GOLD: $1310.80 UP $0.65 (COMEX TO COMEX CLOSING)

Silver: $15.91 UP 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1319.20

silver: $16.08

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 0 NOTICE(S) FOR nil OZ (0.000 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 585 NOTICES FOR 58500 OZ (1.8195 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

8 NOTICE(S) FILED TODAY FOR 40,000 OZ/

total number of notices filed so far this month: 1178 for 5,890,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3444: UP 32

Bitcoin: FINAL EVENING TRADE: $3418 DOWN $15

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2295 CONTRACTS FROM 192,066 UP TO 194,895 ACCOMPANYING YESTERDAY’S 9 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2021 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2021 CONTRACTS. WITH THE TRANSFER OF 2021 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2021 EFP CONTRACTS TRANSLATES INTO 10.105 MILLION OZ ACCOMPANYING:

1.THE 9 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.805 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 42,437 CONTRACTS (FOR 20 TRADING DAYS TOTAL 42,437 CONTRACTS) OR 212.185 MILLION OZ: (AVERAGE PER DAY: 2224 CONTRACTS OR 11.120 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 212.185 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 30.312% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 212.185 MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2295 WITH THE 9 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2021 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 4316 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2021 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2295 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 9 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.84 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .974 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 8 NOTICE(S) FOR 40,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.825 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUGE SIZED 46,978 CONTRACTS DOWN TO 483,390 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $6.15//YESTERDAY’S TRADING).

THE LOSS IN OPEN INTEREST IS DUE TO SPREADERS WHO MUST LIQUIDATE THEIR POSITIONS AS THEY COME INTO AN ACTIVE DELIVERY MONTH. SINCE FEBRUARY IS AN ACTIVE MONTH FOR GOLD, THIS IS WHY WE ALWAYS SEE A CONTRACTION IN OPEN INTEREST ONCE WE APPROACH FIRST DAY NOTICE. SINCE THE SPREADERS HAVE AN IDENTICAL LONG AND SHORT POSITION, THE LIQUIDATION DOES NOT AFFECT PRICE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 10,460 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 10,460 CONTACTS APRIL 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 483,390. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 36,518 CONTRACTS: 46,978 OI CONTRACTS DECREASED AT THE COMEX AND 10,460 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 36,518 CONTRACTS OR 3,651,800 OZ = 113.5 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $6.15.

YESTERDAY, WE HAD 8597 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 159,521 CONTRACTS OR 15,952,100 OZ OR 496.18 TONNES (20 TRADING DAYS AND THUS AVERAGING: 7845 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 496.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 496.18/2550 x 100% TONNES = 19.45% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 496.18 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 46,978 (WITH THE MAJORITY OF THE LOSS COMING FROM THE LIQUIDATION OF THE SPREADERS) DESPITE THE GAIN IN PRICING ($6.15) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,460 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10460 EFP CONTRACTS ISSUED, WE HAD A HUGE LOSS OF 36,518 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,460 CONTRACTS MOVE TO LONDON AND 46,978 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 113.5 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $6.15 IN YESTERDAY’S TRADING AT THE COMEX

we had: 0 notice(s) filed upon for nil oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.65 TODAY

ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD

A DEPOSIT OF 8.23 TONNES OF PAPER GOLD INTO THE GLD

THE GLD AND SLV ARE ABSOLUTE FRAUDS//THERE IS NO METAL BEHIND THEM.

/GLD INVENTORY 823.87 TONNES

Inventory rests tonight: 823.87 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 7 CENTS IN PRICE TODAY:

ANOTHER BIG CHANGE IN SILVER INVENTORY/

A “PAPER DEPOSIT” OF 938,000 OZ

/INVENTORY RESTS AT 309.597 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 2295 CONTRACTS from 192,600 UP TO 194,895 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2021 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2021 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2295 CONTRACTS TO THE 2021 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 4316 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 21.65 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.845 MILLION OZ STANDING IN JANUARY..

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD A GOOD SIZED 2021 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 18.68 PTS OR 0.72% //Hang Sang CLOSED UP 111.17 POINTS OR 0.40% /The Nikkei closed DOWN 108.10 PTS OR 0.52%/ Australia’s all ordinaires CLOSED UP .20%

/Chinese yuan (ONSHORE) closed UP at 6.7170 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.48 dollars per barrel for WTI and 60.53 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.7170 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7295: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/HUAWEI

The fight with the uSA intensifies. Now Huawei asks its suppliers to move production out of the USA

( zerohedge)

4/EUROPEAN AFFAIRS

UK

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)/Russia

6. GLOBAL ISSUES

7. OIL ISSUES

It now looks like we are having legal piracy in the Caribbean has Venezuela has not paid its docking fees. Authorities have followed the ConocoPhillips model of seizing vessels for non payment of fees.

( zerohedge)

8 EMERGING MARKET ISSUES

VENEZUELA/

The USA hands over dollars held at the Fed over to Guaido. Russia has voiced their concern on this as they state that it is Maduro’s government is the real authority. Russia lent Venezuela 3 billion dollars. China also has vast interests inside Venezuela after they have lent considerable amounts of money to them.

( zerohedge)

9. PHYSICAL MARKETS

iii)Mysterious Russian plane removes 20 tonnes of gold from Venezuela’s vaults.

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

( zerohedge)

ii)Market data/

Pending homes sales crash 2.2% month over month. This is a hard data report

(courtesy zerohedge)

a)Apple stock jumps after the algos jump on them beating muted expectations. However iphone sales drop 15% and Chinese sales plunge 5 billion dollars.

Another good Bellwether as to growth growth

( zerohedge)

b)For the second time ever Apple cuts its iphone prices

iv)SWAMP STORIES

a)Trump claims that there is not going to be any deal to consider a wall. Thus he must use his emergency measures to do the deed

( zerohedge)

b)Trump slams his own intelligence officials to “go back to school” with respect to ISIS. He also tells the Deep State to be careful on Iran although economically he has destroyed them

(courtesy zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 24 CONTRACTS DOWN TO 405. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI GAINED BY 1523 CONTRACTS UP TO 139,346 CONTRACTS.

COMPARISON VS LAST YR:

AS A COMPARISON TO LAST YEAR WITH 1 DAY TO GO BEFORE FIRST DAY NOTICE WE HAD 136 CONTRACTS STANDING FOR DELIVERY (VS 405 TODAY/1 DAY BEFORE FIRST DAY NOTICE).

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH AND FEB 2018

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

ON FIRST DAY NOTICE FEB 1 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

U.S.-China War May Be “Just A Shot Away”

– “World’s most dangerous hotspot” is in the South China Sea

– Currency and trade wars can lead to shooting wars warns Rickards

– Chinese buildup in South China Sea like ‘preparing for World War III’ says US senator (see news)

– U.S.-China shooting war could be, as Mick Jagger put it, “just a shot away…”

/arc-anglerfish-arc2-prod-mco.s3.amazonaws.com/public/Z2CQDQ5QBFGXFL5KO5SWQJRPWQ.jpg)

Chinese President Xi Jinping speaks after reviewing the Chinese People’s Liberation Army Navy fleet in the South China Sea on April 12. Xi has urged the PLAN to better prepare for combat, according to state media reports. (Li Gang/Xinhua via AP)

The World’s Most Dangerous Hotspot

By Jim Rickards for the Daily Reckoning

I have warned repeatedly that currency wars and trade wars can lead to shooting wars. Both history and analysis support this thesis.

Currency wars do not exist all the time; they arise under certain conditions and persist until there is either systemic reform or systemic collapse. The conditions that give rise to currency wars are too much debt and too little growth.

In those circumstances, countries try to steal growth from trading partners by cheapening their currencies to promote exports and create export-related jobs.

The problem with currency wars is that they are zero-sum or negative-sum games. It is true that countries can obtain short-term relief by cheapening their currencies, but sooner than later, their trading partners also cheapen their currencies to regain the export advantage.

This process of tit-for-tat devaluations feeds on itself with the pendulum of short-term trade advantage swinging back and forth and no one getting any further ahead.

After a few years, the futility of currency wars becomes apparent, and countries resort to trade wars. This consists of punitive tariffs, export subsidies and nontariff barriers to trade.

The dynamic is the same as in a currency war. The first country to impose tariffs gets a short-term advantage, but retaliation is not long in coming and the initial advantage is eliminated as trading partners impose tariffs in response.

Despite the illusion of short-term advantage, in the long-run everyone is worse off. The original condition of too much debt and too little growth never goes away.

Finally, tensions rise, rival blocs are formed and a shooting war begins. The shooting wars often have a not-so-hidden economic grievance or rationale behind them.

The sequence in the early 20th century began with a currency war that started in Weimar Germany with a hyperinflation (1921–23) and then extended through a French devaluation (1925), a U.K. devaluation (1931), a U.S. devaluation (1933) and another French/U.K. devaluation (1936).

Meanwhile, a global trade war emerged after the Smoot-Hawley tariffs (1930) and comparable tariffs of trading partners of the U.S.

Finally, a shooting war progressed with the Japanese invasion of Manchuria (1931), the Japanese invasion of Beijing and China (1937), the German invasion of Poland (1939) and the Japanese attack on Pearl Harbor (1941).

Eventually, the world was engulfed in the flames of World War II, and the international monetary system came to a complete collapse until the Bretton Woods Conference in 1944.

Is this pattern repressing itself today?

Sadly, the answer appears to be yes. The new currency war began in January 2010 with efforts of the Obama administration to promote U.S. growth with a weak dollar. By August 2011, the U.S. dollar reached an all-time low on the Fed’s broad real index.

Other nations retaliated, and the period of the “cheap dollar” was followed by the “cheap euro” and “cheap yuan” after 2012.

Once again, currency wars proved to be a dead end.

Now the trade wars are well underway. They may be set to resume once the current “truce” between the U.S. and China expires on March 1. If no deal is reached, massive new tariffs will likely take effect.

But the biggest question now is if a shooting war will follow.

There’s little doubt that the most dangerous place in the world today in terms of potential war has been the South China Sea.

I have written frequently about possible confrontations between the U.S. and China in the South China Sea. International law recognizes claims of six separate nations to parts of that sea, and the U.S. is treaty partners with one of them (the Philippines).

China claims the entire sea (except for a narrow shoreline stretch near each surrounding country). China is claiming control based on ancient imperial arrangements and argues that the West and its South Asian allies “stole” the territory from them.

China has aggressively built up man-made islands in the area by dredging sand onto rocks and atolls. These islands are then being fortified with airstrips, anti-aircraft weapons and surveillance technology.

But both the ancient claims and the theft narrative are open to serious dispute. The U.S. and the other nations involved reject those claims and insist on rights of passage and free navigation and sharing of natural resources such as oil, natural gas, undersea mining and seafood among others.

The U.S. and its allies, including Japan and the U.K., have sent naval vessels to cruise waters claimed by China and to uphold rights of passage and their status as open waters.

But the South China Sea is not the only body of water where the conflicts and risks exist.

An even greater potential conflict lies in the Strait of Taiwan, which separates the island of Formosa from the mainland of Red China. China claims Taiwan as a “breakaway province” and part of China. The Taiwanese government claims that it is the lawful government of all of China, although there is a strong independence movement there also.

Two U.S. warships recently passed through the strait as a reaffirmation of rights of free passage and a show of support for Taiwan.

China regards the passage of U.S. vessels as highly provocative and has threatened to block such transits with force. The South China Sea is a problem, but the Taiwan Strait is viewed in existential terms by China.

The entire situation is like a powder keg waiting for the match to light it. The risks include not only intentional combat but accidental shootings and collisions, which are not uncommon at sea, especially when two vessels are shadowing each other.

In fact, the greatest risk might not be an outright attack by either side but an accident or miscommunication that escalates into a firefight. We cannot avoid the real possibility that conflicting naval activities in both bodies of water will result in a violent incident or even war. And once an incident occurs, it could set off a chain of escalation that could result in open warfare.

Trump is not someone to back down when it comes to American interests around the world, and Chinese leadership does not want to appear weak before the U.S.

That’s especially true at a time of great economic uncertainty. Communist Party leadership is desperate to maintain the support of the people, or else it risks losing the “mandate of heaven.”

China does not want war at this time. But diverting the people’s attention away from domestic problems toward a foreign foe is an old trick leaders use to unite the people in times of uncertainty. Rallying the people around the flag is a tried and true method to garner support.

If China’s leadership decides that the risk of losing legitimacy at home outweighs the risk of conflict with the United States, the likelihood of war rises dramatically.

I’m not predicting it, but wars have started over less. Currency wars, trade wars, finally shooting wars. We’re currently two-thirds of the way there.

And as Mick Jagger sang, a U.S.-China shooting war is “just a shot away.”

Regards,

Jim Rickards

via The Daily Reckoning email

News and Commentary

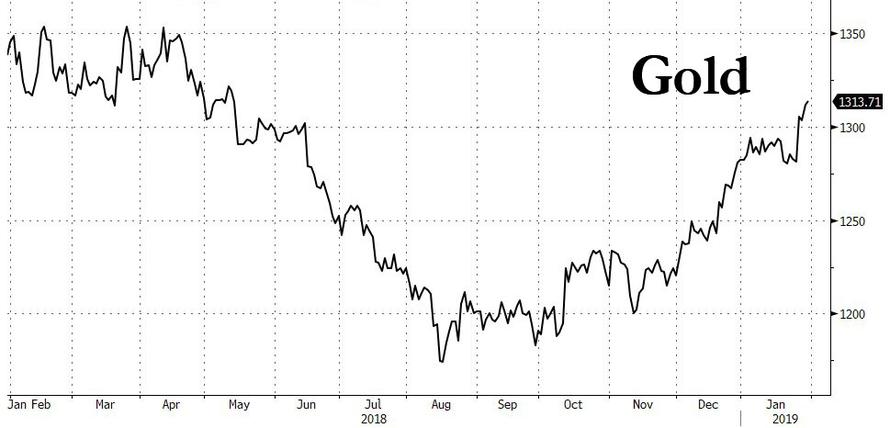

Gold hits eight-month peak on U.S.-China trade woes (CNBC.com)

Gold ends at highest since June, up a third straight session (MarketWatch.com)

Gold Hits 8-Month Highs as Fed Decision Looms (Investing.com)

Palladium to fall behind gold but leave platinum in the dust: Reuters poll (Reuters.com)

May Wins Backing to Reopen Brexit Deal as EU Prepares to Dig In (Bloomberg.com)

Iron Ore Rockets as Vale’s Supply Disruption Convulses Market (Bloomberg.com)

Source: WGC via Marketwatch

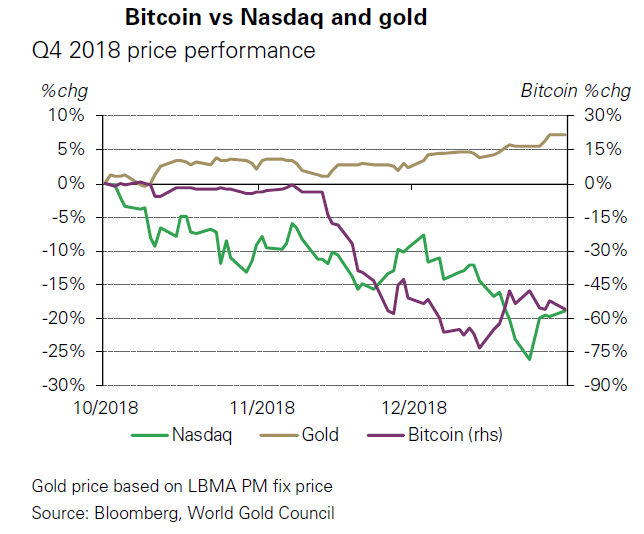

Here’s Why Bitcoin Isn’t The Next Gold, In One Chart (MarketWatch.com)

After Long Slump, ‘This Could Be Gold’s Year’ (CNBC.com)

Venezuela Has 20 Tons of Gold Ready to Ship. Address Unknown (Bloomberg.com)

This Breakout Move In Gold & Silver Is Real (KingWorldNews.com)

PG&E Files For Bankruptcy Protection With $50 Billion In Debt (IndiaTimes.com)

Theresa May Postpones Her Moment of Brexit Reckoning (Bloomberg.com)

Listen on iTunes, Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

29 Jan: USD 1,308.35, GBP 994.48 & EUR 1,143.24 per ounce

28 Jan: USD 1,301.00, GBP 987.98 & EUR 1,139.81 per ounce

25 Jan: USD 1,282.95, GBP 981.33 & EUR 1,132.08 per ounce

24 Jan: USD 1,279.75, GBP 981.70 & EUR 1,128.36 per ounce

23 Jan: USD 1,284.90, GBP 990.14 & EUR 1,131.74 per ounce

22 Jan: USD 1,284.75, GBP 994.14 & EUR 1,130.58 per ounce

21 Jan: USD 1,278.70, GBP 995.08 & EUR 1,124.11 per ounce

Silver Prices (LBMA)

29 Jan: USD 15.85, GBP 12.05 & EUR 13.87 per ounce

28 Jan: USD 15.68, GBP 11.93 & EUR 13.75 per ounce

25 Jan: USD 15.37, GBP 11.74 & EUR 13.55 per ounce

24 Jan: USD 15.30, GBP 11.75 & EUR 13.48 per ounce

23 Jan: USD 15.38, GBP 11.80 & EUR 13.54 per ounce

22 Jan: USD 15.26, GBP 11.84 & EUR 13.44 per ounce

21 Jan: USD 15.26, GBP 11.86 & EUR 13.42 per ounce

Recent Market Updates

– Buy Bitcoin or Gold? Bitcoin Buyers Investing In Gold In 2019

– Gold Consolidates Above $1,300 After 1.2% Gain Last Week

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

At KWN, GoldMoney’s Turk tells monetary metals investors: Enjoy the ride!

Submitted by cpowell on Tue, 2019-01-29 17:45. Section: Daily Dispatches

12:44p ET Tuesday, January 29, 2019

Dear Friend of GATA and Gold:

GoldMoney founder James Turk, interviewed today by King World News, says things are very different lately in the monetary metals market, with prices less susceptible to the usual smashes and geopolitical factors strongly favoring gold and silver.

The current rally is real, Turk says, and he invites monetary metals investors to “enjoy the ride” even though they seem intimidated by the classic “wall of worry.”

Turk’s interview is excerpted at KWN here:

https://kingworldnews.com/james-turk-this-breakout-move-in-gold-silver-i…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Even though gold and silver metals and stocks are manipulated and technical analysis is of no use, Craig Hemke states that some technical signals are indicating a rise for the mining companies

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Technical signals for gold and the mining shares

Submitted by cpowell on Tue, 2019-01-29 21:43. Section: Daily Dispatches

4:40p ET Tuesday, January 29, 2019

Dear Friend of GATA and Gold:

Manipulated as the gold market is, Craig Hemke of the TF Metals Report writes today at Sprott Money, technical analysis of it still matters insofar as fund managers ignorant of the manipulation still trade in reaction to technical signals.

Hemke adds that technical analysis and other factors suggest a couple of “memorable” years ahead for gold and silver investors, and he details some of them in commentary headlined “Technical Signals for Gold and the Mining Shares” here:

https://www.sprottmoney.com/Blog/technical-signals-for-gold-and-the-mini…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Maduro “Open To Talks” As 20 Tons Of Gold Mysteriously Disappears From Venezuela’s Vaults

It’s probably just a coincidence.

One day after a Russian official warned that Venezuela would struggle to meet its financial obligations to Moscow under a $3.15 billion debt-rescheduling deal, Bloomberg is reporting that a mysterious Russian Boeing 777 had landed in Caracas on Tuesday and ferried away 20 tonnes of gold – equivalent to roughly 20% of the country’s holdings of the shiny metal – to an unknown location with little explanation. The story cited a “bombshell tweet” sent by Venezuelan lawmaker Jose Guerra, a “former central bank economist who remains in touch with old colleagues there”, and the “welter of social media speculation” that followed (though Guerra provided no evidence).

To be sure, many outlandish claims have been made in the week since opposition leader Juan Guaido declared himself the legitimate democratically-elected leader of what was once Latin America’s wealthiest nation – creating the biggest threat to Venezuelan President Nicolas Maduro’s rule since the socialist dictator took office in 2013.

Moving the 20 tonnes of gold bars, worth some $840 million, occurred shortly after the UK denied the Maduro regime’s request to retrieve some $1.2 billion in gold being kept in the vaults of the Bank of England.

And with the country owing billions of dollars to Russia and China (not to mention the Venezuela’s long-suffering bondholders), the story’s implication is clear: was this collateral paid to Russian President Vladimir Putin?

On Monday, a plane belonging to Nordwind Airlines, a popular Russian charter operator based in Moscow, landed at the international airport near Caracas,according to flight tracking website FlightRadar24. A Nordwind spokesman declined to comment Wednesday on the purpose of the flight.

While Finance Minister Simon Zerpa declined to comment on the nation’s gold, he said there was no Russian plane at Simon Bolivar International Airport: “I’m going to start bringing Russian and Turkish airplanes every week so everybody gets scared,” he said.

Russia’s Foreign Ministry also had no information about the charter jet, spokeswoman Maria Zakharova said in a message Wednesday. There are no plans to evacuate Russians from Venezuela, she said.

According to BBG, Venezuela has been trying for years to increase its gold reserves via mining. The state gold processor Minerven melts ore into gold bars which are transported by the military (which controls the mining) to the central bank.

The US announced sanctions against the Maduro regime earlier this week, including restrictions on buying the country’s oil, to try and starve his regime of money, while opening access to Venezuelan assets frozen in the US to Guaido to try and help him cement his control of the country.

By Wednesday morning, the regime was feeling pressure to capitulate and begin negotiations, with Maduro reportedly saying he’d be “open to talks” with the opposition, though, as the New York Times noted, ” it is “not clear if the comments were a genuine offer for negotiations with the opposition or a bid to buy time for his embattled government.”

“I am ready to sit down at the negotiating table with the opposition so that we could talk about what benefits Venezuela,” Mr. Maduro said.

Maduro listed several potential mediators for the talks, including Mexico, Uruguay, Bolivia, Russia, the Vatican and other European governments that had encouraged a dialogue. The purported capitulation comes after Maduro had threatened to use the country’s Supreme Court to impose a travel ban on Guaido in what appeared to be an attempt to intimidate him.

President Trump welcomed Maduro’s announcement, while reiterating a warning to US citizens not to travel to Venezuela.

Donald J. Trump

✔@realDonaldTrump

Maduro willing to negotiate with opposition in Venezuela following U.S. sanctions and the cutting off of oil revenues. Guaido is being targeted by Venezuelan Supreme Court. Massive protest expected today. Americans should not travel to Venezuela until further notice.

Still, he has rejected international calls for new elections, which could soon lead to several Western European nations joining the ranks of countries recognizing Guaido as the country’s legitimate ruler.

Refusal to hand over Venezuelan gold means end of Britain as a financial center – Prof. Wolff

Published time: 30 Jan, 2019 13:01

The freezing of Venezuelan gold by the Bank of England is a signal to all countries out of step with US interests to withdraw their money, according to economist and co- founder of Democracy at Work, Professor Richard Wolff.

He told RT America that Britain and its central bank have shown themselves to be “under the thumb of the United States.”

“That is a signal to every country that has or may have difficulties with the US, [that they had] better get their money out of England and out of London because it’s not the safe place as it once was,” he said.

The Bank of England is currently withholding $1.2 billion in gold from Venezuelan President Nicolas Maduro’s government, but is being urged by Washington to release it to the chairman of the National Assembly, Juan Guaido. Last week, the US backed Guaido as the legitimate president of Venezuela, after he declared himself interim president.

According to Professor Wolff, control of Venezuela’s oil has always been an urgent issue for Washington.

He also said that the collapse of Britain as a global power, which was accelerated by Brexit, is now about to take another step.

“One of the few things left for Britain is to be the financial center that London has been for so long. And one of the ways you stay a financial center is if you don’t play games with other people’s money,” he said.

The economist added that it is for the Venezuelans who put the money into the care of the British bank to determine what is done with it, and not for the Bank of England.

“You can be sure that every government in the world is going to rethink putting any money in London, as they used to do, when they are watching this political manipulation with the money that they entrusted to the British. It is very dangerous for the world but for Britain particularly,” said Wolff.

He explained: “What the British are showing is that they can’t continue apparently to be the neutral place where you can safely put your money.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7170/

//OFFSHORE YUAN: 6.7295 /shanghai bourse CLOSED DOWN 18.68 PTS OR 0.72%

HANG SANG CLOSED UP 111.17 POINTS OR 0.40%

2. Nikkei closed DOWN 108.10 POINTS OR 0.52%

3. Europe stocks OPENED ALL MIXED

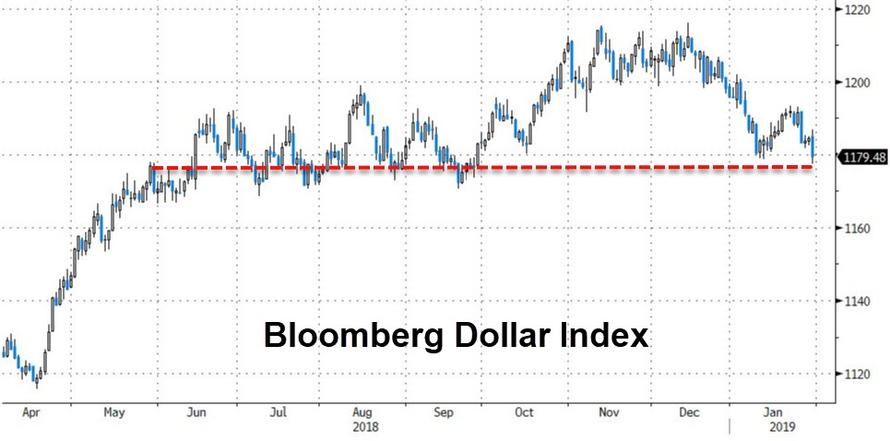

/USA dollar index RISES TO 95.76/Euro RISES TO 1.1437

3b Japan 10 year bond yield: RISES TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.43/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.82 and Brent: 61.91

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.19%/Italian 10 yr bond yield DOWN to 2.61% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.42: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.94

3k Gold at $1312.95 silver at:15.91 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 16/100 in roubles/dollar) 65.89

3m oil into the 53 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.43 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9971 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1403 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.20%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.72% early this morning. Thirty year rate at 3.04%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2712

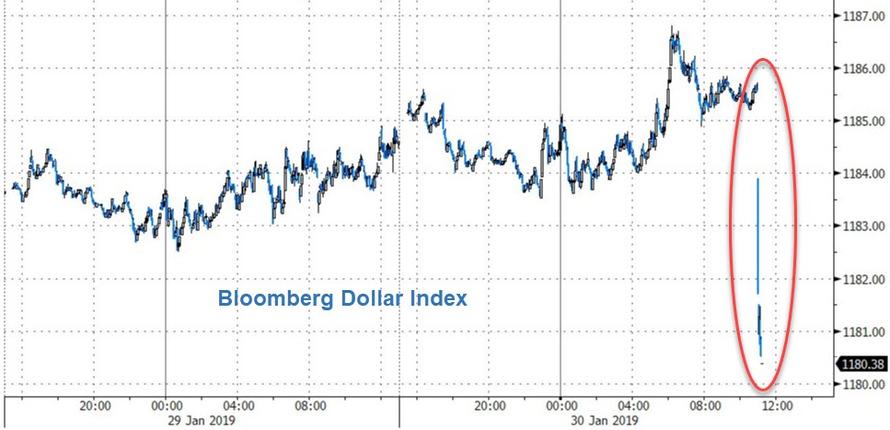

Global Markets Rise Ahead Of Fed And Trade Talks As Gold Hits 8 Month High

World stocks inched up and the dollar steadied on Wednesday after Apple failed to disappoint investors and reported earnings, meeting Wall Street’s lowered expectations, and sending its stock higher in a muted session as investors braced for a barrage of catalysts, from US-China trade talks and the Fed meeting to an avalanche of corporate earnings. The pound halted a two-day decline and U.K. shares rallied after lawmakers voted to renegotiate Brexit.

The MSCI world equity index was fractionally in the green following gains in Asia overnight and a muted start to trading in Europe. The pan-European STOXX 600 benchmark index was flat.

US equity futures all rose, supported by with Apple shares which extending gains in pre-market trading after first-quarter earnings reassured investors that the worst may be past, although it remains very much unclear if Apple can pivot from a cell phone to a “services” company, especially with services revenue growth slowing sharply. In any case, investors were relieved that there was no more bad news after the company shocked financial markets at the start of this month with a revenue warning that sparked fears that U.S.-China trade tensions were taking a toll on the tech sector.

“Apple earnings delivered enough for investors to come back on board,” said Markets.com analyst Neil Wilson. “Although Apple still faces big questions like pricing structure, upgrade cycles, FX headwinds and weaker Chinese demand, we did get a positive answer to the key question on whether services margins can help rerate the stock higher.”

The Stoxx Europe 600 Index was mixed after data showing euro-area economic confidence extended its worst losing streak in a decade, ahead of Sino-U.S. trade talks and a closely watched Fed announcement in which Chair Powell is likely to disappoint markets. The UK’s FTSE 100 traded higher by 0.9%, climbing for a second day and outperforming continental bourses, with CAC also rising 0.5%; DAX trades lower by 0.4%. Investors fretted about the possibility of a “no-deal” British departure from the European Union after UK lawmakers instructed Prime Minister Theresa May on Tuesday to reopen the treaty she had negotiated with Brussels to replace a controversial Irish border arrangement.

Goldman Sachs upped its “no-deal” Brexit probability to 15 percent from 10 percent, and cut the chance of Brexit not happening at all to 35 percent from 40 percent according to Reuters. “Tuesday’s Brexit amendments offered little additional clarity to anyone,” Goldman Sachs analysts wrote.

Earlier in the session, Stocks in Japan and China slid, while they increased in South Korea, Australia and Hong Kong. The yuan advanced to the highest since July on hopes for the U.S.-China trade talks getting underway in Washington. Growing fears that central banks are preparing to reflate “whatever it takes”, helped send gold to an eight-month high, underscoring lingering investor caution.

While Apple CEO Tim Cook said trade tensions between the United States and China were easing, lifting the mood before another round of official talks on Wednesday in Washington, that may prove another unreasonably optimistic take. The two sides are meeting next door to the White House in the highest-level talks since U.S. President Donald Trump and his Chinese counterpart Xi Jinping agreed a 90-day truce in their trade war in December.

“I expect that the Washington summit will help pave the way for an extension of the trade truce. This is also what markets expect and a failure of the talks is not priced in at all,” said Giuseppe Sersale, fund manager at Anthilia Capital. Which is also why the risk of downside following the trade talks is far greater.

Elsewhere, following lackluster corporate earnings in January, all eyes will be on tech giants including Facebook and Microsoft when they report today. That will be the backdrop for the Fed’s policy decision and its assessment of the U.S. economy, while the arrival of Chinese negotiators in Washington for talks to resolve the ongoing trade dispute adds another layer of complexity.

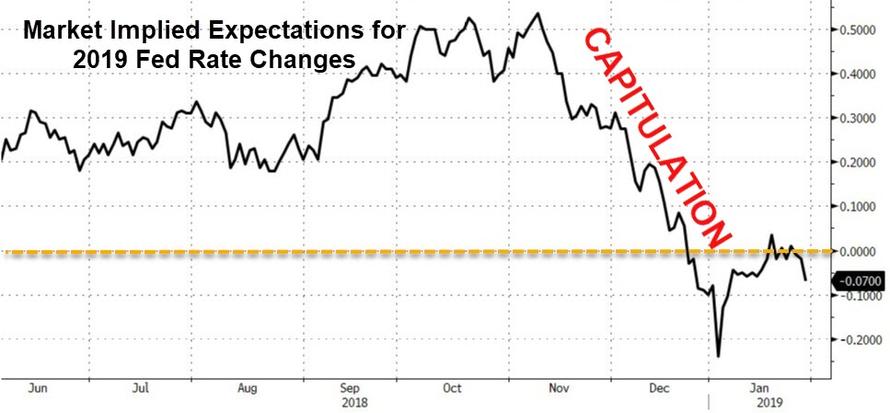

Expectations from Wednesday’s Federal Reserve rates review are that policymakers will reinforce their recent dovish stance, given signs of a slowdown in the U.S. economy. “We believe the Fed is likely to show the flexibility markets are seeking at its upcoming meeting, as it balances still solid domestic economic growth against slower global growth and less significant, but persistent, domestic risks,” said John Lynch, Chief Investment Strategist at LPL Financial.

And yet nobody really has any clue what happens next: “Such is the extent of uncertainty across global markets at the moment that investor sentiment is struggling to gain any meaningful traction,” Simon Ballard, a macro strategist at First Abu Dhabi Bank, said in a note. “The overarching veil of caution suggests that near-term positive momentum potential will likely remain limited. It is still very much global trade and the global rates outlook that sit at the heart of investor focus.”

European bond markets little changed across core and periphery, trading in tight ranges, as are USTs. BTPs shrug off talk of early Italian election, with 5-and 10-year auction well-received. Bloomberg USD index also steady, with Aussie dollar leading G-10 gainers, followed by the pound. Swedish krona edges lower after soft consumer confidence data. In commodities, WTI and Brent both up ~0.3%, metals trading higher across the board

In FX, the Bloomberg Dollar Spot Index was confined to a narrow range as investors look ahead to the Federal Reserve policy decision and U.S.-China trade talks. The pound climbed above $1.31 as bias remained to fade dips, while the Aussie led gains versus its G-10 peers as inflation data beat forecasts. Emerging-market currencies climbed to a fresh seven-month high: the Australian dollar surged 0.5 percent as inflation topped forecasts, while the Chinese yuan reached a six-month high in the offshore market before the trade talks. Elsewhere, the Mexican peso declined as Fitch Ratings cut the debt of state oil company PEMEX to one notch above junk.

Iron ore surged after Brazil’s Vale SA, the world’s largest producer, outlined plans to cut output after a deadly dam breach. Iron ore is now up nearly 30% since November.

WTI crude gained as traders assessed the impact of U.S. sanctions against Venezuela, a major exporter. Brent (+0.6%) and WTI (+0.7%) prices are firmer as the complex reacts to the smaller than expected build in yesterday’s API Crude Stocks alongside reports that Saudi Arabia are planning on further oil production cuts and exports next month; additionally, believing that SPR releases are a solution to the US’s Venezuela oil shortage problem. Follows sanctions announced on Monday which aim to stop the proceeds from PDVSA’s crude exports of around 500,00 BPD to the US.

In addition to the above, expected data include mortgage applications and pending home sales. Alibaba, AT&T, ADP, Boeing, McDonald’s, Microsoft, Nasdaq, Facebook, Mondelez, Qualcomm and Visa are among the slew of companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,645.50

- STOXX Europe 600 up 0.08% to 357.51

- MXAP up 0.1% to 154.52

- MXAPJ up 0.4% to 504.93

- Nikkei down 0.5% to 20,556.54

- Topix down 0.4% to 1,550.76

- Hang Seng Index up 0.4% to 27,642.85

- Shanghai Composite down 0.7% to 2,575.58

- Sensex down 0.06% to 35,570.42

- Australia S&P/ASX 200 up 0.2% to 5,886.70

- Kospi up 1.1% to 2,206.20

- German 10Y yield fell 0.2 bps to 0.198%

- Euro down 0.04% to $1.1428

- Italian 10Y yield fell 3.1 bps to 2.277%

- Spanish 10Y yield rose 1.6 bps to 1.254%

- Brent futures up 0.6% to $61.68/bbl

- Gold spot up 0.1% to $1,313.36

- U.S. Dollar Index little changed at 95.78

Top Overnight News from Bloomberg

- U.K. PM Theresa May promised to renegotiate the most contentious part of her Brexit deal after it was rejected by Parliament. She will now head to Brussels with the threat of economic chaos still looming over her country; The Irish government rejected any softening of the so-called backstop

- Despite the best efforts of central bankers, investors are betting the next phase of European monetary policy will look a lot like the last one; market expectations for the peak rate in this cycle are being slashed, and the implied timing for a first hike since 2011 is being pushed out further by the day

- Iron ore markets were convulsed after Brazil’s Vale outlined plans to cut output after a deadly dam breach. Prices surged, with futures rallying more than 9%

- Italian Deputy Prime Minister Matteo Salvini is facing pressure to force an early election this year from lieutenants frustrated by dealing with an unruly coalition partner

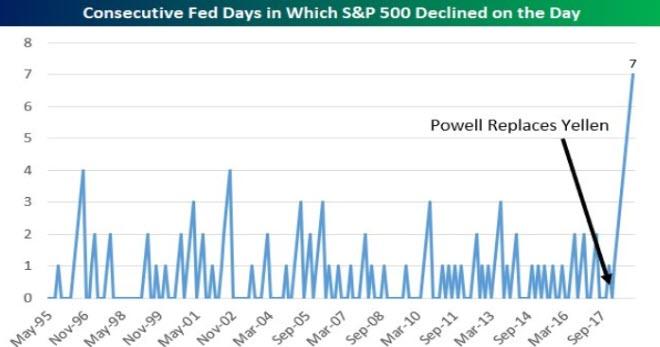

- Jerome Powell will debut the Fed’s latest communications strategy — a press conference eight times a year — by emphasizing patience in raising interest rates, a message the chairman struggled to deliver in December

- From Hong Kong to Japan, exports data for December showed a marked downturn as supply-chain disruptions triggered by U.S.-China tensions and a cyclical slowdown in the world economy, led by China, hit the trade-reliant region

- Brexit will probably split BOE policy makers on how to respond

- U.S. and China are sitting down Wednesday for the first of two days of talks aimed at finding a solution to a trade war. Administration officials and other people familiar with the state of play say the two sides remain far apart

- Several senior members of Matteo Salvini’s League are urging him to capitalize on a growing lead in opinion polls to ditch the anti-establishment Five Star Movement

- A lack of clarity surrounding the U.K.’s departure from the EU pushed confidence among British employers this month to levels last seen in the wake of the Brexit vote

- Average daily foreign-exchange turnover in the U.K. dropped to $2.6t in October 2018, a 4% fall from the record high of $2.7t in April 2018, according to Bank of England data. In North America, daily volume dropped 0.1% to $995b

Asian stocks traded indecisively with the region tentative heading into this week’s key risk events and as participants also digested better than expected Apple results, which only provided brief support to US equity futures after-hours. ASX 200 (+0.1%) and Nikkei 225 (-0.4%) were both subdued although strength across commodities just about kept the Australian benchmark afloat, while Tokyo stocks were weighed by currency effects and uninspiring corporate updates. Elsewhere, Hang Seng (-0.1%) and Shanghai Comp. (-0.3%) declined at the open amid broad weakness in the region and with China Life Insurance shares heavily pressured after it flagged a 50%-70% drop in FY net, although Chinese markets then rebounded off lows amid a non-committal tone ahead of the looming US-China trade talks and after the PBoC injected liquidity for the 1st time in 8 days. Finally, 10yr JGBs were uneventful with prices stuck to within this week’s tight range amid the indecision seen across the region and with an unchanged BoJ Rinban announcement largely ignored.

Top Asian News

- Chinese Firms Slash Profit Forecasts, Fueling Slowdown Fears

- JPMorgan Names Filippo Gori as Deputy CEO for Asia Pacific

- Malaysia Lets Goldman Decide How Much of $7.5b Bank Wants to Pay

- Hong Kong Dollar Spikes as Pre-Holiday Liquidity Tightness Seen

- Calm Has Descended on Asian Stocks Ahead of Fed, Trade Talks

Major European equities have been indecisive [Euro Stoxx 50 U/C] taking lead from the indecisive trade seen overnight ahead of today’s FOMC rate decision and press conference. Benefitting from sterling effects the FTSE 100 (+1.2%) is the outperforming index, with Burberry (+2.5%) in the green in sympathy with LVMH (+6.3%) after their earnings; and stating they are cautiously confident regarding 2019. Other luxury names such as Kering (+3.4%), Christian Dior (+4.0%) and Pandora (+2.0%) are also up in sympathy with LVMH. Sectors are mixed with outperformance in consumer discretionaries and some underperformance in telecom names. Other notable movers include Atos (+8.1%) who, following their earnings and 2019 guidance confirmation, are at the top of the Stoxx 600. Elsewhere, Novartis (-1.2%) are down following results, where the Co. missed on Q4 sales and operating income, as are Siemens (-1.5%) after their Q1 revenue came in just under expectations; Co. also stating they have made no further concessions on the Alstom (-0.5%) merger and will not pursue it at all costs.

Top European News

- Siemens CEO Fires Broadside Against EU With Rail Deal on Brink

- Atos to Hand Out Worldline Shares, Paving Way for More Deals

- Santander Seeks to Move Past Orcel Fiasco With New Plan

- U.K. Lending Slows as Brexit Uncertainty Hangs Over Outlook

- Why Irish Reckon May Still Boxed In on the Brexit Backstop

In FX, the DXY index and Greenback overall looking to the Fed for more direction, as the DXY meanders between 95.875-682.

- AUD – Firmer than expected Australian Q4 CPI data has helped to revive a flagging Aud/Usd, with the pair back up on the 0.7200 handle and close to daily chart resistance around 0.7207, while Aud/Nzd has rebounded firmly over 1.0500, as the Kiwi continues to meet offers around 0.6850 vs the Usd.

- GBP – The next best G10 currency, as initial post-UK Parliamentary Brexit vote downside is reversed to an extent in Cable and Eur/Gbp, with the former reclaiming 1.3100+ status and perhaps deriving some respite from a bounce ahead of the 200 DMA (circa 1.3055). Meanwhile, the cross has recoiled relatively sharply from fresh peaks just shy of 0.8760 towards 0.8715, and perhaps the bulk of noted month end buying interest has now been transacted.

- CAD – Another major ‘outperformer’, or at least holding a firmer line vs its US counterpart within a 1.3235-85 range, and still cushioned by the recuperation in crude prices. Ahead, perhaps a little independent impetus via Canadian average weekly earnings data, but in truth this pales against the sheer volume of US releases on tap, and of course the impending FOMC.

- JPY/EUR – Both flat to a tad softer vs the Dollar, and very confined in the run up to the Fed, as Usd/Jpy continues oscillate between 109.00-50 amidst undulations in broad risk sentiment, and the single currency remains entrenched in a 1.1400-50 band (with the topside also ‘protected’ by the 200 DMA around 1.1444).

- CHF/SEK – The Franc and Krona have extended recent losses/underperformance/retracements, with the Chf perhaps undermined by weaker than forecast Swiss KoF and ZEW sentiment surveys, while the Sek will not have been helped by declines in consumer and industrial confidence that will merely keep the Riksbank on the back-burner. Usd/Chf is hovering above 0.9950 and Eur/Sek just below 10.3900.

In commodities, Brent (+0.6%) and WTI (+0.7%) prices are firmer as the complex reacts to the smaller than expected build in yesterday’s API Crude Stocks alongside reports that Saudi Arabia are planning on further oil production cuts and exports next month; additionally, believing that SPR releases are a solution to the US’s Venezuela oil shortage problem. Follows sanctions announced on Monday which aim to stop the proceeds from PDVSA’s crude exports of around 500,00 BPD to the US. Gold (+0.1%) is trading in the middle of its USD 6/oz range, on a steady dollar ahead of today’s FOMC decision. Elsewhere, Vale’s CEO announced they will take up to 10% of the Co’s output offline to decommission 10 dams following Friday’s dam burst.

Looking at today’s calendar, today’s Fed meeting outcome will no doubt hog much of limelight while the data highlights in the US this afternoon include the January ADP employment change report (183k expected) and December pending home sales (+0.5% mom expected). In Europe this morning we’re kicking off with the December import price index reading in Germany followed by December consumer spending data in France, December money and credit aggregates data in the UK and then January confidence indicators for the Euro Area. Today is also the day that trade talks are due to resume between the US and China with Vice Premier Liu Ge meeting with US Trade Representative Lighthizer and Treasury Secretary Mnuchin in Washington. Finally, it’s a busy day for earnings with reports due from Microsoft, Facebook, Alibaba, Visa, AT&T, Novartis, Boeing and McDonald’s.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.7%

- 8:15am: ADP Employment Change, est. 181,000, prior 271,000

- 10am: Pending Home Sales MoM, est. 0.5%, prior -0.7%; YoY, est. -7.0%, prior -7.7%

- 2pm: FOMC Rate Decision

- U.S. BEA Working With Census, OMB on Economic-Data Schedule

DB’s Jim Reid concludes the overnight wrap

Morning from Dublin where there will be lots of eyebrows raised this morning after the events in U.K. parliament last night. However if you think Brexit negotiations are currently in a deep freeze then spare a thought for those in the Midwest of the US today who will face a once in a generation polar vortex which will bring temperatures down to -53C (-64F). Chicago will be even colder than Antarctica and see lows of -27F, with a wind chill factor making that feel closer to -50F. Good luck to all our readers there. Rather worryingly Chicago police say people are being robbed at gunpoint of their coats and those hideously expensive Canada Goose jackets that were two a penny in Davos last week have been especially targeted. The good news is that if you’ve been desperate to pick up a ticket to Hamilton they are reselling at half-price for tonight in Chicago as no-one wants to brave the elements. So for those that don’t mind the cold there’s your opportunity. Don’t wear your Canada Goose jacket out though.

One area where there was a thawing out last night was that U.K. Parliament now have a mandate for a Brexit deal. The problem is that this mandate has already been ruled out by the EU. Nevertheless Brussels have been asking the U.K. what they want for the last two and a half years and finally we have an outline of what they want. Parliament now seems happy to vote for the withdrawal agreement as long as the Irish backstop is removed/amended in a satisfactory manner.

To recap in as brief a way as possible as everyone might be bored by now, the only amendments that passed were a non-binding one (Spelman) that voted against leaving with no-deal and one (Brady) that asked the government to renegotiate the withdrawal agreement to accommodate an alternative arrangement to the Irish backstop. So Mrs May will go to Brussels and try to reopen negotiations on an agreement that the EU have already said before and after last night’s votes that they won’t reopen. Whether diplomacy can work in the background remains to be seen.

All the reaction I’ve seen from the market overnight talks about it in terms of it being a unicorn-like mission with absolutely no chance of success. However stranger things have happened. Maybe I’m being naive but both the EU and the U.K. don’t want there to be a no-deal and both parties are categoric that there can’t be a hard border in Ireland. To me there is scope for negotiations on that basis. However I haven’t heard anyone that agrees with me yet. Indeed DB’s Oli Harvey downgraded Sterling to neutral overnight and overall thinks developments have on balance become more negative. His updated probabilities are; 1) May pivots to a softer Brexit stance via the Political Declaration on the Future Relationship: 15% (previously 40%), 2) Last-minute ratification on the existing deal in the face of no alternatives 50% (previously 30%), 3) Second referendum: 5% (previously 15%), 4) New election: 15% (previously 10%), 5) No deal Brexit: 15% (previously 5%). See the full report here . In market terms Sterling dropped as various soft or delayed Brexit motions failed to pass and closed -0.74% at $1.3066. Overnight in Asia the Pound has consolidated around those levels and as we go to print it’s at $1.3086.

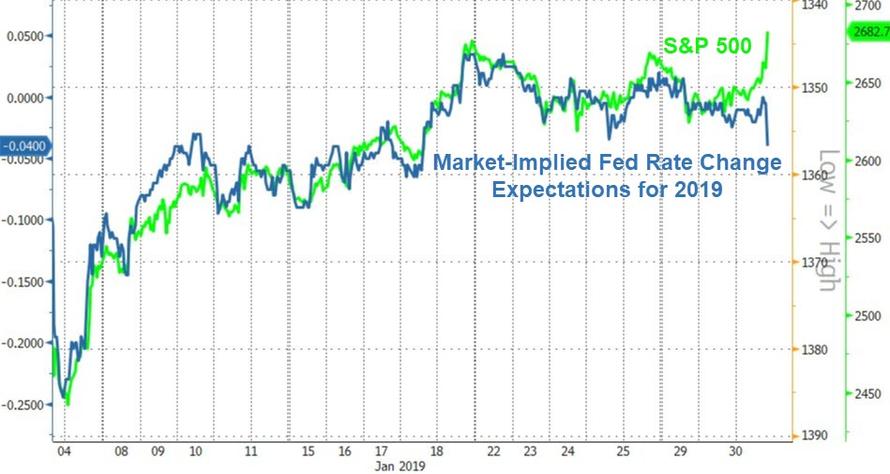

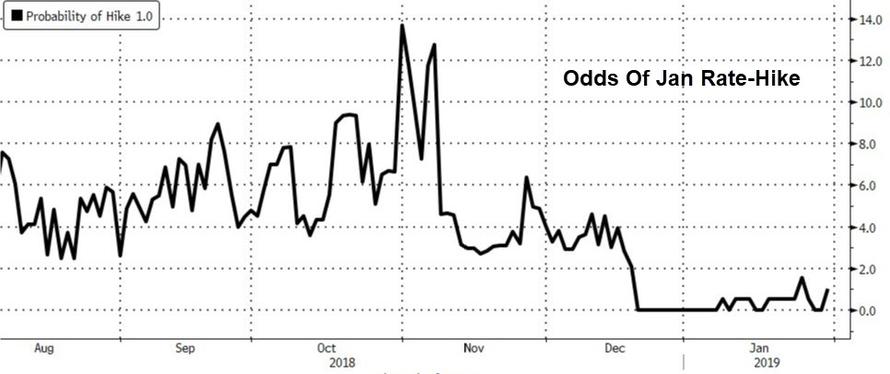

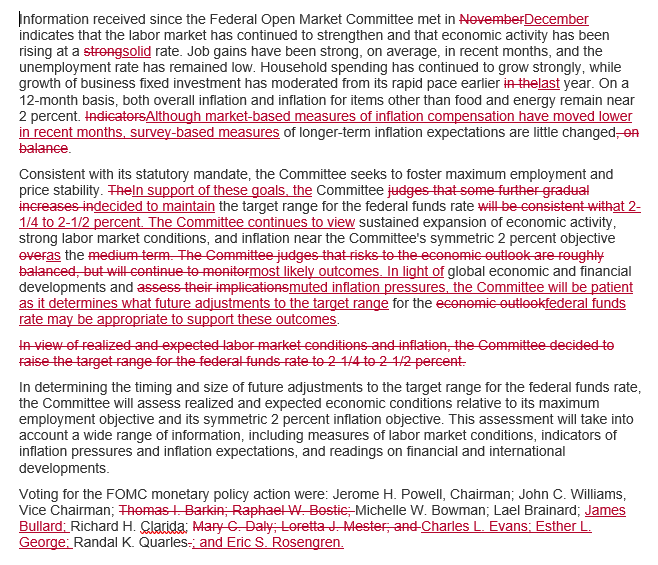

Moving on, we’re now firmly into the business end of the week with the next event for markets to navigate being the first Fed meeting of 2019 tonight. With neither the consensus nor the market pricing in any chance of a hike, most observers will instead be watching to see if the current narrative is maintained. Our US economists expect the most meaningful alteration to the post-meeting statement to be to the forward guidance language. Indeed at the December meeting the statement noted that the “Committee judges that some further gradual increases” in rates would be consistent with the Fed’s dual mandate. Our team believe that this statement is now too strong given intermeeting developments and expect the language to be softened by noting that the Fed expect “further gradual adjustments” in policy will be consistent with the Fed’s objectives. As for Powell’s press conference, our colleagues expect a similar message to be reiterated with the unspoken takeaway likely to be that June is the earliest possible date for another rate increase. The balance sheet topic is likely to be a talking point although our team don’t expect any major announcements.

As you’ll see in the day ahead at the end, we’ve also got a bumper day for earnings scheduled, especially in the tech sector, while trade talks between the US and China also formally get underway again today. Yesterday, in an interview with Fox, Treasury Secretary Mnuchin confirmed that “everything is on the table” in response to a question about Trump potentially dropping all tariffs in return for a good deal. For what it’s worth yesterday our China Chief Economist Zhiwei Zhang published a short update in which he concluded that he expects the two governments to reach a partial trade deal by March 1st, with China making concessions to buy US goods, lower tariffs, and open part of the service sector. Zhiwei believes that the US may stop imposing more tariffs in exchange. That all said, he also expects the Huawei case to extend beyond March.

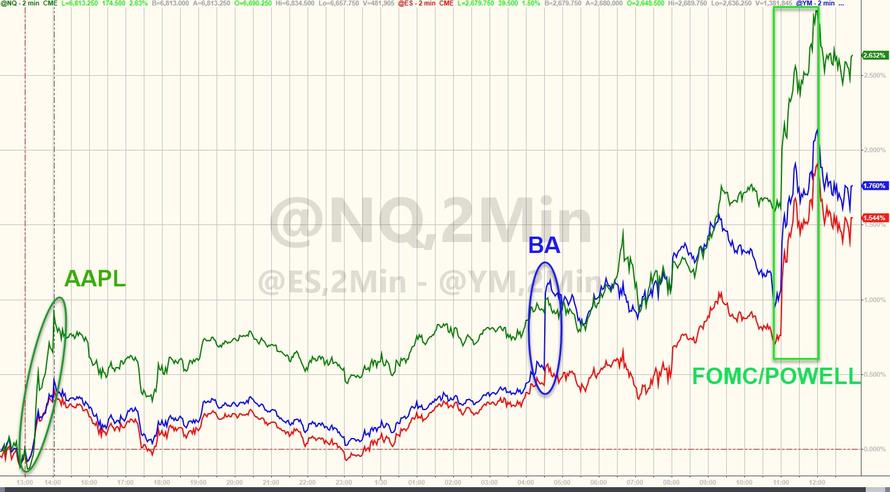

Back to markets, where despite Mnuchin’s comments, corporate earnings and the tech sector spoilt hopes of a bounce back for US equities with the NASDAQ (-0.81%) at the forefront of declines along with the NYSE FANG index (-2.09%) which plummeted for its fifth daily decline in the last seven sessions. After the bell, however, Apple beat earnings expectations and sparked a rally, with shares up +5.9% in post-market trading. This helped NASDAQ futures retrace most of their declines from yesterday, with front-month contracts up +0.66% overnight. Digging into the results, Apple beat on headline earnings, with EPS at $4.18 versus consensus $4.17, and also on revenue, at $84.3bn versus estimates for $83.9. Notably, revenue fell especially hard in China ($13.2bn from $17.9bn last year), as signaled in the company’s earlier guidance.

Prior to this the S&P 500 closed down -0.15% while the DOW (+0.21%) just about managed to stay onside thanks to some positive large-cap earnings. Better than expected results from 3M (+1.94%) and Pfizer (+3.16%) seemingly helped offset some of the post-Caterpillar global growth concerns however at the other end Allergan (-8.60%) and Harley-Davidson (-5.08%) succumbed to heavy falls after their respective results failed to convince the market. Anecdotally, companies’ guidance is mixed on the macro outlook, with Whirlpool CFO Peters saying “continued economic and trade uncertainty to temper overall demand” while Verizon CFO Ellis anticipates “no major impact at this point on the macro economy or even the shutdown”.

Earlier in Europe, the STOXX 600 gained +0.80% while treasuries and bunds traded close to flat. BTP yields rallied -3.1bps to a new 6-month low. The energy sector outperformed, gaining +0.32% in the US and +1.30% in Europe, as Brent crude oil prices rose +2.32% to mostly retrace Monday’s selloff. The move was driven by comments by Saudi Arabia’s Energy Minister Al-Falih, who said that he expects to cut oil output further next month and to keep production “well below” the levels agreed by OPEC. New US sanctions on Venezuela’s national oil company also helped ease the supply outlook, while historically cold weather in the US increases demand for heating oil.

Markets in Asia are also trading slightly cautiously overnight with the Nikkei down -0.32% and bourses in China flat as markets await the start of trade talks. The Hang Seng (+0.27%) and Kospi (+0.27%) have however posted modest gains while EM FX is similarly mixed.

In other news, the latest sentiment indicator in the US took on added focus yesterday in light of uncertainty around government policy and recent financial market volatility. Indeed the January consumer confidence reading slumped even more than expected, to 120.2 (vs. 124.0 expected) from a downwardly revised 126.6 in December. The present situations index was broadly flat at 169.6 however the expectations component fell to 87.3 and the lowest since 2016 likely reflecting the government shutdown. There were lots of people on twitter suggesting that the ratio between the two suggests an imminent recession based on historical observations. However if the disparity mostly reflects the shutdown it could easily reverse and nullify the signal. The graph between the two does look worrying though. On the plus side the ratio of respondents describing jobs as “plentiful” versus respondents saying they are “hard to get” reached a new cyclical high, which points to further labour market strength.

Meanwhile the S&P CoreLogic house price index confirmed that prices rose +4.68% yoy in the 20 biggest cities in November and therefore slowing slightly from October. In Europe we only had the French consumer confidence print for January which surprised to the upside at 91 (vs. 88 expected and 86 in December). That marks a decent correction from the protest’s impacted December reading and is in stark contrast to the PMIs in France that we saw last week.

Looking at today’s calendar, this evening’s Fed meeting outcome will no doubt hog much of limelight while the data highlights in the US this afternoon include the January ADP employment change report (183k expected) and December pending home sales (+0.5% mom expected). In Europe this morning we’re kicking off with the December import price index reading in Germany followed by December consumer spending data in France, December money and credit aggregates data in the UK and then January confidence indicators for the Euro Area. Today is also the day that trade talks are due to resume between the US and China with Vice Premier Liu Ge meeting with US Trade Representative Lighthizer and Treasury Secretary Mnuchin in Washington. Finally, it’s a busy day for earnings with reports due from Microsoft, Facebook, Alibaba, Visa, AT&T, Novartis, Boeing and McDonald’s.

Market

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 18.68 PTS OR 0.72% //Hang Sang CLOSED UP 111.17 POINTS OR 0.40% /The Nikkei closed DOWN 108.10 PTS OR 0.52%/ Australia’s all ordinaires CLOSED UP .20%

/Chinese yuan (ONSHORE) closed UP at 6.7170 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.48 dollars per barrel for WTI and 60.53 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.7170AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7295: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/HUAWEI

The fight with the uSA intensifies. Now Huawei asks its suppliers to move production out of the USA

(courtesy zerohedge)

Huawei Asks Suppliers To Move Production Out Of US: Nikkei

The sweeping indictment against Huawei and its CFO Meng Wanzhou unveiled by Acting Attorney General Matthew Whitaker on Monday has elevated the feud between the US and the world’s largest telecoms equipment provider (and second largest maker of smartphones) to absurd new heights.

And while officials from Huawei and Beijing have denounced the charges as anti-competitive and “politically motivated”, Huawei is apparently already bracing for the other shoe to drop: According to a report by Nikkei, the tech giant has asked suppliers to consider moving some of their production outside the US in case the Congress of the DOJ adopt a ban on American-made parts being sold to the chipmaker. With the memory of the near-demise of ZTE still fresh in its memory, the company has made the request based on the expectation that an order of a full-scale ban on semiconductors and other critical equipment by President Trump is imminent.

The companies asked including Taiwan’s ASE Technology Holding, King Yuan Electronics and Taiwan Semiconductors, among others.

In a bid to minimize this risk, Huawei has informed suppliers such as Taiwan’s ASE Technology Holding and King Yuan Electronics, its top chip packaging and testing providers, that it wants to relocate most production to sites in mainland China, industry sources told the Nikkei Asian Review.

Huawei has also talked with Taiwan Semiconductor Manufacturing Co., the world’s biggest contract chipmaker, about moving some chip production to a site in the Chinese city of Nanjing, sources told Nikkei.

Notably, Huawei shares many of the same suppliers as Apple Inc. And the uncertainties that have been introduced by the US’s campaign against the telecoms giant have made it virtually impossible for some of these companies to adequately assemble their business plans for the coming year.

Many Asian suppliers hoped that Huawei would be their most valuable customer providing growth for 2019 as the smartphone market matures quickly, but those assumptions now appear riddled with uncertainties, according to supply chain sources familiar with the matter.

[…]

The charges against Huawei and Chief Financial Officer Meng Wanzhou, who was arrested in Canada last month on the request of the U.S., have raised the prospect of further earnings downgrades by suppliers after a raft of reductions due to the slowdown in the global smartphone market.

“We don’t know how to make business plans for 2019 after Huawei’s CFO Meng was arrested,” an industry source told the Nikkei Asian Review. “It brought so many risks and uncertainties.”

A ban on selling to Huawei would be a “blow” to producers of semiconductors and other components: “But there’s very little we could do to change that” they said.

Some suppliers are even looking into the terms of their business interruption insurance to see if it covers “political factors.”

ASE Technology Holding, the world’s biggest chip packaging and testing company, is looking into the terms of its business interruption insurance to see whether they include disruption owing to political factors, according to a source familiar with the matter.

The chairman of iPhone assembler Pegatron, Tung Tzu-hsien, told reporters on Jan. 22: “Over the past year, the impact of international political risks on the global tech industry has been unprecedented. It is the greatest that I can recall.”

“We didn’t have to care so much when we produced notebook computers, smartphones or integrated circuits in the past. But now we have to be extremely careful to comply with local laws in each country to avoid stepping on mines,” Tung said on the sidelines of a tech forum.

Shih Po-jun, an analyst at Taipei-based think tank Market Intelligence & Consulting Institute, said the disruption will only continue.

“The U.S. crackdown on Chinese tech – of which Huawei is the most important representative – will not stop here and is likely to have a snowball effect on other Asian suppliers and on the customer end as well,” Shih said. “For those who rely heavily on Huawei or China for their business, they are subject to higher political risks now.”

Despite the Trump administration’s insistence that the indictment won’t affect trade talks with China, every analyst quoted by Nikkei said they don’t see how that’s possible.

“Any relief for the Chinese national champion will likely come at a steep price, and the issue seems set to take a central role in the ongoing U.S.-China trade talks,” Gavekal Research tech analyst Dan Wang said in a daily note following the U.S. indictment.

Not only has the US threatened to ban sales of Huawei products and equipment, but a US-backed campaign to convince allies and foreign telecoms firms to push Huawei out of their markets has born fruit in recent months. China’s largest private company, generating revenue of $100 billion in 2018. It is also China’s top employer, with 180,000 workers globally, and insiders say the company is worried about losing its dominance in Europe, where it has received dozens of contracts to build 5G networks.

Earlier on Tuesday, it was reported that Huawei would be arraigned on some of the charges in a Seattle court on Feb. 28, just days before the deadline for US-China trade talks. We imagine suppliers, who are already reeling from Apple’s latest iPhone sales flop, will be watching the proceedings very closely.

FBI Arrests 2nd Chinese National For Stealing Trade Secrets From Apple

We imagine there’s nothing that would put a damper on trade talks quite like another indictment accusing a Chinese national of doing the exact thing (corporate espionage and stealing US trade secrets) that senior Trump Administration officials had warned would be deal-breaking for future negotiations.