when the Greenback outperformed due to multiple bullish factors and the DXY finally breached 97.000 to register a fresh ytd peak of 97.201. However, a broad upturn in risk sentiment, portfolio re-positioning and some specific impulses have prompted a marked turnaround with the index back down to 96.510 ahead of a busy agenda before NFP on Friday. NZD/AUD/SEK/NOK – The clear G10 front-runners, or heading the widespread recovery charge vs the Usd, as the Kiwi tops 0.6600 with the aid of favourable cross-winds even though the Aud is testing stops around 0.7160 against its US counterpart and holding above 1.0800 within a 1.0820-75 range after significantly better than expected Aussie trade data overnight. Meanwhile, the Swedish Krona is outpacing its Norwegian peer amidst the aforementioned rebound in risk appetite, and both getting some additional impetus from firmer than forecast manufacturing PMIs, as Eur/Sek retreats through 10.3000 and Eur/Nok tests bids ahead of 9.5000. GBP – A few negative/less bullish developments after Wednesday’s Brexit boost, with Nationwide UK house prices slowing to multi-year lows, the manufacturing PMI considerably below consensus and the Brexit Ministry playing down reports about a deal being done and dusted for domestic financial services firms maintaining access to EU markets post-withdrawal, though progress towards an arrangement along ‘equivalence’ lines seems certain. Hence, Cable is back under 1.2900 and through the 10 DMA (around 1.2873) having rallied over a key Fib (1.2911) to test the first line of offers seen between 1.2920-25, and with stops reputedly above 1.2930 on a break. Next up, BoE super Thursday from noon. JPY – Flat and rangy between 113.00-112.75 in contrast to other majors, but with decent expiry interest from 112.45-50 (1 bn) and better risk sentiment on balance likely to keep the headline pair underpinned. EM – Regional currencies are all benefiting from the general Dollar pull-back, but with the Rand outperforming and testing offers/resistance ahead of 14.5000.

In commodities, WTI (-0.7%) and Brent (-1.0%) are lower with the complex extending on yesterday’s losses over rising supply concerns; and subsequently comments from US President Trump that there is sufficient supply to allow for a significant reduction in purchases from Iran. Analysts from Huatai stating that oil investors are now betting on the potential for a global slowdown. Additionally, Goldman Sachs have reiterated their year-end Brent forecast at USD 80/bbl. Gold (+0.8%) prices have rebounded after hitting a 3-week low in the previous session, largely due to marginal dollar weakness. According to the World Gold Council, the yellow metal’s Q3 global demand is slightly higher year-on-year. Elsewhere, aluminium hit a new two year low, following the weak Chinese PMIs on Wednesday and concerns over the US-Sino trade war’s potential impact on global demand.

Looking at the day ahead, we get the preliminary Q3 nonfarm productivity and unit labour cost releases, the latest weekly initial jobless claims print, final revision to the October manufacturing PMI, September construction spending, ISM manufacturing and then October vehicle sales data. Away from all that the big earnings release today is Apple when we’re due to get numbers at the close, while Royal Dutch Shell, Dow Dupont, Kraft Heinz and Credit Suisse are other notable highlights.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 70.9%

- 8:30am: Nonfarm Productivity, est. 2.1%, prior 2.9%; Unit Labor Costs, est. 1.0%, prior -1.0%

- 8:30am: Initial Jobless Claims, est. 212,000, prior 215,000; Continuing Claims, est. 1.64m, prior 1.64m

- 9:45am: Markit US Manufacturing PMI, est. 55.8, prior 55.9

- 10am: Construction Spending MoM, est. 0.0%, prior 0.1%

- 10am: ISM Manufacturing, est. 59, prior 59.8

- Wards Total Vehicle Sales, est. 17.1m, prior 17.4m

DB’s Jim Reid concludes the overnight wrap

What is it about Octobers? History is quite clear that Octobers are by no means always bad, but when they are bad they have a tendency to be quite bad or at least more volatile!

Normally we publish our MTD and YTD performance review on the first of every month in the EMR but because the past month has seen such big and interesting moves we felt that the review deserved a standalone piece. In particular in the review today we will show that if the year ended now, we’d be set for a record % of assets in our universe in negative territory in dollar terms for a year. This follows last year, when the exact opposite was true. Of the assets we track, we saw the least number in negative territory in dollar terms in 2017. This perhaps highlights a world where we’ve moved from peak QE and everything being expensive to QT over the last 2 years. For this analysis we’ve used the data we collate for our long term study and go back to 1901. So this will be published slightly later this morning along with all the usual stats.

However as an interesting aside, in today’s pdf in the EMR we show the typical daily progression of the S&P 500 through the average year using daily data back to 1927. The average year sees the S&P gain +7.53% on a price basis using this data. However by September 6th, the average year has already seen the index climb +6.05%. Over the course of the next 7 weeks this falls back to +4.70% by October 27th. To be fair, September is worse from a performance basis but October has seen bigger ranges. After these two months are left behind, we then see the usual Santa Claus rally and average gains of nearly +3% into YE on average.

Highlighting the fact that volatility increases we also show the +/- 1 standard deviation of the move over the course of the year. The graph quite clearly shows how the range of outcomes increases dramatically in October before calming down through November and December. Why this happens we still don’t know after over 20 years of observing this trend, but 2018 has further advanced the legend of Octobers being difficult. So click on the link for these graphs and watch out for the performance review slightly later this morning.

There’s something ironic about the fact that despite the S&P 500 just having its worst monthly performance since September 2011, the two-day rally into month end of +2.67% which included a climb of +1.09% yesterday was the biggest since February and the third biggest since June 2016. The two-day climb for the NASDAQ of +3.63% was the biggest since June 2016 (following a +2.01% rally yesterday) although in fairness the index is only now just back to within 10% of its all-time closing high back in August while the NYSE FANG index has rallied +5.54% over the last two days (following a climb of +3.59% yesterday) – the biggest two-day gain since February 2016.

So an impressive turnaround which at least has helped to limit some of the damage done in October. Europe also got swept up in the risk-on tone yesterday with the STOXX 600, DAX, CAC and FTSE 100 climbing +1.71%, +1.42%, +2.31% and +1.31% respectively. Italy unperformed but the FTSE MIB did still nudge up +0.27% and BTPs finished -4.6bps lower in yield following an Il Sole report in the morning which suggested that the Italian government may try to make the case to the EU that the ‘effective’ budget may be closer to 2% for 2019 versus the current 2.4% draft when taking into account slowing growth and lower spending on pensions and the planned citizens income.

Overnight in Asia we’ve seen markets extend on yesterday’s gains with the exception of Japan where the Nikkei (-0.88%) and Topix (-0.69%) have struggled with the telecoms sector down around 8% following news of heavy prices cuts on mobile plans. Away from that however the Hang Seng (+1.84%), Shanghai Comp (+1.13%) and Kospi (+0.47%) are all higher along with S&P 500 futures (+0.30%). A more or less in-line Caixin manufacturing PMI in China (50.1 vs. 50.0 expected) was confirmed this morning however notably we did see PMIs fall below 50 in Taiwan, Malaysia and Thailand overnight for the month of October – all export driven economies and signs therefore of the impact of the trade war on the wider region.

Back to yesterday where EM FX (-0.33%) actually weakened despite the move for equities with the likes of the South African Rand (-1.29%), Mexican Peso (-1.40%) and Brazilian Real (-0.68%) all under pressure. The Turkish Lira (-1.92%) underperformed, as the government announced a new suite of substantial tax cuts. Treasuries nudged up another +2.1bps after the US Treasury Department refunding announcement largely met expectations, while there was a similar move for Bunds (+1.6bps) while WTI Oil fell another -1.31% and edged lower for the third consecutive session. Gold and Silver also fell -0.67% and -1.55% respectively as risk-off dissipated.

There wasn’t really a lot of new news to drive markets yesterday although the tech sector was certainly at the heart of it aided by Facebook’s (+3.81%) earnings post the close on Tuesday. Netflix climbed +5.59%, Alphabet +3.91% and Amazon +4.42%. As you’ll see in the day ahead we’ve got Apple’s earnings later this evening so expect another decent test for the sector. Yesterday we got stronger than expected earnings from 25 out of the 34 companies that reported in the S&P 500 with 25 also beating on revenues.

The narrative around this earnings season has focused on the downward revisions to guidance, but our US equity strategy team argues in a note last night that this earnings season is largely a return to historical averages, and that underlying earnings growth remains strong. Beats are around their historical norms, and headline margins continue to climb to record highs. Buybacks continue their blistering pace as companies continue to return capital to investors, though companies are also paying down debt.

In the US, our economists have updated their various market-based models, and conclude that the risks of a recession over the next 12 months is right around its historical average of 15%. We would have sympathy with this but with QT in full force things could look different in 12 months’ time. Their full note is available here.

Meanwhile, yesterday’s headlines out of the Politburo in China suggesting that more stimulus may be on the way is perhaps helping sentiment overnight, however our economists thought the message from the official press release was subtle. They note that the government did recognise the economic slowdown and promised to take “timely actions”, as widely reported by journalists. But the government also mentioned that (1) the focus of the economy has moved from speed to quality; and more importantly (2) some policies have been released, and their effect will be transmitted to the economy with a lag. Our economists think that these subtle messages suggest likely disagreements in the government.

They highlight that while some may be worried about the downside risk to the economy, others may argue the slowdown is natural and push against aggressive policy easing. You can find more in our colleagues’ report here.

Today we will see the BoE meeting at lunchtime. Neither we nor the market are expecting any policy changes with rising external risks and lack of clarity on a transition deal however our UK economists do expect Governor Carney to talk up market pricing of a rate hike next year on the back of stronger wage and output growth in Q3 which should make him sound marginally hawkish. As far as the inflation report is concerned only marginal tweaks are likely compared to the September forecasts.

Speaking of Brexit, Sterling has had a fairly strong last 36 hours. Yesterday the currency strengthened +0.47% following a Bloomberg report in the late afternoon suggesting that Brexit Minister Raab expects a Brexit deal by November 21. However, upon closer examination, this turned out to be a bit of a misleading headline and the pound quickly retraced the some of the move. The letter being cited was a week old and merely said the Raab would be willing to testify to the Brexit Committee on November 21 which could be a suitable date after a deal was struck. But the details were vaguer than the headline. Overnight however Sterling is up another +0.60% and back above $1.280 following a report in the Times suggesting that the UK and Europe have tentatively agreed to all aspects of a future deal on services which would include the EU guaranteeing UK companies access to markets in Europe as long as financial regulation in the UK remained broadly aligned with Europe. Expect some reaction to that today.

Elsewhere in Europe, the race to replace German Chancellor Merkel as party leader is on, with Friedrich Merz giving a long news conference in Berlin to introduce his candidacy. Merz has been out of parliament since 2009, but he is one of the three frontrunners to succeed Merkel. He did not offer any surprising policy positions in his remarks, focusing his remarks on the need for party unity and for including younger voters and women in the process.

On the data front, preliminary October Euro Area CPI printed in line with expectations at +2.2% headline and +1.1% core, from +2.1% and +0.9%, respectively. French and Italian October CPI both printed 0.1pp lower that forecast, at +2.5% and +1.7% respectively. In Germany, September retail sales rose +0.1% mom, less than the +0.5% expected, and, when combined with downward revisions to prior months and a substantial base effect, equal to a -2.6% yoy decline. So further evidence of third quarter softness in Germany.

Before turning to today’s calendar, it’s worth a look ahead to next week’s major event: the US midterm election. Our US team has updated their analysis of the polls, betting odds, and markets ahead of the vote. It looks probable that the Democrats will take control of the House, while the Republicans are likely to retain control of the Senate. The policy implications are a bit ambiguous, as trade policy – the most important area for markets – is somewhat disconnected from the legislature.

As far as the day ahead is concerned then, this morning in Europe we’ll get October house prices data in the UK followed closely by the UK’s manufacturing PMI. Focus should stay here into lunch with the aforementioned BoE meeting before this afternoon in the US we get the preliminary Q3 nonfarm productivity and unit labour cost releases, the latest weekly initial jobless claims print, final revision to the October manufacturing PMI, September construction spending, ISM manufacturing and then October vehicle sales data. Away from all that the big earnings release today is Apple when we’re due to get numbers at the close, while Royal Dutch Shell, Dow Dupont, Kraft Heinz and Credit Suisse are other notable highlights.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 2.94 POINTS OR 0.13% //Hang Sang CLOSED UP 232.81 POINTS OR 1.06% //The Nikkei closed DOWN 232.81 OR 1.06%/ Australia’s all ordinaires CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed UP at 6.9421 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 65.01 dollars per barrel for WTI and 74.63 for Brent. Stocks in Europe OPENED MIXED //. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9421 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9386: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Early last night: the yuan tumbles to new lows amid signs of capital outflows. The yuan broke the 6.98 barrier before recovering with huge Chinese central bank intervention

(courtesy zerohedge)

Chinese Yuan Tumbles To New Cycle Low Amid Signs Of Capital Outflows

As Chinese markets began to wake, yuan just broke below 6.98/USD for the first time in this downswing,despite PBOC liquidity withdrawals sending money market rates spiking (to squeeze yuan shorts).

This has the distinct smell of capital outflows…

It has been a one way street since Golden Week…

And if former UBS Chief Economist George Magnus is right, any hopes for the G20 meeting between Trump and Xi should be extinguished. In a series of tweets, Magnus warned…

Trump and Xi are supposed to meet at the G20 in Buenos Aires at end month. Will they talk trade? They need to cos Trump has already threatened to subject the other of 50% of imports from China to punitive tariffs. This is how he prepares the ground, telling Fox News:

“I think that we will make a great deal with China and it has to be great, because they’ve drained our country,”.

Designed to turn XJP frostier, be even less inclined to bring something to the table, and more anxious not to be seen to be succumbing to foreign pressure.

So I think, barring something going on in the background, these talks are set up to fail, assuming they happen. The 10% tariff rate is due to go to 25% on 200bn $ of goods on 1 Jan anyway, and we shd probably expect WHY to go for the remaining 250bn $ of imports in new year…

2019 big year for China. centenary of founding of CCP. and rivals Soviet CP’s 72 years in power. Xi’s Chinese Dream of Rejuvenation of Chinese Ppl isn’t just a slogan. Being seen to succumb to Trump’s WH is just not on. Expect both sides to dig in further

Begs question as what China will do next. Xant tit for tat any more, as they have run out of room. @davidjlynch in @washingtonpost reminds us that tourism cd be a target.Targeting US firms also could be cranked up. Yuan depreciation also poss tho v risky at home too …

Much longer discussion and background written up in Red Flags, just out in the US this month….the details change with the news and announcements, but the substance is sadly all too clear.

For now, 7.00 looms heavy on the horizon… and everyone knows the target is there to test PBOC.

6.9895 is the historical low for offshore yuan (Jan 2017)...

China Boosts Antarctic Presence With Planned Permanent Airbase, Cites “Strategic Needs”

China is set to significantly expand its presence in Antarctica as it takes the crucial step of establishing its first permanent airport and large landing strip close to its small research outpost, Zhongshan station. After nearly a decade of planning construction of the airport is set to begin in November, which state media and officials are calling a “permanent” base.

Notably, according to Chinese state-run Xinhua News Agency the airfield will support China’s Antarctic “strategy needs” and protect China’s right to speak on “Antarctic airspace control”.

Ceremonial groundbreaking at new Chinese Antarctic airport, via state mediaThe precise location is near the Zhongshan Research Station, which opened in 1989 and is one of two such research outposts, on the east Antarctic coast near the Larsemann Hills, and the project will be overseen by the official Polar Research Institute of China. Chinese media reports details that the airport is to be constructed at a spot about 28 km away from Zhongshan, with a sizable runway at 1,500m long and 80m wide. It is to primarily serve scientists and staff working in the isolated region.

Ceremonial groundbreaking at new Chinese Antarctic airport, via state mediaThe precise location is near the Zhongshan Research Station, which opened in 1989 and is one of two such research outposts, on the east Antarctic coast near the Larsemann Hills, and the project will be overseen by the official Polar Research Institute of China. Chinese media reports details that the airport is to be constructed at a spot about 28 km away from Zhongshan, with a sizable runway at 1,500m long and 80m wide. It is to primarily serve scientists and staff working in the isolated region.

However, it’s no doubt already gotten the attention of American military planners and China observers as it began making headlines Monday, especially after last month Beijing rolled out with its first domestically built icebreaker, this also following the Chinese government releasing “China’s Arctic Policy” in early 2018 — a white paper outlining how China’s Belt and Road Initiative (BRI) will construct infrastructure projects along the northern Arctic routes, and urged its largest shipping companies to conduct trial voyages through the frigid waters. Could Antarctic exploration, on the polar opposite side the globe, be part of a broader vision of a “Polar Silk Road” which aims to find “alternate” routes and spheres of influence to bypass Washington’s choke points in the South China Sea and the Indian Ocean (something which the Arctic route attempts to do)?

According to Chinese state sources, last February researchers laid the foundation of the country’s fifth research facility, which is to be built in the far south of the continent. Construction for the new projects are to begin when the 35th Antarctic expedition departs on November 2 with building to commence later that month. The air field is expected to take two years to complete.

via the South China Morning PostMeanwhile a new Australian media report confirms China is currently outspending other nations in Antarctica, even as Australia has lately tried to shore up its claim to 42% of Antarctica.

via the South China Morning PostMeanwhile a new Australian media report confirms China is currently outspending other nations in Antarctica, even as Australia has lately tried to shore up its claim to 42% of Antarctica.

One analyst cited in the report, Australian National University professor Donald Rothwell, commented, “I’m not necessarily surprised by China’s increased interest and if in the future China is seeking to position itself to play and even greater role in Antarctic affairs and to influence the direction of Antarctic governance then obviously the bigger its presence the more weight its view might have in terms of how those future discussions go,” according to news.com.au.

Some Australian officials fear that their country’s influence is waning as China muscles in. In the most alarming and perhaps sensationalized section of the report it suggests the possibility of “militarization” of the Antarctic region.

According to news.com.au the military and geopolitical implications are as follows:

Last month, former head of the Australian Antarctic Division, Tony Press, told the Australian government it must step up its diplomatic efforts in Antarctic affairs to hold together the current treaty system and avoid militarisation.

At the same time, writing in The Australian, Prof Anne Marie Brady warned that China’s installation of GPS satellite systems on the Australian Antarctic Territory could be used to guide strike weapons and help Beijing develop better technology than the US in coming years.

Specifically, Professor Brady warned: “The US, Russia, and China’s use of their Antarctic ground stations to control offensive weapons systems and relay signals intelligence — all while conducting legitimate scientific activity — has the potential to shift the strategic balance that has maintained peace in the Asia-Pacific for nearly 70 years,” according to the report.

end

Well this did not last long: The USA now accuses Chinese State Owned Company of sealing Micron trade secrets

(courtesy zerohedge)

US Accuses Chinese State-Owned Company Of Stealing Micron Trade Secrets

So much for all that US-China trade truce talk.

Just hours after a presidential tweet expressing optimism about US-China trade talks helped save US stocks from turning red on the first trading day of the month (with an assist from Chinese President Xi Jinping, who later told Chinese media that he would be “willing” to meet with Trump at the G-20 summit later this month), the DOJ has unveiled an indictment filed in California against a Chinese state-owned company and three Taiwanese nationals for allegedly stealing trade secrets from Micron Technologies.

- *U.S. SAYS CHINA STATE-OWNED CO. STOLE MICRON TRADE SECRETS

- *U.S. CRIMINAL COMPLAINT ALSO NAMES THREE TAIWAN NATIONALS

- *UNITED MICROELECTRONICS, FUJIAN JINHUA INDICTED IN U.S.

Allegations about the alleged theft of chip designs from Micron were first detailed in legal documents filed in the US and Taiwan, which were cited by the New York Times in an investigation published back in June detailing China’s efforts to acquire by either legitimate – or, failing that, illegitimate – means trade secrets that the Chinese government saw as vital to its Made in China 2025 initiative.

Micron has been the subject of punitive measures, including an investigation in China, one of its biggest foreign markets, since spurning a $23 billion takeover offer from a Chinese company. Fujian Jinhua Integrated Circuit Company, one of the companies facing indictment, was accused by the NYT of being behind the elaborate technology theft, while Taiwan-based UMC reportedly helped Fujian carry out the heist, claims that both companies denied. The indictment will almost certainly escalate tensions between the US and China, which has been enraged by President Trump’s demand that the Chinese government roll back its support for initiatives tied to Made in China 2025 as part of any trade-dispute settlement.

The indictment also follows remarks from National Security Advisor John Bolton who said earlier Thursday that the US must withdraw from the INF arms-control treaty to counter the aggression of Russia and China, which he accused of ‘taking advantage’ of the treaty.

4.EUROPEAN AFFAIRS

Our resident expert on German and European affairs comments on what will happen next with respect to Merkel. She is a lame duck and will probably seek the presidency of the European Parliament replacing Juncker. Germany has faced Russia trying to solve the Syrian problem..They want a Syria where the migrants return home to their country.

a must read..

(courtesy Tom Luongo)

Lame Duck Merkel Has Only Her Legacy On Her

Mind

German Chancellor Angela Merkel has stepped down as the leader of the Christian Democratic Union, the party she has led for nearly two decades. Yesterday’s election in Hesse, normally a CDU/SPD stronghold was abysmal for them.

She had to do something to quell the revolt brewing against her.

Merkel knew going in what the polls were showing. Unlike American and British polls, it seems the German ones are mostly accurate with pre-election polls coming close to matching the final results.

So, knowing what was coming for her and in the spirit of trying to maintain power for as long as possible Merkel has been moving away from her staunch positions on unlimited immigration and being in lock-step with the U.S. on Russia.

She’s having to walk a tightrope on these two issues as the turmoil in U.S. political circles is pulling her in, effectively, opposite directions.

The globalist Davos Crowd she works for wants the destruction of European culture and individual national sovereignty ground into a paste and power consolidated under the rubric of the European Union.

They also want Russia brought to heel.

On the other hand, President Trump is pushing Merkel on policy on Russia and Ukraine that furthers the image that she is simply a stooge of U.S. geopolitical ambitions. Don’t ever forget that Germany is, for all intents and purposes, an occupied country. So, what the U.S. military establishment wants, Merkel must provide.

So, if she rejects that role and the chaos U.S. policy engenders, particularly Syria, she’s undermining the flow of migrants into Europe.

This is why it was so significant that she and French President Emmanuel Macron joined this weekend’s summit with Russian President Vladimir Putin and Turkish President Recep Tayyip Erdogan in Istanbul.

It ended with an agreement on Syria’s future that lies in direct conflict with the U.S.’s goals of the past seven years.

It was an admission that Assad has prevailed in Syria and the plan to atomize it into yet another failed state has itself failed. Merkel has traded ‘Assad must go’ for ‘no more refugees.’

To President Trump’s credit he then piggy-backed on that statement announcing that the U.S. would be pulling out of Syria very soon now. And that tells me that he is still coordinating in some way with Putin and other world leaders on the direction of his foreign policy in spite of his opposition.

But the key point from the Istanbul statement was that Syria’s rebuilding be prioritized to reverse the flow of migrants so Syrians can go home. While Gilbert Doctorow is unconvinced by France’s position here, I think Merkel has to be focused on assisting Putin in achieving his goal of returning Syria to Syrians.

Because, this is both a political necessity for Merkel as well as her trying to burnish her crumbling political throne to maintain power.

The question is will Germans believe and/or forgive her enough for her to stay in power through her now stated ‘retirement’ from politics in 2021?

I don’t think so and it’s obvious Davos Crowd boy-toy Macron is working overtime to salvage what he can for them as Merkel continues to face up to the political realities across Europe, which is that populism is a natural reaction to these insane policies.

Merkel’s job of consolidating power under the EU is unfinished. They don’t have financial integration. The Grand Army of the EU is still not a popular idea. The euro-zone is a disaster waiting to happen and its internal inconsistencies are adding fuel to an already pretty hot political fire.

On this front, EU integration, she and Macron are on the same page. Because ‘domestically’ from an EU perspective, Brexit still has to be dealt with and the showdown with the Italians is only just beginning.

But Merkel, further weakened by another disastrous state election, isn’t strong enough to fend off her emboldened Italian and British opposition (and I’m not talking about The Gypsum Lady, Theresa May here).

And Macron should stop looking in the mirror long enough to see he’s standing on a quicksand made of blasting powder.

This points to the next major election for Europe, that of the European Parliament in May where all of Merkel’s opposition are focused on wresting control of that body and removing Jean-Claude Juncker or his hand-picked replacement (Merkel herself?) from power.

The obvious transition for Merkel is from German Chancellor to European Commission President. She steps down as Chancellor in May after the EPP wins a majority then to take Juncker’s job.

I’m sure that’s been the plan all along. This way she can continue the work she started without having to face the political backlash at home.

But, again, how close is Germany to snap elections if there is another migrant attack and Chemnitz-like demonstrations. You can only go to the ‘Nazi’ well so many times, even in Germany.

There comes a point where people will have simply had enough and their anger isn’t born of being intolerant but angry at having been betrayed by political leadership which doesn’t speak for them and imported crime, chaos and violence to their homes.

And the puppet German media will not be able to contain the story. The EU’s speech rules will not contain people who want to speak. The clamp down on hate speech, pioneered by Merkel herself is a reaction to the growing tide against her.

And guess what? She can’t stop it.