I WILL UPDATE SPROTT DATA AND THE GLD/SLV DATA LATER TONIGHT.

GOLD: $1224.90 DOWN $5.80 (COMEX TO COMEX CLOSINGS)

Silver: $14.51 DOWN 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1226.50

silver: $14.53

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT: 5 NOTICE(S) FOR 500

Total number of notices filed so far for NOV: 190 for 19000 OZ (0.5909 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

150 NOTICE(S) FILED TODAY FOR

750,000 OZ/

Total number of notices filed so far this month: 1085 for 5,425,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6418: up $44

Bitcoin: FINAL EVENING TRADE: $6460 down 24

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY 1927 CONTRACTS FROM 211,291 UP TO 213,218 DESPITE YESTERDAY’S 9 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 903 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 903 CONTRACTS. WITH THE TRANSFER OF 903 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2903 EFP CONTRACTS TRANSLATES INTO 4.515 MILLION OZ ACCOMPANYING:

1.THE 9 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 6,865,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV:

9589 CONTRACTS (FOR 4 TRADING DAYS TOTAL 9589 CONTRACTS) OR 47.945 MILLION OZ: (AVERAGE PER DAY: 2397 CONTRACTS OR 11.986 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 47.945MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.84% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,477.67 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1927 DESPITE THE 9 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 903 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2830 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 903 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1927 OI COMEX CONTRACTS. AND ALL OF THUS GOOD DEMAND HAPPENED WITH A 9 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.65 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW WELL OVER 6.8 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 150 NOTICE(S) FOR 750,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT OVER 6 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A TINY SIZE OF 476 CONTRACTS UP TO 490,694 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A DROP IN PRICE OF $1.05).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1322 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 1322 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 490,694. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN FAIR SIZED RISE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1798 CONTRACTS: 476 OI CONTRACTS INCREASED AT THE COMEX AND 1322 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 1798 CONTRACTS OR 179,800 OZ = 5.59 TONNES. AND ALL OF THIS GOOD DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.05.

YESTERDAY, WE HAD 4638 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 27,641 CONTRACTS OR 2,764,100 OZ OR 85,97 TONNES (4 TRADING DAYS AND THUS AVERAGING: 6910 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY IN TONNES: 85.97 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 85.97/2550 x 100% TONNES = 3.37% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,295.94* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED INCREASE IN OI AT THE COMEX OF 476 DESPITE THE LOSS IN PRICING ($5.05) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 1322 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 1322 EFP CONTRACTS ISSUED, WE HAD A FAIR RISE OF 1798 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

1322 CONTRACTS MOVE TO LONDON AND 476 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 5.59 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A LOSS OF $1.05 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.80 TODAY: /

A SMALL CHANGES IN GOLD INVENTORY AT THE GLD

A WITHDRAWAL OF .59 TONNESS

/GLD INVENTORY 756.70 TONNES

Inventory rests tonight: 756.70 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS TODAY

NO CHANGES AT THE SLV:

/INVENTORY RESTS AT 326.005 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 1656 CONTRACTS from 211,291 UP TO 212,947 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

903 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 903 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1927 CONTRACTS TO THE 903 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 2830 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 12.795 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW

6.8 MILLION OZ STANDING IN NOVEMBER.

RESULT: A GOOD INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZED 903 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 6.08 POINTS OR 0.23% //Hang Sang CLOSED UP 186.57 POINTS OR 0.72% //The Nikkei closed UP 248.76 OR 1.44%/ Australia’s all ordinaires CLOSED UP 0.91% /Chinese yuan (ONSHORE) closed UP at 6.9146 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 62.73 dollars per barrel for WTI and 72.54 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.9146 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL UP ON THE DOLLAR AT 6.9146: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)ITALY

The following is a very important commentary from our European experts GEFIRA. Here they state that the Italian people must understand that their country is at war

witn Brussels. The EU wants a surplus budget which is impossible with a declining population. The authors outline what will be Italy’s next step

( GEFIRA)

ii)Salvini cuts Migrant allowance from 35 euros to 19 euros per day which will save them 400 million euros. Italy has a declining population and they are in need of workers to take the place of Italians who do not want children. Salvini wants to entice Italians to have more children

iii)Fitch warns the Italian government that it may not survive as the coalition member views are quite diverse( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN

Iran shuts off oil tanker tracking system so the uSA will not know where they oil is going

( zerohedge)

ii)Iran is preparing for along siege

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Perennial loser Barrick now in talks trying to merge their Nevada operations together( Reuters)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

b)Housing is such an important component in GDP calculations for the USA. Mish Shedlock gives a detailed look at the housing market where housing is now the least affordable in a decade

( Mishtalk/Mish Shedlock)

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 425 notices standing for a gain of 26 contacts. We had 3 notices served upon yesterday so we gained a good 29 contracts or an additional 145,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts. QUEUE JUMPING DID RETURN TO THE COMEX ARENA AS THIS PHENOMENON (IN SILVER) HAS BEEN THE NAME OF THE GAME FOR OVER 19 MONTHS.

After November, we have a December contract and here we lost 2077 contracts down to 150,679. January saw a LOSS of 44 contracts DOWN to 978 contracts. March, the next big delivery month after December saw a gain of 3191 contracts up to 49,401.

Venezuela Seeks To Repatriate $550 Million Of Gold From London

Venezuela Seeks Return Of Gold Worth $550 Million From Bank of England

CARACAS (Reuters) – Venezuela is seeking to repatriate about $550 million in gold bars from the Bank of England because of fears it could be caught up in international sanctions on the country, two sources with direct knowledge of the effort told Reuters.

Source: ZeroHedge

Venezuela’s hard currency holdings have dwindled as existing U.S. financial sanctions have effectively blocked President Nicolas Maduro’s government from borrowing on international markets.

The Trump administration on Thursday issued a new round of sanctions banning U.S. citizens from having dealings with anyone involved in “corrupt or deceptive” gold sales from Venezuela, as part of efforts to boost pressure on Maduro.

Maduro’s government is seeking to bring 14 tonnes of gold held in the Bank of England back to Venezuela, according to two public officials with direct knowledge of the operation, who asked not to be identified.

The Bank of England has sought to clarify what Venezuela wants to do with the gold, one of the officials said.

Venezuela’s central bank did not respond to a request for comment. The Bank of England declined to comment.

The plan has been held up for nearly two months due to difficulty in obtaining insurance for the shipment, needed to move a large gold cargo, one of the officials said.

“They are still trying to find insurance coverage, because the costs are high,” the official said.

Venezuela is in its fifth year of recession with annual inflation at more than 400,000 percent, leading to increased incidence of hunger and disease and spurring an exodus of some 2 million citizens.

Maduro says his government is victim of an “economic war” led by the opposition and fueled by Washington’s sanctions. His critics blame the country’s state-led economic model, stringent exchange controls and nationalizations of private companies.

Losing the gold would be a significant blow to the country’s finances. Lack of hard currency can create shortages of basic goods ranging from staple foods to drugs and automobile parts.

The amount is equivalent to five times the total hard currency that Venezuela has sold in 2018 via hard currency auctions that are carried out under the country’s 15-year-old exchange control system, according figures compiled by local consultancy Sintesis Financiera.

The government has promised to auction 2 billion euros in foreign exchange over an unspecified time frame, without saying where it plans to obtain those funds.

But even if Venezuela manages to repatriate the gold, the new U.S. sanctions could make selling it to raise hard currency difficult.

“If the government wants to carry out operations with the gold that it plans to bring, it would have to be done with allied countries because of the sanctions,” said Tamara Herrera, an economist with Sintesis Financiera.

Venezuela has been exporting gold to Turkey in the last year, a business that has grown as Maduro has built up ties with Turkish President Tayyip Erdogan.

Selling the gold directly from the Bank of England to a foreign buyer would be logistically easier than shipping it, but could also risk running foul of sanctions.

Venezuela for decades stored gold that makes up its central bank reserves in foreign bank vaults, which is common among developing countries.

The country’s late socialist leader Hugo Chavez, citing the need for Venezuela to have physical control of central bank assets, in 2011 repatriated around 160 tonnes of gold from banks in the United States and Europe to the central bank in Caracas.

But some of Venezuela’s gold remained in the Bank of England. Starting in 2014, Venezuela used this gold for “swap” operations in which global banks lent Venezuela several billion dollars with the gold as collateral.

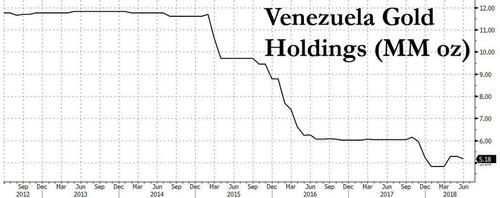

Venezuelan central bank statistics show the central bank’s gold holdings by June this year had dropped to 160 tonnes from 364 tonnes in 2014, as some of the swap agreements expired without Venezuela returning the funds – leaving the gold in the hands of the banks (Goldman Sachs being one of the banks).

In 2017, such swap agreements became difficult due to U.S. sanctions, which blocked U.S. financial institutions from bankrolling any new financing operations.

Full article via Reuters here

News and Commentary

Exclusive: Venezuela seeks to repatriate $550 million of gold from Britain (Reuters.com)

Gold prices steady, eyes on U.S. midterm elections (Reuters.com )

Gold prices post a modest decline as dollar weakens ahead of midterm vote (MarketWatch.com)

Energy stocks lift S&P, Dow; Apple drags (Reuters.com)

Mining bitcoin uses more energy than mining gold (PRI.org)

Source: ZeroHedge

Maduro Scrambles To Repatriate Venezuela’s Gold After Trump Crackdown (ZeroHedge.com)

Rate Reversal Ahead, Bullish For Gold (Youtube.com)

Economic Brake Lights – Mauldin (GoldSeek.com)

SWOT Analysis: Election Spotting – Holmes (GoldSeek.com)

Is The Long Anticipated Crash Among Us – Moran (Youtube.com)

05 Nov: USD 1,231.60, GBP 946.61 & EUR 1,081.96 per ounce

02 Nov: USD 1,235.50, GBP 948.00 & EUR 1,079.83 per ounce

01 Nov: USD 1,223.25, GBP 950.47 & EUR 1,075.85 per ounce

31 Oct: USD 1,217.70, GBP 955.77 & EUR 1,074.25 per ounce

30 Oct: USD 1,220.00, GBP 956.36 & EUR 1,074.33 per ounce

29 Oct: USD 1,230.75, GBP 958.88 & EUR 1,078.38 per ounce

Silver Prices (LBMA)

05 Nov: USD 14.74, GBP 11.33 & EUR 12.96 per ounce

02 Nov: USD 14.82, GBP 11.38 & EUR 12.95 per ounce

01 Nov: USD 14.45, GBP 11.19 & EUR 12.68 per ounce

31 Oct: USD 14.34, GBP 11.23 & EUR 12.64 per ounce

30 Oct: USD 14.43, GBP 11.32 & EUR 12.71 per ounce

29 Oct: USD 14.65, GBP 11.42 & EUR 12.86 per ounce

Recent Market Updates

– Big Short’s Eisman Is Shorting Two U.K. Banks on Brexit

– “Red October” Highlights Importance of Rebalancing Portfolios and Gold’s “Very Positive” Outlook

– Alarm Bells Ring and Gold Rises In October As Stocks and Property Fall Globally

– Gold Analysts At LBMA See 25% Return To $1,532/oz In 12 months

– Gold Improves Investment, Pension and Central Bank Portfolio’s Risk-Adjusted Returns

– Gold Gains Nearly 1% On Week As Global Stock Markets Fall Sharply

– Dublin Housing Boom Set To Bust?

– Palladium Surges To All Time Record High On Russian Supply Concerns

– Happy Birthday GoldCore

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

Venezuela Seeks Return Of Gold Worth $550 Million From Bank of England

CARACAS (Reuters) – Venezuela is seeking to repatriate about $550 million in gold bars from the Bank of England because of fears it could be caught up in international sanctions on the country, two sources with direct knowledge of the effort told Reuters.

Source: ZeroHedge

Venezuela’s hard currency holdings have dwindled as existing U.S. financial sanctions have effectively blocked President Nicolas Maduro’s government from borrowing on international markets.

The Trump administration on Thursday issued a new round of sanctions banning U.S. citizens from having dealings with anyone involved in “corrupt or deceptive” gold sales from Venezuela, as part of efforts to boost pressure on Maduro.

Maduro’s government is seeking to bring 14 tonnes of gold held in the Bank of England back to Venezuela, according to two public officials with direct knowledge of the operation, who asked not to be identified.

The Bank of England has sought to clarify what Venezuela wants to do with the gold, one of the officials said.

Venezuela’s central bank did not respond to a request for comment. The Bank of England declined to comment.

The plan has been held up for nearly two months due to difficulty in obtaining insurance for the shipment, needed to move a large gold cargo, one of the officials said.

“They are still trying to find insurance coverage, because the costs are high,” the official said.

Venezuela is in its fifth year of recession with annual inflation at more than 400,000 percent, leading to increased incidence of hunger and disease and spurring an exodus of some 2 million citizens.

Maduro says his government is victim of an “economic war” led by the opposition and fueled by Washington’s sanctions. His critics blame the country’s state-led economic model, stringent exchange controls and nationalizations of private companies.

Losing the gold would be a significant blow to the country’s finances. Lack of hard currency can create shortages of basic goods ranging from staple foods to drugs and automobile parts.

The amount is equivalent to five times the total hard currency that Venezuela has sold in 2018 via hard currency auctions that are carried out under the country’s 15-year-old exchange control system, according figures compiled by local consultancy Sintesis Financiera.

The government has promised to auction 2 billion euros in foreign exchange over an unspecified time frame, without saying where it plans to obtain those funds.

But even if Venezuela manages to repatriate the gold, the new U.S. sanctions could make selling it to raise hard currency difficult.

“If the government wants to carry out operations with the gold that it plans to bring, it would have to be done with allied countries because of the sanctions,” said Tamara Herrera, an economist with Sintesis Financiera.

Venezuela has been exporting gold to Turkey in the last year, a business that has grown as Maduro has built up ties with Turkish President Tayyip Erdogan.

Selling the gold directly from the Bank of England to a foreign buyer would be logistically easier than shipping it, but could also risk running foul of sanctions.

Venezuela for decades stored gold that makes up its central bank reserves in foreign bank vaults, which is common among developing countries.

The country’s late socialist leader Hugo Chavez, citing the need for Venezuela to have physical control of central bank assets, in 2011 repatriated around 160 tonnes of gold from banks in the United States and Europe to the central bank in Caracas.

But some of Venezuela’s gold remained in the Bank of England. Starting in 2014, Venezuela used this gold for “swap” operations in which global banks lent Venezuela several billion dollars with the gold as collateral.

Venezuelan central bank statistics show the central bank’s gold holdings by June this year had dropped to 160 tonnes from 364 tonnes in 2014, as some of the swap agreements expired without Venezuela returning the funds – leaving the gold in the hands of the banks (Goldman Sachs being one of the banks).

In 2017, such swap agreements became difficult due to U.S. sanctions, which blocked U.S. financial institutions from bankrolling any new financing operations.

Full article via Reuters here

News and Commentary

Exclusive: Venezuela seeks to repatriate $550 million of gold from Britain (Reuters.com)

Gold prices steady, eyes on U.S. midterm elections (Reuters.com )

Gold prices post a modest decline as dollar weakens ahead of midterm vote (MarketWatch.com)

Energy stocks lift S&P, Dow; Apple drags (Reuters.com)

Mining bitcoin uses more energy than mining gold (PRI.org)

Source: ZeroHedge

Maduro Scrambles To Repatriate Venezuela’s Gold After Trump Crackdown (ZeroHedge.com)

Rate Reversal Ahead, Bullish For Gold (Youtube.com)

Economic Brake Lights – Mauldin (GoldSeek.com)

SWOT Analysis: Election Spotting – Holmes (GoldSeek.com)

Is The Long Anticipated Crash Among Us – Moran (Youtube.com)

05 Nov: USD 1,231.60, GBP 946.61 & EUR 1,081.96 per ounce

02 Nov: USD 1,235.50, GBP 948.00 & EUR 1,079.83 per ounce

01 Nov: USD 1,223.25, GBP 950.47 & EUR 1,075.85 per ounce

31 Oct: USD 1,217.70, GBP 955.77 & EUR 1,074.25 per ounce

30 Oct: USD 1,220.00, GBP 956.36 & EUR 1,074.33 per ounce

29 Oct: USD 1,230.75, GBP 958.88 & EUR 1,078.38 per ounce

Silver Prices (LBMA)

05 Nov: USD 14.74, GBP 11.33 & EUR 12.96 per ounce

02 Nov: USD 14.82, GBP 11.38 & EUR 12.95 per ounce

01 Nov: USD 14.45, GBP 11.19 & EUR 12.68 per ounce

31 Oct: USD 14.34, GBP 11.23 & EUR 12.64 per ounce

30 Oct: USD 14.43, GBP 11.32 & EUR 12.71 per ounce

29 Oct: USD 14.65, GBP 11.42 & EUR 12.86 per ounce

Recent Market Updates

– Big Short’s Eisman Is Shorting Two U.K. Banks on Brexit

– “Red October” Highlights Importance of Rebalancing Portfolios and Gold’s “Very Positive” Outlook

– Alarm Bells Ring and Gold Rises In October As Stocks and Property Fall Globally

– Gold Analysts At LBMA See 25% Return To $1,532/oz In 12 months

– Gold Improves Investment, Pension and Central Bank Portfolio’s Risk-Adjusted Returns

– Gold Gains Nearly 1% On Week As Global Stock Markets Fall Sharply

– Dublin Housing Boom Set To Bust?

– Palladium Surges To All Time Record High On Russian Supply Concerns

– Happy Birthday GoldCore

– “IMF Warning Highlights Gold’s Importance As A Diversification and Happy Birthday GoldCore”

Venezuela seeks to repatriate $550 million of gold from Britain, sources tell Reuters

Submitted by cpowell on Mon, 2018-11-05 14:24. Section: Daily Dispatches

By Mayela Armas

Reuters

Monday, November 5, 2018

CARACAS — Venezuela is seeking to repatriate about $550 million in gold bars from the Bank of England because of fears it could be caught up in international sanctions on the country, two sources with direct knowledge of the effort told Reuters.

Venezuela’s hard currency holdings have dwindled as existing U.S. financial sanctions have effectively blocked President Nicolas Maduro’s government from borrowing on international markets.

The Trump administration on Thursday issued a new round of sanctions banning U.S. citizens from having dealings with anyone involved in ‘corrupt or deceptive’ gold sales from Venezuela, as part of efforts to boost pressure on Maduro.

Maduro’s government is seeking to bring 14 tonnes of gold held in the Bank of England back to Venezuela, according to two public officials with direct knowledge of the operation, who asked not to be identified. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-gold-exclusive/exclusive-ve…

* * *

end

Perennial loser Barrick now in talks trying to merge their Nevada operations together

(courtesy Reuters)_

Barrick in talks with Newmont to combine Nevada gold operations, sources tell Reuters

Submitted by cpowell on Mon, 2018-11-05 15:42. Section: Daily Dispatches

By Zandi Shabalalaand Clara Denina

Reuters

Monday, November 5, 2018

LONDON — Barrick Gold Corp, which is being reorganized by Barrick’s $6.1 billion takeover of Randgold Resources, is in talks with Newmont Mining to combine their Nevada gold mining operations, sources told Reuters.

Last month’s tie-up between Barrick and Africa-focused Randgold Resources revived speculation about a joint venture between Newmont and Barrick in Nevada, something the two mining firms explored in 2014 without reaching a deal.

“They have been trying to negotiate for years but Newmont couldn’t agree with Barrick, one source said. “Now that you have a new management team, it’s certain they revived those talks.” …

… For the remainder of the report:

https://www.reuters.com/article/us-barrick-gold-newmont-mining/barrick-i…

END

Refiner Republic Metals Files for Bankruptcy

By Michelle Graff

michelle.graff@nationaljeweler.com

NOVEMBER 6, 2018

New York—One of the country’s largest precious metal refiners filed for bankruptcy Friday following the discovery of “inventory discrepancies” in its books and records this past summer.

Republic Metals Corp., which has its main office in New York and processes metals at a facility in Miami, filed Chapter 11 in U.S. Bankruptcy Court for the Southern District of New York.

The company is looking for a buyer, and on Oct. 29, Swiss refiner Valcambi issued a press release stating that it had “reached an understanding” to acquire Republic Metals Corp. and the companies were “working through the logistics of the planned integration.”

Jennifer Mercer, a spokeswoman for Republic Metals, clarified Monday that no deal had been finalized but that talks with Valcambi are ongoing. A Valcambi spokeswoman did not respond to request for comment.

Founded in 1980 by Richard Rubin, Republic owns Republic Metals Refining Corp. and Republic Carbon Company LLC, which processes spent carbon from metals mines.

In a declaration filed alongside the company’s Chapter 11 petition, Chief Restructuring Officer Scott Avila outlined the events that led up to the decision, starting in April when the company “discovered a significant discrepancy in its inventory accounting” while preparing its full year 2018 and first quarter 2018 financials.

Republic Metals retained accounting firm EisnerAmper LLP, which confirmed that there were discrepancies in both the company’s books and records, though Mercer said she could not elaborate on the scope or nature of the discrepancies.

In late June, the company got together with its senior lenders to ask the banks to give it “breathing room” while it worked to sort out the inventory issues and develop a plan to either rectify them or restructure, the declaration states.

But the banks began to press the company a few weeks later, serving it with termination, default and demand notices July 10.

Around the same time, Republic Metals began looking for a buyer, contacting a “major, strategic metals refiner about [a] possible acquisition”—meaning Valcambi—and bringing Avila on board as CRO.

According to the declaration, the banks agreed to hold off to give Republic Metals a chance to work out a deal with the potential buyer. But as the months passed and no deal was forthcoming, the banks cut off negotiations and one lender, ICBC Standard Bank, suspended the refiner’s ability to pay customers via credit on the London metals exchange, its most common form of payment.

Avila, the company’s board and its creditors opted to file Chapter 11 on Nov. 2, as the refiner has “limited cash” and “the inability to trade metals or deliver refined goods,” the declaration states.

If a deal with Valcambi isn’t reached and the refiner cannot find another buyer, then it will be forced to liquidate its assets and inventory.

Republic Metals Refining Corp. has between 1,000 and 5,000 creditors, with assets totaling $174.8 million but liabilities topping $265 million, according to court papers.

Its largest secured lenders include Mitsubishi International Corp., the New York branch of Coöperatieve Rabobank U.A. and Bank Leumi USA, which is among the lenders that have pulled out of the diamond and jewelry trade in recent years.

The company’s No. 1 unsecured creditor is Parsippany, New Jersey-based Laurelton Sourcing LLC, a subsidiary of Tiffany & Co. According to the Chapter 11 petition, Republic owes Laurelton more than $17 million.

Other trade debts include nearly $10 million owed to Chihuahua, Mexico-headquartered mining company Coeur Mexicana SA de CV; more than $5 million owed to Premier Gold Mines Ltd. in Thunder Bay, Ontario, Canada; and Geib Refining Corp. in Warwick, Rhode Island, which is owed more than $3 million, court records show.

-END-

_________________________________________________________________________________________________

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.146/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9146 /shanghai bourse CLOSED DOWN 6.08 POINTS OR 0,23%

. HANG SANG CLOSED UP 186.57 POINTS OR 0.72%

2. Nikkei closed UP 248.76 POINTS OR 1.44%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 96.27/Euro RISES TO 1.1417

3b Japan 10 year bond yield: RISES TO. +.13/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.16/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.73 and Brent: 72.54

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.43%/Italian 10 yr bond yield UP to 3.35% /SPAIN 10 YR BOND YIELD UP TO 1.58%

3j Greek 10 year bond yield RISES TO : 4.33

3k Gold at $1234.85 silver at:14.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 66.22

3m oil into the 62 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.16DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0033 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1457 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.42%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.19% early this morning. Thirty year rate at 3.42%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3389

Here Come The Political Fireworks: Traders Hunker Down Ahead Of “Shock” Outcome

Ahead of the most important day for US politics in years, global markets have hunkered down, coiling in anticipation or dipping cautiously into the red, as traders braced for midterm elections in the United States while anticipating a “shock outcome” with 2016 still fresh in everyone’s head.

European markets turned lower alongside American futures while Asian shares were fractionally in the green. The pound fluctuated amid Brexit hopes and despair, while Treasury yields dipped and the dollar rose.

Asian trading started off well thanks to the momentum from Monday’s strong US session (excluding Apple) with MSCI’s index of Asia-Pacific shares ex-Japan rising 0.4%. Japan and Hong Kong helped Asia overcome another Chinese wobble, where the Shanghai initially slumped but managed to recover most losses, although Europe slipped into the red early on as investors punished several corporate earnings misses and pre-U.S. midterms nerves took hold.

Apple suppliers such as Taiwan’s Hon Hai Precision Industry were hit by a report that Apple had told its smartphone assemblers to halt plans for additional production lines dedicated to the iPhone XR. The report had also driven Apple shares 2.8% lower in U.S. trade.

Europe’s Stoxx Europe 600 lost traction after a positive start and technology, retail and automakers were among the sectors dragging the index lower. That said, nobody was making any big statements and volumes were more than a third below the 30-day average. “European stock markets are a little in the red as political uncertainty hangs over investor sentiment,” CMC Market analyst David Madden wrote pointing to tensions between Italy and the EU over the country’s budget, China-U.S. trade spat.

S&P futures were rangebound, drifting in a 15 point range from session highs shortly before the European open to session lows as US traders walked in.

For once traders will forget interest rates, earnings and trade war, and will focus entirely on the looming US midterm elections which are seen as the first major referendum on the policies of President Donald Trump, including his sweeping tax cuts and hostile trade policies. Polls point to his Republican party losing control of the House of Representatives which could curb some of his policymaking power. The GOP is expected to retain control of the Senate. Meanwhile, investors have one eye on the U.K., where Theresa May is redoubling efforts to reach a Brexit deal.

For today’s session, it will be all about polling and the results to come over the next 24 hours, so be on the look out for headline risks as exit poll results start to trickle in later in the day. Polls over in the East Coast are now open and that will be followed by the rest of the states in the coming hours.

Having been burned by the outcome of the 2016 presidential election, traders are especially wary: “It is definitely not the time to buy the dip,” said London & Capital’s CIO Pau Morilla-Giner. “Everything that could go well for U.S. consumers in the last couple of years has gone well, but now the tide is turning… At the moment you are running out of drivers of growth in the U.S.”

But while volumes were muted, nerves were distinctly absent from market indicators: the Cboe Skew index – also known as the “black swan” index – hovered near its 2.5 year low hit on Friday, indicating demand for OTM options remains tepid.

“Unlike the U.S. Presidential election or the U.K.’s Brexit referendum, the upcoming U.S. (midterm) elections are not a binary event,” said Yasuo Sakuma, chief investment officer at Libra Investments. “So it’s unlikely to send stocks significantly in one direction, apart from initial quick reactions.”

Back to markets, Italian and Spanish stocks weakened as updated PMI figures confirmed euro zone business growth fell to a two-year low last month due to rising trade tensions. The future output index caused even more concern as it fell to a near four-year low of 60.5 from 62.1.

“Euro zone companies reported a disappointing start to the fourth quarter,” said Chris Williamson, chief business economist at IHS Markit which compiles the data.

Most European government bonds were mixed and range-bound, with Bunds grinding higher, eventually breaching yesterday’s best levels to test 160. In Italy, BTPs reversed early gains after eurozone finance ministers called on Rome to change its budget at a meeting on Monday. The Bund/BTP sprad widened 8bp as Italian officials hold their ground but signal an willingness for “constructive dialogue.”

Political risks also dominated the currency market, with the Bloomberg dollar index confined to 1 point of 1,200 while the pound erased gains before another key Brexit meeting for Theresa May’s administration. The euro hovered around the $1.14 handle as German macro data lent support. Treasuries were little changed in rather thin trading volumes before a 10-year note auction.

The Aussie led gains among G-10 peers in delayed response to RBA’s painting of a slightly more upbeat picture of the economy in the statement accompanying its decision to leave rates unchanged Tuesday. The yen was little changed after earlier falling to its weakest level in a month as advancing Japanese stocks damped demand for haven assets. Emerging-market currencies consolidated.

Gold was little changed but in oil markets crude prices were near multi-month lows after the United States allowed eight countries to continue buying oil from Iran temporarily, easing the likelihood of a sharp supply drop. U.S. West Texas Intermediate crude futures slipped 0.3% to $62.89 a barrel, after hitting a seven-month low of $62.52 on Monday.

Elsewhere, a flurry of earnings are expected, including from Lilly and Ralph Lauren.

US Event Calendar

- S&P 500 futures down 0.2% to 2,735.50

- STOXX Europe 600 down 0.1% to 363.10

- MXAP up 0.8% to 152.88

- MXAPJ up 0.5% to 487.96

- Nikkei up 1.1% to 22,147.75

- Topix up 1.2% to 1,659.35

- Hang Seng Index up 0.7% to 26,120.96

- Shanghai Composite down 0.2% to 2,659.36

- Sensex up 0.2% to 35,025.03

- Australia S&P/ASX 200 up 1% to 5,875.18

- Kospi up 0.6% to 2,089.62

- German 10Y yield fell 0.2 bps to 0.424%

- Euro up 0.07% to $1.1415

- Brent Futures down 0.3% to $72.93/bbl

- Italian 10Y yield rose 0.5 bps to 2.956%

- Spanish 10Y yield rose 1.2 bps to 1.578%

- Gold spot up 0.3% to $1,234.90

- U.S. Dollar Index up 0.01% to 96.29

Top Overnight News from Bloomberg

- U.K. Cabinet ministers expect to be locked in a room to study the latest options for a Brexit deal in strict secrecy on Tuesday as Theresa May redoubles efforts to get a deal this month, according to people familiar with the matter

- German Chancellor Angela Merkel took aim at populist rhetoric that portrays the media as enemies, saying it’s unacceptable to attack critical journalism in a democracy

- China’s vice president said Beijing remained ready to discuss a trade solution with the U.S., and urged changes in global governance to address a surge in populism and rapid technological advances

- President Donald Trump said he is “probably not” meeting Vladimir Putin in Paris this weekend but does expect to meet the Russian president at a summit in Argentina at the end of November

- U.S. gave a stark warning to companies around the world: Evading sanctions on Iran will hurt

- German factory orders unexpectedly rose for a second month in September in a sign that Europe’s largest economy is poised to regain growth momentum toward the end of the year; orders gained 0.3% from the previous month, compared with economists’ predictions for a 0.5% decline

- Italy signaled it’s not ready to budge on its controversial budget even as euro-area finance ministers called on it to prepare revised spending plans that comply with the bloc’s rules, in a sign that the standoff between Brussels and Rome is set to escalate in the coming weeks

- Mitsubishi UFJ Kokusai Asset Management Co. has been piling into Treasuries on expectations that the U.S. yield curve will flatten as the economy gradually slows. It has done so by selling bonds in euro-zone nations, with the exception of Spain

Asian equity markets were mixed as weakness in China clouded over the mostly positive lead from US where the DJIA and S&P 500 closed higher with the latter led by strength in energy names, although the Nasdaq declined amid continued Apple woes after reports the tech giant cancelled a production boost for the budget iPhone XR due to slowing demand. ASX 200 (+1.0%) and Nikkei 225 (+1.1%) traded higher with Australia led also by the energy sector leading as it mirrored the outperformance seen stateside, while the Japanese benchmark benefitted from recent currency weakness and rose back above the 22000 level. Elsewhere, Hang Seng (+0.7%) and Shanghai Comp. (-0.2%) were subdued amid ongoing trade uncertainty and after the PBoC skipped open market operations again, while notable weakness was seen in casino stocks which pulled back from recent gains. Finally, 10yr JGBs were lacklustre after weakness seen in T-notes and with demand subdued by the strength in Japanese stocks.

Top Asian News

- PBOC Adviser: Capital Outflow Pressure Smaller Than 2 Years Ago

- Goldman Names Binnion, Wang as Asia ex-Japan ECM Co-heads: Memo

- Camera Maker Mulls Taking a Note From Taylor Swift on Trade War

- Malaysia Probes More Deals by Ex-Goldman Partner Leissner

Major European indices are mostly in the red (Eurostoxx 50 -0.5%) with underperformance in Spain’s IBEX as the index is dragged lower by heavyweight financial and telecom names. Meanwhile the SMI (Unch) outperforms with the index lifted by Adecco (+3.7%) post-earnings. In terms of sectors, industrials are benefitting from the lower base metal prices, while telecom names lag. Moving onto individual equities, Zalando (-6.0%) is the worst performing stock following their earnings, with Morrisons (-5.0%) also lower on the back of their number. IWG (+7.0%) are out in front following optimistic earnings and conformation of their guidance, while FTSE heavyweight Associated British Food (+2.5%) in the green after the company said they expect an increase in retail profit after reporting their earnings.

Top European News

- German Factory Orders Unexpectedly Rise as Domestic Demand Gains

- Rosneft Uses Record Cash Flow to Pay Off Debt in Volatile Market

- Tria Says Italy Still Has Disagreements With the Commission

- Brexit Endgame Lifts Pound’s Volatility as Euro Stays Subdued

- France Flexible on Date of Digital Tax Implementation: Le Maire

In FX, it is a different day, but familiar feel or trend in G10 land, as Sterling rivals the Antipodean Dollars for major honours. Cable continues ride high on a wave of Brexit deal optimism amidst more reports of an EU offer on the Irish border, and the latest proposal under the guise of an ‘Independent Mechanism’ that would allow the UK options to terminate the temporary customs arrangement. Cable has extended gains to test and briefly eclipse resistance around 1.3080, while Eur/Gbp has slipped further below 0.8750 to just a handful of pips from reported stops at 0.8720 and Gbp/Jpy breached its 200 DMA and 148.00 before losing some momentum. Meanwhile, the Aud has been boosted by relatively upbeat RBA commentary overnight following its monetary policy meeting with 2018 and 2019 growth seen stronger than previously and a tighter labour market expected to lift wages. Hence, Aud/Usd appears firmer above the 0.7200 handle that has been tough to overcome, and eyeing 0.7250 next, while Aud/Nzd has bounced from near 1.0800 to touch 1.0850, as Nzd/Usd remains capped ahead of 0.6700. EUR/CHF/JPY/CAD – All narrowly mixed vs the Greenback, which is trading cautiously ahead of today’s US mid-term elections, with the DXY hovering just above 96.200, as the single currency runs into offers around 1.1425 and ongoing Italian-EU budget issues that are preventing a more concerted attempt on technical resistance around 1.1456-60. Meanwhile, the traditional currency safe-havens, Chf and Jpy remain rangebound between 1.0055-35 and 113.20-45 with the latter looking at a key Fib (circa 113.34) on a closing basis for technical direction. Elsewhere, the Loonie has lost some of its BoC impetus as oil prices sag again, but could derive more independent pointers from Canadian building permits later. Usd/Cad now back above 1.3100 and climbing. EM – Some loss of momentum after Monday’s broad outperformance vs the Usd, but the Try did derive more support earlier to trade within a whisker of 5.3000 on hawkish rhetoric from the CBRT that sounded confident about hitting its inflation target via tight monetary policy, even though Turkish CPI accelerated further above in October.

In commodities, WTI (-0.4%) and Brent (-0.5%) are both lower as details of the US waivers on Iranian oil emerge. So far, China is allowed to buy around 360K BPD of Iranian oil for 180 days, with source reports noting that conditions require the disclosures of counter-parties and settlement methods. Elsewhere, India is allowed to purchase of up 300k BPD of oil, while South Korea was granted a 200k BPD oil waiver. Additionally, comments from US President Trump that he wants to impose the sanctions gradually to prevent shocks to the market, may have contributed to the price decrease. Traders will be eyeing the weekly API crude inventories released later today as a fresh catalyst for prices. Gold (+0.2%) has been gradually rising throughout the session as the yellow metal detaches itself from USD influence to act as a safe haven, meanwhile copper is lower and moving in tandem to the risk tone. Separately, aluminium associations from the US, Canada and Mexico have urged their governments to agree a deal which eliminates US aluminium tariffs from Canada and Mexico without the imposition of import quotas.

US Event Calendar

- 10am: JOLTS Job Openings, est. 7,085, prior 7,136

DB’s Jim Reid concludes the overnight wrap

The main focus today will of course centre on the US midterm elections. According to the betting website predictit.org, the base case of the Democrats taking the House but the Republicans retaining the Senate is around 60% likely. The odds that the Republicans hold both chambers is around 30%, and the odds that the Democrats take both chambers is around 10%. We should know tonight, with the first polls closing at 6pm EST/11pm GMT, though the first major bellwether states to close will be Virginia and Florida at 7pm EST/midnight GMT. The former has some marginal House races in the outskirts of Washington, DC, while the latter has a close Senate race. As the night progresses, we could know the final results by 10pm EST/3am GMT when the last marginal Senate races finish and enough House races are in the books that we should have a firm idea.

If things are still close, it could come down to California and its seven competitive House races, which could, in a worst-case scenario, take days or weeks to finalize as mail-in ballots are counted.

Ahead of the US going to the polls, the most impressive part of the last 24 hours was how well the S&P 500 held up given the renewed weakness in tech. Whilst the S&P closed +0.56%, the NYSE FANG index was down -1.35 % (but off intraday lows of -2.77%). The NASDAQ also fell -0.38% with Apple at that forefront following a drop of -2.84% (-9.28% over 2 days and -13.13% from peak on October 3) after Japan’s Nikkei media outlet reported that the tech behemoth had told assemblers to halt new production capacity of the new iPhone XR until there is more assurance on demand. That move for the NASDAQ was the first move of less than +/-1% since October 23rd (eight business days) and breaks the longest such stretch since December 2008. That came after the STOXX 600 had closed -0.16% in Europe following an intraday range of just 0.53% which was the smallest since the end of September.

This morning in Asia, markets are largely flat to down with the exception of Japan. The Shanghai Comp (-1.05%) and Hang Seng (-0.23%) are lower while the Kospi (+0.02%) is flat and the Nikkei (+1.14%) is up. Elsewhere, futures on the S&P 500 (-0.05%) are flat. In overnight news, the US and China are set to hold diplomatic and security talks in Washington this coming Friday, ahead of the upcoming meeting between their respective presidents on the side lines of the G20 meeting. Elsewhere, the PBoC’s adviser Jun Ma has said that the Chinese yuan hitting the key psychological level of 7 or not “isn’t that crucial” while adding that the capital outflow pressure in China is smaller compared to two years ago. As a reminder DB expect 7.40 next year.

Bond markets were similarly unexciting yesterday. 10y Treasuries ended the session -1.3bps lower at 3.199% and Bunds -0.1bps lower at 0.426%. BTPs ended more or less flat but did pare an early move higher in yield of around +7bps with the rally supported by a downplaying of a Politico report by the EU Commission about the Commission proposing financial sanctions on Italy as soon as November 21st. Finance Minister Tria was quoted as saying in yesterday’s Eurogroup meeting of the Euro-area Finance Ministers that Italy remains committed to reducing its debt ratio and hopes to reach a compromise with the EC while adding that Italy is currently not in the process of changing its budget, but that it was still committed to pursuing a dialogue with the EC.

Meanwhile the data in the US was actually a marginal positive with the ISM non-manufacturing coming in ahead of expectations at 60.3 (vs. 59.0 expected) – albeit down -1.3pts from September’s record reading but still the second-highest since 2005. New orders held relatively steady at 61.5 although employment did nudge down to 59.7 from 62.4 the month prior. That is however more or less in line with the three-month average. The prices subcomponent actually fell nearly 10pts to 61.7 but still remains at elevated levels. The associated text did however, highlight that “tariffs are beginning to impact business” and that construction firms in particular had asked suppliers to hold pricing for six months. Shortly before this the final services PMI in the US was revised up +0.2pts to 54.8.

Staying with the US, it was interesting to see the chart in our US economists’ “Fed Watcher” note yesterday which suggested that wages (in this case total private average hourly earnings) started accelerating as unemployment approached and breached 4% earlier this year. A tipping point of sorts and this fits in with the trend observed in the 1960s when wages also accelerated when the unemployment rate dropped below 4%. This 1960s comparison was something DB research has highlighted in numerous publications over the last year or so.

In other news, where there were no shortage of headlines yesterday was here in the UK with Brexit newsflow once again peaking in the morning after the weekend noise. Reuters broke with the news quoting ITV political editor Robert Peston as saying that the UK government had settled on a no deal Brexit outcome as the most probable in the event of no deal within the next week. As DB’s Oliver Harvey noted, a December agreement is still possible as is an option of extending the Article 50 timeframe (granted by a short duration) so it’s worth taking this headline with a pinch of salt. Further headlines on Brexit included the Sun as saying that no deal is likely this week and that dates for a possible EU summit had been pushed to the 27th and 28th of November – making a parliamentary vote in the first week of December more likely. There were also reports that Brexit Secretary Dominic Raab might resign but this was later downplayed. Meanwhile, late yesterday night, The Times reported that the EU is preparing to offer the UK PM May an independent mechanism by which Britain could end a temporary customs arrangement with the EU. If true, this could help overcome the key sticking point in Brexit talks. However The Times has been a source of numerous headlines of late and it’s not clear that they all have substance. Sterling closed up +0.56 at $1.304 last night and traded at $1.305 this morning. There is a UK cabinet meeting today to discuss Brexit but it doesn’t feel we’re quite ready yet for a breakthrough. Nevertheless it looks like we are inching towards a deal and then the UK parliamentary fun and games will begin.

On the data front, the UK’s services and composite PMIs both softened, following last week’s drop in the manufacturing PMI. The services metric printed at 52.2 versus expectations for 53.3 and down from 53.9 in September, while the composite index came in at 52.1 versus expected 53.4 and down from 54.1. The composite index is now at its lowest level since the Brexit referendum. Separately, Turkish CPI printed at 25.2% yoy, its highest level since 2003, though the monthon- month figure softened to 2.67% from 6.30% in September. The Turkish lira rallied +2.22% to 5.314, its strongest level since early August.

The US’s sanctions on Iran took effect today, though they issued waivers to eight countries (China, India, Italy, South Korea, Turkey, Taiwan, Greece, and Japan) which will allow them to continue importing Iranian crude oil. The waivers will cover around 1.3 million barrels per day, which would equate to small additional cuts from current export levels and would be consistent with the 2012-2015 experience. There was no indication of how long the waivers would remain in effect, and Brent crude oil traded somewhat listlessly to close -0.11%.

As far as the day ahead is concerned, needless to say the US midterms will dominate. Before that, this morning in Europe the early data release is September factory orders numbers out of Germany. Shortly after that the focus turns to the remaining October services and composite PMIs. No change in the composite reading of 52.7 for the Euro Area is expected. Later this morning we’ll get September PPI for the Euro Area before we get the September JOLTS job openings data in the US. Away from that we’re due to hear from the ECB’s Praet, Coeure and Lautenschlaeger at various stages this morning.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 6.08 POINTS OR 0.23% //Hang Sang CLOSED UP 186.57 POINTS OR 0.72% //The Nikkei closed UP 248.76 OR 1.44%/ Australia’s all ordinaires CLOSED UP 0.91% /Chinese yuan (ONSHORE) closed UP at 6.9146 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 62.73 dollars per barrel for WTI and 72.54 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED WELL DOWN AT 6.9146 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL UP ON THE DOLLAR AT 6.9146: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

ITALY

The following is a very important commentary from our European experts GEFIRA. Here they state that the Italian people must understand that their country is at war

witn Brussels. The EU wants a surplus budget which is impossible with a declining population. The authors outline what will be Italy’s next step

(courtesy GEFIRA)

GEFIRA: The Italian People Must Understand That Their Country Is At War

The conflict between the European Union and Italy is a full-blown financial war. Euro countries cannot print their own money and for that reason they cannot have an endless deficit. Countries within the eurozone have to live within their means or else, without the intervention of the ECB, they will go bankrupt. Nobody knows the consequences of an Italian default and debt restructuring, but it can lead to the end of the euro.

To make the euro sustainable, the European financial elites want the Italians to reduce their spending and turn a budget deficit into a budget surplus. However, due to the country’s shrinking population the Italian budget deficit — as we have argued many times – can only increase. The European commission rejects the Italian budget because Rome wants to increase its debt far beyond the limit allowed by the ECB.

“This is the first Italian budget that the EU doesn’t like,” wrote Deputy Prime Minister Luigi Di Maio on Facebook.

“No surprise: This is the first Italian budget written in Rome and not in Brussels!”

Matteo Salvini added:

“This (the rejection of the Italian budget plan by the EU) doesn’t change anything.”.

“They’re not attacking a government but a people. These are things that will anger Italians even more,” he said.

The country has entered a demographic winter and sustainable economic growth is simply impossible, at least for the foreseeable future. As is the case with the whole of Europe, the continent needs a plan to support an ageing and declining population. As if not aware of it, the Brussels-Frankfurt establishment only wants Italy to stick to their austerity program, i.e. decrease public spending and do away with the current Italian administration, which refuses to comply.

To force Prime Minister Luigi Di Maio and Matteo Salvini out of office, the European Union will go to any lengths to destroy the Italian banking sector the way they did it in Greece and Cyprus. In 2015 Greece shut down its banks, ordering them to stay closed for six days, and its central bank imposed restrictions to prevent money from fleeing out of the country.

Jeroen Dijsselbloem, former head of the euro group, suggests that the financial markets should try to lower the value of the Italian bonds. A lower bond value will erode the capital of the Italian banks and make them insolvent. Mario Draghi, head of the ECB, warned last week that a recent sell-off of Italian government bonds was set to dent the capital of Italy’s banks which own about 375 billion euros ($426.30 billion) worth of that paper. The remarks of the Central European Bank’s chairman were carefully prepared as another deliberate attack on the Italian financial system. It is highly unusual for central bankers to warn the bank under their supervision against insolvency, at the same time trying to provoke a preemptive bank run.

“I find it improper for the person in charge of the financial stability in Europe to sound the alarm, even if softened later on, over the health of the Italian lenders since Italy is one of the countries under his banking supervision,” an Italian lawmaker rightly said.

The Italian rulers know that they are under assault and are contemplating how to shield the banks from the European banking authorities. Rome has to come up with a national strategy to preserve its banking system even if this is against the European rules. Matteo Salvini, leader of the Northern League, met with his counterpart from the Five Star Movement, Luigi Di Maio, to discuss the condition of the Italian economy, budget and banks, a spokesman for Salvini said.

“No banks will be in difficulty,” Salvini said.

The two parties, which are running the country in a coalition government, are working in sync, he said. Premier Giuseppe Conte asked government agencies to prepare options to help the lenders if the decline in the value of their holdings of government debt requires them to recapitalize the banks, Corriere della Sera reported.

The leadership in Rome will not leave it to Brussels or Frankfurt bureaucrats to decide whether Italian banks are insolvent or not. In theory, every sovereign government can declare a bank solvent by the stroke of a pen. The Italian authorities can refuse to close their banks and force them to stay in business. Unlike Greece, Italy has a trade balance surplus and the country does not depend on a foreign supply of money to pay for its imports. Keeping insolvent banks open will further undermine the reliability of the euro as a common currency. To put even more pressure on the Italian government, Karsten Wendorff, Member of the Advisory Board of the German federal banks, suggested confiscating private Italian properties to make good for the Italian public debt obligations.

“Instead of a European fund that buys Italian government bonds and that is ultimately backed by European taxpayers, a national fund should be created,” Wendorff wrote in the Frankfurter Allgemeine Zeitung Saturday.

Such a fund would be financed by “national solidarity bonds” that Italian households would be obliged to purchase, for example, to the tune of 20 per cent of their net wealth. At such a rate “almost half of the Italian government debt could be converted into solidarity bonds.” If the plan were to be implemented, it would mean that Italian house owners would be forced to pay 20% of their asset value to foreign banks. The plan is first and foremost a warning to the leadership in Rome against violating their budget rules. Germany is willing to confiscate whatever it is entitled to.

The general public is unaware of the seriousness of the situation. Both Salvini and Matteo – as well as the Italian people – should realize that they are at war with the European establishment which ultimately intends to remove them from power. To win this battle they need unconditional support from the state security apparatus and the Italian people. The confrontation between Rome on the other hand and Brussels and Frankfurt on the other, however, will not break out before the European Parliament elections.

Salvini To Cut Migrant Allowance In Half, Saving €400 Million

Italy’s populist interior minister, and de facto most important politician, Matteo Salvini has continued his assault on what he views as Italy’s biggest problem, and is expected to drastically cut the daily allowance for migrants in Italy, claiming the country could see save up to €400 million by 2019.

According to Il Giornale, the proposal would slash by almost half the current daily allowance of €35 per day to only €19 per day, which would be one of the lowest rates in western Europe. And, according to the Interior Ministry, the cuts would lead to a saving of €400 million in 2019, rising to €500 million in 2020 and €600 million in the years thereafter, unlocking much needed budgetary savings for a country that remains l

The move would also be part of the broader migration and security decree released by Salvini in late September, which also banned residency permits for so-called humanitarian reasons. Migrants will now be classified into two groups: those with recognized asylum claims and those without according to the Italian press. Those with refugee status and recognized underage migrants will have broader access to funding and government programs.

Salvini, who came into power riding on a platform vowing to crackdown on the number of inbound refugees, has managed to greatly reduce the number of migrants coming into Italy by closing Italian ports to migrant rescue NGO vessels who have been accused in the past of co-operating with people smugglers.

Having dealt with the issue of migrants entering Italy illegally, Salvini has recently set his sights on deportations of existing illegals according to Breitbart. Earlier this week he announced a new plan to invest €12 million to fund the deportation of at least 2,700 illegals starting in February and ending in 2021.

As reported back in 2015, one of the arguments proposed by advocates of mass migration and open borders has been using mass migration to counter the falling birthrates in western European nations, helping to boost Europe’s flagging GDP.

Salvini has made his opposition to this so-called “replacement migration” argument clear, saying: “I believe that I’m in government in order to see that our young people have the number of children that they used to a few years ago, and not to transplant the best of Africa’s youth to Europe.”

Instead, and pulling a page out of China’s playbook, Salvini has trying to motivate Italians to have more children, with the government offering free farmland to couples having three or more children. It is unclear if this strategy has any hope of working in a nation in which two-thirds of young adults still live with their parents.

END

Fitch warns the Italian government that it may not survive as the coalition member views are quite diverse

(courtesy zerohedge)

Fitch Warns Italy’s Government May Not Survive Amid Calls For A Vote Of Confidence

Update: Picking a perfect moment to prove Fitch’s point, Bloomberg reports that the Italian government may call a vote of confidence in the Senate on the migration measures. This would aim to strong-arm Five Star dissenters who face expulsion from the party if they vote against the government.

Additionally, Five Star and the League are also at loggerheads in the lower house of parliament over Five Star’s demand in an anti-corruption bill to scrap time limits on how long people can be prosecuted after an initial trial. Salvini has said the government must “avoid trials that last forever, also for the innocent, which would be a defeat for everyone.”

It appears that if the internal bickering within Italy’s “coalition” government continues, the EU may just opt to wait to discuss the Italian deficit with whatever government comes as a replacement.

* * *

While European bond traders have been focused on the escalating standoff between Italy and Brussels over Italy’s budget-busting deficit proposal, which culminated this morning with EU’s Dombrovskis warning that the European Commission is considering a sanction procedure against Italy if the budget does not change – even as Italy has sternly refused to change the budget – this morning the head of Fitch’s sovereign ratings, James McCormack, warned that uncertainty involving Italy’s coalition government is as great a risk for BTP investors as the budget for the simple reason that the government may not survive as its members are “too different.”

Speaking on Bloomberg TV, the Fitch strategist said that there are not many things that the coalition partners agree on, and that raises questions about the government’s survival.

“We are not convinced that this coalition government is actually going to survive. It has very different coalition partners” and there are “not many things that they agree on”, McCormack said.

“Then the question becomes: what happens then? Political uncertainty is not finished in Italy,” he added, expecting Italian political fireworks to continue well into 2019. As a reminder, there is a November 30 deadline for the Italian budget to be approved by European Commission, which then has to pass Italy’s parliament by December 31, with an April 30 “Plan B” extended deadline for Italian approval.

The Fitch analyst also said that if yields on Italian bonds go higher – whether with the active involvement of the ECB, which can be quite convincing as Berlusconi recalls all too well, or without – “this could force the Italian government to think of a different strategy.”

The silver lining to McCormack is that there hasn’t been a blowout in debt-to-GDP, yet: “the debt dynamics are not great, because we are not seeing declining debt. But the debt is not increasing. The debt is pretty stable. It’s high, but it’s stable.”

That will change if the Italian budget passes, as proposed. Which is also why the European Commission will not allow it to happen.

As Bloomberg notes, this means the Italian bond drama could drag on well beyond the budget standoff deadline and volatility may rise as the market deals with two-way risks. Furthermore, if this government collapses in the near future, it would not mean the end of fiscal challenges for Italy. On the other hand, the coalition cabinet has little choice: with Italian growth so weak, it’s not clear if any government can stick to the EU’s budget rules given potential economic and social costs.

Which is why Salvini, Di Mateo and company are trapped, are damned if they cut the deficit, damned if they don’t.

The market is starting to realize this, and the BTP yield spread is edging back toward 300 bps, which is already 1.35% above the five-year average.

The one thing Italy has going for it, is that its debt-to-GDP ratio, while high, has been steady around 133% over the past five years (if still the highest in Europe after Greece).

But that can change with this or another government. As Bloomberg concludes, “with the EU’s Moscovici raising pressure on the budget, the situation might get much worse before it gets better.”

The Challenge For Deutsche Bank – Cost-Cutting & Capital-Deployment Conundra

Authored by Chris Whalen via TheInstitutionalRiskAnalyst.com,