GOLD: $1252.65 UP $3.15 (COMEX TO COMEX CLOSINGS)

Silver: $14.75 UP 10 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1243.60

silver: $14.60

Again, Goldman Sachs takes 100% of the issued gold contracts.

EXCHANGE: COMEX

CONTRACT: DECEMBER 2018 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,249.200000000 USD

INTENT DATE: 12/18/2018 DELIVERY DATE: 12/20/2018

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 1

737 C ADVANTAGE 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 7,277

For comex gold and silver:

DEC

NUMBER OF NOTICES FILED TODAY FOR DEC CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.003 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7277 NOTICES FOR 727600 OZ (22.634 TONNES)

SILVER

FOR DECEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

119 NOTICE(S) FILED TODAY FOR 595,000 OZ/

total number of notices filed so far this month: 4070 for 20,355,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3829: UP 182

Bitcoin: FINAL EVENING TRADE: $3721 up 72.00

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 349 CONTRACTS FROM 173,209 DOWN TO 173,007 DESPITE YESTERDAY’S 4 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 20 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

637 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 637 CONTRACTS. WITH THE TRANSFER OF 637 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 637 EFP CONTRACTS TRANSLATES INTO 3.185 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

NOW 21.040 MILLION OZ INITIALLY STAND FOR DECEMBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DEC: 21,910 CONTRACTS (FOR 13 TRADING DAYS TOTAL 21,910 CONTRACTS) OR 109.550 MILLION OZ: (AVERAGE PER DAY: 1685 CONTRACTS OR 8.426 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 109.550 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 15.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,786.61 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

ACCUMULATION FOR NOVEMBER /2018: 247.18 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 349 WITH THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY.. AS THE BOYS CONTINUE WITH THEIR CUSTOMARY MIGRATION OVER TO ETFS AT THE START OF AN ACTIVE DELIVERY MONTH. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 637 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A TINY SIZED: 288 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 637 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 349 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.65 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .875 BILLION OZ TO BE EXACT or 125% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DEC MONTH/ THEY FILED AT THE COMEX: 119 NOTICE(S) FOR 595,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./AND NOW DEC. AT 21.100 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 4251 CONTRACTS UP TO 412,485 WITH THE GAIN IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $1.50//.YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4718 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 6039 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 412,485. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,290 CONTRACTS: 4251 OI CONTRACTS INCREASED AT THE COMEX AND 6039 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 10,290 CONTRACTS OR 1,029,000 OZ = 32.00 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.50???

YESTERDAY, WE HAD 7213 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC : 109,218 CONTRACTS OR 10,921,800 OZ OR 343.11 TONNES (13 TRADING DAYS AND THUS AVERAGING: 8401 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 343/11 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 343.11/2550 x 100% TONNES = 13.45% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 7110.67 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR NOV 2018: 552.88 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 4,251 WITH THE GAIN IN PRICING ($1.50) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6039 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6039 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 10,290 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6039 CONTRACTS MOVE TO LONDON AND 4251 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 32.00 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $1.50 IN YESTERDAY’S TRADING AT THE COMEX??

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

FILED LATE

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.15 TODAY (PRE FOMC)

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD

I) A DEPOSIT OF 8.23 TONNES OF PAPER GOLD.

/GLD INVENTORY 771.79 TONNES

Inventory rests tonight: 771.79 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 10 CENTS TODAY:

A HUGE CHANGE IN SILVER INVENTORY/

A DEPOSIT OF 751,000 OZ INTO THE SLV INVENTORY

/INVENTORY RESTS AT 318.547 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 349 CONTRACTS from 173,209 DOWN TO 172,860 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

637 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 637 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 349 CONTRACTS TO THE 637 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL GAIN OF 435 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.185 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. AND NOW 21.045 MILLION OZ STANDING IN DECEMBER.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 4 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 637 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 27.09 POINTS OR 1.05% //Hang Sang CLOSED UP 51.14 POINTS OR 0.20% //The Nikkei closed UP 127.53 OR 0.60%/ Australia’s all ordinaires CLOSED DOWN 0.21% /Chinese yuan (ONSHORE) closed DOWN at 6.8988 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 46.52 dollars per barrel for WTI and 56.45 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED DOWN AT 6.8988AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)Trump will not like this: China is accused of a huge hack of thousands of European diplomatic cables

( zerohedge)

4/EUROPEAN AFFAIRS

ITALY

Seems that our Italian friends have won out: The EU has agreed with their 2.04% budgetary deficit. The ECB will now continue with its purchase of Italian bonds as they are the only purchasers of these. Italy gets to spend and will no doubt increase its debt to GDP

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY/SYRIA/USA

The USA after stating days ago that they will be in Syria for quite some time, reversed that edict as they are now preparing for a full withdrawal of forces from Syria. Obviously they did not want to get into the cross-hairs of Turkey. Erdogan is planning a massive invasion from the North targeting the Kurds. Trump realizes this is going to be a quagmire so he is exiting

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

ii)Chinese newspapers are now stating that GATA is not wrong in the gold and silver manipulation by the western banks/governments.( GATA/Chris Powell)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

Hard data continues to point that the uSA economy as well as the global economy is contracting. Today existing home sales tumble 7% year/year.

(courtesy zerohedge)

a)Graham Summers points out that the entire global system is contracting. All you need to see is the price of oil falling, the price of copper falling and the 10 year USA bond falling in yield. On top of that Bellwether Fed ex just reported lousy earnings and told that future earnings will be waning

(courtesy Graham Summers)

c)Illinois is in a mess and so is Chicago. Actually every Chicago homeowner owes $140,000 to bail out just the city’s pension problems( Mish Shedlock/Mishtalk)

d)Jeffrey snider studies the odds aspects of the US Treasury futures and the future contract of it, itself. Generally when the open interest climbs above 900 million it spells trouble, that the Fed is wrong on the reflation scenario.. It is now over 1.1 mllion contracts and it indicates trouble ahead.

iv)SWAMP STORIES

a)A good one: a good analysis of James Comey’s conflicted testimony

(courtesy zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of DECEMBER and here in this front month of December we now have 257 contracts standing for a LOSS of 34 contracts. We had 22 contracts stand for delivery yesterday so we LOST 12 contracts or an additional 60,000 oz will NOT stand for delivery as these guys morphed into London based forwards as well as accepting a fiat bonus.

After December we have the non active January contract month and here we saw a LOSS of 18 contracts up to 1760 contracts. February saw a 1 contract loss to stand at 120. March, the next big delivery month after December saw a LOSS of 393 contracts down to 141,862.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

Everything Bubble Started Bursting In 2018 – GoldCore Video

– Review of 2018: ‘Everything bubble’ started bursting

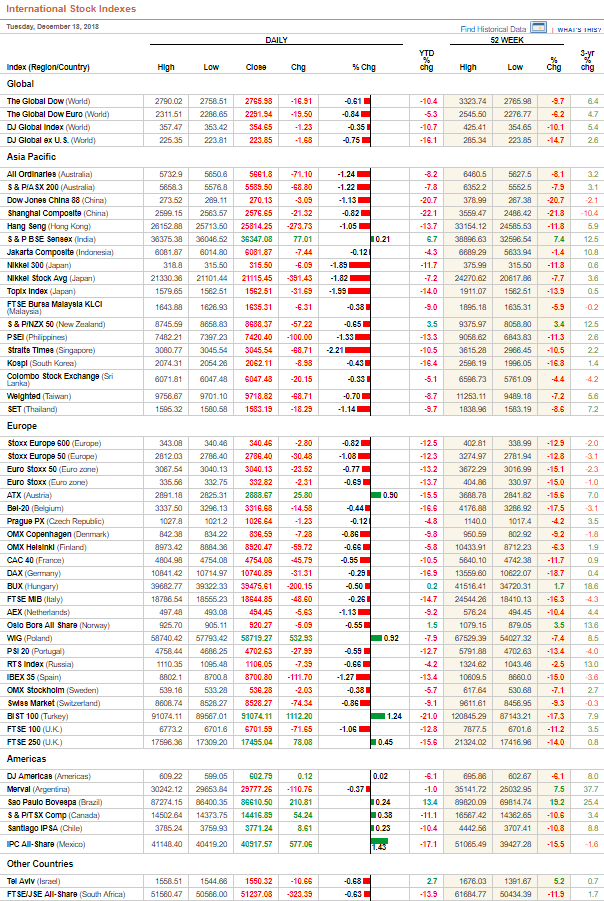

– International stock market indices and many property markets have fallen sharply

– S&P 500 -4.5%, Nikkei -8%, EuroStoxx 50 -12.5%, FTSE -13%, DAX -16.5%

– Of 54 major international stock market indices, only 6 are higher (see table below)

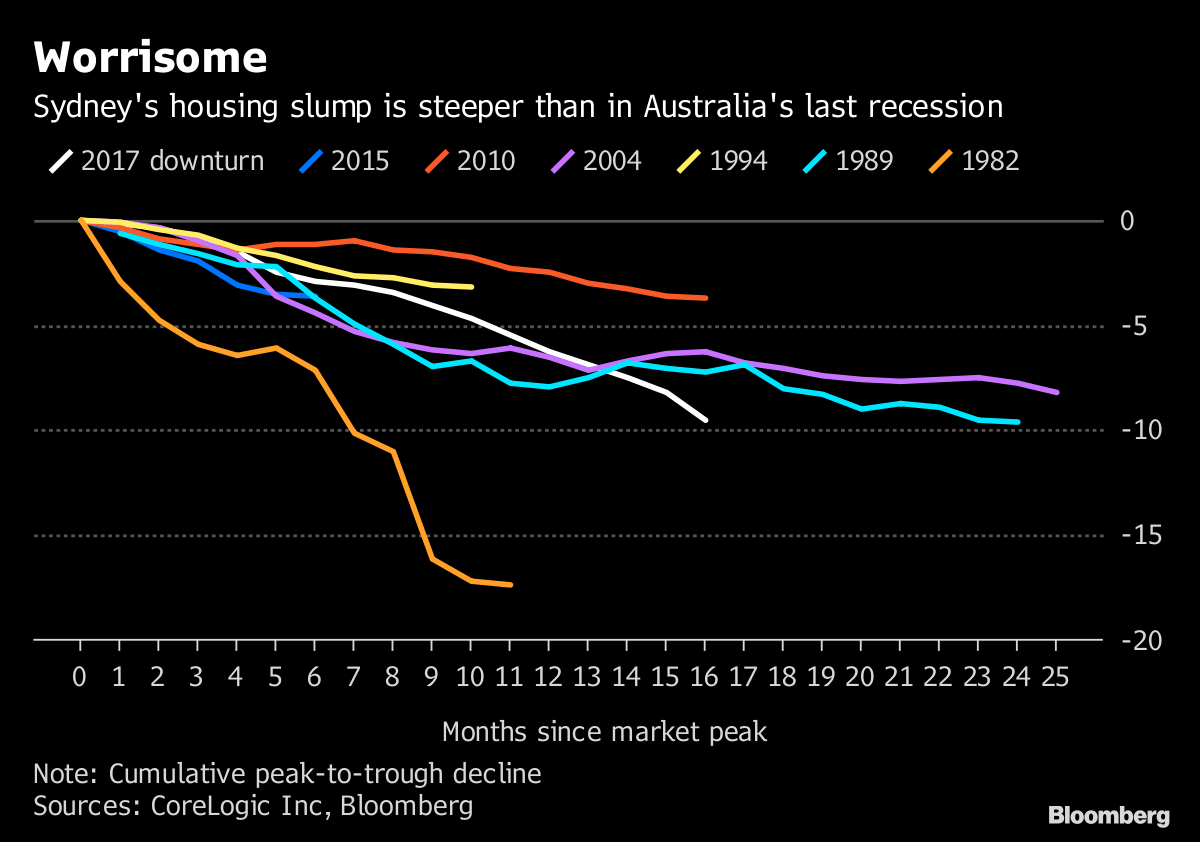

– Global property bubble bursting – London, Sydney and Vancouver fall nearly 10%

– Crypto bubble burst as bitcoin falls from $20k to below $4k and cryptos collapsed

– Collapse of central bank driven asset bubbles to continue and intensify in 2019

– Gold lower in USD in 2018 but gains in EUR, GBP, AUD, CAD and most currencies

Editors note: In our first Goldnomics podcast this time last year, we considered the outlook for markets in ‘What 2018 has in store for financial markets’ (here). A year later our conversation looks quite prescient given how stock market (see below) and property market bubbles have started to burst and the collapse of the crypto and bitcoin bubble.

Source: WSJ

Watch ‘2018 – Everything Bubble Starts Bursting’ video here

CHRISTMAS SCHEDULE

We will be closed from 24th of December (next Monday), and reopen again on the 2nd of January (Wednesday). Our last trading day will be on the 21st of December (this Friday) and insured deliveries will begin again in the first week of January 2019.

We wish all our subscribers & clients a Happy Christmas and a Healthy & Wealthy 2019

Secure Storage Ireland – Click here for information

News and Commentary

Stocks Edge Up Before Fed Decision; Bonds Steady: Markets Wrap (Bloomberg.com)

Fed must take wait-and-see approach for stocks to get ‘sustained’ rally (CNBC.com)

S&P 500 ends flat in volatile trade ahead of Fed meeting (Reuters.com)

Chance of recession rises to the highest level of the Trump presidency: CNBC Fed Survey (CNBC.com)

As Global Equities Take a Hit, Gold Miners Are Doing Fine (Bloomberg.com)

Source: Bloomberg via Yahoo Finance

We Are In a Global Bear Market – Druckenmiller (Bloomberg.com)

This Is A Bear Market – Stocks Slump After Gundlach Unleashes Truth-Bombs (ZeroHedge.com)

How trade wars could easily get out of control (Telegraph.co.uk)

The world changes when you see gold under water (VOANews.com)

Sydney’s 10% Property Plunge Will Be the Central Bank’s Biggest Worry (Yahoo.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

18 Dec: USD 1,248.80, GBP 987.43 & EUR 1,096.70 per ounce

17 Dec: USD 1,239.10, GBP 982.61 & EUR 1,093.13 per ounce

14 Dec: USD 1,239.15, GBP 983.39 & EUR 1,096.90 per ounce

13 Dec: USD 1,244.45, GBP 982.87 & EUR 1,093.62 per ounce

12 Dec: USD 1,244.75, GBP 993.31 & EUR 1,098.24 per ounce

11 Dec: USD 1,248.25, GBP 988.99 & EUR 1,096.59 per ounce

Silver Prices (LBMA)

18 Dec: USD 14.66, GBP 11.55 & EUR 12.86 per ounce

17 Dec: USD 14.60, GBP 11.55 & EUR 12.86 per ounce

14 Dec: USD 14.58, GBP 11.61 & EUR 12.92 per ounce

13 Dec: USD 14.68, GBP 11.60 & EUR 12.90 per ounce

12 Dec: USD 14.66, GBP 11.68 & EUR 12.93 per ounce

11 Dec: USD 14.64, GBP 11.62 & EUR 12.85 per ounce

Recent Market Updates

– Global Financial System Is ‘Unstable’ and Risk Of ‘Clearing System Seizure’, BIS Warns

– Gold Flowing From West To East and Now To Goldman Sachs

– Brexit Risk Sees Gold Rise To Test EUR 1,100 Per Ounce

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

Ronan Manly: Venezuela’s gold in limbo amid tug-of-war at Bank of England

Submitted by cpowell on Tue, 2018-12-18 18:09. Section: Daily Dispatches

1:12p ET Tuesday, December 18, 2018

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly today provides a detailed update about Venezuela’s attempt to repatriate its gold from the Bank of England. As best as Manly can determine, the bank still has not released the metal.

Manly’s report is headlined “Venezuela’s Gold in Limbo amid Tug-of-War at the Bank of England” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/venezuelas-gold-in-limbo-a…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Despite bank confessions, they still refute conspiracy theory on gold/silver rigging

(courtesy Bill Murphy/Dunagan/Reluctant Preppers)

Banks’ confessions refute ‘conspiracy theory’ scorn of gold rigging complaints, Murphy says

Submitted by cpowell on Tue, 2018-12-18 18:32. Section: Daily Dispatches

1:32p ET Tuesday, December 18, 2018

Dear Friend of GATA and Gold:

Dunagun Kaiser of Reluctant Preppers today interviews GATA Chairman Bill Murphy and they express amazement that complaints of gold market manipulation are still dismissed as “conspiracy theory” even as investment banks increasingly confess to market rigging.

Gold’s price, Murphy notes, is a measure of inflation that tends to push interest rates up, and governments aim to suppress the price to help keep interest rates down.

The interview is 28 minutes long and can be viewed at You Tube here:

https://www.youtube.com/watch?v=E1JRtLY0L0I&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Chinese newspapers are now stating that GATA is not wrong in the gold and silver manipulation by the western banks/governments.

(courtesy GATA/Chris Powell)

From China: ‘GATA is not wrong’

Submitted by cpowell on Tue, 2018-12-18 20:11. Section: Daily Dispatches

3:23p ET Tuesday, December 18, 2018

Dear Friend of GATA and Gold:

Thanks to C.C., our new friend in Shanghai, China, for alerting us to Chinese-language commentary published in August in the Hong Kong Economic Journal that cited GATA extensively, even taking for illustration the GATA painting by Alain Despert:

https://www1.hkej.com/dailynews/investment/article/1914231/

Your secretary/treasurer today has had some fun attempting a translation using a couple of internet translator sites and attempting a little editing for clarity while hoping to avoid any change in meaning and any stumbling badly over Chinese idioms. For example, “gold permabulls” translates literally into Chinese as “gold eternal cattle.” (This may be close enough, since many of us who maintain our interest in gold spend most of our days sitting in front of our computers and could afford to lose some weight.)

…

That attempted translation is appended, and clumsy as it may be, a few conclusions fairly may be drawn from it:

— China continues to know all about the Western gold price suppression scheme and even about GATA and there is more to China’s knowledge than was relayed by the cables sent from the U.S. embassy in Beijing to the State Department in Washington some years ago, cables that were revealed by Wikileaks:

http://www.gata.org/node/10380

http://www.gata.org/node/10416

— The author of the Hong Kong Economic Journal commentary appended is following GATA’s work closely and his concluding observation, about silver, implies that he also follows the work of silver market analyst and market-rigging whistleblower Ted Butler.

— Complaints about gold and silver market manipulation can’t get into mainstream Western news organizations despite the most ardent agitation. But such complaints can get into Chinese news organizations quite by themselves. In this respect the news organizations of a nominally communist country are freer than those of what is nominally the Land of the Free.

— And the British poet and humanitarian Arthur Hugh Clough, whose poem “Say Not the Struggle Naught Availeth” was beloved by Winston Churchill in the darkest hours of World War II, may have been right, even with his compass points reversed:

And not by eastern windows only,

When daylight comes, comes in the light.

In front the sun climbs slow, how slowly,

But westward, look, the land is bright.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Gold Permabulls Aren’t Wrong

By Shi Lin Shu

Hong Kong Economic Journal

Monday, August 13, 2018

https://www1.hkej.com/dailynews/investment/article/1914231/

This newspaper’s main writer, Bi Laolin, mentioned me in the headline of his Investor Diary diary column Friday. I was flattered but also so dissatisfied with it.

Bi Laolin wrote that some internet blogs are loyal to gold. This is true. Any time you look at the media or internet, opinions about gold are often in the majority. This is human nature. People are optimistic about the things they like, and the editor of an internet site or news organization intentionally or unintentionally caters to his audience’s psychology. The result of this tendency is that analytical observations are not entirely objective and neutral.

Gold permabulls are not entirely motivated by emotional bias but also by belief that government’s gold policy is flawed — that the authorities and their agents often manipulate the gold and silver market, which is very unfair to the public and investors.

The most iconic of these permabulls is a civil-rights organization called the Gold Anti-Trust Action Committee (GATA), whose symbol is a figure like Don Quixote riding on a horse, holding the GATA banner, leading a crowd to the Federal Reserve headquarters. [Actually, the building in the painting is the U.S. Treasury Department, but no matter.]

GATA took action against a number of large investment banks that manipulate the gold and silver markets and has achieved some success, with a number of large banks being fined, but the market is far from being as fair as GATA hopes.

Bi Laolin praised the spirit of GATA’s Don Quixote but I have previously reminded readers that our identity is that of a general investor or analyst, not that of gold and silver market revolutionists, if, to participate in the market game, you have to face reality and the unspoken rules.

GATA and the gold permabulls are not wrong. The gold market is indeed a long process of repeated climbing, and gold prices are often artificially depressed. … The long haul for gold may be too long for people, but if we see clearly and grasp the main direction of the long trend, gold is valuable. …

[The commentary then does some technical analysis of gold and silver prices before concluding:]

JPMorgan Chase will stop a large number of silver shorting activities, but the data shows that the short-selling by eight traders led by the bank is still equal to 200 days of world silver production, only one day less than a month ago. It seems that the GATA revolution has not yet succeeded and must continue to work.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8988/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8971 /shanghai bourse CLOSED DOWN 27.09 POINTS OR 1.05%

HANG SANG CLOSED UP 51.14 POINTS OR 0.20%

2. Nikkei closed DOWN 127.53 POINTS OR 0.60%

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 96.84/Euro RISES TO 1.1398

3b Japan 10 year bond yield: RISES TO. +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.35/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 46.52 and Brent: 56.45

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.24%/Italian 10 yr bond yield UP to 2.76% /SPAIN 10 YR BOND YIELD UP TO 1.36%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.52: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.29

3k Gold at $1247.70 silver at:14.66 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 10/100 in roubles/dollar) 66.33

3m oil into the 46 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.35 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9937 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1328 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.24%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.82% early this morning. Thirty year rate at 3.07%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3369

Futures Rise Ahead Of Fed; Europe Jumps On Italy Budget Deal

S&P futures rose after yesterday’s volatile session ahead of today’s Fed decision, and European stocks jumped after Italy struck a crucial budget deal with the EU following a downbeat Asian session as oil tried to rebound after a furious three-day selloff that rattled global markets and sent investors scrambling into the safety of government bonds (in record numbers according to BofA).

The Stoxx Europe 600 Index gained 0.5% rising to session highs after four days of declines, with banking and healthcare stocks contributing the most to the gains, after the European Commission decided against launching a disciplinary procedure against Italy over its budget, while carmakers climbing on hopes of a breakthrough on trade.

Rome and Brussels ended their long-running feud over Italy’s 2019 budget, striking a deal on spending plans that had shocked investors and stoked tensions between the country’s populist government and the rest of the EU. Valdis Dombrovskis, the EU commission vice-president responsible for the euro, said the agreement that had been reached would lead to a budget deficit next year of precisely 2.04% of GDP and not a penny less or more compared with 2.4 per cent in Rome’s original plans.

Europe’s rebound followed a weak Asian session which saw equities mostly lower after a disappointing market debut for SoftBank Group’s Japanese telecom business and amid cautious trade ahead of the FOMC rate decision, and after the attempted rebound on Wall St. where the S&P closed little above its 2018 low. Australia’s ASX 200 (-0.2%) was pressured by oil names following the mass decline in the complex, while Nikkei 225 (-0.7%) initially traded with no firm direction amid a choppy JPY before digging deeper into losses and giving up the 21,000 handle. Sentiment across the region was also reflected by the 10% plunge in Softbank’s mobile business in its USD 24bln market debut. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (-0.5%) were mixed as the former was supported by financial names with the four large banks in positive territory. Meanwhile, mainland gains in real estates and utilities were offset by the decline in the energy and healthcare sectors. Finally, JGB futures posted the biggest intraday gain since 2016 on growing concerns over the global economy health, at one point triggering an emergency margin call for JGB futures after the 10Y note future spiked as it triggered stop losses.

Futures on the S&P 500 Index erased losses made in late trading on Tuesday after earnings from FedEx cast doubt on the strength of global trade, and were trading 25 points higher from session – and 2018 – lows of 2,530.95. FedEx, considered a bellwether for the world economy, slashed its 2019 forecasts, noting “ongoing deceleration” in global growth and sending S&P futures sharply lower early in the session only for market to quickly BTFD.

Even with today’s rebound, US stocks are set for their worst December since 1931, the depths of the Great Depression.

“It’s a confluence of several important factors: the market is adjusting its outlook on growth and there is a consensus we will see a slowdown. More importantly, the market is adjusting to the idea this will translate into lower earnings growth,” said Norman Villamin, chief investment officer for private banking at Union Bancaire Privee in Zurich.

“It’s being complicated by the tightening liquidity situation with the Fed expected to move today and the ECB having signaled the end of its (stimulus)”.

Crude was mixed, trading unchanged after the biggest three-day slump since 2016 on slowing demand. Oil’s spectacular fall – down almost 10% since last Thursday – and world stocks’ plunge to 19-month lows spurred speculation the U.S. Federal Reserve might be done with tightening after its policy meeting later in the day. While WTI was unchanged at just above $46 after plunging 6 percent overnight, its 35% fall since October is sending a deflationary pulse through the world just as trade and economic activity are cooling.

Looking at today’s Fed decision, Fed Fund Futures are sticking with a two-in-three chance of a rate rise on Wednesday and Villamin expects the Fed to move twice in 2019. That’s a more hawkish call than the broader market which is pricing less than one rise in 2019, down from three not long back.

“One thing I would like to see is what people are calling a dovish hike,” Ronald Temple, head of U.S. equity and co-head of multi asset at Lazard Asset Management LLC, told Bloomberg TV. “The hiatus on trade helps as well, but I’m a bit more skeptical about how long-lasting that is.”

Beyond the Fed, trade and politics remain the dominant themes. Unless Trump and Congress reach a deal, spending authority expires for a majority of the U.S. government on Friday night. Meanwhile, Treasury Secretary Steven Mnuchin said America and China are planning to hold meetings in January to negotiate a broader trade truce.

The expectations of a Fed pause and the equity selloff sent 10-year Treasury yields to the lowest since August at 2.799 percent down 20 bps in December – while two-year yields touched a three-month trough of 2.629 percent, sliding from November’s 2.977 percent peak. Meanwhile, as noted earlier, Italian debt surged after the European Commission was said to have decided against launching a disciplinary procedure against the country over its budget.

The yield on benchmark Japanese notes slipped to within striking distance of 0% before a rapid turnaround as the surge in demand triggered a margin call.

The Bloomberg Dollar Spot Index fell a third day as traders speculated the Fed may signal Wednesday that it’s approaching a pause in its rate-hike cycle; the greenback retreated versus most of its Group-of-10 peers. The euro advanced and Italian bonds surged to take yields to the lowest in nearly three months after the nation was said to have reached a technical agreement with EU officials over its budget. The pound was steady after U.K. inflation rate slowed to a 20-month low of 2.3% y/y, in line with estimates. The Norwegian krone led gains in G-10, rebounding from a one-year low against the euro, as oil prices stabilized

In commodities, Brent (+0.1%) and WTI (+0.1%) remain in close proximity to recent lows following from yesterdays significant losses where WTI dropped by 7.3%. Prices were mostly unreactive to the surprise 3.5mln barrel build in API crude inventories, where consensus has been for a draw of over 2mln barrels. Markets will be looking to see if EIA data later in the session confirms this build or if the crude stocks consensus of -2.475mln barrels is correct; if the build is confirmed it will be the first in 3 weeks and may generate new downward price pressure.

Gold is trading relatively flat after reaching a 5-month high of USD 1251.43/oz earlier in the session, with the yellow metal continuing to benefit from a softer dollar ahead of the FOMC decision. Elsewhere, profit margins at Chinese steel mills has significantly narrowed in November as the Chinese government has removed overall winter production restriction, now allowing cities and provinces to decide output curbs based on their emissions levels.

Market Snapshot

- S&P 500 futures up 0.8% to 2,559.25

- MXAP up 0.3% to 148.27

- MXAPJ up 0.6% to 479.88

- Nikkei down 0.6% to 20,987.92

- Topix down 0.4% to 1,556.15

- Hang Seng Index up 0.2% to 25,865.39

- Shanghai Composite down 1.1% to 2,549.56

- Sensex up 0.4% to 36,506.13

- Australia S&P/ASX 200 down 0.2% to 5,580.60

- Kospi up 0.8% to 2,078.84

- STOXX Europe 600 up 0.1% to 340.95

- German 10Y yield rose 0.8 bps to 0.252%

- Euro up 0.4% to $1.1403

- Italian 10Y yield fell 2.1 bps to 2.576%

- Spanish 10Y yield fell 2.7 bps to 1.351%

- Brent Futures up 1% to $56.83/bbl

- Gold spot down 0.1% to $1,248.30

- U.S. Dollar Index down 0.2% to 96.87

Top Overnight News from Bloomberg

- The U.S. and China are planning to hold meetings in January to negotiate a broader truce in their trade war but are unlikely to have any face-to-face contact before then, according to Treasury Secretary Steven Mnuchin. READ: Xi’s defiant end to 2018 signals more U.S.-China tension ahead

- Italy’s populist government is betting the European Commission will ratify an informal budget deal on Wednesday to avoid sanctions over its spending plans

- U.K. Cabinet ministers agreed to implement “in full” plans for a no- deal break from the European Union, including 3,500 troops put on standby and 2b pounds ($2.5b) of funds made available for contingencies

- Economic jitters and surging supplies from the U.S. to Russia hammered oil again, with crude suffering its biggest decline in more than three weeks

- Japan’s exports rose 0.1% in November from a year earlier, broadly in line with estimates and reflecting a weakening pace

- Thailand’s central bank raised its benchmark interest rate for the first time since 2011, joining peers in the region in tightening monetary policy this year

- India’s rupee rallied with sovereign bonds as sliding oil prices improved the outlook for the nation’s finances and the central bank extended support via open-market debt purchases

- Citigroup Inc. faces losses of as much as $180 million on loans made to an Asian hedge fund whose foreign-exchange wagers went awry, prompting board-level discussions and a business shakeup, according to a person briefed on the matter

Asian equities were mostly lower amid cautious trade ahead of the FOMC rate decision, and after the attempted rebound

on Wall St. where the S&P closed little above its 2018 low, while the Dow Jones was supported by gains in Goldman Sachs. ASX

200 (-0.2%) was pressured by oil names following the mass decline in the complex, while Nikkei 225 (-0.7%) initially traded with no

firm direction amid a choppy JPY before digging deeper into losses and giving up the 21,000 handle. Sentiment across the region

was also reflected by the 10% plunge in Softbank’s mobile business in its USD 24bln market debut. Elsewhere, Hang Seng

(+0.2%) and Shanghai Comp. (-0.5%) were mixed as the former was supported by financial names with the four large banks in

positive territory. Meanwhile, Mainland gains in real estates and utilities were offset by the decline in the energy and healthcare

sectors. Finally, JGB futures posted the biggest intraday gain since 2016 on growing concerns over the global economy health,

while futures purchases were also exacerbated after BoJ kept 5-10yr purchases steady at JPY 430bln.

Top Asian News

- China Watchers Split on Yuan Outlook; It Comes Down to Trade

- Samsung’s 5G Network Grab Gets Boost With Huawei, ZTE Under Fire

- Third Canadian Citizen Detained in China, National Post Says

- Stocks Edge Up Before Fed Decision; Bonds Steady: Markets Wrap

Major European indices are in the green (Euro Stoxx 50 +0.5%(, with some outperformance seen in the FTSE MIB (+1.6%) with banking names such as UBI Banca (+4.0%) and Intesa Sanpaolo (+3.7%) benefitting from reports that the EU commission has accepted Italy’s 2019 budget deficit at 2.04%. Sectors are mixed with some outperformance seen in the telecom and consumer discretionary sector. Other notable movers include GlaxoSmithKline (+6.6%) in the green as they are to create a new healthcare joint venture with Pfizer estimated combined sales of GBP 9.bln. With Fresenius SE (+3.0%) following an upgraded to buy at Goldman Sachs. Whilst Natixis (-6.5%) are at the bottom of the Stoxx 600 after reporting Q4 revenue will be 10% lower than the previous year. Whilst postal names such as Royal Mail (-2.6%) and Deutsche Post (-4.5%) are down after FedEx cut their guidance.

Top European News

- Europe Loses Taste for Punishing Russia as U.S. Toughens Stance

- Italian Markets Rally as Budget Agreement Seen Reached With EU

- U.K. Unveils Post-Brexit Migrant Plan for Skilled Workers

- Electronics Retailer Ceconomy Latest Victim of Retail Crisis

In FX, the Dollar remains depressed in the run-up to the FOMC in anticipation of a dovish hike if not quite one more and done as a growing number of pundits look for the accompanying statement and guidance to be tweaked via the dot plots and/or removal of further gradual tightening. The index has duly retreated from another 97.000+ test and is holding just above recent lows ahead of 96.500, with the December base so far around 96.360 and ytd peak circa 97.710-715 the obvious bearish and bullish targets depending on the tone of the Fed.

- EUR/AUD/NZD – All vying for top G10 spot and biggest gainer vs the flagging Greenback, but with the single getting an extra lift or rather relief bid on the back of Italy and EU agreement on the 2019 budget that is likely to be officially announced by Italian PM

- Conte shortly. Eur/Usd has subsequently revisited 1.1400+ terrain, albeit just, while Aud/Usd has had another go at 0.7200 and the Kiwi is pivoting 0.6850 even though NZ current account data for Q3 was somewhat disappointing overnight. Note, decent option expiry interest may act as a drag on Eur/Usd with 1 bn at 1.1375 and the same amount between 1.1355-60 rolling off, while there is strong chart resistance ahead of 1.1450 at 1.1442 (earlier December peak) and 1.1445 (Fib).

- JPY/GBP – Also firmer vs the Usd, with the former just off a marginal new mtd high, but perhaps restricted to an extent by option related flow as 1.2 bn resides between 112.00-05 and 1.5 bn sits from 112.40-50, while for the Yen there is also the BoJ’s final policy meeting of 2018 to consider just after tonight’s FOMC. Meanwhile, Brexit continues to put a brake on the Pound, or at least temper Sterling gains as Cable crests 1.2650 and Eur/Gbp hovers around 0.9000 with little reaction to broadly in line UK inflation data or a modest beat on CBI trends that seems to have been released early.

- CAD/CHF – The marginal underperformers, with the Loonie still blighted by crude’s slump and diplomatic strains with China, but just off new ytd lows a fraction above 1.3500 ahead of Canadian CPI data, while the Franc meanders between 0.9910-35 and around 1.1300 vs the Eur.

In commodities, Brent (+0.1%) and WTI (+0.1%) remain in close proximity to recent lows, as global equity markets have begun stabilising, following on from yesterdays significant losses where WTI dropped by 7.3%. Prices were mostly unreactive to the surprise 3.5mln barrel build in API crude inventories, where consensus has been for a draw of over 2mln barrels. Markets will be looking to see if EIA data later in the session confirms this build or if the crude stocks consensus of -2.475mln barrels is correct; if the build is confirmed it will be the first in 3 weeks and may generate new downward price pressure.

Gold is trading relatively flat after reaching a 5-month high of USD 1251.43/oz earlier in the session, with the yellow metal continuing to benefit from a softer dollar ahead of the FOMC decision. Elsewhere, profit margins at Chinese steel mills has significantly narrowed in November as the Chinese government has removed overall winter production restriction, now allowing cities and provinces to decide output curbs based on their emissions levels. Saudi Finance Minister says the 2019 budget allocation to the energy industry, mining and logistics is over 3 times higher than in the previous budget.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 1.6%

- 8:30am: Current Account Balance, est. $125b deficit, prior $101.5b deficit

- 10am: Existing Home Sales, est. 5.2m, prior 5.22m; Existing Home Sales MoM, est. -0.38%, prior 1.4%

- 2pm: FOMC Rate Decision; Interest Rate on Excess Reserves, est. 2.4%, prior 2.2%

DB’s Jim Reid concludes the overnight wrap

Ahead of the Fed meeting conclusion today, yesterday had looked like we’d finally get a dull pre-Xmas session. However a sharp decline in oil prices late in the European session put pay to this. Indeed WTI and Brent tumbled -5.54% and -7.36%, respectively, sending WTI to $46.21/bbl and the lowest since August 2017. The price is also down almost 40% from the October highs just seven weeks ago. Despite the energy sector struggling (-2.35%), the S&P 500 ultimately closed flat, albeit that was after volatile intraday moves of +1.10% and -0.68%. Yesterday’s flat session at least snaps a losing streak of -3.95% over the previous two sessions, but leaving the S&P 500 still on track for its worst December since 1931. Europe struggled but in fairness was still playing catch up (or down) to the US with the STOXX 600 closing -0.82%. US HY underperformed yesterday with spreads +12bps wider. That means they are now +146bps wide of the October tights, and +88bps wider YTD. As recently as November 9th, spreads were still tighter than where they started this year.

The immediate catalyst for the oil move was the publication of Saudi Arabia’s budget plan, which included ambitious oil revenue targets of $177 billion for next year. To reach that number, the Kingdom is either assuming very unrealistic oil prices of around $80 per barrel, or they plan to pump more than the 10.2 million barrels per day target agreed earlier this month.Since the $80 per barrel figure is around 30% more than consensus estimates, the latter scenario looks more probable, which would equate to a significant increase in global supply and would end up being more bearish for prices.

Now to the Fed which starts a run of three central bank meeting outcomes over the next couple of days. Our US economists expect the Fed to raise rates for the fourth time this year (and a 20bp increase to the IOER) – which is in line with the consensus and market pricing. The more important question for our economists is what signal will the Committee send about its policy path in the coming years. They expect the message to be that the Fed remains upbeat on the outlook and expects to raise rates further in coming quarters, but that the pace of normalization is likely to slow next year from its recent quarterly rate as the Fed becomes more data dependent. Reflecting this, our colleagues expect the statement to modify the forward guidance language by noting that gradual increases remain appropriate in the “near term”. Also worth keeping an eye on is the 2019 median dot which our team expect to fall from three hikes to two. This wouldn’t impact our house view for three hikes for next year and, in fact, if the Fed signals some flexibility around the pace of hikes, while maintaining the overall trajectory for the terminal rate, it could help to ease financial conditions which in turn makes three hikes more likely next year. We’ll know more tonight with the meeting outcome due at 7pm GMT and Powell’s press conference shortly after.

Interestingly, in our yield curve note from last week (link here ) we showed how 2s10s has inverted ahead of each of the last 9 recession. However there was one false positive ahead of the 1970 recession where this measure inverted 48 months before the recession. In our view the main reason for a false positive was due to the Fed easing policy via cutting rates in late 1966/early 1967. This was despite the fact that core inflation was on the rise and accelerated more as the fed funds rate declined, and ultimately therefore can be viewed as a policy mistake given that this uptick in inflation continued into the early 1970s. Curves subsequently steepened again in 1967 once the Fed cut rates, however they inverted once more in 1968 as tightening resumed and the Fed corrected its earlier error. The recession then eventually materialised in 1970 after the second inverted YC signal worked with a more normal time lag. We mention this as there could be parallels to today if the Fed responds dovishly to the recent wobbles in markets and recent softness in inflation. This could delay a slowdown (and curve inversion) but at the expense of exacerbating pressures in the labour market and generating higher inflation further down the line. So food for thought as we hit more challenging times for the Fed.

Ahead of today’s meeting, President Trump reiterated his view that the Fed shouldn’t hike, tweeting yesterday that “I hope the people over at the Fed will read today’s Wall Street Journal Editorial before they make yet another mistake. Also don’t let the market become any more illiquid than it already is. Stop with the 50 B’s”. The “50 B’s” reference apparently referred to the balance sheet roll off caps. That tweet did little to move Treasuries with yields lower across the curve – more reflecting the oil move. 10y yields ended -3.4bps lower and the 2s10s curve finished slightly steeper at 16.8bps. It had been a similar story for Europe too where bond yields were broadly 1bp to 2bps lower. Gilts were the exception with yields up 1.6bps however there didn’t appear to be any material new Brexit newsflow from yesterday’s Cabinet meeting.

Also on the cards today is the European Commission meeting to discuss Italy’s budget. Press reports (Bloomberg) suggested that the two sides have reached an informal agreement to avoid a launch of the excessive deficit procedure. Apparently, the deal will include delays to some of the newly planned social spending and a reduction in the size of other programs. Overall the new deficit is reported to be around 2.04% and includes EUR 4bn in cuts versus the original proposal. In an effort to prove their seriousness, the government will also cut their 2019 growth forecasts to 0.9-1.0% from 1.5%. This follows news (Corriere della Sera) that the Commission was still not satisfied by the latest plan presented by the government with the sticking point being that the Commission does not see a sufficient enough reduction in the structural deficit – the important condition to avoiding an EDP. We will find out more today as to whether both sides have indeed reached an agreement.

This morning in Asia markets are continuing to trade mixed with the Nikkei (-0.57%) and Shanghai Comp (-0.25%) trading lower while the Hang Seng (+0.16%) and Kospi (+0.69%) are trading up. In overnight news, the US Treasury Secretary Steven Mnuchin said that the US and China are planning to hold meetings in January to negotiate a broader truce in their trade wars but are unlikely to have any face-to-face contact before then. It’s also worth noting that the three-day annual economic policy-setting meeting of Chinese leaders kicks off today. This could have important policy implications for 2019 and beyond so watch for any headlines. Elsewhere, futures on the S&P 500 are up +0.57% despite FedEx’s stock price being down -5.55% in aftermarket trade as the company slashed its profit forecast for the current fiscal year and decided to pare its international air-freight capacity on account of a darkening view of demand for shipping services outside the US. Interestingly, FedEx has made a U-turn on its guidance just three months after raising it, reflecting an abrupt change in FedEx’s view of the global economy and indicating that the global macroeconomic headwinds are rising.

Meanwhile, yesterday’s data didn’t add a whole lot to the growth debate. The volatile housing starts and building permits series surprised to the upside in November with the former rising +3.2% mom (vs. 0.0% expected) and the latter +5.0% mom (vs. -0.4% expected). However, the rise was concentrated in the south of the US and represented some pay-back from weakness over the last few months, as hurricanes depressed regional activity. In Germany, there was some slight disappointment in the December IFO survey with the business climate reading down 1pt to 101.0 (vs. 101.7 expected) largely due to a drop in the expectations component of 1.4pts to 97.3 (vs. 98.4 expected). That is actually the lowest expectations reading since November 2014 and it appears that the IFO survey is now finally catching up with the slide in the Germany PMIs in recent months.

Looking at the day ahead, the highlight will no doubt be the Fed this evening however prior to that this morning we get November PPI in Germany and the November inflation data docket in the UK. The December CBI trends orders and selling prices survey for the UK is also out just before lunch while in the US we get the Q3 current account balance reading and November existing home sales data. The ECB’s Hansson is also slated to speak today while the other potentially important event to note is the aforementioned European Commission meeting to discuss Italy’s budget and the potential for enforcing the excessive deficit procedure.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 27.09 POINTS OR 1.05% //Hang Sang CLOSED UP 51.14 POINTS OR 0.20% //The Nikkei closed UP 127.53 OR 0.60%/ Australia’s all ordinaires CLOSED DOWN 0.21% /Chinese yuan (ONSHORE) closed DOWN at 6.8988 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 46.52 dollars per barrel for WTI and 56.45 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED DOWN AT 6.8988AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADINGWEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

Trump will not like this: China is accused of a huge hack of thousands of European diplomatic cables

(courtesy zerohedge)

China Accused Of “Huge Hack” Of Thousands Of European Diplomatic Cables

Step side Russia: the new global hacking bogeyman is now officially China.

Just days after the US accused Beijing of hacking hundreds of millions of Marriott accounts and extracting the private data of countless Americans, even as the ongoing diplomatic feud over Chinese “intermediation” in western communications via the likes of Huawei escalates, moments ago the EU unveiled that China was now also the new Wikileaks, accusing hacker tied to China’s People’s Liberation Army of a “huge hack” of its diplomatic cables and reviving fears about vulnerabilities in the 28-country bloc’s data systems.

According to investigators, hackers had accessed cables on a variety of geopolitical issues including terrorism, transatlantic relations, peace in the Middle East, arms control, the South China Sea and the Asia and Oceania working party.

In a campaign dating back at least to 2015, the hackers gained access to more than a hundred organisations including the EU’s Coreu electronic communication network, the FT reported citing a report due to be published on Wednesday by cyber security company Area 1 Security, that exposed the breach. According to the report, Chinese hackers used the Cypriot foreign ministry as an entry point to conduct cyber espionage over several years throughout the block. Other targets included parts of the UN and the AFL-CIO, a confederation of American unions that may have been of interest to the Chinese because it was involved in trade negotiations.

The EU Council secretariat said it was “actively investigating” allegations of a “potential leak of sensitive information”. “The Council Secretariat takes the security of its facilities, including its IT systems, extremely seriously,” it added.

The revelations come as the latest embarrassment to the EU at a time of heightened concerns about the ability of groups linked to perpetual cyberwarfare bogeyman Russia and other powers to exploit weak links in its information and financial networks.

But how do we know it’s China this time and not, say, North Korea, Moscow, or some basement dwelling supporter of Julian Assange? Well, according to Oren Falkowitz, CEO of Area 1, he had “absolute confidence” that a Chinese group was behind the attacks, because of an extensive analysis of their techniques… the same way CrowdStrike had “absolute confidence” Russia hacked the DNC server without, of course, allowing the FBI to also investigate it independent. He linked the hacks to the Strategic Support Force of the People’s Liberation Army.

In a hack surprisingly reminiscent of how “the Russians” got access to John Podesta’s email, Area 1 said the hackers initially accessed the system using unsophisticated phishing techniques, sending an email with a malicious link or attachment to people inside the ministry in Cyprus.

“It only takes access to one of the parties to expose all the other secrets,” Mr Falkowitz said. “You just break the weakest link in the diplomatic chain.”

Of course, cynics may respond that this is just another convenient arrangement meant to escalate cyberwar tensions between the west and China.

The hack is the latest to involve China, whose government reached an agreement with the Obama administration in 2015 designed to curtail corporate espionage hacking companies to steal intellectual property or data, but it did not directly address more conventional cyber espionage against governments. As a trade war escalates between the US and China, the agreement is under pressure.

The thousands of hacked documents revealed concerns in the EU “about an unpredictable [President Donald] Trump administration and struggles to deal with Russia and China and the risk that Iran would revive its nuclear programme”, according to the New York Times, which also had access to the trove.

As for Cyprus being used as the entry point, that too is hardly a coincidence: the alleged use of the Mediterranean island as the “unwitting gateway” for the hack is likely to intensify some EU states’ security focus on Nicosia, after concerns about Russian money and influence there.

As the FT notes, the bloc is grappling separately to plug weaknesses in its financial supervision revealed by revelations that €200bn of suspect cash — largely from clients in Russia and other former Soviet republics — had flowed through the Estonian branch of Denmark’s Danske Bank.

China Arrests Third Canadian Citizen As Feud Worsens

That didn’t take long.

Three days after warning Canada about “escalation” and “grave consequences” amid a worsening diplomatic crisis, China has arrested a third Canadian national, according to Canada’s National Post, which cited a spokesman for Global Affairs Canada, the international arm of the Canadian government. No further details were provided, other than saying the Canadian government was “aware of a Canadian citizen” being detained.

Global Affairs diplomatically refused to connect this third arrest to the arrest of Huawei CFO Meng Wanzhou in Vancouver earlier this month. The executive, the daughter of one of China’s most successful businessmen, was released on bail last week.

According to the Straits Times, when asked about the arrest at a press briefing on Wednesday, Chinese foreign ministry spokesperson Hua Chunying said: “I have not heard about this.”

Former diplomat Michael Kovrig and businessman Michael Spavor are both being held by Chinese authorities for “threatening National Security.”

The National Post noted that China and Chinese media have lashed out at Canada over the arrest of Meng. It also confirmed that the captured Canadian isn’t a diplomat or an entrepreneur.

The arrest of a third Canadian citizen could cloud relations between the two countries, which has been marred amid an ongoing trade dispute between the United States and China.

The National Post could not confirm the identity of the detained citizen. But third-party sources who said they spoke to the family of the person suggest the person is not a diplomatic official, nor an entrepreneur operating in China.

Meng has since been released on bail and is to return to court early next year for what could be an extended legal proceeding.

The Chinese government and state-run media have lashed out against Canada for the arrest, which could dampen Prime Minster Justin Trudeau’s ambitions to launch free trade talks with the country.

The Canadian government hasn’t learned much about the whereabouts or the circumstances of the detention of Kovrig and Spavor, as Beijing has refused to elaborate on the charges facing the two men (beyond threatening national security, presumably by being Canadian) and hasn’t released any information about where they are being held. But if they haven’t gotten the message already, any Canadians lingering on the Mainland should probably take the hint: Get out.

4.EUROPEAN AFFAIRS

ITALY

Seems that our Italian friends have won out: The EU has agreed with their 2.04% budgetary deficit. The ECB will now continue with its purchase of Italian bonds as they are the only purchasers of these. Italy gets to spend and will no doubt increase its debt to GDP

(courtesy zerohedge)

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY/SYRIA/USA

The USA after stating days ago that they will be in Syria for quite some time, reversed that edict as they are now preparing for a full withdrawal of forces from Syria. Obviously they did not want to get into the cross-hairs of Turkey. Erdogan is planning a massive invasion from the North targeting the Kurds. Trump realizes this is going to be a quagmire so he is exiting

(courtesy zerohedge)

In Drastic Reversal, US Prepares “Full Withdrawal” Of Forces From Syria “Immediately”

6. GLOBAL ISSUES

CANADA/TORONTO

7 OIL ISSUES

8. EMERGING MARKETS

Venezuela

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:00

Euro/USA 1.1398 UP .0027 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES ALL GREEN

USA/JAPAN YEN 112.35 DOWN 0.169 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL

GBP/USA 1.2632 DOWN 0.0021 (Brexit March 29/ 2017/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.3447 UP .0009 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS WEDNESDAY morning in Europe, the Euro ROSE by 27 basis point, trading now ABOVE the important 1.08 level RISING to 1.1398/ Last night Shanghai composite CLOSED DOWN 27.09 POINTS OR 1.05%

//Hang Sang CLOSED UP 51.14 POINTS OR 0.20%

/AUSTRALIA CLOSED DOWN 0.21% /EUROPEAN BOURSES GREEN

The NIKKEI: this WEDNESDAY morning CLOSED DOWN 127,53 POINTS OR 0.60%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 51.14 POINTS OR 0.20%

/SHANGHAI CLOSED DOWN 27.09 POINTS OR 1.05%

Australia BOURSE CLOSED DOWN 0.21%

Nikkei (Japan) CLOSED DOWN 127.53 POINTS OR 0.60%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1247.50

silver:$14.67

Early WEDNESDAY morning USA 10 year bond yield: 2.82% !!! DOWN 0 IN POINTS from TUESDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%. (POLICY FED ERROR)/

The 30 yr bond yield 3.07 DOWN 1 IN BASIS POINTS from TUESDAY night. (POLICY FED ERROR)/

USA dollar index early WEDNESDAY morning: 96.84 DOWN 27 CENT(S) from TUESDAY’s close.

This ends early morning numbers WEDNESDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing WEDNESDAY NUMBERS \1: 00 PM

Portuguese 10 year bond yield: 1.65% UP 2 in basis point(s) yield from TUESDAY/

JAPANESE BOND YIELD: +.04% UP 1 BASIS POINTS from TUESDAY/JAPAN losing control of its yield curve/EXTREMELY VOLATILE YESTERDAY…

SPANISH 10 YR BOND YIELD: 1.38% DOWN 0 IN basis point yield from TUESDAY

ITALIAN 10 YR BOND YIELD: 2.77 DOWN 16 POINTS in basis point yield from TUESDAY/

the Italian 10 yr bond yield is trading 139 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: FALLS UP TO +.24% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.53% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR WEDNESDAY

Closing currency crosses for WEDNESDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1421 UP .0049 or 49 basis points

USA/Japan: 112.18 DOWN 0 .340 OR 34 basis points/

Great Britain/USA 1.2601 UP .0006( POUND UP 6 BASIS POINTS)

Canadian dollar UP 21 basis points to 1.3434

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed UP AT 6.8911- ON SHORE (YUAN UP)

THE USA/YUAN OFFSHORE: 6.8936( YUAN UP)

TURKISH LIRA: 5.2661

the 10 yr Japanese bond yield closed at +.04%

Your closing 10 yr USA bond yield DOWN 2 IN basis points from TUESDAY at 2.81 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 3.04 DOWN 4 in basis points on the day /

THE RISE IN BOTH THE 10 YR AND THE 30 YR ARE VERY PROBLEMATIC FOR VALUATIONS

Your closing USA dollar index, 96.68 DOWN 43 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for WEDNESDAY: 4:00 PM

London: CLOSED DOWN 64.35 POINTS OR 0.96%

German Dax : CLOSED DOWN 25.32 POINTS OR 0.24%

Paris Cac CLOSED DOWN 23.37 POINTS OR 0.49%

Spain IBEX CLOSED DOWN 92..30 POINTS OR 1.06%

Italian MIB: CLOSED DOWN: 297.05 POINTS OR 1.59%/

WTI Oil price; 47.61 1:00 pm;

Brent Oil: 57.66 1:00 EST

USA /RUSSIAN / ROUBLE CROSS: 67.61 THE CROSS HIGHER BY .19 ROUBLES/DOLLAR (ROUBLE LOWER BY 19 BASIS PTS)

USA DOLLAR VS TURKISH LIRA: 5.2661 PER ONE USA DOLLAR.

TODAY THE GERMAN YIELD FALLS +.24 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM :47.20

BRENT :56.61

USA 10 YR BOND YIELD: 2.77%…deadly..strong indicator of recession .

USA 30 YR BOND YIELD: 3.01%/.

USA: 2 YR 2.65%

EURO/USA DOLLAR CROSS: 1.1374 ( DOWN 2 BASIS POINTS)

USA/JAPANESE YEN:112.59 UP 0.077 (YEN DOWN 8 BASIS POINTS/ .

USA DOLLAR INDEX: 97.06 DOWN 7 cent(s)/

The British pound at 5 pm: Great Britain Pound/USA: 1.2615 DOWN 40 POINTS FROM YESTERDAY

the Turkish lira close: 5.2948

the Russian rouble: 67.50 down .08 Roubles against the uSA dollar.( down 8 BASIS POINTS)

Canadian dollar: 1.3497 DOWN 42 BASIS pts

USA/CHINESE YUAN (CNY) : 6.8911 (ONSHORE)

USA/CHINESE YUAN(CNH): 6.9040 (OFFSHORE)

German 10 yr bond yield at 5 pm: ,0.24%

The Dow closed DOWN 351.98 POINTS OR 1.49%

NASDAQ closed DOWN 3147.08 POINTS OR 2.17%

VOLATILITY INDEX: 24/88 CLOSED DOWN .70 ???

LIBOR 3 MONTH DURATION: 2.792% .LIBOR RATES ARE RISING/SMALL FALL TODAY

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM FOR THE DAY/WEEKLY SUMMARY/FOLLOWED BY TODAY

Powell Breaks The Market

“Everything was awesome” and then Jay Powell said…

“The balance sheet is on auto pilot, we don’t see balance sheet runoff as creating problems”

And everything broke…

Artist’s impression…

…

* * *

Overnight futures show hopeful buying –

* * *

Overnight futures show hopeful buying – “surely The Fed will deliver and capitulate… for goodness sake, someone has to rescue my FANG portfolio!!??” – But The Fed did not – cutting their rate outlook by a mere one hike, with plenty still seeing 3 hikes ahead in 2019…

And Futures collapsed…

An ugly day…

An ugly week so far…