GOLD: $1213.95 DOWN $8.60 (COMEX TO COMEX CLOSINGS)

Silver: $14.12 DOWN 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1215.00

silver: $14.16

today was options expiry day for the comex and as such the crooks always whack in order to make underwritten contracts expire worthless.

We now have to wait until Friday when the London, LBMA options expire.

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT: 0 NOTICE(S) FOR 100 OZ

Total number of notices filed so far for NOV: 215 for 21500 OZ (0.6687 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1487 for 7,435,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3691: down 88

Bitcoin: FINAL EVENING TRADE: $3872 up $93.00

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A HUGE 8123 CONTRACTS FROM 209,427 DOWN TO 201,304 DESPITE YESTERDAY’S TINY 1 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 710 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 710 CONTRACTS. WITH THE TRANSFER OF 710 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 710 EFP CONTRACTS TRANSLATES INTO 3.55 MILLION OZ ACCOMPANYING:

1.THE 1 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 7,435,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 44,014 CONTRACTS (FOR 18 TRADING DAYS TOTAL 43,014 CONTRACTS) OR 215.070 MILLION OZ: (AVERAGE PER DAY: 2445 CONTRACTS OR 12.22 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 215.070 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 30.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,631.70 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 8123 DESPITE THE TINY 1 CENT LOSS IN SILVER PRICING AT THE COMEX //FRIDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY FAIR SIZED EFP ISSUANCE OF 710 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A GIGANTIC SIZED: 7413 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 710 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 8123 OI COMEX CONTRACTS. AND ALL OF THUS LACK OF DEMAND HAPPENED WITH A 1 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.26 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 7.435 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.048 BILLION OZ TO BE EXACT or 149% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 7.435 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY AN ATMOSPHERIC SIZED 46,809 CONTRACTS DOWN TO 462,033 DESPITE THE TINY LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $0.655//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9246 CONTRACTS:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 9246 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 462,033. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 37,563 CONTRACTS: 46,809 OI CONTRACTS DECREASED AT THE COMEX AND 9246 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 37,563 CONTRACTS OR 3,756,300 OZ = 116.83 TONNES. AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A TINY FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $0.65

YESTERDAY, WE HAD 5072 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 130,577 CONTRACTS OR 13,057,700 OZ OR 406.14 TONNES (18 TRADING DAYS AND THUS AVERAGING: 7254 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY IN TONNES: 406.14 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 406.14/2550 x 100% TONNES = 15.92% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,622.95 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN ATMOSPHERIC SIZED DECREASE IN OI AT THE COMEX OF 46,809 DESPITE THE TINY LOSS IN PRICING ($0.65) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9246 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9246 EFP CONTRACTS ISSUED, WE HAD A GIGANTIC LOSS OF 37,563 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9246 CONTRACTS MOVE TO LONDON AND 46,809 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 116.83 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A LOSS OF $0.65 IN YESTERDAY’S TRADING AT THE COMEX

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN 8.60 TODAY: /

A BIG CHANGE IN GOLD INVENTORY AT THE GLD/

A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD

/GLD INVENTORY 761.74 TONNES

Inventory rests tonight: 761.74 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS TODAY

A BIG CHANGE IN SILVER INVENTORY AT THE SLV

A HUGE WITHDRAWAL OF 2.301 MILLION OZ FROM THE SLV.

/INVENTORY RESTS AT 322.718 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE 8123 CONTRACTS from 209,427 DOWN TO 201,304 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

710 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 710 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 8123 CONTRACTS TO THE 710 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE NET LOSS OF 7413 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 37.07 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 7.435 MILLION OZ STANDING IN NOVEMBER.

RESULT: A HUGE DECREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 710 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 1.13 POINTS OR 0.04% //Hang Sang CLOSED DOWN 44.22 POINTS OR 0.17% //The Nikkei closed UP 140.40 OR 0.64%/ Australia’s all ordinaires CLOSED UP .92% /Chinese yuan (ONSHORE) closed DOWN at 6.9485 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil UP to 51.59 dollars per barrel for WTI and 60.43 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.9485AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9439: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)The algos are going nuts as the markets reacted to a stale Nov 1 phone call. I extremely doubt that there will be a deal between China and the uSA

( zerohedge)

4/EUROPEAN AFFAIRS

ITALY

The fun now begins as the EU delegates have reportedly approved a plan to levy billions of euros in fines against Italy for their 2.4% defict.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/UKRAINE/

Interesting: captured Ukrainian sailors admit to “provoking” the Russian navy in an interrogation video

( zerohedge)

ii)Russia jails the two Ukrainian sailors involved in the Kerch Strait confrontation. This sets up a very explosive situation between the Ukraine and Russia

(courtesy zero hedge)

6. GLOBAL ISSUES

7. OIL ISSUES

Oil back to the 50 dollar handle

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Hugo again writes that the USA can return to sound money if they revalue USA silver eagles from one dollar to $30.00 dollars.a great read

( Hugo Salinas Price/GATA)

iii)To our all gold coin collectors out there. The Saudi gold discs are extremely rare. It seems that these discs were not meant for Aramco. However in 1950, the Philadelphia mint produced saudi gold coins of weight .2354 and it was these that paid for the oil

( JPKonig/GATA)

iv)A must view: Grant Williams states that the gold standard is now needed to restore financial ecology

( Grant Williams/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

LATE NIGHT/EARLY MORNING TRADING:

Trouble ahead as the President states that it is highly likely that he will move ahead with the full compliment of Chinese tariffs boost ie. a full 267 billion dollars worth of goods that the uSA does not already apply a tariff to.

( zerohedge)

ii)Market data/

a)We have been highlighting to you, house data which shows that the USA is slowing down in all related data to housing. Today USA home price growth is the slowest since Trump was elected.

( zerohedge)

a)Surprisingly after the stocks initially fell on the report that Trump is to unleash more auto tariffs next week, the stocks advanced.

( zerohedge)

d)Dave Kranzler on the woes of General Electric:

e)And now the devastation at GM

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 0 notices standing for a loss of 2 contacts. We had 2 notices served upon yesterday so we gained 0 contracts or an additional nil oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts.

After November, we have a December contract and here we LOST 21,728 contracts DOWN to 52,298. January saw a GAIN of 78 contracts up to 1715 contracts. March, the next big delivery month after December saw a gain of 11,092 contracts up to 120,927

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON NOV 27. 2017 WE HAD STILL 43,560 (3 days before first day notice) OPEN INTEREST CONTRACTS LEFT TO BE SERVED UPON AND THIS COMPARES TO TODAY: 51,154 CONTRACTS (3 days before first day notice)

IT ALSO LIKES LIKE WE ARE GOING TO HAVE A DANDY AMOUNT OF SILVER STANDING FOR DELIVERY AT THE COMEX.

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

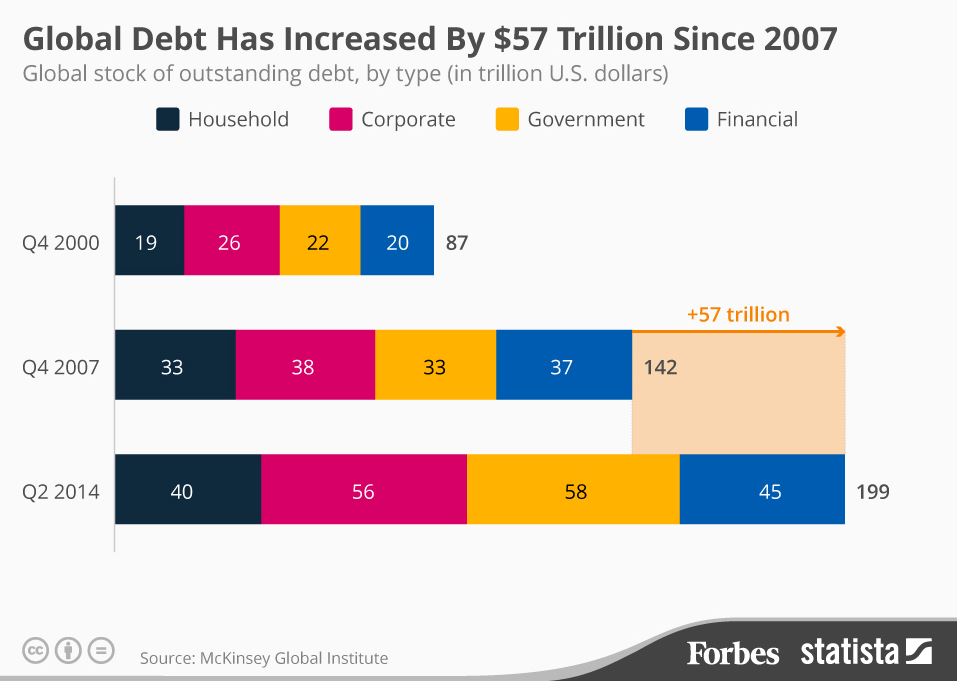

A Worldwide Debt Default Is A Real Possibility

by John Mauldin via Forbes.com

A Worldwide Debt Default Is A Real Possibility

Is debt good or bad? The answer is “Yes.”

Debt is future spending pulled forward in time. It lets you buy something now for which you otherwise don’t have cash yet.

Whether it’s wise or not depends on what you buy. Debt to educate yourself so you can get a better job may be a good idea. Borrowing money to finance your vacation? Probably not.

The problem is that many people, businesses, and governments borrow because they can. It’s been possible in the last decade only because central banks made it so cheap.

It was rational in that respect. But it is growing less so as the central banks start to tighten.

Earlier this year, I wrote a series of articles (synopsis and links here) predicting a debt “train wreck” and eventual liquidation. I dubbed it “The Great Reset.” I estimated we have another year or two before the crisis becomes evident.

Now I’m having second thoughts. Recent events tell me the reckoning could be closer than I thought just a few months ago.

Debt Doesn’t Fuel Growth Anymore

Central banks enable debt because they think it will generate economic growth. Sometimes it does. The problem is they create debt with little regard for how it will be used.

That’s how we get artificial booms and subsequent busts. We are told not to worry about absolute debt levels so long as the economy is growing in line with them.

That makes sense. A country with a larger GDP can carry more debt. But that is increasingly not what is happening.

Let me give you two data points.

Hoisington Investment Management’s Lacy Hunt tracks data that shows debt is losing its ability to stimulate growth. In 2017, one dollar of non-financial debt generated only 40 cents of GDP in the US. It’s even less elsewhere. This is down from more than four dollars of growth for each dollar of debt 50 years ago.

This has seriously worsened over the last decade. China’s debt productivity dropped 42.9% between 2007 and 2017. That was the worst among major economies, but others lost ground, too. All the developed world is pushing on the same string and hoping for results.

Now, if you are used to using debt to stimulate growth, and debt loses its capacity to do so, what happens next? You guessed it: The brilliant powers-that-be add even more debt.

Here’s How Much Debt We Actually Have

This is classic addiction behavior. You have to keep raising the dose to get the same high.

But centuries of history show that every prior debt run-up eventually took its toll on the economy. There is always a Day of Reckoning.

The US economy is so huge and powerful that our current $24.5 trillion government debt (including state and local) could easily grow to $40 trillion before we meet that day. We are one recession away from having a $30 trillion U.S. government debt total.

It will happen seemingly overnight. And deficits will stay well above $1 trillion per year every year after that, not unlike now.

Even though a budget deficit is under $800 billion this year, we added over $1 trillion of actual debt. That is due to “off budget” items that Congress thinks shouldn’t be part of the normal budgetary process.

It includes things like Social Security and Medicare They vary from time to time and year to year and can be anywhere from $200 billion to almost $500 billion.

And here’s the point that you need to understand. The U.S. Treasury borrows those dollars and it goes on the total debt taxpayers owe. The true deficit that adds to the debt is actually much higher than the number you see in the news.

Household and corporate debt is growing fast, too. And not just in the U.S.

Here’s a note from Economic Cycle Research Institute’s Lakshman Achuthan:

Notably, the combined debt of the US, Eurozone, Japan, and China has increased more than ten times as much as their combined GDP [growth] over the past year.

Yes, you read that right. In the last year, the world’s largest economies are generating debt 10X faster than economic growth. Adding debt at that pace, if it continues, will boost the debt-to-GDP ratio at an alarming rate.

Lakshman continues.

Remarkably, then, the global economy—slowing in sync despite soaring debt—finds itself in a situation reminiscent of the Red Queen Effect we referenced 15 years ago, when tax cuts boosted the US budget deficit much more than GDP. As the Red Queen says to Alice in Lewis Carroll’s Through the Looking Glass, “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

This Won’t End Well

I am trying to imagine a scenario where this ends in something less than chaos and crisis. The best I can conceive is a decade-long (and possibly more) stagnation while the debt gets liquidated.

But realistically, that won’t happen because debtors won’t let it. And they outnumber lenders. For this reason, something like “the Great Reset” will happen first.

The rational course would be to delay the inevitable as long as possible. Yet in the U.S. we’re rushing it.

* * *

John’s weekly newsletter is a must-read for investors who want to find out about the trends to watch out for. Get ‘Thoughts from the Frontline’ for free here

News and Commentary

Gold edges lower as dollar holds steady (Reuters.com)

Asian markets cool off as investors await Trump-Xi meeting (MarketWatch.com)

Trump refuses to condemn Russian aggression against Ukraine (CNN.com)

Gold firms on doubts over Fed rate path; focus on G20 (Reuters.com)

Stock Rally Hits Speed Bump With U.S. Tariff Alarm (Bloomberg.com)

Goldman Predicts Commodities Will Soar and Gold Benefit in 2019 (Finance.Yahoo.com)

Grim Stock Signals Piling Up as Wall Street Mulls Recession Odds (Bloomberg.com)

Gold standard is needed to restore financial ecology – Williams (RealVision.com)

Silver As Savings Would Help “Make America Great Again” (Plata.com.mx)

Are these north Wales hills sitting on a gold mine? (BBC.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

26 Nov: USD 1,226.65, GBP 954.58 & EUR 1,079.33 per ounce

23 Nov: USD 1,222.15, GBP 951.69 & EUR 1,075.13 per ounce

22 Nov: USD 1,228.25, GBP 950.42 & EUR 1,074.72 per ounce

21 Nov: USD 1,224.00, GBP 957.29 & EUR 1,075.04 per ounce

20 Nov: USD 1,223.10, GBP 951.45 & EUR 1,069.97 per ounce

19 Nov: USD 1,223.55, GBP 951.07 & EUR 1,070.97 per ounce

Silver Prices (LBMA)

26 Nov: USD 14.38, GBP 11.18 & EUR 12.65 per ounce

23 Nov: USD 14.26, GBP 11.12 & EUR 12.56 per ounce

22 Nov: USD 14.52, GBP 11.26 & EUR 12.72 per ounce

21 Nov: USD 14.42, GBP 11.26 & EUR 12.65 per ounce

20 Nov: USD 14.44, GBP 11.24 & EUR 12.63 per ounce

19 Nov: USD 14.36, GBP 11.21 & EUR 12.57 per ounce

Recent Market Updates

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

– Stock Markets Remains Extremely Overvalued – Hussman

– Stocks are Now in ‘Complete Bitcoin Territory,’ Asset Manager Says

– Brexit’s Safe Haven Is a Dangerous Place

– Gold and Silver Rise As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

– GoldCore Capitalising On Brexit With Dublin Gold Vault

– Store Gold In The Safest Vaults In Ireland

– Investors Set To Store Gold In Dublin Due To Brexit Risks

JPMorgan ignored Butler’s complaints but can’t ignore Justice Department’s

Submitted by cpowell on Mon, 2018-11-26 22:27. Section: Daily Dispatches

5:28p ET Monday, November 26, 2018

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler notes today that he protested hundreds of times to JPMorganChase and the U.S. Commodity Futures Trading Commission that the investment bank was rigging the silver market. Now that a former trader for the bank has confessed in federal court to doing just what Butler long complained of and has asserted that his superiors at the investment bank knew what he was doing, Butler predicts that more prosecutions by the Justice Department involving the bank are probable — along with changes in the silver market.

Butler’s commentary is headlined “Silver Scandal” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/silver-scandal-17492

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Silver Scandal

|

November 26, 2018 – 2:07pm

A few follow up comments about the still rather remarkable announcement by the Department of Justice concerning the guilty plea by the former JPMorgan trader for spoofing in precious metals. Contained in the announcement was the statement that the guilty plea was accepted and sealed on Oct 9, nearly a month before it was unsealed on Nov 6. With a rather short sentencing date approaching on Dec 19, and the time it took to unseal the plea, it may be assumed that the trader has already fully cooperated in the hopes of reducing his jail time, said to approach 30 years with no cooperation.

The thought of facing serious jail time for someone that never thought such an outcome was possible for everyday practices known to supervisors and other traders at the bank had to come as a shock. For years, the trader was riding high, a master of the trading universe in a highly respected position, now suddenly facing incarceration. Companion reporting suggested that JPMorgan itself was unaware of the guilty plea, according to a person with knowledge of the matter. It was not indicated if the CFTC was closely involved. Since the former trader left JPMorgan last year, it’s not hard to imagine how his cooperation with the DOJ could remain unknown to the bank.

No one in the silver market is as crooked as JPMorgan and the announcement by the Department of Justice of a guilty plea by one of its former traders is the first solid connection between my allegations of the past ten years about JPMorgan and a finding of wrongdoing by a trader for the bank in COMEX silver and gold. This goes a very long way towards vindicating my narrative of the past ten years.

It’s been reported by Bloomberg that the Justice Department asked a judge overseeing a civil antitrust case against JPMorgan to postpone the case for six months “to protect the integrity” of its ongoing criminal probe. This indicates that the Justice Department is serious about pursing the matter of a silver price manipulation and JPMorgan’s involvement.

Inside the bank, this must come as a bombshell. Further indictments appear inevitable. If the media gets wind of the full story it could turn into a momentous scandal reaching to the top. A lot of people at JPMorgan must now be sweating bullets. What they have been doing for years is clearly illegal. Nobody can get by using tactics like spoofing to suppress the price of a commodity in the futures market while loading up on the physical asset itself. How could they be so myopic as to pull of this gross manipulation in silver for almost eight years without fear of consequences? They have 150 million ounces of their silver hoard in their COMEX warehouse which is more physical silver than the Hunt Brothers acquired in the 1980 silver scandal.

To repeat, JPM acquired that silver and much more by suppressing the price in the futures market and scooping up physical silver at prices they manipulated lower. That’s a far more serious crime than spoofing. Another major crime in silver (and gold) committed by JPM is that it has never taken a loss in more than a decade when adding to COMEX short positions. The maintenance of a perfect trading record over a decade in something as hazardous as shorting silver is as impossible as a lifetime batting average of 1,000. Only if the game were seriously rigged could such a feat occur. I could provide the DOJ with a paint-by-the-numbers illustrated playbook documenting JPM’s impossibly perfect trading record if they should request it.

One thing is certain, upper management at JPMorgan can’t plead ignorance of what their underlings have pulled off in silver. I have sent my accusations and proof of wrongdoing to the board of directors, the senior management and their legal counsel time and again over the past eight years. In addition, I have sent 1,000 similar emails and letters to the Commodity Futures Trading Commission and the CME group (COMEX). It seems to me that if JPM could have answered and easily explained away the allegations, they would have done so long ago.

The fact that JPMorgan has essentially eliminated their manipulative short position in the past week may mean they are turning over a new leaf. That has profound implications for the silver market.

Ted Butler

November 26, 2018

END

Hugo again writes that the USA can return to sound money if they revalue USA silver eagles from one dollar to $30.00 dollars.

a great read

(courtesy Hugo Salinas Price/GATA)

Hugo Salinas Price: A message for Trump

Submitted by cpowell on Mon, 2018-11-26 22:46. Section: Daily Dispatches

5:47p ET Monday, November 26, 2018

Dear Friend of GATA and Gold:

President Trump could “make American great again,” Hugo Salinas Price of the Mexican Civic Association for Silver writes today, by revaluing U.S. silver eagle coins from their $1 imprinting to $30 for payment of federal taxes. This, Salinas Price writes, would make silver a powerful savings vehicle for Americans. Salinas Price long has been advocating such a system for Mexico as well. His commentary is headlined “A Message for Trump” and it’s posted at the association’s internet site here:

http://plata.com.mx/enUS/More/364?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

To our all gold coin collectors out there. The Saudi gold discs are extremely rare. It seems that these discs were not meant for Aramco. However in 1950, the Philadelphia mint produced saudi gold coins of weight .2354 and it was these that paid for the oil

(courtesy JPKonig/GATA)

J.P. Koning: Why the U.S. Mint once issued gold discs

to Saudi Arabia

Submitted by cpowell on Tue, 2018-11-27 02:45. Section: Daily Dispatches

9:45p ET Monday, November 26, 2018

Dear Friend of GATA and Gold:

Writing at Bullion Star, market analyst and monetary historian J.P. Koning tells the fascinating story of how in the late 1940s the U.S. Mint in Philadelphia made gold coins for the Saudi Arabian government that have become collector’s items with high premiums. But contrary to widespread belief, Koning writes, the coins, dominated only by their weight and purity, had nothing to do with the Arab-American Oil Co.

Koning’s essay is headlined “Why the U.S. Mint Once Issued Gold Discs to Saudi Arabia” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/jp-koning/why-us-mint-once-issued-gold…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

\A must view: Grant Williams states that the gold standard is now needed to restore financial ecology

(courtesy Grant Williams/GATA)

Grant Williams: Gold standard is needed to restore

financial ecology

Submitted by cpowell on Tue, 2018-11-27 03:02. Section: Daily Dispatches

10:04p ET Monday, November 26, 2018

Dear Friend of GATA and Gold:

Grant Williams of the “Things That Make You Go Hmmm” newsletter and the Real Vision video service has posted in the clear his presentation to the Porter Stansberry Conference in Las Vegas on October 1, and it argues that the world’s return to a gold standard is not only possible but a prerequisite for restoring the world’s financial ecology.

… Dispatch continues below …

The removal of the golden anchor of the world financial system in 1971, Williams argues, really messed things up, de-industrializing and financializing the economy of the United States and giving supreme power to bankers.

There’s always plenty of gold to fix things, Williams concludes, as it’s just a matter of price.

Williams’ presentation is titled “Cry Wolf,” is 40 minutes long, and can be viewed at Real Vision here:

https://www.realvision.com/grant-william-keynote-speech

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.or

end

Craig Hemke is coming to the same conclusion as Chris Powell and myself on the EFP’s: they are totally garbage

(courtesy Craig Hemke/Sprott)

GATA) Craig Hemke at Sprott Money: Those ‘exchange for physicals’ at the Comex aren’t real

Submitted by cpowell on 04:39PM ET Tuesday, November 27, 2018. Section: Daily Dispatches

11:44a ET Tuesday, November 27, 2018

Dear Friend of GATA and Gold:

The TF Metal Report’s Craig Hemke, writing today at Sprott Money, does the math on the last year’s worth of the use of the “exchange for physicals” mechanism of settling gold futures contracts on the New York Commodities Exchange. Hemke calculates that nearly 2.4 million Comex gold contracts have been settled this way since last November, totaling 7,442 tonnes of gold.

This total, Hemke notes, is 260 percent of annual gold mine supply and nearly equal to all the gold claimed to be vaulted by the members of the London Bullion Market Association, the Bank of England, and the Comex itself.

How can this be?

Hemke concludes:

“There are no ‘exchanges for physical’ taking place at all — at least not in the sense of actual, unencumbered, and allocated physical metal. Instead, EFPs are just another part of the great scam known as The Fractional Reserve and Digital Derivative Pricing Scheme, where alchemized digital and unallocated gold is foisted upon the masses, who blindly accept ‘exposure to the gold price’ as a substitute for the real thing.”

There’s another question here, which GATA has put in writing to the U.S. Commodity Futures Trading Commission without yet getting a response, despite recruiting a member of Congress to prod the agency. That is, how does the commission regard EFP reporting, since it can’t possibly be accurate in any conventional sense?

Your secretary/treasurer often has wondered if the EFP data reports only the trading back and forth of a very limited amount of gold among brokers for the U.S. government and other governments, to create illusory prices, with little if any actual net transfer of metal. If such trading is conducted at the direction or with the approval of the U.S. Treasury’s Exchange Stabilization Fund and nets to zero gold actually changing hands, it presumably would be outside any regulation or formal reporting.

There might be an excellent story in this stuff for financial journalism, if any news organization dared to attempt it in regard to gold, governments, and central banks.

Gold mining companies might want to investigate it as well if they weren’t more interested in mining their shareholders than in obtaining free-market prices for their metal.

The World Gold Council might seem obliged to be interested too, but its main purpose continues to seem to be to make sure that there never is a world gold council.

As for most gold market analysts, they are too much in love with their charts and formulas to examine any evidence that for many years now there have been no markets at all, just interventions.

Hemke’s outstanding work is headlined “One Full Year of Comex EFPs” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/one-full-year-of- comex-efps-craig-hemke...

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

The Exchange for Physical, whatever it may be, is just another example of the total farce of what The Gold Cartel has turned the gold/silver markets into. I called the CFTC too and they refused to explain to me what was going on. The scene is so ridiculous there is no doubt that it is only a matter of time before those two markets blow up!

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

__________________________________________

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9485/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9439 /shanghai bourse CLOSED DOWN 1.13 POINTS OR 0.04%

. HANG SANG CLOSED DOWN 44.22 POINTS OR 0.17%

2. Nikkei closed UP 140.40 POINTS OR 0.64%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 97.17/Euro FALLS TO 1.1317

3b Japan 10 year bond yield: FALLS TO. +.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113/24/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.59 and Brent: 60.43

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.36%/Italian 10 yr bond yield UP to 3.26% /SPAIN 10 YR BOND YIELD UP TO 1.52%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.90: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.37

3k Gold at $1224.20 silver at:14.30 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 33/100 in roubles/dollar) 66.85

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.63DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9991 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1307 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.36%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.06% early this morning. Thirty year rate at 3.31%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2323

US Futures, Global Markets Slide, Spooked By Trump Trade Comments

US index futures and European shares slumped on Tuesday in a volatile, illiquid session punctuated by some headline confusion, while gains in Asian equities were limited after President Donald Trump said he still intends to go ahead with raising tariffs on China imports from 10% to 25% and that it was highly unlikely he would accept China’s request to refrain from the increase, just days before meeting with his counterpart Xi Jinping.

While ES losses were modest, it is worth noting that earlier in the session, S&P futures swung sharply, gaining as much as 0.5%, then falling back into negative territory, after algos misinterpreted comments from China foreign ministry spokesman Geng Shuang. As we reported earlier, during a media briefing Geng first said that Presidents Trump and Xi agreed to reach mutually beneficial agreements, sparking a vicious rally in futures. Just moments later, however, futures erased gains when Geng later said he was referring to a phone call on Nov. 1. The result was the following:

Following these fireworks, contracts on the Dow, S&P and Nasdaq pointed to a drop at the opening, while Treasuries and the dollar held steady before the Fed’s top two officials were set to speak in the next 48 hours.

European equities gave up initial gains and posted small losses as basic resources and travel names underperformed, with the Stoxx Europe 600 Index edging modestly lower (-0.1%), led by raw materials producers, while bonds rose across Europe and the euro currency edged lower. The pound weakened as traders mulled prospects for parliamentary approval of the Brexit deal, which Trump said could jeopardize Britain’s ability to strike a trade pact with the U.S.

Earlier in the session, Asian markets were mostly positive as the region took impetus from the performance on Wall St, where all majors finished with firm gains on return from the Thanksgiving weekend and with retailers buoyed on the back of Black Friday and Cyber Monday sales. ASX 200 (+1.0%) and Nikkei 225 (+0.6%) were lifted from the open with Australia led higher by tech and financials, while a pullback in USD/JPY limited the upside for the Japanese benchmark. Elsewhere, Hang Seng (-0.2%) and Shanghai

Comp. (+0.1%) were mixed with China somewhat dampened by Trump’s hardball tactics ahead of the meeting with Chinese President Xi at this week’s G20, in which he suggested an intention to proceed with raising tariffs on China imports from 10% to 25% and also warned to place tariffs on the remaining USD 267bln of Chinese imports if they fail to reach a favourable outcome for the US. Furthermore, a slowdown of Chinese Industrial Profit growth and concerns in the Hong Kong property sector also contributed the cautiousness in Chinese markets.

In addition to today’s 8:30am ET comments from Fed vice chair Clarida, trade remains firmly in investors’ minds before leaders of the two biggest economies meet in Buenos Aires at the end of the week. Trump’s comments that it is likely the US will slap tariffs on the remaining Chinese imports and raise tariffs on existing tariffed products have weighed on optimism for U.S. stocks, which climbed on Monday amid hopes a strong start to the holiday season thanks to record online sales will keep growth on track.

Meanwhile, Fed speakers will be closely watched for any indications of a change in Fed thinking over continued rate hikes. Today Fed vice chair’s New York speech at 8:30am will be the main attraction, while Chair Powell’s speech on Wednesday will be parsed for any hints on prospects for a pause in rate increases next year after traders reduced expectations for the pace of monetary policy tightening.

Elsewhere, emerging market currencies weakened and their shares traded little changed. Bitcoin steadied near $3,700 after plunging 14 percent Monday.

In overnight political news, US Special Counsel Mueller’s office said former Trump campaign manager Manafort lied to FBI and Special Counsel in violation of plea agreement.

In commodities, Brent (+0.2%) and WTI (Unch) are nursing initial losses as focus starts turning to the G20 summit over the weekend where markets may get initial hints of what to expect at the Dec 6th OPEC meeting in Vienna. The Saudi Crown Prince, Russian President and US President are to meet, possibly on the side-lines to decide the future of the global oil market. Talk around the market notes that Prince Mohammed Bin Salman may not able to defy US President Trump’s aim for lower oil prices after the White House stood behind the prince in regard to the killing of journalist Khashoggi. Nonetheless, traders will be watching the summit closely, while in the nearer-term, today will see the release of the weekly API where forecasts see headline crude stockpiles printing a drawdown of 0.6mln barrels.

Gold is trading relatively flat as the dollar holds steady following comments from Trump that overnight that he still intends to raise Chinese import tariffs to 25%; these comments come ahead of this week’s G20 summit. Additionally, US-China trade pessimism has caused copper prices to fall for the 3rd consecutive session due to demand concerns. Iron ore futures have dropped to their lowest level in over 4 months, dropping by 5% over concerns that steel prices are to remain pressured by slower demand.

Expected data include Conference Board Consumer Confidence. Bank of Nova Scotia, Couche-Tard, and Salesforce are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.2% at 2,663.0

- STOXX Europe 600 up 0.07% to 358.59

- MXAP up 0.4% to 151.86

- MXAPJ up 0.3% to 486.89

- Nikkei up 0.6% to 21,952.40

- Topix up 0.7% to 1,644.16

- Hang Seng Index down 0.2% to 26,331.96

- Shanghai Composite down 0.04% to 2,574.68

- Sensex up 0.5% to 35,524.01

- Australia S&P/ASX 200 up 1% to 5,728.28

- Kospi up 0.8% to 2,099.42

- German 10Y yield fell 1.2 bps to 0.349%

- Euro down 0.04% to $1.1323

- Italian 10Y yield fell 13.6 bps to 2.9%

- Spanish 10Y yield fell 2.6 bps to 1.536%

- Brent futures up 0.6% to $60.83/bbl

- Gold spot little changed at $1,223.10

- U.S. Dollar Index up 0.1% to 97.15

Top Overnight News from Bloomberg

- President Donald Trump said he’ll likely push forward with plans to increase tariffs on $200 billion of Chinese goods, indicating he would also slap duties on all remaining imports from the Asian nation if negotiations with China’s leader Xi Jinping fail to produce a trade deal

- U.K. Prime Minister Theresa May will put her Brexit deal to Parliament for a decisive vote on Dec. 11, but after her plan was savaged from all sides, the signs are she’s on course to lose. President Trump Says Brexit deal could hurt plans for trade pact with U.S.

- The Brexit deal negotiated by Prime Minister Theresa May will lower economic output over the coming decade compared with staying in the European Union, researchers said. The deal would lower gross domestic product per capita by between 1.9 percent and 5.5 percent versus EU membership, according to a joint paper. Leaving without a deal could lower output per head as much as 8.7 percent.

- Italy’s populist government failed to thrash out a new deficit target for the European Union in late night talks but cracks are starting to show in its battle with the bloc over spending

- Donald Trump plans to keep Treasury Secretary Steven Mnuchin and Commerce Secretary Wilbur Ross amid speculation of a broader shakeup in the president’s Cabinet, according to three people familiar with his thinking

- European Union Trade Commissioner Cecilia Malmstrom sounds an upbeat note about EU talks with the U.S. on revamping global commercial rules while saying the verdict is out on whether President Donald Trump’s administration will stay engaged

- The Turkish lira – – on track for its best November since 2002 — is once again turning into a favorite for fast-money investors and hedge funds. Short-term carry positions have increased by an estimated $5.4 billion since the end of August, according to QNB Finansbank, an Istanbul-based lender

- The Brevan Howard Asia Fund bucked a difficult October for macro funds, and is posting its best return in five years, according to a person with knowledge of the matter

Asian equity markets were mostly positive as the region took impetus from the performance on Wall St, where all majors finished with firm gains on return from the Thanksgiving weekend and with retailers buoyed on the back of Black Friday and Cyber Monday sales. ASX 200 (+1.0%) and Nikkei 225 (+0.6%) were lifted from the open with Australia led higher by tech and financials, while a pullback in USD/JPY limited the upside for the Japanese benchmark. Elsewhere, Hang Seng (-0.2%) and Shanghai Comp. (+0.1%) were mixed with China somewhat dampened by Trump’s hardball tactics ahead of the meeting with Chinese President Xi at this week’s G20, in which he suggested an intention to proceed with raising tariffs on China imports from 10% to 25% and also warned to place tariffs on the remaining USD 267bln of Chinese imports if they fail to reach a favourable outcome for the US. Furthermore, a slowdown of Chinese Industrial Profit growth and concerns in the Hong Kong property sector also contributed the cautiousness in Chinese markets. Finally, 10yr JGBs were uneventful as prices took a breather from its extended but gradual uptrend and with today’s 40yr auction largely ignored despite increases in the b/c and accepted prices.

Top Asian News

- Hong Kong’s Home Market Suffering Worst Declines Since 2016

- Day Two Rebound in Asia Stocks Closes an Eye on Trade Rhetoric

- Genting Malaysia Says Fox World Lawsuit Won’t Impact Operations

European cash indices gave up initial gains (Eurostoxx 50 -0.1%) following a relatively flat open after pre-market gains in index futures were short-lived. Equity futures staged a pre-cash open rally after it was reported that a Chinese Foreign Ministry spokesman was quoted as stating that US President Xi and US President Trump had agreed to mutually beneficial agreements. However gains in futures markets were pared after it was later reported that this was in reference to a November 1st phone call and thus was viewed as stale by the market, particularly considering the hardball interview by Trump in the WSJ yesterday ahead of this week’s G20 summit. On an index basis, the SMI lags its peers (-0.5%) with Credit Suisse (-1.7%) lower following a broker

downgrade at Credit Suisse. In terms of sector specifics, performance is relatively mixed with slight underperformance in material names in-fitting with recent price action in the complex. To the upside, utility names modestly outperform, albeit the moves thus far across the board are relatively small in terms of magnitude. Individual movers this morning include Dialog Semiconductor (-1.4%) amid Apple-inspired losses (post-Trump threat of potential tariffs on iPhones and laptops), Apple share are down 1.7% pre-market. Elsewhere, Rexel (+1.9%) are firmer following a broker upgrade at Credit Suisse, Thomas Cook (-24.5%) shares are notably underperforming following a disappointing trading update, dragging Tui (-4.2%) lower in sympathy.

Top European News

- StanChart Is Said to Weigh a Simpler Structure to Control Costs

- Bain Is Said to Explore Takeover Bid for Germany’s Osram Licht

- UBS Takes Profit on Italy Two-Year Bonds as Budget Tensions Cool

- Thomas Cook’s Dismal Year Gets Worse With Latest Profit Warning

- Italy Compromise Has Convinced One Fund to Add European Banks

In FX, the DXY was overall bid vs G10 counterparts with the aid of the GBP weakness due to the latest Brexit developments. Moreover, Citi’s rebalancing model points to modest USD buying vs. peers going into month end, while Nordea also notes tomorrow’s HIA which is the cut-off date if companies wish to convert foreign currency into USD along with SOMA that happens to fall on Friday as well. The index is currently hovering above 97.000 within a narrow range around the big figure.

- GBP – The standout underperformer vs. peers amid comments from UK Remain loyalist Fallon who said it may be possible to delay the date UK leaves the EU to renegotiate a better deal, inflicting a blow to UK PM May’s so-called “best deal”. As such Cable fell to a low print of 1.2734 ahead of the mid-November base at 1.2724, having already given up the 1.2800 handle following comments from US President Trump who noted that UK may not be able to trade with the US, in an interview last night. If the mid-November low (or Raab trough) is breached, the next levels to note are 1.2696 (October low) and 1.2662 (YTD low). However, looking further ahead Credit Suisse is more optimistic on the outlook for Sterling, with their Cable forecast at 1.4000 by end-2019

- EUR – Holding up well vs. the pound above 0.8850 but not quite challenging the 100DMA 0.8884, though the single currency is lower vs. the buck, with the pair tripping some stops at 1.1310. Obviously, 1.1300 is nearest support and if breached more stops are reported at 1.1290.

- NZD,AUD – Notable, albeit marginal G10 outperformers vs. the buck, with the Kiwi staging another recovery following the weak data (trade overnight), and now looking ahead to the RBNZ semi-annual FSR tonight. NZD/USD hovering just below 0.6800 and AUD/USD near the middle of a 0.7270-15 band.

In commodities, brent (+0.2%) and WTI (Unch) are nursing initial losses as focus starts turning to the G20 summit over the weekend where markets may get initial hints of what to expect at the Dec 6th OPEC meeting in Vienna. The Saudi Crown Prince, Russian President and US President are to meet, possibly on the side-lines to decide the future of the global oil market. Talk around the market notes that Prince Mohammed Bin Salman may not able to defy US President Trump’s aim for lower oil prices after the White House stood behind the prince in regard to the killing of journalist Khashoggi. Nonetheless, traders will be watching the summit closely, while in the nearer-term, today will see the release of the weekly API where forecasts see headline crude stockpiles printing a drawdown of 0.6mln barrels. Gold is trading relatively flat as the dollar holds steady following comments from Trump that overnight that he still intends to raise Chinese import tariffs to 25%; these comments come ahead of this week’s G20 summit. Additionally, US-China trade pessimism has caused copper prices to fall for the 3rd consecutive session due to demand concerns. Iron ore futures have dropped to their lowest level in over 4 months, dropping by 5% over concerns that steel prices are to remain pressured by slower demand.

Looking at the day ahead, we’ll get various house price data points including the September FHFA house price index reading, Q3 house price purchase index reading and September S&P CoreLogic house price data. On top of that we’ll get the November consumer confidence survey which is expected to slip nearly 2pts to 135.8 in light of the recent wobbles in the equity market. That is, however, in the context of the 18-year high that the index reached last month. Away from the data, there will be plenty of focus on Fed Vice-Chair Clarida’s speech in New York today at 8.30am ET, especially around the topics of how he characterizes recent volatility in markets and the prospects for domestic and global growth. Fellow Fed officials Bostic, Evans and George will also speak while the ECB’s Nouy, Costa and Mersch also speak at various stages. It’s worth also noting that starting today and continuing until Thursday, the three top candidates to take over from Merkel as head of the CDU will hold panel debates.

US Event Calendar

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.2%, prior 0.09%; CS 20- City YoY NSA, est. 5.2%, prior 5.49%

- 8:30am: Fed Vice Chairman Clarida Speaks in New York

- 9am: S&P CoreLogic CS 20- City NSA Index, prior 213.7; CS US HPI NSA Index, prior 205.8

- 10am: Conf. Board Consumer Confidence, est. 135.9, prior 137.9; Present Situation, prior 172.8; Expectations, prior 114.6

- 2:30pm: Fed’s Bostic, Evan and George Speak on Panel

DB’s Jim Reid concludes the overnight wrap

We took our three year old Maisie to the building site that is our new house over the weekend and this may have been a mistake as over the last two days she keeps on asking us why our new house is broken. She was particularly upset that a lot of windows and walls were missing and said she doesn’t want to live there as it would be too cold. Meanwhile Daddy’s bank account feels broken this morning as there was talk yesterday that one of our big suppliers might be about to call in the administrators. They have a healthy deposit of ours so it’s very annoying. It’s fair to say that costs are escalating from all angles and the EMR may need to still be running from an old people’s home in 50 years time to fund this.

From broken houses to slightly less broken markets. Given that the two Mondays prior to yesterday had seen moves of -1.66% and -1.97% for the S&P 500, yesterday reversed the trend as better news percolated through on some of the negative stories that have dominated of late. The S&P 500 closed last night +1.56% with the DOW and NASDAQ also up +1.46% and +2.06% respectively. The NYFANG index advanced +3.72%, despite Apple’s underperformance (initially down -1.18% before rebounding to close +1.35%) as the US Supreme Court signalled its willingness to hear a class action lawsuit over its app store pricing. Financials really led the way with the S&P Banks index rallying +2.30% for its best day since July. They had their European counterparts to thank for that, with the STOXX Banks index (+2.91%) seeing its best single day performance since July 2017. The broader STOXX 600 closed +1.23% and DAX +1.45%.

Italy was the main catalyst as sentiment improved on the potential for more positive negotiations with the European Commission. As we reported yesterday, the weekend saw less confrontational remarks from Salvini and Juncker. In addition, Salvini said yesterday that the government is “not getting stuck” over the decimals in the deficit target while fellow Deputy Premier Di Maio confirmed that “if, as part of the negotiation, we need to reduce the forecast deficit slightly, that’s not important to us.” Di Maio went on to say that “the issue is not the conflict with the EU on a deficit of 2.4%, what’s important is that not even a single person is kept out of the core measures.” Prior to this, we also had headlines on Bloomberg suggesting that an official for the League had said that the Government was looking at a new deficit target of 2.2% to 2.3%. Late in the evening, political leaders Conte, Salvini, and Di Maio released a joint statement after their meeting, confirming their less confrontational tone and again deemphasising the decimal place of the deficit number.

As we go to print headline are coming through from Italian finance minister Castelli that the deficit target is “almost certain” to be 2.2%. The question on everyone’s lips is what is the compromise number that the European Commission could realistically accept? A deficit in the 2.2% area is still unlikely to satisfy the EC, however a willingness to negotiate might be seen as the Italian government being aware of the implications of its actions. The Commission could even accept a somewhat vague framework as a rationale to defer a formal decision on Italy until into 2019, potentially alleviating some of the near-term event risk for Italy-linked

assets.

Before all this news the FTSE MIB closed yesterday up +2.77% while Italian Banks (+4.83%) had their best day since June. Two- and ten-year BTPs rallied -11.2bps and -13.8bps respectively – albeit off their yield lows for the session. Speaking of Italy, the ECB’s Peter Praet said yesterday that there has been very limited spill-over from a tightening of financial conditions in Italy to the broader Euro Area, but that conditions in Italy are “unsustainable” and “so something will have to give.” Praet’s general tone outside of this was constructive. His comments suggested that QE will finish in December as widely expected, but also that the ECB will have to clarify was it meant by “reinvesting for an extended period of time.” Praet also confirmed that guidance is “a very strong expectation” but also noted that “downside risks have increased noticeably.” This was notable as the Council has previously said that risks are “balanced.” Praet’s speech raised the anticipation levels for Draghi, who spoke in the afternoon. While his speech was virtually a copy and paste from his last on November 16th, he was later quoted as saying that “world growth momentum has slowed considerably” which is much stronger language compared to that used in the past. The December 13 ECB meeting will be key, and our economists still expect the Governing Council to announce the end of QE. Incoming data will dictate the evolution of policy, but we still expect growth and inflation to progress sufficiently to allow for an interest rate hike in September 2019.

Praet and Draghi are scheduled to speak again this week, on Wednesday and Thursday, respectively. We’ll also get several consequential communications from Federal Reserve officials, with speeches scheduled today for Vice Chair Clarida, tomorrow for Chair Powell, and Friday for NY Fed President Williams. The bottom line so far is that he doesn’t think there is sufficient evidence to ratify the market’s dovish interpretation of recent Fed communications, though that could change depending on what the Fed leadership says about the neutral rate, financial conditions, and global growth. So an important couple of speeches today and tomorrow from Clarida and Powell.

This morning in Asia markets are largely higher with the Nikkei (+0.88%), Shanghai Comp (+0.42%) and Kospi (+0.84%) all up while the Hang Seng (+0.01%) is trading flat after erasing earlier losses. Sentiment seems to have been impacted by US President Trump’s rhetoric, after an interview with the WSJ, that he will likely push forward with plans to increase tariffs on $200 billion of Chinese goods. He also suggested that the US would likely impose tariffs on the remainder of Chinese imports ($267bn) if the trade talks on the sidelines of the G20 fail. So the pressure builds ahead of the summit. Futures on S&P 500 (-0.18%) are pointing towards a softer start.

Back to yesterday, Bund yields edged up +2.1bps yesterday with the Italy news more important than any ECB slowdown worries. That move for BTPs and Bunds means the spread between the two yesterday was -15.9bps tighter and now at the tightest level in nearly three weeks. Meanwhile Treasury yields also backed up +2.0bps and are now sitting at 3.06%. Oil had a part to play in that with Brent and Crude bouncing +3.13% and +2.54% respectively – despite the news that Saudi Arabia had again raised its oil output – perhaps with hopes that the oversupply condition will be addressed at the G20 this week or the OPEC meeting next week. Tensions between Russia and the Ukraine over the weekend seemed to have less of an impact.

Not hurting the decent day for equities yesterday was news of a merger in the Greek Banking sector, however a sub-index of Greek banks did give up an early morning surge of as much as +11.57% to finish flat. A pretty substantial move and retracement! In the US, the auto sector advanced +3.98% for its sixth best day of the year, after General Motors announced a broad new restructuring plan. It plans to cut over 14,000 jobs and close five North American manufacturing plants next year, barring an agreement with its unions. GM’s share price rose +4.79% to a four-month high.

Elsewhere on Brexit, Donald Trump has suggested PM May’s Brexit agreement could threaten a US-UK trade deal. He told reporters the withdrawal agreement “sounds like a great deal for the EU” and meant the UK might not be able to trade with the US. The PM’s office insisted the deal is “very clear” the UK would be able to sign trade deals with countries around the world.

To the day ahead now, where this morning in Europe we’ll get November confidence indicators in France and Italy followed by the CBI’s retailing reported sales data in the UK for November. In the US this afternoon we’ll get various house price data points including the September FHFA house price index reading, Q3 house price purchase index reading and September S&P CoreLogic house price data. On top of that we’ll get the November consumer confidence survey which is expected to slip nearly 2pts to 135.8 in light of the recent wobbles in the equity market. That is, however, in the context of the 18-year high that the index reached last month. Away from the data, there will be plenty of focus on Fed Vice-Chair Clarida’s speech in New York today at 1.30pm GMT, especially around the topics of how he characterizes recent volatility in markets and the prospects for domestic and global growth. Fellow Fed officials Bostic, Evans and George will also speak this evening at 7.30pm GMT while the ECB’s Nouy, Costa and Mersch also speak at various stages. It’s worth also noting that starting today and continuing until Thursday, the three top candidates to take over from Merkel as head of the CDU will hold panel debates.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 1.13 POINTS OR 0.04% //Hang Sang CLOSED DOWN 44.22 POINTS OR 0.17% //The Nikkei closed UP 140.40 OR 0.64%/ Australia’s all ordinaires CLOSED UP .92% /Chinese yuan (ONSHORE) closed DOWN at 6.9485 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil UP to 51.59 dollars per barrel for WTI and 60.43 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.9485AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9439: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

The algos are going nuts as the markets reacted to a stale Nov 1 phone call. I extremely doubt that there will be a deal between China and the uSA

(courtesy zerohedge)

US-China Headline Confusion Sparks Overnight Market Turmoil

Demonstrating how on edge the market is over any favorable (and vice versa) developments in the ongoing US-China trade war, a couple of conflicting headlines out of China shortly before 3am ET sparked turmoil across asset classes.

Just a few hours after Trump’s interview with the WSJ, in which the president signaled that he would slap tariffs on remaining Chinese imports and he’ll likely push forward with plans to increase tariffs on $200 billion of Chinese goods, and which halted a strong Monday rally, S&P futures surged gaining as much as 0.5%, then falling back into negative territory, on comments from China foreign ministry spokesman Geng Shuang.

First, Bloomberg reported that during a briefing, Geng said that President Trump and Chinese leader Xi Jinping agreed to reach mutually beneficial agreements, sparking a rally in futures and a plunge in the dollar.

- TRUMP, XI AGREED TO REACH MUTUALLY BENEFICIAL AGREEMENTS: GENG

However, this quickly reversed and futures erased gains when moments later Geng said he was referring to the phone call on Nov. 1 which Trump had already tweeted about and which has now been long priced in if not forgotten.

- CHINA’S GENG REFERS TO NOV. 1 TRUMP-XI PHONE CALL

The result was the following violent move in the overnight S&P futures, which initially surged nearly 25 points in a matter of seconds, only to reverse the entire move as it emerged that the first headline was taken out of context.

The Bloomberg Dollar Spot Index also went on a roundabout trip between gains and losses as algos went from one extreme to another on the trade headlines.

While nothing had actually changed or been resolved, and there was no actual news following the Chinese presser, the dramatic moves show just how sensitive algos are to any changes in rhetoric and posture, and an indication of how much “coiled” upside there is in risk assets should Trump and Xi makes some soothing comments at the upcoming G-20 summit.

China Ambassador Warns Of “Dire Consequences” If No Deal, Hints At “All Out” War

Earlier today, Trump’s chief economic advisor Larry Kudlow poured cold water on expectations for an imminent resolution of the US-China trade war when he said that negotiations in the run up to this week’s G-20 talks “haven’t yielded any progress”, and unless something changes, the “administration will move ahead with the next phase of tariffs.”

“Things have been moving very slowly between the two countries,” Kudlow said, adding that it was up to Xi to come up with new ideas to break the deadlock. And, echoing a report from the US Trade Representative published earlier this month, Kudlow said there hasn’t been much of a change in China’s approach. “We can’t find much change in their approach,” Kudlow told reporters. “President Xi may have a lot more to say in the bilateral [with Mr Trump], I hope he does by the way, I think we all hope he does…but at the moment, we don‘t see it.”

Just a few hours later, a report by Reuters confirmed that Kudlow won’t be “seeing it” for a long time, because according to China’s ambassador to the US, Cui Tiankai, China is going to this week’s G-20 summit hoping for a deal to ease a damaging trade war with the United States, even as he warned of “dire consequences” if U.S. hardliners – read the trade hawks led by Peter Navarro – try to separate the world’s two largest economies.

China’s ambassador to the United States Cui TiankaiAsked whether he thought hardliners in the White House were seeking to separate the closely linked U.S. and Chinese economies, Cui said he did not think it was possible or helpful to do so, but warned that “I don’t know if people really realize the possible consequences – the impact, the negative impact – if there is such a decoupling.”