GOLD: $1292.80 UP $10.65 (COMEX TO COMEX CLOSINGS)

Silver: $15.74 UP 22 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1294.10

silver: $15.74

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.0031 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 65 NOTICES FOR 6500 OZ (.2021 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

40 NOTICE(S) FILED TODAY FOR 200,000 OZ/

total number of notices filed so far this month: 156 for 780,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3800: down 58

Bitcoin: FINAL EVENING TRADE: $3768 down 92

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 1/1

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,281.000000000 USD

INTENT DATE: 01/02/2019 DELIVERY DATE: 01/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

737 C ADVANTAGE 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 65

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN STRONG SIZED 5,094 CONTRACTS FROM 176,159 UP TO 181,253 WITH YESTERDAY’S GOOD 10 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2242 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2242 CONTRACTS. WITH THE TRANSFER OF 2242 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2242 EFP CONTRACTS TRANSLATES INTO 11.21 MILLION OZ ACCOMPANYING:

1.THE 10 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 4.945 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 5469 CONTRACTS (FOR 2 TRADING DAYS TOTAL 5469 CONTRACTS) OR 27.35 MILLION OZ: (AVERAGE PER DAY: 2734 CONTRACTS OR 13.67 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF DEC: 27.45 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.92% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 27.34 MILLION OZ.

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5094 WITH THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX //MONDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2242 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 7336 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2242 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 5094 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.52 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .881 BILLION OZ TO BE EXACT or 126% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 40 NOTICE(S) FOR 200,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 4.945 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY 1216 CONTRACTS UP TO 452,576 WITH THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $3.35//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A huge SIZED 10,297 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 10,297 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 452,576. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,513 CONTRACTS: 1216 OI CONTRACTS INCREASED AT THE COMEX AND 10,297 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,513 CONTRACTS OR 1,151,300 OZ = 35.81 TONNES. AND ALL OF THIS VERY GOOD DEMAND OCCURRED WITH A GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.35

YESTERDAY, WE HAD 2499 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 12,796 CONTRACTS OR 1,279,600 OZ OR 39.80 TONNES (2 TRADING DAYS AND THUS AVERAGING: 6398 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 39.80 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 39.80/2550 x 100% TONNES = 1.56% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 39.80 TONNES *SURPASSED ANNUAL PROD’N

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 1216 WITH THE GAIN IN PRICING ($3.35) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,297 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,297 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS GAIN OF 11,513 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,297 CONTRACTS MOVE TO LONDON AND 1216 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 35.81 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH THE GAIN OF $3.35 IN YESTERDAY’S TRADING AT THE COMEX

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $10.65 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 795.31 TONNES

Inventory rests tonight: 795.31 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 22 CENTS TODAY:

A SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 118,000 OZ AND THIS NO DOUBT IS TO PAY FOR FEES

/INVENTORY RESTS AT 317.108 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 5094 CONTRACTS from 176,159 UP TO 181,253 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2242 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3227 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 5094 CONTRACTS TO THE 2242 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 7336 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 36.68 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 4.945 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 10 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 2242 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 0.93 PTS OR 0.04% //Hang Sang CLOSED DOWN 65.99 POINTS OR 0.26% /The Nikkei closed HOLIDAY / Australia’s all ordinaires CLOSED UP 1.23%

/Chinese yuan (ONSHORE) closed DOWN at 6.8745AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 46.46 dollars per barrel for WTI and 55.47 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED DOWN AT 6.8745 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8870: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/TAIWAN

Taiwan will never accept reunification with Beijing..this message uttered by its President

( zerohedge)

4/EUROPEAN AFFAIRS

i)EU

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Syria/USA

Trump backtracks a little on leaving Syria as he does not want to expose the Kurds to an invading Turkey. He states that they will leave “over a period of time”

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

We have been outlining to you the big discovery of gas surrounding Israel and Cyprus. Egypt has also discovered gas in their region. Major companies are now looking for more natural gas and if found, this could be a major support for Europe. Right now it is too expensive(7 billion dollars) to carry out the construction of the EastMed Pipeline which would run under the Mediterranean and end up in Italy. The weakest partner in this endeavour is Cyprus. On top of costs, they also have to worry about Turkey who may attack Cyprus to bet its gas.

( Katona/OilPrice.com)

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

ii)Craig is correct: the economic and political conditions now resemble 2010.(courtesy Craig Hemke/Sprott/GATA)

iii)Quite a commentary. Ambrose Evans Pritchard describes in detail how the euro has failed and how its threatens democracy in the region. He believes that the Euro should be abolished and each country should go back to its former currency

( Ambrose Evans Pritchard/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)Two important points here:

i)initial jobless claims jump by 10,000 from 221,000 up to 231,000

ii) Challenger report on layoffs..the highest since 2015 at 43,884 for December with construction layoffs at 8800

without a doubt the economy is faltering..

(courtesy zerohedge)

c)First Apple and now Ford. Apple stopped reporting monthly sales and this has been followed by Ford. They just reported a huge plunge in monthly sales of 9%(courtesy zerohedge)

a)EARLY LAST NIGHT:

Initially last night, apple plunges 8% after cutting Q! revenue. They blame China.

This causes massive flash crashes. The Swiss franc is probably in danger due to the huge amount of stock in Apple owned by the Swiss Government

( zerohedge)

a i)Early this morning

Apple Now down 9%

( zerohedge)

b)Trump correctly states that billions of dollars have been collected due to the tariffs. The actual number is 5 billion dollars and that is just enough to pay for the wall. The problem with tariffs is that it is very inflationary and the added costs must be paid by the consumer

( zerohedge)

c)The Dallas Fed probably has the strongest sector in the USA economy. Its Fed President Kaplan has just set a new message to Powell: “Wait a couple of quarters before hiking. I do not think that Powell will listen.

( zerohedge)

d)We knew that this was coming: The uSA issues a China travel advisory warning of an

He notes that the euro dollar curve outward is now inverted. Eurodollar bets in the future are nothing but a bet on interest rates in the future. In essence it is a future bet on libor. The total notional bet on the eurodollar curve is 11 trillion dollars. In total, these bets mean something, and much more than what Powell believes

a must read…

(courtesy Jeffrey Snider)

f)Yesterday, we brought to you one reason why the Republicans must settle the partial government shutdown by Feb 1: the food/stamp program is run by the agricultural dept and they run out of funds on the 29th of January. Here is the second reason why it must be settled:

iv)SWAMP STORIES

a)We now know that the famous dinner with Putin, vindicates Michael Flynn of treasonous behaviour. He was nothing but a patriot.

(courtesy zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 17 CONTRACTS DOWN TO 481. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 5185 CONTRACTS UP TO 147,723 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

Gold Hedges Stock Market Falls In 2018 Gaining 2.7% In Euros and 3.8% In Pounds

– Gold acts as hedge in 2018 – up 2.7% and 3.8% in euros and pounds (see tables & charts)

– Stocks fall sharply – S&P500, FTSE & Euro Stoxx 5o fall 6.25%, 12.5% & 15% respectively

– Worst year for most international equity indices since 2008

– Sharp falls in economically sensitive commodities: oil (WTI), gasoline and lumber down 24.2%, 27% & 23.8% respectively

– Volatility surges as seen in VIX rising over 110%

– Volatility continues in 2019 as stocks globally fall with Apple falling 8% overnight

– Gold and silver likely to outperform risk assets again in 2019 (see Outlook 2019 Podcast)

Asset performance in 2018 (Finviz.com)

Gold performance in major currencies 2003 to 2018 (Goldprice.org)

Gold in USD In 2018 (GoldCore)

Gold in EUR In 2018 (GoldCore)

Gold in GBP In 2018 (GoldCore)

Silver performance in major currencies 2003 to 2018 (Goldprice.org)

News and Commentary

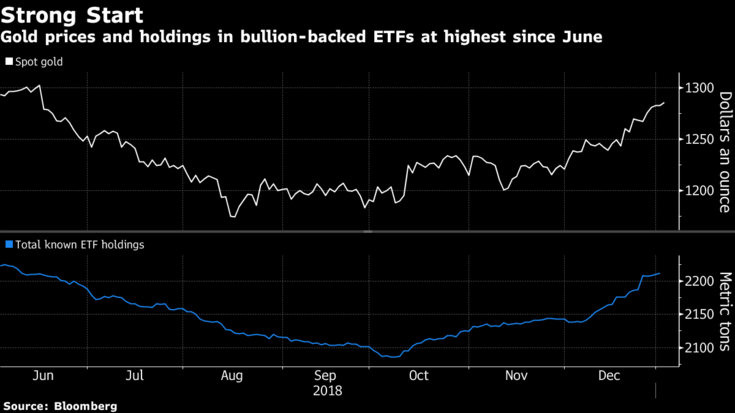

Gold futures settle at highest since June (MarketWatch.com)

Gold Opens 2019 With Fanfare as Warning Signs Flash on Growth (Bloomberg.com)

Gold gains on global growth fears, falling Asian stocks (Reuters.com)

Brexit ‘bad or awful’ for prospects in 2019, say economists (FT.com)

Source: Bloomberg

Systematic investment in gold a good option for a likely volatile 2019 (Business-Standard.com)

The euro has failed, threatens democracy, and should be abolished (Telegraph.co.uk)

ECB Takes “Unprecedented” Step Of Putting Italy’s Banca Carige In Administration (ZeroHedge.com)

2019: It Is Going To Be Much Worse Than You Think… (ZeroHedge.com)

2018 was a bad year for investors, for pretty obvious reasons (MoneyWeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

02 Jan: USD 1,287.20, GBP 1,014.44 & EUR 1,125.27 per ounce

31 Dec: USD 1,281.65, GBP 1,005.45 & EUR 1,120.03 per ounce

28 Dec: USD 1,277.25, GBP 1,009.16 & EUR 1,114.91 per ounce

27 Dec: USD 1,271.10, GBP 1,006.20 & EUR 1,115.26 per ounce

24 Dec: USD 1,261.25, GBP 996.26 & EUR 1,105.23 per ounce

21 Dec: USD 1,257.60, GBP 993.76 & EUR 1,101.53 per ounce

Silver Prices (LBMA)

02 Jan: USD 15.44, GBP 12.19 & EUR 13.51 per ounce

31 Dec: USD 15.47, GBP 12.11 & EUR 13.51 per ounce

28 Dec: USD 15.30, GBP 12.05 & EUR 13.34 per ounce

27 Dec: USD 15.06, GBP 11.92 & EUR 13.22 per ounce

24 Dec: USD 14.68, GBP 11.60 & EUR 12.88 per ounce

21 Dec: USD 14.69, GBP 11.59 & EUR 12.86 per ounce

Recent Market Updates

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

– Everything Bubble Started Bursting In 2018 – GoldCore Video

– Global Financial System Is ‘Unstable’ and Risk Of ‘Clearing System Seizure’, BIS Warns

– Gold Flowing From West To East and Now To Goldman Sachs

– Brexit Risk Sees Gold Rise To Test EUR 1,100 Per Ounce

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

– Irish Central Bank Refuses To Discuss Gold Reserves In Bank of England Vaults

Key Fed yield gauge points to rate cuts for first time since 2008

Submitted by cpowell on Wed, 2019-01-02 14:08. Section: Daily Dispatches

By Gregor Stuart Hunter

Bloomberg News

Wednesday, January 2, 2019

A market indicator watched by the Fed as one of the most accurate gauges of economic health is pricing in lower rates for the first time in more than a decade.

The little-known near-term forward spread, which reflects the difference between the forward rate implied by Treasury bills six quarters from now and the current three-month yield, fell to -0.0653 of a basis point today.

…

…

It was the first time since March 2008 the gauge — seen as a proxy for traders’ outlook on Federal Reserve policy — fell below zero.

Crossing the threshold indicates the market sees easier policy and recession in “the next several quarters,” economists at the U.S. central bank wrote in a research paper dated July 2018. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-02/key-fed-yield-gauge-p…

end

Craig is correct: the economic and political conditions now resemble 2010.

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Expectations for gold and silver in 2019

Submitted by cpowell on Wed, 2019-01-02 22:27. Section: Daily Dispatches

5:27p ET Wednesday, January 2, 2018

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing tonight at Sprott Money, argues that economic and political conditions now resemble those of 2010, when gold and silver last enjoyed strong rallies. While bullion banks will keep striving to suppress the monetary metals, Hemke writes, he expects prices to continuing climbing.

Hemke’s analysis is headlined “Expectations for Gold and Silver in 2019” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/expectations-for-gold-and-silver-in-201…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Quite a commentary. Ambrose Evans Pritchard describes in detail how the euro has failed and how its threatens democracy in the region. He believes that the Euro should be abolished and each country should go back to its former curruency

(courtesy Ambrose Evans Pritchard/GATA)

Ambrose Evans-Pritchard: The euro has failed, threatens democracy, and should be abolished

Submitted by cpowell on Thu, 2019-01-03 02:14. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Wednesday, January 2, 2019

https://www.telegraph.co.uk/business/2019/01/02/euro-has-failed-threaten…

To be charitable, you could say the euro has proved itself merely by surviving until its 20th birthday this January. That is a low bar.

Monetary union has otherwise failed as an economic and political endeavour. The evidence of Europe’s ‘Lost Decade’ is that it can be made to work only under a regime of technocrat Caesaropapism — that is to say by stripping elected parliaments of their lifeblood control over taxation, spending, and the core economic policies of the nation-state.

“One day the house of cards will collapse,” says Professor Otmar Issing, the founding chief economist of the European Central Bank and the chastened prophet of the euro project.

…

The London School of Economics has assembled package of papers by illuminati from Europe and North America to mark this week’s anniversary, published by the journal Comparative Political Studies.

Mark Copelovitch, Jeffry Frieden, and Stefanie Walter do not pull their punches in the prologue. The calamitous European Monetary Union saga has led to the “most serious economic crisis in the history of the European Union.” It has done “more lasting damage” to swaths of Europe than the Great Depression of the 1930s and has pitted eurozone states against each other in a bitter struggle for control over the levers of policy.

The political dynamics have become poisonous. Years of rolling crisis “entrenched and amplified the power and influence of creditor countries such as Germany,” working through the European Central Bank and the European Council.

In other words, EU bodies became debt collectors for the creditor bloc, and enforcers of a German-imposed strategy of debt deflation and fiscal contraction. The burden of adjustment fell on the weaker states, leading to a contractionary bias for the whole system. The Nobel fraternity have watched this display of pre-modern and pre-Keynesian illiteracy with a mixture of horror and despair.

Yet nothing is actually changing. There has been no Truth and Reconciliation to probe the disaster that was allowed to unfold. Those in control of the EU machinery still think they were right. The ideology prevails.

The London School of Economics papers said EU leaders have responded at every stage with half measures in a “sequential cycle of piecemeal reform,” just enough to stop the collapse of EMU without resolving the core deformities of an orphan currency with no fiscal union to back it up. “What is clear is that the status quo cannot persist indefinitely if the euro is to survive in the long term,” it said.

I would argue that the spectacle of an EU in such a shambles from 2010 to 2015 led directly to Brexit. It profoundly shook the moral prestige of the EU and demolished claims of economic competence.

While EU leaders quibbled over decimal points and debt repayment in Brussels, youth jobless rates reached 57 percent in Greece, 56 percent in Spain, and much the same across Italy’s Mezzogiorno. These were levels once unthinkable in a modern developed democracy. They have left a wreckage of “labour hysteresis” that will lower economic speed limits for a generation to come.

Several hundred thousand economic refugees came to work in Britain from the EMU depression belt. A further wave from Eastern Europe came to the UK instead of going to the eurozone as they would have done in normal times. The double surge had maximum impact just before the referendum.

More subtly, the euro crisis revealed that the pathologies of monetary union cannot be managed by normal democratic means. The elected prime ministers of Greece and Italy were toppled in 2010 and 2011 and replaced by EU functionaries in soft coups organized by Brussels and the pro-EMU vested interests of each country.

The ECB switched off liquidity support for Greek commercial banks in 2015, knowingly (and illegally?) precipitating a banking collapse that was hard to reconcile with the ECB’s treaty duty to uphold financial stability. When push come to shove, the reflex was authoritarian. It spoke to the character of the EU. That I why I voted for Brexit.

The London School of Economics says the euro crisis was predictable and was in fact widely predicted. It mimicked countless episodes in Latin America, East Asia, and other emerging markets, where debtors borrowed heavily in dollars they could not print.

The pattern is for countries to succumb to credit booms while money is loose and the “carry trade” is in full bloom. They spiral into busts when confidence evaporates and the capital flows dry up. This is the classic “sudden stop” faced by states that do not borrow in their own currency.

Europe’s elites imagined that current account deficits did not matter in the magical euro union, even though the deficit states in southern Europe and Ireland had lost their sovereign policy instruments and no longer had a lender of last resort behind them. They were therefore no different from Argentina or Thailand.

The elites also failed to grasp that fixed exchange rate systems (without full fiscal union) switch currency risk into default risk. The rating agencies also missed this elephant in the room and so did the International Monetary Fund, as it confessed later in its devastating mea culpa. Ideological capture drained everybody of their senses.

The illusion that monetary union was risk-free led to epic bubbles, made worse by a one-size-fits-all interest rate set for German needs when Germany was in trouble.

When the storm hit, the Berlin-Frankfurt-Brussels riposte was to misrepresent what was in essence as a cross-border banking and capital flow crisis as if it were caused by fiscal profligacy in the south. This became the “morality tale” version of EMU. It lives on in the policy structure.

It was and is fundamentally bogus — except for Greece under New Democracy — but it served the interests of Northern creditors. Prof. Issing says the rescue of Greece in 2010 was in fact a bailout for French and German banks. The IMF has admitted that the country was in effect sacrificed to save the euro and the European banking system at a delicate moment.

Yes, the south was naive. Nations feasted on the windfall of lower interest rates. They let unit labour costs ratchet up, even as Germany was ratcheting them down through the Hartz VI wage squeeze in what was objectively — if not intentionally — a beggar-thy-neighbour policy. They forgot that they cannot devalue their way back to exchange-rate equilibrium.

The EU’s cardinal error was to then try to force the high-debt states to claw back 20 or 30 percent lost labour competitiveness against Germany through “internal devaluations,” a euphemism for slashing demand. This was self-defeating even on its own crude terms. It shrank the economic base and drove up debt ratios faster through the denominator effect.

The London School of Economics says the result of so much damage is that the eurozone’s troubles today “appear disturbingly similar” to those of Japan, trapped in deflationary stagnation for 20 years with broken banks. Except that euroland is not Japan. It is not a cohesive society with a monetary and fiscal machinery working in harmony. “Europe’s debt problems look even more serious and threatening,” the LSE said.

Debt-to-GDP ratios in a string of vulnerable countries are far closer to the danger line now they were at the onset of the global financial crisis a decade ago — up from 68 to 125 percent in Portugal, 36 to 98 percent in Spain, 99 to 131 percent in Italy, 65 to 99 percent in France, 54 to 96 percent in Cyprus, and 103 to 176 percent in Greece (despite haircuts).

A weaker euro, interest rates of minus 0.4 percent, quantitative easing (six years too late), and a belated end to fiscal austerity did induce a modest cyclical recovery from 2015 to 2017 but it is not self-sustaining and is already petering out.

The eurozone risks crashing into the next global downturn with no defences. Rates cannot drop any lower. There is no proper banking union with pan-EMU deposit insurance. The dangers of a sovereign-bank “doom loop” remain. They are on full display again in Italy.

Emmanuel Macron’s grand plan to rebuild EMU on safer foundations has come to nothing. There is no fiscal entity worth the name. Counter-cyclical budget stimulus to fight shocks is prohibited by the machinery of the Stability Pact and Fiscal Compact. The ECB is still unable to act as a full lender of last resort.

Berlin has written a “debt brake” into the German constitution, a way of telling the world that it will not take any serious steps to reduce a current account surplus of 8 percent of GDP — a much greater threat to EMU survival than anything happening in Greece.

The LSE team takes a long view, comparing the eurozone’s travails to struggles between Alexander Hamilton and Thomas Jefferson over the handling of state debts in the United States. The battle saw disputes over the first and second national banks and lasted until the completion of U.S. monetary union in the 1870s — and took a civil war to resolve. “Crafting a functioning economic and monetary union is a long, hard road,” the LSE said.

The presumption is that the Europe’s leaders must in the end agree to some form of fiscal union, but this runs into the fundamental barrier of democracy. Such a system would eviscerate the tax and spending prerogatives of elected parliaments, forgetting the lessons of the English Civil War and indeed the American Revolution.

It can retain democratic legitimacy only if the EU goes the whole way to a supranational federal union akin to the United States, and for this there is not the slightest popular support in any major country.

The ineluctable conclusion is that a monetary union of budgetary sovereign states cannot be made to work, and should not be made to work. The euro is a constitutional anomaly. It must therefore be broken up. All else is self-deception.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8745/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8870 /shanghai bourse CLOSED DOWN 0.93 PTS OR 0.04%

HANG SANG CLOSED DOWN 65.99 POINTS OR 0.31%

2. Nikkei closed HOLIDAY

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 96.66/Euro RISES TO 1.1354

3b Japan 10 year bond yield: FALLS TO. +.00/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 46.64 and Brent: 55.47

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.18%/Italian 10 yr bond yield DOWN to 2.83% /SPAIN 10 YR BOND YIELD UP TO 1.43%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.65: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.41

3k Gold at $1289.05 silver at:15.59 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 68.93

3m oil into the 46 dollar handle for WTI and 55 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.71 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9887 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1226 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.18%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.64% early this morning. Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4701

Global Markets Tumble On Apple Bombshell, Currency Flash Crash

Global markets started the second trading day of 2019 the same way they did the first one: sharply lower, only instead of more economic gloom out of China, today’s bearish catalyst was only the second revenue warning out of Apple in nearly two decades which has sent AAPL stock tumbling 9% this morning, coupled with a subsequent flash crash in a variety of currency pairs, including the JPY, AUD and TRY, which sparked a selloff in risk assets in what has continued to be a painfully illiquid market, as investors scrambled for safety in safe havens such as bonds and gold even as concerns about slowing global and profit growth persisted while the US government shutdown entered its 13th day and no resolution was in sight.

While S&P futures were down 1.6%, Nasdaq futures led the drop for U.S. futures, dipping as much as 2.9% after Apple shocked investors by slashing its revenue guidance citing an “unforeseen” slowdown in China – which Tim Cook somehow discovered only after the quarter ended – and fewer upgrades to its flagship mobile device.

Apple was down 9% in pre-market trading. Technology shares led the Stoxx Europe 600 Index lower while equities in Asia also declined. Treasuries declined along with most European bonds.

“For the moment, investors have reacted by going into non-risky assets,” said Philippe Waechter, chief economist at Ostrum Asset Management, in Paris. “No one wants to take any risk because none of the uncertainties we are facing have been lifted, whether it’s Brexit, this trade war, or growth. Investors are putting their heads in the sand and waiting.”

“That Tim Cook and his company mentioned China as the reason behind the downturn in the company’s outlook seemed to hit exactly the pressure point traders and investors were already alarmed over,” Greg McKenna, markets strategist at McKenna Macro. “That is, the China and global slowdown which seems to have been confirmed by Wednesday’s global manufacturing PMI data.”

Asian stocks Asia-Pac were mixed following the slide in US equity future, with the ASX 200 (+1.4%) lifted by energy names and gold miners amid yesterday’s spike higher in oil and the Apple-triggered bid in the yellow metal, meanwhile Nikkei 225 was closed again due to a public holiday. Elsewhere, Hang Seng (-0.3%) and Shanghai Comp. (unch) swung between gains and losses with the former weighed on by tech names as Apple suppliers ACC Technologies and Sunny Optical slumped over 5% after Apple’s guidance cut while investors braced for Beijing to roll out fresh support measures for the cooling Chinese economy.

“Chinese authorities have got the luxury of having control not just of the fiscal parts of the government tool case, but also the monetary parts … and I suspect the Chinese authorities will use that,” said Jim McCafferty, head of equity research, Asia ex-Japan, at Nomura.

China’s central bank said late on Wednesday it was adjusting policy to benefit more small firms that are having trouble obtaining financing, in its latest move to ease strains on the private sector, a key job creator. While more fiscal and monetary policy support had been expected in coming months on top of modest measures last year, some analysts wonder if more forceful stimulus will be needed to stabilize the world’s second-largest economy.

Major European bourses were firmly in negative territory by midmorning, with Frankfurt’s DAX with its exposure to Chinese trade and tech-heavy constituents, was the biggest faller and down as much as 1.2% while Paris’ CAC40 dropped 1.1 percent and London eased 0.4 percent. Chipmakers who supply parts to Apple were the worst hit, sending technology stocks to their lowest since February 2017.

The shocking Apple news sparked a violent, multi-currency flash crash in holiday-thinned FX markets as growing concerns about the health of the global economy, particularly in China, sent investors scurrying into the safe-haven of the Japanese yen, which surged through levels not seen in years.

In the liquidity dead zone between 5 and 6pm ET, it took just seven minutes for the yen to surge through levels against Aussie dollar that have held through almost a decade. While some pointed to risk aversion triggered by the Apple guidance cut others said Japanese retail investors were behind the trades. Whatever the cause, the moves were exacerbated by algorithmic programs and thin liquidity with Japan on holiday.

As the yen jumped, the Australian dollar slumped to the lowest in almost 10 years as algorithmic programs amplified sharp gyrations amid thin liquidity during a Japanese holiday; the Turkish lira and British pound also tumbled however all pairs have recouped much of their losses since.

The dollar was last 1 percent weaker against the yen at 107.57, having earlier fallen as low as 104.96, its lowest level since March 2018. The Australian dollar at one point hit levels against the Japanese yen not seen since 2011. The euro was up 0.3 percent, buying $1.1375, and the dollar index which tracks the U.S. currency against a basket of major rivals, was 0.3 percent weaker at 96.52.

In rates, Germany’s 10-year bond yield was most recently at 0.185% after hitting a session low of 0.148 percent, while the US 10Y Treasury yield was modestly higher, rising from 2.62%, the lowest since the start of 2018, to 2.6362%. U.S. crude oil fell 0.9% to $46.12 a barrel, and Brent crude was down 0.2% at $54.82. Slowing global growth is expected to coincide with an increase in crude supply, depressing prices. Gold was higher as the dollar weakened, with spot gold trading up 0.2 percent at $1,289.4 per ounce.

Expected data include jobless claims, while automakers report U.S. sales for December. Simply Good Foods, UniFirst due to report earnings

Market Snapshot

- S&P 500 futures down 1.4% to 2,475.50

- STOXX Europe 600 down 0.4% to 335.73

- MXAP up 0.2% to 145.56

- MXAPJ down 0.5% to 465.89

- Nikkei down 0.3% to 20,014.77

- Topix down 0.5% to 1,494.09

- Hang Seng Index down 0.3% to 25,064.36

- Shanghai Composite down 0.04% to 2,464.36

- Sensex down 0.9% to 35,561.57

- Australia S&P/ASX 200 up 1.4% to 5,633.41

- Kospi down 0.8% to 1,993.70

- German 10Y yield rose 1.0 bps to 0.175%

- Euro up 0.3% to $1.1377

- Italian 10Y yield fell 4.9 bps to 2.335%

- Spanish 10Y yield rose 1.5 bps to 1.416%

- Brent Futures down 0.7% to $54.54/bbl

- Gold spot up 0.3% to $1,288.08

- U.S. Dollar Index down 0.3% to 96.52

Top Overnight News from Bloomberg

- President Donald Trump has gained little leverage with Democrats two weeks into the partial government shutdown of his own making, with fewer possible escape routes and a more treacherous path ahead as the GOP relinquishes control of the House.

- The odds of a U.S.-China trade deal are rising because both sides have a clearer sense of each other’s goals and intentions, a former Chinese trade official said ahead of negotiations in Beijing next week.

- It took seven minutes for the yen to surge through levels against Aussie dollar that have held through almost a decade. While some pointed to risk aversion triggered by Apple Inc. cutting its sales outlook, others said Japanese retail investors were behind the trades. Whatever the cause, the moves were exacerbated by algorithmic programs and thin liquidity with Japan on holiday

- Congressional leaders were unable to strike a deal to end a partial shutdown of the federal government at a meeting with Donald Trump on Wednesday, and the president invited them to return to the White House on Friday for further negotiations

- U.S. government officials are publicly withholding judgment on China’s efforts to ease trade tensions ahead of talks next week, raising the prospect that Beijing’s latest economic-reform announcements won’t go far enough to satisfy President Trump’s demands

- In a sign of the urgency felt by the cartel amid tumbling crude prices, leading member Saudi Arabia throttled back production, according to a Bloomberg survey of officials, analysts and ship-tracking data. The group’s pact to curb output only formally started this week

- Fewer Japanese businesses are optimistic about economic growth compared with a year ago amid concerns over global trade tensions, Brexit and a sales tax increase, according to a Sankei newspaper survey of 121 leading companies

- There’s a lack of catalysts on the horizon at the start of 2019 to reverse the slide in Treasury yields as global economic growth wanes and investors shift toward the view that further Federal Reserve tightening would be a mistake

Asia-Pac equities were mixed following the slide in US equity futures after tech-giant Apple fell in excess of 8% after-market following a cut to its Q1 2019 revenue guidance to USD 84.0bln, from previous guidance in the range of USD 89.0-93.0bln. ASX 200 (+1.4%) was lifted by the energy names and gold miners amid yesterday’s spike higher in oil and the Apple-triggered bid in the yellow metal, meanwhile Nikkei 225 was closed again due to a public holiday. Elsewhere, Hang Seng (-0.3%) and Shanghai Comp. (unch) swung between gains and losses with the former weighed on by tech names as Apple suppliers ACC Technologies and Sunny Optical slumped over 5% after Apple’s guidance cut. Meanwhile the Mainland was underpinned by financial names after reports that the PBoC may lower the RRR for banks that lend to small businesses. Of note: China CICC Research stated that the PBoC’s RRR criteria easing could release up to CNY 400bln in liquidity.

Top Asian News

- First China, Now Apple: Bad Start for Asia Stocks Gets Worse

- China Easing Expected as $625 Billion ‘Liquidity Hole’ Looms

- Witching Hour for Currencies Strikes Again as Yen Breaks Loose

- China’s Huolinhe Says Local Govt Approves 6GW Wind Power Project

Major European equities are predominantly in the red [Euro Stoxx 50 -1.1%] with the SMI (+0.1%) outperforming its pears after returning from a market holiday. SMI index heavyweight UBS (+0.5%) are in the green following comments from their Chairman that now is not the right time for a merger; additionally, he expects to remain in office until 2022. The technology sector (-2.8%) is the underperforming sector with the likes of Dialog Semiconductor (-9.0%), STMicroelectronics (-9.4%), ASML (-5.1%) and Infineon (-5.4%) at the bottom of the Stoxx 600 following Apple cutting their Q1 revenue guidance. Other notable stories include Next (+5.2%) in the green after reporting their expected full year price sales growth of +3.2%, which is in line with September’s guidance and thus avoids a profit warning for the Co. Adecco (-4.8%) are down after being downgraded at Credit Suisse. In addition, luxury names are in the red with the likes of Burberry (-4.8%) and Kering (-4.5%) weighed on by growth concerns in China exacerbated by the aforementioned Apple guidance cut.

Top European News

- Ryanair Passenger Growth Slowest Since 2015 After Strike Turmoil

- U.K. Retailers Jump as Next’s Update Comforts Bruised Sector

- Spain Leads European Sovereigns With First Bond Sale of 2019

- European Luxury Stocks Decline on China Slowdown Concern

In FX, price action remains a key focus for investor sentiment amid the wild swings seen during Asia-Pac hours. To recap events, FX markets were rattled amid a surge in the JPY which saw the currency gain circa 8% vs. the AUD and 10% vs. TRY with analysts attributing the move to a multitude of factors including thin markets (Japan away from market again), Apple-inspired risk aversion (following revenue guidance cut) and Japanese retail investors liquidating offside positions.

- In terms of price action at the time, AUD/JPY plummeted from around 75.50 to a low print of 70.50, tripping several stops along the way. Shortly after the stops were taken-out, AUD/JPY pared back a bulk of the move and now trades in close proximity to the 75.00 handle. Elsewhere, at the time, USD/JPY slid sharply below 109.00 to briefly breach 105.00 before recovering to the mid 107.00’s (note, given the velocity of the moves, various platforms have registered differing moves). AUD/USD declined further below 0.7000 to touch levels last seen a decade ago with a session low of 0.6743 before eventually recouping a 0.6900 handle.

- Aussie and Yen crosses reacted in tandem with the sharp swing, the Pound was hit as GBP/JPY fell through 137.00 to levels just shy of 131.50 and as such, Cable lost the 1.2600 handle and briefly clipped 1.2450 to reach 21-month lows before reclaiming 1.2550 with Lloyds noting pivotal resistance between 1.2590-1.2615 and suggesting that a move through this level would allow for “a stronger recovery in the range under 1.2810-50”. From a fundamental perspective, Brexit-related commentary has begun to pick-up as Mrs May returns to work ahead of Parliament reconvening on the 7th; latest reports suggest that the UK PM has been urged to delay the meaningful vote on her Brexit deal for a second time as government whips failed to persuade enough MPs to back it over the Christmas break.

- EUR has been slightly more resilient than some of its peers despite a blip lower in EUR/JPY which led EUR/USD to a session low of 1.1310 with the multi-bloc currency thereafter able to benefit from touted short-covering and a broadly softer USD (DXY currently trades just above 96.50 with losses of circa 0.2%). As such, EUR/USD now trades just above of 1.1350 after running out of steam at 1.1384.

In commodities, Brent (unch.) and WTI (-0.2%) prices remain anchored as concerns over global growth and an oversupplied market continue to prevail; ahead of today’s rescheduled API’s (with EIA’s tomorrow). Saudi Arabia are expected to cut February heavy crude prices for crude sold to Asia because of weaker fuel oil margins; as according to a Reuters survey. Elsewhere, Libya’s NOC have said that the Sharara oil field was breached on Tuesday and output will be cut by 8.5k after operations restart for the main system. Gold (+0.2%) is in the green due to safe haven demand from the Apple-stemmed growth fears; with the yellow metal passing 6-month highs earlier in the session, although prices are around USD 4/oz off of the USD 1292/oz session highs. Elsewhere, copper prices are down succumbing to the negative risk sentiment.

US Event Calendar

- 8:15am: ADP Employment Change, est. 180,000, prior 179,000

- 8:30am: Initial Jobless Claims, est. 220,000, prior 216,000; Continuing Claims, est. 1.69m, prior 1.7m

- 10am: Construction spending data postponed by govt shutdown

- 10am: ISM Manufacturing, est. 57.5, prior 59.3

- Wards Total Vehicle Sales, est. 17.2m, prior 17.4m

DB’s Jim Reid concludes the overnight wrap

Happy New Year to you all and welcome to 2019. With the over-indulging now hopefully all done and the batteries as close to recharged as possible, now is probably as good a time as ever to have one final look back at what was a remarkable year for markets in 2018. Indeed an hour or so before this we published our standalone performance review for December, Q4 and 2018. It includes our update of what has proven to easily be the most requested chart we’ve ever produced – which hopefully isn’t a representation of the many other charts we’ve done – the percentage of assets which delivered a negative total return in dollar and local currency terms. Without giving too much away, only 7 of the 70 assets in our sample posted a positive total return in dollar terms so the first pub quiz question of the year is to correctly guess which assets those were. Answers are in the performance review.

Before you mull over that, and for those that have been away, it’s worth recapping what markets have done over the holiday period which has been anything but a sleepy couple of weeks. The good news is that we’re returning to US equity markets which are broadly speaking higher than where they finished on December 21st. Indeed the S&P 500, NASDAQ and DOW are up +3.87%, +5.26% and +4.01% since then, respectively. The underlying tone has been a lot more fragile however with the point to point moves also masking a few eventful sessions. We had the biggest Christmas Eve decline (-2.71%) for the S&P 500 ever, then the biggest one-day gain (+4.96%) for the S&P 500 since 2009 on Boxing Day and one of the biggest intraday reversals for the S&P 500 one day later on December 27th when the S&P 500 turned a -2.84% decline into a +0.86% gain over the final 90 minutes of trading.

After US markets had closed last night, we got another injection of volatility, as Apple took the rare move of lowering its revenue guidance, citing weakness in “greater China.” Shares dropped as much as -8.50% in after-hours trading with the announcement implying the first holiday quarter slowdown since 2011, but the real drama came in FX markets, where the yen strengthened as much as +3.70% to 104.87 – a full 4 points from the New York close of 108.88 – in a matter of minutes. Simultaneously, the Australian dollar and Turkish lira weakened as much as -3.50% and -8.89% respectively.The moves have partially retraced, in the case of the Yen it’s now trading at 107.09, however still resemble a flash crash. There was some suggestion that the moves were linked to the Apple news, triggering a wave of risk aversion, while a Japanese holiday likely also compounded the issue.

So it would be a stretch to say that there’s much conviction at the moment with moves in markets over the last couple weeks hardly healthy and it goes to show what thin liquidity conditions and year-end rebalancing can do when markets are as fragile as they’ve been in years. The VIX peaked at 36.07 on a closing basis during that run however has since fallen to 23.22 as of last night’s close.

Here in Europe, it feels like equity markets better fit the underlying fragility with the STOXX 600 only up +0.16% including a -0.13% fall yesterday which wasn’t as bad as first feared, partly helped by WTI oil jumping +4.52% from the lows (and as much as +7.73% at one stage). The S&P 500 bounced up to close +0.13% for context, after being down -1.57% at the open. Cash HY spreads are also +15bps and +10bps wider in the US and Europe respectively (+5bps and +6bps yesterday) and so picking up where we left. Meanwhile bonds had been a bit quieter by comparison, however that was until the last couple of sessions. Indeed the big story yesterday was 10y Bund yields hitting a low of 0.145% intraday, before closing at 0.162% and -7.3bps lower on the day. Still, that’s the lowest closing yield since April 2017 and the biggest one-day decline for Bund yields since last May. And to think that we’re now officially in the period of zero net QE purchases by the ECB. Treasuries also hit 2.621% (-6.4bps) yesterday and the lowest since last January, having fallen -16.4bps over the holiday period. The curve flattened -4.3bps yesterday but is close to flat from where we last reported pre-Christmas at 15bps. Amazingly we are now pricing in 2bps of cuts by the Fed in 2019.

Part of that Bund move was catch-up to the Treasury market, since Germany was closed on December 31st, however the wider risk-off move seemed to be attributed to the confirmation that China’s manufacturing sector has entered contraction territory.Indeed the December Caixin manufacturing PMI fell half a point to 49.7 (vs. 50.2 expected) and thus confirmed the official PMI sub-50 reading from a week before. In addition to China, we also saw sub-50 readings from Taiwan, Malaysia and South Korea and so clear evidence that the lack of resolution around the US-China trade issues have impacted the wider region once more. It’s worth adding that our China economists published their 2019 outlook yesterday which you can find here . Of most significance, they have downgraded their growth forecast for China to 6.1% in 2019 (from 6.3%) with a trough of 5.9% in Q2 before a significant change of policy stance around March/April boosts growth in the second half of the year.

This morning in Asia there’s only been limited follow through from the negative Apple news last night to regional bourses.The Hang Seng and Shanghai Comp for example are down -0.37% and -0.06% respectively while the Kospi is down -0.43%. Markets in Japan are closed while bourses in the likes of Malaysia, Thailand and Indonesia are actually up slightly. News that the PBoC is seeking to boost lending to small and micro-sized enterprises is perhaps helping. However it’s a very different picture for US futures with the S&P 500 currently down -1.48% and NASDAQ -2.43%.The Treasury market isn’t trading overnight with Japan closed. So it could be an interesting US open later.

As for the other newsflow since we’ve been away, the partial US government shutdown has entered its 13th day with President Trump digging his heels in over the border wall funding. The new Congress is due to be sworn in today so we’ll see if this helps resolve the disputes. This follows Trump inviting congressional leaders to the White House yesterday. The new Democratic majority will now take control of the House, but the real sticking point for a budget deal is the need for bipartisanship in the Senate, where the GOP will be 7 seats short of a filibuster-proof majority. Some economic data could be delayed if the shutdown continues, namely home sales, retail sales, and durable goods, though Friday’s jobs report will be unaffected. There has seemingly been better news on the trade front where President Trump reported “big progress” on talks with China President Xi Jingping a few days ago. Meanwhile in Italy, the 2019 budget was passed at the eleventh hour at the compromise deficit figure of 2.04% of GDP. As for the latest on Brexit, former UK Brexit Secretary David Davis wrote in the Telegraph yesterday that the UK PM May should delay the vote on her Brexit deal for a second time highlighting that it could lead to a better deal from the EU as the EU is worried about losing the £39bn “divorce payment” that would come with a Brexit deal.

As for the data away from China, we’ve had much softer-than-expected CPI figures in Europe, specifically for Germany (+1.7% yoy vs. +1.9% expected) and Spain (+1.2% yoy vs. +1.5% expected). In the US, Q3 GDP was revised down -0.1pp to 3.4% and the Kansas City and Richmond Fed manufacturing indexes both fell to multi-year lows.That will certainly heighten interest in the ISM manufacturing report due this afternoon. Yesterday’s manufacturing PMI was revised down 0.1pts to 53.8 although the employment and new orders components were the lowest since 2017. In Europe, the manufacturing PMI was confirmed at 51.4 for the Eurozone, mostly unrevised versus the flash, but with Italy’s reading +0.6pts higher at the expense of Spain’s, which fell -1.5pts. The UK print beat expectations at 54.2 versus 52.5, though the qualitative details indicated that the activity increase was due to stock-building ahead of Brexit uncertainties.

Apart from the ISM report, there will be a few other events to note through the rest of this week. Tomorrow, and as mentioned above, we’ve got the December employment report in the US while Fed Chair Powell is due to make an appearance at the AEA annual meeting alongside former Fed Chairs Bernanke and Yellen. Our US economists don’t expect the Chair to break any new ground on the policy front but he may take the opportunity to clarify the message from the December FOMC meeting, in a similar vein to the NY Fed’s Williams who specifically addressed the slight tweak in the forward guidance message.

As for today, this morning we’ll get the December CPI print in Turkey and November M3 money supply data for the Euro Area. Shortly after in the US we get the December ADP employment change report along with the latest claims reading, November construction spending and then the aforementioned December ISM manufacturing print. The latter is expected to fall -1.5pts to 57.8 at a headline level. Later this evening we’ll also get December vehicle sales numbers. Also, as mentioned earlier, today is also the day that the Democrats officially take control of the House with US Congress sworn in.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 0.93 PTS OR 0.04% //Hang Sang CLOSED DOWN 65.99 POINTS OR 0.26% /The Nikkei closed HOLIDAY / Australia’s all ordinaires CLOSED UP 1.23%

/Chinese yuan (ONSHORE) closed DOWN at 6.8745AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 46.46 dollars per barrel for WTI and 55.47 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED DOWN AT 6.8745 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8870: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i)CHINA/TAIWAN

Taiwan will never accept reunification with Beijing..this message uttered by its President

(courtesy zerohedge)

Taiwan Will “Never Accept” Reunification With Beijing, President Says

Following a menacing speech by Chinese President Xi Jinping where he threatened violence against Taiwan should it pursue de jure independence from China and laid bare his intentions to push for a “one country, two systems” arrangement for what China considers to be a ‘rogue province’, pro-independence Taiwanese President Tsai Ing-wen clapped back at Xi in comments to the BBC on Wednesday, where she said the island would never accept reunification with China on Beijing’s terms.

After defending the status quo and calling on Beijing to “face the reality” of Taiwan’s continued independence, Tsai declared on Wednesday that the island, which has functioned like a de facto country since 1949, when defeated nationalists led by Kuomintang leader Chiang Kai Shek fled across the Strait of Taiwan to seek refuge from the Communists, would never agree to the “one country, two systems” arrangement like the one that governs Hong Kong.

But on Wednesday, Taiwan’s President Tsai Ing-wen said the island would never accept reunification with China under the terms offered by Beijing.

“I want to reiterate that Taiwan will never accept ‘one country, two systems’. The vast majority of Taiwanese public opinion also resolutely opposes ‘one country, two systems’, and this is also the ‘Taiwan consensus’.”

Under the “one country, two systems” formula, Taiwan would have the right to run its own affairs; a similar arrangement is used in Hong Kong.

Since cementing his untrammeled power over the Chinese government and clearing the path for lifetime rule, Xi has exerted more pressure on Taiwan to bend to Beijing’s will. Last year, he successfully pressed for global airlines to identify Taiwan as a part of China, and has authorized threatening military exercises in the Taiwan Strait.

But what are the chances that Xi adopts a more aggressive posture toward Taiwan, one that potentially involves military conflict? One BBC analyst said this possibility remains remote.

If anything, China will probably step up its efforts to interfere with Taiwan’s elections to undermine pro-independence parties, while strengthening trade and other economic ties.

China may be a rising military superpower, but sending an invading army across the choppy, well-defended waters of the Taiwan strait would still be a huge military gamble, with success far from guaranteed.

Beyond the slightly more strident tone, Mr Xi’s speech does not appear to signal any dramatic change in those calculations, especially when you take into account the more conciliatory passages offering a further strengthening of trade links.

If there is to be any warfare, it is likely to be of the cyber kind; China is reported to be stepping up its efforts to influence Taiwan’s elections to hurt the prospects of independence-leaning parties and politicians.

The hope has long been that it will be China’s growing economic might, not military force, that will eventually pull Taiwan into its embrace.

But as the trade war with the US simmers and Chinese leaders wary of foreign interference, Xi’s threats to strike back against foreigners who interfere with Taiwan could create further tension with the US, particularly after a Chinese admiral threatened to “sink two aircraft carriers” to send the US a message.

4.EUROPEAN AFFAIRS

/EU

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

/Syria/USA

Trump backtracks a little on leaving Syria as he does not want to expose the Kurds to an invading Turkey. He states that they will leave “over a period of time”

(courtesy zerohedge)

Trump: Syria Is “Sand And Death”, US Exit Will Be “Over A Period Of Time”

After early this week Trump’s promised “full” and “immediate” US troop withdrawal from Syria was put on shaky ground following a prior meeting with hawk Sen. Lindsey Graham, and following immense push back from the career Washington deep state, the president is showing signs that he could be changing his tune.

President Trump said on Wednesday the US will get out of Syria “over a period of time” and in such a way that will protect America’s Kurdish partners on the ground, at a moment pro-Turkish forces backed by Turkey’s army are set to invade and annex Kurdish enclaves in the north of the country.

Mutlu Civiroglu

✔@mutludc

President Donald Trump: …”United States wants to protect Kurds in Syria even as it pulls forces out.”

During a Wednesday Cabinet meeting in front of reporters – the first of the new year – Trump did not provide a timetable for a planned military exit while strongly emphasizing he would “not forget” the extraordinary sacrifices the Kurds made in the fight against ISIS.

The president said:

We have to help them, I want to help them…

They fought with us, they died with us… thousands of Kurds died fighting ISIS. they died for us and with us, and for themselves… I don’t forget.

He did, however, deny widespread reports that he had discussed setting a four month timetable for the withdrawal of 2000+ American troops. Previous language of a “hasty” pullout decision reportedly in part prompted Defense Secretary Jim Mattis to resign.

The Kurdish “People’s Protection Units” (YPG) – the core of the US-backed SDF head a convoy of US military vehicles, via Reuters.On Monday Trump appeared to back off prior language of an “immediate” and hasty pullout while emphasizing the operation would be slow. “We’re slowly sending our troops back home to be with their families, while at the same time fighting Isis remnants,” he stated on Twitter Monday.

The Kurdish “People’s Protection Units” (YPG) – the core of the US-backed SDF head a convoy of US military vehicles, via Reuters.On Monday Trump appeared to back off prior language of an “immediate” and hasty pullout while emphasizing the operation would be slow. “We’re slowly sending our troops back home to be with their families, while at the same time fighting Isis remnants,” he stated on Twitter Monday.

But he also indicated he’s committed to seeing it through: “If anybody but Donald Trump did what I did in Syria, which was an ISIS loaded mess when I became President, they would be a national hero,” Trump tweeted. “ISIS is mostly gone, we’re slowly sending our troops back home to be with their families, while at the same time fighting ISIS remnants.”

Notably, he also told reporters on Wednesday: “Syria was lost long ago. we’re not talking about vast wealth. we’re talking about sand and death,” while also noting:

“It’s not my fault. I didn’t put us there.”

And in a statement sure to give John Bolton a conniption fit, Trump commented in response to a question on Iran’s role in Syria,saying “they can do what they want there, frankly.”

Advocates for a continued US military presence in Syria argue that any pullout would be a gift to Russia, Iran, and Damascus. As a compromise US commanders are currently requesting that Kurdish YPG fighters be allowed to keep their US-supplied weapons, which would anger Turkey.

Meanwhile, the position of French forces involved in the coalition operation to support the Kurds is also made precarious by a US pullout. Macron previously blasted Trump’s announced exit, saying “an ally should be dependable.” Likely it would be impossible for French forces – which maintain a handful of forward operating bases – to stay if American forces completely withdraw.

Syrian Kurdish representatives are currently urging Macron to stay the course in Syria even if the US draws down. Simultaneously there appears increasing indirect coordination between the YPG and the Syrian Army, as talks with Damascus are also said to be making positive momentum in terms of a future settlement of Syria’s Kurdish enclaves.

Iran Rejects Pompeo Warning To Halt Its Space Launches

Hours after Secretary of State Mike Pompeo threatened Iran via Twitter statement over plans to fire off Space Launch Vehicles with, as Pompeo claimed, “virtually the same technology as ICBMs” in a “defiant” launch that will “advance its missile program,” Iran has responded. Iranian Foreign Minister Javad Zarif shot back via Twitter saying “Iran’s launch of space vehicles — & missile tests — are NOT in violation of Res 2231,” which is the UN resolution which endorsed the Joint Comprehensive Plan of Action (JCPA) on Iran’s nuclear program — which the Trump administration pulled out of last May.

FM Zarif wrote on Thursday in response to Pompeo while warning “threats engender threats” and linking to the UN text:

Iran’s launch of space vehicles — & missile tests — are NOT in violation of Res 2231. The US is in material breach of same, & as such it is in no position to lecture anyone on it. Reminder to the US: 1. Res 1929 is dead; 2. threats engender threats, while civility begets civility.

Iran’s defense ministry previously announced plans for three Space Launch Vehicle (SLV) launches in “the coming months,” according to an official statement. This after in late November Iranian Deputy Defense Minister General Qassem Taqizadeh first unveiled plans to send three Iranian made satellites into space soon.

“The satellites have been made by domestic experts and will be put on various orbits,” Taqizadeh said.

Javad Zarif

✔@JZarif

Iran’s launch of space vehicles— & missile tests—are NOT in violation of Res 2231. The US is in material breach of same, & as such it is in no position to lecture anyone on it.

Reminder to the US:

1. Res 1929 is dead;

2. threats engender threats, while civility begets civility.

The last time Iran conducted a space launch was in July 2017, which the US State Department had warned was “provocative”. The US has long held that United Nations Security Council Resolution 2231 prevents any activity related to ballistic missile technology; however, Iran says the wording leaves open the possibility of missile development programs unrelated to the delivery of nuclear weapons.

The resolution says that Iran “is called upon” not to undertake any activity related to ballistic missiles “designed to be capable” of nuclear warhead delivery while stopping short of explicitly banning the activity.

Secretary Pompeo

✔@SecPompeo

#Iran plans to fire off Space Launch Vehicles with virtually same technology as ICBMs. The launch will advance its missile program. US, France, UK & Germany have already stated this is in defiance of UNSCR 2231. We won’t stand by while the regime threatens international security.