GOLD: $1282.15 UP $3.55 (COMEX TO COMEX CLOSINGS)

Silver: $15.52 UP 10 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1284.60

silver: $15.52

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 7 NOTICE(S) FOR 700 OZ (0.0217 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 64 NOTICES FOR 6400 OZ (.1990 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

14 NOTICE(S) FILED TODAY FOR 70,000 OZ/

total number of notices filed so far this month: 116 for 580,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3785: down 11

Bitcoin: FINAL EVENING TRADE: $3850 up 54

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 2/7

DLV615-T CME CLEARING

BUSINESS DATE: 12/31/2018 DAILY DELIVERY NOTICES RUN DATE: 12/31/2018

PRODUCT GROUP: METALS RUN TIME: 20:16:38

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,278.300000000 USD

INTENT DATE: 12/31/2018 DELIVERY DATE: 01/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C MERRILL 2

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 2

661 C JP MORGAN 2

737 C ADVANTAGE 3

800 C RCG 4

____________________________________________________________________________________________

TOTAL: 7 7

MONTH TO DATE: 64

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN SMALL SIZED 1910 CONTRACTS FROM 174,249 UP TO 176,159 WITH MONDAY’S GOOD 6 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

3227 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3227 CONTRACTS. WITH THE TRANSFER OF XXX CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3227 EFP CONTRACTS TRANSLATES INTO 16.13 MILLION OZ ACCOMPANYING:

1.THE 6 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 4.935 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 3227 CONTRACTS (FOR 1 TRADING DAYS TOTAL 3227 CONTRACTS) OR 16.13 MILLION OZ: (AVERAGE PER DAY: 3227 CONTRACTS OR 16.13 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 16.13 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 16.13 MILLION OZ.

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1910 WITH THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX //MONDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 3227 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 5137 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2933 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1910 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.42 WITH RESPECT TO MONDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .881 BILLION OZ TO BE EXACT or 126% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 14 NOTICE(S) FOR 70,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 4.935 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY 3268 CONTRACTS UP TO 451,360 WITH THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $2.20//MONDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5767 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 5767 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 451,360. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5767 CONTRACTS: 3268 OI CONTRACTS INCREASED AT THE COMEX AND 2499 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 5667 CONTRACTS OR 566,700 OZ = 17.93 TONNES. AND ALL OF THIS VERY GOOD DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ MONDAY TO THE TUNE OF $2.20

MONDAY, WE HAD 5426 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 2499 CONTRACTS OR 249,900 OR 7.77 TONNES (1 TRADING DAYS AND THUS AVERAGING: 2499 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 7.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 7.77/2550 x 100% TONNES = 0.3047% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 7.77 TONNES *SURPASSED ANNUAL PROD’N

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3268 DESPITE THE LOSS IN PRICING ($2.20) THAT GOLD UNDERTOOK MONDAY) //.WE ALSO HAD A VERY GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2499 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2499 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 5767 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2499 CONTRACTS MOVE TO LONDON AND 3268 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 17.93 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH THE LOSS OF $2.20 IN MONDAY’S TRADING AT THE COMEX

we had: 7 notice(s) filed upon for 700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.35 TODAY

A GIGANTIC CHANGE IN GOLD INVENTORY AT THE GLD

A WHOPPER OF A DEPOSIT: 7.64 TONNES

THIS IS VERY GOOD FOR US/

/GLD INVENTORY 795.31 TONNES

Inventory rests tonight: 795.31 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER 6 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY

/INVENTORY RESTS AT 317.223 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1910 CONTRACTS from 174,249 UP TO 176,159 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

3227 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3227 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1910 CONTRACTS TO THE 3227 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 5,137 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.13 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 4.935 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 3227 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 28.61 PTS OR 1.15% //Hang Sang CLOSED DOWN 715.35 POINTS OR 2.77% /The Nikkei closed DOWN 62.85 PTS OR .31% / Australia’s all ordinaires CLOSED DOWN 1.47%

/Chinese yuan (ONSHORE) closed up at 6.8576 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 44.96 dollars per barrel for WTI and 53.36 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED UP AT 6.8576 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8718: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/CANADA

A Canadian, Robert Schellenberg is now facing the death penalty after his original sentence of 15 years was deemed too light. A British citizen was executed in 2009 for drug smuggling. It now looks like tensions between China and Canada are ratcheting up and this no doubt is China’s way of retribution against the arrest of Hauwei ‘s CF0 Meng

( zerohedge)

ii)Not good: China is getting more war like: a Chinese admiral wants to sink “two USA aircraft carriers” that are in the South China Sea

( zerohedge)

iii)TUESDAY NIGHT

In a landmark speech, Xi threatens violence as he wants to invade Taiwan. He demands “peaceful” reunification. The markets are not too happy with this

( zerohedge)

iv)China has a housing crisis. There are approximately 50 million apartments unoccupied. Also 22% of all China’s housing market is unoccupied and yet prices are still rising but a much slower face. This is an accident waiting to happen

4/EUROPEAN AFFAIRS

i)EU

Steve Keen is a great economist: he talks about the lousy growth rate in the Eurozone

( Steve keen)

ii)The ECB takes the unprecedented step of putting insolvent Banca Carige in administration. It is interesting that they could not find a partner for a measly 400 million euros. This deepens the Italian banking crisis

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iraq/Syria/USA

This is a game changer; Iraqi jets strike terrorists in Syria at the request of Syria’s Assad. And Iraq is a USA ally?

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

Strange events; at exactly 10’clock the price of oil rose by 2 dollars per barrel without any reason. Also it seems that two Chinese oil companies have been caught off guard with respect to losses in derivatives. The Chinese government is afraid of contagion spreading on price????

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

ii)This is is change; the Indian government is now pondering ending its hostility to gold(Press Trust of India/GATA)

iii)Very surprising: USA mint’s American eagle 2018 for gold and silver at 11 yr lows

(courtesy Reuters/gata)_

iv)Some states are now beginning to offer more sound money policies in competition to the fiat dollar

( Cortez/Mises/GATA)

v)A good history lessen as to how we knew manipulation was in the gold/silver market. Both Reg Howe and myself had shares in the BIS and these crooks confiscated our shares. Reg Howe argued our case of manipulation and not receiving fair value for our shares and we won at the Hague. However we lost on a technicality in Boston.

this is a must read…

( Chris Powell)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

USA MFG PMI plunges to a 15 month low

( zerohedge)

a)A good look at the 1.5 trillion dollar student loan sector of the USA government.

( Simon Black)

d)Trump errs; he believes that the stock market plunge was due to trade wars..the stock market is faltering due to increases in the Fed interest rates( zerohedge)

iv)SWAMP STORIES

This is quite a story. Mueller got the shock of his life when Concord, a Russian owned American enterprise showed up to defends itself against the special prosecutor. The lawyer for Concord ridicules Mueller as he is not allowed to see any evidence of their crime..

what nonsense…

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 1 CONTRACTS DOWN TO 498. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 440 CONTRACTS UP TO 142,667 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

Prepare For Global Debt Bubble Collapse – Outlook 2019

– Are we to prepare for a global Debt Bubble Collapse in 2019?

– 2019 to see the political and economic uncertainty of 2018 continue and likely to deepen

– Investors lulled into a false sense of security by politicians, brokers, bankers etc.

– Much “cheer leading” of the “economic recovery” narrative and by extension financial markets – particularly property and stock markets

– Trade wars, currency wars, Brexit, Italexit, EU contagion are real risks

– Systemic risks posed by Deutsche Bank, Italian/ Irish etc. banks and indeed nations such as Italy, UK, US and the global debt bubble

– Risk assets and property to under-perform and precious metals to outperform

– Hope for best but be prepared for the worst by increased allocations to cash and gold

In the 10th Episode of The Goldnomics Podcast Mark O’Byrne and Stephen Flood are in conversation with Dave Russell as they look forward to 2019 and discuss what might be in store for financial markets if the trends from 2018 continue.

Listen to the full episode or skip directly to one of the following discussion points:

00:57 – Mark O’Byrne: What has 2019 got in store for us and are we expecting a global debt bubble collapse?

03:41 – Stephen Flood: Rising global debt level is unsustainable and several indicators point to a potential debt bubble collapse in 2019.

05:20 – Mark O’Byrne: Interest rate outlook for the next 12 months.

08:45 – Global debt level nears a quarter of a quadrillion ($250 trillion), 320% of total world output.

10:31 – Humongous debt and associated risks: what role are central banks playing?

11:05 – The end of quantitative easing: Any implication on the stock market?

12:30 – Interest rate hike in 2019: Are big banks insulated?

13:41 – Deutsch Bank: A potential cause of another financial liquidity crisis?

17:40 – Ramifications of a no-deal Brexit.

22:32 – Stephen Flood: Will a no-deal Brexit work out well for the UK in the medium/long term?

24:27 – No-deal Brexit and Bail-Ins: Should depositors and investors be concerned?

26:30 – How likely is it that impeachment proceedings will be instituted against Donald Trump in 2019?

31:30 – How good of a strategist is Donald Trump?

32:41 – Inequality and political events in USA: A peep through the lens of The Arc of Inequality.

36:23 – Instability, inequality and The Arc of Inequality: Looking at the role of populist leaders vs. central banks.

38:17 – Instability and inequality: Looking at the role of technological advancement and oligopolists.

40:51 – Globalization and progress in the east (Asia, India and China, etc.): A cause of reduced standard of living in the western world?

41:36 – De-dollarization of the global economy likely to continue in 2019.

45:13 – US to find it more difficult to fund budget deficits in future.

46:42 – Beyond the doom and gloom: where’s the bright spots out there?

49:50 – Asset allocation: How much should be invested in gold?

51:20 – Stock market advice from “experts”: Any need to be cautious?

52:41 – The implications of recent events for silver in 2019.

55:02 – Cryptocurrency: Outlook for Bitcoin in 2019.

58:01 – Silver vs. Bitcoin, which is a better investment option?

59:14 – Potential global financial crisis in 2019: what would be the main catalyst?

Make sure you don’t miss a single episode…… Subscribe to the Goldnomics Podcasts on iTunes, Soundcloud, or YouTube: https://soundcloud.com/goldcore-381451255

YouTube.com/user/GoldCoreLimited

Follow us on social media:

GoldCore on Twitter: https://twitter.com/goldcore

GoldCore on Facebook: https://www.facebook.com/GoldCore/

GoldCore on Linkedin: https://ie.linkedin.com/company/goldcore

Visit our website at: https://www.goldcore.com

Secure Storage Ireland – Click here for information

News and Commentary

Gold settles higher as Fed lifts a key interest rate (MarketWatch.com)

Stocks Retreat on Fears of Fed Mistake; Oil Slumps: Markets Wrap (Bloomberg.com)

Asia Stock Carnage Deepens as Hopes Fizzle With Policy Updates (Bloomberg.com)

Gold steadies, Fed signals ‘some’ rate hikes for 2019 (Reuters.com)

Fed lifts rates, now sees ‘some further’ hikes ahead (Reuters.com)

Source: Bloomberg

Gold Bulls Just Regained the Upper Hand (USFunds.com)

$7.9 trillion pile of negative-yielding debt is growing fast (Bloomberg.com)

China’s holdings of U.S. Treasuries fall to lowest since May 2017 (Bloomberg.com)

Investors Should ‘Run For Cover’ – Greenspan Warns after Yellen, IMF, BIS Warnings (CNBC.com)

Alan Greenspan Warns Investors: Bad Economic Times Are Looming (Fortune.com)

Jarring FedEx Outlook Cut Suggests “Severe Global Recession” (ZeroHedge.com)

France and the Crisis of Democracies (FPCS.es)

Brexit Bulletin: The Predictions Edition (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

Prepare For Global Debt Bubble Collapse with Gold and Silver (Outlook 2019 Podcast)

– Risk assets and property to under-perform and precious metals to outperform (Outlook 2019 Podcast)

– Hope for best but be prepared for the worst by increased allocations to cash, silver and gold

– Market, economic and political uncertainty of 2018 continue and deepen

– Investors lulled into a false sense of security by politicians and assorted financial “experts2

– Much “cheer leading” of the “economic recovery” narrative and by extension markets – particularly property and stock markets

– Trade wars, currency wars, Brexit, Italexit, EU contagion are real risks in 2019

– Systemic risks posed by Deutsche Bank, Italian/ Irish etc. banks and indeed nations such as Italy, UK, US and the global debt bubble

In the 10th Episode of The Goldnomics Podcast, GoldCore Founder Mark O’Byrne and GoldCore CEO Stephen Flood talk to with Dave Russell as they look forward to 2019 and discuss what might be in store for financial markets if the trends from 2018 continue.

Listen to the full episode or skip directly to one of the following discussion points:

00:57 – What has 2019 got in store for us and might there be a a global debt bubble collapse this year?

03:41 – Rising global debt level is unsustainable and several indicators point to a potential debt bubble collapse in 2019.

05:20 – Interest rate outlook for the next 12 months.

08:45 – Global debt level nears a quarter of a quadrillion ($250 trillion), 320% of total world output.

10:31 – Humongous debt and associated risks: what role are central banks playing?

11:05 – The end of quantitative easing: Any implication on the stock market?

12:30 – Interest rate hike in 2019: Are big banks insulated?

13:41 – Deutsch Bank: A potential cause of another financial liquidity crisis?

17:40 – Ramifications of a no-deal Brexit.

22:32 – Will a no-deal Brexit work out well for the UK in the medium/long term?

24:27 – No-deal Brexit and Bail-Ins: Should depositors and investors be concerned?

26:30 – How likely is it that impeachment proceedings will be instituted against Donald Trump in 2019?

31:30 – How good of a strategist is Donald Trump?

32:41 – Inequality and political events in USA: A peep through the lens of The Arc of Inequality.

36:23 – Instability, inequality and The Arc of Inequality: Looking at the role of populist leaders vs. central banks.

38:17 – Instability and inequality: Looking at the role of technological advancement and oligopolists.

40:51 – Globalization and progress in the east (Asia, India and China, etc.): A cause of reduced standard of living in the western world?

41:36 – De-dollarization of the global economy likely to continue in 2019.

45:13 – US to find it more difficult to fund budget deficits in future.

46:42 – Beyond the doom and gloom: where’s the bright spots out there?

49:50 – Asset allocation: How much should be invested in gold?

51:20 – Stock market advice from “experts”: Any need to be cautious?

52:41 – The implications of recent events for silver in 2019.

55:02 – Cryptocurrency: Outlook for Bitcoin in 2019.

58:01 – Silver vs. Bitcoin: Silver is a better investment option?

59:14 – Potential global financial crisis in 2019: what would be the main catalyst?

YouTube.com/user/GoldCoreLimited

Follow us on social media:

GoldCore on Twitter: https://twitter.com/goldcore

GoldCore on Facebook: https://www.facebook.com/GoldCore/

GoldCore on Linkedin: https://ie.linkedin.com/company/goldcore

Visit our website at: https://www.goldcore.com

Secure Storage Ireland – Click here for information

News and Commentary

Asia Stocks Fall as China Data Hits New Year Start (Bloomberg.com)

Asian shares blindsided by dismal China data (Reuters.com)

Democrats maneuver to end shutdown, without Trump wall money (Reuters.com)

U.S. Mint’s American Eagle 2018 gold, silver coin sales at 11-year lows (Reuters.com)

U.S. Stock Futures Slide With European Shares After China Data (Bloomberg.com)

Sydney Housing Slump Deepens as Prices Drop Most Since 1980s (Bloomberg.com)

Source: Bloomberg

Here’s how ugly 2018 was for stocks and other assets (MarketWatch.com)

For the 2019 economic outlook, don’t watch the stock market, watch the Fed (MarketWatch.com)

EU’s JUNCKER WARNS THAT WAR IN EUROPE IS NOT IMPOSSIBLE (Extra.ie)

What if nobody cares about market rigging? Do you? (Gata.org)

Indian government ponders ending hostility to gold (Gata.org)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

31 Dec: USD 1,281.65, GBP 1,005.45 & EUR 1,120.03 per ounce

28 Dec: USD 1,277.25, GBP 1,009.16 & EUR 1,114.91 per ounce

27 Dec: USD 1,271.10, GBP 1,006.20 & EUR 1,115.26 per ounce

24 Dec: USD 1,261.25, GBP 996.26 & EUR 1,105.23 per ounce

21 Dec: USD 1,257.60, GBP 993.76 & EUR 1,101.53 per ounce

20 Dec: USD 1,255.00, GBP 988.69 & EUR 1,093.73 per ounce

19 Dec: USD 1,248.60, GBP 986.77 & EUR 1,094.65 per ounce

Silver Prices (LBMA)

31 Dec: USD 15.47, GBP 12.11 & EUR 13.51 per ounce

28 Dec: USD 15.30, GBP 12.05 & EUR 13.34 per ounce

27 Dec: USD 15.06, GBP 11.92 & EUR 13.22 per ounce

24 Dec: USD 14.68, GBP 11.60 & EUR 12.88 per ounce

21 Dec: USD 14.69, GBP 11.59 & EUR 12.86 per ounce

20 Dec: USD 14.77, GBP 11.64 & EUR 12.88 per ounce

19 Dec: USD 14.65, GBP 11.58 & EUR 12.84 per ounce

Recent Market Updates

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

– Everything Bubble Started Bursting In 2018 – GoldCore Video

– Global Financial System Is ‘Unstable’ and Risk Of ‘Clearing System Seizure’, BIS Warns

– Gold Flowing From West To East and Now To Goldman Sachs

– Brexit Risk Sees Gold Rise To Test EUR 1,100 Per Ounce

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

– “Fake Markets” To Lead to Global Financial Crisis? – Goldnomics Podcast

Indian government ponders ending hostility to gold

Submitted by cpowell on Tue, 2019-01-01 15:19. Section: Daily Dispatches

New Gold Policy Likely Soon; Looking at All Aspects of Yellow Metal, Commerce Minister Says

From the Press Trust of India

via MoneyControl.com, Mumbai

Thursday, December 27, 2018

The government is working on an integrated gold policy, which is expected to be released soon, to promote growth of the yellow metal industry and exports of jewellery, Commerce and Industry Minister Suresh Prabhu said.

“We are pushing for it as we need an integrated policy. In the next few days we will have a meeting of all concerned people to frame the policy on an expeditious basis. We are looking at all elements of gold in the policy,” Prabhu told PTI.

When asked whether the policy will consider the demand of the industry to cut the import duty on gold, he said: “It will also look at that side of it.”

The domestic industry has demanded a cut in the import duty on gold to 4 percent from the current 10 percent.

The minister said that there is no such policy though India is the largest consumer and importer of gold.

India has the potential to become a “good exporter of value-added gold,” he added.

The policy is likely to focus on promoting the domestic gold industry and exports of gems and jewellery, which contribute about 15 percent to total merchandise exports.

In February, Finance Minister Arun Jaitley announced formulation of a comprehensive gold policy to develop gold as an asset class.

Government think-tank Niti Aayog in August suggested that the government to bring down the import duty on gold from 10 percent and asked to slash the goods-and-services tax rate on the precious metal from the current 3 percent.

The think-tank also recommended reviewing and revamping the gold monetization and the sovereign gold bond schemes, besides setting up a gold board and bullion exchanges across the country to have greater financialization of the yellow metal. …

… For the remainder of the report:

https://www.moneycontrol.com/news/economy/policy/new-gold-policy-likely-…

end

Very surprising: USA mint’s American eagle 2018 for gold and silver at 11 yr lows

(courtesy Reuters/gata)_

U.S. Mint’s American Eagle 2018 gold, silver coin sales at 11-year lows

Submitted by cpowell on Tue, 2019-01-01 17:52. Section: Daily Dispatches

By Renita D. Young

Reuters

Monday, December 31, 2018

U.S. Mint sales of American Eagle gold and silver coins dropped to their lowest in 11 years during 2018, U.S. Mint data showed Monday, as investors favored higher-yielding assets despite global stock and bond market volatility late in the year.

Total 2018 sales of American Eagle gold coins sold by the U.S. Mint reached 245,500 ounces, the lowest on a year-over-year basis since 2007. The Mint sold 3,000 ounces of gold coins in December, 85.4 percent lower than November sales, the data showed.

Silver coin sales were 15.7 million ounces, also the lowest since 2007 on an annual basis, according to the U.S. Mint. December American Eagle silver coin sales reached 490,000 ounces, down 70.2 percent from the month prior. …

… For the remainder of the report:

https://www.reuters.com/article/us-usmint-coins/us-mint-american-eagle-2…

end

A good history lessen as to how we knew manipulation was in the gold/silver market. Both Reg Howe and myself had shares in the BIS and these crooks confiscated our shares. Reg Howe argued our case of manipulation and not receiving fair value for our shares and we won at the Hague. However we lost on a technicality in Boston.

this is a must read…

(courtesy Chris Powell)

What if nobody cares about market rigging? Do you?

Submitted by cpowell on Tue, 2019-01-01 21:12. Section: Daily Dispatches

4:21p ET Tuesday, January 1, 2019

Dear Friend of GATA and Gold:

When GATA got started in January 1999 we figured that the rigging we saw in the gold and silver markets was the work of the big investment banks that heavily traded the monetary metals on the futures exchanges. Our idea was to gather evidence of their collusion and then sue them for triple damages under the Sherman Act, the Clayton Act, and the anti-trust laws of the 50 states.

Before long we realized that the U.S. government and allied governments were heavily involved in this rigging, just they had rigged the gold market in the era of the gold standard and the London Gold Pool of the 1960s, and that these governments likely were using the investment banks as brokers for manipulative interventions. So then we aimed to sue these governments as well and we hired a major anti-trust law firm to research the prospect.

…

The advice from our lawyers was not encouraging. If the U.S. government was the main instigator of the market rigging, the lawyers said, it probably was legal under the Gold Reserve Act of 1934, which created the U.S. Treasury Department’s Exchange Stabilization Fund and authorized it to trade not just gold but anything deemed by the treasury secretary to bear on the stability of the dollar. The act authorized the fund to do such trading in secret, making it reportable only to the president.

Nevertheless, in 2000 our consultant Reginald Howe, a lawyer with a degree from Harvard, thought he saw an opportunity to get the gold manipulation issue into court. Howe happened to own shares of the Bank for International Settlements, ( and Harvey: Reg owned 6 shares and I owned 2 shares) which was moving to expropriate those of its shares that were not already owned by governments. Howe knew that the BIS owned a lot of gold and figured that, because of the gold price suppression policy of Western governments, the price being offered by the bank to acquire the privately held shares grossly undervalued them.

Howe also figured that the Gold Reserve Act’s authorization for the U.S. government to trade in gold was not necessarily also authorization for the government to manipulate markets in violation of anti-trust principles.

So with GATA’s endorsement and support, Howe sued the BIS, the Treasury Department, the Federal Reserve, and five big investment banks in U.S. District Court in Boston, accusing them of rigging the gold market and thereby devaluing his shares of the BIS:

http://goldensextant.com/BIS-PFcase.html

A single hearing was held in the case — on November 5, 2001. Your secretary/treasurer attended and reported about it in detail, finding the hearing most notable for eliciting an assertion from an assistant U.S. attorney that the U.S. government claims authority, under the Gold Reserve Act, to trade gold in a way affecting its price — that is, claims the power to rig the gold market:

Of course this was just what our anti-trust law firm had cautioned us about.

The judge evaded the Howe lawsuit’s big issues and dismissed the case on a jurisdictional technicality. (An international arbitration later concluded that Howe was right, that the BIS was paying too little for the shares it was recalling.) But no one in authority had denied the main accusation of Howe’s lawsuit, and, indeed, to the contrary, the lawsuit had compelled the U.S. government to claim, in public, the power and right to rig the gold market.

That was a huge accomplishment. But it required GATA to change tactics from trying to get anti-trust law enforced in court to simple exposure of what the U.S. government and its allies were doing.

As a result GATA began researching the longstanding and continuing policy of gold-market rigging by governments, compiling confirmations from government archives and similar sources and admissions by central bankers themselves, which now are summarized here —

http://www.gata.org/node/14839

— and detailed here:

http://www.gata.org/taxonomy/term/21

Fittingly, the BIS continues to supply a monthly statement of account that, when compared to the previous month’s statement, discloses the bank’s constant if largely surreptitious intervention in the gold market on behalf of its member central banks, an inadvertently helpful monthly contribution to GATA’s documentation file.

Once GATA amassed so much documentation, we thought that surely mainstream financial news organizations would have to address it. Strangely, it seemed, they were not eager to do so — maybe because they did not understand how gold is a determinant of currency values, interest rates, and government bond prices. So in January 2008 we published a full-page, full-color advertisement in The Wall Street Journal, having gathered $264,000 to pay for it:

http://www.gata.org/node/wallstreetjournal

The ad had been your secretary/treasurer’s idea — and it proved to be a disaster. The ad may have been noticed — at least it has been viewed more than 372,000 times at GATA’s internet site — but it drew no response at all, not even from the Journal itself, not even an invitation to the newspaper’s ad department Christmas party that year.

Of course we should have known better. That $264,000 was but a tiny fraction of what JPMorganChase and the other gold-trading investment banks representing the U.S. government spend on advertising every year in the Journal and other mainstream financial news organizations. Then there is the government’s own opposition to raising the gold issue. Some mainstream news organizations will challenge the government on smaller matters, but gold-market rigging — the primary mechanism of rigging the currency and bond markets — seems to be considered the most sensitive issue of national security.

Now and then GATA does get attention from mainstream news organizations, and we seem to have been largely responsible for alerting certain governments to the gold suppression scheme, particularly Russia’s and China’s —

— which for years have been acquiring gold in large amounts, apparently in anticipation of big changes in the world financial system:

http://www.gata.org/node/11373

Other market participants may be acting quietly on GATA’s findings.

But lately we can’t entirely dismiss a disturbing thought: What if we got our wish and the major mainstream financial news organizations, from the Financial Times to Bloomberg News to The Economist, acknowledged prominently that central banks constantly intervene in the gold market to control the monetary metal’s price and protect their own currencies and bonds, primarily through derivatives trading, thereby effectively rigging allmarkets … and nobody cared, because everybody had been corrupted by the rigging?

What if free and transparent markets, limited and accountable government, and fair dealing among peoples and nations are just cliches from a bygone era?

Anyone can understand the demoralization of the monetary metals industry in recent years. But that demoralization would be unimportant compared to demoralization about free and transparent markets and limited and accountable government, values that are the prerequisites of human progress. No mere lawsuits and courts can preserve those values; they will survive only if they live in the hearts of enough people.

If those values do live there, exposure will work eventually, and GATA believes it is on the verge of compelling government to make its most incriminating admissions yet — or its most incriminating refusals to answer.

We mean to press on nevertheless, but we can’t do it well without financial support. So if you have not yet helped us, please consider doing it now:

Even a $5 contribution will be more than GATA has received from Newmont Mining or Barrick Gold, companies that do nothing to fend off the great enemies of their investors. GATA will always do what it can, which has been and will remain far more than it ever was thought able to do.

We see dimly in the present what is small and what is great,

Slow of faith how weak an arm may turn the iron helm of fate.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8576/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8718 /shanghai bourse CLOSED DOWN 28.61 PTS OR 1.15%

HANG SANG CLOSED DOWN 715.35 POINTS OR 2.77%

2. Nikkei closed DOWN 62.85 PTS OR .31%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 96.47/Euro FALLS TO 1.1406

3b Japan 10 year bond yield: FALLS TO. +.00/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.18/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 44.96 and Brent: 53.36

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.16%/Italian 10 yr bond yield DOWN to 2.71% /SPAIN 10 YR BOND YIELD DOWN TO 1.39%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.38

3k Gold at $1284.80 silver at:15.42 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 18/100 in roubles/dollar) 69.63

3m oil into the 44 dollar handle for WTI and 53 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.18 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9856 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1237 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.16%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.65% early this morning. Thirty year rate at 2.99%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3692

Global Market Bloodbath Returns As Futures Tumble, Asia Suffers Worst Start To Year Since 2016

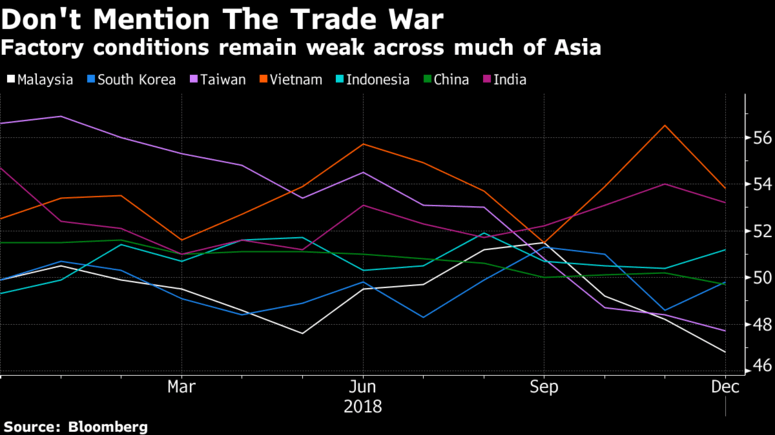

Any hope for a reversal of the ominous market trends of last year and a positive start to 2019 were quickly dashed overnight when what was originally a gain of as much as 0.6% in S&P futures early in the session was promptly extinguished as futures slumped deep in the red alongside a sea of red in global stocks, after the Caixin China PMI manufacturing survey fell into contraction territory for the first time since May 2017, sending Asian stocks tumbling to the worst start to the year since 2016, while poor PMI reports out of Europe only confirmed that the global economy is slowing.

Weak manufacturing-activity surveys across Asia were followed by disappointing numbers in the euro zone, sending MSCI’s index of world shares 0.4% lower.

“The disappointment that came through in December has transferred into January as well,” said Jingyi Pan, a Singapore-based market strategist at IG Asia Pte. While there was some small development in uncertain Washington politics, it’s a reminder of the U.S.-China trade tensions and “brings back to the surface worries on growth,” she said.

Initially, S&P500 futures rose 0.6%, after President Trump invited the top congressional leaders from both parties to a White House briefing on border security Wednesday and suggested he wants to “make a deal” to end the government shutdown. However, this initial optimism faded quickly and futures fell as much as 2.3%, down almost 70 points from session highs reaching a low of 2,452 and trading down 1.4% last, after a closely watched index of Chinese manufacturing for small and medium enterprises had its lowest reading since May 2017, confirming a prior contractionary print from the official Chinese PMI which tracks larger companies. Nasdaq 100 Index futures and those on the Dow Jones dropped 2.2 percent and 1.5 percent respectively.

The overnight mood reversal took place after the Caixin China December manufacturing PMI fell to 49.7 from 50.2 in November, below the 50 “contraction” threshold for the first time since May 2017. That followed the official gauge, which unexpectedly fell into the same zone for the first time since July 2016 on Monday.

“The trend remains lower for now,” Kyle Rodda, an analyst at IG Group Holdings Plc, told Bloomberg TV. “We’ve had rate hikes from the Fed effectively priced out, so we are looking at a situation when markets are thinking that we are entering a period of slower growth.”

It wasn’t just China: Taiwan’s Nikkei and IHS Markit manufacturing purchasing managers’ index fell to 47.7 in December from 48.4 in November, down from 56.6 a year earlier, partly due to a fall in demand for machinery and electronics goods, along with information and communications equipment, amid slowing orders for new smartphones and the simmering trade war. Malaysia’s PMI fell to 46.8 from 48.2, its lowest reading since the series began. New orders were at their weakest since May. South Korea’s PMI remained in contractionary territory for the second consecutive month even as the overall reading nudged higher. Vietnam’s PMI fell to 53.8, while the Philippines PMI fell to 53.2.

“The PMIs are signaling trouble ahead,” said Hak Bin Chua, an economist at Maybank Kim Eng Research. “There have been some healthy trade numbers in some countries, but this is probably short-lived.”

As a result, the benchmark gauge of Asia-Pacific stocks excluding Japan slumped 1.9 percent as traders returned to work in key regions including Hong Kong, China, Taiwan and Korea. Japan markets are closed and reopen on Jan. 4. Wednesday’s plunge, which is the worst start to the year since 2016 was largely the result of the abovementioned plunge in the Chinese Caixin PMI.

“Asian markets took a deep dive into negative territory following another disappointing China Caixin manufacturing PMI reading,” said Margaret Yang, market analyst at CMC Markets, in a note to clients. “China manufacturing PMI is falling at a pace faster than economists’ forecast, suggesting global economic slowdown and trade war is hurting the country’s manufacturing activities.”

Chinese H shares lost 2.8% and Shanghai Composite dropped 1.3% after Caixin manufacturing PMI signals contraction for the first time since May 2017. S&P futures reverse early rally to trade 0.8% weaker; MSCI Asia Pacific index falls 0.9% with Japan and New Zealand markets closed for New Year holidays.

Understandably, U.S.-listed China stocks were among the biggest decliners in Wednesday’s pre-market trading as the iShares China Large-Cap ETF fell 2.5% to its lowest since October before paring the decline; the iShares MSCI Emerging Market ETF fell 1.4%. Stocks trading lower included NIO -4.6%, BiliBili -3.4%, Huya -3.1%, Pinduoduo -2.8%, Tencent Music -2.8%, iQIYI -2.2%, Alibaba -1.8%, Qudian -1.6%, Momo -1.3%

Adding to global growth concerns, Singapore’s export-reliant economy grew only 1.6% in the 4th quarter, down sharply from a revised 3.5% previously, and far below the 3.6% expected print.

The Asian gloom continued in Europe, where stocks also dropped with the Stoxx Europe 600 index trading 0.8% lower, dragged by growth sensitive sectors such as basic resources and autos. Banks and insurers were among the laggards after Europe’s PMI readings confirmed the weakness reported earlier in China, with Italy contracting, while France’s survey signaled activity shrank for the first time since late 2016. The euro-zone reading reached its lowest since February 2016. Future output PMIs were at a six-year low.

IHS Markit PMI™@IHSMarkitPMI#Eurozone Manufacturing #PMI at 51.4 in December. New work declines for third month running; business sentiment hits fresh six-year low. Italy remained in contraction territory and was also joined by France http://ihsmark.it/OfDm50k55pO

There were also renewed fears in Europe over the clean-up of Italy’s banks, with trading in shares of Banca Carige suspended. Carige failed last month to win shareholder backing for a share issue that was part of a rescue plan. An index of Italian bank shares fell 2.5 percent.

“It’s a continuation of the worries over growth. You can see them in the Asian numbers, which all confirm that we have passed peak growth levels,” said Tim Graf, chief macro strategist at State Street Global Advisors. The knock-on effects from China’s slowdown and global trade tensions were rippling across Asia and Europe, he said. “I don’t think the trade story goes away, and Europe, being an open economy, is still vulnerable,” Graf said.

The data suggests there will be no respite for equities or commodities after the losses of 2018, with “Doctor” Copper, a key gauge of world growth sentiment, falling to 3 1/2-month lows , while Brent crude futures fell 1 percent after losing 19.5 percent in 2018

Commodity-driven currencies also lost ground, led by the Australian dollar. Often used as a proxy for China sentiment, the Aussie fell as much as 0.7 percent to its lowest since February 2016 at $0.70015.

Meanwhile, the continuation of the stock market rout again drove investors into the safety of bonds. The 10-year German Bund yield slumped to 20-month lows of 0.18 percent, its biggest one-day fall in two years, while the US 10Y yield dropped below 2.65%, the lowest level since January 2018.

2Y TSY yields were 2.49% , just barely above the cash rate, from a peak of 2.977% in November. The spread between two- and 10-year yields has in turn shrunk to the smallest since 2007, a flattening that has been a portent of recessions in the past. The German 2-10 yield curve is the flattest since November 2016.

Gold and the yen were the other beneficiaries, with the Japanese currency – the best performer of 2018 – continuing its outperformance in 2019 – and while gold topped six-month highs, the yen extended its rally against the dollar to seven-month highs around 108.9. It strengthened to a 19-month peak against the euro.

“Traditional safe-haven type flows are going into the yen. As we see increased volatility (on world markets), the Japanese (investors) are probably repatriatriating foreign assets,” said Charles St Arnaud, senior investment strategist at Lombard Odier Investment Managers.

Meanwhile, after some early weakness, the dollar inched up against a basket of currencies with the Bloomberg dollar index rising to session highs, just above 1197. The greenback has come under pressure from a fall in U.S. Treasury yields as investors wager the Federal Reserve will not raise rates again. While the Fed itself still projects at least two more hikes, money markets now imply a quarter-point cut by mid-2020.

Fed Chairman Jerome Powell may comment on the outlook when he takes part in a discussion with former Fed chairs Janet Yellen and Ben Bernanke on Friday, while the manufacturing survey and the December payrolls report should shed more light when they emerge on Thursday and Friday respectively.

“What is clear is that the global synchronized growth story that propelled risk assets higher has come to the end of its current run,” OCBC Bank told clients. “Inexorably flattening yield curves … have poured cold water on further policy normalization going ahead.”

Market Snapshot

- S&P 500 futures down 1.5% to 2,468.25

- STOXX Europe 600 down 1.1% to 334.12

- MXAP down 0.9% to 145.48

- MXAPJ down 1.8% to 468.48

- Nikkei down 0.3% to 20,014.77

- Topix down 0.5% to 1,494.09

- Hang Seng Index down 2.8% to 25,130.35

- Shanghai Composite down 1.2% to 2,465.29

- Sensex down 0.8% to 35,950.08

- Australia S&P/ASX 200 down 1.6% to 5,557.76

- Kospi down 1.5% to 2,010.00

- German 10Y yield fell 6.3 bps to 0.179%

- Euro down 0.2% to $1.1438

- Italian 10Y yield unchanged at 2.384%

- Spanish 10Y yield fell 0.9 bps to 1.407%

- Brent Futures down 1.4% to $53.05/bbl

- Gold spot up 0.4% to $1,288.01

- U.S. Dollar Index up 0.1% to 96.18

Top Overnight News from Bloomberg

- Factory conditions across some of Asia’s most export-oriented economies slumped in December, hit by the U.S.-China trade war and a fading technology boom.

- In China, the Caixin Media and IHS Markit PMI fell to 49.7 from 50.2, its lowest reading since May 2017. That confirms a trend seen in the official PMI on Monday, which showed a drop to 49.4 in December, the weakest since early 2016

- U.S. stock-index futures erased earlier gains after Caixin PMI dropped into contraction territory, fueling global growth concerns

- President Donald Trump invited the top congressional leaders from both parties to a White House briefing on border security Wednesday and suggested he wants to “make a deal” to end the government shutdown

- President Sergio Mattarella, who has sought to rein in Italy’s populist leaders, took the government to task for ramming spending plans through parliament and warned that the country’s debt mountain penalizes ordinary citizens

- The lackluster demand for Asian dollar bonds is likely to recover as investors who shunned weaker quality notes during the turbulent final quarter of 2018 now see them as too cheap to ignore. Asia dollar bond sales may total $250 billion to $300 billion in 2019, according to a Bloomberg survey

- Yen rises versus all major peers after China’s Caixin manufacturing PMI fell into contraction territory, adding to the weight of other data signaling a slowing Chinese economy and driving demand for haven assets. Aussie leads declines against the dollar, nearing a 70 cents psychological level.

- The European Central Bank took the unprecedented step of placing the cash-strapped Italian lender Banca Carige SpA in temporary administration, a move that could be a prelude to a sale or merger.

Stocks in developing nations fell the most in three weeks as new evidence of slowing Chinese growth compounded investor fears about prospects for the global economy. A closely watched manufacturing gauge in China had its lowest reading since May 2017 amid ongoing trade tensions with America. MSCI’s gauge of stocks slumped after closing out 2017 with four straight days of gains, with shares in Johannesburg tumbling more than three percent. Most emerging-market currencies weakened against the dollar led by Turkey’s lira, while the zloty extended losses versus the euro after Poland’s manufacturing PMI dropped to its lowest mark since 2013. “The disappointment that came through in December has transferred into January as well,” said Jingyi Pan, a Singapore-based market strategist at IG Asia Pte. Political developments in Washington served as a reminder of the U.S.-China trade tensions and brought “back to the surface worries on growth,” she said.

Top Asian News

- China Leads Slump in Asia Factories as Trade War Cools Demand

- Singapore’s Export-Reliant Economy Ends 2018 With Slower Growth

- China’s Xi Seeks Talks to Unify Taiwan With Mainland

- Asia’s Stocks Post Worst Start to Year Since 2016: Blame China

Major European Indices [Euro Stoxx 50 -0.4%] are in the red following on from the poor performance seen in Aisa. (Of note the SMI remains closed due to Berchtold’s day). The CAC (-1.4%) is underperforming its peers with index heavyweight Renault (-3.2%) towards the bottom of the index as the Co’s Renault-Samsung Motors division reported a significant decrease in year-on-year sales for December; in addition, the political situation remains fraught in France. Sectors are also in the red, with some underperformance seen in materials and energy names due to Chinese Manufacturing PMI showing a contraction, and oil prices in the red due to continued oversupply concerns respectively.

Top European News

- Italian Populist Di Maio Promises to Cut Pay for Lawmakers

- Italian Manufacturing Shrinks Again as Nation Nears Recession

- European Banks Stock Drops as Banca Carige Gets Administrators

- German Telecom Companies Sue Regulator Over 5G Auction Rules

In FX, DXY entered the EU session on the backfoot with losses of around 0.3% and below the 96.00 level with JPY out-muscling the greenback during Asia-Pac trade as USD/JPY hit a 7-month low.

- JPY strength was largely driven by the broader risk environment as disappointing Chinese data overnight and the ongoing US government shutdown remain a key focus for investors. As the European session progressed, USD made a resurgence against its peers (ex-JPY) as losses in European equities accelerated following the cash open; DXY reclaimed 96.00 to the upside and trades relatively unchanged.

- EUR/USD eventually fell victim to the recovery in the USD (after testing 1.1500 to the upside during Asia-Pac trade) as the pair slipped below 1.1450 with some analysts also suggesting EUR/JPY selling as a potential catalyst for the move. As such, the pair has drifted towards 675mln of option expiries between 1.1452-30 with this morning’s PMI metrics from the Eurozone unable to spur much in the way of noteworthy price action with core readings unrevised from their prior’s.

- For GBP/USD, the pair began the session on the backfoot and slipped back below 1.2700 despite a high print of 1.2774 seen during Asia-Pac hours. Brexit-related commentary has been relatively light thus far with Parliament not returning from their winter break until 7th Jan. As such, the most interesting development for UK assets today has been the latest manufacturing PMI print which came in at 54.2 vs. Exp. 52.5 (Prev. 53.1). Cable briefly reclaimed 1.2700 to the upside before reversing gains with a pick-up in new orders largely attributed to stock-piling ahead of Brexit.

- AUD/USD fell victim to the disappointing Chinese data overnight which saw Caixin mfg PMI slip into contractionary territory for the first time in 19 months. Losses were also spurred on by the aforementioned pick-up in USD, however, the pair maintains its status on a 0.7000 handle with option-related bids ahead of the key level said to have stopped the rot in the pair.

In commodities, Brent (-1.0%) and WTI (-1.0%) prices are down due to oversupply concerns as US output continues to increase, with US output reaching an all-time high of 11.5mln BPD in October and Russia’s December production of 11.45mln BPD vs. Prev. 11.37mln BPD. Prices are additionally weighed on by signs of a economic slowdown in China, with a Reuters survey of analysts forecasting 2019 average Brent prices at just over USD 69 a barrel; a drop of over USD 5 compared with the previous projection. UAE Energy Minister Mazrouei says that in light of the agreed OPEC+ production cut he is optimistic that oil market balance can be achieved in the first quarter of 2019. Gold (+0.4%) is in the green due to dollar weakness albeit just off of USD 1287.39/oz a 6-month high which was reached earlier in the session. Elsewhere, copper prices have moved lower as Chinese Manufacturing PMI has fallen into a contraction for the first time in 19 months.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 53.9, prior 53.9

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 28.61 PTS OR 1.15% //Hang Sang CLOSED DOWN 715.35 POINTS OR 2.77% /The Nikkei closed DOWN 62.85 PTS OR .31% / Australia’s all ordinaires CLOSED DOWN 1.47%

/Chinese yuan (ONSHORE) closed up at 6.8576 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 44.96 dollars per barrel for WTI and 53.36 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED UP AT 6.8576 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8718: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

Monday night

A Canadian, Robert Schellenberg is now facing the death penalty after his original sentence of 15 years was deemed too light. A British citizen was executed in 2009 for drug smuggling. It now looks like tensions between China and Canada are ratcheting up and this no doubt is China’s way of retribution against the arrest of Hauwei ‘s CF0 Meng

(courtesy zerohedge)

Canadian Facing Death Penalty For Drug Smuggling As China Orders Retrial

A Chinese court has ordered a retrial for a Canadian national accused of smuggling “an enormous amount of drugs” into the Communist nation, arguing that his initial sentence of 15 years imprisonment followed by immediate deportation was too light.

The sentence, which had not been previously reported, was apparently handed down on Nov. 20. But at a hearing on Saturday, the Canadian citizen, Robert Schellenberg, prosecutors accused him of playing a key role in a major drug smuggling operation and argued that his sentence was far too light, according to Reuters.

The Associated Press reported that few details about Schellenberg’s case have been released.

Robert Lloyd Schellenberg was tried in 2016 but his case has been publicized by the Chinese press following the Dec. 1 arrest of the chief financial officer of tech giant Huawei on U.S. charges related to trading with Iran.

Drug offenses are typically punished severely in China, and drug smuggling offenses are often met with the death penalty – as in the case of a British national who was put to death in 2009 for smuggling more than 4,000 grams of heroin into the country. The initial sentence was handed down by the high court in Dalian, the top court in the northeastern province of Laioning.

The Canadian government said it has been offering consular support to Schellenberg in the case, and that it has also been in contact with Chinese officials. Canadian diplomats were at the court when the retrial was ordered. Canada has been following the case for several years, but said it couldn’t offer any more details citing privacy concerns.

Though some fear that a retrial could heighten tensions between China and Canada after China detained two Canadians on charges of endangering national security, Ottawa celebrated a decision by Beijing to release a third Canadian who had been detained for allegedly working illegally in the country. China said her deportation would be counted as an “administrative punishment.”

In one development that could lessen tensions, a Canadian government spokesman said on Friday that a Canadian citizen who was detained in China this month had returned to Canada after being released from custody.

The spokesman did not specify when the Canadian was released or returned to Canada. Earlier in the day, broadcaster CBC identified the citizen as teacher Sarah McIver.

China’s Foreign Ministry said this month that McIver was undergoing “administrative punishment” for working illegally.

McIver was the third Canadian to be detained by China following the Dec. 1 arrest in Vancouver of Meng Wanzhou, chief financial officer of the Chinese telecommunications giant Huawei Technologies Co Ltd [HWT.UL], but a Canadian official said there was no reason to believe that the woman’s detention was linked to the earlier arrests.

Foreign Minister Chrystia Freeland didn’t mention the woman last week when she demanded that Beijing release the detained Canadians, though she did reveal that the former diplomat and businessman currently in custody in Beijing had only been allowed one visit with consular officials.

Beijing is still seething over Canada’s decision to arrest Huawei CFO Meng Wanzhou at the behest of the US. She is now out on bail as she awaits extradition. Should Schellenberger face the death penalty, it would likely ratchet up tensions between Ottawa and Beijing, which has threatened “escalation” in its ongoing diplomatic dispute with Canada.

end

Not good: China is getting more war like: a Chinese admiral wants to sink “two USA aircraft carriers” that are in the South China Sea

(courtesy zerohedge)

Chinese Admiral Wants To “Sink Two US Aircraft Carriers” Over South China Sea

Mere days after Chinese President Xi Jinping vowed to “resolutely” defend China’s security interest – a veiled reference to maintaining its domination of the South China Sea – News.au has published details from a speech delivered two weeks ago by one of China’s leading military commanders where he outlined a strategy to rebuff the US Navy should it take an even more interventionist posture within the nine-dash line.

Rear Admiral Lou Yuan told an audience in Shenzhen that the simmering dispute over the East and South China Seas could be decisively ended by sinking two US aircraft carriers.

Taiwan’s Central News Agency reported that Admiral Lou gave a long speech on the state of Sino-US relations, where he declared that the trade spat was “definitely not simply friction over economics and trade,” but a “prime strategic issue.” And that if China wants the US to back off, it must be willing to attack US ships when they intrude in Chinese territory.

During the Dec. 20 speech to the 2018 Military Industry List summit, Lou declared that China’s anti-ship ballistic and cruise missiles were capable of hitting US carriers, even when they were in the middle of a “bubble” of defensive escorts.

“What the United States fears the most is taking casualties,” Admiral Lou declared.

He said the loss of one super carrier would cost the US the lives of 5000 service men and women. Sinking two would double that toll.

“We’ll see how frightened America is.”

Lou also explained what he described as the US’s five vulnerabilities, and insisted that China must not hesitate to strike back at any of them should a US fleet even dare to stop in Taiwan.

In his speech, he said there were ‘five cornerstones of the United States’ open to exploitation: their military, their money, their talent, their voting system — and their fear of adversaries.

Admiral Lou, who holds an academic military rank – not a service role – said China should “use its strength to attack the enemy’s shortcomings. Attack wherever the enemy is afraid of being hit. Wherever the enemy is weak …”

“If the US naval fleet dares to stop in Taiwan, it is time for the People’s Liberation Army to deploy troops to promote national unity on (invade) the island,” Admiral Lou said.

Should Taiwan become increasingly restive, China possesses the capability to stage a military takeover of the island in 100 hours, Lou said. This eventuality is more likely than many might believe, Lou said, adding that 2018 could be a “year of turmoil” for Taiwan, and that a military conflict was possible.

“Achieving China’s complete unity is a necessary requirement. The achievement of the past 40 years of reform and opening-up has given us the capability and confidence to safeguard our sovereignty. Those who are trying to stir up trouble in the South China Sea and Taiwan should be careful about their future.”

“The PLA is capable of taking over Taiwan within 100 hours with only a few dozen casualties,” said retired lieutenant general Wang Hongguang.

“2018 is a year of turmoil for Taiwan, and a possible military conflict may take place in Taiwan soon. (But) As long as the US doesn’t attack China-built islands and reefs in the South China Sea, no war will take place in the area.”

US military commanders have long warned that China’s growing military presence in the Pacific is a serious threat to US security, and China has underscored these concerns by organizing military drills explicitly to threaten Taiwan. Indeed, a military conflict with China remains one of the most widely cited “black swan” risks to global security – a possibility that has only been exacerbated by the trade conflict.

end

TUESDAY NIGHT

In a landmark speech, Xi threatens violence as he wants to invade Taiwan. He demands “peaceful” reunification. The markets are not too happy with this

(courtesy zerohedge)

In Landmark Speech, Xi Threatens Violence Against Taiwan, Demands ‘Peaceful Reunification’

With trade talks between the US an China finally ramping up, reviving hopes that a deal might end a slump in global equity markets that has carried into the New Year, one would think ‘Taiwan’ would be the last word any investor wanted to hear. But we’ve been hearing it with an alarming frequency lately. From a belligerent Chinese admiral and from President Xi Jinping.

And in a Wednesday speech to commemorate the fortieth anniversary of a landmark shift in China’s Taiwan policy, President Xi offered a vision of the future relationship between China and Taiwan that blatantly contradicts what Taiwan wants for itself – which is, more autonomy, if not outright independence, as the ruling pro-independence party has repeatedly insisted.

Instead, Xi insisted during his speech that China reserves the right to use force to bring Taiwan to heel – but that peaceful “reunification” would be Beijing’s goal. Xi has made resolving the “Taiwan issue” a priority.

Here’s Reuters:

China reserves the right to use force to bring Taiwan under its control but will strive to achieve peaceful “reunification” with the self-ruled island that has a bright future under any future Chinese rule, President Xi Jinping said on Wednesday.

Taiwan is China’s most sensitive issue and is claimed by Beijing as its sacred territory. Xi has stepped up pressure on the democratic island since Tsai Ing-wen from the pro-independence Democratic Progressive Party became president in 2016.

Tsai rejected Xi’s call and instead urged China to embrace democracy.

Xi has set great personal store in resolving what the Communist Party calls the “Taiwan issue,” holding a landmark meeting with then Taiwan president Ma Ying-jeou in Singapore in late 2015, just before Tsai was elected.

Xi argued during his speech that the “one country, two systems” model of governing Hong Kong would be ideal for Taiwan (something that the people of Taiwan vehemently oppose). Xi told the audience, which included Taiwanese business people, that independence for Taiwan would be “a disaster”.

Xi spoke at Beijing’s Great Hall of the People on the 40th anniversary of a landmark Taiwan policy statement.