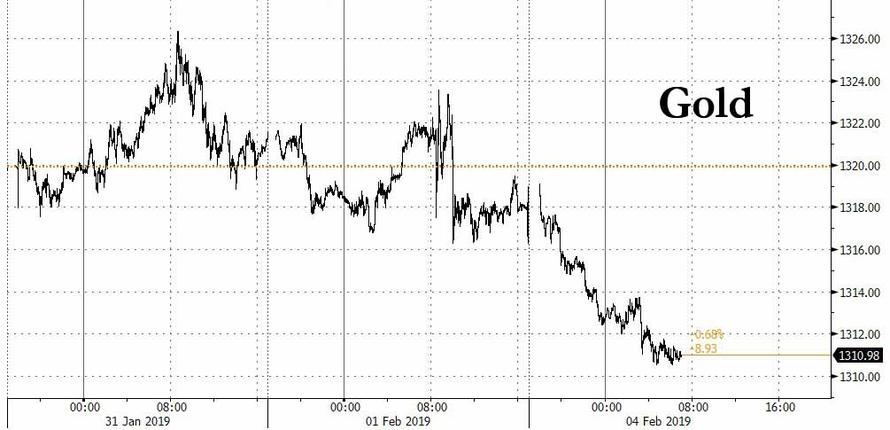

FEB 4/CHINA IS AWAY FOR A WEEK AND THUS EXPECT ALGOS TO GO CRAZY WITH GLEE/GOLD DOWN $2.65 TO $1314.95/SILVER DOWN 4 CENTS TO $15.88/FRANCE IN TURMOIL FOR THE 11TH STRAIGHT WEEKEND/ITALY REJECTS RECOGNIZING GUAIDO AS THE DEFACTO HEAD OF VENEZUEAL/MADURO CONTINUES TO BE DEFIANT AND NOT CALL FOR ELECTIONS/MORE SWAMP STORIES FOR YOU TONIGHT/

Silver: $15.88DOWN 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1312.25

silver: $15.87

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 2254 NOTICE(S) FOR 225,400 OZ (7.010 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 8489 NOTICES FOR 848900 OZ (26.404 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

55 NOTICE(S) FILED TODAY FOR 275,000 OZ/

total number of notices filed so far this month: 394 for 1,970,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3444: DOWN 14

Bitcoin: FINAL EVENING TRADE: $3462 UP $3

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 1276/2254

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,316.900000000 USD

INTENT DATE: 02/01/2019 DELIVERY DATE: 02/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 2

357 C WEDBUSH 6

657 C MORGAN STANLEY 10

657 H MORGAN STANLEY 206

661 C JP MORGAN 2006 607

661 H JP MORGAN 669

685 C RJ OBRIEN 20 2

686 C INTL FCSTONE 11 1

690 C ABN AMRO 61 56

737 C ADVANTAGE 107 76

800 C RCG 32 20

880 H CITIGROUP 606

905 C ADM 9 1

____________________________________________________________________________________________

In silver, the total OPEN INTEREST ROSE BY A HUGE SIZED 35484CONTRACTS FROM 203,388 UP TO 206,872 ACCOMPANYING FRIDAY’S 14 CENT LOSS IN SILVER PRICING AT THECOMEX.TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONGSIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1257 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1257CONTRACTS. WITH THE TRANSFER OF 1257CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1257 EFP CONTRACTS TRANSLATES INTO 6.285 MILLION OZ ACCOMPANYING:

1.THE 14 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.410 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 3463 CONTRACTS (FOR 3 TRADING DAYS TOTAL 3463 CONTRACTS) OR 17.32 MILLION OZ: (AVERAGE PER DAY: 1154 CONTRACTS OR 5.77 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 17.32 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.47% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 234.77 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 35484 WITH THE 14 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1257 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 4741TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1257 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF3484 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 14 CENT LOSS IN PRICE OF SILVERAND A CLOSING PRICE OF $15.92 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.018 BILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 55NOTICE(S) FOR 275,000OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.410 MILLION OZ/

HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A TINY SIZED955CONTRACTS DOWN TO 476,289 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $3.00//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6351 CONTRACTS:

FEBRUARY HAD AN ISSUANCE OF 0CONTACTS APRIL 6708 CONTRACTS, DECEMBER: 0CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 476.289. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5396 CONTRACTS: 955 OI CONTRACTS DECREASED AT THE COMEX AND 6351 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 5396 CONTRACTS OR 539,60, OZ = 16.78 TONNES. AND ALL OF THIS DEMAND OCCURRED WITHA FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.00.

YESTERDAY, WE HAD 6708 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 13,059 CONTRACTS OR 1,305,900 OZ OR 40.61 TONNES (3 TRADING DAYS AND THUS AVERAGING: 4353EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 40.61 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 40.61/2550 x 100% TONNES = 1.59% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,671.96 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED DECREASE IN OI AT THE COMEX OF 955WITH THE LOSS IN PRICING ($3.00) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6351 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6351 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 5396CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6351 CONTRACTS MOVE TO LONDON AND 955 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 16.78 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $3.00 IN YESTERDAY’S TRADING AT THE COMEX

we had: 2254 notice(s) filed upon for 225,400oz of gold at the comex.

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $2.65 TODAY

THE FRAUD CONTINUES:

TWO BIG CHANGES IN GOLD INVENTORY AT THE GLD IN ONE DAY

i)A MASSIVE WITHDRAWAL 8.37 TONNES OF PAPER GOLD AND THIS WAS USED TO LOWER THE PRICE OF GOLD TODAY.

ii) THEN AN ADDITION (DEPOSIT) OF 2.00 TONNES OF GOLD ADDED TO THE GLD.

/GLD INVENTORY 817.40 TONNES

Inventory rests tonight: 817.40 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS IN PRICE TODAY:

A SMALL WITHDRAWAL OF 129,000 OZ AND THAT WOULD PROBABLY PAY FOR FEES

/INVENTORY RESTS AT 310.594 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 3484 CONTRACTS from 203,388 UP TO 206,872 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1257 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1257 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3484 CONTRACTS TO THE 1257OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 4741 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 23.71 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.410 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 14 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1257 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED UP 59.47% /The Nikkei closed UP 14.90 PTS OR 0.21%/ Australia’s all ordinaires CLOSED UP .47%

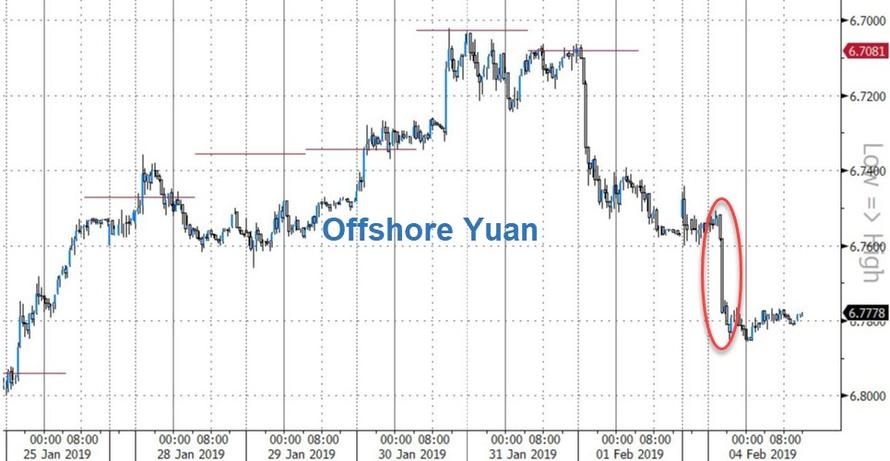

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 55.06 dollars per barrel for WTI and 62.70 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON

//. ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7802: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA

China is in big trouble as its current account shrinks to zero, its total debt to GDP rises to 300% and much of that debt is non performing. A good reason why China is dramatically slowing down

(courtesy Schmid/Epoch times)

4/EUROPEAN AFFAIRS

i)France

The yellow vest march to denounce police violence and they were promptly beaten up by riot police. This is the 11th weekend in a row for protests.

( zerohedge)

ii)The Gatestone Institute’s Guy Milliere explains in detail what is going on in France

( Guy Milliere/Gatestone)

iii)UK/EU

Mish Shedlock is correct: the UK will have only one to two years of pain by walking out of BREXIT but if May continues with her plan there will be permanent idiocy

( Mish Shedlock/Mishtalk)

iv)Italy/Venezuela

Italy thwarts the EU plans to recognize Guaido as legitimate leader of Venezuela.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i) EU

Europe has a new SWIFT system for payment but they will not dare go against the USA on fears of sanctions

( zerohedge)

ii)This will not go over well with Trump: Iran test launches a new long range cruise missile

( zerohedge)

iii)Trump now delays his Syria departure as he must protect Israel from Iranian aggression

( zerohedge)

6. GLOBAL ISSUES

Things are not going off too well for General Motors. They are going to lay off 4250 salaried workers in North America starting Monday.

(courtesy Shannon Jones/Global Research)

and special thanks to Robert H for sending this to us:

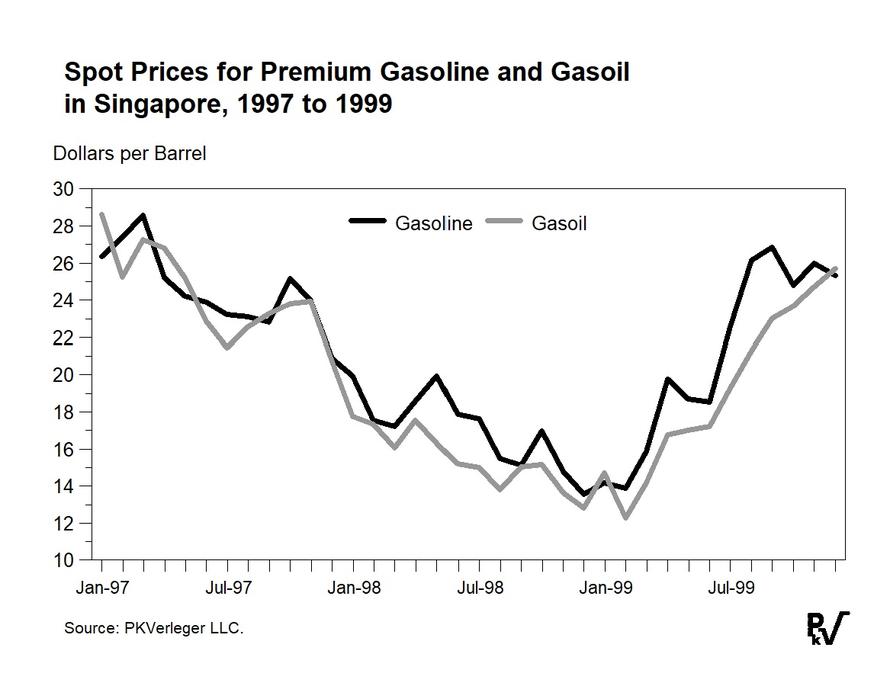

7. OIL ISSUES

The low price of oil can no doubt will have a devastating effect on global oil, especially if the “teapots” dump refined oil at lower and lower prices.

(courtesy Philip Verleger/OilPrice.com

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

Tom Luongo outlines the USA plan to take over Venezuela and put American firms in control of their oil. Luongo states that time is running out on the Americans

( Tom Luongo)

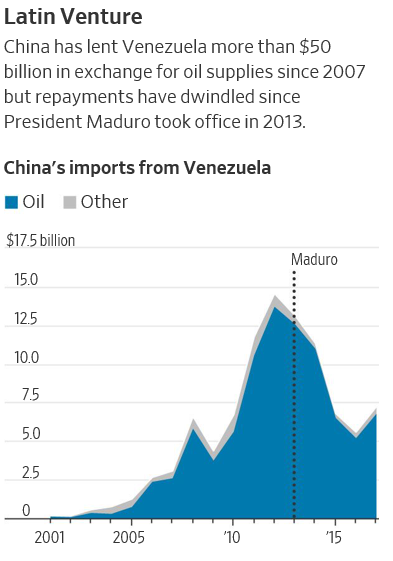

ii)During the past 12 years, China has lent Venezuela 50 billion USA dollars on an oil/loan basis. The loan has been whittled down to $20 billion dollars. Venezuela has not paid much since 2015. Russia is owed $3 billion and thus we may be a USA-China/ USA Russia proxy war in Venezuela especially if Guaido gets into power.

( zerohedge)

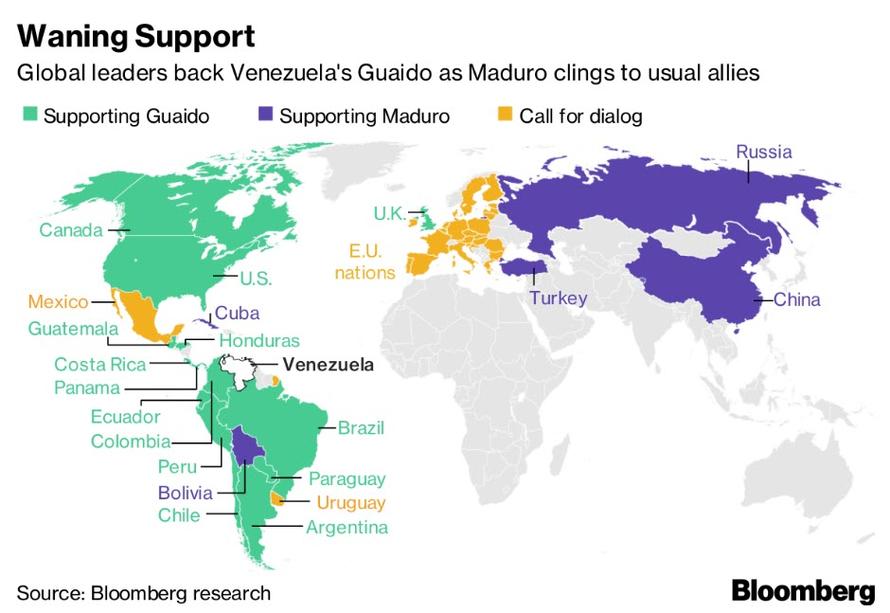

iii)Do not know if this will help but self declared President of Venezuela, Guaido reaches out to China in an attempt to win them over. Trump continues to repeat that military force is an option of which China and Russia will not be happy. However Venezuela is in the sphere of influence of the USA

i)Bus driver genius, Maduro sells 3 tonnes of gold to UAE’s Noor capital( Reuters/GATA)

ii)Very strange for the BIS to execute swaps whereby they are long unallocated gold and short allocated gold. Is the BIS trying to recover lost central bank gold?

( Robert Lambourne/GATA)

iii)Please read…the truth behind the price rigging by the BIS..

( GATA/Chris Powell)

iv)This sovereign wealth fund strongly believes in gold.

( Bloomberg/GATA)

v)Chris Waltzek interview Bill Murphy talking about the years of suppression which has led to company consolidations and acquisitions.

( GATA)

vi)A very important commentary form Jeffrey Snider as he asks if gold trading higher due to fear or reflation. He strongly suggests it is fear and China is the main culprit

(courtesy Jeffrey Snider)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)November was the first month that we witnessed a downturn in many numbers. We know get November factory orders and they tumbling .6% month over month

( zerohedge)

b)It sure does not look good: small business confidence is suddenly collapsing at the fastest pace

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

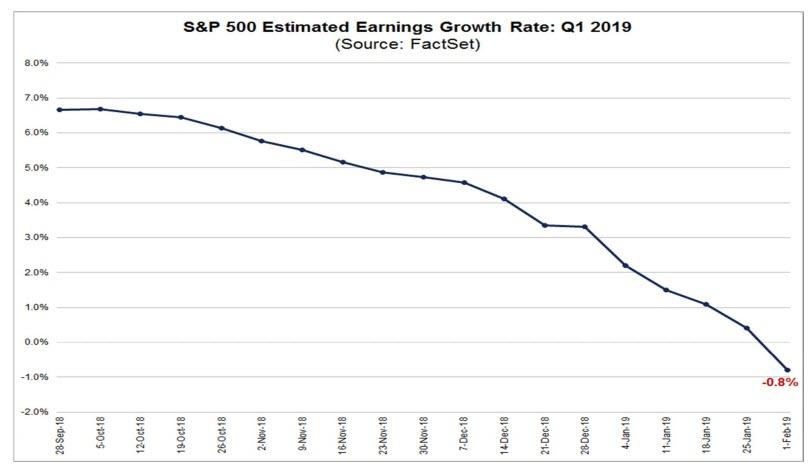

a)Interesting: the first quarter earnings growth is now faltering which should cause some problems for the markets

( zerohedge)

iv)SWAMP STORIES

Funny!! Poor Maxine!!Deutsche bank refused to lend to Trump during the 2016 Presidential race…another Democrat theory down the drain.

( zerohedge)

b)Trump teases that a national emergency is set to be declared to fund the border wall.

( zerohedge)

E)SWAMP STORIES/MAJOR STORIES//THE KING REPORT

end

Let us head over to the comex:

THE TOTAL COMEX GOLD OPEN FELL BY AN TINY SIZED 955CONTRACTS DOWN TO A LEVEL OF 476,289 WITH THE FALL IN THE PRICE OF GOLD ($3.00) INFRIDAY’S COMEX TRADING).FOR TWO YEARS STRAIGHT WE HAVE NOTICED THAT ONE WEEK PRIOR TO FIRST DAY NOTICE OF AN ACTIVE DELIVERY MONTH THE COMEX OPEN INTEREST CONTRACTS AND EFP’S NOTICES EXPONENTIALLY INCREASE AS WELL AS WE WITNESS THE COMEX OPEN INTEREST COLLAPSE. ONCE WE GET TO FIRST DAY NOTICE, THEN THE OPEN INTEREST RISES., THE REASON FOR THE COLLAPSE IN OPEN INTEREST IS THE FORCED LIQUIDATION OF THE SPREADERS.

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JANUARY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS., THAT IS 6351 EFP CONTRACTS WERE ISSUED:

FOR FEBRUARY: 0. FOR APRIL 6351, FOR DECEMBER: 0 AND ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6361 CONTRACTS.

THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON BASED FORWARD.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES:5396 TOTAL CONTRACTSIN THAT 6351 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST A TINY SIZED 955COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES:5396 contracts OR 539600 OZ OR 16.78 TONNES.

We are now in the active contract month of FEBRUARY and here the open interest stands at 3,851 contracts, and thus undergoing a loss of 5238 contracts. We had 5296 contracts stand for delivery yesterday so we gained 58 contractsor 5,800 additional oz will stand for delivery in this very active delivery month of February as they refused to morph into London based forwards as well as negating a sizable fiat bonus.

QUEUE JUMPING RETURNS TO THE COMEX QUITE EARLY IN THE FEBRUARY DELIVERY CYCLE. THE CROOKS ARE SHORT OF GOLD!!

The next non active delivery month after February is March and here we GAINED 47 contracts to stand at 1691. After March, the next big delivery month is April and here the OI rose by 3899 contracts up to 341,078 contracts.

FOR COMPARISON FEBRUARY 2019 TO THE FEBRUARY 2018 COMEX GOLD CONTRACT MONTH

ON FEB 1.2018: 20.07 TONNES OF GOLD STOOD FOR DELIVERY, BUT BY THE END OF MONTH ONLY 8.55 TONNES EVENTUALLY STOOD AS THE REST MORPHED INTO LONDON BASED FORWARDS.

TODAY’S NOTICES FILED:

WE HAD 2254 NOTICES FILED TODAY AT THE COMEX FOR 225,400 OZ. (7.010 tonnes)

Total COMEX silver OI ROSE BY A STRONG SIZED 3484 CONTRACTS FROM 203,388 UP TO 206,872(AND CLOSER TO THE NEW RECORD OI FOR SILVER SET ON AUGUST 22.2018. (THE PREVIOUS RECORD WAS SET APRIL 9.2018/ 243,411 CONTRACTS)AND TODAY’S OI COMEX GAIN OCCURRED DESPITE A 14 CENT LOSS IN PRICING.

WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF FEBRUARY AND THE AMOUNT OF OPEN INTEREST READY TO STAND IS 143 CONTRACTS, HAVING LOST 32 CONTRACTS FROM FRIDAY. WE HAD 53 NOTICES FILED ON FRIDAY SO WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF FEBRUARY.

.

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 1629 CONTRACTS DOWN TO 140,327 CONTRACTS. AFTER MARCH, APRIL MAINTAINED ITS INITIAL 15 OPEN INTEREST CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 5008 CONTRACTS UP TO 34,788 CONTRACTS.

ON A NET BASIS WE GAINED 4741 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 3484 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1257 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 4741 CONTRACTS...AND ALL OF THIS STRONG DEMAND OCCURRED WITH A 14 CENT LOSS IN PRICING// FRIDAY??

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

TODAY’S NUMBER OF NOTICES FILED:

We, today, had 55 notice(s) filed for 275,000 OZ for the FEB, 2019 COMEX contract for silver

Trading Volumes on the COMEX TODAY: 148,067 CONTRACTS

CONFIRMED COMEX VOL. FOR YESTERDAY: 208,534 contracts

Total monthly oz gold served (contracts) so far this month

8489 notices

848,900 OZ

26.404 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

we had 0 dealer entries:

total dealer deposits: NIL oz

total dealer withdrawals: 0 oz

We had 1 kilobar entries

we had 1 deposit into the customer account

i) Into HSBC: 2,000.000 oz exactly

the whole comex is a fraud

total gold customer deposits; 2,000.000 oz

we had 0 gold withdrawals from the customer account:

total gold withdrawing from the customer; NIL oz

we had 1 adjustments….

i) Out of JPMorgan: 115,740.000 oz was adjusted out of the customer and into the dealer.

no settlement yet.

FOR THE FEB 2019 CONTRACT MONTH)

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2254 contract(s) of which 669 notices were stopped (received) by j.P. Morgan dealer and 607 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY/2019. contract month, we take the total number of notices filed so far for the month (8489) x 100 oz , to which we add the difference between the open interest for the front month of FEB. (3851 contract) minus the number of notices served upon today (2254 x 100 oz per contract) equals 1,008,600 OZ OR 31.371 TONNES) the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEB/2019 contract month:

No of notices served (8489 x 100 oz) + {3851)OI for the front month minus the number of notices served upon today (2254 x 100 oz )which equals 1,008,600 oz standing OR 31.371 TONNES in this active delivery month of FEBRUARY.

WE GAINED 58 CONTRACTS OR AN ADDITIONAL 5,800 OZ WILL STAND AT THE COMEX AS THEY REFUSED TO MORPHED INTO A LONDON BASED FORWARD AS WELL AS NEGATING A FIAT BONUS.

THERE ARE ONLY 28.588 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 31.371 TONNES STANDING FOR FEBRUARY

OF WHICH26.404TONNES OF GOLD HAVE ALREADY BEEN SERVED UPON SO FAR THIS MONTH.

total registered or dealer gold: 919,115.667 oz or 28.588 tonnes

total registered and eligible (customer) gold; 8,441,056.807 oz 262.552 tonnes

IN THE LAST 27 MONTHS 92 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOV DELIVERY MONTH

FEB INITIAL standings/SILVER

FEB 4 2019

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

860,485.659 oz

Brinks

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

796.472.243 oz

Brinks

CNT

No of oz served today (contracts)

55

CONTRACT(S)

275,000 OZ)

No of oz to be served (notices)

86 contracts

440,000 oz)

Total monthly oz silver served (contracts)

394 contracts

(1,970,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: 0 oz

we had 2 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 147.7 million oz of total silver inventory or 50.77% of all official comex silver. (149.787 million/295 million)

i) Into Brinks: 196,478.800 oz

ii) Into CNT: 599,993.443 oz

total customer deposits today: 796.472.243 oz

we had 1 withdrawals out of the customer account:

i) Out of Brinks: 860,485.659 oz

total withdrawals: 860,485.659 oz

we had 0 adjustment..

total dealer silver: 88.142 million

total dealer + customer silver: 297.214 million oz

The total number of notices filed today for the FEBRUARY 2019. contract month is represented by 55 contract(s) FOR 275,000 oz

To calculate the number of silver ounces that will stand for delivery in FEB., we take the total number of notices filed for the month so far at 394 x 5,000 oz = 1,970,000 oz to which we add the difference between the open interest for the front month of FEB. (143) and the number of notices served upon today (55x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEBRUARY/2019 contract month: 394(notices served so far)x 5000 oz + OI for front month of FEB( 143) -number of notices served upon today (55)x 5000 oz equals 2,410,000 oz of silver standing for the FEBRUARY contract month. This is a strong number of oz standing for an off delivery month.

WE GAINED 21 CONTRACTS OR AN ADDITIONAL 105,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS AND ALSO NEGATING A FIAT BONUS. QUEUE JUMPING CONTINUES AT THE COMEX UNABATED.

YESTERDAY’S CONFIRMED VOLUME OF 80,139 CONTRACTS EQUATES to 400 million OZ 57.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -3.60% (FEB 4/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.77% to NAV (FEB 4 /2019 )

Note: Sprott silver trust back into NEGATIVE territory at -3.60%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.35/TRADING 12.84/DISCOUNT 3.80

END

And now the Gold inventory at the GLD/

FEB 4/WITH GOLD DOWN $2.65: TWO TRANSACTIONS: i)A MASSIVE WITHDRAWAL OF 8.37 TONNES OF PAPER GOLD WAS REMOVED FROM THE GLD AND THEN ii) a A STRONG DEPOSIT OF 2.00 TONNES/INVENTORY RESTS AT 817.40 TONNES

FEB 1/WITH GOLD DOWN $3.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.87 TONNES

JAN 31/WITH GOLD UP $9.80 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.87 TONNES

JAN 30/WITH GOLD UP $.65: A HUGE HUGE MONSTROUS ADDITION OF 8.23 TONNES OF PAPER GOLD ENTERED THE GLD/INVENTORY RESTS AT 823.87..SO FAR IN JANUARY: 28.56 TONNES HAVE BEEN ADDED

JAN 29/WITH GOLD UP $6.15/A HUGE ADDITION OF 5.88 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 815.64 TONNES

JAN 28/WITH GOLD UP $5.30 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 809.76 TONNES

JAN 25/WITH GOLD UP $17.90: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 809.76 TONNES

jAN 24/WITH GOLD DOWN $3.70?: NO CHANGES AT THE GLD/INVENTORY RESTS AT 809.76 TONNES

JAN 23/WITH GOLD UP 50 CENTS: NO CHANGES AT THE GLD/INVENTORY RESTS AT 809.76 TONNES

JAN 22/WITH GOLD UP A TINY $.85 A MASSIVE PAPER DEPOSIT OF 12.06 TONNES OF GOLD INTO THE FRAUDULENT GLD/INVENTORY RESTS AT 809.76 TONNES

JAN 18/WITH GOLD DOWN $9.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 797.71

JAN 17/WITH GOLD DOWN $1.10: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 797.71

JAN 16/WITH GOLD UP $5.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 797.71

JAN 15/WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 797.71 TONNES

JAN 14/WITH GOLD UP $1.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 797.71 TONNES

JAN 11/WITH GOLD UP $2.30 TODAY ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD/INVENTORY RESTS AT 797.71 TONNES

JAN 10/WITH GOLD DOWN $4.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.18 TONNES

JAN 9/WITH SILVER UP $6.00/ TWO TRANSACTIONS: a) A TINY WITHDRAWAL OF .25 TONNES TO PAY FOR FEES ETC b) A HUGE DEPOSIT OF 2.65 TONNES INTO THE GLD INVENTORY./INVENTORY RESTS AT 799.18 TONNES

JAN 8/WITH GOLD DOWN $3.70 TODAY, A WITHDRAWAL OF 1.47 TONNES AND THIS GOLD WAS USED IN THE RAID/INVENTORY RESTS AT 796.78 TONNES

JAN 7/WITH GOLD UP $4.45 TODAY: A HUGE DEPOSIT OF 2.94 TONNES OF GOLD ENTERED THE GLD/INVENTORY RESTS AT 798.25 TONNES

JAN 4/WITH GOLD DOWN $8.65 TODAY; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.31 TONNES

JAN 3/2019/WITH GOLD UP $10.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 795.31 TONNES

JAN 2.2019/WITH GOLD UP $3.35 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.64 TONNES/INVENTORY RESTS AT 795.31 TONNES

DEC 31/WITH GOLD DOWN $2.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 787.67 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

FEB 4/2019/ Inventory rests tonight at 817.40/ tonnes

*IN LAST 544 TRADING DAYS: 117.65 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 444 TRADING DAYS: A NET 42.38 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

FEB 4/WITH SILVER DOWN 4 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 129,000 OZ TO PAY FOR FEES/.INVENTORY RESTS AT 310.594 MILLION OZ/

FEB 1/WITH SILVER DOWN 14 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 310.723 MILLION OZ/

JAN 31/WITH SILVER UP 15 CENTS TODAY: ANOTHER BIG DEPOSIT OF 1.126 MILLION OZ/INVENTORY RESTS AT 310.723 MILLION OZ/

JAN 30/WITH SILVER UP 7 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 938,000 INTO THE SLV INVENTORY./INVENTORY RESTS AT 309.597 MILLION OZ.

JAN 29/WITH SILVER UP 9 CENTS TODAY/A HUGE DEPOSIT OF 1.408 MILLION OZ IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 308.659 MILLION OZ/

JAN 28/WITH SILVER UP 5 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 307.251 MILLION OZ/

JAN 25/WITH SILVER UP 40 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 307.251 MILLION OZ/

JAN 24/WITH SILVER DOWN 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY

JAN 23/WITH SILVER UP 4 CENTS: A HUGE LOSS OF 938,000 FROM THE SLV/INVENTORY RESTS AT 307.251 MILLION OZ/

JAN 22/WITH SILVER DOWN 5 CENTS: A HUGE DEPOSIT OF 1.179 MILLION OZ INTO THE SLV/SLV IS A FRAUDULENT VEHICLE/INVENTORY RESTS AT 308.189 MILLION OZ/

JAN 18/WITH SILVER DOWN 13 CENTS: NO CHANGE IN SILVER INVENTORY/NO DOUBT THE MASSIVE WITHDRAWAL OF PAPER SILVER WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 307.110

JAN 17/WITH SILVER DOWN 9 CENTS TODAY:ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV; A MASSIVE WITHDRAWAL OF 3.895 MILLION OZ./INVENTORY RESTS AT 307.110 MILLION OZ/

JAN 16/WITH SILVER FLAT TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV

A WITHDRAWAL OF 2.158 MILLION OZ/INVENTORY RESTS AT 311.005 MILLION OZ/

JAN 15/WITH SILVER DOWN 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 469,000 OZ FROM ITS INVENTORY/INVENTORY RESTS AT 313.163 MILLION OZ/

JAN 14/WITH SILVER UP ONE CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 313.632 MILLION OZ/

JAN 11/WITH SILVER UP 4 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 313.632 MILLION OZ/

JAN 10/WITH SILVER DOWN 11 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 313.632 MILLION OZ/

JAN 9/WITH SILVER UP 4 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.126 MILLION OZ/INVENTORY LOWERS TO 313.632 MILLION OZ/???

JAN 8/WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.758 MILLION OZ

JAN 7/WITH SILVER DOWN ONE CENT: A HUGE WITHDRAWAL OF 2.347 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 314.758 MILLION OZ/

JAN 4/WITH SILVER DOWN 3 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 317.105 MILLION OZ

JAN 3/2019/WITH SILVER UP 22 CENTS A SMALL CHANGE TODAY: A WITHDRAWAL OF 118,000 OZ TO PAY FOR FEES: INVENTORY RESTS AT 317.105 MILLION OZ/

JAN 2/2019/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.233 MILLION OZ/

DEC 31/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.233 MILLION OZ/

FEB 4/2019:

Inventory 310.594 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

THE RISE IN LIBOR IS CREATING A SCARCITY OF DOLLARS BECAUSE FOREIGN EXCHANGE SWAPS (COSTS) ARE SIMPLY PROHIBITIVE

YOUR DATA…..

6 Month MM GOFO 2.21/ and libor 6 month duration 2.79

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .58

XXXXXXXX

12 Month MM GOFO

+ 2.50%

LIBOR FOR 12 MONTH DURATION: 2.96

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.67

end

PHYSICAL GOLD/SILVER STORIES

end

i) GOLDCORE BLOG/Mark O’Byrne

7 Financial Truths In An Uncertain 2019

7. Diversify, diversify, diversify – Truly balance your savings and investments 6. Avoid leverage and speculation and focus on saving and owning quality assets 5. Don’t make money the guiding principle for what you have or do 4. Own gold/ silver (in safest ways) & focus on value rather than price in fiat $, €, £ 3. Do everything you can to avoid excessive debt 2. Enjoying the simple things in life – our health and our families health, time with family & friends, good food, time in nature, travel, “a baby’s smile …” 1. “DON’T WORRY, BE HAPPY …14,000 things to be happy about… “

GATA STORIES AS IT RELATES TO PHYSICAL GOLD/SILVERBus driver genius, Maduro sells 3 tonnes of gold to UAE’s Noor capital(courtesy Reuters/GATA)

UAE’s Noor Capital says it bought 3 tonnes of gold from Venezuela

Submitted by cpowell on Sat, 2019-02-02 14:37. Section: Daily Dispatches

By Mayela Armas

Reuters

Friday, February 1, 2019

CARACAS, Venezuela — Abu Dhabi investment firm Noor Capital said today it bought 3 tonnes of gold on Jan. 21 from Venezuela’s central bank, at a time when President Nicolas Maduro is seeking to keep his crisis-stricken government solvent.

Noor Capital said in a statement it would refrain from further transactions until Venezuela’s situation stabilizes and its purchase was in accordance with “international standards and laws in place” as of Jan. 21.

Reuters reported Thursday that Venezuela had shipped 3 tonnes of gold to the United Arab Emirates on Jan. 26 and would sell 15 tonnes more to the country in the coming days.

Venezuela’s plan was to sell 29 tonnes of gold held in Caracas to the UAE by February in order to provide liquidity for imports of basic goods, a senior official said.

Two high-level Venezuelan central bank officials were made to resign on Thursday and today because they did not want to authorize the sale of gold, three sources familiar with the situation said, declining to be named because the situation was sensitive. …

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

Very strange for the BIS to execute swaps whereby they are long unallocated gold and short allocated gold. Is the BIS trying to recover lost central bank gold?

(courtesy Robert Lambourne/GATA)

Robert Lambourne: Is BIS using swaps to recover central bank gold?

Submitted by cpowell on Sat, 2019-02-02 21:09. Section: Documentation

By Robert Lambourne

Saturday, February 2, 2019

Disclosures in the recent monthly statements of account published by the Bank for International Settlements show that the bank is still actively trading in gold swaps, which the bank uses to gain access to gold held by commercial banks.

There is not enough information in the monthly reports to calculate the exact amount of swaps. But based on December’s statement, which was posted very late, only this week —

— it can be estimated that the bank’s gold swaps exceeded 275 tonnes at the end of the month. This compares to estimates of 308 tonnes in November, 372 tonnes in October, 238 tonnes in September, and 370 tonnes in August.

The BIS began using gold swaps more than nine years ago. They were first disclosed in the bank’s annual report for the year ended March 31, 2010. The BIS reported then that it had acquired 346 tonnes of gold through swaps.

Based on a review of the bank’s annual reports, it seems that the BIS was not involved in gold swaps for at least 10 years prior to 2010. As can be seen from the following table, the BIS has used gold swaps extensively since 2010.

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

The BIS rarely comments publicly on its banking activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published on July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were all carried out with commercial banks and so did not involve other central banks.

The article includes comments from people said to be familiar with the BIS’ gold transactions:

“Some analysts speculated that the swap deals were a surreptitious bailout of the European banking system ahead of last week’s publication of stress tests. But bankers and officials have described the transactions as ‘mutually beneficial.’

“‘The client approached us with the idea of buying some gold with the option to sell it back,’ said one European banker, referring to the BIS.

“Another banker said: ‘From time to time central banks or the BIS want to optimize the return on their currency holdings.'”

The comments to the FT confirm that the BIS initiated the discussions on making the swaps with its potential counter parties and was the driving force behind the transactions. Since that interview in 2010 the BIS has offered no more public comments on their use of gold swaps.

Indeed, the BIS has refused GATA’s request to explain its activity and objectives in the gold market and to confirm or dispute this analyst’s conclusions about them:

From disclosures in the BIS’ annual and semi-annual reports, it appears highly likely that the bank’s gold swap activity involves only commercial banks acting as their counterparties rather than other central banks. Since the BIS initiated these transactions, it is fair to ask whether the swaps are being used to top up central bank gold holdings.

The swaps make the BIS long unallocated gold and short allocated gold, which seems a strange position for the supposedly conservatively run central bank of the central banks. This exposure is not highlighted in the voluminous risk-management disclosures made in BIS annual reports.

The nine-year period during which the BIS has been involved with gold swaps has also seen a substantial decline in the volume of gold being deployed in the BIS’ traditional gold banking business. The traditional gold banking business saw the BIS acting as an agent for central banks wishing to deposit gold on an unallocated basis with other central banks based in major gold trading centers.

As an example, this business allowed the gold of Germany’s central bank to be deposited safely on its behalf with the Bank of England though Germany and the United Kingdom were at war from 1939 to 1945. As this traditional gold banking business has declined, there have been occasions when swaps have provided more than 50 percent of the gold deposited by the BIS in unallocated gold accounts with major central banks in gold trading centers — an example such as occurred on March 31, 2017.

So the use of gold swaps has become an important source of gold for the BIS’ banking business. Such a major change to the nature of the BIS’ gold banking has not been explained by the BIS, and it seems a rather odd development since the driving force for the traditional gold banking business was presumably demand from central banks wishing to protect their gold by depositing it with the BIS rather than directly with another central bank in a gold trading center.

One could imagine that Venezuela lately might have preferred to deposit its gold at the Bank of England via a transaction with the BIS rather than directly.

The use of gold swaps to source gold to be deposited in BIS unallocated gold accounts at major central banks does not appear to fit with the original rationale for the bank’s gold banking business. But it does fit the possibility of shortages of central bank gold being filled by the BIS through swaps.

Will the BIS ever explain if this assessment is wrong?

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

END

Please read…the truth behind the price rigging by the BIS..

(courtesy GATA/Chris Powell)

A voice from inside the gold swap and price-rigging business

Submitted by cpowell on Sun, 2019-02-03 16:04. Section: Daily Dispatches

11:17a ET Sunday, February 3, 2019

Dear Friend of GATA and Gold:

GATA consultant Robert Lambourne’s report yesterday about the gold trading signified by the December financial statement of the Bank for International Settlements speculated that the bank’s use of gold swaps might mean to recover gold for central banks that are inconveniently short in their official reserves:

In response to Lambourne’s analysis, a prominent figure in the gold business in London and elsewhere who has followed GATA’s work for many years wrote to your secretary/treasurer with his own account of the swap business and invited GATA to distribute it.

It confirms that central banks trade gold in large part to facilitate gold production by providing cheap financing for mines, to regulate and contain the price of the monetary metal, and thus to discourage increases in the price of all commodities.

…

This echoes and elaborates on the candid admission by Barrick Gold in U.S. District Court in New Orleans in 2003 that in borrowing and selling central bank gold in pursuit of its mining operations, the company had become the agent of the central banks in regulating the gold market:

What follows from our friend formerly in the gold business in London cannot be attached to him by name, as it predictably enough might get our friend in trouble with some powerful people. That makes our friend an anonymous source, something that, for credibility reasons, GATA seldom bothers with. What our friend says is just hearsay to you.

But there is nothing outlandish about our friend’s account and its elaboration fits neatly with everything else GATA has documented, so perhaps it can be offered simply as a plausible possibility about how the world financial system is being operated surreptitiously. Our friend’s account also would be an excellent outline for journalistic pursuit of the world financial system’s operations if the world ever enjoys any serious financial journalism.

Our friend writes as follows.

* * *

“My firm regularly traded unallocated gold swaps with central banks and the Bank for International Settlements in the 1970s and 1980s. This was a major source of gold finance for the mining industry, enabling the BIS and other official gold holders to get a U.S. dollar return on part of their large gold holdings and allowing bullion dealers to provide cheap project finance for miners and jewellers. It also enabled less-creditworthy central banks to manage short-term liquidity issues.

“Effectively this process created a supply of ‘paper gold’ — sometimes but not always marked to market — that had a depressing effect on the gold price.

“Following the near-disasters of the gold short positions of Long-Term Capital Management (1998) and Ashanti (1999), such official activity was greatly reduced. But the more recent sudden major downward moves in the gold price could well have been effected by swap trading.

“After the LTCM and Ashanti incidents, the BIS’ Financial Stability Unit, which was formed in response to those near-disasters, was replicated by central banks around the world. Volatility in the gold price and gold’s status as a proxy for all commodities made it a target for official ‘shock absorber’ actions — something welcomed by both the BIS and the International Monetary Fund.”

* * *

What is so outlandish about GATA’s conclusions about gold and commodity market manipulation?

GATA might be demolished by a public statement from the bank or a group of central banks, accompanied by the disclosure of official documents, asserting that they have nothing to do with the gold market and couldn’t care less about the valuation of the once and possibly future world reserve currency.

Instead all that can be extracted from the BIS is its comprehensive refusal to answer for itself:

Monetary metals mining companies and the World Gold Council refuse to pursue the truth here, though it is crucial to monetary metals investors.

So GATA is grateful to our friend from the gold business for being so candid with us — and with you.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

end

This sovereign wealth fund strongly believes in gold.

(courtesy Bloomberg/GATA)

Gold is one wealth fund’s escape from geopolitics, credit risk

Submitted by cpowell on Sun, 2019-02-03 15:00. Section: Daily Dispatches

By Zulfugar Agayev

Bloomberg News

Sunday, February 3, 2019

For Azerbaijan’s sovereign wealth fund, nothing beats the safety of gold in a world gripped by trade disputes and geopolitical risk.

Known as Sofaz, the fund is looking to almost double its holdings of the precious metal in 2019 to 100 tons after resuming purchases in 2018 following a five-year break. By contrast, it’s steering clear of larger bets on bonds and especially equities, an approach that Executive Director Shahmar Movsumov says allowed the fund to avoid losses last year.

…

We would want to have something that is not someone else’s credit risk,” Movsumov said in an interview in the capital, Baku, on Friday. “In a world where you see the changes in geopolitics, changes in reserve currencies, changes in the dynamics between superpowers and their imminent impact on the financial sector, you want to be on the safe side.” …

Chris Waltzek interview Bill Murphy talking about the years of suppression which has led to company consolidations and acquisitions.

(courtesy GATA)

GoldSeek Radio’s Chris Waltzek interviews GATA Chairman Bill Murphy

Submitted by cpowell on Sun, 2019-02-03 23:03. Section: Daily Dispatches

6p ET Sunday, February 3, 2019

Dear Friend of GATA and Gold:

Years of price suppression have stifled gold exploration and are leading to mining company consolidations and acquisitions, GATA Chairman Bill Murphy says, concurring with GoldSeek Radio’s Chris Waltzek in an interview posted today. When the physical gold market overwhelms the “paper gold” market, Murphy says, the fundamentals for gold will assert themselves and the price will soar.

The interview is 12 minutes long and begins at the 31:40 mark here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

iii) Other Physical stories

Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

(courtesy zerohedge/Chris Powell)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

A sign of JP Morgan Chase Bank is seen in front of their headquarters tower in New York.

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

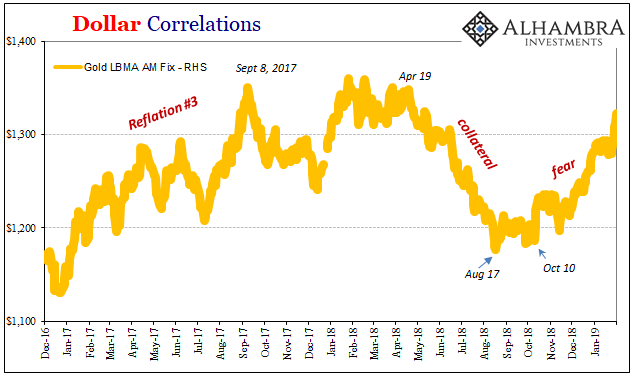

A very important commentary form Jeffrey Snider as he asks if gold trading higher due to fear or reflation. He strongly suggests it is fear and China is the main culprit

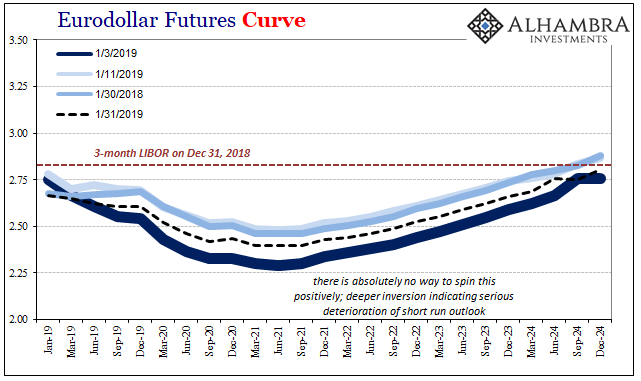

Gold is on fire, but why is it on fire? When the precious metals’ price falls, Stage 2, we have a pretty good idea what that means (collateral). But when it goes the other way, reflation or fear of deflation? Stage 1 or Stage 3?

If it is Stage 1 reflation based on something like the Fed’s turnaround, then we would expect to find US$ markets trading in exactly the same way. Like 2017, when gold was last rising, there should be reflationary corroboration in rising rates, current and expected, along with inflation expectations and curves.

That’s not happening here or anywhere. Even as the “bond market” including eurodollar futures has retraced some of December’s awfulness, it really hasn’t been all that much and the curves are still highly distorted (liquidity risk, therefore clear deflation signal).

This one, a very important set of prices, goes into the fear column.

Maybe gold is up because of something the Chinese are doing. Some kind of reflationary “stimulus” that gets the whole thing restarted after the aborted soft landing the last half of last year. Gold, after all, isn’t determined solely by what may be happening US economy-wise or even in eurodollar capacities. China in monetary overdrive might seem an inflation risk worth hedging.

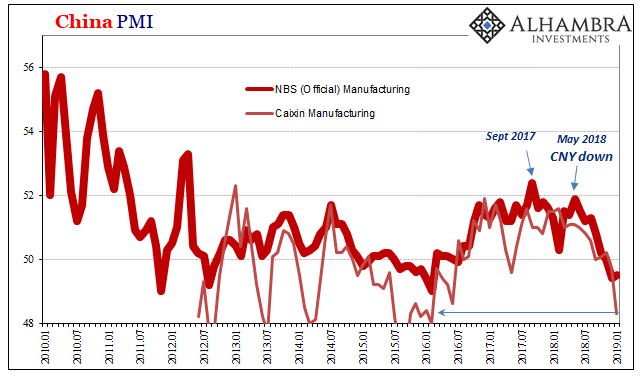

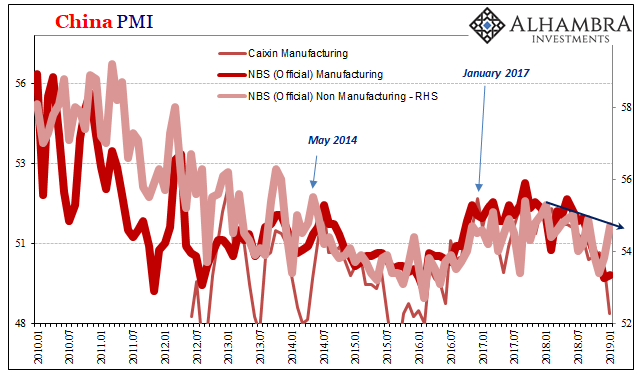

Except, gold really started moving upward back in October when China was engulfed in deflationary liquidation (right from the start of its reopening from the National Day Golden Week). Despite several attempts at “stimulus”, which isn’t stimulus, the Chinese economy continues down the deflation track unabated.

The first look at January 2019 inside China isn’t encouraging. The Chinese NBS reports today that the manufacturing PMI remained below 50 for a second straight month. Though the overall index was marginally higher than December, the subindex for New Orders declined a little further below 50 (and New Export Orders quite a bit below 50). It doesn’t appear Chinese manufacturing is going to turnaround in the next few months.

Neither the New Orders nor New Export Orders components have been this low since the worst point of the global downturn 2015-16. That’s also true of the separate Caixin Manufacturing Survey. Measuring more of medium-sized Chinese producers, this PMI declined to 48.3 in January. It was 51 just seven months ago.

Even what might seem like good news isn’t. The NBS PMI for the services sector rebounded to 54.7 last month from 53.8 the month before. However, this merely continues the same volatile sawtooth pattern, one that has taken on a downward trend of lower highs and lower lows. Not as fast in deceleration as manufacturing, still the wrong direction.

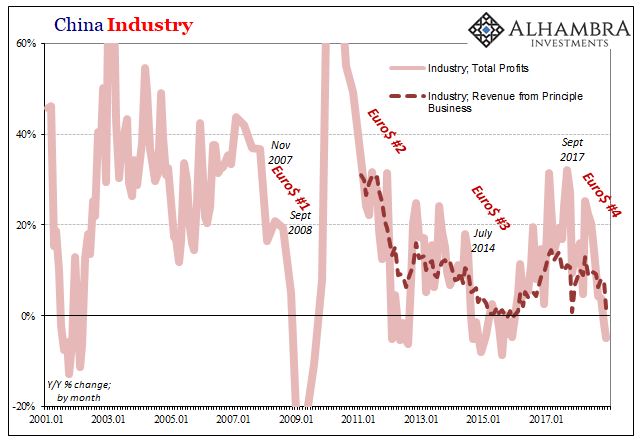

In another report, China’s NBS estimates about industrial revenues and profits for December 2018 show even more deterioration than what’s figured in their PMI’s. On an accumulated basis, Revenues from Principle Activities gained just 8.5% for December. That means for the full-year 2018, sales growth was 8.5% above the total for all of 2017.

In terms of Total Industrial Profits, the accumulated growth rate for December was down to just 10%. These are not encouraging results.

Because accumulated estimates can be biased by what happened early in any year, pulling apart these numbers by month instead gives us a better sense of more recent conditions and directions. On a monthly basis, China’s industrial deterioration is stark: revenues were up just 1.6% year-over-year in December alone, while profits fellby just about 5%.

This is certainly where the PMI’s and industrial figures agree; manufacturing and industry in China hasn’t been this bad since the last time the whole world was in a downturn.

If Chinese industry is behaving like it did in early 2016, the worst parts of Euro$ #3, it sure raises questions about the state of the global economy right now.

I’m pretty sure this one goes in the fear column, too.

That would leave reflation gold with just Jay Powell and Mario Draghi on its side. Since neither of them has any idea what’s going on, I’m not sure other than stocks there is much to think that they’ll get the response right even eventually. Fed funds at 240 bps didn’t break China, nor did trade wars (though they haven’t helped).

In other words, what we are seeing are the variable economic effects of Euro$ #4 just now picking apart the global economy. The Federal Reserve is as much a bystander to it as it was in Euro$’s #1, 2 and 3. The FOMC bungled all those, too, but now it suddenly transforms into an effective, honest bureaucratic machine?

Financial writer Bill Holter and renowned gold and financial expert Jim Sinclair warned last summer there were big problems coming in the global financial system. Today, Sinclair says, “We destroyed everything. We not only destroyed the financial markets, we destroyed society. I’m going for June of this year. The reset button gets reset after a few days of a flash crash that can’t be stopped. We’re flash crashing to hell, piece by piece by piece, until all of a sudden, the motion of the entity cannot be stopped.”

Holter says, “I think President Trump is going to preside over a bankruptcy. He’s gone through bankruptcies with his own companies and understands the process. That’s what this is. It’s the bankruptcy of the corporation of the United States.”

Sinclair adds, “Much of Trump’s business career is in bankruptcy, and he has used it as an asset quite successfully.”

Holter also points out, “Paul Volker, when he was Chairman of the Fed, was able to raise rates and able to tighten the money supply. He was able to create a deep recession. The reason he was able to do that was the country, corporations, individuals and the federal government itself was not over-leveraged in 1980 to the extent it is today. The over-leverage is everywhere today. If Paul Volker came in today and tried to do what he did back in 1979 and 1980, all you would see for markets and the economy is one big black smoking hole. You would have the entire system come down.”

Sinclair warns, “If Bill and I were standing on a street corner as preachers, our sign would read not ‘the end is near.’ Our sign would read, ‘it ended.’”

Sinclair goes on to say, “The flash crash to hell has started because the U.S. dollar is only up for one reason. It’s only up because there is a synthetic short.”

Holter adds, “And if you look at the dollar chart, it is rolling over. The next big move in the dollar is down, which also tells you the next move in any asset priced in dollars is going to cost more dollars because the dollar will weaken dramatically.”

In closing, Sinclair says, “The dollar standard is over. We were on a gold standard, and then poof, Nixon, and out. What has happened to the petro-dollar? Poof, it’s out in comparison to what it was. What system is next? The marbles standard? Gold is going back . . . to a store house of value.”

Join Greg Hunter as he goes One-on-One with Jim Sinclair and Bill Holter of JSMineset.com.

-END-

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.7422/

//OFFSHORE YUAN: 6.7802 /shanghai bourse CLOSED /CHINESE NEW YEAR FOR THE WEEK

HANG SANG CLOSED UP 59.47 POINTS OR .21%

2. Nikkei closed UP 95.38 POINTS OR 0.46%

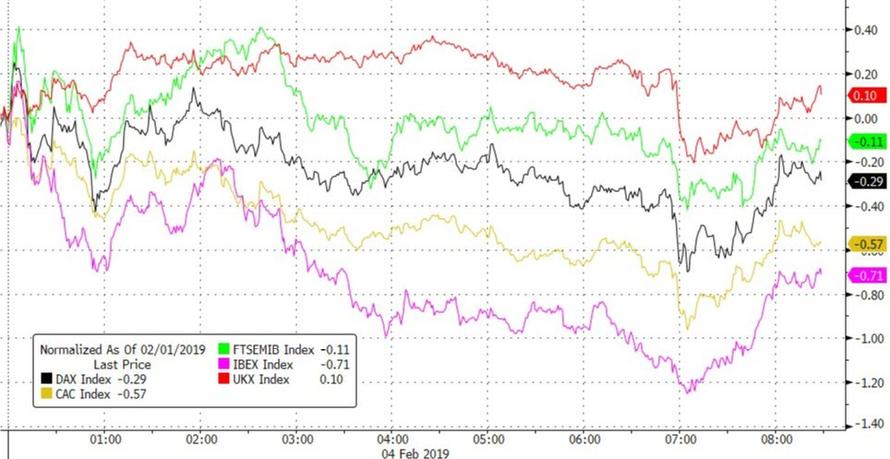

3. Europe stocks OPENED ALL RED EXCEPT LONDON

/USA dollar index RISES TO 95.71/Euro FALLS TO 1.1447

3b Japan 10 year bond yield: FALLS TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.92/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.06 and Brent: 62.70

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.16%/Italian 10 yr bond yield DOWN to 2.75% /SPAIN 10 YR BOND YIELD UP TO 1.23%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.59: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.91

3k Gold at $1310.90 silver at:15.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 8/100 in roubles/dollar) 65.47

3m oil into the 55 dollar handle for WTI and 62handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.89 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9975 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1418 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.16%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

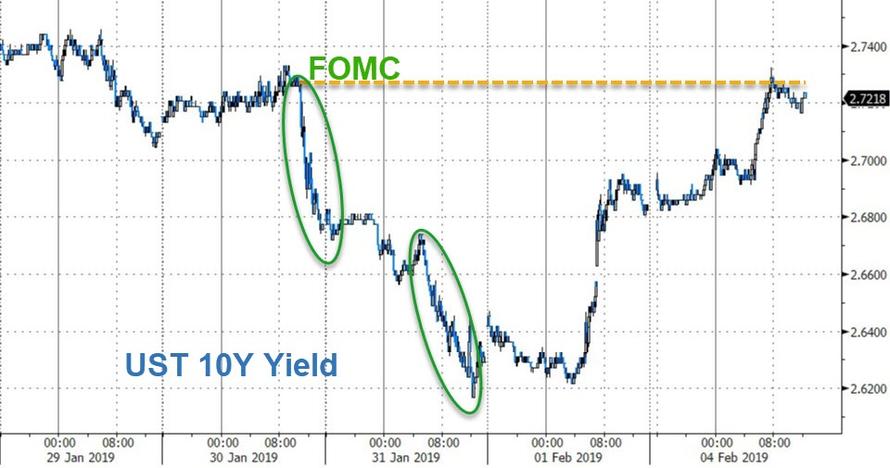

4. USA 10 year treasury bond at 2.70% early this morning. Thirty year rate at 3.049%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2105

Global Markets Flat With China On Weeklong Holiday; Dollar Rises

With much of the market action in recent weeks taking place during the overnight session, it is not a surprise that with China on a week-long Lunar New Year holiday, markets have been rather lethargic, with European bourses and US futures drifting without direction, if slightly lower following Friday’s inconclusive trade talks between the US and China as the dollar traded higher pressuring gold, while Treasury yields were slightly higher.

After a whirlwind week, that included a deluge of earnings, dovish Federal Reserve comments and U.S.-China trade talks in Washington, there is a notable lack of drivers for markets on Monday, particularly in Asia, where China is off and other markets will be shut for days.

US President Trump commented on Saturday that he expects to reach a trade agreement with China soon, while there were also reports that President Trump may meet with Chinese President Xi in Da Nang, Vietnam at the end of February. In related news, China state-owned Cofco Group said it purchased an additional 1 million tons of US soybeans

Investors may again look for direction from a corporate earnings season that’s been mixed so far and where Q1 earnings are now expected to post the first Y/Y decline in 3 years.

In Europe, the French CAC 40 and Germany’s DAX underperformed peers with autos weighing while oil and healthcare companies were the biggest gainers in the Stoxx 600 Index, offsetting declines in carmakers. The energy sector was the marked outperformer as Brent hovered around $63/bbl. In terms of laggards, material names are subdued following weak performances in some base metals during Asia-Pac trade. On the tech and consumer front, Japanese-listed Sony and Panasonic became the latest companies to issue a profit warning, following on from NDIVIA, Apple and Samsung, also citing a slowdown in China, however European tech names largely shrugged this off. The sector is kept afloat by DAX-listed Wirecard (+13.5%) after shares rebounded with a vengeance after an internal investigation into alleged criminal misconduct showed no conclusive findings. Elsewhere, UK-listed gambling names kicked off the week at the top of the Stoxx 600 following a number of positive broker moves at Jefferies, albeit William Hill (+0.4%) and Paddy Power Betfair (+0.4%) have since trimmed gains. Italian FTSE MIB manages small gains of +0.3%, while SMI’s Julius Baer (-4.6%) rested at the foot of the Swiss index amid disappointing earnings in which its CEO highlighted that a cost-to-income ratio of 68% is unlikely this year.

In Asia, trading was subdued as much of the region was closed headed into Lunar New Year holidays and following the indecisive performance in the US last Friday amid mixed employment data. Australia’s ASX 200 (+0.5%) was led higher by energy names and with optimism also seen in the largest weighted financials sector despite the looming Banking Royal Commission final report on the industry which was released after the close and referred 24 misconduct to regulators but did not suggest criminal charges. Nikkei 225 (+0.5%) was underpinned by favourable currency moves and a slew of earnings, but with Sony and Honda among the few notable underperformers after Sony reduced its revenue outlook and Honda posted a 34% drop in 9-month net. Elsewhere, Hang Seng (+0.2%) traded indecisive amid the absence of mainland participants all week and early closure in Hong Kong, while Chinese PMI data over the weekend was somewhat inconclusive in which Caixin Services PMI topped estimates but Caixin Composite PMI weakened from prior.

US equity futures were unchanged after the Dow, S&P 500 and Nasdaq all edged higher on Friday after better-than-expected U.S. jobs report overshadowed a disappointing sales forecast from Amazon. U.S. President Donald Trump told CBS that trade talks with Beijing are “doing very well” and sounded confident an agreement with North Korea was on the horizon. Brent crude set a fresh 2019 high as output fell.

In rates, BTPs rebounded from an early slump brushing off weekend warnings from ECB’s Visco. Gilts reverse a weak open to trade roughly flat, curve small steeper, helping Bunds off the lows. Money markets are betting that ECB policy makers will raise the benchmark deposit rate in only June 2020, compared with earlier expectations for a liftoff this year. That is spurring a rally in everything from benchmark German bonds to Belgian and Spanish debt securities. US Treasury futures grind sideways, 10Y yield steady just under 2.70%. Portuguese bonds look set to extend their peer- beating performance into 2019, after providing investors with the best returns among peripheral euro-area debt markets last year, according to Citigroup.

The currency market felt China’s absence due to the Lunar New Year holiday, with low volumes and tight ranges in the major currencies. The dollar advanced against most Group-of-10 peers while the yen led losses as better-than-expected U.S. data Friday made for a risk-on bias. Some highlights via Bloomberg:

The Bloomberg Dollar Spot Index headed for its longest winning streak in almost two weeks, boosted by a weaker yen, as solid U.S. economic data Friday set the tone at the start of the week

The euro was steady against the dollar, trading near 1.1450 after turo-zone February Sentix investor confidence fell to -3.7 vs est. -1.3

The pound touched a session low after IHS Markit’s gauge for the construction sector fell to 50.6 in January, from 52.8 in December, a markedly worse reading than the 52.5 forecast by economists; The British economy was dealt a blow from Nissan Motor over the weekend, which is ditching commitments to build a new vehicle model in the U.K., the latest company to make contingency plans against a no-deal Brexit scenario

Australia’s dollar fell against most of its Group-of-10 peers as an unexpected slide in building approvals raised the prospect that the central bank may adopt a more dovish tone this week.

Yen declined for a second day as local stocks rallied in risk-on sentiment, though trading was subdued as Lunar New Year holidays start in China

Canadian dollar led gains amid an advance in oil prices

The stronger dollar pressured gold which dropped 0.5% after hitting an 8 month high late last week.

Elsewhere, Venezuelans marched in dueling protests Saturday, with the two men who both claim to be the nation’s leader each exhorting followers to hold firm. The country’s outlook is being followed by oil traders given the country’s share of global exports. Emerging-market currencies and shares fell.

In other geopolitical news, President Putin said the US breached the INF arms treaty and that Russian will also suspend the treaty, while he is said to agree with Defense Ministry proposal to begin development of a mid-range supersonic missile. Turkey President Erdogan said Turkey and Syria have begun low level discussions.

In the latest Brexit news, PM May said she will seek a pragmatic solution regarding Brexit when she returns to Brussels and said she will be armed with a fresh mandate and new ideas. Additionally, UK PM May could be planning for a general election in June, according to reports; reports were later downplayed by Boris Johnson, according to Sky News. UK PM May has also invoked the support of Jeremy Corbyn to insist the EU must offer concessions on her Brexit deal, as she states that she will “battle for Britain” when she travels to Brussels to re-open negotiations. At the same time, UK Business Secretary Clark reportedly urged PM May to rule out a no-deal Brexit and told PM May that Nissan’s decision to cancel production of a new model in its Sunderland factory was a warning sign of what could occur to the UK car industry in the event of failing to reach an agreement.

Looking ahead, notable earnings include Alphabet (market cap of USD 780bln) and Gilead report Q4 earnings while economic data include durable goods, factory orders.

Market Snapshot

S&P 500 futures up 0.1% to 2,706.00

STOXX Europe 600 down 0.06% to 359.48

MXAP up 0.1% to 156.40

MXAPJ down 0.07% to 511.08

Nikkei up 0.5% to 20,883.77

Topix up 1.1% to 1,581.33

Hang Seng Index up 0.2% to 27,990.21

Shanghai Composite up 1.3% to 2,618.23

Sensex up 0.4% to 36,602.03

Australia S&P/ASX 200 up 0.5% to 5,891.20

Kospi down 0.06% to 2,203.46

German 10Y yield unchanged at 0.167%

Euro down 0.09% to $1.1446

Italian 10Y yield rose 15.6 bps to 2.389%

Spanish 10Y yield rose 0.9 bps to 1.232%

Brent Futures up 1.2% to $63.51/bbl

Gold spot down 0.5% to $1,311.22

U.S. Dollar Index up 0.2% to 95.73

Top Overnight News from Bloomberg

Money-market traders are braced for $134b of Treasury bills to be sold between Monday and Wednesday, followed by an additional dose on Thursday via the 4- and 8-week auctions

Two-thirds of Americans oppose President Donald Trump declaring a national emergency if Congress doesn’t offer up the funds he wants to build a wall on the U.S.-Mexican border, a CBS News poll released Sunday shows

Australian building approvals suffered the biggest annual back-to-back drop in almost a decade as a housing slump deepens. Falling unemployment is propping up households and allowing the economy to absorb a property slump, meaning the central bank can afford to stay on the sidelines — for now

Venezuelan President Nicolas Maduro went on Spanish television to denounce foreign meddling as U.S. President Trump signaled he’s confident a transition of power to opposition leader Juan Guaido is under way

Oil held near a two-month high after data showed U.S. production growth slowing at a time when OPEC cuts and American sanctions on Venezuela have already eased concerns over a supply glut

Wall Street firms are preparing to lobby China for changes that would make it easier to bet against its stock market through a trading link from Hong Kong

Federal Reserve Bank of Minneapolis President Neel Kashkari said Fed Chairman Jerome Powell is “coming around” to the view to wait until wages and inflation rise before raising interest rates again, and that the Fed’s latest pause will help keep a “fundamentally healthy” economy on track

Money-market traders are braced for $134b of Treasury bills to be sold between Monday and Wednesday, followed by an additional dose on Thursday via the 4- and 8-week auctions

ECB Governing Council member Ewald Nowotny doesn’t expect recession in Europe despite a lot of economic uncertainty, especially around the situation in Germany