I HAVE BEEN OUT OF COMMISSION FOR THE MOST PART OF THE DAY

SO I MISSED QUITE A FEW STORIES

I HAVE RETRIEVED ALL THE DATA SO IT IS UP TO DATE.

H.

GOLD: $1214.65 UP $5.35 (COMEX TO COMEX CLOSINGS)

Silver: $14.31 UP 21` CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1214.30

silver: $14.31

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT:0 NOTICE(S) FOR nil

Total number of notices filed so far for NOV: 205 for 20500 OZ (0.6376 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1404 for 7.020,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $5643: down $291

Bitcoin: FINAL EVENING TRADE: $5725 down 211

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A TINY 26 CONTRACTS FROM 224,346 UP TO 224,372 WITH YESTERDAY’S 10 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 4195 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 4195 CONTRACTS. WITH THE TRANSFER OF 4195 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4195 EFP CONTRACTS TRANSLATES INTO 20.98 MILLION OZ ACCOMPANYING:

1.THE 10 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 7,035,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 33,047 CONTRACTS (FOR 11 TRADING DAYS TOTAL 33,047 CONTRACTS) OR 165.23 MILLION OZ: (AVERAGE PER DAY: 3004 CONTRACTS OR 15.02 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 165.23 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,591.32 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 26 WITH THE 10 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 4195 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 4221 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4195 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 26 OI COMEX CONTRACTS. AND ALL OF THUS STRONG DEMAND HAPPENED WITH A 10 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.10 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 7.035 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 7.035 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3593 CONTRACTS DOWN TO 535,927 DESPITE THE STRONG GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $8.15).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7875 CONTRACTS:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7875 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 538.899. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED RISE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7254 CONTRACTS: 3593 OI CONTRACTS DECREASED AT THE COMEX AND 7875 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4282 CONTRACTS OR 428,200 OZ = 13.31 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $8.15.

YESTERDAY, WE HAD 7804 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 85,635 CONTRACTS OR 8,583,500 OZ OR 266.96 TONNES (11 TRADING DAYS AND THUS AVERAGING: 7776 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY IN TONNES: 266.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 266.96/2550 x 100% TONNES = 10.46% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,476.29 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 3593 DESPITE THE GAIN IN PRICING ($8.15) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7875 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7875 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC RISE OF 25,940 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7875 CONTRACTS MOVE TO LONDON AND 3593 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 13.31 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A GAIN OF $8.15 IN YESTERDAY’S TRADING AT THE COMEX????.

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.35 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 761.16 TONNES

Inventory rests tonight: 761.16 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 21 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 324.456 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY 26 CONTRACTS from 224.346 UP TO 224.372 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

4195 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4195 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 26 CONTRACTS TO THE 4195 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 4221 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 21.10 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 7.035 MILLION OZ STANDING IN NOVEMBER.

RESULT: A STRONG INCREASE IN SILVER OI AT THE COMEX DESPITE THE 10 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZED 4195 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 35.93POINTS OR 1.36% //Hang Sang CLOSED UP 448.91 POINTS OR 1.75% //The Nikkei closed DOWN 42.86 OR 0.20%/ Australia’s all ordinaires CLOSED UP 0.05% /Chinese yuan (ONSHORE) closed UP at 6.9395 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 56.26 dollars per barrel for WTI and 66.53 for Brent. Stocks in Europe OPENED MIXED//. ONSHORE YUAN CLOSED UP AT 6.9395AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL UP ON THE DOLLAR AT 6.9354: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCE

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

Japan now records it’s second decline in GDP in the last 3 reporting periods. QE is having no effect on its economy. The entire globe is now proving to a trainwreck in too many places. If you want to see what will happen in the USA and Europe, just take a close look at the results inside Japan

(courtesy Jeffrey Snider/Alhambra Investment Partners)

3 C/ CHINA

i)The yuan barely moves as China sends trump a written response to trade reforms but offers insufficient concessions

( zerohedge)

ii)Kyle Bass doubles down on his yuan short and states that he expects a Chinese reset in the next couple of years

4/EUROPEAN AFFAIRS

i)UK

Brexiteer leader Moog demands a no confidence vote. Britain is in chaos this morning. Domenic Raab, key cabinet figure resigns.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

I) Saudi Arabia

Five Saudis face the death penalty over the Khashoggi killing. So far the Crown Prince has been cleared..

( zerohedge)

ii)TURKEY/USA

6. GLOBAL ISSUES

More evidence of a global slowdown: the world’s largest shipper Maersk has sounded the alarm bell on a global slowdown. They label the trade war as a catalyst for the slowdown

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)The Times of India is celebrating the central bank’s decision to buy gold along with its citizens and as such they are selling USA treasuries.

ii)Yes, what a world: the hoarder of gold coins in Iran has been hanged along with his assistant( Bloomberg/GATA)

iii)Craig Hemke is calling gold to rise as the shorts are squeezed. Let us see if he is right

( Craig Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

P G and E imploding

(courtesy zerohedge)

ii)Market data/

a)The power of the Fed

a great read…

( Brandon Smith/Alt Market.com

b)This will definitely slow the housing market as mortgage rates climb closer to 6%

(courtesy Wolf Richter/WolfStreet)

iv)SWAMP STORIES

a)Avenatti arrested for hitting a woman. He feels he will be fully exonerated

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 3 notices standing for a loss of 3 contacts. We had 3 notices served upon yesterday so we gained 0 contracts or an additional nil oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts.

After November, we have a December contract and here we LOST 2063 contracts DOWN to 136.863. January saw a loss of 125 contracts up to 1121 contracts. March, the next big delivery month after December saw a gain of 1495 contracts up to 65,186.

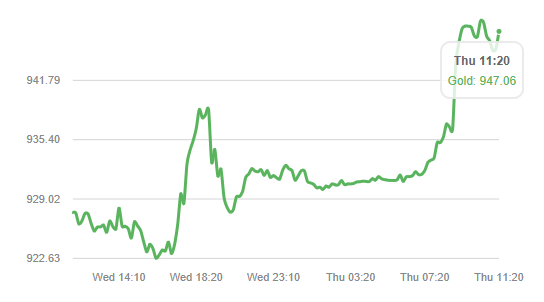

Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

The pound plunged against the euro, the dollar, gold and all leading currencies today as Theresa May’s UK government appeared vulnerable to collapsing and political turmoil risked creating a hard Brexit.

Gold in GBP (24 Hours)

The pound has fallen 2.6% against gold in less than twenty four hours seeing gold rise from £923 to £947 per ounce in sterling terms.

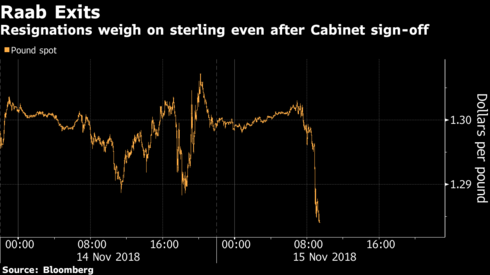

The pound slumped the most in more than 17 months as several U.K. ministers resigned less than 24 hours after Prime Minister Theresa May said she had won cabinet approval for a deal with the European Union.

Brexit Secretary Dominic Raab handed in his resignation to Theresa May over the controversial Brexit proposal.

Mr Raab said he could not support the Prime Minister’s withdrawal agreement from the European Union. He wrote: “It has been an honour to serve in your government as Justice Minister, Housing Minister and Brexit Secretary. I regret to say that following the Cabinet meeting yesterday on the Brexit deal I must resign.”

Financial analysts are concerned about the more ‘extreme’ outcomes to Brexit talks and that potential worst case Brexit risks may now come about.

This makes the pound vulnerable to further falls into year end and in 2019. Longer term, the pound is likely to weaken further as Brexit uncertainty and fallout impacts the slowing UK high street, prperty market and wider economy.

Gold’s record nominal high in sterling terms over £1,120 per ounce looks like being surpassed in 2019 with gold prices just 20% below that now.

News and Commentary

Pound Falls Most Since 2017 as May’s Brexit Divorce Plan Rocked (Bloomberg.com)

Crude’s Collapse Is Sending Shockwaves Across Global Markets (Bloomberg.com)

Gold prices hold steady as dollar eases (Reuters.com)

Paulson keeps stake in gold investments during third-quarter (Reuters.com)

Dow turns negative, giving up 200-point gain, as Apple rolls over (CNBC.com)

Gold: Rising gold price vindicates RBI’s investment plan (EconomicTimes)

Source: Bloomberg

Chaotic 2019 coming & gold will be the ‘best house in a bad neighborhood’ (MarketWatch.com)

Gold Spikes Back Above $1200, Silver Above $14 (ZeroHedge.com )

As Oil Plunges, Energy Junk Bonds Turn Dangerous — Again (GoldSeek.com)

At Some Point the Whole Thing Blows Up (Youtube.com)

Gold Re-Monetization Is Much Closer Than Many Realize (Palisade-Research.com)

Apple Enters Bear Market – Down Over $200 Billion From Record Highs (ZeroHedge.com)

Gold Prices (LBMA AM)

14 Nov: USD 1,201.45, GBP 927.04 & EUR 1,066.05 per ounce

13 Nov: USD 1,197.55, GBP 928.70 & EUR 1,066.18 per ounce

12 Nov: USD 1,207.05, GBP 940.05 & EUR 1,072.34 per ounce

09 Nov: USD 1,219.05, GBP 936.96 & EUR 1,075.81 per ounce

08 Nov: USD 1,223.45, GBP 932.02 & EUR 1,071.01 per ounce

07 Nov: USD 1,235.05, GBP 938.64 & EUR 1,074.62 per ounce

Silver Prices (LBMA)

14 Nov: USD 13.97, GBP 10.80 & EUR 12.39 per ounce

13 Nov: USD 14.02, GBP 10.85 & EUR 12.46 per ounce

12 Nov: USD 14.16, GBP 11.00 & EUR 12.57 per ounce

09 Nov: USD 14.34, GBP 11.01 & EUR 12.63 per ounce

08 Nov: USD 14.49, GBP 11.06 & EUR 12.70 per ounce

07 Nov: USD 14.67, GBP 11.15 & EUR 12.77 per ounce

Recent Market Updates

– GoldCore Capitalising On Brexit With Dublin Gold Vault

– Store Gold In The Safest Vaults In Ireland

– Investors Set To Store Gold In Dublin Due To Brexit Risks

– Investors Start Buying Gold ETFs In October In Bullish Shift

– As Brexit Looms and Stocks Plunge In October – Now May Be The Time to Invest in Gold

– AMERICAN ELECTIONS FARCE AS POLITICIANS IGNORE THE LOOMING $121.7 TRILLION DEBT CRISIS

– Gold ETFs See Strong Demand In Volatile October After Robust Global Gold Demand In Q3

– Venezuela Seeks To Repatriate $550 Million Of Gold From London

– Big Short’s Eisman Is Shorting Two U.K. Banks on Brexit

– “Red October” Highlights Importance of Rebalancing Portfolios and Gold’s “Very Positive” Outlook

– Alarm Bells Ring and Gold Rises In October As Stocks and Property Fall Globally

– Gold Analysts At LBMA See 25% Return To $1,532/oz In 12 months

– Gold Improves Investment, Pension and Central Bank Portfolio’s Risk-Adjusted Returns

NOV 14

Times of India celebrates central bank’s buying gold, selling treasuries

Submitted by cpowell on Wed, 2018-11-14 14:31. Section: Daily Dispatches

Rising Gold Price Vindicates RBI’s Investment Plan

By Gayatri Nayak

The Times of India, Mumbai

Monday, November 12, 2018

MUMBAI — The Reserve Bank of India’s gold purchase plan seems to be paying off as the monthly valuation gains have touched an eight-month high with investor demand for a safe haven rallying the yellow metal.

The value of gold in the country’s foreign exchange reserves rose 1.7 percent in three weeks from October 12 to November 2 at $20.9 billion. Gold prices rose 2 percent during the same period.

India’s reserves are at $393 billion and gold comprises about 5 percent of the total reserves. ...

With currency markets turning volatile since December after the U.S. Federal Reserve started raising interest rates, which caused foreign investors to pull out their funds from the emerging markets including India, the Reserve Bank, like many other central banks, started buying gold as a hedge against volatile currency markets.

It was for the first time in nine years that the RBI was buying gold. It has bought 9.5 lakh troy ounces of gold since December 2017. …

RBI has already sold close to $17 billion worth of U.S. treasury securities between April and August, data with the U.S. Treasury Department showed. This could help the central bank rein in mark-to-market losses.

… For the remainder of the report:

https://economictimes.indiatimes.com/markets/commodities/news/rising-gol…

END

Yes, what a world: the hoarder of gold coins in Iran has been hanged along with his assistant

(courtesy Bloomberg/GATA)

What a world: ‘Sultan of Coins’ is hanged but Jamie Dimon and Blythe Masters live

Submitted by cpowell on Wed, 2018-11-14 18:40. Section: Daily Dispatches

Iran Hangs Gold Coin ‘Sultan’ in Crackdown After U.S. Sanctions

By Ladane Nasseri

Bloomberg News

Wednesday, November 14, 2018

Iran executed a gold dealer known as the “Sultan of Coins” in a warning to merchants not to exploit the country’s financial troubles as U.S. sanctions squeeze the economy.

Vahid Mazloumin was sentenced to death in October after being accused by Iranian authorities of contributing to price hikes by hoarding gold. His assistant, Mohammad Esmail Qassemi, was also hanged early today, state-run Iranian Students News Agency said.

The very specter of sanctions, even before they were resumed in August, plunged the Iranian currency market into turmoil and sent the rial plummeting about 70 percent against the dollar, fueling a surge in prices and encouraging illegal trading.

Mazloumin didn’t hold a permit to trade gold and foreign currency, yet had formed the largest illegal network in that area, according to state-run Fars news agency. He instructed his team to corner the gold coin market to resell at higher prices, amassing about 2 tons of them, local media said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-11-14/as-sanctions-hit-iran…

END

Craig Hemke is calling gold to rise as the shorts are squeezed. Let us see if he is right

(courtesy Craig Hemke/GATA)

Craig Hemke at Sprott Money: Here comes another squeeze of gold shorts

Submitted by cpowell on Wed, 2018-11-14 20:46. Section: Daily Dispatches

3:47p ET Wednesday, November 14, 2018

Dear Friend of GATA and Gold:

Having lured fund managers into shorting gold futures by pushing the price below the 50-day moving average, bullion banks are about to trigger a short squeeze by yanking the price up again, according to the TF Metals Report’s Craig Hemke, writing at Sprott Money.

Hemke writes: “As with each of the past four years, we expect a year-end rally in Comex gold that extends into January. Whether or not this next spec short squeeze sets off that rally will be a function of timing. We’ll wait to see how it plays out. In the meantime, what’s important is that you know it’s coming and can take action to plan and prepare.”

Hemke’s analysis is headlined “Another Gold Spec Short Squeeze Pending” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/another-gold-spec-short-squeeze-pending…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9395/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9354 /shanghai bourse CLOSED UP 35.93POINTS OR 1.36%

. HANG SANG CLOSED UP 448.91 POINTS OR 1.75%

2. Nikkei closed DOWN 42.86POINTS OR 0.20%

3. Europe stocks OPENED ALL MIXED

/USA dollar index RISES TO 97.11/Euro FALLS TO 1.1318

3b Japan 10 year bond yield: FALLS TO. +.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.60/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.26 and Brent: 66.53

3f Gold DOWN/JAPANESE Yen UP/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.37%/Italian 10 yr bond yield UP to 3.49% /SPAIN 10 YR BOND YIELD UP TO 1.63%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 3.12: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.55

3k Gold at $1209.75 silver at:14.13 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 42/100 in roubles/dollar) 67.64

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.46DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0052 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1367 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.37%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.10% early this morning. Thirty year rate at 3.35%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3959

Global Rally Shattered, Europe Slides As Brexit Turmoil Returns

US futures pared earlier gains, European stocks slumped and the pound tumbled after the Brexit crisis returned with a bang to the forefront after a series of British ministers quit in protest at Theresa May’s Brexit deal, plunging the U.K. government into crisis and sparking fresh fears about a May ouster and a hard Brexit.

Today’s turmoil started around 4am ET when Brexit Secretary Dominic Raab announced his resignation on Twitter, the highest profile of several departures on Thursday morning. “No democratic nation has ever signed up to be bound by such an extensive regime, imposed externally without any democratic control over the laws to be applied, nor the ability to decide to exit the arrangement,” he said in his resignation letter. His, and subsequent resignations, threw into doubt May’s ability to secure Parliament’s support for her plan and even to survive as leader.

Dominic Raab

✔@DominicRaab

Today, I have resigned as Brexit Secretary. I cannot in good conscience support the terms proposed for our deal with the EU. Here is my letter to the PM explaining my reasons, and my enduring respect for her.

The pound, which rebounded strongly on Wednesday after May announced she had won cabinet support for the withdrawal draft, tumbled 3 big figures almost instantly on the news, dropping as much as 1.9%, its biggest plunge since 2017.

“The reaction is sterling shows that the chance of no Brexit deal has spiked,” said Tim Graf, Head of Macro Strategy for EMEA at State Street Global Markets. “It also introduces thoughts of a leadership challenge (for British Prime Minister Theresa May) which seems likely now.”

While the prime minister defended her plan as the only way to protect the union of the U.K when addressing law makers in the House of Commons, the renewed threat that May could be replaced and Britain could crash out of the EU with no deal is an unpredictable and high-risk scenario for markets. As the resignations rolled in, the FTSE 100 Index trimmed gains as trading volumes soared to double the 30-day average while gilts surged. European stocks, which started the session in the green, pared all gains and dropped to yesterday’s lows, down 0.4%.

“The truth is no one can accurately predict how this will play over the next few days and weeks,” said Epworth Investment Management Chief Investment Officer Stephen Beer. “However, in some important respects, nothing has changed since the referendum. It remains the case that Brexit is likely to be economically worse for the U.K. than remaining in the European Union. What we have now is more people realizing that.”

S&P 500 had been solidly up before they pared much of their advance, although they have since rebounded to near session highs once more. The yen rose, and gold and the Swiss franc were steady, suggesting the market was not too concerned by the latest Brexit turmoil.

The S&P 500 had fallen for a fifth straight day overnight, with financial stocks hit by fears of tighter regulations once the Democratic Party takes control of the House of Representatives. U.S. stocks were also pressured by concerns that earnings growth might be peaking, trade tensions and a slowing global economy – factors that had triggered a rout in riskier assets in October.

The European turmoil followed a relatively calm Asian session with the MSCI Asia index rising 0.8%, as Hong Kong shares jumped after Tencent earnings beat expectations while Chinese equities rose 1.4%, cheering news that China and the United States were back in contact about their bitter trade disputeas after a report that Chinese officials had sent a letter to the White House outlining a series of potential concessions to the Trump administration, despite subsequent reports that the offering by China was insufficient to meet Trump’s demands. Japanese stocks edged lower while the Australian dollar jumped after a strong local jobs report.

There was some good news overnight: in a closely watched question-and-answer session late on Wednesday Federal Reserve Chairman Jerome Powell played down recent turbulence in equities, saying volatility was only one of many factors that the Fed takes into account. Then again, Powell’s admission confirmed that the Fed put is hundreds of points lower than the S&P’s latest price, which likely means that stocks have a long way to fall before Powell gets truly concerned about the Fed’s beloved “wealth effect.”

UK turmoil also boosted demand for safe-haven German government bonds. Ten-year Bund yields fell over three basis points to 0.36 percent, the lowest in over two weeks.

“While it’s difficult to pin-point a specific event for the risk-off move, recent themes appear to be keeping markets cautious include oil’s recent plummet, Apple’s fall, U.S. political gridlock, China’s slowing growth, tightening liquidity, a hawkish Fed, earnings peak, Italian jitters, and Brexit uncertainty,” wrote economists at ANZ.

Elsewhere, West Texas crude resumed its slide following Wednesday’s rebound from a record losing streak. Emerging-market shares rallied and their currencies strengthened.

“If U.S. stocks are to bounce back, economic indicators will be key,” said Junichi Ishikawa, senior forex strategist at IG Securities in Tokyo. “Focus will be on today’s U.S. retail sales data, which will provide a view of how private consumption -the main component of economic growth- is faring.” U.S. retail sales for October will be released today at 830am ET.

Market Snapshot

- S&P 500 futures little changed at 2,696.50

- STOXX Europe 600 down 0.3% to 361.05

- MXAP up 0.8% to 151.53

- MXAPJ up 1.2% to 485.20

- Nikkei down 0.2% to 21,803.62

- Topix down 0.1% to 1,638.97

- Hang Seng Index up 1.8% to 26,103.34

- Shanghai Composite up 1.4% to 2,668.17

- Sensex up 0.5% to 35,317.74

- Australia S&P/ASX 200 up 0.06% to 5,736.02

- Kospi up 1% to 2,088.06

- German 10Y yield fell 3.9 bps to 0.359%

- Euro up 0.09% to $1.1320

- Italian 10Y yield rose 4.3 bps to 3.117%

- Spanish 10Y yield rose 2.8 bps to 1.646%

- Brent futures little changed at $66.12/bbl

- Gold spot little changed at $1,210.57

- U.S. Dollar Index up 0.6% to 97.34

Top Overnight News from Bloomberg

- Prime Minister Theresa May is fighting for her political life as a growing revolt from within her own party threatens to derail her Brexit plans and force the U.K. out of the European Union with no deal

- Chinese officials have outlined a series of potential concessions to the Trump administration for the first time since the summer as they continue to try to resolve a trade war, according to three people familiar with the discussions

- Federal Reserve Chairman Jerome Powell said the U.S. economy is strong but could face headwinds next year as policy makers weigh how far and fast to raise interest rates

- Apple’s outlook dims as suppliers worldwide sound the alarm, with Austrian-based AMS AG the latest to sound the alarm

- A Saudi royal adviser and a senior intelligence official played key roles in the mission that ultimately led to the killing of government critic Jamal Khashoggi and authorities will seek the death penalty for five people who confessed to the murder

Asian equity markets were eventually mostly higher after the region gradually shrugged off the cautious lead from the losses stateside, where weakness in tech and financials saw all US majors finish in the red. ASX 200 (+0.1%) and Nikkei 225 (-0.2%) were lower throughout most the session as financials lagged although the Australian benchmark staged a late rebound and just about turned positive at the close, while sentiment in Tokyo remained pressured by a firmer currency and as blue-chip banking stocks declined post-earnings. Elsewhere, Hang Seng (+1.7%) and Shanghai Comp. (+1.4%) weathered a choppy start as outperformance in tech kept Chinese markets afloat after a beat on earnings from Hong Kong index-giant and China’s largest tech firm Tencent Holdings. Finally, 10yr JGBs were flat with only minimal support seen despite the losses in Tokyo stocks and with price action also muted following mixed results in today’s 5yr JGB auction. China’s government is said to have sent a written response to the US concerning trade reforms, which reports noted offered insufficient concessions.

Top Asian News

- Tencent-Backed Fashion Site Is Said to Halve IPO Valuation Goal

- Tencent’s Big Beat Falls Flat With Analysts Pining for New Games

- Takeda Offers Mega-Euro Bond Amid Renewed Brexit Upheavals

- Philippines Delivers Fifth Rate Hike to Curb Inflation

European indices are mixed, with the FTSE MIB (-0.5%) lagging alongside broad underperformance in Italian assets. Furthermore, Prysmian (-4.3%) have also weighed on the index after a guidance cut and STMicroelectronics (-2.5%) are lower in sympathy with AMS (-1.3%) who cut guidance pre-market. FTSE 100 (+0.1%) is bucking the trend as recent Brexit updates are weighing on Cable. However, upside for the index is being capped by losses in RBS (-7.3%) and Barclays (-6.0%) in the wake of the rate implications of today’s Brexit turmoil. Elsewhere, Antofagasta (+2.1%) are lower following board approval of expansion to the Los Pelambres copper mine. In contrast Royal Mail (-5.2%) are in the red after reporting lower half year pre-tax profit.

Top European News

- Raab Resignation Means Higher Risk Brexit Deal Fails: Nordea

- Pound Could Fall to $1.25 After Raab, Says Mizuho’s Jones

- Raab Resignation Signals Parliament Vote Challenge: Danske

- Soubry: Raab’s Resignation Marks End of PM’s Withdrawal Pact

- In Brexit Brinkmanship, Europe Was Always Going to Be The Winner

- European Car Sales Slump Again, Testing VW’s Upbeat Outlook

- Four Weeks That Will Determine Fate of the ECB’s Bond Buying

In FX, all eyes were on GBP as the Post-UK Cabinet approval of the withdrawal draft has been extremely short-lived, as Brexit Minister Raab resigned due to reservations over the proposal, followed by McVey (Work and Pensions Secretary and other not as high profile (so far) Government officials. Significantly weaker than forecast retail sales data merely compounded the misery for Sterling, but probably won’t be the final straw amidst reports of more MPs and aides considering their position and an official leadership challenge against PM May. Cable collapsed from 1.3000+ through 1.2900 and the recent 1.2828 low to circa 1.2750 at one stage, with only the November base at 1.2696 protecting the ytd trough (1.2662) aside from any psychological or sentimental support at 1.2700. Meanwhile, Eur/Gbp rallied from around 0.8700 to 0.8845, breaching some interim chart resistance at 0.8766 on the way, and without much effort, before partially retracing. EUR – Although the single currency is benefiting from the Gbp’s demise, it has lost ground vs the Usd after running into offers at 1.1350, but is holding in well above recent lows not far from 1.1200 and may be relatively contained by hefty option expiries at 1.1300 and 112.50-60 in 1.5 bn and 1.6 bn respectively. AUD – The clear G10 outperformer and retaining the bulk of its overnight gains vs the Greenback on the back of an upbeat Aussie jobs report – Aud/Usd currently around 0.7260 within a 0.7300-0.7230 range, and with the Aud/NZD cross back above 1.0650 as the Kiwi pivots 0.6800 against the Usd. DXY – The Dollar is mixed vs major counterparts and broadly weaker against EM currency, but the index has rebounded firmly above 97.000, largely due to the aforementioned Pound rout and knock-on effects.

In commodities, gold (+0.9%) prices have extended gains above USD 1200/oz as the dollar continues to fall from the 16-month highs that were reached at the start of the week. Separately, copper has been boosted following China sending a written response to US trade reforms, although it has been noted that it offers insufficient concessions. Brent (-0.1%) and WTI (-0.2%) initially traded higher, and were mostly unaffected by the larger than expected build in API inventory. but have since reverted into negative territory following the dollar beginning to strengthen again. Of note reports that Russia have cut oil output to 11.38mln BPD for the first two weeks of November. Markets will be looking ahead to the EIA weekly data later today.

As for today’s calendar,the highlight is the October retail sales report which will be a first look for forecasters into Q4 consumer spending. The consensus is for a +0.5% mom headline reading, and +0.4% readings for the core and control group components – the latter of course important as it’s a direct input into the BEA’s estimate of consumers’ spending on goods in the GDP numbers. Away from that we’ll also get regional November manufacturing reports from the NY and Philly Fed’s, October import price index, initial jobless claims, and September business inventories. Away from the data it’s another busy day for ECB speakers with Coeure, Praet and de Guindos due to speak. The Fed’s Quarles will also appear before the Senate, before Chair Powell speaks again – albeit on hurricane recovery efforts so it’s unlikely to be market sensitive – and Bostic and Kashkari speak tonight. Oh and there might be a few more Brexit headlines.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 20, prior 21.1

- 8:30am: Philadelphia Fed Business Outlook, est. 20, prior 22.2

- 8:30am: Retail Sales Advance MoM, est. 0.5%, prior 0.1%; Ex Auto MoM, est. 0.5%, prior -0.1%;

- Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.0%; Retail Sales Control Group, est. 0.4%, prior 0.5%

- 8:30am: Import Price Index MoM, est. 0.1%, prior 0.5%; 8:30am: Import Price Index YoY, est. 3.3%, prior 3.5%

- 8:30am: Export Price Index MoM, est. 0.05%, prior 0.0%; 8:30am: Export Price Index YoY, prior 2.7%

- 8:30am: Initial Jobless Claims, est. 213,000, prior 214,000; Continuing Claims, est. 1.63m, prior 1.62m

- 9:45am: Bloomberg Consumer Comfort, prior 61.3

- 10am: Business Inventories, est. 0.3%, prior 0.5%

- 10am: Fed’s Quarles to Appear before Senate Banking Panel

- 11:30am: Fed’s Powell Reviews Post-Hurricane Harvey Recovery Efforts

- 1pm: Fed’s Bostic Speaks in Madrid

- 3pm: Fed’s Kashkari Speaks to Minnesota AgriGrowth Council

DB’s Jim Reid concludes the overnight wrap

Before we get into Brexit, inflation, oil and the likes I’d like to ask the more experienced parents out there if your children have ever had a more insignificant part in a nativity play than my three year old Maisie has just been given. In her pre-school performance at Xmas she’s been cast as a “bell”. I’ll resist the urge to storm into school and ask why she’s not playing Mary.

The bells looked like they were tolling for PM May’s Brexit deal yesterday morning, as the initial political response to her withdrawal agreement proved to be quite negative and the pound shed as much as -0.73% at its intraday lows. However, May ended the day by again rising from the flames and securing Cabinet approval for her plan, and the pound ultimately rallied +0.16% on the day to just below $1.30 by the US close but traded between $1.2882 and $1.3072 during a turbulent session.

The pound did close off the immediate cabinet backing highs as PM May described the outcome as “collective agreement,” conspicuously avoiding the word “unanimous” in a possible acknowledgement of internal pushback. The government then released the almost 600-page withdrawal agreement, which will be scrutinised by MPs and the press over the coming days for any surprises. The Parliamentary arithmetic still looks quite dicey, and it’s noteworthy that Boris Johnson waited 48 hours after Chequers to resign, so PM May is certainly still exposed to further dissent/resignations from her cabinet in the hours and days ahead.

The good thing about Brexit is that most other things that are going on in markets right now feel fairly straightforward by comparison. Despite WTI oil finally snapping its unwanted record-breaking run of 12 consecutive daily declines with a rebound of +0.84% yesterday, US markets struggled once again yesterday with the NASDAQ leading the way with a -0.90% decline, followed closely by the S&P 500 (-0.76%) and DOW (-0.81%). Apple underperformed again, down -2.82% as investors continued to digest the news of reduced upstream demand from the company’s suppliers. That’s five trading sessions in a row that the S&P has dropped now which is the third worst run this year following the two six-day consecutive loss runs in October. We’ve now had 27 down days over the 39 trading days since the index peaked on September 20, the longest such streak since November 2008 amid the post-Lehman fallout.

Late last night we did have some non-Brexit related news when Fed Chair Powell spoke positively about the US economy and downplayed concerns about financial market volatility. He argued that the US economy can continue to grow and can even pick up pace in the future, though he did note some downside risks from fading fiscal stimulus, slower growth abroad, and any greater-than-expected impacts of rate hikes. Powell mentioned that credit spreads remain tight, suggesting that it will take broader risk-off price action in markets to affect his reasoning than just an equity selloff. Finally, he asserted that all meetings will be “live” moving forward, since they will now all be accompanied by press conferences.

This morning in Asia, markets are off to a mixed start with the Nikkei (-0.50%) down while the Hang Seng (+0.61%), Shanghai Comp (+0.68%) and Kospi (+0.10%) are all up. Elsewhere, futures on the S&P 500 (-0.17%) are pointing towards a slightly negative start.

Credit markets are starting to get more and more attention of late especially in the US. Even Powell mentioned them last night – albeit in a positive light. As a reminder, our view has been that US HY has been far too expensive this year. Other indices have hit our targets, but HY has stubbornly held in. This week, the downgrade of GE has first rocked IG credit and then the significant re-pricing of oil has had an impact on HY energy bonds once again. Just to recap on US HY, in October we finally saw some cracks start to appear as spreads widened more than 70bps (tight to wide). Whilst the first week of November seemed to bring some reprieve to credit markets, the last few days have seen some further notable moves wider. USD HY has widened the best part of +40bps with HY energy more than +50bps wider. Both series are now at their wides for the year with USD HY now more than +30bps wider YTD. USD IG has widened nearly 10bps from the recent November tights and is up against their YTD wides. Similarly EUR IG and HY credit is now also at the wides for the year at around 45bps and 150bps wider respectively.

Back to markets yesterday, sentiment was actually initially positive at the open following a marginally dovish US CPI report (more on that below) but weakness soon followed and equity markets in Europe failed to hold onto an intraday recovery with the STOXX 600 finishing down -0.60% and DAX -0.52%. Bond markets were once again a sideshow with Treasuries (-1.8bps) and Bunds (-1.1bps) a touch stronger.

Talking of European equities our strategist Sebastian Raedler has published his 2019 market outlook this morning. He sees upside for the Euro area and China PMI over the coming months, implying tactical upside for the Stoxx 600 to 385 by Q1, 6% above current levels. However, from Q2 onwards, he sees renewed downside for the market as the Euro area real bond yield (i.e. the discount rate for European equities) starts rising on the back of a recovery in Euro area core inflation and the EUR appreciates in line with our FX strategists’ projections, leading the Stoxx 600 to fade to 345 by end-2019, 5% below current levels. See here for the report.

Moving on. It wouldn’t be a recap without mentioning Italy and it was interesting to hear DB’s Clemente De Lucia’s take on the letter Italy sent to Brussels late Tuesday which broadly confirmed the original version of the DBP. In Clemente’s view, the tone of the letter was tough suggesting that a compromise with Brussels is a long way from being reached. The new, higher levels of planned privatisation is very unlikely to change the mind of the Commission. Such initiatives are very difficult to monitor and, in the past, Italy have missed their targets. As for where things stand now, a Eurogroup meeting is scheduled for December 3rd, which means we could see an EDP launched as soon as early next month. It could be an interesting final month of the year for politics in Europe with this and Brexit. The FTSE MIB closed down -0.78% yesterday and slightly underperformed the rest of Europe, while 2y and 10y BTPs rose +4.8bps and +4.5bps respectively. Talking of politics, our German experts last night published a piece on what Merkel succession race means for Europe. See here for more.

In other news, yesterday was a packed day for data although there wasn’t a huge amount to move the dial. In Germany, Q3 GDP came in slightly weaker than the downwardly revised forecast at -0.2% qoq. The first negative quarterly print since early 2015 is likely to be temporary though, with new car emissions tests disrupting car production. In France the final October CPI print was confirmed at +0.1% mom and unrevised versus the flash, while here in the UK, CPI missed to the downside slightly at +0.1% mom (vs. +0.2% expected) for the headline level, although the core did hold at +1.9% yoy as expected. Shortly after that euro area GDP for Q3 was confirmed at +0.2% qoq as expected.

Meanwhile, as mentioned above the October CPI report in the US was at the margin a tad disappointing in the context of a small rounding down in the annual rate for the core to +2.1% yoy from +2.2%. The six-month annualised reading is also now down to +1.95% which is food for thought for the Fed maybe. The October reading itself was confirmed at +0.2% mom as consensus expected (+0.1926% unrounded) with positive payback from used cars in particular.

As for today’s calendar, this morning in Europe we’ve got October retail sales data out in the UK first thing, followed later on by the September trade balance reading for the euro area. In the US the highlight is the October retail sales report which will be a first look for forecasters into Q4 consumer spending. The consensus is for a +0.5% mom headline reading, and +0.4% readings for the core and control group components – the latter of course important as it’s a direct input into the BEA’s estimate of consumers’ spending on goods in the GDP numbers.

Away from that we’ll also get regional November manufacturing reports from the NY and Philly Fed’s, October import price index, initial jobless claims, and September business inventories. Away from the data it’s another busy day for ECB speakers with Coeure, Praet and de Guindos due to speak. The Fed’s Quarles will also appear before the Senate, before Chair Powell speaks again – albeit on hurricane recovery efforts so it’s unlikely to be market sensitive – and Bostic and Kashkari speak tonight. Oh and there might be a few more Brexit headlines.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 35.93POINTS OR 1.36% //Hang Sang CLOSED UP 448.91 POINTS OR 1.75% //The Nikkei closed DOWN 42.86 OR 0.20%/ Australia’s all ordinaires CLOSED UP 0.05% /Chinese yuan (ONSHORE) closed UP at 6.9395 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 56.26 dollars per barrel for WTI and 66.53 for Brent. Stocks in Europe OPENED MIXED//. ONSHORE YUAN CLOSED UP AT 6.9395AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED WELL UP ON THE DOLLAR AT 6.9354: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING SLIGHTLY WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

Japan now records it’s second decline in GDP in the last 3 reporting periods. QE is having no effect on its economy. The entire globe is now proving to a trainwreck in too many places. If you want to see what will happen in the USA and Europe, just take a close look at the results inside Japan

(courtesy Jeffrey Snider/Alhambra Investment Partners)

3 C CHINA

The yuan barely moves as China sends trump a written response to trade reforms but offers insufficient concessions

(courtesy zerohedge)

China Sends Trump Written Response To Trade Reform Demands, Offers Insufficient Concessions

Ahead of the much-anticipated meeting between presidents Trump and Xi on the sidelines of a G20 summit in Argentina at the end of November during which hopes run high for at least a modest de-escalation of trade tensions, on Wednesday China delivered a written response to U.S. demands for wide-ranging trade reforms, a move which according to Reuters could trigger negotiations to bring an end to a withering trade war between the world’s top economies.

Reuters’ sources said that China had sent a written response to Trump’s demands on intellectual property theft, industrial subsidies, Chinese entry barriers to American businesses and the U.S. trade deficit with China, although it was unclear if the response contained concessions that would satisfy Trump’s demands for change.

For the actual contents of the letter, we have to go to Bloomberg which reports that the text “outlines a series of potential concessions to the Trump administration for the first time since the summer” as they continue to try to resolve a trade war between the world’s two largest economies.

However, the commitments – for now – fall short of the type of major structural reforms that President Donald Trump has been demanding, “two of the sources said, cautioning that a long road lies ahead in negotiations. One person said that talks are continuing and constructive.”

Then again they can’t be that constructive because one of the sources said the letter “raised doubts” over how substantive a deal Trump could make with Chinese counterpart Xi Jinping when the two leaders meet later this month.

Most of the document appeared to be a rehash of previous changes already made by Beijing, such as raising equity caps on foreign investment in certain industries, according to one person. It did not contain the sort of commitment to change industrial policies such as Xi’s “Made in China 2025” that Washington has been seeking, according to one person familiar with the discussions.

Two other people familiar with the talks also said the Chinese offer was a sign of what they characterized as constructive discussions between the two sides ahead of the planned G20 meeting between the two leaders.

Of course, if it was truly constructive, the Yuan would be surging, yet one look at the offshore currency, shows that the USDCNH has barely budged from its Tuesday closing price of 6.945, although it also remains well away from the key 7.00 level.

Kyle Bass Doubles-Down On Yuan Short, Calls For “China Reset”

Nearly 18 months after Hayman Capital’s Kyle Bass declared that he intended to stand by his massive offshore yuan short even as his fund moved deep into the red (unlike all of those other “tourist China bears” who had jumped ship at the first stirrings of dollar weakness), the Dallas hedge fund manager revealed that he had finally broken even after his fund sunk 20% last year, according to Reuters.

Which means now is the perfect time to double down…

Bass, who has long argued that the yuan will slide 30% against the dollar as the country’s credit bubble bursts,told his audience that he has added to his currency short as the currency hovers just above the big round 7-to-the-dollar level. He also praised President Trump’s trade policies, which he said would be “100% healthy for the next 10 years”, though he clarified that he was “not a Trump voter” and that he would jump at the opportunity to throw his support behind Michael Bloomberg.

“Tariffs come and go,” Bass said.

“But how do you negotiate with someone…with the hopes that they would liberalize their economy and do the things they said they would do, and especially don’t do the things they said they wouldn’t do, and yet they’ve done everything exactly as they always have?”

Trump’s shortcomings, Bass said, include his tweeting and other means by which he communicates his message.

“‘Trade wars are good,’ that was an insane comment to say,” Bass said of Trump. “What he should have said is, ‘We’re going to reciprocate with China, where they’re going to let us into their markets, we’re going to let them into ours…’ His actions were proper, but his comments were improper.”

As corporate defaults soar, Bass believes that China is headed for a “reset” that he expects to arrive during “the next couple of years.”

He projected that China could lose more than $2.5 trillion of equity, more than triple the size of the U.S bank bailout during the 2008 financial crisis, and would have to print more than $25 trillion of renmimbi to counteract the impact of slowing economic growth and declining credit on its banks.

“It’s insane how levered this market has become,” Bass said.

“You’re starting to see bankruptcies across the board in China that are hard to hide, if you look at the corporate default rate, the bankruptcy rate, M1 and M2 (money supply), the slowest money growth in over four decades.”

“We’ll have a reset in China, and I think it will happen in the next couple of years,” Bass concluded.

Chinese companies are already feeling the impact of its slowing credit impulse…

…As defaults soar…

…And small- and medium-sized companies resort to ‘imaginative’ strategies for paying down their debt – including striking an agreement with creditors for a ‘payment in kind’ of ham

4.EUROPEAN AFFAIRS

Brexiteer leader Moog demands a no confidence vote. Britain is in chaos this morning. Domenic Raab, key cabinet figure resigns.

(courtesy zerohedge)

Brexiteer Leader Demands May ‘No Confidence’ Vote As Brexit Chaos Intensifies

Update VIII: Mogg’s “no confidence” letter is in…

Harry Cole

✔@MrHarryCole

MOGG LETTER IN – confirmed

…We now await further reports about a ‘no confidence’ vote that seems ‘almost inevitable’, though some reports suggest the ERG group of hardline Brexiteers is split on whether to call for a leadership challenge.

Laura Kuenssberg

✔@bbclaurak

Boris Johnson has just arrived at ERG meeting – feels very much like this is on and letters from Brexiteers about to go in en masse

Reflecting on reports that Gove has accepted the Brexit Secretary role, BBG has published a brief summary of what Gove as BS would mean for the deal.

He’s a Brexiteer but also more pragmatic than a lot of his fellow campaigners. He’s spoken out in the past in favor of the idea of clinching Brexit – any Brexit – and then tweaking it later to improve it. Gove would need to weigh up whether he wants the job, though. Two Brexiteers quit after realizing the job didn’t wield much power, as the deal was cooked by May’s team. The EU is unlikely to budge, so there’s no chance to wade back in and secure a heroic renegotiation from Brussels. Does he want to be the minister for no deal Dan, I will add the Soros commentary and then get coffee.

According to the Westminster rumor mill, Rory Stewart could replace Gove as environment secretary if Gove accepts the Brexit Secretary job.

Laura Hughes

✔@Laura_K_Hughes

Hearing from a minister that Rory Stewart could become the new Environment Secretary if Michael Gove accepts Brexit Secretary role.

* * *

Update VII: Just as May is fighting for her political future, more unsympathetic EU bureaucrats are turning up the pressure. The latest was EU Council Head Donald Tusk, who said that “Since the very beginning, we have had no doubt that Brexit is a lose-lose situation and that our negotiations have only been about damage control.”

This statement makes the EU’s ulterior motive clear: To frustrate Parliament and hopefully stop the Brexit. Tusk also confirmed that the Nov. 25 EU Brexit summit is on…with or without a deal in the UK.

Another junior cabinet minister just tendered his resignation: North East Hampshire MP Ranil Jayawardena, a parliamentary private secretary to the Ministry of Justice, has also offered his resignation. As Jawawardena leaves, Gove has reportedly accepted the Brexit Secretary role.

Team Ranil

✔@TeamRanil

Cutting against earlier reports that Mordaunt would begrudgingly remain in May’s cabinet, the minister is reportedly meeting with May Thursday afternoon to push for a “free vote” on the Brexit plan – which No. 10 is adamantly against (most likely because they would lose). This is the clearest indication yet that Mordaunt could become the third senior minister to resign.

Steven Swinford

✔@Steven_Swinford

BREAKING

I’m told that Penny Mordaunt going to see PM later this afternoon. She’s pushing for a free vote on the Brexit deal, which the No 10 is adamant will not happen.

Could she become the third Cabinet resignation of this extraordinary day? We’ll know in a few hours…

Meanwhile, rumors are circulating that the ERG has reached the 48-letter threshold to call for a leadership challenge, though there’s been nothing concrete yet. Back in Westminster, Theresa May has been answering questions from agitated MPs for more than two hours – most of them hostile, as BBG pointed out. And the Sun is reporting that the confidence vote in May is “already on.”

Harry Cole

✔@MrHarryCole

Sounds to me like a confidence vote already on. Whips informally sounding out MPs on which way they would vote….

* * *

Update VI: The Telegraph is reporting that Gove has been offered the position of Brexit secretary, but he’s unsure whether to accept following Raab’s resignation, as he also has reservations about the deal.

Steven Swinford

✔@Steven_Swinford

BREAKING

Michael Gove has been offered the job of Brexit Secretary, sources confirm.

But he’s still wrestling with whether he will stay on at all in the wake of Raab’s resignation. Which will it be?

Meanwhile, rumors are circulating that Penny Mordaunt may become the third senior minister to resign on Thursday.

Watch video of Raab’s interview with the BBC:

BBC Breaking News

✔@BBCBreaking

Draft #Brexit deal is “damaging for the economy but devastating for public trust in our democracy” – says ex-Brexit Secretary Dominic Raab in his first post resignation interview http://bbc.in/2QHUT6H

And video of Scotland’s Mundell calling him a “carpetbagger”.

Matt Chorley

✔@MattChorley

Representing Border@ITVBorderRB

Representing Border@ITVBorderRBEXCLUSIVE: Watch @DavidMundellDCT hit out at @DominicRaab‘s resignation, calling him a “carpet bagger” and says he himself won’t resign.

Here’s a quick roundup of Thursday’s most notable developments, courtesy of RanSquawk.

- UK Brexit Secretary Raab has resigned

- Secretary of State for Work and Pensions Esther McVey

- Parliamentary Under-Secretary of State for Exiting the European Union Suella Braverman

- Parliamentary Private Secretary in the Department of Education Anne-Marie Trevelyan

- James Rothwell Telegraph Brexit correspondent tweeted that “a plugged-in Tory source, not a Brexiteer, reckons 6 Cabinet

- resignations to follow Raab, three unknowns, the rest will back the deal. (Newswires)

- Those who will not resign:

- Steven Swinford of the Telegraph tweets “Jeremy Hunt and Sajid Javid are going nowhere, I’m told”. (Newswires)

- Steven Swinford Telegraph Deputy Political editor tweets that Gove isn’t in the Commons because of a personal issue. He decided

- to stay because stakes so high – if he left it would have precipitated exodus. Now Raab’s gone everything changes.. (Newswires)

- Beth Rigby tweets “Understand that Leadsom is not resigning before business questions”. (Newswires)

- No confidence vote:

- ITV’s Peston says that Tory MP’s tell him that 48 letters of no-confidence are to be lodged by lunchtime today. (Newswires)

- Steven Swinford Telegraph Deputy Political Editor tweets Jacob Rees-Mogg just threatened to submit his letter of no confidence in

- the Chamber, which he later submitted. (Newswires)

- Parliament Vote:

- DUP MP Shannon says they feel betrayed and will “certainly” vote against May’s Brexit deal. (Newswires)

- Recent reports suggest that the Parliamentary meaningful vote on Brexit could take place on December 18th. (Newswires)

Amid the chaos, some see a “straightforward” path from here:

Thornton McEnery@ThorntonMcEneryStraightforward from here:

1. Torys depose Theresa May

2. Brexit fails

3. Britain remains

4. Election called

5. Prime Minister Liam Gallagher

* * *

…

[Message clipped] View entire message

Italian Yields Spike After Salvini Advisor Warns Italy Will Exit Eurozone If League Wins

Majority

As if there wasn’t enough non-stop chaos out of the UK as the fate of Brexit and Theresa May is being decided on twitter, between flashing red Bloomberg headlines, and media speculation and rumors, moments ago Italy decided to remind everyone just how unstable its own political situation is, when Claudio Borghi, chief economic advisor to Italy’s de facto leader Salvini, said that the EU has used “made-up numbers” in judging Italy’s budget (the EU has effectively accused Italy of doing the same), and then asked if the EU would have the “courage” to sanction Italy.

As a reminder, the last time a populist European played chicken with the EU, the ECB promptly caused Greek banks to be shuttered indefinitely and Varoufakis’ political career was promptly over. Maybe this time it will be different.

But what really spooked markets, and caught traders’ attention, was the following headline from Reuters:

- BORGHI, CHIEF ECONOMIC ADVISOR TO SALVINI: IF THE LEAGUE GETS A MAJORITY IN THE NEXT ELECTIONS ITALY WILL EXIT THE EUROZONE

In kneejerk reaction, yields on 10Y BTPs spiked to session highs, hitting 3.54%..

… and sending “lo spread” between German and Italian bonds to 315bps, creeping ever closer to the 400bps red line beyond which the Italian bank runs will likely begin.

Amid this chaos out of Italy, Europe’s Stoxx 600 Index has fallen 1%, hitting its lowest intraday level since Oct. 31, dragged not only by the sell-off in U.K. stocks due to Brexit risks, but fresh concerns about “Italeave” as Europe suddenly finds itself defending its integrity on two fronts.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

I) Saudi Arabia

Five Saudis face the death penalty over the Khashoggi killing. So far the Crown Prince has been cleared..

(courtesy zerohedge)

Five Saudis Face Death Penalty Over Khashoggi Killing; Crown Prince Cleared

Saudi Arabia public prosecutor Sheikh Shaalan al-Shaalan said on Thursday that the kingdom will seek the death penalty for five suspects among the 11 charged in the killing of journalist Jamal Khashoggi, confirming suspicions that members of the murder squad purportedly sent to “interrogate” Khashoggi will now themselves face beheadings as the Saudi Royal Family closes ranks around the Crown Prince, per the FT.

As for Mohammed bin Salman who runs the day to day affairs of the world’s top oil exporter and is the de facto head of OPEC, the prosecutor said had “no knowledge” of the mission, effectively absolving him of any domestic suspicion, if not international.

The charges were handed down after the kingdom dismissed five senior intelligence officers and arrested 18 Saudi nationals in connection with Khashoggi’s disappearance. The Saudi insider-turned-dissident journalist disappeared on Oct. 2 after entering the Saudi Arabian consulate in Istanbul to pick up documents that would have allowed him to marry his fiance. Khashoggi was a legal resident of Virginia.

According to the Saudi prosecutor, five people charged are believed to have been involved in “ordering and executing the crime,” according to CNN.

The prosecutor said that the former Saudi deputy intelligence chief, Ahmed al-Assiri, ordered a mission to force Khashoggi to go back to Saudi Arabia and formed a team of 15 people.

They were divided into three groups, the Saudi Public Prosecutor said: a negotiation team, an intelligence team and a logistical team.

It was the head of the negotiating team who ordered the killing of Khashoggi, the prosecutor said.

The Saudis stuck by latest (ever changing) narrative that the Washington Post columnist was killed after a mission to abduct him went awry. The deputy chief of intelligence ordered that Khashoggi be brought back to the kingdom, Shaalan said. The team killed him after the talks failed and his body was handed to a “collaborator” in Turkey, he said.

Asked whether Saud al-Qahtanti, an aide to Prince Mohammed, had any role in the case, Shaalan said that a royal adviser had a coordinating role and had provided information. The former adviser was now under investigation, the prosecutor said, declining to reveal the names of any of those facing charges.

Al-Shaalan did reveal that a total of 21 suspects are now being held in connection with the case. Notably, the decision to charge the 5 comes after National Security Advisor John Bolton repudiated reports that a recording of Khashoggi’s murder made by Turkish authorities suggested that Crown Prince Mohammad bin Salman was behind the murder plot.

But as long as OPEC+ is planning to do “whatever it takes” to boost oil prices, the US’s willingness to give the Saudis a pass could always be tested if crude prices again turn sharply higher.

White House Weighs Kicking Out Cleric Gulen From US To Appease Erdogan; Lira Surges

In what is the most shocking geopolitical news of the day, NBC reports that the Trump administration is weighing extraditing the nemesis of Turkish President Recep Erdogan, cleric Fethulah Gulen who has been living for years in relative seclusion in rural Pennsylvania, from the U.S. in order to placate Turkey over the murder of journalist Jamal Khashoggi.

According to the NBC report, Trump administration officials last month asked federal law enforcement agencies to examine legal ways of removing the exiled Turkish cleric in an attempt to persuade Erdogan to ease pressure on the Saudi government. The effort includes directives to the Justice Department and FBI that officials reopen Turkey’s case for his extradition, as well as a request to the Homeland Security Department for information about his legal status, four sources told NBC.

In hopes of finding immigration irregularities, the White House has requested details about Gulen’s residency status in the U.S. Gulen – who has been living in Pennsylvania since the late 1990s – has a Green Card.

As NBC also adds, there was a certain level of incredulity at this sequence of events: career officials at the agencies pushed back on the White House requests, the U.S. officials and people briefed on the requests said.

“At first there were eye rolls, but once they realized it was a serious request, the career guys were furious,” said a senior U.S. official involved in the process.

What is strange is that while Trump appears eager to appease Erdogan by handing him his arch enemy, the person whom the Turkish president has blamed for creating a “shadow government”, and being responsible for the failed 2016 coup attempt, a Turkish official said the government does not link its concerns about the Khashoggi murder with Gulen’s extradition case.

“We definitely see no connection between the two,” the official said. “We want to see action on the end of the United States in terms of the extradition of Gulen. And we’re going to continue our investigation on behalf of the Khashoggi case.”

So why the extradition push? According to NBC, the secret effort to resolve one of the leading tensions in U.S.-Turkey relations – Gulen’s residency in the U.S. – provides a window into how President Donald Trump is trying to navigate hostility between two key allies after Saudi officials murdered Khashoggi on October 2 at the kingdom’s consulate in Istanbul.

It suggests the White House could be looking for ways to appease and contain Erdogan’s ire over the murder while preserving Trump’s close alliance with Saudi Arabia’s controversial de facto leader, Crown Prince Mohammed bin Salman.

Trump has been desperate to brush aside the entire Khashoggi affair so Riyadh can continue to purchase billions in US weapons without complaints from Congress; Erdogan, meanwhile, has kept the pressure up by leaking pieces of evidence and repeatedly speaking out to accuse Prince Mohammed of orchestrating the murder of Khashoggi.

Of course, as regular readers know, Erdogan has for years demanded the U.S. send Gulen back to Turkey, however such requests have been regularly denied by both the Obama and Trump administration, at least until now.

The Turkish leader accuses the elderly cleric of being a terrorist who was behind a failed coup against Erdogan’s government in 2016. After the coup attempt, Ankara made a formal request to the U.S. for Gulen’s extradition.

Turkish officials made clear to Secretary of State Mike Pompeo during his Oct. 17 meeting with Erdogan in Ankara that they wanted the Trump administration to turn over Gulen, the U.S. officials and people familiar with the matter said.

“That was their number one ask,” said a person briefed on the meeting.

One option that Turkish and Trump administration officials recently discussed is forcing Gulen to relocate to South Africa rather than sending him directly to Turkey if extradition is not possible, said the U.S. officials and people briefed on the discussions. But the U.S. does not have any legal justification to send Gulen to South Africa, they said, so that wouldn’t be a viable option unless he went willingly.

Whether or not Gulen is ultimately extradited remains unclear, however the fact that Trump is even considering this shows just how much leverage the Turkish president now has over Trump. As a result, it will hardly come as a surprise that the Turkish Lira has surged on the news, rising to just above 5.300 after trading at 5.45 earlier…

… as Turkey slowly emerges as one of the most powerful nations in the middle east, engaged in friendly diplomatic relations with Moscow on one hand, while seemingly calling the shots in the US as well.

6. GLOBAL ISSUES

More evidence of a global slowdown: the world’s largest shipper Maersk has sounded the alarm bell on a global slowdown. They label the trade war as a catalyst for the slowdown

(courtesy zerohedge)

World’s Largest Shipper Warns Of Early 2019 Slowdown

The world’s largest shipper A.P. Moller-Maersk sounded the alarm on Wednesday by announcing there would be a tremendous “price to be paid” for President Trump’s trade war as global demand has now plummeted to its lowest level in more than two years.