GOLD: $1318.90 UP $8.00 (COMEX TO COMEX CLOSING)

Silver: $15.76 UP 19 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1321.50

silver: $15.79

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 928 NOTICE(S) FOR 92800 OZ (2.886 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10,161 NOTICES FOR 1016100 OZ (31.604 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 565 for 2,825,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3611:UP $21

Bitcoin: FINAL EVENING TRADE: $3611 down $12.

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 796/928

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,309.800000000 USD

INTENT DATE: 02/14/2019 DELIVERY DATE: 02/19/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 19

661 C JP MORGAN 689

661 H JP MORGAN 127

685 C RJ OBRIEN 4

686 C INTL FCSTONE 1

737 C ADVANTAGE 1 88

880 H CITIGROUP 927

____________________________________________________________________________________________

TOTAL: 928 928

MONTH TO DATE: 10,161

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A STRONG SIZED 1891 CONTRACTS FROM 221,610 DOWN TO 219,719 WITH YESTERDAY’S 11 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2316 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2316 CONTRACTS. WITH THE TRANSFER OF 2316 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2316 EFP CONTRACTS TRANSLATES INTO 11.58 MILLION OZ ACCOMPANYING:

1.THE 11 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.830 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 15,839 CONTRACTS (FOR 11 TRADING DAYS TOTAL 15,839 CONTRACTS) OR 79.195 MILLION OZ: (AVERAGE PER DAY: 1439 CONTRACTS OR 7.1995 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 79.195 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.30% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 287.72 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1891 WITH THE 11 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2316 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 425 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2316 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1891 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 11 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.57 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.830 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A TINY SIZED 353 CONTRACTS DOWN TO 479,544 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $1.10//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 7780 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 7783 CONTRACTS, DECEMBER: 350 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 479,544. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7780 CONTRACTS: 353 OI CONTRACTS DECREASED AT THE COMEX AND 8133 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7780 CONTRACTS OR 778,000 OZ = 24.19 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.10.

YESTERDAY, WE HAD 7361 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 60,225 CONTRACTS OR 6,022,500 OZ OR 187.32 TONNES (11 TRADING DAYS AND THUS AVERAGING: 5,475 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE GOOD SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 187.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 187.32/2550 x 100% TONNES = 7.34% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 707.46 TONNES (CORRECTED)

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED DECREASE IN OI AT THE COMEX OF 353 WITH THE LOSS IN PRICING ($1.10) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8133 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8133 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 8581 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8133 CONTRACTS MOVE TO LONDON AND 353 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 24.19 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $1.10 IN YESTERDAY’S TRADING AT THE COMEX

we had: 928 notice(s) filed upon for 92800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.00 TODAY

THE CROOKS CONTINUE WITH THEIR ATTACK ON THE GLD

THEY WITHDREW ANOTHER: 2.04 TONNES OF GOLD AND THAT WILL BE USED TO RAID GOLD/

/GLD INVENTORY 796.85 TONNES

Inventory rests tonight: 796.85 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 11 CENTS IN PRICE TODAY:

STRANGE!! A GOOD DEPOSIT OF 423,000 OZ

/INVENTORY RESTS AT 307.358 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 1891 CONTRACTS from 221,610 DOWN TO 219,719 AND MOVING FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2316 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2316 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1891 CONTRACTS TO THE 2316 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A TINY GAIN OF 425 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.125 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.830 MILLION OZ STANDING IN FEBRUARY.

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 11 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 2316 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 37.32 POINTS OR 1.37% //Hang Sang CLOSED DOWN 531.21 POINTS OR 1.87% /The Nikkei closed DOWN 239.08 POINTS OR 1.13%/ Australia’s all ordinaires CLOSED UP 0.15%

/Chinese yuan (ONSHORE) closed UP at 6.7709 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 54.70 dollars per barrel for WTI and 64.94 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7709 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7792: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/USA

After both Xi and Mnuchin sounded upbeat on their negotiations, Xi hinted that China will not budge on its economic reforms which is exactly what we promised you. He will offer more purchases of USA goods but will not budget on the more important structural reforms like stealing USA technology

( zerohedge)

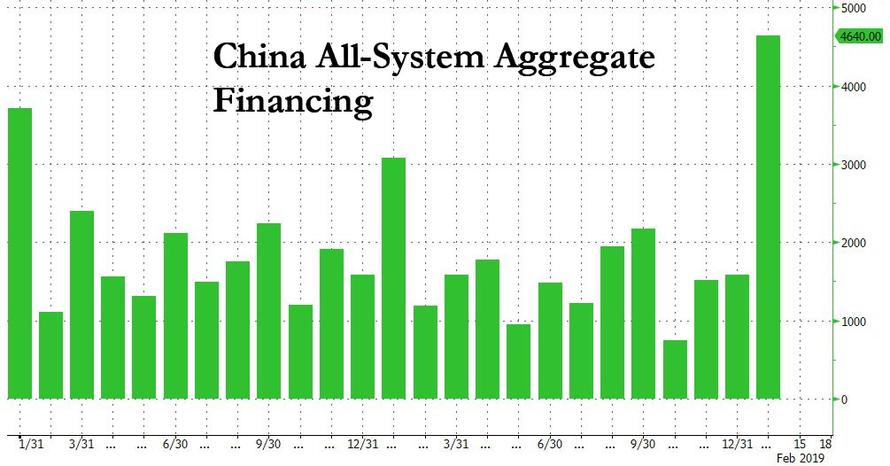

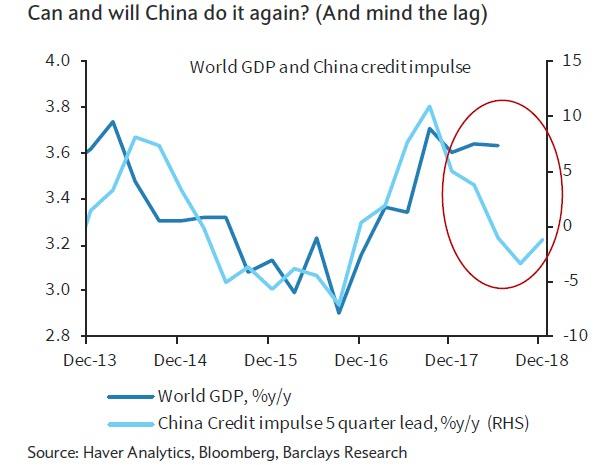

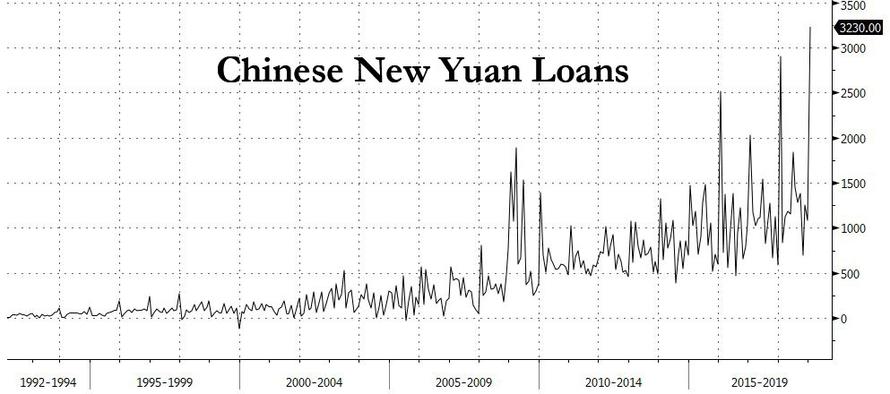

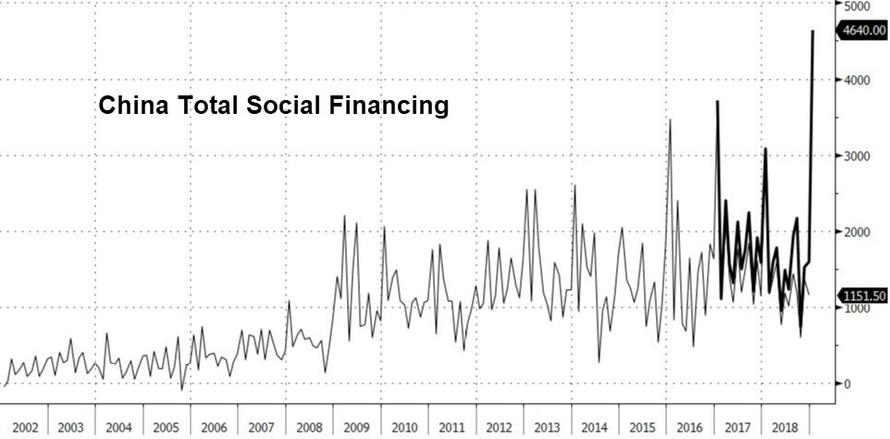

ii) this is what caused the Dow to skyrocket 500 points from its lows: China unleashes a massive credit injection. This is good for gold. China unleashed a huge 3.23 trillion yuan (482 billion dollars worth of loans). The Total Social Financing (TSF) rose to a massive 4.64 trillion yuan or 685 billion dollars. The new TSF loans now total 30 billion USA dollars. This is a massive debt and they will implode

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK/CHINA

Just after UK Defense Secretary Williamson threatened to send a warship to the Pacific and namely into the South China Seas, China dramatically canceled UK trade talks

(courtesy zerohedge)

ii)SPAIN

Sanchez calls for an election on April 28 after losing his budget battle. Should be an interesting few months

(courtesy zerohedge)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran/SYRIA/USA

Our resident expert on Middle East affair , Tom Luongo discusses that it is Putin who is pushing for peace. He will holding back Erdogan from attacking the Kurds. He is angry at Erdogan for not finishing off ISIS in Idlib province.

(courtesy Tom Luongo)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

9. PHYSICAL MARKETS

i)To prevent high frequency trading which accounts for some of the rigging in the precious metals, Ice is going to use speed bumps. The problem is that this is such a tiny fraction of the rigging.

ii)Mainstream media finally catching on as they state their favourability to gold/

( the Economist/London/GATA)

iii)The world is catching on the phony government stats coming out. The latest was on inflation…

( Li/CNBC/GATA)

iv)Amazing: Sibanye announces that it may have to cut 6,000 mining jobs in South Africa due to losses. Successive governments in South Africa could not care less about gold market suppression

(Sanderson/London’s Financial Times/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

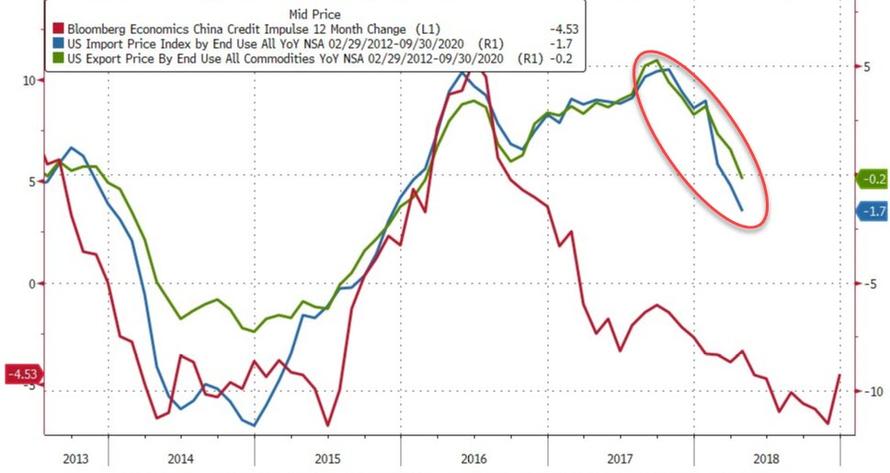

a)With China imploding we expect to see USA import and export prices tumble and lo and behold we received just that as China exports its deflation big time. This is very worrisome for manufacturers as they try and compete with China.

( zerohedge)

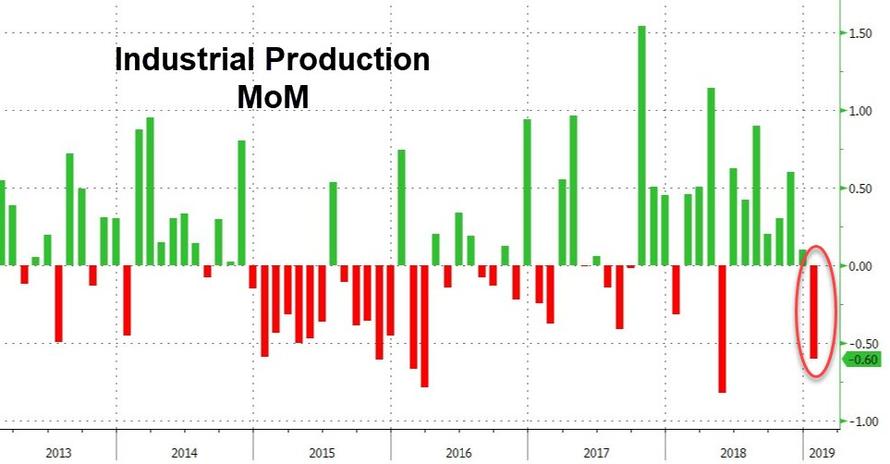

b)Another biggy!! USA industrial production plunges in January with the key manufacturing sector contracts badly. Good reason for the stock market to rise.. (it was caused by the massive stimulus from China)

(courtesy zerohedge)

c)Soft data U. of Michigan sentiment rebounds but inflation forecasts hit a record low. This data comes out right after government goes back to work

( zerohedge)

b)Socialized healthcare exposes reality: 30,000 dead due to record long hospital waiting times. It takes months to have corrective surgery and I am a prime example of it in Canada,.

iv)SWAMP STORIES

a)A New Jersey pension fund might ditch a hedge fund, Chatham Asset Management, that owns 80% of the National Enquirer which is in deep financial straits.

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 6492 CONTRACTS DOWN TO 107,410 CONTRACTS. AFTER MARCH, APRIL ADVANCES TO 85 CONTRACTS FOR A GAIN OF 13 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 4422 CONTRACTS UP TO 72,684 CONTRACTS.

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i

Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

– Invest in gold as a hedge, in pensions & as a store of value – Rogoff

– Investing in and owning gold as a hedge will become more important as it will have “enormous value” in a cashless society

– Bitcoin and cryptocurrencies are not an effective replacement for paper money … but gold’s role is likely to increase as cash is used less and “the trend towards digital currencies” will benefit gold

– “There is an incredible disconnect between the fact that cash is disappearing in legal, tax-compliant transactions but exploding in terms of how much central banks are printing” says Rogoff

– It makes sense for investors, HNW individuals, pension funds and central banks to invest a “percentage of their assets in gold” as a hedge

– “Gold is also likely to increase in value” as central bank and global investment demand increases

– “As a hedge, gold has enormous value…” Rogoff concludes

News and Commentary

Gold ends lower, building on a weekly decline (MarketWatch.com)

Gold rises as weak U.S. economic data drags dollar (Reuters.com)

Trump to sign border bill, declare emergency: McConnell (Bloomberg.com)

Weakest U.S. retail sales since 2009 cast pall over economy (Reuters.com)

Bitcoin trading in crisis-stricken Venezuela has just hit an all-time high (CNBC.com)

South African Gold Output Plunges Most in Six Years in December (Bloomberg.com)

The Case for Gold – The Economist (Gata.org)

Headlines Say There’s No Inflation, But Look at What’s Getting More Expensive (CNBC.com)

Intercontinental Exchange admits metals market vulnerability to rigging (Bloomberg.com)

6,000 miners to lose jobs but South Africa doesn’t care about gold price suppression (FT.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

14 Feb: USD 1,305.65, GBP 1017.49 & EUR 1,158.50 per ounce

13 Feb: USD 1,311.15, GBP 1017.45 & EUR 1,158.79 per ounce

12 Feb: USD 1,311.60, GBP 1021.21 & EUR 1,163.00 per ounce

11 Feb: USD 1,306.40, GBP 1014.81 & EUR 1,157.08 per ounce

08 Feb: USD 1,311.10, GBP 1012.04 & EUR 1,156.65 per ounce

07 Feb: USD 1,310.00, GBP 1009.49 & EUR 1,154.11 per ounce

06 Feb: USD 1,313.35, GBP 1013.51 & EUR 1,152.86 per ounce

Silver Prices (LBMA)

14 Feb: USD 15.58, GBP 12.17 & EUR 13.83 per ounce

13 Feb: USD 15.69, GBP 12.13 & EUR 13.85 per ounce

12 Feb: USD 15.81, GBP 12.30 & EUR 14.01 per ounce

11 Feb: USD 15.70, GBP 12.16 & EUR 13.88 per ounce

08 Feb: USD 15.78, GBP 12.18 & EUR 13.92 per ounce

07 Feb: USD 15.71, GBP 12.20 & EUR 13.87 per ounce

06 Feb: USD 15.73, GBP 12.15 & EUR 13.82 per ounce

Recent Market Updates

– Valentine’s Day Record Spending Due to Gold Love Trade?

– Gold Prices In Pounds and Euros Gain More as Economic Growth Falters in the UK and EU

– Irish Investors Storing Their Gold Bullion In Ireland

– Large Gold Bullion Shipment Moves From London to Dublin Gold Vaults As Brexit Concerns Deepen

– Store Gold Bullion In Safest Ways – Learning from Tragic Venezuela Today

– The Vital Importance of Gold As A Strategic Asset In 2019

– ITALEXIT: Italy’s Debt Crisis Will “Rock EU To Its Foundations” – Banking Crisis and Euro Exit Are Likely

– “Right” Trump and “Left” Ocasio-Cortez Will Join Forces And Debase The Dollar

– 7 Financial Truths In An Uncertain 2019

Intercontinental Exchange admits metals market vulnerability to rigging

Submitted by cpowell on Thu, 2019-02-14 16:04. Section: Daily Dispatches

‘Flash Boys’-Style Speed Bump Planned for Futures Markets

By Nick Baker

Bloomberg News

Wednesday, February 13, 2019

Intercontinental Exchange Inc.’s futures market wants to join the battle against the fastest traders.

The Atlanta-based exchange plans a 3-millisecond trading delay, or speed bump, for its gold and silver futures contracts, according to a regulatory filing. The U.S. Commodity Futures Trading Commission today asked for public comment on the proposal.

Michael Lewis’s 2014 book, “Flash Boys,” popularized the idea of using speed bumps to curb the light-speed pace of modern financial markets and prevent alleged abuses of so-called high-frequency traders. Lewis’ protagonists, the founders of IEX Group Inc., introduced a delay on their stock exchange in 2016, and a tiny equities market ICE owns, NYSE American, also has one. But this latest move would bring a speed bump to derivatives markets.

The delay would be introduced “initially” for gold and silver, areas where ICE currently does very little business. An ICE spokesman declined to say whether it would later be applied to other markets. ICE is a leader in other products such as oil futures. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-02-13/a-flash-boys-style-sp…

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

The world is catching on the phony government stats coming out. The latest was on inflation…

(courtesy Li/CNBC/GATA)

No inflation? What planet do the government statisticians live on?

Submitted by cpowell on Thu, 2019-02-14 16:22. Section: Daily Dispatches

Headlines Say There’s No Inflation, But Look at What’s Getting More Expensive

By Yun Li

CNBC, New York

Wednesday, February 13, 2019

U.S. consumer prices were unchanged in January on the headline level, but looking under the hood, some of the most basic consumption including rent, food and medical care are all getting more expensive.

“Please stop telling me there is no inflation,” Peter Boockvar, chief investment officer at Bleakley Advisory Group, said in a note Wednesday after the consumer price index report. He pointed out that services inflation excluding energy has grown persistently with a 0.2 percent increase month over month and 2.8 percent rise year over year.

…

The headline figure saw no change in January largely because cheaper gasoline offset the increases in other areas. Gasoline prices fell 5.5 percent last month after dropping 5.8 percent in December.

On the surface, the headline CPI number is showing that inflation is contained. But the core rate of inflation, which doesn’t consider energy and food prices because they fluctuate easily, has risen 0.2 percent for each of the past five months. …

… For the remainder of the report:

https://www.cnbc.com/2019/02/13/headlines-say-theres-no-inflation-but-lo…

end

Mainstream media finally catching on as they state their favourability to gold/

(courtesy the Economist/London)

Yikes! Times ARE changing — The snots at The Economist pontificate favorably about gold

Submitted by cpowell on Fri, 2019-02-15 01:52. Section: Daily Dispatches

Catching the Gold Bug

When Trouble Strikes, Where Should You Hide? The Case for Gold

The Grand Central Theory of Markets

The Buttonwood column

The Economist, London

Thursday, February 14, 2019

https://www.economist.com/finance-and-economics/2019/02/16/when-trouble-…

Imagine you have an assignation in New York.

You have not been told where you should meet the other person and she has not been told where to meet you. You have no understanding of where to find her or where she might usually be found. She is as ignorant of you.

You cannot communicate. You must somehow guess how to find each other and make those guesses coincide.

Where should you go? And at what time of day?

…

A good answer is Grand Central Station at noon. That was the response of the majority asked by Thomas Schelling, a game theorist and Nobel prize winner in economics, in experiments reported “The Strategy of Conflict,” published in 1960. People are often able to act tacitly in concert if they know that others are trying to do the same, said Schelling. Most situations throw up a clue, a “focal point,” around which to co-ordinate, even if it takes imagination as much as logic to find it.

Now imagine the world economy goes into a tailspin. There is panic selling of risky assets. Where should you seek safety? Cash is the most liquid asset; but which kind? The dollar is a natural focal point. Yet America’s fiscal indiscipline and its sizable current-account deficit might give pause. Other currencies have their faults too. There is one other destination you might consider, if only because others are starting to think the same way. And that is gold.

A lot of people respond to this suggestion by backing away gently while claiming an urgent appointment elsewhere. Gold keeps some strange company. Ardent gold bugs seem to know a lot about firearms, the best places with access to fresh water, and the best ways to preserve food. And what, after all, are its merits? It is supposed to be an inflation hedge. Yet there is not much of that to hedge against. Inflation barely threatens the standard rich-world target of 2 percent. And after gaining $100 an ounce recently, gold is hardly cheap by past standards, in inflation-adjusted terms.

Consider the alternatives, though. The euro is flawed. It has no unique sovereign issuer to stand behind it. And the yuan is not a currency you can trade easily. The yen, admittedly, is a good bolthole. Japan’s net foreign assets — what Japan’s residents own abroad minus what they owe to foreigners — are worth $3 trillion, or 60 percent of annual GDP. In a crisis, some of that capital comes home, pushing up the yen. Those seeking safety follow suit. The Swiss franc has similar appeal.

Still, there is a downside. Past form suggests both countries are likely to cap a rise in their currencies by printing more of them. Short-term interest rates have been negative for years in Japan, Switzerland and the euro area, in part to deter currency strength. By contrast gold’s yield — zero — seems almost racy.

And the dollar? As a global currency it has no peers. During the last big crisis, in 2008, the dollar rallied. There had been lots of global borrowing in greenbacks. So when trouble struck, there was a scramble for dollar liquidity. The world still has a large short position on the dollar, in that there has been heavy borrowing in the currency beyond America’s shores. Yet the world is also long dollar assets. America’s listed firms make up the bulk of global stock market indices. Its government-bond market has swollen to 100 percent of GDP. And the dollar still accounts for the bulk of official reserves.

Tellingly, the managers of those rainy-day funds seem a mite concerned that they are crammed into the same spot. The share of dollars in the $10.7 trillion of reserves reported to the IMF has dropped from over 65 percent when Donald Trump was elected president to below 62 percent in the latest figures. This may in part be a response to growing political risks.

The dollar’s central role in global trade and finance allows America to impose financial sanctions to great effect. It has been doing so with greater frequency, so Russia, for instance, has drastically cut the dollar share of its reserves, to 22 percent, while raising the shares of euros and yuan. Russia has been a big buyer of gold, too. In that, it is not alone. Net purchases of gold by central banks rose by 74 percent last year to the highest since 1971, the year the dollar’s peg to the gold price broke.

Now, as then, there are growing concerns that the dollar is a crowded trade. It is as if there are so many people in Grand Central Station that it is impossible to find the person you’re supposed to meet there—or if you do find them, you cannot fight your way out without mishap. It is why gold is starting to appeal again as a spot to converge upon. You would have to mix with some strange people there. But can you really say that you would never visit?

end

Amazing: Sibanye announces that it may have to cut 6,000 mining jobs in South Africa due to losses. Successive governments in South Africa could not care less about gold market suppression

(Sanderson/London’s Financial Times/GATA)

6,000 miners to lose jobs but South Africa doesn’t care about gold price suppression

Submitted by cpowell on Fri, 2019-02-15 06:20. Section: Daily Dispatches

South Africa’s Sibanye Weighs Slashing 6,000 Jobs to Stem Gold Losses

By Henry Sanderson

Financial Times, London

Thursday, February 14, 2019

South African miner Sibanye-Stillwater said it may have to cut nearly 6,000 jobs as part of a restructuring of its gold mines due to ongoing losses.

Sibanye said it would enter into formal consultations with its workforce following “numerous initiatives to contain losses” at certain shafts at its Beatrix and Driefontein gold mining operations.

…

.The talks come following strikes and a number of deaths at Sibanye’s deep-shaft gold mining operations last year.

The company said it may have to cut roughly 5,870 jobs and 800 contractors depending on the outcome of the formal consultation. Sibanye employs around 61,000 people in South Africa.

“Contemplating potential restructuring of this nature is never taken lightly and we are aware of the possible impact on many of our colleagues,” Neal Froneman, chief executive of Sibanye, said. “Our best attempts to address the ongoing losses at these operations, have, however, been unsuccessful and sustaining these losses may threaten the viability of our other operations.” …

… For the remainder of the report:

https://www.ft.com/content/5a08bcf0-3052-11e9-ba00-0251022932c8

LAWRIE WILLIAMS:: Russia closing gap on China as World No.1 gold miner?

Assuming the veracity of the latest figures from official sources in China and Russia the latter is expanding its gold output while the former’s output is contracting. The latest figures are as follows: China’s 2018 gold output, as announced by the China Gold Association, was around 401 tonnes, down from 426 tonnes in 2017 – a fall of almost 6%, while Russia’s 2018 gold output was up nearly 2.5% to 314 tonnes according to the country’s Finance Ministry. If the figures are correct, and the trend continues, Russia could surpass China as the world’s largest gold producer within around 4 years given that China’s output is seen as continuing to fall given ever-increasing environmental strictures, while Russia’s output is continuing to advance.

Russia has already overtaken China in the size of its official gold reserves as reported to the IMF, although we continue to express our doubts about the veracity of the Chinese total (See: China officially adds to gold reserves again)

In 2017, according to the major gold analytical consultancies, Russia was the third largest global gold producer – but vying with Australia for second place. Interestingly the aforementioned consultancies invariably come up with lower annual estimates for Russian gold production than that announced by the Finance Ministry – but they also come up with lower estimates for Australian domestic production than that calculated by Melbourne- based consultancy Surbiton Associates, which should, on past performance, be publishing its latest estimate for Australia’s 2018 gold production in around two to three weeks’ time. Last year Surbiton put Australian output at 301 tonnes and, if anything we would take the Surbiton figure as being perhaps closer to that nation’s true position than the big global consultancies’ estimates given Surbiton’s almost total specialisation in the Australian gold sector.

Whether global gold output will be seen to have fallen, plateaued, or risen marginally in 2018 compared with the prior year still remains open to question. Notably another of the world’s top gold mining countries – South Africa – has ,according to its national statistical body, Statistics South Africa, seen a sharp decline in its 2018 gold output. During the second half of the year at least the country’s gold output saw a double digit percentage fall virtually every month. We suspect that once the final annual figures are tallied, the country which once dominated global gold production will find itself still in place as the world’s seventh largest gold producer but may well see its total output falling by around 20 tonnes to the mid 130 tonne level – a very significant drop.

We shall have to wait and see what the major analytical consultancies make of the global picture when they publish their annual assessments – probably not until end- March/early April. We increasingly suspect that they may show global gold output will have peaked in 2018, given the lack of major new discoveries and a global downturn in gold exploration activity, coupled with declining grades at some existing operations and forced closures of some older marginal mines as they become uneconomic. Perhaps Peak Gold is actually with us at last!

15 Feb 2019

-END-

Gold production plunges to its worst level since 2012

ECONOMY / 15 FEBRUARY 2019, 10:30AM / KABELO KHUMALO

JOHANNESBURG – The ramifications of the nearly four- month-long strike at Sibanye-Stillwater’s gold division by the Association of Mineworkers and Construction Union (Amcu) were yesterday laid bare with gold production in December plunging to its worst level since October 2012.

Data from Statistics South Africa showed that gold output tanked 31 percent year-on-year in December.

Production in the mining sector as a whole fell 4.8 percent year-on-year in December. Full mining production decreased 1.6 percent.

FNB chief economist Mamello Matikinca-Ngwenya said the plunge in gold production had detracted 4.6percentage points from the headline reading.

“This can likely be ascribed to the Amcu strike at the Sibanye-Stillwater gold operation,” Matinkica- Ngwenya asserted.

“We are concerned about the outlook for 2019, despite the relatively weak 2018 base as rising input costs, low commodity prices, electrical generation and slowing Chinese growth present material downside risks to the mining sector,” he added.

About 15000 Amcu members at Sibanye downed tools in November last year, demanding an R1000 annual wage increase for the next three years.

They have clashed with colleagues from the rival National Union of Mineworkers, which, alongside other unions, signed a deal with Sibanye, and whose members have returned to work.

Professor Francis Petersen of the University of the Free State said that production output from South African gold mines had been declining over the past seven years.

“South Africa’s gold production accounts for only 4 percent of the global gold production and new investment in this sector is highly unlikely in South Africa,” Petersen said.

Other data from StatsSA also showed that iron ore output fell 14.3percent on an annualised basis, while production of other metallic minerals plunged 18.4percent on a yearly basis.

With December’s official activity data now all in, the figures indicate a soft end to 2018.

Retail sales in December also decreased by 1.4percent year-on-year, the worst figure since January 2017, while manufacturing output inched up just 0.1 percent on an annualised basis – its weakest increase since September.

Capital Economics economist John Ashbourne said that the data was more positive when looked at in the quarter- on-quarter, seasonally-adjusted annualised rate that aligns with official gross domestic product.

“Mining output was actually stronger over the quarter as a whole than it had been in quarter three, while the slowdowns in manufacturing and retail were modest,” said Ashbourne.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7709/

//OFFSHORE YUAN: 6.7792 /shanghai bourse CLOSED DOWN 37.32 POINTS OR 1.37% /

HANG SANG CLOSED DOWN 531.21 POINTS OR 1.87%

2. Nikkei closed DOWN 239.08 POINTS OR 1.13%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 97.08/Euro FALLS TO 1.1269

3b Japan 10 year bond yield: FALLS TO. –.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.47/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.70 and Brent: 64.94

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.10%/Italian 10 yr bond yield DOWN to 2.88% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.78: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.86

3k Gold at $1317.20 silver at:15.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 66.67

3m oil into the 54 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.47 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0062 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1339 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.10%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.66% early this morning. Thirty year rate at 2.99%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2674

Early futures jump on trade deal optimism. That faded fast on news from the Wall Street Journal that China/USA trade talks are deadlocked

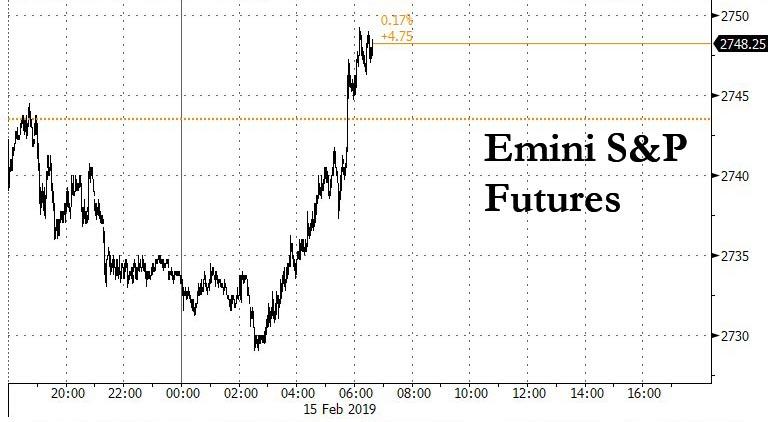

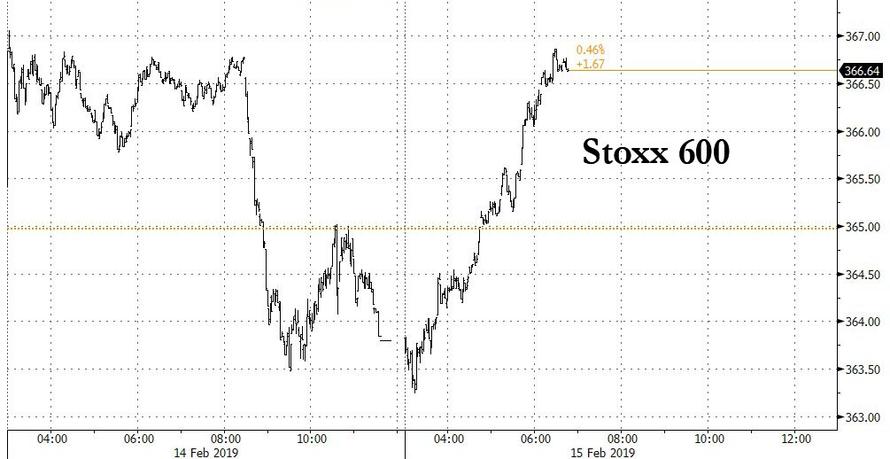

S&P Futures Reverse Overnight Losses As Trade Talks Optimism Returns

After a lackluster start to global markets on the last day of the week following the conclusion of yet another indecisive round of trade talks between the US and China where nothing was resolved aside from reports of a possible MOU to lay out “next steps” in the ongoing negotiations, global markets rebounded as ye olde “trade deal optimism” returned after China’s president said trade talks would continue in Washington DC next week (as if there was any other option with the March 1 deadline looming). This helped reverse overnight stock losses, with US equity futures jumping almost 20 points from session lows, just as Europe opened for trade, with the Stoxx 600 rising 0.8% on “hope.”

“Negotiations between both sides have achieved important progress in another step,” president Xi said after the 6th trade talks wrapped up in Beijing, quoted China’s Xinhua News Agency. “Next week, both sides are going to meet in Washington. I hope you keep up the good work, and push for a mutually-benefiting and win-win agreement.”

Xi said he values the “good working relationship” with President Donald Trump very much, and is willing to keep in touch with him in various ways. He added that China was “willing to solve the bilateral economic disputes and frictions through cooperation, and push for an agreement that both sides can accept. But cooperation has principles.”

Echoing the upbeat mood from the meeting, Treasury Secretary Steven Mnuchin sounded a positive note on Friday, saying he and U.S. Trade Representative Robert Lighthizer held “productive meetings” with China’s Vice Premier Liu He. They both also met Xi later in the day.

Steven Mnuchin

✔@stevenmnuchin1

Productive meetings with China’s Vice Premier Liu He and @USTradeRep Amb. Lighthizer.

Adding to the optimism was Trump’s uber trade hawk, Robert Lighthizer who said “We feel we have made headway on very, very important and difficult issues,” adding that “we have additional work we have to do but we are hopeful.”

Trade tensions between the U.S. and Beijing continue to dictate sentiment as the two sides race to reach a deal that would avert a tariff increase on Chinese goods by March 1. Growth concerns have also plagued investors after China’s factory inflation decelerated on softening demand.

And even though the two sides remained far apart this week on structural reforms to China’s economy that the U.S. has requested, according to three U.S. and Chinese officials quoted by Bloomberg, who said it would likely take a meeting between Xi and Trump to seal a deal, kicking the can was all algos needed to unleash global buying programs, and world markets were once again a familiar sea of green as we close out the week.

Propped up by this can-kicking optimism, European stocks burst out of the gate, with banks and media stocks pushing the Stoxx Europe 600 Index higher after a slow start, and wiping out all of Thursday’s losses. Even so, European car stocks, a bellwether for the continent’s economy, fell 1 percent as sales dropped for the 5th month in a row, and the deadline approached for a U.S. Commerce Department that could lead to the imposition of tariffs.

Sectors in Europe were mixed in early trading, with some outperformance seen in telecom names, after Telecom Italia (+6.0%) are towards the top of the Stoxx 600 after Italy’s state holding CDP said the board has authorisation to increase their stake to 10% in the next 12 months. Other notable movers include, Vivendi (+7.6%) who are topping the Stoxx 600 following their earnings release and comments that Bollore is to step down from the Co’s board in April. Separately, RBS (+1.3%) are in the green, following a beat on Q4 pre-tax operating profit and a special dividend for 2018. EDF (-4.6%) are near the bottom of the Stoxx 600, after their earnings release this morning.

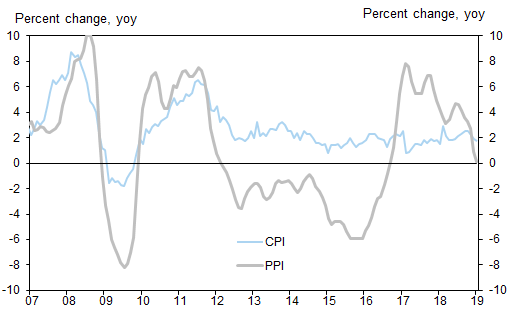

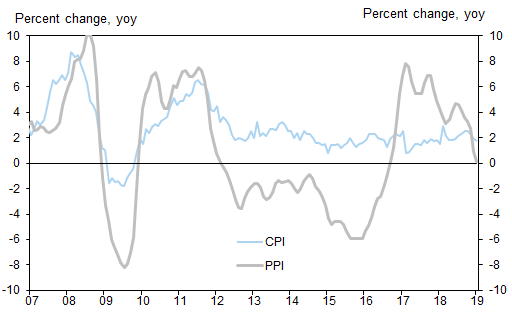

Meanwhile, Asian shares retreated, perhaps because today’s “trade deal optimism” emerged too late to push Asian stocks higher, with Chinese stocks falling as weak factory prices highlighted the tough environment for industrial profitability, adding to other disappointing economic data. China’s CPI inflation eased further to 1.7% Y/Y in January from 1.9% in December, below consensus expectations (in month-on-month terms, headline CPI prices continued to decline by 0.6% in Jan). At the same time, year-over-year PPI inflation moderated further to 0.1% yoy in January, the lowest since October 2016, with prices down 4.7% mom s.a. ann in January. The petroleum industry still saw the largest deceleration in inflation, followed by chemicals and ferrous/nonferrous metals.

Asia-Pacific shares outside Japan fell 1.1 percent as market in Seoul, Tokyo and Shanghai all lost ground. Worries about the United States, which many considered a bright spot in the world economy, offset some optimism over trade talks in Beijing between the United States and China.

One remarkable aspect of the overnight session that was ignored by some traders was the record surge in China’s total aggregate financing, which exploded higher by a record 4.64 trillion yuan in January, far above the 3.31 trillion yuan expected, and nearly three times greater than December’s 1.59 trillion total. While New Loans beat expectations only modestly, printing at 3.23 trillion Yuan, the surge in aggregate credit was enough to push M2 from record lows, rising 8.4% from December’s 8.1%, and above the 8.2% expected.

With China’s credit creation by far the most important variable for the global economy, keep a close eye on this series for the next few months to see if Beijing can reflate markets.

In Washington, Congress sent President Donald Trump legislation he said he’ll sign to avoid another government shutdown as a new dispute looms over his decision to declare a national emergency to get more federal money for a border wall.

In the latest Brexit news, PM May’s officials are reportedly preparing to compromise on their demands to re-write the Brexit agreement and tell the EU it doesn’t want to renegotiate the agreement. EU and UK Brexit discussions are reportedly planned for Monday in Brussels where Brexit Secretary Barclays will meet with EU’s Chief Brexit Negotiator Barnier. Sky News’ Tamara Cohen tweets “Dominic Grieve says a dozen pro-European ministers would resign if we were heading for no deal at end of Feb – including several in cabinet.”

In currencies, the Japanese yen and other safe-haven currencies made gains as the market awaited developments in the trade talks. The dollar remained fairly robust in spite of the U.S. retail figures, trading up 0.2 percent at 97.1 against a basket of major currencies. The euro was 0.2 percent lower at $1.1278 and headed for a second week of losses. It is down by 1.7 percent so far this year after discouraging economic data from the euro zone. In the U.K., the pound saw choppy trading after Parliament refused to endorse Prime Minister Theresa May’s approach to resolving the Brexit deadlock.

In rates, the 10-year U.S. Treasuries yield fell to 2.6483 percent, wiping out most of its rise this week. Italian bonds pared declines as equities rebound, while core bonds are steady to slightly outperform semi-core. Spain is little moved by PM Sanchez calling a snap election for April 28.

Elsewhere, oil climbed on supply cuts and reduced output. Brent (+0.5%) and WTI (+0.5%) are firmer as markets received updates on US-China trade talks. Despite being firmer, prices are off session highs with Brent slipping back below USD 65.0/bbl after moving past this level for the first time this year earlier in the session Elsewhere, Saudi Arabia has suspended production at its Safaniyah offshore oilfield which is the world’s largest offshore oilfield with a capacity of up to 1.5mln BPD; production may be suspended until March. However, this is not expected to significantly impact Saudi Arabia’s supply level, with Saudi Aramco subsequently confirming that their facilities, including this one, are safe and normal. Looking ahead we have the Baker Hughes Rig count which last week say total rigs increase by 4. Gold (+0.3%) is largely unchanged in spite of the cautious risk environment and some dollar strength ahead of the 2nd largest SOMA day with USD 23.3bln of liquidity being drained.

Market Snapshot

- S&P 500 futures unch at 2,742.00

- STOXX Europe 600 up 0.2% to 364.57

- MXAP down 0.9% to 155.73

- MXAPJ down 1.1% to 509.67

- Nikkei down 1.1% to 20,900.63

- Topix down 0.8% to 1,577.29

- Hang Seng Index down 1.9% to 27,900.84

- Shanghai Composite down 1.4% to 2,682.39

- Sensex down 0.4% to 35,741.69

- Australia S&P/ASX 200 up 0.1% to 6,066.10

- Kospi down 1.3% to 2,196.09

- German 10Y yield fell 0.6 bps to 0.097%

- Euro down 0.2% to $1.1278

- Italian 10Y yield rose 1.9 bps to 2.444%

- Spanish 10Y yield rose 1.1 bps to 1.253%

- Brent futures up 0.3% to $64.78/bbl

- Gold spot up 0.2% to $1,315.38

- U.S. Dollar Index up 0.1% to 97.04

Top Overnight News

- Treasury Secretary Steven Mnuchin sounded a positive note on Friday as U.S.-China trade talks drew to a close in Beijing, as both sides tried to reach a deal that would avert a tariff increase on Chinese goods by March 1. China and U.S. will continue trade talks with the same group of people next week, SCMP reports, citing an unidentified person

- In closed-door sessions this week, the U.S. and China have failed to narrow the gap around structural reforms to China’s economy that the U.S. has requested, according to three U.S. and Chinese officials who asked not to be identified because the talks were private. They said it would likely take a meeting between Xi and President Donald Trump to seal a deal

- U.K. Brexit Secretary Stephen Barclay privately told the EU’s chief negotiator, Michel Barnier, the U.K. doesn’t need to re-open the divorce agreement and would accept other ways to address British concerns, a person familiar with the talks said

- Spanish Prime Minister Pedro Sanchez called a snap election, pitching the country into a period of fresh political uncertainty after a parliament veto of his budget laid bare his minority government’s inability to pass key legislation

- Europe equity funds saw outflows of $5.9b in the week to Feb. 13, their second largest weekly outflows on record, according to BofAML strategists citing EPFR Global data

- The combined units of Pimco and Allianz Global Investors faced 31 billion euros ($35 billion) of outflows from their funds in the final three months of the year, helping to drive assets under management down by 51 billion euros. Net outflows at compared with inflows of 27 billion euros in the third quarter

- British Prime Minister Theresa May’s officials are preparing to compromise on their demands for a re-write of the Brexit agreement, according to a person familiar with the matter

- Donald Trump plans to use unilateral authority to spend more than $8 billion to construct physical barriers along the U.S.-Mexico border, according to a White House official, a maneuver that risks provoking a lengthy legal battle over presidential powers. Congress sends Trump bill to avert shutdown amid emergency plan

- China’s factory inflation decelerated for a seventh month, adding to concerns about the return of deflation and the impact that will have on already weak corporate profits

- The Australian dollar has been buffeted by cross-currents at home and abroad, but its decline has provided some support to growth, Reserve Bank of Australia Assistant Governor Christopher Kent said Friday

- Oil headed for its biggest weekly gain in a month as the OPEC+ coalition’s supply cuts overshadowed renewed concern over whether the world’s two largest economies will be able to reach a trade deal

Asian equity markets traded mostly negative following the weakness of their counterparts in US, where sentiment was dampened by a surprise contraction in Retail Sales. Furthermore, participants were also wary due to events in Washington where Congress passed the government funding and border security bill, which President Trump is expected to sign but is also anticipated to declare a national emergency. ASX 200 (+0.1%) and Nikkei 225 (-1.1%) were lower from although the Australian benchmark later recovered led by strength in telecoms and energy, while losses in Japan were exacerbated by a firmer currency. Elsewhere, Hang Seng (-1.8%) and Shanghai Comp. (-1.4%) weakened after further PBoC inaction resulted to a liquidity drain of CNY 680bln for the week and as participants digested softer than expected CPI data, while ongoing trade talks further added to the cautious tone with US and China said to be far apart on reform demands. Finally, 10yr JGBs tracked the recent gains in T-notes as the risk averse tone spurred a flight to safety, although some of the gains were eventually pared following a softer 10yr inflation-indexed auction.

Top Asian News

- Khazanah Said to Raise $102m Selling BDO Bank Shares at Bottom

- Hillhouse Dumped Tech Stocks Just as They Were Headed for Rally

- Philippine Stocks Upgraded to Overweight at Daiwa on Inflation

- China’s Slowing Factory Prices Add to Deflation, Profit Concerns

Major European equities have drifter higher from the open [Euro Stoxx 50 +0.7%] amidst trade optimism between the world’s two largest economies. Initial underperformance was experienced in the Dax (+0.4%) weighed on by the likes of Wirecard (-0.6%) alongside auto-names with Daimler (-0.5%), Volkswagen (-0.3%) and BMW (-0.8%) in the red following poor new EU27 car registrations data this morning, though optimistic trade developments somewhat supported sentiment. Both sides have expressed progress in talks, though dialogue is set to continue next week as not enough was agreed on to seal a deal. Sectors are similarly mixed with some outperformance seen in telecom names, after Telecom Italia (+6.0%) are towards the top of the Stoxx 600 after Italy’s state holding CDP said the board has authorisation to increase their stake to 10% in the next 12 months. Other notable movers include, Vivendi (+7.6%) who are topping the Stoxx 600 following their earnings release and comments that Bollore is to step down from the Co’s board in April. Separately, RBS (+1.3%) are in the green, following a beat on Q4 pre-tax operating profit and a special dividend for 2018. EDF (-4.6%) are near the bottom of the Stoxx 600, after their earnings release this morning.

Top European News

- EDF Declines as 2019 Profit Outlook Falls Short of Expectations

- U.K. Retail Sales Jump As Discounts Spur Spending on Clothing

- Spain’s Sanchez Calls Snap Election for April 28 After Stalemate

- Europe Car Sales Drop Signaling Trouble for Region’s Economy

- Scout24 Gets $5.5 Billion Boost to Rival Axel Springer, Ebay

In FX, GBP is back on the 1.2800 handle, albeit barely, and Eur/Gbp has slipped back towards 0.8800 in wake of a much bigger than forecast rebound in UK retail sales. However, Brexit remains at the fore and PM May suffered another heavy defeat in Parliament ahead of the next meaningful vote at the end of February, so the Pound is still prone to set-backs in the run up to March 29, at least.

- JPY – Usd/Jpy has pulled back further from Thursday’s new 2019 high, and an even more pronounced reversal could bring big option expiries into play at the 110.00 strike (2.6 bn). The rationale, less euphoria/optimism on the US-China trade front as talks in Beijing ended on a promising note, but with core issues still unresolved and more negotiation now scheduled to take place in Washington next week as the clock ticks down to March 1’s tariff deadline (unless that date is extended).

- CAD/NZD/AUD/EUR/CHF – All narrowly mixed against a relatively static Greenback, as the DXY nestles just above the 97.000 level, with the Loonie pivoting 1.3300 after yesterday’s weak Canadian data trumped US retail sales, claims and PPI misses against the backdrop of stalling oil prices. Meanwhile, the Kiwi continues to outflank the Aussie down under, as Nzd/Usd hovers just below 0.6850 and Aud/Usd clings to 0.7100, with the cross sticking close to recent lows circa 1.0375. Note, comments from RBA’s Kent hardly helped the Aud, as he essentially welcomed the weaker currency on the grounds that the domestic economy has slack and inflation is low. Elsewhere, the single currency remains heavy on rebounds through 1.1300 and also has hefty option expiry interest to contend with as 1 bn sits between 1.1250-60 and 1.3 bn from 1.1270-80, while SOMA positioning could add even more downside pressure, as today is the 2nd largest on record (Usd23.3 bn). The Franc is still meandering off recent lows within a tight 1.0070-50 range and equally restrained vs the Eur between 1.1355-35.

In commodities, Brent (+0.5%) and WTI (+0.5%) are firmer as markets received updates on US-China trade talks, in the form of a memorandum of understanding, while recent reports indicate that talks have concluded. Despite being firmer, prices are off session highs with Brent slipping back below USD 65.0/bbl after moving past this level for the first time this year earlier in the session Elsewhere, Saudi Arabia has suspended production at its Safaniyah offshore oilfield which is the world’s largest offshore oilfield with a capacity of up to 1.5mln BPD; production may be suspended until March. However, this is not expected to significantly impact Saudi Arabia’s supply level, with Saudi Aramco subsequently confirming that their facilities, including this one, are safe and normal. Looking ahead we have the Baker Hughes Rig count which last week say total rigs increase by 4. Gold (+0.3%) is largely unchanged in spite of the cautious risk environment and some dollar strength ahead of the 2nd largest SOMA day with USD 23.3bln of liquidity being drained. Elsewhere, Vale’s CEO says that the miner’s safety procedures have not worked; while researchers at World Mine Tailings Failures have stated that these events are becoming more frequent.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 7, prior 3.9

- 8:30am: Import Price Index MoM, est. -0.2%, prior -1.0%

- 8:30am: Export Price Index MoM, est. -0.1%, prior -0.6%

- 9:15am: Industrial Production MoM, est. 0.1%, prior 0.3%;

- Capacity Utilization, est. 78.7%, prior 78.7%

- Manufacturing (SIC) Production, est. 0.0%, prior 1.1%

- 10am: Mortgage Delinquencies, prior 4.47%; MBA Mortgage Foreclosures, prior 0.99%

- 10am: U. of Mich. Sentiment, est. 93.5, prior 91.2; Current Conditions, est. 111.6, prior 108.8; Expectations, est. 85.5, prior 79.9

- 4pm: Net Long-term TIC Flows, prior $37.6b

- 4pm: Total Net TIC Flows, prior $31.0b

DB’s Jim Reid concludes the overnight wrap

Wow. That was the hottest Valentines’ Day I’ve experienced since I was in my early 20s. I was even dripping with sweat last night as a result. Yes in the U.K. yesterday an “African plume” made it the warmest February 14th since 1988 and I’ve just chosen this week to start cycling to the station again so given I was dressed for deep winter I got home dripping with sweat. If this warm weather carries on all weekend they’ll only be one outcome…… Chronic Hay-fever!!

After hot markets of late, a little bit of cold water has been poured on bourses over the last 24 hours. We saw the double-whammy of soft data releases in Germany and the US, and some negative trade headlines to dampen the mood. Just on the former, Germany posted 0.0% qoq growth in Q4 (vs. +0.1% expected) although in unrounded terms this was ever so marginally positive at +0.02%. This equates to an output increase of €150m versus Q3. In other words, Germany was €150m away from a recession if we use the usual definition of two consecutive negative quarters. For physical comparison, that’s about one and a half of Airbus’s short-haul A320 planes or just over a third of an A380 jumbo jet (albeit the final assembly of the latter is done in France). Kudos to our European Economics team for that stat. Today’s EuroMillions draw is in the region of €160m too for an alternative perspective. Win that and you could be worth an amount equivalent to the increase in output in Q4 of a country of 82.5m people.

Meanwhile, yesterday’s retail sales figures in the US might result in a few more ‘r’ words being bandied around such was the extent of the weakness. Headline sales in December tumbled -1.2% mom compared to expectations for a +0.1% mom rise. It was even worse for the core readings with ex auto and gas sales down -1.4% mom (vs. +0.4% expected) and the control group down -1.7% mom (vs. +0.4% expected). A reminder that the latter is an input into the GDP accounts. In fact the control group reading was down by the most in a single month since January 2000. So not particularly pretty any way you cut it. The talk amongst our economists was that the data was a bit of a head scratcher in that it belies other reliable data sources. Nevertheless the Atlanta Fed Q4 GDP tracker is now down to 1.5% from 2.6%. Not to be ignored also was the weekly initial jobless claims reading (239k vs. 225k expected) which rose 4k from the week prior. That puts the four-week moving average at 232k and the highest since January 2018. There’s some suggestion that weather had an impact but it’s proving hard to ignore the sustained tick up in recent weeks despite the external issues impacting the data. Overnight our US economists pushed back their Fed call by 3 months to a hike in September 2019 and one in March 2020. They’ve also removed a additional final hike that originally was expected in 2020. See here for the rationale.

In terms of markets, the big moves were reserved for rates where 10y Treasuries touched a low of 2.641% intraday, before closing slightly off that at 2.650%, albeit still -5.2bps down on the day. In Europe we saw Bunds flirt with the 10bps level again before closing at 0.103% (-1.9bps). OATs rallied -2.2bps and Gilts -2.7bps while Italy (+1.9bps) and Spain (+0.6bps) were weaker. As for what that meant for equity markets, the S&P 500 (-0.27%) snapped its four-day winning run with financials (-1.16%) the real laggard on a sector basis. The DOW and NASDAQ closed -0.41% and +0.09% respectively while the STOXX 600 – which in fairness was little moved post the Germany data – pared gains of as much as +0.57% to close -0.32%. European Banks were down -1.48% while the DAX (-0.69%) unsurprisingly underperformed. Meanwhile in currencies, the USD didn’t really know how to react and instead ebbed and flowed over the course of the day before ending -0.08%. Commodity markets were quiet with oil a shade higher by the end of play.

This morning in Asia markets are largely heading lower following Wall Street’s lead with the Nikkei (-1.19%), Hang Seng (-1.64%), Shanghai Comp (-0.62%) and Kospi (-1.54%) all down. On the margin negative trade headlines mentioned below and China’s weaker than expected economic data are weighing on sentiment. Elsewhere, futures on the S&P 500 are also down -0.35%. On the economic data out of China, January CPI came in at +1.7% yoy (vs. +1.9% yoy expected; slowest pace of increase since January 2018) while PPI stood at +0.1% yoy (vs. +0.3% yoy expected; slowest pace of increase since October 2016).

Over in politics, President Trump is reportedly going to sign the funding deal today negotiated by House and Senate lawmakers. The deal would provide additional funding for border security, albeit not a wall as the President has asked for, which will according to Bloomberg headlines prompt him to declare a national emergency in order to divert funding from other sources to wall construction. We got further hints in this direction overnight with the White House spokeswoman Sarah Huckabee Sanders saying in a statement that, “President Trump will sign the government funding bill, and as he has stated before, he will also take other executive action — including a national emergency — to ensure we stop the national security and humanitarian crisis at the border.” Such a move is likely to be challenged in the courts, which will likely take months or years to resolve. More immediately relevant, the funding deal will avert a shutdown, which will allow government programs to continue operating, enable the IRS to continue disbursing tax refunds, and permit statistical agencies to continue their data releases unimpeded.

As for the latest on the US-China trade talks, Mnuchin and Lighthizer are meeting China President Xi Jinping today so all eyes on any soundbites we get from that. At the moment we haven’t heard of any scheduled post-meeting press conferences however that could all change. Yesterday’s comments from Kudlow about there being “no decision” on extending a deadline for imposing higher tariffs on China and the Bloomberg headline about both sides being “far apart on reform demands” appeared to take some of the sting out of markets. The reports suggested that USTR Lighthizer is pushing for strict timelines and specific deliverables to ensure a robust verification mechanism, but China is resisting the measures as an unfair infringement on their sovereignty. In fairness, the stories make sense in connection with other recent reports that the two sides may push for an extension in order to buy more time. In the meantime, the Financial Times has reported overnight that the US and China were scrambling to reach at least a “memorandum of understanding” by the end of today’s meeting so as to pave the way for a meeting between President Trump and his Chinese counterpart Xi Jinping.

In other news, last night’s vote in the House of Commons ended in yet another defeat for Prime Minister May, though this one was not especially significant as she’s promised a vote in two weeks on any revised agreement she gets with EU leaders. If she fails then the likelihood is that Parliament will increasingly take over proceedings. The pound ultimately ended the session -0.33% weaker.

In Fedspeak, the highlight was Governor Brainard’s interview with CNBC, her first remarks since the December FOMC meeting. She said that the “balance-sheet normalization process probably should come to an end later this year,” becoming the first FOMC speaker to lay down such a precise marker. Brainard noted that she would like to maintain a large enough buffer of excess reserves to make it easy for the fed to control short-term interest rates and avoid excess volatility. She also said that “downside risks have definitely increased” and “we’ll have to wait and see what the right move, if any, later in the year is.” So further evidence of a consensus for a near-term rate pause, and given Brainard’s history of being sensitive to overseas headwinds, it’s not surprising that she specifically mentioned “I’m very attentive to the international outlook.”

Coming back to data, the other important release out in the US yesterday was the January PPI report. While the ex food and energy reading actually came in above consensus (+0.3% mom vs. +0.2% expected), it didn’t go unnoticed that the healthcare component – which accounts for about 20% of the core PCE index – was a little on the soft side at just +0.11% mom. That suggests some downside for the core PCE when we get the January reading next month.

Finally, as for the day ahead, this morning in Europe the highlights are January retail sales data in the UK and the December trade balance reading for the Euro Area. In the US we’ve got a busy end to the week with the February empire manufacturing reading (+7.0 expected), January import price index reading (-0.1% mom expected), January industrial production reading (+0.1% mom expected) and preliminary February University of Michigan consumer sentiment survey print (93.5 expected). Away from that it’s the turn of the Fed’s Bostic to speak this afternoon, while over at the ECB we’re due to hear from both Coeure and Angeloni. Expect US-China trade talks to also be a big focus.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 37.32 POINTS OR 1.37% //Hang Sang CLOSED DOWN 531.21 POINTS OR 1.87% /The Nikkei closed DOWN 239.08 POINTS OR 1.13%/ Australia’s all ordinaires CLOSED UP 0.15%

/Chinese yuan (ONSHORE) closed UP at 6.7709 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 54.70 dollars per barrel for WTI and 64.94 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7709 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7792: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED