GOLD: $1222.65 UP $8.00 (COMEX TO COMEX CLOSINGS)

Silver: $14.40 UP 9 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1221.50

silver: $14.42

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT:0 NOTICE(S) FOR nil

Total number of notices filed so far for NOV: 205 for 20500 OZ (0.6376 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3 NOTICE(S) FILED TODAY FOR

15,000 OZ/

Total number of notices filed so far this month: 1407 for 7,035,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $5661: down $93

Bitcoin: FINAL EVENING TRADE: $5638 down 130

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL 492 CONTRACTS FROM 224,372 UP TO 224,864 DESPITE YESTERDAY’S STRONG 21 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 951 EFP’S FOR DECEMBER AND 75 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1026 CONTRACTS. WITH THE TRANSFER OF 1026 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1026 EFP CONTRACTS TRANSLATES INTO 5.13 MILLION OZ ACCOMPANYING:

1.THE 21 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 7,050,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 34,073 CONTRACTS (FOR 12 TRADING DAYS TOTAL 34,073 CONTRACTS) OR 170.37 MILLION OZ: (AVERAGE PER DAY: 2839 CONTRACTS OR 14.19 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 170.37 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24/28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,596.45 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 492 DESPITE THE STRONG 21 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1026 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1518 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1026 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 492 OI COMEX CONTRACTS. AND ALL OF THUS STRONG DEMAND HAPPENED WITH A 21 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.31 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 7.050 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 7.050 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3225 CONTRACTS DOWN TO 532,702 DESPITE THE STRONG GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $5.35).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5938 CONTRACTS:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 5938 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 532,702. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED RISE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2718 CONTRACTS: 3225 OI CONTRACTS DECREASED AT THE COMEX AND 5938 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 2713 CONTRACTS OR 271,300 OZ = 8.43 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $5.35.

YESTERDAY, WE HAD 7875 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 92,573 CONTRACTS OR 9,257,300 OZ OR 287.94 TONNES (12 TRADING DAYS AND THUS AVERAGING: 7714 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY IN TONNES: 287.94 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 287.94/2550 x 100% TONNES = 11.29% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,494.75 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3225 DESPITE THE GAIN IN PRICING ($5.35) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5938 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5938 EFP CONTRACTS ISSUED, WE HAD AN GOOD RISE OF 2713 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5938 CONTRACTS MOVE TO LONDON AND 3225 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 8.33 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A GAIN OF $5.35 IN YESTERDAY’S TRADING AT THE COMEX????.

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.00 TODAY: /

A BIG CHANGES IN GOLD INVENTORY AT THE GLD/

A WITHDRAWAL OF 1.48 TONNES OF GOLD

/GLD INVENTORY 759.68 TONNES

Inventory rests tonight: 759.68 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 9 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 324.456 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 492 CONTRACTS from 224.372 UP TO 224,864 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

951 CONTRACTS FOR DECEMBER. 75 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1026 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 492 CONTRACTS TO THE 1026 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 1518 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.59 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 7.050 MILLION OZ STANDING IN NOVEMBER.

RESULT: A GOOD INCREASE IN SILVER OI AT THE COMEX DESPITE THE 21 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZED 1026 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 10.94POINTS OR 0.41% //Hang Sang CLOSED UP 30.19 POINTS OR 0.31% //The Nikkei closed DOWN 123.28 OR 0.57%/ Australia’s all ordinaires CLOSED DOWN 0.04% /Chinese yuan (ONSHORE) closed DOWN at 6.9505 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil UP to 57.18 dollars per barrel for WTI and 67.90 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.9505AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL DOWN ON THE DOLLAR AT 6.9388: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)UK

The chief whip cancels his meeting this morning as the EU hints at a revision to the Brexit. The pound temporarily rises. Still many defections and this could present huge turmoil in EU/Pound trading

( zerohedge)

ii)The truth behind the whole Brexit mess by our resident expert on this, Tom Luongo

(courtesy Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

Another sign that the global economy is slowing dramatically: October EU data continues to show no relife.

( zerohedge)

7. OIL ISSUES

the sad case of Canada’s oil crisis. Their oil is basically shut in and that is why they are getting 15 dollars per barrel

( Zaremba/Oil Price.com

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Brandon White of BMG writes gold remonetization is much closer than everybody realizes. He looks at the fact that many central banks are buying gold.(courtesy BMG/White/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

i)The dollar and the bond yields tumble on Fed Vice Chairman Clarida warning that global growth is slowing. We have been highlighting this to you for the past few years. Clarida contradicts Powell by saying that they are close to the neutral rate..whatever that means.

( zerohedge)

ii)A joke: after rising on hopes of a Chinese deal, it reversed course as humans realized the Trump-China comments meant nothing

ii)Market data/

Another indicator showing that USA economy is slowing down dramatically: this time auto assemblies tumble hurting the industrial production number.

(courtesy zerohedge)

a)This is interesting: PG and E was heading higher in morning trading despite by downgraded by Moody’s.

Why? there is a report that PG and E will not go bankrupt. However they admit that they might be responsible for the “campfire” blaze that is wrecking havoc in Northern California.

( zerohedge)

b)Dramatic shots of an entire town destroyed..P G and E states that down lines was probably the cause of the start of the “campfire” destruction.

(zerohedge)

c)Quite a story: The new Goldman CEO is outraged by the 1MDB scandal. How could this honest Goldman Sachs company enter into criminal arrangements that hurt a nation terribly.

d)This is interesting: The Wall Street Journal agrees with Trump that the Fed should stop hiking because of the damage that it is doing

e)Blain explains GE’s credit meltdown is going to be a huge problem for markets(Bill Blain)

iv)SWAMP STORIES

a)Jim Acosta’s White House credentials restored temporarily after a judge’s ruling

( zerohedge)

b)OH!! THIS IS GOOD. Judge Sullivan has ordered Hillary to answer additional questions under oath about her private email server. This is an action brought on by judicial watch

(courtesy zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 6 notices standing for a gain of 3 contacts. We had 0 notices served upon yesterday so we gained 3 contracts or an additional 15,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts.

After November, we have a December contract and here we LOST 4670 contracts DOWN to 132,193. January saw a GAIN of 19 contracts up to 1140 contracts. March, the next big delivery month after December saw a gain of 4830 contracts up to 70,016

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON NOV 16. 2017 WE HAD STILL 106,594 OPEN INTEREST CONTRACTS LEFT TO BE SERVED UPON AND THIS COMPARES TO TODAY: 133,003 CONTRACTS

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

i) into Brinks: 601,608.580 oz

Gold Rises As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

Key Gold and Precious Metals News, Commentary and Charts This Week

Gold and silver have eked out slight gains this week as stock markets came under pressure due to concerns about tech and oil sector valuations, Italian banks and political and financial turmoil due to Brexit.

Gold is 0.65% higher for the week in dollars and has seen greater gains in euro (+0.8%) and the pound (+2.17%). The latter has fallen due to political turmoil in the UK and Brexit concerns.

Weekly relative performance (Finviz.com)

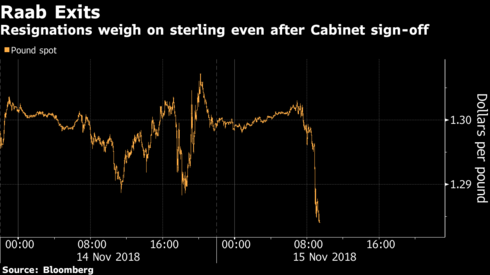

The pound tumbled after UK Brexit Secretary Dominic Raab resigned. He was the highest-profile of several departures yesterday.

Brexit backer Jacob Rees-Mogg and Prime Minster contender later joined calls for a vote of no confidence in PM Theresa May. The turmoil throws into doubt her ability to secure the UK Parliament’s support for her exit plan – and even to survive as leader.

Bookies have made the left wing Labour leader Jeremy Corbyn the favourite to take over from Mrs May – who they give 4/5 to be out before the end of 2018. This will further pressure the pound and should see gold reach new record highs in sterling terms in the months.

Stocks in the U.S., Europe and Asia are lower for the week with U.S. stocks being particularly weak. The S&P, DJIA and Nasdaq are down 2.1%, 3% and 2.8% respectively.

Oil prices have bounced a bit higher but have collapsed nearly 12% (WTI) so far in November which suggests there may be concerns about oil demand and economic growth in the coming months.

It was an important week for GoldCore as we launched the first institutional-grade gold vault in Ireland. Irish, UK and international investors can for the first time store gold bullion bars and coins in professionally managed, secure, institutional grade vaults in Dublin.

The announcement was widely picked up with Reuters, Irish Times, CNBC, Bloomberg (terminal) and others covering it and we covered it in our subsequently released Goldnomics video update.

Here is how Bloomberg covered the story:

GoldCore Offers Dublin Gold Storage as Brexit Concerns Mount

By Rupert Rowling (Bloomberg) —

Gold brokerage GoldCore has opened an institutional-grade vault near Dublin as clients are expected to move their holdings from London to other jurisdictions as Brexit concerns mount, it said in a statement.

- Storage is managed in collaboration with Loomis International.

- Since the vault’s soft launch on Oct. 15, ~30% of demand has come from GoldCore’s customers moving metal from London, CEO Stephen Flood said.

- “We expect the amount of gold stored by our clients in Dublin to exceed that of London sometime in 2019, as U.K. and Irish clients seek to spread their holdings across jurisdictions,” Flood said.

o Storage in Dublin has already surpassed Singapore and Hong Kong, and may usurp London as the No. 2 location, behind Zurich.

All in all another interesting week in the precious metal and wider markets as gold and silver slowly reassert themselves as hedging assets. They are protecting investors with exposure to stocks and indeed to currencies as was seen in gold’s gains in British pounds this week.

It represents an opportune time to rebalance portfolios and diversify out of overvalued assets and into undervalued safe haven gold.

From all the GoldCore team – have a great weekend!

Charts and Tables this Week

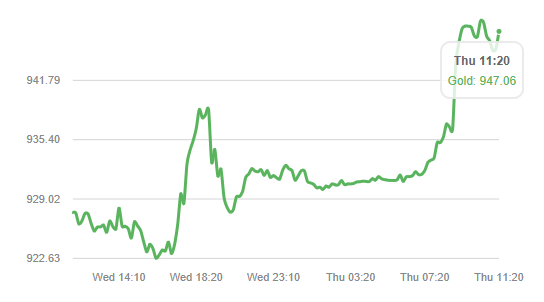

Gold in GBP – 24 Hours (GoldCore)

Source: Bloomberg

Gold to Silver Ratio via ZeroHedge.com

DJIA and Oil – 1999 to Today (Source: Marketwatch)

DJIA and Oil – 1999 to Today (Source: Marketwatch)

Market Updates and Key News this Week

Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

Investors Set To Store Gold In Dublin For First Time As Brexit Risks Grow

GoldCore Capitalising On Brexit With Dublin Gold Vault (Reuters)

Investors Start Buying Gold ETFs In October In Bullish Shift

Pound Falls Most Since 2017 as May’s Brexit Divorce Plan Rocked

Silver Cheapest To Gold In 25 Years – Watch China

American Elections Farce as Politicians Ignore the Looming $21.7 and 100 Trillion Debt Crisis

Today’s News and Commentary

PRECIOUS-Gold nears one-week high on Brexit deal logjam (Reuters.com)

Gold prices edge higher amid Brexit turmoil (Reuters.com)

Gold steady, in a range above $1210 (FXStreet.com)

Gold bugs might find hope in this chart (MarketWatch.com)

Fed plans major review of how it pursues inflation, employment goals (Reuters.com)

Italy gets support from Germany over budget spending plan (CNBC.com)

Tudor Jones says we’re in a global debt bubble and headed for some ‘scary moments’ (CNBC.com)

A disorderly Brexit will harm ‘unstable’ Italy, says former PM Letta (CNBC.com)

Bank of England’s withholding Venezuela’s gold may signal shortage in London (GoldSeek.com)

Mortgage Rates May Hit 6% Sooner – What Will that Do to Housing Bubble 2? (WolfStreet.com)

Learn More and Watch Direct Access Gold Video Here

Gold Prices (LBMA AM)

15 Nov: USD 1,210.60, GBP 948.26 & EUR 1,072.71 per ounce

14 Nov: USD 1,201.45, GBP 927.04 & EUR 1,066.05 per ounce

13 Nov: USD 1,197.55, GBP 928.70 & EUR 1,066.18 per ounce

12 Nov: USD 1,207.05, GBP 940.05 & EUR 1,072.34 per ounce

09 Nov: USD 1,219.05, GBP 936.96 & EUR 1,075.81 per ounce

08 Nov: USD 1,223.45, GBP 932.02 & EUR 1,071.01 per ounce

Silver Prices (LBMA)

15 Nov: USD 14.13, GBP 11.02 & EUR 12.49 per ounce

14 Nov: USD 13.97, GBP 10.80 & EUR 12.39 per ounce

13 Nov: USD 14.02, GBP 10.85 & EUR 12.46 per ounce

12 Nov: USD 14.16, GBP 11.00 & EUR 12.57 per ounce

09 Nov: USD 14.34, GBP 11.01 & EUR 12.63 per ounce

08 Nov: USD 14.49, GBP 11.06 & EUR 12.70 per ounce

Recent Market Updates

–– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

– GoldCore Capitalising On Brexit With Dublin Gold Vault

– Store Gold In The Safest Vaults In Ireland

– Investors Set To Store Gold In Dublin Due To Brexit Risks

– Investors Start Buying Gold ETFs In October In Bullish Shift

– As Brexit Looms and Stocks Plunge In October – Now May Be The Time to Invest in Gold

– AMERICAN ELECTIONS FARCE AS POLITICIANS IGNORE THE LOOMING $121.7 TRILLION DEBT CRISIS

– Gold ETFs See Strong Demand In Volatile October After Robust Global Gold Demand In Q3

– Venezuela Seeks To Repatriate $550 Million Of Gold From London

– Big Short’s Eisman Is Shorting Two U.K. Banks on Brexit

– “Red October” Highlights Importance of Rebalancing Portfolios and Gold’s “Very Positive” Outlook

NOV 16

Cheating Venezuela, Bank of England tempts other nations to withdraw their gold

Submitted by cpowell on Thu, 2018-11-15 18:18. Section: Daily Dispatches

1:20p ET Thursday, November 11, 2018

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly writes today that the Bank of England has no good reason to refuse to repatriate Venezuela’s gold as requested, that the refusal is blatantly political, and that it invites other nations to remove their gold from the bank now that the bank has shown itself to be an unreliable fiduciary.

Manly’s analysis is headlined “Bank of England Refuses to Return 14 Tonnes of Gold to Venezuela” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/bank-of-englands-refusal-t…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Brandon White of BMG writes gold remonetization is much closer than everybody realizes. He looks at the fact that many central banks are buying gold.

(courtesy BMG/White/GATA)

Brandon White: Gold remonetization is much closer

than many realize

Submitted by cpowell on Fri, 2018-11-16 00:57. Section: Daily Dispatches

7:58p ET Thursday, November 15, 2018

Dear Friend of GATA and Gold:

The financial world doesn’t seem to have realized it yet, Brandon White of bullion dealer BMG Group in Canada writes today for Palisade Research, but gold already has been remonetized by central banks as the ultimate risk-free asset, money without counterparty risk.

Central banks lately have been heavily buying gold, White notes, and the growing danger of another liquidity crisis is making gold even more attractive to financial managers.

White’s analysis is headlined “Gold Remonetization Is Much Closer than Many Realize” and it’s posted at Palisade Research here:

https://palisade-research.com/gold-re-monetization-2019/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Majority Of Silver Miners All-In Sustaining Costs

Significantly Higher Than The Silver Spot Price

Seven of the top nine silver miners have costs of production higher than the silver price. Here’s Steve St. Angelo to explain the implications…

by Steve St Angelo of SRSrocco Report

The Primary Silver Miners lastest results were quite dismal as their All-In Sustaining Costs to produce silver were considerably higher than the market price. Many of the silver miners production costs increased in the third quarter of 2018 due to higher energy, material, and labor costs.

Only one silver mining company out of the group posted a profit of $6.8 million for the quarter, and that was Fortuna Silver Mines. The biggest loser was Coeur Mining which suffered a $53 million loss for the period. Even the largest silver miner in the group, Pan American Silver, reported a surprise loss of $9 million Q3 2018.

Now, according to the silver mining companies All-In Sustaining Costs (AISC), only two were lower than the current silver market price:

When I put together this chart, the silver price was trading at $14.02 but has jumped up to $14.17 as the broader markets continue to sell off. However, as we can see, seven of the nine top primary silver miners AISC is higher than the silver market price (BLUE BAR). The highest AISC of $22.39 per ounce is awarded to SSR Mining which changed its name from Silver Standard. SSR Mining is mostly a gold mining company with a very high-cost open-pit silver mine in Argentina called their Puna Operations.

Back in the heyday, Silver Standard’s Piquitas Operation in Argentina was producing nearly 9 million ounces of silver (2012). Unfortunately, SSR Mining shut down operations at Piquitas last year and is now only processing stockpiles. So, with just processing stockpiles, SSR Mining’s AISC is $8 more than the current silver market price.

While Pan American Silver and Fortuna published lower AISC’s than the silver market price, the average AISC for the entire group was $16.10. Even if I was to remove the highest (SSR Mining @ $22.39) and the lowest (Fortuna @ $10.80), the average All-In Sustaining Cost of these miners would still be $15.95. Thus, the top primary silver miners average AISC is $2 higher than the present silver market price.

I find it quite interesting that the gold and silver prices continue to show strength during major selloffs in the broader markets. At some point, investors are going to rotate out of falling stocks and real estate and into the precious metals and the miners. However, FEAR has not yet made its way into the investor psyche… but it will.

Furthermore, if we consider the Free Cash Flow in the primary silver miners, they are spending $2.5 more per ounce than they are receiving from cash from operations:

The two miners with positive Free Cash Flow in Q3 2018 was Pan American Silver ($8.1 million) and Fortuna ($5.6 million). However, the majority suffered negative free cash flow with Coeur Mining being the highest at -$33.7 million. The net free cash flow for the group was a negative $52 million. Thus, the group was spending $2.6 per ounce more than the cash received from operations.

I calculated that figure by dividing the negative free cash flow of $52 million by the 19.5 million oz produced by the group.

It has been a while since I posted information on the silver miners. If you have read my articles going back to 2012, you will notice that the group is smaller. That is due to the shutdown of the Tahoe Resources Escobal Silver Mine in Guatemala, and the removal of SilverCorp Metals and another smaller company. I had 12 primary silver miners in my group, but now am only concentrating on nine.

Ever since the Muddy Waters Research came out with negative information on SilverCorp Metals, located in China, I don’t trust the company’s data. While some readers may be upset with this call, I suggest that you watch the documentary, THE CHINA HUSTLE:

In the movie, Carson Block of Muddy Waters provides details of why he believed SilverCorp Metals was not truthful with its data, which is why he shorted the stock. To be clear, I am not negative on SilverCorp Metals; rather I remain neutral in that I’d rather not use their data in my analysis. Each investor needs to make their mind up on the matter.That being said, the primary silver miners are struggling with the low silver price. While the silver price could go lower, I still believe silver is closer to a low than the stock and real estate markets. With that understanding, there is a great deal less risk owning silver today than owning most stocks and real estate.

It’s Quite Surprising That Pan American Silver Wants To Buy Troubled Tahoe Resources

Today, Pan American Silver announced its intention to purchase Tahoe Resources and its troubled Escobal Silver Mine in Guatemala that has been shut down for more than a year. You can read about my take on the Escobal Mine here: WORLD’S 2ND LARGEST SILVER MINE SHUT DOWN: Implications For Company & Market.

The local peoples living around the Escobal Mine have been against the silver project ever since the beginning. The Guatemalan Supreme Court stepped in and revoked Tahoe’s Escobal Mining license until a consultation of the indigenous communities had been taken. To me, it is a serious GAMBLE for Pan American to take on this problem.

While the Escobal Mine is the second largest primary silver mine in the world, the evidence I have read suggests that the local people do NOT WANT the mine to reopen. I have read some western articles suggesting that the local people are protesting so that they can be compensated by a percentage of the mines earnings. However, the articles coming from the local papers in Guatemala state the exact opposite. The local people want nothing to do with the mine and would like it to remain closed so they can be assured that the area around them will not be polluted and to also protect their valuable water supply for farming.

So, it will be interesting to see if Pan American Silver can resolve these issues with the local people, but I have my doubts. Of course, anything is possible, but it still surprising to see Pan American Silver acquire such a troubled asset when they could have concentrated on other projects in their pipeline.

Lastly, even though the primary silver miners are currently struggling, I believe it’s only a temporary situation. As I have stated over the past year, when the markets crack, the precious metals and the miners will be the GO-TO ASSETS. Unfortunately, most precious metals investors have given up on the metals and the miners, but this is precisely the time to start getting interested. Only successful investors buy when the price and sentiment are at an extreme low.

________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9505/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9388 /shanghai bourse CLOSED UP 10.94POINTS OR 0.41%

. HANG SANG CLOSED UP 30.19 POINTS OR 0.31%

2. Nikkei closed DOWN 123.28POINTS OR 0.57%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 97.16/Euro RISES TO 1.1337

3b Japan 10 year bond yield: FALLS TO. +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.60/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.18 and Brent: 67.90

3f Gold UP/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.36%/Italian 10 yr bond yield UP to 3.45% /SPAIN 10 YR BOND YIELD UP TO 1.63%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 3.09: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.58

3k Gold at $1217.10 silver at:14.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 18/100 in roubles/dollar) 66.04

3m oil into the 57 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.18DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0074 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1433 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.36%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.10% early this morning. Thirty year rate at 3.35%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3546

Futures Falls On Chip Carnage As World Await Brexit Verdict

Stocks in Europe faded early gains and S&P futures fell after a mixed session in Asia as chip stocks were taken to the woodshed on poor guidance from Nvidia and Applied Materials sparked fears that the chip bull run is over, while investors wondered whether China and America can de-escalate their trade war after mixed signals by US officials just days before the G-20 summit.

The euro failed to rebound while the sterling halted its biggest drop in 2 years after some of the most dramatic 24 hours yet in the Brexit process and another turbulent week for world markets. With reports of a UK leadership coup still rife and fear that the country could crash out of the EU without an agreement, cable struggled to rise above $1.28.

Meanwhile traders around the world were waiting for an outcome from the ongoing Brexit saga: “If and when a vote on the withdrawal agreement occurs is uncertain. Whether the withdrawal bill is passed by both houses of Parliament is uncertain,” Joseph Capurso, a senior currency strategist at CBA, said in a note. “Whether the Prime Minister resigns or is challenged for the leadership is uncertain. And, whether there is a second referendum and/or an election is uncertain.”

Fears over political turmoil in the UK and Italy dragged Europe’s Stoxx 600 back into the red, set for its first weekly drop in three, trimming Friday’s gain as AstraZeneca’s drop weighed on the gauge after a cancer-drug setback while telecom names were outperforming. Utilities started the session lower in the wake of yesterday’s ECJ decision which deemed the UK’s scheme for ensuring power supplies during the winter months as a violation of state aid rules. Other individual movers include Vivendi (+4.2%) sit at the top of the Stoxx 600 after posting impressive Q3 sales metrics and announcing a potential sale of part of their Universal Music Group division. Elsewhere, AstraZeneca (-2.3%) and Shire (-1.3%) have been seen lower throughout the session after both posting disappointing drug updates.

Not helping sentiment, ECB head Mario Draghi said the bank still plans to dial back its stimulus at the end of the year, but acknowledged the economy had hit a soft patch and inflation may rise more slowly than expected. “If firms start to become more uncertain about the growth and inflation outlook, the squeeze on margins could prove more persistent,” Draghi told a conference.

Earlier in the day, Asian shares ended the session in the red (MSCI Asia -0.2% to 151.52), led lower by declines in Japan, even as China and Hong Kong rose after initial reports the United States might pause further China tariffs were denied by Commerce Secretary Wilbur Ross who damped hopes of any imminent trade deal with China. The Nikkei fell 0.6% pressured by a drop in the USDJPY after China Mofcom began an investigation into alleged dumping of machine tools by Japanese firms. The Hang Seng (+0.3%) and Shanghai Comp. (+0.4%) swung between gains and losses after continued liquidity inaction by the PBoC which skipped Reverse Repos for a 16th consecutive occasion.

S&P futures were hit on fresh slowdown concerns, this time out of the semiconductor/chip space, after Nvidia gave a dire sales forecast, projecting a 20% drop in revenue while a disappointing outlook from Applied Materials indicated the chip industry is holding off on expansion plans in the face of a murky outlook for electronics demand. The chipmaking sector saw another bout of selling in Asia, wiping at least $11.2 billion in market value amid signals that demand for servers, personal computers and mobile is falling.

Also falling after hours were shares of AMD and Intel, dragging Nasdaq futures lower.

“It started with Apple, then Nvidia … Since performances of these companies set the tone for the global tech and chip industries, related Japanese stocks will likely be sluggish for a while,” said Takatoshi Itoshima, a strategist at Pictet Asset Management.

The Bloomberg Dollar Spot Index was little changed after Fed Chairman Powell flagged his concern over potential headwinds for the U.S. economy, while the pound staged a modest rebound on reports that some pro-Brexit ministers decided to stay in their governmental posts. The pound gained as U.K. Prime Minister Theresa May defied demands to quit and amid reports her environment secretary wouldn’t resign, following the resignation of several ministers Thursday. The yen rallied as trade stress simmered, with investors trying to gauge whether China and the U.S. can de-escalate their dispute.

Also under water was the cryptocurrency Bitcoin, which hit a one-year trough overnight. It had tumbled 10 percent early in the week when support at $6,000 gave way. It was last changing hands at $5,500 on the Bitstamp platform.

Treasuries were steady while 10-year yields on German bonds were set for their biggest weekly fall in three weeks, in a sign that the Brexit uncertainty and worries about Italy’s finances, continued to support demand. Italian bonds edged higher even as European Commission Vice President Valdis Dombrovskis said in an interview with Il Sole 24 Ore that the country’s government was openly defying EU budget rules. Emerging-market currencies consolidated recent gains while oil prices extended their rebound.

Oil prices rose, helped by a decline in U.S. fuel stockpiles and the possibility of a cut in OPEC output. Brent (+1.3%) and WTI (+1.1%) are both in the green and continuing their rebound seen yesterday with WTI hovering around USD 57.00bbl. Energy newsflow remains light, post-yesterday’s DoE report, however, Iraq’s North Oil Co. have announced that they have resumed Kiruk oil exports heading towards the Turkish port of Ceyhan. Looking ahead, the main highlight on the calendar will be the Baker Hughes rig count. Elsewhere, natural gas futures are relatively steady after their 19% decline yesterday which came in the wake of a 20% increase the day before.

In geopolitical news, US Republican and Democrat Senators filed a bipartisan bill seeking to suspend arms sales to Saudi Arabia in response to war in Yemen and killing of journalist. North Korean Leader Kim inspected test of new high-tech tactical weapons, according to Yonhap citing North Korean state media

Today’s data include October industrial production and capacity utilization. Viacom is among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.3% to 2,725.25

- STOXX Europe 600 down 0.01% to 358.38

- MXAP down 0.2% to 151.52

- MXAPJ up 0.2% to 486.84

- Nikkei down 0.6% to 21,680.34

- Topix down 0.6% to 1,629.30

- Hang Seng Index up 0.3% to 26,183.53

- Shanghai Composite up 0.4% to 2,679.11

- Sensex up 0.5% to 35,446.11

- Australia S&P/ASX 200 down 0.1% to 5,730.55

- Kospi up 0.2% to 2,092.40

- Brent futures up 1.2% to $67.41/bbl

- Gold spot up 0.3% to $1,216.36

- U.S. Dollar Index little changed at 96.93

- German 10Y yield rose 0.8 bps to 0.368%

- Euro up 0.2% to $1.1346

- Italian 10Y yield rose 0.3 bps to 3.12%

- Spanish 10Y yield fell 1.4 bps to 1.617%

Top Overnight News

- Fed Chairman Jerome Powell has laid out a scenario for a pause in the central bank’s interest-rate hiking campaign sometime next year by highlighting potential headwinds to the U.S. economy.

- British Prime Minister Theresa May is defying demands to quit as she battles to keep control of her fractious government long enough to deliver a Brexit deal that’s drawn ire from across the political spectrum.

- Pro-Brexit ministers Michael Gove, Liam Fox, Chris Grayling, Penny Mordaunt and Andrea Leadsom have decided together not to quit the government, Times reporter Tim Shipman said on Twitter.

- ECB’s Draghi sees no reason for expansion to come to abrupt end, he said at an event in Frankfurt, Germany.

- PG&E Corp. rallied as much as 49 percent in extended trading Thursday after the head of the California Public Utilities Commission said he can’t imagine allowing the state’s largest utility to go into bankruptcy as it faces billions of dollars in potential liability from deadly wildfires

- Deutsche Bank AG and Bank of America Corp. have been contacted by U.S. criminal investigators for information about transactions they handled for a small bank branch in Estonia that’s at the center of one of the biggest money-laundering investigations in history, according to two people familiar with the matter.

Asia-Pac stocks traded indecisively as the region lacked fresh catalysts and as uncertainty regarding Brexit and US-China trade played on investor’s minds. ASX 200 (-0.1%) and Nikkei 225 (-0.6%) were choppy with outperformance of tech and mining names in Australia overshadowed by a lacklustre broader market, while the Japanese benchmark was subdued by mild flows into the JPY and after China Mofcom began an investigation into alleged dumping of machine tools by Japanese firms. Elsewhere, Hang Seng (+0.3%) and Shanghai Comp. (+0.4%) swung between gains and losses after continued liquidity inaction by the PBoC which skipped OMOs for a 16th consecutive occasion, while participants were also tentative amid ongoing trade uncertainty after conflicting reports regarding the next round of China tariffs being placed on hold which USTR Lighthizer later denied. Finally, 10yr JGBs were mildly higher with prices underpinned amid an indecisive tone seen in stocks and with the BoJ also present in the market for JPY 680bln of JGBs in the belly to super-long end.

Top Asian News

- China’s Kindergarten Crackdown Is the Latest Disaster for Stocks

- Modi Is Said to Enlist Tata for Jet Airways Rescue Ahead of Vote

- Philippines Shuts 3 Miners, Suspends 9 Others After Review

- Indian Central Bank Board to Discuss Surplus Funds Transfer

European equities trade relatively flat (Eurostoxx 50 +0.2%) in the wake of mixed trade headlines overnight for the US and China. Performance across European indices is relatively equal whilst focus once again falls on the FTSE 100 (U/C) which remains at the whim of Brexit-inspired fluctuations in the GBP. Once again, potential upside for the index is being capped by losses in domestically focused banking names (RBS -3.0%, Lloyds -2.1%) as Brexit uncertainty continues to dampen investor sentiment. In terms of sector specifics, most sectors are trading higher with mild outperformance seen in telecom names. Utilities started the session lower in the wake of yesterday’s ECJ decision which deemed the UK’s scheme for ensuring power supplies during the winter months as a violation of state aid rules. Other individual movers include Vivendi (+4.2%) sit at the top of the Stoxx 600 after posting impressive Q3 sales metrics and announcing a potential sale of part of their Universal Music Group division. Elsewhere, AstraZeneca (-2.3%) and Shire (-1.3%) have been seen lower throughout the session after both posting disappointing drug updates.

Top European News

- Finnish Software Company Basware Is Said to Explore Sale

- Vauxhall Owner Said to Weigh Closing a Factory Post-Brexit

- Amid Brexit Gloom, Deutsche Bank Sees Frankfurt as Next London

- Nyrstar Surges on Hopes Over Trafigura Refinancing Talks

Currencies:

- GBP – The Pound is not the biggest net mover for a change, but still one of the most volatile and vulnerable as Cable pivots 1.2800 and Eur/Gbp trades between 0.8850-80. The fall-out from Wednesday’s Cabinet meeting continues as UK PM May strives to sell the Brexit draft, but facing a rising rebellion within the Conservative Party that appears to have reached the critical mass required to trigger a no confidence vote. However, some positive news with a key Minister deciding not to follow others out of the Government, as Gove opts to stay rather than go. In terms of technical impulses, Cable is holding above yesterday’s 1.2725 low, ahead of chart support around 1.2710-00 that protects mtd and ytd troughs at 1.2696 and 1.2662 respectively, while near term resistance is seen around 1.2836 before 1.2850, but 1 bn option expiries at 1.2800 could well exert more influence into the NY cut. For Eur/Gbp, several MAs form support blow 0.8850 and the 100 DMA at 0.8910 may hamper further gains if 0.8900 is breached.

- JPY – Maintaining a firm underlying safe-haven bid as broad risk sentiment remains fragile and China is reportedly investigating machine dumping by Japan – Usd/Jpy near the bottom of a 113.20-65 range.

- EUR/CAD/CHF – All narrowly mixed vs the Greenback, with the single currency keeping afloat of 1.1300 and eyeing a Fib at 1.1358, while the Loonie is holding recent recovery gains through 1.3200 as oil prices continue their rebound and the Franc meanders between 1.0075-50 vs 1.1000+ earlier this week when the broad Dollar and DXY were in the ascendency (index well above 97.000 vs just below the figure presently).

- EM – The Lira is off best levels, but still relatively bid after reports that the US could Turkish cleric Gulen in an attempt to assuage President Erdogan to adopt a less aggressive stance against Saudi Arabia over the Khashoggi killing. Usd/Try now near the middle of a 5.3240-3940 band.

In commodities, gold (+0.2%) is trading relatively flat after hitting new weekly highs of USD 1218.39/oz earlier in the session; following uneventful overnight trade. Elsewhere, Shanghai Zinc prices have risen due to London Metal Exchange stockpiles falling to decade-low levels. Brent (+1.3%) and WTI (+1.1%) are both in the green and continuing their rebound seen yesterday with WTI hovering around USD 57.00bbl. Energy newsflow remains light, post-yesterday’s DoE report, however, Iraq’s North Oil Co. have announced that they have resumed Kiruk oil exports heading towards the Turkish port of Ceyhan. Looking ahead, the main highlight on the calendar will be the Baker Hughes rig count. Elsewhere, natural gas futures are relatively steady after their 19% decline yesterday which came in the wake of a 20% increase the day before.

US Event Calendar

- 9:15am: Industrial Production MoM, est. 0.2%, prior 0.3%; Manufacturing (SIC) Production, est. 0.2%, prior 0.2%

- 11am: Kansas City Fed Manf. Activity, est. 11, prior 8

- 4pm: Total Net TIC Flows, prior $108.2b, Net Long-term TIC Flows, prior $131.8b

DB’s Jim Reid concludes the overnight wrap

Yesterday was an extraordinary day where we saw rival factions go into battle, huge infighting, disloyalty, a colossal power struggle, and lots of head scratching over who will win out and where this is all going to end. Indeed, the teaser trailer for the final Game of Thrones series out next April was finally released. However, a remarkable 3 hour UK parliamentary session where PM May was grilled from all sides of the House of Commons probably topped it for drama even if it lacked the CGI effects.

Before we lay out our views on what’s happened over the last 24 hours in our homeland, it’s worth quickly recapping what markets have done as unlike in previous months, it’s not just Sterling which has borne the brunt.

Yes, the Pound did fall -1.65% relative to the Dollar for the biggest one-day decline since October 2016. It was also down -1.86% against the Euro. More dramatic was the move for Gilts where 10y yields rallied -13.3bps and the most since August 2016. They are also now down -37.6bps from the intraday October highs and there’s now only about 12.5bps of hikes priced in for next year by the BoE. In equities, the overseas earnings-focused FTSE 100 closed flat but the more domestically orientated FTSE 250 ended -1.31%. The sector breakdowns were starker with an index of UK homebuilders closing down -6.76% and the most since the referendum in June 2016 and UK banks selectively weak. RBS at one stage tumbled -10.20% intraday before closing -9.63%. Barclays and Lloyds were down -4.11% and -5.04% respectively. The biggest movers in credit indices were unsurprisingly UK assets too. Looking across iTraxx Main, nine of the top 10 widest credits were UK names with the top three being Marks & Spencer (+17bps), Barclays (+17bps) and RBS (+16bps). How much of these moves were Brexit specific and how much were concerns about what a Jeremy Corbyn led Labour Party General Election win might mean for various companies was difficult to disentangle.

The pain for UK assets spread throughout Europe too, with the DAX, CAC and FTSE MIB finishing -0.52%, -0.70% and -0.90%. Bunds rallied -3.7bps and are now down to 0.358% and testing the October lows again. Treasuries also rallied slightly, with 2- and 10-year yields down -1.5 and -1.2bps. US equities rallied strongly throughout the afternoon session in New York, with the S&P 500 retracing losses of as much as -1.14% to close +1.06%, for the 15th widest trading range of the year. Other major indexes staged similar rebounds, with the DOW up +0.83% and the NASAQ gaining +1.72%. The price action reflected a partial unwind of the last few sessions’ sharp moves, with the best-performing sectors being those that had recently sold off. Energy gained +1.47%, as WTI oil rallied +0.46%, and tech advanced +2.46%. Sentiment was also boosted by comments from US Commerce Secretary Ross, in which he described the upcoming meeting between Presidents Trump and Xi as “the big event” and said that “if it goes well, it’ll set the framework for going forward.” This suggests that there is scope for real compromise later this month at the November 30-December 1 G20 summit.

This morning in Asia, markets are largely up following Wall Street’s lead with the exception of Japan. The Hang Seng (+0.29%), Shanghai Comp (+0.71%) and Kospi (+0.40%) are all higher along with most Asian markets while the Nikkei (-0.29%) is down. Elsewhere, futures on the S&P 500 (-0.21%) are pointing towards a softer open.

So back to the main story. All eyes now are on whether or not we’ll get a vote of no confidence for PM May. The remarkable 3 hour Parliamentary session yesterday left you feeling in no uncertain terms that the Withdrawal Agreement (WA) is highly unlikely to pass in its current form. However, before we even get there, the leadership challenge is the next hurdle. The odds of such a contest appeared to substantially increase yesterday with headlines speculating that close to the required 48 MPs had written to the Conservative 1922 Committee including arch-Brexiteer Jacob Rees-Mogg. This came after two cabinet members yesterday resigned including Dominic Raab – the Brexit Secretary. PM May reportedly offered Tory MP Michael Gove – one of the staunchest Brexiteers – the job of Brexit minister to replace Raab, though media reports suggested that he will resign his post completely instead, which would be a negative signal for May’s ability to keep her coalition together. Other junior ministers also resigned through the day. Overnight, the Telegraph reported that the DUP will scrap its coalition with the Conservatives unless/until PM May is replaced. This would be materially negative news for the embattled PM and for markets, but the pound traded flat amid thin overnight liquidity.

The dilemma for those Brexiteer Tories wanting a leadership contest is that if they force one and May survives (she only needs a majority but, in reality, a narrow win could make her position untenable) she is safe from a challenge for 12 months. The dilemma for those Brexiteers voting against her WA is that this may lead to a series of events that brings a second referendum and the possibility of no Brexit at all. The dilemma for the remain Tory MPs is that if they vote against either or both of Mrs May and the WA, it may topple Mrs May and lead to a leadership challenge. It is highly likely that a hard Brexiteer will be one of the two candidates put to the grass root membership, and given demographics they would have a strong chance of winning and would thus pursue a harder Brexit. So no side has the upper hand at the moment.

As discussed above, the last twenty four hours have illustrated that there is seemingly no parliamentary majority for the current WA. At the same time, there is little prospect of further negotiation with the EU27, given the limited timeline. As DB’s Oliver Harvey wrote yesterday, May is therefore trapped in a bind. The only way to secure parliamentary support for the current deal will be under considerable market pressure, perhaps after multiple failed votes. There are two other options perhaps. One is a pivot towards a much softer form of Brexit – such as EEA membership plus a permanent customs union – however it’s not clear if there’s sufficient time on the EU side to agree to this. The other is a second referendum. This in itself would likely split the Tory Party although it would likely gain parliamentary support. The difficulty will be deciding what question to pose to electors. Some suggest there might be two.

Believe it or not, there was some non-Brexit newsflow yesterday. In Italy, Deputy PM Salvini’s Chief Economic Advisor Claudio Borghi made headlines by responding to a tweet in a manner that seemed to imply that if the League gets a majority in the next election, then Italy would exit the Eurozone. In fairness, this wasn’t how I read the reply but markets traded off the headlines and didn’t really look for the tweet. It was entirely inconsistent with what he’s said in the past and he later denied it outright. However, Italian assets did still react and underperformed post the headline. BTPs sold off +8.9bps from their strongest intraday level, but ultimately closed flat. Elsewhere the US announced sanctions against a total of 17 Saudi Arabian officials concerning the death of Khashoggi. Those sanctions including freezing assets of the officials and limiting access to the US financial system.

The Turkish Lira was already gaining yesterday, but was boosted further by reports that the US is considering removing the Turkish cleric Fethullah Gulen from US territory and ultimately closed +1.94% stronger. Turkish authorities have accused Gulen of coordinating an attempted coup in 2016, though the US has not endorsed the claims. If confirmed, the move by the US would represent a considerable thaw in relations between the two countries after they reached a nadir earlier this year.

Meanwhile the economic data that was out was truly a sideshow however for completeness, euro area new car registrations fell -7.3% yoy in October. This partially reflects the idiosyncrasies associated with new emissions rules and shows some bounce back from September’s -23.5% decline. The euro area’s seasonally adjusted trade balance printed at 13.4bn euros, a touch softer than expected. In the UK, retail sales fell -0.5% mom and softened to +2.2% yoy, versus expectations for +0.2% and +2.8%. Core retail sales missed by a similar margin. In contrast, October US retail sales beat expectations, rising +0.8% mom (versus expected +0.5%), though the control group marginally missed, rising +0.3% versus expected +0.4%. November activity surveys from the Philadelphia and New York Federal Reserve Banks were mixed, with the Philly index dropping to 12.9 from 22.2 and the NY index rising to 23.3 from 21.1.

Before we take a look at day ahead, in credit, Michal in our team published a one-pager “After Red October, Better Credit Fund Flows in November So Far” in which he provides an update on recent IG fund flows and puts them in the broader context of other asset classes. You can download the report here . Now as for the day ahead, well it’s hard to look past anything other than Brexit headlines dominating. However there are some data releases due. In Europe we’ll get final October CPI revisions for the Euro Area and Italy while in the US we’ll get October industrial production and the November Kansas City Fed PMI. We’ll also hear from ECB President Draghi this morning in Frankfurt before the Bundesbank’s Weidmann speaks at the same event this afternoon. Over at the Fed, Evans speaks in the afternoon. Oh and their might be some Brexit headlines to consider.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 10.94POINTS OR 0.41% //Hang Sang CLOSED UP 30.19 POINTS OR 0.31% //The Nikkei closed DOWN 123.28 OR 0.57%/ Australia’s all ordinaires CLOSED DOWN 0.04% /Chinese yuan (ONSHORE) closed DOWN at 6.9505 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil UP to 57.18 dollars per barrel for WTI and 67.90 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.9505AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL DOWN ON THE DOLLAR AT 6.9388: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

UK

The chief whip cancels his meeting this morning as the EU hints at a revision to the Brexit. The pound temporarily rises. Still many defections and this could present huge turmoil in EU/Pound trading

(courtesy zerohedge)

Chief Whip Cancels Morning Meeting As EU Hints At Revision To Brexit

‘Backstop’

Update (8 am ET): The pound is spiking heading into the US trading day, moving back above $1.28, as the anxieties over a potential leadership challenge and mass exodus of May’s cabinet.

Some encouraging developments in the late morning: Parliament chief whip has canceled a meeting with lawmakers about the Brexit deal, according to Buzzfeed. And in an encouraging sign that the EU and the UK might be able to iron out some of the more controversial aspects of the backstop, EU ministers are expected to focus on changing the wording of the deal to stop it from potentially binding the UK to the customs union “indefinitely”. This would ameliorate the biggest concern voiced by intransigent Tory MPs.

Still, the confusing contradictory reports about a ‘no confidence’ vote have continued:

Jessica Elgot

✔@jessicaelgot

This morning we are being briefed that the 48 letters have been reached and also that they have not been reached, and also that people are taking time to think at the weekend and also that they are already over the limit. The only person who actually knows is Graham Brady.

* * *

Update (7:15 am ET): As reports out of Westminster suggest that the threshold for a ‘no confidence’ vote in Theresa May has been reached, No. 10 insists that it hasn’t.

Laura Hughes

✔@Laura_K_Hughes

Downing Street source says it’s not true they are preparing for a no confidence motion.

* * *

Update (7 am ET): Tory MP Steve Baker says his list of no-confidence letters suggests that the 48-vote threshold has been reached, with perhaps another 12 coming in on top of that.

Though it’s impossible to say for sure because people are “sometimes coy”.

Laura Kuenssberg

✔@bbclaurak

Steve Baker confirms his list does indeed suggest 48 letter threshold has been reached with maybe a dozen more – but he says impossible to know for sure because colleagues aren’t sometimes coy about what they have actually done

* * *

Update (6:30 am ET): As of 11:30 London Time on Friday, the count for publicly disclosed letters of no confidence in May submitted to the conservatives’ 1922 committee stands at 20…the threshold for calling a vote is 48.

Laura Kuenssberg

✔@bbclaurak

Public number of letters calling for May to go is 20 …. so hard to know if 48 threshold has been reached yet or will be today or over weekend

Laura Kuenssberg

✔@bbclaurak

Public number of letters calling for May to go is 20 …. so hard to know if 48 threshold has been reached yet or will be today or over weekend

Laura Kuenssberg

✔@bbclaurak

Brexiteers hoping they’ll get there unambiguously today

Brexiteers understand that they probably wouldn’t win a no confidence vote. But their plan is to use the vote to demonstrate to May that her draft plan wouldn’t pass in the Commons. More conflicting reports about whether the European Research Group has passed the 48-letter threshold circulated on Friday. But the only man who knows for sure is Tory kingmaker Graham Brady, the MP in charge of the Tory’s 1922 committee.

Here’s a list of MPs who have submitted, or said they plan to submit, letters of no confidence (courtesy of BBG):

- Jacob Rees-Mogg

- Mark Francois

- John Whittingdale

- Steve Baker

- Henry Smith

- Simon Clarke

- Anne Marie Morris

- Lee Rowley

- Sheryll Murray

- Martin Vickers

- Adam Holloway

- Ben Bradley

- Maria Caulfield

Submitted previously:

- Nadine Dorries (some weeks ago)

- Laurence Robertson (a few months ago)

- Andrew Bridgen (July)

- Andrea Jenkyns (June)

- Peter Bone (BBC – submitted some time ago)

- Philip Davies (July)

- James Duddridge (a month ago)

* * *

As May scrambles to stop any further resignations, No. 10 Downing Street insists that there will be a new Brexit secretary by the end of the weekend. Some have even suggested that May should take on the role in addition to her prime ministerial duties. Others have speculated that Trade Secretary Liam Fox would be the logical candidate.

* * *

After what was presumably a “long night of the soul” for Environment Secretary Michael Gove, the Tory cabinet minister has decided to split the difference in terms of decisions that would disappoint and delight his boss, Prime Minister Theresa May. He won’t take the Brexit Secretary post vacated on Thursday by Dominic Raab. But – for now, at least – the “tortured” Gove won’t be resigning, according to the London Times.

Laura Kuenssberg

✔@bbclaurak

Gove is NOT resigning – source close to him says ‘Michael is staying at Defra. He thinks it is important to continue working with Cabinet colleagues to ensure the best outcome for the country’

Though some sources said he could still quit by the end of the weekend.

Tiernan Douieb

✔@TiernanDouieb

Michael Gove is ‘tortured’? Finally some news about him I like hearing!

But that was about all of the good news for May, who is facing another brutal day of trying to rally fractured Tories behind what she firmly insists is the ‘best deal possible.’ Shortly after former culture secretary John Whittingdale became the latest Tory to announce he had submitted a letter of no-confidence in May, the embattled prime minister did the next logical thing: She sat for a 30-minute radio interview where she continued to try and sell her deal and insisted she would carry on as prime minister.

Following the interview, which received mixed reviews and which ended with a question comparing May with Neville Chamberlain, the prime minister was confronted with reports that the 1922 committee (the private committee for the Conservative Party in the House of Commons) had received the requisite 48 letters to call for a ‘no confidence’ vote in May. According to media reports, the vote could happen in the coming days (though, in a repeat of the drama from Thursday, those reports were swiftly refuted).

Amid all these news, the GBPUSD has been pegged firmly against 1.28, waiting for any major news to break one way or the other.

Circling back to Gove, looked chipper this morning as he confronted the horde of reporters lurking outside his London home.

The scrutiny was understandably intense, with CNN offering this trenchant analysis of the ‘breakfast indicator’.

It appears that Michael Gove is carrying a paper bag from Patisserie Valerie, a British cafe chain that’s in deep financial trouble. Is this a subtle message? Its chief executive resigned on Thursday. His name? (Paul) May.

And as one reporter noted: “stranger things have happened.”

Robert Peston

✔@Peston

Gove not resigning. Well stranger things have happened

And although May has insisted that a “People’s Vote” on the deal (which would function as effectively a second Brexit referendum) won’t happen, Labour MPs insist that such a vote is growing increasingly likely (as their chances of seizing power grow). Tom Watson, Labour’s deputy leader, has said a fresh referendum on Brexit is now “more likely,” according to the Independent.

With Gove sticking around, reporters are turning their attention to another restive senior member of May’s government: International Development Secretary Penny Mordaunt. Approached about her resignation plans this morning, Mordaunt insisted: “I’ve got nothing to say.” Though, according to the latest round of reports, the UK press doesn’t expect any more resignations on Friday as Mordaunt and Commons leader Andrea Leadsom have reportedly agreed to stay on.

With UK markets still recovering from the brutality of Wednesday and especially Thursday, Bloomberg has published a handy guide that functioned more like a warning: All of those analysts who projected a drop in the pound below $1.25 if May’s deal is ultimately defeated might be conservative. They even invoked the memory of the October 2016 ‘flash crash’.

But if lawmakers reject the deal, the currency vigilantes may re-emerge en masse over the low-liquidity Christmas period, ratcheting up pressure on a divided Parliament. Remember the 6% flash crash in October 2016 when the pound was pummeled in just one minute in thin Asian trading?

But it wouldn’t even take an outright rejection of the deal to reawaken the ‘currency vigilantes’. Indeed, as anybody who has been watching the tape probably could guess, they are already with us.

end

The truth behind the whole Brexit mess by our resident expert on this, Tom Luongo

(courtesy Tom Luongo)

May Forces Brexit Betrayal To Its Crisis Point

The only words that were left out of Theresa May’s announcement of achieving Cabinet approval over her Brexit deal were Mission Accomplished.

Theresa May was put in charge of the U.K. to betray Brexit from the beginning. She always represented the interests of the European Union and those in British Parliament that backed remaining in the EU.

No one in British ‘high society’ wanted Brexit to pass. No. One.

No one in Europe’s power elite wanted Brexit to pass. No. One.

No one in the U.S.’s power elite wanted Brexit to pass. No. One.

When it did pass, The Davos Crowd began the process of sabotaging it. The fear mongering has done nothing but intensify. And May has done nothing but waffle back and forth, walking the political tight rope to remain in power while trying to sell EU slavery to the both sides in British Parliament.

We’re 29 months later and the U.K. is no closer to being out of the EU than the day of the vote. Why?

Because Theresa May’s 585 page ‘deal’ is the worst of all possible outcomes. If it passes it will leave the EU with near full control over British trade and tax policy while the British people and government have no say or vote in the matter.

It’s punishment for the people getting uppity about their future and wanting something different than what had been planned for them.

Mr. Juncker and his replacement will never have to suffer another one of Nigel Farage’s vicious farragoes detailing their venality ever again. YouTube will get a whole lot less interesting.

It’s almost like this whole charade was designed this way.

Because it was.

May has tried to run out the clock and scare everyone into accepting a deal that is worse than the situation pre-Brexit because somehow a terrible deal is better than no deal. But, that’s the opposite of the truth.

And she knows it. She’s always known it but she’s gone into these negotiations like the fragile wisp of a thing she truly is.

There’s a reason I call her “The Gypsum Lady.” She’s simply the opposite of Margaret Thatcher who always knew what the EU was about and fought to her last political breath to avoid the trap the U.K. is now caught in.

The U.K. has had all of the leverage in Brexit talks but May has gone out of her way to not use any of it while the feckless and evil vampires in Europe purposefully complicate issues which are the height of irrelevancy.

She has caved on every issue to the point of further eroding what’s left of British sovereignty. This deal leaves the U.K. at the mercy of Latvia or Greece in negotiating any trade agreement with Canada. Because for a deal between member states to be approved, all members have to approve of it.

So, yeah, great job Mrs. May. Mission Accomplished. They are popping champagne corks in Brussels now.

But, this is a Brexit people can be proud of.

Orwell would be proud of Theresa May for this one.

You people are leaving. Let the EU worry about controlling their borders. And if Ireland doesn’t like the diktats coming from Brussels than they can decide for themselves if staying in the EU is worth the trouble.

The entire Irish border issue is simply not May’s problem to solve. Neither is the customs union or any of the other stuff. These are the EU’s problems. They are the ones who don’t want the Brits to leave.

Let them figure out how they are going to trade with the U.K. It is so obvious that this entire Brexit ‘negotiation’ is about protecting the European project as a proxy for the right of German automakers to export their cars at advantageous exchange rates to the U.K. at everyone’s expense.

Same as it was in the days of The Iron Lady.

If all of this wasn’t so predictable it would be comical.

Because the only people more useless than Theresa May are the Tories who care only about keeping their current level of the perks of office.

The biggest takeaway from this Brexit fiasco is that even more people will check out of the political system. They will see it even more clearly for what it is, an irredeemable miasma of pelf and privilege that has zero interest in protecting the rights of its citizens or the value of their labor.

It doesn’t matter if it’s voter fraud in the U.S. or a drawn out betrayal of a binding referendum. There comes a point where those not at the political fringes look behind the veil and realize changing the nameplate above the door doesn’t change the policy.

And once they realize that confidence fails and systems collapse.

Brexit was the last gasp of a dying empire to assert its national relevancy. Even if this deal is rejected by parliament the process has sown deep divisions which will lead to the next trap and the next and the next and the next.

By then Theresa May will be a distant memory, being properly rewarded by her masters for a job very well done.

* * *

Please support the production of independent and alternative political and financial commentary by joining my Patreon and subscribing to the Gold Goats ‘n Guns Investment Newsletter for just $12/month.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

I) Saudi Arabia

6. GLOBAL ISSUES

Another sign that the global economy is slowing dramatically: October EU data continues to show no relife.

(courtesy zerohedge)

Global Auto Industry Collapse Continues As October EU Data Shows No Relief

The outlook for the global automobile market has been increasingly dire lately, especially after a third quarter that saw sales drop in many major markets across the globe, including China. Now, the latest data from Europe suggests that the difficulties may be nowhere close to over despite optimistic fourth quarter guidance by companies like Volkswagen and Daimler AG.