GOLD: $1290.95 UP $1.65 (COMEX TO COMEX CLOSINGS)

Silver: $15.64 UP 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1291.50

silver: $15.65

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 8 NOTICE(S) FOR 800 OZ (0.0248 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 533 NOTICES FOR 525 OZ (1.6578 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

29 NOTICE(S) FILED TODAY FOR 145,000 OZ/

total number of notices filed so far this month: 615 for 3,075,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3499: UP 23

Bitcoin: FINAL EVENING TRADE: $3625 up 150

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 6/8

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,287.100000000 USD

INTENT DATE: 01/11/2019 DELIVERY DATE: 01/15/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 6

737 C ADVANTAGE 8 2

____________________________________________________________________________________________

TOTAL: 8 8

MONTH TO DATE: 533

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN GOOD SIZED 1111 CONTRACTS FROM 188,825 UP TO 189,936 WITH FRIDAY’S 4 RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2272 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2272 CONTRACTS. WITH THE TRANSFER OF 2272 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2272 EFP CONTRACTS TRANSLATES INTO 11.36 MILLION OZ ACCOMPANYING:

1.THE 4 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.455 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 26,126 CONTRACTS (FOR 9 TRADING DAYS TOTAL 26,126 CONTRACTS) OR 130.63 MILLION OZ: (AVERAGE PER DAY: 2902 CONTRACTS OR 14.514 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 130.63 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 18.56% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 130.63 MILLION OZ.

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1111 WITH THE 4 CENT RISE IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2272 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 3389 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2272 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1111 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.63 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 29 NOTICE(S) FOR 145,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.455 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 1939 CONTRACTS UP TO 479,784 WITH THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $2.30//FRIDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5979 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 5979 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 479,784. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7918 CONTRACTS: 1939 OI CONTRACTS INCREASED AT THE COMEX AND 5979 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7918 CONTRACTS OR 791,800 OZ = 24.63 TONNES. AND ALL OF THIS VERY STRONG DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $2.30??????????

FRIDAY, WE HAD 6128 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 73,384 CONTRACTS OR 7,338,400 OZ OR 228.25 TONNES (9 TRADING DAYS AND THUS AVERAGING: 8153 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 228.25 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 228.25/2550 x 100% TONNES = 8.95% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 228.25 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 1939 WITH THE GAIN IN PRICING ($2.30) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A VERY HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5979 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5979 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 7918 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5979 CONTRACTS MOVE TO LONDON AND 1939 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 30.01 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $2.30 IN FRIDAY’S TRADING AT THE COMEX??????????

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.65 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY/

/INVENTORY RESTS AT 313.632 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1111 CONTRACTS from 188,825 UP TO 189,936 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2272 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2272 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1111 CONTRACTS TO THE 2272 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3383 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.92 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.455 MILLION OZ STANDING IN JANUARY..

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 4 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD ANOTHER STRONG SIZE 2272 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 18.07 PTS OR 0.71% //Hang Sang CLOSED DOWN 368.96 POINTS OR 1.38% /The Nikkei closed HOLIDAY / Australia’s all ordinaires CLOSED DOWN 0.03%

/Chinese yuan (ONSHORE) closed DOWN at 6.7656 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.10 dollars per barrel for WTI and 59.91 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7656 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7683: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/USA

This is interesting: The Huawei executive arrested on espionage charges in Poland has been fired by the company as they supposedly had no knowledge of his criminal activity

( zerohedge)

II)CHINA //CANADA

iii)China, no doubt will be panicking as suddenly their capital outflows are soaring again. This will be good for gold(courtesy zerohedge)

iv)The following is huge news: Chinese giant Alibaba, the world’s largest retailer warns about slowing growth

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

Week NO 9: total turmoil as yellow vest battle riot police

( zerohedge)

ii)GERMANY

German business leaders blast Trump for Nordsteam 2 sanctions as they claim it is an attack on EU sovereignty. And yet the uSA pays for a much greater share of NATO and defense of Europe than Germany.

( zerohedge)

iii)The three nightmare scenarios facing Europeans:

- Brexit

- Macron and the yellow vests

- Theresa May’s election

all three areas going against the neo-cons..

( Tom Luongo)

iv)An excellent commentary from Claudio Grass as he explains the shockwaves from the Yellow vest movement; why it is occurring and why contagion is spreading to other parts of Europe

( Claudio Grass)

v)It is possible that on Tuesday’s vote, Theresa May could be removed as Corbyn is contemplating a non confidence vote

( zerohedge)

vi)Bill Blain explains the mess that the UK is in with respect to Brexit talks and the huge costs the country will endure if it leaves. It also will endure huge costs if it stays in the union

( Bill Blain)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

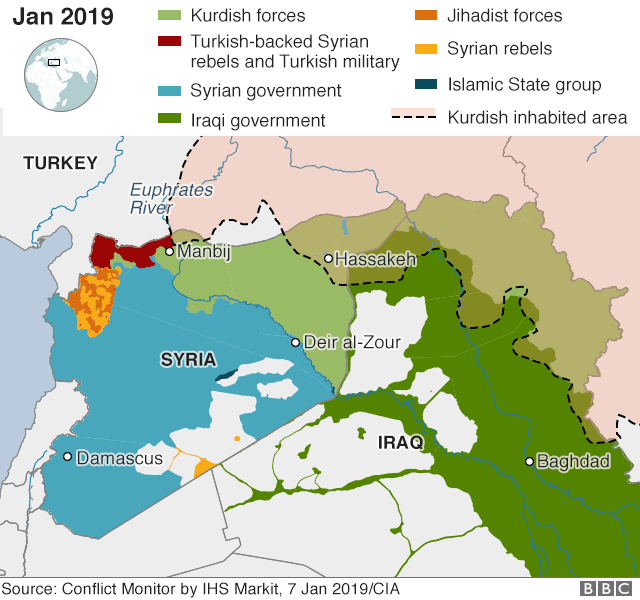

i)TURKEY/USA/SYRIA/KURDS

Trump threatens to devastate Turkey economically if the Kurds are attacked. This sends the lira sliding

( zerohedge)

ii)Turkey dismisses Trump’s threat to devastate the Turkish economy

(courtesy zerohedge)

iii)Iran

Today one of Iran’s military cargo planes crashes killing 15. Iran is desperate to obtain airplane spare parts as its passenger airline industry is in shambles.

zerohedge)

6. GLOBAL ISSUES

An excellent commentary from Tom Luongo on how the USA is losing influence around the globe

( Tom Luongo)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

Pompeo calls for regime change in Venezuela after the “illegitimate” Maduro re election

(courtesy zero hedge)

9. PHYSICAL MARKETS

Mathew Lynn describes how Europe is tanking as industrial production has hit Germany and other European nations pretty hard. Europe depends on exports to survive. Europe is following China on a huge nosedive economically

( Mathew Lynn/London Telegraph/GATA)

ii)The Tocqueville letter written by John Hathaway describes the explosion of USA debt and how that will foretell the dollar’s eventual devaluation against gold

iii)Dollars are scarce around the world as the uSA sucks up all dollars to pay for their 1 trillion deficit. Zimbabwe seeks a new currency to back their economy but cannot find one..maybe they can go back to using sea shells like they did in 600 BCE…( Bloomberg/GATA)

iv)The Bank of China will now executive payment in yuan on USA e commerce platforms. Another dagger into the heart of USA hegemony

( Reuters/GATA)

v)nobody believes that China only added 10 tonnes of gold to their official reserves. Ronan explains what is behind the low amount of official gold announced. Remember that China produces 432 tonnes of gold last year and sold none. This gold must be included into official reserves and yet it is not.

( Ronan Manly/GATA)

vi)Newmont Mining buys out the ailing Goldcorp in a 10 billion dollar deal. When you see gold deals like this and Barrick you know the end game is being played out.

(courtesy zerohedge)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)Brandon Smith is one smart cookie and he must be followed. He states quite categorically that the uSA will continue to raise interest rates and crash the system. The elites want a single global government and central bank and when this crashes, the iMF and the World Bank will come to the rescue of nations. Stock markets will fall especially around the middle of the month when the Fed cuts its balance sheet the most. Main street (as we have shown to you) has been collapsing since 2018..the stock market which is a lagging indicator will collapse this year.

a must read…

Brandon Smith

b)P G and E is reportedly planning to announce bankruptcy protection, this morning.

( zerohedge)

c)this is going to be very costly to Californians: P g and E shares crash by 50% as its CEO quits ahead of bankruptcy filing

( zerohedge)

d)Gundlach explains the real deficit of the uSA at 1.3 trillion. He also is sounding the alarm bell over the huge $122 trillion in unfunded liabilities. I think he is low on this front..others have pegged the unfunded liabilities in the uSA at over 225 trillion dollars

( zerohedge)

e)this should hurt the USA first quarter GDP: a massive winter buries the eastrn section of the uSA

( zerohedge)

f)In prepared remarks William Barr wants Mueller to finish his Russian probe and then have the public see that report

iv)SWAMP STORIES

a)Not really a surprise here: Trump goes on a tweetstorm after the New York Times reveals that the FBI went on an escalated witch hunt on Trump with respect to Russian collusion immediately after Comey was fired.

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 23 CONTRACTS DOWN TO 452. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 1109 CONTRACTS DOWN TO 142,992 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 4500.78 oz of gold was withdrawn from the customer account of Scotia

140 kilobars

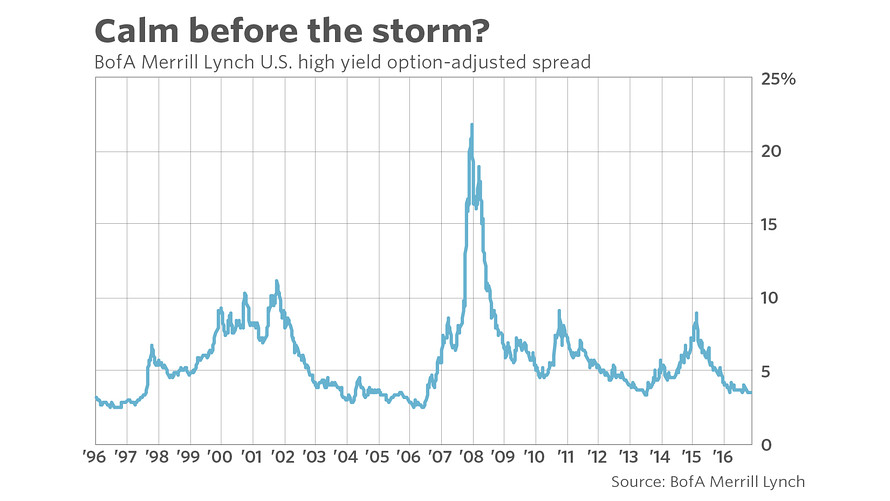

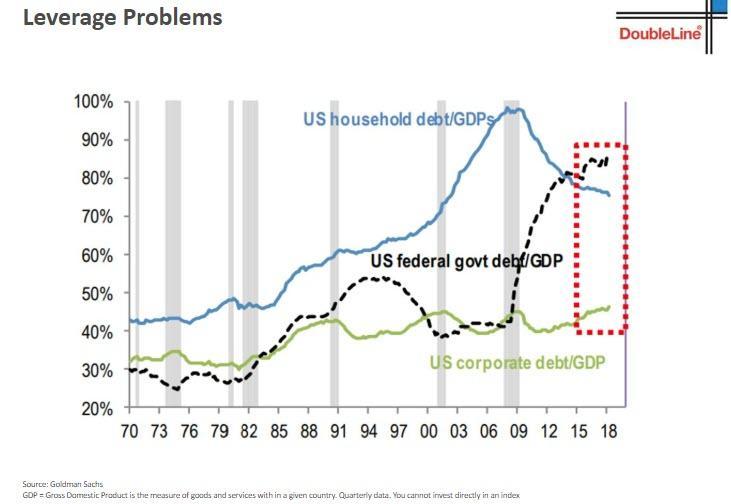

Where Will The “Pending” Financial Crisis Originate?

– Case for a pending financial collapse is well grounded warns Rickards

– “Ticking time bomb” the Federal Reserve has created is set to go off…

– Economist warns U.S. high-yield debt, default of “junk bonds” could cause next crisis

– Systemic risk is “more dangerous than ever” as “entire system is larger than before”

– Protect wealth by allocating at least 10% of assets in physical gold and silver

Source: BofA Merrill Lynch via Marketwatch.com

from The Daily Reckoning:

The case for a pending financial collapse is well grounded. Financial crises occur on a regular basis including 1987, 1994, 1998, 2000, 2007-08.

That averages out to about once every five years for the past thirty years. There has not been a financial crisis for ten years so the world is overdue. It’s also the case that each crisis is bigger than the one before and requires more intervention by the central banks.

The reason has to do with the system scale. In complex dynamic systems such as capital markets, risk is an exponential function of system scale. Increasing market scale correlates with exponentially larger market collapses.

This means a market panic far larger than the Panic of 2008.

Today, systemic risk is more dangerous than ever because the entire system is larger than before.

Due to central bank intervention, total global debt has increased by about $150 trillion over the past 15 years. Too-big-to-fail banks are bigger than ever, have a larger percentage of the total assets of the banking system and have much larger derivatives books.

Each credit and liquidity crisis starts out differently and ends up the same. Each crisis begins with distress in a particular overborrowed sector and then spreads from sector to sector until the whole world is screaming, “I want my money back!”

First, one asset class has a surprise drop. The leveraged investors sell the sinking asset, but soon the asset is unwanted by anyone. Margin calls roll in. Investors then sell good assets to raise cash to meet the margin calls. This spreads the panic to banks and dealers who were not originally involved with the weak asset.

Soon the contagion spreads to all banks and assets, as everyone wants their money back all at once. Banks begin to fail, panic spreads and finally central banks step in to separate winners and losers and re-liquefy the system for the benefit of the winners.

Typically, small investors (and some bankrupt banks) get hurt the worst while the big banks get bailed out and live to fight another day.

That much panics have in common. What varies in financial panics is not how they end but how they begin. The 1987 crash started with computerized trading. The 1994 panic began in Mexico. The 1997–98 panic started in Asian emerging markets but soon spread to Russia and the big banks. The 2000 crash began with dot-coms. The 2008 panic was triggered by defaults in subprime mortgages.

The problem is that regulators are like generals fighting the last war. In 2008, the global financial crisis started in the U.S. mortgage market and spread quickly to the overleveraged banking sector.

Since then, mortgage lending standards have been tightened considerably and bank capital requirements have been raised steeply. Banks and mortgage lenders may be safer today, but the system is not. Risk has simply shifted.

What will trigger the next panic?

Prominent economist Carmen Reinhart says the place to watch is U.S. high-yield debt, aka “junk bonds.”

I’ve also raised the same argument. We’re facing a devastating wave of junk bond defaults. The next financial collapse will quite possibly come from junk bonds.

Let’s unpack this…

Since the great financial crisis, extremely low interest rates allowed the total number of highly speculative corporate bonds, or “junk bonds,” to rise about 60% — a record high. Many businesses became extremely leveraged as a result. Estimates put the total amount of junk bonds outstanding at about $3.7 trillion.

The danger is that when the next downturn comes, many corporations will be unable to service their debt. Defaults will spread throughout the system like a deadly contagion, and the damage will be enormous.

This is from a report by Mariarosa Verde, Moody’s senior credit officer:

This extended period of benign credit conditions has helped many weak, highly leveraged companies to avoid default… A number of very weak issuers are living on borrowed time while benign conditions last… These companies are poised to default when credit conditions eventually become more difficult… The record number of highly leveraged companies has set the stage for a particularly large wave of defaults when the next period of broad economic stress eventually arrives.

If default rates are only 10% — a conservative assumption — this corporate debt fiasco will be at least six times larger than the subprime losses in 2007-08.

Many investors will be caught completely unprepared. Once the tsunami hits, no one will be spared. The stock market is going to collapse in the face of rising credit losses and tightening credit conditions.

But corporate debt is not the only dagger hanging over the economy. Credit conditions have already begun to affect the real economy. Student loan losses are also skyrocketing. Losses are also soaring on subprime auto loans, which has put a lid on new car sales. As these losses ripple through the economy, mortgages and credit cards will be the next to feel the pinch.

Have we already seen the beginning of the next crisis? No one knows for sure, but the time to prepare is now. Once the market falls apart, it’ll be too late to act.

That’s why the time to buy gold is now, while it’s cheap. When you need it most, once the crisis hits, it’ll cost a fortune.

Both the panics of 1998 and 2008 began over a year before they reached the level of an acute global liquidity crisis.

Investors has ample time to reduce risky positions, increase cash and gold allocations and move to the sidelines until the crisis abated. At that point there were bargains galore for those with cash.

An investor with cash in 2008 could have preserved wealth during the crisis and nearly quadrupled his money since then by buying the Dow Jones index at 6,550 (even with the recent turmoil, today it’s still around 23,600).

Relatively few investors did this. Instead they suffered from “fear of missing out” as markets rose until the panic began. They persisted in the mistaken belief that they could “get out in time” if markets reversed, not realizing that reversals happen much faster than rallies. They held onto losing positions hoping they would “come back” (they did after 10 years) and so on.

Simple behavioral biases stand in the way of doing the right thing almost every time.

For now, it’s not clear which way things will break next. Volatility is back and markets are still in a precarious position. Fed chairman Jay Powell threw markets a bone last Friday when he basically said all rate hikes are off until further notice and that he’s willing to scale back QT “if needed.” Markets have naturally rallied since Powell’s remarks.

If you still need proof that today’s rigged markets still require support from the Fed, here it is. But it’s far from clear the next crisis can be avoided at this point.

You don’t want to be heavily exposed to these markets. It’s far better to get out too early than too late. You should not be the last to be get ready. Start now to decrease equity allocations and increase your allocations to cash and gold so you can weather the coming storm.

Preparation means 10% percent of your investible assets in gold or silver and another 30% in cash.

That allocation will preserve wealth and provide dry powder for bottom-fishing in the crisis to come.

Regards,

Jim Rickards

The Daily Reckoning offers constant trends and research driven facts on markets and gold. Sign up for the Daily Reckoning e-letter here

News and Commentary

Stocks Fall, Bonds Climb as China Data Disappoints: Markets Wrap (Bloomberg.com)

May to Set Out EU Assurances to Try to Save Deal: Brexit Update (Bloomberg.com)

Gold prices edge higher on expectations of Fed pause (Reuters.com)

Gold Prices Aim Higher as Viacom Exits China, Souring Risk Appetite (DailyFX.com)

Goldman Predicts Gold Prices to Climb to Highest Since 2013 ($1,425 an ounce) (Bloomberg.com)

No Gold/Silver CoT Reports today due to U.S. Gov. Shutdown (GoldSeek.com)

4 Men Face Trial in Berlin for Giant Gold Coin Heist (Theepochtimes.com)

The Next Eurozone Crisis Has Already Started (Telegraph.co.uk)

The Next American Car Recession Has Already Started (Bloomberg.com)

Cars Have Just Been Crushed: The US Auto Market Is Officially In Recession Again (ZeroHedge.com)

Yellow Vests: Shockwaves Felt Around The Continent (ClaudioGrass.ch)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

11 Jan: USD 1,298.80, GBP 1,012.91 & EUR 1,123.96 per ounce

10 Jan: USD 1,292.40, GBP 1,012.98 & EUR 1,121.54 per ounce

09 Jan: USD 1,281.30, GBP 1,006.41 & EUR 1,118.32 per ounce

08 Jan: USD 1,291.90, GBP 1,006.71 & EUR 1,121.62 per ounce

07 Jan: USD 1,291.50, GBP 1,013.83 & EUR 1,129.03 per ounce

04 Jan: USD 1,290.35, GBP 1,016.80 & EUR 1,131.24 per ounce

Silver Prices (LBMA)

11 Jan: USD 15.68, GBP 12.23 & EUR 13.60 per ounce

10 Jan: USD 15.70, GBP 12.33 & EUR 13.63 per ounce

09 Jan: USD 15.62, GBP 12.27 & EUR 13.64 per ounce

08 Jan: USD 15.64, GBP 12.24 & EUR 13.64 per ounce

07 Jan: USD 15.75, GBP 12.35 & EUR 13.77 per ounce

04 Jan: USD 15.70, GBP 12.40 & EUR 13.76 per ounce

Recent Market Updates

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

– Prepare For Global Debt Bubble Collapse – Outlook 2019

– Happy Christmas From All The Team in GoldCore

– Gold Prices Likely To Go Higher In 2019 After 4% Gain In Q4 2018

* * *

GATA STORIES AS IT RELATES TO PHYSICAL GOLD/SILVER

A must read:

Mathew Lynn describes how Europe is tanking as industrial production has hit Germany and other European nations pretty hard. Europe depends on exports to survive. Europe is following China on a huge nosedive economically

(courtesy Mathew Lynn/London Telegraph/GATA)

Matthew Lynn: Next eurozone crisis has begun and will lead to more money creation

Submitted by cpowell on Fri, 2019-01-11 16:18. Section: Daily Dispatches

The Next Eurozone Crisis Has Already Started

By Matthew Lynn

The Telegraph, London

Friday, January 11, 2019

https://www.telegraph.co.uk/business/2019/01/11/next-eurozone-crisis-has…

Industrial output is in crashing. Retail sales have stagnated. Business confidence has dropped, and investment is heading south. A sharp slowdown might have been expected for Britain heading out of the European Union, America where the President is busily ripping up half a century worth of carefully constructed trade agreements, or China, which has been on a decade of wild, credit-fuelled growth. But the real slowdown is happening in the one place where few economists expected it. It is now painfully obvious that the eurozone is heading into a sharp recession.

…

The numbers coming out of all its main economies, from Germany to France, Italy and Spain, are relentlessly bad. What does that mean? Far from winding up quantitative easing, the European Central Bank will be forced to step in with emergency measures to rescue a failing economy — but it may well prove too little, too late .2018 was meant to be the year when the eurozone consolidated its steady recovery, agreed on reforms to fix the flaws in the single currency, pressed forward with reforms to boost its competitiveness, and gave the rest of the world a lesson in balanced, sustainable growth. Over the past year, a ton of investors’ money has bought into the Euro-boom story. Steady recovery would drive voters away from populist parties, encourage reform, and create a virtuous circle of expansion and renewal.

The script has not quite worked out as planned, however. Today brought yet another wave of disappointing numbers. Italian industrial production was down 2.6 percent year on year. In Spain, industrial output was also down 2.6 percent, the fastest rate of contraction since May 2013. The day before, we learned that French industrial output was down by 1.3 percent in November, and Germany, which is meant to be the main engine of the continent, recorded a decline 1.9 percent for the month, as well as re-calculating October’s data to show a steeper drop than reported earlier.

The eurozone is now seeing a synchronised slowdown right across all its major economies. Germany looks certain to be in technical recession, defined as two consecutive quarters of shrinking output, and France and Italy will not be far behind. Spain, which had been growing faster than most of the continent, is slowing and so will the smaller economies. Add all that up, and it clear the whole continent is heading into a fresh downturn, even though employment and output have yet to recover their 2008 levels.

Sure, there are some special factors to explain that. German industry has been hit by the slowdown of its massive auto industry, and especially the re-tooling of factories to meet new diesel and regulatory standards. In France, the Gilets Jaunes protestors haven’t exactly helped: riots and boarded up shops are not the kind of thing that encourages people to go out and spend money, even in a county that is used to protests. Italy is engulfed in a political fight with Brussels over its budget policies and is suffering a fresh round of banking problems. Arguably, once those are overcome, growth will get back to normal.

Well, perhaps. The trouble is, those sound suspiciously like excuses. In fact, every economy always faces a few challenges, and the eurozone’s are no worse than anyone else’s. Indeed, they look relatively mild compared to many of its competitors. The UK has to contend with the chaos of Brexit, and the United States with rising interest rates, and rising protectionism. Even so, both are now growing faster.

In fact, there are two big weaknesses. First, led by Germany, the whole of Europe has allowed itself to become dangerously dependent on exports. The German trade surplus at more than 8 percent of GDP leaves that country brutally exposed to the cross-winds of global trade.

But it not just Germany. In 2017, the surplus for the zone as a whole hit a massive E345 billion, up from E207 billion five years earlier. The whole continent is hooked on exports. Talk of trade wars, a slowdown in China, and a hit to the emerging markets all mean the European economy suffers first from any slowdown (Brexit is hardly helping either, with Germany’s surplus with the UK already narrowing and likely to fall further). An export-led model is great when the global economy is expanding – but can turn against you very quickly.

Next, the euro remains a relentlessly deflationary currency that has ripped demand out of whole economies. With weakened banking systems, towering imbalances between the core and the periphery, puny wage growth, relentless austerity, and mass unemployment, it has proved itself over two decades incapable of generating any meaningful internal demand. Most countries can reflate their economies with consumer spending, easier credit, and a cheaper currency. The euro-zone can’t do any of that.

The fleeting recovery of the 2017 and early 2018 now looks to have been fuelled purely by the two trillion of freshly minted euros the ECB threw at the economy. It has proved incapable of creating a self-sustaining recovery. Th ECB was expected to start normalising policy this year, ending QE and raising interest rates. In the face of the latest data, a rise in rates can now be ruled out. The central bank is far more likely to have to start printing money again by the spring — but by then it may already be too late to pull the zone out of a slump.

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Tocqueville gold letter: Explosion in U.S. debt foretells dollar’s devaluation against gold

Submitted by cpowell on Sat, 2019-01-12 15:49. Section: Daily Dispatches

10:48a ET Saturday, January 12, 2019

Dear Friend of GATA and Gold:

In the Tocqueville gold letter for January, fund manager John Hathaway argues that the explosion of U.S. government debt to banana republic levels foretells a big devaluation of the dollar against gold. (Just don’t ask him why it hasn’t happened already.)

The letter is headlined “Tocqueville Gold Strategy Fourth Quarter 2018 Investor Letter” and it’s posted at the Tocqueville internet site here:

http://tocqueville.com/tocqueville-gold-strategy-fourth-quarter-2018-inv…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

nobody believes that China only added 10 tonnes of gold to their official reserves. Ronan explains what is behind the low amount of official gold announced. Remember that China produces 432 tonnes of gold last year and sold none. This gold must be included into official reserves and yet it is not.

(courtesy Ronan Manly/GATA)

Ronan Manly: Separating truth from fiction in China’s golden game of poker

Submitted by cpowell on Sat, 2019-01-12 18:47. Section: Daily Dispatches

1:48p ET Saturday, January 12, 2019

Dear Friend of GATA and Gold:

Bullion Star gold market researcher Ronan Manly explains today why China’s recent announcement of a small increase in its gold reserves is unbelievably small and possibly just a warning shot toward the United States. Manly’s analysis is headlined “Separating Truth from Fiction in China’s Golden Game of Poker” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/separating-truth-from-fict…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Dollars are scarce around the world as the uSA sucks up all dollars to pay for their 1 trillion deficit. Zimbabwe seeks a new currency to back their economy but cannot find one..maybe they can go back to using sea shells like they did in 600 BCE…

(courtesy Bloomberg/GATA)

Sea shells? Oxen? Zimbabwe plans a new currency as dollar shortage bites

Submitted by cpowell on Sun, 2019-01-13 00:28. Section: Daily Dispatches

Another resource- and gold-rich country insisting on being poor.

* * *

By MacDonald Dzirutwe

Bloomberg News

Saturday, January 12, 2019

HARARE, Zimbabwe — Zimbabwe will introduce a new currency in the next 12 months, the country’s finance minister said, as a shortage of U.S. dollars plunges the financial system into disarray, forcing businesses to close and threatening unrest.

…

The southern African nation abandoned its own hyperinflation-wrecked currency in 2009 at the height of an economic recession, adopting the greenback and other currencies including sterling and the South African rand.

But without enough hard currency to back up the $10 billion of electronic funds trapped in local bank accounts, businesses and civil servants are demanding payment in cash which can be deposited and used to make payments both inside and outside the country. …

… For the remainder of the report:

https://af.reuters.com/article/commoditiesNews/idAFL8N1ZC056

* * *

END

The Bank of China will now executive payment in yuan on USA e commerce platforms. Another dagger into the heart of USA hegemony

(courtesy Reuters/GATA)

Bank of China to enable payment in yuan on U.S. e-commerce platforms

Submitted by cpowell on Sun, 2019-01-13 16:14. Section: Daily Dispatches

By Tom Daly

Reuters

Sunday, January 13, 2019

BEIJING — Bank of China’s New York branch will enable Chinese firms to receive payment in yuan rather than dollars from their sales on U.S. e-commerce platforms this year, the official Xinhua news agency reported today.

Pledging to introduce more services for small and medium-sized enterprises engaged in cross-border trade between the United States and China, executives from the branch said payment in yuan would be possible by tapping new functions of e-MPay, a cross-border payment system launched by the branch in 2016.

…

The branch is developing a system using an existing platform to “facilitate trade finance for e-commerce players,” said Xu Chen, president and chief executive officer of Bank of China USA, Xinhua reported, without providing further details. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-banking-usa/bank-of-china-to-en…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

-END-

Newmont Mining buys out the ailing Goldcorp in a 10 billion dollar deal. When you see gold deals like this and Barrick you know the end game is being played out.

(courtesy zerohedge)

Newmont Mining To Buy Goldcorp In $10 Billion Deal To Create World’s Largest Gold Miner

In the latest deal in what’s becoming a wave of consolidation among gold miners, Newmont Mining announced on Monday that it would buy smaller miner Gold Corp in a deal valued at $10 billion.

The deal could create the largest gold miner in the world, with operations stretching from the Americas, to Australia and Ghana, the companies said. Newmont will offer 0.3280 of its share and two cents for each share of its Canadian rival, according to CNBC. The deal is the largest in the space since Randgold and Barrick announced their plans to merge back in September.

As the Wall Street Journal pointed out, the depletion of global gold mines and the resulting increase in extraction costs has pushed gold miners to seek cost efficiencies and smaller-scale combinations.

“The strategic rationale for combining Goldcorp with Newmont is powerfully compelling on many levels.” Goldcorp Chief Executive Officer David Garofalo said in a statement. Goldcorp shares climbed 1.3% in premarket trading on the news. The GDX, an ETF of gold miners, also climbed on the news.

Russia Prepares To Buy Up To $10 Billion In Bitcoin To Evade US Sanctions

While the market has been increasingly focused on the rising headwinds in the global economy in general, and China’s economic slowdown in particular, while the media is obsessing over daily revelations that Trump may or may not have colluded with Russia to get elected, a far more critical, if underreported, shift has been taking place over the past year.

As we reported in June, whether due to concerns over draconian western sanctions and asset confiscations following the poisoning of former Russian military officer Sergei Skripal, or simply because it wanted to diversify away from the dollar, Russia liquidated virtually all of its Treasury holdings in the late spring and early summer, in the process sparking a major repricing of the 10Y US Treasury, whose yield jumped from 2.70% at the start of April to a high of 3.10% in May, a move which economists were struggling to explain at the time.

The obvious next question is what did Russia do with the proceeds, and it came as little surprise that, as we wrote back in July, as Russia was selling nearly $100BN worth of Treasurys, it was aggressively buying gold.

In addition to gold, the Kremlin also instructed the Russian finance ministry to load up on Yuan, something which we noted at the end of September, when we showed the surge in reserves allocated to the Chinese Yuan.

As part of its reallocation away from the dollar, Russia also bought a substantial amount of other non-USD currencies, and according to a recent report, the money pulled from the dollar reserves was redistributed to increase the share of the euro to 32%, the yuan to 14.7%, and another 14.7% of the portfolio was invested in other currencies, including the British pound (6.3%), Japanese yen (4.5%), as well as Canadian (2.3%) and Australian (1%) dollars.

And now, the final missing piece of Russia’s massive capital reallocation out of the petrodollars has emerged, after the Telegraph reported that Moscow is preparing an investment in Bitcoin in a bid to tackle US sanctions, according to a Russian economist with close ties to the Kremlin.

According to Vladislav Ginko, an economist at the state-funded Russian Presidential Academy of National Economy and Public Administration, the government is taking steps to minimize the impact of US sanctions that have hit the Russian rouble by replacing some of its US dollar reserves with the world’s most popular cryptocurrency.

Quoted by The Telegraph, Ginko said he believes Russia’s de-dollarization decision is fundamentally a move to “protect its national interests” due to a possible interruption of “US nominated payments flows for Russian oil and gas” and claims that the investment in bitcoin could be as much as $10bn (£7.8bn); a material enough amount to send the price of bitcoin sharply higher.

When would Russia’s next capital reallocation take place? According to the Russian economist, the purchases could start as soon as next month. Cryptocurrencies have seen a surge of interest in Russia, where President Putin has expressed an interest in the digital assets in recent months. Ginko believes Bitcoin and the wider cryptocurrency industry now account for 8% of Russia’s GDP, and investment to bolster the country’s reserves with Bitcoin could start as soon as February.

“[The] Russian government is about to make a step to start diversifying financial reserves into Bitcoin since Russia [is] forced by US sanctions to dump US Treasury bonds and [take] back US dollars,” Ginko said.

“These sanctions and the will to adopt modern financial technologies lead Russia to the way of investing its reserves into Bitcoin.”

While the Central Bank of Russia has yet to confirm or deny the report and has yet to publish official plans, it said in a statement to The Daily Telegraph that it “publishes information on the foreign assets management with a six-month lag”. As noted above, an asset reallocation would be expected by a country which has been aggressively de-dollarizing by boosting its holdings of the euro, Chinese renminbi and Japanese yen.

Speaking to The Telegraph, eToro senior market analyst Mati Greenspan said that there is “definitely an interest from the [Russian] government to do this”.

What is most surprising is the sheer size of Russia’s proposed reallocation: the alleged plan to invest in the digital asset would see the state acquire almost a sixth of the world’s Bitcoin float, though since the buy order would push the price and valuation sharply higher, that would reduce Russia’s purchasing power.

Furthermore, since the Russian government would be unable to open an account with an exchange to buy cryptocurrencies, any investment plans could involve the setup of an “intermediary cryptocurrency” that can then be exchanged for Bitcoin. The new cryptocurrency would have to be offered by a broker such as Sberbank, a state-owned bank, and would act as what’s known as a utility token.

“The proposal that I understand is on the desk of the finance minister at the moment is to create some sort of intermediary cryptocurrency,” Greenspan said.

Putin has been a fan of cryptos for years, after he personally met with Vitalik Buterin, the 24-year-old Russian founder of cryptocurrency Ethereum in 2017 to discuss possibilities in the sector, and has also met personally with the Ethereum head in recent months according to The Telegraph.

“We know that Vladimir Putin is a big advocate of blockchain technology,” said Greenspan.

“Obviously he doesn’t like the sanctions that have been placed on him and he’s already said that these types of sanctions are going to lead to de-dollarisation. This is more or less the direction the Russian government is going.”

News of the potential Russian reallocation provided a sharp boost in crypto prices this morning, which have resumed their drift in the past week after bitcoin once again dipped below $4000 with many experts, the same ones who never anticipated bitcoin could reach $20,000 in December 2017, predicting that the crypto space is doomed.

If Putin indeed plans on buying up nearly 20% of the outstanding bitcoin float, not only will reports of bitcoin’s imminent death prove to be greatly exaggerated, but should the market attempt to frontrun Russia and/or should the total float shrink dramatically, the third, and biggest cryptobubble yet is about to be unleashed, something which will likely be facilitated by Chinese capital outflows which as we reported earlier, appear to have returned, just as they did shortly before bitcoin exploded from $200 to $20,000.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7656/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7683 /shanghai bourse CLOSED DOWN 18.07 PTS OR 0.71%

HANG SANG CLOSED DOWN 368.96POINTS OR 1/38%

2. Nikkei closed

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 95.63/Euro FALLS TO 1.1458

3b Japan 10 year bond yield: FALLS TO. +.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.10 and Brent: 59.91

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.21%/Italian 10 yr bond yield UP to 2.88% /SPAIN 10 YR BOND YIELD DOWN TO 1.42%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.67: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.36

3k Gold at $1295.10 silver at:15.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 28/100 in roubles/dollar) 67.17

3m oil into the 51 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.11 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9825 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1257 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.21%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.68% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5147

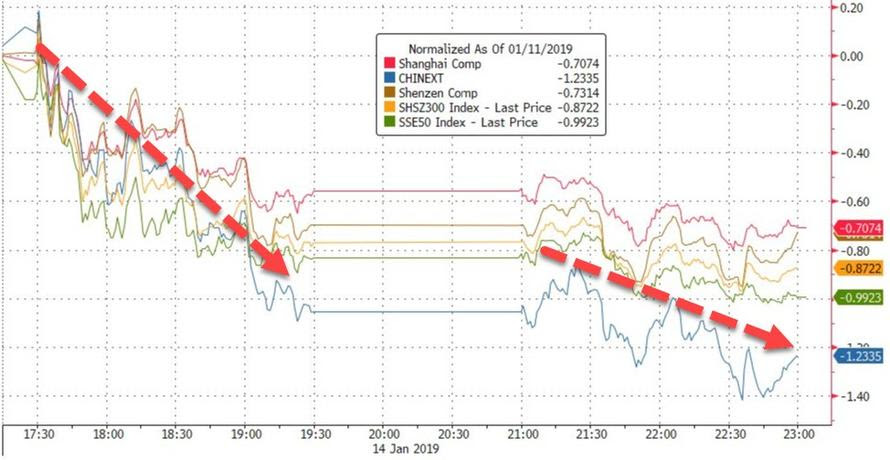

Futures Tumble Following Dismal Chinese Trade Data

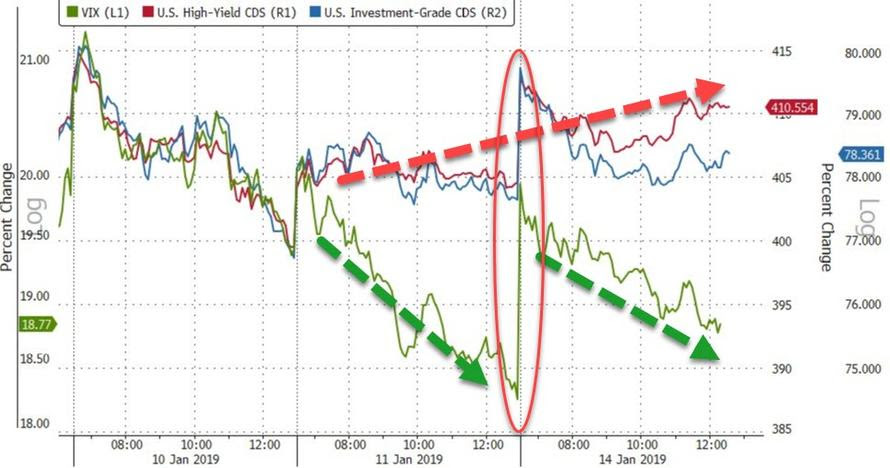

The torrid post-Christmas rally, which fizzled last Friday, appears to be officially dead just as earnings season begins, with futures sliding early in the session only seeing the drop accelerated after dismal trade data out of China reignited concerns about global growth and ahead of a key Brexit vote on Tuesday, leading to a sea of red in global markets with S&P futures down 1% to session lows around 6am ET, alongside sliding stocks in Europe and Asia. Treasury yields fell to 2.66% while the dollar held steady.

Tech stocks were the biggest losers in the Stoxx Europe 600 Index on renewed fears about a China hard-landing; in Asia, losses were most pronounced in Hong Kong after China posted the worst import and export figures since 2016. The index of Europe’s leading 300 shares slipped 0.7 percent in early trade to 1,365 points. Germany’s DAX and France’s CAC fell around 0.6 percent, with shares in European tech and luxury goods companies and the automotive sector suffering some of the biggest declines.

“We believe trade growth next year will slow significantly on huge uncertainty and high base,” Citi analysts wrote in a note, predicting China’s exports and imports to fall 5.1 percent and 6.8 percent respectively this year. “Significant uncertainty remains as to whether there could be a ‘deal’ after March 1,” they added.

The falls in Europe followed hefty declines in Asia where MSCI’s broadest index of Asia-Pacific ex-Japan shares lost around 1 percent from Friday’s 1-1/2 month high – its biggest single-day percentage drop since Jan. 2. Chinese and Hong Kong shares suffered the worst hits.

Early on Monday, China reported dismal trade data with exports unexpectedly falling the most since 2016 in December, while imports also contracted, pointing to further weakness in the world’s second-largest economy in 2019 and deteriorating global demand. Specifically, China December exports tumbled Fall -4.4% Y/y in Dollar Terms, the weakest year-on-year reading since January 2017, and down from +3.9% in November; far below the 2.0% consensus increase, while imports plunged -7.6% from +2.9% in Nov, badly missing the 4.5% expected increase, ironically resulting in the biggest trade surplus on record of $57.1BN. In month-on-month terms, the contraction of exports and imports accelerated further in December. In sequential terms, exports contracted 6.2% mom sa non-annualized, down further from a decrease of 3.4% in November

“Today’s data reflect an end to export front-loading and the start of payback effects, while the global slowdown could also weigh on China’s exports,” Nomura economists wrote in a note, referring to a surge in shipments to the U.S. over much of last year as companies rushed to beat further tariffs.

The large contraction in Chinese imports was broadly consistent with a significant decrease of exports in December from Korea and Taiwan to China. Exports growth has been weaker than expected over the past two months, and sequential momentum has slowed significantly to a contraction since November from a strong rebound in September, which has been probably due to the fading impact from front-loading ahead of 10% tariffs levied on $200bn Chinese goods starting in late September (and ahead of the potential—and so far delayed—increase of tariffs on these goods to 25%). According to Goldman, exports growth is likely to remain soft in the near future, given moderation in global growth momentum suggested by GS Leading Current Activity Indicator, even though a faster-than-expected waning of impact from front-loading could potentially pose less downward pressure for exports in the coming months. Adding to policymakers’ worries, data on Monday also showed China posted its biggest trade surplus with the United States on record in 2018, which could prompt President Donald Trump to turn up the heat on Beijing in their bitter trade dispute.

The dismal December trade readings suggest China’s economy may have cooled faster than expected late in the year, despite a slew of growth-boosting measures in recent months ranging from higher infrastructure spending to tax cuts. Some analysts had already speculated that Beijing may have to speed up and intensify its policy easing and stimulus measures this year after factory activity shrank in December.

Elsewhere, ahead of a critical Brexit vote on Tuesday, UK PM May warned that failure to back her Brexit deal risks a no-deal Brexit and is to say she believes parliament will more likely block Brexit than the UK leave without a deal, according to the PM’s office. In separate reports, the UK government commented that any defeat by less than 100 votes on Tuesday would be counted as a good result. Furthermore, reports in The Times noted that Brussels expects the UK to ask for an extension to Article 50 to allow Brexit to be delayed if the House of Commons rejects Theresa May’s deal tomorrow, while there were separate reports that Pro-EU MPs are said to publish draft legislation on Monday for a 2nd referendum.

All this adds to tensions as traders watch the record rally of the last two weeks finally collapse and as the banks are set to report earnings. As Bloomberg notes, this month’s buoyancy in global equities, triggered by signs of progress in U.S.-China trade talks and dovish commentary from Federal Reserve officials, faces a test with the Chinese data underscoring the impact of the trade spat. The next hurdles to clear will be a slew of U.S. bank profit reports and earnings season, amid worries global growth is slowing. Also weighing on sentiment is the partial U.S government shutdown that’s entered its fourth week.

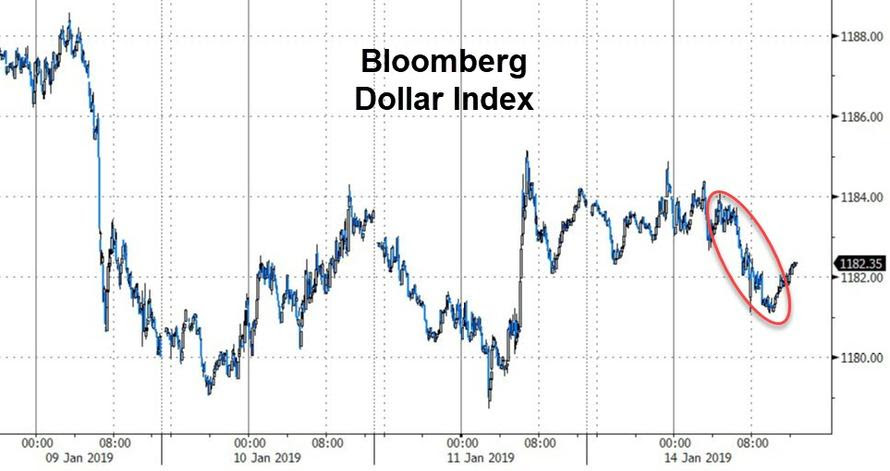

In FX, the Bloomberg Dollar Spot Index was little changed while the yen climbed as Chinese trade data and caution ahead of key earnings curbed risk appetite. The euro hit a session low after data showed euro-zone industrial production contracted 3.3% y/y in November, compared to an estimate of a 2.1% decline; Bunds gained, lagging Treasuries, while Italian bonds fell ahead of possible supply. Sweden’s krona recovered from an earlier decline after inflation data beat analyst estimates, while matching the central bank’s forecast. Finally, the Turkish lira slumped after Trump warned Turkey not to attack Kurdish forces in Syria after a planned U.S. pullout, saying it would be economically devastated if it did so.

The prospect of slowing global growth also roiled commodity markets, with oil prices slipping 1% after initially rising, and industrial metals copper and aluminum losing ground in both London and Shanghai. Meanwhile safe havens trades benefited from the equity pullback with U.S. 10-year Treasury yields falling to as low as 2.6690 percent – their lowest level in a week – while gold prices gained as Newmont announced it would buy Goldcorp to create the world’s largest gold miner.

In geopol news, President Trump tweeted that US is starting long overdue pullout from Syria, while he also threatened to devastate Turkey economically if Turkey hits the Kurds and likewise doesn’t want the Kurds to provoke Turkey. Iran suggested it could restart its nuclear program as its nuclear program chief stated that they have started preliminary activities for designing a modern process for 20% uranium enrichment for its reactor in Tehran. In separate news, US President Trump’s reportedly instructed the Pentagon last year to provide military options to strike Iran.

In other news, PG&E (PCG) said to be in discussions with banks about multi-billion dollar bankruptcy financing and may inform employees on Monday it is preparing a bankruptcy filing for January 29th.; the Co’s CEO Williams is leaving with general council John Simon to takeover in the interim. Company shares are down 50% pre-market.

For the U.S. trading day ahead, banks will be in sharp focus as they kick off the earnings season. Quarterly results from Citigroup are due on Monday followed by JPMorgan Chase, Wells Fargo, Goldman Sachs and Morgan Stanley later in the week. Expectations are dour with profits for U.S. companies forecast to rise 6.4 percent, down from an Oct. 1 estimate of 10.2 percent and a big drop from 2018’s tax cut-fueled gain of more than 20 percent. Investor attention was also on the U.S. government shutdown, now in its 24th day, and with no resolution in sight.

Market Snapshot

- S&P 500 futures down 1% to 2,569.00

- STOXX Europe 600 down 0.5% to 347.32

- MXAP down 0.4% to 150.88

- MXAPJ down 0.9% to 486.56

- Nikkei up 1% to 20,359.70

- Topix up 0.5% to 1,529.73

- Hang Seng Index down 1.4% to 26,298.33

- Shanghai Composite down 0.7% to 2,535.77

- Sensex down 0.4% to 35,862.08

- Australia S&P/ASX 200 down 0.02% to 5,773.37

- Kospi down 0.5% to 2,064.52

- German 10Y yield fell 1.9 bps to 0.22%

- Euro up 0.02% to $1.1471

- Italian 10Y yield fell 3.5 bps to 2.493%

- Spanish 10Y yield fell 1.2 bps to 1.433%

- Brent futures down 1.8% to $59.40/bbl

- Gold spot up 0.3% to $1,294.05

- U.S. Dollar Index little changed at 95.67

Top Overnight News from Bloomberg

- Trump’s refusal to reopen the U.S. government reflects the growing influence of his acting Chief of Staff Mick Mulvaney and senior adviser Stephen Miller, hard-right conservatives who are closer to the president thanks to turnover within the White House

- With Washington mired in gridlock and markets flashing all sorts of warning signs, the majority of Americans expects 2019 to be a grim one for their finances, according to a new study

- Industrial output in the euro area fell the most in almost three years in November, raising questions over the economy’s ability to regain momentum after a broad-based slowdown

- Greek Prime Minister Alexis Tsipras’s political future is on the line this week after a coalition breakdown prompted him to call a confidence vote in parliament set for Wednesday, raising the risk of an early election

- Italy’s economy is probably in a phase of stagnation not recession, Finance Minister Giovanni Tria said in a newspaper interview, adding that the country’s deficit will be kept under control

- Germany should try to head off an economic slowdown by easing the tax burden on companies, according to the new chairwoman of Chancellor Angela Merkel’s Christian Democrats

Asian equity markets began the week subdued following the indecisive close on Wall St last Friday as the US government shutdown extended to its longest in history, while disappointing Chinese trade data and the absence of Japanese participants for Coming of Age Day also contributed to the downbeat sentiment. ASX 200 (Unch.) failed to hold on to early gains as strength in Telecoms and its largest weighted Financials sector was eventually overwhelmed by losses in the broader market, while KOSPI (-0.5%) was lacklustre amid softness in the index heavyweights including Samsung Electronics and Hyundai Motor. Hang Seng (-1.4%) and Shanghai Comp. (-0.7%) were also pressured as Chinese Exports and Imports figures took a further hit from the US-China trade dispute, although losses in the mainland were capped after the PBoC injected liquidity to the interbank market in which it utilized 28-day reverse repos for the first time since June last year. PBoC injected CNY 80bln via 7-day and CNY 20bln in 28-day reverse repos for a net daily injection of CNY 20bln. PBoC set CNY mid-point at 6.7560 (Prev. 6.7909).

Top Asian News

- China Doubles Foreign Investment Limit in Further Opening

- CapitaLand CEO Puts Stamp on Developer With $4.4 Billion Deal

- Etihad Agrees to Raise Stake in India’s Jet to 49%, Report Says

- Jet Airways Jumps on Report Founder Goyal Is Giving Up Control

- China Is Said to Extend Foreign Bond Quota for 28 More Firms

Major European Indices are in the red [Euro Stoxx 50 -1.0%], with some underperformance seen in the SMI (-1.1%) weighed on by poor performance in luxury names such as Richemont (-2.1%) and Swatch (-1.0%) following poor Chinese trade data. Other luxury names including Pandora (-6.5%), and LVMH (-3.5%) are in the red on the back of this as well; Burberry (+0.3%) is bucking the luxury trend after being upgraded at Bank of America Merrill Lynch. Sectors are similarly in the red with some slight outperformance seen in healthcare. Other notable movers include Next (-2.9%) in the red after being downgraded at Credit Suisse, and Dialog Semiconductor (+4.3%) after reporting a 7% Y/Y increase in full year revenue.

Top European News

- Orsted Shares Slump Most Since July as Asset Sale Scuppered

- Telecom Italia Is Said to Bid for BT’s Scandal-Plagued Business

- Monte Paschi Drops After ECB Says It Has Capital, Profit Issues

- Euro-Area Production Slump Adds to Gloom for Economic Outlook

- Continental AG Issues Gloomy Auto Market Forecast for First Half

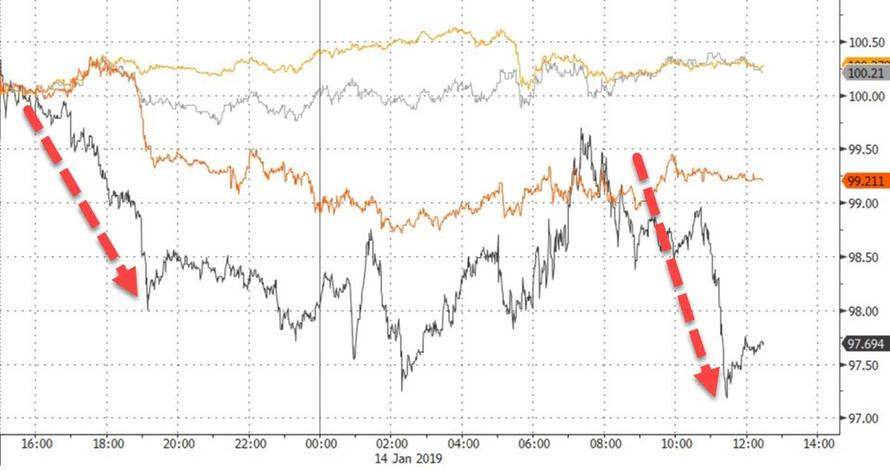

In FX, it has been a relatively docile session for the USD thus far as the index sits around the middle of tight 95.527-726 range as the US government shutdown extends to the longest in history. Subsequently, the US data originally scheduled for release today (building permits, advanced goods trade balance and durable goods) have been cancelled.

- AUD/NZD/CNY/JPY – The major G10 movers, all in the aftermath of below-forecast Chinese trade data as exports and imports both declined to a 6-month low in USD terms vs. expected rises. As such trade-proxy AUD/USD fell around 0.4% to test its 100 DMA at around 0.7180 while NZD/USD declined 0.3% to test its 200 DMA at around 0.6797, ahead of its 50 DMA at 0.6789 as the technicals are still poised to form a golden cross. Meanwhile, global-growth fears sparked safe-haven demand into the Yen as USD/JPY tested 108.00 to the downside ahead of a Fib level at 107.91, of note 1.1bln in option expiries sit between 108.00-15. Finally, the Yuan snapped a three-day winning streak but remains sub-6.80 vs. the greenback, though the currency is of course dampened by the disappointing trade figures, USD/CNY is capped by a firmer PBoC CNY fix of 6.7560 (Prev. 6.7909). In terms of techincals, USD/CNH breached its 50 HMA to the upside at 6.7692 with the 100 HMA above the 6.8000 level. It is also worth noting that Goldman Sachs raised their 3, 6, 12 month USD/CNH forecast to 6.80 (Prev. 6.95), 6.80 (Prev. 7.10) and 6.70 (Prev. 6.90) respectively citing an improvement in sentiment around US-Sino trade talks.

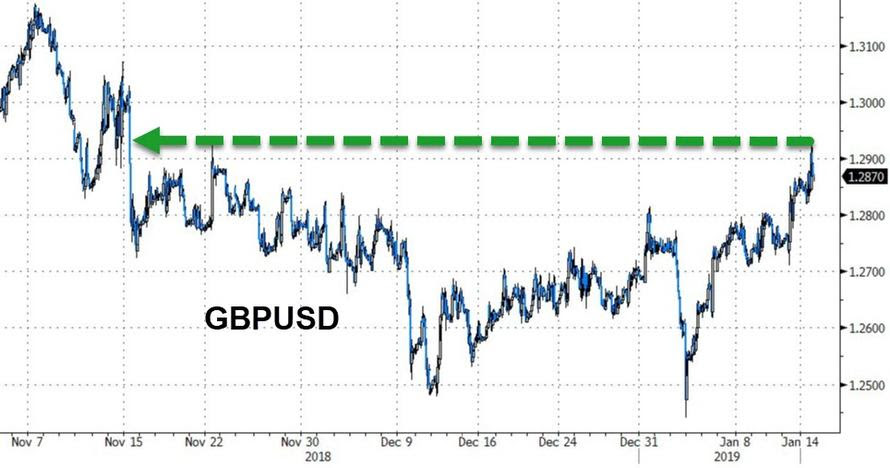

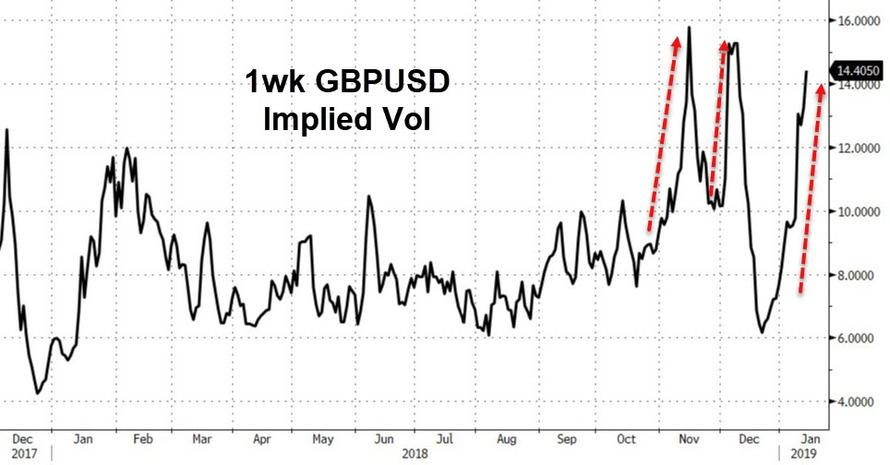

- GBP, EUR – Both little changed on the day, while the latter is largely fluctuating with the dollar and the Pound awaits tomorrows meaningful vote, which was originally scheduled for December 11th last year. The deal is widely expected to be voted down and BBC reports that around 100 Tory and the 10 DUP MPs are expected to join the Labour and the opposition parties in voting against the deal. In terms of where we stand with Brexit, PM May is to deliver a speech at 15:30 GMT where she will warn that Parliament is more likely to block Brexit rather than let Britain leave without a deal. Furthermore, the assurances provided by Brussels are also understood to not be enough to sway MPs towards PM May’s deal scheduled for 19:00GMT tomorrow. Cable was largely unfazed by the release of the EU assurances which offered little in the way of legally-binding material MPs sough for. From a technical standpoint, Cable recently saw a pop higher and rests just below its 100 DMA at 1.2893 with no notable option expiries for the day. Going back to the EUR, the currency was relatively unmoved by below-forecast industrial production figures following Germany’s dismal IP release last week. EUR/USD is currently below its 100 DMA at 1.1476 and in close proximity to the psychological (and 200 HMA) at 1.1450, while there is nothing notable to report regarding option expiries.

- TRY – The stand-out EM underperformer as USD/TRY reclaimed 5.50 to the upside amid a tweet by US President Trump over the weekend where he threatened to devastate Turkey if Turkey hits the Kurds, subsequently pouring cold water over what seemed like a fruitful relationship between the countries.

In commodities, Brent (-1.4%) and WTI (-1.6%) prices are in the red, just below USD 60.00/bbl and USD 51.00/bbl respectively, as the risk tone stemming from the ongoing US government shutdown and disappointing Chinese trade data weighs on markets. Regarding China, December oil imports of 10.35mln BPD, down from November’s figure but up from the 7.97mln BPD for December 2017. Separately, Saudi Energy Minister Al Falih stated that in his opinion OPEC+ has taken enough action to balance the oil market this year, and that there is no need for an extraordinary OPEC meeting before April. Gold (+0.4%) is in the green, towards the sessions high of USD 1294.57/oz as the aforementioned risk tone weighs on markets. Elsewhere, China’s 2018 iron ore imports fell -1% Y/Y, the first yearly decline since 2010. In contrast China’s 2018 copper imports increased 12.9% to a record high of 5.3mln tonnes.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

For those disappointed with the news on Friday that Mr Trump has cancelled his trip to the World Economic Forum in Davos next week, then fear not. I’ll be making my debut at the event and will be presenting at two Deutsche Bank hosted events. If you or anyone you work with are attending and would like to come along please let me know and I’ll let you know how to register. I’m hoping Bono finds time away from fixing the world’s problems to attend one of my sessions. Failing that I’d be happy to discuss my views on the yield curve with Angelina Jolie.

That’s for next week. For this it’s all about the Brexit vote, what happens next, and the start of US earnings season. Before we preview this, today marks the 24th day of the US government shutdown eclipsing the previous longest ever (21 days) seen in 1995-96. For markets the main inconvenience so far is the delay in some data releases. This Wednesday’s US retail sales release is the highest profile casualty to date data wise. Our economists highlighted that the 2013 shutdown was calculated to have cost about 0.1% of GDP per week lost. However at 850k furloughed workers, the shutdown over 5 years ago led to double the temporary losses of jobs than the current impasse has created. So the overall economic impact should be minimal for now even if it is distressing for those directly impacted. However the longer it goes on the more the lack of visibility on data will be a problem and the more it will start to make a meaningful impact on the immediate economic outlook. We’re not there yet but we’re also not seemingly near a solution.

Outside of US politics the main story this week will be Brexit. The Withdrawal Agreement vote takes place tomorrow evening but The Times on Saturday suggested that if an earlier amendment (the amendments get voted on first) is passed that rejects the deal but also rejects a no-deal then it’s still possible the vote won’t take place and the government will admit defeat but avoid the actual process. Regardless of what happens it seems possible that the deal won’t pass and we could get a constitutional head scratcher of a week. The opposition Labour Party will likely call a no-confidence motion that they have very little chance of winning but more importantly the weekend press (Bloomberg) is increasingly suggesting that Parliament will try to wrestle control of Brexit from Mrs May after Tuesday. Meanwhile, in a last ditch effort PM May is going to make a speech today appealing to members of Parliament to vote for her deal and at the same time warning them that there’s now more chance of them blocking Brexit than of Britain leaving the European Union without a deal.

Overnight the Guardian has reported that the EU27 is considering extending the Article 50 deadline until July should the UK request it assuming Mrs May loses tomorrow. To extend beyond the Euro Parliamentary elections would show the EU are keen to avoid a no-deal. If true one could argue that we’ll now increasingly likely to get a rolling extension until we get a deal, the U.K. decides to stay in, or there is a Parliamentary majority for a no-deal exit (highly unlikely). This news if verified would ultimately reduce the pathways to a hard, cliff edge Brexit.