GOLD: $1241.95 DOWN $4.85 (COMEX TO COMEX CLOSINGS)

Silver: $14.53 UP 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1243.00

silver: $14.56

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 662 NOTICE(S) FOR 66200 OZ (2.059 tonnes)

Total number of notices filed so far for DEC: 6742 for 674200 OZ (20.9704 TONNES)

SILVER

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

Total number of notices filed so far this month: 341921 for 17,105,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3371: DOWN 60

Bitcoin: FINAL EVENING TRADE: $3409 DOWN 28

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A GOOD SIZED 3009 CONTRACTS FROM 179,473 DOWN TO 178,609 WITH YESTERDAY’S 8 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 20 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1446 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1446 CONTRACTS. WITH THE TRANSFER OF 1446 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1446 EFP CONTRACTS TRANSLATES INTO 7.23 MILLION OZ ACCOMPANYING:

1.THE 8 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 19.465 INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 10,690 CONTRACTS (FOR 7 TRADING DAYS TOTAL 10,690 CONTRACTS) OR 53.45 MILLION OZ: (AVERAGE PER DAY: 1527 CONTRACTS OR 7.63 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 53.45 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.63% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,730.48 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2864 WITH THE 8 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY.. AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1446 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A STRONG SIZED: 1418 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1446 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3009 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 8 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.52 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .898 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 19.465 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3952 CONTRACTS DOWN TO 403,733 WITH THE FALL IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $3.05//.YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8044 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 8044 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 403,733. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4092 CONTRACTS: 3932 OI CONTRACTS DECREASED AT THE COMEX AND 8044 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4092 CONTRACTS OR 409,200 OZ = 13.92 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.05

YESTERDAY, WE HAD 7908 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 55,254 CONTRACTS OR 5,525,400 OZ OR 171.86 TONNES (7 TRADING DAYS AND THUS AVERAGING: 7893 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 171.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 171.86/2550 x 100% TONNES = 6.73% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,936.24 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3952 WITH THE LOSS IN PRICING ($3.05) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8044 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8044 EFP CONTRACTS ISSUED, WE HAD AN GOOD GAIN OF 4092 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8044 CONTRACTS MOVE TO LONDON AND 3952 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 12.73 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE FALL OF $3.05 IN YESTERDAY’S TRADING AT THE COMEX

we had: 662 notice(s) filed upon for 66,200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.85 TODAY

A SMALL CHANGE IN GOLD INVENTORY:

A DEPOSIT OF .59 TONNES INTO THE GLD INVENTORY

/GLD INVENTORY 759.73 TONNES

Inventory rests tonight: 759.73 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 318.735 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A GOOD SIZED 3009 CONTRACTS from 179,473 DOWN TO 176,464 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1446 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1446 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3009 CONTRACTS TO THE 1446 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE LOSS OF 1563 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 7.815 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 19.465 MILLION OZ STANDING IN DECEMBER.

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 8 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1446 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 9.51 POINTS OR 0.37% //Hang Sang CLOSED UP 19.29 POINTS OR 0.07% //The Nikkei closed DOWN 71.48 OR 0.34%/ Australia’s all ordinaires CLOSED UP 0.42% /Chinese yuan (ONSHORE) closed UP at 6.8985 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.57 dollars per barrel for WTI and 60.45 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.8985AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8968: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)The stock market reacts to China’s move to cut auto tariffs. Due to the extreme lower wages in China, a cut in tariffs for American cars will have no effect on Chinese purchases of cars.

( zerohedge)

ii)Zero hedge correctly labels the real war is intellectual property and China’s aid to be the leader in the next generation of products.

( zerohedge)

iii)Not good: China arrests a former Canadian diplomat as we fear China is in reprisal form due to Meng’s arrest

(zerohedge)

iv)The war between China and the USA escalated again with Trump condemning China over hacking and economic espionage

( zerohedge)

v)China, Japan/Softbank

4/EUROPEAN AFFAIRS

i)UK

The chaos inside the UK due to the Brexit problems…

( zerohedge)

ii)Europe insists that the Brexit deal will not be renegotiated as Theresa May hopes to “run out the clock”

( zerohedge)

ii b)It is such a mess in Britain that many traders are refusing to trade the pound any more

ic)The pound falls to an 18 month low on the report that the conservatives have the 48 no confidence votes. Now we await to see if the labour party joins in ousting May

iv)France

It now seems that France has solved Italy’s deficit problem as Macron has decided to lower taxes big time in the wake of the riots in his country. His budgetary deficit for 2019 will now widen to 3.6% much higher than Italy’s 2.4%. As we say in chess, check Mr Draghi…your move

(courtesy zerohedge)

v)And now its credit risk now soars

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

i)Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

iii)Reuters is running a study purporting that an illegal gold rush in destroying the Amazon rainforest.

( zerohedge)

iv)Detour mines extends the deadline has shareholders have so far voted to oust 5 out of 9 directors

( National Post/Friedman/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

Interesting: core PPI surges but the total PPI weakens due to lower energy costs.

(courtesy zerohedge)

i)Oh OH! this is dangerous; GE falls to its March 2009 low of $6.66. GE is a large derivative player and no doubt that they are off side of many of their trades

(courtesy zerohedge)

ii)the bond king has spoken: the economy is slowing down

also with the stock market woes, bonds should have rallied a lot more

Gundlach states that there will be no rate hikes in 2019

and he also states that the Fed is very worried on the flattening of the yield curve

(Jeff Gundlach)

iv)SWAMP STORIES

a)Nadler is claiming that Trump ordering the payoffs to mistresses would certainly be an impeachable offense. Many from Fox TV disagree

( zerohedge)

b)Trump, Pelosi and Schumer square off in a shouting match in the Oval office. The Democrats do not want a wall whereas Trump demands it. The Democrats do not want to shut down government.

( zerohedge)

c)this is going to be really exciting once Lindsay Graham becomes head of the Senate Judiciary Committee. He is going to ask for a special counsel to probe all things of Clinton including Uranium one

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 473 contracts standing for a loss of 92 contracts. We had 91 contracts stand for delivery yesterday so we lost 1 contract or an additional 5,000 oz will not stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus.

After December we have the non active January contract month and here we saw a gain of 4 contracts up to 1929 contracts. February saw its another 10 contract gain to stand at 79. March, the next big delivery month after December saw a loss of 2427 contracts down to 145,431

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

we still have not had any adjustments out of the dealer to the customer account to signify a settlement

EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

by John Mauldin

Someone asked recently how many times I had “crossed the pond” to Europe. I really don’t know. Certainly dozens of times. It’s been several times a year for as long as I remember.

Graphic: European Central Bank

That makes me an extremely unusual American. Most of us never visit Europe, except maybe for a rare dream vacation. And that’s okay because our own country is wonderful and has a lifetime of sights to see. But it does affect our perspective on the world.

Many of us don’t fully grasp how important Europe is to the US and global economy.

We may soon get a lesson on that. I’ve talked about Italy’s ongoing debt crisis, which is not improving, but Europe has other problems, too.

Worse, events are coalescing such that several potential crises—all major on their own—could strike at the same time, and not too long from now.

As I’ve been saying for about three years, there is no reason for the US to have a recession on its own. I think events elsewhere will push us into it, and Europe is a really big current risk. I know from my visits to Europe and discussions with friends there, they see all sorts of problems with Trump and particularly his tariffs.

However, another concern is that the various actors in Europe are not playing nice with each other. I tell my European friends the same forces that yielded Trump are coming to a European country near them. In some places, they already have.

So, in my never-ending quest to keep you ahead of the curve, I’ll review what’s happening “over there.” This may be a turnabout for European readers who rely on me to describe what’s happening over here. But as you’ll see, we are far more connected than separated by distance.

(Note: The link is to my favorite version of “Over There” written by George M. Cohan, here sung by James Cagney in 1942 for the film Yankee Doodle Dandy. It was written at the beginning of World War I and quickly became the number one song of not just that era but also the World War II era. Younger generations may not remember music with so much unbridled, enthusiastic patriotism. They can be excused for not quite understanding such feverish intensity. It was a different era.)

Monetary Drug Withdrawal

Last week my British friend Jim Mellon sent me a fascinating article with an alarming title: “News from Euroland—Recession Imminent.” I’m not certain when Jim sleeps, as I get a few emails from him every day at seemingly random times, always with pithy, on-target reading material. (Although I can usually figure out when he is in Great Britain by their timing.)

Now, I am not one who falls prey to click-bait headlines (nor is Jim) and I’m also well aware Europe’s economy is weakening. I would not have said recession was imminent but reading this article left me more than a little concerned. The author, economist Victor Hill, ties events together in ways many haven’t considered.

Hill begins the piece this way.

Across Europe, and particularly in the 18-member Eurozone, the economic news is sobering. It’s now clear that the credit crunch in emerging markets which has played out over most of this year, plus the slowdown in China, are having negative consequences in Europe. Yet, despite the ongoing trauma of Brexit, the UK is cruising along relatively smoothly—for now.

A number of critical events are about to coincide…

The first such event is the impending end of the European Central Bank’s quantitative easing “Asset Purchasing Programme,” which has been propping up asset prices with wholesale purchases of bonds, stocks, and anything else that isn’t nailed down.

Mario Draghi and his crew borrowed our Federal Reserve’s plan and, if possible, made it even crazier. You can see in the chart they have been stepping down purchases. The pace should reach zero in early 2019. But this doesn’t account for assorted other loan programs, which some would like to see continue or even expand. Germany opposes all such policies and I think will get its way, especially since Draghi will be leaving next year.

This means the Eurozone is about to lose a monetary drug on which it has grown highly dependent. But those 18 nations will not be the only ones affected. The larger EU needs a thriving core to stimulate growth for the whole continent.

Note that Draghi will finish his term as ECB president in October 2019. Economists (what do they know?) project he will make his first interest rate increase just one month before he leaves, in September. That means taking rates from -0.40 bps to -0.20, still below zero.

In all likelihood, his replacement will have to be approved by Germany. What will be the new president’s appetite for negative rates even in the face of recession? Will he listen to the Bundesbank? Will the ECB once again expand its balance sheet? What is left to buy? All good questions with no answers yet but potential market dangers.

And if Europe falls into recession earlier in 2019, will Draghi reverse himself and resume expanding the balance sheet, buying yet more assets that are not nailed down? The Italians would certainly like that.

European Disunion and Brexit

Hill’s second “critical event” is Brexit, the latest plan for which is set for a December 11 vote in the UK’s Parliament. As of now its prospects look dim, at least without changes that the EU sidesays it won’t accept. That may not be true because, as we have learned, European officials are masters at vowing inflexibility and then bending when forced.

But let’s have some sympathy for Prime Minister Theresa May. She is dealing with a rebellion in her own party, has lost numerous votes and it is not clear she can force her (let’s call it) Brexit-lite proposal through Parliament. You can read about her troubles here.

This deal has monster implications for economics and investments and you really need to pay attention. I think I would vote against, not that anyone in Great Britain will care, as it seems to me that her compromise leaves Europe with more control over what a “final” agreement would look like. It’s not exactly what the “leave” crowd originally wanted. But in reality there are no good choices. If this is voted down, I see real chances for problems everywhere.

Another national vote might seem sensible, except that would look like the elites keep taking votes until they get the outcome they want. It would make a large part of the country upset no matter what. As I said, no good choices…

Regardless, it is highly uncertain what happens next. The UK gave formal notice it would leave the EU on March 29, 2019, whether terms of separation are reached by then or not. A “hard Brexit” would be chaotic, to say the least, as it would leave businesses trying to operate in a legal vacuum. World Trade Organization rules might serve as a backstop in some matters but the massive trade volume between the UK and EU would certainly slow. Can they walk that notice back? Fudge a little bit on the date? This is the EU. They can do anything they bloody well like. Damn the rules and full speed ahead…

On the other hand, remaining in the EU would enrage the millions who voted to leave and probably bring down the May government. Where it would go from there is anyone’s guess. It is hard to even imagine “democratic socialist” Jeremy Corbin as Prime Minister. So both economies are probably in for a shock unless some miracle produces orderly separation terms in the next three months, which seems unlikely.

The third critical event, says Hill, is the growing Italian crisis, which I’ve been warning about for quite some time. That kettle is getting ready to boil over. Now banks in Italy are having trouble refinancing their bond issues, which is forcing them to curtail lending to an already-weak private sector. Rising mortgage rates are cutting into consumer spending. Italy is arguably already in recession but the situation looks likely to get worse—which is a big problem for its creditors, mainly Germany, which we will discuss in a bit.

But Hill says, I think correctly, that the Italian crisis is no longer just economic, if it ever “just” was. It is emblematic of a culture war that is pitting anti-immigration populist movements against “elites” they believe are hostile to their interests. As happened elsewhere, unemployed and working-class people are losing faith in the system. We see this most recently in the violent gas-tax protests in France.

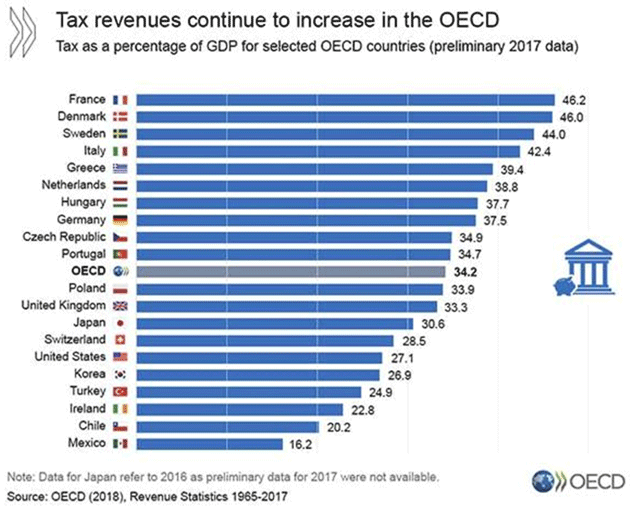

This protest movement has an altogether different feel when you pay close attention. It is not just about higher fuel taxes. It is about almost half the country being angry at the educated city-dwelling elite while the brunt of increased taxes falls on an increasingly burdened rural middle class. The French government now consumes 46.2% of GDP, making it the most-taxed OECD nation. Even a slight tax increase affects the working class disproportionately. And when it increases taxes on something like diesel fuel, which is critical in rural areas, it is particularly hard.

Image: Mish Shedlock

In Europe and around the world, we see this pushback against what is seen as an elite group at the top (the “Protected”) which pays no attention to the problems of their less successful “Unprotected” brethren. And those brethren are demanding attention.

This “morality play” is spreading through Europe. We now see German political patriarch Wolfgang Schauble backing a candidate to replace Merkel as head of the CDU (Christian Democratic Union), who is openly courting the same voters that have left their party and gone to the anti-immigration and populist Alternative for Germany (AfD). That means a conservative push for Germany and a more populist approach for mainstream parties.

The common thread running through these events is the idea of a united Europe. This idea was a driving force in the foundation of the European Union and is common in the establishment and/or “elite.” Up until a few years ago, the idea was popular across the political spectrum but support has weakened as economic times changed. It was never particularly feasible, but the effort made sense for a continent so damaged by centuries of repeated wars. The problem is that the EU can’t achieve its goals unless it gets stronger and much of the public has had its fill of centralization. I don’t know how they can solve this. Brexit, if it happens, may turn out to have been the test case for a full dissolution.

How that will unfold is hard to predict. For now, there are more immediate problems. Victor Hill thinks “a disorderly Brexit will be the spark that sets the Eurozone tinderbox aflame in the first half of 2019.” The tinderbox is already full in Italy and France. It won’t take much heat for that kettle to boil over.

But that’s not all.

Trade Threats

Speaking of unity, last weekend’s Buenos Aires G20 summit was a chance for world leaders to forge common ground on important global issues. That’s not exactly what happened but President Trump’s trade discussion with Chinese president Xi Jinping looked initially like a bright spot. They agreed to stop making things worse for a few months, at least. Markets were more skeptical after digesting the news—rightly so, at least from my standpoint.

As I’ve said, there are real issues with China on intellectual property and more. It is not unreasonable to ask for an open and fair playing field. China is no longer an emerging market nation. It has emerged, at least the eastern half. Beijing should play by the same rules as the rest of the developed world. But getting agreement with China is going to be a hard slog.

One encouraging but little-reported G20 event: US Secretary of State Mike Pompeo and Treasury Secretary Steven Mnuchin gathered their peers from the smaller G7 group for an unscheduled dinner. According to Ian Bremmer, they made significant progress on working together to solve the China issues. This should be positive if it continues.

Meanwhile, however, Louis Gave explains why problems with China may be bad news for Europe at a time when Europe doesn’t need any more challenges (bold is mine).

It is no secret that Trump is surrounded by men who want to “take China down,” who have argued at length that China is a house of cards built on unsustainable credit, and that all the US needs to do is give a gentle nudge for the whole edifice to come crashing down. So far, this talk of China’s vulnerability has proved way off-target. For all of the dire predictions of an imminent debt crisis and financial meltdown, China is still standing very much upright.

So, if Trump wants a win, where should he look? If a long cold war of attrition with China doesn’t look promising, perhaps bashing Europe—specifically Europe’s auto industry and lack of defense spending—could prove more attractive, especially as Europe is now politically rudderless and economically slowing. My bet would be that in the coming weeks, Trump stops speaking about China, and instead starts bashing Europe. And doubtless his favorite targets will be France and Germany, perhaps as payback for the slights he endured at last month’s commemoration of the World War I armistice. If nothing else, Trump has shown that he is a firm believer in the old adage that revenge is a dish best served cold.

I pay attention when Louis speaks. He often sees events that happen “around the curve.” His premise is simple: The automotive industry drives the German economy. Germany, in turn, drives the European economy. So if Trump decides to follow through on the car tariffs he’s threatened, it could be a serious blow. German auto executives met with him in Washington this week but the threat is still alive.

Oh, and one more thing. Deutsche Bank, Germany’s financial crown jewel, seems to be in deep trouble. Its shares, which never recovered from the 2007–2008 ugliness, dropped to all-time lows this week after German police raided the bank’s offices in a money-laundering probe. We don’t know exactly what the fire is but there sure is a lot of smoke. Other European banks are not exactly thriving but DB seems to be in particular trouble.

It is hard for us in the US to realize how important European banks are. European businesses, particularly small ones, get almost all their financing from banks. When Italian banks have trouble funding their bonds, that means Italian businesses will suffer.

So add all this up. We could see Europe faced with monetary tightening, hard Brexit, an Italian breakdown, popular unrest not just in France but all over, a trade war and a German/Italian bank crisis all at the same time. Again, this is not a far-off possibility. It could all be happening in the next three or four months.

If some combination of these crises develops into a perfect storm, the pain won’t stay in Europe. US, Canadian, Latin American, and Asian companies that do business with Europe will lose sales and have to lay off workers. Lenders everywhere who own Euro debt will face losses. Highly leveraged derivatives could blow up, forcing bailouts and currency interventions. We don’t know where it would lead but certainly nowhere good.

And it will end up being played out in the equity markets all over the world. Stay tuned…

The markets have been quite volatile for the past few weeks. My preferred ETF trading strategy, called Mauldin Smart Core, has performed well in this environment. Full disclosure, I have recently closed my own personal investment advisory firm down and moved my registration to my longtime friend Steve Blumenthal of CMG. As a personal business strategy, he has all the infrastructure and team to support me, and it really does allow me to spend more time researching and reading and writing. I am co-portfolio manager for the Mauldin Smart Core strategies which is available as a mutual fund or managed accounts.

We have done a report called “Investing During the Great Reset,” which explains our strategy and rationale. If nothing else, it will show you how I want to deal with the risk of a coming potential bear market and give you ideas for doing it yourself or in your own firm. Of course, I hope that some of you will become clients. But I am perfectly willing to help you whether you do or not. I want as many people as possible to get from where we are today to the other side of The Great Reset.

Full article on Mauldin Economics

Secure Storage Ireland – Click here for information

Secure Storage Ireland – Click here for information

News and Commentary

Gold gains on weaker dollar, chance of slower US rate hikes (CNBC.com)

Gold is regaining poise in Asia, rising call demand suggests more gains ahead (FXStreet.com)

Dow erases 500-point drop and closes higher in another wild session (CNBC.com)

Apple helps Wall St. pull back after S&P hits eight-month low (Reuters.com)

Fed seen slowing, or even stopping, rate hikes next year (Reuters.com)

Source: KingWorldNews

Gold is looking interesting (Macromon)

Gold will take out 5 years of highs in 50 trading days – Oliver (KingWorldNews.com)

What’s next for global markets? Keep a close eye on the oil price (MoneyWeek.com)

Here’s what mortgage ‘rate lock’ looks like, in one chart (MarketWatch.com)

Bear Markets Everywhere: Over Half The World Is Now Down 20% Or More (ZeroHedge.com)

Australia Warned To Prepare For “Severe Housing Collapse” And “Banking Crisis” (ZeroHedge.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

10 Dec: USD 1,246.80, GBP 980.61 & EUR 1,092.57 per ounce

07 Dec: USD 1,241.20, GBP 972.98 & EUR 1,091.51 per ounce

06 Dec: USD 1,236.45, GBP 971.48 & EUR 1,091.66 per ounce

05 Dec: USD 1,236.15, GBP 970.13 & EUR 1,090.16 per ounce

04 Dec: USD 1,239.25, GBP 966.74 & EUR 1,086.45 per ounce

03 Dec: USD 1,231.05, GBP 966.00 & EUR 1,084.92 per ounce

Silver Prices (LBMA)

10 Dec: USD 14.53, GBP 11.48 & EUR 12.73 per ounce

07 Dec: USD 14.49, GBP 11.34 & EUR 12.73 per ounce

06 Dec: USD 14.38, GBP 11.28 & EUR 12.68 per ounce

05 Dec: USD 14.48, GBP 11.34 & EUR 12.75 per ounce

04 Dec: USD 14.55, GBP 11.35 & EUR 12.77 per ounce

03 Dec: USD 14.39, GBP 11.31 & EUR 12.69 per ounce

Recent Market Updates

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

– Gold Is “Coiled” and Looks Set To Surge Like Natural Gas — Bloomberg Intelligence

– “Collapse Of Civilisation Is On The Horizon” – Attenborough Warns World Leaders

– Deutsche Bank May Cause The Next Global Crisis

– Ireland’s Mr Gold Reveals Nuggets Of Wisdom For When The Next Crash Comes

– BREXIT May Lead to UK Property Crash and Depression

– General Motors And General Electric Highlight The Ponzi Scheme That Is The US Economy

– A Worldwide Debt Default Is A Real Possibility

USAGold’s December letter: Where are we now in the investor cycle?

Submitted by cpowell on Mon, 2018-12-10 20:52. Section: Daily Dispatches

3:54p ET Monday, December 10, 2018

Dear Friend of GATA and Gold:

USAGold’s December News & Views letter records what seems to be the changing of tides in the market away from stocks and bonds and toward the long-unloved monetary metals. The letter is headlined “Where Are We Now In the Investor Cycle?” and it’s posted here:

http://www.usagold.com/publications/NewsViewsDEc2018.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Reuters is running a study purporting that an illegal gold rush in destroying the Amazon rainforest.

(courtesy zerohedge)

Illegal gold rush destroying Amazon rainforest, study says

Submitted by cpowell on Mon, 2018-12-10 23:47. Section: Daily Dispatches

By Anastasia Moloney

Reuters

Monday, December 10, 2018

BOGOTA, Colombia — A rise in small-scale illegal gold mining is destroying swathes of the Amazon rainforest, according to research released today that maps the scale of the damage for the first time.

Researchers used satellite imagery and government data to identify at least 2,312 illegal mining sites across six countries in South America — Brazil, Bolivia, Colombia, Peru, Ecuador, and Venezuela. …

… For the remainder of the report:

https://www.reuters.com/article/us-latam-forests-mining/illegal-gold-rus..

Detour mines extends the deadline has shareholders have so far voted to oust 5 out of 9 directors

(courtesy National Post/Friedman/GATA)

Paulson cries foul as Detour Gold extends voting to halt a board coup

Submitted by cpowell on Tue, 2018-12-11 01:24. Section: Daily Dispatches

‘This Is What Despots and Dictators Do’: Paulson Cries Foul as Detour Gold Extends Voting to Halt a Board Coup

By Gabriel Friedman

National Post, Toronto

Monday, December 10, 2018

Detour Gold Corp.’s management was left scrambling to fight off a board coup on Monday, after a crucial initial vote showed shareholders wanted to oust at least five out of its nine directors.

The board extended the deadline to vote, with ballots that had been due last Friday now due on Wednesday and a meeting to count final votes postponed from Tuesday until Thursday.

Detour’s management has been under fire from a group of shareholders led by U.S. billionaire John Paulson, whose hedge fund Paulson & Co. owns 5.7 per cent of the company. The campaign complained about abysmal returns at the Toronto-based miner including a 70 per cent fall in market capitalization since July 2016.

“This is unheard of. Shareholders have voted,” Marcelo Kim, a Paulson & Co. partner who led the campaign, wrote in an email. “They don’t like the result, so they are trying to change it? This is what despots and dictators do.” …

… For the remainder of the report:

https://business.financialpost.com/commodities/mining/this-is-what-despo…

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

White House to Nominate Treasury Official to Run CFTC in 2019

Heath Tarbert, currently assistant secretary for international markets, expected to succeed J. Christopher Giancarlo

By Gabriel T. Rubin

Dec. 10, 2018 3:44 p.m. ET

WASHINGTON—The White House plans to nominate Heath Tarbert, a senior Treasury Department official, to serve as chairman of the Commodity Futures Trading Commission when the current agency head’s term ends in 2019, according to people familiar with the matter.

-END-

LAWRIE WILLIAMS: Nervous equities should give gold price momentum

At the start of the current week U.S. equities opened down significantly again before picking up during the day and ending marginally higher overall. Markets are nervous and unsure what’s going to happen next – recovery or crash? There are plenty of respected advisers out there calling it either way.

As for gold a stronger dollar saw it slip back before making something of a recovery, but a break upwards through the psychological $1,250 level remained elusive. Some put this down to price management in the futures markets, and this certainly can’t be ruled out. A higher gold price implies significant dollar weakness and a visible sign that the U.S. economy is not nearly as healthy as the powers that be – the U.S. Administration, Treasury and the Fed – would like it to appear to be. After all President Trump is keen to try to demonstrate to the U.S. people that his policies are bringing prosperity and that the country is not headed for recession. A strong equities market helps reinforce that impression!

But the tariff war with China (the only one that really matters) may be backfiring. Chinese imports are still rising and U.S. exports to China are diving because of the strong dollar and the imposition of retaliatory tariffs. Hardly the outcome President Trump was looking for. And the whole situation has been exacerbated by the arrest and detention in Canada of China’s biggest tech company, Huawei’s, CFO at the U.S. behest pending possible extradition on Iran sanctions avoidance charges.

To put this in perspective, Huawei is at the forefront of global 5G technology, arguably is the world’s leading supplier of telecoms networking technology and a bigger seller of mobile phones than Apple. It is the world No. 2 cellphone manufacturer after South Korea’s Samsung, while Apple is only No. 3 and worryingly for the U.S., the latter company – until very recently the world’s largest by market capitalization – does around 20% of its business in China. Apple’s saving grace may be that it has huge manufacturing facilities in China and employs over 4 million Chinese so any retaliatory action may be limited, but the sales fallout in China given the adverse publicity generated by Meng Wanzhou’s arrest could be very significant. One suspects Apple executives will restrict any global travel plans until some kind of solution is reached regarding Meng’s arrest in Vancouver while changing planes. Indeed other executives of major U.S. companies will probably be doing likewise.

The arrested Meng Wanzhou is not only Huawei’s CFO, but also the daughter of the company’s founder, and this is a political firestorm already in process. Much of the world is becoming increasingly incensed at the U.S. applying its own domestic laws to real, or imagined, breaches by foreign entities which may be carrying out deals which are legal in their own countries. If anything could throw a new dimension into the trade war negotiations the arrest, and possible extradition of Meng would be it.

We suspect an initial compromise may be implemented which could reduce some of the political tensions – but still see the problem continuing. The bail hearing continues tomorrow and I suspect we will see Meng released on bail, but prevented from leaving Canada pending the extradition hearing. China won’t see this as a satisfactory outcome which will ensure the contretemps will continue, but at least it would ease Meng’s ordeal.

The arrest is but another significant factor which could well affect the U.S. tech sector in particular – and the this has been at the forefront of the huge equities markets gains in the past few years. Historically the gold price thrives on economic uncertainty with people choosing it as an insurance asset and wealth protector – not necessarily as a vehicle to enhance their investment value. It tends to perform steadily rather than spectacularly, but in the past couple of years its performance has been muted as people have looked for seemingly ever increasing gains first in bitcoin and then in the general equities markets. But bitcoin has collapsed, and is seemingly continuing on its downwards path despite recent attempts in the media to talk it back up, while equities markets are suddenly looking very uncertain after some huge falls. Price management and dollar strength has so far resulted in gold’s growth being suppressed, but the longer market uncertainty persists, the more likely it becomes that an unstoppable degree of upwards price momentum will fall into place. We don’t necessarily see a spectacular and sudden rise in price, but a steady one which should see it through $1,250, and perhaps back through $1,300 by the year end – and onwards and upwards in 2019, particularly if the U.S. Fed eases up on its proposed interest rate normalization plans, which currently seems more likely than not.

If equities resume their fall this week – and unless Meng Wanzhou is released rapidly they may well do so – then the Fed might even delay the planned rate rise considered highly likely at the FOMC meeting in a week’s time which would give a big and immediate boost for the gold price. But we consider this unlikely as things stand, but a reduction in the number of planned rate increases in 2019 has definitely to be on the cards. Next week’s ever-opaque Fed statements will thus be perused by financial commentators with special interest.

Whatever happens at the FOMC meeting we consider that gold will increasingly appear on institutions’ and individuals’ investment horizons and price momentum will continue to build into 2019. How far this will take us on the upwards path remains to be seen.

11 Dec 2018

________________________________________

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8985/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8968 /shanghai bourse CLOSED UP 9.51 POINTS OR 0.37%

HANG SANG CLOSED UP 19.29 POINTS OR 0.07%

2. Nikkei closed DOWN 71.48 POINTS OR 0.34%

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 96.93/Euro RISES TO 1.1395

3b Japan 10 year bond yield: RISES TO. +.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.13/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.37 and Brent: 60.45

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.26%/Italian 10 yr bond yield DOWN to 3.11% /SPAIN 10 YR BOND YIELD UP TO 1.46%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.85: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.26

3k Gold at $1247.75 silver at:14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 42/100 in roubles/dollar) 66.28

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.13DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9884 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1264 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.26%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.88% early this morning. Thirty year rate at 3.15%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3544

Global Stocks, S&P Futures Surge On Fresh Trade War De-escalation Hopes

After several days of precipitous market drops, and following yesterday’s dramatic Apple-led intraday rebound, the biggest since February, S&P futures and European stock markets are sharply higher even as Asian shares slipped, as investor sentiment was boosted by fresh prospects of a thaw in the trade war following overnight news that Chinese Vice Premier Liu He discussed a timetable for trade talks with Treasury Secretary Steven Mnuchin, coupled with a report this morning from Bloomberg that China is moving toward cutting its trade-war tariffs on imported U.S.-made cars, a step which had previously been brandished by President Donald Trump as a concession won during trade talks in Argentina.

The big news overnight was a report according to China’s Mofcom which said Vice Premier Liu He spoke by phone with US Treasury Secretary Mnuchin and Trade Representative Lighthizer in which both sides exchanged views on implementing consensus reached by their leaders, while they also exchanged views on pushing forward timetable and road map for next stage of trade discussions. The news – taken as a positive sign for trade war de-escalation – sent S&P futures as much as 20 points higher, shrugging off losses in the Asian benchmark and a drop in Japanese equities…

… while Europe’s Stoxx 600 was trading at session highs, up over 1.5% as a result of a late catch up with yesterday’s S&P rebound, led by THE construction, basic resources, builders and telecom sectors even with today’s rebound it was still heading for its worst year since 2008.

European automakers also surged following the Bloomberg report that China is said to be moving on the US auto tariffs reduction that US President Trump has previously tweeted on. The proposal has been submitted for review, however, the decision has not been finalised and still could change.

Yet investors also have an eye on the continuing flap over Canada’s arrest of the chief financial officer of Huawei Technologies Co. And among a plethora of political risks, the U.K. is seeking reassurances from European partners over Brexit and fears linger over the possibility a French protest movement could escalate further.

After crashing on Monday to a 21 month low as Theresa May postponed a key Brexit vote in parliament, the pound staged a rally, trimming some of Monday’s tumble as the UK Prime Minister tried to convince EU leaders to renegotiate the current Brexit deal.

The broader risk-on sentiment weakened the dollar weakened while Treasuries and European sovereign bonds fell.

With market having been gripped by a growing sense of panic, some – like Nomura’s Charlie McElligott – have warned that the next move could be a furious rally higher as hedge funds scramble to recover some of their YTD losses in the last few days of 2018.

“Markets are highly volatile,” said hedge-fund pioneer Paul Tudor Jones at a conference in New York. “I can easily see a situation in 2019 where all the deleveraging that we’ve experienced in the last month and a half — really, the last four or five months — all that deleveraging gets reinvested back into the market.”

Meanwhile in India’s assets saw a choppy session, with stocks initially roiled by a surprise resignation of the central bank governor on Monday, before posting a recovery as traders mulled the implications for Prime Minister Narendra Modi of regional election results. Emerging-market currencies and shares edged higher. Oil climbed with most metals.

The dollar dropped versus most of its G-10 peers as concerns over a possible deterioration in U.S.-China trade talks persisted, while short-term positioning and U.K. wage data helped lift the pound from a 20-month low. The pound headed for its first gain in three days versus the dollar, having tumbled Monday to its lowest level since April 2017 after the U.K. Prime Minister opted to delay a key vote on her Brexit deal. The yen climbed against major global currencies as U.K. Prime Minister Theresa May’s Brexit vote deferral and weakness in equity markets deterred risk-taking

Brent (+0.9%) and WTI (+1.0%) prices rebounded, despite drifting lower at the start of the session following comments from Russian Energy Minister Novak that Russia plans to cut oil output by 50k-60k BPD in January which is significantly below the 228,000 BPD figure targeted as part of the latest OPEC deal. Novak adds that they will gradually reduce oil output. Separately, high level internal reports are to cut output by 139k BPD following the OPEC deal. Looking ahead today sees the API weekly data release, which saw a crude stocks build of 5.6mln last week. Gold has strengthened on a softer dollar, although the yellow metal is still off of the 5-month high of USD 1250.55/oz reached in the previous session. Separately, exploration by Rio Tinto in Australia has yet to find any economically viable copper ore veins; the site had been touted as being potentially rich in copper.

Expected data include PPIs and small-business optimism index. American Eagle and Pivotal Software are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.7% to 2,662.00

- MXAP down 0.3% to 147.99

- MXAPJ up 0.1% to 477.40

- Nikkei down 0.3% to 21,148.02

- Topix down 0.9% to 1,575.31

- Hang Seng Index up 0.07% to 25,771.67

- Shanghai Composite up 0.4% to 2,594.09

- Sensex up 0.2% to 35,044.71

- Australia S&P/ASX 200 up 0.4% to 5,575.88

- Kospi down 0.04% to 2,052.97

- STOXX Europe 600 up 1.4% to 343.77

- German 10Y yield rose 2.6 bps to 0.272%

- Euro up 0.2% to $1.1383

- Italian 10Y yield fell 2.6 bps to 2.74%

- Spanish 10Y yield rose 1.7 bps to 1.46%

- Brent futures up 0.5% to $60.45/bbl

- Gold spot up 0.3% to $1,248.54

- U.S. Dollar Index down 0.3% to 96.97

Top Overnight News from Bloomberg

- Top Chinese and American trade officials spoke by phone, signaling that dialog between the two nations on trade issues is at least continuing despite a diplomatic row over the arrest of a senior Chinese businesswoman

- Faced with a Brexit vote she can’t win, Theresa May appears to be gambling that running down the clock to a no-deal departure might change the arithmetic in Parliament

- The European Union won’t allow U.K. Prime Minister Theresa May to reopen negotiations over the Brexit divorce deal — but it could offer some of the reassurances she says she wants, officials said.

- In India, Urjit Patel’s shock exit as governor of the central bank roiled financial markets already nervous about early election results showing Prime Minister Narendra Modi’s ruling party losing support in key states.

- OPEC’s surprise output reduction has wrong-footed short-sellers. Hedge funds increased wagers against rising Brent crude prices for a 10th straight week in the period that ended last Tuesday and cut bullish bets on West Texas Intermediate oil to the lowest in almost six years

- Allies of Republican Representative Mark Meadows are pressing for him to be Donald Trump’s new chief of staff as the White House weighed other serious contenders, including U.S. Trade Representative Robert Lighthizer, for the vital leadership post

- Jerome Powell is ramping up Federal Reserve communication to build public trust and help insulate it from political attack

- Indian assets swung as investors weighed Modi’s performance in the polls in states which are key to his reelection bid in 2019

Asian equity markets were mixed as sentiment in the region only found mild solace from the tech-led recovery on Wall St. ASX 200 (+0.4%) was firmer at the open in which outperformance in the tech sector helped the index pick itself up from around 2-year lows although this later stalled amid weakness in energy and financials, while Nikkei 225 (-0.3%) swung between gains and losses due to a lack of fresh drivers and an indecisive currency. Shanghai Comp. (+0.4) and Hang Seng (unch.) were also choppy on trade uncertainty amid lingering concerns the Huawei situation could spill-over to US-China trade talks, although there were reports that Vice Premier Liu spoke with US Treasury Secretary Mnuchin and US Trade Representative Lighthizer in which they exchanged views on pushing forward the timetable and road map for the next stages of trade discussions. Meanwhile, India markets were initially pressured following the shock resignation by RBI Governor Patel which many viewed to be in protest for government meddling, while the state assembly elections added to the woes for the government with the ruling BJP party on track to lose some states to the main opposition ahead of next year’s general election. Finally, 10yr JGBs were uneventful amid the indecisive risk tone and with participants following mixed results at the 30yr JGB auction.

Top Asian News

- Macau Casino Stocks Jump as Analysts Flag December Revenue Hopes

- Tencent Music Guides Pricing Around Midpoint in $1.2 Billion IPO

- HNA Is Said to Tap Credit Suisse to Revive Sale of Pactera Unit

- Goldman Sachs Buys Minority Stake in Turkey’s Hurriyet Emlak

- India Rupee, Stocks, Bonds Drop as RBI Chief’s Exit Roils Market

Major European Indices are in the green [Euro Stoxx 50 +1.6%], with some outperformance seen in the SMI (+1.6%) bolstered by strong performance in index heavyweight Novartis (+1.6%) after the FDA approved Pear Therapeutics mobile application, which their Sandoz unit will be rolling out in the US. The SMI is also bolstered by LafargeHolcim (+3.6%), which is benefitting from outperformance in the materials sector seen today on the back of US and Chinese representatives planning the next steps in trade discussions. FTSE 100 (+1.3%) is lagging its peers, amidst currency effects from ongoing Brexit developments. Other notable equity movers are WPP (+6.5%) after an update to guidance, and Ashtead Group (+4.2%) after they announced full year expected results to be ahead of expectations.

Top European News

- Amsterdam Brothels to Get a Review by City’s First Female Mayor

- Danske to Sell Swedish Pension Assets to Polaris, Acathia

- Vivendi Urges Telecom Italia to Hold Shareholders Meeting

- Future of ‘Macronomics’ Tested by Violence on French Streets

- Casino Debt Swaps Rise to Record as French Protests Add Pressure

In FX, the GBP is ahead of the pack in terms of broad G10 currency advances vs the Greenback as the DXY ducks back under the 97.000 level. Cable has bounced further from yesterday’s new 2018 low circa 1.2507, through the pre-official cancellation of the Brexit vote base around a big figure higher and just shy of 1.2640, mainly on short covering and consolidation, but also with the aid of strong UK average earnings. Meanwhile, Eur/Gbp has retreated towards 0.9000 having cleared 0.9050 and topped out not too far from 0.9100.

- EUR/CHF/SEK/NOK – The next best majors, with the single currency maintaining its recovery momentum off 1.1350 lows vs the Usd, but capped ahead of 1.1400 and perhaps conscious of hefty option interest between 1.1390 and the bog figure (2 bn). The Franc remains relatively firm within a 0.9905-0.9865 range and above 1.1250 vs the Eur, while the Scandi crowns have clawed back recent losses amidst an improvement in risk sentiment, and with the Sek awaiting Swedish inflation data on Wednesday after significantly stronger than forecast Norwegian CPI metrics yesterday. Eur/Nok is around 9.7000 and Eur/Sek back below 10.3000.

- JPY – Also trying to pare losses vs the Dollar after extending its downturn from 112.25 to 113.35 and extremely close to a Fib level, but unable to rebound through 113.00 where heavy supply is touted and a 1.5 bn option expiry resides.

- AUD/CAD/NZD – Mixed fortunes once again as the Aud reclaims 0.7200+ status vs its US counterpart, albeit just, on more promising vibes regarding US-China trade, which have also nudged the Aud/Nzd cross back up towards 1.0500, as the Kiwi losses sight of 0.6900 vs the Usd. Meanwhile, the Loonie is back on the 1.3400 handle and regaining some composure alongside crude prices.

- EM – The Try continues to underperform on bearish technical rather than fresh fundamental impulses, but did glean support from another upbeat snapshot of Turkey’s current account to trade back near 5.3500 vs the Dollar from 5.4000+ at one stage.

In commodities, Brent (+0.9%) and WTI (+1.0%) prices have strengthened, despite drifting lower at the start of the session following comments from Russian Energy Minister Novak that Russia plans to cut oil output by 50k-60k BPD in January; which is significantly below the 228,000 BPD figure targeted as part of the latest OPEC deal. Novak adds that they will gradually reduce oil output. Separately, high level internal reports are to cut output by 139k BPD following the OPEC deal. Looking ahead today sees the API weekly data release, which saw a crude stocks build of 5.6mln last week. Gold has strengthened on a softer dollar, although the yellow metal is still off of the 5-month high of USD 1250.55/oz reached in the previous session. Separately, exploration by Rio Tinto in Australia has yet to find any economically viable copper ore veins; the site had been touted as being potentially rich in copper.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.0%, prior 0.6%; PPI Ex Food and Energy MoM, est. 0.1%, prior 0.5%

- 8:30am: PPI Final Demand YoY, est. 2.5%, prior 2.9%; PPI Ex Food and Energy YoY, est. 2.5%, prior 2.6%

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 9.51 POINTS OR 0.37% //Hang Sang CLOSED UP 19.29 POINTS OR 0.07% //The Nikkei closed DOWN 71.48 OR 0.34%/ Australia’s all ordinaires CLOSED UP 0.42% /Chinese yuan (ONSHORE) closed UP at 6.8985 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.57 dollars per barrel for WTI and 60.45 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.8985AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8968: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

The stock market reacts to China’s move to cut auto tariffs. Due to the extreme lower wages in China, a cut in tariffs for American cars will have no effect on Chinese purchases of cars.

(courtesy zerohedge)

China Moves To Cut Auto Tariffs, Sending Futures Higher

Conflicting trade war headlines have flooded out of Beijing over the past week, complicating analysts’ attempts to parse exactly how the arrest of Huawei CFO Meng Wanzhou has impacted the prospects for a future deal. But amid the chaos, a headline that hit the tap a few minutes ago could set the stage for US stocks to build on yesterday’s late-day rebound.

According to Bloomberg, China is moving to cut its trade-war tariffs on US autos. US equity futures spiked on the news, mirroring their reaction from last Monday after Trump bragged about the concession twitter, only for Treasury Secretary Steven Mnuchin and advisor Larry Kudlow to pour cold water on the president’s boasts by saying that the cuts had merely bee “discussed”.

Bloomberg said China is planning to cut tariffs on US-made cars to 15% from the current 40% has been submitted to China’s Cabinet to be reviewed in the coming days. China boosted tariffs on US-made cars to 40% as part of a raft of retaliatory measures against the US imposed over the summer. To be sure, nothing is set in stone just yet. The decision is being reviewed, and could still change.

While US automakers will undoubtedly benefit from the move, Bloomberg pointed out that European automakers like Mercedes-Benz and BMW will be the biggest beneficiaries after both companies – which have sizable manufacturing operations in the US – warned about lower profits this year.

European auto stocks have posted the largest gains on the news:

Here’s a roundup of headlines from BBG:

- Faurecia stock rises 5%

- Volkswagen stock jumps 4.3%

- VW controlling shareholder Porsche SE gains 4.7%

- Stoxx Europe Automobiles & Parts Index rises 2.9%, 2nd-biggest jump on broader index

- Among car suppliers, Continental +3.7%, Valeo +3.5%

- Daimler +3.1%, PSA +2.5%

Unless something goes seriously wrong in the next two-and-a-half hours, expect stocks to rip higher at the open:

Jim Cramer

✔@jimcramer

Now an insane rally on China looking to cut tariffs on US cars.

END

Zero hedge correctly labels the real war is intellectual property and China’s aid to be the leader in the next generation of products.

(courtesy zerohedge)

This is What The “Trade” War With China Is Really All About

Forget soybeans, auto imports, iPhones, crude oil, and cheap Chinese gadgets. Also forget tariffs, duties, and subsidies. Even forget weapons.

The real reason behind the US-China “trade” war has little to do with actual trade, and everything to do with what China’s president, Xi Jinping, said when he visited a memory chip plant in the city of Wuhan earlier this year. In a white lab coat, he made an unexpectedly sentimental remark, comparing a computer chip to a human heart: “No matter how big a person is, he or she can never be strong without a sound and strong heart”.

What is really at the basis of the ongoing civilizational conflict between the US and China, a feud which many say has gradually devolved into a new cold war if few top politicians are willing to call it for what it is, are China’s ambitions to be a leader in next-generation technology, such as artificial intelligence, which rest on whether or not it can design and manufacture cutting-edge chips, and is why Xi has pledged at least $150 billion to build up the sector.

But, as the FT notes, China’s plan has alarmed the US, and chips, or semiconductors, have become the central battlefield in the trade war between the two countries. And it is a battle in which China has a very visible Achilles heel.

Even with the so-called truce between the two sides signed last weekend, and which promptly unraveled after the Huawei CFO’s arrest was unveiled last week, Washington plans to ramp up export controls next year on so-called foundational technologies — those that can enable development in a broad range of sectors — and the equipment for manufacturing chips is one of the key target areas under discussion.

This is a concern for China as the $412 billion global semiconductor industry rests on the shoulders of just six equipment companies, with three of them based in the US. Together, these companies make nearly all of the crucial hardware and software tools needed to manufacture chips, meaning an American export ban would choke off China’s access to the basic tools needed to make their latest chip designs.

“You cannot build a semiconductor facility without using the big major equipment companies, none of which are Chinese,” said Brett Simpson, the founder of Arete Research, an equity research group. “If you fight a war with no guns you’re going to lose. And they don’t have the guns.”

To observe China’s reliance on foreign products, look no further than the over $300 billion in semiconductor equipment China has imported over just the past 12 months.

To be sure, under Beijing’s auspices, Chinese chip companies have made enormous gains in semiconductor design as well as chip testing and packaging, in an attempt to catch up to the US. Several private and state-owned Chinese companies — Intel-backed Tsinghua Unigroup, Cambricon Technologies and Huawei’s HiSilicon among them — have already begun to venture into designing the leading edge chips capable of AI applications.

But, as the FT, notes, the real difficulty is not in designing the chips, but in making them: “From a design perspective, Chinese companies are at least on par with anyone else in the world,” said Risto Puhakka, president of VSLI Research. “Where they have a challenge is if they decide to make a very cutting-edge chip.”

The country’s recent scramble, amid the push for China 2025 strategic plan, to become technologically self-sufficient in chip production is clearly visible in the next chart, showing the big spike in recent imports of equipment for semiconductor manufacturing.

Still, as Chinese semiconductor plants try to catch up, they have few choices when outfitting or upgrading their chip foundries. The reason: only a few equipment suppliers remain after a decade of consolidation.

Foremost among them is the Netherland’s ASML, which makes the photolithography machines that print and etch designs on to silicon wafers. It is the only supplier of the extreme ultra violet (EUV) lithography machines needed to make a 7-nanometre processor, the industry’s current gold standard.

Over in the US, Lam Research and Applied Materials as well as Japanese company Tokyo Electron dominate the market for equipment that can deposit billions of transistors and other active components on to a single chip. Another US company, KLA Tencor, sells much of the technology used in testing and monitoring the quality of chip production.

It is China’s reliance on these companies, more than any down swing in the stock market, that has made it vulnerable.

“Firms like Applied Materials, Lam Research and KLA-Tencor made 10 to 20 per cent of their revenues in China in 2017, a share which is expected to rise in 2018,” said Dan Wang, an analyst at Beijing research group Gavekal Dragonomics. “China is a large and growing market for them, and these companies don’t want export controls that are too restrictive.”

What would happen if the trade war escalates to prevent China from catching up with the US technologically?

Under current laws, an export ban on semiconductor equipment would mean both foreign companies, such as Samsung and Intel with foundries located in China, as well as wholly owned Chinese foundries would be unable to buy American equipment, though foreign companies are likely to be able to apply for waivers.