GOLD: $1310.90 DOWN $1.10 (COMEX TO COMEX CLOSING)

Silver: $15.57 DOWN 11 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1312.50

silver: $15.62

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 8 NOTICE(S) FOR 800 OZ (0.0249 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 9233 NOTICES FOR 923300 OZ (28.718 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

28 NOTICE(S) FILED TODAY FOR 140,000 OZ/

total number of notices filed so far this month: 565 for 2,825,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3591:DOWN $19

Bitcoin: FINAL EVENING TRADE: $3611 down $12.

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 7

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,310.800000000 USD

INTENT DATE: 02/13/2019 DELIVERY DATE: 02/15/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 3

661 H JP MORGAN 4

737 C ADVANTAGE 8 1

____________________________________________________________________________________________

TOTAL: 8 8

MONTH TO DATE: 9,233

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A STRONG SIZED 3685 CONTRACTS FROM 217,925 UP TO 221,610 DESPITE YESTERDAY’S 4 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2782 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 600 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3382 CONTRACTS. WITH THE TRANSFER OF 3382 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3392 EFP CONTRACTS TRANSLATES INTO 17.195 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.830 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 13,523 CONTRACTS (FOR 10 TRADING DAYS TOTAL 13,443 CONTRACTS) OR 67.215 MILLION OZ: (AVERAGE PER DAY: 1352 CONTRACTS OR 6.760 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 67.215 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.65% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 276.14 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7067 DESPITE THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 3382 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 7067 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3382 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3685 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.68 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 28 NOTICE(S) FOR 140,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.830 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 3814 CONTRACTS UP TO 479,897 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $1.40//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 7361 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 7361 CONTRACTS, DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 479,897. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,175 CONTRACTS: 3814 OI CONTRACTS INCREASED AT THE COMEX AND 7361 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,175 CONTRACTS OR 1,117,500 OZ = 35.34 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.40.

YESTERDAY, WE HAD 1819 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 52,092 CONTRACTS OR 5,209,200 OZ OR 162.02 TONNES (10 TRADING DAYS AND THUS AVERAGING: 5,209 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE GOOD SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 162.02 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 162.02/2550 x 100% TONNES = 6.35% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 682.17 TONNES (CORRECTED)

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 3814 WITH THE GAIN IN PRICING ($1.40) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7361 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7361 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 13,729 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7361 CONTRACTS MOVE TO LONDON AND 3814 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 34.75 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $1.40 IN YESTERDAY’S TRADING AT THE COMEX

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD down $1.10 TODAY

THE CROOKS CONTINUE WITH THEIR ATTACK ON THE GLD

THEY WITHDREW ANOTHER: 2.04 TONNES OF GOLD AND THAT WILL BE USED TO RAID GOLD/

/GLD INVENTORY 796.85 TONNES

Inventory rests tonight: 798.85 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 11 CENTS IN PRICE TODAY:

STRANGE!! A GOOD DEPOSIT OF 423,000 OZ

/INVENTORY RESTS AT 307.358 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 3685 CONTRACTS from 217,925 UP TO 221,610 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2782 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 600 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3382 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3685 CONTRACTS TO THE 3382 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN OF 8667 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 35.34 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.830 MILLION OZ STANDING IN FEBRUARY.

RESULT: A VERY STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 3382 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 1.37 POINTS OR 0.05% //Hang Sang CLOSED DOWN 65.54 POINTS OR 0.23% /The Nikkei closed DOWN 4.77 POINTS OR 0.02%/ Australia’s all ordinaires CLOSED DOWN 0.01%

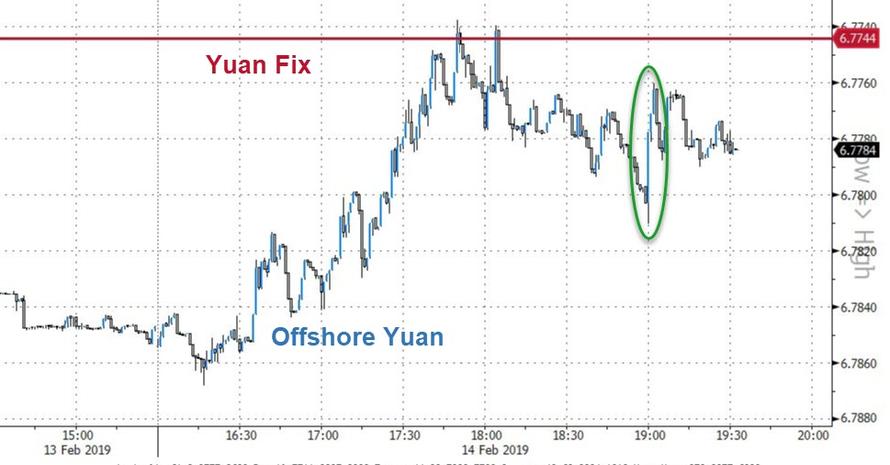

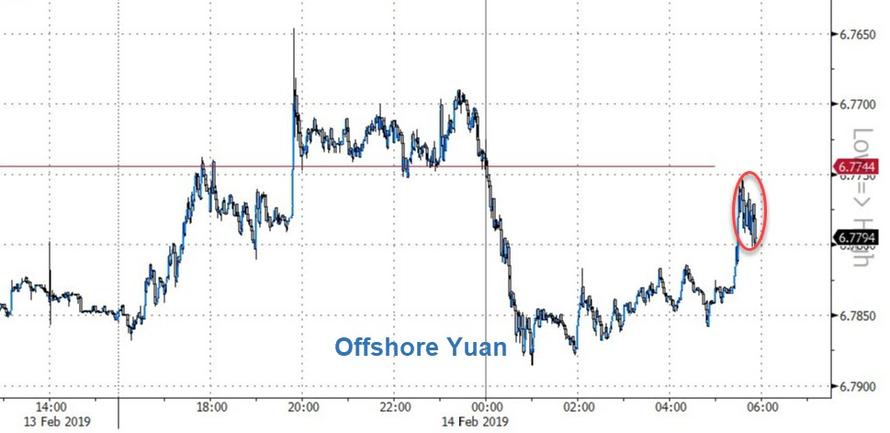

/Chinese yuan (ONSHORE) closed UP at 6.7745 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 54.39 dollars per barrel for WTI and 64.35 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED UP // LAST AT 6.7745 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7840: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i)Interesting: China’s global exports surge in January but trade with the USA tumbles:

( zerohedge)

ii)THIS MORNING: THE CHINESE MEDIA DENY REPORTS OF A TRADE DEADLINE EXTENSION

( zerohedge)

iii)LAST NIGHT:

We have to put up with this nonsense for another 60 days as Trump is considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days. Obviously the talks are not doing well!

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

UK

This study finds a no deal Brexit would hurt Germany the most as exports into the UK would plummet. They state that Germany would lose 103,000 jobs

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

9. PHYSICAL MARKETS

i)uSA Gold expects a breakout in gold’s price this year

(USA Gold//GATA)

ii)Ted Butler strongly believes that the Dept of Justice and the FBI will end JPMorgan’s silver rigging

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)Early trading this morning after release of a huge retail sales slump in December and then news that trade talks are “deadlocked”..as we promised you it would be

( zero hedge)

c)then: late morning: bounce fails and S and P tumble below key technical level(zerohedge)

ii)Market data/

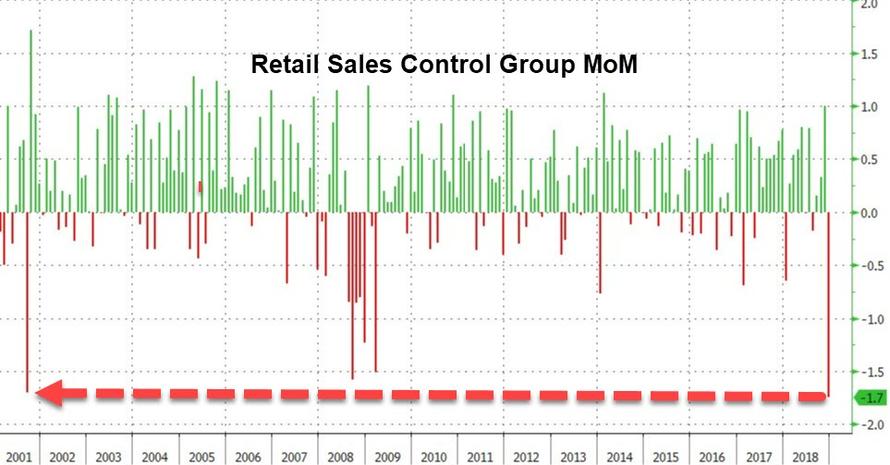

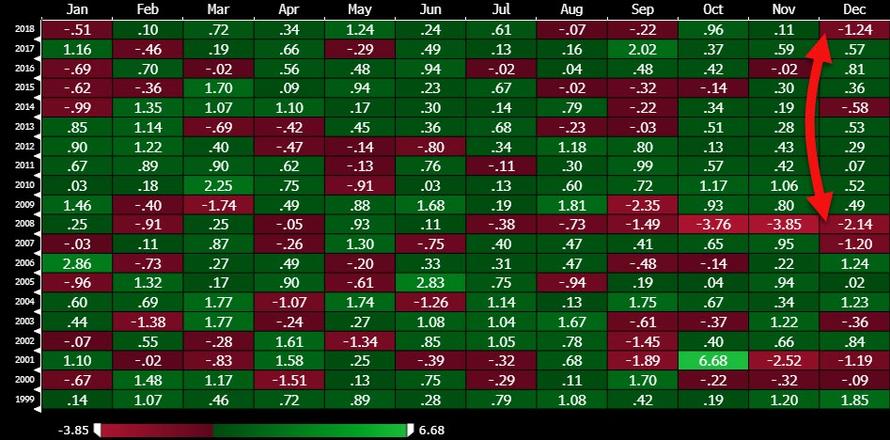

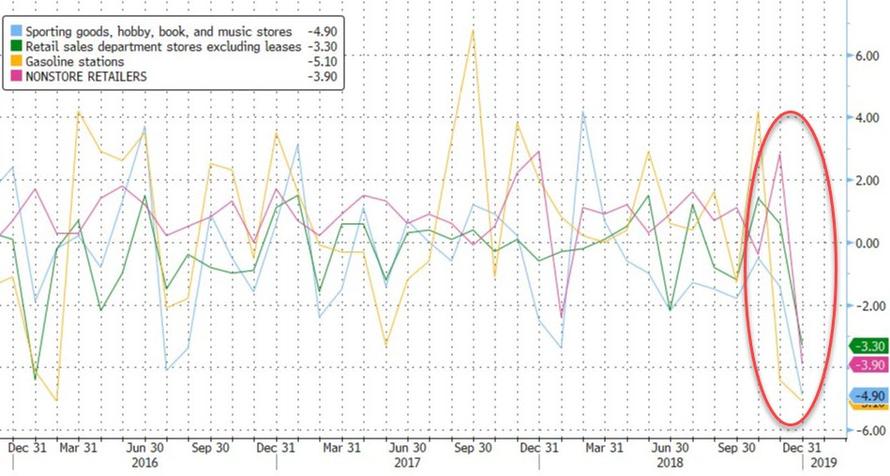

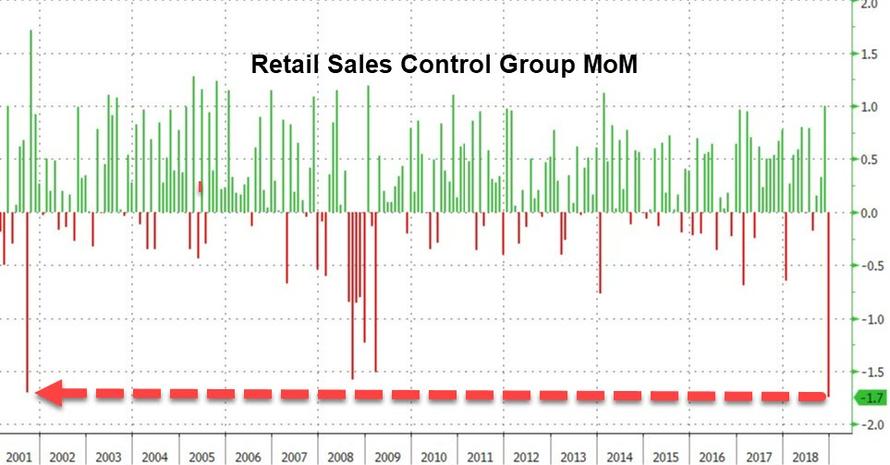

a)The biggy!! the all important retail sales collapsed in December and this was the worst Christmas reading in quite some decade, in at least 10 years. Needless to say that this will be a disaster for 4th quarter GDP where it will probably fall into the 1% category.

( zerohedge)

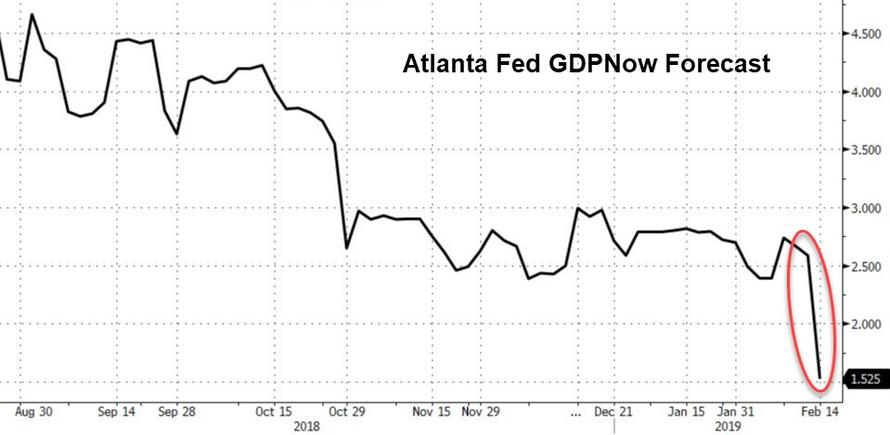

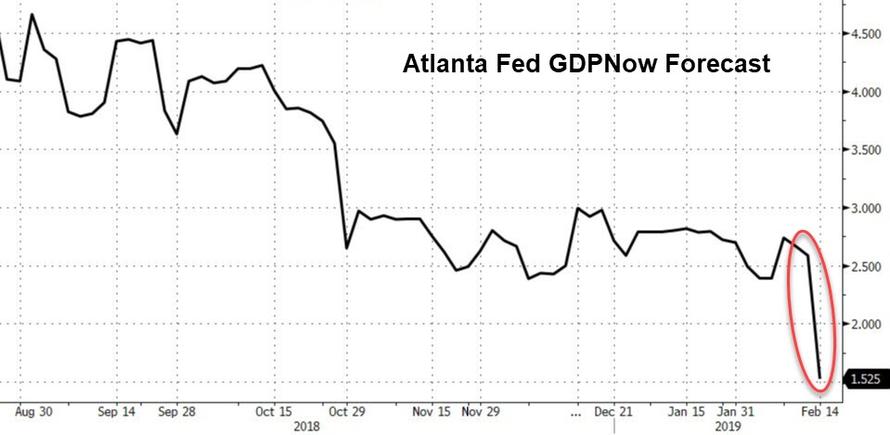

aii)Three banks lower their estimate for GDP to 2.0%. However the Atlanta Fed lowers its estimate to 1.6%. Eventually this number will settle around 1.00%

( zerohedge)

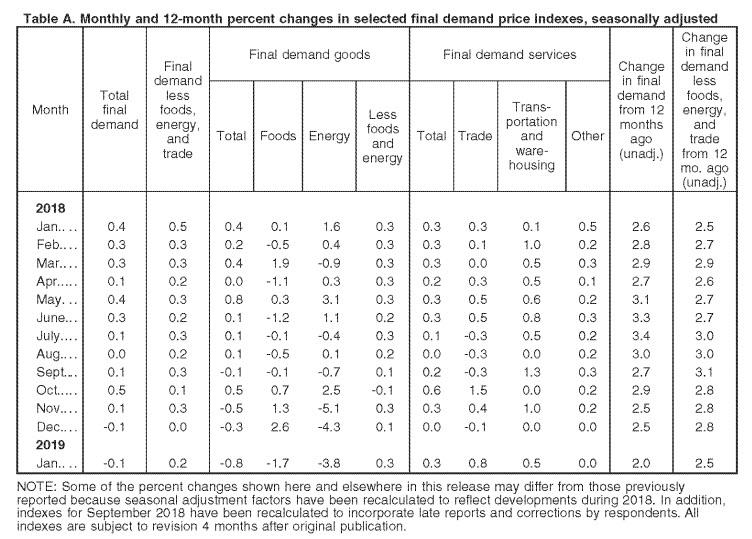

c)The Fed will not be excited with this; PPI growth is the slowest since July 2017..with the chief culprit being energy

( zerohedge)

iv)SWAMP STORIES

a)Judge Berman throws out the plea deal with Manafort so he will not get any credit for helping the prosecution.He will spend the rest of his days in prison unless Trump gives him a pardon.

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 3848 CONTRACTS DOWN TO 113,902 CONTRACTS. AFTER MARCH, APRIL RISES AT 72 CONTRACTS FOR A GAIN OF 15 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 5668 CONTRACTS UP TO 68,262 CONTRACTS.

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i

Gold P

Ted Butler is confident that Justice Dept. will stop JPM’s silver rigging

Submitted by cpowell on Thu, 2019-02-14 01:39. Section: Daily Dispatches

8:38p ET Wednesday, February 13, 2019

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler, interviewed by Jim Cook of Investment Rarities in Bloomington, Minnesota, today explains why he remains so bullish on silver and thinks the U.S. Justice Department is really beginning to move against rigging of the silver market by JPMorganChase. The interview is headlined “Jim Cook Interviews Ted Butler” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/jim-cook-interviews-ted-butler-17578

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Jim Cook Interviews Ted Butler

|

Theodore Butler writes a $400 newsletter on silver. He is considered by many to be the world’s foremost authority on silver. Eighteen years ago he predicted that silver would go up ten times, which it did. We caught up with him at his home in Florida.

Q: As the world’s leading silver bull, are you expecting fireworks in silver?

A: More so than ever.

Q: You know of course that a lot of people who own silver have grown impatient. What do you say to them?

A: I feel the same impatience, however my expectations are based upon an extremely bullish set of facts. Impatience has nothing to do with it.

Q: How do you arrive at your bullish facts?

A: I study the Commitment of Traders and Bank Participation reports and numerous other statistics, trends and reports. There are any number of bullish arguments for why silver is a great buy right now.

Q: What are some of those bullish arguments?

A: Silver has never been more necessary. It is a vital component of just about every modern product. Production of silver has been flat for years. Quite simply, there will not be enough silver to go around and price rationing will be required.

Q: Anything else?

A: What makes the case for buying silver so compelling is the current low price. If silver was priced at $30 or $50 or $100 an ounce, the argument for buying would be much less compelling.

Q: Why is the price so low?

A: Because the price has been rigged by excessive paper speculation on the COMEX, largely at the hands of JPMorgan. For 11 years, JPMorgan has been the largest paper short seller and for the past 8 years it has also been the largest physical silver buyer. It is the financial manipulation of all time and I believe totally illegal.

Q: I know you have maintained this for years, but nothing’s come of it.

A: It certainly explains why silver has been down for so long.

Q: People want a reason for this long period of depressed prices to end. Do you see any reason?

A: Yes I do. On Nov. 6, the Department of Justice announced it was conducting an investigation of manipulation of precious metals prices on the COMEX. It came as part of a guilty plea by a former trader of JPMorgan. To me, this represents the greatest single opportunity for busting JPMorgan’s manipulation of silver prices.

Q: What if the Justice Department doesn’t see what you see?

A: We’re talking about both the Justice Department and the FBI. I consider it highly unlikely that either would conclude differently. Instead of asking me what if the DOJ and FBI don’t see what I allege, you should be asking what happens if they do agree with me.

Q: What happens if they agree?

A: It means the silver manipulation comes to an end and the price is set free. Consequently, you would be much better off owning it now because afterwards it will be obvious to the world what has been going on in silver.

Q: What happens if you are wrong?

A: If I’m wrong and the Justice Department doesn’t step up to the plate and end the manipulation, the downside is limited because the price of silver is already in the gutter and close to the cost of production. It’s not often one gets such a low risk and high profit opportunity.

Q: So you’re saying that things would stay the same?

A: No, I’m quite certain the Justice Department will act to some degree. In any case, JPMorgan’s role is going to diminish because the world is finding out what they have been doing. For one thing, they have accumulated 800 million ounces of physical silver. They know silver’s potential. That fact will prove to a lot of investors just how bullish the future is for the price of silver.

END

uSA Gold expects a breakout in gold’s price this year

(USA Gold//GATA)

USAGold’s News & Views finds expectations of gold’s breakout year

Submitted by cpowell on Thu, 2019-02-14 01:44. Section: Daily Dispatches

8:44p ET Wednesday, February 13, 2019

Dear Friend of GATA and Gold:

USAGold’s “News & Views” newsletter for February asks whether 2019 will be gold’s “breakout” year and finds a fair number of analysts who indeed expect that it will be. The newsletter is posted in the clear at USAGold here:

http://www.usagold.com/cpmforum/nv1002-feb19/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7745/

//OFFSHORE YUAN: 6.7840 /shanghai bourse CLOSED DOWN 1.37 POINTS OR 0.05% /

HANG SANG CLOSED DOWN 65.54 POINTS OR 0.23%

2. Nikkei closed DOWN 65.54 POINTS OR 0.23%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 96.84/Euro RISES TO 1.1304

3b Japan 10 year bond yield: RISES TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.39 and Brent: 64/35

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE:DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.11%/Italian 10 yr bond yield DOWN to 2.78% /SPAIN 10 YR BOND YIELD DOWN TO 1.23%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.67: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.86

3k Gold at $1305.05 silver at:15.53 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 48/100 in roubles/dollar) 66.97

3m oil into the 54 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.03 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0086 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1365 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.11%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.68% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3116

Early futures jump on trade deal optimism. That faded fast on news from the Wall Street Journal that China/USA trade talks are deadlocked

Futures Jump On Latest Daily Trade Deal Optimism

It’s deja vu all over again, with global markets a sea of green, buoyed by US-China trade talk sentiment following a Bloomberg report that the US is considering a 60-day extension to the China March 1 tariff deadline (even if implicitly this confirms that there was virtually no progress made in the last few months, refuting the optimism of an imminent deal that helped push stocks over 17% from the December lows.

The big news catalyst overnight hit late on Monday night following a report that Trump was considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days, after earlier telling reporters that trade talks are “going along very well” and, with Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer in China, investors had been daring to hope for good news.

And while traders were happy to bid up risk assets for one more day on a variation of the same positive news that has hit wires – or Trump’s twitter feed – for the past two months, they ignored a tweet from the editor in chief of China’s Global Times who said that “speculations of trade negotiations will be extended are inaccurate.”

Hu Xijin 胡锡进@HuXijin_GTI learned from source close to China-US trade talks that speculations of trade negotiations will be extended are inaccurate. The only thing that is certain now is the talks are underway.

This is also a reminder that bullish expectations have been disappointed before – in fact every single time – and so the reaction in Asian markets was muted with Shanghai stocks closing flat, having jumped 2% on Wednesday to levels last seen in late September.

Meanwhile, on the other side of the Pacific, S&P futures levitated, now well above their 200 DMA, while European shares climbed for a fourth day to a three month high on, what else, optimism about U.S.-China trade talks though news that Germany only dodged recession by the narrowest of margins as its economy stagnated in Q4 following a Q3 contraction, left the euro feeling unloved on Valentine’s Day.

Strong results from Nestle, AstraZeneca and plane giant Airbus – which announced the discontinuation of its iconic A380 superjumbo – offset by a report from Credit Suisse which showed that trading losses eclipsed wealth-management gains, lifted the European STOXX 600 index 0.5% to put it on course for its best week since early November. A U.S. proposal for new sanctions on Russian banks and oil and gas firms sent shares in Moscow tumbling more than 2 percent and ignited rouble FX volatility gauges, while Russia’s 10-year bonds dropped the most since since November.

Earlier, MSCI’s index of Asia-Pacific shares ex-Japan eased 0.15%, though that was off a peak last seen in early October. Japan’s Nikkei touched its highest this year as a weakening yen boosted export stocks. China also shrugged off solid trade numbers, which however were distorted as exporters front-loaded their activities just before the Chinese New Year holidays. Beijing reported exports surged 9.1% in January from a year earlier, confounding expectations for a fall, while imports dipped by a surprisingly slight 1.5%.

“Cupid continues to shoot out bullish arrows across financial markets with last week’s blip almost forgotten about for now,” DB’s Jim Reid said in a morning note (see below).

However, as Reuters notes, “the euro did not share the feeling however” and the common currency struggled near a three-month low following the latest German GDP numbers, with fallout from global trade disputes and Brexit threatening to heap even more pressure on Europe’s rapidly slowing economy.

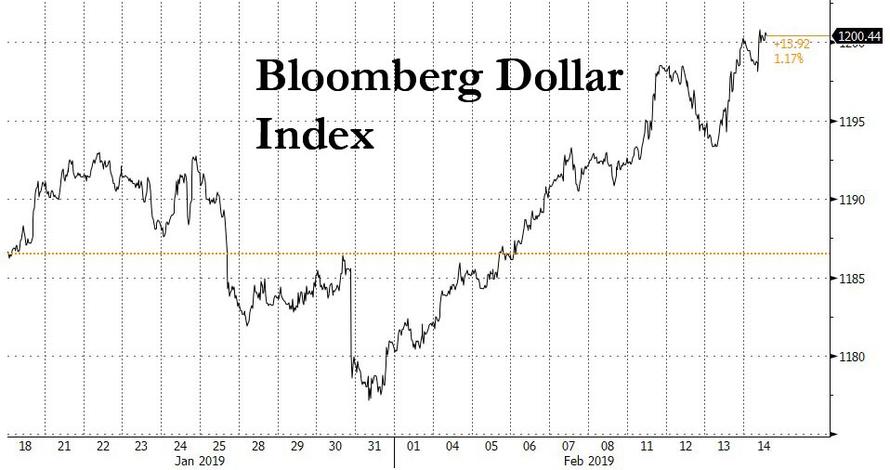

Elsewhere in FX, the dollar held its gains against most G10 peers during the European trading session, with the Bloomberg dollar index surging above 1,200, resuming its recent levitation and confounding many traders who were expecting it to slide. The greenback is now at its highest level since mid-December.

Meanwhile, the recent improvement in risk appetite undermined the safe haven yen and propelled the dollar to its best levels of the year so far at 111.05. The Australian dollar, often used as a liquid proxy for China risks, gained 0.4 percent to $0.7114 and S&P 500 futures added 0.15 percent. The Aussie dollar had already got a small lift when Chinese trade data handily beat expectations in a welcome relief for the global economy. The pound slumped ahead of another parliamentary vote on British Prime Minister Theresa May’s Brexit plan.

Treasuries steadied alongside the dollar, and oil advanced. European core sovereign bonds edged higher and the single currency fluctuated after data showed the euro region’s biggest economy stagnated in the fourth quarter, but dodged recession.

Oil continued its rebound as falling shipments from Saudi Arabia and Venezuela outweighed gains in U.S. crude stockpiles. And the pound edged lower ahead of Parliament’s latest set of votes on Theresa May’s Brexit strategy, and on dovish remarks from a Bank of England policy maker.

In the latest Brexit news, ERG is said to have told the Chief Whip they will not back the government today unless the motion on leaving the EU was changed (currently includes an amendment which Brexiteers believe removes the option of leaving without a deal) which the government refused. UK PM May spokesman says a no-deal Brexit remains on the table, and PM May is expected to speak to other EU leaders today. Separately, BoE’s Vlieghe says he considers appropriate pace of monetary tightening is somewhat slower:

- The degree of future monetary tightening will in part depend on how large GBP appreciation is

- In the case of a no-deal scenario I judge that an easing or an extended pause in monetary policy is more likely to be the appropriate policy response than a tightening

- If a Brexit deal is made, a path of Bank Rate that involves around one quarter point hike per year seems a reasonable central case

- As before, this future rate path is a forecast not a promise, and just as there is considerable uncertainty around the forecast for growth and inflation

- The BoE would hike rates after a no-deal Brexit if needed, even if it is politically unpopular

In commodity markets, oil prices found support as top exporter Saudi Arabia said it would cut crude exports and deliver an even deeper output cut. U.S. crude was up 56 cents, or 1 percent, at $54.42 a barrel, while Brent crude futures rose 97 cents to $64.50, its highest since November. Meanwhile, spot gold edged up 0.18% to $1,308.56 per ounce.

Economic data include PPI, retail sales and initial jobless claims. Coca-Cola, Nvidia and Duke Energy are due to report earnings

Market Snapshot

- S&P 500 futures up 0.3% to 2,756.75

- STOXX Europe 600 up 0.5% to 366.79

- MXAP down 0.1% to 156.96

- MXAPJ down 0.1% to 515.58

- Nikkei down 0.02% to 21,139.71

- Topix up 0.03% to 1,589.81

- Hang Seng Index down 0.2% to 28,432.05

- Shanghai Composite down 0.05% to 2,719.70

- Sensex down 0.5% to 35,870.44

- Australia S&P/ASX 200 down 0.07% to 6,059.39

- Kospi up 1.1% to 2,225.85

- German 10Y yield fell 1.1 bps to 0.112%

- Euro up 0.06% to $1.1268

- Brent futures up 1.5% to $64.53/bbl

- Italian 10Y yield fell 5.9 bps to 2.425%

- Spanish 10Y yield fell 0.6 bps to 1.228%

- Brent futures up 1.5% to $64.53/bbl

- Gold spot little changed at $1,306.46

- U.S. Dollar Index down 0.04% to 97.09

Top Overnight News

- President Donald Trump is considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days as the world’s two biggest economies try to negotiate a solution to their trade dispute, according to people familiar with the matter

- A no-deal Brexit is more likely to require an easing than a tightening of monetary policy, according to Bank of England policy maker Gertjan Vlieghe

- Bank of Italy Governor Ignazio Visco dismissed concerns over increasingly tense relations between the Bank of Italy and the nation’s populist administration, saying that the central bank isn’t under attack and that its independence requires it to be accountable.

- U.K. Prime Minister Theresa May faces a revolt from pro-Brexit members of her Conservative Party in a vote Thursday to give her more time to secure binding changes to the divorce accord with the EU

- A no-deal Brexit would be “extremely harmful” to British industry, eroding investment years into the future, the president of the U.K.’s biggest business lobby said

- Chinese export growth unexpectedly rebounded in January, while imports fell, with companies trying to ship goods before Lunar New Year holidays likely boosting the result

- Just hours after Morgan Stanley cut its recommendation on Russia amid “complacency” over new sanctions, the U.S. Senate introduced legislation to punish the country — spurring a selloff in assets

- Trump is eyeing a path to avoid another government shutdown where he would reluctantly accept the congressional border-security deal and attempt to tap other funds for his wall

- U.K. housing market stayed in the doldrums at the start of the year as Brexit caused both buyers and sellers to hesitate on deals

Asian equity markets were indecisive as the momentum from Wall St, where stocks notched a 4th consecutive gain and extended on YTD highs, was counterbalanced by cautiousness amid Chinese trade data and as senior level US-China trade talks began in Beijing. ASX 200 (-0.1%) was relatively flat following a deluge of earnings releases although the energy sector outperformed after the recent gains in crude prices, while Nikkei 225 (flat) was also flimsy due to mixed GDP data and a choppy currency. Elsewhere, Hang Seng (-0.2%) and Shanghai Comp. (-0.1%) declined at the open following another substantial liquidity drain by the PBoC and amid tentativeness heading into the key trade data which was expected to show continued ill-effects from the US-China trade dispute. Chinese stocks then only partially recovered despite the data topping estimates across the board with many wary due to Lunar New Year distortions and as the data also showed imports from US fell by 41.2% Y/Y, while reports that President Trump was mulling a 60-day extension to the tariff deadline was only gradual in its support. Finally, 10yr JGBs were higher following the less than inspiring Japanese GDP data which despite showing that Japan’s economy returned to an expansion, the headline Q/Q growth fell short of estimates and there were also downward revisions to the prior readings. Furthermore, the BoJ were present in the market for JPY 580bln of JGBs with the bulk concentrated on 5yr-10yr maturities. US President Trump is said to weigh 60-day extension for tariff deadline according to sources, while there had been earlier comments from President Trump that the trade deal with China is going very well. This was however downplayed by the China Global Times Editor

Top Asian News

- India January Wholesale Prices Rise 2.76% Y/y; Est. 3.70%

- Asia Stocks Hover Around Highest Since October Amid Trade Talks

- Ant Financial Agrees to Buy U.K. Payments Firm WorldFirst

- The Tariffs No One Seems to Want Edge Closer to Trump’s Arsenal

Following an earnings filled open, major European indices are predominantly in the green [Euro Stoxx 50 +0.4%] with some slight outperformance in the CAC (+0.6%) and SMI (+0.6%), following earnings from Airbus (+4.9%) and Nestle (+3.1%); with the latter the largest Co. in Europe carrying a 3% weighting in the Euro Stoxx 600. Sectors are also predominantly in positive territory, although there is some slight underperformance in Financial names; weighed on by the likes of Credit Suisse (-1.6%) who have moved lower following earnings, where they proposed a dividend of CHF 0.26 vs. Exp. CHF 0.30. Other notable movers include, AstraZeneca (+4.9%) who are higher after their earnings beat on expectations, with Legrand (+7.3%) also in the green after earnings. Towards the bottom of the Stoxx 600 are Telenet (-4.4%) who’s full-year operating profit missed expectations. Elsewhere, Wirecard (+7.4%) are higher, with latest reports in German press suggesting that short sellers were aware about the FT article relating to the Co before it’s publication.

Top European News

- Puma Falls Most Since December on Profit Forecast Short of Views

- RBS Said to Be Among Eight Banks in Euro Bond Cartel Probe

- EU Crackdown on Tax Breaks Takes Hit as Belgium Wins Court Clash

- Commerzbank Delivers on Costs as Zielke Cuts Some Targets

In FX, the Dollar continues find buyers on dips, and the latest pull-back in the DXY was notably shallow before the index reclaimed 97.000+ status on its way to another fresh ytd best (albeit marginal at 97.291). The Buck remains supported on encouraging US-China trade developments and prospects that President Trump will sign-off on the bipartisan funding proposal in time to avoid another Government shutdown, but also as major and EM currency counterparts weaken further on independent/specific bearish factors.

- NZD/AUD – Some erosion of momentum due to the aforementioned general Greenback bid, but the Kiwi and Aussie are still outperforming in wake of overnight Chinese trade data showing a larger than expected surplus. Nzd/Usd is holding firm above 0.6800 and also deriving support from cross-positioning as Aud/Nzd ducks under 1.0400 and Aud/Usd retreats faster from 0.7130+ peaks again to test support around 0.7100.

- EUR/CHF/JPY/GBP/CAD – All narrowly mixed vs the Usd, with the single currency trying to keep tabs on the 1.1300 handle, but weighed down by the latest weaker than expected German macro release as the former Eurozone powerhouse stagnated in Q4 following contraction in the previous quarter. Meanwhile, the Franc is edging closer to 1.1000, with sub-forecast and deflationary Swiss producer/import prices a drag, and its safe-haven peer has also extended losses through 111.00 to new 2019 lows. The Pound lost more ground ahead of today’s Brexit vote, with Cable only saved by short covering/profit taking after testing the 55 DMA (1.2813) and withstanding broadly dovish rhetoric from BoE’s Vlieghe. Elsewhere, the Loonie is pivoting 1.3250 ahead of Canadian manufacturing sales and new home price data, with the ongoing recovery in crude only mildly supportive.

- EM – As noted above, regional currencies are underperforming against the Usd, and with the Rub and Try also negatively impacted by sanctions and data misses respectively. Rouble back below 66.7500 and Lira under 5.3100 at worst.

In commodities, WTI (+1.0%) and Brent (+1.5%) continue on their upward trajectory with prices underpinned by trade hopes alongside lower Saudi output forecasts. In early EU trade, Russian Energy Minister Novak noted that there are no proposals as of yet to lift oil production due to tail risk from Venezuela. Furthermore, Novak stated that Moscow are aiming to cut February output ahead of schedule. Overnight, Chinese trade balance numbers were released wherein imports of crude in January topped 10mln BPD, +5% Y/Y/. ING notes that despite the Y/Y increase, this is still off from record levels seen at the back-end of 2018; 10.48mln BPD in November and 10.35mln BPD in December, “the very strong imports seen towards the end of last year seem to reflect refiners using their import quota licences before the end of the year” says ING. Metals are relatively mixed with gold (Unch) flat ahead of the widely watched trade talks in Beijing. Elsewhere, copper climbed higher following a wider-than-expected trade surplus from China, the world’s largest consumer of the red metal. Furthermore, copper imports into China rose by 12% from December to just under 480k tonnes in January, the highest level since September 2018; according to customs data. Finally, Dalian iron ore rebounded after declining over 4% in the last two sessions, though the recent Vale-induced rally in the base metal have reportedly damped appetite at Chinese Steel mills.

In terms of the day ahead, it’s busy in the US this afternoon with the January PPI (+0.2% mom core reading expected) report due out alongside the December retail sales report (+0.4% mom core reading expected) and the latest weekly initial jobless claims reading (-9k decline to 225k expected). Later on we’ll get November business inventories. Away from that the Fed’s Harker will speak again today while the BoE’s Vlieghe is also due to speak this morning. Italian Finance Minister Tria is also due to speak this afternoon. As highlighted earlier expect politics to also be a focus with the Brexit vote and US-China trade meetings.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior -0.2%; PPI Ex Food and Energy MoM, est. 0.2%, prior -0.1%

- 8:30am: PPI Final Demand YoY, est. 2.1%, prior 2.5%; PPI Ex Food and Energy YoY, est. 2.5%, prior 2.7%

- 8:30am: Initial Jobless Claims, est. 225,000, prior 234,000; Continuing Claims, est. 1.74m, prior 1.74m

- 8:30am: Retail Sales Advance MoM, est. 0.1%, prior 0.2%; Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.5%

- Retail Sales Control Group, est. 0.35%, prior 0.9%

- 9:45am: Bloomberg Consumer Comfort, prior 58.2

- 10am: Business Inventories, est. 0.2%, prior 0.6%

DB’s Jim Reid concludes the overnight wrap

Today is the day I’m always late for work as its an annual battle to fight my way through the deluge of cards posted through my letter box first thing in the morning. Not to mention the balloons and other assorted gifts. So Happy Valentine’s Day everyone. In the real world I’ll probably end up empty handed again apart from cards from my children although I learnt something a little upsetting yesterday. When I’ve come from work over the last couple of weeks one of the twins has pointed at me and has started saying “Dada”. It’s really sweet. Over dinner last night I was saying to my wife how lovely it was to get such a greeting and that it makes my day. She looked a bit sheepish and said that she’d be meaning to tell me something. She went on to say that every man he has seen over the last couple of weeks he has pointed at and said “Dada”. This includes our builders, the gardener, the postman, the Sainsbury’s delivery man and other Dads who go to the same classes. Sigh. Next she’ll be telling me the cards I get from them tonight weren’t done by them.

Cupid continues to shoot out bullish arrows across financial markets with last week’s blip almost forgotten about for now. Given that much of the mini sell-off last week was due to European growth being downgraded, it will be interesting to see if Germany can avoid a technical recession (+0.1% expected) in today’s Q4 GDP release and what the headlines and sentiment will be after. More on that in the day ahead. The big data release yesterday was US CPI but that did little to disturb this week’s rebound. Indeed market sentiment continues to be dictated by the twin pillars of the prospect of the US government staying open past Friday and at the margin more positive than negative US-China trade sound bites. The latter should take on more focus today and tomorrow following the news we noted in yesterday’s EMR from the South China Post that China President Xi Jinping will be meeting with US representatives Lighthizer and Mnuchin tomorrow. This opens the possibility of getting more detailed commentary from the US and/or China sides as to how talks are progressing. In the meantime Lighthizer and Mnuchin are due to meet delegates from China today including perhaps Vice-Premier Liu He. Adding to the positive sound bites around trade talks, Trump said overnight that “I think it’s going along very well, They’re showing us tremendous respect.” Further, Bloomberg has also reported overnight (citing sources) that President Trump is considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days from March 1 to give negotiations more time to continue.

Despite positive trade headlines, markets this morning in Asia are trading mixed with the Nikkei up (+0.08%) while the Hang Seng (-0.42%), Shanghai Comp (-0.30%) and Kospi (-0.10%) are all down. However, all the indices are off their lows since trade headlines trickled in. Elsewhere, futures on the S&P 500 are up +0.11% and all G10 currencies are largely trading up (0.1%-0.5%) against the greenback with the exception of the Japanese yen. Overnight, China also released its January trade stats with exports unexpectedly rising +9.1% yoy (vs -3.3% yoy expected) while imports declined -1.5% yoy (vs. -10.2% yoy expected) leaving the trade surplus at $39.16bn (vs. $34.30bn expected). In terms of China’s trade with the US in January, exports to the US dropped by -2.4% yoy in dollar terms while imports slumped by more than -41% yoy leading to China’s January trade surplus with the US at $27.3bn vs. a peak of $35.5bn in November 2018, although November’s numbers are likely to have been impacted by front loading of China’s exports to the US ahead of tariff implementation in December. Interestingly though China’s January trade surplus with the US at $27.3bn is still higher than the average January trade surplus (c. $21.65bn) with the US over the past 4 years. Elsewhere Japan’s preliminary annualised Q4 GDP growth came in line with consensus at +1.4% qoq annualised with business spending standing at +2.4% qoq (vs. +1.8% qoq expected) while private consumption stood at +0.6% qoq (vs. +0.7% qoq expected).

As for the government shutdown, yesterday the Washington Post reported that Trump is likely to sign the legislation in order to avert a shutdown but then also likely pursue an executive order to reallocate federal funds towards barrier projects. In public remarks, Trump said, “a shutdown would be a terrible thing, I don’t want to see another one, there’s no reason for it,” so hopefully that will prove conclusive. The House of Representatives is set to vote later today, where passage is almost assured, before sending the bill to the Senate tonight for approval before President Trump gives his final approval or veto.

Back to markets where the S&P 500, DOW and NASDAQ rose another +0.27%, +0.46% and +0.08%, respectively, by the closing bell last night. All three indexes had jumped higher at the open, with the S&P 500 up as much as +0.62%, but all three subsequently retraced after Republican Senator Marco Rubio announced a plan to change tax laws to make share buybacks less favourable. Currently, buybacks boost equity prices but investors can defer their tax liability and pay it at a time of their choosing. In contrast, dividends are taxed as ordinary income. Rubio’s plan would equalize the tax treatment between the two techniques. This follows a Democratic proposal from Senators Sanders and Schumer, which would place different limits on buybacks. So there may be hints of a bipartisan consensus forming on the topic, which would presumably be negative for equity markets all other things being equal. S&P 500 companies bought back around $650 billion of their own shares last year, on a net basis. This compares with around $450 billion in 2017.

Even though markets fell from the morning highs, that’s four consecutive daily gains for the S&P and it’s put the index at within just 1.37% of the December highs. Impressively it’s also back to within 6.42% of the all-time high from back in September after being off as much as 19.78% at one stage and over 20% intra-day at the lows. Meanwhile rates sold-off marginally post yesterday’s ever so slightly stronger than expected US CPI print. The move was hardly eye-watering though with Treasuries rising from a low 2.679% to 2.713% post the data, before closing at 2.708% and +2.0bps on the day. The 2s10s curve flattened -0.9bps while the USD (+0.47%) resumed its upward march once again to reach a two-month high. That move weighed on emerging markets, as EM currencies posted their worst day since last August, dropping -0.89%, and EM equities shed -0.71%. HY credit spreads tightened -3bps. Nick in my team yesterday put out a note showing that although its tempting to favour US HY over European on growth differentials, he shows how cheap Euro HY is on a relative basis. See the report here .

It was a similar story for markets in Europe where the STOXX 600 closed +0.60%. That puts the week-to-date move at +1.93% and the YTD move now at +6.30% and back within 0.15% of last week’s YTD highs before growth and trade fears resurfaced. We are still -10.35% below 2018’s high which compares to the equivalent figure of -6.39% mentioned above for the S&P500. The FTSE MIB (+0.93%) was up a little more than most but the IBEX (-0.01%) was the notable underperformer with the risk of a snap election rising in Spain. Yesterday, parliament rejected the Socialist Party’s 2019 budget with Casado – leader of the opposition People’s Party – telling reporters that there is now no excuse for PM Sanchez to delay an election, with Bloomberg citing April as the likely month the election would take place. Recent polls suggest that political support is fairly fragmented at the moment in Spain with a centre-right coalition most likely. Spanish bonds were flat yesterday which compared to a -6.0bps rally for BTPs.

Coming back to that US CPI report, the core reading for January was confirmed as rising +0.2% mom and in line with expectations although the unrounded reading was a slightly more hawkish +0.2395% (it wont be long before we add a 5th decimal!). That meant the annual rate held at +2.2% yoy compared to expectations for +2.1% while both the 3m (+2.2%) and 6m (+2.6%) annualized rates remain solid and consistent with inflation at or slightly above the Fed’s target.

Over at the Fed it was a busy day for speeches, with Atlanta President Bostic, Cleveland President Mester, and Philadelphia President Harker all speaking. None are voting members of the FOMC this year and all delivered fairly boilerplate remarks, focusing on the strong US economy but elevated uncertainties. Bostic said “we can take our time” to get to neutral, which is perhaps revealing as it suggests that he views current rates as still-below their neutral level. Mester suggested that a switch from inflation rate targeting to price level targeting has some appeal, which is a topic that will become more prominent when the Fed launches their planned policy review in June. Finally, Harker reiterated his previous view in favour of one hike this year and one next year, though it is noteworthy that he does not seem to have shifted his views over the last two months, despite a shift on the rest of the committee. The center of the committee seems to have moved toward the doves, but the doves have not yet moved any further.

Meanwhile, Brexit headlines have hit a lull with PM May having bought further time. A reminder though that the neutral motion vote is due today with some indications that the ERG might pull support leading to a government defeat. This is however just symbolic. The real fun and games will occur in two weeks time. Sterling closed-0.35% last night with yesterday’s January inflation data in the UK doing little to move the dial either. Core CPI rose three-tenths to +1.9% yoy as expected which puts the next focus on the labour market data next week which is arguably more important given the BoE tightening bias which is predicated on firming domestic costs.

As for the other data that was out yesterday, the December industrial production print for the Euro Area was confirmed at a much weaker than expected -0.9% mom (vs. -0.4% expected). That did however more closely reflect the country level data last week so the consensus reading was a little misleading. The euro finished -0.51% yesterday.

For those of an accounting bent, as companies begin to adopt the new Human Capital Reporting standard, Luke Templeman on my team has calculated the “Human Capital Return on Investment” for European stocks – one of the key requirements. This feeds directly into fair valuation calculations and just one unexpected outcome was that in 2018, share price returns were more correlated with “Human Capital RoI” than they were with a stock’s Return on Equity. Click here .

In terms of the day ahead, this morning the big focus will be on the preliminary Q4 GDP print in Germany, due about an hour after this hits your emails. The consensus expects a +0.1% mom reading which as a reminder follows a negative reading in Q3 (-0.2% qoq). However given the slim margins it’s not impossible that Germany could be in a technical recession. Also due out this morning is Q4 employment data in France followed later by the second reading on Q4 GDP for the Euro Area (no change from +0.2% qoq flash expected). Meanwhile, it’s busy in the US this afternoon with the January PPI (+0.2% mom core reading expected) report due out alongside the December retail sales report (+0.4% mom core reading expected) and the latest weekly initial jobless claims reading (-9k decline to 225k expected). Later on we’ll get November business inventories. Away from that the Fed’s Harker will speak again today while the BoE’s Vlieghe is also due to speak this morning. Italian Finance Minister Tria is also due to speak this afternoon. As highlighted earlier expect politics to also be a focus with the Brexit vote and US-China trade meetings.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 1.37 POINTS OR 0.05% //Hang Sang CLOSED DOWN 65.54 POINTS OR 0.23% /The Nikkei closed DOWN 4.77 POINTS OR 0.02%/ Australia’s all ordinaires CLOSED DOWN 0.01%

/Chinese yuan (ONSHORE) closed UP at 6.7745 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 54.39 dollars per barrel for WTI and 64.35 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED UP // LAST AT 6.7745 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7840: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/USA

Interesting: China’s global exports surge in January but trade with the USA tumbles:

(courtesy zerohedge)

China Global Exports Surge In January But Trade With US Tumbles

Amid intensifying trade talks, Chinese exports rebounded dramatically in January as companies trying to ship goods ahead of the Lunar New Year shutdown likely exaggerated the gains.

In USD terms, exports rose 9.1% in January from a year earlier (far above expectations of a 3.3% decline and December’s 4.4% YoY drop). Imports also smashed expectations: falling just 1.5% against expectations for a 10.2% collapse.

In Yuan terms, Exports rose and even more impressive 13.9% YoY and imports rose 2.9% YoY (both far better than expected).

The overall trade surplus fell in both Yuan and USD terms from December.

Impressive numbers, but as Bloomberg details, the Lunar New Year break coming about 10 days earlier than last year probably boosted January’s shipments, as companies rushed to ship more goods ahead of the holiday shutdown of many factories and companies.

Trade with US tumbled with both exports and imports plunging further in January.

China Jan. exports to U.S. was $36.54b and imports from U.S. was $9.24b, according to website of General Administration of Customs.

Also of note, China’s crude oil imports -2.7%MoM to 10.07m b/d last month, according to Bloomberg calculations based on data from General Administration of Customs Thursday.

“We expect that growth of exports in 2019 will decelerate from 2018, even if there is a deal not to raise tariffs on $200 billion in Chinese imports, due to lackluster global economy,” UBS AG economist Ning Zhang said.

“But if there’s a deal to scrap all the existing tariffs, that will be a different scenario, and the exports will not weaken significantly.”

The initial reaction was a kneejerk higher in yuan but that is fading…

END

LAST NIGHT:

We have to put up with this nonsense for another 60 days as Trump is considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days. Obviously the talks are not doing well!

(courtesy zerohedge)

Futures, Yuan Spike On China Tariff Delay Headlines

US equity futures and China’s yuan both kneejerked higher on Bloomberg reports that President Trump is considering pushing back the deadline for imposition of higher tariffs on Chinese imports by 60 days.

Having already hinted at it during a pool spray today that he was open to letting the March 1 deadline for more than doubling tariffs on $200 billion of Chinese goods slide if the two countries are close to a deal, Bloomberg reports that, according to people familiar with the matter,Trump is weighing whether to add 60 days to the current deadline to give negotiations more time to continue.

Yuan spiked…

As did US futures…

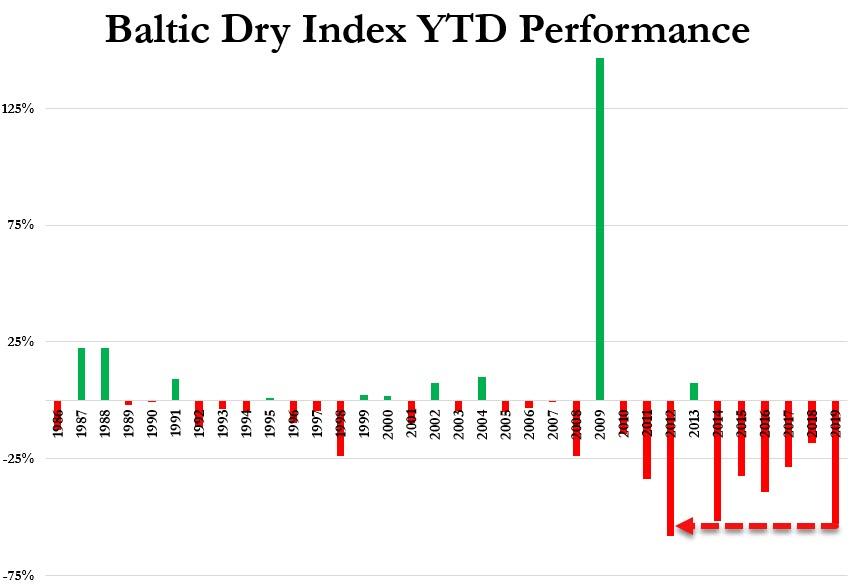

However, some human traders (as opposed to headline algos) are wondering why this would be perceived as bullish at all as it simply indicates they are no closer to deal than they were 60 days ago and the 10% tariffs will remain in effect – weighing on global trade (as the Baltic Dry Index collapse suggests)…

end

THIS MORNING: THE CHINESE MEDIA DENY REPORTS OF A TRADE DEADLINE EXTENSION

(courtesy zerohedge)

Chinese Media Deny Reports Of Trade Deadline Extension

Update: The editor of the English-language Global Times – a mouthpiece for the Communist Party – has disputed reports that a deadline delay has been discussed.

The only thing that’s certain right now is that “talks are underway.”

Hu Xijin 胡锡进@HuXijin_GTI learned from source close to China-US trade talks that speculations of trade negotiations will be extended are inaccurate. The only thing that is certain now is the talks are underway.

* * *

In a report that will likely be cheered by investors, many of whom believe an extension of the Trump administration’s “hard” trade deadline would be the best-case scenario for stocks (given that, by all accounts, the two sides are nowhere agreement on the sweeping trade deal that Trump had promised), Bloombergreported late on Thursday that President Trump was considering a 60-day extension of the March 1 deadline, as the world’s two biggest economies try to negotiate a solution to their trade dispute.

Though he has said he’s not “inclined” to extend the deadline, several sources close to the president reportedly told BBG that an extension would be approved if the two sides are close to a deal that includes “deep structural changes to China’s economic policies.”

“I think it’s going along very well,” Trump told reporters in the Oval Office this week. “They’re showing us tremendous respect.”

The news spiked both the Yuan:

… And US futures:

The extension would allow time for President Trump and President Xi Jinping to meet in person, something Trump has insisted must happen before he would sign off on a trade deal. A mid-level delegation of US trade officials has been in Beijing this week reportedly negotiating on an enforcement mechanism to ensure Beijing’s compliance with the deal, as well as cobbling together a deal framework that can be presented to both leaders. BBG added that an extension might depend on the outcome of a meeting between Lighthizer and Xi that’s expected to take place this week.

“The outcome of the China-U.S. high-level economic and trade negotiations may be related to the future development and stability of the world economy,” Chinese Foreign Ministry spokeswoman Hua Chunying said at a regular briefing Thursday in Beijing.“Both parties hope to reach a mutually beneficial agreement. The best thing we can do now is to let both sides concentrate on consultations.”

The US has pushed for a range of reforms to the Chinese economy, from how China manages its own economy, to its foreign trade practices. Trump has insisted that China take steps to reduce the US-China trade deficit, while Lighthizer has specifically focused on ending Beijing’s institutionalized IP theft and the advantages given to Chinese state-sponsored companies operating in China’s domestic market.

Shortly after Trump and Xi agreed to the trade truce during a dinner in Buenos Aires on Dec. 1, the president and Lighthizer, who is in charge of the trade talks on the US side, insisted that the March 1 deadline wouldn’t be moved. But reports so far suggest that only moderate progress has been made.

Still, an extension would be enough of a signal to markets that progress is being made. The biggest issue for the Trump Administration would be holding the Chinese accountable to ensure that this is the only delay necessary.

end

4.EUROPEAN AFFAIRS

/UK

This study finds a no deal Brexit would hurt Germany the most as exports into the UK would plummet. They state that Germany would lose 103,000 jobs

(courtesy zerohedge)

Where A No-Deal Brexit Would Hit Hardest

In recent weeks, the chances of a dreaded no-deal Brexit occurring have increased exponentially ahead of the deadline on March 29th.

A new study has looked into that scenario’s potential impact on jobs across the world. Statista’s Niall McCarthy notes that the analysis was carried out by the Halle Institute for Economic Research (IWH), focusing on 56 industrial sectors across 43 countries while assuming a 25 percent drop in EU exports to the UK in the event of a hard Brexit.

It found that Germany could lose the most jobs with around 103,000 threatened if the UK crashes out of the EU with no deal.

You will find more infographics at Statista

Even though Europe’s economic powerhouse could be impacted most in terms of the sheer number of jobs, the situation is different when it comes to the share of total employment threatened.

In this case, only 0.24 percent of Germany’s workforce would be under threat compared to 1.03 percent of all jobs in Ireland. That’s despite “only” 19,800 Irish jobs potentially being impacted.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran

6. GLOBAL ISSUES

end

7 OIL ISSUES

8. EMERGING MARKETS

Venezuela/USA

end

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:00 AM….

Euro/USA 1.1268 UP .0003 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES GREEN

USA/JAPAN YEN 111.03 UP .097 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2809 DOWN 0.0046 (Brexit March 29/ 2017/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.3263 UP .0003 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS THURSDAY morning in Europe, the Euro ROSE by 3 basis points, trading now ABOVE the important 1.08 level RISING to 1.1293/ Last night Shanghai composite closed DOWN 1.37 POINTS OR 0.05%/

//Hang Sang CLOSED DOWN 65.54 POINTS OR 0.23%

/AUSTRALIA CLOSED DOWN .01% /EUROPEAN BOURSES GREEN

The NIKKEI: this THURSDAY morning CLOSED DOWN 4.77 POINTS OR 0.02%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED DOWN 65.54 POINTS OR 0.23%

/SHANGHAI CLOSED UP 1.37 POINTS OR 0.05%

Australia BOURSE CLOSED DOWN 0.01%

Nikkei (Japan) CLOSED DOWN 4.77 POINTS OR 0.02%

INDIA’S SENSEX IN THE RED

Gold very early morning trading: 1304.70

silver:$15.54

Early THURSDAY morning USA 10 year bond yield: 2.68% !!! DOWN 2 IN POINTS from WEDNESDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%. (POLICY FED ERROR)/

The 30 yr bond yield 3.02 DOWN 1 IN BASIS POINTS from WEDNESDAY night. (POLICY FED ERROR)/

USA dollar index early THURSDAY morning: 97.22 UP 19 CENT(S) from WEDNESDAY’s close.

This ends early morning numbers THURSDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing THURSDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.57% DOWN 2 in basis point(s) yield from WEDNESDAY/

JAPANESE BOND YIELD: -.01% UP 0 BASIS POINTS from WEDNESDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.24% UP 1 IN basis point yield from WEDNESDAY

ITALIAN 10 YR BOND YIELD: 2.80 UP 2 POINTS in basis point yield from MONDAY/

the Italian 10 yr bond yield is trading 156 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: FALLS UP TO +.10% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.70% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR THURSDAY

Closing currency crosses for THURSDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1283 UP .0018 or 18 basis points

USA/Japan: 110.68 DOWN 0.250 OR 25 basis points/

Great Britain/USA 1.2795 DOWN.0059( POUND DOWN 59 BASIS POINTS)

Canadian dollar DOWN 49 basis points to 1.3308

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed HOLIDAY AT 6.7720 0N SHORE

THE USA/YUAN OFFSHORE: 6.7833( YUAN DOWN)

TURKISH LIRA: 5.3045

the 10 yr Japanese bond yield closed at -.01%

Your closing 10 yr USA bond yield DOWN 3 IN basis points from WEDNESDAY at 2.66 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 3.02 DOWN 1 in basis points on the day /

THE RISE IN BOTH THE 10 YR AND THE 30 YR ARE VERY PROBLEMATIC FOR VALUATIONS

Your closing USA dollar index, 97.17 UP 4 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for THURSDAY: 12:00 PM

London: CLOSED UP 6,17 OR 0.09%

German Dax : DOWN 77.43 POINTS OR 0.69%

Paris Cac CLOSED DOWN 11,75 POINTS OR 0.23%

Spain IBEX CLOSED DOWN 29.90 POINTS OR 0.33%

Italian MIB: CLOSED DOWN 154,94 POINTS OR 0.79%

WTI Oil price; 53.97 1:00 pm;

Brent Oil: 6423 12:00 EST

USA /RUSSIAN / ROUBLE CROSS: 67.01 THE CROSS HIGHER BY 0.52 ROUBLES/DOLLAR (ROUBLE LOWER BY 52 BASIS PTS)

TODAY THE GERMAN YIELD LOWERS TO +.10 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM : 54.56

BRENT : 64.56

USA 10 YR BOND YIELD: … 2.66..

USA 30 YR BOND YIELD: 3.01

EURO/USA DOLLAR CROSS: 1.1293 ( UP 28 BASIS POINTS)

USA/JAPANESE YEN:110.53 DOWN .403 (YEN UP 40 BASIS POINTS/..

.

USA DOLLAR INDEX: 97.03 DOWN 10 cent(s)/

The British pound at 4 pm: Great Britain Pound/USA:1.2793 DOWN 62 POINTS FROM YESTERDAY

the Turkish lira close: 5.2818

the Russian rouble 66.67 down .17 Roubles against the uSA dollar.( DOWN 17 BASIS POINTS)

Canadian dollar: 1.389 DOWN 30 BASIS pts

USA/CHINESE YUAN (CNY) : 6.7720 (ONSHORE)/CLOSED FOR THE WEEK

USA/CHINESE YUAN(CNH): 6.7777 (OFFSHORE)

German 10 yr bond yield at 5 pm: ,0.10%

The Dow closed DOWN 103.61 POINTS OR 0.41%

NASDAQ closed UP 6.58 POINTS OR 0.09%

VOLATILITY INDEX: 15.99 CLOSED UP .34

LIBOR 3 MONTH DURATION: 2.684%

FROM 2.692

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM FOR THE DAY/WEEKLY SUMMARY/FOLLOWED BY TODAY

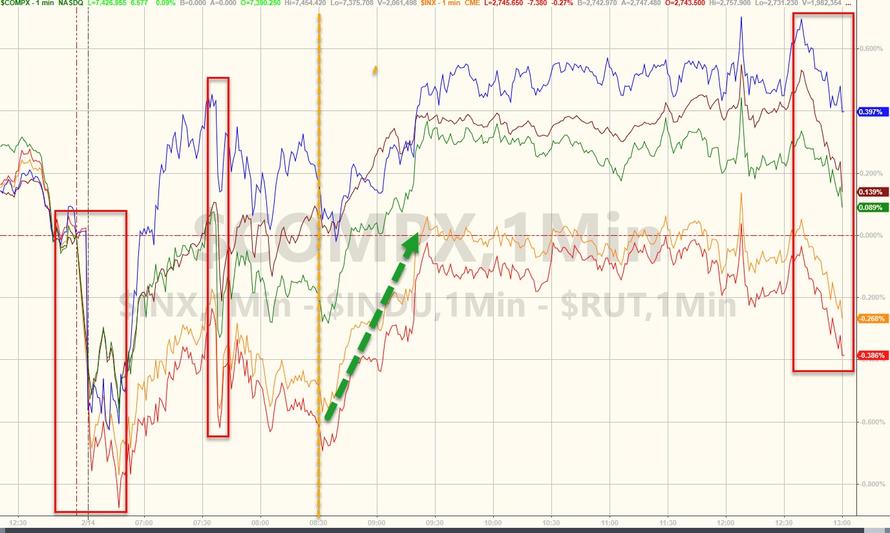

Stocks Stumble After Retail Rout, Coke Collapse, Bezos Bombshell, & Trade Turmoil

The algos were in charge today as headline after headline spooked stocks and sparked buying panics…

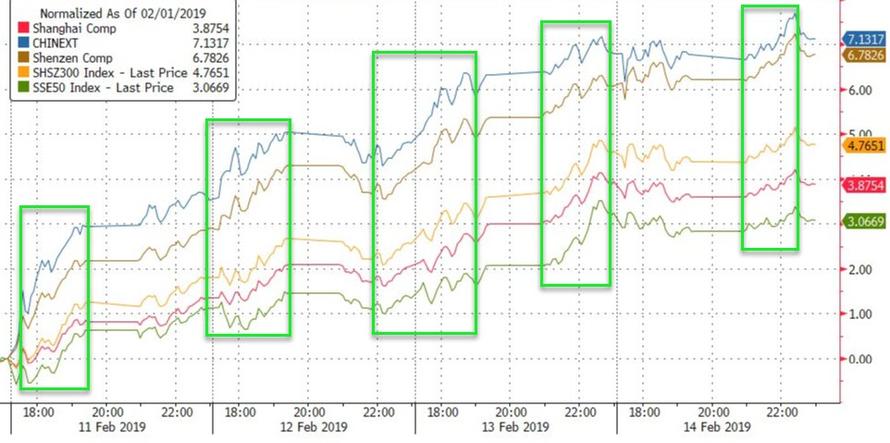

China continues to extend post-new year gains…

European markets dropped today (hurt by US retail sales sentiment)…

And before we get to US markets, let’s just ponder this shitshow…

And GDP expectations are cratering…