GOLD: $1207.80 DOWN $16.80 (COMEX TO COMEX CLOSINGS)

Silver: $14.15 DOWN 29 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1209.45

silver: $14.16

IT IS MUCH EASIER FOR THE BOYS TO RAID ON FRIDAY BECAUSE CHINA AND LONDON ARE CLOSED AT NOON AND THUS THE CROOKS DO NOT HAVE TO WORRY ABOUT BEING DELIVERED UPON UNTIL MONDAY.

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT:1 NOTICE(S) FOR 100

Total number of notices filed so far for NOV: 194 for 19400 OZ (0.6034 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

28 NOTICE(S) FILED TODAY FOR

140,000 OZ/

Total number of notices filed so far this month: 1391 for 6,955,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6435: down $43

Bitcoin: FINAL EVENING TRADE: $6410 down 716

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY 2546 CONTRACTS FROM 214,502 DOWN TO 211,956 WITH YESTERDAY’S 15 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 3282 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3282 CONTRACTS. WITH THE TRANSFER OF 3282 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3282 EFP CONTRACTS TRANSLATES INTO 16.41 MILLION OZ ACCOMPANYING:

1.THE 15 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 6,970,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV:

17,929 CONTRACTS (FOR 7 TRADING DAYS TOTAL 17,929 CONTRACTS) OR 89.65MILLION OZ: (AVERAGE PER DAY: 2561 CONTRACTS OR 12.806 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 89.65 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.80% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,519.37 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2546 WITH THE 15 CENT DECLINE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 3282 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED: 736 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3282 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2546 OI COMEX CONTRACTS. AND ALL OF THUS GOOD DEMAND HAPPENED WITH A 15 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.44 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 6.970 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 28 NOTICE(S) FOR 140,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 6.970 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 3544 CONTRACTS UP TO 499,905 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A DROP IN PRICE OF $3.30).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7692 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7692 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 499,905. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED RISE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,236 CONTRACTS: 53544 OI CONTRACTS INCREASED AT THE COMEX AND 7692 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,236 CONTRACTS OR 1,123,600 OZ = 34.94 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.30???.

YESTERDAY, WE HAD 5364 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 50,571 CONTRACTS OR 5,057,100 OZ OR 157.29 TONNES (7 TRADING DAYS AND THUS AVERAGING: 7224 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY IN TONNES: 157.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 157/29/2550 x 100% TONNES = 6/16% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,367.25 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3544 DESPITE THE LOSS IN PRICING ($3.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7692 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7692 EFP CONTRACTS ISSUED, WE HAD A STRONG RISE OF 11,236 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7692 CONTRACTS MOVE TO LONDON AND 3544 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 34.94 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A LOSS OF $3,30 IN YESTERDAY’S TRADING AT THE COMEX????.

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $16.80 TODAY: /

no changes in gold inventory at the GLD

/GLD INVENTORY 755.23 TONNES

Inventory rests tonight: 755.23 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 29 CENTS TODAY

A NO CHANGES AT THE SLV:

/INVENTORY RESTS AT 325.724 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY 2546 CONTRACTS from 214,502 DOWN TO 211,956 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

3282 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3282 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2546 CONTRACTS TO THE 3282 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR NET GAIN OF 736 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.494 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 6.97 MILLION OZ STANDING IN NOVEMBER.

RESULT: A GOOD INCREASE IN SILVER OI AT THE COMEX WITH THE 15 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZED 3282 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 36.76 POINTS OR 1.39% //Hang Sang CLOSED DOWN 625.80 POINTS OR 2.39% //The Nikkei closed DOWN 236.67 OR 1.05%/ Australia’s all ordinaires CLOSED DOWN 0.08% /Chinese yuan (ONSHORE) closed DOWN at 6.9484 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 59.81 dollars per barrel for WTI and 69.74 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.9484 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL DOWN ON THE DOLLAR AT 6.9437: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Massive amounts of dollars are leaving China. It is no doubt the sucking of these dollars by Trump who needs to fund 1.9 trillion of debt and Fed roll off. It is creating a nightmare scenario for the Chinese as they too along with emerging markets are suffering from a lack of dollars

( Jeffery Snider/Alhambra Investments)

a must read….

ii)This is major!! POBC has given a directive that large banks must issue 1/3 of their entire loans to private companies even though they know that 2/3 of these will probably default. This sent Chinese stocks plummeting because they know this is unsustainable

iii)Ken Rogoff is correct: as China is slowing down, instead of lower interest rates, we will witness higher rates and that will doom the world’ global economy

( Ken Rogoff/Guardian)

4/EUROPEAN AFFAIRS

i)FRANCE/IRAN/USA

Macron is leading France in protecting the Iran/EU oil trade from USA sanctions

( Paraskova /OilPrice.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran/USA

Pompeo correctly states that the leadership must decide if they want their people to eat

( zerohedge)

ii)SAUDI ARABIA

6. GLOBAL ISSUES

7. OIL ISSUES

Canada/USA

This is a key defeat for Trump as a judge blocks the construction of the Keystone XL pipeline. This is very bad for Canada

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

ARGENTINA

Argentina faces China as it signs a $8.7 billion swap deal similar to the one signed with Venezuela’s swap with China. It sure looks like the west is losing ground to China..

(courtesy zerohedge)

9. PHYSICAL MARKETS

b)Chinese demand for gold in October remains strong at 143 tonnes.

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

i(Not good: GE collapses to an 8 handle. The price is unchanged from 1995

( zerohedge)

ii)Raid today as stocks fall as well as gold. Yields tumble after a hot PPI.

( zerohedge)

ii)Market data/

a)Pay special attention to the following: Graham is correct…the Fed just told everyone that they are on their own and that their is no Fed put

( Graham Summers)

b)Soft data, University of Michigan sentiment slides and for the first time “hope” also fades along with buying plans

The USA economy is faltering badly

( zerohedge)

a)Recount looms again in Florida after the Republican victories but suspicions galore about possible vote tampering

( zerohedge)

b)Looks like we have voter fraud in both Arizona and Florida..no who would have guessed

(courtesy zerohedge)

iv)SWAMP STORIES

a)Here is the list of people who might replace Sessions on a permanent basis.

( zerohedge)

b)

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 31 notices standing for a loss of 247 contacts. We had 275 notices served upon yesterday so we gained another 28 contracts or an additional 140,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts. QUEUE JUMPING DID RETURN TO THE COMEX ARENA AS THIS PHENOMENON (IN SILVER) HAS BEEN THE NAME OF THE GAME FOR OVER 19 MONTHS.

After November, we have a December contract and here we lost 3528 contracts down to 142,538. January saw a gain of 70 contracts up to 1060 contracts. March, the next big delivery month after December saw a loss of 681 contracts up to 53,854.

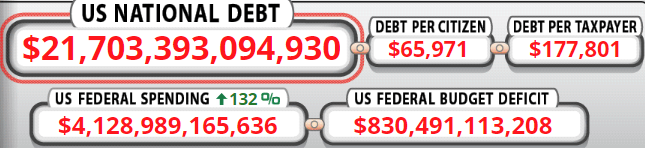

AMERICAN ELECTIONS FARCE AS POLITICIANS IGNORE THE LOOMING $121.7 TRILLION DEBT CRISIS

In today’s update we look at yet another ‘Punch and Judy’ American election farce which once again ignored the ‘Elephant in the room’ – the inevitable U.S. $121.7 trillion debt crisis and the coming global $250 trillion debt crisis.

We examine the “Punch and Judy” farce that were the American elections this week in which both the politicians, the media and the people again managed to completely ignore one of the greatest financial, economic and societal challenges facing the U.S. and indeed the world – the coming U.S. and global debt crisis.

Trump said he would erase America’s debt in 8 years. It’s now bigger than ever. When this promise was made, the national debt stood at $19 trillion. When Trump became President the US National debt was just below $20 trillion; it has since risen to $21.7 trillion.

During Obama’s presidency, the total national debt has risen from $10.6 trillion to nearly $20 trillion.

This debt is just the nominal national debt and there is also the not insignificant matter of the between $100 trillion and $200 trillion in unfunded liabilities – for medicare, medicaid and social security. As the Baby Boomers retire, these liabilities are coming due in the coming years.

The U.S., like the EU and most western nations, is “kicking the can down the road.” Consequently, a U.S. and global debt crisis looks likely in the coming months and years.

Trump was elected on a promise to reduce the debt and government spending including that on the military and the Deep State. Not only has he failed miserably in this goal – he had done the opposite. He has not been a man of his word and like a lot of politicians – both Republican and Democrat, left and right – he talks the talk but completely fails to walk the walk!

Politics in the U.S. and globally has been reduced to a modern ‘Punch and Judy’ show. It is akin to a kids puppet show in which the competitors beat each other up and it is a distraction for the child like electorate. The politicians resemble mere puppets to corporate and Wall Street vested interests who are ‘pulling the strings’ and enriching themselves from behind the political stage.

This is happening at the expense of individuals, families, farmers, entrepreneurs, small and medium size enterprises, less politically connected corporations and banks and ultimately society itself.

Massive military expenditures are justified – nearly half of U.S. government expenditure now goes to the arms industry – by scaring the people with the latest bogeyman du jour. There are evil villains every where as the Deep State and their corrupt and idiotic politicians and a compliant media who do the fear mongering of the Deep State. Constant political and media fear mongering and “cat calls” of “look behind you” at the latest enemy of the day.

The lists grows longer by the day:

Evil Russia in Soviet era to evil Saddam Hussein and Iraq (once an ally) to Gadafi in Libya (once an ally) to North Korea (who were an existential threat and evil one week and then became allies more recently and “Little Rocket Man” may become an enemy again if necessary) to evil Muslims everywhere (except fundamentalist Saudi Arabia who West sells arms to) to evil Russians again in recent years, and now we appear set for an even bigger enemy – those evil Chinese who are now hacking our devices and trying to monitor us. Western governments would never do such a thing!

Tweedle Dum Tweedle Dee: During the 2000 United States presidential election, candidate Ralph Nader claimed that George W. Bush and Al Gore were not very different in their policies and how they had become captured by corporate and Wall Street interests. He rightly called them the parties and candidates – Tweedledum and Tweedledee.

Trajectory towards empire is inexorable and now has a momentum and life of its own alas. Ralph Nader, Ron Paul were opportunities to change the trajectory which were not embraced unfortunately.

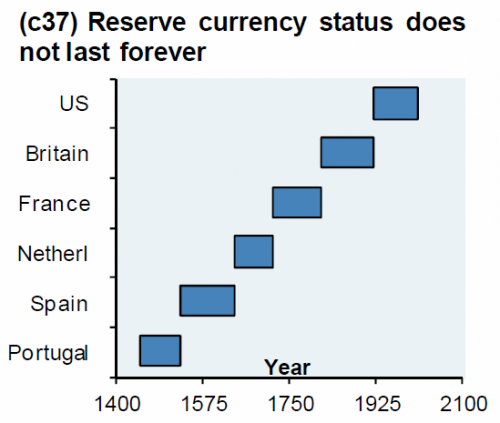

Ultimately all of this bodes badly for the US, its economy and the US dollar.

The threats posed to the U.S. dollar as the global reserve currency of the world and the coming dollar and fiat currency devaluations as currency wars intensify make owning physical gold in the safest ways possible essential to all who wish to preserve wealth in the coming years.

NOV 9

Bank of England stalls return of Venezuela’s gold

Submitted by cpowell on Fri, 2018-11-09 01:37. Section: Daily Dispatches

This should clean out the rest of the Bank of England’s custodial gold PDQ.

* * *

Maduro Scrambles to Bring Venezuela’s Gold Back from the UK

By Stephen Gibbs

The Times, London

Wednesday, November 7, 2018

CARACAS — President Maduro of Venezuela is trying to repatriate at least 14 tonnes of gold held at the Bank of England, fearing that access could be frozen under U.S. sanctions against his regime.

The bank has refused to release the gold bars, worth about L420 million, according to sources. British officials are understood to have insisted that standard measures to prevent money laundering be taken — including clarification of the Venezuelan government’s intentions for the gold.

There are concerns that Mr Maduro may seize the gold, which is owned by the state, and sell it for personal gain. …

… For the remainder of the report:

https://www.thetimes.co.uk/article/maduro-scrambles-to-bring-venezuela-s…

* * *

end

LAWRIE WILLIAMS : Chinese gold demand may be slipping, but only just

The latest figures for Shanghai Gold Exchange (SGE) monthly gold withdrawals are in (for October) and they show a marginal downturn from those for the same month a year earlier. But then October can be an anomalous month given the week long Golden Week holiday at the beginning of the month during which time the SGE is closed for business so perhaps not too much should be read into the latest data.

Withdrawals for the year to date are still marginally up on a year earlier, so we will have to wait for November’s figures (usually a strong month) to see if there is any specific trend downwards yet. A Table showing the monthly gold withdrawals data year to date, with comparative figures for the prior two years, is shown below:

At the moment China is still on track for another2,000 tonne plus gold withdrawals year, but if full year demand slips a little we shouldn’t be too surprised. Gold imports from Switzerland and Hong Kong – the two principal published sources for China’s direct gold imports, both appear to be slipping a little and the U.S.-imposed tariffs will be having some adverse impacts on China’s domestic economy which may be leading to a reduction in disposable income among the gold-buying public.. The country’s own gold production is reported to be slipping too as tighter environmental controls are being implemented leading to reduced production, and even closures, at some of the country’s own gold mines.

We continue to equate SGE gold withdrawal levels to our own estimate of China’s gold demand, although some of the prominent gold consultancies may disagree and come up with lower figures. However SGE gold withdrawal figures consistently would seem to equate far closer to known Chinese gold imports, plus the country’s own production plus an allowance for scrap conversion than do the consultancies’ published demand estimates. At the very least SGE gold withdrawals have to represent a measure of the country’s gold flows which is comparable month on month and year on year with previous years.

end

No wonder gold fell in October: BIS intervention rose sharply after falling in August and September

(courtesy Robert Lambourne)

With BIS intervention rising sharply in October, gold price stalled

By: Robert Lambourne

— Published: Friday, 9 November 2018 |

After falling in August and September, intervention in the gold market by the Bank for International Settlements via gold swaps increased substantially in October, according to the bank’s monthly statement of account, published this week:

https://www.bis.org/banking/balsheet/statofacc181031.pd f

The bank’s August and September statements are here:

https://www.bis.org/banking/balsheet/statofacc180831.pd f

https://www.bis.org/banking/balsheet/statofacc180930.pd f

Perhaps not coincidentally, the gold price rose in August and September as the BIS reduced its intervention in the market and then stalled and leveled out in October as the bank greatly increased its intervention again.

The monthly statements of the BIS give only summary information on the bank’s use of gold swaps and other gold-related derivatives. The information in the statements is not sufficient to calculate a precise amount of gold-related derivatives, including swaps. But, after subtracting the gold reported owned by the BIS itself, the bank’s total estimated gold exposure as of October 31 was around 372 tonnes — 134 tonnes, or 56 percent, greater than the approximately 238 tonnes as of September 30.

As of August 31 the bank’s total estimated gold exposure was around 370 tonnes and around 485 tonnes as of July 31.

When it comes to its activities in the gold market, the BIS provides little information on what it is doing, why, and for whom:

http://www.gata.org/node/17793

But the bank continues to trade actively in gold swaps to source gold to its member central banks and other financial entities, as evidenced by the increase in October.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9484/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9437 /shanghai bourse CLOSED DOWN 36/76 POINTS OR 1.39%

. HANG SANG CLOSED DOWN 628.80 POINTS OR 2.39%

2. Nikkei closed DOWN 236.67POINTS OR 1.05%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 96.77/Euro FALLS TO 1.1348

3b Japan 10 year bond yield: FALLS TO. +.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.86/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.81 and Brent: 69.74

3f Gold DOWN/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.43%/Italian 10 yr bond yield UP to 3.44% /SPAIN 10 YR BOND YIELD UP TO 1.60%

3j Greek 10 year bond yield RISES TO : 4.40

3k Gold at $1218.95 silver at:14.33 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 36/100 in roubles/dollar) 67.28

3m oil into the 59 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.86DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0063 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1421 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.43%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.21% early this morning. Thirty year rate at 3.41%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4891

Global Stocks, Oil Tumble As Dollar Surges And

Familiar Fears Return

Was the Wednesday post-election rally a one-hit wonder? Was the FOMC, despite its surprisingly sparse statement, superhawkish? Was nothing actually fixed this week (narrator: “it wasn’t”) and are all the “same old” fears – trade wars, interest rates, China, tighter financial conditions, peak earnings, slowing global economy – haunting the market making a comeback?

Those are questions on traders’ minds this morning as global markets were headed for their biggest drop in two weeks, awash in a sea of red, as the MSCI World index fell half a percent, its biggest drop since Oct. 26 …

… as Brent tumbles below $70/barrel to a 6 month low, while WTI is now 21% below its recent high and has entered a bear market, now down for a record 10th consecutive day in a row…

… and as the dollar surge brings it just shy of the 2018 highs as the yuan resumed weakening on growing concerns about a slowdown in China, despite inflation data out of Beijing overnight that came in as expected.

While the Fed’s decision to hold rates was expected, some traders had expected an even more dovish approach and a mention of the October rout; its absence led to an overly hawkish take with the Fed confirming a December increase is a distinct possibility for the robust US economy. That contrasts sharply with China, where cooling producer price inflation and falling car sales suggested an economy struggling to gain traction.

“Worries about trade wars and how the slowdown in China will impact the rest of the world mean stocks appear to be more risky, so there’s a typical risk-off move in markets today,” said DZ Bank rates strategist Pascal Segesser.

And as “plain vanilla” growth risks return now that the election is gone, stocks in Hong Kong and China were the main losers in Asia, where a financial sector sub-index fell more than 2 percent after China’s banking watchdog told lenders to allocate at least a third of new loans to private companies, raising the prospects of a jump in bad assets. Additionally, a decline in Chinese PPI, weak car sales and a disappointing outlook from a top online travel company combined to reignite lingering concerns about the health of the world’s second-biggest economy as BBG notes. As as result, the Shanghai Composite, a barometer for overall risk sentiment outside the US, continued to slide, and was down 1.4%, closing just below 2,600, its lowest level since the end of September.

European stocks followed Asia lower, with Europe’s Stoxx 600 Index down 0.7%, dragged lower by mining and energy shares after crude oil entered a bear market and most industrial metals fell, while disappointing forecasts from Richemont and Thyssenkrup AG also weighed on the index.

US equity futures contracts pointed to second day of declines for U.S. stocks.

Losses in equities pressured bond yields lower, with debt in Germany and the United States rising across the board, pressured by world trade frictions and a budget standoff between Italy and Brussels.

Meanwhile, in FX, the confident Fed boosted the dollar, which had weakened sharply after mid-term elections this week raised the prospects of U.S. political gridlock. The greenback gained a quarter of a percent against the euro and half a percent against the British pound, and is back to just shy of its 2018 highs. The DXY dollar index gained 0.25 percent to 96.86. The Aussie swung to a loss as the central bank’s economic forecasts disappointed traders. The pound erased some of this week’s gains as the Irish border continued to be the biggest hurdle to a Brexit divorce deal; U.K. data was mixed, with the trade deficit shrinking while industrial production and services figures were underwhelming.

In commodities, oil prices fell to multi-month lows as global supply increased and investors worried about the impact from soaring US output, set to hit a record 12mmbpd, and concerns about fuel demand from of lower economic growth and trade disputes. Benchmark Brent crude oil fell to its lowest since early April, down more than 18 percent since reaching four-year highs at the beginning of October. Also overnight, the sturdy dollar tarnished the appetite for safe-haven gold with the price down 0.2% at $1221.42 an ounce.

Market Snapshot

- S&P 500 futures down 0.4% to 2,796.50

- STOXX Europe 600 down 0.5% to 365.14

- MXAP down 1.1% to 152.39

- MXAPJ down 1.4% to 485.31

- Nikkei down 1.1% to 22,250.25

- Topix down 0.5% to 1,672.98

- Hang Seng Index down 2.4% to 25,601.92

- Shanghai Composite down 1.4% to 2,598.87

- Sensex down 0.2% to 35,156.02

- Australia S&P/ASX 200 down 0.1% to 5,921.85

- Kospi down 0.3% to 2,086.09

- German 10Y yield fell 2.8 bps to 0.429%

- Euro down 0.2% to $1.1338

- Brent Futures down 0.2% to $70.49/bbl

- Italian 10Y yield rose 5.7 bps to 3.025%

- Spanish 10Y yield fell 0.6 bps to 1.602%

- Brent Futures down 0.2% to $70.50/bbl

- Gold spot down 0.3% to $1,220.88

- U.S. Dollar Index up 0.1% to 96.85

Top Overnight News

- Labor Secretary Alex Acosta, former New Jersey Governor Chris Christie, and U.S. Appeals Court Judge Edith Jones are among the people White House aides and outside advisers are considering to replace Jeff Sessions as the nation’s top law enforcement officer

- The White House is unprepared to defend itself against a coming wave of investigations by newly empowered House Democrats, who have vowed to probe everything from cabinet members’ ethics scandals to conflicts of interest involving the president’s business empire

- UBS risks billions in fines as its two biggest legal cases in years are hitting the final stretch, in a test of Chief Executive Officer Sergio Ermotti’s strategy of taking on French and U.S. authorities

- China laid out banks’ lending targets for private companies, as it aims to boost large banks’ loans to private companies to at least one-third of new corporate lending

- India’s government is asking the central bank to hand over a part of its surplus reserves to put that to more productive use, an official told reporters

- Amid optimism a Brexit deal could be reached soon, the Irish border issue continues to be the biggest hurdle while crunching the numbers suggests any deal faces a difficult journey through Parliament

Asian equity markets traded lower following a lacklustre lead from Wall St where the mid-term stock rally stalled as focus shifted to the FOMC. ASX 200 (-0.1%) and Nikkei 225 (-1.1%) were lower with energy stocks pressured after a continued slump in oil prices and as soft earnings results also clouded over Tokyo sentiment. Hang Seng (-2.4%) and Shanghai Comp. (-1.4%) were the worst hit in the region as tech and energy stocks lagged, while continued PBoC liquidity inaction and inline inflation data proved to be inconclusive for sentiment. Finally, 10yr JGBs were flat with prices uneventful as the pressure from the recent losses in T-notes was counterbalanced by the risk averse tone and BoJ’s presence in the market for JPY 980bln of JGBs across the curve.

Top Asian News

- A Fifth of China’s Housing Is Empty. That’s 50 Million Homes

- PBOC’s Yi Warns of Uncertainties in Fed’s Policy, Trade Tensions

- Russia Challenges U.S. in Hosting Taliban at Afghan Talks

- China Banks Fall on Concern Loan Targets Are a Step Too Far

Major European equities are lower across the board (Eurostoxx 50 -0.8%) as the sentiment seen in Asia spills over onto the region. Material names lag amid the slump in base metal prices, while consumer staples outperform. The finance sector is also experiencing weakness with the likes of Spanish banks exposed to Mexico (BBVA -6.7%, Sabadell -2.8%, Santander -2.4%) pressured after Mexican banks fell overnight amid a surprise proposal from the incoming President AMLO to scrap bank fees. (Note: BBVA made 28% of its revenues and 34% of its operating income from Mexico last year.) Meanwhile, UBS (-4.3%) shares declines after the US Justice Department filed a lawsuit against the bank for defrauding investors in its sales of mortgage-backed securities leading up to the global financial crisis. Over in Germany, steel-maker Thyssenkrupp (-11.0%) shares slumped after the company announced a profit warning due to provisions for an ongoing cartel probe and quality problems at its auto business. Elsewhere, Richemont (-6.7%) shares declines amid disappointing earnings, hitting the likes of European Luxury names (LVMH -2.0%, Kering -3.6%) in sympathy.

Top European News

- Turkey Cancels 3 Bond Auctions on Reduced Financing Needs

- Pound Skeptics Turn Believers as Brexit Divorce Deal Looks Near

- France Seizes Ryanair Plane to Force State Aid Repayment

- Telecom Italia Scraps Debt Plan, Sees $2.3 Billion Writedown

In FX, the dollar appears to have stopped for the Greenback on Wednesday, and its resurgence from mid-term election lows has been fuelled to a degree by the latest FOMC policy statement that effectively underpins market expectations for a December hike. Amidst almost universal gains vs currency counterparts, the index is now nudging 97.000 from just shy of 95.700 at one stage and the 2018 peak of 97.201 is back within striking distance. GBP – Brexit impulses continue to ebb and flow between positive vibes on deal prospects and the proverbial cliff edge withdrawal, but the bottom line is that Irish border and back-stop differences remain unresolved to leave the UK at risk of failing to agree terms at home and/or with the EU. Hence, Sterling has lost momentum and is underperforming alongside the NOK (undermined by much softer than expected Norwegian inflation data to trade down around 9.5700 vs the Eur) within the G10 ranks, as Cable teeters above 1.3000, and largely shrugged off a barrage of UK data (GDP firm and trade above consensus, but other elements less encouraging). CAD/EUR – The next worst majors, with Loonie hit by collapsing oil prices and sliding towards 1.3200 vs its US peer, while the single currency continues its relatively sharp and abrupt pull-back from 1.1500 to retest support ahead of the 1.1300 ytd low. Ongoing Italian-EU budget differences are weighing along with more signs of a slowdown, or even weakness in the Eurozone economy, while hefty option expiries are also eyed (1.1300 in 1.1 bn, 1.1340-50 in 2.0 bn and 1.1375 in 1.3 bn for example). AUD/NZD – Also falling prey to their US rival’s revival and hardly helped by neutral or wait-and-see policy guidance from the RBA or RBNZ, as Aud/Usd recoils to sub-0.7250 and Nzd/Usd backs off further from almost 0.6800 to under 0.6750.

In commodities, WTI (-1.6%) and Brent (-1.4%) lost the USD 60/bbl and USD 70/bbl handles respectively, after the complex entered into bear market territory amid rising supply and concerns of a slowdown in global economic growth. Both benchmarks declined around 20% from the four-year highs reached at the front end of October and are set for a fifth straight week of declines, while North Sea Brent Crude hit seven-month lows. The slide has been exacerbated by US’ decision to permit eight countries to continue importing Iranian oil after the imposition of sanctions on the OPEC member, as well as record production of crude oil over in the States. Looking ahead, investors and traders will be focusing on this weekend’s meeting of OPEC and its allies where they are set to discuss output strategies in Abu Dhabi on Sunday. During the week, there were source reports that Russia and Saudi are to start discussing oil production cuts in 2019. This comes after OPEC’s October production reached the highest level since 2016, while Russia hiked its output in the prior month to recent highs of 11.4mln BPD. Producers on Sunday will have to discuss the threat of a glut alongside the prospect of lower demand from faltering EM economies and repercussions from US-Sino trade disputes.

Elsewhere, metals trade lower across the board with copper underperforming amid post-FOMC dollar strength and concerns regarding slowing global economic growth. Among precious metals, spot gold (-0.3%) tracks USD action, with the yellow metal dropping to the lowest level this month, while spot silver (-0.4%) is set for its largest weekly percentage decline in nine weeks. US Federal judge blocked Keystone XL Pipeline stating that US administration’s justification for the approval was incomplete, while the judge added that the State Department failed to evaluate climate impact, oil spills and cultural resources.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.2%, prior 0.2%; Ex Food and Energy MoM, est. 0.2%, prior 0.2%; Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.4%

- 8:30am: PPI Final Demand YoY, est. 2.5%, prior 2.6%; Ex Food and Energy YoY, est. 2.3%, prior 2.5%; Ex Food, Energy, Trade YoY, prior 2.9%

- 8:45am: Bloomberg Nov. United States Economic Survey

- 10am: Wholesale Inventories MoM, est. 0.3%, prior 0.3%; Wholesale Trade Sales MoM, est. 0.4%, prior 0.8%

- 10am: U. of Mich. Sentiment, est. 98, prior 98.6; Expectations, est. 87.2, prior 89.3; Current Conditions, est. 114.9, prior 113.1

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 36.76 POINTS OR 1.39% //Hang Sang CLOSED DOWN 625.80 POINTS OR 2.39% //The Nikkei closed DOWN 236.67 OR 1.05%/ Australia’s all ordinaires CLOSED DOWN 0.08% /Chinese yuan (ONSHORE) closed DOWN at 6.9484 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 59.81 dollars per barrel for WTI and 69.74 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.9484 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL DOWN ON THE DOLLAR AT 6.9437: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Massive amounts of dollars are leaving China. It is no doubt the sucking of these dollars by Trump who needs to fund 1.9 trillion of debt and Fed roll off. It is creating a nightmare scenario for the Chinese as they too along with emerging markets are suffering from a lack of dollars

(courtesy Jeffery Snider/Alhambra Investments)

a must read….

China’s (Not) SAFE

Authored by Jeffrey Snider via Alhambra Investment Partners,

In another sign of repeating 2015, the Chinese are beginning to mobilize their “reserves” again. Three years ago, in a futile attempt to staunch CNY’s stubborn “devaluation” various government authorities blew through just about $1 trillion. It didn’t work. You would think that everyone could learn from this episode.

I think the Chinese did, which is why in 2017 they engineered the bypass through Hong Kong in order to hide the continued peril; capital outflows in the mistaken parlance of the mainstream. All that changed, unsurprisingly, in January.

At first, unlike 2015, it was a trickle. Only small balances were deployed scattershot suggesting that officials weren’t going to repeat their mistake. Western Economists may still view foreign reserves as insurance against this kind of thing, but eurodollar squeeze #3 proved conclusively the absurdity of being so monetarily ignorant.

If you can’t steady your currency with $1 trillion, no one can. Period.

To chuck that mind-boggling amount into the ether and get nothing to show for it is about as conclusive a demonstration. The PBOC and others’ reluctance to do the same thing in 2018 is therefore understandable. They let CNY go mostly unaddressed (apart from some clandestine operations here or there) because what else were they going to do?

This, I believe, explains why CNY plummeted in 2018 compared to the “ticking clock” stairstep decline two and three years ago. That’s another aspect monetary officials may now appreciate, how in the end the mobilization of reserves tends to make things worse.

All that may be changing, however. I have to assume with great reluctance, pretty much they don’t know what else to do. Foreign reserves are flowing out of the government’s various pockets all over again. China’s State Administration of Foreign Exchange (SAFE) reported that in September 2018 total foreign reserves fell by $22.69 billion. It was the most since January, that prior month a one-off fix.

Today, SAFE estimates that in October China shed another $33.93 billion. This was the largest monthly usage since the last ticking clock in 2016. On a 2-month basis, it is pretty clear things are getting serious in China with CNY hanging just on the other side of 7.0.

It is a pretty clear signal for escalation. Of what? All these things are connected; from eurodollars to Chinese foreign reserves to Chinese internal money (RMB). They all follow from this exogenous state. As the eurodollar system goes, so does everything else in China (as well as everywhere else).

In this case, if A = B, and B = C, then obviously A = C. In other words, all the factors pictured below (3 charts) are the same thing approached from different Chinese angles: eurodollars.

Thus, working backward, the more China feels compelled to act against various forms of internal monetary tightness we know right then its origin. China tells us everything we need to know about the eurodollar system, and therefore the dollar nobody on this side of the world pays any attention to (continuing the age-old policy of benign neglect that in the past eleven years has devolved into just criminal neglect).

The dollar shortage, or eurodollar squeeze, however you wish to call it, is growing more disruptive not less (where’s federal funds lately?) We can see the results of the disorder scattered all across the globe. Nothing is more consistent with the sudden struggles in the European economy of late as China’s declining foreign reserve balances.

Likewise, the absolutely huge warning in the oil market, the futures curve going contango, is very much related to China going 2015.

The list of unwelcome developments is multiplying and amplifying. Even the Western mainstream is finding it more and more difficult to just skate past all this. Bloomberg last week (thanks M. Simmons):

The world’s major economies that entered 2018 accelerating in sync risk entering 2019 decelerating in sync.

The shift is being led by China, where the economy’s weakest performance since 2009 is set to worsen unless a peace can be struck in the trade war with the U.S. Factory readings from Asia already show a fallout, with Taiwan, Thailand and Malaysia slipping into contraction territory.

The euro-area too is losing momentum, expanding in the third quarter at half the pace of the prior three months as Italy and Germany stagnated.

Even the US may not be invulnerable, if the Economists quoted by the article are right (though they don’t know why, sticking with this trade war theory). I wrote back in September, as for months before, just where this is all heading:

From 2003 to 2009, it went: globally synchronized growth, decoupling, globally synchronized downturn. From 2010 to 2012, it went: globally synchronized growth, decoupling, globally synchronized downturn. From 2013 to 2016, it went: strong global growth (not synchronized), decoupling, synchronized downturn.

Last year to this year, it has gone: globally synchronized growth, decoupling. What comes next?

The answer is given to us by SAFE.

Unprecedented “Desperation” Lending Directive Sends Chinese Stocks Reeling

On November 8, China shocked markets with its latest targeted stimulus in the form of an “unprecedented” lending directive ordering large banks to issue loans to private companies to at least one-third of new corporate lending, said Guo Shuqing, chairman of the China Banking and Insurance Regulatory Commission. The announcement sparked a new round of investor concerns about what is being unsaid about China’s opaque, private enterprises, raising prospects of a fresh spike in bad assets.

Guo’s comments were the latest attempt by authorities to try to improve funding access for China’s non-state companies, which have been struggling to get bank loans in the aftermath of China’s crackdown on shadow lending. More importantly, it was the first time financial regulators had given targets on private lending, confirmation that earlier efforts hadn’t sparked the necessary credit activity.

More importantly, this is the first time China set formal goals for private lending, a step it refrained from even during the financial crisis of 2008 according to Bloomberg. The stimulus package it implemented at the time swelled bad debt levels, which now threaten to swallow any new money poured into private companies. Non-state firms defaulted on 67.4 billion yuan ($9.7 billion) of local bonds this year, 4.2 times that of 2017, while the overall Chinese market is headed for a year of record defaults in 2018.

According to commentators, the new policy was prompted by the need to ensure that China’s private firms, already challenged by China’s state-owned behemoths, survive amid a plunging stock market, record corporate defaults and a cooling economy. At the same time, the target for small and medium-sized banks is higher, at two-thirds of new corporate loans, with Guo adding that he wants to see loans to private companies account for at least half of total new corporate loans in three years.

But most importantly, this targeted lending will increase market concern on banks’ “civic duty” with Huatai Securities predicting a new sharp spike in NPL ratio amid the accelerating economic slowdown, which would prove negative for short-term sentiment.

“There is desperation among regulators, and sometimes muddled polices are difficult to avoid under this kind of pressure,” said Jiang Liangqing, a Beijing-based fund manager at Ruisen Capital Management. “Investors are voting with their feet.”

* * *

Also this week, PBOC Governor Yi announced a policy combination of “3 arrows” to support additional liquidity to the private sector, including bank loans, debt and equity financing. The arrows, per Goldman, were the following:

- Firstly, PBOC is looking into the possibility of promoting equity financing for private firms. The central bank is working with various financial institutions such as fund managers and brokerages on this initiative.

- Secondly, PBOC will expand a recently launched scheme to promote private firms’ bond issuance in collaboration with financial regulators. Three companies have already raised 1.9 billion yuan of bonds with over-subscription, and 30 more private enterprises are preparing for bond issuance.

- Thirdly, PBOC will add a new metric in the MPA formula to encourage lending to private companies. They will also increase the supply of long term and reasonably priced funding for financial institutions (further RRR cuts would fit this goal, in our view).

As Goldman notes, “it is rare for a senior official to openly acknowledge previous policy missteps.” As a result, this is likely in response to the recent meetings hosted by President Xi, especially the one with entrepreneurs. That meeting was unique in that it carried the highest political authority and at the same time was very specific in terms of the measures to be taken.

As such, it likely put the onus on senior officials who attended the meeting to act in a timely manner. While the governor stated there is no change in the overall monetary policy stance, which is described as prudent, and more support for the real economy via more bond issuance had been stated previously, his comment on past policy missteps suggests a change in policy stance. Rather, the reiteration of the current policy stance should be read more as an indication that the PBOC will be measured in terms of the size of additional loosening. In terms of more tangible measures, Goldman now sees a higher probability that TSF growth will accelerate from now, but likely at a very measured pace. Worse, many of these new funds will end up funding underperforming assets, resulting in a spike in on-performing loans and more bad debt.

Sure enough, overnight the Shanghai Composite was hammered again, sliding 1.4% to the lowest level since the end of September, and back below 2,600…

… while the Shenzhen Financial index sliding 2.2%, following another drop the previous day.

The Friday drop followed a Thursday rout when the news was first announced which saw the major banks tumble as a result of this latest government intervention in capital allocation, with the following results: Bank of Shanghai -4%, China Merchants Bank -4%, ICBC -3.3%, Agricultural Bank of China -2.9%, Industrial Bank -2.5%, Bank of China -1.6%, Bank of Communications -1.3%

end

Ken Rogoff is correct: as China is slowing down, instead of lower interest rates, we will witness higher rates and that will doom the world’ global economy

(courtesy Ken Rogoff/Guardian)

“A Chinese Recession Is Inevitable” – Ken Rogoff Ruins ‘Decoupled-America’ Narrative

Authored by Kenneth Rogoff, op-ed via The Guardian,

Analysts say a Chinese recession would only hurt the region. That may be wishful thinking…

When China finally has its inevitable growth recession – which will almost surely be amplified by a financial crisis, given the economy’s massive leverage – how will the rest of world be affected? With US President Donald Trump’s trade war hitting China just as growth was already slowing, this is no idle question.

Typical estimates, for example those embodied in the International Monetary Fund’s assessments of country risk, suggest an economic slowdown in China will hurt everyone. But the acute pain, according to the IMF, will be more regionally concentrated and confined than would be the case for a deep recession in the United States.

Unfortunately, this might be wishful thinking.

First, the effect on international capital markets could be vastly greater than Chinese capital market linkages would suggest. However jittery global investors may be about prospects for profit growth, a hit to Chinese growth would make things a lot worse. Although it is true that the US is still by far the biggest importer of final consumption goods (a large share of Chinese manufacturing imports are intermediate goods that end up being embodied in exports to the US and Europe), foreign firms nonetheless still enjoy huge profits on sales in China.

Investors today are also concerned about rising interest rates, which not only put a damper on consumption and investment, but also reduce the market value of companies (particularly tech firms) whose valuations depend heavily on profit growth far in the future. A Chinese recession could again make the situation worse.

I appreciate the usual Keynesian thinking that if any economy anywhere slows, this lowers world aggregate demand, and therefore puts downward pressure on global interest rates. But modern thinking is more nuanced. High Asian saving rates over the past two decades have been a significant factor in the low overall level of real (inflation-adjusted) interest rates in both the US and Europe, thanks to the fact that underdeveloped Asian capital markets simply cannot constructively absorb the surplus savings.

Former US Federal Reserve chair Ben Bernanke famously characterised this much-studied phenomenon as a key component of the “global savings glut”. Thus, instead of leading to lower global real interest rates, a Chinese slowdown that spreads across Asia could paradoxically lead to higher interest rates elsewhere – especially if a second Asian financial crisis leads to a sharp draw-down of central bank reserves. Thus, for global capital markets, a Chinese recession could easily prove to be a double whammy.

As bad as a slowdown in exports to China would be for many countries, a significant rise in global interest rates would be much worse. Eurozone leaders, particularly German Chancellor Angela Merkel, get less credit than they deserve for holding together the politically and economically fragile single currency against steep economic and political odds. But their task would have been well-nigh impossible but for the ultra-low global interest rates that have allowed politically paralysed eurozone officials to skirt needed debt write-downs and restructurings in the periphery.

When the advanced countries had their financial crisis a decade ago, emerging markets recovered relatively quickly, thanks to low debt levels and strong commodity prices. Today, however, debt levels have risen significantly, and a sharp rise in global real interest rates would almost certainly extend today’s brewing crises beyond the handful of countries (including Argentina and Turkey) that have already been hit.

Nor is the US immune. For the moment, the US can finance its trillion-dollar deficits at relatively low cost. But the relatively short-term duration of its borrowing – under four years if one integrates the Treasury and Federal Reserve balance sheets – means that a rise in interest rates would soon cause debt service to crowd out needed expenditures in other areas. At the same time, Trump’s trade war also threatens to undermine the US economy’s dynamism. Its somewhat arbitrary and politically driven nature makes it at least as harmful to US growth as the regulations Trump has so proudly eliminated. Those who assumed that Trump’s stance on trade was mostly campaign bluster should be worried.

The good news is that trade negotiations often seem intractable until the 11th hour. The US and China could reach an agreement before Trump’s punitive tariffs go into effect on 1 January. Such an agreement, one hopes, would reflect a maturing of China’s attitude toward intellectual property rights – akin to what occurred in the US during the late 19th century. (In America’s high growth years, US entrepreneurs often thought little of pilfering patented inventions from the United Kingdom.)

A recession in China, amplified by a financial crisis, would constitute the third leg of the debt super-cycle that began in the US in 2008 and moved to Europe in 2010. Up to this point, the Chinese authorities have done a remarkable job in postponing the inevitable slowdown. Unfortunately, when the downturn arrives, the world is likely to discover that China’s economy matters even more than most people thought.

end

4.EUROPEAN AFFAIRS

FRANCE/IRAN/USA

Macron is leading France in protecting the Iran/EU oil trade from USA sanctions

(courtesy Paraskova /OilPrice.com)

France Takes The Lead In Protecting Iran Oil Trade From U.S. Sanctions

Authored by Tsvetana Paraskova via Oilprice.com,

France aims to lead the European Union (EU) efforts in defying U.S. sanctions on Iran, by supporting the creation of a payment mechanism to keep trade with Iran and making the euro more powerful, France’s Economy Minister Bruno Le Maire said in an interview with the Financial Times.

“Europe refuses to allow the US to be the trade policeman of the world,” Le Maire told FT, adding that the EU needs to “affirm its sovereignty” in the rift between the EU and the United States over the sanctions on Iran.

The EU has been trying to create a special purpose vehicle (SPV) that would allow the bloc to continue buying Iranian oil and keep trade in other products with Iran after the U.S. sanctions on Tehran return.

The idea behind the SPV is to have it act as a clearing house into which buyers of Iranian oil would pay, allowing the EU to trade oil with Iran without having to directly pay the Islamic Republic.

As the U.S. sanctions on Iran snapped back on Monday, the SPV hasn’t been operational and reports have had it that the undertaking is very complicated and politically sensitive. The bloc is also said to be struggling with the set-up, because no EU member is willing to host it for fear of angering the United States, the Financial Times reported recently, citing EU diplomats.

On Monday, the Belgium-based international financial messaging system SWIFT said that it would comply with the U.S. sanctions on Iran and would cut off sanctioned Iranian banks from its network. This was a blow to the EU’s attempts to defy the U.S. sanctions.

The decision by SWIFT highlights the need for an SPV, France’s Le Maire told FT, but he refused to name countries that could host such a special vehicle. Yet, there have been expressions of interest, he told FT.

Meanwhile, the United States has been dismissive of the idea of an SPV, and Brian Hook, U.S. Special Representative for Iran and Senior Policy Advisor to the Secretary of State, said in a press briefing with European reporters on Monday:

“We have not seen much, if any, demand for the Special Purpose Vehicle. I think if you take a look at the over 100 corporations that have decided to choose the United States market over the Iranian market, they’re not looking to avail themselves of any type of vehicle.”

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran/USA

Pompeo correctly states that the leadership must decide if they want their people to eat

(courtesy zerohedge)

Iran’s Leadership Must Decide “If They Want Their

People To Eat” – Pompeo

Less than a week after US Secretary of State Secretary Mike Pompeo told Fox News Sunday that the “Iranians are responsible for the starvation’ of Yemeni civilians” he’s again issued hugely provocative words, telling the BBC during an interview that Iranian “leadership has to make a decision that they want their people to eat”in reference to the latest round of US sanctions.

As the interview was with BBC Persian, Pompeo’s words were immediately translated from English and broadcast to the Iranian public through BBC’s Persian-language publication. Pompeo repeated his theme that Iran is the world’s foremost state sponsor of terror and a “destabilizing influence” in the Middle East while ultimately blaming the country’s economic suffering on the intransigence of the country’s leaders.

Pompeo’s words came on the heels of Iran’s foreign ministry issuing a formal response to this week’s US sanctions snap back on the energy sector, publishing a 3-minute video of FM Javad Zarif on Tuesday wherein Zarif emphasized that the sanctions mainly targeted average Iranian citizens, referencing “the economic warfare that directly targets the Iranian people.”

The most contentious segment of the BBC interview was as follows:

QUESTION: You say you are not punishing the people. You say that the sanctions are not targeting the people. But what if —

SECRETARY POMPEO: No, they’re not.

QUESTION: But what if the sanctions hurt the Iranian people, the ordinary lives of them?

SECRETARY POMPEO: The folks who are hurting the Iranian people are the ayatollah and Qasem Soleimani and the Iranian leadership. That’s who is bringing the difficulties to Iran today. And you see this. You see this when you read of the protests. You see this when Iranian people have a chance to speak, although we know the human rights there don’t permit the Iranian people to speak freely. It’s the regime that is inflicting harm on the Iranian people, not the world and not the United States.

QUESTION: But as you – but you say that this is not a democratic regime. You say that the regime doesn’t care for Iranian people. But you say you do care for Iranian people.

SECRETARY POMPEO: We do.

But with hundreds of thousands of common Iranians reportedly now struggling to find life-saving medicines due to the sanctions, we doubt the Iranian public is going to be convinced of Washington’s “care” and “concern” for common Iranians.

In the weeks leading up to the November 5th round of sanctions European governments attempted to persuade the White House to agree to guarantees or waivers of Iranian imports of basic foods and medicine — pleas that were reportedly rebuffed.

Addressing the medicine issue in the BBC interview, Pompeo denied that the US was disallowing the flow of life-saving drugs into the country, and made the following assertion: “Not only are the transactions themselves exempted – that is, the transactions in medicine, for example – but the financial transactions connected to that activity also are authorized,” he said.

Pompeo also claimed that “None of the sanctions that have been imposed prevent humanitarian assistance and, indeed, there are big exemptions for medicine for sure, pharmaceuticals, but also more broadly than that for agricultural imports too.”

Saudi Crown Prince Claims Assassination Attempt Against Him Was Thwarted

BBC Arabic reports based an exclusive Jerusalem Post story that Saudi Crown Prince Mohammed Bin Salman told a group of Evangelical leaders who met with him in Riyadh earlier this month there was a recent plot to assassinate him, and that the plan was thwarted by Egyptian intelligence.

The Jerusalem Post first broke the story this week based on accounts of the returning Evangelical delegation who met with the crown prince on November 1. Joel Rosenberg, who led the delegation of American Evangelical Christians said MbS relayed that the head of Egyptian intelligence recently came to Riyadh to inform Saudi authorities that a terrorist cell with Saudi citizens had been caught in northern Sinai. “They were planning to assassinate me,” MbS told the American delegation.

Image via BloombergThe assassination plotters were reportedly arrested on Egyptian soil but it is unclear if they were transferred to Saudi Arabia or if they remain in an Egyptian prison. Likely MbS revealed the detail to elicit sympathy at a moment when for over a month he’s faced unprecedented media scrutiny over the October 2nd murder of journalist Jamal Khashoggi in Istanbul.

Image via BloombergThe assassination plotters were reportedly arrested on Egyptian soil but it is unclear if they were transferred to Saudi Arabia or if they remain in an Egyptian prison. Likely MbS revealed the detail to elicit sympathy at a moment when for over a month he’s faced unprecedented media scrutiny over the October 2nd murder of journalist Jamal Khashoggi in Istanbul.

He told the Evangelical delegation concerning Khashoggi’s death that his “enemies are exploiting this to the fullest” — perhaps implying that he’s put at greater risk of an assassination attempt or violence due to the backlash and wave of criticism he’s currently facing. He denied being behind the Khashoggi killing and condemned it as “a mistake” and a “heinous act” that will not go unpunished.

MbS further recently tried to present himself as vital to the West’s war on terror, and said further in the meeting with American pastors: “We must fight the extremists and defeat them or they will stop us and the reforms we are making to make life better for the people of Saudi Arabia.” He also vowed to shore up relations with the US and other regional allies and said: “We are fighting extremists in the ideological war and we are fighting terrorists in a physical war,” according to the Jerusalem Post.

MbS told a delegation of American Evangelical Christian Leaders in Riyadh that he was subject of an assassination plot. Interestingly, at a time when a number of international leaders have appeared to pull back public support for MbS, Israeli officials have issued rare positive words in defense of the Salman regime after recent years of quiet behind the scenes coordination with Saudi intelligence in places like Syria or Yemen. Last week Israeli Prime Minister Benjamin Netanyahu said at a summit with East European leadersin Bulgaria that while the killing of the Saudi journalist at the Saudi consulate in Istanbul was “horrendous,” stability in Saudi Arabia is vital to global security.

MbS told a delegation of American Evangelical Christian Leaders in Riyadh that he was subject of an assassination plot. Interestingly, at a time when a number of international leaders have appeared to pull back public support for MbS, Israeli officials have issued rare positive words in defense of the Salman regime after recent years of quiet behind the scenes coordination with Saudi intelligence in places like Syria or Yemen. Last week Israeli Prime Minister Benjamin Netanyahu said at a summit with East European leadersin Bulgaria that while the killing of the Saudi journalist at the Saudi consulate in Istanbul was “horrendous,” stability in Saudi Arabia is vital to global security.

Netanyahu’s frank assessment of the Khashoggi affair was as follows, according to Haaretz:

What happened in the Istanbul consulate was horrendous, and it should be duly dealt with. Yet at the same time I say that it is very important for the stability of the world, of the region and of the world, that Saudi Arabia remains stable.

Likely MbS will continue to emphasize his “war on terror” rhetoric to continue to attract positive relations with both Washington and Israel, and will also put himself forward as the victim.

Perhaps we will hear of more thwarted “assassination plots” to come from the mouths of Saudi officials, eliciting sympathy from a momentarily hostile press and world officials.

6. GLOBAL ISSUES

7 OIL ISSUES

Canada/USA

This is a key defeat for Trump as a judge blocks the construction of the Keystone XL pipeline. This is very bad for Canada

(courtesy zerohedge)

In Major Defeat For Trump, Judge Blocks Construction

Of Keystone XL Pipeline

In a setback for the Trump administration, a federal judge in Montana temporarily halted construction of the Keystone XL oil pipeline late on Thursday on the grounds that the U.S. government did not complete a full analysis of the environmental impact of the TransCanada Corp project and failed to justify its decision granting a permit for the 1,200-mile long project designed to connect Canada’s tar sands crude oil with refineries on the Texas Gulf Coast. The ruling came in a lawsuit that several environmental groups filed against the U.S. government in 2017, soon after President Donald Trump announced a presidential permit for the project.

The judge, Brian Morris of the U.S. District Court in Montana, said President Trump’s State Department ignored crucial issues of climate change in order to further the president’s goal of letting the pipeline be built. In doing so, the administration ran afoul of the Administrative Procedure Act, which requires “reasoned” explanations for government decisions, particularly when they represent reversals of well-studied actions.

Morris wrote that a U.S. State Department environmental analysis “fell short of a ‘hard look’” at the cumulative effects of greenhouse gas emissions and the impact on Native American land resources. He also ruled the analysis failed to fully review the effects of the current oil price on the pipeline’s viability and did not fully model potential oil spills and offer mitigations measures.

However, the decision does not permanently block a pipeline permit. It requires the administration to conduct a more thorough review of potential adverse impacts related to climate change, cultural resources and endangered species. The court essentially ordered a do-over.

Morris, a former clerk to the late Chief Justice William Rehnquist, was appointed to the bench by President Obama.

* * *

The ruling is a victory for environmentalists, tribal groups and ranchers who have spent more than a decade fighting against construction of the pipeline that will carry heavy crude to Steele City, Nebraska, from Canada’s oilsands in Alberta.

“The Trump administration tried to force this dirty pipeline project on the American people, but they can’t ignore the threats it would pose to our clean water, our climate, and our communities,” said the Sierra Club, one of the environmental groups involved in the lawsuit, adding that “today’s ruling makes it clear once and for all that it’s time for TransCanada to give up on their Keystone XL pipe dream.” The lawsuit prompting Thursday’s order was brought by a collection of opponents, including the indigenous Environmental Network and the Northern Plains Resource Council, a conservation coalition based in Montana.

On the other hand, the ruling was a major defeat for Trump, who attacked the Obama administration for stopping the project in the face of protests and an environmental impact study. Trump signed an executive order two days into his presidency setting in motion a course reversal on the Keystone XL pipeline as well as the Dakota Access pipeline.

In addition to the president, the ruling deals a major setback for TransCanada and could possibly delay the construction of the $8 billion, 1,180 mile (1,900 km) pipeline. It’s intended to be an extension of TransCanada’s existing Keystone pipeline, which was completed in 2013. Keystone XL (the initials stand for “export limited”) would transport up to 830,000 barrels of crude oil per day from Alberta, Canada, and Montana to Oklahoma and the Gulf Coast. In the U.S., the pipeline would stretch 875 miles through Montana, South Dakota and Nebraska, with the rest continuing into Canada.