GOLD: $1291.00 UP $6.00 (COMEX TO COMEX CLOSINGS)

Silver: $15.70 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1293.50

silver: $15.75

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 46 NOTICE(S) FOR 4600 OZ (0.1430 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 444 NOTICES FOR 44400 OZ (1.3810 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

22 NOTICE(S) FILED TODAY FOR 110,000 OZ/

total number of notices filed so far this month: 320 for 1,600,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3975: UP 18

Bitcoin: FINAL EVENING TRADE: $3967 UP 12

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 11/46

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,283.200000000 USD

INTENT DATE: 01/08/2019 DELIVERY DATE: 01/10/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C MERRILL 4

657 C MORGAN STANLEY 3

657 H MORGAN STANLEY 5

661 C JP MORGAN 11

737 C ADVANTAGE 22 11

800 C RCG 21 12

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 46 46

MONTH TO DATE: 444

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN HUGE SIZED 4844 CONTRACTS FROM 181,546 UP TO 186,506 DESPITE YESTERDAY’S 4 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2475 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2475 CONTRACTS. WITH THE TRANSFER OF 2475 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2475 EFP CONTRACTS TRANSLATES INTO 4.89 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.170 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 17,264 CONTRACTS (FOR 6 TRADING DAYS TOTAL 17,264 CONTRACTS) OR 86.320 MILLION OZ: (AVERAGE PER DAY: 2877 CONTRACTS OR 14.388 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 86.320 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.32% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 86.320 MILLION OZ.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4844 DESPITE THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 2475 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 7319 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2475 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4844 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.66 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 22 NOTICE(S) FOR 1200,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.170 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUGE 9011 CONTRACTS DOWN TO 455,232 WITH THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $3.70//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8444 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 8444 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 455,232. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN TINY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 567 CONTRACTS: 9011 OI CONTRACTS DECREASED AT THE COMEX AND 8444 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 567 CONTRACTS OR 56700 OZ = 1.76 TONNES. AND ALL OF THIS VERY GOOD DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.70

YESTERDAY, WE HAD 5365 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 53,823 CONTRACTS OR 5,382,300 OZ OR 167.41TONNES (6 TRADING DAYS AND THUS AVERAGING: 8970 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 167.41 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 167.41/2550 x 100% TONNES = 6.56% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 167.41 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 9011 WITH THE LOSS IN PRICING ($3.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8444 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8444 EFP CONTRACTS ISSUED, WE HAD A TINY LOSS OF 567 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8444 CONTRACTS MOVE TO LONDON AND 9011 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 1.76 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $3.70 IN YESTERDAY’S TRADING AT THE COMEX

we had: 46 notice(s) filed upon for 4600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP$6.00 TODAY

TWO TRANSACTIONS:

I)A MINOR WITHDRAWAL OF .25 TONNES AND THAT IS GENERALLY TO PAY FOR FEES LIKE INSURANCE AND STORAGE COSTS

II) A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO THE GLD/

/GLD INVENTORY 799.18 TONNES

Inventory rests tonight: 799.18 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY:

A HUGE CHANGES IN SILVER INVENTORY/

A WITHDRAWAL OF 1.126 MILLION OZ (WITH SILVER UP AGAIN?//SLV IS A CROOKED ORGANIZATION)

/INVENTORY RESTS AT 313.632 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE SIZED 4844 CONTRACTS from 181,662 UP TO 186,506 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2475 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2475 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4844 CONTRACTS TO THE 2475 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 7319 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 36.595 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.170 MILLION OZ STANDING IN JANUARY..

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 4 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 2475 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 17.88 PTS OR 0.71% //Hang Sang CLOSED UP 586.87 POINTS OR 2.27% /The Nikkei closed UP 220.02 POINTS OR 1.10% / Australia’s all ordinaires CLOSED UP 0.95%

/Chinese yuan (ONSHORE) closed DOWN at 6.8279 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 50.91 dollars per barrel for WTI and 59.71 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.8279 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8321: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)FRANCE

Looks to me like martial law: France moves to ban all protests as PM announces a major crackdown on yellow vests

( zerohedge)

ii)FRANCE

Macron may trigger a huge debt crisis with his yellow vest crackdown as nobody will buy French bonds except the ECB who have already announced a shutdown on purchases of EU bonds on Jan 1.2019

( Tom Luongo)

iv)UK

another embarrassing defeat for Theresa May as they pass an amendment which will probably kill her Brexit deal

( zerohedge)

v)GERMANY

My goodness: The prosecutors in the Deutsche bank tax evasion case (Panama Papers) had 900 clients that evaded German tax. This is going to hurt Deutsche bank considerably

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey/USA

the Turkish newspaper is reading Trump incorrectly: They state that a “soft coup” against Trump is underway and that is why he is slowing down the process of his removal of troops from Syria

( zerohedge

6. GLOBAL ISSUES

a)Again, we are receiving information that the entire globe has seized. Apple for the second time in 2 months has just slashed its iphone production

( zerohedge)

b)And now the second bad news of the day for Apple: they are cutting prices

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Venezuela

9. PHYSICAL MARKETS

i)It has almost been 10 years for Denmark to experience negative interest rates and they are not letting up.

( Rigillo/Bloomberg/GATA)

ii)Henrich is stating what we have been telling you for years; The Fed has been propping up the stock market

( Henrich/MarketWatch/GATA)

iii)Craig is not sure that we have a yuan-gold peg for the 2019 trading year

(Craig Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

the dollar is getting pummeled

( zerohedge)

ii)Market data/

a)USA consumer credit hits an all time high amid record student and auto loans. Both of these loans total basically 4 trillion dollars

( zerohedge)

a)S and P downgrades the PG and E to junk and thus another fallen angel. This will launch a 800 million collateral call as PG and E is no longer eligible debt for collateral

( zerohedge)

b)Fitch threatens to join S and P in cutting the uSA debt from its AAA rating. The reason: the upcoming debt ceiling battle

( zerohedge)

c)The strong and powerful State Street bank had its new CEO fire 15% of senior manangment as its shares slump

(courtesy zerohedge)

iv)SWAMP STORIES

a)Our deep state Deputy Attorney General is expected to resign in the coming weeks and it will occur at the same time as Barr is confirmed. What a chicken!

( zerohedge)

b)The feud between Pelosi and Trump intensifies after Trump threatens to pull Fema funds (issued for the California fires). Trump claims that California did nothing to prevent the fires

(zerohedge).

c)To be expected; Trump walks out of a meeting with Chuck and Nancy after both state that even if Trump opens up government there will be no money for the wall.

(courtesy zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 21 CONTRACTS DOWN TO 464. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 1398 CONTRACTS UP TO 146.225 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 500.65 oz of gold was withdrawn from the customer account of Scotia

Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– “We’re experiencing a slowdown,” says Blackrock fund manager

– Global Allocation Fund adding to gold exposure through ETFs

– Gold “has had a very consistent record of helping mitigate equity risk when volatility is rising”

– Gold bullion has been a “store of value for a very long time”

Gold may extend gains as global growth slows, equity market volatility remains elevated and the Federal Reserve is expected to ease back on the pace of policy tightening this year, according to a BlackRock Inc. money manager, who says the precious metal offers an effective hedge.

Source: COMEX and Bloomberg

“Recession fears are probably overblown, but I do think we’re experiencing a slowdown,” Russ Koesterich, portfolio manager at the $60 billion BlackRock Global Allocation Fund, said in an interview, citing decelerations in the U.S., China and Europe.

While BlackRock doesn’t have a price target, it’s been raising bullion holdings since the third quarter through exchange-traded funds.

Bullion surged in December as global stocks capped their worst annual performance since the financial crisis. Investors took fright at signs of economic weakness in the world’s largest economies, with China grappling against the U.S. trade war. Other political uncertainties, such as Brexit and the partial U.S. government shutdown, have also buttressed demand for havens.

“We’re constructive on gold,” Koesterich said in the phone interview on Friday. “We think it’s going to be a valuable portfolio hedge. We’re multi-asset investors: we think about its effect on the entire portfolio, and what we see value in right now is gold’s value as a diversifier.”

Gold futures advanced 7.1 percent on the Comex in the final quarter of 2018 as worldwide ETF holdings expanded, and prices carried on rallying in the opening days of the new year to top $1,300 an ounce on Friday, before a standout U.S. jobs report spurred a small drop. The metal was last at about $1,293.

The Fed raised rates four times in 2018 and investors have been trying to assess how many hikes, if any, policy makers will deliver this year. On Friday, Chairman Jerome Powell signaled that rises could be paused if the U.S. economy weakened. A more data-dependent Fed, combined with net softer U.S. data, could hurt the dollar, according to Goldman Sachs Group Inc.

With the dollar and interest rates expected to be range bound, this could be bullish for gold, according to Koesterich.

“There were two things that worked against gold for most of last year — one was rising real interest rates, and the second was a strong dollar — and those were a function of the Fed consistently raising U.S. rates,” said Koesterich. “If there’s a pause in that trend, that will remove or mitigate two of the headwinds that hurt gold during the first nine months of the year.”

Investors are paying close attention to the partial government shutdown, which is now into its third week as President Donald Trump and Republicans remain at an impasse with Democrats over border security funding. While the deadlock isn’t overly significant for the economy or financial markets, it has the potential to undermine confidence if it drags on, Koesterich said.

The “shutdown is occurring in the context of a lot of political uncertainty, trade frictions,” said Koesterich. “The relationship between uncertainty, volatility and gold’s relative performance, it’s something that’s worth watching. It has been a store of value for a very long time, and again, it has had a very consistent record of helping mitigate equity risk when volatility is rising.”

Editors note: Gold bullion, not gold ETFs, has been a store of value for thousands of years. Gold ETFs have yet to be tested in a major geopolitical or financial crisis. They are excellent vehicles for getting exposure to the gold and silver price, long or short, but should not be confused with store of value and safe haven gold and silver coins and bars.

News and Commentary

Stocks Advance on Renewed Trade Hopes; Oil Climbs: Markets Wrap (Bloomberg.com)

Gold steady as market awaits news on trade deal (Reuters.com)

World Bank sees global growth slowing in 2019 to 2.9% (Reuters.com)

Gold prices end with a loss as stocks, dollar advance (MarketWatch.com)

World stocks rise on U.S.-China trade talk hopes (Reuters.com)

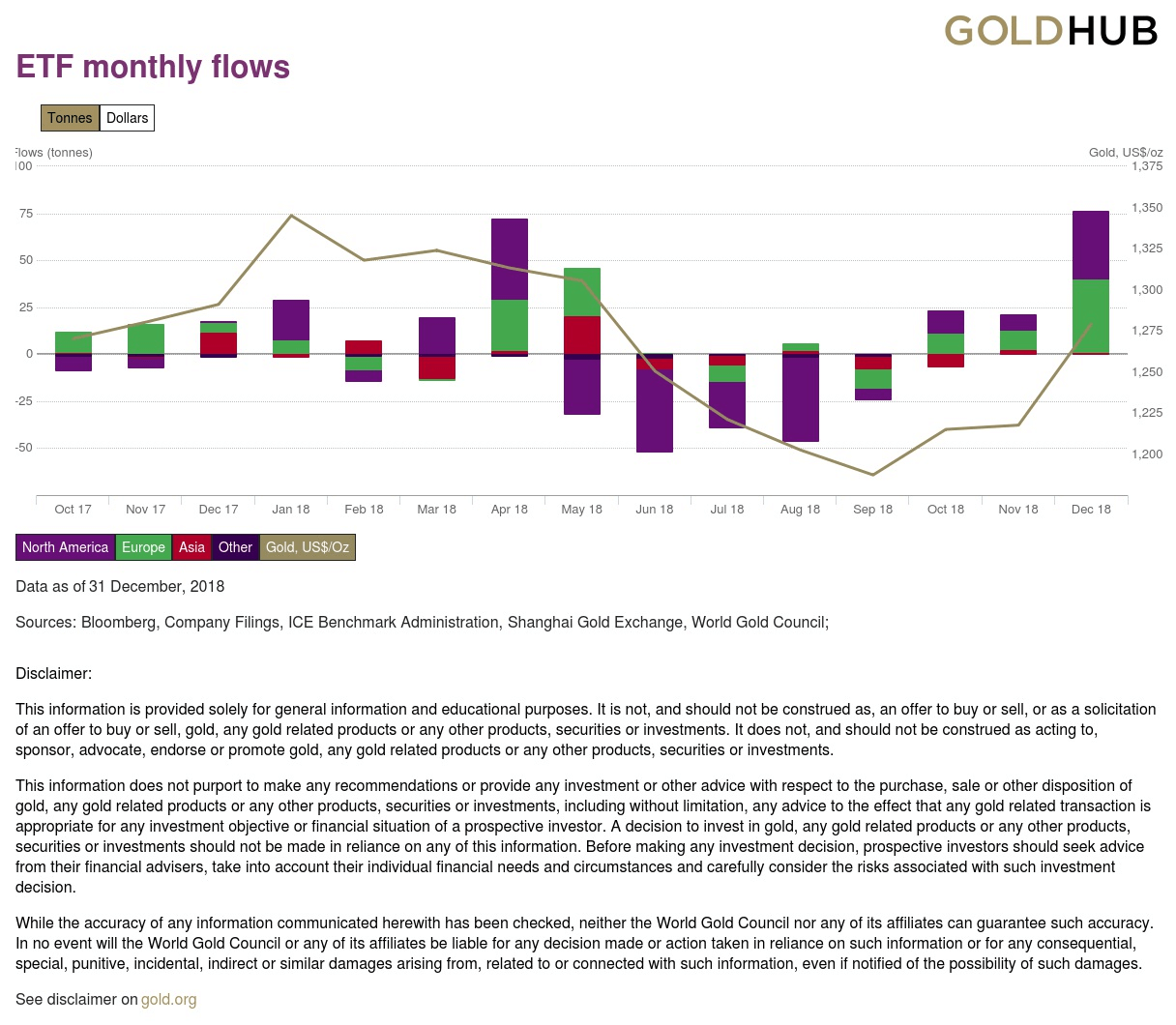

Global gold-backed ETF holdings grew 3% in 2018 (MiningWeekly.com)

Global gold-backed ETF holdings grew 3% in 2018 (Gold.org)

Gold Is The Go-To Safe Haven Of 2019 (DollarCollapse.com)

Ugly truth is that Fed is propping up the stock market (MarketWatch.com)

How likely is it that Social Security will go broke? (MarketWatch.com)

Even Bond Traders Don’t Believe This Rally (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

08 Jan: USD 1,291.90, GBP 1,006.71 & EUR 1,121.62 per ounce

07 Jan: USD 1,291.50, GBP 1,013.83 & EUR 1,129.03 per ounce

04 Jan: USD 1,290.35, GBP 1,016.80 & EUR 1,131.24 per ounce

03 Jan: USD 1,287.95, GBP 1,024.05 & EUR 1,132.62 per ounce

02 Jan: USD 1,287.20, GBP 1,014.44 & EUR 1,125.27 per ounce

31 Dec: USD 1,281.65, GBP 1,005.45 & EUR 1,120.03 per ounce

Silver Prices (LBMA)

08 Jan: USD 15.64, GBP 12.24 & EUR 13.64 per ounce

07 Jan: USD 15.75, GBP 12.35 & EUR 13.77 per ounce

05 Jan: USD 15.75, GBP 12.35 & EUR 13.77 per ounce

04 Jan: USD 15.70, GBP 12.40 & EUR 13.76 per ounce

03 Jan: USD 15.53, GBP 12.37 & EUR 13.70 per ounce

02 Jan: USD 15.44, GBP 12.19 & EUR 13.51 per ounce

31 Dec: USD 15.47, GBP 12.11 & EUR 13.51 per ounce

Recent Market Updates

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

– Everything Bubble Started Bursting In 2018 – GoldCore Video

– Global Financial System Is ‘Unstable’ and Risk Of ‘Clearing System Seizure’, BIS Warns

– Gold Flowing From West To East and Now To Goldman Sachs

* * *

GATA STORIES AS IT RELATES TO PHYSICAL GOLD/SILVER

It has almost been 10 years for Denmark to experience negative interest rates and they are not letting up.

(courtesy Rigillo/Bloomberg/GATA)

Denmark may be first to try a decade of negative interest rates

Submitted by cpowell on Tue, 2019-01-08 16:40. Section: Daily Dispatches

By Nick Rigillo

Bloomberg News

Tuesday, January 8, 2019

The world’s longest experiment with negative interest rates may end up lasting an entire decade.

Not until 2021 at the earliest will Danes have a chance to see positive rates again, according to Danske Bank. The country’s policy rate first dropped below zero in 2012.

…

.Danske Bank senior analyst Jens Naervig Pedersen says last year’s pattern of krone depreciation, which had some economists predicting rate hikes, won’t continue. In fact, he expects the Danish currency to appreciate in 2019. And with the central bank’s sole purpose being to defend the krone’s peg to the euro, a stronger exchange rate makes monetary tightening in Denmark less likely.

Nowhere else have people lived with negative interest rates as long as in AAA-rated Denmark. The policy has protected the currency peg, but it has also turbo-charged the mortgage market and pushed those trying to save money into riskier assets. Meanwhile banks have done a bit less traditional lending and a lot more wealth management. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-08/a-decade-of-negative-…

END

Henrich is stating what we have been telling you for years; The Fed has been propping up the stock market

(courtesy Henrich/MarketWatch/GATA)

Sven Henrich: Ugly truth is that Fed is propping up the stock market

Submitted by cpowell on Tue, 2019-01-08 16:50. Section: Daily Dispatches

By Sven Henrich

MarketWatch, New York

Monday, January 7, 2019

For years critics of U.S. central-bank policy have been dismissed as Negative Nellies, but the ugly truth is staring us in the face: Stock-market advances remain a game of artificial liquidity and central-bank jawboning, not organic growth. And now the jig is up.

As I’ve been saying for a long time: There is zero evidence that markets can make or sustain new highs without some sort of intervention on the side of central banks. None. Zero. Zilch.

…

And don’t think this is hyperbole on my part. I will, of course, present evidence.

In March 2009 markets bottomed on the expansion of QE1 (Wuantitative Easing, Part 1), which was introduced following the initial announcement in November 2008. Every major correction since then has been met with major central-bank interventions: QE2, Twist, QE3, and so on.

When market tumbled in 2015 and 2016, global central banks embarked on the largest combined intervention effort in history. The sum: More than $5 trillion between 2016 and 2017, giving us a grand total of over $15 trillion, courtesy of the U.S. Federal Reserve, the European Central Bank, and the Bank of Japan. …

… For the remainder of the commentary:

https://www.marketwatch.com/story/stock-market-investors-its-time-to-hea…

END

Craig is not sure that we have a yuan-gold peg for the 2019 trading year

(Craig Hemke/GATA)

Craig Hemke at Sprott Money: The yuan-gold ‘peg’ in 2019

Submitted by cpowell on Tue, 2019-01-08 22:47. Section: Daily Dispatches

5:45p ET Tuesday, January 8, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing tonight at Sprott Money, re-examines the correlation of gold prices with the Chinese yuan but can’t be sure that some entity is tying them together.

Hemke also examines the trends of gold and silver generally and senses that speculators are moving from short to long.

His analysis is headlined “The Yuan-Gold Peg in 2019” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-yuan-gold-peg-in-2019-craig-hemke-0…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

EN D

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8279/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.8321 /shanghai bourse CLOSED UP 17,88 PTS OR 0.71%

HANG SANG CLOSED UP 586.87 POINTS OR 2.27%

2. Nikkei closed UP 220.02 POINTS OR 1.10%

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 95.86/Euro FALLS TO 1.1449

3b Japan 10 year bond yield: RISES TO. +.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.91/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.91 and Brent: 59.71

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.28%/Italian 10 yr bond yield UP to 2.92% /SPAIN 10 YR BOND YIELD UP TO 1.51%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.32

3k Gold at $1282.00 silver at:15.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 20/100 in roubles/dollar) 67.10

3m oil into the 50 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.91 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9795 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1227 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.28%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.73% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5301

US Futures Extend Longest Gain Since November As Trade Talks Conclude

Global stocks rose, and US equity futures extended their longest winning streak since November, rising for a 4th day as the US and China concluded three days of trade talks on what Bloomberg reported was an “optimistic note”.

World stocks extended gains to hit a near-four week high, WTI crude oil rose above $50 and most industrial metals advanced on Wednesday on optimism that the United States and China may be inching toward a trade deal, soothing fears an all-out trade war could hit a slowing global economy, while China stepped up measures to spur consumption. Reuters reported that a senior Chinese official said Beijing plans to introduce policies to boost domestic spending on items such as autos and home appliances this year.

“The positive news around the trade talks is giving a boost to risk assets – it’s what the global economy needs to see,” said Chris Scicluna, head of economic research at Daiwa Capital Markets in London. “There are also reports of new initiatives by China to boost spending and that’s desirable from the perspective of Chinese and global growth.”

As reported earlier, delegations from China and the U.S. ended talks that had lasted longer than expected in Beijing on Wednesday amid signs of progress on issues including purchases of U.S. farm and energy commodities and increased access to China’s markets. Officials said details will be released soon with Global Times editor Hu Xijin tweeting that “the trade talks, though arduous, were conducted in a pleasant and candid atmosphere. Neither side has made the briefing, because the US delegation is on the plane now. The two sides will release message at the same time on Thursday morning Beijing time.”

Trade developments between the U.S. and China have remained a focal point for traders after a report that Trump was eager to strike a deal to help revive the flagging stock rally he was happy to take credit for. While concerns linger about the impact of protectionist tensions on global growth, a favorable outcome would set up a potential Goldilocks scenario for markets after Fed Chair Powell’s apparent dovish shift last week eased fears about tightening financial conditions.

As a result of growing trade optimism, MSCI’s all-country index rose another 0.4% in a fourth straight day of gains. Asian bourses saw a strong finish with Japan’s Nikkei and China’s blue-chip CSI 300 closing up 1% while the tech-heavy South Korean KOSPI jumped nearly 2%.

European bourses then picked up the Asian baton, with the pan-European STOXX 600 rising more than 1% with German and French benchmarks leading the way.

U.S. equity futures also rose, set for another strong day on Wall Street after the S&P 500 gained nearly 1 percent on Tuesday; US futures are now higher for 4 consecutive days – the longest stretch since November.

Not everyone was optimistic however: Kate Moore, chief equity strategist at BlackRock told Bloomberg that “we could get some more stabilization and a floor in the market if we make strides towards an agreement” on trade, but “this is going to be an issue overhanging markets I believe for multiple years.”

Meanwhile, stocks got another boost overnight after Trump demanded in his televised address that Congress provide billions for a border wall with Mexico, but stopped short of declaring a national emergency or making any other dramatic announcements. In Trump’s first-ever prime-time address, he said there is an increasing security crisis at the US southern border and that Americans are hurt by uncontrolled, illegal migration, while he also said they requested USD 5.7bln for a border wall which will be a steel barrier. Following the speech, US House Speaker Pelosi responded that President Trump is rejecting bipartisan deal to reopen government and has chosen fear over shutdown impasse, while Senate minority leader Schumer called for the government to reopen while debate over border continues. At the same time, the government shutdown continues, now in its 19th day, thanks to the impasse over funding.

Curiously, and in another sign of subsiding worries about the U.S. economic outlook, Fed funds rate futures show traders are now pricing in a small chance of a rate hike in 2019, a change from late last week when futures markets had priced in a cut by the end of the year. “Slowly but surely, the numerous headwinds that contributed to the market sell-off in the final quarter of 2018 are becoming less gale force and more strong breeze,” Craig Erlam at OANDA wrote in a note. “There is a clear risk that conditions could deteriorate quickly but at the moment, the storm is passing and investors are seeing opportunities in the wreckage.”

In currency markets, the dollar consolidated recent losses before a series of Fed speakers and the minutes of FOMC’s latest decision, while Treasuries were little changed. Commodity currencies and stocks traded in the green on renewed trade hopes, with emerging-market currencies edging north. The dollar index eased 0.2% to 95.69 against a basket of currencies, hovering close to a 2-1/2 month low hit on Monday. The euro traded at $1.1464 while the dollar stood at 108.90 yen. Theresa May’s Brexit deal returns to Parliament while one-week volatility in the pound rallied on the Jan. 15 vote risk.

In Asia, the yuan led gains, rising in offshore trading by 0.4% to its strongest level in five weeks. Asian currencies as rising on optimism the U.S. and China will be able to defuse their trade war outweighed a worsening global growth outlook. “With little by way of domestic economic data to provide any guidance for Asian currencies, the focus remains on the ongoing U.S.-China trade talks,” says Khoon Goh, head of Asia research at ANZ in Singapore. Expectations some sort of deal could be reached have buoyed regional assets, but foreign investor equity flows into the region remain muted, suggesting there’s still some caution, he said. EM Asian currency prospects have improved owing to factors including the better-than-expected China services PMI and U.S. jobs data, says Christopher Wong, a senior FX strategist at Maybank in Singapore. Still, risks remain as growth momentum is easing and there’s concern over the corporate earnings outlook, Wong said.

Elsewhere, oil prices extended their gains, rising nearly 1% with U.S. WTI crude oil futures rose above $50 per barrel overnight for the first time in 2019, after 9 consecutive days of gains.

U.S. bond yields also climbed, with the benchmark 10-year Treasuries yield rising as high as 2.7404%, compared with its one-year low of 2.543% hit just before Friday’s strong payrolls data.

Looking ahead to today, the FOMC minutes this evening will likely be the highlight and with the Brexit debate resuming in parliament any headlines there will also be closely watched. The minutes will provide more color on the Committee’s thinking around several key issues for market participants—namely, their views about headwinds from slowing global growth, progress on the Fed’s balance sheet strategy, and the debate around the neutral policy rate. After Powell’s early-year semi U-turn, the minutes could be slightly dated though. Other expected data include mortgage applications, while the Fed is scheduled to release FOMC meeting minutes, ahead of Powell’s speech at to the Economic Club of Washington D.C. on Thursday. Constellation Brands and Lennar are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,577.75

- STOXX Europe 600 up 1% to 349.14

- MXAP up 1.4% to 150.53

- MXAPJ up 1.6% to 486.48

- Nikkei up 1.1% to 20,427.06

- Topix up 1.1% to 1,535.11

- Hang Seng Index up 2.3% to 26,462.32

- Shanghai Composite up 0.7% to 2,544.34

- Sensex up 0.5% to 36,158.62

- Australia S&P/ASX 200 up 1% to 5,778.29

- Kospi up 2% to 2,064.71

- German 10Y yield rose 7.7 bps to 0.303%

- Euro up 0.2% to $1.1469

- Italian 10Y yield rose 5.4 bps to 2.592%

- Spanish 10Y yield rose 0.4 bps to 1.517%

- Brent futures up 1.7% to $59.73/bbl

- Gold spot down 0.3% to $1,281.08

- U.S. Dollar Index down 0.1% to 95.85

Top Overnight News from Bloomberg

- President Donald Trump is increasingly eager to strike a deal with China soon in an effort to perk up financial markets that have slumped on concerns over the trade war, according to people familiar with internal White House deliberations

- The two countries wrapped up three days of trade talks, with people familiar saying their positions were closer on areas including energy and agriculture but further apart on harder issues. The one-day extension of the talks shows both sides are serious about negotiations, Chinese foreign ministry spokesman Lu Kang says

- A rare flurry of schedule changes by regional legislatures across China suggests that President Xi Jinping may be clearing the calendar for a long-awaited Communist Party gathering later this month

- China’s Finance Ministry is set to propose a small increase in the targeted budget deficit for this year as officials seek to balance support for the economy with the need to keep control of debt levels

- The yen’s spectacular start to 2019 has been a case of too much, too soon for two influential investment firms that between them manage about $1 trillion in assets. AllianceBernstein Ltd. sold the currency as it surged 4 percent last week amid the dollar’s flash crash. Manulife Asset Management cut its holdings of the yen against the Australian dollar that day

Asian equity markets were higher across the board as sentiment remained underpinned by trade hopes after US-China discussions were extended into a 3rd day and with progress said to have been made on issues including purchases of US goods, while US President Trump also provided encouragement as he stated that talks were going well. As such, ASX 200 (+1.0%) and Nikkei 225 (+1.1%) were positive as they benefitted from the trade-related optimism which had inspired a 3rd consecutive gain amongst the US majors, with notable strength also seen in Australia’s energy names after WTI reclaimed the USD 50/bbl level to the upside. Hang Seng (+2.3%) and Shanghai Comp. (+0.7%) were also in the green as focus centred on trade while reports suggested that US President Trump wants a China trade deal soon to boost markets. Finally, 10yr JGBs tracked the downside in T-notes as the broad gains in stocks sapped safe-haven demand, while the BoJ’s Rinban announcement was also somewhat trivial with the central bank only in the market for around JPY 450bln concentrated in the belly.

Top Asian News

- Philippine Bulls on a Roll as Overseas Stocks Funds Trickle Back

- China Is Said to Propose Wider 2019 Fiscal Deficit Amid Slowdown

- BlackRock Sees Rally in Asia Credit After Losses Last Year

- Rare China Schedule Changes Suggest Major Policy Meeting Is Near

Major European indices are in the green [Euro Stoxx 50 +0.8%] as market sentiment remains fixated around the recently concluded US-China trade talks, with China’s foreign ministry indicating that they are taking the talks very seriously. Germany’s DAX (+0.9%) is outperforming its peers, with auto names such as Volkswagen (+2.9%) and BMW (+1.5%) in the green on the aforementioned trade talk sentiment; Daimler (+3.7%) lead the German auto’s with Mercedes-Benz selling 2.31mln cars in 2018 likely to make them that year’s best-selling premium auto. Sectors are broadly in the green, with consumer discretionary the outperforming sector with luxury names such as Kering (+3.8%) and Burberry (+2.8%) up as US-China talks conclude. Other notable movers include Ted Baker (+11.3%) after announcing a 12% increase in retail sales for the 5 weeks to January 5th. Elsewhere, Taylor Wimpey (+6.9%) after Co report good trading performance, with 2018 total home completions +3%. At the bottom of the Stoxx 600 are ADP (-4.7%) after reports that the French government are considering delaying privatisation until 2020.

Top European News

- Deutsche Bank Drops as UBS Sees a Challenging Fourth Quarter

- Autos Lead Gains in Europe on Trade Optimism, China Stimulus

- Future Daimler CEO Sees Record Year Despite Global Auto Slowdown

- Sainsbury’s Holiday Sales Fall as Cautious Consumers Hold Back

In FX, the dollar eases further below 96.000 following a rangebound Asia-Pac session amid trade optimism with the third day of trade talks giving off somewhat of an upbeat vibe. China’s Foreign Ministry stated that the longer talks signified the country’s seriousness, while the China Global Times Editor also took note of the positive sentiment surrounding the dialogue. As such the DXY remains closer to the bottom of a 95.925-660 range ahead of the FOMC Minutes later today (full preview available on the Research Suite).

- GBP, EUR – The Pound extended on gains before paring a bulk of the move with fears of a no-deal Brexit receding as the UK Government seems to be losing more power in Parliament. To recap recent events, the Government was defeated in a vote regarding the Finance Bill which limits the scope for tax changes in the event of a no-deal. Additionally, if Labour and Tory rebels vote down the business motion (due at around 1300GMT), then Parliament will take control of the timing of the meaningful vote debate from the Government, i.e. PM May will not have room to further delay it. Furthermore, Business Insider also reported that UK businesses will make urgent public interventions about the perils of a no-deal Brexit should MPs vote down the deal on the 15th. Subsequently, Cable retreated to near the bottom of a 1.2712-77 range with resistance seen at 1.2790 (yesterday’s high) and support at 1.2712 (7th Jan low). Meanwhile, the EUR is marginally firmer, mostly on the back of a softer USD as an EZ upbeat unemployment rate and wider-than-expected German trade surplus did little to budge the single currency as exports fell more-than-expected.

- SEK,NOK – The Scandi Crowns are mixed with the SEK marginally softer following the release of the Riksbank Minutes from the December meeting which initially saw a firmer Crown as several Board Members noted that even though the inflation forecast for the next few years has also been revised downwards slightly, the conditions are still good for inflation to remain close to the 2% inflation target. Nordea notes that the release was marginally dovish given the risks surrounding the repo path downgrade. As Such EUR/SEK pared back the initial move lower to test 10.2400 to the upside (vs. low of 10.1967) ahead of its 200 HMA at 10.2428.

- AUD, NZD, CAD – The non-US dollars are on the front foot amid commodity price action with the Kiwi leading the gains. AUD was briefly hampered by the release of disappointing Australian building approvals overnight while AMP Capital’s Chief Economist said he sees the RBA cutting rates to 1.00% this year (currently 1.50%) due to a fall in building approvals and negative wealth effects from declining house prices dragging on economic growth. In terms of technical, AUD/USD sees clean air to the downside until the psychological level at 0.7000, while NZD/USD is capped at its 50 DMA 0.6782 and trading just above its 20 DMA 0.6744. Meanwhile USD/CAD sits near the bottom of a 1.3223-79 range with the rise in oil supporting the Loonie ahead of the BoC interest rate decision (full preview available on the Research Suite), looking at technicals, the pair’s 50 HMA (to the upside) sits at 1.3284 with clean air seen to the downside until 1.3200 the figure.

- JPY – The marked G10 underperformer as the safe-haven currency unwinds risks premium given the positivity around US-Sino trade talks with USD/JPY residing just below 109.00, having already tested the psychological level. On a technical front, past the 109.00 psychological level, 109.16 is a reported Fib level ahead of resistance at 109.73 (2nd Jan high).

In commodities, Brent (+1.7%) and WTI (+1.9%) prices are higher, with WTI breaching the USD 50/bbl level to the upside, and approaching USD 51/bbl, on hopes that a resolution can be achieved between the US and China. Alongside Brent testing, and briefly crossing, USD 60.00/bbl. Prices garnered further support from yesterday’s API crude inventories, which showed a larger than expected draw of -6.127mln vs. Exp. -2.7mln. Markets will be looking ahead to EIA data later on in the session, where expectations for weekly crude stocks are for a -3.3mln draw. UAE Energy Minister Mazrouei stated that the volatility in oil prices last year was counterproductive, and OPEC have stopped chasing an illogical or impractical price. Elsewhere, Berenberg have cut their 2019 Brent price forecast from USD 82.5/bbl to USD 65/bbl; and Morgan Stanley have updated their Brent forecast to USD 61.00/bbl vs. Prev. USD 69.00/bbl. Gold (-0.3%) prices have remained subdued by the positive risk sentiment from the US-China trade progress. Elsewhere, US plans to remove sanctions on Rusal, the Russian aluminium Co, are suggested to be of limited benefit to US consumers as aluminium import tariffs mean produces would require significantly greater prices in order to incentivise shipments.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -8.5%

- 2pm: FOMC Meeting Minutes

- 8:20am: Fed’s Bostic Speaks in Chattanooga on Economic Outlook

- 9am: Fed’s Evans Speaks on Economy and Monetary Policy

- 11:30am: Fed’s Rosengren Speaks on the Economic Outlook

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

May I be the 150th person to wish you a Happy New Year. It’s my first day back at work today and I’m writing this en route to Switzerland. Over the last two weeks in the Alps I’ve had numerous hot chocolates, bottles of red, tartiflettes, pizzas, burgers, portions of chips, hot marshmallows, ice creams and fondues. To balance this I’ve skinned up the mountain 12 times, done 20-odd snowy and hilly dog walks and looked after three excitable children. On balance there has still been more input than output though and am therefore relieved to be back at work so my body can have a rest from all angles. We nervously put 3 year old Maisie into ski school and thankfully she seemed to enjoy it. If you want to see what a three year old skiing with irresponsible parents looks like (post ski school) click on my Bloomberg header this morning to see.

If the end of 2018 was all uphill for risk, 2019 has so far seen the market wax up its skis, sharpen its edges and point them downhill. A reminder that our forecasts for 2018 and 2019 were both bearish based on the withdrawal of central bank liquidity and the lagged impact on global volatility and risk of the Fed tightening cycle. However we turned tactically bullish for Q1 2019 in the latter half of November which in timing terms proved to be too early (or wrong depending on where we end up!). We would stand by this prediction and think the early months of this year will be the best as the risks of a near-term recession and worse case trade scenarios are eventually seen to be overdone. However after that we will still live in a world of less central bank liquidity after years of excess and a period where the lagged impact of the prior Fed hikes will resonate. We still think the US yield curve (2s10s) will be the best indicator of the probability of a recession in 2020 (see our Yield Curve 101 note here from late last year for more). For us it needs to invert to suggest one is coming over the following 12-18 months. In turn, whether it inverts depends on the interplay between the Fed and the market. The worst case scenario is a Fed that ploughs through and continues to hike when the market disagrees with them (rightly or wrongly, and 10-year yields fall) or the data doesn’t justify it. A Fed at odds with the market is still very possible, especially after last Friday’s strong payroll and earnings data. However Powell’s speech last week indicated a more dovish approach than his pre-Xmas musings which is largely why 2019 has started well. So overall, all to play for, but the Fed and market interplay is likely to be the key battleground this year. Today’s Fed minutes (possibly a bit dated since Powell has already spoken since the meeting), multiple Fedspeak today (Evans, Bostic, and Rosengren) and tomorrow (Powell, Clarida, Bullard, Evans, Barkin, and Kashkari) and Friday’s US CPI will be the next major landmarks on this.

So momentum continues to favour those who point the skis straight down the mountain even if US markets did experience some intraday volatility, opening up +1% before fading back into the red around lunchtime, and ultimately rallying back to end the session near the highs. The S&P 500, DOW and NASDAQ each notched up a third day of consecutive gains. That means that if we exclude the impact of the Boxing Day surge then this three-day run (+5.17%) for the S&P is the strongest since August 2015 and sits in the top 3 since the start of 2010. The 4 out of 5 ‘up’ days to start the year is something that’s happened 11 times out of 92 including this year. We’ve had a perfect start (5 out of 5) 6 times.

On a sector basis, the gains were somewhat mixed. There was no clear outperformance by either cyclicals or defensives, as buying was broad-based. 81% of S&P 500 companies advanced, the third consecutive session with over 77% of stocks in the index gaining. That’s the best such streak since July. One soft spot was semiconductors, which fell -0.48% as Samsung announced soft demand for its chips business and missed consensus fourth quarter earnings expectations.

Credit continues to make headway with US HY spreads another 16bps tighter yesterday (and 76bps tighter over the last 3 sessions). Euro HY also started to catch up with spreads 9bps tighter while the STOXX 600 notched up a +0.87% gain. Autos were up +1.41% and +1.23% in Europe and the US, respectively, seemingly on the news that China was looking to boost auto purchases this year. Oil also played a part in yesterday’s risk on moves with WTI Oil up +2.47%, placing it up +9.49% YTD already. EM equities gained +0.33% while currencies fell -0.12%. Oil importers were pressured, with the Indian rupee and South African rand down -0.74% and -0.65%, though Turkey underperformed heavily (-1.75%) as President Erodogan escalated his rhetorical battle with US National Security Advisor Bolton, saying “Bolton made a serious mistake (…) we will not compromise.”

There was also a bit of a lift in sentiment from President Trump’s comments on the US-China trade negotiations, specifically saying that “talks with China are going very well”. On the other hand, he also tweeted a quote from a steel union official supporting his tariffs, so it’s not clear what the takeaway message should be. Dow Jones also reported later that trade progress was being made although the two sides were (unsurprisingly) not ready to conclude a deal. It now confirmed that the US delegation is to remain in Beijing for a third day of talks today and China has confirmed that they will release a post-meeting statement once talks are concluded although it’s not entirely clear if the US delegation will release a statement themselves. The more important talks are likely to come later this month in any case. Elsewhere, Bloomberg reported (citing sources) that President Trump is increasingly keen to strike a deal with China soon in an effort to perk up financial markets that have slumped on concerns over the trade war. In the meantime, the White House has crafted a bill which seeks to give the president broad authority to increase US tariffs if he considers other countries’ tariff and non-tariff measures to be too restrictive and President Trump is expected to urge Congress in his State of the Union address later this month to pass the new legislation.

Moving onto Trump’s first televised national address overnight. It was fairly low on substance for markets as he said more of same while discussing the ongoing US government shutdown and immigration policy. He reiterated that he considers the situation on the US’s southern border to be a crisis and called on Congress to authorize $5 bn for increased border security and a wall. Congressional Democrats subsequently gave no indication that they will meet his demands. So for now, the shutdown is set to continue and around 800,000 federal employees will miss their pay checks on Friday. Nevertheless, S&P 500 futures rallied into and during the address and are trading +0.47% higher this morning. President Trump is set to meet with the congress leaders today at 3pm (New York time) to further discuss the issue.

This morning in Asia risk has continued to rally hard with the Nikkei (+1.43%), Hang Seng (+2.46%), Shanghai Comp (+1.59%) and Kospi (+1.88%) all up. Besides the positivity around the ongoing US-China trade negotiations, sentiment is also getting aided by the overnight news (per Bloomberg) that China’s Finance Ministry is set to propose an annual fiscal deficit target of 2.8% of GDP for 2019, marking a small budget expansion from the deficit target of 2.6% in 2018. The target isn’t final though and is subject to approval at a meeting of the National People’s Congress, China’s legislature, in March. Meanwhile, Japan’s November real cash earnings data also came in strong at +1.1% yoy (vs. +0.4% yoy expected). Elsewhere, crude oil prices (WTI +1.59% and Brent +1.35%) are continuing their upward move this morning.

In other news, former Fed economist Nellie Liang withdrew her nomination for a seat on the Fed’s board of governors possibly giving an opportunity to President Trump to nominate someone whose views on interest rates are more streamlined with his own. Elsewhere, the World Bank lowered its growth projections in 2019 for the global economy by 0.1pp to 2.9% largely by shaving off 0.5pp growth for emerging markets to 4.2% while also downgrading its growth forecast for the Euro area slightly and keeping the growth forecast for the US at 2.5%.

As for Brexit, the parliament vote appears to now be confirmed for January 15th. Much of the newsflow ahead of the debate yesterday centred around PM May seeking EU assurances on the backstop provision however there didn’t appear to be any meaningful progress. Indeed, France’s Europe Minister said “there is nothing more we can do” to adjust the deal. A spokesman for PM May also denied that UK officials were talking to the EU about an Article 50 extension. Elsewhere the government lost a vote on funding a no-deal Brexit last night which complicates things a little for them as Parliament tries to stop a no-deal Brexit. Sterling faded in the afternoon yesterday to close down -0.46% while Gilts were a touch weaker (+2.0bps).

That wasn’t out of line with other bond markets however with Treasuries +3.2bps higher at 2.728% and the 2s10s curve at 14.0bps (-1.1bps), while in Europe Bunds nudged up to 0.226% (+0.5bps). BTPs (+5.5bps) stood out after coming within a couple of basis points of 3% again (closed 2.954%) after the recent (post-budget drama) 6 month low of 2.67% on January 2nd. Supply appeared to weigh with Bloomberg reporting that Italy’s Treasury was preparing a 15y bond deal, while yesterday we also had deal announcements from Ireland and Portugal, likely to price today.

The headline grabber data release in Europe yesterday came in the form of another soft print out of Germany, this time with the November industrial production report. Production was reported as falling -1.9% yoy compared to expectations for +0.3% mom, resulting in the annual figure dropping to -4.7% yoy and the lowest since 2009. Issues related to the auto sector, the timing of public holidays and, believe it or not, low water levels on the river Rhine (my favourite excuse ever) were all highlighted as negatively impacting the data. That appeared to filter through to weaker confidence readings for the broader Euro Area yesterday with the December releases out while in the US there wasn’t much excitement from yesterday’s releases. The December NFIB small business optimism reading fell 0.4pts in December to 104.4 but was well ahead of expectations while the November JOLTS report showed a steady quits rate at 2.3% and a modest tick lower in the hiring rate to 3.8% from 4.0%. These point to continued improvement in the wage outlook.

Looking ahead to today, the FOMC minutes this evening will likely be the highlight and with the Brexit debate resuming in parliament any headlines there will also be closely watched. Our team expect that the minutes will provide more colour on the Committee’s thinking around several key issues for market participants—namely, their views about headwinds from slowing global growth, progress on the Fed’s balance sheet strategy, and the debate around the neutral policy rate. After Powell’s early-year semi U-turn, the minutes could be slightly dated though.

As for other data that’s due out, we’ll get November trade stats out of Germany this morning followed by Q3 unit labour costs data for the UK and the November unemployment rate for the Euro Area. In the US we’ll also get the latest MBA mortgage applications data. There should be plenty of eyes on today’s Fedspeak also in light of Powell’s comments last week with Bostic (1.20pm GMT), Evans (2pm GMT) and Rosengren (4.30pm GMT) all on the cards. The BoE’s Carney is also due to participate in an online Q&A this afternoon. Finally it’s worth noting that US Trade Representative Lighthizer is due to meet EU Trade Commissioner Malmstrom today to discuss bilateral trade liberalization. It’s expected that both will also meet Japan’s trade and industry minister Seko to discuss China’s trade practices.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 17.88 PTS OR 0.71% //Hang Sang CLOSED UP 586.87 POINTS OR 2.27% /The Nikkei closed UP 220.02 POINTS OR 1.10% / Australia’s all ordinaires CLOSED UP 0.95%

/Chinese yuan (ONSHORE) closed DOWN at 6.8279 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 50.91 dollars per barrel for WTI and 59.71 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.8279 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8321: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

(courtesy zerohedge)

Reuters Exposes Huawei’s Deep Ties To Iran And Syria

Reuters reporters have been covering Huawei’s business dealings in Iran for years, with reports about Huawei’s illegal sales of US-made equipment to an Iranian telecoms firm dating back to 2012. Some of these reports have been cited in the US case against Huawei CFO Meng Wanzhou, who was arrested in Canada on Dec. 1 on allegations she knowingly misled banks about Huawei’s relationship with its Hong Kong-based “partner” Skycom, which Reuters exposed for facilitating sales to Iranian companies in violation of US sanctions.

And in its latest report on Huawei’s dealings in the Islamic Republic, Reuters examined corporate filings and other documents in Iran and Syria which proved that Huawei’s relationship with Skycom and another firm – Syria-based shell company Canicula Holdings – is even deeper than had previously been reported. These revelations show that Huawei’s business dealings in both countries are even more extensive than previously believed.

The filings cited by Reuters revealed that a senior Huawei executive named Shi Yaohong was also the Iranian manager at Skycom (before the company, recently exposed as a fully-owned subsidiary of Huawei, was dissolved). They also revealed that three individuals with Chinese names had signing rights for bank accounts tied to both Huawei and Skycom.

The documents reveal that a high-level Huawei executive appears to have been appointed Skycom’s Iran manager. They also show that at least three Chinese-named individuals had signing rights for both Huawei and Skycom bank accounts in Iran. Reuters also discovered that a Middle Eastern lawyer said Huawei conducted operations in Syria through Canicula.

The previously unreported ties between Huawei and the two companies could bear on the U.S. case against Meng, who is the daughter of Huawei founder Ren Zhengfei, by further undermining Huawei’s claims that Skycom was merely an arms-length business partner.

But despite the company’s efforts to portray its operations in Iran as a past transgression, Reuters report suggests that Huawei is still operating in Syria and Iran. Like Iran, Syria is another country impacted by US and EU sanctions, and its also home to a Huawei subsidiary that does business with Syrian telecoms firms.

The subsidiary, Canicula, is connected to Iran through MTN Syria, which has a subsidiary that operates in Iran. Though Huawei had apparently tried to cover its tracks – presumably after catching wind of the US investigation – by publishing notices proclaiming that Canicula was no longer operating in Syria.

And a Middle East based lawyer who once worked with Huawei told Reuters that Huawei continues to operate in both Syria and Iran despite what appear to be attempts to throw off US investigators.

Until two years ago, Canicula had an office in Syria, another country that has been subject to U.S. and European Union sanctions. In May 2014, a Middle Eastern business website called Aliqtisadi.com published a brief article about the dissolution of a Huawei company in Syria that specialized in automated teller machine (ATM) equipment. Osama Karawani, an attorney who was identified as the appointed liquidator, wrote a letter asking for a correction, stating that the article had caused “serious damage” to Huawei.

Karawani said the article suggested that Huawei itself had been dissolved, not just the ATM company. In his letter, which was linked to on the Aliqtisadi website, he said Huawei was still in business.

“Huawei was never dissolved,” he wrote; he added that it “has been and is still operating in Syria through several companies which are Huawei Technologies Ltd and Canicula Holdings Ltd.”Huawei Technologies is one of Huawei’s main operating companies.

[…]

In December 2017, a notice was placed in a Syrian newspaper by “the General Director of the branch of the company Canicula Ltd.” He was not named. It announced that Canicula had “totally stopped operating” in Syria two months before. No explanation was given.

Meanwhile, Skycom’s corporate filings in Iran revealed that Shi, who is Huawei’s head of Middle East operations according to his LinkedIn page, and others were signatories on Huawei bank accounts.

A company record filed by Skycom in Iran that was entered in the Iranian registry in December 2011 states that a “Shi Yaohong” had been elected as manager of Skycom’s Iran branch for two years. Huawei employs an executive named Shi Yaohong.

According to his LinkedIn profile, Shi was named Huawei’s “President Middle East Region” in June 2012. An Emirates News Agency press release identified him in November 2010 as “President of Huawei Etisalat Key Account.” Etisalat is a major Middle Eastern telecommunications group and a Huawei partner.

Shi, now president of Huawei’s software business unit, hung up the phone when Reuters asked him about his relationship with Skycom.

Many corporate records filed by Skycom in Iran list signatories for its bank accounts in the country. Most of the names are Chinese; at least three of the individuals had signing rights for both Skycom and Huawei bank accounts. (One of the names is listed in the Iranian registry with two slightly different spellings but has the same passport number.) U.S. authorities allege in the court documents filed in Canada that Huawei employees were signatories on Skycom bank accounts between 2007 and 2013.

But the most damning quote comes at the very end of the story, and is attributed to an anonymous source with knowledge of Huawei’s history in the region: “Skycom was just a front” for Huawei.

All in all, this doesn’t bode well for Meng and her chances of evading a lengthy sentence once she is extradited to the US.

Beijing Trade Talks Conclude: China, US To Release “Message” Thursday

After the ‘mid-level’ talks between US and Chinese delegations in Beijing were extended for a third day on Wednesday, the negotiations have reportedly wrapped up, with both sides touting that they are “serious” about coming to an agreement, and that significant progress has been made, according to CNBC.

With the US delegation on its way back to Washington, China’s Foreign Ministry hinted that the talks had been a success and said it would soon release a statement on the outcome.

The Editor-in-Chief of China’s Global Times said that “though arduous” the trade talks were productive and that both sides were waiting for the US delegation to arrive back in Washington before delivering official statements on the outlook for a deal.

Hu Xijin 胡锡进@HuXijin_GTChina-US trade talks have ended. Based on what I know, the situation is quite positive. The two sides are still in consultation on the wording of the message, so the two versions can be coordinated.

Hu Xijin 胡锡进@HuXijin_GTFrom what I know, the trade talks, though arduous, were conducted in a pleasant and candid atmosphere. Neither side has made the briefing, because the US delegation is on the plane now. The two sides will release message at the same time on Thursday morning Beijing time.

Meanwhile, US Under Secretary of Agriculture for Trade and Foreign Agricultural Affairs Ted McKinney told a group of reporter’s at the delegation’s hotel that he thought negotiations “went just fine.”

“It’s been a good one for us,” he said.

US markets climbed on Tuesday even as traders priced in a slightly more hawkish Fed as many apparently bought in to the narrative that both sides are doing everything in their power to come to an agreement (with equities moving higher after Bloomberg reported that Trump is desperate for a deal because he hopes it might send stocks back toward ATHs).

Though there were some reports that the two sides were further apart than some of the headlines let on.

However, people familiar with the talks told Reuters on Tuesday that the two sides were further apart on Chinese structural reforms that the Trump administration is demandingin order to stop alleged theft and forced transfer of U.S. technology, and on how Beijing will be held to its promises.

In another sign of confidence, China has approved another large order of US soybeans while also approving five GMO crops for import – its latest effort to boost imports from the US in accordance with one of Trump’s key demands.

In what is widely seen as a goodwill gesture, China on Tuesday issued long-awaited approvals for the import of five genetically modified crops, which could boost its purchases of U.S. grains as farmers decide which crops to plant in the spring.

On Monday, Chinese importers made another large purchase of U.S. soybeans, their third in the past month.

Trump and other White House officials have insisted that the US has leverage because of China’s rapidly cooling economic growth and the fact that its market dropped 25% last year (though Chinese stocks have slightly outperformed the US since the US imposed its first round of China-specific tariffs in July) . However, China has insisted that the trade strife harms both countries equally, and that it would not yield to any “unreasonable concessions.”

China is keen to put an end to its trade dispute with the United States but will not make any “unreasonable concessions” and any agreement must involve compromise on both sides, state newspaper the China Daily said on Wednesday.

The paper said in an editorial that Beijing’s stance remains firm that the dispute harms both countries and disrupts the international trade order and supply chains.

Setting the meeting off to an auspicious start, Liu He, China’s top economic official, dropped in and greeted the US trade delegation – led by Deputy U.S. Trade Representative Jeffrey Gerrish – on Monday. We now await confirmation that Liu and a delegation of more-senior officials will travel to Washington next week for the next round of talks.

The US and China have agreed to a “hard” deadline for an agreement of March 2.

END

After all that hype, the statement was nothing but a “nothingburger”

(courtesy zerohedge)

US Issues Statement On Trade Meeting In Beijing

The long-anticipated statement from the US Trade Representative on the just concluded 3 days of talks in Beijing has been released and it appears to be another “nothingburger”:

Alan Rappeport

✔@arappeport

In readout of China talks, USTR says officials discussed the need for any agreement w/ China to provide for “complete implementation subject to ongoing verification and effective enforcement.”