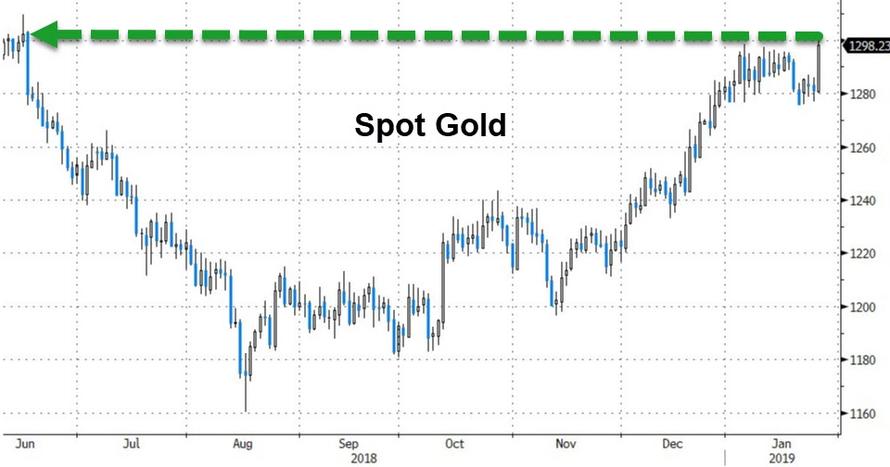

GOLD: $1298.80 UP $17.90 (COMEX TO COMEX CLOSING)

Silver: $15.70 UP 40 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1303.10

silver: $15.75

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 5 NOTICE(S) FOR 500 OZ (0.0155 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 555 NOTICES FOR 55100 OZ (1.7262 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 814 for 4,070,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

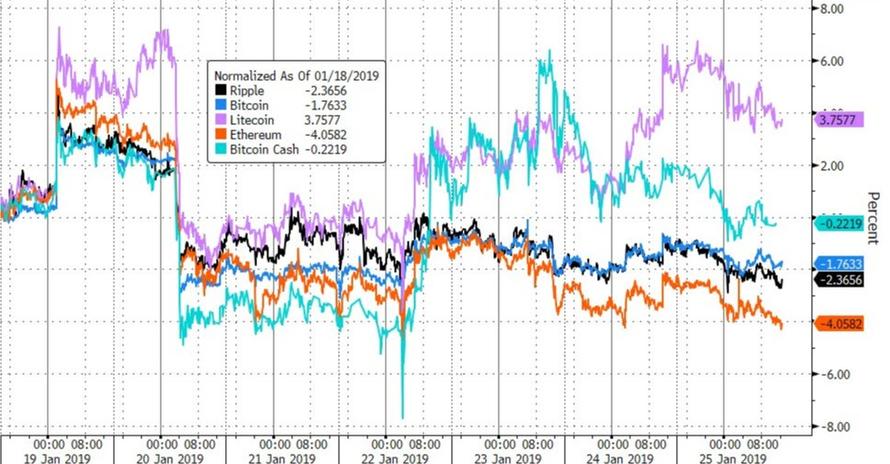

Bitcoin: OPENING MORNING TRADE $3555: DOWN 18

Bitcoin: FINAL EVENING TRADE: $3558 DOWN $6

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 2/5

EXCHANGE: COMEX

CONTRACT: JANUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,279.100000000 USD

INTENT DATE: 01/24/2019 DELIVERY DATE: 01/28/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 C HSBC 4

657 C MORGAN STANLEY 1

661 C JP MORGAN 2

737 C ADVANTAGE 2

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 5 5

MONTH TO DATE: 560

Starting Monday we generally see a contraction in open interest once we approach first day notice in an active month. This usually begins 4 days prior to first day notice. The fall is due to spreaders who generally must liquidate. The contraction in OI never effects price because each trade has a buy and a sell of gold at the exact same price..i.e. a buy order and a sell order.

However while this is going on, we had a huge gain in gold price today and that should have caused our bankers to supply endless paper. It will be interesting to see the OI for comex gold for Monday.

Also remember that we are 4 days away from options expiry from London/OTC gold/silver. These expire at around 12 noon on the 31 st of January. So expect the crooks to take advantage of the higher price as they continue to supply unlimited non backed paper.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A FAIR SIZED 1296 CONTRACTS FROM 187,993 DOWN TO 186,697 DESPITE YESTERDAY’S 7 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED SLIGHTLY FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

731 EFP’S FOR MARCH, 0 FOR APRIL AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 731 CONTRACTS. WITH THE TRANSFER OF 731 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 731 EFP CONTRACTS TRANSLATES INTO 2.555 MILLION OZ ACCOMPANYING:

1.THE 7 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.805 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 35,145 CONTRACTS (FOR 17 TRADING DAYS TOTAL 35,145 CONTRACTS) OR 175.73 MILLION OZ: (AVERAGE PER DAY: 2067 CONTRACTS OR 10.336 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 175.73 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.10% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 175.73 MILLION OZ.

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1296 WITH THE 7 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 731 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 565 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 731 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1296 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 7 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.30 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 13 NOTICE(S) FOR 65,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.825 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A FAIR SIZED 1574 CONTRACTS DOWN TO 523,228 WITH THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $3.70//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7069 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 7069 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 523,228. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5495 CONTRACTS: 1574 OI CONTRACTS DECREASED AT THE COMEX AND 7069 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 5495 CONTRACTS OR 549,500 OZ = 17.09 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.70???

YESTERDAY, WE HAD 6530 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 132,737 CONTRACTS OR 13,272,700 OZ OR 412.86 TONNES (17 TRADING DAYS AND THUS AVERAGING: 7854 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAYS IN TONNES: 412.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 412.86/2550 x 100% TONNES = 16.19% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 412.86 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 1574 WITH THE LOSS IN PRICING ($3.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7069 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7069 EFP CONTRACTS ISSUED, WE HAD ANOTHER STRONG GAIN OF 5495 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7069 CONTRACTS MOVE TO LONDON AND 1574 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 17.09 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $3.70 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 8TH STRAIGHT DAY THAT WE RECORDED STRONG RISES IN OI ON BOTH EXCHANGES!

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $17.90 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 809.76 TONNES

Inventory rests tonight: 809.76 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 40 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY/

/INVENTORY RESTS AT 307.251 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 1296 CONTRACTS from 187,993 DOWN TO 186,697 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

731 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 731 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1296 CONTRACTS TO THE 731 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 565 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 2.825 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.825 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 7 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 731 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 10.03 PTS OR 0.39% //Hang Sang CLOSED UP 448.21 POINTS OR 1,65% /The Nikkei closed UP 198.93 PTS OR 0.97%/ Australia’s all ordinaires CLOSED UP 0.68%

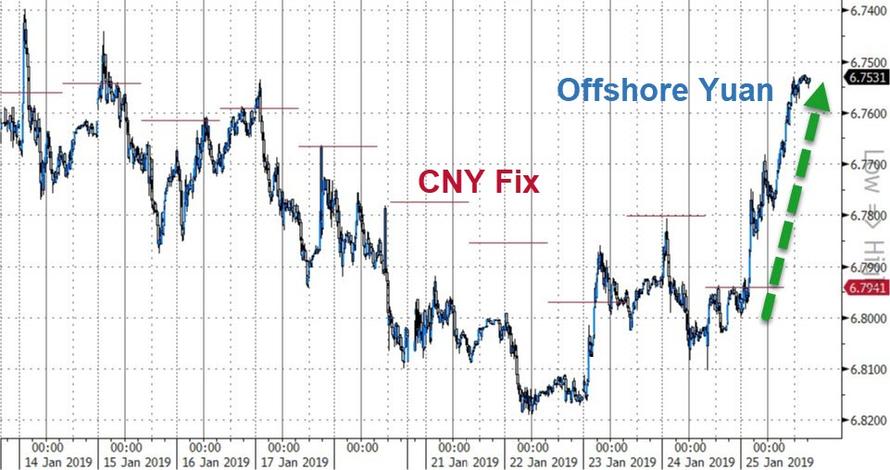

/Chinese yuan (ONSHORE) closed UP at 6.7595 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.04 dollars per barrel for WTI and 60.73 for Brent. Stocks in Europe OPENED /GREEN

//. ONSHORE YUAN CLOSED UP AT 6.7595 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7665: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA/Sweden

b) REPORT ON JAPAN

3 C/ CHINA

i)CHINA/USA

Our resident expert on Chinese affairs, Gordon Chang offers a good look at China’s ambitions and the continuing hostility showed by Chinese generals and admirals

( Gordon Chang)

ii)Futures rally on a report Vice Ministers are heading to Washington for trade talks. Nothing is going to happen in these talks unless Meng is released from a Cdn jail and the USA must stop its extradition of her

( zerohedge)

iii)Very quietly PBOC announces a quasi QE by allowing the swapping of worthless Perpetual bonds for Treasuries. The Chinese hope to keep the Ponzi scheme alive

( zerohedge)

iv)China threatens to pull money from Silicon Valley unless the Huawei affair ends. The former Governor of the POBC also states that he feels the trade war will become a tech war and he is right

( zerohedge)

v)Scary! USA warships enter the Taiwan strait but this time, up above are Chinese bombers

4/EUROPEAN AFFAIRS

FRANCE/BELGIUM, HUNGARY ETC

Why the protests in these countries are different this time

an excellent presentation by Claudio Grass of Mises

(Grass/Mises)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

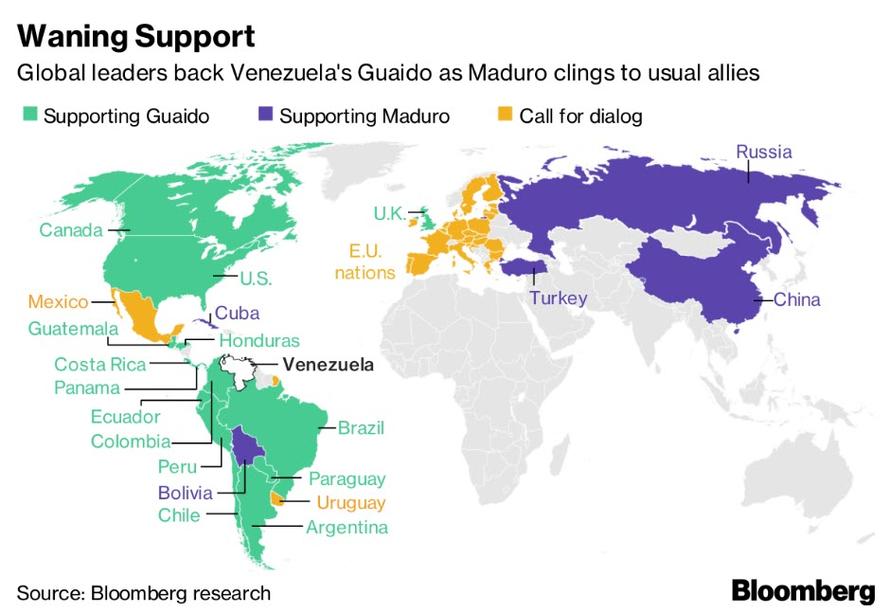

i)/Russia/Venezuela/USA

This will certainly escalate the situation: Russia sends in security contractors to protect Maduro. Venezuela is in the uSA sphere of influence. The problem is that billions of dollars was loaned to Venezuela by Russia and China invested large sums of money as well

( zerohedge)

6. GLOBAL ISSUES

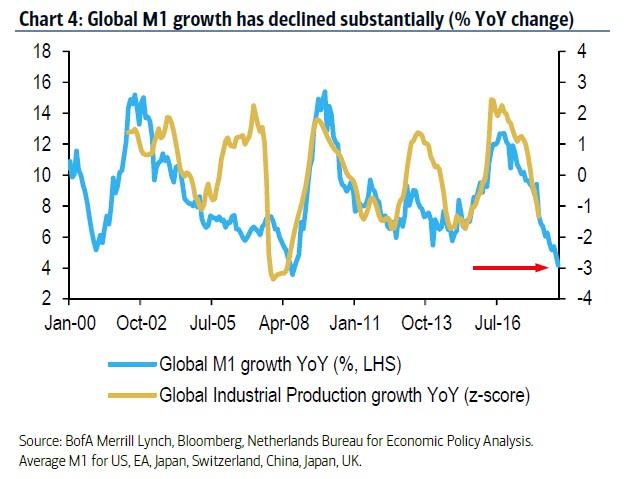

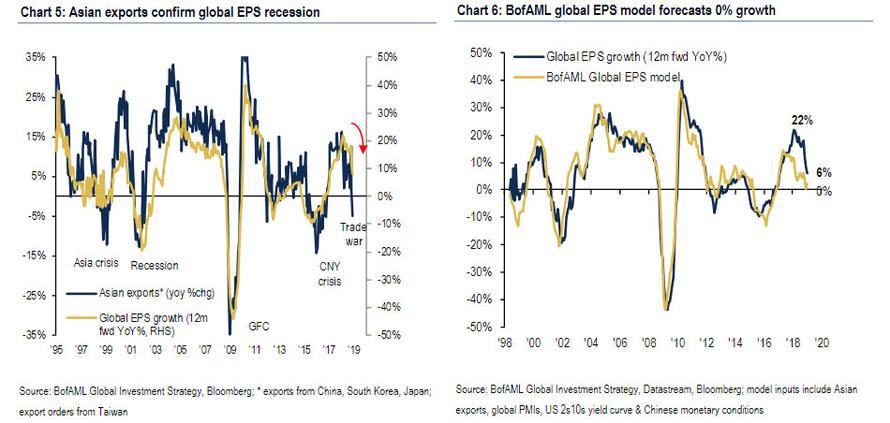

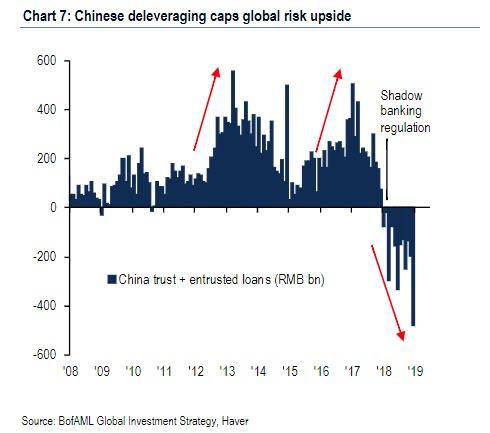

Asian exports, the life-blood for their economies is tumbling and as such confirms a global earnings recession. The Low M1 growth certainly suggests that global industrial production is negative and that will prove that we have an earnings recession. No wonder China decided to do a quasi QE this morning.

(courtesy zerohedge)

7. OIL ISSUES

Tom Luongo discusses the truth behind what the USA wants to do with respect to Venezuela and its oil

(courtesy Tom Luongo

8 EMERGING MARKET ISSUES

i)VENEZUELA

USA orders non emergency government employees out of Venezuela

(courtesy zerohedge)

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

Another Bellwether stock reports revenue misses and disappointing earnings..and they cut outlook. Obviously the meatheads are looking at the Chinese trade delegation coming as a reason to buy stocks.

( zerohedge)

a)Eliz. Warren now proposes a 2% tax on citizens with a wealth of 50 million dollars. This is an annual tax. She also proposes a 3% annual tax on assets worth 1 billion dollars. She wants an annual audit on all citizens with a wealth of over 50 million dollars.

I guess that would redistribute the wealth in a hurry.

( zerohedge)

b)This Wall Street Journal report caught everybody of guard and was the principal reason for gold’s rise. The Journal is reporting that the Fed wants to end its QT much earlier than expected. This goes against what Brandon Smith believes

(courtesy zerohedge)

iv)SWAMP STORIES

Trump is now ready to proclaim an National Emergency and put 7 billion dollars for building the wall. This will be done without congressional approval

( zerohedge)

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 19 CONTRACTS DOWN TO 445. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 1969 CONTRACTS DOWN TO 135,792 CONTRACTS.

AS A COMPARISON TO LAST YEAR WITH 4 DAYS TO GO BEFORE FIRST DAY NOTICE WE HAD 146 CONTRACTS STANDING FOR DELIVERY (VS 445 TODAY).

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

by Mark O’Byrne in Business and Finance

Historically, gold has proven to be a very safe investment – could it remain so in times of a massive global debt bubble, Brexit, trade wars and an uncertain world economy?

“You have to choose between trusting to the natural stability of gold and the natural stability of the honesty and intelligence of the members of the government. And, with due respect for these gentlemen, I advise you, as long as the capitalist system lasts, to vote for gold.”

The words of the witty Irish playwright and philosopher George Bernard Shaw, will resonate with investors in Ireland , the UK and internationally today given the UK government’s handling of Brexit and the rise of Trump and other radical politicians on the left and right.

Populist politicians are creating increasing political, economic and financial risks for us all. This is clearly seen in the complete mess that is Brexit – for Ireland, the UK and indeed the EU.

Shaw was a keen student of history and saw the economic problems that monarchies and governments have created over the years. Only the most foolhardy investor would claim that the coming years will be any different than our past.

Gold’s safe-haven historical status

A massive global debt bubble, Brexit, the risk of Italy leaving the EU, an increasingly fractured EU, aggressive Trump foreign and economic policies and an increasingly polarised and uncertain world cast shadows over our economies and financial markets.

There are very real risks posed by the gigantic global debt bubble – the world is nearing $250 trillion in debt and the global debt to GDP ratio has risen to 320%.

Shaw was also alluding to gold’s safe-haven status throughout history. Paper currency devaluations and indeed stock, bond and property market crashes are much more common throughout history than many people realise.

Gold has protected people from war, recession, depressions, inflation and currency devaluations. History clearly shows this. There have been numerous stock and property bubbles in the last 100 years. When they collapsed those that did not have all their eggs in the one basket and had diversified and owned some physical gold protected and indeed grew their wealth.

It has not been enough to simply own gold as on occasion, desperate governments have enacted draconian legislation that allowed them to confiscate their citizen’s gold. Roosevelt in 1933 and Mao in 1949 are the two primary examples of this.

Movement towards owning physical gold in safe jurisdictions

This precedent and many others involving property and land confiscation, ‘bank holidays’ and nationalisation of strategic assets have seen a trend towards risk averse investors opting for physical gold rather than digital gold in the form of ETFs and “platform gold” or “.com gold” in recent years.

This and the precarious debt position of the U.S., the UK and other large debtor nations has also seen a movement towards owning physical gold in safer jurisdictions.

Investors have been showing a preference for owning gold in wealthy creditor nations that also respect wealth and property rights. Switzerland, Singapore and Hong Kong have been the primary beneficiaries of these gold flows and they remain the favoured jurisdictions of our clients and gold investors internationally.

However, more recently we have had both UK and Irish clients asking us to provide secure storage in Dublin in Ireland and we are now delighted to be able to provide that option for the first time.

Gold’s purchasing track record

Gold has an excellent track record in maintaining its purchasing power relative to currencies and other assets.

Besides history, there is also a significant body of empirical evidence in the form of academic research and research from independent asset allocation experts which shows that gold is an important diversification for investors which reduces portfolio volatility and enhances returns.

Gold is a hedge and financial insurance in an uncertain political and economic world. Gold stored in safe vaults in Dublin and other safe jurisdictions will again act as a safe haven asset when it is needed in 2019 and the coming years.

Courtesy of Business and Finance

News and Commentary

Gold steadies on U.S. government shutdown, trade jitters (Reuters.com)

US Mint sales bounce back with bumper January (BullionByPost.co.uk)

Why Goldman’s commodities chief is bullish on oil and gold right now (MarketWatch.com)

EU ministers reject easing of liquidity rules for gold trading (Reuters.com)

Gold Will Protect From Increasing Market Volatility in 2019 (BusinesAndFinance.com)

IMF Fears Political Rage Will Block Rescue by Fed in Next Crisis (Gata.org)

Palladium’s Slide Accelerates on Dollar’s Rise; Gold Down Too (Investing.com)

Blockchain to shake up mining and precious metals sector (ING.com)

Chemical elements which make up mobile phones placed on ‘endangered list’ (St-Andrews.Ac.UK)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

24 Jan: USD 1,279.75, GBP 981.70 & EUR 1,128.36 per ounce

23 Jan: USD 1,284.90, GBP 990.14 & EUR 1,131.74 per ounce

22 Jan: USD 1,284.75, GBP 994.14 & EUR 1,130.58 per ounce

21 Jan: USD 1,278.70, GBP 995.08 & EUR 1,124.11 per ounce

18 Jan: USD 1,285.05, GBP 993.34 & EUR 1,126.86 per ounce

17 Jan: USD 1,294.00, GBP 1,004.92 & EUR 1,135.87 per ounce

16 Jan: USD 1,290.50, GBP 1,002.46 & EUR 1,130.99 per ounce

Silver Prices (LBMA)

24 Jan: USD 15.30, GBP 11.75 & EUR 13.48 per ounce

23 Jan: USD 15.38, GBP 11.80 & EUR 13.54 per ounce

22 Jan: USD 15.26, GBP 11.84 & EUR 13.44 per ounce

21 Jan: USD 15.26, GBP 11.86 & EUR 13.42 per ounce

18 Jan: USD 15.47, GBP 11.96 & EUR 13.56 per ounce

17 Jan: USD 15.57, GBP 12.08 & EUR 13.66 per ounce

16 Jan: USD 15.54, GBP 12.09 & EUR 13.66 per ounce

Recent Market Updates

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

– Financial Advice In 2019: Own Gold To Hedge $250 Trillion Global Debt Bubble – GoldCore In Irish Times

Ambrose Evans-Pritchard: IMF fears political rage will block rescue by Fed in next crisis

Submitted by cpowell on Fri, 2019-01-25 01:18. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Thursday, January 24, 2019

https://www.telegraph.co.uk/business/2019/01/24/imf-fears-political-rage…

The International Monetary Fund has warned that the system of global cooperation that saved world finance in the 2008 crisis may break down if there is another major shock or a deep recession.

David Lipton, the IMF’s second-highest official, said it is unclear whether the US Federal Reserve would again be able to extend $1 trillion of dollar “swap lines” to fellow central banks — the critical measure that halted a dangerous chain-reaction after the collapse of Lehman Brothers and AIG.

…

I fear that if at any time we have a worse than garden variety recession there will be anger and limitations in the way governments can respond,” he told a group at the World Economic Forum in Davos today.

“If there is a substantial crisis we may need central banks to act again in an extraordinary way. For the Fed this requires a fiscal backstop from the US Treasury, and at the beginning there may be some reluctance. I wonder whether they will be so willing to extend the swap lines,” Mr Lipton said.

It is a polite way of saying that the Trump administration might ask why it should “bail out” the Europeans who have been less than friendly to this White House, and why they should rescue the rest of the world. By the time the explosive consequences became clear it would be too late.

“So we have got to be very careful. There must not be unforced errors. We must ensure that the next recession when it comes is a garden variety,” said Mr Lipton, a leading figure in regulatory circles.

The lines are vitally needed because the world has built up $12.8 trillion of offshore dollar debt outside the Fed’s jurisdiction.

European, Japanese, and Canadian banks, among others, borrow on the capital markets at short-term maturities for worldwide lending in dollars. These markets can freeze up suddenly, as they discovered in October 2008.

Their own central banks are unable to print dollars and mostly have insufficient dollar reserves to provide emergency liquidity and stabilize the financial system in such circumstances. Only the Fed can act as the ultimate lender-of-last resort to the globalised dollar economy.

Mr Lipton said there was deep residual anger from the 2008 crisis. “People are hurt and they are less impressed than we that we did a clean-up afterwards,” he said.

He fears a nasty cocktail in the next downturn because much of the damage is likely to come from hidden leverage in asset management companies, with asset slumps hitting household wealth directly.

Mark Carney, the governor of the Bank of England, said at a separate Davos session that banks were now much safer than a decade ago, but risks of potentially systemic scale were building up elsewhere.

He raised a red flag over the money that has flooded into asset management, driven by a hunger for high yields after quantitative easing and low interest rates made it hard to generate returns.

The Achilles’ heel is the buildup of $30 trillion of assets held in funds, which are supposed to offer daily liquidity to investors but are invested heavily in underlying assets that not liquid. These assets are hard to sell “even in good times and very illiquid in bad times,” Mr Carney warned.

It is a classic example of borrowing short to invest long — the perennial cause of crises over the ages. There may also be further icebergs hidden from view. “Is there additional leverage in these entities that may add to the dynamics? That’s one of the big issues in global finance at the moment,” he said.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

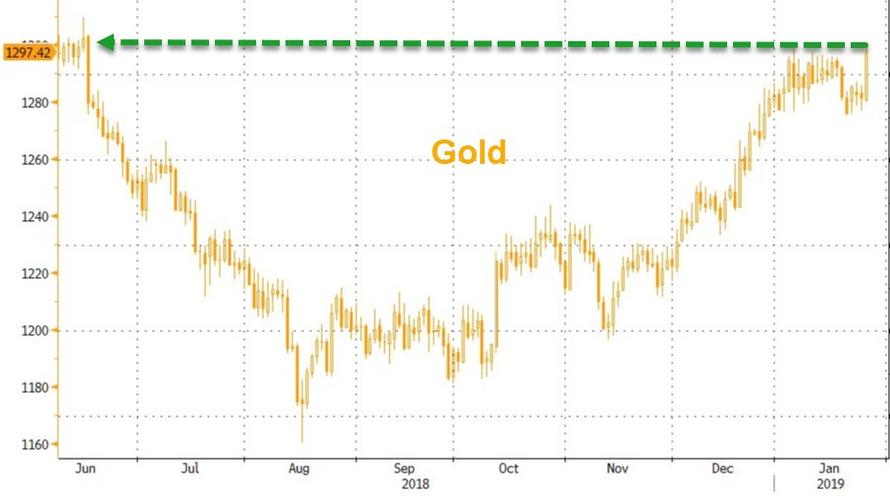

Gold Surges Above $1300 As Dollar Dumps

The dollar is nosediving this morning, tumbling to 10-day lows, having stumbled initially on the Stone news. As the dollar dumps, gold is spiking…

…trading back at $1300 at 7-month highs…

Gold is getting very close to a ‘Golden Cross’…

Gold futures show very heavy volume on this surge…

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7593/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS ON TRUCE/

//OFFSHORE YUAN: 6.7665 /shanghai bourse CLOSED UP 10.03 PTS OR 0.39%

HANG SANG CLOSED UP 448.21 POINTS OR 1.65%

2. Nikkei closed UP 198.93 POINTS OR 0.97%

3. Europe stocks OPENED ALL GREEN

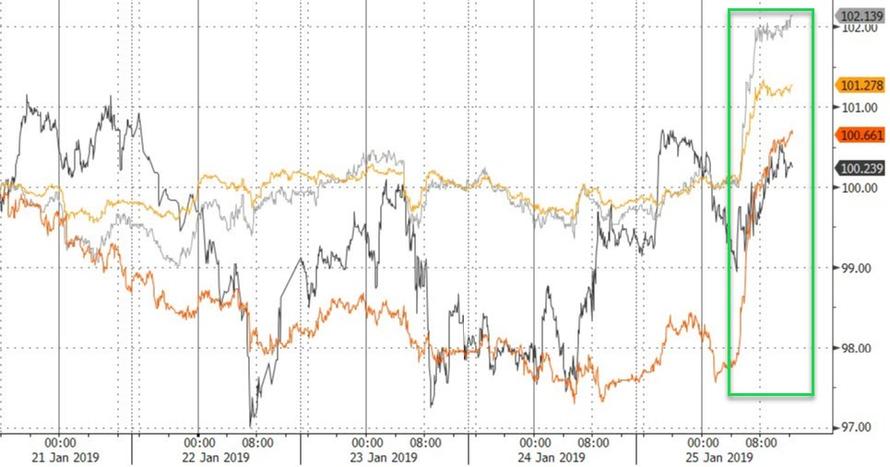

/USA dollar index RISES TO 96.32/Euro RISES TO 1.1345

3b Japan 10 year bond yield: FALLS TO. +.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.86/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.04 and Brent: 60.73

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.18%/Italian 10 yr bond yield DOWN to 2.66% /SPAIN 10 YR BOND YIELD DOWN TO 1.22%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.48: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.16

3k Gold at $1283.90 silver at:15.38 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 41/100 in roubles/dollar) 66.17

3m oil into the 53 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.86 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9968 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1308 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.18%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.73% early this morning. Thirty year rate at 3.05%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2743

Stocks Rally After Shrugging Off Trade Concerns, Dismal German Data

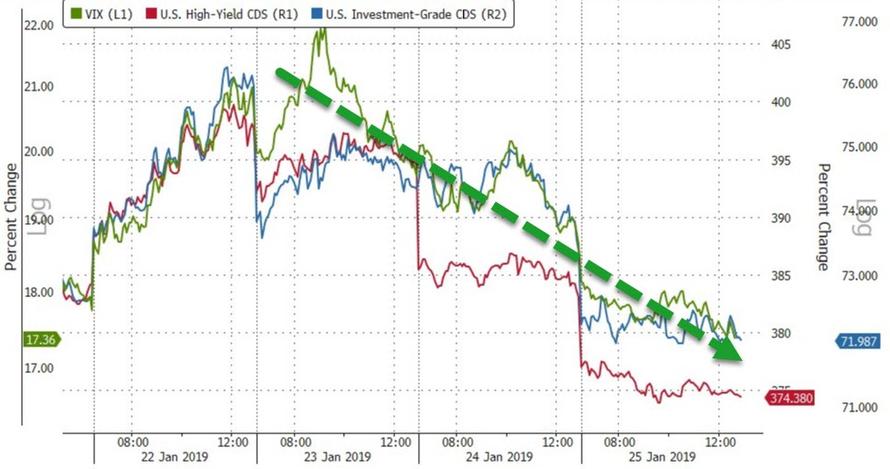

It’s a sea of green across global markets, which resumed their rally overnight with European stock and US equity futures following Asian peers higher, shrugging off softer numbers from tech giant Intel and weaker German IFO data, buoyed by strong earnings and optimism from some positive trade-related comments by U.S. officials ahead of next week’s meeting, while tech shares rallied. Gold and oil climbed, while the dollar hit session lows following news Trump advisor Roger Stone was arrested for witness tampering.

European markets opened higher, led by automakers and tech stocks which rose 1.5% and 1%, respectively. Europe’s STOXX 600 index hit its highest since Dec. 4, up 0.8% on the day. Trade optimism received a fresh boost of optimism after Bloomberg reported that a Chinese delegation including deputy ministers will arrive in Washington on Monday to prepare for high-level trade talks led by Vice Premier Liu He.

The euro gained even as German business sentiment measured by the IFO Survey fell for the 5th month in a row to 99.1 its weakest level in almost three years, while the expectations component tumbled to the lowest level since 2012; confirming a recession in Europe’s biggest economy is closer than most expect; core European sovereign bonds stabilized after rallying for most of the week.

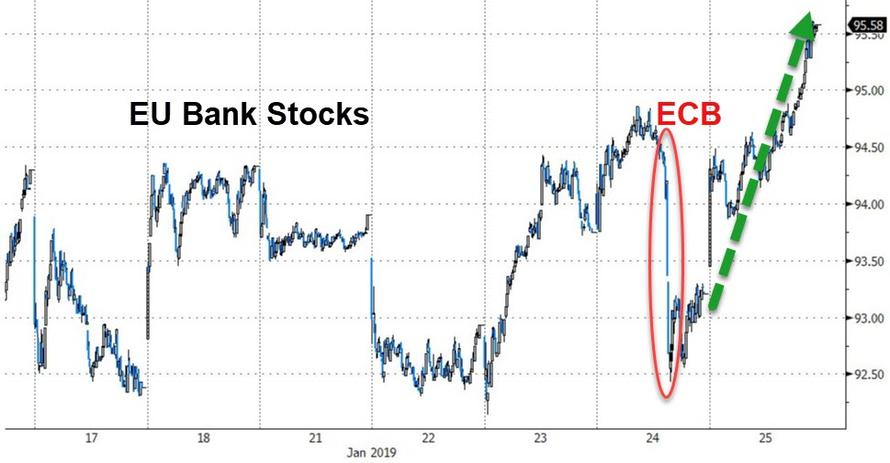

On Thursday, the euro fell to its lowest in six weeks following Thursday’s European Central Bank meeting in which Mario Draghi painted an increasingly downbeat picture of the European economy.

Europe’s gains came as stocks rose overnight in Asia and the United States on the back of strong earnings from U.S. tech firms. The MSCI All-Country World Index was up 0.3% on the day, but the gauge was set to break a four-week winning streak as weak economic data and cautious soundings from central banks pulled the index half a percent down on the week. Chipmaker and software stocks led the way in Asia, shrugging off weaker 2019 forecasts from Intel, which fell in pre-market trading.

Global stocks are poised for their first weekly drop of 2019, with investors questioning the validity of the post-Christmas rally as the earnings season rolls on. Traders are grasping at straws for hints at progress on trade ahead of discussions next week in Washington, while also assessing the economic impact of the 35-day government shutdown that’s hampering the normal flow of official data: “I’m reasonably positive,” Axel Merk, chief investment officer at Merk Investments LLC in San Francisco, told Bloomberg TV. “I don’t think we have an imminent recession which is usually one of the key ingredients to a real bear market, but it’s prudent to diversify.”

Markets reversed losses from earlier in the week even though according to the latest Reuters polls of hundreds of economists from around the world, a synchronized global economic slowdown is underway and any escalation in the U.S.-China trade war would trigger a sharper downturn, and despite a downgrade of US stocks to Neutral by Citi.

Offsetting the economic gloom, in a note to clients, UBS Global Wealth Management’s CIO Mark Haefele said that rhetoric on U.S.-China trade has become more positive, and that Beijing has taken steps to stimulate its economy.

“While economic and earnings growth is slowing, we believe it is unlikely that growth will drop far below trend,” he said. “At the same time, there are reasons to be cautious about policymakers’ ability to follow through on their rhetoric.”

Chinese Vice Premier Liu He will visit the United States on Jan. 30 and 31 for the next round of trade negotiations with Washington. The two sides are “miles and miles” from resolving trade issues but there is a fair chance they will get a deal, U.S. Commerce Secretary Wilbur Ross said on Thursday.

In US political news, President Trump said he wants a prorated down payment on the wall in any short-term government funding bill and that if Senate Majority Leader McConnell and Minority Leader Schumer can reach an agreement on government funding, he would support it. However, US House Speaker Pelosi said the idea of including a down payment on wall is a non-starter and Democrats were said to not support any kind of border wall funds which was made clear to McConnell, while Pelosi was later reported to postpone a press conference concerning counter offer to President Trump.

In central bank news, ECB dove Benoit Coeure said he sees a lot of political uncertainty and that economic slowdown is a surprise to the ECB, adds jury still out on how persistent slowdown will be and that rate guidance may have to be adjusted at some point. While, ECB’s Villeroy (Dovish) stated they remain committed to keeping interest rates low and ECB will probably downgrade the GDP forecast in March. Finally ECB’s Vasiliauskas (Hawkish) stated that there is no reason to change ECB guidance at the moment.

In currencies, the dollar fell 0.2%, hitting session lows shortly after news that Trump advisor Roger Stone had been arrested by the FBI. The euro rebounded 0.36% at $1.1345, recovering from a six-week low hit in the wake of ECB President Mario Draghi’s downbeat comments on Thursday. The ECB’s post-meeting statement for the first time since April 2017 alluded to “downside risks” to growth.

The British pound was also higher, rising 0.2 percent to $1.3076 after brushing a two-month high of $1.3140, lifted after The Sun reported on Thursday that Northern Ireland’s Democratic Unionist Party has privately decided to back May’s Brexit deal next week if it includes a clear time limit to the Irish backstop.

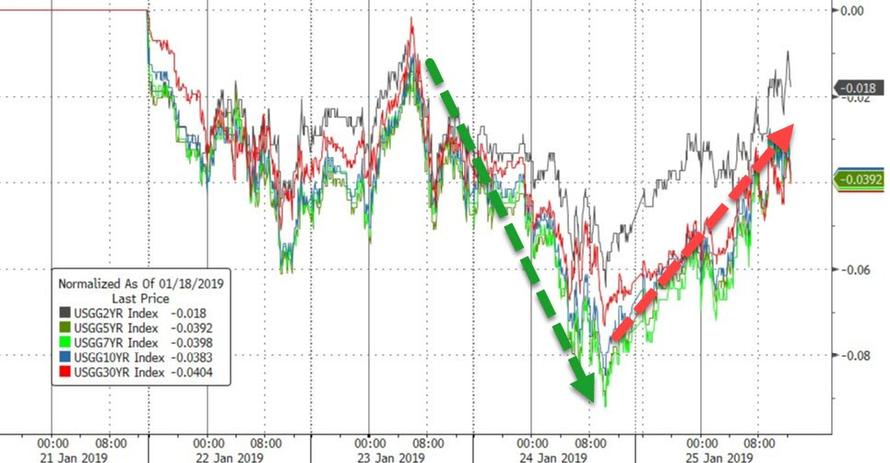

10-year U.S. Treasurys yields were slightly higher at 2.729% after dropping to a one-week low as pessimism over global growth supported safe-haven government debt.

In commodities, Brent (-0.1%) and WTI (+0.2%) prices are mixed and off of session highs, just under USD 62/bbl and USD 54/bbl respectively; in spite of yesterday’s unexpected EIA crude inventory build of 7.97mln vs. Exp. -0.042mln draw. Elsewhere, Russia was China’s largest crude oil supplier for December and 2018; with Russia being the largest crude supplier to China for the third year in a row. Gold (+0.3%) is marginally higher on the weakness in dollar, in spite of the positive risk sentiment reducing safe haven demand for the yellow metal. Copper prices are benefiting from market sentiment, whilst palladium has lost over 8% since reaching a high of just under USD 1400/oz last week.

Today’s publication of durable goods orders and new home sales is postponed by government shutdown. AbbVie and Colgate-Palmolive are reporting earnings.

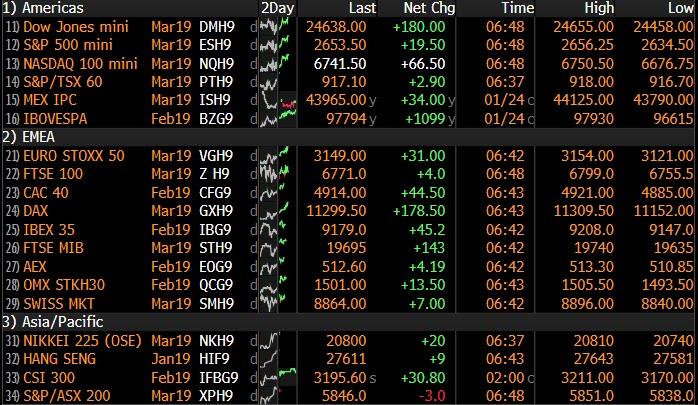

Market Snapshot

- S&P 500 futures up 0.6% to 2,650.75

- STOXX Europe 600 up 0.7% to 358.16

- MXAP up 1% to 154.44

- MXAPJ up 1.2% to 503.03

- Nikkei up 1% to 20,773.56

- Topix up 0.9% to 1,566.10

- Hang Seng Index up 1.7% to 27,569.19

- Shanghai Composite up 0.4% to 2,601.72

- Sensex down 0.6% to 35,985.79

- Australia S&P/ASX 200 up 0.7% to 5,905.61

- Kospi up 1.5% to 2,177.73

- German 10Y yield rose 0.8 bps to 0.188%

- Euro up 0.2% to $1.1330

- Italian 10Y yield fell 9.1 bps to 2.303%

- Spanish 10Y yield fell 2.0 bps to 1.22%

- Brent futures little changed at $61.13/bbl

- Gold spot up 0.2% to $1,283.61

- U.S. Dollar Index down 0.2% to 96.43

Top Overnight News

- A Chinese delegation including deputy ministers will arrive in Washington on Monday to prepare for high-level trade talks led by Vice Premier Liu He, according to people briefed on the matter

- Commerce Secretary Wilbur Ross said the U.S. and China are eager to end their trade war, but the outcome will hinge on whether Beijing will deepen economic reforms and further open up its markets. “We’re miles and miles from getting a resolution,” he said in an interview on CNBC on Thursday

- U.K. Chancellor of the Exchequer Philip Hammond warned that leaving the European Union without a deal would betray voters who were promised a “more prosperous future” if they chose Brexit. EU ties itself in knots on Irish border amid Brexit tension

- Senators began a new effort to end the 34-day partial government shutdown after blocking two rival spending bills. The White House signaled President Donald Trump was open to a plan to reopen agencies for three weeks, but at a price

- The Greek parliament’s historic vote on the agreement with the Republic of Macedonia over the latter’s name, was pushed to Friday, with not enough time for all listed lawmakers to speak Thursday

- Oil rose for a third day as a deepening crisis in Venezuela that threatens to complicate OPEC’s task of balancing world oil supplies outweighed a surprise jump in U.S. crude inventories

- Bank of England Governor Mark Carney said threats of jail for bankers are just a bluff and the real weapon to improve behavior is hitting pay packets

- U.K. Chancellor of the Exchequer Philip Hammond suggested he could quit the government in protest if the U.K. plunges out of the European Union with no-deal in nine weeks’ time

- Benoit Coeure and Francois Villeroy de Galhau — two of the top contenders to become the next ECB president — said they don’t know if the institution will be able to raise interest rates this year

A jubilant tone was observed across the Asia-Pac majors heading into the weekend, which followed the mostly positive performance of their global peers amid firmer US PMI data and a dovish tone from the ECB. ASX 200 (+0.7%) and Nikkei 225 (+1.0%) were buoyed by broad gains across the sectors and with Japanese exporters supported by favourable currency flows, although not all was rosy as healthcare lagged in Australia and steep losses in AMP Capital. Elsewhere, Hang Seng (+1.6%) and Shanghai Comp. (+0.4%) advanced as the 2nd phase of the PBoC’s RRR cut took effect and with outperformance seen in tech names including Tencent after regulators approved 2 of the Co.’s mobile phone games. However, gains in the mainland were initially capped after the PBoC‘s continued inaction resulted to a net weekly drain of CNY 770bln, in which it cited high liquidity levels due to the RRR cut. Finally, 10yr JGBs remained close to this week’s best levels after the prior day’s extended gains and with the BoJ also present in the market for government bonds with 5yr-10yr maturities, although prices have slightly eased with demand for bonds subdued by the risk appetite.

Top Asian News

- Goldman, Morgan Stanley Are Said to Ask to Cancel Jardine Trades

- Sinopec Says It Lost $688m on ‘Misjudged’ Oil Prices

- It’s Happy Friday Mode for Asia Traders as Stock Rally Lives On

- Yuan- Free FX Strategies for Betting on China. Or Against It

Major European indices are in the green [Euro Stoxx 50 +1.1%], the FTSE 100 (+0.4%) is the underperforming index given the impact of yesterday’s dovish ECB, alongside overnight sterling strength following reports that the DUP may agree to PM may’s deal if the Irish backstop has a time limit. The index is also weighed on by poor performance in Vodafone (-2.2%) who missed on their Q3 service revenue. Sectors are in the green, with underperformance in telecom names given the aforementioned earnings from Vodafone. Other notable movers include Telia (-3.3%) who are at the bottom of the Stoxx 600 after the Co. missed on Q4 revenue and adjusted EBITDA. Similarly, Givaudan (-3.3%) are near the bottom of the Stoxx 600 following a miss on Q4 revenue and adjusted EBITA.

Top European News

- ECB Presidential Contenders Wary on Chance of 2019 Rate Hike

- German Business Confidence Deteriorates Amid Heightened Risks

- Maersk Ready to Move Ahead With Drilling Unit IPO, CEO Says

- EU Ties Itself in Knots on Irish Border Amid Brexit Tension

- Russia Central Bank to Boost FX Buying as Ruble Steadies

In FX, the Dollar and overall index retraced some of yesterday’s trade and ECB-induced gains in which DXY reached highs just shy of 96.700. The index fell back below its 50 DMA at 96.549 and through the 96.500 level to currently hover nearer the bottom of a 96.300-530 range, with a 96.680 Fib also keeping the upside capped. Meanwhile, the US government shutdown is set to notch its 35th day after the US Senate blocked two competing proposals (although this was expected) and as a result today’s US building permits, durable goods and new home sales data will be postponed.

- EUR – Staging a recovery from post-ECB lows, when EUR/USD briefly lost the 1.1300 handle. Back above the level now, the single currency was largely unreactive to unsurprising narratives from ECB’s Coeure and Villeroy, while the release of an overall downbeat German ifo survey and downgrades in the ECB SPF also did little to wobble the Euro. EUR/USD now close to the top of a 1.1300-50 range ahead of a Fib level at 1.1351. In terms of option expiries, the pair sees EUR 1.96bln scattered around 1.1300-25, EUR 1.5bln between 1.1350-60 and EUR 2.8bln between 1.1375-1.1400.

- CAD – Rising oil prices and an easing buck sent USD/CAD back below its 50 DMA at 1.3350 to an intraday low of 1.3311 ahead of the psychological 1.3300 level with reported bids around the figure. A marginal pullback in energy sent USD/CAD back up to around the middle of a 1.3311-3361 band ahead of the Canadian budget balance release later today.

- GBP –Tumultuous day for the Pound after a Sun article provided Cable with the fuel to sky rocket past the 1.3100 handle to a high just shy of 1.3140, well above the December low of 1.2477. The article reported that PM’s coalition party, the DUP, are willing to back her Brexit deal if the Premier can get an expiry date to the backstop, though is widely expected to be rejected by the EC. Nonetheless, the idea of unity in the government aided the Pound to set fresh yearly highs vs. the buck. However, Cable has pared back most of the overnight gains, albeit holding just above its 200 DMA (1.3055-60) and closer to the bottom of 1.3057-3139 parameters.

- JPY – Choppy session thus far, but overall back on a decline amid the broad upturn in risk appetite around the market after USD/JPY rose above its 30 DMA at 109.79 to reach intraday highs of 109.91 (vs. low of 109.52) ahead of USD 1.2bln of option expiries at the 110.00 strike for the NY cut.

In commodities, Brent (-0.1%) and WTI (+0.2%) prices are mixed and off of session highs, just under USD 62/bbl and USD 54/bbl respectively; in spite of yesterday’s unexpected EIA crude inventory build of 7.97mln vs. Exp. -0.042mln draw. Elsewhere, Russia was China’s largest crude oil supplier for December and 2018; with Russia being the largest crude supplier to China for the third year in a row. Looking ahead we have the Baker Hughes rig count, where last week total rigs decreased by 25 to 1050. Gold (+0.3%) is marginally higher on the weakness in dollar, in spite of the positive risk sentiment reducing safe haven demand for the yellow metal. Copper prices are benefiting from market sentiment, whilst palladium has lost over 8% since reaching a high of just under USD 1400/oz last week.

US Event Calendar

- 8:30am: Durable goods orders data postponed by govt shutdown

- 10am: New home sales data postponed by govt shutdown

DB’s Jim Reid concludes the overnight wrap

As I finish this off I’m on the earliest train out of Davos and back to Zurich before travelling home. We had a DB drinks reception for our clients last night and one said to me that in 11 years of coming here the best advice would be to trade in the opposite direction to the main theme of the conference over the next 12 months. If you believe that then you should trade if favour of a return to globalisation trends in 2019 as the conference was generally concerned about its immediate path. Our CEO overheard this and said that on the main panel he was on, the head of the WTO was the contrarian. He said that 2019 will end up being around the lowest tariff year on record and an improvement on 2018. Clearly this relies on China and US either sorting out their differences or at least announcing a truce. However, it’s a reminder that although global trade has come off the peak, tariffs are still historically low outside of the main dispute. Personally, I think globalisation is in reverse but whether it’s a soft landing or not depends on policy. All to play for.

Back to the real (financial) world and yesterday lived up to the billing of being a busy day in markets with much weaker-than-expected European PMIs initially setting the tone. Draghi and the ECB then played for time – given March is where they get their latest staff forecasts – but acknowledged that risks were now to the downside. Elsewhere, Wilbur Ross downplayed expectations that a US-China trade deal is any closer, US jobless claims hit the lowest since around the time man first walked on the moon, and it was also a day where the government shutdown looked likely to continue for some time yet, even if there have been overnight attempts to find a deal to temporarily open government. So plenty to discuss.

However, by the end of play the main US equity indices hadn’t moved much as the S&P 500 eked out a +0.14% gain while the DOW dropped -0.09%. More positively, tech stocks rallied with the NASDAQ up +0.68%. The Philadelphia Semiconductor index advanced +5.73% on the back of strong earnings from Texas Instruments, Lam Research, and Xilinx. The STOXX 600 pared gains of as much as +0.49%, heading into negative territory after the ECB before closing +0.22%. Rates fell across the continent, as 10y Bunds and OATs finished -4.4bps and -5.0bps lower. BTPs outperformed, with yields down -9.3bps, to 2.66% and to the lowest level since last July. Treasuries rallied as well, with 10-year yields ending -2.5bps lower while the dollar rallied +0.45%.

The euro experienced sharp moves amid the data and ECB meeting. First, the single currency weakened around -0.44% following the soft PMI data (details below). It then held its level around 1.1340 as the ECB policy statement kept policy unchanged, which maintained forward guidance (“interest rates to remain at their present levels at least through the summer”) and said reinvestments will continue for an extended time beyond the first rate hike.

The euro then took another leg lower to 1.1307 after Draghi said the risks to the outlook have “moved to the downside.” However, this shift was ultimately viewed as somewhat incremental and the euro retraced all its moves to return to flat on the session as the press conference continued. Draghi confirmed that the Council decision was unanimous on changing the outlook but that the Council “didn’t discuss policy implications”. There was apparently “unanimity” among the council supporting the view that the “likelihood of recession is low”, but DB’s Mark Wall thinks the Governing Council is divided on the outlook, between one camp who expect uncertainties (Brexit, trade, etc.) to be resolved positively and another who is more worried about European domestic demand. The tension between these two views will probably not be resolved until the ECB publishes new staff forecast at its March meeting. Mark’s full thoughts are available here.

On other policy questions, there was also no decision made on TLTRO, although it was mentioned by several officials and clearly talked about, while the positive side effects were talked up by Draghi later on. That perhaps leaves the option open for March but didn’t provide any insight beyond that. The issue of negative rates and their impact on banks was also posed to Draghi, however, it was mostly a repeat of the line he used in December. Draghi specifically said that “we have to see how the continuation of negative rates will affect this balance” in response to a question on if the ECB would have to do something about it. Again a non-committal answer.

As highlighted earlier, in the midst of Draghi speaking, headlines also hit the wires from across the pond and specifically comments from US Trade Secretary Ross. He said that the US and China were “miles and miles” away from a resolution, which caused a kneejerk reaction in markets but then followed by saying that there is a “fair chance” that the two countries would arrive at a trade deal. He also added that it was “unlikely” that next week’s meetings between the two sides would result in a final solution. Crystal clear then. Later on, Director of the National Economic Council Larry Kudlow said that President Trump was optimistic about talks with China, so no shortage of noise on the trade front.

President Trump himself tweeted later in the session about the ongoing government shutdown, saying “We will not Cave!” and escalating the tension. The senate voted on two bills to reopen government, but neither received enough support to pass. Overnight, the debate has seemingly moved on as to whether government could reopen for three weeks if Mr Trump received a down payment for the wall. Pelosi has already poured cold water on the idea but it perhaps shows that negotiations aren’t completely breaking down. In the background, the Washington Post reported that White House Chief of Staff Mick Mulvaney has asked all executive departments and agencies for lists of their highest-impact programs which could be negatively affected if the shutdown continues into March or April. Probably always good to prepare for the worst, but such a long shutdown, if realised, would have serious implications for the US economy.

In Asia this morning, technology stocks are leading markets higher, with the Nikkei (+1.06%), Hang Seng (+1,34%), Shanghai Comp (+0.57%) and Kospi (+1.49%) all moving upwards. Other significant news overnight has come from the UK, where sterling rose 0.5% against the dollar to its highest level in over two months, after the Sun reported that the DUP would be prepared to back Prime Minister May’s Brexit deal if there were a time limit to the Irish backstop. The news comes ahead of Tuesday’s debate in the House of Commons, where Parliament will have the opportunity to vote on a variety of amendments put forward by MPs to May’s Brexit plan.

Back to the details of the PMIs, which actually ended up requiring a bit of digging through such was the disparity between sectors and countries. However, the bottom line is that momentum is certainly weaker. The composite reading for the Euro Area for instance came in at 50.7 compared to expectations for 51.4. That’s also down 0.4pts from the soft December reading and is the lowest now since July 2013. The data is also consistent with GDP growth of just +0.1% qoq, which paints downside risks to the consensus forecast for 2019 growth of around 1.3% (DB 1.2%). In terms of sectors, manufacturing slumped more, by 0.9pts to 50.5 (vs. 51.4 expected) while the services reading fell 0.4pts to 50.8 (vs. 51.5 expected). As you can see though both were much softer than expected.

What was interesting was the split between Germany and France. In France the services reading tumbled further by 1.5pts to 47.5 (vs. 50.5 expected) and to the lowest in nearly 5 years. The manufacturing reading bounced back in contrast to 51.2 (vs. 50.0 expected) from 49.7, however, the extent of the drop in the services reading left the composite at 47.9 versus 48.7 in December. So rather worryingly there was little sign of a rebound after recent protests. In Germany the pain was reserved for the manufacturing sector, which tumbled to 49.9 from 51.5. That’s the first sub-50 reading since November 2014. The services reading did, however, rise 1.4pts to 53.1, which left the composite at 52.1 and up 0.5pts from December. Our economists also highlight that the implied non-core PMI numbers aren’t pretty with the implied non-core composite down 1pt equally, shared by the manufacturing and services sectors. Manufacturing PMIs for Italy and Spain will print next Friday alongside the final readings across the globe.

The associated statement with the PMIs highlighted “ongoing auto sector weakness, Brexit worries, trade wars and the protests in France” as reasons dampening growth in both sectors but also that the survey responses “indicate that a deeper malaise has set in at the start of the year” and that “companies are concerned about a wider economic slowdown gathering momentum, with rising political and economic uncertainty increasingly affecting risk appetite and demand”. With the manufacturing reading for the Euro Area and Germany now down in 12 of the last 13 months, a quick refresh of our equity versus PMI regression analysis shows that the STOXX and DAX are still around 14% and 17% ‘cheap’ respectively and that implied PMIs are actually more like 46.0 for the Euro Area and 43.7 for Germany based on equity markets. France looks 16% ‘cheap’ by the same measure. So despite the decline in PMIs, equity markets have oversold by this basic measure in Europe. However, for there to be a sustainable rebound, the PMIs need to find a base. Something they have struggled to do for over a year now.

In the US, initial jobless claims fell to 199k, the lowest level since 1969, as the US labour market continues to strengthen. Continuing claims fell from 1,737k to 1,713k, near the cyclical and multi-decade lows. The US PMIs, while not as significant as the European vintages, showed some improvement with the manufacturing index up to 54.9 from 53.8. The services reading fell 0.2pts to 54.2, while the composite print ticked up to 54.5 from 54.4. The Kansas City Fed’s manufacturing index rose to 5 from 3, though the anecdotal details suggested some concerns over both tariffs and the government shutdown. Altogether, the PMIs and KC Fed index did not move the needle for our expectations of next Friday’s ISM manufacturing report.

Finally, the day ahead will feature the January IFO survey in Germany this morning along with the January CBI reported sales survey in the UK. The US session is meant to feature the December durable and capital goods orders data, as well as the January new home sales print, however, the government shutdown will delay that once more. The earnings calendar features AbbVie and Colgate-Palmolive, as well as Ericsson in Europe.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 10.03 PTS OR 0.39% //Hang Sang CLOSED UP 448.21 POINTS OR 1,65% /The Nikkei closed UP 198.93 PTS OR 0.97%/ Australia’s all ordinaires CLOSED UP 0.68%

/Chinese yuan (ONSHORE) closed UP at 6.7595 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.04 dollars per barrel for WTI and 60.73 for Brent. Stocks in Europe OPENED /GREEN

//. ONSHORE YUAN CLOSED UP AT 6.7595 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7665: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i)CHINA/USA

Our resident expert on Chinese affairs, Gordon Chang offers a good look at China’s ambitions and the continuing hostility showed by Chinese generals and admirals

(courtesy Gordon Chang)

Opposing China’s Dangerous Ambitions

Authored by Gordon Chang via The Gatestone Institute,

- Admiral John Richardson is apparently worried about a lack of communication. Communication is not the problem. The problem is that Chinese generals and admirals have been and continue to be hostile, belligerent, and bellicose.

- “We do not want war. This is how you prevent it. Remember, show overwhelming power not indecision or weakness. Some Chinese will read the smoke signals correctly.” – Arthur Waldron, University of Pennsylvania.

- The best way to avoid conflict in the Taiwan Strait is to make it clear to Beijing that America will defend Taiwan.

- In the first half of 2012, the U.S., despite firm obligations to defend the Philippines, did nothing when China took over Scarborough Shoal in the South China Sea. When Chinese generals and admirals saw Washington’s failure to act, they turned the heat on other Philippine reefs and islets, went after Japan’s islands in the East China Sea, and began reclaiming and militarizing features in the Spratly chain. Feebleness only emboldens Chinese aggression. There will be no good endings in Asia until Washington disabuses Beijing of the arrogant belief that it can take whatever it demands.

The sharp downturn in ties between the world’s two most fearsome militaries was evident when America’s highest naval officer, Chief of Naval Operations Admiral John Richardson, went to Beijing this month. Pictured: Admiral Richardson (right) is greeted by senior Chinese defense officials at the People’s Liberation Army Naval Research Academy in Beijing, on January 14, 2019 (U.S. Navy photo)

The sharp downturn in ties between the world’s two most fearsome militaries was evident when America’s highest naval officer, Chief of Naval Operations Admiral John Richardson, went to Beijing this month.

Chinese officers were ready for Richardson: they issued hostile words, especially about U.S. relations with Taiwan. In response, CNO Richardson stuck to Washington’s decades-old script of cooperation.

It is time for American policymakers to change that script by, among other things, dropping themes of engagement, introducing notions of reciprocity, and showing resolve of their own.

Richardson struck an upbeat note as he left China on his second official visit as America’s top admiral.

“I very much appreciate the hospitality I received in China,” he tweeted on January 16.

“I had some great discussions with my counterparts and I look forward to strengthening our relationship as we move forward.”

The admiral’s words were in sharp contrast to those of the Chinese counterparts. They threatened military action against the United States. Moreover, Global Times, the tabloid controlled by the Communist Party’s People’s Daily, in an editorial, made veiled threats directed at Richardson.

“Beijing needs to take practical action to help the U.S. correct its vision,” the paper noted, after referring to military action to enforce Beijing’s expansive territorial claims.

“China must have the ability to make rivals pay unbearable costs.”

The mismatch in the tone of the American and Chinese messaging suggest that something might possibly be wrong.

For a start, something definitely seems wrong at the top of the People’s Liberation Army. Twice last month, senior Chinese officers publicly urged unprovoked attacks on the U.S. Navy. In the second of the outbursts, on January 20, Rear Admiral Luo Yuan said he wanted to use Dong Feng-21D and Dong Feng-26 ballistic missiles to sink two aircraft carriers and create 10,000 American “casualties.”

Although these bellicose statements do not represent official policy, they can nonetheless be seen as reflecting thinking in senior officer ranks. In any event, they should be deeply troubling.

The proper American response was not Richardson’s “I look forward to continuing our dialog as we seek common ground and opportunities for cooperation.” Richardson’s response should have been, “I am cancelling my trip to China.”

Richardson, prior to the China trip, defended his visit:

“A routine exchange of views is essential, especially in times of friction, in order to reduce risk and avoid miscalculation. Honest and frank dialogue can improve the relationship in constructive ways, help explore areas where we share common interests, and reduce risk while we work through our differences.”

“Common interests”? We hear not only unacceptably belligerent words from Luo and others; we have been seeing, and still see, dangerous Chinese actions in the global commons.

On September 30, the Lanzhou, a Chinese destroyer, came within 45 yards of the USS Decatur as it crossed the bow of the American warship near Gaven Reef in the South China Sea. The Decatur had to swerve to avoid a collision. The U.S. Navy diplomatically called the Lanzhou’s maneuverings “unsafe and unprofessional.”

Despite the risky conduct — and despite Beijing’s denial of a requested Hong Kong port call for the USS Wasp for October — the U.S. Navy sought permission for the Ronald Reagan Strike Group to pay a port call in Hong Kong, a special administrative region of People’s Republic of China, just weeks after the Decatur-Lanzhou incident.

James Fanell, a leading commentator on U.S. Navy interactions with China, told Gatestone that the port-call request undermined President Trump’s tougher policy line:

“What seems clear is that the PRC has successfully convinced generations of Pentagon leaders that ‘mil-to-mil’ relations are important for promoting security, despite the overwhelming empirical evidence proving otherwise.”

Fanell, who as a captain served as the chief intelligence officer for the Pacific Fleet, is correct about the evidence. Over time, the Chinese military has conducted a series of dangerous intercepts of the U.S. Navy and Air Force on and over the South China Sea and East China Sea.

Admiral Richardson is apparently worried about a lack of communication. Communication is not the problem. The problem is that Chinese generals and admirals have been and continue to be hostile, belligerent, and bellicose.

Moreover, no amount of talking is going to make these flag officers less so. In fact, American efforts at dialogue are making matters worse. U.S. Navy admirals may think they are acting responsibly and constructively, but the Chinese are obviously perceiving weakness and acting accordingly. The most likely explanation for Luo’s comments last month is that he thought America can be intimidated into leaving the region.

General Li Zuocheng, a member of the Communist Party’s Central Military Commission, also attempted intimidation. He told Richardson in Beijing that the People’s Liberation Army would bear “any cost” to prevent foreign interference in Taiwan matters.

After leaving China, Richardson, to his great credit, suggested sending a carrier strike group through the Taiwan Strait. “We don’t really see any kind of limitation on whatever type of ship could pass through those waters,” he told reporters in Tokyo.

The next step for the U.S. is to drive a carrier through the Strait, as the Navy last did in 2007 after the Chinese denied a port call in Hong Kong.

Why stop with just one carrier strike group? Arthur Waldron of the University of Pennsylvania told Gatestone that, to make a lasting impression on Beijing, the U.S. should arrange a Taiwan Strait passage with not only the supercarrier Ronald Reagan but also a flotilla of “some Japanese subs and the Izumo; any British, French, or Australian ships available; and the Taiwan navy shadowing it.” He also recommends sending along planes to add to the effect.

“We do not want war,” Waldron wrote in a message to defense professionals last week.

“This is how you prevent it. Remember, show overwhelming power not indecision or weakness. Some Chinese will read the smoke signals correctly.”

The best way to avoid conflict in the Taiwan Strait, as Waldron suggests, is to make it clear to Beijing that America will defend Taiwan. In the last two months, Beijing has been making threats to invade. Unfortunately, as Joseph Bosco, a former China desk officer in the Office of the Secretary of Defense, points out, the best Washington can do at the moment is issue “mushy diplomatese” that the Chinese can interpret as a lack of American resolve.

“You can bet,” Bosco told Gatestone last week, “China’s calculations would change dramatically if President Trump or Secretary Pompeo or the new SecDef or John Bolton were to utter these words publicly to Beijing: ‘We will defend Taiwan under any circumstances.'”

That would, he said, “effectively reconstitute the 1954 U.S.-Taiwan mutual defense treaty” and “alter the strategic dynamic in Washington’s and Taipei’s favor.”

Some — actually a lot — of “altering” is absolutely necessary, and now is not a moment too soon. In the first half of 2012, the U.S., despite firm obligations to defend the Philippines, did nothing when China took over Scarborough Shoal in the South China Sea. When Chinese generals and admirals saw Washington’s failure to act, they turned the heat on other Philippine reefs and islets, went after Japan’s islands in the East China Sea, and began reclaiming and militarizing features in the Spratly Islands chain. Feebleness only emboldens Chinese aggression.

There will be no good endings in Asia until Washington disabuses Beijing of the arrogant belief that it can take whatever it demands.

How to do that? Perhaps, in addition to sailing through the Taiwan Strait, Admiral Richardson can arrange for a few U.S. Navy vessels to make a port call on the island and linger for a while.

end

Futures rally on a report Vice Ministers are heading to Washington for trade talks. Nothing is going to happen in these talks unless Meng is released from a Cdn jail and the USA must stop its extradition of her

(courtesy zerohedge)

Futures Rally On Report Chinese Vice Ministers Heading To Washington For Trade Talks

Given that algos aren’t widely regarded for their ability to detect nuance, Wilbur Ross’s comment yesterday that the US and China remained “miles and miles” apart on trade (though he clarified that this “shouldn’t be too surprising” since the most important talks had yet to take place) ignited a selloff that prompted one of the worst daily selloffs in US stocks since the earliest trading days of the year.

It was only the latest example of Trump administration officials seemingly taking turns talking up – and talking down – the prospects for a trade deal. But with the administration fearful of a sustained selloff – particularly when trade optimism is seemingly the only bulwark against more market chaos – the White House has found a way to reassure investors once again that everything is as it should be with the deadline for a trade agreement looming in the not too distant future.

And ironically, the news that’s sparking optimism in the equity space on Friday is confirmation that a delegation led by two senior Chinese ministers would head to Washington next week to prime the pump for a visit by Liu He, China’s top trade negotiator, and a group of other senior officials later this month.

Though they would seem to undermine the credibility of all future trade-related denials, the report published by Bloomberg, which follows denials by both the White House and Beijing of an FT report claiming that the US had cancelled the meeting (which sent markets into a tailspin early this week), has helped renew optimism in the trade-talk process on Friday.

A Chinese delegation including deputy ministers will arrive in Washington on Monday to prepare for high-level trade talks led by Vice Premier Liu He, according to people briefed on the matter.

Vice Commerce Minister Wang Shouwen and Vice Finance Minister Liao Min will arrive in the U.S. on Jan 28, according to two of the people who asked not to be named as the discussions aren’t public. China’s central bank governor Yi Gang will join the talks, one of the people said. It wasn’t immediately clear which other officials will attend.

Liu will arrive in the US on Jan. 30 to meet with Trade Rep Robert Lighthizer for talks that the US has billed as “very, very important”. At that point, with only five weeks remaining until the deadline for escalating tariffs on $200 billion in Chinese goods, investors should start to get an idea of the likelihood of an amicable outcome.