GOLD: $1238.45 UP $1.60 (COMEX TO COMEX CLOSINGS)

Silver: $14.44 DOWN 5 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1238.00

silver: $14.47

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 1150 NOTICE(S) FOR 115,000 OZ (3.57 tonnes)

Total number of notices filed so far for DEC: 5275 for 527,500 OZ (16.407 TONNES)

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

173 NOTICE(S) FILED TODAY FOR 865,000 OZ/

Total number of notices filed so far this month: 3200 for 16,000,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3769: up 2

Bitcoin: FINAL EVENING TRADE: $3744 DOWN 82

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 1366 CONTRACTS FROM 179,909 DOWN TO 178,649 WITH YESTERDAY’S 6 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1752 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1752 CONTRACTS. WITH THE TRANSFER OF 1752 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1752 EFP CONTRACTS TRANSLATES INTO 8.76 MILLION OZ ACCOMPANYING:

1.THE 6 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 19.070 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 6227 CONTRACTS (FOR 4 TRADING DAYS TOTAL 6227 CONTRACTS) OR 31.14 MILLION OZ: (AVERAGE PER DAY: 1556 CONTRACTS OR 7.78 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 31.14 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.44% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,708.16 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1366 WITH THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 1260 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A TINY SIZED: 386 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1752 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1366 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.55 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .9050 BILLION OZ TO BE EXACT or 129% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 173 NOTICE(S) FOR 865,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 19.070 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY CONSIDERABLE SIZED 3905 CONTRACTS DOWN TO 396,014 WITH THE GAIN IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $4.25//.YESTERDAY’S TRADING) AS THESE GUYS JOINED SILVER IN THE ROUTINE MIGRATION OVER TO ETF’S AS WE APPROACH AN ACTIVE DELIVERY MONTH.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5375 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 5375 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 396,014. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1470 CONTRACTS: 3905 OI CONTRACTS DECREASED AT THE COMEX AND 5375 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 1752 CONTRACTS OR 175,200 OZ = 4.572 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.25

YESTERDAY, WE HAD 5233 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 31,323 CONTRACTS OR 3,132,300 OZ OR 97.42 TONNES (4 TRADING DAYS AND THUS AVERAGING: 7831 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAYS IN TONNES: 97.42 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 97.42/2550 x 100% TONNES = 3.82% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,861.81 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3905 WITH THE LOSS IN PRICING ($4.25) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5233 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5375 EFP CONTRACTS ISSUED, WE HAD A FAIR GAIN OF 2030 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5375 CONTRACTS MOVE TO LONDON AND 3905 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 6,14 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE FALL OF $4.25 IN YESTERDAY’S TRADING AT THE COMEX

we had: 1150 notice(s) filed upon for 115,000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.60 TODAY

NO CHANGE IN GOLD INVENTORY

/GLD INVENTORY 758.21 TONNES

Inventory rests tonight: 758.21 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 5 CENTS TODAY:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV

ANOTHER HUGE WITHDRAWAL OF 2.817 MILLION OZ/

/INVENTORY RESTS AT 318.735 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 1366 CONTRACTS from 179,909 DOWN TO 178,543 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1752 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1752 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1366 CONTRACTS TO THE 1752 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 386 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 1.930 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 19.070 MILLION OZ STANDING IN DECEMBER.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 6 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1752 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 44.62 POINTS OR 1.68% //Hang Sang CLOSED DOWN 663.30 POINTS OR 2.47% //The Nikkei closed DOWN 417.71 OR 1.91%/ Australia’s all ordinaires CLOSED DOWN 0.22% /Chinese yuan (ONSHORE) closed DOWN at 6.8934 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51/53 dollars per barrel for WTI and 60.11 for Brent. Stocks inEurope OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8934AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8965: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)It sure looks like the truce is over!! On behalf of the USA Canada arrests the CFO of Huawei and the daughter of the founder Ren Zhengfei. I am sure that Xi is not thrilled with this. The charge: the firm sold goods to Iran despite sanctions.

( zerohedge)

ii)Wednesday evening trading due to the above event; Dow futures crash over 500 points

(courtesy zerohedge)

iii)Deutsche bank announces that the arrest is a clear signal that the trade war is escalating to a new level.

( zerohedge)

iv)The USA attack on Huawei intensifies with the arrest of its CFO. You will recall that the USA outlawed all purchases of Huawei by the military as their were rumours of that Chinese have a backdoor entry into their products. That caused a storm of protests from China as this has not been proven. Now they arrested the founders daughter ( its CFO) and China has announced it will take appropriate measures

(courtesy zerohedge)

v)Bill Blain explains why the arrest is a big deal as the USA tries to limit Chinese growth in the technology field.

This global trade war in his words will become a shooting war…

( Bill Blain)

vi)A defiant Huawei states that it will not change ties with suppliers due to USA pressure and it knows no reason for the arrest of its CFO. The company states it is obeys all USA rules on not supplying sanctioned state actors

(courtesy zerohedge)

vii)I do not think that the markets will like this: as Bolton was sitting down for dinner with Xi, he was aware of the Huawei’s arrest. he is not sure if Trump new..

( zerohedge)

viii)We now learn the origins of the Huawei investigation: it was HSBC that flagged transactions between Huawei and Iran who sold the country parts mfg in the uSA

4/EUROPEAN AFFAIRS

i)UK

Chaos in Gr Britain as May lost 3 procedural votes. Bloomberg outlines what will happen after the Brexit vote.

(courtesy zerohedge)

ii)FRANCE

My goodness: France is set to deploy 89,000 cops as they fear a huge yellow vest rebellion on Saturday..and it seems that they are preparing for a coup attempt

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia/USA

The USA seems intent on annoying Russia as it prepares to sail a warship into the Black Sea, citing the Kerch Strait incident which was totally the fault of the Ukraine.

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

Oil crashes after the Saudis propose a smaller than expected production cut, honouring Trump

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Von Greyerz states that gold will rise as central banks run out of metal to lease…and debts cannot be repaid.

iii)Why we should buy gold

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)With Trump putting on huge tariffs with China, it seems that it did not help as the uSA recorded another huge trade deficit, the worst in a decade at 55.5 billion dollars. Exports well and imports rose.and the deficit with China rose to 43 billion dollars. Not only that but the trade deficit ex petroleum rose to a new record. Next month’s reading will be worse than this month as petroleum plummeted.

(courtesy zerohedge)

d)Yesterday we again received a phony ISM report that manufacturing was rising. However Markit reported on dismal findings. Today, identical results with the USA service sector( zerohedge)

a)The USA beige book confirms that the USA economy is slowing

( zerohedge)

b)Seems that the Fed does not believe our crooked friends over at Wells Fargo on the reform plan to limit illegal behaviour

c)the following commentary from Dave Kranzler is a must read. Here he correctly describes the dilemma facing the Fed and the USA. You will note that the trade deficits are rising instead of falling. This is because of Trump’s trade wars which has caused the dollar to rise and thus gold to fall. If Trump wants to win the trade wars he must let the dollar fall and fall big time and that will cause gold to rise.

( Dave Kranzler/IRD)

d)Seems like a well placed WSJ article to juice to stock market

( zerohedge)

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 787 contracts standing for a loss of 189 contracts. We had 245 contracts stand for delivery yesterday so we gained 56 contracts or an additional 280,000 oz will stand for delivery as these guys refused to morph into London based forwards as well as negating to accept a fiat bonus. We continue where we left off last month as queue jumping in silver is the norm for at least 20 months.

After December we have the non active January contract month and here we saw a gain of 4 contracts up to 1942 contracts. February saw its another 12 contract gain to stand at 47. March, the next big delivery month after December saw a loss of 1233 contracts down to 145,700

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

“Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– What are “Fake Markets” and will they lead to another global financial crisis?

– What do fake markets mean for stock and bond market performance in the future?

– Is this the right time to re-balance portfolios and hold more cash and gold?

Markets are fake today as they are “heavily manipulated by monetary authorities.”

“Fake markets” mean investors are all on the “same side of the boat and the boat can capsize.”

Listen to the full episode or skip directly to one of the following discussion points:

00:30 – Francesco Filia and Stephen Flood: can the performance of stock markets be trusted as a barometer for economic performance?

01:06 – Stay updated in all developments in precious metals by signing up for GoldCore’s market update on http://www.goldcore.com

01:27 – Meet Francesco Filia, CEO & CIO at Fasanara Capital.

02:28 – Francesco: Understanding fake markets and why you should be concerned.

03:10 – Fake markets today due to complete manipulation of markets by monetary authorities.

05:14 – Francesco: Understanding the difference between passive and active investments.

07:59 – Are ETFs a cause for concern?

10:10 – Swiss National Bank & Swiss equity market: A bubble waiting to burst?

11:40 – How strong is the argument for passive investments

12:19 – Greek Tier One Capital and the assumption of zero default risk: How sustainable is this?

14:08 – The definition of “Fake Markets.”

15:42 – Fake markets, systemic risk and investors: Identifying and avoiding the pitfalls.

17:40 – Are systemic risk indicators better than volatility based indicators?

19:50 – The Rate of Recovery: A good indicator of the temperament of the market?

22:10 – Is complexity theory a better way to understand markets?

24:09 – What can investors do to insulate themselves in Fake Markets?

25:48 – What can gold do to your portfolio in the event of a market correction?

28:03 – How can markets be fixed?

31:44 – Can central banks or official sector intervention fix the market?

32:54 – What can central banks do to protect the market and ensure systemic stability?

34:08 – Has the market bubble created more income inequality?

36:12 – Low rates: can bonds still save the day?

37:28 – Coming market transition: Any need for panic?

38:02 – Is this the right time to rebalance portfolios and hold more cash and gold?

Make sure you don’t miss a single episode… Subscribe to the Goldnomics Podcasts on iTunes, Soundcloud, Blubrry or YouTube

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

Gold inches higher as dollar dips amid risk aversion (CNBC.com)

Asian markets plunge, led by tech stocks, after Huawei exec’s arrest (MarketWatch.com)

May’s Brexit deal under fire as legal advice stiffens opposition (Reuters.com)

Gold prices end lower, a day after settling at their highest in over 4 months (MarketWatch.com)

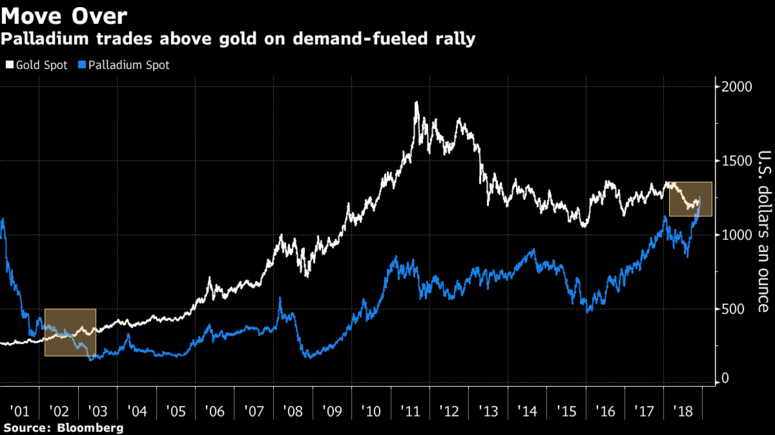

Gold Gets Leapfrogged as Palladium Extends Rally to New Record (Bloomberg.com)

Source: Bloomberg

Market reaction to the French riots goes a long way to explaining them (MoneyWeek.com)

Carnage Continues: US Futures Flash Crash After Huawei CFO Arrest (ZeroHedge.com)

Yield Curve Just Inverted for the First Time in Years. Time to Reconsider Risk? (GoldSeek.com)

Empty Words Are Failing. A Timeline For What Comes Next (DollarCollapse.com)

Story of a Gold Coin (Plata.com.mx)

Is Wall Street still too bullish on FAANG? Some say so (CNBC.com)

Gold Prices (LBMA PM)

05 Dec: USD 1,236.15, GBP 970.13 & EUR 1,090.16 per ounce

04 Dec: USD 1,239.25, GBP 966.74 & EUR 1,086.45 per ounce

03 Dec: USD 1,231.05, GBP 966.00 & EUR 1,084.92 per ounce

30 Nov: USD 1,220.45, GBP 956.95 & EUR 1,073.75 per ounce

29 Nov: USD 1,226.25, GBP 960.03 & EUR 1,077.87 per ounce

28 Nov: USD 1,213.20, GBP 949.69 & EUR 1,074.77 per ounce

Silver Prices (LBMA)

05 Dec: USD 14.48, GBP 11.34 & EUR 12.75 per ounce

04 Dec: USD 14.55, GBP 11.35 & EUR 12.77 per ounce

03 Dec: USD 14.39, GBP 11.31 & EUR 12.69 per ounce

30 Nov: USD 14.24, GBP 11.16 & EUR 12.52 per ounce

29 Nov: USD 14.26, GBP 11.17 & EUR 12.55 per ounce

28 Nov: USD 14.15, GBP 11.06 & EUR 12.54 per ounce

Recent Market Updates

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

– Risk of Lower Lows in Gold Remains Prior to Spectacular Rally to Follow

– Gold and Silver Hold Firm as Stocks and Oil Lower in to US Holiday Weekend

– Is Brexit a Massive Threat to Globalisation?

With inflation, central banks guarantee rising gold

price, von Greyerz tells’Keiser Report’

Submitted by cpowell on Thu, 2018-12-06 04:38. Section: Daily Dispatches

11:40p ET Wednesday, December 5, 2018

Dear Friend of GATA and Gold:

Interviewed last week by Max Keiser on Russia Today’s “The Keiser Report,” Swiss bullion dealer Egon von Greyerz said Western central banks will exhaust their gold reserves through leasing and other price-suppressing mechanisms as metal moves from West to East even as central banking generally will forever underwrite gold prices with inflation. With world debt now reaching four times the world’s annual productivity, von Greyerz said, that debt can never been repaid except through massive inflation.

So when will gold have its day? Von Greyerz predicts that it will come within the next five to seven years.

Keiser’s interview with von Greyerz is 13 minutes long and begins at the 12:45 mark at YouTube here:

https://www.youtube.com/watch?v=Q55xde1cUfo&feature=youtu.be&t=768

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Why Buy Gold Now? Because Of The “I Don’t Knows”…

Authored by Simon Black via SovereignMan.com,

From 2000 through 2012, the price of gold increased every year, rising from around $280 an ounce to nearly $1,700. It was an unprecedented run.

Then, in 2013, gold took a nose dive, losing over 27% of its value.

It was widely reported that the Swiss National Bank, the former bastion of monetary conservatism, lost $10 billion that year just on its gold holdings.

As you probably know, central banks hold a portion of their reserves in gold. The practice goes back to when central banks actually had to have gold on hand to trade in and out of paper money (or even trade for goods and services).

And central banks still hold reserves in gold today, even though they don’t need it to transact like they used to.

So that begs the question, did the Swiss National Bank actually lose $10 billion? It still had every ounce of gold in its vaults. And gold, after all, ismoney.

Plus, the SNB wasn’t holding gold to speculate…

Today, central banks hold gold as a hedge against fiat money. These are the guys with their fingers on the printing press… so they know exactly the effect they have on money.

And right now, banks are buying up gold hand over fist. Central banks currently hold 20% of all the gold ever mined—33,000 metric tons.

And JPMorgan Chase says they’ll buy another 650 tons this year and next.

Why?

Gold is for the I don’t knows.

And right now, there are a LOT of I don’t knows.

Markets have been going crazy over the past few months.

After a record bull run for stocks, we are now seeing massive volatility with the Dow regularly jumping 500+ points in a single day. Just yesterday, the Dow fell a whopping 800 points.

And there’s plenty of reasons for market to be worried today. For one, we’re 10 years in to a raging bull market… and it’ getting long in the tooth.

Plus, the Fed is raising interest rates. And when the price of money gets more expensive, people get a little tighter with it. That means it’s tougher for businesses and individuals to borrow. All things equal, higher rates mean lower prices.

Before last week, Fed Chairman Powell said rates were “well below” where they should be. And the markets reacted negatively.

Then, last week, after seeing how fragile markets were, Powell said rates are “just below” where they should be.

Just that one word difference sent markets soaring. But the joy was short lived.

There’s also the trade war with China, intensified by the Trump administration tariffs.

And then at the summit in Buenos Aries last week, China and the USA suddenly came to an agreement. They will halt the tariffs for 90 days for a three-month truce in the trade war. That sent markets soaring.

Then people read some tweet from Trump and worried the tariffs might be back on… markets dumped.

If there is one thing markets hate, it is uncertainty. And there’s plenty of uncertainty to go around today.

And while we’re seeing these late-cycle swings in the market, gold is as steady as ever…

While the DOW dips and climbs by hundreds of points, gold is still hanging out just below $1,250 an ounce. And it really hasn’t made any major moves up or down since 2013.

Yet today, an ounce of gold has about the same purchasing power as it had 1,100 years ago… talk about steady.

So while every other asset is still at or near all time highs, gold is relatively cheap.

Gold has held its ground during all this market volatility.

That is exactly how you want insurance to act. It holds steady in the face of craziness, even selling for a discount when everything else is as expensive as it ever has been.

It makes more sense to buy something cheap, that no one is excited about, while people clamber for exciting but massively overvalued stocks like Tesla and Netflix.

Since 2008 this massive monetary experiment of quantitative easing has sent stocks and assets to dizzying, unsustainable highs.

We think this experiment is coming to an end. The day of reckoning is close.

Stocks are up and down, trade wars are on and off, interest rates could keep soaring, or level off…

What do you do for the I don’t knows?

You get some cheap gold while you still can.

And by the way, while gold is on sale, silver is an even better deal.

In ancient times, the price ratio between gold and silver was about 15:1, meaning an ounce of gold was worth about 15 ounces of silver.

But over the past decades, this ratio has been closer to 50:1—an ounce of gold sold for 50 times what an ounce of silver sold for.

Today, that ratio is about 85:1.

To be fair, this could mean gold is overvalued, not that silver in undervalued.

But when gold has the same purchasing power as a millennium ago… when it has stayed steady the past seven years and grew every year of the decade before that…

It’s a safe bet that gold goes up, and silver does too, possibly even more than gold.

end

________________________________________

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8934/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8964 /shanghai bourse CLOSED DOWN 44.62 POINTS OR 1.68%

. HANG SANG CLOSED DOWN 663.30 POINTS OR 2.47%

2. Nikkei closed DOWN 417,71 POINTS OR 1.91%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 97.03/Euro FALLS TO 1.1347

3b Japan 10 year bond yield: FALLS TO. +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.80/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.53 and Brent: 60.11

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.25%/Italian 10 yr bond yield DOWN to 3.14% /SPAIN 10 YR BOND YIELD UP TO 1.45%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.89: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.22

3k Gold at $1236.35 silver at:14.37 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 44/100 in roubles/dollar) 66.95

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.80DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9965 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1309 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.25%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.89% early this morning. Thirty year rate at 3.15%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3716

Global Markets, Futures Plunge As Traders Brace For

China’s Response

It is a sea of red out there as traders brace for China’s response.

Shortly after S&P futures flash crashed at the start of the overnight session, with the CME triggering multiple Velocity Logic events causing 10-sec pauses to slow down trading…

… after US markets were shut to commemorate the death of George H.W. Bush on Wednesday, global stock markets tumbled for a third day on Thursday as the arrest of the CFO of Chinese telecom giant Huawei in Canada for extradition to the United States prompted fears of fresh tensions between the two economic superpowers, and sparked dread as to how China would respond.

S&P futures by as much as 1.9% during the Asian session in a sudden and unexpected move that sent world equity markets reeling, and was trading near session lows, just above 2,650 this morning.

That was just the start of it, and in the latest US-China trade war linked shockwave to slam global markets, these were some of the stand out moves:

- Dow Jones futures were off more than 450 points; Nasdaq futs fell 2.4 percent as Apple suppliers plunged amid renewed production cuts

- Europe’s Stoxx 600 tumbled 2.2% to the lowest in almost two years

- Germany’s DAX tumbled below 11,000 for the first time in two years

- WTI crashed below $51 after Saudi Energy Minister Khalid Al-Falih said OPEC hasn’t yet reached a deal on production cuts

- Deutsche Bank plunged to a new record low, dropping as low as €7.71

- The yuan dropped the most since October.

- Treasuries jumped again, sending the 10Y yield to 2.89%

- The Bloomberg dollar index spiked amid safe-haven flows, rising just shy of 2018 highs.

- The MSCI Asia Pacific Index posted its worst day in six weeks

- China’s 2nd largest telecom equipment maker ZTE Corp crashed 9% in Hong Kong

News of the arrest of Huawei’s CFO Meng Wanzhou, the daughter of the firm’s founder, who was detained by Canadian police on the same day Trump and Xi held their dinner in Buenos Aires, triggered renewed fireworks coming just as Washington and Beijing prepare for crucial trade negotiations and threatened to reignite U.S.-China tensions. The yuan dropped the most since October.

Asian markets took a beating. Huawei is not listed but China’s second-largest telecom equipment maker ZTE Corp sank 9% in Hong Kong while most of the nearby national bourses lost at least 2 percent. Japan’s Nikkei shed 1.9%, closing at its lowest level since Oct. 30, with semi-conductor related shares leading the losses. MSCI’s ex-Japan Asia-Pacific index lost 2.0%; Hong Kong’s Hang Seng dropped 2.5% while Chinese bluechips lost 2.1% to take their 2018 slump to 20%.

Europe slumped too in early trading as 3 percent falls for the tech sector, miners and also carmakers kicked London, Frankfurt and Paris to two-year lows.

Needless to say, early market commentary was dire:

- “We had this very ugly new turn and just the degree to which the market has reacted just suggests to me that they are vulnerable right now,” said Saxo Bank’s head of FX strategy John Hardy. “It think we should all be very careful, it is not looking good, especially if the S&P 500 goes to new lows.”

- “There are so many forces weighing against markets right now, whether it’s the China slowdown, weak European data, Fed hikes, uncertainty around trade and now Brexit as well,” Bilal Hafeez, head of fixed-income research for EMEA at Nomura, told Bloomberg TV. “We really need to see some stabilization in any of those factors to see markets stabilize now.”

- “This move against the Huawei CFO has just added another spanner in the works,” Eleanor Creagh, strategist at Saxo Capital Markets, told Bloomberg TV in Sydney. “It’s really illustrative of the fact that the trade truce we saw over the weekend between Trump and Xi doesn’t really do much to mend the underlying relationship between the U.S. and China that is still deteriorating.”

And while Hardy said that President Trump may try to send some reassuring tweets later, for now traders are not taking any chances with S&P 500 futures near session lows, down almost 2 percent, and over 5% in the past two trading days after Tuesday’s 3.2% plunge. The losses would have been even steeper had CME Group’s Chicago Mercantile Exchange not implemented a series of 10-second trading halts in Asia that had limited the initial drop.

Not helping sentiment, overnight BOJ Governor Haruhiko Kuroda said economic risks from abroad could be severe, and the Federal Reserve’s Beige Book report showed fading optimism over growth prospects at U.S. firms citing growing instances of economic “slowdown”.

The plunge persisted even though a Chinese government spokesman said that China and the U.S. have reached agreement in the sectors of agriculture, autos, and energy, and China will immediately start implementing that consensus. Still, there’s no official, confirmed statement of what China agreed as part of the deal.

“China will start from agricultural products, autos and energy to immediately implement specific items that China and the U.S. have agreed upon,” Ministry of Commerce Spokesman Gao Feng told reporters in Beijing. “In the next 90 days we will work in accordance with the clear timetable and road map to negotiate in areas where both sides have an interest and there are mutual benefits, such as intellectual property rights protection, technology cooperation, market access, and the trade balance.”

That reassurance however faded in light of the shocking arrest, and the yuan eased 0.3% to 6.8835 per dollar in offshore trade. China’s foreign ministry said neither Canada and the United States had clarified their reason for the move but a source had earlier told Reuters it was related to violations of U.S. sanctions on Iran.

The arrest again heightened the sense of a major collision between the world’s two largest economic powers not just over tariffs but also over technological hegemony. Britain’s BT Group said it was removing Huawei’s equipment from the core of its existing 3G and 4G mobile operations. Australia and New Zealand have also rejected Huawei’s products.

“The U.S. has been telling its allies not to use Huawei products for security reasons and is likely to continue to put pressure on its allies,” said Norihiro Fujito, chief investment strategist at Mitsubishi UFJ Morgan Stanley Securities. “So while there was a brief moment of optimism after the weekend U.S.-China talks but the reality is, it won’t be that easy.”

Meanwhile, half way around the word, traders were also on pins and needles waiting to hear from the OPEC+ meeting in Vienna about what kind of cuts OPEC and other oil producers like Russia could make to their output. And in the latest price shock, WTI plunged almost 5% just above $50 a barrel as Saudi Arabia’s energy minister said going into the day long meeting that 1 million “would be enough”; with consensus among analysts for somewhere between 1-1.3 million barrels per day, this led to a quick waterfall in oil prices.

At the same time, and adding to worries about U.S. recession risks, the Treasury yield curve remained inverted between two- and five-year zones; the 10Y yield dropped as low as 2.87% overnight – a 3 month low – amid a flood to safety. Yields on German 10Y bunds held near six-month lows in risk off environment.

The Bloomberg Dollar Spot Index headed for a third day of gains as part of the global flight to safety. The yen led gains in G-10 as havens were supported. Elsewhere in FX, the euro barely budged at $1.1338 and the Canadian dollar languished near the 18-month low it had hit the previous day after cautious noises from the Bank of Canada. The pound drifted as U.K. Prime Minister Theresa May searched for a compromise to avoid a crushing defeat on her Brexit deal in a key vote in Parliament next week.

In the latest Brexit news, UK PM May was being pushed by cabinet members to postpone next week’s Parliament vote on Brexit amid worries she is facing a loss so disastrous it could collapse the government. Instead, cabinet members believe that the PM should devote more time to selling the deal. Furthermore, reports have suggested that PM May has sent her Chief Whip to try find a way forward with the ERG by offering a potential Parliamentary ‘lock’ which would require lawmakers to give their consent before some of the more controversial parts of the UK’s exit from the EU came into effect.

U.S. jobs data is due on Friday. If the figures show any sign of serious weakness, markets are likely to react HSBC’s head of macro economic strategy, Shuji Shirota, said.

Expected data include trade balance and factory orders. Kroger, Broadcom, and Lululemon are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 1.7% to 2656.25

- STOXX Europe 600 down 1.8% to 347.85

- MXAP down 1.8% to 150.77

- MXAPJ down 2% to 485.10

- Nikkei down 1.9% to 21,501.62

- Topix down 1.8% to 1,610.60

- Hang Seng Index down 2.5% to 26,156.38

- Shanghai Composite down 1.7% to 2,605.18

- Sensex down 1.4% to 35,366.35

- Australia S&P/ASX 200 down 0.2% to 5,657.65

- Kospi down 1.6% to 2,068.69

- German 10Y yield fell 1.9 bps to 0.258%

- Euro unchanged at $1.1344

- Italian 10Y yield fell 9.4 bps to 2.696%

- Spanish 10Y yield fell 0.8 bps to 1.451%

- Brent futures down 4% to $59.07/bbl

- Gold spot little changed at $1,236.64

- U.S. Dollar Index little changed at 97.12

Top Overnight Headlines

- Huawei Technologies CFO was arrested in Canada over potential violations of U.S. sanctions on Iran, provoking outrage from China and complicating thorny trade negotiations just as they enter a critical juncture

- Saudi Arabia proposed a moderate oil- production cut from OPEC and its allies that would gently rebalance the market, seeking to walk a fine line between preventing a surplus and appeasing U.S. President Donald Trump

- German factory orders unexpectedly rose for a third month, underpinning growth momentum after Europe’s largest economy contracted in the third quarter

- The EU’s highest court will say next week whether the U.K. should be allowed to reverse Brexit, in a landmark ruling that could offer hope to those who want the country to stay in the bloc

- President Donald Trump has used tariffs as one of his most powerful tools for fighting his trade wars, but he’s also wielding leverage with another weapon: uncertainty

- Federal Reserve Chairman Jerome Powell wants to avoid being tagged as the fool in the shower. And that’s why he’s likely to be especially cautious about marching interest rates higher in 2019

Asian stocks were lower across the board for a 3rd consecutive day with sentiment dampened after the US market closure and reports that Canada arrested Huawei’s CFO at the request of US authorities for alleged violations of sanctions against Iran. This prompted demands by China’s Embassy for an immediate release of the executive and led to concerns of the potential ramifications to trade discussions which weighed heavily on US equity futures. As such, Emini S&P declined by over 60 points and DJIA futures were down by more than 500 points shortly after the reopen which forced the CME to intervene to prevent a harder drop, while ASX 200 (-0.2%) and Nikkei 225 (-1.9%) were also weaker with the latter pressured by detrimental currency flows. Hang Seng (-2.5%) and Shanghai Comp. (-1.6%) conformed to the negativity with the Hong Kong benchmark underperforming amid losses across all its components and as local money markets rates edged higher again, while the PBoC announcement of a 1-yr Medium-term Lending Facility failed to support China with the operation at a reduced amount of CNY 187.5bln vs. Prev. CNY 403.5bln. Finally, 10yr JGBs were higher amid a continuation of the declines across yields and with safe-haven demand also underpinned by the weakness across equities.

Top Asian News

- SoftBank Is Said to Place All Shares for $23 Billion IPO

- Takeda Downgrade Looms After Shareholders Approve Shire Deal

- China’s Drugmakers Plunge Most Since 2009 on Price Concerns

- Anta-Led Consortium Is Said to Near Deal to Acquire Amer Sports

European equities (Eurostoxx -2.0%) have taken the lead from US futures and Asia-Pac trade overnight with US-Chinese trade concerns reignited by news that Canada arrested Huawei’s CFO at the request of US authorities for alleged violations of sanctions against Iran. This prompted demands by China’s Embassy for an immediate release of the executive, which subsequently weighed heavily on US equity futures. Despite commentary from China ahead of the open stating that their ultimate goal in US-China negotiations is to remove all tariffs, overnight developments have weighed heavily on sentiment in Europe thus far. The follow-through of events overnight has placed weight on IT names with STMicroelectronics (a supplier to Huawei) lower by -4.8% with losses also observed in Dialog Semiconductor (-2.6%) and Infineon (-3.3%) among others . Elsewhere, energy names underperform amid initial comments from the OPEC ministers in Vienna, signalling a potential cut in the low end of the expected range. In turn, European Oil and Gas Index fell 3.4% in-fitting with price action in the oil complex (BP -4.3%, Total -2.5%).

Top European News

- Italy’s Salvini Says He Opposes New Taxes for Auto Sector: Ansa

- Populists Split as Conte Seeks Deficit Trim for Juncker Meeting

- German Orders Rise for Third Month, Underpinning Recovery Hopes

- VW Brand Speeds Up Profit Target Ahead of Electric-Car Push

In FX, JPY/USD/CHF – All beneficiaries of safe-haven positioning/demand, as the global stock rout continues and intensifies, but to varying degrees with Usd/Jpy retreating below 113.00 while Usd/Chf holds near parity and the DXY remains around 97.000 amidst heavy losses in certain G10 counterparts. However, some hefty and layered option expiries in Usd/Jpy could keep that pair in check, with 1.6 bn rolling off between 112.75-80 and a similar amount sitting at 112.95-113.00, ahead of more 1+ bn maturities above the figure up to 113.75.

- AUD/CAD/NZD – The non-US Dollars have extended declines vs the Greenback and underperformance against other majors, as bearish independent impulses exacerbate the negative impact of broader risk aversion. Aud/Usd is now testing 0.7200 bids and psychological support following dovish commentary from RBA’s Debelle in wake of this week’s disappointing GDP data, with rate cuts back on the agenda if the economy slows further and the baseline scenario of the next policy move being a hike does not pan out. By the same token, and with the added pressure of collapsing crude prices amidst talk of no more than 1 mn output cuts from OPEC+, the Loonie has continued its post-BoC plunge to circa 1.3440, while the Kiwi has slipped below 0.6900 towards 0.6850, but is deriving underlying support from the greater demise in the Aud again, as the cross retreats through 1.0500 and to a fresh ytd low around 1.0480.

- GBP/EUR – The Pound and single currency are both holding up reasonably well given the increasingly risk-off environment, not to mention ongoing Brexit and Italian budget tension, as Cable maintains 1.2700+ status and Eur/Usd stays above 1.1300. Note, mega option expiries in close proximity from 1.1295-1.1300, 113.50-60 to 1.1380 (1.65 bn, 1.7 bn and circa 1.4 bn respectively).

In commodities, Brent (-4.3%) and WTI (-4.2%) have continued to drift lower as the 175th OPEC meeting begins, with initial remarks from OPEC delegates suggesting that OPEC+ could only cut 1mln BPD if Russia agrees to cut 150k BPD, adding they would be willing to cut over 1.3mln BPD if Russia cuts 250k BPD. Sources thereafter went on to state that any cut is unlikely to be over 1.4mln BPD. Russia’s role in the agreement continues to remain a source of speculation with prices hampered by comments from the Russian Energy Minister Novak suggesting that it is difficult for Russia to cut output quickly in Winter. WTI and Brent crude futures were then dragged lower once again after the Saudi Energy Minister Al-Falih says there is no agreement yet to cut but all options are on the table, including a no deal. Al-Falih then added that a 1mln BPD cut will be enough for OPEC+, a comment which appeared to add to the downside in energy markets with the level touted not well received by the market, particularly after he then went on to state that the KSA are content with the current oil price. Furthermore, questions also remain over who might not participate in any output cut with NOC’s Sanallah contradicting comments from the Oman oil minister overnight after stating that Libya is hoping for an exemption from the OPEC cuts. Additionally, Iran continues to hold a tough stance in negotiations by stating that they will not be a part of any deal to reduce output until sanctions are removed. Note, this week’s DoE report will be released today due to yesterday’s market closure. Gold is trading flat within a tight USD 5/oz range, with spot palladium trading at a premium to gold for the first time in 16 years; as prices hit record levels of USD 1246.50 in the previous session. Separately, China has reportedly asked steel mills in the province of Tangshan to being implementing winter curbs due to a reduction in air quality.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 153.6%

- 8:15am: ADP Employment Change, est. 195,000, prior 227,000

- 8:30am: Trade Balance, est. $55.0b deficit, prior $54.0b deficit

- 8:30am: Nonfarm Productivity, est. 2.3%, prior 2.2%; Unit Labor Costs, est. 1.0%, prior 1.2%

- 8:30am: Initial Jobless Claims, est. 225,000, prior 234,000; Continuing Claims, est. 1.69m, prior 1.71m

- 9:45am: Bloomberg Consumer Comfort, prior 60.6

- 9:45am: Markit US Services PMI, est. 54.4, prior 54.4; Markit US Composite PMI, prior 54.4

- 10am: ISM Non-Manufacturing Index, est. 59, prior 60.3

- 10am: Factory Orders, est. -2.0%, prior 0.7%; Factory Orders Ex Trans, prior 0.4%

- 10am: Durable Goods Orders, est. -2.38%, prior -4.4%; Durables Ex Transportation, est. 0.1%, prior 0.1%

- 10am: Cap Goods Orders Nondef Ex Air, prior 0.0%; Cap Goods Ship Nondef Ex Air, prior 0.3%

- 12pm: Household Change in Net Worth, prior $2.19t

- 12:15pm: Fed’s Bostic Speaks on the U.S. Economic Outlook

- 6:30pm: Fed’s Williams Holds Discussion With Mervyn King in NY

- 6:45pm: Powell Gives Brief Welcome Remarks at Housing Conference

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 44.62 POINTS OR 1.68% //Hang Sang CLOSED DOWN 663.30 POINTS OR 2.47% //The Nikkei closed DOWN 417.71 OR 1.91%/ Australia’s all ordinaires CLOSED DOWN 0.22% /Chinese yuan (ONSHORE) closed DOWN at 6.8934 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51/53 dollars per barrel for WTI and 60.11 for Brent. Stocks inEurope OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8934AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8965: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

It sure looks like the truce is over!! On behalf of the USA Canada arrests the CFO of Huawei and the daughter of the founder Ren Zhengfei. I am sure that Xi is not thrilled with this. The charge: the firm sold goods to Iran despite sanctions.

(courtesy zerohedge)

Trade Truce Over? Canada Arrests Huawei CFO At US Request

Mere hours after Chinese officials finally affirmed President Trump’s description of Saturday’s trade ‘truce’ – this after fears that the true nature of the agreement might have been “lost in translation” helped trigger the worst one-day market selloff since October – the DOJ has gone ahead and kicked the hornet’s nest, seriously jeopardizing the prospects for a prolonged trade detente between the world’s two biggest economies.

Canada’s Globe and Mail reported late on Wednesday that on December 1 – on the same day as the Trump-Xi dinner – Canadian authorities arrested Wanzhou Meng, the CFO of Huawei Technologies and daughter of the telecom giant’s founder, Ren Zhengfei. An ex-officer with the People’s Liberation Army, Ren is one of the country’s most revered business figures.

“Wanzhou Meng was arrested in Vancouver on December 1. She is sought for extradition by the United States, and a bail hearing has been set for Friday,” Justice department Ian McLeod said in a statement to The Globe and Mail. “As there is a publication ban in effect, we cannot provide any further detail at this time. The ban was sought by Ms. Meng.

Meng is said to be a “rising star” at Shenzhen-based Huawei, the world’s second-largest maker of telecommunications equipment. Reuters reported in 2013 that Ms. Meng served on the board of a Hong Kong-based Skycom Tech that later attempted to sell embargoed Hewitt Packard computer equipment to Iran’s largest mobile-phone operator. At least 13 pages of the Skycom proposal were marked “Huawei confidential” and carried Huawei’s logo. Huawei has said neither it nor Skycom ultimately provided the HP equipment. HP said it prohibits the sale of its products to Iran.

The CFO is now facing extradition to the US on suspicions that she violated US sanctions against Iran(allegations that nearly resulted in a devastating Treasury “death sentence” earlier this year for Huawei rival ZTE).

Prosecutors in New York have been investigating suspicions that Huawei violated US sanctions against Iran since earlier this year. News of the probe was first reported in April. The G&M adds that the probe is being run out of the U.S. attorney’s office in Brooklyn.

We seriously doubt the Chinese leaders will interpret Wanzhou’s arrest as a gesture of good faith and trust at a time when negotiations over a possible trade truce were expected to finally begin in earnest after a months-long standoff.

To understand the magnitude of this arrest, just imagine how the US would react if Beijing arrested Jeff Bezos’ (hypothetical) daughter?

As investors digest the implications of the DOJ’s investigation, expect a kneejerk response where investors shoot first Thursday and dump shares of big Huawei suppliers, as they did with ZTE. Should they do the same with broader S&P futures amid concerns that the trade truce is back to square one zero, Trump will have a choice: releasing Meng or watching the any last hopes of Christmas rally fade into the distance.

end

Wednesday evening trading due to the above event; Dow futures crash over 500 points

(courtesy zerohedge)

Carnage Continues: US Futures Crash At Re-Open After Huawei CFO Arrest

Having taken a day off to watch Bush’s funeral – drifting modestly higher before the early close – reports of the arrest of Huawei’s CFO at the request of US authorities has sparked carnage at the re-open.

As we detailed earlier, mere hours after Chinese officials finally affirmed President Trump’s description of Saturday’s trade ‘truce’ – this after fears that the true nature of the agreement might have been “lost in translation” helped trigger the worst one-day market selloff since October – the DOJ has gone ahead and kicked the hornet’s nest, seriously jeopardizing the prospects for a prolonged trade detente between the world’s two biggest economies.

Dow futures were down over 500 points as they opened…

The selling is across all the major US index futures…

For now there is no reaction in Yuan or Treasuries.

For now it appears that the trade truce is back to square one zero, leaving Trump with a choice: releasing Meng or watching the any last hopes of Christmas rally fade into the distance.

end

The USA attack on Huawei intensifies with the arrest of its CFO. You will recall that the USA outlawed all purchases of Huawei by the military as their were rumours of that Chinese have a backdoor entry into their products. That caused a storm of protests from China as this has not been proven. Now they arrested the founders daughter ( its CFO) and China has announced it will take appropriate measures

(courtesy zerohedge)

China Outraged At Arrest Of Huawei CFO, Warns It Will “Take All Measures”

So much for a trade war truce between China and the US, or a stock market Christmas rally for that matter.

Shortly after the news hit that Huawei CFO Wanzhou Meng — also deputy chairwoman and the daughter of Huawei’s founder — was arrested on December 1, or right around the time Trump and Xi were having dinner in Buenos Aires last Saturday, and faces extradition to the U.S. as a result of a DOJ investigation into whether the Chinese telecom giant sold gear to Iran despite sanctions on exports to the region, China immediately lodged a formal protest publishing a statement at its embassy in Canada, and demanding the U.S. and its neighbor “rectify wrongdoings” and free Meng, warning it would “closely follow the development of the issue” and will “take all measures” to protect the legitimate rights and interests of Chinese citizens.

Full statement below:

Remarks of the Spokesperson of the Chinese Embassy in Canada on the issue of a Chinese citizen arrested by the Canadian side

At the request of the US side, the Canadian side arrested a Chinese citizen not violating any American or Canadian law. The Chinese side firmly opposes and strongly protests over such kind of actions which seriously harmed the human rights of the victim. The Chinese side has lodged stern representations with the US and Canadian side, and urged them to immediately correct the wrongdoing and restore the personal freedom of Ms. Meng Wanzhou.

We will closely follow the development of the issue and take all measures to resolutely protect the legitimate rights and interests of Chinese citizens.

Meng’s arrest will immediately heighten tensions between Washington and Beijing just days after the world’s two largest economies agreed on a truce in their growing trade conflict. It will, or at least should, also prompt any US execs currently in China to think long and hard if that’s where they want to be, say, tomorrow when Xi decides to retaliate in kind.

Meng’s father Ren Zhengfei, a former army engineer who’s regularly named among China’s top business executives, has won acclaim at home for turning an electronics reseller into the world’s second-largest smartphone maker and a major producer of networking gear.

As Bloomberg notes, the CFO’s arrest will be regarded back home as an attack on China’s foremost corporate champions. While Alibaba and Tencent dominate headlines thanks to flashy growth and high-profile billionaire founders, Ren’s company is by far China’s most global technology company, with operations spanning Africa, Europe and Asia.

“Tencent and Alibaba may be domestic champions and huge platforms in of their own rights, but Huawei has become a global powerhouse,” said Neil Campling, an analyst at Mirabaud Securities Ltd. It is “5G standards that are at the heart of the wider IP debate and why the U.S. and her allies are now doing everything they can to cut to the heart of the Chinese technology IP revolution.”

At the same time, Huawei’s technological ambitions have also gotten the company in hot water with the US: its massive push into future mobile communications has raised hackles in the U.S. and become a focal point for American attempts to contain China’s ascendance.

Going back to the arrest, the U.S. Justice Department declined to comment about the circumstances involving the CFO, although the biggest question on everyone’s mind right now is whether Trump was aware of the pending arrest at the time of his dinner with the Chinese president, and why exactly he had greenlighted the move which would certainly result in another diplomatic scandal, promptly crushing and goodwill that was generated at the G-20 dinner.

Meanwhile, in a statement, Huawei said the arrest was made on behalf of the U.S. so Meng could be extradited to “face unspecified charges” in the Eastern District of New York.

“The company has been provided very little information regarding the charges and is not aware of any wrongdoing by Ms. Meng,” Huawei said. “The company believes the Canadian and U.S. legal systems will ultimately reach a just conclusion. Huawei complies with all applicable laws and regulations where it operates, including applicable export control and sanction laws and regulations of the UN, U.S. and EU.”

Tensions between the Chinese telecom giant and U.S. authorities escalated in 2016, when the US voiced concerns for the first time that Huawei and others could install back doors in their equipment that would let them monitor users in the U.S. Huawei has denied those allegations. The Pentagon stopped offering Huawei’s devices on U.S. military bases citing security concerns. Best Buy Co., one of the largest electronics retailers in the U.S., also recently stopped selling Huawei products.

In August, U.S. President Donald Trump signed a bill banning the government’s use of Huawei technology based on the security concerns. The same month, Australia banned the use of Huawei’s equipment for new faster 5G wireless networks in the country and New Zealand last week did the same, citing national security concerns. Similar moves are under consideration in the U.K. The U.S., which believes Huawei’s equipment can be used for spying, is contacting key allies including Germany, Italy and Japan, to get them to persuade companies in their countries to avoid using equipment from Huawei, the Wall Street Journal reported last week.

In 2016, the Commerce Department sought information regarding whether Huawei was possibly sending U.S. technology to Syria and North Korea as well as Iran.

The U.S. previously banned ZTE Corp., a Huawei competitor, for violating a sanctions settlement over transactions with Iran and North Korea.

The cynics out there may claim that the US response is merely in place to delay the development of the company which in the third quarter overtook Apple as the No. 2 global smartphone maker, shipping more than 52.2 million units according to Gartner Inc.

“This is what you call playing hard ball,” said Michael Every, head of Asia financial markets research at Rabobank in Hong Kong. “China is already asking for her release, as can be expected, but if the charges are serious, don’t expect the US to blink.”

The biggest question is what will China do next. One look at futures, which flash crashed earlier when the news of the CFO’s arrest first hit, suggests that whatever it is, Beijing will probably not be happy.

END

Deutsche bank announces that the arrest is a clear signal that the trade war is escalating to a new level.

( zerohedge)

Deutsche Bank: “This Is A Clear Signal That The Trade War Is Escalating To A New Level”

As if traders did not have enough reasons to be worried, here is Deutsche Bank’s Chief China Economist Zhiwei Zhang, who writes that the arrest of Huawei’s CFO on Dec 1 due to an US extradition request over Iran sanctions “is a clear signal that the trade war is escalating to a new level. We think the probability of US and China reaching a trade deal by Mar 1 has dropped to 30% from 40%. US business interests in China face higher risk than before.”

Some more details:

Huawei has been widely recognized as one of the most successful technology companies in China. This news pushed policy makers in Beijing into an awkward position. Public opinion in China will likely become more negative in respect to the trade war, and potentially against US companies. The government may find it difficult to tell the public that they have offered significant concessions to the US. The trade talk has just been resumed at the G20 meeting; now its outlook has darkened.

As we highlighted on Nov 20 , technology has become the focus of bilateral economic tension. The US government already proposed imposition of export controls on “emerging technologies”. This Huawei event suggests indeed technology has become the new battleground.

With futures in freefall this morning, the market clearly agrees.

END

Bill Blain explains why the arrest is a big deal as the USA tries to limit Chinese growth in the technology field.

This global trade war in his words will become a shooting war…

(courtesy Bill Blain)

Blain: “I Think The Global Trade War Is Now A Shooting War”

Blain’s Morning Porridge submitted by Bill Blain

“Why So Serious?”

I think the Global Trade War is now a shooting war.

A few weeks ago one of my very smart CIO contacts warned me the real story of the year isn’t just the implications for supply chains from a Trade Spat, but a more fundamental “Tech Cold War” between China and the US for dominance. It’s a battle that will shortly reach epic proportions, force huge change in the global tech supply chain, and has massive implications for current incumbents.

Over this last few days, its all going off. The US, Australia, NZ and the UK have banned Huawei from new 5G systems over embedded spy tech and “security” issues. Now we learn that even as Xi and Trump were meeting, the CFO of Huawei was arrested in Canada for violating US sanctions on Iran! She is also the daughter of Hauwei’s founder.

I suspect the news will trigger a massive downtrade in stocks today. Brace, Brace, Brace!

The core objective of Trump’s trade war threats are to contain China’s becoming a technological equal and competitor after all its learnt from access and replication of US tech. If we see a full Tech War with lines drawn, then its potentially clobbers everything from Apple down. It means a choice between US Tech or China Tech.

“Made in China 2025” is the Chinese target of becoming the leader in tech, and avoiding just being a US manufacturing centre. Its happening – Hauwei’s lead in 5G is just one example.

More on this next week – but its going to be a massive story. Blade Runner anyone?

* * *

Meanwhile, story on BBerg y’day says it’s the worst market since 1972. Did you know 1972 was the longest year ever? 2 leap seconds were added (one in June and one in Dec), making it 366 days and 2 seconds long.

I don’t particularly remember 1972.. swimmer David Wilkie came to our school to show off his Olympic silver medal, I had a double digit birthday, Werner Von Braun resigned from NASA, the Vietnam war rumbled on and Britain went to war with Iceland over cod. But I don’t remember the markets so clearly.

Last year nearly every major asset class posted decent gains. This year everything looks pants. Just like 1972! This year not a single major asset class has posted returns in excess of 5%. Treasuries and Investment grade bonds, Hi-yield, US, International or Emerging Stocks, real estate and commodities have all had awful years.. So much for retiring…

Of course, at this point someone will Samba onto the stage singing that Brazil stocks are up 17% in 2018! (A new populist president has had a positive effect..)

Or you could make the comment that over 2 years – 1 year is such an arbitrary number – even US stocks are currently up 10%. Why the long faces..? Over the last 9 years and 240 days… the S&P is up 294%! Wowser. Best not to forget the lessons of 2018. (Quick… what are they?)

The one area that interests me particularly is Residential – it’s the largest asset class on the planet – around $300 trillion, but it’s very granular – lots of tiny lots owned by individuals. Its also the closest in terms of relation to global GDP. Lets assume we get past these little hiccups in Brexit, trade wars, and a possible recession next year, and go back to the simple reality Resi is a rather effective way to track and beat growth.. Might be worth thinking about – while lots of funds are looking to exit “Resi” trades – might be time to go contrarian!

end

A defiant Huawei states that it will not change ties with suppliers due to USA pressure and it knows no reason for the arrest of its CFO. The company states it is obeys all USA rules on not supplying sanctioned state actors

(courtesy zerohedge)

A Defiant Huawei Says It Won’t Change Ties With Suppliers Due To US Pressure

A defiant Huawei Technologies sent a letter on Thursday night to its global supply-chain partners, which was seen by Sina, according to which it won’t change ties with its suppliers, and adding that it has “very little” information regarding U.S. accusations against its CFO Meng Wanzhou, and has “no knowledge of any improper behavior on the CFO’s part.”

The company added that it believes the Canadian, U.S., judicial systems will come to fair conclusions to the case; and that Huawei will update its partners if it has further information

But most notably, Huawei said the American “use of all sorts of means to pressure business goes against fair competition” adding that won’t change its cooperation with global supply-chain partners because of the U.S. actions.

Meanwhile, everyone’s attention remains glued to Trump’s twitter feed who in addition to not tweeting about the market for quite a while, has yet to opine on the Huawei scandal du jour.

end

I do not think that the markets will like this: as Bolton was sitting down for dinner with Xi, he was aware of the Huawei’s arrest. he is not sure if Trump new..

(courtesy zerohedge)

Bolton Was Aware Huawei CFO Was Arrested While Having Dinner With Xi

The market isn’t going to like this…

During an interview with NPR’s Morning Edition, National Security Advisor John Bolton revealed that he knew in advance that Canadian police were preparing to arrest Huawei CFO Wanzhou Meng, meaning that Bolton knew that Meng was being taken into custody when he sat down alongside President Trump for Saturday’s dinner trade talks with Chinese President Xi Jinping.