GOLD: $1317.60 DOWN $3.00 (COMEX TO COMEX CLOSING)

Silver: $15.92 DOWN 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1317.60

silver: $15.92

Late this afternoon begins the long Chinese New Year celebrations. So it was easy for our crooks to start whacking as they knew the physical Chinese zone will not come back until Monday Feb 11.

I am very encouraged to see that throughout options expiry on both comex and London/OTC, the crooks were afraid to supply paper gold/silver. They can only offer paper when they know chances of delivery are smaller.

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 5296 NOTICE(S) FOR 529600 OZ (16.472 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6235 NOTICES FOR 623500 OZ (19.393 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

53 NOTICE(S) FILED TODAY FOR 265,000 OZ/

total number of notices filed so far this month: 339 for 1,695,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

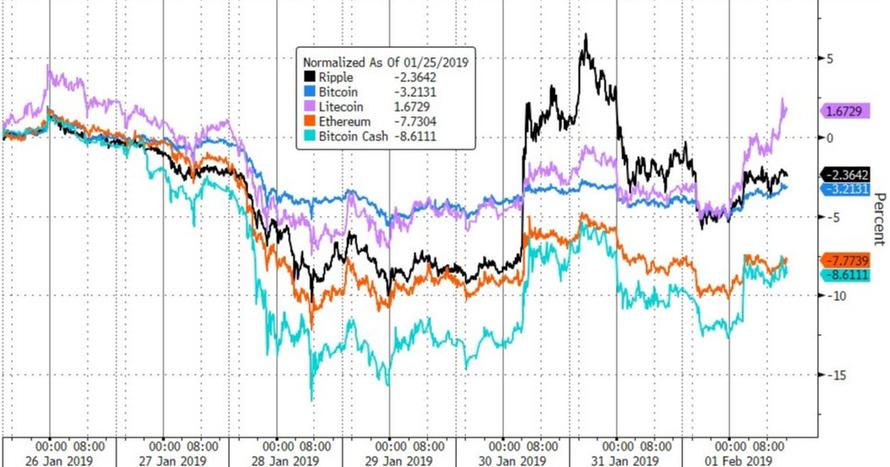

Bitcoin: OPENING MORNING TRADE $3466: UP 31

Bitcoin: FINAL EVENING TRADE: $3477 UP $43

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 3020/5296

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,319.700000000 USD

INTENT DATE: 01/31/2019 DELIVERY DATE: 02/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 2

072 H GOLDMAN 4005

132 C SG AMERICAS 18

323 C HSBC 317

323 H HSBC 830

357 C WEDBUSH 6

624 C MERRILL 97

657 H MORGAN STANLEY 494

661 C JP MORGAN 2 1489

661 H JP MORGAN 1529

685 C RJ OBRIEN 10

686 C INTL FCSTONE 15

690 C ABN AMRO 155

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 18 107

800 C RCG 7 32

880 H CITIGROUP 1449

905 C ADM 2 7

____________________________________________________________________________________________

TOTAL: 5,296 5,296

MONTH TO DATE: 6,235

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUGE SIZED 4074 CONTRACTS FROM 199,314 UP TO 203,388 ACCOMPANYING YESTERDAY’S 15 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2206 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2206 CONTRACTS. WITH THE TRANSFER OF 2206 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2206 EFP CONTRACTS TRANSLATES INTO 11.03 MILLION OZ ACCOMPANYING:

1.THE 15 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.350 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 43,491 CONTRACTS (FOR 1 TRADING DAYS TOTAL 2206 CONTRACTS) OR 11.03 MILLION OZ: (AVERAGE PER DAY: 2206 CONTRACTS OR 11.03 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 11.03 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 228.485 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4074 WITH THE 15 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 2206 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 6280 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2206 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4074 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 15 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.06 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.018 BILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 53 NOTICE(S) FOR 265,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.350 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 5783 CONTRACTS UP TO 477,244 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $9.80//YESTERDAY’S TRADING). WE HAVE NOW ENDED THE FORCED LIQUIDATION OF SPREADERS AS WE PASS FIRST DAY NOTICE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6708 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 0 CONTACTS APRIL 6708 CONTRACTS, DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 477,244. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,491 CONTRACTS: 5783 OI CONTRACTS INCREASED AT THE COMEX AND 6708 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 12,491 CONTRACTS OR 1,249,100 OZ = 38.85 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $9.80.

YESTERDAY, WE HAD 11,261 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 6708 CONTRACTS OR 670,800 OZ OR 20.86 TONNES (1 TRADING DAYS AND THUS AVERAGING: 6708 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 20.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.86/2550 x 100% TONNES = 0.818% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,552.21 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 5783 (LIQUIDATION OF THE SPREADERS HAS CEASED) DESPITE THE GAIN IN PRICING ($9.80) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6708 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6708 EFP CONTRACTS ISSUED, WE HAD A HUGE GAIN OF 12,491 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6708 CONTRACTS MOVE TO LONDON AND 5783 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 38.85 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $9.80 IN YESTERDAY’S TRADING AT THE COMEX

we had: 5296 notice(s) filed upon for 529,600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.00 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 823.87 TONNES

Inventory rests tonight: 823.87 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS IN PRICE TODAY:

/INVENTORY RESTS AT 310.723 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 4074 CONTRACTS from 199,314 UP TO 203,388 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2206 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2206 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4074 CONTRACTS TO THE 2206 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 6280 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 31.40 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.350 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 15 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 2206 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 33.66 PTS OR 1.30% //Hang Sang CLOSED DOWN 11.73 POINTS OR 0.04% /The Nikkei closed UP 14.90 PTS OR 0.07%/ Australia’s all ordinaires CLOSED DOWN .03%

/Chinese yuan (ONSHORE) closed UP at 6.7354 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.73 dollars per barrel for WTI and 60.81 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED DOWN AT 6.7354AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7469: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA

( zerohedge)

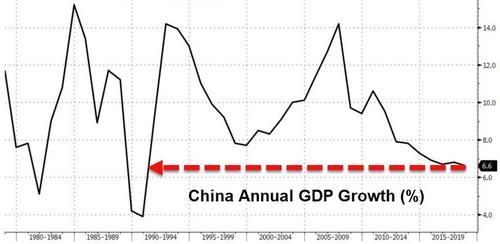

ii)How is this for alarm bells: A huge 440 Chinese companies issued profit warnings in just one day. Interestingly enough almost all of them(86%) were profitable last year.

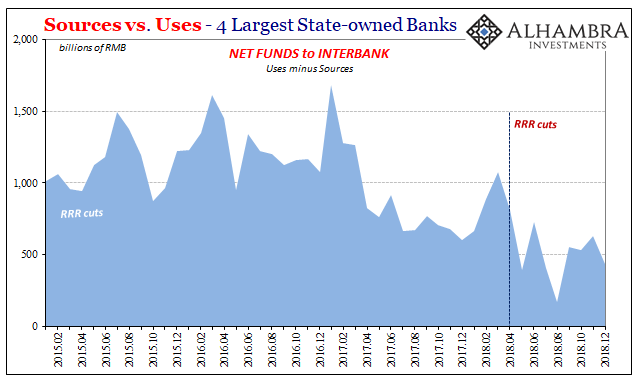

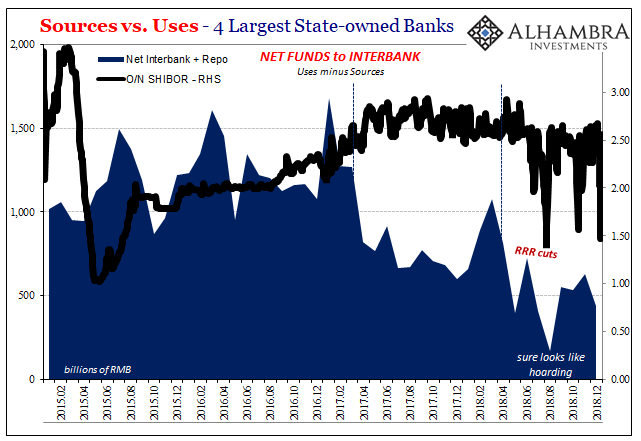

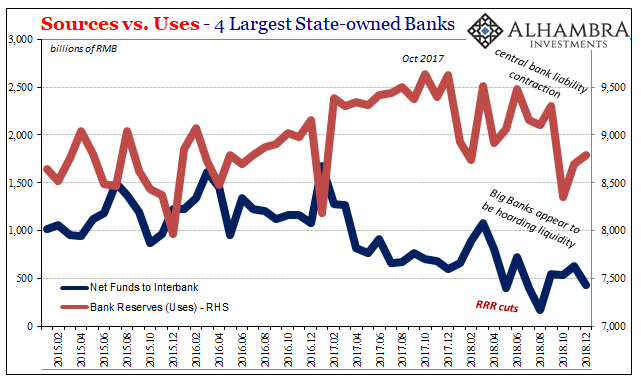

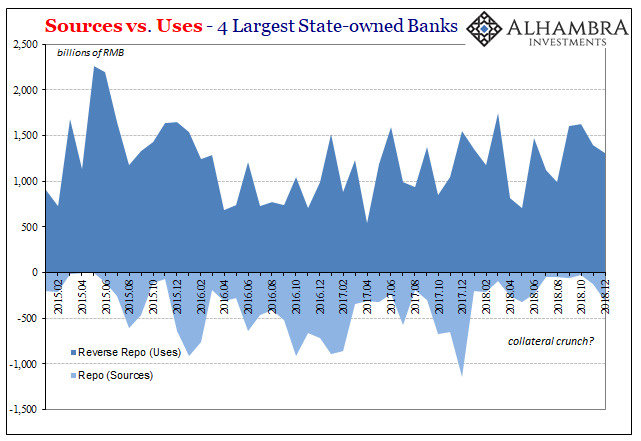

iii)A little difficult to understand. However, the heart of this important commentary is that Chinese RRR cuts which are meant by the POBC to stimulate the Chinese economy is doing the opposite: the banks are hoarding because the Chinese economy is faltering and with it many dark holes.

4/EUROPEAN AFFAIRS

i)UK/EU

A good one..how the Brexit nonsense and the 11 weeks of protests in France are/will have a devastating effect on the EU economies

( Tom Luongo)

ii)They are back: The EU needs for money so it is accusing 8 banks of rigging European government bond markets.

Only European government bonds?

( zerohedge)

iii)Italy/EU

What total absurdity: Salivini has been charged with kidnapping migrants as they try and enter Italian shores. Salvini is continually gaining strength against its coalition partner. The EU are running scared.

(courtesy Tom Luongo)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/USA

Twitter bans over 2,000 pro Maduro accounts in Venezuela as demands for regime change escalate

( zerohedge)

9. PHYSICAL MARKETS

II)Former bus driver and leader of the bankrupt nation of Venezuela sells 15 tonnes of gold to the UAE for paper Euros. Maduro is such a nut case.

( Reuters)

III)Quite a story: the 20 tonnes of gold that was suppose to be on a Russian plane did not board that aircraft. Actually the 20 tonnes of gold is still on the ground as the world tells all authorities not to buy this gold as Maduro will steal the money. I guess he cannot bury the gold in Venezuela as he probably will not be alive to enjoy it.

( Bloomberg/GATA)

IV)Ronan Manly makes the case that all of those nations that supposedly story their gold at the Bank of England, he wishes them the best of luck..they might never see the stuff again

( Ronan Manly/Bullionstar)

V)This continues on from last week where Macleod states that trade wars and increases in tariffs will only add to the trade/current account deficit

( Alasdair Macleod)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

JOBS REPORT

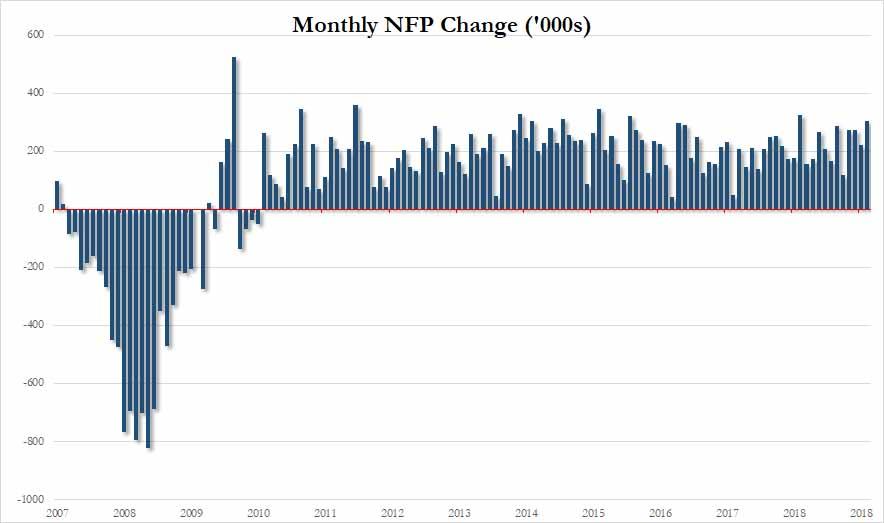

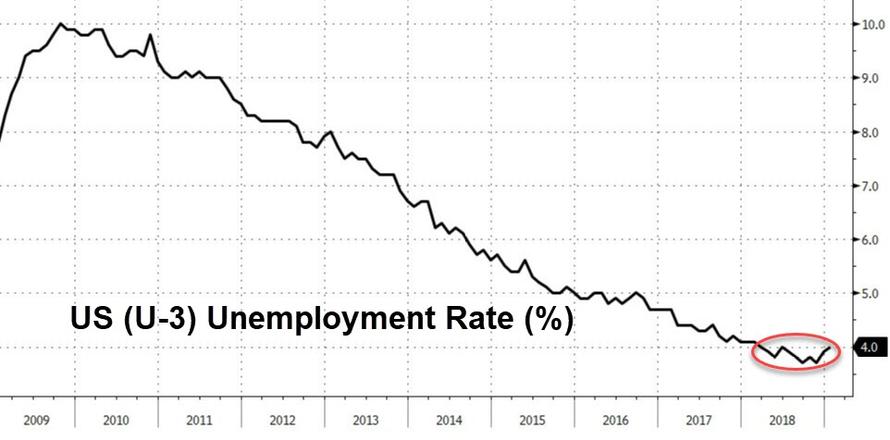

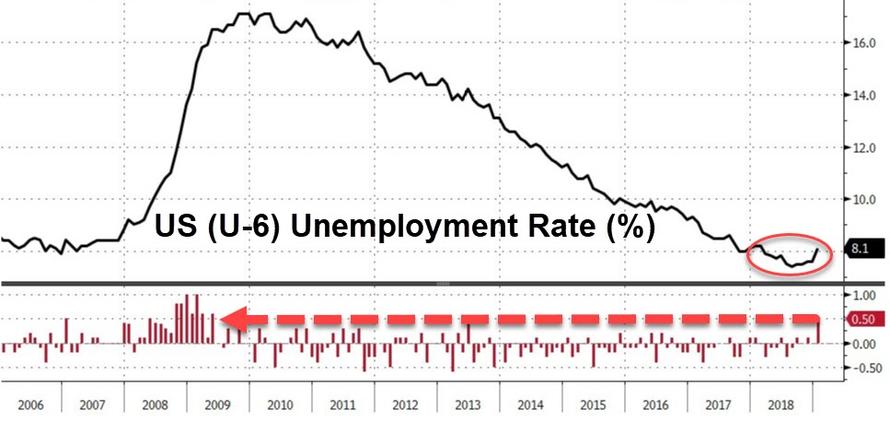

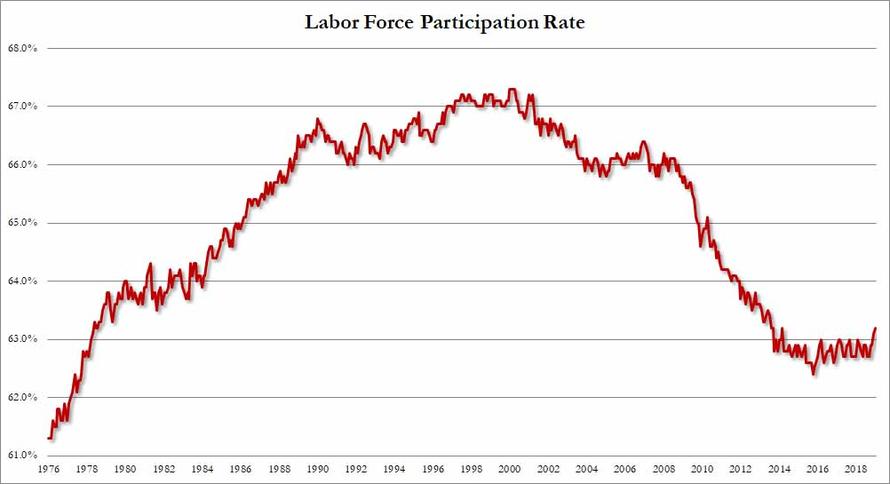

a)The bogus January payroll report: the USA supposedly added 304,000 jobs last month ans now they will bring out Trump and Kudlow to crow

( zerohedge)

( zerohedge)

ii)Market data/

( zerohedge)

b)trust me on this: there will be no trade deal with China because China will not deal with the forced transfer of technology and other important demands of the USA

important..

(courtesy zerohedge)

iv)SWAMP STORIES

New evidence destroys Adam Schiff’s theory that Donald Jr spoke to his father

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI ROSE BY 1749 CONTRACTS UP TO 141,956 CONTRACTS. AFTER MARCH, APRIL RECEIVED ITS INITIAL 15 OPEN INTEREST CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 1836 CONTRACTS UP TO 29,790 CONTRACTS.

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

i) Into Brinks dealer: 564.937.98 oz

Central Banks Buy More Gold In 2018 Than Any Year Since 1967

– Surge in gold purchases by central banks and strong demand for gold coins and bars in Europe and Iran helped push global demand for gold up 4 percent last year

Source: World Gold Council

The Queen inspects a gold vault at the Bank of England

Source: World Gold Council

Central Banks Are on the Biggest Gold-Buying Spree in a Half Century (Bloomberg)

Central Banks Bought More Gold in 2018 Than Any Year Since 1967: WGC (Reuters)

Gold Demand Trends Full year and Q4 2018 (Full Report from World Gold Council here)

News and Commentary

Gold hits 9-month peak on Fed rate freeze; eyes monthly gain (Reuters.com)

Exclusive: Venezuela prepares to fly tonnes of central bank gold to UAE – source (Reuters.com)

Fed pause sets stocks for best January on record, yields fall (Reuters.com)

Gold prices settle higher, up a 4th month in a row (MarketWatch.com)

Source: Bloomberg

Gold Demand Trends Full year and Q4 2018 (WGC) (Gold.org)

Central Banks Are on the Biggest Gold-Buying Spree in a Half Century (Bloomberg.com)

How India Elections Could Mean a Surge in Gold Buying (Bloomberg.com)

Silver Shortage Promises to Boost Price in 2019 (Bloomberg.com)

Italy Officially Slides Into Recession After Budget Battle With Brussels (ZeroHedge.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

31 Jan: USD 1,322.50, GBP 1006.95 & EUR 1,152.16 per ounce

30 Jan: USD 1,312.95, GBP 1002.04 & EUR 1,148.44 per ounce

29 Jan: USD 1,308.35, GBP 994.48 & EUR 1,143.24 per ounce

28 Jan: USD 1,301.00, GBP 987.98 & EUR 1,139.81 per ounce

25 Jan: USD 1,282.95, GBP 981.33 & EUR 1,132.08 per ounce

24 Jan: USD 1,279.75, GBP 981.70 & EUR 1,128.36 per ounce

23 Jan: USD 1,284.90, GBP 990.14 & EUR 1,131.74 per ounce

Silver Prices (LBMA)

31 Jan: USD 16.07, GBP 12.24 & EUR 13.99 per ounce

30 Jan: USD 15.91, GBP 12.15 & EUR 13.92 per ounce

29 Jan: USD 15.85, GBP 12.05 & EUR 13.87 per ounce

28 Jan: USD 15.68, GBP 11.93 & EUR 13.75 per ounce

25 Jan: USD 15.37, GBP 11.74 & EUR 13.55 per ounce

24 Jan: USD 15.30, GBP 11.75 & EUR 13.48 per ounce

23 Jan: USD 15.38, GBP 11.80 & EUR 13.54 per ounce

Recent Market Updates

– Gold Breaks Out of Range After Dovish Fed – Further 1% Gain to $1,321/oz

– U.S.-China War May Be “Just A Shot Away”

– Buy Bitcoin or Gold? Bitcoin Buyers Investing In Gold In 2019

– Gold Consolidates Above $1,300 After 1.2% Gain Last Week

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

But Pierre Lassonde and Doug Casey say central banks don’t care about gold

Submitted by cpowell on Thu, 2019-01-31 15:10. Section: Daily Dispatches

Central Banks Are on the Biggest Gold-Buying Spree in a Half Century

By Rupert Rowling and Susanne Barton

Bloomberg News

Thursday, January 31, 2019

Central banks bought more bullion last year than anytime since 1971, when the U.S. ended the gold standard.

Governments added 651.5 tons of gold to their coffers in 2018, a 74 percent increase from the previous year, according to a report from the World Gold Council.

Russia, which is “de-dollarizing” its reserves, was the biggest buyer, followed by Turkey and Kazakhstan. Hungary also made a large purchase, citing gold’s lack of counterparty risk and role as a hedge against changes in the international finance system, the WGC said.”Central banks chose to significantly increase their gold reserves, reinforcing the importance of gold as a reserve asset,” the WGC said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-31/gold-demand-up-amid-b…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Former bus driver and leader of the bankrupt nation of Venezuela sells 15 tonnes of gold to the UAE for paper Euros. Maduro is such a nut case.

(courtesy Reuters)

Venezuela to sell 15 tonnes of gold to UAE for euros, source tells Reuters

Submitted by cpowell on Thu, 2019-01-31 21:27. Section: Daily Dispatches

By Corina Pons and Mayela Armas

Reuters

Thursday, January 31, 2019

CARACAS, Venezuela — Venezuela will sell 15 tonnes of gold from central bank vaults to the United Arab Emirates in coming days in return for euros in cash, a senior official with knowledge of the plan said, in an effort by the troubled OPEC member to stay solvent.

The sale this year of gold reserves that back the bolivar currency began with a shipment on Jan. 26 of 3 tonnes, the official said, and follows the export last year of $900 million of mostly unrefined gold to Turkey.

…

In total, the plan is to sell 29 tonnes of gold held in Caracas by February, the source said, requesting anonymity in order to speak freely. Venezuela had reserves of 132 tonnes between the central bank’s vaults and the Bank of England at the end of November, according to central bank data.… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-politics-gold-exclusive/exc…

* * *

END

Quite a story: the 20 tonnes of gold that was suppose to be on a Russian plane did not board that aircraft. Actually the 20 tonnes of gold is still on the ground as the world tells all authorities not to buy this gold as Maduro will steal the money. I guess he cannot bury the gold in Venezuela as he probably will not be alive to enjoy it.

(courtesy Bloomberg/GATA)

Venezuela’s 20-ton pile of gold in suspense in Caracas vault

Submitted by cpowell on Fri, 2019-02-01 04:28. Section: Daily Dispatches

By Patricia Laya

Bloomberg News

Thursday, January 31, 2019

With 20 tons of gold stacked up for loading and shipping out of Venezuelan vaults, the mystery surrounding them — and the saber-rattling they’re sparking — is intensifying.

The Russian airplane that a Venezuelan lawmaker alleged was in Caracas to spirit the gold away left the country without it. But now a cargo plane has landed from Dubai, triggering a new wave of speculation that the gold is headed there instead.

As Nicolas Maduro, the authoritarian ruler, tries to stave off mounting international pressure to relinquish power, the fate of those gold bars has become a cause of great concern both in Venezuela and abroad. Valued at about $850 million, they are an important source of wealth in a country that has plunged into extreme poverty under Maduro’s leadership.

On Thursday, Marco Rubio, the Florida senator who has helped spearhead the U.S.’s hard-line stance toward the Maduro regime, fired off a tweet calling out the United Arab Emirates’ Noor Capital as the financial firm orchestrating the gold transaction with Venezuelan authorities. Rubio went on to warn the firm that both it and any airline it hires to take the gold away will be subject to U.S. Treasury sanctions.

As of late today the 20 tons had yet to leave the central bank, according to a person with direct knowledge of the matter. They had, though, been weighed and separated for shipment, the person said. He did not know where the gold might be heading or the nature of the transaction. The cargo plane was still at the airport in Caracas, according to the website Flightradar24.

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-02-01/maduro-s-20-ton-pile-…

END

Ronan Manly makes the case that all of those nations that supposedly story their gold at the Bank of England, he wishes them the best of luck..they might never see the stuff again

(courtesy Ronan Manly/Bullionstar)

Store Your Gold At The Bank Of England And You Might Never See It Again

Submitted by Ronan Manly, BullionStar.com

In early November 2018, it first came to light that the Bank of England in London was delaying and blocking the withdrawal of 14 tonnes of gold owned by the Venezuelan central bank, Banco Central de Venezuela (BCV). At the time, Reuters and The Times of London both reported that according to unnamed British ‘public officials’, the delays were being caused by the difficulty and cost of obtaining insurance for the gold shipment back to Venezuela, and also due to “standard measures to prevent money-laundering“.

As I explained in a BullionStar article on 15 November titled ‘Bank of England refuses to return 14 tonnes of gold to Venezuela’, the explanations given to Reuters and the Times for the withdrawal delays were completely bogus, and that the real reason for blocking the BCV gold withdrawal was undoubtedly US and UK joint government interventions to stall the withdrawal. As I wrote at the time:

“The reasons put forward by official sources in the Reuters and Times articles for why Venezuela can’t withdraw its gold from the Bank of England are clearly bogus. The more logical and likely explanation is that the US, through the White House, US Treasury and State Department have been liaising with the British Foreign office and HM Treasury to put pressure on the Bank of England to delay and push back on Venezuela’s gold withdrawal request.”

As it turns out, this was an entirely correct prediction, since by 25 January, Bloomberg confirmed in an ‘exclusive report’ (two and a half months later) that:

“The Bank of England’s decision to deny Maduro officials’ withdrawal request comes after top U.S. officials, including Secretary of StateMichael Pompeo and National Security Adviser John Bolton, lobbied their U.K. counterparts to help cut off the regime from its overseas assets, according to one of the people, who asked not to be identified.”

Why Bloomberg took so long to state the obvious is not clear, but from the outset, the entire interventionalist playbook of the Americans and British in this saga has been entirely predictable to anyone observing the situation. This intervention by the Bank of England on behalf of the US and UK shows a complete disregard for sovereign gold property rights, and the Bank of England has now literally ripped up a custody gold storage agreement that it had entered into with another of the world’s central banks.

Predicting the Coup – Look to the Gold

More interestingly, the Bank of England’s stalling tactics on the BCV gold withdrawal has also been useful in predicting the timing of the current Western powers’ move against Maduro and in signaling how long this foreign backed coup has been in the planning in Washington DC and elsewhere. Let’s look at a few facts and their timing.

From at least early September 2018, the Bank of England (BoE) began stalling on allowing a central bank gold custody customer (the BCV) to withdraw sovereign property (gold bars) that the BCV had entrusted to the Bank of England under a gold custody agreement.

Why early September 2018? Because, as the Reuters report dated 5 November stated, the BCV gold withdrawal request had “been held up for nearly two months”. This would put the original BCV withdrawal request to at least early September. And since the BCV’s gold withdrawal request was not actioned by the BoE at that time in early September, then this implies that the Bank of England already had its instructions to begin stalling the BCV during at least early September, which also implies that the British and US governments were already involved.

Arguably, concern in Bank of England, British Foreign Office and US State Department circles, and associated hatching of plans to stall and block BCV gold bar withdrawals, could have began as early as April 2018. This was the month in which the BCV paid Citibank $172 million to recover gold bars at the Bank of England that the BCV had put up as collateral in a gold swap operation with Citibank. According to a Reuters article last June about the termination of this BCV-Citi gold swap, “the policy [of the BCV] is to recover the gold“.

So when the swap was closed out last April, the Bank of England and associated intelligence actors (UK Treasury, Foreign Office, State Department, US Treasury etc) would all have known that the BCV again had title to some gold bars in the Bank of England’s vaults and wanted to “recover the gold”. So its also possible that the BCV gold withdrawal request to the Bank of England was pending from at least May onwards.

Stalling while awaiting backup

It is now also apparent that the Bank of England was engaged in its stalling tactics while waiting for new US sanctions to come into affect as well as for the beginning of Maduro’s new presidential term on 10 January 2019, when the US and associated allies then upped the coup rhetoric.

Specific sanctions appeared on 01 November, when the United States signed Executive Order 13850, an order which imposed sanctions on Venezuela’s gold industry and which bullies the global gold industry not to do business with Venezuela and its gold sector. To put the issue into the public domain and control the narrative in the run up to Washington’s intervention, Reuters and the Times were then feed various bogus stories a few days later by “public officials” and “British officials”, and the resulting stories published firstly by Reuters (story one) and then by the Times (story two).

On the election front, while Venezuela’s president Maduro was re-elected in elections that were held on 20 May 2018, his inauguration was only held on 10 January this year. As other countries jumped on the bandwagon condemning Maduro’s new term and endorsing the relatively unknown Venezuelan national assembly leader Juan Guaidó, if the Bank of England was able to stall until 10 January, then it’s stalling tactics would appear more palatable since by then reneging a sovereign gold custody contract could be buried amid the media scramble and merely be another footnote in the escalating conflict.

This, the Bank of England has managed to do to an extent. In early December, the BoE stalled in its meeting with BCV president Calixto Ortega Sánchez and Venezuelan finance minister Simón Zerpa Delgado when they flew over from Caracas to London for a meeting requesting BCV gold withdrawal. See BullionStar article from 18 December, titled “Venezuela’s gold in limbo amid tug-of-war at the Bank of England” for more details.

The BoE’s stalling also enabled the US-backed Venezuelan opposition to throw its own spanner in the works during December, when Venezuelan opposition politicians Julio Borges (former Venezuelan national assembly president and founder of the Justice First party) and Carlos Vecchio (co-founder of the Voluntad Popular party) petitioned the BoE’s governor Mark Carney to “refuse the handover of fourteen tonnes of gold“.

John Bolton: From the Swamp?

Doubling down on the Gold, doubling up the Stake

In the immediate aftermath of Maduro’s re-inauguration, a number of intriguing developments regarding the BCV’s gold at the Bank of England have also now come to light. These developments merit attention, and are briefly summarised below.

Firstly, the BCV significantly upped the ante in December 2018 by doubling down on its gold holdings at the Bank of England. It did this by closing out another gold swap, this time one that its had on the table with the now troubled Deutsche Bank. This is according to a Reuters reportout of Caracas dated 21 January. According to Reuters, the BCV’s gold holdings at the Bank of England:

“more than doubled in December to 31 tonnes, or around $1.3 billion, after Venezuela returned funds it had borrowed from Deutsche Bank through a financing arrangement that uses gold as collateral, known as a swap…

..Under the deal struck with Deutsche Bank in 2015, Venezuela put up 17 tonnes of gold in exchange for a loan.“

By upping the amount of gold at stake from 14 tonnes to 31 tonnes, the BCV piled on the pressure with the BoE. If 14 tonnes sounds like a lot of gold, then 31 tonnes sounds like a lot more.

Back in December, I did a calculation of how many Good Delivery gold bars equates to 14 tonnes and wrote that it “would be in the region of about 1125 gold bars” which was 27% of the original 4,089 gold bars that the BCV left stored at the Bank of England in late 2011. I said that:

“This is the gold now being frozen by the Bank of England, about 1125 gold bars. If this gold is in custody, it will be set-aside or allocated and the BCV will know the individual serial numbers of every bar.

…the BCV should at the very least publish for everybody to see, the weight list / serial number list of all of these gold bars so that they cannot be confiscated or used by the Bank of England or bullion banks for other purposes, such as being sold to other central bank customers or sold to gold-backed ETFs.”

If 1,125 Good Delivery gold bars equate to 14 tonnes, then about 2,491 Good Delivery gold bars equate to 31 tonnes. So the BCV is now looking to withdraw approximately 2,500 wholesale gold bars from the Bank of England vaults in London. That is not a small number, and should cause ‘consternation’ among the LBMA and Bank of England vault managers that the reputation of the London Gold Market has now been tainted by freezing the withdrawal of 2500 large gold bars belonging to another sovereign nation. Not to mention ‘consternation’ among the world’s other central banks (more then 70 central bank gold custody customers) which store their gold in the BoE vaults in London.

Guaido and Maduro

Late January news also saw official confirmation from Bloomberg that the trip to the Bank of England in December by the Venezuelan central bank president Ortega Venezuelan finance minister Zerpa Delgado had been a waste of time. Again confirming the stalling tactics of the G30 member (Mark Carney) led Bank of England. According to a January 25 article by Bloomberg:

“those talks were unsuccessful, and communications between the two sides have broken down since. Central bank officials in Caracas have been ordered to no longer try contacting the Bank of England. These central bankers have been told that Bank of England staffers will not respond to them, citing compliance reasons, said a Venezuelan official…”

On 27 January, Reuters revealed that Venezuela’s political opposition, not content with just a letter from Borges and Vecchio to Mark Carney in December which pleaded to “refuse the handover of fourteen tonnes of gold“, had gone one step further and roped in Venezuela’s presidential contender Juan Guaido to write additional letters both to British prime minister Theresa May and the BoE’s governor Carney, claiming that Venezuela’s Maduro aimed to sell the BCV gold. “I am writing to ask you to stop this illegitimate transaction” said the Guaido letters, according to Reuters. Remarkably, Guaido’s letter to Thersea May was his first letter ever to a foreign head of government, and shows the desperation of the US-UK forces to block access to this 31 tonnes of gold. Who said gold was just a pet rock?

On 28 January, Britain’s Foreign Office also entered the meddling, when Foreign Office minister Alan Duncan, with a straight face, told the British parliament in a parliamentary debate that the fate of the 31 tonnes of gold:

“is a decision for the Bank of England, not for government……It is they who have to make a decision on this.”

Duncan conveniently forget to mention that “top U.S. officials, including Secretary of State Michael Pompeo lobbied his UK counterparts” (i.e. Duncan) to help cut off Venezuela’s overseas assets. Duncan’s comments can be read on Hansard here, and a Bloomberg summary is here. So the British government is fully involved in blocking the BCV gold withdrawal request from the Bank of England but pretends that its an independent decision from the Bank of England – which itself has been stalling on the withdrawal request for months now.

Troops guarding central bank of Hungary’s gold repatriated from London

Conclusion

In all of this saga, perhaps the most amusing aspect is how any central bank now thinks that the Bank of England and London Gold Market are free from political risk and that London is somehow still a secure and safe place for central banks to store gold bars and to trade gold bars.

Back on the 30 January 2012, when the last shipment of gold came back into Caracas on the instruction of former Venezuelan president Hugo Chavez, the then BCV head Nelson Merentes noted that:

“gold stored in BCV [in Caracas] will reach 86% of the total while the rest, about 50 tonnes, will stay in the banks in which the Republic needs to maintain open accounts for international financial operations.”

Merentes was of course referring here to the Bank of England vaults, where the BCV left 4,089 Good Deliver bars in storage when it repatriated another 12,819 Good Delivery bars to Caracas. These 4,089 Good Delivery gold bars at the Bank of England’s vaults totaled approximately 50.8 tonnes. Fast forward exactly 7 years later and it’s laughable that the Venezuelan gold that was left in London for international financial operations has been blocked by the very custodian that was supposed to be minding that gold on behalf of another central bank.

In the same vein, all of the smug central bankers around Europe who countered calls for their nations’ to repatriate gold from London with the argument that it was being safely held in an international trading center, will now have to backtrack on their claims that the Bank of England vaults are free from political and confiscation risk.

To cite just a few, Germany’s Bundesbank has 432 tonnes of gold stored in London which it claims is stored there “to be able to exchange gold for foreign currencies at gold trading centres abroad within a short space of time.”

The Austrian central bank keeps about 84 tonnes of gold at the Bank of England in London and 56 tonnes in Zurich, which it justifies at these locations since “different storage locations helps the Austrian central bank reduce concentration risk, while still being able to use gold in the gold markets of London and Zurich should the need arise.”

The Bundesbank also claims that

“the part of the Bundesbank’s gold reserves which is to remain abroad could, in particular, be activated in an emergency. Therefore one part will remain… in London, the world’s largest trading centre for gold.

In the event of a crisis, the gold could be pledged as collateral or sold at the storage site abroad, without having to be transported. In this way, the Bundesbank could raise liquidity in a foreign reserve currency.”

The Central Bank of Hungary now looks to have been shrewd when it purchased 28.4 tonnes of gold at the Bank of England last October, and immediately repatriated all of this newly bought gold back to Budapest, and in an instant ring-fenced that gold from confiscation and political interference at the now compromised Bank of England. With many governments and nations of myriad political systems and styles holdings gold in the Bank of England vaults, some of these central banks must at least be wondering if its now time to get their gold out of London.

In a short space of time, the Bank of England reputation’s as an impartial and safe location for the storage and trading of gold looks to have been irreversibly damaged.

This article was originally published on the BullionStar.com website under the title “Bank of England tears up its Gold Custody contract with Venezuela’s central bank”.

end

This continues on from last week where Macleod states that trade wars and increases in tariffs will only add to the trade/current account deficit

(courtesy Alasdair Macleod)

Alasdair Macleod: Trade wars — a catalyst for economic crisis

Submitted by cpowell on Fri, 2019-02-01 00:54. Section: Daily Dispatches

7:50p ET Thursday, January 31, 2019

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod argues tonight that trade wars will weaken the U.S. dollar by reducing the flow abroad of dollars that have been recycled into U.S. Treasury instruments.

Macleod writes: “The dollar is likely to face a developing problem. It is already becoming evident that surplus dollars arising from the slowdown in international trade are shifting out of the dollar into other currencies and gold. …

…

The dollar’s bear market appears to be resuming after completing an eight-month counter-trend consolidation. Given record levels of foreign ownership of dollars and dollar investments, further declines in the dollar could easily trigger currency liquidation, making it impossible for the U.S. government to continue to fund budget deficits from foreign investors.”

Macleod’s analysis is headlined “Trade Wars — A Catalyst for Economic Crisis” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/trade-wars-a-catal…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

a proven accounting identity to show that the end result of President Trump’s trade tariffs would be to increase the trade deficit, assuming there is no change in the savings rate. The savings rate is important, because if it does not change, then the budget deficit must be financed by any combination of three variables: monetary inflation, the expansion of bank credit, or capital inflows. This is captured in that equation, where the trade balance is the balance of payments, thereby including capital flows as well as goods and services:

(Imports – Exports) = (Investment – Savings) + (Government Spending – Taxes)

It assumes the economy is working normally, and as we shall see, there is no major economic contraction or systemic crisis.

This article explores the implications of the relationship between the twin deficits in the context of the current situation for the United States, which may or may not be on the edge of a significant economic retrenchment. It looks at the detail of how trade tariffs act on the economy at the current stage of its credit cycle and the implications for the economic outlook and for monetary policy. It examines the problem through the lens of sound economic theory, but empirical evidence is invoked as well for confirmation.

The empirical evidence

Looking at history, we find that the effect of tariff increases has depended on the stage of the credit cycle. The best clearest examples are the tariffs introduced after the First World War (the Fordney-McCumber tariffs of 1922) early in the credit cycle, and the Smoot-Hawley Tariff Act of 1930 at the end of it. On the face of it, Fordney-McCumber had little effect, while Smoot-Hawley, it is generally agreed, had a significant effect. Of course, this is in the context of a US-centric viewpoint.

The Fordney-McCumber tariffs were introduced early in the US’s credit cycle. At that time, the US economy still had the legacy of wartime production, whereby imported goods and agricultural products were minimal, having been virtually eliminated by wartime economic planning. The impact of tariffs on the US’s domestic economy was therefore barely relevant to the economic situation. Consequently, unlike the European economies which had been ravaged by war, US agricultural and industrial production were both higher in 1920 than they had been in 1913, the year before the outbreak of war. The effect on Europe was another matter.

European economies found themselves needing dollars to pay reparations (in Germany’s case) and to repay war debt in the case of the Allies. US Tariffs made it extremely difficult for the Europeans to earn those dollars. A number of European economies collapsed into hyperinflation as governments continued the wartime practice of money-printing to finance themselves and service wartime obligations.

Another factor affecting America was the collapse of agricultural prices from inflated wartime levels. By 1921, wheat had collapsed from $2.58 a bushel to 92 cents and hogs from 19 cents per pound to under 7 cents. Tariffs did not help farmers, because at that time, they depended on export markets to a significant degree. And when other countries introduced or increased their tariffs against agricultural products as a response to US tariffs, they proved to be wholly counterproductive for US farmers.

Of course, tariffs were not the sole problem for America’s farmers. Rapid mechanisation increased Canada’s wheat yields, the Argentine was increasing beef production and Cuba exporting large quantities of sugar. Consumers were benefiting from catastrophically lower prices despite tariffs. Other than the pain faced by producers, pain which in free markets is only alleviated by redeploying economic resources away from overcapacity in agriculture, the overall economic effect of the Fordney-McCumber tariffs on America was not significant.

Smoot-Hawley was different. Congress voted in favour of it on 31 October 1929, and the stockmarket clearly saw it coming. The Wall Street Crash commenced on Black Thursday, 24 October, when the market fell 11% that day, before recovering most of the fall. Black Monday followed, when the market fell 13%. By the close on Tuesday 29 October the market had lost over 34% in just fifteen calendar days.

At today’s stock prices, that would be a loss of over 8,000 Dow points. The stockmarket continued its fall to a low on 13 November of 198.7 on the Dow, and after rallying for six months entered a pernicious and continual bear market to a final low of 41.22 on 8 July 1932.

It is always a mistake to attribute a market failure to a single cause: the only certainty was the market fell. However, the importance of the Smoot-Hawley vote to the stockmarket is often missed by economic historians.

The difference between late-1929 and today perhaps, is that Congress voting for it then was a definite event, whereas Trump’s tariffs are progressing as a fluid mixture of bluff and fact. Another key difference was the dollar’s gold exchange standard of $20.67 to the ounce. So long as the exchange rate was defended, a slump would certainly lead more dramatically to widespread bankruptcies. Markets therefore had to discount the enhanced risks from trade protectionism to the economy more immediately compared with today’s fiat currency economy, when it is assumed future investment risk will be ameliorated by monetary expansion.

Pursuing this line of thought is unlikely to lead us to a definite conclusion. A more fruitful approach is to look at the effect of tariffs and trade protectionism in the context of the credit cycle. We have established from our examination of the 1921 Fordney-McCumber tariffs that early in the credit cycle trade protectionism had a limited impact on financial markets and the economy. It stands to reason that an economy floating on a tide of money and credit is in a different position, and more vulnerable to disruption from upsetting events such as the introduction of tariffs.

Adverse changes in trade policy at any time are an upset to market assumptions, and it is clear from both Smoot-Hawley and common sense that Trump’s trade interventions today are a serious spanner in the works of highly valued markets. That is tantamount at the minimum to a claim that Trump has upset the speculators. This is evidently the case, but to understand why Trump’s trade protectionism should be taken more seriously, we need to examine in greater detail the flows implied in the equation at the beginning of this article linking the two deficits.

Why external trade has become central to the whole US economy

Since the oil shocks of the early 1970s, the US has relied on foreign holders of dollars to accumulate US Treasuries issued to finance budget deficits. That recycling of dollars earned by foreigners selling more things to America than America buys from foreigners has through trade imbalances allowed the US Government to run mounting budget deficits.

The Americans have become used to foreigners having no credible alternative to reinvesting their accumulating dollars. However, we can now see that the dollar hegemony behind this proposition is being eroded by China and Russia, acting as the powers which are increasingly directing Asian trade flows. Clearly, as their determination to do away with dollars bears fruit, instead of currently held dollars remaining invested they will be surplus to trade requirements and sold. So far, they have been bought by other foreigners, which is why we see China’s holdings of US Treasuries decline, while those of other foreigners increase, and why Russia’s disposal of cash dollars earned through energy sales has little apparent effect on the exchanges. Meanwhile, the US Government has managed to fund itself without a critical increase in borrowing costs.

This cannot continue ad infinitum, because relative to the volumes of trade concerned and the size of the US economy, there are already large quantities of dollar balances and dollar investments accumulated in foreign hands, which on the last available figures at over $22tn exceed US GDP of around $20tn.

The failure of American trade policy is to not recognise the consequences of upsetting what has become a very delicate balance in capital flows. By imposing aggressively protectionist policies, the Trump presidency has set back cross-border trade significantly, reducing the future availability of dollars from non-domestic sources to fund the budget deficit. Furthermore, US efforts to restrict inward commercial investment by China muddy these waters further.

On these grounds alone, we can see that attempts to restrict Chinese imports are cutting off a vital source of future finance for the US Government. Yet, the accounting identity that explains the twin deficit phenomenon tells us in the absence of an increase in the savings rate the trade deficit will continue. Furthermore, due to tax cuts the budget deficit is still increasing at this late stage of the credit cycle, and an emerging slowdown in the rate of GDP growth tells us it will increase even more rapidly than currently forecast.

Therefore, American protectionist policies risk destabilising the market for US Treasuries, which have increasingly relied on foreign buyers recycling their surplus dollars. The question then arises as to what happens if a contraction in international trade develops out of the current slowdown.

The ending of the dollar’s hegemony

The dollar is likely to face a developing problem. It is already becoming evident that surplus dollars arising from the slowdown in international trade are shifting out of the dollar into other currencies and gold. The following chart of the dollar’s trade weighted index illustrates the position.

The dollar’s bear market appears to be resuming after completing an eight-month counter-trend consolidation. Given record levels of foreign ownership of dollars and dollar investments, further declines in the dollar could easily trigger currency liquidation, making it impossible for the US Government to continue to fund budget deficits from foreign investors.It appears this is a periodic problem, first encountered when the dollar devalued in 1934, and then in the 1960s when the gold pool failed. This time, with the dollar being unbacked by gold, there is little to stop the dollar’s exchange rate falling as cross-border capital is repatriated to their currencies of origin or into gold.A secondary effect of today’s trade policies has been to interrupt the Fed’s monetary normalisation, leading to what the Fed hopes is just a temporary pause in the process. This assumes the banks are not going to become more risk-averse and is where a contraction in international trade could disrupt the expansion of bank credit, upon which financial markets in particular have become so reliant. How this might occur is an important question that should be addressed.

How contacting trade contracts bank credit

To understand the mechanisms of how changes in the trade balance can affect the level of bank credit, we must first explain why in the absence of a change in savings, a budget imbalance leads to a similar trade imbalance.

Let us assume a government is running a budget deficit. The deficit represents excess spending over tax and other incidental income and requires to be financed. If the government issues bonds, the extent to which they are subscribed to by members of the public, their pension funds and insurance policies, is not inflationary financing, merely diverting capital resources from other investments. If the government issues bonds that are subscribed to by banks, then they are financed through the expansion of bank credit, and unless that credit is withdrawn from other bank customers, it is inflationary. Lastly, the deficit may be financed by the central bank, directly or indirectly buying government bonds and bills. This is also inflationary.

As the government spends the proceeds of these bond issues, to the extent they are not financed by private sector savings they put extra currency into circulation. This extra currency ends up mostly in the hands of consumers through welfare payments, as well as earnings and payments by the government for goods and services. But given there is a degree of inelasticity between the supply of extra goods and services and the inflation-fuelled demand for them, it takes time for markets to respond to the inflationary demand. Consequently, imported goods and services rise to fill in the gap, the more so because they are unaffected, at least initially, by price pressures arising from the monetary inflation.

In effect, it is the expansion of money and credit that emanates from covering a budget deficit, assuming no change in total savings, that leads to a trade deficit. What happens to the exchange rate depends on whether the currency proceeds arising from imports are reinvested or simply sold on the foreign exchanges. Balance of payments figures are designed to capture the net position between trade and capital flows, and it is these figures that are used in the deficit relationship.

All this assumes a reasonable degree of economic stability. That is to say, trade continues without severe disruption. It is not the case at the end of a long credit cycle, when capital misallocation in the private sector has become so great that sooner or later market forces emerge to trigger a correction. It is at that point obstacles to balance of payment flows are likely to have the greatest impact, setting off and intensifying an unwinding of the accumulated distortions in the domestic economy.

This was the reason the events following the passing of Smoot-Hawley were so different from those following Fordney-McCumber. The approval of key provisions in Smoot-Hawley by Congress in October 1929 crashed Wall Street in the preceding fortnight, and when President Hoover signed it into law the following June, not only did Wall Street continue to fall for a further two years, but retaliatory action from other nations ensured the ensuing global economic disaster worsened and America’s exports in turn suffered badly.

We are at the same point in the credit cycle, which has run for a similar time as that of the 1920s, and we have an analogous rise in American protectionism. Complacency is common to both. Irving Fisher, the renowned American economist, reflected the super-optimism before the crash of 1929 when he stated the stock market had reached a permanently high plateau. Even Keynes and Winston Churchill were taken in and lost money.

They were far from being alone, and the prospect of a substantial fall in stocks today is widely assumed to be unjustified scaremongering. When he was wiser after the event, Fisher went on to define the vicious relationship between falling collateral values and contracting bank credit. Insofar as today’s economists claim it was the cause of the depression’s severity, they are incorrect. The cause was the monetary and speculative excesses that had built up before the crash. If anything, the imbalances and misallocation of capital today should be a far greater concern than they were in 1929.

We know that a feature of the post-Smoot-Hawley events was the unwinding of malinvestments, and the severe contraction of outstanding bank credit that accompanied it. Thousands of banks went under. A repeat of these events today is wholly unexpected, with even the bears thinking the economy can be rescued by just lowering interest rates and reverting to quantitative easing. However, a proper and thorough examination of the risks today reveals that a slowdown triggered by trade protectionism will be almost impossible to prevent escalating into a full-blown slump.

The central question in any analysis of future economic and monetary prospects has to be what will happen to the twin deficits. We know as surely as the sun will rise tomorrow and every day thereafter that as an economy moves from a stockmarket fall towards a slump, budget deficits will rise inexorably, particularly in the welfare states. Yet, with demand collapsing in the private sector, trade deficits cannot increase in lock-step with budget deficits. The only way the national accounts can be balanced in a fiat-money economy is for there to be an offsetting contraction in bank obligations to the private sector. A contraction of bank credit in this event will be impossible to stop, and it matters not how well capitalised a bank is for regulatory purposes. Fractional reserve gearing will ensure that widespread bank insolvencies and bankruptcies ensue.

It seems increasingly likely that spurred on by falling stockmarkets and dollar weakness, a foreign liquidation of an overhang of dollar cash and assets will follow. If so, the dollar will fall and in accordance with Irving Fisher’s analysis, a self-feeding implosion of private sector bank lending will then take place. Whether other currencies fall with the dollar is immaterial: the fall will be measured in its purchasing power and credibility measured in gold.

The difference from the experience of the events that led into the Great Depression is today’s money is not backed by gold. Inflationists believe that the problems of the 1930s could have been solved if the gold standard had been abandoned, or if excess gold reserves had been monetised. They argue that similar conditions today can be avoided by allowing the currency to weaken, and therefore to prevent prices from sliding.

Monetary policy today is and surely will continue to be guided by these inflationist assumptions. Central banks, led by the Fed, the ECB, Bank of Japan and Bank of England will coordinate aggressive money expansion in a vain attempt to prevent a slump developing. And while the quantity of outstanding bank credit contracts, it will be more than made up for by the expansion of central bank money. Today’s central bankers are unquestionably on the same course set by Rudolf Havenstein, president of the Reichsbank during Germany’s hyperinflation of 1920-23.

Havenstein was imbued in a system that financed itself predominantly through money-printing. Today’s central bankers are not much different, believing that inflation of the money quantity must be a continuing, and if necessary accelerating process.

Conclusion

Pre-Keynesian economic theory, refined by the Austrian school, identified the credit cycle as the primary cause of periodic booms and busts. To this we can add a sporadic cycle of trade protectionism, which at the wrong moment can have a devastating effect. While it is impossible to satisfactorily link cause and effect, there is little doubt that it was the combination of Smoot-Hawley tariffs and the end of an inflation-fuelled boom that devasted the world economy in the 1930s.

This article has shown that similar conditions exist today. We must hope that they don’t repeat, but it would be foolish to ignore the possibility.

The obvious difference is currencies are now unbacked, giving governments an initial policy choice. They can let commercial banks go bust, as happened in large numbers in the 1930s and cut government spending to preserve a degree of currency stability. Or they can trash their currencies in an attempt to protect jobs and the state. We can be sure in advance the course that will be taken.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Good Morning Bill/Harvey (from Africa)

Yesterday I wrote a note on the rise of the PetroYuan. The other side of the coin is the health, or otherwise, of the PetroDollar. This morning the European Tour tees off for the second round of its inaugural full tournament in Saudi Arabia. Last year the BBC broke ranks and published an article (with a picture) concerning current crucifixions in that Kingdom. On Tuesday, the BBC golfing editor published an editorial that was extremely critical of named leading UK golfers who were playing in this tournament, thus indicating that they were oblivious to the human rights record of the Saudis. Is it business as usual for the PetroDollar if leading golfers are admonished by a bastion of MSM for just playing golf in that country? Talking of countries behaving badly, I hear that New York and at least one other state are legalizing full term abortion. I was talking to someone from the baby organ harvesting industry, and she said that the product is far superior when harvested one minute after birth, instead of one minute before birth (now quite legal). She said that her industry was working on a business model based on the premise “what is just two minutes between friends’’.

I think it was Putin who said that it was very difficult to deal with Americans who confuse Austria with Australia. Well ‘’down under’’ (that would be a reference to Australia if you are unsure), the tarmac on the roads is melting (apart from other catastrophes).The actuaries (and the politicians) balance out the prevailing +45 degrees Celsius in Australia with the frozen Niagara Falls and declare ,on average everything is normal and awesome. Chris Martenson was spot on in his interview with Greg Hunter, just before the announcement of the Fed capitulation, with his succinct message: ’’this time it is truly over, there is no way back’’. I read a headline that suggested that this new kid on the block, Alexandria Ocasio Cortez is one of the few (only?) politicians that appreciates that humanity is on the cusp of extermination. The headline quoted her statement of “12 years to the midnight hour’’ but actually Dane Wigington says it is just eleven years, but congratulations to her for referencing the consequences of demonic climate engineering. Imagine, sometime in the near future when Alexandria becomes more powerful and is in a position to print even more trillions to fund all her ideas on free stuff. Paul Krugman is already penciled in are her senior financial advisor and just envisage , no matter how many fiat ameros are created, his perpetual criticism that it is not enough, it is simply not enough.

Accumulate and hold onto your physical gold as TEOTWAWKI bears nigh. If you think the market has got things right, please try this test. Hold 6 single ounce gold coins in one hand and hold one of those green containers of 500 American silver Eagles in the other hand and ask yourself whether current pricing equivalence intuitively seems remotely fair. Don’t be stupid-it is impossible to hold 500 Eagles in just one hand, but did you know that?

Regards

Nicholas

end

Silver eagle sales jump in January

(courtesy Steve St Angelo/SRSRocco )

Silver Eagle sales jump in January

(SRSRocco) – As the demand for precious metals shows some life once again, sales of the U.S. Mint Silver Eagles jumped in January. Not only have Gold, and Silver Eagle sales increased, so have the precious metals prices. In the past two months, gold and silver prices have gained 7% and 11% respectively. Today, gold reached $1,320, while silver topped $16.

While January sales of Silver Eagles fell to a low last year at 3.2 million oz (Moz), down from 5.1 Moz in 2017, they picked up this month surpassing 4 Moz. According to the U.S. Mint’s most recent update, Silver Eagle sales totaled 4,017,500 versus 3,235,000 last year:

————————

end

We now have total silver supply for 2018 at 26,000 tonnes or 835.9 million oz. This includes scrap supplies from silver melting of around 180 million oz. Thus supply form the mines are decreasing coming in at 656 million oz. Demand is just over 1.04 billion oz and thus the deficit is again at around 200 million oz.

(courtesy Bloomberg)

Silver Shortage Promises to Boost Price in 2019

(Bloomberg) — Think of it as a potential silver lining for investors. A deepening shortage is promising to help boost prices as haven demand for the precious white metal rebounds in 2019.

Silver surged 9.1 percent in December, its biggest monthly gain in almost two years. The commodity has benefited as a persistent trade war, weakening dollar and prospects of slower pace of U.S. rate increases drove haven demand for precious metals. The price outlook is improving at a time when demand for gold’s cheaper cousin is poised to top production for a seventh straight year.

With miners avoiding new projects amid global economic uncertainty, the price could spike as high as $17.50 an ounce from about $15.87 now, according to a Bloomberg survey of 11 traders and analysts. About 26,000 tons of silver is expected to be produced this year, according to estimates by Robin Bhar, a London-based analyst at Societe Generale SA. That would be the least since 2013, and means global physical demand will again top output.(Harvey: 26,000 tonnes = 835.9 million oz./they also include scrap as supply./)

“Supply growth has started to slow, more than for any other precious metal,” said John LaForge, the head of real assets strategy at Wells Fargo Investment Institute.

What do all the headlines mean for future demand? As technical analyst Michael Oliver told mining analyst Jay Taylor in a recent interview:

Even [financial advisors] who don’t like gold are getting calls from clients asking “how come we don’t have any gold in our accounts? It’s the best performing asset for the last six months.” Once non-gold people realize it’s the best performing asset out there, they’ll be forced into it, which will widen the investor base for gold mining stocks. If just a small part of what’s in the broader stock market flowed into gold that’s a huge rush of money for such a small sector. The gold and silver miners will probably be the best place on the planet.

-END-

Saw this from expert John Brimelow: Gold smuggling into India is set to increase 25 to 50% this year owing to the high prices and import duties of 10%

(courtesy scrap Register)

Gold smuggling into India liable to increase 50% in 2019

MUMBAI (Scrap Register): India is likely to witness a sharp increase of 25-50 per cent in the entry of smuggled gold in 2019 from the previous year owing to the high price of the precious metal and import duty of 10 per cent imposed by the government.

Gold prices have risen 10 per cent to more than Rs 33,000 per 10 gram since Dec 28, 2018.

The volume of smuggled gold may increase to 150-180 tonnes this year from around 120 tonnes estimated to have entered the country last year.

In the B2B (business-to-business) segment, people are preferring to deal in cash rather than cheque, which is an indication that smuggling is going up. The price difference between cash and cheque in the spot market is around Rs 50,000 per kg of gold.

Demand is muted due to high price, the industry had expected the momentum to pick up from December 15 with the onset of the wedding season. Consumers are waiting for Gold prices to cool off, which does not seem likely to happen in the near future.

-END-

An excellent reason not to invest in cyrptocurrencies: Canadian exchange Quadriga is seeking bankruptcy protection after the mysterious death (from Crohn’s????) of its founder, Gerry Cotton. He seems to have died without telling anyone the keys! to open the cold storage wallets

(courtesy zerohedge)

Crypto Exchange Seeks Bankruptcy Protection After Founder’s Mysterious Death

More than ten years after the birth of bitcoin, the crypto industry remains riddle will con artists, scammers and fraud. And sometimes, businesses that for years appeared to be legitimate enterprises will suddenly be outed as long-running frauds – a la Bernie Madoff – when they hit a speed bump.

For Canadian crypto exchange QuadrigaCX, that moment of truth apparently arrived earlier this month when its CEO Gerry Cotten died suddenly from complications related to Crohn’s disease . According to a statement from the company, he died while traveling in India where “he was opening an orphanage to provide a home and safe refuge for children in need.”

QuadrigaCX@QuadrigaCoinEx

QuadrigaCX@QuadrigaCoinExWe’ve posted an update regarding the latest on our company operations: https://www.quadrigacx.com/

Since his death, 115,000 customers of the exchange have been struggling with Mt. Gox-style “liquidity issues” as those trying to withdraw their funds have suddenly found it extremely difficult – if not impossible – to do so successfully. Finally, on Thursday, Quadriga’s board released a statement announcing that it would be filing for bankruptcy protection. In the statement, the company said the filing was prompted by an inability “to locate and secure our very significant cryptocurrency reserves held in cold wallets.”

An application for creditor protection in accordance with the Companies’ Creditors Arrangement Act (CCAA) was filed today in the Nova Scotia Supreme Court to allow us the opportunity to address the significant financial issues that have affected our ability to serve our customers. The Court is being asked at a preliminary hearing on Tuesday February 5 to appoint a monitor, Ernst & Young Inc., as an independent third party to oversee these proceedings.