GOLD: $1283.25 DOWN $9.65 (COMEX TO COMEX CLOSINGS)

Silver: $15.38 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1281.50

silver: $15.34

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.003 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 539 NOTICES FOR 53900 OZ (1.6858 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

23 NOTICE(S) FILED TODAY FOR 115,000 OZ/

total number of notices filed so far this month: 791 for 3,995,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3591: DOWN 26

Bitcoin: FINAL EVENING TRADE: $3597 DOWN $16

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 1/1

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,291.000000000 USD

INTENT DATE: 01/17/2019 DELIVERY DATE: 01/22/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

737 C ADVANTAGE 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 542

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN SMALL SIZED 315 CONTRACTS FROM 192,911 UP TO 193,226 DESPITE YESTERDAY’S 9 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1215 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1215 CONTRACTS. WITH THE TRANSFER OF 1215 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1215 EFP CONTRACTS TRANSLATES INTO 6.075 MILLION OZ ACCOMPANYING:

1.THE 9 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.725 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 30,189 CONTRACTS (FOR 13 TRADING DAYS TOTAL 30,189 CONTRACTS) OR 150.945 MILLION OZ: (AVERAGE PER DAY: 2322 CONTRACTS OR 11.611 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 150.945 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.55% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 150.945 MILLION OZ.

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 315 DESPITE THE 9 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 315 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1530 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1215 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 315 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 9 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.51 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 23 NOTICE(S) FOR 115,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.725 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 8884 CONTRACTS UP TO 510,097 DESPITE THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $1.10//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3423 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 3423 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 510,097. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,307 CONTRACTS:98884 OI CONTRACTS INCREASED AT THE COMEX AND 3423 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 12,307 CONTRACTS OR 1,230,700 OZ = 39.27 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.10???

YESTERDAY, WE HAD 7276 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 101,629 CONTRACTS OR 10,162,900 OZ OR 316.11 TONNES (13 TRADING DAYS AND THUS AVERAGING: 7817 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 316.11 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 316.11/2550 x 100% TONNES = 12.39% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 316.11 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 8884 DESPITE THE LOSS IN PRICING ($1.10) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3423 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3423 EFP CONTRACTS ISSUED, WE HAD ANOTHER GOOD GAIN OF 12,307 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3423 CONTRACTS MOVE TO LONDON AND 8884 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 38.27 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $1.10 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 5TH STRAIGHT DAY THAT WE RECORDED STRONG RISES IN OI ON BOTH EXCHANGES!

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $9.65 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 13 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY/

/INVENTORY RESTS AT 307.110 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 315 CONTRACTS from 192,911 UP TO 193,226 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1215 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1215 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 315 CONTRACTS TO THE 1215 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1530 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.65 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.725 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING FALL THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1215 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 36.37 PTS OR 1.42% //Hang Sang CLOSED UP 335.18 POINTS OR 1.25% /The Nikkei closed UP 263.80 PTS OR 1.29%/ Australia’s all ordinaires CLOSED UP 0.53%

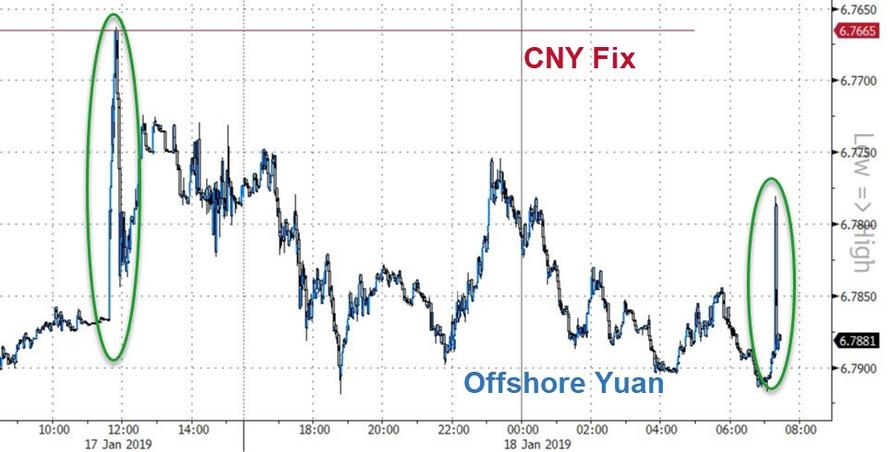

/Chinese yuan (ONSHORE) closed DOWN at 6.7787 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.59 dollars per barrel for WTI and 61.74 for Brent. Stocks in Europe OPENED /GREEN

//. ONSHORE YUAN CLOSED DOWN AT 6.7787 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7874: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA/Sweden

North Korea and the USA hold secret talks in Stockholm It seems that North Korea really wants to dispose of its nuclear arsenal

(courtesy zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA

After seeing flash crashes in two of China’s major real estate developers, we are witnessing property developers implode as the market is freaking out over 55 billion dollars worth of debt coming due in 2019

( zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE/UK

Odey, a BREXIT supporter warns that if Great Britain does not leave the EU, a “revolution” will begin

( zerohedge)

ii)FRANCE

LePen is now moving closer to the centre as she states that leaving the Euro is “no longer a priority” .

A leopard cannot change it’s spots

(courtesy zerohedge)

iii)GERMANY/HUAWEI (CHINA)

This is not good for China as now powerhouse Germany is exploring a ban on Hauwei products.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

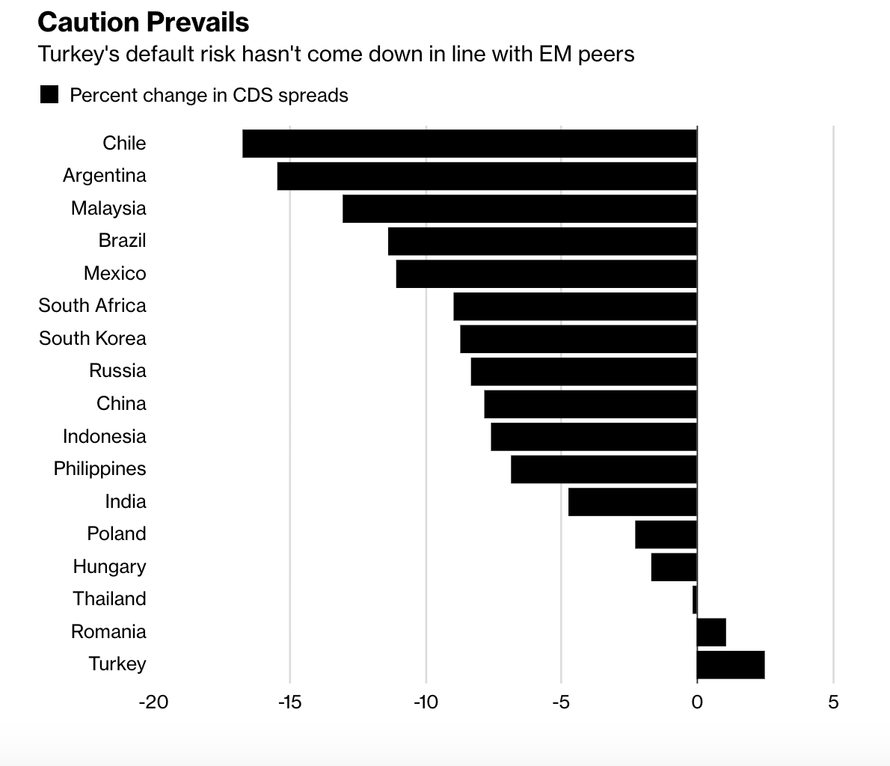

TURKEY

This should shake up some central bankers: The Turkish parliament is now set to grant Erdogan emergency powers to combat “”economic disaster” Despite the fact that a family member is head of its central bank, he wants complete control.

( zerohedge)

6. GLOBAL ISSUES

MALAYSIA/GOLDMAN SACHS

Malaysia tells Goldman Sachs that if they repay the loss in the 1MDB scandal of $7.5 billion, it may drop criminal charges against the bank

( zerohedge)

7. OIL ISSUES

i)Very popular Art Berman discusses the false accounting of shale oil The reserves are at best 60% of what the owners believe they have

( Art Berman/PeakProsperity.com)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)No doubt phony numbers coming from the uSA: after terrible numbers for the past 3 months, we witness a 1.1% surge in manufacturing output..the most in almost a year…go figure..

(courtesy zerohedge)

a)Trumps’s new plan is for missile interceptors, sensors and radars to shield every city in the USA

( zero hedge)

b)More evidence that the economy turned south: Greenwich homes plunge 17% as they piggyback on weakness from Manhattan

iv)SWAMP STORIES

a) Not good: Trump supposedly instructs Michael Cohen to lie to congress about the Moscow project according to BuzzFeed.

(courtesy zerohedge)

a ii) Skeptics shred the buzzfeed article above as nonsense: has not seen any evidence

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 5 CONTRACTS DOWN TO 454. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 63 CONTRACTS UP TO 144,596 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 2089.75 oz

65 KILOBARS

i) Into Brinks: 1226,386.600 0z

Three Reasons Gold May Embark On An Extended Rally

– History may repeat itself for gold demand and prices as world economy looks set to slow

– Three reasons for gold’s extended rally from 2008 to 2011 may be making a comeback

– As global growth looks to be slowing, hopes grow for repeat of 2008-11 rally that saw gold almost triple in value

by Clyde Russell of Thomson Reuters

The three legs that supported gold’s extended rally from just after the 2008 global recession until the all-time peak in 2011 may be making something of a comeback this year.

Gold in USD 10 Years – GoldCore.com

This is sparking hopes that the precious metal may finally break out of a fairly narrow five-year range, although it’s still far from certain that the dynamics for a sustained rally are entrenched.

The 2008-11 rally that saw spot gold almost triple in value to reach a record of $1,920.30 an ounce was built on three pillars, namely strong physical demand from top buyers China and India, robust central bank purchases, and appetite for a safe haven investment amid the fallout from the global recession.

Watch Our Latest Video Updates On YouTube Here

News and Commentary

McEwen Says Gold Market Confidence Is Coming Back (Bloomberg.com)

Sam Zell Says Gold ‘Is a Good Hedge’ (Bloomberg.com)

Palladium holds near record levels on supply woes; gold steady (Reuters.com)

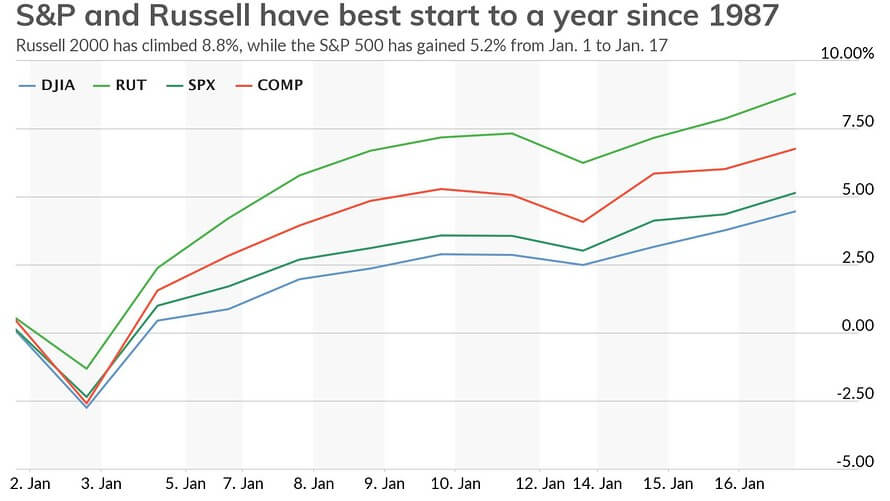

The stock market hasn’t started a year this strongly since 1987 — uh-oh! (MarketWatch.com)

Palladium Reaches Another Record as JPMorgan Sees More Upside (Bloomberg.com)

Image Credit: Dow Jones Market Data

Silver: Back In Focus (SilverSeek.com)

U.S. Government Debt Bomb Much Higher Than Americans Realize (24HGold.com)

J.P. Koning: How California stayed with gold when the rest of the U.S. adopted fiat money (Gata.org)

Eleven Economic Reports Delayed Due to Gov’t Shutdown: Do We Even Need Them? (24HGold.com)

Top Ten Trends Lead to Gold (24HGold.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

Gold Prices (LBMA PM)

17 Jan: USD 1,294.00, GBP 1,004.92 & EUR 1,135.87 per ounce

16 Jan: USD 1,290.50, GBP 1,002.46 & EUR 1,130.99 per ounce

15 Jan: USD 1,289.35, GBP 1,002.99 & EUR 1,127.67 per ounce

14 Jan: USD 1,293.70, GBP 1,007.02 & EUR 1,129.27 per ounce

11 Jan: USD 1,298.80, GBP 1,012.91 & EUR 1,123.96 per ounce

10 Jan: USD 1,292.40, GBP 1,012.98 & EUR 1,121.54 per ounce

09 Jan: USD 1,281.30, GBP 1,006.41 & EUR 1,118.32 per ounce

Silver Prices (LBMA)

17 Jan: USD 15.57, GBP 12.08 & EUR 13.66 per ounce

16 Jan: USD 15.54, GBP 12.09 & EUR 13.66 per ounce

15 Jan: USD 15.60, GBP 12.13 & EUR 13.65 per ounce

14 Jan: USD 15.61, GBP 12.13 & EUR 13.61 per ounce

11 Jan: USD 15.68, GBP 12.23 & EUR 13.60 per ounce

10 Jan: USD 15.70, GBP 12.33 & EUR 13.63 per ounce

09 Jan: USD 15.62, GBP 12.27 & EUR 13.64 per ounce

Recent Market Updates

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

end

–

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7787/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7874 /shanghai bourse CLOSED UP 36.37 PTS OR 1.42%

HANG SANG CLOSED UP 335.18 POINTS OR 1.25%

2. Nikkei closed UP 263.80 POINTS OR 1.29%

3. Europe stocks OPENED ALL GREEN

/USA dollar index FALLS TO 96.04/Euro RISES TO 1.1406

3b Japan 10 year bond yield: RISES TO. +.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.40/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.59 and Brent: 61.74

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.26%/Italian 10 yr bond yield DOWN to 2.72% /SPAIN 10 YR BOND YIELD DOWN TO 1.35%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.46: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.19

3k Gold at $1282.10 silver at:15.42 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 9/100 in roubles/dollar) 66.36

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.40 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9935 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1322 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.76% early this morning. Thirty year rate at 3.09%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3584

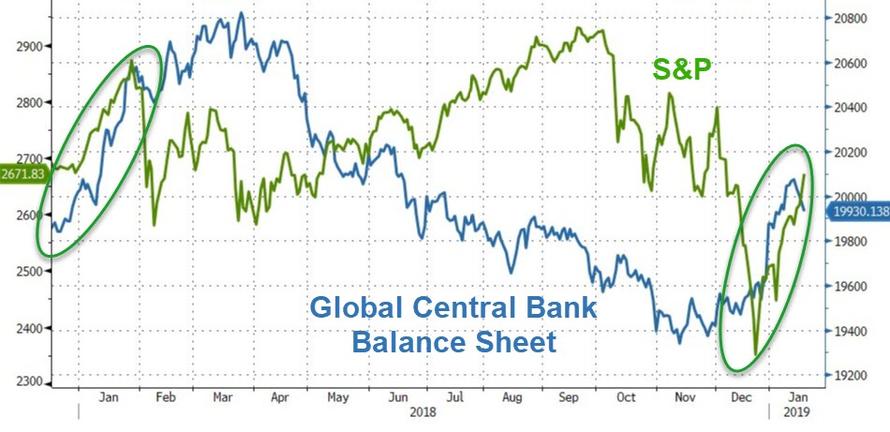

Futures, Global Markets Surge On Renewed China Stimulus And Trade Optimism

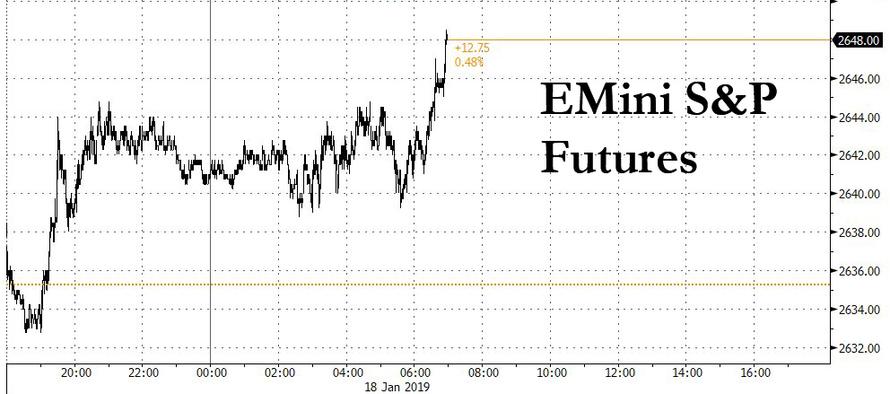

The “Mnuchin Plunge Protection Team/Government Shutdown” rally extended overnight, and is now more than 13% from the Dec 24 lows with US equity futures and European stocks rising following a strong Asian session following a since-denied WSJ report that the US is considering easing Chinese tariffs to boost the market, followed by a report that China has told local governments to push consumption of cars and home appliances. The result is a sea of green in global markets, which look set to close the week at one month highs, while safe haven assets continued to decline with Treasuries, the yen and gold all edging lower.

As a result of resurgent trade dispute optimism coupled with ongoing rumors of further stimulus from China, a Fed which has removed the threat of further rate hikes and an ok earnings season so far, global stocks rose to their highest in more than a month on Friday.

European stocks rose to the highest since early December, carrying over the trade optimism from the Asian session where major equity indices posted >1% gains after the WSJ reported that the US was considering lifting China import tariffs, and even though the Treasury promptly rejected the report, the story reinforced speculation the administration is more eager for a deal and helped upward momentum now that the 50DMA resistance has been breached in the S&P500.

“The story was probably not as interesting as the headlines suggested, as the story states that the proposal comes from Treasury Secretary Steven Mnuchin (a China dove), while the US Trade Representative Robert Lighthizer (China hawk) opposes the idea,” strategists at Danske Bank wrote in a note to clients. “Nonetheless, we still interpret the story as another sign that a US-China trade deal is moving closer and markets probably do as well.”

Europe’s Stoxx50 rose 1.4%, crossing above the 50DMA for the first time since September, with banks enjoying the largest gains (+1.8%), recovering Thursday’s losses to resume the week’s rally, while Autos also rallied (+1.5%) supported by reports that China told local governments should boost policy support for consumption of home appliances and cars, according to a statement from the National Development and Reform Commission.

China’s ministries called for boosting consumption in rural areas, including raising the quality of products consumed, and called for an increase in marketing of high- quality industrial products to rural areas. In short, China is telegraphing that consumption is to play a bigger role in dealing with downward economic pressures, although it is unclear just how this is possible when consumer debt in China has exploded in recent years, especially mortgage loans and credit card debt.

News of additional Chinese stimulus helped lift the MSCI index of Asia-Pacific shares ex Japan by 0.55%; the index has gained 1.3 percent this week, while the Shanghai Composite was up 1 percent. Australian stocks rose 0.5%, South Korea’s KOSPI advanced 0.6 percent and Japan’s Nikkei gained more than 1 percent to a one-month high.

The gains across regions helped lift the MSCI All-Country World Index to its highest since early December. The index was set for its fourth straight weekly gain, its longest weekly winning streak in six months, a furious rally that started the day after the US government was shut down, when Steven Mnuchin summoned the Plunge Protection Team, and as president Trump said “I think it’s a tremendous opportunity to buy. Really a great opportunity to buy.” So far he has been right.

In the US, S&P futures traded at session highs , up 0.5% following the S&P 500 cash Index’s first close above its 50-day average since early December. The yen fell for a fourth day and oil extended a third week of gains toward $53 a barrel in New York

The bid for risk assets weighed on long dated bond maturities as curves bear steepened and swap spreads tighten. 10Y TSY yields rose to session highs of 2.77% the highest level in three weeks, while long-end Gilts underperformed with yields rising ~3.5bps before stalling. Peripheral bonds continue to trade well, led by BTPs which pare some of the early ~8bp tightening to Germany.

In FX trading, DXY trades to the lower end of a tight range, EURUSD reclaims 1.14, GBP backs away from 1.3000. The dollar was supported after U.S. Treasury yields rose amid improved risk appetite. The dollar was set for its first weekly rise in five. The euro rose to $1.1398 after dipping overnight. It was on track for a weekly loss of 0.7 percent. The pound was 0.3 percent lower at $1.2950 after climbing to a two-month peak of $1.3001 on hopes that Britain can avoid a no-deal Brexit.

As Bloomberg notes, stocks and junk bonds are heading into the weekend with momentum after investors got some relief over concerns about the growth and rates outlook from U.S. economic data and central bankers. Chicago Fed President Charles Evans said the American economy is doing well, allowing that “we can easily be patient” in deciding on further interest-rate increases. Global stocks powered toward their fourth weekly gain.

“We think valuations are attractive,” said Marija Veitmane, senior multi-asset strategist at State Street. “There’s quite a lot of bad news already priced in. Lack of bad news is good news, and we can see markets re-pricing back to higher multiples.”

In overnight political news, the White House confirmed US President Trump cancelled the delegation trip to Davos amid government shutdown, while the White House also stated that US President Trump and Treasury Secretary Mnuchin are to hold Oval Office meeting today. Elsewhere, US Treasury Secretary Mnuchin has declined a request to testify next week regarding government shutdown according to US House Ways and Means Committee Chairman Neal, while the US Treasury instead offered to send senior officials to the Way and Means hearing.

EU Commission has proposed negotiating mandates for trade talks with the US, the EU seeks cover tariff removal for industrial goods and regulatory cooperation. Trade Commissioner Malmstrom added that EU are ready to put cars into the negotiations with the US; we are not proposing to restart broad free trade agreements with the US. German government spokesman, when asked about mulling the ban of Huawei from its 5G network, said security is important for Germany.

In commodities, crude oil futures extended Thursday’s gains, adding 0.8% to $52.49 per barrel. Brent crude was up 0.6 percent at $61.56 per barrel and on track to gain roughly 2% on the week. Elsewhere in commodities, palladium was 1.5 percent higher at $1,417.00 an ounce after rising to an all-time high of $1,434.50 overnight. Demand has recently outstripped supply for the metal, used in emissions-reducing catalytic converters for cars. Palladium also appeared to get a boost from hopes for further government stimulus in China, the world’s biggest auto market. Spot gold was down 0.3 percent at $1,299.06 an ounce, after relinquishing its spot as the most expensive precious metal to palladium early in December.

Expected data include industrial production and University of Michigan Consumer Sentiment. State Street and Schlumberger are among companies reporting earnings

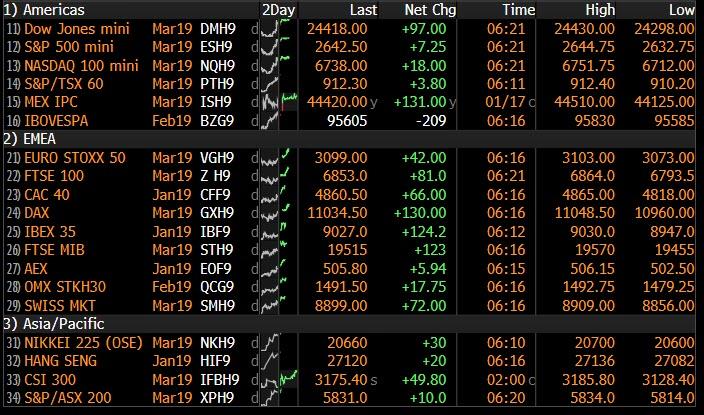

Market Snapshot

- S&P 500 futures up 0.5% to 2,647

- STOXX Europe 600 up 1% to 354.35

- MXAP up 0.6% to 153.27

- MXAPJ up 0.7% to 498.07

- Nikkei up 1.3% to 20,666.07

- Topix up 0.9% to 1,557.59

- Hang Seng Index up 1.3% to 27,090.81

- Shanghai Composite up 1.4% to 2,596.01

- Sensex up 0.02% to 36,382.51

- Australia S&P/ASX 200 up 0.5% to 5,879.59

- Kospi up 0.8% to 2,124.28

- German 10Y yield rose 2.6 bps to 0.269%

- Euro up 0.07% to $1.1397

- Brent Futures up 0.9% to $61.75/bbl

- Italian 10Y yield rose 1.0 bps to 2.406%

- Spanish 10Y yield fell 1.6 bps to 1.348%

- Brent futures up 0.9% to $61.75/bbl

- Gold spot down 0.5% to $1,285.34

- U.S. Dollar Index up 0.04% to 96.11

Top Overnight News from Bloomberg

- President Trump told his lawyer Michael Cohen to lie to Congress about talks to build a Trump Tower in Moscow, BuzzFeed reports, citing two unidentified federal law enforcement officials involved in a probe of the matter

- Investors have been flocking to the safety of longer-dated gilts, preferring them over shorter maturities, a sign that they think the risks surrounding the economy are growing. At the same time, they are betting that inflation will become a headache for policy makers

- Theresa May met leading pro-Brexit Tories and promised them she won’t agree to keep Britain in a customs union with the EU, according to people familiar with the matter. She was also firm there won’t be an extension to the March 29 deadline and she’s not going to rule out leaving the EU with no deal

- The European Commission said it is “not taking any chances” in preparing for Brexit as the possibility of a no-deal divorce was seen to increase after May was defeated in Parliament this week

- Trump administration officials are considering measures to roll back tariffs on Chinese products in order to calm financial markets, the Wall Street Journal reported, a report the Treasury Department quickly denied

- Norway Prime Minister Erna Solberg has tightened her grip on politics with a deal that secures a parliamentary majority to a conservative-led government in Norway for the first time in more than three decades

- Japan’s key inflation gauge slowed again in December, highlighting the difficulty of reaching the central bank’s 2% price goal. Yen at 98 would trigger BOJ to take action, economists say

- China’s ambassador to Canada warned that excluding Huawei Technologies Co. from its next-generation wireless network will have repercussions

- India’s government signaled it’s ready to sacrifice fiscal discipline to stoke economic growth, as it prepares to unveil its last spending plan next month before a general election

- Global oil demand remains on course to be stronger this year than in 2018 as a boost from lower fuel prices counters slowing economic activity, according to the International Energy Agency

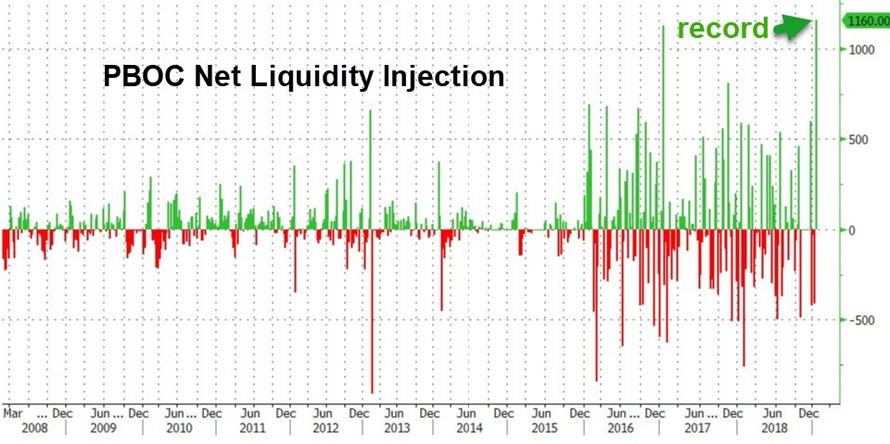

Asian equity markets traded higher across the board as the region took impetus from Wall St where the major indices were lifted on hopes of easing trade tensions after the US was said to mull lifting China trade tariffs to break the stalemate, although the Treasury was quick to downplay the prospects regarding this. As such, ASX 200 (+0.5%) and Nikkei 225 (+1.3%) were positive with broad gains across the sectors and with the Japanese benchmark the outperformer as it coat-tailed on the favourable currency moves. Hang Seng (+1.3%) and Shanghai Comp. (+1.4%) were boosted by the trade hopes with US and China also said to be in discussions on reopening access for US poultry exports to China, while the PBoC’s continued efforts this week resulted to a substantial net weekly injection of CNY 1.16tln to the interbank market. Finally, 10yr JGBs were lower as they tracked the downside in T-notes and with demand for bonds subdued by the positive sentiment across stock markets in the region, but with losses limited amid improved demand in the enhanced liquidity auction for 10yr, 20yr & 30yr JGBs.

Top Asian News

- Serial Defaulter IL&FS in Spotlight as Bond Payment Due

- Alibaba Is Said to Postpone Some Hiring, Cut Travel Spending

- Carlyle, Nomura Are Said to Weigh Bid for Orion Breweries

- Asia’s Richest Man Outlines His Plan to Take on Amazon in India

Major European equities are firmly in the green amidst positive trade updates [Euro Stoxx 50 +1.6%]. FTSE MIB (+1.0%) was initially weighed on by the poor performance of index heavyweight Telecom Italia (-7.0%) at the bottom of the Stoxx 600 after saying they expect 2018 organic EBITDA of domestic business unit to be in the lower mid-single digits compared to the previous year; adding that this may influence 2019. Major sectors are similarly in the green with some underperformance in telecom names on the back of aforementioned Telecom Italia. Other notable movers include Casino (+6.6%) after the Co’s CFO states that despite the French protests they expect to meet 2018 profit goals. Ryanair (-1.7%) have dropped to their lowest level in around 4 years as the Co. have cut their full year guidance. Easyjet (-2.4%) have been dealt a double blow this morning suffering from the Ryanair guidance cut and a downgrade at JP Morgan. Foxconn have cut 50k jobs at their iPhone factory since October, the scale of the cut is not necessarily deeper than prior years but it is significantly earlier; according to Nikkei citing industry sources.

Top European News

- Sweden Ends Historic Political Impasse as Government Is Formed

- ECB Has Narrow Window for Rate Hikes Before Economy Is Too Soft

- Telecom Italia Shares Plunge on Domestic Profit Warning

- Ryanair Earnings Outlook Takes Another Dive on Winter Fares

In FX, the USD Little changed and within a tight 96.000-140 band following yesterday’s volatile trade amid reports that the US are said to be mulling rolling back on China trade tariffs in an attempt to break the stalemate in talks, although the Treasury was quick to downplay the prospects regarding this. Furthermore, participants will be eyeing the meeting between US President Trump and Treasury Secretary Mnuchin at 17:45 GMT for any fresh details on trade or the government shutdown. DXY keeps its head above 96.000 and north of its 100 DMA at 96.055 ahead of the US industrial production data. Wells Fargo notes that a solid print in December IP would show that the industrial sector remains stable, while “a weaker print, on the other hand, may further stoke fears surrounding ongoing trade tensions and Fed policy.”

- GBP – The table has turned for the Pound after yesterday’s climb to test 1.3000 to the upside amid continued hopes of an Article 50 extension with reports stating that the EU are prepared to delay Brexit until at least July. In terms of the latest, the Northern Irish DUP party is reportedly leaning towards a Norway-style deal if it removes the threat of a NI backstop. This type of deal would essentially remove customs checks and allow for trade deals to be struck outside of the EU, though one key rule which must be accepted is the free movement of goods, services, persons and capital to and from EU and EEA member states. PM May has scheduled meetings with party leaders (ex-Labour) to find some common ground before she heads to Brussels. Labour MPs have accepted the PM’s invitation to cross-party talks in a move which defies party leader Corbyn following his demand for a no-deal Brexit to be taken off the table before dialogue can commence. GBP/USD edged lower at the start of the EU session though further downside was seen just before the release of disappointing UK December retail sales (Y/Y 3.0% vs. Exp. 3.6%), with the ONS citing weak sales as shoppers brought forward spending for Black Friday discounts. Subsequently, Cable fell to an intraday low of 1.2930 (vs.; high 1.2993) and currently stands as the G10 underperformer.

- EUR – Relatively uneventful and stuck in sideways Dollar-dominated trade as EUR/USD flirts with the 1.1400 handle ahead of the ECB interest rate decision next week where focus will be on EZ growth outlook. In related news, Bank of America Merrill Lynch has cut its 2019 Euro area growth forecast to 1.1% (Prev. 1.4%) and added that balance of risks remains clearly tilted to the downside. EUR/USD remains above its 50 DMA at 1.1380 ahead of heavy option expiries for today’s NY cut with 4bln at strikes 1.1375-1.1405 and a further 2bln between 1.1415-25 which may cap upside.

In commodities, Brent (+1.3%) and WTI (+1.4%) prices are benefitting from the positive market sentiment generated by potential US-China trade progress, currently just above USD 61/bbl and USD 52/bbl respectively. IEA’s report maintains their global oil demand growth estimate at 1.4mln BPD, and global oil supply fell by 950k BPD in December. However, the report does highlight that Russia raised their oil production in December to 11.5mln BPD and that it is unclear when they will cut production. For context, yesterday Russian Energy Minister Novak said that Russia will try to accelerate cuts in their oil output, but that there are technical limitations.

Gold (-0.5%) has suffered in the US-China stemmed positive risk environment, with the yellow metal residing towards the bottom of its USD 5/oz range. LME copper has breached USD 6000/tonne to the upside on reports stating the US are considering lifting tariffs on China; although this was swiftly downplayed. Elsewhere, spot palladium resides just below its all-time record of USD 1434.50/oz achieved on Thursday.

US Event Calendar

- 9:15am: Industrial Production MoM, est. 0.2%, prior 0.6%; Manufacturing (SIC) Production, est. 0.3%, prior 0.0%

- 10am: U. of Mich. Sentiment, est. 96.8, prior 98.3; Current Conditions, est. 116, prior 116.1; Expectations, est. 86.5, prior 87

DB’s Jim Reid concludes the overnight wrap

Mrs May is the latest to pull out of going to Davos next week due to her pressing Brexit concerns at home. She’s followed Mr Trump (Government shutdown) and Mr Macron (Gilet Jaunes) as having more important domestic issues to resolve. I’m increasingly feeling like it’s only me (and Will.I.Am) going. Although I actually now have my own domestic issues that may threaten my participation. Yes my builders told me yesterday that my porch (or portico) on my renovation project is rotten and falling down so we need to urgently decide on options. Sadly the only viable option is to work harder to pay for a new one. As a reminder if you or anyone from your organisation is going to Davos next week please let them know that I’ll be speaking about “The end of the globalisation supercycle (1980-2016)” on Wednesday morning and on “Whether robots will take your job?” on Thursday. If you or they want an invite please contact me.

Meanwhile the rally edges on and US markets got a late boost last night after the Wall Street Journal reported that the US may be approaching a trade détente with China, though officials almost immediately refuted the story. The S&P 500 jumped as much as +1.11% on the headlines, which said that “U.S. officials are debating ratcheting back tariffs on Chinese imports as a way to calm markets” and that “the president has made clear he wants a deal.” Equities retraced a bit after a Treasury spokesman denied the reports, but the S&P 500 still closed +0.76% higher for its third day of gains and 9 out of 12 so far in 2019. The DOW and NASDAQ also posting healthy climbs of +0.67% and +0.71% respectively. After playing the hero the day prior, banks for the most part of the day, did their best to reverse that move post Morgan Stanley’s numbers (more on that shortly). The Huawei investigation also lurked in the background from the day before while a weaker than expected update from Societe Generale also weighed on European financials. Indeed European banks closed down -1.20% (after being +2.51% the day before) with US banks rallying from losses of -0.91% to close up +0.93% while the STOXX 600 clawed back earlier losses to finish broadly unchanged (+0.04%) by the closing bell. High yield spreads in the US and European were similarly muted but still edged -4bps and -2bps tighter respectively.

After the closing bell last night Netflix reported somewhat disappointing results for the fourth quarter, as revenues disappointed. The company’s topline came in at $4.19bn last quarter, versus expectations for $4.21bn, and its guidance for the current quarter was notably soft at $4.49bn, versus expected $4.60bn. Nevertheless, the company added a healthy 8.8 million new subscribers, taking its total number of paying subscribers to 139 million, which would make the Netflix nation the 10th largest country in the world by population. The stock is trading down -3.93%, but it’s still up almost 50% since Christmas Eve. Remarkable.

US equity futures are trading up +0.22% overnight while sentiment across the rest of Asia is being buoyed by the positive trade headlines from last night with the Nikkei (+1.25%), Hang Seng (+1.04%), Shanghai Comp (+0.79%) and Kospi (+0.63%) all up. In term of overnight data releases, Japan’s December CPI and core-core CPI came in line with expectations and both at +0.3% yoy while core CPI was a one-tenth below consensus at +0.7% yoy.

Back to markets yesterday, Treasuries had actually broken below 2.70% at one stage early in the morning before closing a few basis points off that at 2.745%. A stronger-than-expected Philly Fed reading helped the reversal while in Europe Bunds closed +1.9bps higher with BTPs +1bp higher. The ECB’s Lautenschlaeger stuck to the script in an interview with Politico, saying that she would wait for March projections before revisiting her view of a 2019 rate hike. Staying in Europe, it’s worth flagging an MNI article yesterday (which granted hasn’t proven to be the most reliable source of late) suggesting that the ECB is growing increasingly concerned about a deepening economic slowdown which could prove longer-lasting. The market doesn’t price the next ECB hike until mid-2020 anyways, so it’s clearly already taking a dovish view relative to the ECB at the moment.

We thought we all needed a breather from Brexit so we’ve shunted it down the pecking order today. In terms of the latest update, yesterday we got confirmation that the Commons vote on PM May’s Plan B will now be on January 29th with May presenting it on Monday. Corbyn did say that a second referendum remains an option but failed to commit to it. Corbyn also appealed to all Labour MPs not to speak to May’s government until she meets the party’s conditions for talks. That is: until ‘no deal’ is off the table. However it’s clear that several Labour MPs have already met Mrs May. It seems the government have issued a note alongside these cross party talks that suggests a second referendum would take over a year to organise which for them might be an argument for suggesting it as unfeasible. Most campaigners would disagree about the necessary time frame. Nevertheless you could argue that the very discussion of another referendum puts the option back on the table and slightly raises the odds of it being realised. Obviously, another referendum would inject another dose of uncertainty into the process though. On the other hand, anything that delays things over a year could at least kick the uncertainty down the road and maybe allow for a near-term rally.

We’re a very long way from such an outcome, but the pound rallied notably yesterday, advancing +0.83% to its strongest level in two months at $1.2992. The currency was perhaps supported by a coincidental YouGov poll that suggested support for “Remain” had increased to 56% and a 12 point margin over “leave” – a post-2016 record. Overall the market yesterday perhaps appreciated the combination of the potential for a longer delay to Brexit, some engagement by Labour backbenchers in talks, all options being discussed, a second referendum being mentioned, and the supportive poll. On the other side, May reportedly promised hard-Brext-supporting MPs that she would not agree to keep the UK in the EU customs union, which would presumably be negative for the likelihood of a soft Brexit but did nothing to dampen the steady sterling rally. Meanwhile, The Times reported that the DUP is now edging towards a customs union and The Telegraph reported that as many as 20 mid-ranking ministers have indicated that they are prepared to quit the Government so they can support backbench moves to stop a no-deal Brexit. Expect lots more conflicting headlines to come. As a reminder, earlier this week our FX strategistic published “it’s time to buy the pound”. The link is here .

Coming back to the bank results yesterday, Morgan Stanley shares closed down -4.41% after reporting a miss at both the revenue and earnings lines. Like the bank’s peers, FICC revenues tumbled much more than expected (down -30% yoy) and in fact the most of the five big US banks. In addition there was also a miss in the equities division although the outlook was left broadly unchanged. Here in Europe, Societe Generale fell -5.66% after releasing a Q4 profit warning which cited weaker performance in the investment bank.

On the Fed front, Governor Quarles, who admittedly is more involved in financial regulation than monetary policy, gave a rosy view of the economic outlook. He said “the core base case remains very strong” though “clearly markets are more attuned currently to the downside risks.” So yet another example that FOMC members are unifying around the same message of strong growth but heightened risks given financial conditions. After US markets closed, Chicago Fed President Evans repeated his recent dovish rhetoric, saying that the Fed is “at a good point for pausing,” and that there could be fewer than two hikes this year.

As for the US data, the Philly Fed business outlook reading printed at +17.0 for January compared to expectations for a much more modest rise to +9.5 (vs. a downwardly revised +9.1 in December). That’s the highest reading since October however the details were slightly more mixed. New orders rose to the highest since July last year at 21.3 however prices paid slid to a thirteen-month low at 32.7 – which plays into the Fed patience argument. On an ISM-adjusted basis the series actually slid to 54.8 compared to 55.3 previously. That’s a steeper slide than the move implied by empire manufacturing earlier this month, but the trend remains downward going into the start of the year.

The other data out in the US yesterday was the latest weekly initial jobless claims print which fell -3k to 213k and towards the current cycle lows again. The details did however confirm another tick up in claims at a state level in Washington, DC as a result of the shutdown. DC is in fact showing the highest level of claims since 1996, the previous record-holder for longest-ever shutdown.

Meanwhile in Europe there were no surprises with the final December core CPI reading for the Euro Area at +1.0% mom (unrevised versus the flash). Here in the UK there was some interest in the BoE credit conditions survey with the data revealing that UK lenders expect demand for credit card lending over the next three months to fall at the fastest pace since records started in 2007. UK lenders also expect mortgage demand to fall at the fastest pace in eight years. So certainly a softer survey and it’s worth noting that the BoE follow the data closely so something to keep in mind. On that, Dutch tech company Philips announced yesterday that it would close its factory in Suffolk and transfer its operations to the Netherlands. So the wider Brexit impact on UK growth is becoming more and more apparent and as our UK economists noted this will make life for the BoE difficult when undertaking the supply side review on the 7th Feb inflation report.

Finally, to the day ahead now where this morning we get the November current account balance reading for the Euro Area followed later by December UK retail sales data. This afternoon in the US there should be some interest in the December industrial production print (+0.2% mom expected) along with the preliminary University of Michigan consumer sentiment survey for January. Away that we’re due to hear from the Bank of Italy’s Visco and Italian Finance Minister Tria at an event this morning in Rome at 9am GMT, while this afternoon the Fed’s Williams (at 2.05pm GMT) and Harker (4pm GMT) are slated to speak. Schlumberger is the highlight on a quiet day of earnings releases.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 36.37 PTS OR 1.42% //Hang Sang CLOSED UP 335.18 POINTS OR 1.25% /The Nikkei closed UP 263.80 PTS OR 1.29%/ Australia’s all ordinaires CLOSED UP 0.53%

/Chinese yuan (ONSHORE) closed DOWN at 6.7787 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.59 dollars per barrel for WTI and 61.74 for Brent. Stocks in Europe OPENED /GREEN

//. ONSHORE YUAN CLOSED DOWN AT 6.7787 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7874: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i)CHINA

After seeing flash crashes in two of China’s major real estate developers, we are witnessing property developers implode as the market is freaking out over 55 billion dollars worth of debt coming due in 2019

(courtesy zerohedge)

Chinese Property Developers Implode As Market Freaks Out Over $55 Billion Debt Cliff

Earlier this month, when we reported that in the latest warning about China’s housing sector, the Communist Party’s People’s Daily warned that China’s regional economies need to reduce their reliance on the property market for growth and instead focus on sustainable longer-term development, we wondered if “something was afoot with China’s housing sector.”

The story is familiar: in recent years, hundreds of cities across China have seen upswings in their local property markets under a long-term plan by Beijing to further urbanize the country. The process of building new homes and revamping old ones has only accelerated in the last few years, backed by local governments keen to boost land sales and meet red-hot property demand. Indeed, the total sales of China’s top 100 real estate developers soared 35% last year. But repeating a now familiar warning that the party is over, Beijing has once again expressed concern that some cities, looking for rapid expansion, have grown their property markets too quickly and at the expense of new industry development, adding potential froth to real estate prices.

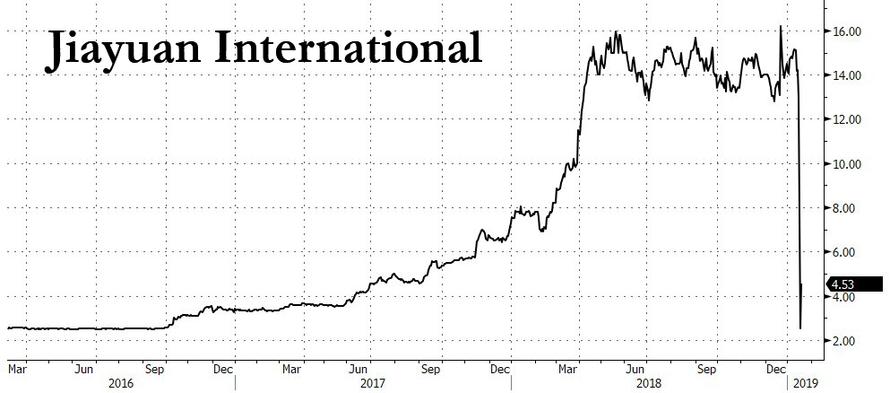

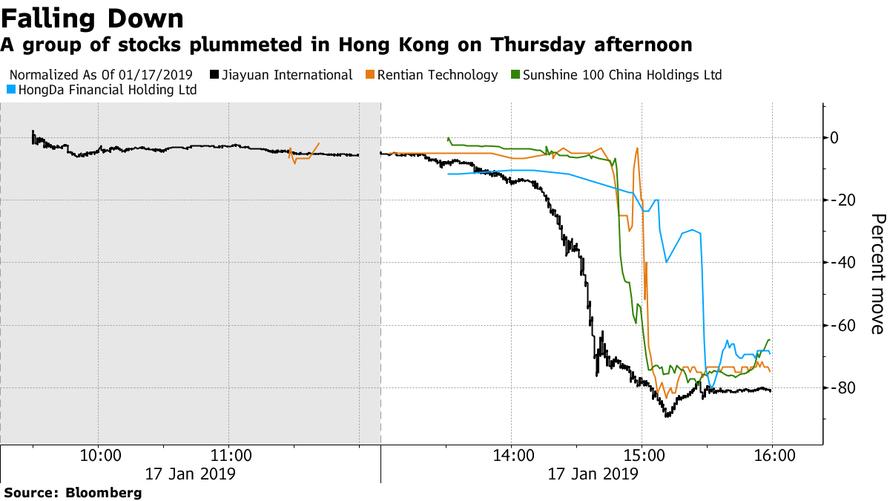

Two weeks later, our concern that something is not quite well with China’s housing sector was validated by the market overnight when shares in Jiayuan International, a prominent Chinese property developer, imploded in late trading in Hong Kong on Thursday, its stock collapsing 81% due to investor unease over a sector that is staggering under vast debts just as the world’s second-biggest economy slows.

According to analysts, all of whom were dumbfounded by today’s move, said that the stock, which flash crashed after a chaotic day’s trading that wiped more than $3 billion from its market capitalisation with the selling promptly spilling over to many of its peers…

… was engulfed by concern that Jiayuan would default on a $350 million bond that matures this week.

As we reported earlier this morning, the panic liquidation over Jiayuan also ensnared rival property company Sunshine 100 China Holdings, whose shares plunged 65% moments after Jiayuan’s collapse when traders realized that the two companies share a director.

“Some of these companies might have cross-shareholdings in each other and when one of those starts to tumble, it brings down other related stocks,” said Bocom strategist Hao Hong. “It’s likely more similar stock crashes could happen this year. A lot of share pledges in Hong Kong are underwater, and as soon as the positions are liquidated it triggers an avalanche.“

The property development sector has become especially vulnerable to sharp selloffs as it has accumulated large amounts of dollar debt, while the flagging Chinese economy has boosted fears about future prospects for China’s housing sector in what may end up being the country’s first hard landing in decades.

But the biggest problem is the upcoming debt cliff, which will force the sector to refinance at the worst possible time: according to the Financial Times, Chinese developers have about $55 billion of maturing onshore debt in 2019, which as discussed this morning accentuates concern over potential defaults.

The sector is under pressure because of “potential concern over bond defaults, as [the companies] have offshore funding coming due,” said Morningstar analyst Phillip Zhong. As a result “the cost of refinancing is quite expensive.”

In hopes of reversing the market panic, the company published a statement on its website after the Hong Kong stock market closed on Thursday, in which Jiayuan said that it had repaid the $350 million bond, adding that “its current financial situation is healthy and business operations is normal.”

Clearly the market did not agree, although what exactly caused the stock to lose 80% of its value in one day remains a mystery, because while traders blamed everything from massive leverage, to stock pledges, to some variation of cross-asset holdings and interlinked collateral for the latest flash crash, the reality is that nobody really knows what happened as Castor Pang, head of research at Core Pacific-Yamaichi confirmed: “No one really knows what’s going on here. For common investors, it’s a very surprising and tough situation as there was no time to get out.”

* * *

The bigger problem, beside the “avalanche” of overnight Hong Kong flash crashes is that after a boom in recent years, China’s property market is cooling, with developers forced to announce sharp price to move inventory, in the process leading to public anger over a sharp drop in prevailing prices. As we reported in October, this led to homeowners protesting in the streets last year in several large cities to demand refunds after developers cut prices to stimulate sales.

And then there is the issue of the $55 billion in coming property developer debt maturities which risks to blow up the local debt market as rates gradually rise. Refinancing maturing debt “has always been a concern for lower-rated companies” in the property business, and will be particularly urgent this year given the scale of the debt maturing, said Mr Zhong.

Quoted by the FT, Nicole Wong, an analyst at CLSA, noted that recent stimulus measures by the central bank are “aimed at only the very big [developers]”.

The silver lining is that the overnight crash in property developer shares was not enough to unsettle the wider Hong Kong market, with the benchmark Hang Seng index closing barely down.

Still, traders are growing more nervous that the tipping point is near: Wee Liat Lee, head of financial group and property research in Asia at BNP Paribas, said the issue of systemic risk “is a problem . . . the Chinese economy is pretty dependent on property as a sector, in terms of investment and reliance of local government on land sales and revenue”.

“But I think this is an issue the Chinese government realised a long time ago,” he added. “It’s a structural problem that takes quite a bit of time to unwind.”

Failing that, Beijing will just bail out the entire housing sector as it has done on so many prior occasions. The alternative is the one thing that keeps every politician in Beijing up at night: revolution.

Foxconn Cuts 50,000 Jobs Due To iPhone Sales Slowdown

In the latest indication that the slump in sales of Apple’s most recent batch of iPhones isn’t a transitory trend, Nikkei Asia Review on Friday reported that Foxconn, one of Apple’s biggest and most important iPhone suppliers, is cutting seasonal staff more swiftly than in previous years, a sign that it is bracing for weak sales in the months ahead as the industry suffers its worst downturn in 10 years.

Normally, the 50,000 contract workers who have been let go at Foxconn’s most important factory in Zhengzhou would have been kept around for a few more months, as the manufacturer gradually reduced its employee head count.

The report comes after Apple announced plans to cut iPhone production for the second time in two months.

Around 50,000 contract workers have been let go since October at Foxconn Technology Group’s most important iPhone factory at Zhengzhou, in China’s Henan Province, according to an industry source familiar with the situation. Normally, the contracts of these workers would be renewed every month from August until mid- to late January, when the workforce is traditionally scaled back for the slow iPhone production season.

The depth of the cuts isn’t deeper than in previous years, it’s just happening much earlier than expected, as many workers were asked to leave before year-end as expectations for holiday sales slumped.

The scale of the cuts is not necessarily deeper than previous years, it is simply significantly earlier, industry sources said. “It’s quite different this year to ask assembly line workers to leave before the year-end,” a source with knowledge of Foxconn’s reductions said.

Other important iPhone suppliers have let workers go much earlier than usual as they struggle with slower-than-expected demand for Apple’s iconic product. The California tech giant earlier this month shocked the market by warning of a slump in revenues at the end of 2018. This year is also shaping up to be difficult, with further declines expected in the smartphone market, while the ongoing U.S.-China trade war is taking a heavy toll.

Foxconn isn’t alone in its cutbacks: Other companies further down the supply chain are also cutting jobs.

Pegatron, Apple’s second-biggest iPhone assembler, began canceling monthly labor contracts in November. A source close to the company said its normal practice was to reduce the 200,000-strong head count by tens of thousands every month until reaching about 100,000 – the minimum required for daily operation, according to one source familiar with the situation. “And for [2018], it just happened sooner than in the past because of poor demand.”

Industry sources said early cutbacks were happening further down the supply chain as well. One key component supplier based in Shenzhen had asked 4,000 workers to take an extended “vacation” from October to March, a person with knowledge of the situation said. “The company has not actively laid off those workers yet. It will decide whether or not to lay them off after March 1,” the source said.

To be sure, Foxconn’s cutbacks stretch beyond its iPhone manufacturing units. It is also paring back the number of managers and consolidating business units as it aims to cut 100,000 permanent positions.

Meanwhile, Foxconn – formally Hon Hai Precision Industry – is in the middle of an aggressive cost-cutting program as it braces for a difficult 2019. In addition to letting contract workers go early, it is hoping to reduce expenses with an organizational restructuring, according to people close to the Taiwanese company. It has recently merged business units making Apple’s MacBooks and iPads with another division making laptops and desktops for Dell and Acer.

The result of the consolidation will be steep cuts to management jobs and back office support staff such as human resources, administration, accounting and finance, and utility support jobs. “Previously, each business unit had its own supporting staff, and by merging business divisions, Foxconn can slash some 50% of those supporting jobs and even condense managerial positions too,” a person familiar with the reshuffle told the Nikkei Asian Review.

The reorganization is part of Foxconn’s push to cut 100,000 jobs out of about 1.1 million by the end of 2018 across all of its affiliates and subsidiaries, as reported by Nikkei Asian Review in November. Foxconn aims to cut costs by some 20 billion yuan ($2.96 billion) in 2019 compared with 2018, according to an internal document dubbed the “1031 project” seen by Nikkei.

To be sure, Foxconn’s embrace of automation has been partly responsible for the reduction in its head count. But as smartphone sales slowed last year, Foxconn and other iPhone suppliers revealed steep declines in revenue, with Foxconn’s yoy revenue falling 8% in December compared with the same month last year.

But as Apple CEO Tim Cook has decided to stop breaking out iPhone sales and to place more emphasis on the company’s software and other product offerings should, investors (including the Oracle of Omaha himself) who are hoping for a return to $1 trillion market cap should probably hope that the company hurries up and launches its next-generation iPhone Air Pods. Or maybe – just maybe – cutting prices on its increasingly expensive flagship product.

4.EUROPEAN AFFAIRS

/UK

Odey, a BREXIT supporter warns that if Great Britain does not leave the EU, a “revolution” will begin

(courtesy zerohedge)

Crispin Odey Warns Of “Revolution” If Brexit Fails

For Crispin Odey, revenge is a dish best served at 2 and 20 degrees.

The hedge fund manager, who suffered years of underperformance with many, including occasionally this site, predicting his demise when year after year Odey dared to “fight the Fed” and go all in on his bet for a “violent unwind” of the QE bubble, finally enjoyed a triumphant return in 2018 when, as we reported in December, his performance in 2018 was absolutely stellar, topping the HSBC hedge fund league table and generating nearly double the return of his next closest peer with a 52% YTD return for his European fund.

Now, still fresh from his victory tour, the billionaire hedge fund investor has once again turned to a topic that is near and dear to his heart, namely Brexit – which he backed and which has been the source of much of his profits last year – and in an interview with Financial News, Odey warned of a “revolution” if politicians fail to ensure the UK leaves the European Union.

While the high-profile investor, who donated generously to the Vote Leave campaign in 2016, prompted some confusion last was weekend when he quoted as saying Brexit “ain’t gonna happen” because “I just can’t see how it happens with that configuration of parliament”, speaking to Financial News, Odey elaborated saying his comment referred only to the short-term political outlook, and that he believes that Brexit can – and must – happen in the long run.

“All I was saying, which maybe was misquoted, was that it was very obvious, given the constitution of parliament, that we weren’t going to get a Brexit,” he said. “It doesn’t mean that they [politicians] are not going to get scared about what they are going to do when they have to face constituents, having promised that they would deliver Brexit.”

Odey then warned ominously that “in the long-term, usually what the people want, the people get. Otherwise there’s a revolution.”

His latest predictions come in a week of turmoil for UK politics, with parliament delivering a crushing defeat to Prime Minister Theresa May’s EU withdrawal agreement on January 15 and the PM surviving a vote of no confidence in her government just one day later. May will now work with MPs across all parties to try and find a way of moving Brexit forward, with the UK’s official exit date of March 29 fast approaching.

To be sure, Odey is anything if unconflicted: he donated £873,323 to the Vote Leave campaign. Along with Paul Marshall, co-founder of Marshall Wace, and Savvas Savouri, chief economist of Toscafund Asset Management, Odey is one of the City’s most high-profile Brexit backers according to FN.

He also restated his belief that the pound would now strengthen, having bet against the UK currency in the recent past. “Sterling has been oversold,” Odey said. “If sterling is likely to be rising, why be short on it?”

This is another trade where he has been spot on because after flash crashing early in January, on Thursday the pound rose to the highest since Nov. 15, squeezing numerous shorts, after U.K. opposition leader Jeremy Corbyn said that a second referendum remains an option in the Brexit saga.

And in totally separate news, Orlando Montagu, a partner at Odey Asset Management, announced he is leaving the company in March to focus on his family’s famous: the sandwich. Montagu is a direct descendant of the 4th Earl of Sandwich, who was credited with inventing the snack in the 18th century. He will leave Odey Asset Management at the end of March after more than 16 years at the firm. He’ll work at his family’s mostly U.S.-based business, also known as Earl of Sandwich, which has plans to open in London.

Speaking to Bloomberg, Montagu, who is deputy chairman and part of the executive committee which runs the hedge-fund firm., said “the timing feels right. Crispin is performing well, clients are making money and the Odey team is upbeat.”

end

FRANCE

LePen is now moving closer to the centre as she states that leaving the Euro is “no longer a priority” .

A leopard cannot change it’s spots

(courtesy zerorhedge)

Marine Le Pen Says Leaving The Euro “No Longer A Priority”

Though they have calmed somewhat since they first erupted late last year, the Yellow Vest protests are set to continue this week as French President Emmanuel Macron’s offerings of olive branches in the form of rolling back a planned gas-tax hike (the original impetus for the protests), promising to blow out the deficit to offer more government benefits and even abandoning plans to go to Davos have done little to quiet the public outrage over his “presidency for the rich.”

And as his popularity drops to unprecedented lows, polls suggest that the party of his former rival for the presidency, the National Rally party’s Marine Le Pen, has overtaken Macron’s “En Marche” in popularity. And as Le Pen and her fellow pan-European populists organize to mount a credible challenge to the Brussels establishment during the upcoming European Parliamentary elections in May, Le Pen is making a notable pivot in her party’s platform, presumably to try and make it more appealing to more centrist Europeans.

According to RT France, Le Pen told the press on Thursday that leaving the euro – once a hallmark of her party’s position – was “no longer a priority” for National Rally.

“Unquestionably, the euro is a blow for France” but out “is no longer a priority,” Le Pen said Thursday, advocating a change in monetary governance of the European Union.

“If we change the monetary” governance and “we see that it is sufficient to allow the French economy to recover the handicaps that have been created by the currency, we will keep the change. We are pragmatic, we are not ideologues,” said the president of the National Assembly in the margins of her wishes to the press at the headquarters of his party in Nanterre.

Though opposing the euro will no longer be a priority, Le Pen had some disparaging words for the European Central Bank, a sign that she is pivoting to an economically populist agenda targeting inequality and immigration. Instead of directing its policies to the benefit of European workers, the ECB’s focus on inflation has led it to a monetary stimulus policy that has helped widen inequality.

“The governance that has been chosen and which aims for the ECB [European Central Bank] to fight only against inflation and to refuse to fight against unemployment, poses a real problem,” said the finalist of the presidential election in 2017.

“Money creation by the EU, instead of being sent to agencies to invest in the real economy or even directly to states…is for banks and is lost, diluted in the virtual economy,” she said.

Instead of focusing on leaving the euro, Le Pen would rather RN focus on border sovereignty and economic issues like the French budget, a position that echoes that of Italy’s populist leaders, who recently faced down the EU and won permission to blow out the country’s budget deficit.

end

GERMANY/HUAWEI (CHINA)

This is not good for China as now powerhouse Germany is exploring a ban on Jauwei products.

(courtesy zerohedge)

Germany Reportedly Exploring Ban On Huawei Products

With the US launching a federal investigation into Huawei over alleged theft of intellectual property from US carrier T-Mobile, and US lawmakers once again weighing a ban on sales of US-made microchips to ZTE and Huawei over suspicions that both companies violated US sanctions on Iran, the US’s campaign to shut Huawei out of Western markets took yet another step forward on Thursday when the Wall Street Journal reported that Germany is considering a ban of Huawei products in the country’s 5G networks.

The effort, reported by WSJ and German newspaper Handelsblatt, is focusing on indirectly banning Huawei from telecom networks’ “core networks” – the essential functionality of a mobile network. And while the effort is focused on 5G, it could also apply to 3G and 4G networks.

The German official said raising security requirements would be the only legal way to de facto exclude Huawei from all crucial tenders in Germany as the country has no other legislation that would justify an outright ban.