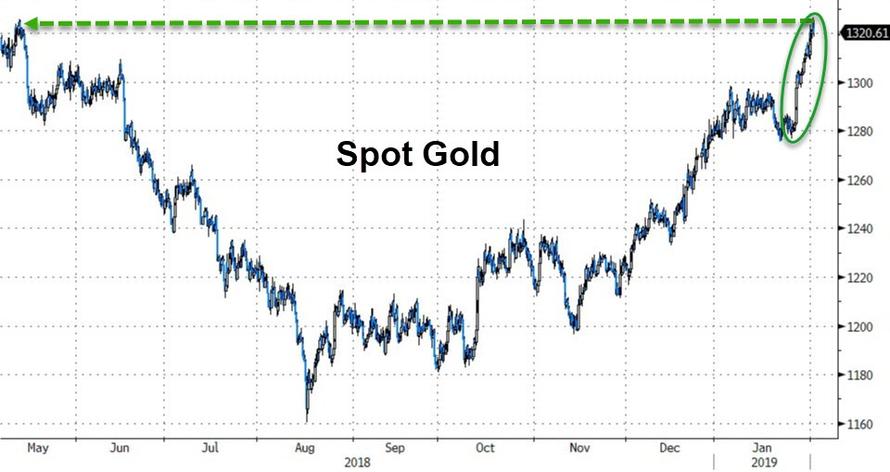

GOLD: $1320.60 UP $9.80 (COMEX TO COMEX CLOSING)

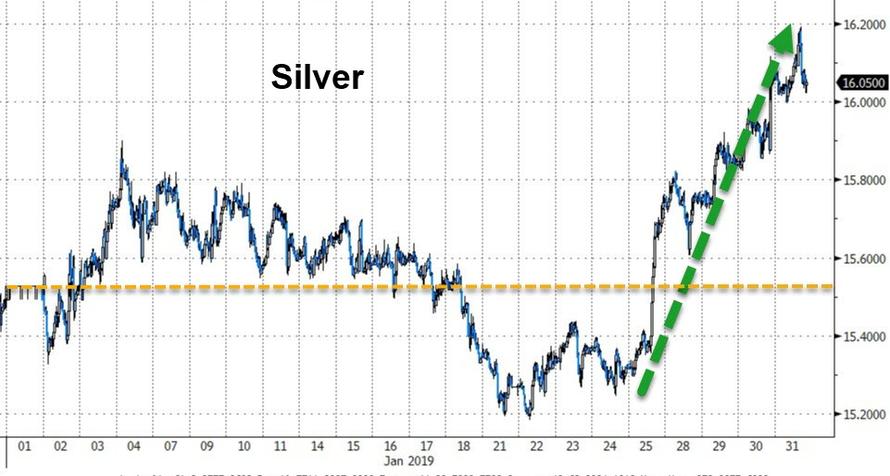

Silver: $16.06 UP 15 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1322.00

silver: $16.06

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 939 NOTICE(S) FOR 93900 OZ (2.9206 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 939 NOTICES FOR 93900 OZ (2.9206 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

286 NOTICE(S) FILED TODAY FOR 1430,000 OZ/

total number of notices filed so far this month: 286 for 1,430,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3429: DOWN 23

Bitcoin: FINAL EVENING TRADE: $3440 DOWN $16

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 540/939

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,309.900000000 USD

INTENT DATE: 01/30/2019 DELIVERY DATE: 02/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 18

657 C MORGAN STANLEY 44

657 H MORGAN STANLEY 87

661 C JP MORGAN 828 286

661 H JP MORGAN 254

685 C RJ OBRIEN 3

686 C INTL FCSTONE 2

690 C ABN AMRO 23

737 C ADVANTAGE 5 18

800 C RCG 2 7

880 H CITIGROUP 240

905 C ADM 60 1

____________________________________________________________________________________________

TOTAL: 939 939

MONTH TO DATE: 939

This is the first time in quite a while that we have seen zero whacks on expiry week. The bankers are now in serious trouble as gold and silver quietly rise

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUGE SIZED 4419 CONTRACTS FROM 194,895 UP TO 199,314 ACCOMPANYING YESTERDAY’S 7 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

803 EFP’S FOR MARCH, 0 FOR APRIL, 251 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1054 CONTRACTS. WITH THE TRANSFER OF 1054 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1054 EFP CONTRACTS TRANSLATES INTO 5.27 MILLION OZ ACCOMPANYING:

1.THE 7 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.050 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 43,491 CONTRACTS (FOR 21 TRADING DAYS TOTAL 43,491 CONTRACTS) OR 217.455 MILLION OZ: (AVERAGE PER DAY: 2071 CONTRACTS OR 10.355 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 217.455 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 31.055% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 217.455 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4419 WITH THE 7 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1054 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 5473 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1054 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4419 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 7 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.91 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .998 BILLION OZ TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 286 NOTICE(S) FOR 1430,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.050 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUGE SIZED 11,929 CONTRACTS DOWN TO 471,461 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $0.65//YESTERDAY’S TRADING).

THE LOSS IN OPEN INTEREST IS DUE TO SPREADERS WHO MUST LIQUIDATE THEIR POSITIONS AS THEY COME INTO AN ACTIVE DELIVERY MONTH. SINCE FEBRUARY IS AN ACTIVE MONTH FOR GOLD, THIS IS WHY WE ALWAYS SEE A CONTRACTION IN OPEN INTEREST ONCE WE APPROACH FIRST DAY NOTICE. SINCE THE SPREADERS HAVE AN IDENTICAL LONG AND SHORT POSITION, THE LIQUIDATION DOES NOT AFFECT PRICE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11,261 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 1110 CONTACTS APRIL 8884 CONTRACTS, DECEMBER: 1267 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 471,461. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN TINY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 668 CONTRACTS: 11,929 OI CONTRACTS DECREASED AT THE COMEX AND 11,261 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 668 CONTRACTS OR 66,800 OZ = 2.077 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $0.65.

YESTERDAY, WE HAD 10,460 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 170,782 CONTRACTS OR 17,078,200 OZ OR 531.20 TONNES (21 TRADING DAYS AND THUS AVERAGING: 8132 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAYS IN TONNES: 531.20 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 531.20/2550 x 100% TONNES = 20.83% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,531.20 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED DECREASE IN OI AT THE COMEX OF 11,929 (WITH THE MAJORITY OF THE LOSS COMING FROM THE LIQUIDATION OF THE SPREADERS) DESPITE THE GAIN IN PRICING ($0.65) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,261 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,261 EFP CONTRACTS ISSUED, WE HAD A SMALL LOSS OF 668 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,261 CONTRACTS MOVE TO LONDON AND 11,929 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 2.077 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $0.65 IN YESTERDAY’S TRADING AT THE COMEX

we had: 939 notice(s) filed upon for 93,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $9.80 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 823.87 TONNES

Inventory rests tonight: 823.87 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 15 CENTS IN PRICE TODAY:

ANOTHER BIG CHANGE IN SILVER INVENTORY/

A “PAPER DEPOSIT” OF 1,126,000 OZ

/INVENTORY RESTS AT 310.723 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 4419 CONTRACTS from 194,895 UP TO 199,314 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

803 CONTRACTS FOR MARCH. 251 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1054 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4419 CONTRACTS TO THE 1054 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 5473 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 27.36 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.050 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 7 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1054 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 9.00 PTS OR 0.35% //Hang Sang CLOSED UP 299.62 POINTS OR 1.08% /The Nikkei closed UP 216.95 PTS OR 1.06%/ Australia’s all ordinaires CLOSED DOWN .23%

/Chinese yuan (ONSHORE) closed UP at 6.7040 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 52.48 dollars per barrel for WTI and 60.53 for Brent. Stocks in Europe OPENED GREEN

//. ONSHORE YUAN CLOSED UP AT 6.7040AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7110: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i

i) CHINA/FOXCONN/USA

After much fanfare last year China’s Foxconn is now reconsidering his huge plan to hire 13,000 Wisconsin workers. Trump is not a happy camper on this news

( zerohedge)

ii)

4/EUROPEAN AFFAIRS

i)UK

Tom Luongo, our resident expert on European affairs discusses how the Davos crowd has failed with respect to their plans on thwarting a Brexit.

( TomLuongo)

ii)Do not expect a Brexit deal from the EU until the last minute. Remember that the EU needs England far greater than England needs the EU

( zerohedge)

iii)ITALY

Not good! Italy falls into recession as its 4th quarter GDP falls to negative .20%. The previous quarter fell by .1% and we now have two quarters of negative growth and that fits the definition of a recession

(courtesy zerohedge)

iv)France:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN/EU

This is a huge blow to USA hegemony as Europe launches its alternative to SWIFT (INSTEX) to fund Iran. Trump will be furious and he may be so angry that he will pull out of NATO

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/USA/CITGO

Venezuela’s principal asset in the USA is Citgo which refines 5% of all USA gasoline. It is now weighing its option for bankruptcy. This is where the fun begins…Citgo is a wholly owned asset of PDVSA which is in default and sovereign Russia which lent 3 billion dollars to Venezuela has CITCO shares as collateral. If CITGO goes bust, then Russia owns 49.9% of the stock. The USA wants to transfer the assets to the Guaido

popcorn anyone?…

(courtesy zerohedge)

9. PHYSICAL MARKETS

ii)A good interview of Chris Powell with Jay Taylor as the outline the rigging of gold/silver metal and shares of mining companies.

( Chris Powell./GATA/Jay Taylor)

iii)All 50 states should adopt this: West Virginia proposes eliminating all taxes on gold and silver

( Cortez/MoneyMetalsNews Service)

iv)We have been continually supplying to information that the White House and the Bank of England do not want anybody dealing with the Venezuelans in gold.

( Reuters/GATA)

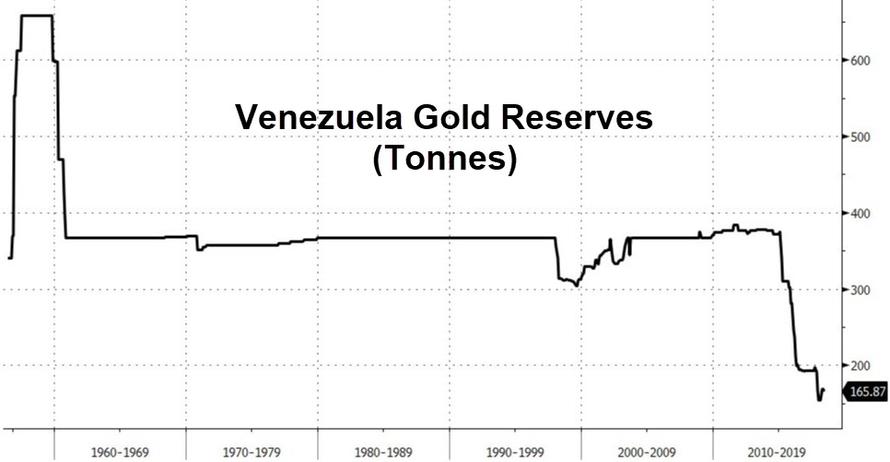

v)I would bet that most of Venezuela’s gold has been disposed of by Maduro

( Bloomberg/GATA)

vi)Ronan Manly states correctly that the Bank of England tore up its gold custody contract with Venezuela. No doubt that their plan to confiscate gold had the approval of the uSA. I feel the real reason that the Bank of England did to return the gold to Venezuela was not for political reasons but for the fact that the goldis gone.

(Ronan Manly/Bullionstar)

vii)A good reason why you do not invest in Bitcoin or any cryptocurrency:l over 1 billion dollars were of cryptos were stolen last year.

( zerohedge)

viii)Venezuela cashes out of 18 tonnes of gold as this was sold to the United Arab Emirates.

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)The Chicago national manufacturing PMI plummets to two year lows

( zerohedge)

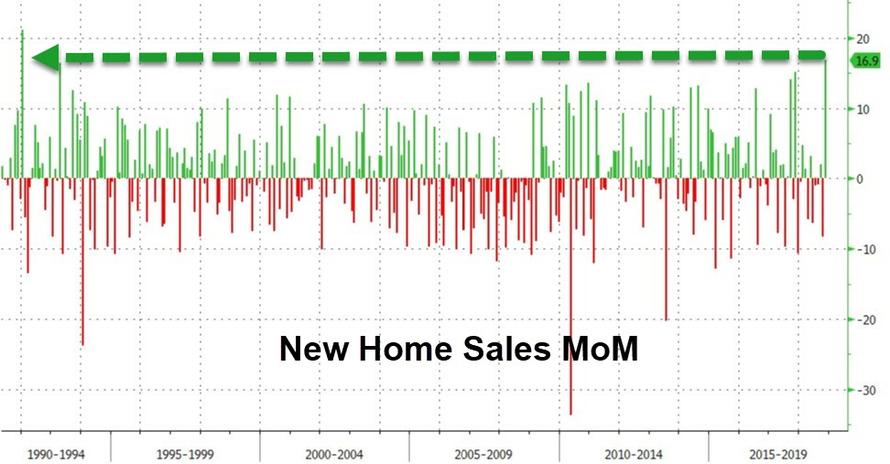

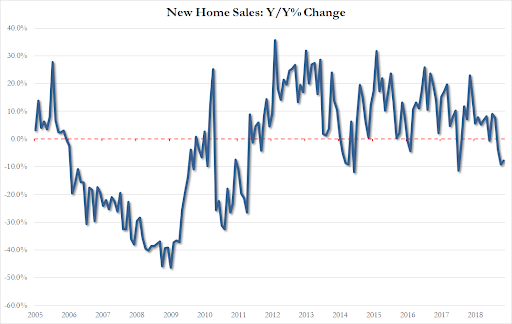

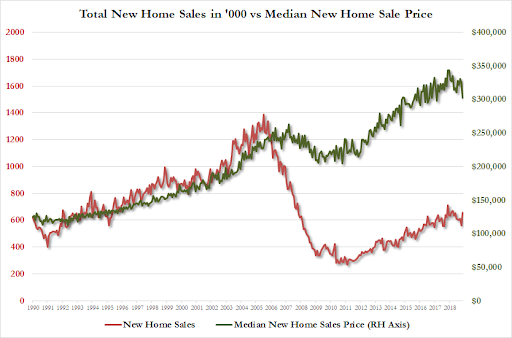

b)Quite a surprise: after continual lousy housing reports, we get November new home sales rise 16.9% month/month. This is the biggest rise since 1992. Probably somebody goofed with the numbers

c)Pending home sales tumble to the lowest level in 5 years. This kind of affirms by belief that the new home sales above is fake

a)The key Conference Board Future expectations signaled recession..a clear sign that the USA is heading lower.

Gundlach slams Powell for caving to the stock market.

(courtesy Gundlach/zerohedge)

c)Trump will not accept any trade deal unless China opens up its market to manufacturers, bankers and farmers.

I extremely doubt that China will comply with this especially the banker front.

( zerohedge)

d)No final deal with China will be announced until Trump meets Xi. No action on the wall discussions as of yet

d)Trump will not accept any trade deal unless China opens up its market to manufacturers, bankers and farmers.I extremely doubt that China will comply with this especially the banker front.

( zerohedge)

e)Amazon is a good Bellwether on the retail front: its shares drop after guidance in the next quarter to its worst revenue growth in 18 years.

iv)SWAMP STORIES

a)Lindsay Graham demands an FBI briefing as to why the FBI needed 29 agents to arrest Roger Stone knowing full well that he was not a flight risk

( zerohedge)

b)The Belarus prostitute that was named in the Steele dossier now admits that she fabricated the evidence claim on Trump.

( zerohedge)

end

Let us head over to the comex:

410 contracts x 5,000 oz per contract = 2,050,000 oz

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 1861 CONTRACTS UP TO 140,207 CONTRACTS. AFTER MARCH, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 2161 CONTRACTS UP TO 27,954 CONTRACTS.

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

i) Into Brinks: 1794.65

i) Out of Delaware: 801.057 iz

ii) Out of HSBC: 897.173 oz

i) Into Brinks dealer: 564.937.98 oz

U.S.-China War M

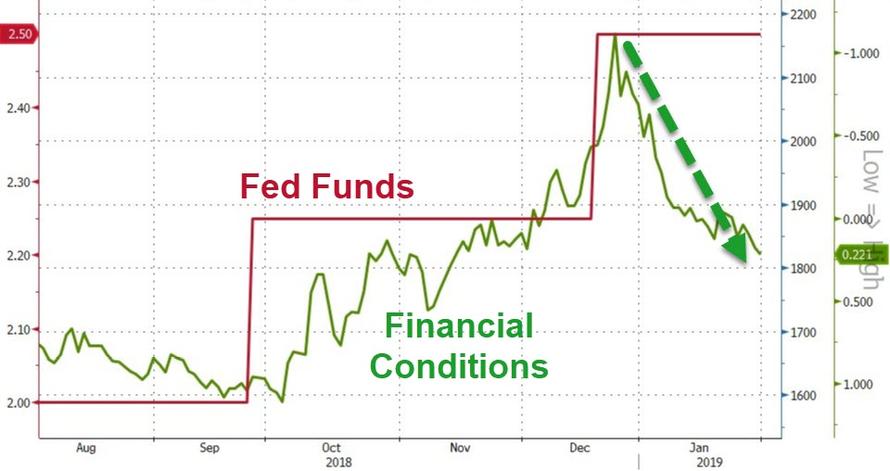

Fed caves on rates and balance-sheet tightening

Submitted by cpowell on Wed, 2019-01-30 19:28. Section: Daily Dispatches

Chairman Powell’s grandfather Dick responds on behalf of monetary metals investors:

http://www.gata.org/files/DickPowellSings.wma

And:

https://www.youtube.com/watch?v=Gt6soO6O6Jg

* * *

Fed Adopts ‘Patient’ Rate Stance With Balance-Sheet Flexibility

By Craig Torres

Bloomberg News

Wednesday, January 30, 2019

The Federal Reserve said today it will be “patient” on any future interest-rate moves and signaled flexibility on the path for reducing its balance sheet, in a substantial pivot away from its bias just last month toward higher borrowing costs.

… The Federal Open Market Committee “will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support” a strong labor market and inflation near 2 percent, the central bank said in a statement Wednesday following a two-day meeting in Washington.

In a separate special statement, the Fed said it’s “prepared to adjust any of the details for completing balance sheet normalization in light of economic and financial developments.” The central bank also said it would be ready to alter the balance sheet’s size and composition if the economy warrants a looser monetary policy than the federal funds could achieve on its own.

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-30/fed-adopts-patient-ra…

.END

A good interview of Chris Powell with Jay Taylor as the outline the rigging of gold/silver metal and shares of mining companies.

(courtesy Chris Powell./GATA/Jay Taylor)

Financial letter writer Jay Taylor interviews GATA secretary on gold price rigging

Submitted by cpowell on Wed, 2019-01-30 19:51. Section: Daily Dispatches

2:50p ET Wednesday, January 30, 2019

Dear Friend of GATA and Gold:

Financial letter writer Jay Taylor (https://www.miningstocks.com/), long a friend of gold and GATA, interviewed your secretary/treasurer yesterday about the mechanics and objectives of gold price suppression by central banks. The interview is 21 minutes long and can be heard at YouTube here:

https://www.youtube.com/watch?v=xqH7Dv42VHU

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

All 50 states should adopt this: West Virginia proposes eliminating all taxes on gold and silver

(courtesy Cortez/MoneyMetalsNews Service)

West Virginia state legislator proposes eliminating all taxes on gold and silver

Submitted by cpowell on Thu, 2019-01-31 00:53. Section: Daily Dispatches

By JP Cortez

Money Metals News Service

Wednesday, January 30, 2019

CHARLESTON, West Virginia — West Virginia legislator Delegate Pat McGeehan, R-1st District has introduced the West Virginia Sound Money Act, House Bill 2684, to eliminate all tax liability on gold and silver in the state.

Following the Wyoming Legal Tender Act, which passed in Wyoming overwhelmingly last year, the West Virginia Sound Money Act is a similar measure that will remove all taxation on gold and silver, including sales and use tax, property tax, individual income tax, and corporate income tax.

…Under current law West Virginia citizens are discouraged from insulating their savings against the devaluation of the dollar because they are penalized with taxation for doing so. House Bill 2684 removes the disincentives to using gold and silver for this purpose. …

… For the remainder of the report:

https://www.moneymetals.com/news/2019/01/30/west-virginia-gold-silver-ta…

END

We have been continually supplying to information that the White House and the Bank of England do not want anybody dealing with the Venezuelans in gold.

(courtesy Reuters/GATA)

Don’t deal in Venezuelan gold, White House says in anti-Maduro push

Submitted by cpowell on Thu, 2019-01-31 01:04. Section: Daily Dispatches

By Shaylim Castro and Jeff Mason

Reuters

Tuesday, January 29, 2019

CARACAS, Venezuela — The White House warned traders on Wednesday not to deal in Venezuelan gold or oil following its imposition of stiff sanctions aimed at forcing socialist President Nicolas Maduro from power.

National security adviser John Bolton tweeted that traders should not deal in gold, oil, or other commodities “being stolen” from the Venezuelan people, as opponents of Maduro’s government worried that a Russian-operated plane had shipped gold out of Caracas this afternoon. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-politics/dont-deal-in-venez…

END

I would bet that most of Venezuela’s gold has been disposed of by Maduro

(courtesy Bloomberg/GATA)

In Maduro’s Venezuela, even counting gold bars is a challenge

Submitted by cpowell on Thu, 2019-01-31 01:33. Section: Daily Dispatches

By Laura Millan Lombrana

Bloomberg News

Wednesday, January 30, 2019

Venezuela is home to rich gold deposits and holds billions of dollars of foreign reserves in gold bars in the central bank’s vaults. The question is: How much is there?

The answer has taken on added significance as beleaguered President Nicolas Maduro faces increasing pressure to resign. Last week countries including the U.S. and U.K. recognized the leader of the National Assembly, Juan Guaido, as the Venezuela’s legitimate leader, amid mass protests. On Monday, the Trump administration issued new sanctions that effectively block crude exports to the U.S., where Venezuela gets the bulk of its cash.

…

While crude is by far Venezuela’s largest export, refined oil and then gold both make up significant sources of revenue, according to data compiled by the Observatory of Economic Complexity of the Massachusetts Institute of Technology. But both the nation’s gold reserves and mining production have dropped in recent years as Maduro’s regime used the yellow metal to generate hard currency in international transactions — and even to exchange it for food and medicine. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-30/in-maduro-s-venezuela…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Ronan Manly states correctly that the Bank of England tore up its gold custody contract with Venezuela. No doubt that their plan to confiscate gold had the approval of the uSA. I feel the real reason that the Bank of England did to return the gold to Venezuela was not for political reasons but for the fact that the goldis gone.

(Ronan Manly/Bullionstar)

Ronan Manly: Bank of England tears up its gold custody contract with Venezuela

Submitted by cpowell on Thu, 2019-01-31 02:17. Section: Daily Dispatches

9:18p ET Wednesday, January 30, 2019

Dear Friend of GATA and Gold:

Confiscation of Venezuela’s gold by the Bank of England, Bullion Star gold researcher Ronan Manly writes today, seems to have been plotted by the United Kingdom and the United States last April when Venezuela’s central bank paid Citibank $172 million to recover gold bars kept at the Bank of England that had been given as collateral for a loan.

…

In any case, Manly writes, the Bank of England’s reputation as a safe and impartial custodian of international gold reserves has been destroyed.

Of course Venezuela’s removal of so much gold from the Bank of England might have greatly endangered the gold price management operation of the major central banks, which is centered on the Bank of England.

Manly’s analysis is headlined “Bank of England Tears Up Its Gold Custody Contract with Venezuela’s Central Bank” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/bank-of-england-tears-up-i…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Venezuela Central Bank Begins Shipping 18 Tons Of Gold To UAE

Venezuela has sold and shipped three tons of central bank gold to the United Arab Emirates (UAE) on January 26 and is preparing to ship 15 more tons, according to Reuters. At today’s spot price of $1,320 per ounce, the sale will total roughly $760 million USD.

Steve Kopack

✔@SteveKopack

Reuters reports, citing sources, that a three ton shipment of Venezuela’s central bank gold left for the UAE on January 26 and the country is preparing a 15 ton shipment in the coming days.

The shipment constitutes 11% of Venezuela’s current gold reserves, and follows the export last year of $900 million of unrefined gold to the UAE and Turkey.

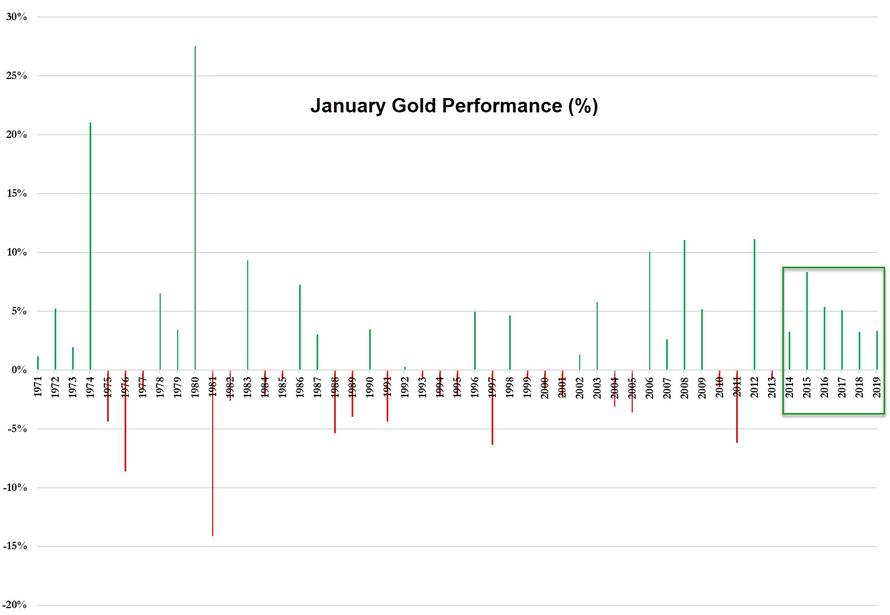

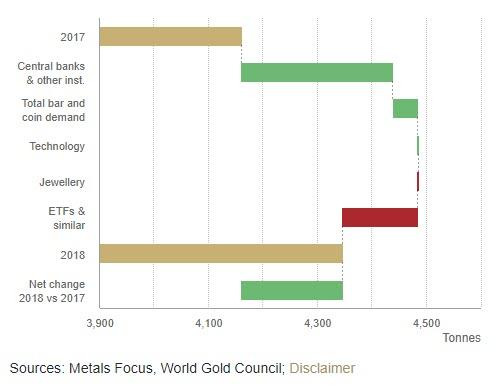

Central Banks’ Gold-Buying Spree Reaches 50-Year High

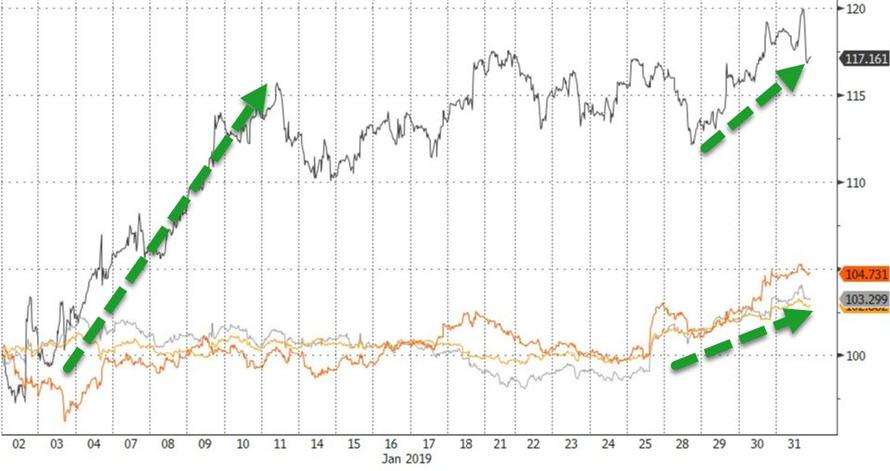

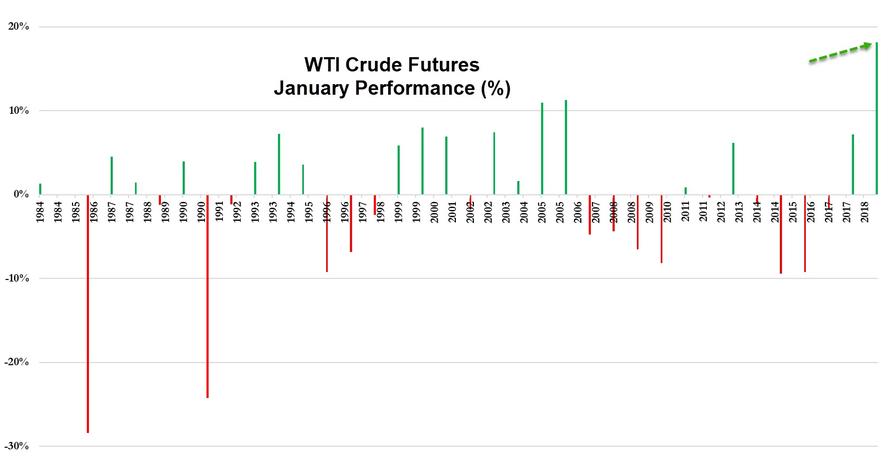

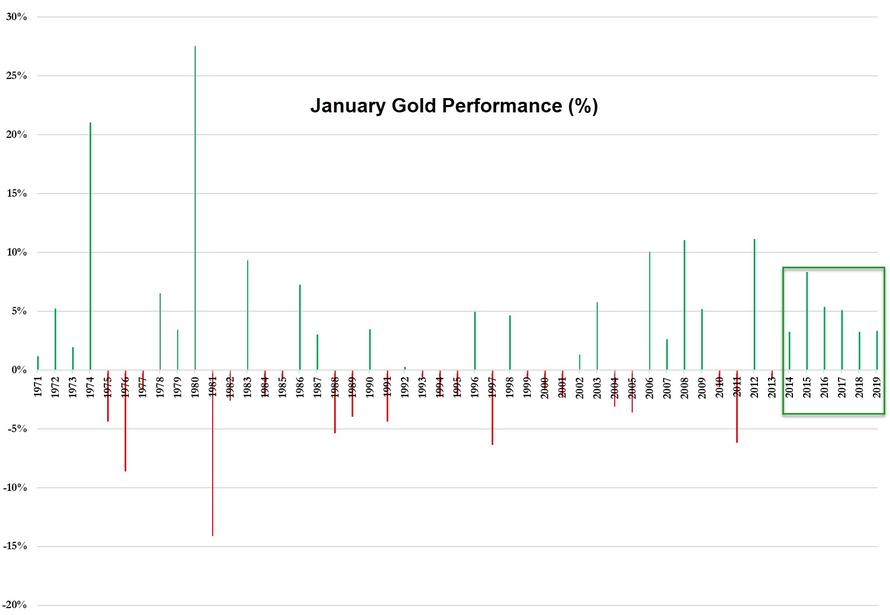

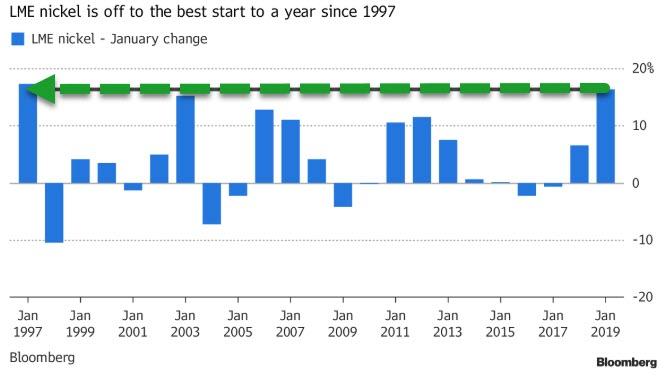

Gold is poised to close out January with a fourth straight monthly gain after the Fed’s uber-dovish flip-flop seemed to signal that it’s done raising interest rates (reportedly for a while but that’s never happened before)…

Raoul Pal

✔@RaoulGMI

The Fed have never, ever “paused” a full hiking cycle. The always end up cutting. Each cutting cycle has led to a recession except mid 1990’s and 1987. Odds are in favour of the Fed having gone too far already and the stock market figuring it out in due course…

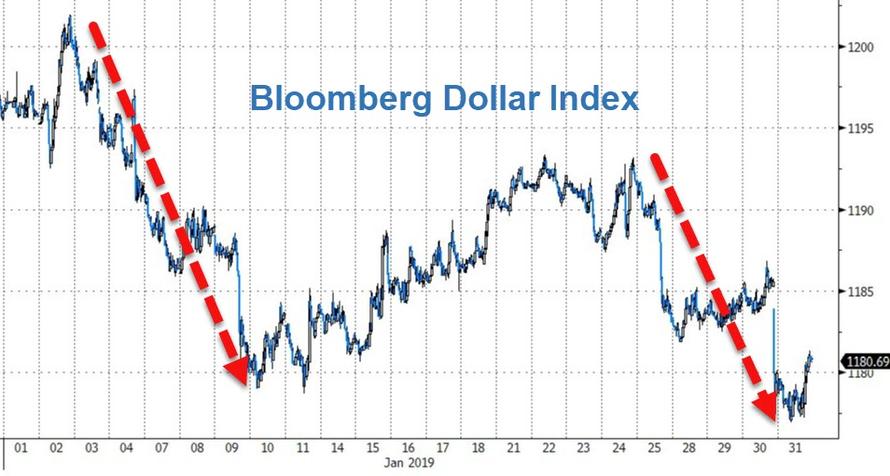

Which has hurt the dollar, helping gold to its sixth January gains in a row as investors sought a haven against slowing growth and U.S.-China trade disputes.

While short interest in GLD (Gold ETF) has soared along with price…

Bloomberg survey results show a decidedly positive bias on the precious metal (Bullish: 13 Bearish: 2 Neutral: 2)

If the Fed’s rate-hike cycle really has come to an end for now, the sooner-than-expected dollar weakness may help gold to “rise more quickly and more sharply,” Commerzbank said in a note.

“Both the tone and language of the Fed statement and presser appeared more accommodative versus consensus expectations,” Citigroup Inc. analysts including Aakash Doshi wrote in a note. “To take advantage of an ongoing gold market rally, investors might consider positioning for upside.”

“Gold is benefiting from a lower dollar in general, as well as safe-haven buyers hedging against the outcome of the U.S.-China trade talks,” Jeffrey Halley, senior market analyst at Oanda Corp. in Singapore, said in a note.

Still, there’s no guarantee gold will keep appreciating at the same pace.

Ole Hansen, head of commodity strategy at Saxo Bank, said by email. While the bank maintains a bullish view on gold, “some caution may now be warranted,” he said.

“With stocks rallying and emerging market assets receiving a boost, the buy-gold story has faded, at least for now,” Hansen said.

And as BCS Global Markets said in a note, the big range in analysts’ outlook for gold this year shows “that there is actually no consensus.”

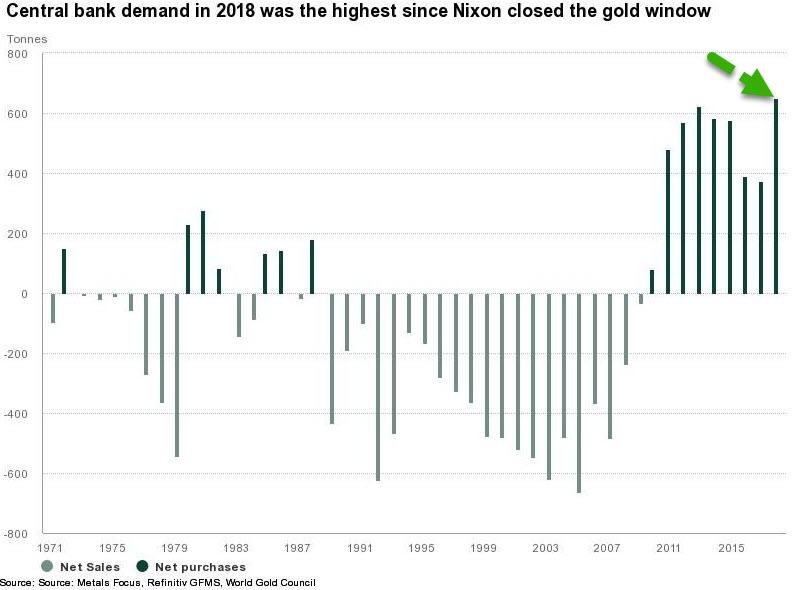

However, there is one group of global ‘investors’ who are waving in those bullion trucks with both hands and feet – The world’s central banks…

Central banks bought last year the most gold in 47 years, with 651.5 tonnes (74% higher YoY). This is the highest level of annual net purchases since the suspension of dollar convertibility into gold in 1971…

Additionally, Bloomberg’s Javier Blas notes that the 2018 gold buying spree by central banks isn’t just the biggest in 47 years, but also the second highest annual total on record (only surpassed by 1967, when central bank gold reserves increased by 1,404 tonnes).

“Heightened geopolitical and economic uncertainty throughout the year increasingly drove central banks to diversify their reserves and re-focus their attention on the principal objective of investing in safe and liquid assets,” said the World Gold Council report released on Thursday.

Strong central bank and consumer demand offset ETF outflows…

More central banks look to gold.

Russia, Kazakhstan and Turkey again accounted for a large portion of demand in 2018. But their share fell to 58 % – from 94 % in 2017 – as other central banks chose to significantly increase their gold reserves, reinforcing the importance of gold as a reserve asset.

Notably, European central banks also bought gold last year. Hungary made one of the largest purchases, increasing its gold reserves ten-fold in October, to 31.5t. This is the highest level for nearly 30 years. The central bank cited gold’s role as a hedge against future structural changes in the international financial system, as well as its lack of counterparty or credit risk, as reasons for the purchase. Similarly, Poland was another European central bank which bought last year. Gold reserves rose by 25.7t during 2018, +25% y-o-y.

Indian net purchases were another notable component of central bank demand in 2018. Monthly purchases began in March and picked up in the second half of the year. In total, gold reserves rose by 40.5t, the highest annual growth since the purchase of 200t from the International Monetary Fund In 2009.5 In its Annual Report 2017-2018 the bank stated: “Diversification of India’s Foreign Currency Assets (FCA) continued during the year with attention being ascribed to risk management, including cyber security risk. The gold portfolio has also been activated.”

Mongolia announced that it had bought 22t of gold in 2018, in line with its stated target. This represented a 10% increase on 2017 purchases. One of the drivers of this growth was a five-month “National Gold to the Fund of Treasures” campaign, which encouraged miners and individuals to sell their gold to the central bank.6

In September, the Central Bank of Iraq stated that it had taken advantage of lower gold prices to buy 6.5t. This was the first annual increase since 2014 and took total gold reserves to 96.3t, accounting for 6.7% of total reserves.

The State Oil Fund of Azerbaijan (SOFAZ) also re-entered the market last year. Gold reserves grew by 14.3t by the end Q3, an increase of nearly 50% from end-2017.7 Having been on the side-lines of the gold market since the end of 2013, this marked a change in policy for the fund. In December 2018, President Ilham Aliyev approved updated investment guidelines that would allow SOFAZ to invest up to 10% of its portfolio in gold. Currently, gold accounts for 4.3% of SOFAZ’s portfolio.

So, what do the central banks know that mom-and-pop FAANG-buyer don’t?

end

A good reason why you do not invest in Bitcoin or any cryptocurrency:l over 1 billion dollars were of cryptos were stolen last year.

(courtesy zerohedge)

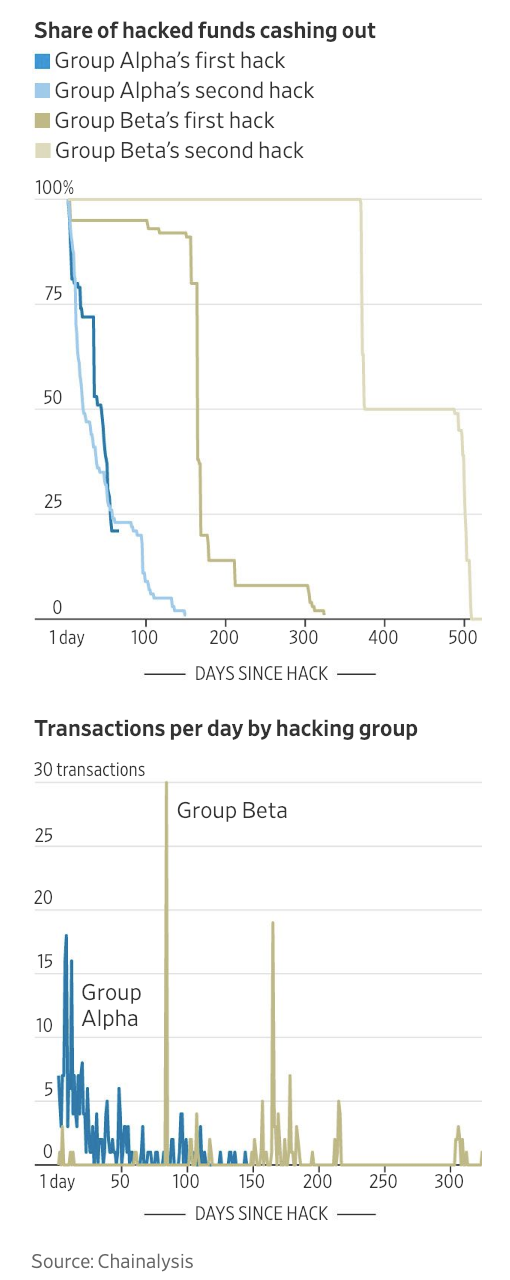

Explosive Report Claims Two Hackers Stole $1 Billion In Crypto

Crypto related hacks have fallen in frequency since the great crypto bust of 2018 – or at the very least, they don’t grab headlines like they once did. They’ve also become an accepted risk of trading in crypto: Gone are the days when a devastating hack like the one that brought down Mt. Gox back in 2014 have had serious repercussions for the entire crypto market.

But that hasn’t deterred firms like Chainalysis, the respected crypto forensics firm that has reportedly helped the FBI and other US law enforcement agencies track illicit activity and bust money launderers using crypto, from exploring the methods used by hackers to conceal the provenance of stolen coins on a system that touts transparency as one of its biggest selling points.

During the course of its research, Chainalysis happened upon a surprising finding: Just as there are “whales” who hold concentrated portions of crypto wealth, so there are whale-like hackers who are responsible for much of the thievery that has plagued the eco-system. According to a Wall Street Journal summary of Chainalysis’ findings, two groups of highly sophisticated criminals appear to have stolen some $1 billion in cryptocurrency, an amount that accounts for the majority of the money lost to hackers. Some $1.7 billion in crypto has been reported stolen over the years, mainly from exchanges (Mt. Gox and Bitfinex being two of the most infamous hacks).

Chainalysis spent about three months tracking the stolen funds in known hacks, and noted that there’s a slight chance that its analysis is incorrect.

The analysts at Chainalys christened the groups “Alpha” group and “Beta” group. The MOs of the two groups differ in one important way. While established government-linked groups like the Lazarus Group have been identified as the culprits behind certain hacks (like the hack of South Korea’s Bithumb), Chainalysis said these two groups appear to be independent – and possibly amateur – criminals.

Chainalysis’s digital investigators determined that likely wasn’t the case when they analyzed the transaction flows from known hacks. The firm believes it has connected most of the hacks to two groups, which it labeled alpha and beta.

Alpha is “a giant, tightly controlled organization at least partly driven by nonmonetary goals,” Chainalysis said in its report. Beta, the second group, is smaller and less organized, a “heavily sanctioned organization absolutely focused on the money,” according to the report.

Chainalysis said the two hacker groups employed an extensive network of digital wallets to hide their tracks and later converted the money to physical cash through online exchanges and individual transactions. The stolen funds were transferred an average of 5,000 times before they were converted into cash, Chainalysis found.

Alpha tends to immediately begin shuffling the funds around, according to the report. One hack involved 15,000 transfers. The entity converted about three-quarters of its stolen funds into cash within an average of 30 days.

Beta, on the other hand, may sit on the stolen funds for up to 18 months, waiting for any publicity surrounding the hack to fade. “When they feel ready to cash out, they quickly hit one exchange, cashing out over 50% of funds within days,” the report said.

Though thieves prefer unregulated exchanges (as the bust of shadowy exchange BTC-e showed), thieves will sometimes use regulated exchanges to launder the funds. Because by the time the funds have gone through so many transfers, even exchanges with stringent AML controls can’t trace them.

end

huge trading in the petroyuan scheme. Hopefully this will translate into massive imports of gold into China as owners and sellers of oil receive first yuan and then transfer those yuan into gold:

courtesy Nicholas B

PetroYuan and Other Topical Matters

Good Morning Bill/Harvey, (from Africa)

A few minutes ago (2.00 am ET) the Shanghai Energy Exchange closed its futures trading book for January 2019.The first full month of trading on the petroyuan futures contract was April 2018, when total turnover was just over half a trillion yuan. In November and December 2018, aggregate monthly turnover plateaued between 4.1 trillion and 4.2 trillion yuan and this has now increased to Yuan 4,642,063,051,800 in respect of January 2019.This turnover is achieved between the hours of 9-11.30 and 13.30-15.00 on weekdays –Shanghai is 13 hours ahead of ET so these rather restricted trading periods are basically in operation when the West sleeps. 24/7 trading is only an imperative for the obscene, corrupted COMEX/GLOBEX platforms so that peak illiquid periods can be identified in which to engineer the biggest possible impact from criminally manipulative paper trades.

Let us unpack this January 2019 data and see what it means on the ground. A barrel of oil is currently about Yuan 380 (three months out). The turnover data as reported on the Shanghai International Energy Exchange is ‘double sided’ and hence the number to dissect is only half the total as recorded above, which equates to Yuan2,321,031,525,900.

· Therefore about 6.1 billion barrels traded in January 2019 in lots of 1,000 barrels per trade.

· Open interest tends to evaporate (or rather be rolled forward) as the front month contract expiration approaches. The total open interest upon expiration of the SC1902 contract today was only 84 lots (84,000 barrels). Currently 42,048,000 million barrels are standing for 28th February 2018, but don’t hold your breath.

· There is, however, a genuine and detailed ‘’exchange for physical ‘(efp) mechanism” outlined in the rules of the Shanghai Energy Exchange .Such efp totals are excluded from the Exchange’s reported data, which is a pity, but perhaps is necessary to delay the onset of open warfare if the petrodollar hegemony was seen to be challenged in such an overt manner.

· China’s physical importation requirement for crude oil is reported to be about 7.6 million bpd to supplement domestic production of about 3.8 million bpd .About 203 million barrels trade daily (based on 30 days) on the Shanghai futures so would it be absurd to postulate that about 3.7% of this figure results in efp transactions. Perhaps most of China’s physical oil imports still occur on petrodollar denominated platforms, but is this probable?

Virtually no commentator mentions this inexorable crescendo in the emergence of the petroyaun, but it is clearly a principal component in the financial plumbing now being constructed on many fronts to enable USD trading platforms to be de emphasized as the East prepares to wean itself from the consequences of the abusive and delinquent mismanagement of the global reserve currency as exercised by the FED and USA politicians.

Tomorrow the BLS will release the Jan.2019 NFP report. (Zero Hedge reported that Larry Kudlow knew the no. two weeks ago.) I have a query. The BLS mendaciously fabricates its monthly survey data, but what is the sequence thereafter? Does the BLS apply the Birth/Death model inflator (which should be a deflator) and then only ‘’goal seeks’’ by applying quadruple or quintuple seasonal adjustment factors, or are the seasonal adjustment factors applied to the fabricated base data first, and then only is the Birth/Death model inflator (which should be a deflator) used as a final massaging tool? But then does the answer matter one little bit.

Also tomorrow the ‘transparent’’ LBMA will release 90 days in arrears, as at 31st October 2018, the (metronomically constant) loco London precious metal vault holdings. Don’t laugh because if you also collected data on horseback and then input this data into antiquated ledgers, you would also release your results in arrears, but maybe (say) only by 10 days or so. I am not a conspiracy theorist so I am inclined to accept this LBMA data as being (more or less) reasonably accurate .But just like the NFP data, it is pure propaganda, because the LBMA would never allow any visibility into the total claims on this physical gold. At last I have discovered why there are various estimates about the extent of fractional reserving in respect of total claims on this physical loco London gold. 140 times (as per Andrew Maguire last week) is the estimate of fractional reserving on the assumption that all gold bars comply with LBMA minimum .995 finesse requirements. But thanks, inter alia, to Robert Rubin, this fractional reserving estimate increases to 236 times when all identified tungsten contaminated bars are excluded. Then there is the immortal quotation of Don Rumsfeld about known knowns, known unknowns and unknown unknowns. The unknown unknown in this case relates to a contingency for tungsten contaminated bars that have hitherto escaped official detection, and when factored into the equation, this additional contamination moves the fractional reserving estimate up to 272 times (meaning that there are 272 legitimate claims on every ounce of non-tungsten contaminated physical vault gold). I recall once reading a claim that fractional reserving was as high as 500/1, but after yesterday’s Fed capitulation will fractional reserving of even 10/1 be manageable?

Regards

Nicholas

*J. Johnson’s Latest

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7040/

//OFFSHORE YUAN: 6.7110 /shanghai bourse CLOSED UP 9.00 PTS OR 0.35%

HANG SANG CLOSED UP 299,62 POINTS OR 1.08%

2. Nikkei closed UP 216.95 POINTS OR 1.06%

3. Europe stocks OPENED ALL MIXED

/USA dollar index FALLS TO 95.29/Euro RISES TO 1.1494

3b Japan 10 year bond yield: RISES TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.58/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.22 and Brent: 61.84

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.18%/Italian 10 yr bond yield DOWN to 2.60% /SPAIN 10 YR BOND YIELD DOWN TO 1.22%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.42: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.88

3k Gold at $1323.10 silver at:16.10 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 10/100 in roubles/dollar) 65.30

3m oil into the 53 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9931 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1415 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.18%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

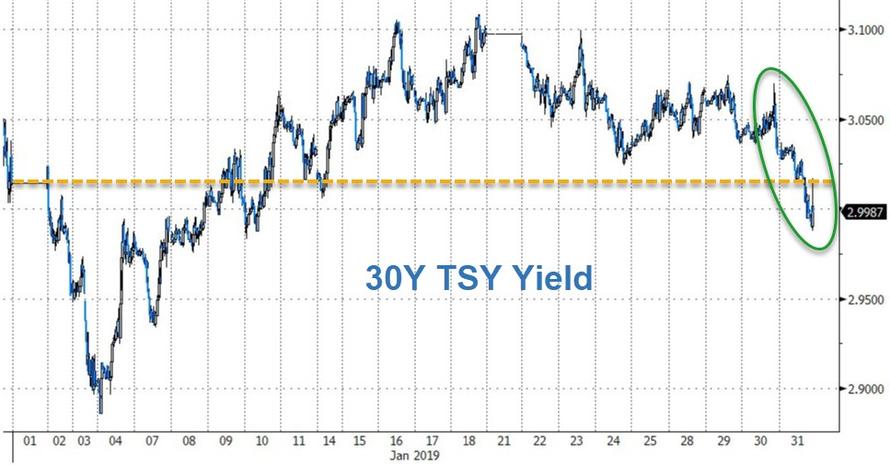

4. USA 10 year treasury bond at 2.69% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.1942

Global Stock Rally Fades After Italy Slides Into Recession

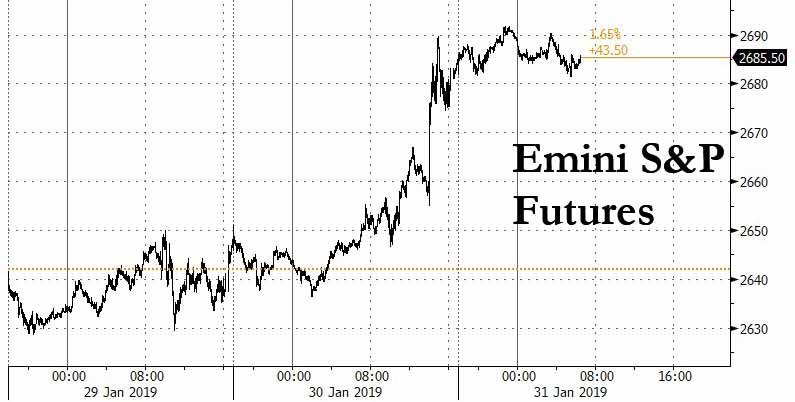

The total capitulation by the Federal Reserve which confirmed all it cares about is the stock market, propelled world stocks to their best January on record on Thursday, although in a deja vu of last January, when stocks similarly soared only to flop spectacularly, traders were trying not to get too carried away.

An overnight rally in global markets, helped by a dovish capitulation by the Fed which sent the S&P 1.55% higher on Wednesday as well as strong results from Facebook that sent the stock 11% higher premarket, faded overnight following another contractionary print in China’s official manufacturing PMI (49.5, up from 49.4 in Dec and above the 49.3 estimate), and the latest GDP print out of Italy which confirmed that the country had entered a recession for the first time in 6 years.

Even with the modest fade in sentiment, the MSCI world stocks index rose 0.5% and for the 20th day out of the last 23. For January it is up more than 7.2% which is its best January since the index began in 1988 and the best performance in any month since December 2015. “The rally really does lift all boats,” said Pictet emerging market portfolio manager Guido Chamorro.

S&P futures and European stocks traded mixed on Thursday following catch up gains in Asia as investors took a pause in the wake of mixed corporate earnings despite now open support from the Federal Reserve which signaled an extended rate hike pause and announced it will be flexible on the path for reducing its balance sheet, sending the S&P to an 8-week high even as Nasdaq contracts stayed in the green, helped by better-than-expected results at Facebook. Meanwhile, Treasury yields and the dollar extended Wednesday’s declines. As a result, S&P futs were unchanged before President Trump was set to meet top China trade negotiator Chinese Vice Premier Liu He in the second day of the US-China trade talks.

Europe’s Stoxx 600 Index trimmed early gains of as much as 0.6%, dragged lower by banks and telecos as energy companies rose following strong results from Shell. Italy’s FTSE MIB index dropped on data showing the country fell into recession at the end of 2018, its first in 6 years.

Germany’s DAX drifted 1% off session high, as Deutsche Bank weighs on the index following news the German lender could be forced to merge with Commerzbank by mid-year if its results dont improve. FTSE-100 up 0.6%

MSCI’s index of Asia-Pacific shares rose to its highest since October helped by a 1% jump on Japan’s Nikkei which shrugged off the normal headwind of a higher yen. The main emerging market index skipped to a more than 8 percent January gain while the Shanghai Composite Index climbed 0.3 percent despite data showing China’s factory activity contracted for a second straight month.

Emerging-market stocks were poised for their best monthly gain in almost three years and while Powell’s dovish turn boosted currencies for a seventh day as the dollar extended its decline. The MSCI emerging-market equity index added to yesterday’s advance to head for a four-month high. The currency gauge was set for its longest winning streak in more than a year, with South Africa’s rand, Turkey’s lira and Brazil’s real leading gains since the U.S. central bank’s statement on Wednesday.

In FX, the Bloomberg Dollar index slipped to the the lowest since Sept. 27 as focus turned to US payrolls data due Friday; the greenback fell versus all G-10 peers, while the yen and risk-sensitive currencies led gains following the dovish Fed remarks; Treasuries rallied, outperforming Bunds. The euro reversed gains to trade below the 1.15 handle; the common currency initially shrugged off weaker-than-forecast German retail sales (-4.3% m/m in Dec. vs est. -0.6%) before edging lower despite euro-area growth in the three months through December matching estimates at 1.2% y/y, pressured by Italian GDP data.

With Wednesday’s statement the Fed helped ease fears that it would continue with plans to tighten policy even in the face of cooling economic data. The Fed said it would be “patient” about any future rate hikes and signaled flexibility in reducing its bond holdings, adding fuel to the emerging-market rally that began as 2018 drew to a close.

Investors now have a wary eye on meetings between Chinese negotiators and their counterparts in Washington as talks to resolve the trade dispute continue.

“I suspect the Fed news will trump everything, and people will look at the news, whatever comes in these earnings, against the backdrop of what the Fed is doing,” Gavin Friend, senior market strategist at National Australia Bank in London, said in a podcast. “It could be the catalyst for a breakthrough in key levels in the dollar index against major currencies.”

Looking at today’s key event, President Trump will meet with Chinese Vice Premier Liu He at 15:30 EST today. Trump also said it is highly unlikely he would be willing to include ‘Dreamers’ in negotiations regarding border security and government funding, while there were separate reports that the White House is said to prepare an emergency wall plan. US Democrats reportedly suggested openness for a compromise with President Trump, despite unveiling initial proposal for border security which doesn’t include a physical barrier.

In the latest Brexit news, the EU stands ready to take Brexit to a last-minute summit rather than bend the knee to demands from UK PM May, according to diplomats citing the scheduled summit on March 21-22. UK PM May is also said to be putting together a series of measures in an attempt to woo Labour MPs to support her Brexit deal; measures include cash injections into leave-supporting deprived areas.

In the commodity markets, oil prices rose for a third day, pushed up by lower imports into the United States amid OPEC efforts to tighten the market, and as Venezuela struggles to keep up its crude exports after Washington imposed sanctions on the nation. U.S. West Texas Intermediate crude futures were at $54.47 per barrel, up 24 cents, or 0.4 percent, from their last settlement. Brent was up 36 cents, or 0.6 percent, at $62.01 per barrel.

Expected data include jobless claims and new home sales. Blackstone, Conoco, Ferrari, GE, Mastercard, UPS, and Amazon are among companies reporting earnings.

Market Snapshot

- S&P 500 futures little changed at 2,684.25

- STOXX Europe 600 up 0.1% to 358.96

- MXAP up 1.2% to 156.58

- MXAPJ up 0.8% to 510.49

- Nikkei up 1.1% to 20,773.49

- Topix up 1.1% to 1,567.49

- Hang Seng Index up 1.1% to 27,942.47

- Shanghai Composite up 0.4% to 2,584.57

- Sensex up 1.8% to 36,246.18

- Australia S&P/ASX 200 down 0.4% to 5,864.65

- Kospi down 0.06% to 2,204.85

- Brent futures up 0.4% to $61.90/bbl

- Gold spot up 0.2% to $1,321.92

- U.S. Dollar Index little changed at 95.31

- German 10Y yield fell 2.3 bps to 0.165%

- Euro up 0.06% to $1.1487

- Italian 10Y yield fell 3.4 bps to 2.243%

- Spanish 10Y yield fell 3.7 bps to 1.217%

Top Overnight News from Bloomberg

- U.S. President Donald Trump will meet China’s top trade negotiator in the Oval Office on Thursday for high-level talks, with little indication that Beijing will bend to American demands to deepen economic reforms

- Italy fell into recession at the end of 2018, capping a year of political turmoil, higher borrowing costs and fiscal tensions that took their toll on the economy. The contraction will put further pressure on the coalition government, which already appears to be fraying

- The European Union is prepared to take Brexit down to a last-minute, high-stakes summit rather than cave into U.K. Prime Minister Theresa May’s demands over the next few weeks, diplomats said

- The number of Chinese companies warning on earnings is turning into a flood as a deadline looms on Thursday, with no industry spared from worsening demand

Asian stocks were mostly higher across the board as they took impetus from their counterparts in US where sentiment was lifted on the back of earnings and a dovish Fed, while the region also digested better than expected Chinese PMI data. ASX 200 (-0.4%) and Nikkei 225 (+1.1%) both initially benefitted from the rising tide in the aftermath of the FOMC, although weakness in Australia’s largest weighted financial sector later dragged on the local bourse, while a slew of corporate updates shared the focus for Japan. Hang Seng (+1.1%) and Shanghai Comp. (+0.4%) conformed to the positive tone following better than expected Chinese Manufacturing PMI and Non-Manufacturing PMI data, while another PBoC liquidity injection ahead of next week’s Lunar New Year and ongoing US-China trade talks also contributed to the optimism. Finally, 10yr JGBs were initially higher as they tracked the upside in T-notes post-FOMC and as the BoJ Summary of Opinions unsurprisingly reiterated the need to persistently continue powerful monetary easing, although gains were later pared despite stronger 2yr auction results as upside was restricted by the firm risk sentiment.

Top Asian News

- Ship Giants to Join Forces in Korea to Fend Off China Threat

All Major European indices initially opened higher [Euro Stoxx 50 -0.3%] continuing the overnight gains seen in Asia which benefited from a dovish Fed alongside strong earnings from Facebook, who were up 11.5% after-market; although European indices have since reverted much of this following an earnings dominated open. FTSE 100 (+0.5%) is benefitting from Shell (+4.1%) and Diageo (+4.0%) due to both companies’ earnings beating on expectations; Shell’s strong performance has subsequently led to outperformance in the energy sector (+2.3%). The SMI (U/C) is the underperforming sector, weighed on by Swatch (-5.4%) who are at the bottom of the Stoxx 600 after their FY group sales missed expectations; although losses are capped by strong performance in Roche (+2.2%) following their earnings. Other notable movers include, Unilever (-3.7%) who anticipate 2019 underlying sales growth at the bottom of their 3-5% range; and as such are down on the day. Elsewhere, Wirecard (+1.8%) have recouped some of the losses seen in the previous session due to an FT article reporting that an executive has been accused of using forged contracts. And BT (-2.6%) are down despite reiterating EBITDA guidance at the top end of expectations for FY18/19, as Philip Jansen is to take over as CEO from Gavin Patterson on Friday.

Top European News

- Spain’s Economy Remains Bright Spot Amid Euro-Area Slowdown

- Shell Pledges to ‘Do It All’ as Cash Surge Underpins Returns

- As Wirecard Gets Bigger, So Does the Target on Its Back

- Nestle Chairman Signals He’s Open to a Full Sale of Skin Health

In FX, odds looked stacked against the Greenback following an arguably even more dovish twist from the FOMC than many or most were looking for (effectively announced a pause in the tightening cycle, with patience going forward and not necessarily further hikes at this stage, or much more balance sheet reduction). This, coupled with some ‘strong’ sell signals for month end portfolio rebalancing saw the Buck slump to new recent lows vs G10 peers, while the DXY slipped under its 200 DMA (95.290) at one stage to 95.127 before stabilising and perhaps benefiting from early SOMA-related positioning (front-running ahead of the usual flow window).

- JPY – The main beneficiary of post-Fed Dollar weakness and pronounced US Treasury curve bull-steepening, as Usd/Jpy reversed sharply from 109.50+ peaks into the FOMC to circa 108.50. Note, however, option expiries between 108.90-109.00 in 1 bn may limit further downside in the headline pair ahead of the NY cut.

- AUD/NZD – Also revelling in the broadly bearish Usd hue, plus a revival in risk appetite, which partly Fed induced and underscored by improvements in China’s manufacturing and services PMIs overnight. Aud/Usd is consolidating off fresh multi-week highs circa 0.7275 having blasted through daily tech resistance around 0.7207 that had been containing advances ahead of the FOMC, while Nzd/Usd is pivoting 0.6900 with the Kiwi drawing additional momentum from S&P’s NZ rating outlook upgrade to positive from stable.

- GBP/CHF/CAD – All firmer vs the US Dollar, albeit marginally, as Cable continues to trade heavily around 1.3150 amidst the ongoing Brexit hiatus, while the Franc remains in a 0.9900-50 range and Loonie meanders between 1.3120-55 awaiting some independent impetus from looming Canadian GDP and PPI data before a speech from BoC’s Wilkins.

- EUR – The single currency finally breached its 100 DMA around 1.1443, and 1.1450 on its way to a 1.1515 peak vs the Usd, but has been undermined by more poor Eurozone data in the shape of German retail sales and Italian GDP (both negative and worse than forecast). Note, the aforementioned SOMA interests also have a tendency to weigh on Eur/Usd more than other Usd/major pairings.

In commodities, it was a mixed session in the commodities complex thus far, as the energy benchmarks pare back a bulk of yesterday’s Fed-induced gains with WTI (-0.2%) drifting into negative territory and Brent (+0.5%) off best levels. Oil prices have been on a downwards trajectory for most of the EU session with a brief Brent dip below USD 61.50/bbl, coinciding with the Iraqi oil ministry stating 40 oil wells are to be drilled in the Southern Manjoon oilfield. As reference the Manjoon oil field is estimated to have reserves of almost 12.6bln barrels. Otherwise, new-flow has been light in the complex with traders keeping a close eye on US-Sino trade developments with Vice Premier Liu He due to meet US President Trump at the Oval office around 20:30 GMT. On the Venezuelan front, Chinese energy giant PetroChina is reportedly planning to drop Venezuelan state-owned PDVSA amid the US oil sanctions on the company in the backdrop of Venezuela’s political turmoil. The sanctions seem to have a muted impact in the oil market thus far as US already stated that any shortfalls in output will be countered with the use of the US Strategic Petroleum Reserve. Meanwhile, prices are somewhat underpinned by the OPEC production cuts with figures stating output amongst the members fell 900k BPD, (vs. 800K planned at the latest meeting); as according to JBC.

Elsewhere, metal prices are supported by the still-subdued dollar with spot gold poised to end the month with a fourth consecutive monthly gain, prices reached levels last seen in May 2018 as the yellow metal advances above USD 1320/oz. Citigroup notes that the precious metal is benefitting from a weaker buck alongside safe-haven buyers hedging against the outcome of the US-China trade talks. Moving on, nickel and steel prices are expected to be weighed on by a soaring output of the raw material in China and Indonesia and as such, BMO analysts expect the nickel deficit to narrow to 96k tonnes in 2019 vs. current 129k tonnes.

Looking at the day ahead, we’re due to get Q4 ECI (+0.8% qoq expected), latest weekly initial jobless claims, November new home sales and the January Chicago PMI (2.3pt drop to 61.5 expected). Away from the data the ECB’s Coeure, Mersch and Weidmann are due to speak at separate events while earnings highlights include Amazon, Royal Dutch Shell, Unilever, DowDuPont, General Electrics, Diageo and ConocoPhillips.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 35.3%

- 8:30am: Employment Cost Index, est. 0.8%, prior 0.8%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 199,000; Continuing Claims, est. 1.72m, prior 1.71m

- 9:45am: Chicago Purchasing Manager, est. 61.5, prior 65.4

- 10am: New Home Sales, est. 570,000, prior 544,000; MoM, est. 4.78%, prior -8.9%

- 4pm: Total Net TIC Flows, prior $42.0b

DB’s Jim Reid concludes the overnight wrap

If you’re in the U.K. I hope you’ve met today’s tax return deadline. I still haven’t quite finished mine and I’m a little stressed as to when I’ll get the chance. This is the most complicated of my life as during the last tax year I sold all my worldly possessions (apart from my family and my golf clubs) to buy our new house. I’ve had to go through 24 years of files to work out what I’d originally paid for all the assets that I subsequently sold. Surprisingly some were actually sold higher than where I’d bought them. Others less so! At least next year’s will now be easy as pretty much all I own is tied up in a vastly overpriced U.K. house in a post Brexit era.

On the positive side this last day of January will be greeted with more enthusiasm than the last day of the previous two very poor months for performance. The Fed helped supercharge this last night with US markets advancing to their highest levels since early December after delivering a surprisingly dovish policy statement at yesterday’s meeting. It marked the first Fed meeting day in which the S&P 500 rallied since Chair Powell’s tenure began, snapping a streak of seven straight losses on Fed meeting days. Has Mr Powell now yielded to the desires and moods of financial markets? Indeed, yesterday was the best “Fed day” performance since December 2014, when then-Chair Yellen struck a similarly dovish tone and the committee inserted a reference to being “patient” into the statement.

The p-word was again a key factor at yesterday’s meeting, as its re-introduction marked one of several notably dovish changes that supported yesterday’s market reaction. As a reminder, yesterday was the first of the previous “off” meetings with a press conference. There was also the normal policy statement, but no update to FOMC participants’ macro and interest rate forecasts.

The new policy statement had four notable changes that all leaned in a dovish direction: theyi) removed the “further gradual increases” description of the policy path, ii) added “market-based measures of inflation compensation have moved lower,” iii) added a reference to “muted inflation pressures,” and iv) added a sentence saying “the Committee will be patient as it determines what future adjustments” to rates will be appropriate. Taking items i and iv together, the committee therefore removed its tightening bias, and looking at ii and iii this indicates that incoming hard data and market pricing on the inflation front are the key variables to watch before the fed returns to its tightening track. The policy statement was accompanied by a separate note which committed to using the fed funds rate as the main policy tool and to maintaining enough excess reserves moving forward to maintain the “floor” system. That was consistent with our economists’ expectations, but still represents an official confirmation.

Our economists now believe that the risk to their call for two more rate hikes later this year and another one next year has shifted a bit further to the downside, though the substantial further lift to financial conditions resulting from yesterday’s announcement somewhat limits this downside risk. See here for their full summary of the meeting.

Now to recap the strong day of market rallies. Yields on two-year Treasuries rallied -6.5bps while 10-year yields fell a more modest -3.2bps, leading the yield curve to bull steepen +3.2bps. The dollar dropped -0.50%, with the euro gaining +0.41% and emerging markets outperforming, up +0.65%. The NASDAQ advanced +2.20%, while the S&P 500 and DOW rallied +1.57% and +1.77% respectively, though to be fair the major indexes were already around 1 percent higher on the session before the Fed gave the rally an extra boost. The main factor during morning trading in New York was positive earnings reports (more details below).

After the close markets also had to contend with a couple of bellwether numbers in the tech space, with Facebook and Microsoft highlighting results. Thesocial media giant beat expectations on profits, revenue, and active users, and shares rallied over 11% overnight. Microsoft’s earnings and sales figures were slightly below analysts’ expectations, and shares slid -4%. Qualcomm’s revenues were a touch soft as well, but a healthy beat on profits helped shares rally over 2%. Net-net, NASDAQ futures are up +0.42% while the rest of Asia is taking the lead from Wall Street with healthy gains for the Nikkei (+1.16%), Hang Seng (+1.06%), Shanghai Comp (+0.69%) and Kospi (+0.36%).

We haven’t heard any sound bites to come from the US-China trade talks as of yet with talks continuing today however sentiment overnight has also partially been helped by the January PMIs in China where both the manufacturing (54.7 vs. 53.8 expected) and services (49.5 vs. 49.3 expected) prints came in higher than expected. The manufacturing reading also rose 0.9pts from December and it leaves the composite 0.6pts higher at 53.2, and therefore the highest since September last year.

Back to yesterday, where the earnings highlights included a +6.83% rally for Apple (post the numbers after the close on Tuesday), Boeing (+6.30%), AMD (+19.95%) and Anthem (+9.12%). The Boeing numbers were notable insofar as the company reported $100bn of annual sales for the first time in its 102-year history, while also forecasting further revenue growth for this year. Management also eased some of the recent concerns over China’s outlook, saying “we continue to see strong demand in China.”

Closer to home, Italy is starting to creep up on people’s radars again. Yesterday there was some focus on a Bloomberg story suggesting that Deputy PM Salvini is facing internal pressure to force early elections due to frustration over the League’s coalition partner 5SM. Cabinet Undersecretary Giorgetti is one who has publically voiced frustration. This story is also having legs given the rising support for the League based on a weekly average of opinion polls (Bloomberg) which puts their support at 32% (from 20% in April 2018) versus 25% for the 5SM (from 35%). The same article does however go on to say that Salvini is not looking at early elections and is supposedly talking down such expectations within the party. That said we’ve become more than accustomed to elections in Italy with 65 governments since 1946, equivalent to a new government every 1.1 years and 91 in the last 117 years.

Markets are also well versed on recessions in Italy with 5 since the adoption of the euro (equivalent to an average real GDP growth rate of +0.12% qoq). This morning we get a first look at Q4’18 GDP with the consensus expecting a -0.1% qoq reading. As a reminder this follows -0.1% qoq in Q3 and so assuming the consensus is correct, a negative reading will push Italy into another technical recession. For all the above BTPs outperformed yesterday with 10y yields -3.4bps lower compared to -1.1bps for Bunds and -1.5bps for OATs. At 2.596%, yields are now rivalling July levels from last year. It’s worth adding that the FTSE MIB (+0.36%) also outperformed the DAX (-0.33%) yesterday and performed in line with the STOXX 600 (+0.36%).

As for Brexit it was another day of swings and roundabouts for Sterling which traded as high as $1.315 and as low as $1.306. The newsflow mainly centered around the EU side yesterday with Juncker saying that a “disorderly Brexit is now more likely” and that the “withdrawal accord won’t be renegotiated”. That’s not a great surprise as it’s a reiteration of what Juncker has said previously. Ireland PM Varadkar also said that the “EU is not offering a renegotiation of a deal” and there are “no plans to organize an emergency summit”. Ireland’s Foreign Minister Coveney also said that he’s skeptical that there are workable alternatives to the backstop, a view reinforced by Angela Merkel’s spokesman who said “the opening of the exit deal is not on the table”. Comments then that hardly fuel much confidence that the stalemate will be broken. Over to Mrs May. My personal view is that there is scope for a deal but that the EU and Irish might conclude that Parliament is so anti no-deal and slowly gaining more control that if they hold off long enough the chamber will find a way of forcing the government to commit to this. This weakens the UK’s negotiating position in my opinion. As bad as no-deal might be, if you’re negotiating you need the genuine threat of it to strengthen your hand.

Back to the continent, where yesterday in Germany, the Economy Ministry officially slashed its forecast for 2019 growth to 1.0% compared to the 1.8% forecast made in October. That would be the weakest since 2013. It’s worth noting that Bunds are back to within just 3.5bps off the early January closing lows, which at the time were the lowest since 2016.

As far as yesterday’s data was concerned, in the US the ADP employment change report for January surprised to the upside at 213k (vs. 181k expected) ahead of payrolls tomorrow while pending home sales for December printed at -2.2% mom (vs. +0.5% expected). In Germany consumer confidence for Germany ticked up 0.3pts to 10.8 while for the Euro Area, economic, business and services confidence indicators all weakened marginally. Here in the UK net consumer credit was slightly weaker than consensus in December (0.7bn vs. 0.8bn expected) while mortgage approvals fell slightly to 63.8k (vs. 63.1k expected).