GOLD: $1292.80 DOWN $1.10 (COMEX TO COMEX CLOSINGS)

Silver: $15.51 DOWN 9 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1292.30

silver: $15.53

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 0 NOTICE(S) FOR nil OZ (0.000 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 538 NOTICES FOR 53800 OZ (1.6734 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

124 NOTICE(S) FILED TODAY FOR 620,000 OZ/

total number of notices filed so far this month: 644 for 3,220,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3571: DOWN 19

Bitcoin: FINAL EVENING TRADE: $3606 UP $17

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN FAIR SIZED 989 CONTRACTS FROM 191,922 UP TO 192,911 DESPITE YESTERDAY’S 0 CENT PERFORMANCE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1396 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1396 CONTRACTS. WITH THE TRANSFER OF 1396 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1396 EFP CONTRACTS TRANSLATES INTO 6.981 MILLION OZ ACCOMPANYING:

1.THE 0 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.625 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 28,974 CONTRACTS (FOR 12 TRADING DAYS TOTAL 28,974 CONTRACTS) OR 144.870 MILLION OZ: (AVERAGE PER DAY: 2415 CONTRACTS OR 12.073 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 144.87 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.69% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 144.87 MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 989 DESPITE THE 0 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1396 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2385 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1396 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 989 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 0 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.60 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 124 NOTICE(S) FOR 620,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.625 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A TINY SIZED 392 CONTRACTS DOWN TO 501,213 DESPITE THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $5.40//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 7276 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 7276 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 501,213. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6,884 CONTRACTS: 392 OI CONTRACTS DECREASED AT THE COMEX AND 7276 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 6,884 CONTRACTS OR 688400 OZ = 21.41 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $5.40

YESTERDAY, WE HAD 11,496 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 98,201 CONTRACTS OR 9,820,100 OZ OR 305.45 TONNES (12 TRADING DAYS AND THUS AVERAGING: 8183 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 305.45 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 305.45/2550 x 100% TONNES = 11.97% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 305.45 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED DECREASE IN OI AT THE COMEX OF 392 DESPITE THE GAIN IN PRICING ($5.45) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7276 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7276 EFP CONTRACTS ISSUED, WE HAD ANOTHER GOOD GAIN OF 6,884 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7276 CONTRACTS MOVE TO LONDON AND 392 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 21.41 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE RISE OF $5.40 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 4TH STRAIGHT DAY THAT WE RECORDED STRONG RISES IN OI ON BOTH EXCHANGES!

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.10 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 797.71 TONNES

Inventory rests tonight: 797.71 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 9 CENTS IN PRICE TODAY:

A HUGE CHANGE IN SILVER INVENTORY/

WE HAD A MASSIVE WITHDRAWAL OF 3.895 MILLION OZ ON SUCH A TINY LOSS IN PRICE??/

GLD AND SLV ARE MASSIVE FRAUDS

/INVENTORY RESTS AT 307.110 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 989 CONTRACTS from 191,920 UP TO 192,911 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1396 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1396 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 989 CONTRACTS TO THE 1396 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2385 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 11.93 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.625 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 0 CENT PRICING FALL THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1396 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 10.79 PTS OR 0.42% //Hang Sang CLOSED DOWN 146.47 POINTS OR 0.54% /The Nikkei closed DOWN 40.48 PTS OR .20%/ Australia’s all ordinaires CLOSED UP 0.27%

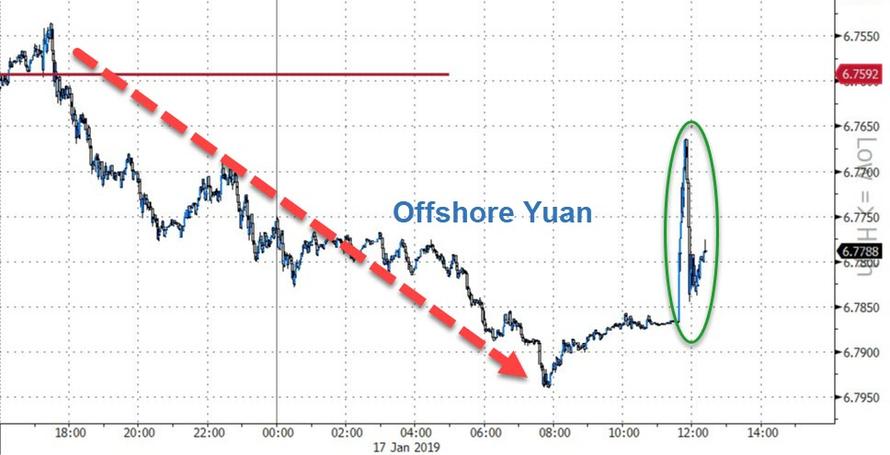

/Chinese yuan (ONSHORE) closed DOWN at 6.7709 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.28 dollars per barrel for WTI and 60.21 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7709 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7805: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/CHINA

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA

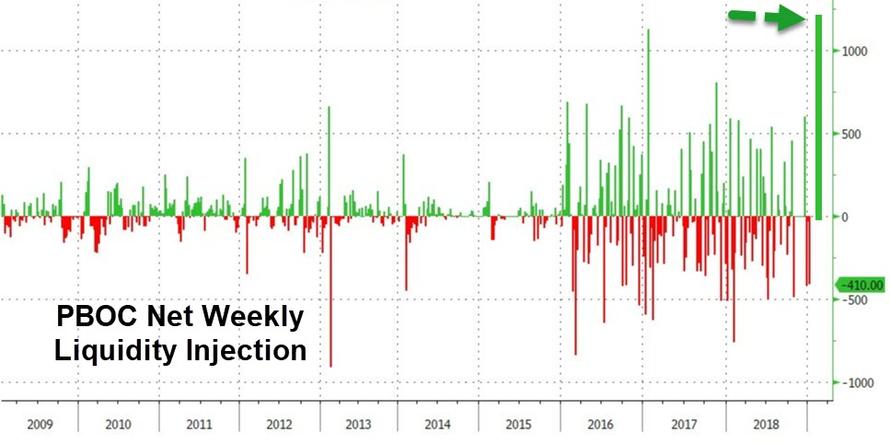

for three days in a row, China has unleashed massive liquidity: the total sum 1.1 trillion yuan or 162.96 billion dollars worth of stimulation..and that is huge.

( zerohedge)

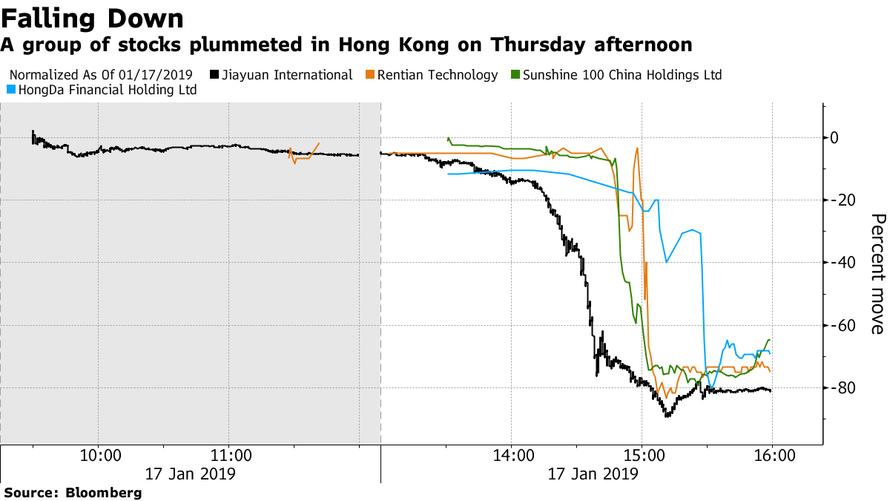

ii)This is unbelievable: Hong Kong stocks suddenly plummet in an avalanche of flash crashes and that spread to other stocks. Nobody knows what was going on to cause this flash crash

( zerohedge

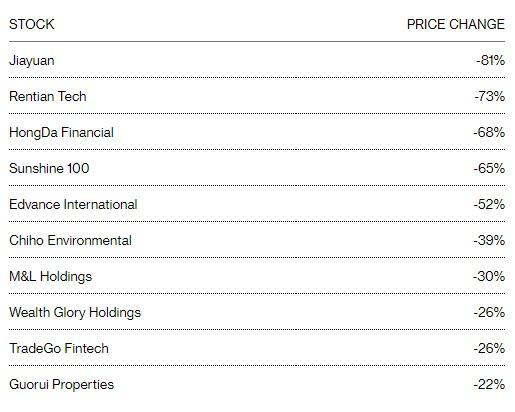

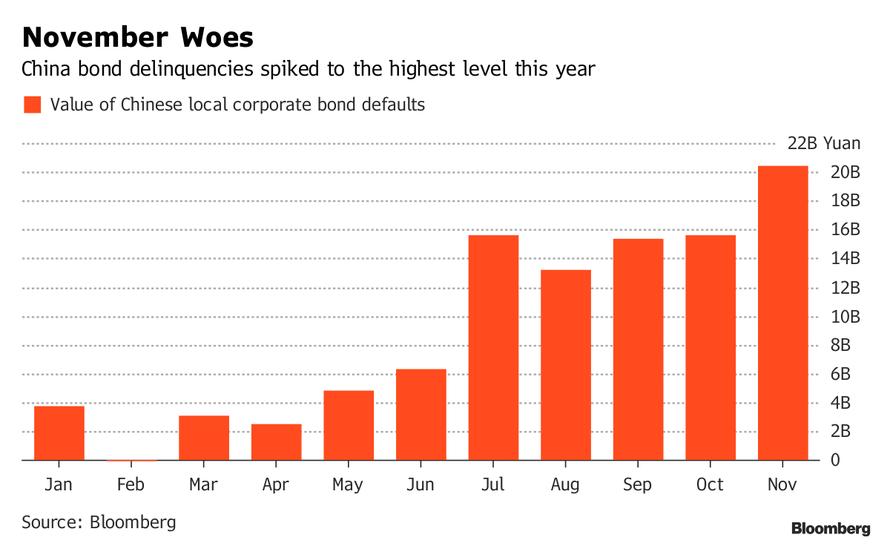

iii)This is a fascinating story. The following Chinese company defaulted on a bond even though their reported cash by 15 times the entire due debt. Obviously the accounting was fraudulent and most likely we will begin many of these

( zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE/

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

We have been pointing this out to you for quite a while: Russia’s resilience in the face of sanctions.

It’s economy is set to overtake Germany in the next decade, albeit that they have a lot more citizens than Germany

( zerohedge)

6. GLOBAL ISSUES

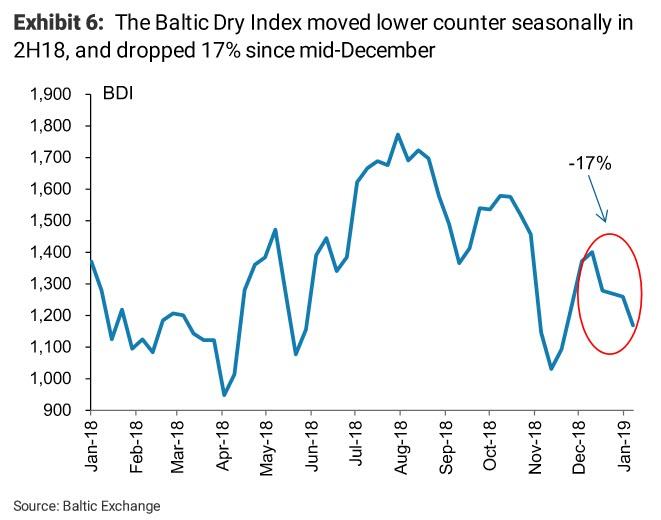

Shipping data, into China and out flashes red as Chinese shipping rates collapse along with the Baltic dry index

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

iii)A good history lesson today as Konig describes the affinity to gold for early Californians

( JPKonig/GATA)

v)Palladium hit $1400.00 per oz on supply problems. The demand for Palladium rose to 8.5 million oz with production at 7.5 million oz. Thus above ground palladium must be used to satisfy demand. Very shortly will be Platinum use in cars increase because of the lack of Palladium.

(Scrap register and Bloomberg)

vi)Sam Zell is the real estate king on Wall Street. He has never bought any gold in his 77 year old life. His gives his reasons why he is buying gold.

( zerohedge)/Sam Zell)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

They should throw these guys into jail: first stocks rise then fade after the treasury denies reports that the uSA is weighing lifting Chinese tariffs to calm markets

( zerohedge)

ii)Market data/

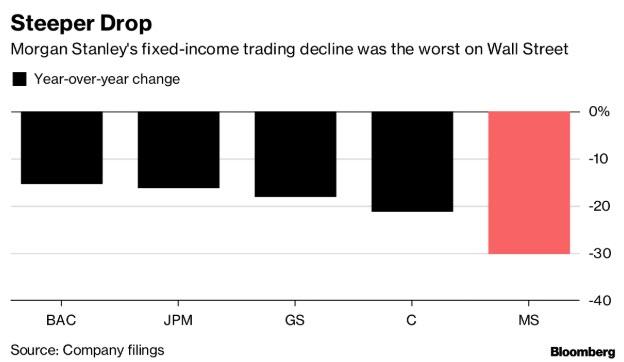

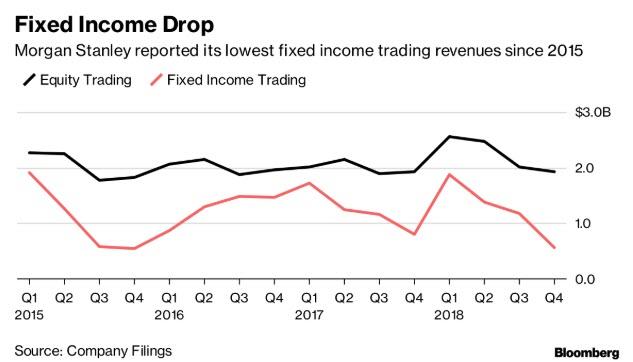

i)It seems that most of the big boys are having trouble in the fixed income department. Now, it is 5 out of 5 big investment banks have reported disappointing FICC revenue.(MORGAN STANLEY)

( zerohedge)

(courtesy zero hedge)

a)Goldman Sachs warns of a big hit to the economy as the rich cut their spending once they see how badly they are doing with their stocks.

( zerohedge)

b)My goodness! This did not take long: for the second time in only two years, children’s clothing retailer Gymboree Group has filed for chapter 11 as the bloodbath in the retail space continue! They reported that they had poor holiday sales. Also dept store Shopko filed.

(courtesy zerohedge)

c)Sears accepts a $5.2 billion dollar rescue package from its big owner/investor Eddie Lampert

( zerohedge)

iv)SWAMP STORIES

This is quite a story…John Solomon receives tips from committee members concerning the Bruce Ohr testimony. Bruce Ohr warned the FBI of the Clinton connection with respect to the Steele dossier as well as its possible bias. Ohr told the FBI a lot earlier than thought..well before Steele was fired..and well before the FISA warrants were issued. Not only that but Ohr meet with Mueller’s top lieutenant Weissmann and briefed him on the issues well before the Mueller investigation started. The key point here is that the FBI knew that the Steele dossier was suspect and not verified but they went ahead and filed with the FISA court anyway. A lot of people will be going to jail on this.

(courtesy zerohedge)

b)funny: Trump cancels Pelosi’s foreign trip (using a military plane) because of the shutdown. However if she wants to fly commercial that is up to her but she has to pay for it.

(courtesy zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 1 CONTRACT DOWN TO 459. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 1983 CONTRACTS UP TO 144,533 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Out of Scotia: 160.75 oz

i) Into Brinks: 15,187.500 oz

ii) Into CNT: 587,464.400 oz

Political Turmoil in UK & US Sees Gold Hit 2 Week High

For first time in over 16 years, palladium futures settle at a premium to gold futures

Gold futures on Wednesday resumed their climb toward the psychologically important price of $1,300 an ounce, settling at their highest in nearly two weeks on the back of political turmoil in the U.K. and U.S.

Caution among traders had deepened “ahead of a no-confidence vote on British Prime Minister Theresa May’s government and other geopolitical risks, including the U.S. government shutdown, loom large in investors minds,” said Mark O’Byrne, research director at GoldCore.

“Physical demand for gold coins and bars has picked up in the U.K. and Ireland, due to Brexit and U.K. political uncertainty,” he added.

Excerpt of article and full article can be accessed on MarketWatch here.

Watch Our Latest Video Updates On YouTube Here

News and Commentary

Gold at highest in nearly 2 weeks on political turmoil in the U.K., U.S. (MarketWatch.com)

Palladium prices hit record on supply deficit, gold firm on rate views (Reuters.com)

Theresa May’s government survives a no-confidence vote after its crushing Brexit defeat (CNBC.com)

Shutdown could delay trade talks with EU, Japan, Grassley warns (MarketWatch.com)

Pessimism About U.K. Housing Is at Its Worst in Two Decades (Bloomberg.com)

Turkey set to refine more Venezuelan gold as Maduro sends committee (AhvalNews.com)

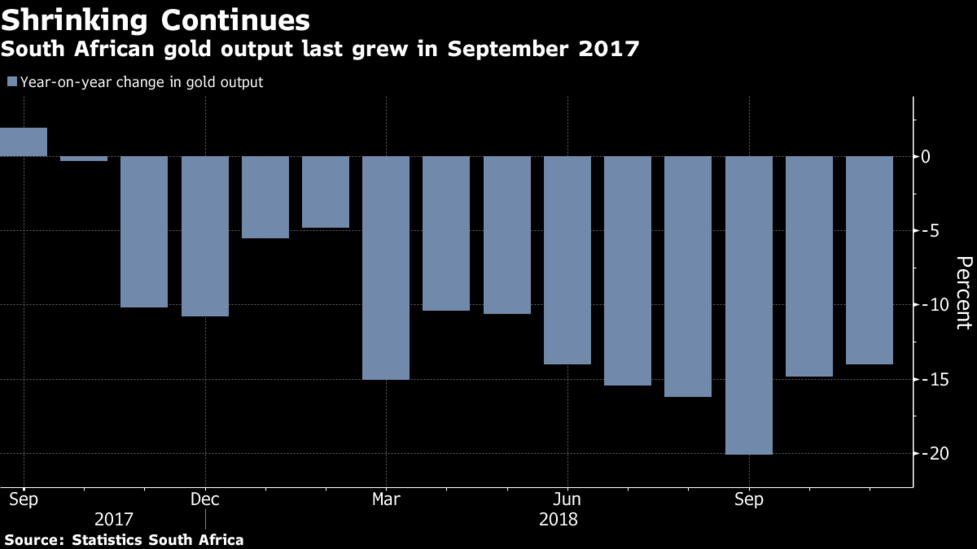

South African Gold Output Has Longest Losing Streak Since 2012 (Bloomberg.com)

“Geopolitical risks, including the U.S. government shutdown, loom large in investors minds,” said GoldCore

(MarketWatch.com)”

Goldman Says Rich People Will Drag Down the U.S. Economy by Spending Less (Bloomberg.com)

London house prices:Brexit ‘horror show’ provokes fears of steeper decline (HomesAndProperty.co.uk)

‘Patron Saint’ of the Investing Business: Remembering Jack Bogle (Bloomberg.com)

Regulators Urge Deutsche Bank To Merge With European Rival (To Spread The Pain) (ZeroHedge.com)

Polgar: “World Is Comfortably Unaware Of Approaching Disaster” (ZeroHedge.com)

The Newmont-Goldcorp Deal Is Positive News for Gold Sector (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA PM)

16 Jan: USD 1,290.50, GBP 1,002.46 & EUR 1,130.99 per ounce

15 Jan: USD 1,289.35, GBP 1,002.99 & EUR 1,127.67 per ounce

14 Jan: USD 1,293.70, GBP 1,007.02 & EUR 1,129.27 per ounce

11 Jan: USD 1,298.80, GBP 1,012.91 & EUR 1,123.96 per ounce

10 Jan: USD 1,292.40, GBP 1,012.98 & EUR 1,121.54 per ounce

09 Jan: USD 1,281.30, GBP 1,006.41 & EUR 1,118.32 per ounce

08 Jan: USD 1,291.90, GBP 1,006.71 & EUR 1,121.62 per ounce

Silver Prices (LBMA)

16 Jan: USD 15.54, GBP 12.09 & EUR 13.66 per ounce

15 Jan: USD 15.60, GBP 12.13 & EUR 13.65 per ounce

14 Jan: USD 15.61, GBP 12.13 & EUR 13.61 per ounce

11 Jan: USD 15.68, GBP 12.23 & EUR 13.60 per ounce

10 Jan: USD 15.70, GBP 12.33 & EUR 13.63 per ounce

09 Jan: USD 15.62, GBP 12.27 & EUR 13.64 per ounce

08 Jan: USD 15.64, GBP 12.24 & EUR 13.64 per ounce

Recent Market Updates

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

– China Adds 320,000 Ounces To Gold Reserves – First Central Bank Purchase Since October 2016

– Gold At 6 Month High At $1,300 and All Time Record Highs In Australian Dollars Over $1,870

– Gold Hedges Stock Market Falls In 2018 – Gains 2.7% In Euros and 3.8% In Pounds

– Hope For Best In 2019 But Prepare For Worst by Increased Allocations to Gold and Silver – Outlook 2019 Podcast

Wary investors drawn to gold’s allure

Submitted by cpowell on Wed, 2019-01-16 15:56. Section: Daily Dispatches

By Henry Sanderson and Neil Hume

Financial Times, London

Monday, January 15, 2019

If gold is anything to go by, investors are increasingly anxious about the state of the world.

Volatile equity markets and fears of a global economic slowdown have helped gold rally 10 per cent from its August lows, putting it among the best performing metals over that period.

It is a sharp contrast to much of the past two years, when rising US interest rates, a strong dollar, and buoyant equity markets hurt gold bugs and the shares of miners such as Barrick Gold, Newmont Mining and Goldcorp. And when there was a correction in US stocks in early 2018, the gold price failed to benefit.

…

Almost a year on, the big question is whether 2019 could prove a profitable year to own gold, which is typically bought as hedge or haven by investors.

The amount of physical gold in exchange traded funds has risen to 71.9 million ounces, close to the record high of 72 million touched in May 2018.

“We haven’t seen flows like this since the first half of 2016, when the gold market really took off,” says Joe Foster, a portfolio manager at VanEck in New York.

“There seems to be a change in sentiment and investor psychology. People are waking up to the fact that we are late in the economic cycle and we could be ending it in the next year or two. That brings more risk into the system. That’s why gold is moving up.” …

Some investors believe rising concerns over US debt levels could sharpen gold’s allure, according to John Hathaway, a senior portfolio manager at Tocqueville Asset Management in New York.

Last week Fitch Ratings warned that a continued government shutdown in the US could lead to a credit downgrade on the country’s debt, which is rated AAA by the agency.

“The US is beginning to sport a debt-to-GDP ratio worthy of any banana republic,” says Mr Hathaway. “We believe that exposure to gold is both timely and potentially rewarding.”

Higher levels of debt will also make it hard for the Fed to raise rates and tighten monetary policy, adds Trey Reik, a senior portfolio manager at Sprott Asset Management in Connecticut.

“I do think the dollar is in the midst of a long-term weakening,” he says. “You cannot raise rates with that much debt in the system without causing economic collapse.”

The buying of gold by central banks is also at its highest level since 2015, as many authorities remain keen to diversify away from the dollar. …

For the remainder of the report:

https://on.ft.com/2FutTpl

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

Seems that Newmont CEO’s Goldberg is very unenthusiastic about the prospects for gold. Chris Powell believes that he is quite content with central bank intervention in his medium.

(courtesy TomDiChristopher/CNBC/GATA)

Newmont CEO is unenthusiastic about prospects for gold price

Submitted by cpowell on Wed, 2019-01-16 18:02. Section: Daily Dispatches

He sounds content with central bank intervention against monetary metal.

* * *

Newmont Mining CEO Says Goldcorp Deal is Designed to ‘Survive’ a Drop in Gold Price

By Tom DiChristopher

CNBC, New York

Wednesday, January 16, 2019

Newmont Mining’s $10 billion purchase of Goldcorp does not mean the metals miner is making a bullish call on gold, according to CEO Gary Goldberg.

Instead, the global gold and copper miner is seeking to optimize Goldcorp’s assets during a period when the cost of the yellow metal has flat-lined and the industry is undergoing significant consolidation.

We’re designing our business to survive through the cycles in prices. We’re not predicting an up or down,” Goldberg told CNBC.

“As we go through our longer-term plans, we use a $1,200 gold price and we’re really focused on returns and making sure that any project, any business” can justify going forward. …

… For the remainder of the report:

https://www.cnbc.com/2019/01/16/newmont-says-goldcorp-deal-designed-to-s…

* * *

…

END

A good history lesson today as Konig describes the affinity to gold for early Californians

(courtesy JPKonig/GATA)

J.P. Koning: How California stayed with gold when the rest of the U.S. adopted fiat money

Submitted by cpowell on Thu, 2019-01-17 02:15. Section: Daily Dispatches

9:15p ET Wednesday, January 16, 2019

Dear Friend of GATA and Gold:

Bullion Star’s J.P. Koning tonight reviews early California’s attachment to gold as money and its rejection of the U.S. national government’s fiat currency “greenbacks” during the Civil War. Koning concludes that the primary determinant of currency use is whatever most people are using, even if the majority’s currency is steadily devaluing.

Koning’s analysis is headlined “How California Stayed with Gold When the Rest of the U.S. Adopted Fiat Money” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/jp-koning/how-california-stayed-with-g…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

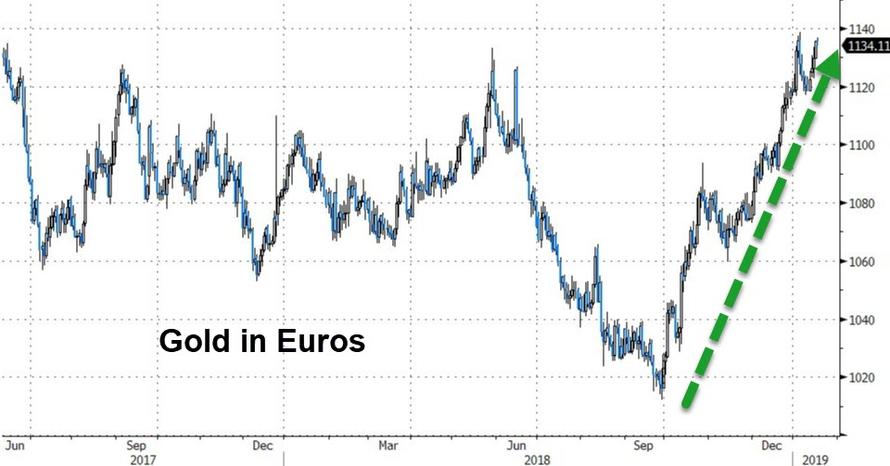

Euro-Gold Ratio Is A Canary In The Monetary Coalmine

For weeks I’ve been telling my subscribers that something changed in the gold market. Since Donald Trump’s election there was a pretty clear pair trade between the U.S. dollar and gold.

And that trade was most manifested in the price of gold in euros.

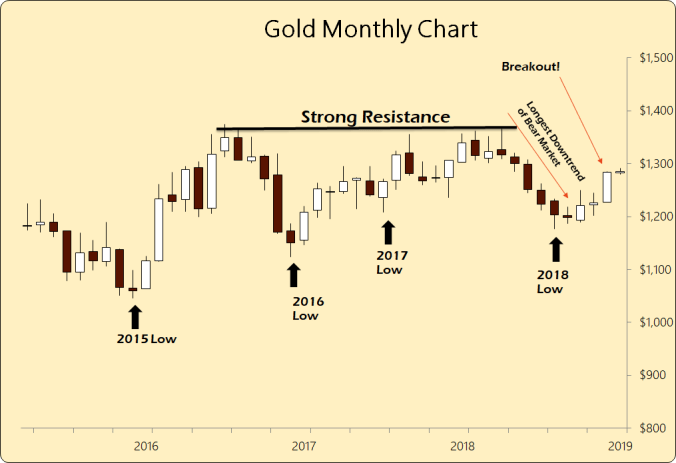

During last summer gold experienced its worse (in terms of time) downtrend of the seven-year bear market.

But since bottoming in October it has rallied, albeit weakly. It is still mired in that bear market, gamely trying to push through the $1300 barrier. The important zone is the $1365-75 post-Brexit vote area.

And with Brexit very much up in the air at this point, despite the best efforts to project otherwise by The Davos Crowd and their political/media quislings, gold’s relative weakness is a real worry for long-suffering gold bulls.

While the currently monthly chart is a mildly-bullish uptrend, and has been since December 2015, it is a counter-trend withing a broader bear market that has not finished.

But, we know all this. Nothing about gold has been interesting for months. Newmont Minng (NYSE:NEM) and Goldcorp (NYSE:GG) announced a huge merger the other day, funds are scrubbing gold from both their names and their portfolios, investors have lost all interest.

That is because the real story is not what’s happening in the U.S., and consequently the dollar, it is Europe.

And this is reflected in the euro.

As I said at the beginning, the election of Donald Trump created a very strong pair trade between the euro and gold. Since the October bottom, however, that trade is breaking down.

Look at the strength of the move by gold in euros since the October low. This is now challenging the 2018 high — a triple top breakdown — and hinting at a push towards €1200.

This is a far more bullish move than we saw in dollars. And it says that the breakdown in gold last summer may very well be the false move to get everyone on the wrong side of the trade.

New bull or bear markets happen only when a significant majority of actors are betting with the current trend which has played out. Once everyone is a bull there are no more buyers and vice versa.

It also screams that investors are now looking at gold as a safe-haven play again and it is not purely trading as a currency pair. There is a new dynamic at play that hasn’t been there, frankly, since the run up to Brexit.

Moreover, it has been plainly obvious watching the day-to-day trading of both gold and the euro that there is a concerted effort to manage this price level.

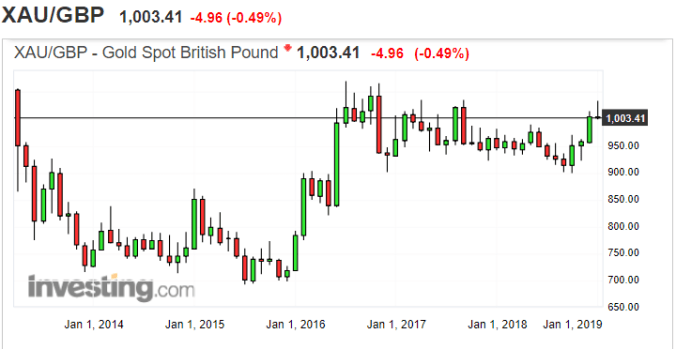

Gold isn’t breaking out in Japanese Yen or Swiss Francs, at this point only the euro and the British pound.

So despite the Project Fear mongers, gold is making the right noises about where things are heading. Gold’s primary role is as a check on the public’s confidence of political institutions.

A secular bull market only happens when Gold is rising against every government currency. Given the importance of the EU to the global trade and financial status quo a breakdown there politically has the potential to turn a localized bull market into a secular one.

end

An email from Nicholas B to Bill Murphy and myself: an excellent analogy to gold/silver

Building Sand

Good Morning Bill/Harvey,

The availability and supply of quality building sand will soon become a headline issue: building sand is a very thick, heavy, wet sand, and the dredging of sea and river beds in respect of its procurement is creating even more ecological problems. On the other hand, surface desert sand has been refined and thinned by millennia of exposure to the elements and is quite useless, although its supply is theoretically almost infinite. Imagine an off -the- scale powerful cabal, in an attempt to control the price of building sand constructed a futures market for 99% of the trade in all types of sand, but the market was styled as merely a market for generic sand. Prices were perpetually suppressed by short sellers providing an infinite supply of desert sand contracts and the market made no distinction between these vaporous, useless promises and the true ability to supply real building sand. One day a powerful building contractor instituted a market for price discovery in respect of building sand only and participants had to prove that any sell side contract was backed by immediately deliverable inventory. The headline price of building sand consequently climbed 50 fold in the next few months. It was then also realized that the market for generic sand was ,in fact, only a market for desert sand and was therefore totally discredited and immediately became irrelevant.

If you are currently fretting because the COT report is not produced during this shutdown period, ask why you are troubled. Do you believe that you have the ability to examine this COT data for a previous Tuesday but only released to you on Friday (whilst the cabal has real time access to all data-including where every single stop order is positioned) and that somehow you will have the skills to front run the forthcoming inevitable wash and rinse cycle. Wake up and prepare for the inevitable re entry of physical gold into the monetary system, when every one rapturously understands the distinction between physical gold and undeliverable paper promises backed by absolutely nothing at all..

Regards

Nicholas

end

Russia’s gold & foreign currency reserves surge for third consecutive year

Published time: 16 Jan, 2019 11:08

The Central Bank of Russia reports that foreign exchange reserves saw a significant boost of 8.3 percent over the 12 months through January 1 of the current year.

Reserves reportedly grew to over $468 billion from $432 billion at the beginning of last January. According to the regulator, reserves grew for the third consecutive year. In 2017, growth totaled $55 billion, while 2016 saw an increase of $9.3 billion.

The value of gold in the reserves increased by nearly five percent to $86.9 billion in December, with the share of the precious metal surging to 18.5 percent. Last year, saw the value of gold in Russia’s reserves grow by over $10 billion, marking an increase of 13 percent.

The aggregate value of the national reserves grew by 0.6 percent to $381 billion in December, and showed an increase of 7.2 percent last year.

Russia’s growing reserves in the last three years seem to point to an adjustment to economic sanctions imposed by the US and the European Union in 2014. Western penalties had a significant initial impact on Russia’s reserves, which saw a decrease of $124 billion in 2014 and a $17 billion contraction the following year.

Russia’s international reserves are highly liquid foreign assets comprising stocks of monetary gold, foreign currencies and Special Drawing Right (SDR) assets, which are at the disposal of the Central Bank of Russia and the government.

Earlier this month, Russia’s central bank reported that it cut the share of the US dollar in the country’s foreign reserves to a historic low, transferring nearly $100 billion into the euro, the Japanese yen and the Chinese yuan. The step came as a part of a broader state policy on eliminating a reliance on the greenback.

-END-

Palladium hit $1400.00 per oz on supply problems. The demand for Palladium rose to 8.5 million oz with production at 7.5 million oz. Thus above ground palladium must be used to satisfy demand. Very shortly will be Platinum use in cars increase because of the lack of Palladium.

two commentaries

Scrap register and Bloomberg

Long-term outlook remains strong for Palladium

NEW YORK (Scrap Register): Metals Focus looks for palladium to remain strong in the long term although it may be due for a profit-taking pullback after hitting recent record highs.

Analysts reported that palladium demand for automotive catalysts has risen from 5.8 million ounces in 2010 to an estimated 8.5 million last year.

“Coupled with constrained mine production growth, this has resulted in palladium demand outpacing global supply over much of this decade,” the consultancy said, noting that last year’s supply/demand deficit was an estimated 1.1 million ounces, meaning above-ground stocks have been falling.

“Looking ahead, we believe palladium’s fundamentals remain strong,” Metals Focus said.

In the short-term, however, some profit-taking seems likely. This could be triggered by further indications of a global economic slowdown or bad news from the auto industry. A further loosening of the leasing market could also contribute to such a move.

Still, Metals Focus added, any correction lower in prices is likely to be short-lived and treated as a buying opportunity. Overall, therefore, following a brief price downturn, we forecast further upside for palladium later this year, Metals Focus added.

Indeed, we believe that this trend will continue into 2020 and beyond, as persistent deficits push the palladium price through new record highs, the firm added.

-END-

Palladium Reaches Another Record as JPMorgan Sees More Upside

Bloomberg

January 17, 2019, 5:48 AM CST Updated on January 17, 2019, 10:10 AM CST

Near-term supply shortage has driven metal to fresh highs

Price in uncharted territory, led by technicals: JPMorgan

Palladium held gains after rocketing through $1,400 an ounce for the first time, extending its gravity-defying rally even amid signs that global vehicle sales are slowing.

The precious metal, primarily used in the auto industry for catalytic converters, has surged more than 65 percent since the middle of August. The bull run has been driven by an acute shortage of immediate supply as car manufacturers scramble to get ahold of the metal to meet more stringent emission controls.

-END-

Sam Zell is the real estate king on Wall Street. He has never bought any gold in his 77 year old life. His gives his reasons why he is buying gold.

(courtesy zerohedge)/Sam Zell

Billionaire Investor Sam Zell Says He’s Buying Gold “For The First Time In My Life”

Amid a cresting wave of consolidation in the gold mining space as spending on new mines has dried up since 2011, billionaire investor Sam Zell is buying the shiny metal “for the first time in his life” because he sees opportunities stemming from an expected shortage in supply.

https://www.bloomberg.com/multimedia/api/embed/iframe?id=1733008a-ecd9-4e73-8654-73a51ce30c2f

Gold notably didn’t perform as well as many might have expected during the eruption of market volatility during Q4, but some investors see scope for the shiny metal to embark on its strongest rally since the crisis after years of lackluster returns as global economic growth slows and investors look for somewhere to hide.

That, and the impending supply crunch that Zell envisions from the drop in new mining capacity – the capacity of unmined gold still buried in existing mines shrank by 40% in 2017 – are the two reasons why Zell has been buying.

“For the first time in my life, I bought gold because it is a good hedge,” Sam Zell, the founder of Equity Group Investments, said in a Bloomberg TV interview. “Supply is shrinking and that is going to have a positive impact on the price.”

“The amount of capital being put into new gold mines is a most nonexistent,” Zell said. “All of the money is being used to buy up rivals.”

And though official rate of inflation has started to decelerate once again in recent months, signs that the actual rate of inflation in the underlying economy is higher than it might appear could also be a positive for the shiny metal.

end

–

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7709/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7895 /shanghai bourse CLOSED DOWN 10.79 PTS OR 0.42%

HANG SANG CLOSED DOWN 146.47 POINTS OR 0.54%

2. Nikkei closed DOWN 40.48 POINTS OR .20%

3. Europe stocks OPENED ALL RED

/USA dollar index FALLS TO 98.02/Euro FALLS TO 1.1401

3b Japan 10 year bond yield: FALLS TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.74/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.28 and Brent: 60.21

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.22%/Italian 10 yr bond yield DOWN to 2.73% /SPAIN 10 YR BOND YIELD DOWN TO 1.35%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.51: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.22

3k Gold at $1292.55 silver at:15.53 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 22/100 in roubles/dollar) 66.51

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.74 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9922 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1312 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

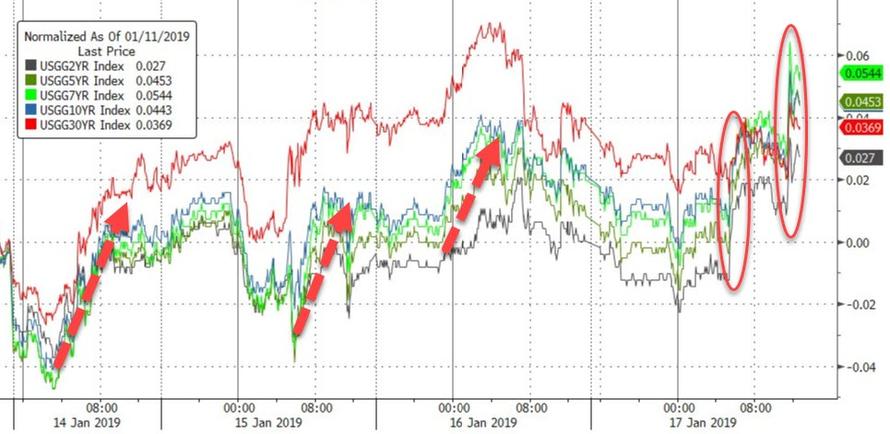

4. USA 10 year treasury bond at 2.71% early this morning. Thirty year rate at 3.06%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3706

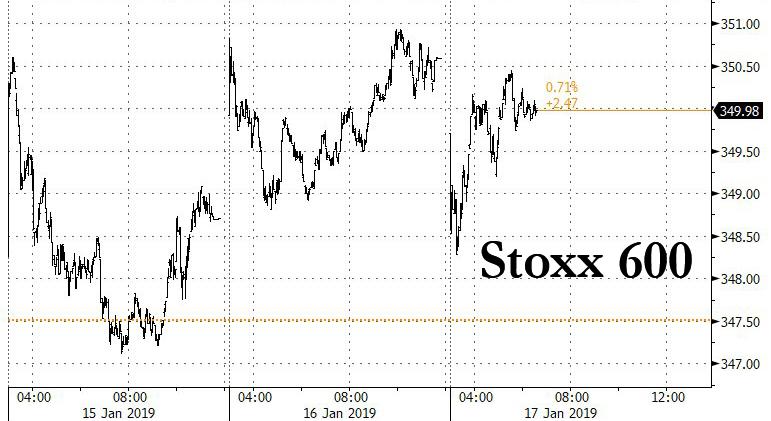

US Futures, European Stocks Slide As Trade Fears Return

US equity futures and European markets fell after a mixed session in Asia as a better than expected start to earnings season was overshadowed by resurfacing trade tensions between the U.S. and China amid a federal investigation into Huawei Technologies for allegedly stealing trade secrets, as fears about profits and global economic headwinds returned on news Apple plans to cut back hiring for some divisions while Singapore exports unexpectedly fell. Treasuries and the dollar were mixed.

Europe’s Stoxx 600 Index was down 0.2%, dragged lower by autos and leisure stocks, although defensive food and drink stocks rebound from Wednesday’s drop. After being the top performing sector Wednesday, the Stoxx 600 Bank Index declined 1.5% in early trading, making it the worst performing industry group in Europe on the day, and erasing nearly half of Wednesday’s gain after French bank Societe Generale warned it now sees a 20% trading revenue drop on challenging markets, dragging its stock as much as 4% lower. The Stoxx 600 Automobiles & Parts index slumped, hitting Germany’s auto and export-heavy DAX, after Senate Finance Committee Chairman Chuck Grassley said President Donald Trump was inclined to impose tariffs on European cars to win better terms on agriculture.

“There is some focus on the Grassley comments in relation to auto trade tariffs and also reference to there not being much progress in the U.S. China negotiations last week,” said Bank of Tokyo Mitsubishi strategist Derek Halpenny. “There has obviously there has been a lot of optimism (in markets) since the start of the year and risk appetite has had a pretty good run, but this will place a few question marks over that.”

In the UK, the FTSE 100 Index underperformed despite a stable pound, as Prime Minister Theresa May began talks with her political rivals to try deliver a Brexit deal.

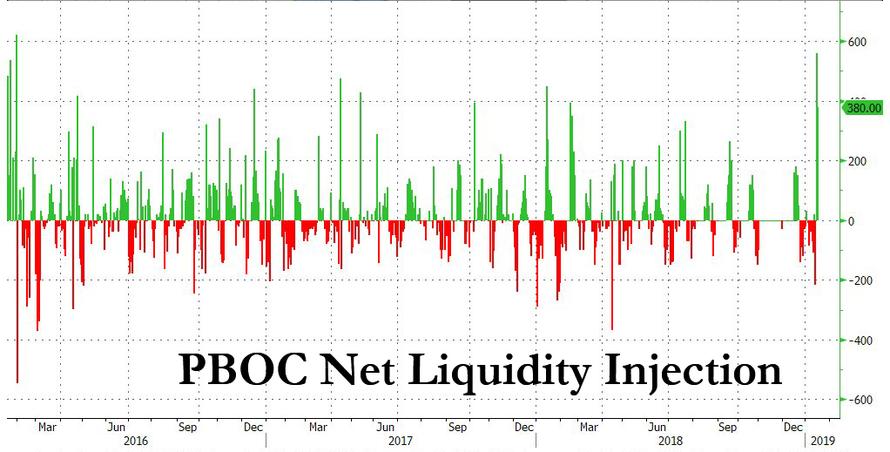

Fresh news was thin as European trading got underway, but traders had more than enough to digest from last 24 hours to follow Asia’s overnight dip into the red. China’s blue-chip index ended down 0.55%, led lower by a decline in the country’s second-largest home appliances maker, Gree Electric, after it warned of slower profit growth as the economy loses steam. Chinese Premier Li Keqiang promised increased government investment this year and the country’s central bank injected more cash into the financial system, bringing the amount for the week to 1.14 trillion yuan ($168.74 billion).

Shares in Hong Kong tumbled, and some companies dropped more than 75 percent without obvious explanations.

Stoking some caution was news that U.S. lawmakers introduced bills on Wednesday that would ban the sale of U.S. chips or other components to Huawei or other Chinese telecommunications companies that violate U.S. sanctions or export control laws. That came shortly before the Wall Street Journal reported federal prosecutors were investigating allegations that Huawei stole trade secrets from U.S. businesses. Separately, Handelsblatt reported the German government is actively considering stricter security requirements and other ways to exclude Huawei from a buildout of fifth-generation (5G) mobile networks.

Also lurking were worries that the U.S. government shutdown – now in its record 27th day – was starting to take a toll on its economy. White House economic adviser Kevin Hassett said the shutdown would shave 0.13% off quarterly economic growth for each week it goes on.

A better-than-expected start to the earnings season has so far not been enough to spur an extended rally, and on Thursday S&P futures were down 0.3%, the sames as Dow futures while Nasdaq fuitures were 0.4% lower. The VIX was trading 1.5% higher.

As Bloomberg writes this morning, risk assets are showing fresh signs of fatigue after a stronger start to 2019 than 2018’s (and the January meltup), when optimism about trade tensions and central bank support overshadowed a litany of concerns as the global economy slowed. Now with both the U.S. government shutdown and Brexit impasse dragging on, and lingering stress between America and China, there are plenty of reasons for caution.

Over in Brexit-land, as expected, British Prime Minister Theresa May narrowly won a confidence vote overnight and invited other party leaders for talks to try to break the impasse on a Brexit agreement. An outline for Plan B is due by next Monday. Markets assume the exit date will be extended past March 29.

“Nothing has happened in the last 24 hours to dissuade us from the view that we are headed in the direction of an Article 50 delay, a softer Brexit or no Brexit,” said Ray Attrill, head of FX strategy at NAB. This left the pound steady at $1.2872, though still short of Monday’s peak at $1.2929. It reached a seven-week low against the euro before steadying at 88.50 pence

UK PM May said there is now an opportunity to find a way forward on the Brexit and that she intends to deliver on Brexit which she believes it is her duty to do so. PM May also said we must work out what lawmakers want and that she spoke to several parties although the Labour party leader has yet to take part in discussions, while there were comments from Labour Party leader Corbyn who declared there will be no talks with PM May until a no-deal Brexit is off the table.

BBC’s Political Correspondent Nick Eardley tweets “Tory sources predict majority of Conservatives in Commons would refuse to back permanent customs union and several ministers would quit.” Subsequently reported that the EU are to condition any potential delay to Brexit on an agreement being struck between UK PM May and opposition leader Corbyn, according to El Pais.

In central bank news, Fed’s Kashkari (Non-Voter, Dove) said Fed has less room to cut rates in future downturn but has other tools, while he repeated that he wants to see wage growth and inflation before backing a rate hike.

In the ongoing shutdown drama, President Trump signed bill to give Federal workers back pay from the shutdown, while there was also reports that the White House threatened to veto the stopgap bill the House is preparing, while US Senate Finance Committee Chairman Grassley said Trump administration’s trade negotiations may be delayed due to government shutdown.

In currencies, the U.S. dollar was mixed, easing against the yen to 108.79 but flat versus the euro at $1.1396. The dollar index was up at 96.088. The yen led G10 gains following a U.S. probe into China’s Huawei and as equities and emerging-market currencies drifted lower. The dollar rose on supportive early London flows yet lost steam as the session progressed and the euro and sterling eventually erased modest losses. Commodity currencies were under pressure as risk sentiment waned, with Treasuries edging up and oil lower.

In commodities, oil traded lower, with U.S. crude remaining close to $52 a barrel as traders worried about the strength of demand in the United States after its gasoline stockpiles grew last week more than analysts had expected. Brent (-1.0%) and WTI (-1.2%) prices hover under $61/bbl and $52/bbl respectively, weighed on by the record EIA US crude production figure of 11.9mln BPD for the previous week, an increase from the prior of 11.7mln BPD; a level which was already the largest national output globally. Elsewhere, it has been reported that Russian Energy Minister Novak and Saudi Energy Minister Al Falih are to meet at next weeks Davos summit. Separately, Libyan oil ports Es Sider, Zueitina and Hariga have reportedly reopened following weather improvements. Palladium hit record highs thanks to increasing demand and lower supply. Spot gold was little changed at $1,294.91 per ounce.

The publication of housing starts and building permits is postponed because of the government shutdown. U.S. initial jobless claims are expected to be little changed against last week, while the Philadelphia Fed Business Outlook and the Bloomberg Consumer Comfort will be watched.

Morgan Stanley, PPG Industries and Fastenal are among companies reporting earnings before the market opens, while Netflix and American Express will report after the close.

Markets Snapshot

- S&P 500 futures down 0.4% to 2,604.00

- STOXX Europe 600 down 0.2% to 349.81

- MXAP up 0.06% to 152.46

- MXAPJ down 0.1% to 494.41

- Nikkei down 0.2% to 20,402.27

- Topix up 0.4% to 1,543.20

- Hang Seng Index down 0.5% to 26,755.63

- Shanghai Composite down 0.4% to 2,559.64

- Sensex up 0.3% to 36,415.78

- Australia S&P/ASX 200 up 0.3% to 5,850.05

- Kospi up 0.05% to 2,107.06

- German 10Y yield rose 0.3 bps to 0.227%

- Euro up 0.07% to $1.1400

- Italian 10Y yield fell 11.7 bps to 2.396%

- Spanish 10Y yield fell 1.4 bps to 1.361%

- Brent futures down 0.7% to $60.92/bbl

- Gold spot little changed at $1,293.94

- U.S. Dollar Index little changed at 96.10

Asian equity markets were choppy throughout the session but eventually followed suit to the gains on Wall St, where financials led after strong earnings from banking powerhouses Goldman Sachs and Bank of America. ASX 200 (+0.3%) and Nikkei 225 (-0.2%) were mixed as resilience in financials and commodity-related sectors kept the Australian benchmark afloat, while Tokyo trade was hampered again by currency effects. Hang Seng (-0.5%) briefly surmounted the 27,000 level for the first time since early December where it then met resistance and Shanghai Comp. (-0.4%) swung between gains and losses as participants digested another substantial liquidity operation by the PBoC, as well as US-China concerns after reports that US prosecutors are to pursue criminal charges against Huawei over theft of trade secrets. Finally, 10yr JGB futures recovered from the prior day’s lows but with price action kept range-bound on the session alongside the indecisive risk tone in the region and a relatively tepid Rinban announcement by the BoJ.

Top Asian News

- China Confirms Vice Premier Liu to Attend Trade Talks in U.S.

- China’s Coffee Unicorn Is Burning Millions to Overtake Starbucks

- Debt-Laden Indian Airline Jet Working With Banks on Bailout Plan

- Erdogan Gets Emergency Powers to Use If Turkish Economy at Risk

- Time to Sell Rally in Developed Market Stocks: Credit Suisse

Major European equities (ex-SMI) are mostly in the red, albeit off worst levels [Euro Stoxx 50 -0.3%]. The DAX (-0.3%) is the underperforming index weighed on by the poor performance in the auto sector (-0.9%), following US Senate Finance Committee Chairman Grassley commenting that he believes US President Trump is inclined to impose new US auto tariffs; with Daimler (-1.4%), Volkswagen (-1.4%) and BMW (-0.6%) in the red as a result. Sectors are broadly in the red, with financials underperforming due to Societe Generale (-4.0%) being firmly in the red after stating that Q4 2018 was impacted by disposals. Other notable movers include Sage Group (+5.7%) towards the top of the Stoxx 600 after the Co reiterated their full year 2019 guidance. Elsewhere, ITV (-6.8%) and Voestalpine (-6.2%) are at the bottom of the Stoxx 600 following a broker downgrade and profit warning respectively.

Top European News

- Alstom Warns Siemens Rail Deal Could Be Blocked by Europe

- Italy’s League Said to Seek Far-Right Ally to Box In Five Star

- U.K. Nuclear Plans Ditched as Hitachi Sees $2.8 Billion Charge

- Primark Owner Gains After Holiday Rebound From Tough November

In FX, it has been a choppy day for the Dollar as the index fluctuated in a range of 96.021-250 with upside triggered by rising tensions between US and China regarding Huawei. In terms of the latest, US prosecutors are to pursue criminal charges against the company over trade secret theft, while separate reports noted that US lawmakers are looking to pass a bill which bans chip sales to Huawei and ZTE. In response, the Chinese Foreign ministry urged US lawmakers to stop this bill. On the technical front the index sits just above its 100 DMA at 96.045 ahead of its 50 DMA at 96.639, just below the 2019 peak at 96.960.

- JPY– The Yen firmer on the back of safe-haven demand amid the aforementioned Huawei-related US-Sino tensions. USD/JPY retreats further below the recently-claimed 109.00 level to a low of 108.72 as the pair is underpinned by its 50 HMA around the intraday low. In terms of option expiries, nothing major to report today, however tomorrow sees some USD 3bln between 109.00-10.

- EUR – The Euro was largely unreactive to the in-line December inflation figures as the single currency continues to move in tandem with the Dollar, thus EUR/USD has experienced a relatively choppy session in the range of 1.1372-1.1404 ahead of comments from ECB-hawk Lautenschlager who is due to speak in Dublin at 1100GMT following a recently published interview in which she said she will wait for the March projections before changing her view about a rate hike this year. In terms of option expiries, tomorrow sees 4bln scattered between 1.1400-25.

- GBP – Sideways action following PM May’s victory at last night’s Labour-tabled vote of no confidence in which the Premier defeated the motion via 325 vs 306 votes, as expected. Sterling sold off with Cable re-testing 1.2700 to the downside in the run up to the results before spiking higher to levels just shy of 1.2900 upon the announcement. In terms of the latest, Spanish press reported that the EU are to condition any potential delay to Brexit on an agreement being struck between UK PM May and opposition leader Corbyn, though Sterling was unreactive to this as Corbyn already made it clear that he will not hold talks with the Premier until a no-deal Brexit is off the table. GBP/USD action is largely dominated by Dollar fluctuation as the pair remains choppy sub-1.2900 and below its 100 DMA at 1.2893.

In commodities, Brent (-1.0%) and WTI (-1.2%) prices hover under USD 61/bbl and USD 52/bbl respectively, weighed on by the record EIA US crude production figure of 11.9mln BPD for the previous week, an increase from the prior of 11.7mln BPD; a level which was already the largest national output globally. Elsewhere, it has been reported that Russian Energy Minister Novak and Saudi Energy Minister Al Falih are to meet at next weeks Davos summit. Separately, Libyan oil ports Es Sider, Zueitina and Hariga have reportedly reopened following weather improvements. Gold has traded within a narrow USD 4/oz range, as the dollar has also traded largely unchanged due to a lack of catalysts. Elsewhere, the US Senate voted to reject legislation to keep sanctions on companies linked to Oleg Deripaska, including Rusal. Separately, steel company Voestalpine have issued their second profit warning in 4 months; citing US plant operating problems and cartel investigation provisions as the cause. OPEC monthly report: OPEC crude production fell 751k bpd in December to average 31.58mln bpd, according to secondary sources with cuts led by Saudi Arabia, Libya.

Looking at the day ahead, we get more housing market data with December housing starts and building permits numbers although these will likely be delayed due to the govt shutdown. There should also be some focus on the Philly Fed business outlook print in light of the weak empire manufacturing reading earlier this week, while the other data due is the latest weekly initial jobless claims reading. It’s worth noting that Japan’s December CPI reading is also due out late this evening. Away from all that the ECB’s Lautenschlaeger is due to speak this morning in Dublin while the Fed’s Quarles speaks this afternoon at an insurance forum. Meanwhile the OPEC monthly report is due out while earnings wise it’s the turn of Netflix and Morgan Stanley today.

US Event Calendar

- NOTE: Housing starts/bldg permits data postponed by govt shutdown

- 8:30am: Philadelphia Fed Business Outlook, est. 9.5, prior 9.4

- 8:30am: Initial Jobless Claims, est. 220,000, prior 216,000

- 8:30am: Continuing Claims, est. 1.73m, prior 1.72m

DB’s Jim Reid concludes the overnight wrap

Watching the House of Commons over the last 48 hours has been a good appetiser for the final series of Game of Thrones out this April. Well we haven’t had dragons…….. yet! It seems that the new series is out on April 14th and I move in to my new house supposedly (builder permitting) on April 22nd. Given that the size and quality differential between the TV in my temporary rental accommodation and my new house is substantial I will likely be going off the grid and away from civilisation for 8 or 9 days from mid April to avoid spoiler alerts before I move in and watch two episodes back to back.

I wonder what difference going off the grid for 8 or 9 days now would mean in terms of progress on Brexit when you returned. Now PM May has won her confidence vote by 325-306 (ironically by a ratio of 52:48), things have to move fast to ensure she reports back to the house by Monday (as required) on the next steps. In her post-vote remarks, she continued her pivot toward a softer Brexit, saying “we must find solutions that are negotiable and command sufficient support in this House.” She said she planned to begin talks immediately with senior parliamentarians and leaders of all parties, which was encouragingly conciliatory. The latter point, indicating she would invite Corbyn and other opposition leaders to contribute was new and positive.

However, Mr. Corbyn and the LibDem’s both indicated that they will not meet unless and until May commits to removing the possibility of a “no-deal” outcome, a move that she has so far refused. In a late televised statement though, PM May said she had met with the LibDem leader already while expressing disappointment that Labour aren’t currently prepared to talk. Pressure is now building on the Labour Party to announce what their strategy is. Previously they have said that if they can’t force a general election then they will pivot towards a second referendum. We will wait and see. Four other opposition parties wrote a letter urging the Labour Party to back the second referendum with the implication that if they didn’t then these parties may not support any further confidence votes called by Labour in the Government. So it’s less likely that Labour can hide behind no firm policy and repeated try to bring the government down. Elsewhere the SNP’s Ian Blackford committed to working with May, but did reiterate their call for a “people’s vote” to be on the table. Finally, the DUP’s Nigel Dodds (whose 10 votes effectively provided May her majority in the confidence vote) called for the UK to leave the EU as one country, in a possible move to resist any regulatory divergence between Northern Ireland and the rest of the UK.

DB’s strategists still think the direction of travel is unequivocally toward a soft Brexit and a stronger pound. For them to be right, someone has to back down though and while I personally think there would be a cross party majority for staying in the customs union such a move could split the Conservative Party and as such be a poisoned chalice to them. What will Mrs May see as the priority? Keeping her party from the risks of a damaging split or trying to find a deal? The next stage of negotiations really feels like one ginormous game of “whac-a-mole”.

The pound was directionless yesterday (and this morning), bouncing around the $1.2870 level all day ahead of the vote, and ultimately closing in that region, up +0.14% on the day. The FTSE 100 dipped -0.47%, consistent with the prior rally in sterling after Tuesday’s vote.

The London Times reported late yesterday afternoon that the EU is considering offering a delay of Brexit until 2020. It comes from a credible source but whether it’s realistic is another matter. Many Conservative MPs would probably not be keen on the extension being that long. It wouldn’t do much to focus minds in the short-term and also allow more time to build more and more momentum for a second referendum which creates a more binary outcome and uncertainties. So interesting (if true) that the EU are prepared to offer a lot of road for the can to be kicked along but not too sure it will be that useful.

Earlier, the EU, via Barnier, confirmed that they would actively engage with a softer Brexit approach on the future relationship while late in the afternoon the Handelsblatt reported that the EU is ready to make further offers on the backstop, but that EU officials want the initiative to come from Ireland. So a lot of noise, some small steps in a positive direction but a long way to go to get this resolved.

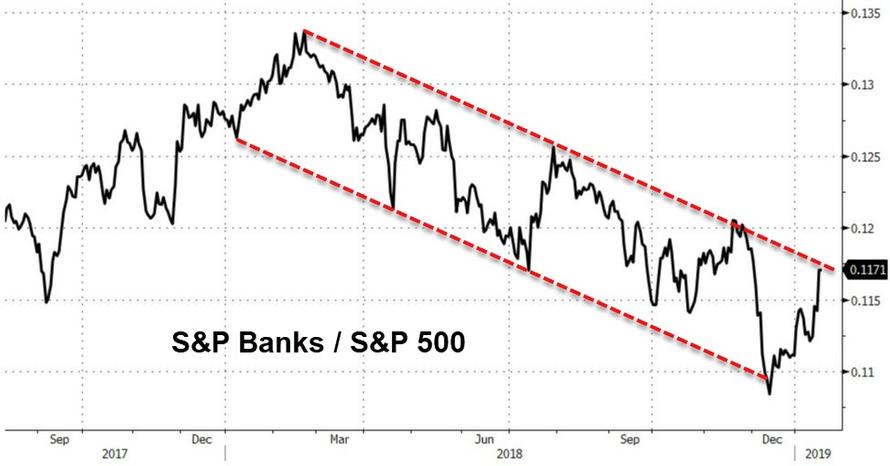

Around all this, risk assets had US bank earnings to thank yesterday as the S&P 500, DOW, and NASDAQ notched up modest gains of +0.21%, +0.59%, and +0.15% respectively with the banks sector of the S&P rallying +2.72% and to the highest since early December. This followed results from Bank of America (+7.16%) and Goldman Sachs (+9.63%). Like what we’ve seen with the other US banks so far, there were much bigger-than-expected revenue declines in FICC trading however the market has instead focused on positive net interest income and investment banking fees, and to the rosier outlooks being painted by management.

Just before US markets closed, the Wall Street Journal reported that US federal prosecutors are close to indicting Chinese tech firm Huawei for allegedly stealing trade secrets from US businesses. The move could exacerbate economic tensions between the US and China, and the S&P 500 promptly surrendered half of its gains. Regardless, this year still ranks as the 10th best start to a year ever for the S&P 500 (out of the 92 years we have daily data) with a +4.35% YTD gain. In fact it’s the best start since 1987 based on data through to the 16th of January each year while the NASDAQ (+6.02%) has had its best start since the post-tech crisis rebound of 2003.

Credit also performed well yesterday with US HY cash spreads finishing -7bps tighter. That puts the rally back from the January 3rd wides this year at an impressive -92bps. US IG spreads were 2bps tighter and are now 12bps tighter over the same period while Treasury yields ticked +1.1bps higher to 2.722% and continue to be a bit of a sideshow at the moment. European bond markets weakened slightly as well, with Bund yields +1.8bps, though BTPs rallied -12.0bps. Sentiment around the Italian banking sector improved after Finance Minister Tria told reporters that banks are reducing NPLs in line with their plans, in a rebuke to reporting earlier this week that hinted at potential NPL problems. Italian bank stocks rallied +3.97%, back to flat on the week.

Oil continued its strong run, with WTI crude prices rising +0.48% for their 11th gain over the last 13 sessions, the best stretch since October 2017. US inventories data showed a 2.68million barrel draw in US stockpiles, though gasoline inventories continued to build. Saudi Arabia reportedly cut its crude shipments to US refineries, which could reflect either a reduction in Saudi supply or reduced demand from US refiners given the large stockpiles of refined products. Overall, the data did not give a clear signal on where prices are heading, though our strategists target further gains over the medium term.

Overnight in Asia markets are largely up with the Shanghai Comp (+0.46%) and Hang Seng (+0.37%) reversing early losses and leading the gains likely on overnight news that China is speeding up its investment law approval process that would create measures for the administration to protect the intellectual property of foreign investors and protect them from forced transfer of technologies. This is clearly a move towards addressing two of the thorniest issues in the US-China trade talks. The official Xinhua News Agency reported that the National People’s Congress Standing Committee has scheduled a special session for January 29-30 to consider the bill and a personnel reshuffle. Interestingly the closed door gathering will start just a day prior to China’s Vice Premier Liu’s expected travel to the US for trade talks. In the meantime, Kospi (+0.16%) is also up while the Nikkei (-0.09%) is trading flattish after a volatile start to today’s session on a strengthening yen (+0.08%). Elsewhere, futures on S&P 500 are down -0.28% while all the G10 currencies (except the yen) and most Asian currencies are trading weak against the greenback this morning. In commodities, crude oil prices (WTI -0.59% and Brent -0.51%) are heading lower today after the spectacular run described above.

In other news it’s been confirmed that US Secretary of State Pompeo will meet with a senior North Korean official overseeing nuclear talks this Friday with the view that this could lead to a second summit soon. The North Korean representative, Kim Yong Chol, will reportedly bring a new letter for President Trump from Kim Jung Un. In his New Year’s address, the dictator suggested that he may seek a “new path” if talks do not progress, potentially signaling more binary risks moving forward, toward either further reconciliation or a breakdown in discussions.

The Fed released its regular beige book, with anecdotal economic details. The report said that wages grew across skill levels, though the gains remain modest. The economy continues to grow but the report cited some weak spots emerging, and price gains remain “modest to moderate.” Overall, the report is consistent with slowing, but still positive growth, and since inflationary pressures remain muted, it should allow the Fed to maintain its stance of paused rate hikes.

As far as yesterday’s data was concerned, in the US the NAHB housing market index surprised to the upside at 58 versus expectations of 56. That was only the third monthly improvement since 2017, and it at least provides some relief from the recent fall which has seen the index drop from a peak of 74 at the end of 2017. The other data out in the US was the December import price index which fell slightly less than expected at a headline level (-1.0% mom vs. -1.3% expected) and rose a bit more than expected on the core measure (+0.3% mom vs. 0.0% expected). Here in the UK, we got the December inflation data and there was a small upside surprise in the core reading at +1.9% yoy (vs. +1.8% expected). The headline was on the money at +2.1% yoy with the overall message not really changing the narrative from our economists that inflation is slipping faster than expected and should settle below target this year.

To the day ahead now where this morning in Europe we’ll get the final December CPI revisions for the Euro Area (no change from +1.0% yoy expected) along with November construction output data. In the US this afternoon there’s more housing market data due with December housing starts and building permits numbers. There should also be some focus on the Philly Fed business outlook print in light of the weak empire manufacturing reading earlier this week, while the other data due is the latest weekly initial jobless claims reading. It’s worth noting that Japan’s December CPI reading is also due out late this evening. Away from all that the ECB’s Lautenschlaeger is due to speak this morning in Dublin while the Fed’s Quarles speaks this afternoon at an insurance forum. Meanwhile the OPEC monthly report is due out while earnings wise it’s the turn of Netflix and Morgan Stanley today.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 10.79 PTS OR 0.42% //Hang Sang CLOSED DOWN 146.47 POINTS OR 0.54% /The Nikkei closed DOWN 40.48 PTS OR .20%/ Australia’s all ordinaires CLOSED UP 0.27%

/Chinese yuan (ONSHORE) closed DOWN at 6.7709 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 51.28 dollars per barrel for WTI and 60.21 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7709 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7805: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i)CHINA

for three days in a row, China has unleashed massive liquidity: the total sum 1.1 trillion yuan or 162.96 billion dollars worth of stimulation..and that is huge.

(courtesy zerohedge)

China Injects Gargantuan 1.1 Trillion In Liquidity This Week

Following what Bloomberg calculated was a record net reverse repo liquidity injection on Wednesday, when the PBOC injected a whopping 560 billion yuan of liquidity into the financial system via open market operations, the Chinese central bank has done it again and in Thursday’s open market operation, it sold 250BN yuan in 7 Day repos (slightly below yesterday’s record 350BN), and 150BN in 28 Day repos, which net of maturities resulted in a whopping net 380BN yuan ($56.2BN) liquidity injection.

This brings the net liquidity injection this week to a near record 1.14 Trillion yuan (Monday 20BN, Tuesday 180BN, Wednesday 560BN and Thursday 380BN) and the week is not even over yet – should tomorrow’s reverse repo be of similar magnitude, then this week will go down in history as China’s biggest liquidity injection on record.

As yesterday, today’s massive liquidity injection was aimed at “keeping reasonable and sufficient liquidity in banking system as liquidity falls relatively fast during peak season for tax payments,” according to a statement from the PBOC, although why this year should be such a significant outlier, even when factoring in the liquidity needs ahead of the Lunar new year, to prior periods was not exactly clear.

There is, of course, a much simpler explanation: with Chinese economic and trade data turning from bad to worse with every passing day, Beijing’s response is increasingly one of a panicked “spasm”, as Nomura’s Charlie McElligott wrote today when he noted that with regard to the response of Chinese authorities in addressing their economic slowdown and credit crunch, “it had to get worse before it got better”—recently collapsing Chinese data has now clearly forced an escalation of easing-/stimulus-/liquidity- policies, as follows:

- Two days ago in a press conference between the PBoC, the MoF and the NDRC, Beijing announced new tax cuts, fresh measures to stabilize auto consumption and an announcement that authorities are supportive of increasing issuance of local government “special bonds” to stimulate infrastructure spending were all made in a “stimulus” spasm.

- Overnight Chinese Premier Li has called for more investments in infrastructure and services, while also voicing support for a “stepping-up” of targeted economic controls from authorities.