SORRY FOR MY COMMENTARY BEING SHORT

HAD A POWER FAILURE

GOLD: $1284.60 UP $0.50 (COMEX TO COMEX CLOSINGS)

Silver: $15.37 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1284.60

silver: $15.37

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 7 NOTICE(S) FOR 700 OZ (0.0217 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 551 NOTICES FOR 55100 OZ (1.7138 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 807 for 4,035,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3576: UP 5

Bitcoin: FINAL EVENING TRADE: $3576 UP $1

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 4/7

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,282.500000000 USD

INTENT DATE: 01/22/2019 DELIVERY DATE: 01/24/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 7

661 C JP MORGAN 4

737 C ADVANTAGE 2

____________________________________________________________________________________________

TOTAL: 7 7

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2025 CONTRACTS FROM 190,699 DOWN TO 188,674 WITH YESTERDAY’S 5 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1199 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1199 CONTRACTS. WITH THE TRANSFER OF 1199 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1199 EFP CONTRACTS TRANSLATES INTO 5.995 MILLION OZ ACCOMPANYING:

1.THE 5 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.805 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 31,876 CONTRACTS (FOR 15 TRADING DAYS TOTAL 31,876 CONTRACTS) OR 159.380 MILLION OZ: (AVERAGE PER DAY: 2125 CONTRACTS OR 10.625 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 159.380 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.7% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 159.380 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2025 WITH THE 5 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE OF 1199 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 826 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1199 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2025 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.33 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 13 NOTICE(S) FOR 65,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.805 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 5111 CONTRACTS UP TO 513,509 DESPITE THE LOSS IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $0.85//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8694 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 8694 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 513,509. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,805 CONTRACTS: 5111 OI CONTRACTS INCREASED AT THE COMEX AND 8894 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 13,805 CONTRACTS OR 1,380,500 OZ = 42.93 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A TINY RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $0.85???

YESTERDAY, WE HAD 8815 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 119,138 CONTRACTS OR 11,913,800 OZ OR 370.56 TONNES (15 TRADING DAYS AND THUS AVERAGING: 7888 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAYS IN TONNES: 370.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 370.56/2550 x 100% TONNES = 14.53% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 370.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 5111 WITH THE GAIN IN PRICING ($0,85) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8694 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8694 EFP CONTRACTS ISSUED, WE HAD ANOTHER STRONG GAIN OF 13,805 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8694 CONTRACTS MOVE TO LONDON AND 5111 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 42.93 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $0.85 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 6TH STRAIGHT DAY THAT WE RECORDED STRONG RISES IN OI ON BOTH EXCHANGES!

we had: 7 notice(s) filed upon for 700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.50 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 809.76 TONNES

Inventory rests tonight: 809.76 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS IN PRICE TODAY:

A HUGE CHANGE IN SILVER INVENTORY/

A WITHDRAWAL OF 0.938 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 307.251 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2025 CONTRACTS from 190,699 DOWN TO 188,674 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1199 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1199 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2025 CONTRACTS TO THE 1199 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 826 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 2.425 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.805 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 5 CENT PRICING FALL THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1199 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 1.30 PTS OR 0.05% //Hang Sang CLOSED UP 2.75 POINTS OR 0.01% /The Nikkei closed DOWN 29.19 PTS OR 0.14%/ Australia’s all ordinaires CLOSED DOWN 0.26%

/Chinese yuan (ONSHORE) closed UP at 6.7871 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.38 dollars per barrel for WTI and 62.02 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7871 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA/Sweden

b) REPORT ON JAPAN

USA/Yen rises (yen falls) hits 110 after they report an export slump.

( zerohedge)

3 C/ CHINA

i)CHINA

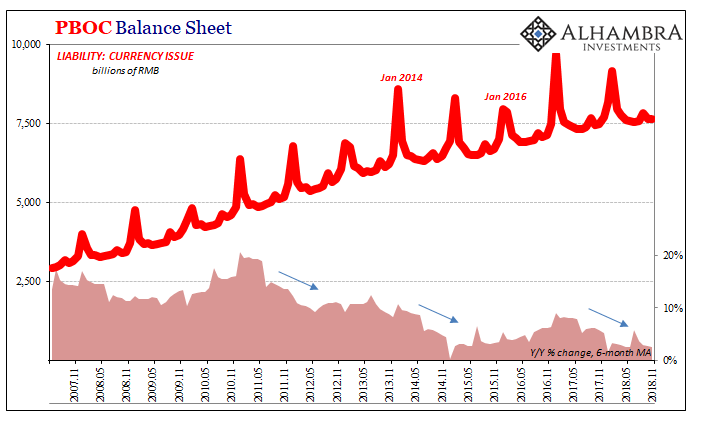

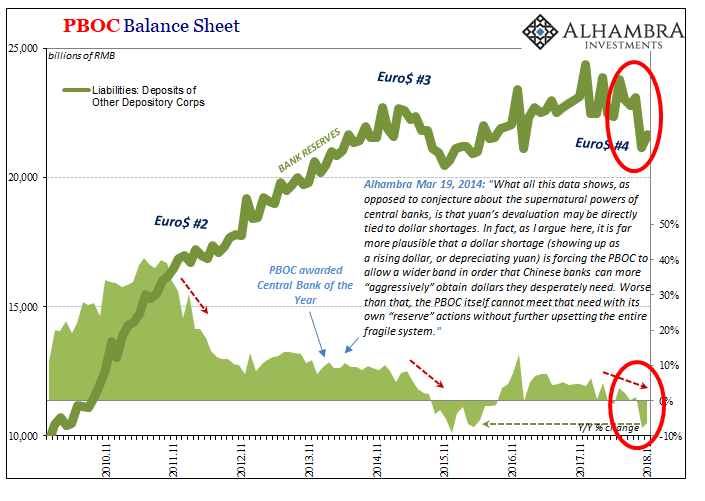

A good commentary from Jeffrey Snider today as he describes the decline of the euro dollar story is reaching its final chapters. Euro dollars is simply uSA dollars held outside of the uSA. Because of the lack of growth in the emerging markets, Asian markets and European markets, we are witnessing a decline in those dollars. The high deficits of Trump is also sucking into the USA vast sums of dollars and that is killing the rest of the globe

( Jeffrey Snider)

4/EUROPEAN AFFAIRS

i)GERMANY/DEUTSCHE BANK

The Fed is now probing Deutsche bank’s role in the money laundering scandal with respect to Estonia’s Danske bank

( zerohedge)

ii)UK

iii)Tom Luongo describes May’s Plan B: calling the remainers bluff

( Tom Luongo)

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

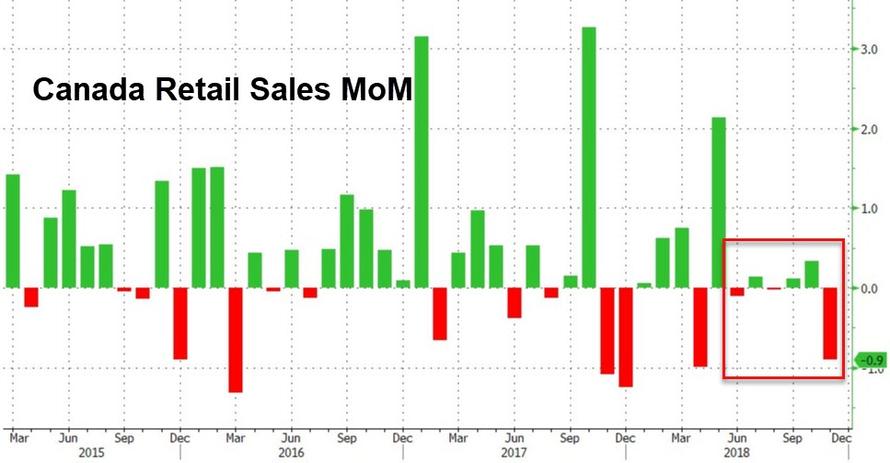

Canada

This is not good for Canada as retail sales tumble .9% month over month. Previous retail sales from August to Oct. were also revised downwards. Canada has joined the rest of the world in a downward spiral

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

iii)Ron Paul on the auditing of the Fed

( Ron Paul)

iv)Now Arizona is proposing securing the state’s financial reserves into gold and silver

( Cortez/GATA)

v)The CEO of the Moscow Stock Exchange wants to replace USA gold with Russian gold

( GATA/RT))

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

Mid morning

Stocks Give Up Early Gains As Dollar Dumps, VIX Jumps

China trade talks stalling, shutdown impasse, and Hassett warning growth could be zero… it seems that ‘bad news’ is bad news again!!

S&P was up 0.8% early – that’s all gone now…

As VIX spiked…

With Nasdaq leading the drop since Friday…

And as stocks sank so did the dollar…

Did anyone else notice that US equity market stopped going up when China stopped adding trillions in liquidity?

ii)Market data/

a)Mish talks about 8 wall prototypes of which none meet operational standards or for that matter, Trump’s cost estimate..and it is far less than thought…

(Mish Shedlock/Mishtalk)

b)The Shutdown is now 31 days and we have now have two missing paycheck periods. It seems that the IRS employees are starting to bail

iv)SWAMP STORIES

a)Buzz Feed actually details documents on the Trump Tower project in Moscow

( zerohedge)

b)Trump is now furious with Giuliani after many botched interview

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI ROSE BY 3 CONTRACTS DOWN TO 449. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 2885 CONTRACTS DOWN TO 138,907 CONTRACTS.

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

i) Into Brinks: 619,094.98 0z

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

I wrote “Crash Alert!” on Dec. 12, a little over a month ago https://www.milesfranklin.com/crash-alert-3/#respondPlease re read this so we don’t have to go over the nuts and bolts here. Since then, we watched equity markets all over the world take a dive into year end where most finished in bear market territory. As the new year started, we have seen equity markets bounce to relieve the vast oversold conditions. I believe the “dead cat” bounce phase has now run its course and the selling will resume shortly and into an outright panic mode.

Over the last month we have learned more regarding the real economies, very little of it good. The most important areas of weakness are trade and real estate volume/price weakness worldwide. Both of these are in confirmed downtrends and both are lynchpins to the financial system. Trade, because it provides “cash flow”, and real estate not only because it is a global asset of “wealth” but more importantly because real estate is COLLATERAL. This last point is very important because “collateral” to the banking (financial) system is now smaller than it was 6+ months ago when it was already too thin. Remember, higher rates had already directly affected bonds (collateral), now real estate is an obvious symptom of weakness and collateral shrinkage.

Back in early December I warned that liquidity was drying up and would culminate in a panic move. This did occur and the response from central banks has been as expected, they blinked. The ECB’s balance sheet shows zero sign of shrinking as promised. The PBOC has lowered the RRR rate earlier in the month and they also pumped the financial system with nearly $100 billion just last week alone. The Fed has also made mention of less or no more rate hikes in dovish fashion. Oddly, we now know publicly that the “plunge protection team” does in fact exist as CNBC and others were applauding. No more conspiracy theory with this one …

So here we are after the bounce and after the oversold pressures have been released. I believe we are now set for the event that will make history, namely a financial train wreck in a very compressed time frame. Why do I see this? Because of the backdrop and where we have come from to where math and logic say we will ultimately go. Think about the “backdrop” for a moment. The world is awash in debt that cannot be paid back which very importantly includes the issuer of the reserve currency, the U.S.. From a timing standpoint, maybe the most important backdrop is on the geo political front. All over the world, the globalists are being pushed back by populists as even former presidents in various nations have recently been arrested and protests by the great unwashed abound.

My point is this, in the real world …the populace has had enough of higher taxes and stagnant/declining living standards while being told everything is great. Though not to their liking, globalists are being routed.

Market psychology has already been cracked, during normal times we would at least retest the lows but these are far from normal times. We do not face a normal bear market where central banks can reflate again. The collateral does not exist for this to happen. Because the gross debt is unpayable and total promises made are impossible to honor, a total reset is in store. Whether this is an overnight (weekend) event or a very compressed 2-4 week event is irrelevant. Asset “values” will be unrecognizable afterward with current eyes. The next 2-4 weeks are very important in my opinion because even in garden variety bear markets, it is the action of the retest or failure of support that matters most. Big changes are afoot!

The above spoke mainly to equity markets because that is what the average person sees and uses for judgement. Credit markets are far more important. I believe we have gotten to the stage where credit markets are actually too big for central banks who have for years acted as the “plunge protection team” of debt. There is just one hitch, when a fractional reserve debt system gets so large, it requires exponentially more new debt to continue which makes a system already too large for central banks …even larger!

Lastly I want to make mention that crashes throughout history have all occurred from oversold levels. I mention this because our next move in equities is downward from the current short term overbought levels and a retest of the lows is in store. You will most likely soon see the markets greatly oversold again and will be told they offer a fabulous buying opportunity. I think not. Rather, I believe the Dec. lows will fail and true fear will set in. “Fear” even by those pulling the strings because they will know they have lost control. I don’t think we will have long to find out if this is the case. The volatility genie is fully out of the bottle, she won’t go back in until the landscape is vastly different …!

This article was held one day for our subscribers and then made public.

Standing watch,

Bill Holter

Holter-Sinclair collaboration

end

–

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7877/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7971 /shanghai bourse CLOSED UP 1.30 PTS OR 0.05%

HANG SANG CLOSED UP 2.75 POINTS OR 0.01%

2. Nikkei closed DOWN 29.19 POINTS OR 0.14%

3. Europe stocks OPENED ALL GREEN

/USA dollar index RISES TO 96.26/Euro FALLS TO 1.1363

3b Japan 10 year bond yield: RISES TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.66/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.38 and Brent: 62.02

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.25%/Italian 10 yr bond yield DOWN to 2.77% /SPAIN 10 YR BOND YIELD DOWN TO 1.33%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.52: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.16

3k Gold at $1285.05 silver at:15.41 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 32/100 in roubles/dollar) 66.18

3m oil into the 53 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.66 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9973 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1332 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.25%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.76% early this morning. Thirty year rate at 3.08%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3067

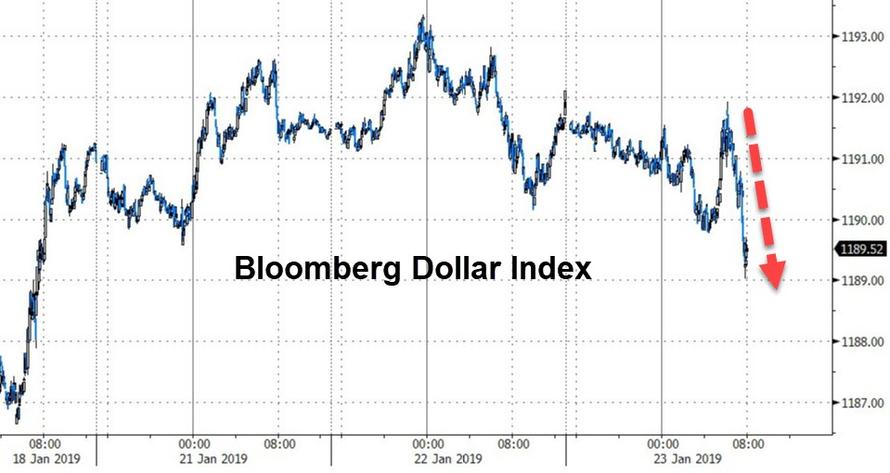

Global Rally Returns As Markets Fade Trade Fears, Dollar Slides

One day after the biggest S&P drop in a month, stocks have regained their composure putting trade and global growth concerns on the backburner, and global stock indices are generally a sea of green this morning.

Trading was initially choppy overnight as hopes of more stimulus measures from China to shore up economic growth clashed with worries over progress between Washington and Beijing to resolve a trade spat between the world’s top two economies. The MSCI world equity index was down 0.1 percent, with Asian equity markets choppy as the region attempted to shrug off the headwinds from the US, where stocks slumped on Tuesday as the risk averse tone and lingering global growth concerns caught up with the major US indices on return from their extended weekend.

The FT reported that the US turned down China’s offer for preparatory trade talks, which was later denied by NEC Director Larry Kudlow helping U.S. equities pare some losses though the fresh concerns about U.S.-China relations kept share prices in check. Early trade jitters pushed the MSCI index of Asia-Pacific shares ex-Japan lower by 0.2%, stalling after climbing to a seven-week high on Monday.

“The main culprit for the risk-off tone this morning is the change in sentiment around U.S.-China trade talks …. That seeped into Asia overnight and Europe this morning,” said Edward Park, deputy chief investment officer at Brooks MacDonald. (Harvey: a big joke)

Australia’s ASX 200 (-0.3%) was subdued with underperformance in the energy sector after crude prices slipped by over 2% and Nikkei 225 (-0.1%) was dampened by disappointing trade data including the sharpest drop in exports since October 2016.

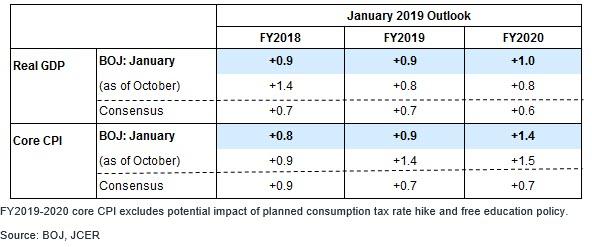

However, sentiment in Tokyo was propped up by a weaker currency after the BOJ cut its inflationary outlook slashing 2019 core CPI from 1.4% to 0.9%, even as it kept its monetary policy, sending the USDJPY to new highs and boosting local stocks while Japan Display shares surged on reports it is in investment discussions with TPK and Silk Road Fund. 10yr JGBs traded sideways throughout most the session amid the indecisive risk tone in stocks and then saw choppy trade in reflection of sentiment in the region and following an unsurprising BoJ decision to keep policy setting unchanged.

Elsewhere, Hang Seng and Shanghai Composite confirmed trader indecisiveness after mixed actions by the PBoC as it conducted a Targeted Medium-term Lending Facility for the first time ever which was at a lower rate than MLF rates and is aimed at spurring lending to small firms, but conversely refrained from reverse repo operations which resulted to a daily drain of CNY 350bln.

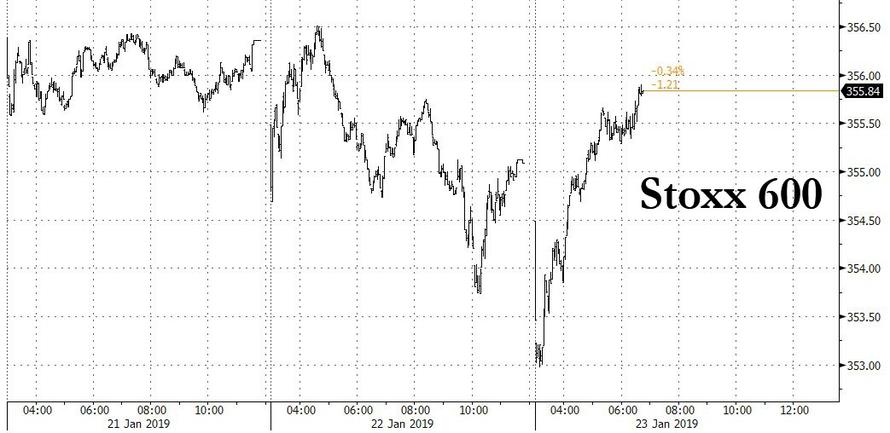

A fresh batch of disappointing corporate updates from European companies further knocked confidence about fourth-quarter earnings, pushing European stocks lower for a third session at the start of trading, with the Stoxx 600 down as much as 0.5%, with bourses all across Europe losing ground as a profit warning by Ingenico sent the French payment group down over 12 percent and hit the whole European tech sector.

However, sentiment reversed sharply just after the open, with most European equities trading mostly higher [Euro Stoxx 50 +0.2%], after recovering from opening losses, taking the lead from Wall Street.

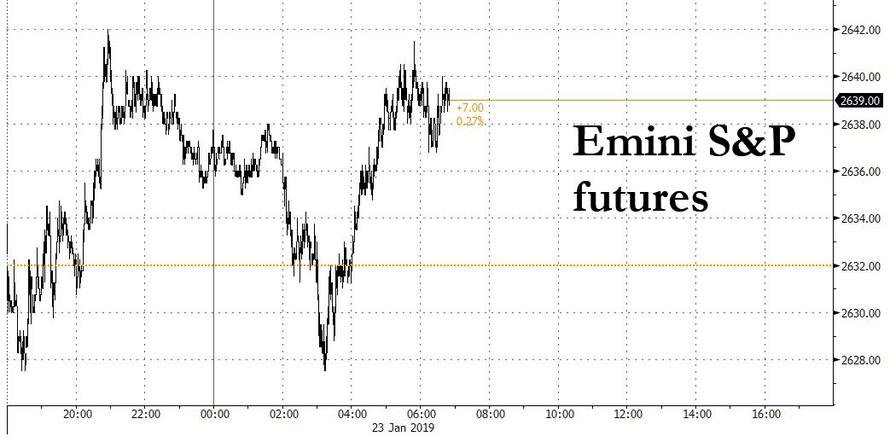

Echoing the rebound in Europe, U.S. futures pointed to a positive start for Wall Street after the S&P 500, Nasdaq and the Dow all posted their biggest one-day percentage drops since Jan. 3 on Tuesday.

Still, despite a modest return of bullish sentiment, the ride ahead will be bumpy: Justin Onuekwusi, a fund manager at Legal & General said central banks’ stimulus unwinding, China’s slowdown, the broader impact of trade wars and populist rhetoric from politicians were all keeping markets on edge. “All these issues have an impact on markets. Every time you have an increase in rhetoric, markets react. It feels like there is a greater political risk premium. The biggest near-term risk is that as you see markets fall, confidence drops and you get people not spending which becomes self-perpetuating. The near-term probability of that has increased.”

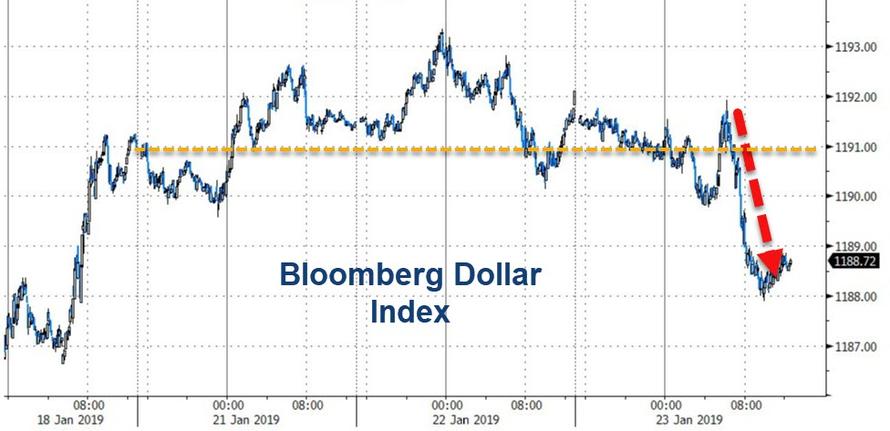

In FX, the U.S. dollar slumped to session lows having trading near a three-week high earlier after the Bank of Japan left monetary policy unchanged as expected, boosting risk appetite and sending the yen lower. The Bloomberg Dollar Spot Index fell for the first time in seven days in a rather muted session in currencies, with short-term positioning dictating price action. The yen weakened as the BOJ lowered its inflation outlook, while the kiwi advanced as consumer-price data beat estimates. Treasuries slipped as oil prices rose, while euro-area bonds were mixed as stocks in Europe and U.S. equity futures rebounded. Sterling rose as the U.K. parliament moved closer to ruling out a no-deal Brexit. The euro was a shade lower at $1.1358 but remained in close reach of a three-week low of $1.1336 set on Tuesday, weighed by recent weakness in the euro zone economy and worries about fallout from Brexit.

In the key central bank event overnight, the BoJ kept monetary policy settings unchanged as expected with NIRP held at -0.1% and 10yr JGB yield target at around 0%. Furthermore, the BoJ extended its lending scheme for 1 year and stated that economic momentum for reaching price goal is sustained but lacking strength, while it added that risks to price and economic outlooks are skewed to the downside. BoJ reduced Real GDP forecasts for FY18 but raised Real GDP forecasts for FY19 and FY20, while it reduced Core CPI forecasts on all years through to FY20. BoJ Governor Kuroda said the downward revision to price outlook is due to the temporary decline in oil prices, Kuroda expects inflation to pick up towards the 2% target. Adding that downside risks from overseas are heightening due to US-China trade friction and European problems.

In the latest Brexit developments, PM May is reportedly set to force ministers to keep a no deal Brexit on the table despite threats of ministerial resignations. This has been seen as a defence mechanism against the Labour Party’s potential support for the Cooper-Boles Brexit delay plan. UK Tory party Brexiteers concerned about prospects of a delay, have suggested they could be won over if UK PM May can get a serious concession from the EU on backstop. Following this, ITV’s Paul Brand tweets “Jacob Rees-Mogg will say in a speech today that the backstop remains “the one absolute obstacle” to backing PM’s deal BUT he’s “encouraged by signs of movement”. Sun’s Steve Hawkes reports “Labour has told second referendum campaigners it is backing the Cooper-Boles Amendment”. Has subsequently been confirmed by a Labour party source, stating it is ‘highly likely’ they will back the amendment.

In commodities, Brent (+0.8%) and WTI (+0.8%) prices have nursed initial losses and moved into positive territory due a turnaround in risk sentiment. Following on from Saudi Energy Minister Al Falih’s withdrawal from the WEF at Davos, Russian Energy Minister Novak has also cancelled his trip; Novak was due to speak on Friday on the Great Energy Race alongside IEA’s Birol. Separately, IEA’s Birol has stated that oil demand will grow by at least 1mln BPD. In terms of forecasting DNB have cut their 2019 Brent forecast to USD 70/bbl vs. Prev. USD 75/bbl. Of note API’s have been rescheduled to today due to Monday’s US market holiday.

Gold has marginally benefitted from the risk sentiment, with the yellow metal trading at the top of it’s narrow USD 4/oz range; currently just under USD 1285/oz. Elsewhere, China’s December scrap metals imports increased to 510k tonnes, their highest figure since May, ahead of China tightening waste imports in 2019.

Expected data include mortgage applications. Abbott, Comcast, P&G, and Ford are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.2% to 2,636.25

- STOXX Europe 600 down 0.05% to 354.91

- MXAP down 0.3% to 152.23

- MXAPJ down 0.1% to 494.65

- Nikkei down 0.1% to 20,593.72

- Topix down 0.6% to 1,547.03

- Hang Seng Index up 0.01% to 27,008.20

- Shanghai Composite up 0.05% to 2,581.00

- Sensex down 0.6% to 36,217.48

- Australia S&P/ASX 200 down 0.3% to 5,843.72

- Kospi up 0.5% to 2,127.78

- German 10Y yield rose 0.3 bps to 0.239%

- Euro down 0.01% to $1.1359

- Italian 10Y yield fell 1.7 bps to 2.383%

- Spanish 10Y yield fell 1.3 bps to 1.321%

- Brent futures up 0.7% to $61.94/bbl

- Gold spot little changed at $1,285.00

- U.S. Dollar Index little changed at 96.36

Top Overnight News from Bloomberg

- The European Union is prepared to hit 20 billion euros ($22.7 billion) of U.S. goods with tariffs should President Donald Trump follow through on a threat to impose duties on EU cars and auto parts, said a senior trade official for the bloc

- The European Commission is pushing the Irish government to lay out its plans for the border in the event of a no-deal Brexit, a person familiar with the matter said

- The U.K. parliament is inching toward a plan to delay Brexit to prevent Britain dropping out of the European Union without a deal, with the opposition Labour Party now increasingly likely to support the proposal

- Debt levels in the U.K. aren’t necessarily a cause for concern, according to Bank of England Deputy Governor Ben Broadbent

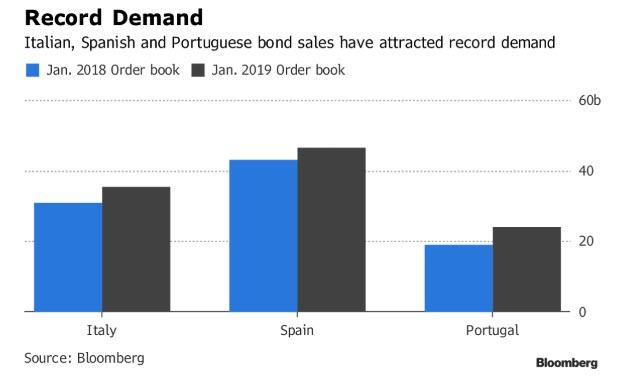

- Investors are seeking record amounts of bonds from Southern Europe, emerging from the sidelines after last year’s political turmoil in Italy. Sovereign bond offerings from Italy, Spain and Portugal this month have all drawn unprecedented bidding for a total of 106 billion euros ($120 billion), up 14 percent from a year ago. That has helped drive a slide in peripheral euro-area yields in the past two weeks

- The chairman of Thailand’s Election Commission says a general election is to be held on March 24

Asian equity markets were choppy as the region attempted to shrug off the headwinds from Wall St, where stocks declined as the risk averse tone and lingering global growth concerns caught up with the major US indices on return from their extended weekend. Furthermore, it was also reported that the US turned down China’s offer for preparatory trade talks, which was later denied by NEC Director Kudlow. Nonetheless, ASX 200 (-0.3%) was subdued with underperformance in the energy sector after crude prices slipped by over 2% and Nikkei 225 (-0.1%) was dampened by disappointing trade data including the sharpest drop in exports since October 2016. However, sentiment in Tokyo was later propped up by a weaker currency, while Japan Display shares surged on reports it is in investment discussions with TPK and Silk Road Fund. Hang Seng (U/C) and Shanghai Comp. (U/C) conformed to the indecisiveness after mixed actions by the PBoC as it conducted a Targeted Medium-term Lending Facility for the first time ever which was at a lower rate than MLF rates and is aimed at spurring lending to small firms, but conversely refrained from reverse repo operations which resulted to a daily drain of CNY 350bln. Finally, 10yr JGBs traded sideways throughout most the session amid the indecisive risk tone in stocks and with participants side-lined prior to the BoJ policy announcement, but then saw choppy trade in reflection of sentiment in the region and following an unsurprising BoJ decision to keep policy setting unchanged.

Top Asian News

- China Meat Giant Surges as Founder Returns After Vanishing

- China Companies Suspected of Buying Own Bonds to Spur Demand

- Thailand to Hold First General Election Since Coup in 2014

- BOJ Leaves Stimulus Unchanged as It Cuts Inflation Outlook Again

- The January Rally Is Waning in Asia Stocks, Just Like Last Year

Major European equities are mostly higher [Euro Stoxx 50 +0.2%], after recovering from opening losses, taking the lead from Wall Street. US stocks were affected by growth concerns, alongside subsequently denied reports that the US turned down an offer by two Chinese vice-ministers to attend preparatory trade talks in the US. Sectors have strengthened somewhat from their negative opening, and are now mixed with underperformance in energy names and outperformance in utilities. Tech names have been underperforming following ASML (-1.8%) cutting Q1 sales guidance, with the likes of STMicroelectronics (-1.4%) down in sympathy. Other notable movers include Carrefour (+6.7%) are at the top of the Stoxx 600 following earnings where they confirmed all targets for their 2022 transformation plan. Separately, RPC Group (+4.6%) are firmly in the green after recommending a final cash offering of GBP 7.82/shr; with Co’s directors seeing the acquisition terms as fair and reasonable. In contrast, at the bottom of the Stoxx 600 are Ingenico (-13.2%) after reporting a FY18 EBITDA miss.

Top European News

- Still Here? Brexit Delay Might Worsen EU’s Election Headache; Fox Warns No-Deal Exit Is ‘Real Possibility’: Brexit Update

- Record Bidding for Southern Europe’s Debt Shows Pent-Up Demand

- Salvini Takes a Swing at Merkel and Forecasts Losses for Macron

- Apollo Seals $4 Billion Deal for Ketchup-to-Lotions Packager RPC

- Patisserie Valerie Collapses as Luke Johnson’s Rescue Fails

In FX, a relatively muted session for the Dollar thus far with the index hovering around the middle of a tight 96.268-378 range after NEC Director Kudlow dismissed reports that US turned down an offer from China for trade talks. The US government shutdown is now rolling onto its 33rd day, although there were reports overnight that US Senate are to vote on two separate bills on Thursday which could potentially bring an end to the shutdown. Meanwhile, BLS stated the January 2019 Employment Situation will be published as scheduled on February 1, 2019, at 1330GMT. ING noted that the 800k workers affected by the shutdown represent only 0.5% of the total US NFP, noting that the impact to the US economy will be modest but noticeable.

- JPY – On the backfoot in early EU trade following the BoJ rate decision in which the Central Bank kept the NIRP at -0.1% and the 10yr JGB yield target around 0% as expected while also reducing inflation forecasts, which was widely touted beforehand. Furthermore, Japan logged the first trade annual deficit in three years, as the cost of energy imports surged. As such USD/JPY breached its 100 and 50 HMAs (at 109.45 and 109.53 respectively) to a high of 109.73 (vs low of 109.33) with little to report on the options expiry front.

- GBP, EUR – The Pound continues on its upwards trajectory amid ongoing hopes of an Article 50 extension despite the UK Governments constant dismissal of the option, though the latest suggests that support for the Cooper amendment (to give Parliament power to extend Article 50) is stacking up, with reports of the Labour party also supporting the amendment. Lloyd’s notes that the recent Sterling strength was more than they anticipated, though a clean break through 1.3000 is still needed for “re-energised momentum” to the upside. GBP/USD remains closer to the top of a 1.2945-1.3000 range ahead of its 200 DMA at 1.3081. Meanwhile the EUR remains flat within

In commodities, Brent (+0.8%) and WTI (+0.8%) prices have nursed initial losses and moved into positive territory due a turnaround in risk sentiment. Following on from Saudi Energy Minister Al Falih’s withdrawal from the WEF at Davos, Russian Energy Minister Novak has also cancelled his trip; Novak was due to speak on Friday on the Great Energy Race alongside IEA’s Birol. Separately, IEA’s Birol has stated that oil demand will grow by at least 1mln BPD. In terms of forecasting DNB have cut their 2019 Brent forecast to USD 70/bbl vs. Prev. USD 75/bbl. Of note API’s have been rescheduled to today due to Monday’s US market holiday. Gold (Unch) has marginally benefitted from the risk sentiment, with the yellow metal trading at the top of it’s narrow USD 4/oz range; currently just under USD 1285/oz. Elsewhere, China’s December scrap metals imports increased to 510k tonnes, their highest figure since May, ahead of China tightening waste imports in 2019.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 13.5%

- 9am: FHFA House Price Index MoM, est. 0.3%, prior 0.3%

- 10am: Richmond Fed Manufact. Index, est. -2, prior -8

DB’s Jim Reid concludes the overnight wrap

Good morning from the highest city in Europe. Davos is very cold and please expect lots of Canada Goose jackets if you catch up with events on the telly over the rest of this week. I looked at buying one before I came out so as to fit in with the Davos set. When I saw how much they cost I realised I would rather not fit in. Actually, I got there late last night and the only non-restaurant places I found to eat were a kebab shop and a Co-op supermarket. I was wondering whether Bono has ever had a similar dilemma between the two choices. As I’m staying in a self-catering apartment and after much deliberation I opted for the latter and cooked myself a pizza. In nearly a quarter of a century it’s probably the first business trip that I’ve cooked for myself. I quite enjoyed it. Anyway, if you’re in town let me know, especially if you want to attend one of my sessions.

The cold air has obviously also infiltrated markets this week. US bourses reopening yesterday failed to stem the reversal of some of the new year optimism. Indeed, the latest headlines on the earnings and trade fronts weighed on sentiment. Equity markets failed to recover from heavy falls at the open with the S&P 500, DOW and NASDAQ closing down -1.42%, -1.22% and -1.91% respectively. The NYFANG index dropped -3.38% as Amazon and Netflix posted their worst days of the year.

Markets took another leg lower in the US afternoon session, after headlines broke that US negotiators declined a proposed meeting between with mid-level Chinese officials, apparently citing lack of progress on China’s industrial policies, especially the alleged forced technology transfers. The meeting would have been with Vice-Minister of Commerce Wang and Vice-Minister of Finance Liao, to lay groundwork for next week’s planned meeting between senior officials namely Vice-Premier Liu, US Trade Representative Lighthizer, and Treasury Secretary Mnuchin. Those talks are still scheduled to take place, but expectations for a breakthrough have now fallen. Late in the day, Trump Administration officials formally denied the reports however head of the National Economic Council Kudlow did add that “enforcement is absolutely crucial to the success of these talks. In any case the damage to markets had been done.

Earnings also played a part in the sogginess, as poor results from Halliburton, Johnson & Johnson and Stanley Black & Decker weighed on the industrials and consumer discretionary sectors (down -2.07% and -1.79% respectively). All three companies declined following their latest quarterly reports with the common denominator being management comments about a challenging outlook ahead, highlighted by Black & Decker CEO Loree saying “economic growth is slowing”. This more than offset gains to eBay (+6.13%) which rallied after one of its bigger shareholders, Elliot Management, proposed a five-step plan which in their view could result in eBay’s share price almost doubling. The energy sector also suffered (-2.20%), as WTI oil tumbled -1.91% however did at least pare a sharper slide earlier in the session. That move came despite there not really being an obvious catalyst aside from the various growth concerns which have been highlighted in recent days – none of which are particularly new news.

Meanwhile, here in Europe UBS also missed at both the earnings and sales lines following its quarterly report which resulted in shares falling -3.17% in Switzerland – albeit off the early lows. That weighed on the wider European Banks index which closed down -1.03% and for the fifth time in the last seven sessions while the STOXX 600 ended -0.36%. HY credit spreads widened +4bps and +12bps in Europe and the US respectively. In contrast bonds were slightly stronger, albeit only modestly so, with Bunds ending -2.0bps lower and Treasuries -4.5bps. The 2s10s curve also flattened -1.6 bps but the reality is that it still remains rooted in the 10-20bp range that it’s been in since the end of November.

Overnight the focus has turned to the BoJ where, as expected, there have been no changes to policy. Also as expected are the lower inflation forecasts in the BoJ’s outlook, the fourth consecutive quarter they have done so. For the fiscal year starting April, core CPI is expected to be 0.9% compared to 1.4% previously. With the backdrop of lower inflation and with the consumption tax looming, the hurdle to the BoJ contemplating adjusting policy continues to look high. JGBs are slightly weaker this morning post the decision with the 10y up less than a basis point to -0.004% with Kuroda due to speak shortly. The Yen has weakened -0.25% while the Nikkei (+0.04%) is broadly flat. That’s the case also for the Hang Seng (+0.06%) and Shanghai Comp (+0.07%) with the Kospi (+0.24%) outperforming. The good news is that the slide for US equity futures also appears to have come to an end with S&P 500 contracts up +0.15%. That may reflect the news that lawmakers in the Senate have agreed to hold separate votes today on rival proposals in order to reopen the government.

Moving on. There was some interest in the ECB’s bank lending survey yesterday which was softer compared to recent surveys. The net percentage of banks reporting tightening standards to enterprises was closer to even with -1 in Q4 compared to -6 in Q3. Demand for loans also continued its slowing trend from recent quarters with the net balance to enterprises falling to +9 versus +12 in Q3. It was a similar story for housing loans although demand for the latter did pick up. At a country level the softness was mostly reserved for Italy and Spain. Notably the outlook for Q1 also implies further moderation which fits in with lower growth expectations for the Euro Area this year. At a minimum the data should add to the anticipation levels for tomorrow’s PMIs and ECB policy meeting. Our economists’ preview for the meeting is available here. They don’t think any big policy changes are imminent, but think the council could shift its characterisation of the balance of risks to the downside. Apart from that, they’ll focus on any hints regarding new TLTROs and/or any discussion of a potential one-off deposit rate hike.

Here in the UK it was nice to get some rare positive news in the form of the latest labour report. Indeed there were positive surprises for the November unemployment rate (down one-tenth to 4.0% vs. 4.1% expected), average weekly earnings (up one-tenth to +3.4% 3m/yoy vs. +3.3% expected) and employment change (141k 3m/3m vs. 87k expected) prints. That of course compares to what have been weaker PMIs in the UK recently and the ongoing Brexit saga so this somewhat complicates the picture for the BoE with the supply side narrative of a tighter UK labour market very much intact. A hike by August is less than 50% priced however it will challenge the BoE not to sound overly dovish given the strength in the hard data.

The only other data worth flagging yesterday in Europe was the January ZEW survey in Germany where there was a big slump in the current situations component to 27.6 (vs. 43.0 expected) compared to 45.3 in December. However the expectations component did climb 2.5pts to -15.0 and bettered expectations for a fall to -18.5.

In the US, monthly existing home sales fell short of expectations, rising by 4.99 million in December compared to expectations for 5.25 million, the slowest pace and biggest downside miss since November 2015. Mortgage applications have picked up over the last couple weeks as long end interest rates have fallen, so there could be scope for a rebound in the near future. We’ll get the latest MBA mortgage application data later today.

In terms of the day ahead, this morning in Europe we’ll get January confidence indicators out of France followed later on by the January CBI survey in the UK. In the US this afternoon it’ll be worth keeping an eye on the January Richmond Fed manufacturing survey (-2 expected vs. -8 previously) in light of some weak regional Fed surveys so far this month, while the November FHFA house price index is also due out. This afternoon we’ll also get the January consumer confidence reading for the Euro Area. Away from that we’re due to hear from the BoE’s Broadbent while the second day of the Davos forum gets underway. Earnings wise we’re due to get quarterly reports from United Technology, Proctor & Gamble and Ford.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 1.30 PTS OR 0.05% //Hang Sang CLOSED UP 2.75 POINTS OR 0.01% /The Nikkei closed DOWN 29.19 PTS OR 0.14%/ Australia’s all ordinaires CLOSED DOWN 0.26%

/Chinese yuan (ONSHORE) closed UP at 6.7871 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.38 dollars per barrel for WTI and 62.02 for Brent. Stocks in Europe OPENED /RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7871 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7971: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

USA/Yen rises (yen falls) hits 110 after they report an export slump.

(courtesy zerohedge)

USDJPY Hits 110 After Dovish BOJ, Export Slump

The yen has been weakening all day, and moments ago the USDJPY hit 110.00, the highest level since the start of the year – rising alongside 10Y TSY yields and S&P futures – after Japan’s exports fall and Bank of Japan cuts inflation outlook again.

On Wednesday morning, in its latest policy decision, the Bank of Japan kept its monetary policy unchanged as expected, but cut its inflation forecast, and now expects CPI forecast for the fiscal year starting in April to be only 0.9% down from 1.4%, citing lower oil prices, but really just the latest admission that Abenomics is failing to gain traction. The BOJ also trimmed its estimate for fiscal 2020 to 1.4% from 1.5%.

The BOJ also revised down sharply its outlook for FY2018 real GDP growth to 0.9%, from 1.4% as of October 2018. This revision was likely made to reflect the large negative growth (-2.5% qoq annualized) recorded in the second estimate for 3Q2018 real GDP due to the impact of natural disasters.

While the BOJ’s statement on the risk balance was largely unchanged, the BOJ looks to have adopted a more cautious tone on overseas economic trends with the addition of the comment “[s]uch downside risks concerning overseas economies are likely to be heightening recently, and it also is necessary to pay close attention to their impact on firms’ and households’ sentiment in Japan.”

Because it’s never “your” fault when you are a central banker, it is always “someone else’s fault.”

“The yen came under pressure as the perception that the current low interest-rate condition in Japan will continue longer after the BOJ cut its inflation forecast,” said Daisaku Ueno, chief FX strategist at Mitsubishi UFJ Morgan Stanley Securities.

“BOJ’s decision to lower its inflation forecast has added to the perception that it will continue its current ultra-loose monetary policy for longer, without suggesting it will ease further”, said Tadashi Matsukawa, head of fixed-income investment at Pinebridge Investments Japan.

There was more bad news for Kuroda and Abe overnight, when Japan’s exports tumbled 3.8% Y/Y in December, twice as bad as the expected -1.9%, and the lowest since October 2016, in yet another confirmation that i) global trade is slowing rapidly and ii) Japan will need to find a way to lower the Yen even more if it hopes to boost the country’s exports.

Still, as Bloomberg notes, the dollar continues to face stiff resistance near 110 yen as two key psychological risk factors – U.S.-China trade tensions and U.S. government funding legislation – remain unresolved. That said, as Japanese interest rates are expected to stay low, local investors may decided to send their money abroad, which could provide support to USD/JPY.

3 C CHINA

i)CHINA

A good commentary from Jeffrey Snider today as he describes the decline of the euro dollar story is reaching its final chapters. Euro dollars is simply uSA dollars held outside of the uSA. Because of the lack of growth in the emerging markets, Asian markets and European markets, we are witnessing a decline in those dollars. The high deficits of Trump is also sucking into the USA vast sums of dollars and that is killing the rest of the globe

(courtesy Jeffrey Snider)

China’s Eurodollar Story Reaches Its Final Chapters

Authored by Jeffrey Snider via Alhambra Investment Partners,

Imagine yourself as a rural Chinese farmer. Even the term “farmer” makes it sound better than it really is. This is a life out of the 19th century, subsistence at best the daily struggle just to survive. Flourishing is a dream.

Only, you can see just on the other side of the hill the bright reflective lights of one of China’s many glittering modern cities. Not only are you reminded of the stark difference between what must be the life of its denizens and yours, not too long ago your neighbor or distant relative was privileged enough to move out of the peasantry and into the light and city life of relative comfort and fortune.

You try not to be bitter because this transformation will some day be your transformation, biding your time until your number is called. You put up with a lot along the way, from clear restrictions to your personal freedom and human rights to ungodly pollution, but through it all you keep reminding yourself that even if you don’t live long enough, for your one permitted child their future is assured.

And then one day the government says, “sorry, we are all full up over here in paradise.”

China isn’t quite there yet, but that day is coming maybe even rapidly approaching. What’s more, Chinese officials know it. While Economists in the West were suckered into globally synchronized growth, the Communists knew it was nothing more than a marketing slogan. Long before trade wars, China’s economy in 2017 had reached its reflationary plateau and frighteningly it was a shallow one.

…of the 300 to 500 million peasants slated to become middle class workers, what happens if only 200 million end up having been given the order to move into the fancy new cities? (In truth, it doesn’t work like that; it works the same as anywhere else where the relatively affluent already in cities move into the new stuff and the newly arrived rural farmers take over the old left behind). This is the real danger and the real task for the Chinese government. A no-growth world means there isn’t anything for those still on the outside to do, and therefore no need for them in the cities.

If that was the best they could do when everything was supposedly going right, what was the downside when things didn’t go right? Furthermore, given recent history of the global reserve currency system, eurodollar not dollar, what were the chances “going right” was going to last more than maybe a few quarters longer?

On top of all that, the Chinese Communists remain keenly aware what happened in Russia when the Soviet Communists’ economy ran out on them. They aren’t around to tell the story.

More and more China’s officials are sounding the alarm. It is the political backlash against a world without growth. You can listen to Jay Powell and Mario Draghi if you like, and maybe Xi Jinping does as a matter of pure hope. But as the supreme official for what is always a fragile proposition (authoritarian states tend to be that way) Emperor Xi doesn’t have the luxury. He knows what could happen when he instructs local officials to give the “we are full” signal.

President Xi Jinping stressed the need to maintain political stability in an unusual meeting of China’s top leaders – a fresh sign the ruling party is growing concerned about the social implications of the slowing economy.

No kidding. China’s economic predicament is intractable. Even those who all throughout 2018 were speaking of the trade war can sense that this is so much bigger than tariffs on soybeans. Mainstream news stories once eager to blame American officials for a minor slowdown have come to realize this is internal Chinese demand on the brink.

Only, nobody can figure out why.

Eurodollar, not dollar. I wrote in October 2017 that the Chinese were warning the world about the state of the global economy because they are forced to be realistic about it by their dollar short. No one wanted to listen because Economists.

There is every reason to suspect that Chinese officials are increasingly accepting of a no-growth paradigm, and therefore it would be prudent (from the Communist perspective) to get ahead of any potential fault-lines that may develop in response to China without any “miracle(s).” With an end to the labor market transformation in sight, as indicated most spectacularly by FAI, it just might get a little dicey out in rural China.

That was five quarters ago, and I’ll repeat it again – this was long before trade wars.

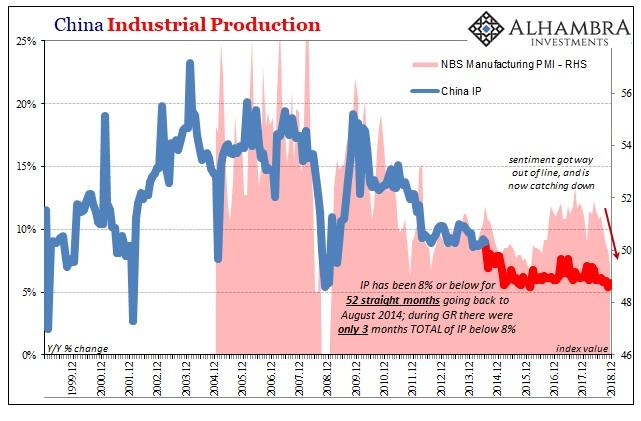

The latest economic statistics from China display the unmistakable direction. The Chinese economy is not crashing, but there is no doubt it is slowing. In the bigger picture, there really is no difference anymore.

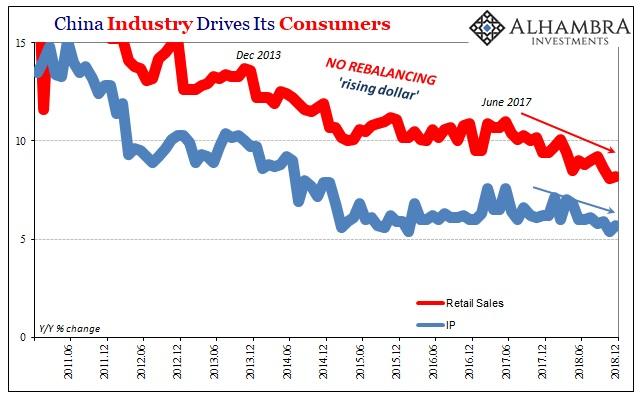

Industrial Production was a little better at 5.7% year-over-year in December than the atrocious 5.4% growth in November, that just means slightly less atrocious.

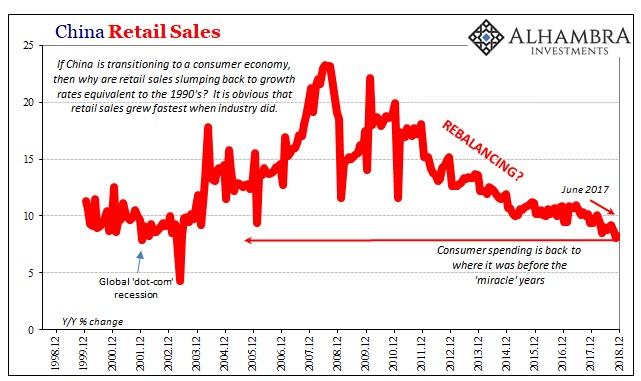

Retail Sales were up 8.2% last month, a tick above the 8.1% recorded the month before. November’s rate was the worst in a long time, again being a little better than the worst is still in the same category.

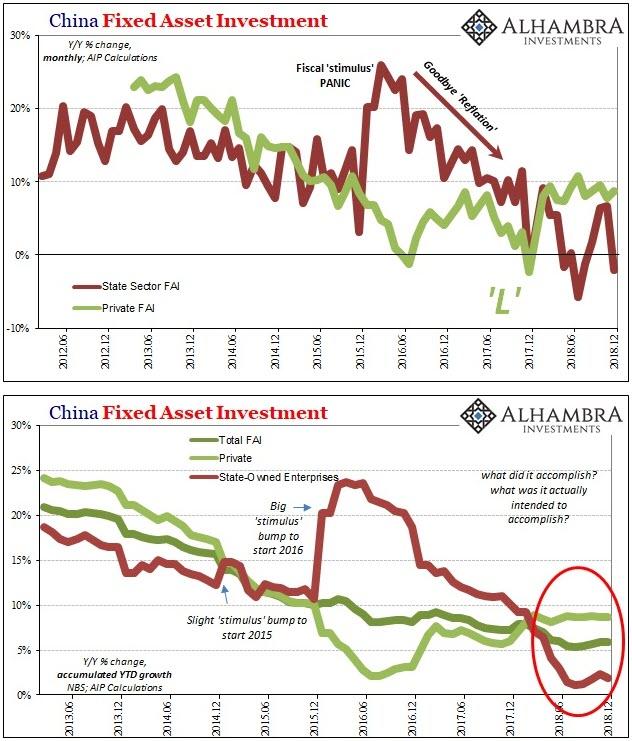

Accumulated Fixed Asset Investment (FAI) managed growth of 5.9% for all of 2018 over 2017. Private FAI was slightly higher last year than the year before, 8.7% compared to 6.0%, but that was a low level to come back to and nowhere near the 25% to 30% growth that used to be China’s urbanizing baseline. And much of that private FAI was directed into China’s longstanding property bubble.

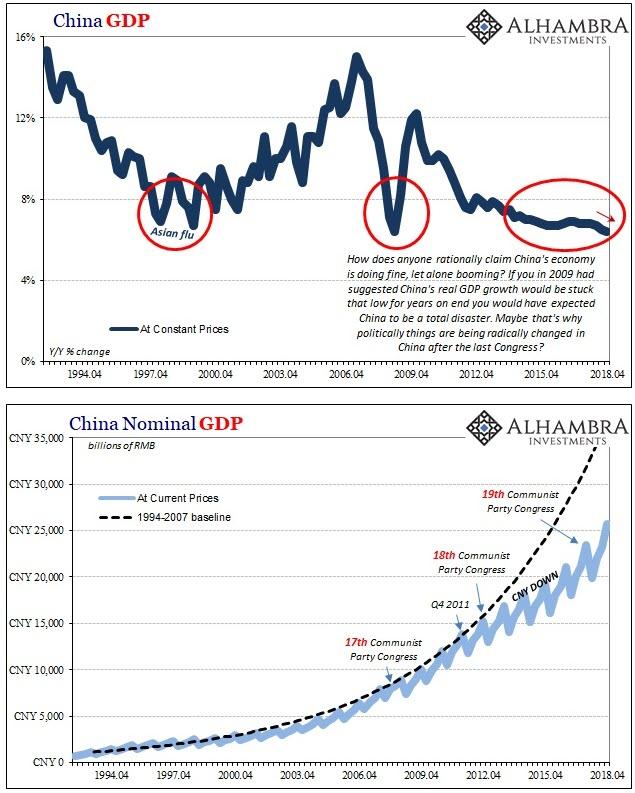

GDP growth in Q4 (6.4%) was the worst in decades.

Xi’s predicament is very real, not that anyone should have any sympathy for a despot. By itself, slowing wouldn’t be too much to be concerned about; coming down from such a low start, however, changes the game entirely. There can be no growth and the probability the paradigm will change for the better is now exceedingly low. If you are a Communist, it isn’t just prudence to prepare for the scenario, it is full-on survival at this point.

When China signed on to the eurodollar system, they did so thinking it was a one-way ticket to paradise. Even after 2008, there were complaints about it (Zhou in March 2009) but no serious challenge once it looked like Emerging Markets were going to emerge maybe even the winner – it was widely believed there was a “new normal” in the West leaving growth the exclusive property of the East (and South).

It was a higher order mistake along the lines of these “decoupling” outbreaks. In the immediate aftermath of the Great “Recession” everyone acted as if the developing world was going to decouple from the lack of recovery in the developed world.

There is no decoupling, however, only variances in the time dimension. It was only a matter of time before the eurodollar’s “L” struck China, Asia, and all the rest of the global economy, too. Even when it did half a decade ago people still couldn’t grasp the enormity of what was failing.

While Janet Yellen was busy with exit strategies and transitory factors, this is exactly what had happened. The eurodollar decay was not transitory, it just doesn’t happen all at once. That’s really all 2017 was, a pause in the global monetary deconstruction.

It’s back again and in a big way. The Chinese Communists have been battening down the hatches for five quarters already. The negative signals are as much political and social in nature as economic or financial.In fact, the econ stats more and more merely confirm the alarming political developments.

4.EUROPEAN AFFAIRS

GERMANY/DEUTSCHE BANK

The Fed is now probing Deutsche bank’s role in the money laundering scandal with respect to Estonia’s Danske bank

(courtesy zerohedge)

Fed Probing Deutsche Bank’s Role In Largest-Ever Money Laundering Scandal

As rumors about a possible Deutsche Bank merger with rival troubled German lender Commerzbank continue to swirl despite the seemingly never-ending investigations into a suite of alleged misdeeds by the bank, Bloomberg has given would be merger arbs weighing whether to buy the German lender’s battered shares one more reason to hold off.

In a follow-up to a report late last year that the Department of Justice had expanded its probe into what could be the largest money laundering scandal in history – that is, the infamous Danske Bank money laundering scandal, which involved some $230 billion of suspicious money flowing into Western Europe from shadowy sources in the former Soviet Union – by looking into the role played by the various correspondent banks that cleared many of these transactions (a group that included DB, BofA and JPM), Bloomberg reported on Wednesday that the Federal Reserve is examining how DB moved billions of dollars on behalf of Danske’s Estonian branch, the epicenter of the fraud.

Though this line of inquiry is said to be in its early stages, the implications are clear: US regulators are growing increasingly dissatisfied with correspondent banks and their deference on all KYC-related issues to the client banks whose transactions they are clearing.

Deutsche Bank said that month it has controls in place when acting as a correspondent for other banks, but its ability to know about their clients is limited. As a correspondent, “your only relationship is with the bank and the bank itself has the responsibility to check its own client to monitor the transaction and to do all these kinds of checks”, a company representative said at the time.

The Fed is exploring whether Deutsche “adequately monitored funds” moving through Danske’s Estonian branch.

The Fed’s probe is in an early stage as it scrutinizes whether Deutsche Bank’s U.S. operations adequately monitored funds from an Estonian branch of Danske Bank A/S, according to two people briefed on the situation, who asked not to be named because the inquiry isn’t public. Danske, which used correspondent banks such as Deutsche Bank to move money abroad, has admitted that much of about $230 billion that flowed through the tiny Estonian outpost may have been dirty.

For what it’s worth, DB denied that the Fed or other US regulators or law enforcement agencies were investigating the bank. Instead, it said they were merely asking questions.

“There are no probes,” Deutsche Bank said in an emailed statement, but the bank “received several requests for information from regulators and law enforcement agencies around the world. It is not surprising at all that the investigating authorities and banks themselves have an interest in the Danske case and the lessons to be learned from it. Deutsche Bank continues to provide information to and cooperate with the investigating agencies.”

The Fed is supposed to ensure that banks in its jurisdiction properly scrutinize their clients. One factor that may have attracted scrutiny from the Fed was testimony from a Danske whistleblower who told lawmakers in Denmark that DB moved $150 billion – the bulk of the suspected illicit cash – on behalf of Danske.

The U.S. requires banks operating under its jurisdiction to scrutinize clients and their dealings to detect potential money laundering and alert authorities to suspicious transactions. The Fed is among regulators that ensure banks have adequate systems in place to fulfill those duties.

A Danske Bank whistle-blower who outlined the illicit flow of cash through that firm has said much of it passed through Deutsche Bank in the U.S., and one of the people said the Fed is focusing on the German lender’s trust bank. Deutsche Bank has been cooperating with the Fed, the people said.

A Fed spokesman said it doesn’t publicly discuss confidential probes.

Last week, DB CEO Christian Sewing said he had launched an internal probe into the bank’s correspondent banking practices even though he hasn’t seen anything to suggest wrongdoing. Much of the illicit activity under investigation took place between 2007 and 2015.

The bank had previously reviewed its actions in the case, Sewing said at an event in Berlin. He urged people not to “prejudge” the bank or its employees, presuming their innocence unless proven guilty.

Whether the Fed probe results in financial penalties remains to be seen. But banks and investors should take note: Correspondent banks, who have previously been allowed to feign ignorance when their involvement in money laundering violations has come to light, might soon be facing a lot more scrutiny.

Pound Climbs As Labour Backs Measure To Delay Brexit

Update (6 am ET): The pound has continued its ascent on headlines affirming that Labour intends to back the Cooper amendment, which would push the government to try and delay Brexit Day if Prime Minister May fails to pass a deal by late February.

Meanwhile, Michel Barnier, the EU’s chief Brexit negotiator, said during an interview with the Luxembourg Times that the EU would only back extending the Brexit dealine if there is a “stable majority” for a deal. He also said that if the UK believes the backstop is an insurmountable obstacle, they could likely secure another deal if they tack to a softer Brexit (which would presumably include remaining in the customs union and/or the single market).

* * *

The British pound vaulted back above $1.30 Wednesday morning as it rose for a third day, returning to its highs from November, on reports that the Labour Party was on the cusp of backing a proposal put forth by one of its members that would force the government to seek a delay of Brexit until the end of the year.

With the next big parliamentary vote on Theresa May’s Brexit deal (this time, the “Plan B” iteration) coming next week, on Tuesday night, those who want to amend the government motion calling for the vote to force the government to rule out a no-deal Brexit, received some good news. Amid the crush of plans hoping to delay or derail Brexit, Labour MP Yvette Cooper put forth an amendment that would require May to seek a delay of Brexit if a deal isn’t passed by Feb. 26.

Yvette Cooper

During an interview on the BBC’s Newsnight last night, Shadow Chancellor John McDonnell all but announced that Labour would support the Cooper amendment, calling it a “sensible proposal” and adding that it was “increasingly likely” that Labour would vote for it. Given the number of rebel Tories who have said they would support the Cooper amendment, it has a high likelihood of passing if it’s called for a vote.

BBC Newsnight

✔@BBCNewsnight

“Yvette Cooper has put an amendment down, which I think is sensible,” says Labour shadow chancellor John McDonnell adding “it’s increasingly likely” Labour would back her amendment@johnmcdonnellMP | #newsnight

Analysts said the amendment is leading to intensifying optimism that no deal will be avoided.

The rally in GBP “reflects building optimism that a ‘no-deal’ Brexit will be avoided,” said Lee Hardman, an analyst at MUFG. “There have been some encouraging signs that the risk of delaying Brexit could prompt rebel Conservative MPs and the DUP to consider backing an amended version of PM May’s deal.”

Tories have tried to portray the amendment as unconstitutional, though the Guardian reported that there is precedent for legislation being proposed by backbenchers being called for a vote. Liam Fox, a Brexiteer and May’s international trade secretary, claimed that the amendment was constitutionally improper. He said that amendments that call for “taking control” of the “initiation of legislation” pose “a real danger.”

Sterling climbed 0.4% to $1.3004, its highest level since mid-November, after advancing 0.6% in previous two days.

As the prime minister tries to rally support for her revise deal, May will face off with Labour leader Jeremy Corbyn on Wednesday during another session of PMQs.

end

Tom Luongo describes May’s Plan B: calling the remainers bluff

(courtesy Tom Luongo)

Luongo: May’s Brexit ‘Plan B’ Is To Call Remainers’ Bluff

Authored by Tom Luongo via The Strategic Culture Foundation,

Earlier this week I did something I never thought I’d ever do. I watched over two hours of British Parliament. This was the session wherein Prime Minister Theresa May outlined her so-called Plan B deal for Brexit.

Needless to say, it wasn’t warmly received.

But a funny thing has happened on the way to Brexit. And I am as shocked to type this as anyone who follows me will be shocked to read it.

Theresa May has risen to become Brexit’s main champion.

As I said in my last article here:

Theresa “The Gypsum Lady” May went through an extraordinary twenty-four hours. First, seeing her truly horrific Brexit deal go down in historic defeat and then, somehow, surviving a ‘No-Confidence’ vote which left her in a stronger position than before it.

It looks like May rightly calculated that the twenty or so Tory Remainers would put party before the European Union as their personal political positions would be terminally weakened if they voted her out of office.

Blue Monday’s Parliamentary session confirmed for me that she has emerged from this fight stronger than she’s been since before the 2017 snap election debacle. May rightly pointed out, patiently and with a twinkle of smugness, that all calls for extending Article 50 or holding a second referendum were irrelevant.

Article 50 happens on March 29th and the whining of Remainer MP’s can’t stop it.

So, if they want a deal with the EU, then they have to give her and the government clear parameters to go back to Brussels to negotiate from. Otherwise, March 29th comes and Brexit on World Trade Organization rules commences.

But May also knows that her offer for talks with all sides of the House is a bit of a lie. She knows that the fractious nature of the Remain position precludes them coming up with a deal offer that will get majority support of the House of Commons.

And if you needed proof of this all you had to do was watch the endless parade of MPs.

For two hours I watched Remainer after Remainer grandstand and virtue signal about the need for the “People’s Vote” and whine for more time. The SNP threatened to leave the U.K. multiple times if they didn’t get their way.

It was like watching children have a tantrum over not getting their cookie.

None of them proposed one constructive solution to break the deadlock in the House. They simply stuck to their talking points and fulminated.

And May was firm. She may have even graduated from ‘The Gypsum Lady’ to ‘Calcite’ or ‘Feldspar.’

If she delivers a real Brexit that leaves the EU spluttering into their lattes and Remainers simpering about how unfair it all is, I’ll take back most of the mean things I’ve said about her.

The Remain crowd has had two years to influence negotiations knowing a “No-Deal” Brexit was the default position. They thought they could play politics, use Brexit chaos as a way for Labour to seize power and destroy the Tories.