GOLD: $1289.30 UP $2.30 (COMEX TO COMEX CLOSINGS)

Silver: $15.63 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1287.85

silver: $15.60

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 45 NOTICE(S) FOR 4500 OZ (0.1399 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 525 NOTICES FOR 525 OZ (1.6329 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

142 NOTICE(S) FILED TODAY FOR 710,000 OZ/

total number of notices filed so far this month: 586 for 2,930,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3584: UP 2

Bitcoin: FINAL EVENING TRADE: $3612 up 43

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 32/45

BUSINESS DATE: 01/10/2019 DAILY DELIVERY NOTICES RUN DATE: 01/10/2019

PRODUCT GROUP: METALS RUN TIME: 20:28:07

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,284.700000000 USD

INTENT DATE: 01/10/2019 DELIVERY DATE: 01/14/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 C HSBC 45

624 C MERRILL 2

657 C MORGAN STANLEY 4

661 C JP MORGAN 32

737 C ADVANTAGE 7

____________________________________________________________________________________________

TOTAL: 45 45

MONTH TO DATE: 525

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN TINY SIZED 212 CONTRACTS FROM 188,613 UP TO 188,825 DESPITE YESTERDAY’S 11 CENT DROP IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2171 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2171 CONTRACTS. WITH THE TRANSFER OF 2171 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2171 EFP CONTRACTS TRANSLATES INTO 10.855 MILLION OZ ACCOMPANYING:

1.THE 11 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.300 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 23,854 CONTRACTS (FOR 8 TRADING DAYS TOTAL 23,843 CONTRACTS) OR 119.27 MILLION OZ: (AVERAGE PER DAY: 2981 CONTRACTS OR 14.908 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 119.27 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.02% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 119.27 MILLION OZ.

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 221 DESPITE THE 11 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 2171 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 2383 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2171 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 212 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 11 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.59 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 142 NOTICE(S) FOR 7100,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.300 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS 12,902 CONTRACTS UP TO 477,845 DESPITE THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $4.00//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6128 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 6128 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 477,845. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN (FOR THE SECOND STRAIGHT DAY) IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,220 CONTRACTS: 12,902 OI CONTRACTS INCREASED AT THE COMEX AND 6128 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 18,220 CONTRACTS OR 1,822,000 OZ = 56.67 TONNES. AND ALL OF THIS VERY HUMONGOUS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.00??????????

YESTERDAY, WE HAD 7454 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 67,405 CONTRACTS OR 6,740,500 OZ OR 209.65 TONNES (8 TRADING DAYS AND THUS AVERAGING: 8425 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 209.65 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 209.65/2550 x 100% TONNES = 7/47% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 209.65 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 12,902 DESPITE THE LOSS IN PRICING ($4.00) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6128 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6128 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC GAIN OF 18,220 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6128 CONTRACTS MOVE TO LONDON AND 12,902 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 56.67 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $4.00 IN YESTERDAY’S TRADING AT THE COMEX??????????

we had: 45 notice(s) filed upon for 4500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.30 TODAY

ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD/

A WITHDRAWAL OF 1.47 TONNES OF GOLD WHICH WAS USED TODAY TO SUPPRESS GOLD’S RISE

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY/

/INVENTORY RESTS AT 313.632 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 212 CONTRACTS from 188,613 UP TO 188,825 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2171 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2171 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 335 CONTRACTS TO THE 2171 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 2383 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 11.92 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.300 MILLION OZ STANDING IN JANUARY..

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 11 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 2171 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 18.78 PTS OR 0.74% //Hang Sang CLOSED UP 145.84 POINTS OR 0.55% /The Nikkei closed UP 195.90 POINTS OR 0.97% / Australia’s all ordinaires CLOSED DOWN 0.33%

/Chinese yuan (ONSHORE) closed DOWN at 6.7427 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.98 dollars per barrel for WTI and 61.92 for Brent. Stocks in Europe OPENED /MIXED

//. ONSHORE YUAN CLOSED UP AT 6.7427 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7473: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/USA/POLAND

It does not get any worse of Huawei. Poland arrests a key Huawei executive based in Poland on espionage as well as a high executive in the Polish government.

( zerohedge)

ii(the POBC not excited seeing the rise in the yuan so it jawboned it lower:

( zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

The yellow vest movement urges supporters to break the bank by causing a bank run. The yellow vest movement is moving also to England

(courtesy zerohedge)

ii) the history of the Euro and how it will influence the destruction of the euro project

A super commentary from Alasdair Macleod on the euro as it stands today. It gives a terrific history of how we got to this position today. As i have pointed out to you on several occasions, the ECB has stopped purchasing of all Euro based countries on Dec 31.2018. This will lead to the collapse of Europe as there will be nobody around to purchase the bonds of Italy, Portugal, France and Belgium

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY/USA

Erdogan refuses Washington’s ultimatum to abandon the huge arms deal negotiated with Moscow

( zerohedge)

iii)This morning: US withdraws some of its troops from Syria contrary to what Bolton and Pompeo stated

( zerohedge)

( zerohedge)

v)RUSSIA

Russia de dollarizes again as the government shifts 100 billion dollars to yuan yen, the euro and the Canadian dollar

( Mac Slavo/SHFTPlan.com)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)Brazil

9. PHYSICAL MARKETS

4 on trial for the theft of the largest Cdn gold coin ever minted: 221 pounds from the Berlin museum]

( APnews/GATA)

ii)Barrick’s new CEO dismisses the media’s obsession that they will move their headquarters from Canada as sheer hysteria

( Bochove/Bloomberg/GATA)

iii)Yellow vest protesters are aiming to crash the French banking system by removing their euros from the banks. Also the yellow vest protests are moving to London where we will see protests there on the weekend

( AP/GATA)

this was brought to your attention yesterday but it is worth repeating:

( Ted Butler/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

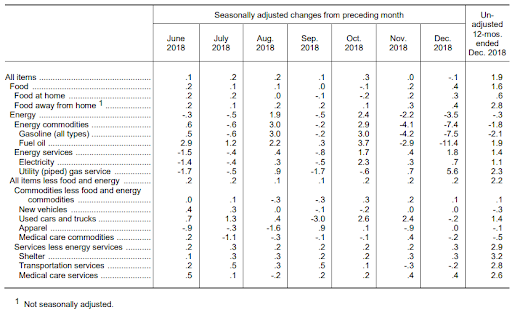

The all important CPI comes in at the slowest growth since August 2017 at 1.9% y/y

( zerohedge)

a)Earnings season has got off to a dismal start with a huge number of warnings, guidance cuts and mass layoffs

( zerohedge)

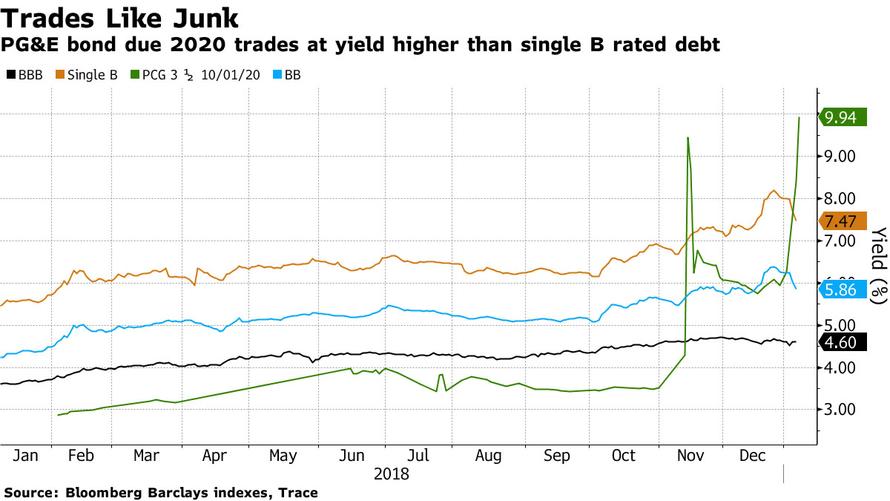

b)Moody’s downgrades P G and E and that triggers a 800 million dollar collateral call against the company. It has only 400 million of liquid cash.

iv)SWAMP STORIES

This was long overdue; Trump is now planning to ease immigration restrictions on skilled workers such as IT programmers and doctors. This will appease both Democrats who desire increase immigration and Republicans

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 3 CONTRACTS DOWN TO 475. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 1051 CONTRACTS DOWN TO 144,101 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 128.60 oz of gold was withdrawn from the customer account of Scotia

4 kilobars

Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

Gold Outlook 2019 – World Gold Council

As we look ahead, we expect that the interplay between market risk and economic growth in 2019 will drive gold demand. And we explore three key trends that we expect will influence its price performance:

- financial market instability

- monetary policy and the US dollar

- structural economic reforms.

Against this backdrop, we believe that gold has an increasingly relevant role to play in investors’ portfolios.

Gold Outperformed Most Assets In 2018

Why gold why now

Gold’s performance in the near term is heavily influenced by perceptions of risk, the direction of the dollar, and the impact of structural economic reforms. As it stands, we believe that these factors likely will continue to make gold attractive.

In the longer term, gold will be supported by the development of the middle class in emerging markets, its role as an asset of last resort, and the ever-expanding use of gold in technological applications.

In addition, central banks continue to buy gold to diversify their foreign reserves and counterbalance fiat currency risk, particularly as emerging market central banks tend to have high allocations of US treasuries. Central bank demand for gold in 2018 alone was the highest since 2015, as a wider set of countries added gold to their foreign reserves for diversification and safety.

More generally, there are four attributes that make gold a valuable strategic asset by providing investors:

- a source of return

- low correlation to major asset classes in both expansionary and recessionary periods

- a mainstream asset that is as liquid as other financial securities

- a history of improved portfolio risk-adjusted returns.

‘Outlook 2019: Global economic trends and their impact on gold’ – Full report from World Gold Council here

News and Commentary

Palladium hits record high on China impetus; lower dollar lifts gold (Reuters.com)

Gold lifted by weaker dollar as market ponders pace of Fed interest-rate hikes (MarketWatch.com)

Bank of England’s Carney sees China’s yuan as possible reserve currency (Reuters.com)

ISIS ‘kills’ five UK soldiers in Syria rocket attack (RT.com)

Stock Rally Takes a Break as Bonds Rise, Oil Drops: Markets Wrap (Bloomberg.com)

Tanzania’s president orders central bank to create gold reserve (TheEastAfrican.co.ke)

May Stares Into Brexit Abyss as Parliament Takes Control (Bloomberg.com)

These Nine Charts Show Just How Deeply Brexit Has Divided Britain (Bloomberg.com)

The EU In 2019 – The Problem Of Survival (ZeroHedge.com)

Outlook 2019: Economic trends and their impact on gold (Gold.org)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

09 Jan: USD 1,281.30, GBP 1,006.41 & EUR 1,118.32 per ounce

08 Jan: USD 1,291.90, GBP 1,006.71 & EUR 1,121.62 per ounce

07 Jan: USD 1,291.50, GBP 1,013.83 & EUR 1,129.03 per ounce

04 Jan: USD 1,290.35, GBP 1,016.80 & EUR 1,131.24 per ounce

03 Jan: USD 1,287.95, GBP 1,024.05 & EUR 1,132.62 per ounce

02 Jan: USD 1,287.20, GBP 1,014.44 & EUR 1,125.27 per ounce

Silver Prices (LBMA)

09 Jan: USD 15.62, GBP 12.27 & EUR 13.64 per ounce

08 Jan: USD 15.64, GBP 12.24 & EUR 13.64 per ounce

07 Jan: USD 15.75, GBP 12.35 & EUR 13.77 per ounce

04 Jan: USD 15.70, GBP 12.40 & EUR 13.76 per ounce

03 Jan: USD 15.53, GBP 12.37 & EUR 13.70 per ounce

02 Jan: USD 15.44, GBP 12.19 & EUR 13.51 per ounce

Recent Market Updates

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

– Everything Bubble Started Bursting In 2018 – GoldCore Video

Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

11, January

– Gold to outperform stocks again in 2019 as seen in 2018 and last 15 years

– 15% to 20% gains for gold and 30% to 40% gains for silver quiet likely

– Given scale of under valuation, strong fundamentals including robust demand and anemic supply and high level of risk, both precious metals are likely to surge in 2019 and 2020

– Gold and silver likely to reach highs over $1,650 and $28 per ounce

– On the high side, we may see a price increase of 30% for gold in 2019 as was seen in 2007 and 2010 and silver may surge 80% as it did in 2010 is possible (see table)

– Past performance is no guarantee of future returns but along with the positive supply and demand fundamentals and the uncertain economic backdrop, they give an indication of possible returns

– Currency reset would see gold to $5,000 to $10,000 and silver at over $250 per ounce as predicted by Rickards and others

Watch Latest Video Update On YouTube Here

Mark O’Byrne Executive Director

-END-

* * *

GATA STORIES AS IT RELATES TO PHYSICAL GOLD/SILVER

For your interest:

4 on trial for the theft of the largest Cdn gold coin ever minted: 221 pounds from the Berlin museum]

(courtesy APnews/GATA)

4 on trial in theft of huge gold coin from Berlin museum

Submitted by cpowell on Thu, 2019-01-10 15:11. Section: Daily Dispatches

From the Associated Press, New York

Thursday, January 10, 2019

https://www.apnews.com/783eafeee37b4eeeaf178534c465ae43

BERLIN — Four young men have gone on trial over the brazen theft of a 100-kilogram (221-pound) Canadian gold coin from a Berlin museum.

The “Big Maple Leaf” coin, worth several million dollars, was stolen from the Bode Museum in March 2017.

…

Three men, identified only as Wissam R., Ahmed R., and Wayci R., are accused of stealing the coin during the night using a wheelbarrow to haul it away. The fourth suspect, Dennis W., worked as a guard at the museum for a private security firm and is accused of scouting out the scene.

German news agency DPA reported that the four men, aged between 20 and 24 years, went on trial today in Berlin district court.

Investigators believe that the suspects cut up the coin and sold the pieces.

* * *

end

Barrick’s new CEO dismisses the media’s obsession that they will move their headquarters from Canada as sheer hysteria

(courtesy Bochove/Bloomberg/GATA)

Barrick Gold’s new CEO dismisses Canada HQ debate as ‘hysteria’

Submitted by cpowell on Thu, 2019-01-10 18:49. Section: Daily Dispatches

By Dnaielle Bochove

Bloomberg News

Thursday, January 10, 2019

Barrick Gold Corp.’s new chief executive is surprised by the “hysteria” over whether the world’s largest gold miner will remain a Canadian company.

Barely a week after his Channel Islands-based Randgold Resources Ltd. merged with Barrick, Mark Bristow says he is determined to keep the global miner headquartered in Toronto — or at least as committed as he is to any head office.

Mining industries have to catch up with the reality of the times,” Bristow said in a phone interview from Jackson Hole, Wyoming, where he maintains a home. “We can’t sit in this massive corporate office — this old tradition — trying to run an organization that’s global by remote control.”

Bristow’s comments come in the wake of critical commentary by industry veteran Pierre Lassonde, who said Barrick’s reduced presence in Canada amounts to the kind of hollowing out of the country’s mining sector that Barrick’s late founder, Peter Munk, vigorously opposed. Lassonde particularly criticized that Barrick’s top company leaders — Bristow, Chief Financial Officer Graham Shuttleworth, and Executive Chairman John Thornton — aren’t based in Canada. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-10/barrick-gold-s-new-ce…

… end

Yellow vest protesters are aiming to crash the French banking system by removing their euros from the banks. Also the yellow vest protests are moving to London where we will see protests there on the weekend

(courtesy AP/GATA)

Yellow vest protesters aim to crash French banking system

Submitted by cpowell on Fri, 2019-01-11 00:56. Section: Daily Dispatches

Yellow Vest Protesters to Withdraw All Their Euros in Massive Run on French Banks

From News Corp., Associated Press, and Agence France-Presse

via News Corp. Australia, Sydney

Thursday, January 10, 2019

Yellow vest activists are urging French citizens to empty their bank accounts and spark a massive run on the country’s banks in their longstanding fight with the government — which could lead to the collapse of its banking system.

The call for citizens to withdraw all their euros come as copycat protests are planned for Britain on the weekend.

The left-wing “People’s Assembly” activist group has invited thousands of people to wear yellow vests at an anti-austerity “Britain is broken” march in central London this weekend.

“See you on the streets and don’t forget your #YellowVests,” the group, which is demanding a general election to end the ruling Conservatives’ program of austerity, wrote on Facebook. …

… For the remainder of the report:

https://www.news.com.au/world/europe/yellow-vest-protesters-call-for-hug…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

…

end

this was brought to your attention yesterday but it is worth repeating:

(courtesy Ted Butler/GATA)

Ted Butler: Questions only the Justice Department can get answered about silver manipulation

Submitted by cpowell on Fri, 2019-01-11 01:50. Section: Daily Dispatches

8:50p ET Thursday, January 10, 2019

Dear Friend of GATA and Gold:

Now that the U.S. Justice Department has induced a former trader for JPMorganChase to confess to manipulating the silver market, silver market watchdog Ted Butler writes today that the department should be pursuing several questions that go beyond the “spoofing” highlighted by the guilty plea. Butler helpfully spells them out.

…

Butler concludes: “Having raised the issue of a silver manipulation for more than 30 years and the specific allegation that JPMorgan was the main manipulator since 2008, there would be something wrong if I didn’t feel that the involvement of the Justice Department was the most important development I have seen over both time periods. I have petitioned the U.S. Commodity Futures Trading Commission and CME Group for decades to no avail. It may turn out that I am putting too much faith in the Justice Department for confirming my allegations, but it is at the very pinnacle of a regulatory food chain. It would be unreasonable not to have faith that the Justice Department will do the right thing.”

Butler’s commentary is headlined “Questions Only the Justice Department Can Get Answered” and it’s posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/questions-only-doj-can-get-answered-175…

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-questions-only-the-doj-c…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7427/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7473 /shanghai bourse CLOSED UP 18.78 PTS OR 0.74%

HANG SANG CLOSED UP 145.84 POINTS OR 0.55%

2. Nikkei closed UP 195.98 POINTS OR 0.97%

3. Europe stocks OPENED ALL MIXED

/USA dollar index FALLS TO 95.35/Euro RISES TO 1.1522

3b Japan 10 year bond yield: FALLS TO. +.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.91/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52/98 and Brent: 61.98

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.24%/Italian 10 yr bond yield UP to 2.84% /SPAIN 10 YR BOND YIELD DOWN TO 1.44%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.60: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.29

3k Gold at $1292.10 silver at:15.69 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 9/100 in roubles/dollar) 66.95

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.28 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9829 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1326 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.24%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.71% early this morning. Thirty year rate at 3.04%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

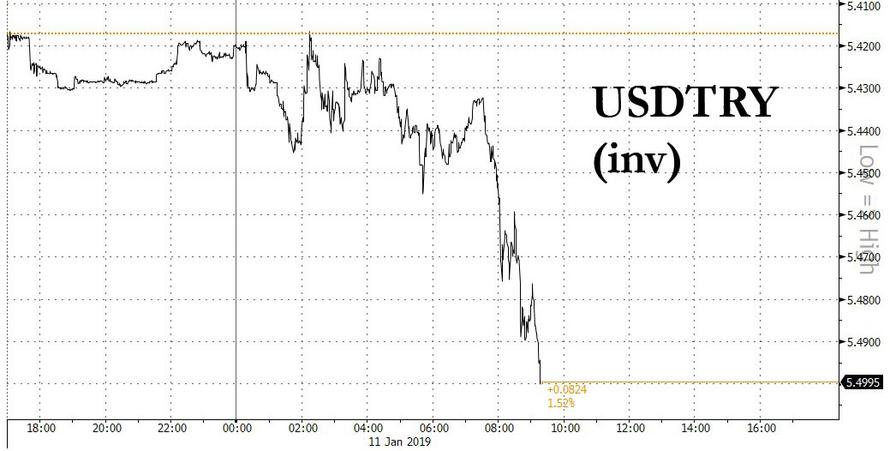

6. TURKISH LIRA: UP TO 5.4464

Futures Slide, Global Rally Fizzles; Oil Set For Longest Rally On Record

“Powell seems to have improved at the art of Fedspeak, using many words but not saying anything substantively new”

Deutsche Bank

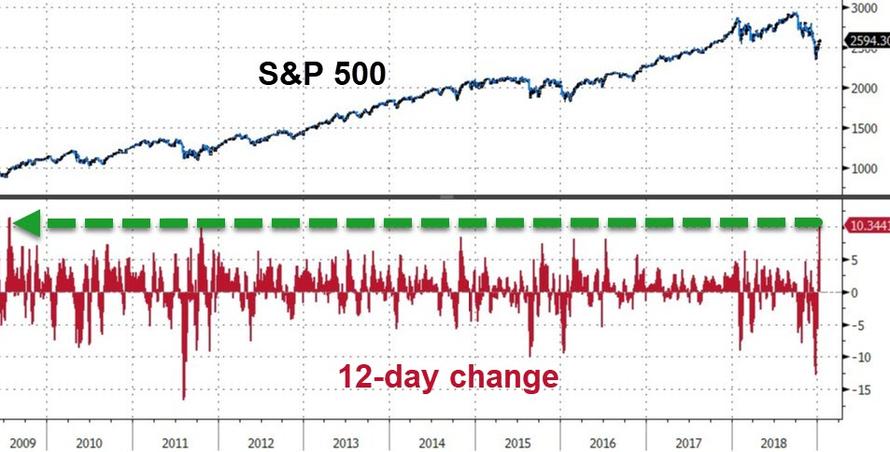

For the second day in a row, the S&P’s recent torrid post-Christmas rally which has seen the S&P up +10.44% over the last 11 sessions, the best such stretch since October 2011, is in danger of ending as U.S. stock futures edged lower 0.3%, while European shares were mixed and Asian markets rose at as sentiment was bolstered by continued dovish tone from the Federal Reserve and hopes for a breakthrough on trade. The dollar slide continued even as Treasuries finally advanced and the oil rally continued for a record 10th day, while the US government shutdown tied the longest ever, as it entered its 21st day.

With renewed promises of patience from Federal Reserve, as Fed vice chair Clarida followed Powell on Thursday evening saying the central bank should be ready to adjust monetary policy if headwinds to the economy from financial markets or global growth prove persistent, suggesting caution about moving ahead with interest-rate increases, while the ECB was mulling another dump of cheap money in the form of TLTRO and news that trade talks between Washington and Beijing are moving to higher levels, the Friday feeling was in full effect, even if it appeared to peak in the US where futures initially rose then dropped to session lows.

The Fed’s dovish stance also pushed down the dollar and nudged Treasury yields lower after five days of gains again. That cheered emerging markets and confidence more generally having been flattened during the brutal end to 2018: “Equities are having a good run after a pretty horrible end to last year,” said Rabobank quantitative analyst Bas Van Geffen. “It is the changing wording of the Fed, it seems to be making more and more room for an eventual pause (in the rate hike cycle)”.

Asia had crawled to a 5-week high overnight as shares rose in Shanghai, Tokyo, Seoul and Hong Kong while European stocks were on the edge of fourth straight day of gains and longest winning streak since September. S&P 500 futures and Nasdaq indexes pointed to a slightly softer open in New York after jumping early in the session after Steven Mnuchin said Chinese Vice Premier Liu He will “most likely” visit Washington on Jan. 30 and 31 for further trade talks. China’s yuan, which slumped last year as trade tensions worsened, is heading for its best week since 2005, back when the country dropped a fixed peg to the dollar.

A pause to the recent massively overbought rally is to be expected: the S&P 500 is now up more than 10% from its Dec. 26 low – one day after Steven Mnuchin spoke to the Plunge Protection team. The S&P is also up on 6 out of the 7 sessions in 2019 so far and each of the last 5. That’s the best streak since September and if it rises again today, it will achieve in the second week of the year a feat that only occurred twice in all of 2018. The index is now up +10.44% over the last 11 sessions, the best such stretch since October 2011.

In Asia, the ASX 200 (-0.3%) and Nikkei 225 (+1.0%) were mixed with the initial upside in Australia clouded by weakness in the key financials and mining related sectors, while the Japanese benchmark outperformed as it coat-tailed on the recent USD/JPY moves. Elsewhere, Shanghai Comp. (+0.7%) and Hang Seng (+0.5%) conformed to the overall positive risk tone following the recent trade-related optimism with Vice Premier Liu He said to possibly visit the US later this month and amid hopes of further supportive measures as China may adopt more tax cuts for the manufacturing sector.

Failing to carry over Asian strength, European indices are mixed, having pared back some of the initial gains from the open. Some initial outperformance was seen in the FTSE 100 (+0.1%) jumped as much as 0.7 percent on the back of the latest slide in sterling against the euro on mounting Brexit uncertainty while UK housing names were higher after the sector was upgraded by BAML, with Persimmon (+4.4%), Taylor Wimpey (+4.8%) and Barratt Development (+2.6%) at the top of the index, however, the index was later pressured on currency effects as Sterling whipsawed on Brexit developments. Other notable movers include, Richemont (+2.3%) after the Co’s Q3 revenue of EUR 3.92bln was in line with the expected EUR 3.93bln and posting a 5% rise in constant currency sales for the October-December period.

The market’s bullish mood was supported by Fed Chairman Jerome Powell who underscored the message of patience with further interest-rate hikes, while saying the central bank will keep shrinking its balance sheet. At the Economic Club of Washington on Thursday, Fed chief Jerome Powell reiterated the U.S. central bank would be patient about hiking interest rates.

“The word ‘patient’ is used often when the Fed’s policy direction is still tightening but its next rate hike can wait for a considerable time. So risk assets now enjoy support from what we can call Powell put,” said Tomoaki Shishido, economist at Nomura Securities. “Similarly, Trump also softened his stance on China after sharp falls in stock prices. He has offered an olive branch to China and there’s no reason China would not want to accept it,” he added.

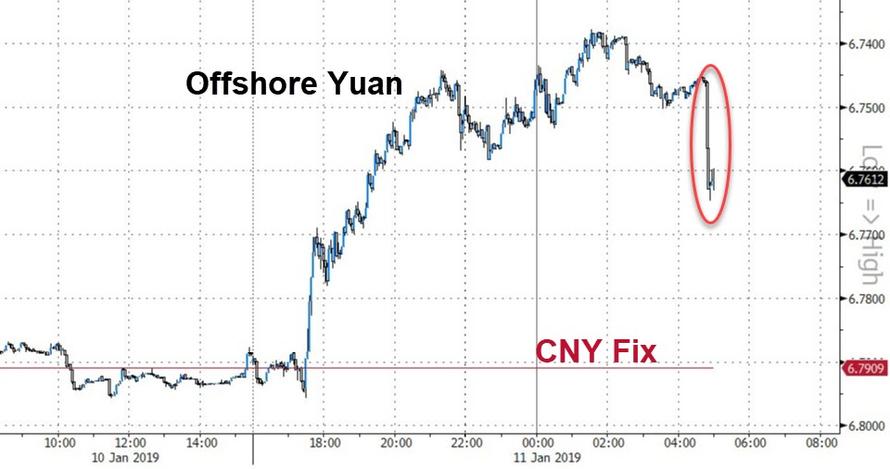

In FX, the dollar was on course for its fourth straight weekly fall against other top world currencies having also hit a three-month low the previous day. The flip side was that the Japanese yen was a shade higher again at 108.29 per dollar and the euro was up at $1.1530 on course for its best week since August. But it is China’s yuan that has been the real mover though. Against the backdrop of the sensitive trade negotiations, the Chinese currency has risen 1.8 percent this week which is its biggest gain since July 2005 when Beijing abandoned the yuan’s peg to the dollar.

Yuan traders had started offloading dollars in their proprietary accounts on Thursday following the wrap-up of three-day U.S.-China trade talks in Beijing. Markets treated absence of any bad news from those negotiations as good news. “Some corporate clients were joining to sell their dollars,” said a trader at a foreign bank in Shanghai.

Bond markets have been turning too. U.S. Treasury debt prices erased early gains after a soft 30-year bond auction and in reaction to Powell’s comments on the Fed “substantially” reducing the size of its balance sheet. The 10-year U.S. Treasuries yield last stood over 2bps lower at 2.7168%.

Finally in commodities, the notable mover was crude as oil rose for a 10th consecutive day, heading for its longest run of gains on record, as OPEC cutbacks reined in supply while the plunging dollar boosted demand. Futures returned to a bull market this week after recovering more than 20% from the lows reached in December. Saudi Arabia gave assurances on Wednesday that the production cuts by OPEC and its partners that came into effect this month will be deep enough to prevent any surplus.

“Sentiment in the oil market has turned around this week,” said Jens Naervig Pedersen, senior analyst at Danske Bank A/S in Copenhagen. The reversal “is on the back of a combination of OPEC+ production cuts taking effect, a stabilization in risk sentiment in equity markets and a weaker dollar. In addition, the oil market will be monitoring trade talks, which seem to progress slowly.”

In us political news, President Trump said he will most likely declare an emergency if there is no border deal but added should be able to make a deal with Congress, while there were earlier reports that US President Trump had been briefed regarding plan to use Army Corps of Engineers funding to border wall construction. Also commented that he has the absolute right to declare a national emergency and is not doing it yet but will do if shutdown carries on.

In the latest Brexit news, it is looking increasingly likely to be delayed beyond March 29th amid a backlog of essential bills, according to Cabinet Ministers cited by the Evening Standard. However, this has been dismissed by a UK PM May spokesperson. UK PM May launched an appeal to Britain’s biggest unions last night in an attempt to win Labour support for her Brexit deal.

The partial U.S. government shutdown threatens to extend into a fourth week with about 800,000 federal workers set to miss their first paychecks. Economic data include CPI inflation readings

Market Snapshot

- S&P 500 futures down 0.3% at 2,588

- STOXX Europe 600 up 0.3% to 350.07

- MXAP up 0.5% to 151.74

- MXAPJ up 0.4% to 491.54

- Nikkei up 1% to 20,359.70

- Topix up 0.5% to 1,529.73

- Hang Seng Index up 0.6% to 26,667.27

- Shanghai Composite up 0.7% to 2,553.83

- Sensex down 0.3% to 36,012.53

- Australia S&P/ASX 200 down 0.4% to 5,774.58

- Kospi up 0.6% to 2,075.57

- German 10Y yield fell 2.0 bps to 0.235%

- Euro up 0.2% to $1.1522

- Brent Futures up 1% to $62.30/bbl

- Italian 10Y yield rose 0.9 bps to 2.527%

- Spanish 10Y yield fell 2.4 bps to 1.427%

- Brent Futures up 1% to $62.30/bbl

- Gold spot up 0.5% to $1,293.34

- U.S. Dollar Index down 0.2% to 95.38

Top Overnight News from Bloomberg

- Chinese Vice Premier Liu He is said to be scheduled to visit Washington on January 30 and 31 for further trade talks

- Fed Vice Chairman Richard Clarida said the central bank should be ready to adjust monetary policy if headwinds to the economy from financial markets or global growth prove persistent, suggesting caution about moving ahead with interest-rate increases

- Japan’s Prime Minister Shinzo Abe told Theresa May the whole world wants to avoid a no-deal Brexit even as she faces likely defeat when Parliament votes on her plan next week

- The Trump administration was said to have directed the U.S. Army Corps of Engineers to examine whether the wall could be funded using money from emergency funding. Trump cancels trip to Davos gathering as shutdown grinds on

- The European Central Bank should wait until the spring before tweaking its policy and keep all options open amid economic weakness and a fragile global outlook, according to Governing Council member Francois Villeroy de Galhau

- Fast-money traders seem to have lost their stomach for betting on an interest rate lift-off in the heart of Europe. They entered 2019 with the smallest value of short wagers against German bunds in more than two years, according to exchange- traded product data

- A trader who wants BNP Paribas SA to pay him 163 million euros ($188 million) over a “fat-finger” mistake is betting that Paris judges will help him avoid having to give up most of the claim

- Emmanuel Macron next week launches a three- month national debate that he hopes will dissipate the anger displayed in the recent violent protests, without derailing the reforms he insists France needs

- An American military official tells AP the U.S.-led military coalition has begun the process of withdrawing troops from Syria

Asian equity markets traded mostly higher following the 5th consecutive session of gains on Wall Street as global sentiment remained underpined by perceptions of a more patient Fed approach. ASX 200 (-0.3%) and Nikkei 225 (+1.0%) were mixed with the initial upside in Australia clouded by weakness in the key financials and mining related sectors, while the Japanese benchmark outperformed as it coat-tailed on the recent USD/JPY moves. Elsewhere, Shanghai Comp. (+0.7%) and Hang Seng (+0.5%) conformed to the overall positive risk tone following the recent trade-related optimism with Vice Premier Liu He said to possibly visit the US later this month and amid hopes of further supportive measures as China may adopt more tax cuts for the manufacturing sector. Finally, 10yr JGBs were lacklustre on profit taking following recent gains and with demand also limited by the upside in riskier assets.

Top Asian News

- Nissan Shunned in Bond Market on Ghosn But Banks Seen Supportive

- Why Ghosn’s Still Jailed and What It Says About Japan: QuickTake

- What India’s Top Three Mutual Funds Bought and Sold in December

- Chinese Stocks Post Biggest Weekly Gain in Nearly Two Months

Major European indices are mixed [Euro Stoxx 50 Unch], having pared back some of the initial gains from the open. Some initial outperformance was seen in the FTSE 100 (+0.1%) which is lead by strong performances in UK housing names after the sector was upgraded by BAML, with Persimmon (+4.4%), Taylor Wimpey (+4.8%) and Barratt Development (+2.6%) at the top of the index, however, the index was later pressured on currency effects as Sterling whipsawed on Brexit developments. Sectors are similarly in the green with some slight outperformance seen in energy names. Other notable movers include, Richemont (+2.3%) after the Co’s Q3 revenue of EUR 3.92bln was in line with the expected EUR 3.93bln and posting a 5% rise in constant currency sales for the October-December period. Meanwhile, Suez (-3.1%), Veolia (-2.6%) and Sage Group (-2.6%) are all in the red after being downgraded.

Top European News

- Crispin Odey Says Believes Brexit Will Not Happen: Reuters

- Euro Bond Supply Avalanche Meets Wall of Cash From Fund Managers

In FX, the dollar session was choppy but ultimately on the backfoot after losing the 95.500 level in early Asia-Pac trade as the Fed signalled a more patient approach ahead of the US CPI release later today. Both Fed Chair Powell and Vice Chair Clarida noted the Central Bank has the ability to be patient and flexible on rates given the State-side inflation data. As such the DXY fell to an overnight session low of 95.322 (vs. high of 95.508) and currently hovers around the middle of the range with US CPI in sight. Lloyds notes that the sharp decline in energy will likely weight on the headline CPI as they forecast a fall to 1.9% from 2.2%, though they expect the core figure to remain steady at 2.2%.

- AUD,NZD, CNY, CAD – The marked outperformers and major beneficiaries as the USD/CNY is poised for its best week since 2005 with aid from the dovish Fed and a sub-6.80 PBoC fix. AUD/USD currently resides north of 0.7200 (vs. low of 0.7183) and reached levels last seen mid-December as optimistic Australian retail sales also underpinned the Aussie currency. Meanwhile, the Kiwi stands at the G10 leader as tailwind from its antipodean counterpart boosted the NZD/USD above its 50 and 200 DMA at 0.6786 and 0.6799 respectively to test 0.6840 to the upside, with the DMAs also set to form a golden cross. Finally, the Loonie is on the front foot as it reaps its reward from the declining greenback and the rising oil price with USD/CAD now below 1.3200 (vs. high of 1.3245) ahead of its 100 DMA at 1.3169.

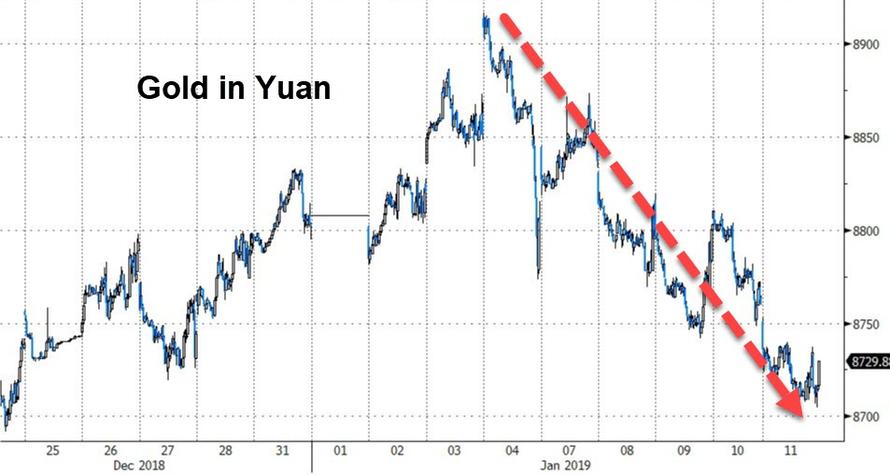

In commodities, Brent (+0.6%) and WTI (+0.8%) prices are in the green benefiting from the positive sentiment seen across US and Asian sessions after dovish comments from multiple Fed speakers. Russian oil output for January 1st-10th has dropped to 11.38mln BPD from 11.45mln BPD in December; additionally, Russian Energy Minister Novak is reportedly planning to attend the upcoming January 22nd-25th Davos summit. Gold (+0.5%) prices are just shy of USD 1295.2/oz, the sessions high, following dovish comments from the Fed applying downward pressure to the dollar. Copper prices are similarly higher on the positive market sentiment, in particular that Chinese Vice Premier He is to visit the US later on in the month. Elsewhere, India’s steel ministry is refusing to back down on tougher import rules on steel, pressuring automakers into using local steel instead.

US Event Calendar

- 8:30am: US CPI MoM, est. -0.1%, prior 0.0%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- US CPI YoY, est. 1.9%, prior 2.2%; CPI Ex Food and Energy YoY, est. 2.2%, prior 2.2%

- 8:30am: Real Avg Weekly Earnings YoY, est. 1.2%, prior 0.54%;

- 2pm: Treasury monthly budget statement postponed by govt shutdown

DB’s Jim Reid concludes the overnight wrap

Fortune continues to favour the brave in markets at the moment following another broadly positive last 24 hours for risk assets. It may have been a less convincing session on Wall Street last night compared to recent days with the S&P 500 for example passing between gains and losses no less than 19 times, however, a +0.45% closing move for the index does now mean it’s finished higher in 6 out of the 7 sessions in 2019 so far and each of the last 5. That’s the best streak since September and if it rises again today, it will achieve in the second week of the year a feat that only occurred twice in all of 2018. The index is now up +10.44% over the last 11 sessions, the best such stretch since October 2011.

There’s little doubt that sentiment over this period has been largely driven by communications from the Fed, and it’s no surprise that attention focused yesterday on Chair Powell’s public remarks. However, as we enter the 12th month of his Chairmanship, he seems to have improved at the art of Fedspeak, using many words but not saying anything substantively new. Markets were broadly unchanged during and immediately after his speech, and the S&P 500 rallied through the afternoon to ultimately close higher.

In terms of substance, Powell reiterated that the economy is “doing quite nicely” though he is attentive to “the financial markets expressing a view about the concern about downside risks associated with global growth and with trade.” To balance the divergent signals between strong data and tepid markets, Powell said he plans to “be patient and flexible and wait and see what does evolve.” So that’s consistent with our economists’ base expectations for two more rate hikes this year. Powell also repeated his guidance on the balance sheet runoff and the uncertainty over its terminal size, and he mentioned China as a key uncertainty to the global growth outlook.

After markets closed, Vice Chair Clarida presented a similar message. He referenced tighter financial conditions and global growth as key “crosswinds” affecting the US economy, and argued that “if these crosswinds are sustained, appropriate forward-looking monetary policy should respond.” He said the Fed would change its balance sheet policy if necessary, though any policy shifts would have to be consistent with their mandate. So, another Fed official seemingly in support of a pause in the rate hike cycle.

Back to markets where the DOW and NASDAQ also gained +0.51% and +0.42%, respectively yesterday. The VIX also ended at 19.50 which was down about half a point while 2y and 10y rates +2.3bps and +3.2bps respectively, meaning the curve was about 1bp higher at +16.5bps. The USD strengthened +0.32% while WTI oil closed up +0.44% to take its remarkable run of daily gains to 9 and the longest since January 2010. The price is up +17.89% during this current run which is the most over 9 sessions since March 2016.

Early on in the day there was some damage done by the US retail sector with Macy’s grabbing much of headlines with shares plummeting -17.69% for its worst-ever loss, after cutting its annual earnings forecast. Kohl’s also dropped -4.81% after reporting disappointing holiday period sales while Barnes & Noble dropped -15.76% in the wake of also downgrading earnings guidance. Target’s (-2.85%) holiday sales actually appeared more in-line with estimates however the company failed to escape the wider sector carnage. It was a similar story for retail CDS with spreads +36bps wider for Macy’s, +16bps wider for Kohl’s and +12bps for Nordstrom. The broader CDX IG index did however finish 2bps tighter while US HY cash spreads also tightened 2bps for its fifth consecutive rally, over which it has narrowed a remarkable -87bps.

Speaking of earnings, next week we’re due to get Q4 reports from 35 S&P 500 companies including the banks. So this should give investors something else to focus on other than the repetitive trade-related headlines of late. As an early preview, Q4 earnings growth is expected to be 11.4% which compares to around 25% growth reported in each of the prior three quarters according to data from Factset. Still, if Q4 comes in in-line this would be the fifth straight quarter of double digits earnings growth. It’s worth also noting that over the past five years on average, actual earnings have exceeded estimated earnings by nearly 5%. So history would suggest that there is upside to forecasts.

The partial government shutdown in the US is also busy repeating and has now entered its 21st day, tying the longest-ever shutdown, with around 800k federal workers expected to not receive their paychecks today. Indeed, there was a big uptick in jobless claims in DC last week, as furloughed workers are entitled to unemployment benefits until the shutdown is resolved, so we’re beginning to see the effects of the standoff in the macro data. Another side-effect of the shutdown is the delay to some of the GDP-sensitive data releases which is making life harder for economists to get a comprehensive read of how the US is tracking in the last couple months. With the Fed emphasizing data dependency this is clearly proving an issue. Today’s December CPI report won’t be affected however with the consensus expecting a +0.2% mom core reading which should be enough to hold the annual rate at +2.2% yoy. Our US economists expect the same which should keep Fed rate hikes in play this year if various uncertainties are resolved.

To Asia now where markets are largely tracking Wall Street’s gains last night with the Nikkei (+0.97%) leading the way, followed by the Hang Seng (+0.18%), Shanghai Comp (0.16%) and Kospi (+0.61%). Sentiment has also been given a boost by an overnight tweet from a WSJ journalist confirming that China’s Vice Premier Liu He is scheduled to visit US for trade talks on Jan 30 and 31st. Meanwhile, China’s onshore yuan is up +0.58% to 6.7495, the highest since July 2018 with the weakness in US dollar (-0.19%) also contributing to the rise. Futures in the US are however slightly down as we type (S&P 500 -0.11%).

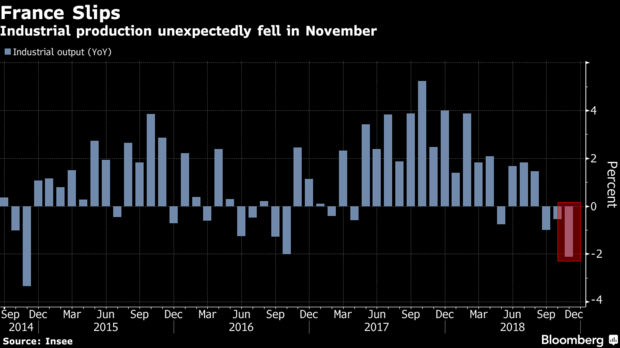

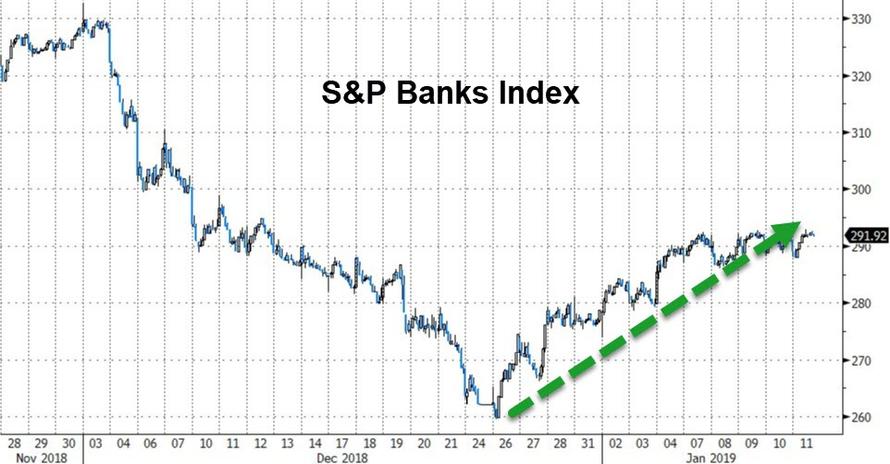

Back to yesterday where in Europe the STOXX 600 more than fought off an early decline at the open to close up +0.34%. There were gains also for the DAX (+0.26%) and FTSE MIB (+0.63%) although the CAC (-0.16%) underperformed not helped by a soft French industrial production print (-1.3% mom vs. 0.0% expected). Bonds were a touch stronger (Bunds -2.2bps) with the ECB minutes confirming that the board did discuss changing the communication on language to acknowledge economic risks as tilting to the downside, although holding fire at the meeting. There was also a reference to TLTROs, which may have helped an index of bank stocks to outperform, gaining +0.75%.

In other news, PM May confirmed late afternoon yesterday that the UK is still in talks with the EU over the backstop and that government is still seeking support for a deal across parliament. Yesterday Labour leader Corbyn said that he would take a confidence motion when it can succeed (so not necessarily immediately after next week’s vote, should May lose) and also that his party would not rule out an Article 50 extension should Labour come to power. Overall though there wasn’t much new in Labour’s policy on Brexit yesterday and Sterling nudged down -0.33% by the end of play. Across the pond it’s worth adding that President Trump said that he will not attend Davos later this month as a result of the government shutdown. An indication maybe that the shutdown will continue for a while longer, or alternatively perhaps the ski conditions aren’t up to scratch yet.

Finally, looking at the rest of the day ahead, this morning and shortly after this hits your emails we’re due to get the December Bank of France industrial sentiment reading followed later by a data dump out of the UK which includes November trade balance, industrial and manufacturing production, construction output and monthly GDP data. This afternoon in the US the aforementioned US CPI report will no doubt be the big highlight, especially with the monthly budget statement postponed due to the partial government shutdown. Meanwhile, we’ll finally get a rest from all the Fedspeak with no speeches due however over at the ECB we are due to hear from Mersch and Visco.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 18.78 PTS OR 0.74% //Hang Sang CLOSED UP 145.84 POINTS OR 0.55% /The Nikkei closed UP 195.90 POINTS OR 0.97% / Australia’s all ordinaires CLOSED DOWN 0.33%

/Chinese yuan (ONSHORE) closed DOWN at 6.7427 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.98 dollars per barrel for WTI and 61.92 for Brent. Stocks in Europe OPENED /MIXED

//. ONSHORE YUAN CLOSED UP AT 6.7427 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7473: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

Poland Arrests Huawei Executive On Espionage Charges

In the latest sign that the US’s western allies are heeding its warnings about the espionage threat posed by Huawei and its executives, the Wall Street Journal reported on Friday that Poland had arrested a Huawei executive based in the country and accused him of “conducting high-level espionage on behalf of a Chinese spy agency.”

According to a source quoted by Reuters, the executive was well-known in local tech circles.

“The Chinese national is a businessman working for a major electronics company…the Pole is a person known in circles associated with cyber business,” Maciej Wasik, the deputy head of Poland’s special services, told PAP.

Officers from Poland’s counterintelligence agency have searched Huawei’s office, leaving with documents and electronic data. They also searched the executive’s home on Tuesday.

The executive’s name wasn’t released. A Chinese national, he was identified only as a graduate of one of China’s top intelligence colleges, as well as a former employee of the Chinese consulate in the port city of Gdansk.

But the Chinese national wasn’t the only person arrested in the crackdown: Polish police also arrested a citizen who was identified as a former top official in the Polish intelligence agency’s IT security department.

“Huawei is aware of the situation, and we are looking into it,” a spokesman for the company said.

Both suspects have been charged with espionage, a crime that carries up to 10 years’ imprisonment. They have reportedly pleaded not guilty. The arrest comes little more than a month after Huawei CFO Meng Wanzhou was arrested in Vancouver on charges of helping the company violate US and EU sanctions against Iran.

While little is known about this incident, we will be watching out for reports that Chinese authorities have arrested a handful of Polish nationals on vague “national security”-related violations.

end

the POBC not excited seeing the rise in the yuan so it jawboned it lower:

(courtesy zerohedge)

Yuan Slides After PBOC Reportedly Wary Of Recent Sharp Gains

As we detailed last night, the recent surge in the yuan has been almost unprecedented against a backdrop of dismal economic data, a still tightening Fed and an aggressively easing PBOC.

And it appears PBOC has had enough of it as MNI reports this morning that the central bank does not want a sharp appreciation by the yuan, citing a source close to the People’s Bank of China.

That prompted an immediate reversal of some of yesterday’s gains…

Not entirely a surprise, as Michael Every, head of Asia financial markets research at Rabobank in Hong Kong, warned:

“The yuan can hold up fine” until the Fed hikes again, trade tensions resume and China “goes all-in on stimulus,”

“It’s a ‘when’ and not an ‘if’ for when it reverses direction again and we test new lows.”

It seems when is now. Will Yuan catch down to ‘fundamentals’?

4.EUROPEAN AFFAIRS

FRANCE

The yellow vest movement urges supporters to break the bank by causing a bank run. The yellow vest movement is moving also to England

(courtesy zerohedge)

French Yellow Vest Protesters Urge Supporters To Spark Bank Run With Mass Withdrawals

Activists from the Gilets Jaunes (Yellow Vest) movement have vandalized nearly 60% of France’s country-wide speed camera network, according to Interior Minister Christophe Castaner, who said that the wilful damage was a threat to road safety and endangered lives, according to the BBC.

The BBC’s Hugh Schofield, in Paris, said evidence of the vandalism is visible to anyone driving around France, with radar cameras covered in paint or black tape to stop them working.

But the extent of the damage – now believed to affect more than half of all 3,200 speed cameras in the country’s network – was unknown until Mr Castaner’s statement on Thursday.

He said the devices had been “neutralised, attacked, or destroyed” by members of the protest movement. –BBC

Speed limits in France have become a hot-button topic, after the Macron government lowered the limit on many roads from 90 km/h (55 mph) to 80 km/h (50 mph) early last year.

Yellow Vest protesters upset over an increase in fuel taxes have also complained about the rising costs of commuting for those who can’t afford to live near urban centers where they work – citing speed cameras and toll roads in their complaints.

Bank run?

While the Yellow Vest movement has been taking to the streets for violent clashes with French police, activists from the movement are now recommending that French protesters empty their bank accounts to spark a bank run – in a move which one protester, Maxime Nicolle, called a “tax collector’s referendum.”

“We are going to get our bread back … You’re making money with our dough, and we’re fed up,” said Nicolle in a video message, as reported by the Associated Press.

The movement’s adherents said they hoped the banking action will force the French government to heed their demands, especially giving citizens the right to propose and vote on new laws. –Associated Press

And while outraged Yellow Vests continue their protests, the Macron government is scrambling to calm down the anti-government movement with a series of economic measures which have thus far proven ineffective.

Prime Minister Edouard Philippe gave details Wednesday of a “big debate” the government plans to start next week in all the regions of France.

“We want it to be rich, impartial and fruitful,” Philippe said.

The debates will focus on four main topics: climate change, democratic issues, taxes and public services, the prime minister said. Anyone can propose a local event and an internet platform will provide another venue for discussion, he said.

President Emmanuel Macron proposed the debate as a way for the government to hear and to respond to the movement’s central complaints.

Macron also announced 10 billion euros ($11.5 billion) worth of measures to boost the purchasing power of French households. –Associated Press

Around 200 Yellow Vest protesters – which included trade union members, gathered in the Paris suburb of Creteil, as Macron visited a handball facility turned into a handball gymnasium (what?).

Police used tear gas to keep angry protesters away from the French leader.

Pound Jumps On Report Brexit To Be Delayed

Brexit Day is less than three months away and never during the process has the UK’s fumbling attempt to organize an ‘orderly’ exit from the trade block looked more fraught with conflict and chaos. After returning from their holiday break this week, MPs promptly rebelled against the government, passing a series of amendments over objections from the government that will make it extremely difficult to run down the clock to force MPs to either hold their noses and accept the deal she negotiated with the EU, or risk the pandemonium that could follow a ‘no deal’ Brexit.

With circumstances finally starting to shift this week following months of deadlock, murmurs about the possibility of delaying Brexit Day have grown ever-louder. Which is why it’s hardly a surprise that, on Friday, an anonymously sourced report in the Evening Standard cited “senior cabinet officials” claiming Brexit Day would likely be delayed sparked a brief rally in the pound.

GBP/USD climbed as much as 0.8% to $1.2851, leaving it on track to strengthen for a fourth-straight week.

In the report, ES’s sources pointed out that the withdrawal treaty isn’t the only long-running controversy that must be brought to a conclusion before Brexit Day. There are at least “six essential bills” that must be passed before Britain leaves the European Union.

Here’s a quick rundown of that, and two other controversies that stand in the way of a workable Brexit:

- Senior ministers told the Standard that a majority of the Cabinet now support the idea of staging indicative votes in the Commons to see if a different Brexit plan is supported, despite Theresa May publicly opposing the idea.

- Work and Pensions Secretary Amber Rudd refused three times on live radio to deny she would resign if the Prime Minister attempted a disorderly departure from the EU without securing a withdrawal deal.

- Foreign Secretary Jeremy Hunt warned that “Brexit paralysis” was a risk if MPs vote down Mrs May’s deal on Tuesday but lack a majority for a different deal. He said it was clear that a no-deal Brexit would be blocked by Parliament following the landmark votes earlier this week.

While a delayed Brexit deadline would be positive for the pound, it would not be a “big game changer” due to the lack of clarity around what Parliament wants, said Mikael Olai Milhoj, analyst at Danske Bank.

“Positive as it means lower probability of no-deal Brexit, but should not be a big game changer”.

The rally started to fade as Theresa May poured cold water on the reports, saying there is not such plan in place and that the government’s policy is not to delay the UK’s departure from the EU.

END

A super commentary from Alasdair Macleod on the euro as it stands today. It gives a terrific history of how we got to this position today. As i have pointed out to you on several occasions, the ECB has stopped purchasing of all Euro based countries on Dec 31.2018. This will lead to the collapse of Europe as there will be nobody around to purchase the bonds of Italy, Portugal, France and Belgium

(courtesy zerohedge)

The Tragedy Of The Euro

Authored by Alasdair Macleod via GoldMoney.com,

After two decades, the euro’s minders look set to drive the Eurozone into deep trouble. December was the last month of the ECB’s monthly purchases of government debt. A softening global economy will increase government deficits unexpectedly. The consequence will be a new cycle of sharply rising bond yields for the weakest Eurozone members, and systemically destabilising losses in the bond portfolios owned by Eurozone banks

The blame-game

It’s the twentieth anniversary of the euro’s existence, and far from being celebrated it is being blamed for many, if not all of the Eurozone’s ills.

However, the euro cannot be blamed for the monetary and policy failures of the ECB, national central banks and politicians. It is just a fiat currency, like all the others, only with a different provenance. All fiat currencies owe their function as a medium of exchange from the faith its users have in it. But unlike other currencies in their respective jurisdictions, the euro has become a talisman for monetary and economic failures in the European Union.

Recognize that, and we have a chance of understanding why the Eurozone has its troubles and why there are mounting risks of a new Eurozone systemic crisis. These troubles will not be resolved by replacing the euro with one of its founding components, or, indeed, a whole new fiat-money construct. It is here to stay, because it is not in the users’ interest to ditch it.

As is so often the case, the motivation for blaming the euro for some or all the Eurozone’s troubles is to shift responsibility from the real culprits, which are the institutions that created and manage it. This article briefly summarizes the key points in the history of the euro project and notes how the mistakes of the past are being repeated without the safety-net of the ECB’s asset purchases.

The birth of the euro

To swap a number of existing currencies for a wholly new currency requires the users to accept that the purchasing powers of the old will be transferred to the new. This was not going to be a certainty, and the greatest reservations would come from the people of Germany. Germans saved, and therefore risked the security of their deposits in a new money and monetary system. They were reassured by the presence of the hard-money men in the Bundesbank, who had a mission to protect the mark’s characteristics against the weaknesses that would almost certainly be transferred into the new euro from more inflationary currencies.

These anxieties were assuaged to a degree by establishing the ECB in Frankfurt, close to the watchful eye of the Bundesbank. The other nations were sold the project as bringing greater monetary stability than offered by their individual currencies and the reduction of cross-border transaction costs. Borrowers in formally inflationary currencies also relished the prospect of lower interest rates.

It was clear at the outset that the new omnibus euro required new disciplines, and it was here that the system failed from the outset. Having sensibly set out the euro’s parameters in the Maastricht Agreement, political considerations then took over. The raison d’être of the euro, so far as the politicians were concerned, was to further the European Project and getting countries into the new Eurozone became more important than compliance with the terms.

The terms had been set in the Maastricht Treaty in February 1992, which was signed by the twelve members of the pre-existing European Community. To qualify, membership of the euro required an inflation rate no more than 1.5% higher than the average rate of the three lowest member states, a fiscal deficit of no more than 3% at the end of the preceding fiscal year, a ratio of gross government debt to GDP of no more than 60%, membership of the exchange rate mechanism for two years without devaluation, and long-term interest rates no more than 2% higher than the inflation rates of the three lowest inflation rates.

This was sensible stuff but was then ignored by the Maastricht signatories. Only Luxembourg fully qualified for membership under the Maastricht terms.

Even the EU’s sheet-anchor, Germany, failed. Her budget deficit in 1996 was 4% of GDP. France’s was managed (manipulated?) down to 4% from 5%. Greece’s budget deficit after some very creative accounting was shown as 8%, and Italy’s must have had a papal blessing, because it miraculously fell from 8% to 4%.

Germany’s government debt to GDP in 1996 embarrassingly just exceeded the 60% criteria level set at Maastricht. Belgium’s stood at 130%, Italy’s at 124%, and Greece’s (reportedly) at 110%. What debt? We see no debt. Of the original Maastricht signatories, only France and the UK squeezed through on this condition.

Despite this fudge, ten of the twelve Maastricht signatories went ahead and adopted the euro in 1999 and as circulating currency in 2002. The UK had dropped out of the EMU in September 1992, and Greece was so obviously non-compliant its entry was delayed by two years.

Until the Lehman crisis, national interest rates had converged towards Germany’s under the aegis of a common monetary policy. The ECB’s interest rate policy was necessarily a compromise. At one end of the spectrum were the low rates previously enjoyed by the economies with solid savings rates. These were Germany, Luxembourg, Finland, the Netherlands and Austria.