GOLD: $1284.35 DOWN $8.45 (COMEX TO COMEX CLOSINGS)

Silver: $15.71 DOWN 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1285.20

silver: $15.71

TODAY THEY RELEASED THE JOBS REPORT. NOT ONLY ARE THEY USING A PHONY BIRTH DEATH MODEL TO CREATE JOBS OUT OF THIN AIR, THEY HAVE A NEW MODEL USING “BUSINESS INTERESTS” OR CONSULTANTS..A TOTALLY MADE UP NUMBER.

THE REPORT IS A TOTAL JOKE!

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 29 NOTICE(S) FOR 2900 OZ (0.0902 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 94 NOTICES FOR 9400 OZ (.2923 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

24 NOTICE(S) FILED TODAY FOR 120,000 OZ/

total number of notices filed so far this month: 180 for 900,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3758: DOWN 13

Bitcoin: FINAL EVENING TRADE: $3748 down 18

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 8/94

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,291.800000000 USD

INTENT DATE: 01/03/2019 DELIVERY DATE: 01/07/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C MERRILL 7

657 C MORGAN STANLEY 3

657 H MORGAN STANLEY 7

661 C JP MORGAN 8

737 C ADVANTAGE 3

800 C RCG 1

800 H RCG 29

____________________________________________________________________________________________

TOTAL: 29 29

MONTH TO DATE: 94

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY AN CONSIDERABLE SIZED 3250 CONTRACTS FROM 181,253 DOWN TO 178,003 DESPITE YESTERDAY’S GOOD 22 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGELY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

3306 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3306 CONTRACTS. WITH THE TRANSFER OF 3306 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3306 EFP CONTRACTS TRANSLATES INTO 16.530 MILLION OZ ACCOMPANYING:

1.THE 22 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 4.965 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 8775 CONTRACTS (FOR 3 TRADING DAYS TOTAL 8775 CONTRACTS) OR 43.875 MILLION OZ: (AVERAGE PER DAY: 2925 CONTRACTS OR 14.625 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 43.875 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.27% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 43.875 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3250 DESPITE THE STRONG 22 CENT GAIN IN SILVER PRICING AT THE COMEX //MONDAY..THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3306 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A TINY SIZED: 56 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3306 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3250 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 22 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.74 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .881 BILLION OZ TO BE EXACT or 126% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 24 NOTICE(S) FOR 120,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 4.965 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD 4632 CONTRACTS UP TO 457,208 WITH THE STRONG GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $10.65//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 12,530 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 12,530 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 457,208. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN HUGE SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 17,162 CONTRACTS: 4,632 OI CONTRACTS INCREASED AT THE COMEX AND 12,530 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 17,162 CONTRACTS OR 1,716,200 OZ = 53.38 TONNES. AND ALL OF THIS VERY HUGE DEMAND OCCURRED WITH A STRONG GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $10.65

YESTERDAY, WE HAD 10297 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 25,326 CONTRACTS OR 2,532,600 OZ OR 78.77 TONNES (3 TRADING DAYS AND THUS AVERAGING: 8442 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 78.77 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 78.77/2550 x 100% TONNES = 3.09% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 78.77 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 4632 WITH THE GAIN IN PRICING ($10.65) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,530 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,530 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS GAIN OF 17,162 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,530 CONTRACTS MOVE TO LONDON AND 4632 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 53.38 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH THE GAIN OF $10.65 IN YESTERDAY’S TRADING AT THE COMEX

we had: 29 notice(s) filed upon for 2900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $8.45 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 795.31 TONNES

Inventory rests tonight: 795.31 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 3 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY/

/INVENTORY RESTS AT 317.105 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 3250 CONTRACTS from 181,253 DOWN TO 178,003 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

3306 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3306 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3250 CONTRACTS TO THE 3306 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A TINY GAIN OF 56 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 0.280 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 4.965 MILLION OZ STANDING IN JANUARY..

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 22 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 3306 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 50.51 PTS OR 2.05% //Hang Sang CLOSED UP 561.67 POINTS OR 2.24% /The Nikkei closed DOWN 452.81 POINTS OR 2.26% / Australia’s all ordinaires CLOSED DOWN 0.31%

/Chinese yuan (ONSHORE) closed UP at 6.8649 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 47.92 dollars per barrel for WTI and 57.03 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.8649 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8775: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/

China is in deep trouble especially after last weeks’s terrible PMI numbers. Today they announced a RRR cut as liquidity is drying up. However the cuts will occur only on Jan 15 and Jan 25 to offset liquidity concerns prior to its New Year.. It is business as usual for China

( zerohedge)

4/EUROPEAN AFFAIRS

EMU

The European Monetary Zone is generally a good manufacturing producer led by Germany etc. Today the Eurozone PMI slipped to almost contraction, coming in at 51.1 in December, its weakest report in almost 4 years;

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN/USA

This no doubt will alarm Mike Pompeo and Trump: Iran to upgrade its speedboats in the Gulf with stealth technology as they want to encounter the uSA Navy in the Gulf.

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)No doubt about it: a phony jobs report: they state that payrolls rose by 312,000 and that will probably give Powell the signal to continue with his crazy rate hikes

(courtesy zerohedge)

c)Today the hourly rate increased and that is sending a bad signal to the markets namely because profits will be hit

d)I believe that this job report is a big bunch of crap: the December number includes that a huge 181,000 new jobs were created in the 55 yr old and higher bracket..while the younger sector saw a loss of 11,000 jobs…and the hourly rate goes higher//with WalMart greeters?

the report is a phony

(courtesy zerohedge)

e)This causes markets to soar: Powell is listening carefully to markets. It does not matter..he will

ii)Market data/

a)A very important commentary from Jeffrey Snyder. He comments that the global economy is in big trouble and it is led by the USA.

The highlights two very important points:

- the Eurodollar futures curve

- the oil price/contango/glut we are witnessing

- the huge rise in the GC repo rate by an astonishing 300 basis points.

All 3 measures are indicating that the entire global growth is coming to a halt. The Eurodollar curve futures are falling in the next few years out to 2021 This market is 11 trillion dollars and is almost impossible to manipulate. Investors are voting with their money that interest rates will be falling because of lousy growth. The oil price contango indicates an oil glut caused by the very same lousy global growth. The huge rise in the GC repo rate by 300 points indicates a poor lack of collateral as the growth wanes.

a must read..

( Jeffrey Snider/Alhambra Investment Partners)

d)The impact of the government shutdown is already beginning to hit the economy

iv)SWAMP STORIES

a)Mike Pence on Tucker Carlson: shutdown will continue until the USA gets its wall funding

( zerohedge)

b)The newly elected House defies Trump by voting to reopen government. It has no wall funding so this was a total waste of time

( zerohedge)

c)The newly elected House defies Trump by voting to reopen government. It has no wall funding so this was a total waste of time

( zerohedge)

d)That did not take long: two members of the House are already demanding the impeachment of Trump. Brad Sherman re introduced his bill to impeach him

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI ROSE BY 5 CONTRACTS UP TO 486. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 4004 CONTRACTS DOWN TO 143,455 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) out of Scotia: 2000.083 oz

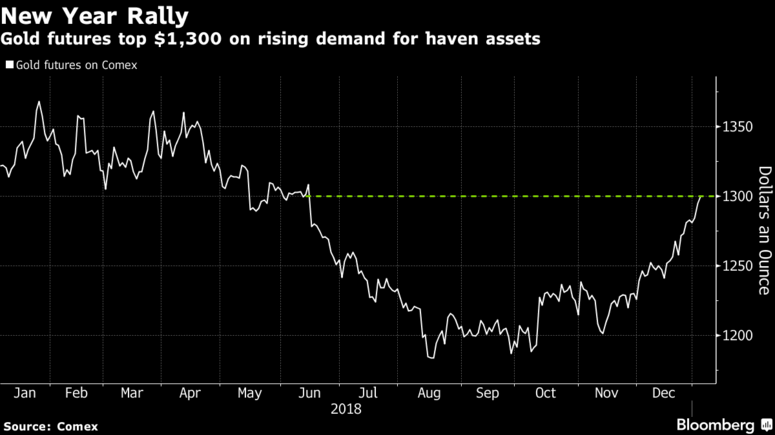

Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold over 6-month high at $1,300 on global slowdown fears

– Bullion surges 5% in December and consolidates on gains this week

– Gold surges to all time record highs in Australian dollars ($1,871)

– Safe haven demand for safe havens as risk assets sold

– Apple’s poor outlook sees stocks fall; Markets now wagering on Fed rate cut

– “2019 is already getting off to a volatile start and we expect to see the political and economic uncertainty of 2018 continue and deepen,” GoldCore told Bloomberg News

Gold price in Australian dollars – 1 year (GoldCore)

We are bullish on gold in this quarter and in 2019 as the market backdrop looks very supportive indeed. For the first time in many years, I am positive on the gold price in the short and medium term – meaning this quarter and the next year or two.

However, we are concerned that gold may have become overbought from a trading perspective in the very short term.

Thus, in the very short term we could see a bit of a pullback. A retracement of some 50% of the recent gains should be expected. A shallow pullback should be greeted as an opportunity to acquire gold at these still under valued levels.

Investors who are allocating to gold for the first time, would be best to dollar, pound or euro cost average into physical gold by buying 50% in the coming days, then 25% in the next month or so and then the remaining 25% withing three to six months. Not having an exposure to physical gold makes investors exposed to major financial and systemic risk.

2019 is already getting off to a volatile start and we expect to see the political and economic uncertainty of 2018 continue and deepen as we told Bloomberg this week.

Gold will continue to act as a hedge in 2019 as it did in 2018.

Gold’s hedging and safe haven credentials were clearly seen again in recent months – especially for UK, EU and Australian investors. Gold gained 2.7% and 3.8% in euros and pounds (see tables & charts). Gold rose 8.5% in Australian dollars in 2018 as the Australian economy slowed down and property and stock markets in Australia fell.

Trade wars, Brexit, EU contagion and the risk of the global debt bubble bursting remain real risks that will likely impact risk assets in 2018, as we discussed in our just released and well received Outlook 2019 Podcast.

We believe risk assets will continue to under perform, while gold (and silver) outperform again in 2019. The record nominal highs seen in Australian dollars this week will be seen in pounds, euros, dollars and other currencies in the coming year or two – possibly as soon as late 2019 or 2020.

As ever, it is prudent to hope for the best but be prepared for less benign financial scenarios by diversification and owning precious metals in the safest ways possible.

Wishing you and yours a healthy and prosperous 2019.

News and Commentary

Gold Bursts Above $1,300 as Slowdown Tremors Spur New Year Rally (Bloomberg.com)

Gold climbs to over 6-month peak on global slowdown fears (Reuters.com)

House passes bill to end government shutdown without border wall money (CNBC.com)

Markets now wagering on Fed rate cut, China-U.S. trade talks calm nerves (Reuters.com)

Apple Woes Send Stocks Swooning as Treasuries Jump (Bloomberg.com)

Source: Bloomberg

Market’s Obstacles Are Both Macro and Micro – GoldCore via Bloomberg (Bloomberg.com)

Safe Havens Are Back: Yen, Gold and Bonds Are Bought as Risk Assets Sold (Bloomberg.com)

Gold Soars Above $1,300; Nikkei, JGB Yields Tumble As Rout Goes Global (ZeroHedge.com)

Why Apple’s sales warning has rattled the currency markets (MoneyWeek.com)

The Bad Stuff That the Stock Market Worried About Is Starting to Happen (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

03 Jan: USD 1,287.95, GBP 1,024.05 & EUR 1,132.62 per ounce

02 Jan: USD 1,287.20, GBP 1,014.44 & EUR 1,125.27 per ounce

31 Dec: USD 1,281.65, GBP 1,005.45 & EUR 1,120.03 per ounce

28 Dec: USD 1,277.25, GBP 1,009.16 & EUR 1,114.91 per ounce

27 Dec: USD 1,271.10, GBP 1,006.20 & EUR 1,115.26 per ounce

24 Dec: USD 1,261.25, GBP 996.26 & EUR 1,105.23 per ounce

21 Dec: USD 1,257.60, GBP 993.76 & EUR 1,101.53 per ounce

Silver Prices (LBMA)

03 Jan: USD 15.53, GBP 12.37 & EUR 13.70 per ounce

02 Jan: USD 15.44, GBP 12.19 & EUR 13.51 per ounce

31 Dec: USD 15.47, GBP 12.11 & EUR 13.51 per ounce

28 Dec: USD 15.30, GBP 12.05 & EUR 13.34 per ounce

27 Dec: USD 15.06, GBP 11.92 & EUR 13.22 per ounce

24 Dec: USD 14.68, GBP 11.60 & EUR 12.88 per ounce

21 Dec: USD 14.69, GBP 11.59 & EUR 12.86 per ounce

Recent Market Updates

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

– Everything Bubble Started Bursting In 2018 – GoldCore Video

– Global Financial System Is ‘Unstable’ and Risk Of ‘Clearing System Seizure’, BIS Warns

– Gold Flowing From West To East and Now To Goldman Sachs

– Brexit Risk Sees Gold Rise To Test EUR 1,100 Per Ounce

– Yellen Warns Another Financial Crisis Is Brewing

– Gold Krugerrand Coin Worth $1,200 Donated To Charity Again

– EU Recession Imminent – Euro Disunion as Brexit, Italy and End of QE Loom

– Gold and Silver Gained 2% and 3% Last Week While Stocks Dropped Nearly 5%

Gold-rich Zimbabwe can’t even cadge a beer anymore

Submitted by cpowell on Thu, 2019-01-03 21:28. Section: Daily Dispatches

Anheuser-Busch InBev Zimbabwe Charges Hard Currency to Fight Dollar Shortage

By John Bowker

Bloomberg News

Thursday, January 3, 2019

Delta Corp Ltd., part owned by Anheuser-Busch InBev SA/NV, told Zimbabwean customers it will accept only hard currency for its beverages as local businesses struggle to cope with foreign-exchange shortages.

The maker of Castle Lager, Chibuku sorghum beer, and a range of soft drinks hasn’t been able to pay some international suppliers for “extended periods,” choking off access to further credit, the Harare-based company told retailers and wholesalers in a letter dated Jan. 2. Delta, which will implement the measure from Friday, isn’t receiving enough foreign currency from banks to pay for imports, it said.

…

Our business has been adversely affected by the prevailing shortages of foreign currency,” wrote Delta, about 23 percent owned by the world’s biggest brewer. This has led to orders not being met or prolonged stock shortages, the company said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-03/ab-inbev-zimbabwe-cha…

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Nicholas B on the huge amount of EFP issuance over the past year:

(courtesy Nicholas B.

Good Afternoon Bill, Harvey

After spending hundreds of hours following the fate of the world last year, I believe that nothing is more catastrophic than the destruction of the eco system as deliberately manufactured by the climate engineers. Dane Wigington believes that humanity has far less than a score of years, at the current rate of deliberate climate destruction, before life on earth dives into a terminal decline. In joint second place (but a long way behind in terms of relative importance) would be the horrendous consequences of 5G and the impact of vaccinations aimed at implementing Agenda 21-an American child apparently has 36 vaccinations before the age of 6. In second place is the UK with 24 vaccinations and both countries exhibit abysmal overall health profiles of their populations,

Now that the final EFP figures for 2018 are completed, it is noteworthy that about three times annual global mine supply (excluding Russia and China) was required in the case of these manipulative paper contracts to subdue the headline price of paper gold, and about four times global mine supply in the case of silver. If you are one of the plethora of commentators who believe that the paper price of the precious metals may rise a little bit in 2019, what is the premise underwriting such forecasts? Naked short, undeliverable paper contracts, in an infinite abundance, dominate the price setting mechanism of the precious metals in the hopelessly corrupt and unregulated futures markets. Why would the price be allowed to rise just a tiny little bit in such circumstances? The only reason would be that the central planners are taking too much strain in suppressing the physical markets, and believe that marginally higher headline paper prices of precious metals might alleviate some of this pressure in the physical markets, where there are copious reports of the unavailability of deliverable metal in any kind of reasonable volume. Fractional reserving in these opaque and hopelessly corrupt markets is reported to be contained within the ‘’narrow’’ parameters of 100 to 500 to one-take your pick .Is it not probable that any indication of unsustainable pressure on physical precious metal price suppression leading to marginal upward pricing adjustments is merely a precursor to the advent of the hegemony of physical metal over vaporous paper contracts and then its ‘rocket time’’.

The collapse of Tower 7 and the consequent conspiracy of silence has been one of many melanomas (or should that be melanomata?) dominating recent USA history. Now at last I hear that these 9/11 crimes will be the subject of a Grand Jury hearing (is that the news that visibly upset the Bush family so much during the funeral?). Who knows! Maybe the criminal conspiracy to suppress physical precious metal will also have its ‘day in the sun’. Just because only one man (Harvey) monitors EFP contracts and otherwise there is a (universal conspiracy of) silence, does not mean that this status quo will continue for ever.

Regards

Nicholas

end

Gold trading today:

Gold Pukes

Because nothing says confidence in monetary and fiscal policy planners like a surge in gold – that cannot be allowed…

Gold punched back into the red for 2019…

Silver is down but not so much…

From fear-driven flows into the precious metal to puking up the barbarous relic in 24 hours… on the back of one data item?

Stocks are almost back to unchanged (blue) but bonds (red) lead the year so far…

Silver has been outperforming gold for the last two weeks…

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8649/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8775 /shanghai bourse CLOSED UP 50.51 PTS OR 2.05%

HANG SANG CLOSED UP 561.67 POINTS OR 2.24%

2. Nikkei closed DOWN 452.81 POINTS OR 2.26%

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 96.15/Euro RISES TO 1.1413

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.99/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 47.92 and Brent: 57.03

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.19%/Italian 10 yr bond yield UP to 2.86% /SPAIN 10 YR BOND YIELD UP TO 1.45%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.67: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.40

3k Gold at $1291.40 silver at:15.73 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 85/100 in roubles/dollar) 68.00

3m oil into the 47 dollar handle for WTI and 57 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.99 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9864 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1259 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.19%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.60% early this morning. Thirty year rate at 2.94%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4144

Global Stocks Surge On Renewed Trade Optimism, Chinese RRR Cut

The global market rollercoaster continues, with stocks around the world surging on the back of renewed trade optimism and a Chinese RRR cut one day after a vicious rout hit equities following the unexpected Apple guidance cut and a miserable US manufacturing ISM print.

Stocks climbed in Europe and Asia and U.S. equity futures indicated a sharply higher open after the US and China confirmed fresh trade negotiations next week, while havens slipped, as Treasuries fell, the yen weakening and gold dipped after hitting $1,300 overnight.

After initially trading lower, S&P futures rebounded after news that vice ministers from the two countries are preparing to hold talks starting Monday, and were trading 1.4% higher on Friday morning after tumbling 2.5% on Thursday.

Optimism for a resolution to the U.S. government shutdown and over trade talks could ease two of the major overhangs that have dogged equities in recent days. The talks will be the first face-to-face negotiation between the two countries since President Donald Trump and his counterpart Xi Jinping agreed to a 90-day truce in their trade war last month.

“I wouldn’t be surprised if we get better communication on trade,” said Stefan Hofer, chief investment strategist at LGT Bank. Still, “we have beginning-of-the-year jitters, low levels of liquidity and exaggerated swings, which feed people’s worst fears — which I simply can’t sign up to at the moment.”

The Stoxx Europe 600 Index also rebounded from two days of losses as every sector advanced led by basic resources and commodity stocks, even as activity among euro zone businesses dipped to its weakest in just over four years in December as their already downbeat expectations also turned more pessimistic, a survey showed on Friday. Markit’s Euro Zone Composite Final PMI held above the 50 mark that separates growth from contraction, but fell to 51.1 from November’s 52.7, also below a flash reading of 51.3 (Services PMIs were as follows: Spain 54.0 vs 53.7 est; Italy 50.5 vs 50.1 est; France 49.0 vs 49.7 est; Germany 51.8 vs 52.5 est; Eurozone 51.2 vs 51.4 est.). That will be disappointing news for policymakers at the European Central Bank, who ended their 2.6 trillion euro ($2.95 trillion) asset purchase program – one of the main sources of stimulus for the bloc’s economy – last month.

IHS Markit PMI™@IHSMarkitPMI

Earlier, most Asian markets ended higher. Stocks in Japan were the exception, as traders there returned from a holiday, and were catching down to the USDJPY flash crash earlier this week.

Adding to the optimistic tone was a long overdue liquidity injection by the Chinese central bank which cut the required reserve ratio by 1% to release cash into the economy and support rapidly stalling growth. The RRR for banks will drop by 0.5 percentage point on January 15 and a further 0.5 percentage point on January 25, the PBOC said on its website. And yet despite the market’s euphoric take, the PBOC action is far less than meets the eye as the PBOC also announced that its Medium-term Lending Facility loans maturing in the first quarter won’t be rolled over, and the amount of liquidity released will only be able to offset the funding squeeze ahead of the Chinese New Year. So while the cut will release a net 800 billion yuan ($116 billion) of liquidity, it will merely go to replenish liquidity that will be lost to the MLF and continued reverse repo liquidity withdrawals, dousing hopes that “this is it” and China is finally injecting massive amounts of liquidity into the economy.

The latest reduction announced is the first all-inclusive RRR cut since March 2016. China’s top leaders have pledged to keep monetary policy prudent while striking an “appropriate” balance between tightening and loosening in 2019, part of the steps to ratchet up stimulus to support growth. Ahead of the news, which came after China’s markets closed, the Shanghai Composite closed 2.0% higher, while the offshore yuan pared gains slightly to trade 0.1% higher at 6.8763 per dollar.

Traders will now be watching today’s key economic event – the December jobs report – for evidence of how U.S. employers capped a strong year of the scorching US labor market, and as we previewed overnight, should the report surprise strongly to the upside it may be a traditional case of “good news is bad news.”

Fed Chair Powell is also due to take part in the American Economics Association annual meeting along with former Chairs Yellen and Bernanke this morning. Powell is not expected to break any new ground but it will be worth seeing if he reiterates the message made by NY Fed President Williams when he flashed out in more granular detail in the Fed’s messaging in the December statement, specifically addressing the slight tweak in forward guidance. Clearly any comments around recent market volatility and also yesterday’s ISM report will be closely watched too.

Elsewhere, the dollar was largely steady while the yen trimmed some of the big jump from a day earlier and the Aussie dollar rallied as China confirmed trade talks with U.S. next week; gold slipped after touching $1,300 overnight. GBP/USD gained in line with risk-sensitive currencies, failing to get a boost from slightly better-than- expected U.K. services data

Treasury yields led most government bond rates higher. Italian bonds bull steepen, while Bunds fell to day lows after PBOC move.

Elsewhere, oil built on recent gains, with Brent crude heading for its biggest weekly advance since 2016 as traders weighed signs that OPEC is following through on production cuts against hints of an economic slowdown. OPEC cut crude output in December, a Reuters survey showed, and the American Petroleum Institute (API) reported a 4.5 million-barrel drop in crude inventories. Brent crude was up $1.25 to $57.20 a barrel at 1113 GMT, while WTI was up 90 cents at $47.99.

“Recent Chinese data is not confirming the doom-and-gloom trend,” said Olivier Jakob, oil analyst at Petromatrix. “And you’ve got OPEC cutting.”

In addition to payrolls, Fed Chair Powell will make first public remarks since Dec. 19 at the annual meeting of the American Economic Association in Atlanta. Expected data include December’s jobs reports, while Lamb Weston, Cal-Maine Foods are due to report earnings

Market Snapshot

- S&P 500 futures up 1.3% to 2,479.50

- STOXX Europe 600 up 1.3% to 338.22

- MXAP down 0.2% to 145.22

- MXAPJ up 0.9% to 469.31

- Nikkei down 2.3% to 19,561.96

- Topix down 1.5% to 1,471.16

- Hang Seng Index up 2.2% to 25,626.03

- Shanghai Composite up 2.1% to 2,514.87

- Sensex up 0.6% to 35,728.09

- Australia S&P/ASX 200 down 0.3% to 5,619.36

- Kospi up 0.8% to 2,010.25

- German 10Y yield rose 2.7 bps to 0.18%

- Euro up 0.2% to $1.1415

- Brent Futures up 1.5% to $56.79/bbl

- Italian 10Y yield rose 16.5 bps to 2.5%

- Spanish 10Y yield rose 1.0 bps to 1.439%

- Brent Futures up 1.5% to $56.79/bbl

- Gold spot down 0.3% to $1,290.57

- U.S. Dollar Index down 0.2% to 96.14

Top Overnight News

- China’s central bank said that it will cut the required reserve ratio by 0.5 percentage point on Jan. 15 and further by 0.5 percentage point on Jan. 25, acting to release cash into the economy to support growth

- China said a U.S. delegation will visit next week for trade talks, confirming the two sides will have their first face-to- face negotiation since President Donald Trump and his counterpart Xi Jinping agreed to a 90-day truce in their trade war last month

- A YouGov poll of Tory members found that in a three-way referendum, 57% of them would prefer to leave EU with no deal, 23% would choose Prime Minister Theresa May’s deal and 15% would choose remaining in EU, Telegraph reports, citing the survey carried out for the Economic and Social Research Council- funded Party Members Project

- The new House Democratic majority voted Thursday to end the partial government shutdown but brought Congress no closer to resolving the impasse over Trump’s demand to pay for a border wall

- Japan’s benchmark bond yield fell to the lowest in more than two years as a stronger yen and a slowdown in global manufacturing spurred demand for the assets as a haven

- The bond market’s aggressive overhaul of its outlook for Federal Reserve policy is creating kinks in the front end of the Treasury yield curve. Yields on the two- and five-year sectors fell relative to shorter-dated maturities Thursday, causing portions of the curve to invert

- President Donald Trump’s trade war with China will force many U.S. companies to join Apple Inc. in announcing lower than expected earnings, the chairman of the White House Council of Economic Advisers said. Among U.S. companies issuing estimates for the fourth quarter, 46 percent have revised the outlook lower

- Gold advanced above $1,300 an ounce to extend a new year rally

- German unemployment fell to a record low, extending its five-year decline, as companies signaled confidence in Europe’s largest economy

- U.K. house price growth slowed to five-year low at 0.5% in 2018, down from 2.6% a year earlier, according to data by Nationwide Building Society

Asian equities were mixed following the slide in US stocks as disappointing ISM manufacturing data added to global growth fears after Apple’s trade-related profit warning. The Dow shed in excess of 600 points while the S&P fell further below the 2500 level and the Nasdaq tumbled 3.0% as the tech sector fell over 5.0%. ASX 200 (-0.3%) and Nikkei 225 (-2.2%) both failed to benefit from the higher base metal prices as the indices bore the brunt of the tech decline on Wall St, while the latter also played catch-up after a week-long holiday. Elsewhere, Hang Seng (+2.4%) and Shanghai Comp. (+2.0%) outperformed after erasing opening losses as almost all Chinese sectors turned green (gains led by oil names and financial firms) on the back of constructive trade developments, with China’s MOFCOM confirming that trade talks with the US are to take place next week, while the release of above-forecast Caixin services PMI exacerbated gains in the bourses.

Top Asian News

- China, U.S. to Hold Vice-Minister Level Trade Talks Jan. 7-8

- Huawei Demotes Workers After Embarrassing Tweet From An iPhone

- India Government Says It’s on Track to Meet Electricity Deadline

- China Stocks Rebound After Bleak Start to 2019; Brokerages Jump

Major European equities are in the green [Euro Stoxx 50 +1.2%] with the SMI (+0.5%) lagging its peers, weighed on by underperformance in the healthcare sector with index heavyweights Roche (-0.2%) and Novartis (-0.1%) in the red. All sectors, including the aforementioned healthcare sector, are in the green with outperformance seen in materials on the back of positive China trade developments. Mining names such as Thyssenkrupp (+3.5%) and Anglo American (+2.8%) sit towards the top of the Stoxx 600. Other notable stories include BMW (+1.6%) and Volkswagen (+1.3%) who are up after reporting increased US December vehicles sales of +0.3% and +5.0% respectively. Elsewhere, Bayer (+3.3%) are higher after the federal judge overseeing lawsuits alleging that their glyphosate-based weed killer causes cancer has granted the Co’s request to split the upcoming trial into two phases.

Top European News

- German Unemployment Falls Despite Mounting Risks to Economy

- Soft Services Expansion Brings U.K. Economy Close to Stagnation

- Ghosn to Get a Day in Court Almost Two Months After Shock Arrest

- Poll Shows Most Tories Would Choose No-Deal Brexit: Telegraph

Price action for FX markets thus far has been significantly more orderly than the JPY-inspired volatility seen on late Wednesday as traders await key macro and central bank updates. Starting with the JPY, the Japanese currency has given back some gains to its major counterparts with USD/JPY hovering around the 108.00 level. The story for USD/JPY is more one of JPY weakness rather than USD strength with the DXY in negative territory, albeit still on a 96.00 handle. From a JPY perspective, Japan MOF’s Currency Head Asakawa stated overnight that he is worried about the volatile FX moves and will take steps on forex if needed. Going back to the USD, given recent disappointing macro data, today’s jobs reports from the US will be one of the more pertinent ones as of late from a Fed-perspective. Given the recent market turmoil, markets now fully price in a rate cut by April 2020 vs. the Fed’s view of two hikes in 2019 and one hike in 2020. Amid the starkly opposing views, an out of line report could have major ramifications for the USD either way. However, with Powell speaking two hours after the release, moves in the DXY may lack some conviction as participants await the latest communication from the Fed Chair.

- Elsewhere, EUR/USD has been able to capitalize on the USD weakness and retain status on a 1.1400 handle within the mid-point of its 2019 range thus far. On the data front, core EZ service PMI readings fell short of analyst estimates who had forecast unchanged readings from the prior report. This was then followed by EZ-wide inflation metrics which revealed a decline in headline CPI Y/Y to 1.6% from 1.9% vs. Exp. 1.8% but did little to place any major weight on the multi-bloc currency.

- GBP is exerting some strength against its major counterparts as GBP/USD continues to extend its post-flash crash ascent with the move pausing for breath after breaching Monday’s low of 1.2682. The Pound was unable to garner much in the way of support despite a beat on the all-important Services PMI (51.2 vs. Exp. 50.7) with Markit suggesting “The meagre service sector expansion recorded in December is indicative of the economy growing by just 0.1% in the closing quarter of 2018”.

- AUD/USD has continued to extend its advance above 0.7000 with traders looking to see if the antipodean can see the week out above the psychological level and thus spur hopes for a near-term recovery. AUD was given a further helping hand briefly after the PBOC announced a 100bps cut to bank’s RRR. However, the move higher will fleeting given it had already been touted by Premier Li and was seen as more of a targeted adjustment to cover the Lunar New Year period rather than an unveiling of major stimulus.

In commodities, Brent (+2.2%) and WTI (+2.2%) prices are higher, with WTI trading around the USD 48.00/bbl level and Brent just above the USD 57.00/bbl level. This support comes after a larger than expected draw in API weekly crude stocks of -4.5mln vs. Exp. -3.1mln, with markets now looking towards today’s EIA release. In addition, the Iraq oil ministry has reportedly taken measures to cut output by 3% from October’s level of 4.653mln BPD. Elsewhere, Energy Intel’s Amena Bakr has tweeted that Saudi Arabia are to announce a jump in oil reserves. Gold (-0.2%) has turned negative as the positive trade news from China improved the risk sentiment, with the yellow metal trading just over USD 1290/oz. Additionally, copper prices have improved on the back of positive Chinese trade news with the metal recovering from a 18-month low hit in the previous session.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 183,500, prior 155,000

- 8:30am: Unemployment Rate, est. 3.7%, prior 3.7%

- 8:30am: Average Hourly Earnings MoM, est. 0.3%, prior 0.2%; YoY, est. 3.0%, prior 3.1%

- 8:30am: Average Weekly Hours All Employees, est. 34.5, prior 34.4

- 8:30am: Underemployment Rate, prior 7.6%

- 9:45am: Markit US Composite PMI, prior 53.6; Markit US Services PMI, est. 53.4, prior 53.4

DB’s Jim Reid concludes the overnight wrap

It’s fair to say that the holiday period for markets is well and truly over with the ghost of 2018’s past rearing its ugly head for risk assets yesterday. To be fair it never really felt like markets took a break, given some of the violent price action that we’ve seen in the last couple of weeks, but the early focus yesterday was all about the double whammy of Apple shares crashing following their revenue guidance cut and then the compounding pain of a much worse-than-feared US ISM manufacturing report.

The end result was -2.48%, -2.83% and -3.04% declines for the S&P 500, DOW and NASDAQ respectively. The S&P 500 has now traded down by at least -2% on six occasions in the last month, the worst such streak since September to October 2011. In addition to the two main factors mentioned above, sentiment was further hurt by additional ratcheting up of US-China tensions. White House Adviser Kevin Hassett said in reference to the Apple announcement that “it’s not going to be just Apple” and that “there are a heck of a lot of US companies that have sales in China that are going to be watching their earnings being downgraded next year until we get a deal with China”. Separately, the US State Department issued a travel warning for US nationals in China, further evidencing that the clash may be escalating beyond the realm of trade and tariffs. Overnight we’ve learned that delegations from China and the US will meet for talks on January 7th and 8thin Beijing although the US Chamber of Commerce has already warned not to expect any major breakthroughs. This will be the first set of talks since Presidents Trump and Xi Jinping agreed to a 90-day truce last month.

Somewhat fittingly, Apple proved to be a perfect example of the feedback from China. Its shares plummeted -9.96% for the biggest drop since January 2013 and to the lowest level since April 2017. Each of Microsoft, Amazon, and Alphabet have all now overtaken Apple in the biggest company in the world table, with Apple’s market cap down -$75bn alone yesterday. The total market value decline since Apple’s peak last October is -$446bn, or the equivalent of Coca-Cola and Pfizer combined. As a result the NYSE FANG index tumbled -3.77% while there were also notable falls for other large caps like Caterpillar (-3.92%), 3M (-3.84%) and DowDupont (-3.63%). In credit markets US HY spreads finished +11bps wider and CDX HY widened +6bps. Benchmark 10-year Treasury yields also rallied -9.2bps from their intraday highs to close -6.7bps lower on the day at 2.554% which is the first time that we’ve seen Treasuries with a 2.5%-handle since January 17th last year. Two-year yields declined -9.0bps to trade below the fed funds rate for the first time since October 2008. The curve steepened slightly to 17.3bps however the 2s5s curve touched a new cyclical low of -4.4bps before retracing to end the session 1.0p lower at -2.3bps. Meanwhile, Gold benefited from the risk off tone to close up +0.75% while Copper shed -2.10%.

The good news is that sentiment has improved in Asia overnight with the Hang Seng (+1.41%), Shanghai Comp (+1.81%) and Kospi (+0.60%) all up as we go to print. The Nikkei (-2.82%) is sharply lower however is playing catch up after markets in Japan were closed for holidays. That news we mentioned earlier about China and the US planning to meet appears to be helping the more constructive tone, as is the stronger than expected Caixin services PMI out of China this morning (53.9 vs. 53.0 expected) and news that China will strengthen its counter-cyclical macro policy adjustment and cut taxes and fees to support small and private companies. Meanwhile, US futures are also up (+0.51%) after the new US House Democratic majority voted to end the partial government shutdown. This still needs to be taken with a pinch of salt as Congress is no closer to resolving the impasse over President Donald Trump’s demand to pay for a border wall.

Brexit headlines are also back with the Telegraph reporting that a YouGov poll of Tory members found that in a three-way referendum, 57% of them would prefer to leave the EU with no deal, 23% would choose Prime Minister Theresa May’s deal and 15% would choose to remain in the EU. Interestingly, if the options are down to two i.e., May’s deal or no deal, only 29% of Tory members said they would vote for May’s deal, while 64% said they would vote to leave without a deal, with the remainder undecided. The poll also found 59% of Tory members are opposed to the current EU Withdrawal Agreement, with just 38% supporting it and the rest unsure.

Back to yesterday, where that ISM manufacturing print that we noted above came in at 54.1 compared to expectations for 57.5 and a reading of 59.3 in November. So that is now the lowest reading since November 2016 and the biggest one-month drop since October 2008. The blame game laid with the new orders component which fell a staggering -11pts to 51.1 and the lowest now since January 2016. The employment component slid a comparatively more palatable -2.2pts to 56.2 while the prices paid component fell -5.8pts to 54.9 and to the lowest since June 2017. The associated statement also highlighted that six industries reported a contraction in December and that “growth appears to have stopped” and “resources are still focused on re-sourcing for US tariff migration out of China”. Trade issues were highlighted numerous times.

The big question now is: what will the Fed do, and could we see them start to shift further from their tightening stance to one closer to neutral? DB’s Alan Ruskin made an important point yesterday though which is that while the latest ISM reading looks weak relative to recent past, it is still consistent with above trend rates of growth. Clearly though, the market will be super sensitive to the next round of data and especially the first round of January prints to see if there’s further downward momentum (US economic surprises are at 16-month negative levels now). It’s worth noting that the market has become so sceptical about the Fed that we’re now down to -18bps of cuts in 2019, or in other words a 75% chance of a full cut. That compares to over 2 hikes that were being priced in for 2019 at the peak in November. So it’s been a remarkable shift in sentiment.

It’s apt timing then that today we’re got a couple of potentially pivotal events to look forward to. Will the final employment report for the US in 2018 change the tide today, extend the pain, or will markets shrug it aside? The main focus should be on the earnings figure with the consensus currently pegged at a +0.3% mom average hourly earnings print for December with base effects expected to lower the year-on-year reading to +3.0%. That matches the forecasts of our US economists and they also expect average weekly hours to kick up a tenth 34.5 hours. Interestingly they note that this would imply a very healthy +4.9% annual pace of nominal income growth and is one reason why they believe bond market participants may be underappreciating the Fed’s ability to further hike rates this year. As for payrolls, the market is at 180k (vs. 155k in November) while our house view is for 175k. Our team believe that this will be sufficient to lower the unemployment rate to 3.6%.

Shortly after that, Fed Chair Powell is due to take part in the American Economics Association annual meeting along with former Chairs Yellen and Bernanke at 3.15pm GMT. We’re not expecting Powell to break any new ground but it will be worth seeing if he reiterates the message made by NY Fed President Williams when he flashed out in more granular detail in the Fed’s messaging in the December statement, specifically addressing the slight tweak in forward guidance. Clearly any comments around recent market volatility and also yesterday’s ISM report will be closely watched too.

Speaking of the Fed, yesterday we heard from Dallas Fed President Kaplan. Although a non-voter this year, Kaplan advocated for the Fed to take a pause on the tightening cycle “in the first couple of quarters this year” and also added that “my base case would be no action at all”. Kaplan cited the softer global growth outlook, deceleration in interest-rate sensitive sectors, and tighter financial conditions as evidence that a pause is warranted. He also mentioned “there are a number of things we could do” to slow the pace of balance sheet normalization, but stressed that “I’m not there yet.” It’s worth noting that Kaplan has been slightly more dovish that the centre of the committee and also has previously highlighted concerns from some of the signals from markets including the recent flattening in the curve. So although dovish the tone wasn’t a complete surprise.

Jumping ship, in today’s EMR we’ve updated our equity versus PMI charts and table which you can find in the PDF in which we regress PMIs versus year over year changes in equity markets. This follows the latest round of PMIs in Europe and China and the ISM reading in the US. The numbers make for fairly eye watering reading now. While PMIs have dropped from their highs fairly significantly, the plunge in equity markets has far outweighed this and in fact we’re pricing in implied PMIs of between 42.3 and 45.6 in Europe, 43.6 in the UK, 46.0 in China and an ISM of 46.6 in the US. Indeed on this basis equity markets are 18% ‘cheap’ in the US, between 11% (Italy) and 25% (Germany) cheap in Europe and 30% cheap in China. As we always say with this the data it is intended as a guide and best to look over a longer period of time rather than for a particular point but it still makes for an interesting read-through.

Back to yesterday, where for completeness, it wasn’t much better for markets in Europe although bourses did at least hold out better than US markets. The STOXX 600 finished -0.98% while the DAX and CAC were -1.55% and -1.66% respectively. HY cash spreads were +10bps wider while Crossover was +12bps wider. Senior and sub financials also got hit to the tune of +6bps and +14bps respectively. Meanwhile Bunds closed at 0.150% and the lowest since November 2016 while the risk off moves appeared to hit BTPs (in addition to news that Banca Carige was going into administration) where yields rose +16.8bps and the most since September.

Wrapping up the other data that was out yesterday, mortgage applications fell -8.5% last week to their lowest level since 2000. The ADP employment report showed a net increase of 271k jobs last month, more than the 179k expected though the November figure was revised down by 22k. Initial jobless claims ticked up +15k but remain near their cyclical lows. In the UK, the construction PMI softened to 52.8 from 53.4.

Finally to the day ahead, where the highlight no doubt comes this afternoon with the aforementioned US employment report. Prior to that though we get the final December PMIs (services and composite readings) in Europe including a first look at the data for the non-core and UK, as well as the preliminary December CPI reading in France, Italy and the Euro Area. For the latter, the core is expected to hold steady at +1.0% yoy but the headline decline three-tenths to +1.7% yoy as a result of the oil price move. We’ll also get November money and credit aggregates data in the UK. Meanwhile, also out in the US this afternoon are the final December PMIs. A final reminder that Fed Chair Powell speaks today along with Yellen and Bernanke, while the Fed’s Barkin also speaks later this evening.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 50.51 PTS OR 2.05% //Hang Sang CLOSED UP 561.67 POINTS OR 2.24% /The Nikkei closed DOWN 452.81 POINTS OR 2.26% / Australia’s all ordinaires CLOSED DOWN 0.31%

/Chinese yuan (ONSHORE) closed UP at 6.8649 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 47.92 dollars per barrel for WTI and 57.03 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.8649 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8775: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

China Announces RRR Cut Plans To Cover Lunar New Year Liquidity

US equity futures extended gains in a kneejerk reaction to headlines proclaiming China cutting the reserve requirement ratio.

The headline looks impressive…

- CHINA CUTS BANK RESERVE RATIO BY 1 PERCENTAGE POINT

And the algos liked it…

However, two points make this less exciting “stimulus” news than we suspect the narrative will proclaim.

First is that, according to a statement from the central bank, the RRR cuts of 0.5 percentage point each will occur on Jan. 15 and Jan. 25 in a move to offset liquidity fluctuations ahead of Chinese Lunar New Year.

- PBOC says the RRR cuts to replace medium-term lending facilities maturing in 1Q

- PBOC says it will continue prudent monetary policy and won’t flood economy with liquidity

- PBOC says move to boost financial support for small and private companies

- PBOC to ensure reasonable growth of credit and aggregate financing

- PBOC to stabilize macro leverage ratio

In other words this is ‘business as usual’ monetary injection to cover an increasingly panicked financial system dry of liquidity.

And second is that, recent previous monetary and fiscal easing efforts have utterly failed to generate any material economic activity pick up. As we noted previously, since June 2018, China has been loosening monetary and fiscal policies in an attempt to refloat the sinking red ponzi amid the shadow banking system’s deflation.

As the following chart from Goldman Sachs shows, it is not working as the Current Activity Indicator continues to slump…

It seems no matter what China throws at it, the economy (or the market) won’t behave as the text-books say it should.

As Goldman previously concluded: “There are reasons to be concerned [that easing is becoming less effective]...”

Beijing Has Detained 13 Canadians Since Arrest Of Huawei CFO

When the US published its latest travel advisory warning its citizens about the “arbitrary law enforcement” risks they could face in China (and offering a list of recommended precautions for those obstinate enough to ignore the government’s warnings), some wondered, why now? With trade negotiations set to begin in earnest next week, one would think that the US wouldn’t want to kick the hornet’s nest (though, in fairness, the DOJ’s steady stream of indictments against Chinese government-sponsored hackers have continued, as has the prosecution of Huawei CFO Meng Wanzhou).

Well, Canada’s Globe and Mail might have just answered that question by confirming that the Beijing’s suspected retaliation against Ottawa over Meng’s arrest has been even more severe than previously believed. According to the paper, 13 Canadians have been detained in China since Dec. 1 – the day Meng was arrested by Canadian authorities after landing in Vancouver.

Spavor and Kovrig

Until now, the arrests of only three Canadians – those of businessman Michael Spavor, former diplomat Michael Kovrig and teacher Sarah McIver (who has been deported) – had been publicly known.

Fortunately, eight of the 13 detainees have been released. And the Canadian government has so far refused to confirm the identities of the other 10.

But still, the report begs the question: Why has Justin Trudeau’s government been so reluctant to issue a travel advisory of its own, as conservative lawmakers have been urging him to do?

Global Affairs Canada spokesman Guillaume Bérubé said in a statement to The Globe and Mail that the government is aware that 13 Canadians have been detained in China, excluding Hong Kong, since Dec. 1, 2018. Previously, only Michael Kovrig, Michael Spavor and Sarah McIver were publicly known to have been detained in China since Canada arrested Ms. Meng, chief financial officer of Huawei Technologies Co. Ltd. They were taken into custody after China promised retaliation for Ms. Meng’s arrest.

Mr. Bérubé said in the statement that at least eight of the 13 have been released. Global Affairs Canada did not disclose the identities of the other 10 Canadians.

Meanwhile, a top Chinese prosecutor said this week that Spavor and Kovrig had “without a doubt” violated laws pertaining to national security – though some suspect that this is merely a ruse to hold them in custody, since Chinese law offers broad latitude to authorities when it comes to issues of national security. McIver has been released and returned to Canada, but that’s all that is known about the releases.

All told, some 200 Canadians are involved in some form of legal proceedings in China for a variety of alleged crimes and infractions – including one man who has been accused of smuggling “an enormous amount” of drugs into the country. Many are out on bail or on probation. Over the years, the number of Canadians detained in China has remained relatively constant (by comparison, some 900 Canadians are being held in US jails).

But that doesn’t mean the recent spike in arrests isn’t troubling.

As Tory lawmakers push for Canada to issue a travel advisor of its own, some report hearing anecdotal evidence about a spike in detentions of westerners in China.

The Conservatives are urging the government to issue a new travel warning for China in light of the detentions on Dec. 10 of Mr. Kovrig, an analyst for the non-profit organization International Crisis Group, and Mr. Spavor, who owns an organization that brings visitors to North Korea.

Tory foreign affairs critic Erin O’Toole said he is concerned China is also using “administrative harassment” of Canadians, such as Ms. McIver, as retaliation. He said he is hearing from parents who are anxious about adult children teaching in China.

“In one case, there was a mother speaking to me about her son who had seen some other Western-looking teachers picked up by authorities on the street. Now, I have no idea if those were Canadians, but this was a son telling his mother, ‘I’m a little concerned about what I see to be a bit more of a security interest in westerners,'” Mr. O’Toole said.

And rightfully so. China has likened Meng’s detention to a kidnapping and has warned Ottawa to “prepare for escalation.”

In its travel advisory, the US warned about Beijing’s tendency to issue “exit bans” for foreigners without informing the target – sometimes they don’t learn of the ban until they try to leave China and are stopped at airports or the border.

It’s just the latest reason why any Westerners living or traveling on the mainland might want to considering getting out of Dodge.

END

this will certainly get under the skin of Xi: the senate seeks an aggressive clamp down on Chinese tech espionage. This is a good part of their business

(courtesy zerohedge)

Senate Bill Seeks Aggressive Clamp Down On Chinese Tech Espionage

After top FBI officials testified before the Senate Judiciary Committee last month that Chinese espionage poses the “most severe” threat currently facing American security, and after greater scrutiny of major Chinese telecommunications that had before operated with seeming impunity in the US like Huawei Technologies Co. and ZTE Corp. — especially following the arrest of Huawei’s CFO Meng Wanzhou and others in Canada — senators are now proposing a bill to combat technology threats from China.

Senators Mark Warner and Marco Rubio during a previous press conference on Russian election meddling. via GettySenators Mark Warner and Marco Rubio are co-sponsoring legislation that seeks to counter the risk of state-sponsored technology theft by establishing an “Office of Critical Technologies and Security” overseen by the White House. The bill would add greater teeth and oversight to current Trump administration efforts to quash Chinese attempts at stealing technology secrets from US firms, which often also involves supply chain infiltration at foreign manufacturing sites, following a related bill signed into law last August which attempted to strengthen a panel that reviews foreign-based investments in the US for national security risks, but which was widely viewed as “watered down” when it came to China.

Senators Mark Warner and Marco Rubio during a previous press conference on Russian election meddling. via GettySenators Mark Warner and Marco Rubio are co-sponsoring legislation that seeks to counter the risk of state-sponsored technology theft by establishing an “Office of Critical Technologies and Security” overseen by the White House. The bill would add greater teeth and oversight to current Trump administration efforts to quash Chinese attempts at stealing technology secrets from US firms, which often also involves supply chain infiltration at foreign manufacturing sites, following a related bill signed into law last August which attempted to strengthen a panel that reviews foreign-based investments in the US for national security risks, but which was widely viewed as “watered down” when it came to China.

Mark Warner (D-VA) described, “It is clear that China is determined to use every tool in its arsenal to surpass the United States technologically and dominate us economically.” Continuing his Friday statement, he said, “We need a whole-of-government technology strategy to protect U.S. competitiveness in emerging and dual-use technologies and address the Chinese threat.”

And Rubio (R-FL) specified the China tech theft threat as follows:

China continues to conduct a coordinated assault on U.S. intellectual property, U.S. businesses, and our government networks and information with the full backing of the Chinese Communist Party.

Rubio added, “The United States needs a more coordinated approach to directly counter this critical threat and ensure we better protect U.S. technology.”

This follows months of multiple major instances of China caught in brazen acts of theft of American technology and trade secrets, though which only very slowly picked up steam in the mainstream media.

Trump has consistently blasted China’s “unfair trade practices” which includes stealing US intellectual property as the “cost of doing business” with Beijing. The issue has sent tensions soaring amidst a trade war that’s already disrupted the flow of hundreds of billions of dollars worth of goods, potentially slowing growth.

Last month Presidents Trump and Xi Jinping called for a truce in their escalating trade war following a sideline meeting at the G20 summit in Buenos Aires, and starting early next week the two sides are set to hold governmental trade talks in Beijing (Jan 7-8).

4.EUROPEAN AFFAIRS

/EMU

The European Monetary Zone is generally a good manufacturing producer led by Germany etc. Today the Eurozone PMI slipped to almost contraction, coming in at 51.1 in December, its weakest report in almost 4 years;

(courtesy zerohedge)

Eurozone PMI Plunges To Four Year Lows

US, China, and now European composite PMIs have all tumbled in December with Eurozone PMI slipping to 51.1 – its weakest in four years

Growth in manufacturing and services slowed more than initially reported in December – weighed down by public protests in France, Germany’s continued struggles in the car industry, and renewed weakness in Italy. Composite gauges for output expectations and new orders were the worst since late 2014.

Under the hood, the European nations are highly varied (from best to worst):

- Ireland: 55.5 (9-month low)

- Spain: 53.4 (3-month low)

- Germany: 51.6 (66-month low)

- Italy: 50.0 (3-month low)

- France: 48.7 (49-month low)

Chris Williamson, Chief Business Economist at IHS Markit said:

“The eurozone economy moved down another gear at the end of 2018, with growth down considerably from the elevated rates at the start of the year. December saw business activity grow at the weakest rate since late-2014 as inflows of new work barely rose. Levels of unfinished business are now falling for the first time in nearly four years as previously-received orders are not being fully replaced with new work.

“While a drop in business activity in France could be partly blamed on the ‘yellow vest’ protests, the rest of the region lacks any such mitigating factors, albeit with the recent weakness of the autos sector hopefully a temporary set-back.

“Importantly, with expectations of output dropping to the lowest for over four years, companies are not anticipating any imminent revival in demand. Worries reflect multiple headwinds from trade wars, Brexit, heightened political uncertainty, financial market volatility and slower global economic growth.

“Employment growth has already taken a knock as companies take a more cautious approach to hiring in the face of weaker order books. Jobs growth has hit a two-year low.

“Better news came in the form of an easing in price pressures to the lowest for over a year, which should provide some breathing space for the European Central Bank to review its policy guidance.”

Finally, Williamson confirms this survey signals weakness ahead…

“The data are consistent with eurozone GDP rising by just under 0.3% in the fourth quarter, but with quarterly growth momentum slowing to 0.15% in December.

How long before Draghi reverses to easing again?

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN/USA