GOLD: $1315.25 UP $0.30 (COMEX TO COMEX CLOSING)

Silver: $15.85 DOWN 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1315.20

silver: $15.85

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 319 NOTICE(S) FOR 31900 OZ (0.9922 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 8808 NOTICES FOR 880,800 OZ (27.396 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

106 NOTICE(S) FILED TODAY FOR 530,000 OZ/

total number of notices filed so far this month: 500 for 2,500,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3471: DOWN 1

Bitcoin: FINAL EVENING TRADE: $3464 UP $2

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 167/319

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,314.300000000 USD

INTENT DATE: 02/04/2019 DELIVERY DATE: 02/06/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

435 H SCOTIA CAPITAL 160

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 24

661 C JP MORGAN 71

661 H JP MORGAN 96

686 C INTL FCSTONE 1 3

690 C ABN AMRO 60 8

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 76 23

800 C MAREX SPEC 20 7

880 H CITIGROUP 86

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 319 319

MONTH TO DATE: 8,808

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A STRONG SIZED 2587 CONTRACTS FROM 206,692 UP TO 209,459 ACCOMPANYING YESTERDAY’S 4 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

512 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 512 CONTRACTS. WITH THE TRANSFER OF 512 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 512 EFP CONTRACTS TRANSLATES INTO 2.560 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.410 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 3975 CONTRACTS (FOR 4 TRADING DAYS TOTAL 3975 CONTRACTS) OR 19.875 MILLION OZ: (AVERAGE PER DAY: 994 CONTRACTS OR 4.968 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 19.875 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.83% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 237.33 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2587 WITH THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 512 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 3099 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 512 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2587 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.88 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.047 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 106 NOTICE(S) FOR 530,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.410 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A FAIR SIZED 1776 CONTRACTS DOWN TO 474,513 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $2.65//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 10,064 CONTRACTS:

MARCH HAD AN ISSUANCE OF 185 CONTACTS APRIL 9879 CONTRACTS, DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 474,513. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8286 CONTRACTS: 1362 OI CONTRACTS DECREASED AT THE COMEX AND 10,064 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 8286 CONTRACTS OR 828,600, OZ = 25.77 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.65.

YESTERDAY, WE HAD 6351 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 23,123 CONTRACTS OR 2,312,300 OZ OR 71.92 TONNES (4 TRADING DAYS AND THUS AVERAGING: 5780 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAYS IN TONNES: 71.92 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 71.92/2550 x 100% TONNES = 2.82% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,703.26 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 1776 WITH THE LOSS IN PRICING ($2.65) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,064 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,064 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 8672 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,064 CONTRACTS MOVE TO LONDON AND 1776 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 25.77 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $2.65 IN YESTERDAY’S TRADING AT THE COMEX

we had: 319 notice(s) filed upon for 31,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.30 TODAY

THE FRAUD CONTINUES:

A MASSIVE PAPER WITHDRAWAL OF 4.11 TONNES

/GLD INVENTORY 813.29 TONNES

Inventory rests tonight: 813.29 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 3 CENTS IN PRICE TODAY:

NO CHANGE IN INVENTORY AT THE SLV.

/INVENTORY RESTS AT 310.594 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 2587 CONTRACTS from 206,892 UP TO 209,459 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

512 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 512 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2587 CONTRACTS TO THE 512 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3099 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 15.49 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.410 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 4 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 512 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed DOWN 39.32 PTS OR 0.19%/ Australia’s all ordinaires CLOSED UP 1.76%

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 54.28 dollars per barrel for WTI and 62.11 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7651: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

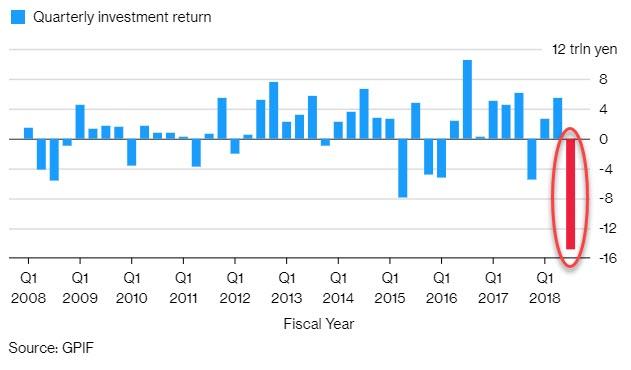

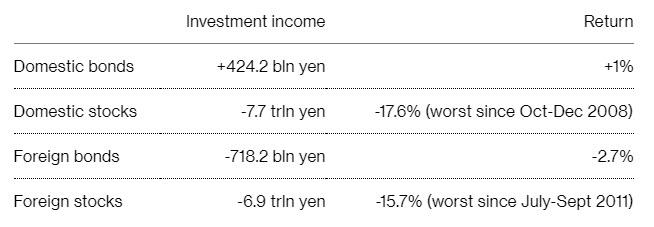

By goodness what a loss: in its 4th quarter, the largest Japanese Pension fund: GPIF lost 136 billion usa dollars in the last 3 months of the year with the downfall in stocks.

( zerohedge)

3 C/ CHINA

i) CHINA

Huawei lawyers in Canada are fighting the USA’s “politically motivated” prosecution in order to win her freedom. Although the bar is low, she may win on this;

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

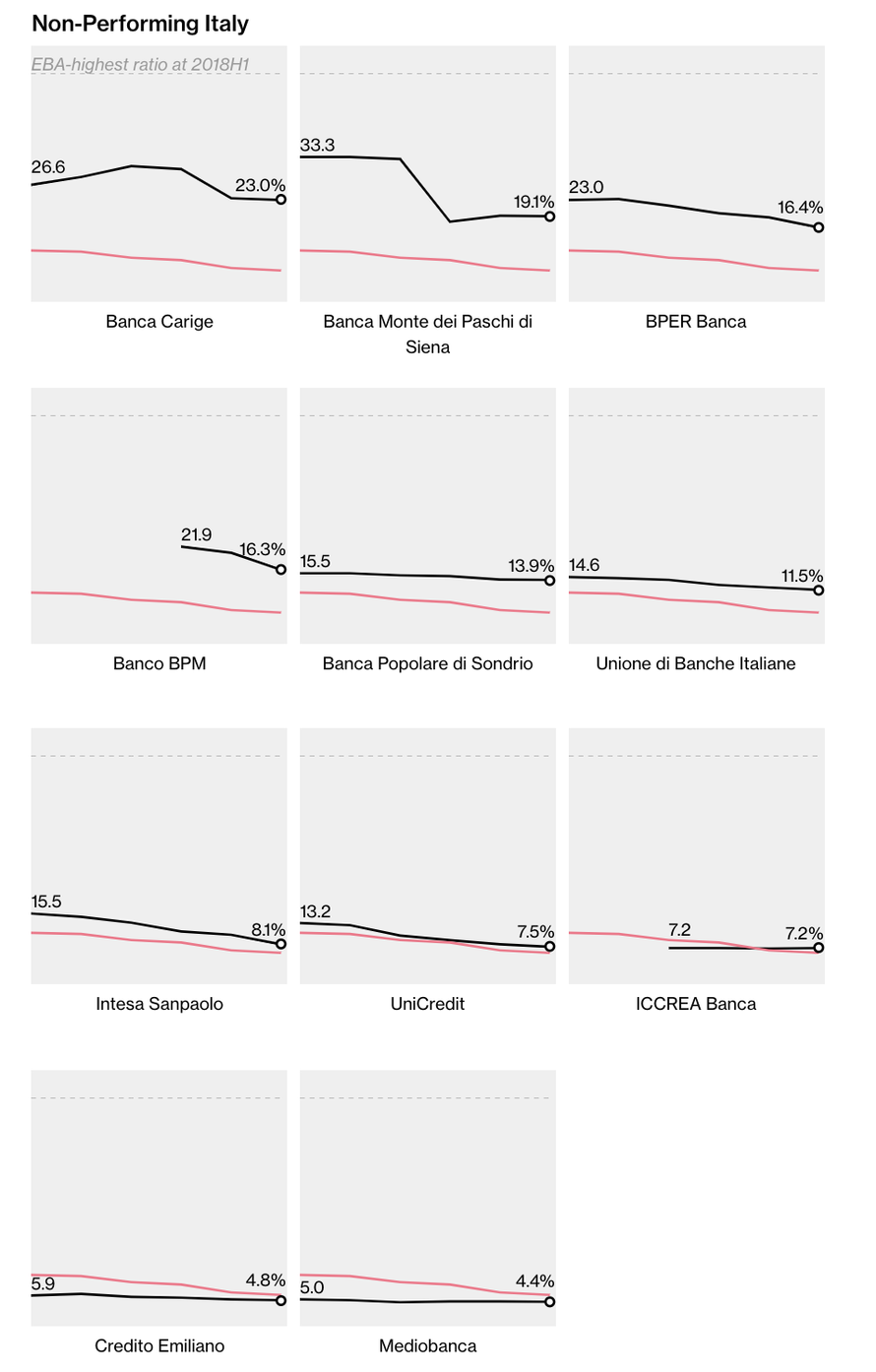

italy

Italy has one of the highest debts in Europe at 1.5 trillion euros or 1.7 trillion uSA dollars. An Italian debt crisis would take down the entire EU

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Trump continues to show his allegiance to Israel as he shows his support to AIPAC

( Tom Luongo)

ii)Turkey

6. GLOBAL ISSUES

This is very good news: Trump is set to hire Dr David Malpass, a strong gold bug to lead the World Bank. Something must be up as he is also set to nominate Dr Judy Shelton to the Fed board

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

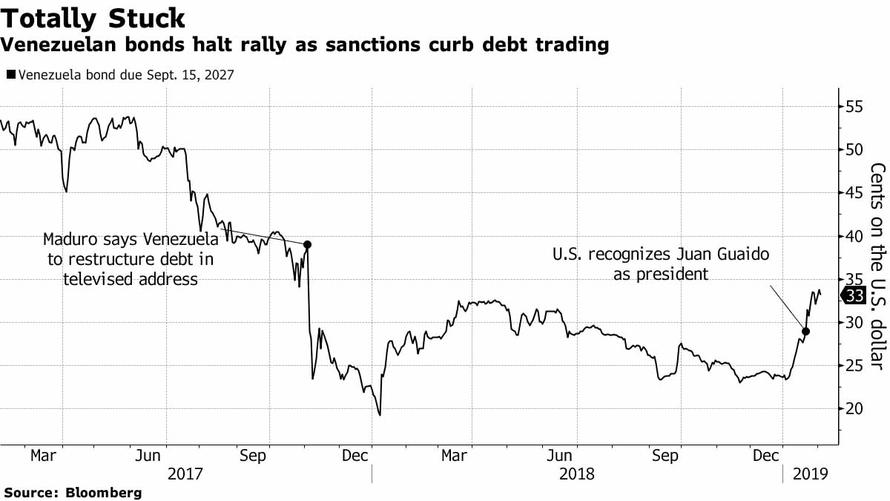

i)VENEZUELA/USA

a)Trading in sovereign Venezuela bonds have dried to zero after the Trump sanctions

( zerohedge)

b)More trouble for Maduro has a flotilla of Venezuelan oil tankers are stranded off the Gulf of Mexico

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

Even though the January PMI manufacturing rose, the usually stronger USA service PMI plunged led by new orders

( zerohedge

a)Interesting: Trump and Powell met for an informal dinner and details emerge that Powell will maintain his dovish position on interest rate hikes/balance sheet roll-offs

( zerohedge)

b)Once the uSA experiences a downturn, it will be the huge BBB corporate debt group will will cause the implosion of uSA finances.

( John Rubino/DollarCollapse,com)

c)Why the left vilifies Tulsi Gabbard..as she reveals the bankruptcy of the American left

iv)SWAMP STORIES

a)The Trump Inaugural committee has been subpoenaed by New York Prosecutors (Democrats) to see if they misspent some of their $107 million dollars received in donations.

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 2327 CONTRACTS DOWN TO 138,000 CONTRACTS. AFTER MARCH, APRIL ROSE FROM ITS INITIAL 15 OPEN INTEREST CONTRACTS BY 2 CONTRACTS TO STAND AT 17. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 4395 CONTRACTS UP TO 39,193 CONTRACTS.

FOR COMPARISON SILVER COMEX CONTRACT MONTH FEB 2018 VS FEB 2019

ON FIRST DAY NOTICE FEB 1/2018 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

TODAY THE INITIAL AMOUNT OF SILVER STANDING IS 2.050 MILLION OZ./

“Right” Trump and “Left” Ocasio-Cortez Will Join Forces And Debase The Dollar

– Intellectuals are laying the groundwork for “a tower of debt higher than any ever seen in world history”

– Alexandria Ocasio-Cortez (AOC) and Donald J Trump (DJT) will soon be on the same side by coming to love massive debt, “$2-trillion federal deficits,” ultra loose monetary policies and the debasement of the dollar

– Beyond “good and evil” and moving to “dumb and dumber” monetary and economic policies may see dollar go the way of bolívars in Venezuela today

by Bill Bonner via Bonner & Partners

The intellectuals are laying the groundwork.

That is, they’re digging the foundations for an extraordinary structure – a tower of debt higher than any ever seen in world history.

The primary architect? Paul Krugman? Jerome Powell? Joseph Stiglitz?

Nope. Not an architect at all… but a politician.

Low-Interest People

It’s none other than Alexandria Ocasio-Cortez (AOC), the ambitious young representative of New York’s 14th district, who has the shovel in her hands.

She may be the youngest woman ever elected to Congress, but she wasn’t born yesterday. And she may not know any more about economics than Donald J. Trump. But she knows a winning trend when she sees one.

And circa 2019, debt is becoming more popular than internet hook-ups.

Our dear readers generally approve when we poke fun at liberals like Ms. Ocasio-Cortez. But they hate it when we talk smack about the president. Many see the contest in Washington as a fight between good and evil. And they know what side they’re on!

We predict, however, that AOC and DJT will soon be on the same side. Beyond good and evil. Just dumb.

Both are already “low-interest kind of people.” And when the going gets tough, both will come to love Modern Monetary Theory, MMT… and $2-trillion federal deficits.

Silly Duffers

One of our dicta here at the Diary: People come to think what they have to think when they have to think it. Markets make opinions, in other words, not the other way around.

And markets are running into trouble. The trends that were so felicitous for so long – falling interest rates and rising stock prices – have now stalled, or even reversed.

The private sector faces a recession. Wall Street sees a bear market coming. In Washington, tax receipts will fall… as costs continue to rise.

How to keep the jig up? The politicians – left, right, and center – will come to see: debt isn’t so bad!

What were those previous generations thinking, they will wonder? Scrimping and saving, balancing budgets, making trade-offs – and for what? The silly duffers didn’t know any better.

The intellectual drift in favor of more government debt was put forward this week in the pages of the “pink paper,” the Financial Times:

A government can issue debt to pay for whatever it likes. It can pay to fight a war, to lower taxes for a preferred group, to soften the sharp edges of a recession. The United States has, in fact, issued debt to pay for all of these things. American politicians say that public debt crowds out private investment, that it’s unsustainable and will turn the country into Argentina. Or Greece. Or now, Venezuela. But regardless of what they say, what American politicians do is vote for more debt.

The FT is right about that. Year in, year out… boom or bust… Democrat or Republican – they voted for more debt. Modern Monetary Theory is at least realistic about it.

Noting that politicians are not shy about going into debt – without any horrible consequences; not recently, at any rate – the MMTers fantasize about a world in which government can get as much money as it pleases. Debt shouldn’t be a limitation.

A government issues money, they reason. Why does it have to borrow at all?

This seemed like such a breath of fresh monetary air that many economists and politicians practically hyperventilated. Here was a theory that seemed to validate a widespread practice – spending more than you earn. It was the feds’ money to begin with; why shouldn’t they spend as much as they want?

Ms. AOC is often posed the question directly. She favors free universities, free healthcare, free this, free that – “How can we afford it?” ask skeptics.

But she’s ready with the MMT answer: “How do we pay for anything?”

Touché!

“We” don’t pay for anything. The feds pay… with resources that – one way or another – they’ve squeezed out of us. In theory, it doesn’t matter how they get it. Debt. Taxes. Inflation. Take your pick.

Chartalist System

What really counts is the total amount of resources the feds take. The more they squander, the less is left for real output and growth. And the practical advantage of debt over inflation (just printing money) is that it limits the take.

Borrowed money has a cost. The more the feds borrow, the higher interest rates go. Then, the economy slumps… tax revenues decline… and the feds are worse off than ever.

Then, of course, the feds finagle a fix, getting the central bank – the Fed – to buy up their debt, so interest rates don’t go up. This ends up being very close to a pure MMT or Chartalist system, where the feds are, in effect, printing the money to pay for their quack programs.

But the central insight of MMT is deeply flawed. It confuses the feds’ “money” with real money.

MMT admits that their spending is limited only by the resources available in the real world. But that is why we have real money in the first place – to make sure the limits are respected.

Fake money only works for as long as it mimics real money; that is, only so long as it respects the limits of real resources. After all, a car is not a car because the feds say it’s a car; it’s a car because it takes you where you want to go.

And as soon as the feds’ money stops taking you where you want to go – like Zim dollars in Zimbabwe in 2006 or bolívars in Venezuela today – MMT falls apart. The feds could “print” all they wanted; it wouldn’t buy them a ham sandwich.

Fortunately, the U.S. dollar still has some miles left on it. But with politicians like AOC and DJT at the wheel, it’s just a matter of time before the limits come off… and it ends up in a ditch.

Sign up for only daily newsletter featuring the unique ideas of bestselling financial author Bill Bonner. From Wall Street to Washington, Bill leaves no idol un-busted and no stone unturned…

News and Commentary

Gold posts second loss in a row, but analysts see higher prices ahead (MarketWatch.com)

Gold slips as dollar gains as China closed for Lunar New Year (Reuters.com)

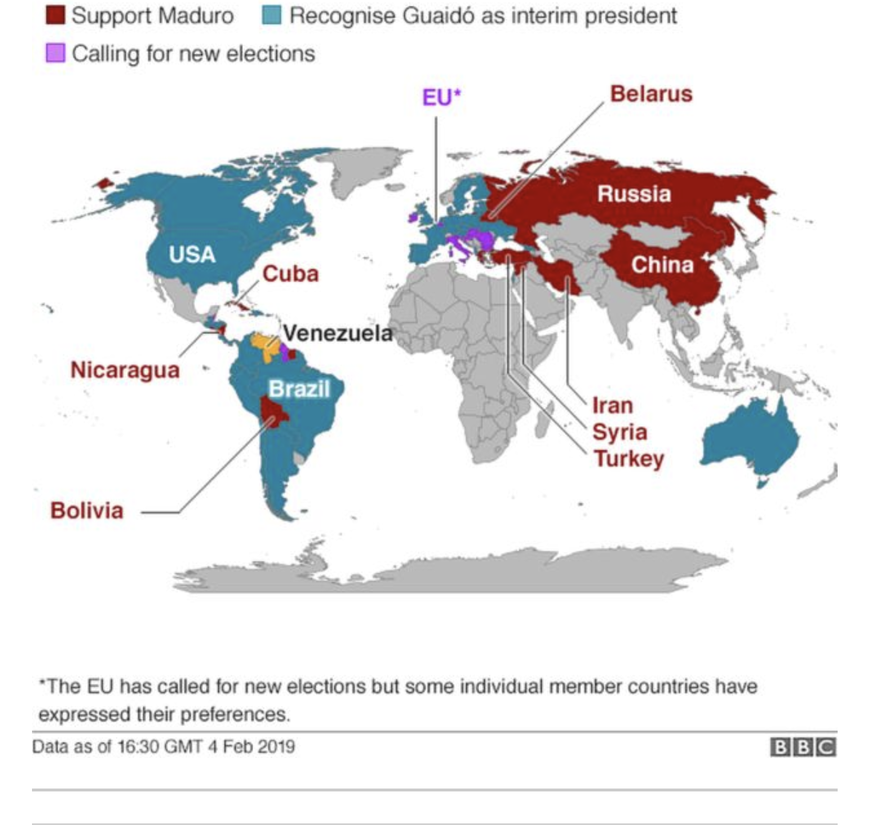

Major European nations recognize Guaido as Venezuela president (Reuters.com)

Asahi to emerge as largest gold, silver refiner in US after Republic acquisition (SPGlobal.com)

Why Italy’s Debts Are Europe’s Big Problem. Source: Bloomberg

Why Italy’s Debts Are Europe’s Big Problem (Bloomberg.com)

World Bank And IMF Are In Crisis. It’s Time To Push A Radical New Vision (TheGuardian.com)

Rickards: “The Plan To Ditch King Dollar” (DailyReckoning.com)

Turtles All the Way Down – Hussman (HussmanFunds.com)

New-Age Precious Metals Investor: The Coming Pension Fund Disaster (SRSRoccoReport.com)

Can the U.S. and China Avoid War? Kyle Bass Interview (RealVision.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

04 Feb: USD 1,311.00, GBP 1004.36 & EUR 1,145.55 per ounce

01 Feb: USD 1,320.75, GBP 1008.54 & EUR 1,150.83 per ounce

31 Jan: USD 1,322.50, GBP 1006.95 & EUR 1,152.16 per ounce

30 Jan: USD 1,312.95, GBP 1002.04 & EUR 1,148.44 per ounce

29 Jan: USD 1,308.35, GBP 994.48 & EUR 1,143.24 per ounce

28 Jan: USD 1,301.00, GBP 987.98 & EUR 1,139.81 per ounce

25 Jan: USD 1,282.95, GBP 981.33 & EUR 1,132.08 per ounce

Silver Prices (LBMA)

04 Feb: USD 15.74, GBP 12.05 & EUR 13.75 per ounce

01 Feb: USD 16.01, GBP 12.26 & EUR 13.96 per ounce

31 Jan: USD 16.07, GBP 12.24 & EUR 13.99 per ounce

30 Jan: USD 15.91, GBP 12.15 & EUR 13.92 per ounce

29 Jan: USD 15.85, GBP 12.05 & EUR 13.87 per ounce

28 Jan: USD 15.68, GBP 11.93 & EUR 13.75 per ounce

25 Jan: USD 15.37, GBP 11.74 & EUR 13.55 per ounce

Recent Market Updates

– 7 Financial Truths In An Uncertain 2019

– Central Banks Buy More Gold In 2018 Than Any Year Since 1967

– Gold Breaks Out of Range After Dovish Fed – Further 1% Gain to $1,321/oz

– U.S.-China War May Be “Just A Shot Away”

– Buy Bitcoin or Gold? Bitcoin Buyers Investing In Gold In 2019

– Gold Consolidates Above $1,300 After 1.2% Gain Last Week

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

New York Sun: Trump’s ideal nominee for the Fed

Submitted by cpowell on Mon, 2019-02-04 18:39. Section: Daily Dispatches

From The New York Sun

Monday, February 4, 2019

It looks like this could be the moment at which President Trump makes his move in respect of the Federal Reserve. We say that because the chatter we hear is that he’s considering nominating to its board of governors the economist Judy Shelton. The Sun endorses her heartily. It would mark a brilliant start to redeeming his campaign promises in respect of monetary policy and our central bank.

Ms. Shelton is no stranger to readers of Sun editorials — or the editorial page of The Wall Street Journal. She has long since emerged as one of the most articulate, but measured, advocates of the idea that our economic troubles spring in large part, if not exclusively, from the fiat nature of our currency. And that we need to bring back into our political economy the idea of sound money. …

… For the remainder of the commentary:

https://www.nysun.com/editorials/trumps-ideal-nominee-for-the-fed/90559/

end

Congressman Mooney demands that the CFTC answer our questions re gold/silver market rigging

a must read..

(courtesy MoneyMetals.com/GATA)

Answer GATA’s questions on gold market rigging, congressman tells CFTC

Submitted by cpowell on Tue, 2019-02-05 21:13. Section: Daily Dispatches

Congressman Demands CFTC Explain Its Failure to Find Silver Market Manipulation Where Justice Department Did

From Money Metals News Service, Eagle, Idaho

Tuesday, February 5, 2019

https://www.moneymetals.com/news/2019/02/05/cftc-silver-market-manipulat…

WASHINGTON — A member of the U.S. House Financial Services Committee today pressed the Commodities Futures Trading Commission on its conspicuous failure to uncover the very silver market manipulation now being prosecuted by the U.S. Department of Justice.

In a probing letter dated today to CFTC Chairman J. Christopher Giancarlo, Rep. Alex X. Mooney, R-West Virginia, writes:

“The U.S. Justice Department obtained a guilty plea from a former commodities trader for JPMorganChase & Co. to charges of manipulating the gold and silver markets between 2009 and 2015, and its investigation into the actions of related parties is ongoing.

The period at issue substantially overlaps the time during which your commission was investigating complaints of manipulation of the silver market — 2008 to 2013. However, in 2013 the commission announced that it had closed its investigation without finding any wrongdoing.

“Why did the commission fail to find the wrongdoing the Justice Department has confirmed and continues to investigate? Also, will the commission now be re-opening its investigation into silver market manipulation and opening an investigation into gold market manipulation? If not, why not?”

Meanwhile, Rep. Mooney asks about the CFTC’s recent refusal to answer questions posed by a non-profit watchdog group called the Gold Anti-Trust Action Committee (GATA) that investigates government interventions in gold and silver markets:

Rep. Mooney’s letter seeks answers from the CFTC about its apparent reporting discrepancies, the unusual correlation between the Chinese yuan and the gold price, and whether the CFTC believes it has jurisdiction over gold market trading by the U.S. government or foreign governments.

“Congressman Mooney understands that a lack of transparency in the gold and silver markets not only undermines confidence, but also enables governments and powerful financial interests to manipulate currencies and asset prices to Americans’ great detriment,” said Jp Cortez, policy director for the Sound Money Defense League.

“Gold and silver are true money, and the CFTC has a responsibility to expose and punish those who seek to secretly manipulate its value.”

Rep. Mooney’s letter to CFTC Chairman J. Christopher Giancarlo can be accessed here:

http://gata.org/files/MooneyLetterToCFTC-02-05-2019.pdf

The Sound Money Defense League is a public policy group working nationally to bring back gold and silver as America’s constitutional money. The group also maintains America’s Sound Money Index.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

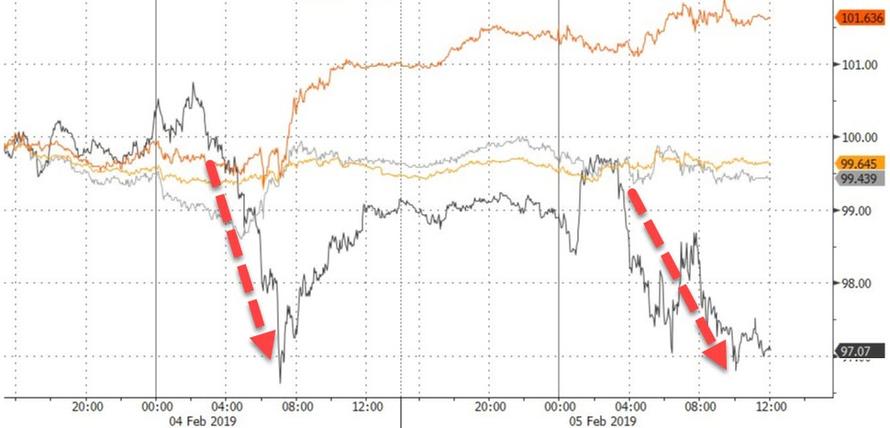

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7422/

//OFFSHORE YUAN: 6.7651 /shanghai bourse CLOSED /CHINESE NEW YEAR FOR THE WEEK

HANG SANG CLOSED

2. Nikkei closed DOWN 39.32 POINTS OR 0.19%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 95.93/Euro FALLS TO 1.1422

3b Japan 10 year bond yield: FALLS TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109/93/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.28 and Brent: 62.11

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.20%/Italian 10 yr bond yield DOWN to 2.76% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.56: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.89

3k Gold at $1313.70 silver at:15.84 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 8/100 in roubles/dollar) 65.49

3m oil into the 54 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.95 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0012 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1434 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.20%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.73% early this morning. Thirty year rate at 3.07%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2016

Global Stocks Hit 2 Month High On Muted Levitation, Iron Ore Soars

Despite yesterday’s disappointing Google results, which saw the search giant beat estimates but its stock slump as investors were concerned by surging costs and expenses, global stocks extended their red hot start to 2019, hitting a 2 month high, boosted by Europe’s miners and banks while the dollar gained for a fourth day as traders waited for U.S. President Donald Trump’s State of the Union address following news the president had unexpectedly had dinner with Fed Chair Powell and Vice Chairs Clarida.

After initially dipping, S&P futures gradually turned higher on Tuesday, tracking shares in Europe where the Stoxx 600 Index headed for the sixth advance in a row, even as chip suppliers Infineon Technologies and AMS issued warnings about future growth, boosted by strong earnings from oil giant BP, which reported that its profits had doubled, while another move higher in crude prices overnight pushed the oil and gas sector up 1.5%. Also helping were euro area PMIs, which were revised slightly upward. Still, the common currency was lower as disappointing data from Italy hung over the region. Sterling fell slightly following a weak services report.

Miners were also up sharply as traders reacted to news that Brazil had ordered Vale, the world’s largest iron ore miner, to close eight of its dams following a deadly collapse that killed over 300 people last month. As a result, iron ore prices continued their surge and are now at a near 2-year high.

“Our fundamental view is there no reason for this incredible move, so is it just speculation, a frenzy about possible stimulus in China?,” said Saxo Bank’s head of FX Strategy John Hardy. “What should we do with it? I don’t know, but it should be noted.”

In Asia, the overnight session remained muted as China and large parts of Asia were closed for Lunar New Year celebrations overnight but what markets were open continued to push higher. Japan’s Nikkei marked its highest level in seven weeks at one point before fading to finish slightly lower. Australian shares suffered no such fatigue, jumping 2%, with long-battered financials surging on short-covering after a special government-appointed misconduct inquiry left the structure of the country’s powerful banks in place, while the RBA kept the Cash Rate Target unchanged at 1.50% as expected while reiterating that low rates are supporting the economy and that progress on inflation and unemployment is expected to be gradual. Furthermore, the RBA noted that the labour market remains strong and that it sees a gradual inflation pick up over next couple of years but added that the central scenario for GDP growth is to average around 3% this year and to slow in 2020 vs. Prev. forecast of around 3.5% growth for the next 2 years back at the December meeting.

With Europe continuing to rally, the MSCI index of global stocks reached a two-month high, after enjoying its best January on record, rising more than 13% from a near two-year low hit in late December.

On Wall Street, the S&P 500 gained on Monday, with technology and industrials the biggest winners, 100-day moving averages sliced through and the VIX dropping to its lowest in four months. As noted earlier, the Fed took the unusual step of issuing a statement on Monday saying that its head Jerome Powell had told President Donald Trump and Treasury Secretary Steven Mnuchin that “the path of policy will depend entirely on incoming economic information.”

In the currency markets, the dollar fluctuated and was trading unchanged following recent gains against its major peers as investors continued to weigh last Friday’s strong payrolls number offset by disappointing production and capex data. The Bloomberg Dollar index was steady, holding a three-day advance; U.S. and European sovereign yield curves bear steepened with Treasuries outperforming Bunds. The euro edged lower, touching a day low versus the dollar after weak PMIs out of Italy and France.

Cable dropped 0.2% to a 1.3013 day low after the worse-than-forecast U.K. services PMI data. The krona slipped against all G-10 peers apart from the Swiss franc, with the Swedish currency touching a day low after services and composite PMIs slipped in January; USD/CHF rose to 1.0011, an 11-week high

The Australian dollar gained 0.5% to $0.7260, erasing earlier losses amid short covering, after the Reserve Bank of Australia left policy unchanged at its first meeting this year but sounded less dovish than the markets had expected. The Aussie had earlier fallen fell as much as 0.5 percent after a slump in retail sales reinforced concerns about the health of the economy.

Traders will next focus on today’s main event, President Donald Trump’s delayed State of the Union address, due at 2100 ET Tuesday as well as U.S. ISM non-manufacturing figures, also due later in the day. Trump told a White House event over the weekend that he might declare a national “emergency” because Democrats in Congress weren’t moving toward a deal to provide money to build a wall on the border with Mexico. Such a step would likely prompt a court challenge from Democrats.

“If President Trump persists in his long-promised wall along the U.S.-Mexico border in the upcoming address, it would cap the dollar’s rally,” said Kengo Suzuki, chief FX strategist at Mizuho Securities.

Also late on Monday, Trump’s inaugural committee said it received a subpoena for documents. Elsewhere, there were separate reports that US Rep. Neal is building a case to subpoena US President Trump’s tax returns.

In Brexit news, Europe’s top official offered Britain a legal guarantee that it would not be trapped by the Irish backstop last night but was swiftly rejected by Brexiteer MPs. As a reminder, UK PM May is heading to Northern Ireland in a bid to salvage her Brexit deal by finding an alternative to the “toxic” backstop proposal. UK Ministers are secretly planning to unilaterally cut tariffs on all imports to zero in the event of a no-deal Brexit, in a move that could flood the market with cheap goods and “ruin” industry, according to a HuffPost UK exclusive.

In geopolitical news, the UN sanctions monitor report said North Korea nuclear and ballistic missile program remains intact and that North Korea is working to protect those capabilities from military strikes. Furthermore, it added that North Korea is violating UN arms embargo and is breaching sanctions through illegal ship-to-ship transfers of petroleum products and coal.

Elsewhere, West Texas oil climbed as traders weighed output cuts from the OPEC producer group and its partners against expectations for rising U.S. crude inventories. Emerging-market shares and currencies drifted. Looking at today’s key events, President Trump will deliver a delayed State of the Union address. Scheduled earnings include Disney, Suncor Energy, Estee Lauder.

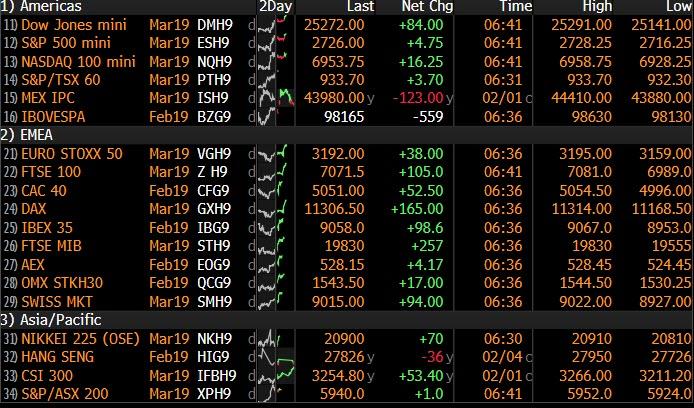

Market Snapshot

- S&P 500 futures up 0.1% to 2,724.00

- STOXX Europe 600 up 0.8% to 362.64

- MXAP up 0.3% to 156.79

- MXAPJ up 0.4% to 513.34

- Nikkei down 0.2% to 20,844.45

- Topix up 0.1% to 1,582.88

- Hang Seng Index up 0.2% to 27,990.21

- Shanghai Composite up 1.3% to 2,618.23

- Sensex up 0.2% to 36,657.21

- Australia S&P/ASX 200 up 2% to 6,005.92

- Kospi down 0.06% to 2,203.46

- German 10Y yield rose 2.1 bps to 0.198%

- Euro down 0.2% to $1.1417

- Brent Futures up 0.5% to $62.85/bbl

- Italian 10Y yield fell 1.3 bps to 2.376%

- Spanish 10Y yield rose 0.2 bps to 1.246%

- Brent Futures up 0.5% to $62.85/bbl

- Gold spot down 0.06% to $1,311.47

- U.S. Dollar Index up 0.1% to 95.96

Top Overnight News from BBG

- Trump’s inaugural committee is under scrutiny by federal prosecutors in New York, adding new legal woes for the president and his allies that stretch beyond the probe led by Special Counsel Robert Mueller

- The president’s second State of the Union promises to be one of the most dramatic moments in recent memory for the annual address to Congress. The appearance will be shadowed by the threat of another government shutdown, and he has hinted that he may make news — a national emergency declaration on the U.S. southern border, a proposal on drug prices or on AIDS, or dates and locations for summits with the leaders of China and North Korea

- The U.K.’s dominant services sector barely grew in January, bringing the economy to a near- halt. Companies said they were less likely to start new projects and that clients were spending more cautiously because of a lack of clarity around Brexit

- Danuta Huebner, head of the European Parliament’s constitutional-affairs committee, said the prospect of a U.K. withdrawal from the EU on March 29 without a divorce agreement is so alarming that Britain’s partners in the bloc would seriously consider a later date for departure to ensure it took place in an orderly fashion

- A manufacturing and export-led slump in Italy’s economy spilled into services at the start of the year, aggravating an already fragile economic situation in the euro area. Business activity among Italian services providers shrank in January and forced companies to reduce headcount for the first time in more than two years

Asia-Pac equity markets found some early support from the tech-led gains on Wall St, although later turned somewhat mixed amid focus on earnings and with most the region shut for the Lunar New Year. Nonetheless, ASX 200 (+2.0%) was the stellar performer due to strength in its largest weighted financials sector as banks seemingly made light of the Banking Royal Commission final report regarding misconduct in the industry. As such, Australia’s banking powerhouses all edged firm gains in the aftermath of the report which recommended against structural separation and referred 24 misconduct cases to regulators but did not suggest criminal charges, while many viewed the report as unlikely to result in fundamental reforms for the industry in the long-term and Moody’s also noted that the recommendations will likely preserve profitability in the industry. Nikkei 225 (-0.2%) shrugged off opening gains and traded flat as earnings remained the main driver for price action in Tokyo after Panasonic cut its outlook, while Yahoo Japan outperformed following an upward revision to its FY giudance. Finally, 10yr JGBs were initially pressured as they followed suit to the recent downside in T-notes, although prices later rebounded following the 10yr auction in which the b/c and accepted prices increased from prior, while the average yield slipped to negative territory. The RBA kept the Cash Rate Target unchanged at 1.50% as expected. The RBA reiterated that low rates are supporting the economy and that progress on inflation and unemployment is expected to be gradual. Furthermore, the RBA noted that the labour market remains strong and that it sees a gradual inflation pick up over next couple of years but added that the central scenario for GDP growth is to average around 3% this year and to slow in 2020 vs. Prev. forecast of around 3.5% growth for the next 2 years back at the December meeting

Top Asia News

- RBA Leaves Key Rate at 1.5% as Seen by All 32 Economists

- Polls Not a Risk to India’s Growth, Focus on Investment: SocGen

- Tycoons on the Run to Play Pivotal Role in World’s Largest Vote

- Overseas Funds Sour on Indian Bonds as Budget Math Weighs

- Norinchukin Bank Added 3 Trillion Yen of CDOs Since March

An upbeat session for European equities thus far following on from a holiday-thinned Asia-Pac session as the region is fuelled by a number of large-cap earnings. Major indices extended on opening gains and are firmly in positive territory (Euro Stoxx 50 +1.0%) with Britain’s FTSE 100 (+1.4%) leading the advances amid upbeat earnings from heavyweight BP (+5.2%), wherein the oil-giant beat on adjusted net and revenue forecasts while also expecting higher underlying production and lower refining margins this fiscal year. Sectors are experiencing broad-based gains with the energy sector the marked outperformer as earnings from BP lifts the likes of Royal Dutch Shell (+1.7%) and Total (+1.6%) in sympathy. Elsewhere, the tech sector is largely resilient to a guidance cut from AMS (-13.2%), as the rebound in Wirecard (+6.5%) keeps the sector afloat. Meanwhile, Infineon (-0.3%) numbers printed largely in-line, though the company now expects 2019 revenue growth to be at the bottom end of the forecast range. Finally, Indivior (-11.4%) shares fell as much as 24% at the EU open after the US Federal Court rejected its appeal for another hearing regarding patent infringement by a low-cost copycat drug developed by Dr Reddy.

Top European News

- Services Bring U.K. Economy to Near-Halt as Brexit Approaches

- Italy’s Broadening Slump Weighs Down the Euro-Area Economy

- Panalpina Shareholders May Want to Exit Long Positions: Stifel

- Salvini’s League Rises to 33.8% in SWG Poll; Five Star Declines

In FX, although the USD is mixed vs major currency rivals, the index has inched a bit closer to the 96.000 mark, largely by virtue of the aforementioned Eur/Usd decline and that pair’s biggest weighting in the basket.

- AUD was the top G10 performer after a sharp turnaround in fortunes overnight, as the Aussie recovered impressively from sub-0.7200 lows vs the Usd and circa 1.0455 vs the Nzd in wake of a less dovish than many anticipated RBA policy statement. This, despite yet more disappointing data in the form of retail sales and downgrades to the outlook for growth in 2019 and 2020. Aud/Usd is now back up near 0.7250 and Aud/Nzd has rebounded over 1.0500+.

- CHF – The Franc has extended recent losses vs the Greenback and just traded down through parity amidst broadly risk on trade highlighted by broad EU equity market gains, and the Chf seemingly taking some of the strain from the Jpy that has rebounded from 110.00+ vs the Usd.

- EUR/GBP – Both on the back foot vs the Dollar and inching closer towards downside big figures at 1.1400 and 1.3000 respectively. The single currency tested bids around 1.1410 before gleaning some traction from a firmer than flash pan-Eurozone services PMI as sub-50.00 Italian and French prints were offset by more encouraging Spanish and German surveys (in headline terms at least). However, Eur/Usd remains precarious below several daily chart levels and just above decent option expiries between 1.1400-10 (1.1 bn). Conversely, Cable has now breached the 200 DMA (around 1.3038) following a 3rd and most worrying UK PMI miss given the importance of services to overall GDP. The Pound is holding just above late January lows, while Eur/Gbp has rebounded towards recent peaks not far from 0.8800.

- CAD – The Loonie continues track moves in crude prices and is back on the front foot vs its US counterpart having rebounded above the 200 DMA (1.3130) and retesting chart/psychological resistance at 1.3100.

In commodities, a relatively choppy session for the oil market as earlier losses were nursed after a muted Asia-Pac trade. WTI (+1.1%) and Brent (+0.7%) edged higher in recent trade amid the overall market risk-appetite wherein the former reclaimed USD 53/bbl, while the latter hovers around the USD 63/bbl level. News flow has been light for the complex with participants awaiting the release of the weekly API crude inventories for a further catalyst. Elsewhere, metals have been mixed with spot gold (+0.1%) largely moving in tandem with the buck, meanwhile copper is outperforming in the complex with prices holding onto most of yesterday’s risk-fuelled gains. Finally, iron ore prices remain on an upward trajectory as Brazilian mining-giant Vale suspended operations at its Brucutu mine to comply with a court order regarding safety improvement at the mine, ING notes “the mine halt could impact 30mtpa of iron ore supply if Vale is unable to successfully appeal the decision.”

Looking at the day ahead, we’ll also get the remaining PMIs along with the January ISM non-manufacturing (57.0 expected). Tonight at 9pm is President Trump’s State of the Union address while the main earnings highlights today are Walt Disney and BP

US Event Calendar

- 9:45am: Markit US Services PMI, est. 54.2, prior 54.2

- 9:45am: Markit US Composite PMI, prior 54.5

- 10am: ISM Non-Manufacturing Index, est. 57.1, prior 57.6

DB’s Jim Reid concludes the overnight wrap

I hope the various winter colds are bypassing you more than they are our family. Both twins have cold induced conjunctivitis and bad coughs. They are walking around a lot with their eyes closed up and bumping into everything. Maisie has an awful cough and slight conjunctivitis too. Calpol is fast going out of stock where we live as a result. Meanwhile, both my wife and I are fighting off the same thing with my hay fever only being kept in check by the snow and tablets. As part of the design of the new house we are considering incorporating a permanent cross on the front door to warn people away.

Fortunately markets continue to shake off their pre-Xmas bout of man-flu but the last 24 hours were about as slow as we’ve seen so far this year. Major equity markets rallied but in thin trading. Volumes in Hong Kong were 54% lower than the 100-day average, as the Chinese mainland was closed for the lunar new year holiday. In Europe and the US, volumes were 15-30% lower than usual, but most benchmark indexes nevertheless grinded higher throughout the session. The NASDAQ led gains, up +1.15% into Alphabet’s earnings report. The S&P 500 and the DOW gained +0.68% and +0.70% respectively. Meanwhile the VIX edged lower to 15.73, its lowest level since the spike higher in early October last year. In Europe, the STOXX eked out a +0.06% gain, but this masked some differentiation across the continent. Italy’s FTSE MIB was up +0.15% with Spain’s IBEX down -0.49%. Spanish banks underperformed, with Banco de Sabadell and CaixaBank trading down -4.80% and -4.54% after weak earnings on Friday.

After the US close, Alphabet (Google’s parent company) reported somewhat disappointing earnings. While revenues rose more than expected in the fourth quarter and the closely-watched “paid clicks” metric rose an impressive 66%, investors focused on the erosion in profit margins from 24% to 21%. Given where we are in the cycle, it’s understandable that investors are attentive to signs of profit compression, and Alphabet’s share price slid around -3.10% in overnight trading.

The good news is that bond markets were a bit more exciting, especially Treasuries, where 10y yields rose +3.9bps which puts them up +9.4bps from the pre-payrolls levels of Friday. The move was led by a stronger day for the Greenback – which included the yen passing 110 for the first time this year (close 109.88) – as well as a busy day for US IG issuance. The moves in Europe were a lot less exaggerated but the direction of travel was the same with 10y Bunds cheapening +1.1bps. The euro also slid -0.16% although the single currency didn’t appear too fussed after ECB Governing Council member Nowotny said that he doesn’t see a recession in Europe despite recent weak data (especially in Germany). To be fair I can’t remember a central bank saying they see one coming but readers feel free to correct me.

The good news for those that found yesterday a bit dull is that there is potential for things to get a little more interesting today firstly with the final January PMIs due out in Europe this morning and then President Trump’s delayed State of the Union address due late this evening. Just on the latter, Trump is due to deliver his address at 9pm ET which is 2am GMT in the UK tomorrow morning. The average speech is around 50 minutes but for context, Trump’s speech last year was the third-longest ever at 80 minutes. Whilst it’s near-impossible to predict what will or won’t be said, expect the contentious border wall issue to be a talking point especially given rising tensions between Trump and House Speaker Pelosi. Indeed Politico believe that the biggest question is whether Trump will use the platform to declare a national emergency at the southern border as justification for beginning construction.

Overnight, one of the main stories has been news of a rare meeting between the Fed Chair Powell and the US President Trump to discuss recent economic developments and the outlook. However the Fed said in a statement that Mr. Powell didn’t share his expectations for monetary policy, “except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook,” while adding that his comments were “consistent with his remarks at his press conference of last week.” So, nothing new in particular but it was interesting they met. The meeting was also attended by Fed Vice Chair Clarida and Treasury Secretary Steven Mnuchin. Elsewhere, the Fed’s Loretta Mester (non-voter) said that the monetary policy is not “far behind or far ahead of the curve,” while adding that the Fed might get back to raising interest rates if the economy performs on the lines of her expectations even as she acknowledged a growing set of downside risks to her outlook for continued above-trend growth.

Back to markets where this morning in Asia sentiment is mixed with Hong Kong, China and South Korea’s equity markets closed for holidays. The Nikkei (+0.04%) is trading flattish post erasing early gains. Futures on the S&P 500 are down -0.10% this morning with the disappointing result from Alphabet weighing slightly. In terms of overnight data releases, Japan’s January composite PMI came in at 50.9 (vs. 52.0 last month) with the services PMI standing at 51.6 (vs. 51.0 last month). Elsewhere the UK’s January BRC like for like sales came in at +1.8% yoy (vs. -0.2% yoy expected).

In other news, Sterling chopped around a bit yesterday amid sporadic Brexit headlines. It was initially weaker into mid-afternoon firstly after Tory lawmaker Rees-Mogg said that he would accept a Brexit deal without an Irish backstop, backing up comments from the ERG that pro Brexit Tory MPs won’t support a compromise being proposed by May to add an addendum to the existing Withdrawal Agreement. Later in the session the Pound spiked back above 1.31 post the (albeit limited) story that Merkel was dropping hints of a trying to find a ‘creative’ Brexit compromise. The currency quickly retraced those gains to end the session -0.32% weaker at 1.3037 as the top EU negotiators poured cold water on the prospect of reopening the Withdrawal Agreement, with Michel Barnier saying that the backstop is the “only operational solution” to address the Irish border.

Finally the limited amount of economic data that was out yesterday didn’t do a whole lot to move the dial. Perhaps the most interesting was here in the UK where the January construction PMI slumped a notable -2.2pts to 50.6 (vs. 52.5 expected) and to the lowest since March last year. That of course follows the weaker than expected manufacturing PMI out last Friday. Elsewhere Italy’s preliminary CPI print for January was confirmed at -1.7% mom which wasn’t quite as bad as feared (-1.9% expected). The annual rate for the headline and core readings have however both slipped to +0.9% yoy. The euro area’s Sentix sentiment survey of 4,500 private and institutional investors fell to -3.7, its lowest level since 2014.

In the US, revisions to core capex orders were disappointing at -0.6% mom (vs. -0.1% expected) while core shipments were revised down a further tenth to -0.2% mom. This data is for November so looks a little out of date now with the BEA beginning the process of working through the large backlog of data releases. Later in the session, the Fed released their Q1 Senior Loan Officer Survey, which showed that C&I lending conditions tightened for the first time in two years. Banks’ reported willingness to lend to consumers also fell to its lowest level since 2009. However, the survey took place in later December, amid the nadir for equity markets, so it may somewhat overstate the severity of conditions.

To the day ahead now where the early focus data this morning will be on the final January PMIs in Europe. In terms of expectations, no change from the 50.8 flash services reading for the Euro Area is expected, however expect the market to be closely watching the data in France (following the big plummet in the flash to 47.5) and Italy (which stood at 50.5 in December). Also out this morning are December retail sales for the Euro Area while this afternoon in the US we’ll also get the remaining PMIs along with the January ISM non-manufacturing (57.0 expected). As mentioned near the top, early tomorrow morning (UK time) and late this evening (US time) we’ve got President Trump’s State of the Union address while the main earnings highlights today are Walt Disney and BP.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED CHINESE NEW YEAR //Hang Sang CLOSED NEW YEAR /The Nikkei closed DOWN 39.32 PTS OR 0.19%/ Australia’s all ordinaires CLOSED UP 1.76%

/Chinese yuan (ONSHORE) closed DOWN at 6.7422 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 54.28 dollars per barrel for WTI and 62.11 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED DOWN AT 6.7422AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7651: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

By goodness what a loss: in its 4th quarter, the largest Japanese Pension fund: GPIF lost 136 billion usa dollars in the last 3 months of the year with the downfall in stocks.

(courtesy zerohedge)

“No Need To Be Pessimistic” – World’s Biggest Pension Fund Suffers Record Collapse In Q4

“fleshwound”?

The world’s largest pension fund – in the world’s most demographically-challenged nation – suffered a stunning record loss in the last quarter as its Abe-supporting domestic-stock-buying-spree crushed Japan’s Government Pension Investment Fund (GPIF).

Bloomberg reports thatGPIF lost 9.1 percent, or 14.8 trillion yen ($136 billion), in the three months ended Dec. 31, it said in Tokyo on Friday. The decline in value and the rate of loss were the steepest based on comparable data back to April 2008. Domestic stocks were the fund’s worst performing investment, followed by foreign equities. Assets fell to 150.7 trillion yen at the end of December from a record 165.6 trillion yen in September.

While global central-bank-liquidity driven gains in global stocks helped the GPIF generate returns for the previous two fiscal years, December’s global rout underscored the risks facing the fund since it revamped strategy in 2014 to accumulate stocks and pare domestic bonds – something they vehemently deny is anything but prudent independent risk-managed behavior.

Bloomberg notes that the GPIF may have little choice but to invest in equities as fixed-income yields, especially those of Japanese government debt, are too low, said Naoki Fujiwara, chief fund manager at Shinkin Asset Management Co. in Tokyo.

“It makes sense for the GPIF to hold some risk assets in this environment because yields are low globally and bond investments don’t give good returns,” Fujiwara said.

“Yet from a pensioner’s point of view, it takes too much risk on its investments.”

But that won’t stop Abe (and Kuroda) from pushing their nation’s “independent” pension fund administrators to keep buying the dip in domestic stocks… or else.

Analysts are mixed on what to make of this collapse… some are blindly toeing the government line that any quarter now, everything will be awesome.

Shingo Ide, the chief equity strategist at NLI Research Institute in Tokyo, points out that the GPIF’s long-term performance is more important than quarterly moves. GPIF’s cumulative investment return since fiscal 2001 was 56.7 trillion yen for an annualized 2.7 percent gain.

“There’s no need to be pessimistic just because GPIF would incur loss on its investment on a quarterly basis,” Ide said.

“For pension funds, it’s more important to focus on how they secure long-term returns rather than their quarterly performance.”

But some worry about just how much risk GPIF carries…

Still, with about half of its assets in domestic and foreign equities, the GPIF’s performance may be in danger of declining as concerns about the U.S.-China trade war and the U.K.’s departure from the European Union increase the risk of a global economic slowdown, according to Hidenori Suezawa, an analyst at SMBC Nikko Securities Inc. in Tokyo.

“Trade frictions between the U.S. and China haven’t been fully solved yet and there’s a possibility that the Brexit problem may be prolonged,” Suezawa said.

“We can’t be optimistic about the investment performance toward March.”

And yet, as we noted previously, it may be about to get even worse. As Sumitomo Mitsui strategist Ayako Sera said, the GPIF has little choice but to diversify into alternative assets and high-yield bonds if it wants higher returns because Japan’s bonds, which make up about 27% of the GPIF’s assets, have virtually zero returns (well, the may rise as high as 0.2% as per the BOJ’s latest announcement) as the Bank of Japan maintains its unprecedented monetary easing.

“The GPIF’s biggest problem is it can’t keep taking in domestic bonds – especially government bonds – as a staple with Japanese interest rates so low,” Sera said.

“The fund needs to sample a wider variety of dishes.”

Apparently that’s prudent banker talk for “we need to put more pensions into, well, junk.” What it really is, is the famous yield creep to justify buying ever riskier securities, which of course, are “not risky” because the GPIF can hold in perpetuity, which somehow means the laws of the business cycle no longer matter.

3 C CHINA

Huawei lawyers in Canada are fighting the USA’s “politically motivated” prosecution in order to win her freedom. Although the bar is low, she may win on this;

(courtesy zerohedge)

Canadian lawyers for Huawei CFO Meng Wanzhou allege that the US’s campaign to extradite the daughter of the telecoms giant’s founder has “the cloud of politicization hanging over it.” And this, her legal team believes, might be a way out.

In an interview with Canadian newspaper the Globe and Mail, Meng’s legal team revealed that their defense of the Chinese executive will rest on the idea that the US is attempting to abuse the extradition process for political purposes, echoing Beijing’s accusations that the US has turned Meng into a political pawn. The defense’s argument will also rely heavily on comments made by John MacCallum, the former Canadian ambassador to Beijing, who was fired last month after saying that Meng had “a strong case” to fight extradition.

To be sure, the vast majority of extradition requests are granted by the Canadian government. The US finally filed its request just before the deadline last week. Canadian courts now have 30 days to mull the request and issue a motion to proceed.

But given the “political overlay” in the Meng case (which is obvious to all despite US officials’ insistence that the US’s crackdown on Huawei is “totally separate” from the ongoing trade spat), lead counsel Richard Peck believes there’s a strong defense to be made. Peck, who has been practicing law in Canada for more than 45 years, said he believes the case is more politicized than that of former Chilean dictator Augusto Pinochet, whom Spain sought to extradite from the UK more than 20 years ago.

“He [Mr. McCallum] mentions some of the potential defences – and certainly, I think any person that knows this area would see the potential for those defences arising,” Richard Peck, the lead counsel for Ms. Meng, told The Globe and Mail in a telephone interview from his Vancouver office.

“The political overlay of this case is remarkable. That’s probably the one thing that sets it apart from any other extradition case I’ve ever seen. It’s got this cloud of politicization hanging over it.”

Canada’s extradition act explicitly states that extradition requests are not to be made for political purposes. However, even Peck admits that the bar for these requests is “very low”, with the requesting government only needing to prove evidence of criminality – that is, enough evidence of wrongdoing to warrant a charge. Meng’s legal team is also looking at a defense based on the concept of double criminality – that the crimes alleged by the US (i.e. lying to banks to facilitate violations of US sanctions) would be considered crimes in Canada.

The question being raised by commentators in the media, Mr. Peck said, is, “‘Is this case really about this allegation against the client or is it bigger than that – is it more of a politically driven case?’ That could form in theory part of an abuse-of-process argument.”

The theory is being actively explored by Ms. Meng’s legal team.

The team has four core Canadian members, including Eric Gottardi, a partner in Mr. Peck’s law firm; David Martin, also of Vancouver; and Scott Fenton of Toronto. They are supplemented by Reid Weingarten, of New York and Washington, and three of his colleagues at Steptoe & Johnson, a 500-lawyer international firm, which includes an office in Beijing.

Each member has been assigned a task, Mr. Gottardi explained. “One person might be looking at double criminality [whether the charges would be crimes in Canada]. Someone else is looking at the political character aspect and some of these other issues people have talked about in the media, like Ambassador McCallum. I’m trying to run those issues to ground right now, and bring them back to the group to decide which ones will be viable going forward.”

[…]

But in this case, Mr. Gottardi said, “we’ve got quite arguable factual issues that go to some of the core principles of the Extradition Act. Whether or not the essence of the conduct that we’re looking at, which is tied into sanctions violations, is even illegal in Canada.”

However, in what might seem like a gift to Meng’s legal team, President Trump said that he wouldn’t hesitate to intervene in Meng’s prosecution if it could help facilitate a trade deal with China, lending an unmistakably political tinge to the process.

The significance of this remark – as well as the timing of US indictments against Huawei and Meng, which were handed down just before the start of the latest round of trade talks – has not been lost on Meng’s legal team.

“Some of the comments by the executive of the United States we have to look at very closely in terms of how they impact the fairness of the Canadian extradition hearing and how easy it will be for Canada to adhere to the rule of law,” Mr. Gottardi said.

[…]

“Looking at the press conference and the indictment and starting to gather evidence in the United States and Canada, we’re starting to get the sense that this isn’t a run-of-the-mill prosecution.”

No extradition hearing date has yet been set in the Meng case

4.EUROPEAN AFFAIRS

italy

Italy has one of the highest debts in Europe at 1.5 trillion euros or 1.7 trillion uSA dollars. An Italian debt crisis would take down the entire EU

(courtesy zerohedge)

How An Italian Debt Crisis Could Take Down The EU

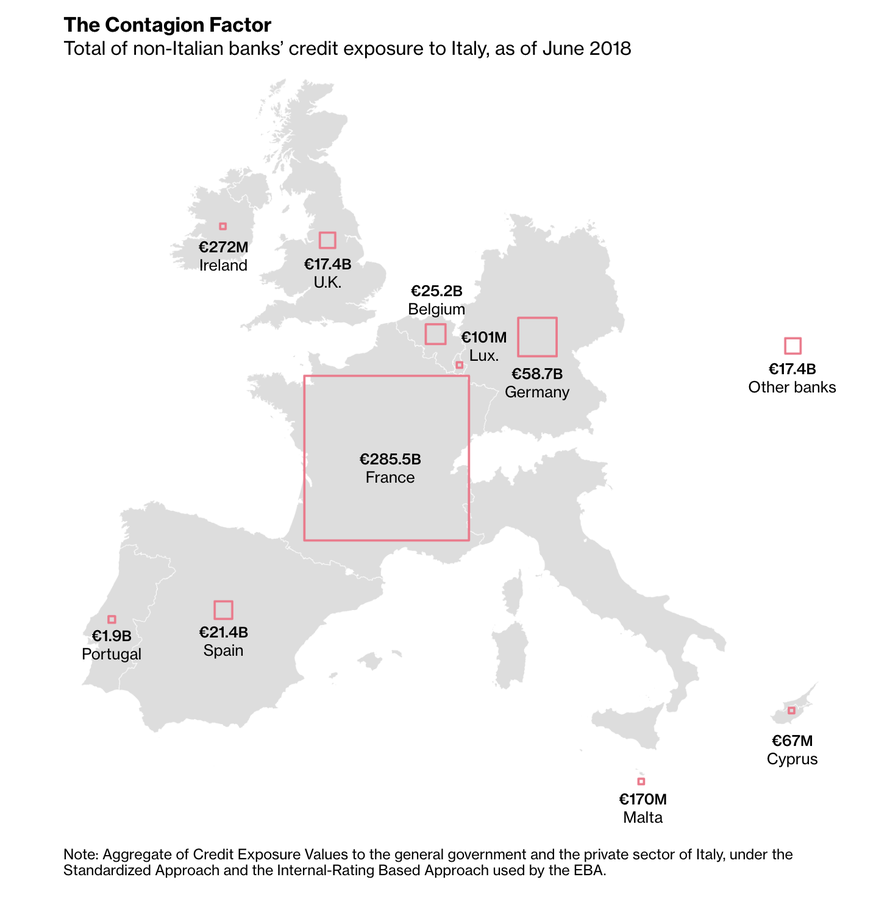

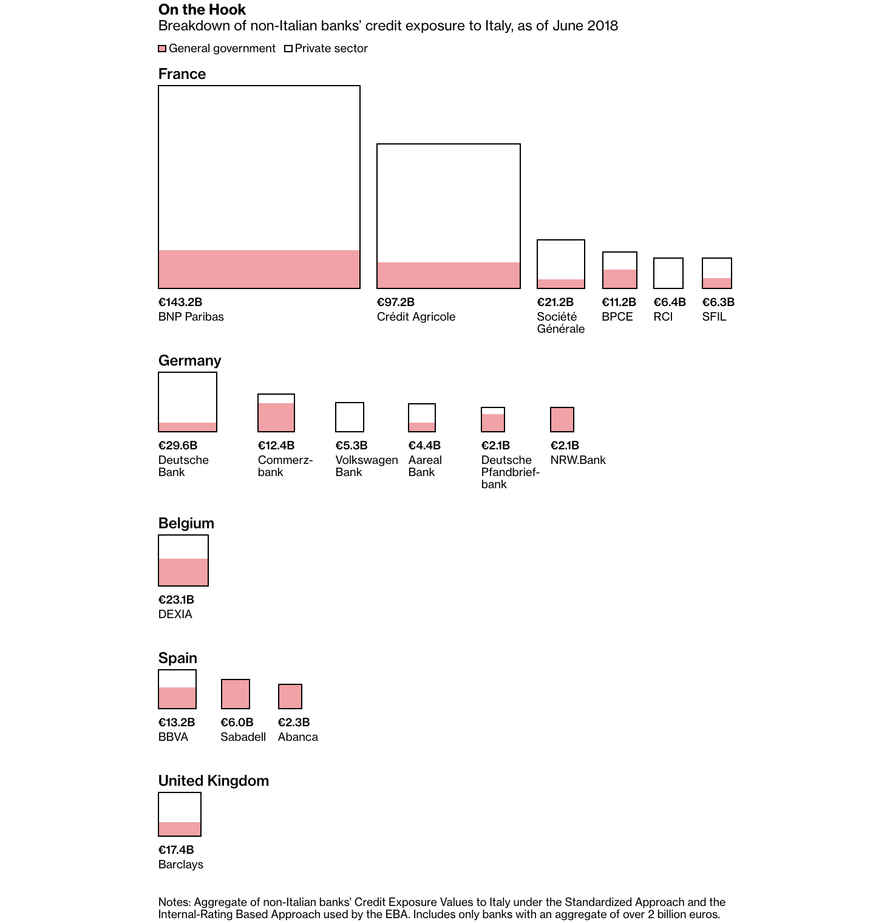

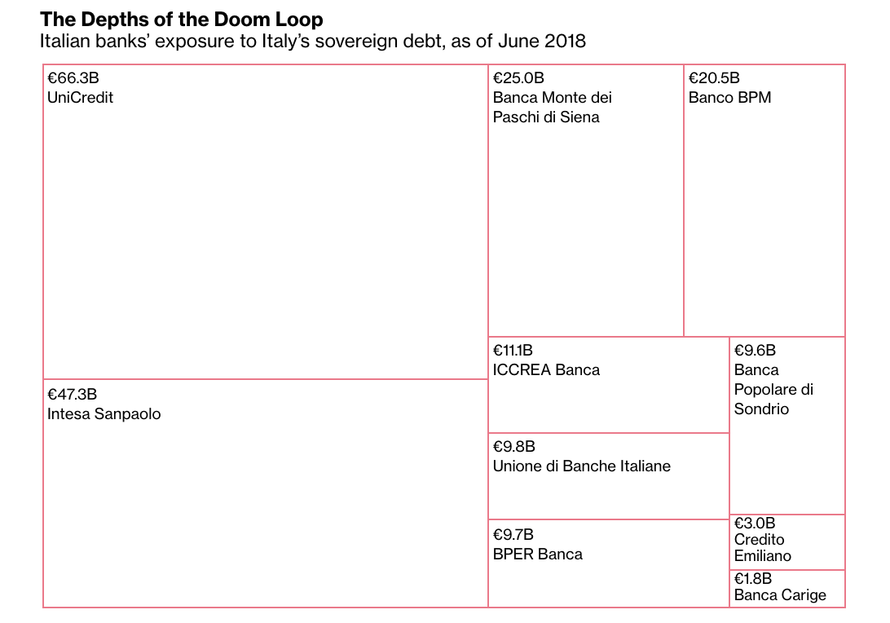

Plagued by another run of bank bailouts and simmering tensions between the partners in its ruling coalition, Italy’s brief reprieve following the detente between its populist rulers and angry bureaucrats in Brussels is already beginning to fade. As Bloomberg reminded us on Monday, Italy’s $1.7 trillion pile of public debt – the third largest sovereign debt pool in Europe – is threatening to set off a chain reaction that could hammer banks from Rome, to Madrid, to Frankfurt – and beyond.

Just the mention of the precarity of Italian debt markets “can induce a shudder of financial fear like no other” in bureaucrats and businessmen alike – particularly after Italy’s economy slid into a recession during Q4.

While much of Italy’s debt burden is held by its banks and private citizens, lenders outside of Italy are holding some 425 billion euros ($486 billion) in public and private debt.

The Bloomberg analysis of Italy’s financial foibles follows more reports that Italy’s ruling coalition between the anti-immigrant, pro-business League and the vaguely left-wing populist Five-Star Movement has become increasingly strained. Per BBG, the two parties are fighting a battle on two fronts over the construction of a high speed Alpine rail and a legal case involving League leader Matteo Salvini over his refusal to let the Dicotti migrant ship to dock in an Italian port last summer.

After M5S intimated that it could support the investigation, the League warned that such a move would be tantamount to “blackmail” against Salvini, whose lieutenants have been pushing for him to take advantage of the party’s rising poll numbers and push for early elections later this year. However, Salvini has rebuffed these demands, warning that there’s nothing stopping Italian President Sergio Mattarella from calling for a new coalition instead of new elections.

On the other hand, the League is growing increasingly weary of the “Citizens’ Income”, one of the boldest proposals included in Italy’s 2019 budget, which calls for a guaranteed subsidy for all Italians under the poverty line, provided they can prove they are looking for work.

On Monday, Luigi Di Maio and Prime Minister Giuseppe Conte presented the first of the cards that will carry the income during a ceremony that Salvini decided to skip, according to BBG. As many as 5 million Italians could be eligible for the microchip-embedded cards.

“We’ll be injecting 8 billion euros ($9.2 billion) into the real economy every year – people will be able to spend those 8 billion,” Di Maio said, at one point channeling Albert Einstein, saying those who claim something is impossible should leave those who are actually doing it alone.

However, the plan has irked business owners, who constitute some of the League’s most reliable supporters.

Circling back to the threat posed by Italian debt, BBG’s analysis showed that French banks are the most exposed, as BNP Paribas and Credit Agricole own retail banking units in Italy.

To keep operating without massive budget cuts (something neither party in the ruling coalition has shown any sign of supporting) Italy must sell 400 billion euros ($457 billion) of debt per year. But since Italy’s banks hold so much of the country’s debt, declines in the price of Italian bonds inevitably hurts the shares of Italian banks, and also forces them to hold more capital on their books to ensure liquidity from the ECB. This creates the potential for a negative feedback loop known as the “doom loop”.

Put another way, “a government crisis could drag down the banking system or a banking crisis could suck in the government.”

And while NPLs held by Italian banks have declined in recent years (as no fewer than seven Italian banks have required bailouts in the past three years)…