GOLD: $1246.80 UP $8.35 (COMEX TO COMEX CLOSINGS)

Silver: $14.60 UP 16 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1248.70

silver: $14.62

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 707 NOTICE(S) FOR 70,700 OZ (2.199 tonnes)

Total number of notices filed so far for DEC: 5982 for 527,500 OZ (18.606 TONNES)

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

128 NOTICE(S) FILED TODAY FOR 640,000 OZ/

Total number of notices filed so far this month: 3328 for 16,640,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3503: DOWN 106

Bitcoin: FINAL EVENING TRADE: $3463 DOWN136

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A SMALL SIZED 125 CONTRACTS FROM 178,649 DOWN TO 178,358 WITH YESTERDAY’S 5 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

526 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 526 CONTRACTS. WITH THE TRANSFER OF 526 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 526 EFP CONTRACTS TRANSLATES INTO 2.630 MILLION OZ ACCOMPANYING:

1.THE 5 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 19.070 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 6753 CONTRACTS (FOR 5 TRADING DAYS TOTAL 6753 CONTRACTS) OR 33.76 MILLION OZ: (AVERAGE PER DAY: 1351 CONTRACTS OR 6.75 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 33.76 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.82% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,710.79 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 185 WITH THE 5 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 526 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A TINY SIZED: 526 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 526 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 185 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.44 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9050 BILLION OZ TO BE EXACT or 129% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 128 NOTICE(S) FOR 640,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 19.070 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY SMALL SIZED 804 CONTRACTS UP TO 396,818 WITH THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $1.60//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7979 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 7979 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 396,818. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8783 CONTRACTS: 804 OI CONTRACTS INCREASED AT THE COMEX AND 7979 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 8783 CONTRACTS OR 878,300 OZ = 27.32 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A TINY RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.60??

YESTERDAY, WE HAD 5375 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 39,302 CONTRACTS OR 3,930,200 OZ OR 122.24 TONNES (5 TRADING DAYS AND THUS AVERAGING: 7860 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAYS IN TONNES: 122.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 122.24/2550 x 100% TONNES = 4/79% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,886.63 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED INCREASE IN OI AT THE COMEX OF 804 WITH THE GAIN IN PRICING ($1.60) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7979 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7979 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 8783 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7979 CONTRACTS MOVE TO LONDON AND 804 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 27.32 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE RISE OF $1.60 IN YESTERDAY’S TRADING AT THE COMEX

we had: 707 notice(s) filed upon for 70,700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.35 TODAY

A BIG CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.51 TONNES

/GLD INVENTORY 759.73 TONNES

Inventory rests tonight: 759.73 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 16 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 318.735 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 185 CONTRACTS from 178,543 DOWN TO 178,358 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

526 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 526 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 185 CONTRACTS TO THE 526 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 341 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 1.705 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 19.070 MILLION OZ STANDING IN DECEMBER.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 5 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 526 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 0.71 POINTS OR 0.03% //Hang Sang CLOSED DOWN 92.62 POINTS OR 0.82% //The Nikkei closed DOWN 177.06 OR 0.82%/ Australia’s all ordinaires CLOSED UP 0.37% /Chinese yuan (ONSHORE) closed UP at 6.8815 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.86 dollars per barrel for WTI and 60.84 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.8815AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8881: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

a)The following is a must must read as Luongo explains the folly of Trump’s trade wars and how ultimately the USA will fall

( Tom Luongo)

b)China is still acting cool as they prepare on some sort of retaliation to the Huawei CFO arrest

( zerohedge)

c)Not good: Huawei CFO has been charged with fraud as one of companies subsidiaries, Skycom, concealed the true relationship with Huawei as the subsidiary dealt with Iran and sold them stuff with USA made stuff.

( zerohedge)

Now that we witness the arrest of Meng on fraud charges, I guess it is safe to say that no American will wish to travel to China. Employees of USA owned companies

in China are also very worried

( zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

France overtakes Denmark and Sweden as the most taxed nation on earth.

( Mish Shedlock/Mishtalk)

ibFRANCE

Tomorrow ought to be interesting as france readies a fleet of armoured vehicles ahead of “act iv” of the yellow vest fiots.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

CANADA

With Canada in turmoil with growth decelerating and a material weaker oil sector and a drop in business sentiment, somehow Canada added a very strong 94,000 jobs last month….we are learning how to fudge data from our neighbour to the south

( zerohedge)

7. OIL ISSUES

Oil rises on a bigger than expected production cut

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)GOOD LUCK TO THE VENEZUELANS WHO ARE TRYING TO REPATRIATE THEIR LAST 14 TONNES OF GOLD

( Reuters/GATA)

iii)Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

iv) I have been watching the comex gold deliveries this month and we have seen a big change. For one, instead of gold deliveries morphing into London based forwards, we are witnessing more gold standing at the comex. To tell you the truth, I did not pay attention to the fact that the stoppers or users of the deliveries were to a large extent Goldman Sachs and one major player from JPMorgan..

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)early morning after the release of the jobs report

gold jumps on poor jobs report/oil jumps on Saudi /OPEC oil deal/dollar dumps

( zerohedge)

b)After the USA sent out the mouthpiece Kudlow to jolt the markets northbound, the effect did not last long as investors started to dump big time

( zerohedge)

ii)Market data/

a)A big miss in the Nov. payrolls a rise to a disappointing 155,000 gain instead of 195,000. Two other downers: hourly earnings rose by only .2% instead of .3% and the average hrly week fell from 34.5 down to 35.4. All of this was blamed on the weather. The entire jobs report is a phony. It does not disclose the huge number of poor souls that give up trying to find a job

( zero hedge)

c)Soft data U.Mich sentiment is flat and the hope section plummets as home buying conditions hit a 10 yr low( zerohedge)

a)Good looking girl! Heather Nauert is to be named UN ambassador. She lacks experience but she will be fine

( zerohedge)

b)This is ominous for the Democrats…the CFO of the Clinton foundation is spilling the beans as he states:

iv)SWAMP STORIES

a)Trump slams the FBI, Comey as Mueller is set to release documents on Cohen and Manafort which may give some insight into the fake Russian probe

( zerohedge)

b)the clowns are at it again. Why waste time questioning these bozos. Trump should just release the classified documents and be done with it. The public is smart enough to realize what is going on.

( zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 630 contracts standing for a loss of 157 contracts. We had 173 contracts stand for delivery yesterday so we gained 16 contracts or an additional 80,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating to accept a fiat bonus. We continue where we left off last month as queue jumping in silver is the norm for at least 20 months.

After December we have the non active January contract month and here we saw a gain of 11 contracts up to 1953 contracts. February saw its another 4 contract gain to stand at 51. March, the next big delivery month after December saw a GAIN of 142 contracts UP to 145,842

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– As Brexit looms, the Central Bank of Ireland has refused to discuss the location and value of Irish gold reserves

– No date given for removal of “commercially sensitive” gold reserves from Bank of England vaults

– Bank of England vaults in London believed to hold almost €200 million of Irish gold

– Ireland’s financial system & economy is hugely exposed to a Brexit downturn

IRELAND’S Central Bank has refused to say if it plans to move almost €200m worth of gold bars from the vaults of the Bank of England as a result of Brexit, insisting that any such move would be “commercially sensitive”.

The gold reserves have been held by its UK counterpart for a number of years, and the Central Bank has traditionally been coy on the precise details of the reserves, and the terms of the arrangement it has with the Bank of England.

It refused to be drawn yesterday on whether the reserves would be removed from the Bank of England either before or after the Brexit deadline of next March.

“It is for the Central Bank to determine how Ireland’s gold reserves ought to be managed,” a spokeswoman told the Irish Independent.

“The Central Bank’s portfolio is managed in line with approved parameters, which are kept under regular review and we report on key activities and developments in our annual report,” she added.

“The Central Bank’s transactions in gold are commercially sensitive and no further comment can be made at this time,” she said.

The latest Central Bank annual report shows that it had €209.3m worth of gold and gold receivables on its books at the end of 2017.

It’s believed that included €193.5m worth of fine gold held as gold bars with the Bank of England, and an additional amount of gold coins held at the Central Bank.

Editors note: This is an important story which we have covered quite frequently over the years and indeed have prompted politicians and journalists to ask questions about. Hopefully, on this occasion the story gets a bit of traction and there is a debate about the location, value and actual ownership of Irish gold reserves.

Ireland’s gold reserves and indeed the private ownership of gold by Irish investors, pension funds etc is important given the risks posed to Ireland today.

Ireland’s financial system and economy is hugely exposed to a Brexit downturn with more than a quarter of lending by main Irish banks to borrowers in the UK as reported by the Irish Independent today.

Institutional gold vaults are now available in Ireland for the first time via GoldCore and its storage partners. We will be giving the Central Bank of Ireland a call to see if we can assist them with repatriating the Irish gold reserves to where they belong – in secure vaults in Ireland.

Related Content

Does Bank Of England Hold €235 Million Of Irish Gold Reserves? (GoldCore)

UK bank sits on a pot of €235m in Irish gold (GoldCore via Irish Independent)

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

Gold notches a gain as stock market tumbles amid intensifying U.S.-China clash (MarketWatch.com)

Gold notches a gain as stock market tumbles amid intensifying U.S.-China clash (MarketWatch.com)

Gold climbs to near 5-month peak as dollar, stocks decline (CNBC.com)

Gold-backed ETFs up on stock volatility in November (Reuters.com)

Dow rebounds from 780-point plunge, ends day just slightly lower (CNBC.com)

Venezuelan officials seek meeting with Bank of England over gold repatriation (Reuters.com)

Source: Gold.org

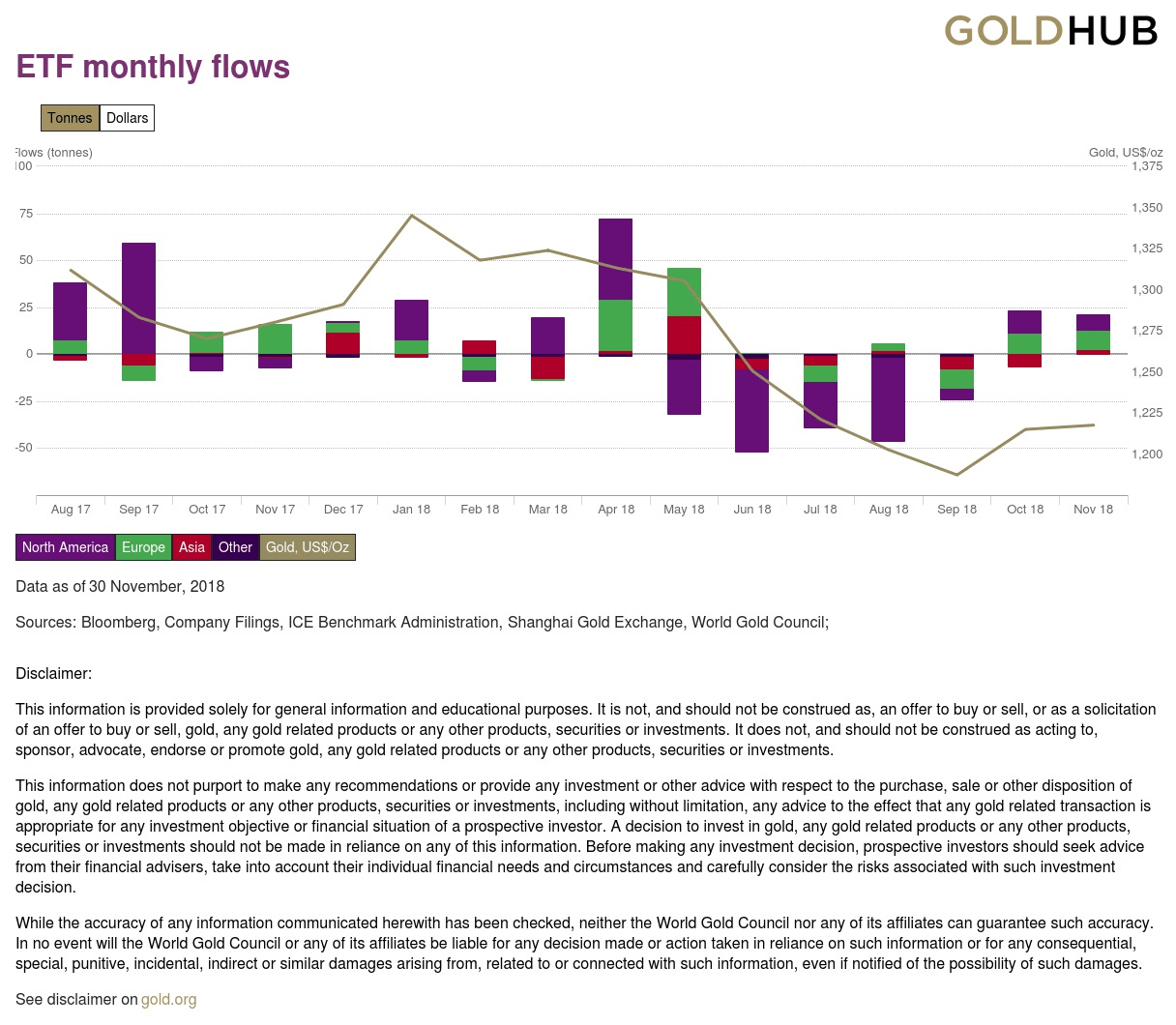

Global gold backed ETF flows are now positive in 2018 (Gold.org)

Gold tends to bottom quicker and display an inverse correlation to risk assets. (MarketWatch.com)

Why buy gold now? Because I don’t know (SovereignMan.com)

The Art Of Defaulting (ValueWalk.com)

Panic Buying Hits Palladium Market: What Comes Next? (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

06 Dec: USD 1,236.45, GBP 971.48 & EUR 1,091.66 per ounce

05 Dec: USD 1,236.15, GBP 970.13 & EUR 1,090.16 per ounce

04 Dec: USD 1,239.25, GBP 966.74 & EUR 1,086.45 per ounce

03 Dec: USD 1,231.05, GBP 966.00 & EUR 1,084.92 per ounce

30 Nov: USD 1,220.45, GBP 956.95 & EUR 1,073.75 per ounce

29 Nov: USD 1,226.25, GBP 960.03 & EUR 1,077.87 per ounce

Silver Prices (LBMA)

06 Dec: USD 14.38, GBP 11.28 & EUR 12.68 per ounce

05 Dec: USD 14.48, GBP 11.34 & EUR 12.75 per ounce

04 Dec: USD 14.55, GBP 11.35 & EUR 12.77 per ounce

03 Dec: USD 14.39, GBP 11.31 & EUR 12.69 per ounce

30 Nov: USD 14.24, GBP 11.16 & EUR 12.52 per ounce

29 Nov: USD 14.26, GBP 11.17 & EUR 12.55 per ounce

Recent Market Updates

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

Brandon White: Arctic trails, winter gales, and gold’s secret tales

Submitted by cpowell on Thu, 2018-12-06 19:53. Section: Daily Dispatches

2:55p ET Thursday, December 6, 2018

Dear Friend of GATA and Gold:

The London Bullion Market Association’s new format for reporting gold trading by its members is less complete and understandable than the previous one, BMG Group market analyst Brandon White writes today for Palisade Research. Essentially, White writes, the LBMA appears to be preventing disclosure of central bank intervention in the gold market. His analysis is headlined “Arctic Trails, Winter Gales, and Gold’s Secret Tales” and it’s posted at Palisade Research’s internet site here:

https://palisade-research.com/golds-secrets/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

GOOD LUCK TO THE VENEZUELANS WHO ARE TRYING TO REPATRIATE THEIR LAST 14 TONNES OF GOLD

(courtesy Reuters/GATA)

Venezuelan officials seek meeting with Bank of

England over gold repatriation,sources tell Reuters

Submitted by cpowell on Fri, 2018-12-07 01:57. Section: Daily Dispatches

By Mayela Armas

Reuters

Thursday, December 6, 2018

CARACAS — Two high-ranking Venezuelan officials are traveling to London with plans to meet with the Bank of England over the repatriation of $550 million in gold held in the bank’s coffers, according to two sources with knowledge of the situation.

The government of President Nicolas Maduro is seeking to bring 14 tonnes of gold back to Venezuela because of fears it could be caught up in international sanctions on the country, sources told Reuters this month.

…

The gold is a crucial asset for the struggling OPEC nation, where hyperinflation is expected to reach 1 million percent this year and a broad economic collapse has fueled an exodus of some 3 million people since 2015.

Maduro’s critics, including exiled opposition leader Julio Borges, have argued that the gold should not be repatriated because it could be used to finance corruption.

Finance Minister Simon Zerpa, who is under sanction by the United States over corruption concerns, and Central Bank Chief Calixto Ortega plan to discuss the issue with Bank of England officials on Friday, said the sources, who asked not to be identified. …

The Trump administration levied a new round of sanctions a month ago against Venezuela meant to disrupt its gold exports.

But blocking repatriation of Venezuela’s gold would be politically explosive for the Bank of England.

The bank offers gold custodian services to many developing countries, which would likely be concerned that they could be targeted for having adversarial relationships with Washington. …

… For the remainders of the report:

https://www.reuters.com/article/us-venezuela-gold/venezuela-officials-se…

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

London metals trader told CFTC, Justice about JPM’s market rigging 7 years ago

Submitted by cpowell on Fri, 2018-12-07 18:18. Section: Daily Dispatches

1:20p ET Friday, December 7, 2018

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire, interviewed today by King World News, says he alerted the U.S. Commodity Futures Trading Commission and Justice Department seven years ago to the gold and silver market rigging done by a JPMorganChase trader who recently confessed in a plea bargain with the Justice Department.

Maguire says the Justice Department’s intervention here, which has delayed civil lawsuits against the investment bank, aims to buy time so higher-ups can be protected.

Maguire’s interview is excerpted at KWN here:

https://kingworldnews.com/whistleblower-andrew-maguire-a-trip-down-the-r…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

What Do China And Goldman Sachs Have In Common?

Gold is not only flowing from West to East.

It is also flowing into the house account at Goldman Sachs. Or at least the paper claims for it in New York.

Below is the monthly report showing the large amounts of physical gold which have been steadily flowing through the Shanghai markets into strong hands in China.

Few commentators are talking about this.

What is less familiar, and what I have not read about much, is the very large amount of gold that Goldman Sachs has been taking delivery on the Comex this month.

Below are a few of the clearing reports below.

![]()

![]()

![]()

![]()

Notice that the big takers are the house account at Goldman, and some presumably large customer at JPM.

What’s up with that?

end

________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8815/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8881 /shanghai bourse CLOSED UP 0.71 POINTS OR 0.03%

. HANG SANG CLOSED DOWN 92.62 POINTS OR 0.82%

2. Nikkei closed UP 177.06 POINTS OR 0.82%

3. Europe stocks OPENED ALL GREEN

/USA dollar index RISES TO 96.95/Euro FALLS TO 1.1370

3b Japan 10 year bond yield: FALLS TO. +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.80/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.86 and Brent: 60.84

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.25%/Italian 10 yr bond yield DOWN to 3.16% /SPAIN 10 YR BOND YIELD UP TO 1.46%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.91: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.23

3k Gold at $1240.40 silver at:14.49 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 7/100 in roubles/dollar) 66.93

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.85DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9933 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1294 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.25%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning. Thirty year rate at 3.14%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3314

S&P Futures Slide, Europe Jumps As Traders Beg For

Chaotic Week To Week

There is a sense of almost detached resignation amid trading desks as we enter the last trading day of a chaotic, volatile week that has whipsawed and stopped out virtually everyone after the Nasdaq saw the biggest intraday reversal since April, and pattern and momentum trading has become impossible with one headline tape-bomb following another.

After yesterday furious tumble and sharp, last hour rebound, US equity futures are once again lower expecting fresh developments in the Huawei CFO arrest and trade war saga while today’s payroll report may redirect the Fed’s tightening focus in wage growth comes in hotter than the 3.1% expected; at the same time European stocks have rebounded from their worst day in more than two years while Asian shares posted modest gains as investors sought to end a bruising week on a more upbeat note. While stock trading was far calmer than Thursday, signs of stress remained just below the surface as the dollar jumped, Treasuries rose and oil whipsawed amid fears Iran could scuttle today’s OPEC deal.

The MSCI All-Country World Index, which tracks shares in 47 countries, was up 0.3% on the day, on track to end the week down 2%.

After Europe’s Stoxx 600 Index sharp drop on Thursday, which tumbled the most since the U.K. voted to leave the EU in 2016, Friday saw Europe’s broadest index jump 1.2% as every sector rallied following the cautious trade in the Asia-Pac session and the rebound seen on Wall Street where the Dow clawed back nearly 700 points from intraday lows. European sectors are experiencing broad-based gains with marginal outperformance in the tech sector as IT names bounce back from yesterday’s Huawei-driven slump.

Technology stocks lead gains on Stoxx 600 Index, with the SX8P Index up as much as 2.3%, outperforming the 1.1% gain in the wider index; Nokia topped the sector index with a 5.9% advance in Helsinki after Thursday’s public holiday, having missed out on initial gains from rival Huawei’s troubles that earlier boosted Ericsson. Inderes said the arrest of Huawei CFO over potential violations of American sanctions on Iran will benefit Nokia and Ericsson, who are the main rivals of Huawei and ZTE. Similarly, Jefferies wrote in a note on Chinese networks that China may have to offer significant concessions to buy Huawei an “out of jail” card and reach a trade deal, with China’s tech subsidies and “buy local” policies potentially under attack. “For example, why would Nokia and Ericsson have only 20% share in China’s 4G market,” analysts wrote.

Meanwhile, energy names were volatile as the complex awaits further hints from the key OPEC+ meeting today. In terms of individual movers, Fresenius SE (-15.0%) fell to the foot of the Stoxx 600 after the company cut medium-term guidance, citing lower profit expectations at its clinics unit Helios and medical arm Fresenius Medical Care (-7.8%). The news sent Fresenius BBB- rated bonds tumbling, renewing fears of a deluge of “fallen angels.” On the flip side, Bpost (+7.5%) and Tesco (+4.8%) are hovering near the top of the pan-Europe index amid broker upgrades.

Earlier in the session, Japanese equities outperformed as most Asian gauges nudged higher. MSCI’s broadest index of Asia-Pacific shares outside Japan nudged up 0.2%, though that followed a 1.8 percent drubbing on Thursday. Japan’s Nikkei added 0.8 percent. Chinese shares, which were up earlier in the day, slipped into negative territory with the blue chips off 0.1 percent.

E-Mini futures for the S&P 500 also started firmer but were last down 0.4 percent. Markets face a test from U.S. payrolls data later in the session amid speculation that the U.S. economy is heading for a tough patch after years of solid growth.

Will the last employment report released this year (the December report comes out in early January) help markets to continue to form a base?The consensus for nonfarm payrolls today is for a 198k print, following the stronger-than expected 250k reading last month.Average hourly earnings are expected to rise +0.3% mom which should be enough to keep the annual reading at +3.1% yoy while the unemployment rate is expected to hold steady at 3.7%. DB’s economists are more or less in line with the consensus with a 200k forecast and also expect earnings to climb +0.3% mom, however that would be consistent with a small tick up in the annual rate to +3.17% and the fastest pace since April 2009. They also expect the current pace of job growth to push the unemployment rate down to 3.6% which would be the lowest since December 1969.

Meanwhile, Fed Chairman Jerome Powell confused traders when late on Thursday, he emphasized the strength of the labor market, throwing a wrench into trader expectations the Fed is poised to pause tightening – arguably the catalyst for Thursday’s market-closing ramp following a WSJ article which reported Fed officials were considering whether to signal a new wait-and-see mentality after a likely rate increase at their meeting in December.

While Friday’s market has stabilized, for many the recent gyrations are just too much. For Dennis Debusschere, head of portfolio strategy at Evercore ISI, there’s still far too much risk to wade back into a market this riven by volatility. “Overall still untradeable in our opinion, until we get more clarity on trade and we think it will pay to wait this out,” he wrote in a note to clients Thursday. “That being said, our desk is open for business if you’re feeling up to trading this backdrop.”

Meanwhile, the big question is what happens next year: “The big question mark still is what’s going to happen in 2019” with the Fed, Omar Aguilar, CIO of equities and multi-asset strategies at Charles Schwab, told Bloomberg TV. “The jobs report could easily be the catalyst that will tell us a little more about what the path may be.”

Expecting that a big slowdown is coming, interest rate futures rallied hard in massive volumes with the market now pricing in less than half a hike next year, compared to just a month ago when they had been betting on more than two increases. Treasuries extended their blistering rally, driving 10-year yields down to a three-month trough at 2.8260 percent, before last trading at 2.8863 percent. Yields on two-year notes fell a huge 10 basis points at one stage on Thursday and were last at 2.75 percent. Investors also steamrolled the yield curve to its flattest in over a decade, a trend that has historically presaged economic slowdowns and even recessions.

The seismic shock spread far and wide. Yields on 10-year paper sank to the lowest in six months in Germany, almost 12 months in Canada and 16 months in Australia. Italian debt climbed as European bonds largely drifted.

The greenback advanced against most of its Group-of-10 peers ahead of U.S. jobs data that are expected to show hiring slowed last month. The pound fell as U.K. Prime Minister Theresa May was said to be weighing a plan to postpone the vote on her Brexit deal.

In commodity markets, gold firmed to near a five-month peak as the dollar eased and the threat of higher interest rates waned. Spot gold stood 0.1 percent higher at $1,239.49 per ounce. Oil was less favored, however, falling further as OPEC delayed a decision on output cuts while awaiting support from non-OPEC heavyweight Russia. Brent futures fell 0.5 percent to $59.77 a barrel, while U.S. crude also lost half a percent to $51.19. Cryptocurrencies continued their collapse with fresh losses after U.S. regulators dashed hopes that a Bitcoin exchange-traded fund would appear before the end of this year.

Market Snapshot

- S&P 500 futures down 0.4% to 2,680.00

- STOXX Europe 600 up 1.3% to 347.69

- MXAP up 0.2% to 151.21

- MXAPJ up 0.2% to 485.67

- Nikkei up 0.8% to 21,678.68

- Topix up 0.6% to 1,620.45

- Hang Seng Index down 0.4% to 26,063.76

- Shanghai Composite up 0.03% to 2,605.89

- Sensex up 0.9% to 35,631.53

- Australia S&P/ASX 200 up 0.4% to 5,681.49

- Kospi up 0.3% to 2,075.76

- German 10Y yield rose 0.8 bps to 0.244%

- Euro down 0.05% to $1.1368

- Italian 10Y yield rose 13.9 bps to 2.835%

- Spanish 10Y yield unchanged at 1.46%

- Brent futures up 0.2% to $60.16/bbl

- Gold spot up 0.2% to $1,239.70

- U.S. Dollar Index little changed at 96.88

Top Overnight News from Bloomberg

- The arrest of Huawei Technologies Co. Chief Financial Officer Meng Wanzhou in Canada over potential violations of American sanctions on Iran has triggered a debate in China over whether to carry on with trade talks with the U.S. or link the two issues and retaliate; Meng will have a bail hearing Friday to determine whether she is a flight risk and should remain in detention during proceedings on extradition to the U.S.

- Oil extended losses near $51 a barrel after OPEC entered a second day of talks in an attempt to draw up a deal to cut output. Iran sees no possibility of agreeing to reduce its output, Oil Minister Bijan Zanganeh said Friday

- Theresa May met with her top ministers in London on Thursday to discuss options of delaying the Dec. 11 Parliamentary vote on her Brexit deal to avoid a landslide defeat that would risk a major U.K. political crisis, according to a person familiar with the matter

- EU leaders are poised to turn their next summit into a Brexit crisis meeting, but so far, it doesn’t look like they’re willing to offer her anything that could help to break the deadlock in the U.K. Parliament

- Angela Merkel’s long exit from politics begins Friday when her party gathers in Hamburg to decide whether to appoint her chosen successor as its new leader or break with the legacy of her 13 years in charge of Germany

- Italian Finance Minister Giovanni Tria has complained that he is the victim of one ambush after another as his future is called into question amid tensions with populist leaders over a spending spree to fund election policies, according to newspaper Il Giornale

Asian stocks saw cautious gains with the region getting an early tailwind after the sharp rebound on Wall St, where most majors inished lower albeit off worse levels as tech recovered and the DJIA clawed back nearly 700 points from intraday lows. ASX 200 (+0.4%) and Nikkei 225 (+0.8%) were both higher at the open but gradually pared some of the gains as the risk tone began to turn cautious heading into today’s key-risk NFP jobs data. Hang Seng (-0.3%) and Shanghai Comp (U/C) were indecisive amid further PBoC inaction in which it remained net neutral for a 5th consecutive week and with the upcoming Chinese trade data over the weekend adding to tentativeness, while pharmaceuticals were the worst hit due to concerns of price declines from the government’s centralized procurement program. Finally, 10yr JGBs were flat amid a similar picture in T-note futures and although early selling pressure was seen in Japanese bonds alongside the strong open in stocks, prices later recovered as the risk appetite somewhat dissipated.

Top Asian News

- China’s FX Reserves Rose Despite Intervention, Outflow Signs

- Hong Kong May Slip Into Recession in 2019, Deutsche Bank Warns

- SoftBank Seeks to Assuage Investors on Pre-IPO Mobile Outage

- Southeast Asia Reserves Recover a Bit in November as Rout Eases

European equities extended on gains from the cash open (Eurostoxx 50 +1.2%) following the cautious trade in the Asia-Pac session and the rebound seen on Wall St where the Dow clawed back nearly 700 points from intraday lows. European sectors are experiencing broad-based gains with marginal outperformance in the tech sector as IT names bounce back from yesterday’s Huawei-driven slump. Meanwhile, energy names are volatile (currently marginally underperforming) as the complex awaits further hints from the key OPEC+ meeting today. In terms of individual movers, Fresenius SE (-15.0%) fell to the foot of the Stoxx 600 after the company cut medium-term guidance, citing lower profit expectations at its clinics unit Helios and medical arm Fresenius Medical Care (-7.8%). On the flip side, Bpost (+7.5%) and Tesco (+4.8%) are hovering near the top of the pan-Europe index amid broker upgrades.

Top European News

- LandSec, Undeterred by Brexit, Makes New Bet on London Offices

- Danske Says It’s Looking Into Selling Its Swedish Pension Assets

- Chinese Group Agrees to Buy Amer Sports in $5.2 Billion Deal

- Bad Air Warnings in London And Paris Peak With Fish And Chips

Currencies:

- DXY – Typically rangebound trade in the run up to US labour data, and with markets also monitoring OPEC+ headlines as a decision on whether to cut output and if so by how much remains highly uncertain. The index is hovering just under the 97.000 handle within a 96.767-96.931 band, and well within nearest technical support and resistance levels at 96.300 and 97.311 respectively.

- GBP – A marginal G10 underperformer as Cable retreats back below 1.2750 from just above 1.2800 at one stage, but this could be more flow-related rather than anything fundamental as Eur/Gbp rallied towards 0.8930 peaks from just under the big figure into the Frankfurt fixing before drifting back again. However, Halifax house prices were much weaker than expected and latest Brexit news is hardly Sterling supportive given more speculation about delaying the meaningful vote to try and avoid a resounding rejection, even though the Government appears to be resolute and standing firm on December 11.

- NZD/AUD – The Kiwi is at the opposite end of a relatively narrow Usd/Major spectrum, and like the Pound also impacted by indirect factors to a degree, if not in the main. Indeed, Nzd/Usd remains capped ahead of 0.6900, but Aud/Nzd is pivoting 1.0500 as the Aussie unit continues to feel the adverse effects of recent bearish impulses, namely softer than forecast Q3 GDP and a more dovish RBA via Debelle. Hence, Aud/Usd is softer between 0.7210-40 parameters and bound to be wary of huge option expiries from 0.7250-60 in 6.6 bn that form a formidable barrier ahead of circa 1.2 bn up at 0.7300.

- EUR/JPY – In the pre-NFP ‘hiatus’ and awaiting anything further on the Italian budget front, option expiries may also exert directional impetus on Eur/Usd and Usd/Jpy, as the former faces 2+ bn at the 1.1400 strike and latter is flanked by 1+ bn at 112.50 and 113.00.

- CAD – The Loonie has pared a bit more lost ground from recent lows, albeit partly due to a broad Usd retracement, eyeing OPEC and also Canada’s jobs report given latest BoC guidance indicating even greater data dependency. Usd/Cad currently just shy of the 1.3400 mark vs 1.3440+ at one stage yesterday.

In commodities, WTI (+0.2%) and Brent (+0.9%) are choppy in what was a volatile session thus far as comments from energy ministers emerged ahead of the key OPEC+ meeting, after yesterday’s OPEC talks ended with no deal for the first time in almost five years. Brent rose after source reports noted that Moscow are ready to cut output by 200k BPD (below OPEC’s desire of 250k-300k but above Russia’s prior “maximum” of 150k) if OPEC are willing to curb production by over 1mln BPD. Prices then fell to session lows following a less constructive tone from Saudi Energy Minister who reiterated that he is not confident there will be a deal today, which came after delegates noted that OPEC talks are focused on a combined OPEC+ cut of 1mln BPD (650k from OPEC and 350k from Non-OPEC). Markets are awaiting the start of the OPEC+ meeting after delegates stated that talks are at deadlocked as Iran appears to be the main sticking point to an OPEC deal, though sources emerged stating that Iran, Venezuela and Libya are set to get exemptions from cuts, adding that OPEC and Russia are looking for a symbolic production commitment from Iran as fears arise that Iran may not be able to follow-through on curb pledges due to US sanctions. In terms of metals, gold hovers around session highs and is set for the best week since August with the USD trading in a tight range ahead of the key US jobs data later today, while London copper rose over a percent is underpinned by the positive risk tone.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 198,000, prior 250,000

- Unemployment Rate, est. 3.7%, prior 3.7%; Underemployment Rate, prior 7.4%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.2%; YoY, est. 3.1%, prior 3.1%

- 8:30am: Average Weekly Hours All Employees, est. 34.5, prior 34.5

- 10am: Wholesale Inventories MoM, est. 0.7%, prior 0.7%; Wholesale Trade Sales MoM, prior 0.2%

- 10am: U. of Mich. Sentiment, est. 97, prior 97.5; Current Conditions, prior 112.3; Expectations, prior 88.1

- 3pm: Consumer Credit, est. $15.0b, prior $10.9b

DB’s Jim Reid concludes the overnight wrap

The age of innocence has truly gone in financial markets after a turbulent 24 hours but one that saw a spectacular rally after Europe closed last night and one that has steadily carried on in Asia overnight (more on this below). Before we get to that I’m on an intense client marketing roadshow at the moment on the 2019 Credit outlook and there are a litany of worries out there from investors. Maybe I’m trying to be too cute here but I think the problems we’re seeing in credit at the moment are more of a “ghost of Xmas future” rather than a sign of an imminent disaster scenario. However my overall confidence that credit will blow up around the end of this cycle has only intensified in the last couple of weeks. Liquidity is awful in credit and it’s been a broken two way market for several years (probably as long as I’ve worked in it – 24 years). However this has got worse this cycle as the size of the market has grown rapidly but dealer balance sheets have reduced. As such you can buy massive size at new issue but your ability to sell in secondary is constrained to a small percentage of this. This didn’t matter much when inflows dominated – as they mostly did in this cycle pre-2018 – but in a year of outflows across the board the lack of a proper two way market is increasingly being felt. As discussed I don’t think this is the start of the crisis yet but be warned that when this economic cycle does roll over or even starts to operate at stall speed the credit market will be very messy and will influence other markets again.

On the positive side and despite a very steep mid-session selloff, US markets ultimately closed well off the lows. The DOW, S&P 500 and NASDAQ finished -0.32%, -0.15% and +0.42% respectively, though they traded as low as -3.14%, -2.91%, and -2.43% respectively, around noon in New York. At its lows, the S&P 500 was on course for its worst two-session stretch since February, and before that you’d have to go back to August 2015 or 2011 to find the last episode with as steep a two-day drop. The DOW and S&P 500 dipped into negative territory for the year again, but clawed back and are now +0.92% and +0.84% YTD (+3.16% and +2.69% on a total return basis). The NASDAQ has clung to its outperformance, as it is now up +4.13% this year, or +5.20% on a total return basis, though of course the difference is narrower in the low-dividend paying, high-growth tech index.

Unsurprisingly, the moves yesterday coincided with higher volatility with the VIX climbing as much as +5.2pts to 25.94 and pretty much back to the October highs, though it too rallied alongside the equity market to end close to flat at 21.15. Meanwhile, the price action was even uglier in Europe as the US lows were around the close. The STOXX 600 plunged -3.09% and is down -4.22% in two days – the most in two days since June 2016. Nowhere was safe. The DAX (-3.48%), CAC (-3.32%), FTSE MIB (-3.54%) and IBEX (-2.75%) all saw huge moves lower. The DAX has now joined the Italy’s FSTEMIB in bear market territory, as it is now -20.49% off its highs earlier this year. The FTSEMIB is down -24.04% from its highs. European Banks – which were already down nearly -27% YTD going into yesterday – tumbled -4.29% for the biggest daily fall since May and the third biggest since immediately after Brexit. The index is now at the lowest since October 2016 and within 17% of the June 2016 lows all of a sudden. US Banks fell -1.87%, though they had dipped -4.3% at their troughs to touch the lowest level since September 2017.

As for credit, HY cash spreads in Europe and the US were +8.5bps and +14.8bps wider respectively. For context, US spreads are now at the widest since December 2016 and this is the best performing broad credit market over the last couple of years. In bond markets, 10y Treasuries rallied-2.4bps but was as much as 9bps lower intra-day. Thanks to an outperformance at the front end (two-year fell -3.7bps), the 2s10s curve actually ended a shade steeper at 13.0bps (+1.3bps on the day). However that move for the 10y now puts it at the lowest since September at 2.89%, and only +48.6bps above where we started the year. The spread on the Dec 19 to Dec 18 eurodollar contract – indicative for what is priced into Fed hikes for next year – is down to just 16bps. It was at 60bps in October. This certainly appears to be too low, though a Wall Street Journal article yesterday seemed to signal a willingness by the Fed to moderate its pace of rate hikes. Finally, in Europe, Bunds closed -4.1bps lower at 0.236%.

Quite amazing moves with Bunds continuing to defy all fundamental logic and trading instead as a risk-off lightning rod. There was some talk that the sharp moves lower at the open yesterday were exaggerated by the unexpected midweek close for markets in the US which resulted in futures systems failing to be programmed to adjust and orders backing up. However the combination of a -2.25% drop for WTI (-5.2% at the lows) post the OPEC meeting (more below) and the Huawei story that we mentioned yesterday certainly aided to the initial malaise. There was some talk that both the Chinese and US authorities would have been aware of the arrest before last weekend’s talks and as such this story shouldn’t be necessarily a threat to the truce, though Reuters reported last night that President Trump did not know about the planned arrest. The implications of this are unclear, since it could mean that Trump has less direct control over the arresting agency, but it could also indicate that the move is not part of trade policy. Either way, how this development will be key for the market moving forward, especially any response from Chinese officials.

This morning in Asia markets are largely trading higher with the Nikkei (+0.60%), Hang Seng (+0.21%), Shanghai Comp (+0.08%) and Kospi (+0.51%) all up. Elsewhere, futures on the S&P 500 (-0.11%) are pointing towards a flattish start. Meantime crude oil (WTI -0.39% and Brent -0.60%) prices are continuing to trade lower this morning. It wouldn’t be an EMR worth it’s place in the daily schedule without an Italy and Brexit update. As we go to print Italian daily La Stampa has reported that the Italian Premier Conte and Deputy Premier Di Maio are in favour of the resignation of Finance Minister Tria while Deputy Premier Salvini is against his resignation. So signs of tension. In the U.K. a few press articles (like Bloomberg) are suggesting that PM May is considering postponing Tuesday’s big vote. There doesn’t seem to be a lot of substance to the story at the moment but it mentions going back to the EU for concessions on the Irish backstop as one possibility. How the EU will feel would be the obvious question.

As mentioned earlier, oil had a difficult session yesterday, falling back to its recent lows with WTI touching a $50 handle and Brent trading back below $60 per barrel. The first day of the OPEC summit did not appear promising for the odds of a new production deal, as the ministers apparently discussed a 1 million barrel per day cut, below the 1.5 million needed to balance the market.The Libyan oil minister abruptly left before the day’s meetings concluded, and the organization canceled their scheduled press conference. The Russian delegation will join the OPEC contingent today in an effort to finalize a deal, but Saudi Energy Minister al-Falih said that “Russia is not ready for a substantial cut.” Watch this space today.

Overnight, the Fed Chair Powell delivered an upbeat message on the US economy and the Job market ahead of today’s payrolls release. He said, “our economy is currently performing very well overall, with strong job creation and gradually rising wages,’’ while adding, “in fact, by many national-level measures, our labour market is very strong.’’ Elsewhere, the Fed’s John Williams said yesterday that the biggest challenge which the policy makers are facing is achieving a soft landing. He said, “we have a pretty strong economy — unemployment pretty low, inflation near our goal — it’s just managing a soft landing, keeping this expansion going for the next few years.”

So will the last employment report released this year (the December report comes out in early January) help markets to continue to form a base? The consensus for nonfarm payrolls today is for a 198k print, following the stronger-thanexpected 250k reading last month. Average hourly earnings are expected to rise +0.3% mom which should be enough to keep the annual reading at +3.1% yoy while the unemployment rate is expected to hold steady at 3.7%. Our US economists are more or less in line with the consensus with a 200k forecast and also expect earnings to climb +0.3% mom, however that would be consistent with a small tick up in the annual rate to +3.17% and the fastest pace since April 2009. They also expect the current pace of job growth to push the unemployment rate down to 3.6% which would be the lowest since December 1969.

Going into that, yesterday’s ADP employment change report for November was a tad disappointing at 179k (vs. 195k expected) while more interestingly the recent tick up in initial jobless claims held with the print coming in at 231k. The four-week moving average is now 228k and the highest since April having gotten as low as 206k in September. So the climb, while not yet at concerning levels, is certainly notable and worth watching now on a week to week basis. As for the other interesting data points yesterday, the October trade deficit was confirmed as reaching a new cyclical wide. The ISM non-manufacturing print for November was a relative positive after coming in at 60.7, up 0.4pts from October and ahead of expectations for a decline to 59.0. Worth noting is that the three-month moving average of non-manufacturing ISM is now the highest on record which is a fairly reliable lead indicator for private nonfarm payrolls. US durable goods orders for October were revised slightly higher to -4.3% mom from -4.4%, though the core measures stayed at 0.0% mom. Factory orders declined -2.1% mom, though both were nevertheless higher year-on-year.

As for the day ahead, the aforementioned November employment in the US will no doubt be front and centre, however, prior to that, we’ve October industrial production prints in Germany and France, along with Q3 labour costs in the former, and the final Q3 GDP revisions for the Euro Area (no change from +0.2% qoq second reading expected). We’ll also get the monthly inflation reporting for November in the UK. Also due out in the US is October wholesale inventories and trade sales, the preliminary December University of Michigan survey and October consumer credit. November foreign reserves data in China is also expected out at some point. Away from that the OPEC/OPEC+ meeting moves into the final day while the ECB’s Coeure and Fed’s Brainard are scheduled to speak. Today is also the day that Germany’s ruling CDU party elects a new chair to succeed Merkel. Our FX strategists noted yesterday that according to polls, the result should be a close call between general secretary Annegret Kramp-Karranbauer (AKK) and Friedrich Merz. Broadly speaking, AKK stands for a continuation of the Merkel-era strategy of positioning the CDU at the centre of the political spectrum, whereas Merz stands for a sharpening of the party’s traditional profile as a centre-right party. Last night our German economics team put out a piece explaining the event and suggesting that Merz would be good for the DAX and AKK good for the Euro.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 0.71 POINTS OR 0.03% //Hang Sang CLOSED DOWN 92.62 POINTS OR 0.82% //The Nikkei closed DOWN 177.06 OR 0.82%/ Australia’s all ordinaires CLOSED UP 0.37% /Chinese yuan (ONSHORE) closed UP at 6.8815 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.86 dollars per barrel for WTI and 60.84 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.8815AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8881: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

The following is a must must read as Luongo explains the folly of Trump’s trade wars and how ultimately the USA will fall

(courtesy Tom Luongo)

Mr. Tariff Ups The Ante On China

Donald Trump just jumped the shark calling himself, “Mr. Tariff.” He believes a trade deficit is akin to stealing the wealth of a nation. It isn’t.

Under normal conditions a trade deficit is simply a reflection of the difference in comparative advantage of one country’s workers over another. And the value of the currency is supposed to rise and fall to offset that state of affairs over time.

Donald Trump has, in the words of David Stockman, “A 17th century view on global trade.”

It is one born of a complete misunderstanding of how and why trade imbalances occur, why they will re-balance if allowed and why, ultimately, they are irrelevant.

But, Trump can’t or won’t see it that way. He refuses to accept that we are the creators of our persistent trade deficit with China. That the trade deficit stems from running budget deficits and applying Keynesian counter-cyclical monetary policy or, worse, QE to protect domestic asset prices.

It also stems from our being the world’s reserve currency which places an insane demand on the Fed to keep the flow of dollars rising to liquefy global trade.

He complains that international tariffs regimes are unfair. But, as Stockman has consistently pointed out tariff levels globally are nearly non-existent running at around 3% on average. This is the period of freest trade we’ve seen in the era of the modern nation state, but Trump looks at these niggling things, these small things and can’t see the forest for them.

Mr. Inflexible

It speaks of ideological possession on the subject. It speaks to inflexibility of mind.

“Germany taxes our cars too high, slap a tariff on them.” He’s obsessed with German car exports. Germans don’t buy GM’s because they are shitty cars, not because they are more expensive.

A level playing field won’t help a company handed over to the UAW, stiffing the bondholders, and run by morons. The only reason GM still functions is because they make bad cars to sell to people who can’t afford a good car and ‘patriots’ who buy Silverados instead of F-150s.

“Canada won’t buy our milk,slap on tariffs and threaten NAFTA,” cries Mr. Tariff. Not that NAFTA shouldn’t just be abolished completely, but whatever, Trump doesn’t believe in free trade, he believes in extortive trade because, ‘Merica First.

If China won’t import our oil but buys Iran’s instead, then they are our enemy then we sanction them and extort higher imports of it.

It’s all childish and immoral in a way that is, frankly, embarrassing to anyone with three working brain cells to rub together and make a spark.

But, the real undercurrent in all of this is Trump’s obsession with China ‘stealing our technology’ and leap-frogging the U.S. as a technology leader.

Which way on Huawei?

And that’s why Huawei’s CFO was arrested in Canada while Trump was negotiating with Chinese Premier Xi Jinping over the weekend over the company violating U.S. sanctions on Iran.

Leaving aside the pure insanity of Canada arresting a Chinese national for her company violating U.S. sanctions on Iran which China was not a party to, this is a dangerous escalation by the U.S. over what is, essentially, something that is ultimately not enforceable, U.S. technology licensing.

It’s simply bullying. But, since Trump is a bully, what else is new?

But, the real issue here is that, in very short order, Huawei has become a global leader in 5G infrastructure technology which the U.S. is falling behind on. And now with this arrest Trump is betting that he can scare everyone else into not buying their superior products through the ruinous application of sanctions policies.

The West has been systematically cutting Huawei out of the global 5G rollout because of ‘security’ concerns. More like profit concerns. It is, simply, typical protectionism by Mr. Tariff himself.

And he’s made no bones about any of this. Trump has stated quite emphatically that all a policy has to do is pass his ‘America First’ sniff test and it’ll get implemented.

And since he’s not a deep thinker, all he cares about are first-order effects and how he can sell it on his Twitter feed to his now brain-dead base who believes all of this ‘China hacked muh everything’ narrative we’re being inundated with all of a sudden.

Trump knows that now China’s tech industry isn’t just the manufacturing arm of U.S. multinationals. We’re staring at equivalence in a lot of areas. And the rate of catch up China is playing in this arena is threatening our long-term competitiveness.

Hence going after Huawei, a phenomenal success story, and ZTE. While Apple focuses on tactical things like end-user products — phones, watches, and media services — Huawei started there, creating homegrown Chinese variants of the iPhone and built a company focused on the future of communications infrastructure, 5G, with the end-user product the face of the company to build Apple-like brand loyalty in China.

This is the public face of the future trade war. Will Americans continue buying, say, iPhones and watches over their Chinese knock-off counterparts at half the price?

Flow not Stock, Don

So, I understand completely Trump’s problem with the current situation and the past that led to this state of affairs. What I disagree with is the magic of tariffs to reverse the flow of capital out of the country.

He’s taken some steps in the right direction — tax cuts, tax amnesty for repatriating offshore corporate profits, lowering certain regulations — but that’s not nearly enough. It can’t and won’t solve the real problem of the expense of doing business in the U.S.

His critics on the left are right that a lot of those tax breaks didn’t go to fund new sustainable growth and that a lot of it went to fuel buybacks and pay dividends. But they miss the reason why, it isn’t because Trump wanted to repay his corporate overlords, it’s because idiotic leftist policy inertia and insane monetary policy has kept the cost of business expansion higher than protecting the corporate balance sheet or returning the money to shareholders.

His $1 trillion per year deficit, itself a source of the trade imbalance with China, will explode now that his growth story is dying, emerging markets are starved for dollars, supply chains are freezing up because of the U.S.’s increasingly erratic behavior and debt levels around the world choking out growth.

Trump wants a weaker dollar, and for a little while he may get it as the market misreads what’s happening here. Any Fed dovishness will be seen as dollar negative versus being globally accommodative to worsening economic conditions amplifying debt servicing costs.

His classic mercantilist mindset will applaud this and it might abate the worsening trade deficit numbers for a time, but it won’t change the trend against him regardless of the Fed raising rates or not in 2019.

The world economy is deflating and Trump’s tariffs, arrests and sanctions only tell people that capital is not welcome in the U.S. His only saving grace in 2019 is that the leadership in Europe is even dumber on these issues than he is.

The consumer is ultimately sovereign. It’s their money and its their time. If you are so arrogant as to believe you are indispensable to your customers you will find out very quickly what they think of that. And customers of the U.S. dollar are rapidly coming to the conclusion that the cost of doing business in it is too high.

In the game of global capital you don’t have to be good, you just have to treat it slightly better than everyone else to see the inflows come your way. Trump is alienating everyone and ensuring that companies like Huawei find ways to never do business with the U.S. ever again.

end

China is still acting cool as they prepare on some sort of retaliation to the Huawei CFO arrest

(courtesy zerohedge)

China Prepares Retaliation To Huawei CFO Arrest

As Beijing’s outrage over the arrest of Huawei CFO Wanzhou Meng simmers ahead of her Friday arraignment in a Canadian court, Bloomberg has shed some light on how news of her arrest has resonated with different factions in the Chinese leadership.

The upshot is that while officials in charge of managing China’s trade negotiations believe China shouldn’t allow Wanzhou’s arrest to impact trade negotiations, hardline national security officials believethe arrest is an embarrassment to Chinese leader Xi Jinping,who reportedly had ‘no idea’ that the daughter of a Chinese business icon and Communist Party member had been arrested in Canada – and that China should use trade talks as leverage to demand that she be released.

Western media outlets have reported that, while White House officials and National Security Advisor John Bolton knew about Wanzhou’s arrest before Saturday’s meeting between Trump and Xi, the president somehow had no idea.

Now, BBG is reporting that Xi similarly had no idea that one of his country’s most prominent executives had been taken into custody hours before he sat down with Trump. This asymmetry is viewed as deeply embarrassing to China’s leader, and many believe that simply letting trade negotiations to move forward as plan would be an unconscionable capitulation – particularly if (as many analysts believe) the Trump Administration intends to use her arrest as leverage.

Still others believe that Wanzhou’s arrest is a “gift” for Xi, because it gives cover for the Chinese to dig in their heels and accuse the US of using the trade war as a pretext to stymie China’s ascent as a global superpower. In light of Wanzhou’s arrest, such a stance would likely garner more sympathy from the rest of the world.

As China contemplates how to respond, at least there is one silver lining:It helps China appear sincere to the world in wanting to resolve the trade war. He can say he is trying to resolve the issue but the US has an entrenched strategy to cut off China’s rise as a global power – a theme that state-run media picked up on Friday.

“The Huawei arrest gives China’s leaders a huge gift,’ said Barry Naughton, a professor at the University of California in San Diego who studies China. “It makes super plausible the narrative they’ve been trying to promote all along: ‘The U.S. just can’t stand our rise, they can’t stand to lose their dominance, they can’t treat anybody like an equal.'”

But one salient fact has been agreed on by all sides: Wanzhou’s arrest doesn’t bode well for a trade detente.