GOLD: $1344.95 UP $3.10 (COMEX TO COMEX CLOSING)

Silver: $16.20 UP 19 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1338.70

silver: $16.06

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 90 NOTICE(S) FOR 9000 OZ (0.2799 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10,323 NOTICES FOR 1,032,300 OZ (32.108 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 565 for 2,825,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3956:UP $45

Bitcoin: FINAL EVENING TRADE: $3958 UP $47.

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 3338 CONTRACTS FROM 217,484 UP TO 220,822 WITH YESTERDAY’S STRONG 25 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2717 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2717 CONTRACTS. WITH THE TRANSFER OF 2717 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2717 EFP CONTRACTS TRANSLATES INTO 13.585 MILLION OZ ACCOMPANYING:

1.THE 25 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.830 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 19,788 CONTRACTS (FOR 13 TRADING DAYS TOTAL 19,788 CONTRACTS) OR 98.940 MILLION OZ: (AVERAGE PER DAY: 1413 CONTRACTS OR 7.067 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 98.940 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.12% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 307.465 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3338 WITH THE 25 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2717 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GIGANTIC SIZED: 6055 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2717 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3338 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 25 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.01 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.1055 BILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.830 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY AN ATMOSPHERIC SIZED 22,416 CONTRACTS UP TO 504,639 WITH THE GAIN IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $22.95//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 10,210 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 9860 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 350 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 504,639. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN AN OUT OF THIS WORLD- SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 32,628 CONTRACTS: 22,416 OI CONTRACTS INCREASED AT THE COMEX AND 10,210 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 32,628 CONTRACTS OR 3,262,800 OZ = 101.48 TONNES. AND ALL OF THIS POWERFUL DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $22.95.

YESTERDAY, WE HAD 5665 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 76,100 CONTRACTS OR 7,610,000 OZ OR 236.70 TONNES (13 TRADING DAYS AND THUS AVERAGING: 5,854 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 236.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 236.70/2550 x 100% TONNES = 9.28% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 756.83 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN ATMOSPHERIC SIZED INCREASE IN OI AT THE COMEX OF 22,416 WITH THE GAIN IN PRICING ($22.95) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,210 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,210 EFP CONTRACTS ISSUED, WE HAD AN OUT OF THIS WORLD GAIN OF 32,628 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,210 CONTRACTS MOVE TO LONDON AND 22,416 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 101.48 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $22.95 IN YESTERDAY’S TRADING AT THE COMEX

we had: 90 notice(s) filed upon for 9000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.10 TODAY

SURPRISE: NO CHANGE IN GOLD INVENTORY TODAY

/GLD INVENTORY 792.45 TONNES

Inventory rests tonight: 792.45 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 19 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY/

/INVENTORY RESTS AT 308.296 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 3338 CONTRACTS from 217,484 UP TO 220,822 AND CLOSER T0 THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2717 CONTRACTS FOR MARCH. 0 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2717 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3338 CONTRACTS TO THE 2717 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN OF 6055 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 30.2745 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.830 MILLION OZ STANDING IN FEBRUARY.

RESULT: A POWERFUL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 25 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 2717 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 5.57 POINTS OR 0.20% //Hang Sang CLOSED UP 285.92 POINTS OR 1.81% /The Nikkei closed U[ 128.84 POINTS OR 0.160%/ Australia’s all ordinaires CLOSED DOWN 0.14%

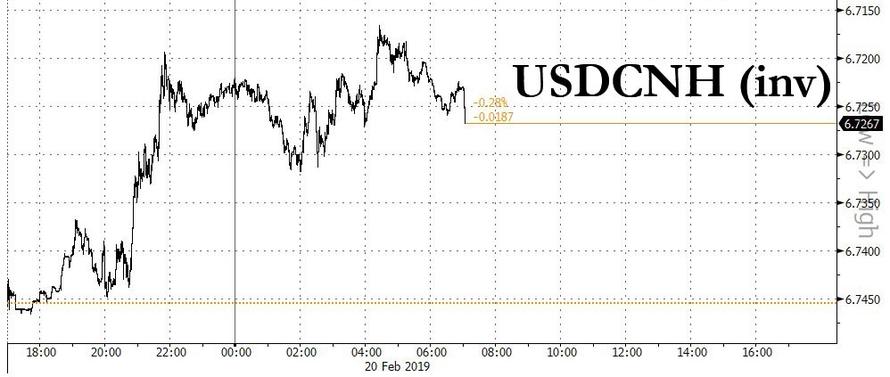

/Chinese yuan (ONSHORE) closed UP at 6.7230 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7230 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7253: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/USA/Europe

China warns (threatens) that new USA tariffs will be ‘catastrophic” for global stocks

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

UK manufacturers are beginning to sound the alarm bell on a no deal BREXIT…they catastrophic events

( zerohedge)

ii)ITALY

Wow!! this is big…Salvini is gaining big time in popularity as he forms a broad coalition of eurosceptic groups. He is set to form the second biggest party in the European parliamentary elections held in May.

( zerohedge)

iv)UK The pound is hit as 3 more Tory MP’s quit and join the “Independent Group”. This may lead to an election as May’s minority government is getting less and less support

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia

Very scary!! Russia is advancing in weaponry at an alarming pace. They now state that they will point weapons at the USA directly if it deploys missiles to Europe

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

Border class imminent:

( zerohedge)

9. PHYSICAL MARKETS

ii)Graham Summers:

gold understands perfectly what is coming!!

( Graham Summers/Phoenix Research Capital)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

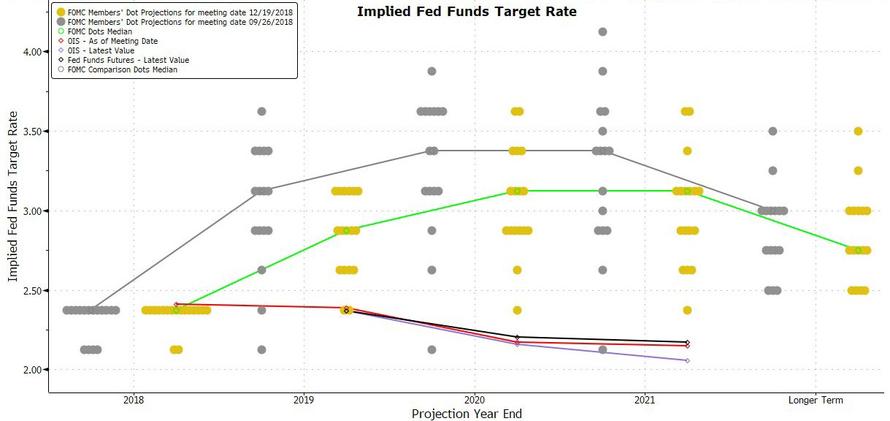

ii)Market data/ FOMC

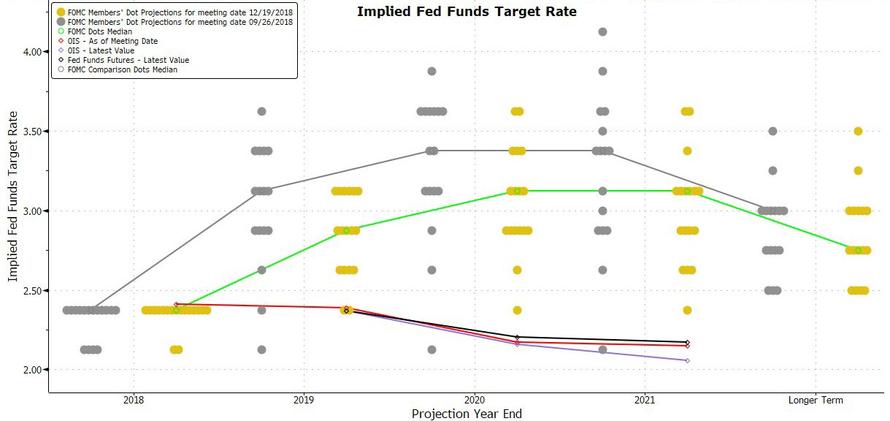

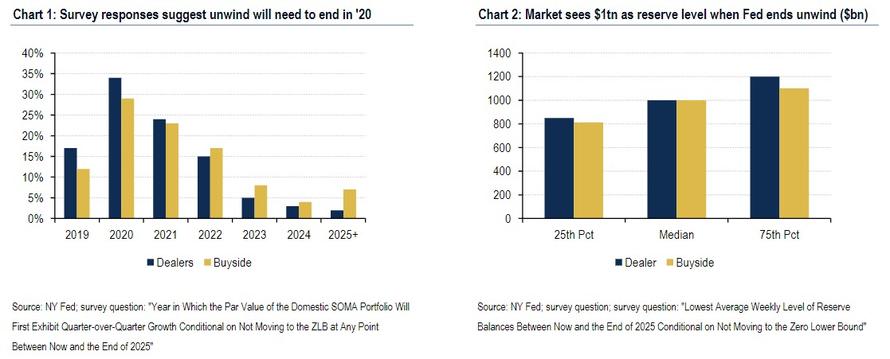

This should be extremely gold bullish, but then we are dealing with crooked banks: almost all the clown Fed officials want a plan to stop their roll off of treasuries form the balance sheet. This they want done by year end.

(courtesy, zerohedge)

iv)SWAMP STORIES

a)It is time for a new special prosecutor who will investigate the investigators

( Raul Meijer)

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 11,916 CONTRACTS DOWN TO 87,344 CONTRACTS. AFTER MARCH, APRIL ADVANCES TO 248 CONTRACTS FOR A GAIN OF 30 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 14,503 CONTRACTS UP TO 92,289 CONTRACTS.

FIRST DAY NOTICE IS THURSDAY FEB 28.2019

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i Out of Scotia: 2250.50 oz (70 kilobars)

Global Financial Crisis II Is Upon Us – Jim Willie Interviews Mark O’Byrne

Global Financial Crisis II Is Upon Us – Jim Willie Interviews Mark O’Byrne

– Jim Willie interviews Mark O’Byrne of GoldCore about the slowly erupting Global Financial Crisis II and the importance of being financially prepared but also “psychologically prepared”

– “Not a single thing has been fixed” and vitally important people prepare now for the “next phase” of the currency wars and the global financial crisis which is set to impact financial markets, stocks, bonds, banks (what happened to Wells Fargo last week?) and bankrupt governments in the UK, EU and US

– The Global Monetary RESET will see the “Third World” dollar sharply devalued and paper wealth and assets including stocks, corporate and government bonds become much more volatile and risky

– US Treasuries are no longer a risk free asset as the United States will either “formally default or restructure” the $22 trillion US debt and the $100 trillion to $200 trillion of unfunded government liabilities

– Gold coins and bars are the primary store of value in the coming Currency Wars and the Cashless Society, especially given the likelihood of COMEX gold defaults and collapse of the LBMA unallocated gold market says Mark O’Byrne

– Jim Willie on the coming radical changes in the global gold market and reversion to physical price discovery and new pricing involving premiums on physical gold (kilo gold bars) in major gold trading, storage and liquidity centres such as Zurich, Mumbai, Singapore, Shanghai etc

– Asset allocation and the case for having much higher allocations to gold and silver as safe haven dollar and Treasuries are questioned due to the “Third World finances” of the U.S. Jim Willie recommends higher allocations to physical precious metals and says tongue in cheek, “more like 40% in gold and the rest in silver”

– Key facts about owning gold and silver coins and bars, premiums on gold and silver bullion, the safest vaults and the safest jurisdictions or countries in the world

– Importance of having actual gold & silver coins and bars in your possession or having outright legal ownership of physical bullion in allocated and segregated storage, in bailment and in your name

– Global Financial Crisis II is “going to be much, much bigger” … prepare now

Jim Willie of the Golden Jackass Interview of GoldCore’s Mark O’Byrne via and courtesy of Gadfly TV

News and Commentary

Gold Surges on Elevated Geopolitical Uncertainty (WSJ.com)

PRECIOUS-Palladium eyes $1,500/oz in record surge; gold hits 10-mth high (CNBC.com)

Gold rallies to a 10-month high as trade-talk continuation captures market (MarketWatch.com)

Gold hits 10-month peak on hopes for U.S.-China trade talks (Reuters.com)

Fed’s Williams says new economic outlook necessary for rate hikes (Reuters.com)

The Utterly Unbelievable Scale of U.S. Debt Right Now (NationalPost.com)

Modern Monetary Madness (GoldSeek.com)

Bears could be in for a ‘great few weeks’ as S&P 500 hits a wall (MarketWatch.com)

A drop in U.S. stocks may be fast and furious, according to Elliott Wave theory (MarketWatch.com)

UK Manufacturers Deny “Scaremongering”, Fear “Catastrophic” No-Deal Brexit (ZeroHedge.com)

Listen on iTunes, Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

19 Feb: USD 1,329.55, GBP 1028.81 & EUR 1,175.72 per ounce

18 Feb: USD 1,323.95, GBP 1025.13 & EUR 1,169.58 per ounce

15 Feb: USD 1,319.00, GBP 1027.64 & EUR 1,168.17 per ounce

14 Feb: USD 1,305.65, GBP 1017.49 & EUR 1,158.50 per ounce

13 Feb: USD 1,311.15, GBP 1017.45 & EUR 1,158.79 per ounce

12 Feb: USD 1,311.60, GBP 1021.21 & EUR 1,163.00 per ounce

Silver Prices (LBMA)

19 Feb: USD 15.78, GBP 12.22 & EUR 13.99 per ounce

18 Feb: USD 15.76, GBP 12.19 & EUR 13.91 per ounce

15 Feb: USD 15.67, GBP 12.23 & EUR 13.90 per ounce

14 Feb: USD 15.58, GBP 12.17 & EUR 13.83 per ounce

13 Feb: USD 15.69, GBP 12.13 & EUR 13.85 per ounce

12 Feb: USD 15.81, GBP 12.30 & EUR 14.01 per ounce

Recent Market Updates

– 7 Major Flaws Of The Global Financial System – Excellent Infographic

– The Case for Gold In 2019 – The Economist

– Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

– Valentine’s Day Record Spending Due to Gold Love Trade?

– Gold Prices In Pounds and Euros Gain More as Economic Growth Falters in the UK and EU

– Irish Investors Storing Their Gold Bullion In Ireland

–

– Large Gold Bullion Shipment Moves From London to Dublin Gold Vaults As Brexit Concerns Deepen

– Store Gold Bullion In Safest Ways – Learning from Tragic Venezuela Today

– The Vital Importance of Gold As A Strategic Asset In 2019</strong

Ronan Manly: Unaccountability with Australia’s gold is typical of central banking

Submitted by cpowell on Tue, 2019-02-19 16:06. Section: Daily Dispatches

11:05a ET Tuesday, February 19, 2019

Dear Friend of GATA and Gold:

Elaborating on his interview with Russia Today this week about the refusal of the Reserve Bank of Australia and the Bank of England to account for Australia’s supposed gold reserves —

http://www.gata.org/node/18881

— Bullion Star gold researcher Ronan Manly details how secrecy and unaccountability with gold are actually the policies of major central banks in their longstanding campaign to drive the monetary metal out of the world financial system.

Manly notes that this campaign is well documented at GATA’s internet site.

His analysis is headlined “Australia’s Gold at the Bank of England — Extended Q&A” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/australias-gold-at-the-ban…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Graham Summers:

gold understands perfectly what is coming!!

(courtesy Graham Summers/Phoenix Research Capital)

Gold Knows What Is Coming… And It’s Not Pretty

Gold continues to soar, up 14% in the last six months and now challenging its 2018 highs.

If you’re looking to understand why Gold continues to rally, you don’t have to look any further than the political arena where more and more politicians are calling for wealth taxes and cash grabs.

Gold knows that these folks are not going to limit their plans to the super wealthy… it knows that eventually the calls will be for a tax on NET wealth…which is why it continues to move higher.

Gold ALSO knows that Central Banks are trapped… and will be forced to turn on the money printing presses shortly.

In the last week, the Bank of Japan, the European Central Bank, and the Federal Reserve have ALL abandoned any pretense of normalizing policy.

While they have yet to start easing just yet, it’s now only a matter of time.

Gold is rallying as investors look for a safe haven that CANNOT be devalued by Central Bank or stolen by the political class. Gold knows that BOTH of those items (theft of capital and devaluation of currencies) is only going to get worse going forward.

Indeed, we’ve uncovered a secret document outlining how the Fed plans to both seize and STEAL savings during the next crisis/ recession.

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7230/

//OFFSHORE YUAN: 6.7254 /shanghai bourse CLOSED UP 5.57 POINTS OR 0.20% /

HANG SANG CLOSED UP 285.92 POINTS OR 1.81%

2. Nikkei closed UP 128.84 POINTS OR 0.60%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 96.59/Euro FALLS TO 1.1337

3b Japan 10 year bond yield: FALLS TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.76/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.66 and Brent: 66.00

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.10%/Italian 10 yr bond yield DOWN to 2.83% /SPAIN 10 YR BOND YIELD DOWN TO 1.20%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.73: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.77

3k Gold at $1343.55 silver at:16.05 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 3/100 in roubles/dollar) 65.74

3m oil into the 55 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0067 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1351 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.10%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.63% early this morning. Thirty year rate at 2.97%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3150

Global Stocks Hit 4 Month High As US Futures Drop Ahead Of Fed Minutes; Yuan Soars

World stocks hit a four-month high on – what else – hopes of progress in trade talks between the United States and China, even as US equity futures drifted lower, offsetting a rise in European and Asian stocks as traders awaited the release of minutes from the latest Fed meeting. The dollar snapped a 4-day losing streak while the yuan jumped after a Bloomberg report that Trump is asking China to keep its currency stable (and hence less market-determined).

The bullish mood was boosted after Donald Trump said negotiations with China were going well and suggested he was open to extending the deadline to complete them beyond March 1 which is anything but “magical.”

European automakers led an advance in the Stoxx 600 Index, which erased Tuesday’s drop, even as miner Glencore fell on lower-than-expected earnings, while Lloyds rose after it unveiled a 1.75 billion pounds ($2.3 billion) buyback plan. UK. grocer J Sainsbury plunged on antitrust objections to its planned takeover of Walmart’s Asda.

Meanwhile, European banks continued to be pressured by expectations that the ECB will restart a program to provide long-term cheap loans, or TLTROs, to banks to boost a faltering economy, depressing yields, while on Monday the BOJ flagged its readiness to ease further.

Earlier, the MSCI index of Asia-Pacific ex-Japan rose as much as 1.1% to mark its highest levels since Oct. 2. Hong Kong’s Hang Seng gained as much as 1.3 percent to six-month highs, while Korea’s Kospi and Taiwan’s index recovered to levels last seen in early October. Japan’s Nikkei added 0.6 percent to two-month highs.

Boosted by fresh dovish sentiment, emerging-market stocks and currencies jumped the most in three weeks amid optimism that trade negotiations between Washington and Beijing will lead to a deal. The South African rand and Turkish lira bucked the rally.

The yuan led the advance among developing markets, bolstering its Asian peers, after Bloomberg reported that the U.S. is asking China to keep the value of its currency stable as part of the negotiations. The onshore Yuan strengthened as much as 439 pips on Wed to close at 6.7236/USD, its biggest intra-day gain in more than a month, and the highest since the end of Jan, and the biggest rise since Jan 10th. The offshore yuan was last trading at 6.7265 after rising as high as 7.164.

And speaking of China’s currency, Premier Li said that China has not and will not change monetary policy; will not resort to ‘flood-like’ stimulus. RRR cut in January reflected that there is sufficient room for cuts, adding that increasing bill financing and short-term loans may create the potential for risks.

Elsewhere in FX, the dollar snapped a four-day losing streak before the release of Fed January minutes, rising 0.2 percent against the yen after Japan recorded its biggest annual drop in exports in January for more than two years, and on recent dovish Bank of Japan signals.

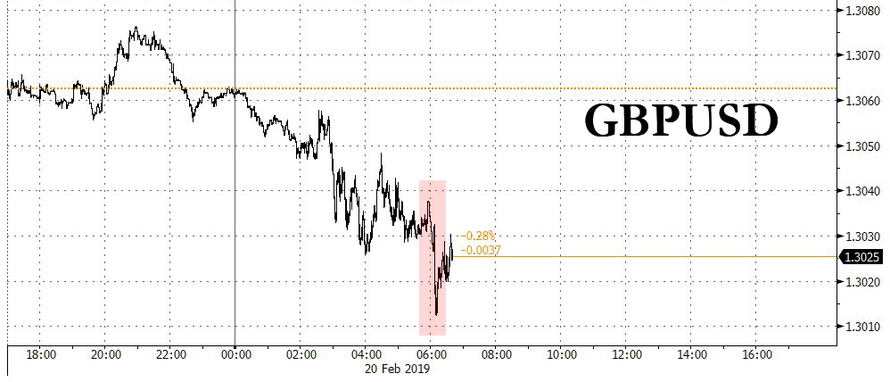

The pound slipped as Prime Minister Theresa May headed back to Brussels in a last-ditch attempt to save her Brexit deal and as three Conservatives quit to join a new party, while the euro lacked a clear sense of direction after ECB’s Praet said a decision on TLTROs may not be made at the March meeting. The rand dropped before Finance Minister Tito Mboweni’s budget speech on Wednesday.

In rates, European bonds mostly edged up, but Italian notes fell while US Treasuries were unchanged after some mixed trading earlier.

In the latest Brexit news, PM May is reportedly to present the EU with fresh legal proposals to break the Irish backstop deadlock and which will hopefully convince Brexiteers to support her deal. In related news, a spokesperson said PM May and Brexit Ministers updated cabinet on Brexit and that the UK is still looking to reopen the withdrawal agreement. Meanwhile, in a shocking development, UK Tory MPs Heidi Allen, Anna Soubry and Sarah Wollaston have resigned from the Conservative Party and joined the Independent Group; talkRadio’s Kempsell confirms, with the news sending cable to session lows.

Prior to this, ITV’s Peston tweets that if, as he expects, four Tory MPs quit the party today to become independent, PM May’s minority government will become even more of a minority, with less grips on the Commons, so a general election moves nearer.

Finally, UK Chancellor Hammond said a no-deal Brexit would be mutual calamity for UK and EU, while he also noted that the most urgent task is to reach an agreement that will protect trading relationship with EU. Furthermore, Hammond said the Malthouse initiative is a valuable effort to allay backstop concerns in the future but added that EU will not consider a replacement to the backstop now.

Looking at key trading catalysts, Bloomberg notes that as the U.S. and China continuing tough negotiations toward a trade deal, focus has shifted to a key campaign promise made by President Donald Trump, namely addressing Beijing’s periodic devaluation of the yuan. Investors will also be preoccupied by the release of minutes from the Federal Reserve later on Wednesday and from the European Central Bank a day later, and they’ll have a glut of German data to contend with toward the end of the week.

“At the start of the year with the upshoot in equities, everything was sort of moving together,” Peter Borish, chief strategist at Quad Capital LLC, told Bloomberg TV in New York. “We are now starting to not see that and that is always the first sign of warning signals in the market place that it might be getting ready for a correction.”

Elsewhere, oil prices hovered near 2019 highs, supported by OPEC-led supply cuts and U.S. sanctions on Iran and Venezuela, but further gains were capped by soaring U.S. production and expectations of an economic slowdown. International Brent crude futures stood at $66.30 per barrel, having hit a three-month high of $66.83 per barrel earlier this week. Gold traded at the highest since April and palladium soared to a record as a shortage started to bite.

Expected data include mortgage applications and FOMC minutes. Analog Devices, CVS, Synopsys and Cheesecake Factory are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 2,775.50

- STOXX Europe 600 up 0.2% to 369.58

- MXAP up 0.8% to 158.66

- MXAPJ up 1.1% to 519.33

- Nikkei up 0.6% to 21,431.49

- Topix up 0.4% to 1,613.47

- Hang Seng Index up 1% to 28,514.05

- Shanghai Composite up 0.2% to 2,761.22

- Sensex up 1% to 35,688.98

- Australia S&P/ASX 200 down 0.2% to 6,096.49

- Kospi up 1.1% to 2,229.76

- German 10Y yield fell 0.7 bps to 0.098%

- Euro up 0.1% to $1.1353

- Italian 10Y yield rose 2.2 bps to 2.429%

- Spanish 10Y yield fell 0.5 bps to 1.203%

- Brent futures down 0.5% to $66.13/bbl

- Gold spot up 0.3% to $1,345.24

- U.S. Dollar Index little changed to 96.56

Top Overnight News from Bloomberg

- The U.S. is said to have asked China to keep its currency stable as part of a new trade deal, a move aimed at discouraging officials in Beijing from devaluing the yuan to offset the impact of American tariffs. That request is at odds with years of global pressure on China, from the Group of 20 economies in particular, to move toward a free-floating currency

- British government sees Theresa May’s meeting on Wednesday with EC President Juncker in Brussels as a crucial chance to get legally binding changes to the so- called Irish border backstop

- Joan Ryan becomes the eighth U.K. Labour MP to quit the party, accusing Leader Jeremy Corbyn of “presiding over a culture of anti-Jewish racism and hatred of Israel,” according to a tweet from the lawmaker

- Corbyn’s closest ally Shadow Chancellor John McDonnell, says the Labour leader must listen to critics x

- Theresa May faces many problems as she tries to nail down a divorce agreement with the European Union but one looms over them all: pro-Brexit Tories do not trust her.

- Japanese exports fell in January as shipments to China tumbled, adding to signs slowing global demand is weighing on the export-dependent economy

- President Trump said he is no rush to conclude a nuclear deal with North Korean leader Kim Jong Un because he has a strong relationship with the North Korean leader and U.S. sanctions against the country remain in place

- ECB officials will discuss new long-term loans for banks shortly, even though it’s unclear yet whether a decision will be taken, according to Executive Board member Peter Praet

- The British government sees May’s meeting on Wednesday with European Commission President Jean-Claude Juncker as a crucial chance to get legally binding changes to the so-called Irish border backstop, which has proved the biggest obstacle to getting a Brexit deal

- Indonesia’s finance ministry is studying various forms of incentives for sovereign bond holders, including lower tax for those holding the securities for a longer period

Asian stocks traded somewhat indecisively following the cautious gains seen on Wall St. ahead of this week’s key events including FOMC minutes and US-China trade talks. ASX 200 (-0.2%) and Nikkei 225 (+0.6%) were mixed with Australia dragged lower by continued underperformance in Consumer Staples after Woolworth shares slumped more than 5% post-earnings, while Tokyo stocks were propped up as the impact of a weaker currency eclipsed the concerns from the steepest decline in Japanese Exports for more than 2 years. Elsewhere, Hang Seng (+1.0%) and Shanghai Comp. (+0.2%) were also varied as the mainland lagged despite the PBoC announcement of its first liquidity injection since before the Lunar New Year, as the amount was a relatively paltry CNY 20bln and with participants also kept tentative ahead of upcoming senior level trade discussions between US and China. Finally, 10yr JGBs were subdued with price action contained by an indecisive risk tone in the region and after having recently hit resistance at 153.00, while the absence of the BoJ in the market also contributed to the lacklustre trade.

Top Asian News

- Zhenjiang Said to Be Mulled for Local Debt Resolution Test Unit

- Hong Kong to Take Back Part of Biggest Golf Course for Homes

- Baht Reaches Highest Since 2013 Amid Broader Dollar Weakness

- India’s Giant IT Industry Rode a Rally in Global Tech Spending

Major indices in Europe have somewhat waned off earlier highs [Euro Stoxx 50 Unch] following a relatively indecisive Asia-Pac session. Sectors are mixed with outperformance in industrials given the price action in the base metal complex, while energy names marginally lag their peers. In terms of notable movers, Sainsbury’s (-16.4%) shares plumbed the depths after the supermarket was dealt a blow by the UK CMA, which stated that the proposed Sainsbury’s-Asda has extensive competition concerns, whilst adding that the two companies will have to shut a significant number of stores or face rejection. The companies now have until 13th March to respond to the CMA’s findings, with a final report by the CMA to be issued by 30th April. Elsewhere, Swedbank (-11.1%) has become the latest financial institute embroiled in the Danske Bank (-1.0%) money laundering scandal, following reports of the Co. being linked to USD 4.3bln in illicit transfers. Finally, regarding earnings-driven stocks, Glencore (-0.5%) gave up initial gains as indices came off highs, while Lloyds (+3.9%) maintained its positive at the top of the FTSE amid a GBP 1.75bln share buyback programme alongside a dividend hike.

Top European News

- Brexit Jobs Boom Has a Flip Side That’s Holding the Economy Back

- Lloyds Unveils $2.3 Billion Buyback Ahead of U.K. Turmoil

- Glencore Plans New Buyback as Trading Profit Disappoints

- Daimler Joins Jumbo Euro Corporate-Bond Rush as Spreads Tumble

In FX, the Greenback has regained some poise after its relatively pronounced downturn late yesterday amidst uncharacteristically dovish comments from Fed’s Mester regarding balance sheet run-offs, as she intimated a willingness to back an end to QT by or even before the end of 2019, albeit keeping options open for a 25 bp hike later this year. However, the index remains depressed and not far off sub-96.500 lows in anticipation that the upcoming FOMC minutes will reiterate the shift in policy guidance to a pause in normalisation and patience before any further adjustments.

- AUD/JPY/NZD/GBP – All on the backfoot vs the Usd, or paring gains to be more precise, as Aud/Usd eases back towards 0.7150 from circa 0.7175 at best in wake of moderately softer than forecast Q4 Aussie wage data overnight. Meanwhile, a bigger than expected Japanese trade deficit due to the worst export showing since October 2016 compounded post-BoJ Governor Kuroda Jpy weakness as it slips a bit further towards 111.00, but again could glean some traction from option expiry interest given 1.1 bn rolling off between 110.75-85 at the NY cut. Indeed, the Kiwi and Pound are marginally underperforming as Nzd/Usd hovers near the bottom end of a 0.6885-63 range and the Aud/Nzd cross consolidates recovery gains above 1.0400, while Cable runs out of steam ahead of 1.3100 having spiked from sub-1.2900 through 1.3000 in double quick time on Tuesday and topping out around 1.3075 ahead of today’s UK PM May-EU Juncker showdown later today.

- CAD/EUR – The Loonie continues to reap the most from pre-Fed minutes US Dollar defensive positioning and remains close to multi-week peaks above 1.3200 even though crude prices have encountered more offers/resistance around 2019 highs, while the single currency has formed a firmer base over 1.1300 having closed above a 1.1313 Fib and now eyeing another resistance level at 1.1362 for a stronger bullish technical signal.

- EM – Contrasting performances for the Yuan and Rand, as the former draws momentum from a stronger PBoC fix, fresh liquidity and positivity surrounding US-China trade talks to test 6.7200 levels vs the Usd, but pre-budget jitters hit the latter with the Zar down to 14.1500 at one stage.

In commodities, Brent (-0.4%) and WTI (-0.3%) prices are subdued after being rangebound throughout the Asia session where WTI reached 2019 highs of USD 56.39.bbl, as markets await today’s FOMC minutes and the beginning of high-level US-China trade talks tomorrow with USTR Lighthizer. The EIA forecasts that US total shale regions oil production will average 8.3938mln barrels in March, which is 84mln barrels above February’s estimate of 8.31mln barrels. Separately, there have been reports of a fire at a PDVSA crude pumping station, which has a 300k BPD capacity; although, as details surrounding the fire are sparse the impact on production is currently unclear. Looking ahead, API’s weekly inventory numbers are to be released today due to the US market holiday on Monday, market expectations are that US crude oil inventories increased over the prior week by 3.1mln barrels. Note, some abnormality may be observed today in WTI trading due to the expiration of the March WTO contract. Gold (+0.1%) is trading within a thin USD 5/oz range, as the yellow metal follows cautiousness seen in the dollar ahead of today’s FOMC. Elsewhere, spot-Palladium has convincingly moved above the USD 1500/oz level reaching USD 1504.46/oz; as the metals 7-month rally, which has been driven by a supply shortage, continues. Separately, German inspection frim TUV SUD has stated that it will no longer certify Vale owned tailings dams, following a Vale owned dam bursting last month.

Looking at the day ahead now, while there’s no data due in the US, we will get the FOMC meeting minutes from the January meeting. Expect the minutes to shed more light on how the Fed’s domestic and global growth outlook may be evolving and the lens through which the Committee may view incoming inflation data in the near term. Expect some focus on the balance sheet normalisation program too, which may reiterate Brainard’s view that the Fed will likely end the roll-off of maturing securities by year-end. Away from that, we’re due to hear from the ECB’s Praet this morning and Fed’s Kaplan this evening, while the US-China trade meetings and meeting between UK PM May and EC’s Juncker should also be a big focus for the market.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -3.7%

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Last month I highlighted the strange occurrence where over the course of a week my Spotify account was seemingly hacked as obscure French/Moroccan music was mysteriously added to my library. If you missed that one you can review it here . Well today it’s our turn to hack into your Spotify account as DB has just launched a new podcast series called Podzept. We have a selection of articles at our launch including one from me on “What the history of populism can teach us today”. They are available on Spotify, Apple Podcast and Stitcher. Feel free to search for Deutsche Bank Research, Podzept or simply follow the links to these sites on this page http://www.dbresearch.com/podzept . We’d be interested to hear from readers (and listeners) whether this is an interesting medium on which to receive research. On public sites like this there is a regulatory restriction on the type of research we can provide so the EMR is at this stage unlikely to be a candidate. However if there is large enough demand for it we’ll look into how we might be able to do it in the future. So all thoughts on whether some research works as a podcast are welcome.

Markets are quiet this week so no excuse to not download Podzept. Nevertheless, one gets the sense that we are all on tenterhooks to a certain degree, waiting for what could be major developments on trade and the now infamous S232 report on autos and US national security. One of our US economists Justin Weidner did some digging last night into the timeline from last year’s 232 steel report. That report was submitted to the President on January 11th, but was not released to the public (in its redacted form) until February 16th. The President subsequently made a determination on March 8. So if history repeats itself it would suggest that (official) details about the 232 auto report won’t come out until mid-March, or whenever they are done redacting the private information.

However, history may not repeat itself but it’s interesting that Mr Trump has yet to make any comments (even via tweets). This could mean one of three things; a) the above timeline is reasonable, b) the results are market friendly, c) Mr Trump and the administration are being careful not to escalate trade tensions at such a delicate stage of the China talks. Unfortunately, I’ve no idea which is closest to reality but it feels like we’re all now constantly looking over our shoulder with this report lurking on someone’s desk somewhere. It’s very important as with European growth so low it could be the straw that breaks the camel’s back in terms of a recession if it goes the wrong way.

On the other main trade front, news flow has the potential to pick up pace with meetings continuing between the US and China today. Mnuchin and Lighthizer will then join talks with China Vice-Premier Liu He again tomorrow. After Europe closed last night, headlines emerged that the US is asking China to keep the yuan stable as part of the negotiations between the world’s two largest economies to ensure devaluations aren’t used to offset tariff increases. The same article on Bloomberg suggested the two countries are discussing how to address currency policy in a “Memorandum of Understanding” that would form the basis of a deal that ultimately will have to be approved by Mr Trump and Xi Jinping. On the positive side, this story hints that talks are progressing. However, later in the session, top White House economist Kevin Hassett told reporters that there is still a lot of progress to make. The overall feeling is that it is 1 step forward, three-quarters of a step back at the moment. So positive momentum but still fragile. Before we review markets, the other main event today is the latest FOMC minutes. See the day ahead at the end for a preview of what to expect.

Steady incremental US positivity seems to be the theme at the moment with Europe a little more in limbo. Last night the S&P 500, DOW and NASDAQ closed +0.15%, +0.03% and +0.19% respectively. The retail sector outperformed, gaining +0.65%, largely thanks to a bumper earnings report from Walmart (+2.21%), which showed their best holiday season performance in a decade. The report from the world’s largest retail store provided some comfort after last week’s terrible retail sales report for December, as it looks increasingly likely that the poor data was an aberration. Commodity markets were also in focus, as the S&P 500 materials index was the best performing major subindex on the day, up +0.58%. Copper (+2.63%) and gold (+1.07%) both rallied, helping mining firms, aided by the weaker dollar which depreciated -0.41%. Gold hit a 10-month high and is now within 2 percentage points of its highest level in 5 years.

Prior to this, Europe had reversed much of the good progress made on Monday with the STOXX 600 ending -0.22%. High yield spreads closed +3bps wider in the US and flat in Europe, while in bond markets both Treasuries (-2.9bps) and Bunds (-0.4bps) firmed up a bit, which was in contrast to BTPs, which sold-off +2.3bps. Disappointing data (more on that below) appeared to be the catalyst.

Overnight in Asia, markets are trading mixed with the Nikkei (+0.38%), Hang Seng (+0.66%) and Kospi (+0.90%) all up while the Shanghai Comp (-0.15%) is heading lower in directionless trading. China’s onshore yuan is up +0.56% this morning likely on the story above that the US are demanding that China keep its currency stable. However, most EM currencies are generally trading strong against the greenback this morning. Elsewhere, futures on the S&P 500 (-0.07%) are trading flattish. In terms of data, Japan’s January trade balance was released overnight with exports declining -8.4% yoy (vs. -5.7% yoy expected) and imports at -0.6% yoy (vs. -3.5% yoy expected) leading to an adjusted trade balance of JPY -370.0bn (vs. JPY -150.7bn expected). The data highlighted that Japan’s exports have now declined for two months in a row for the first time since 2016 and sent the Japanese yen weaker (-0.18%).

Meanwhile, the latest on Brexit is that UK PM May is due to meet with EC President Juncker in Brussels this evening at 5.30pm GMT in what was being billed as a “significant” meeting according to the UK Government yesterday. Bloomberg quoted a source as saying that the meeting is expected to be a “stock-take” of the progress both sides have made ahead of Attorney General Cox potentially setting out his legal position on the backstop tomorrow. Yesterday, we got reaffirmation that the EU will not reopen the withdrawal agreement with the UK and will not accept a time limit on the Irish backstop. So, little sign of any softening of the EU approach, which isn’t a great surprise given next week’s parliamentary vote, which is still targeted for before February 27th. Sterling rallied +1.08% last night for its best session since November, when it rallied +1.93% on positive Brexit momentum and a broadly weaker dollar.

As for other snippets of news, ECB Vice-President Guindos continued the mantra of a more dovish way of thinking between the ECB Council, saying yesterday that policy makers are analysing the slowdown and have a large range of tools to respond with, which includes changing the language on forward guidance. Guindos did add that this wouldn’t happen before a “thorough analysis”. Elsewhere, over in the US, we learned that Bernie Sanders was seeking to run for the 2020 Democratic presidential nomination. Expect there to be more and more newsflow picking up ahead of the next presidential election with tax policy in particular becoming more of talking point. Yesterday, Bloomberg ran a story concerning Elizabeth Warren’s proposal for a universal child care plan funded by a tax on the ultra-wealthy. This higher-tax agenda from the left looks set to run a lot further.

Finally, in terms of the data that was out yesterday, in the UK we saw the unemployment rate hold steady in December at 4.0% as expected, while headline wages missed slightly (+3.4% 3m/yoy vs. +3.5% expected), albeit offset by an in-line core wages reading (+3.4% 3m/yoy). The data was largely in line with BoE forecasts and continues to underscore the divergence between soft survey data and the firming labour market. In Germany, the headline February ZEW survey reading disappointed at +15.0 (vs. +20.0 expected). That represented a drop of 12.6pts from January. Meanwhile, in Italy, as noted at the top, both industrial sales (-7.3% yoy from +0.5% previously) and orders (-5.3% yoy from -2.2% previously) data was very soft.

In the US, the only noteworthy data release was the NAHB home builders market index, which rose +4pts to 62, its biggest jump since 2017 and a potential signal that the real estate sector is bottoming out. A reading above 50 indicates that more builders view conditions as good than poor. The S&P 500 homebuilders index outperformed yesterday, gaining +0.79%.

On the Fedspeak front, NY Fed President Williams said that it would take “a different outlook either for growth or inflation” for him to support additional rate hikes. This isn’t a huge surprise given his previous comments, but it does further solidify the view that policy is on hold for now unless there is a major upside or downside surprise. Cleveland Fed President Mester said that she supports ending the balance sheet runoff by year-end, endorsing the view articulated by Governor Brainard last week. This is certainly a topic that will be discussed more this year, and maybe in the FOMC minutes due later today.

Looking at the day ahead now, the early release this morning comes from Germany with the January PPI report. Later this morning we’ll get the February CBI survey in the UK before the February consumer confidence reading for the Euro Area is out this afternoon. While there’s no data due in the US, we will get the FOMC meeting minutes from the January meeting. Our US economists expect the minutes to shed more light on how the Fed’s domestic and global growth outlook may be evolving and the lens through which the Committee may view incoming inflation data in the near term. Expect some focus on the balance sheet normalisation program too, which our colleagues expect to reiterate Brainard’s view that the Fed will likely end the roll-off of maturing securities by year-end. Away from that, we’re due to hear from the ECB’s Praet this morning and Fed’s Kaplan this evening, while the US-China trade meetings and meeting between UK PM May and EC’s Juncker should also be a big focus for the market.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 5.57 POINTS OR 0.20% //Hang Sang CLOSED UP 285.92 POINTS OR 1.81% /The Nikkei closed U[ 128.84 POINTS OR 0.160%/ Australia’s all ordinaires CLOSED DOWN 0.14%

/Chinese yuan (ONSHORE) closed UP at 6.7230 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7230 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7253: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/USA/EUROPE

China warns (threatens) that new USA tariffs will be ‘catastrophic” for global stocks

(courtesy zerohedge)

China Warns New US Tariffs Will Be “Catastrophic” For Global Stocks

Chinese state-run newspaper the Global Times warned – or perhaps threatened – late Tuesday that failed trade negotiations would have dire consequences for global stocks.

The threat of a market catastrophe has pigeonholed the US into striking a deal with Beijing, the report suggests although many are confident that the situation is flipped.

“[Trump’s] words further stoked the stock markets of the US, which reached the highest in two months and so increased pressure on the Trump administration to close the deal with China,” said the Global Times in an Op-Ed, adding that if the Trump team “imposes more tariffs on Chinese products while China responds with fiercer countermeasures,” it would “be a catastrophic strike to global stock markets.”

“In terms of avoiding such blows, the Trump administration is probably the most pressured,” the Op-Ed continues. “Thus in general, by the end of the trade negotiations, China and the US have become more psychologically equal” (according to the state-run outlet). As a result, “both sides would eventually lose,” the Times warned.

Why China’s implicit threat? Perhaps because, as Shard’s Bill Blain noted earlier today, at least in the context of its economy, China is already losing the trade war, and therefore has little to lose by escalating the war of words. This is what Blain said overnight:

The recent data highlights the Chinese economy may be slowing faster than XI can maintain his grip – he’s weaker than ever before. (Raising one scenario threat of a long-drawn out period of uncertainty if he is marginalised/deposed and a power struggle follows. That could be very destabilising and disruptive for the Occidental economies desperate to sell the China!)

We reckon XI knows he’s out of time and has to settle – handing Trump a critical victory. Long-term the US-China tech-war is difficult to call. Trump is determined to garner payback for China IP theft, and its difficult to imagine the rest of Asia adopting Chinese tech systems if they lose the current trade war to the US. However, you can’t just undo years of China tech development. My techy contacts tell me Huawai’s boasts about the US’ inability to close them is partial bluff and bluster – it’s not as advanced or robust as it claims, plus the US is going to insist on wrecking it – which could prove another long-term friction point.

The next question is how much of a favorable outcome the market has already priced in. Yesterday the S&P 500 rose modestly after President Trump suggested that the two largest economies might have more time to hammer out a deal without raising tariffs by the March 1 deadline, however it gave up much of the gains into the close suggesting that all good news may now be priced in..

Meanwhile, a Chinese trade delegation is currently in Washington D.C. this week for the latest round of trade negotiations, however with the March 1 deadline a little more than a week away, signs of any tangible progress are sorely lacking.

And speaking of China’s economic context, the world’s most populous economy is facing an accelerating slowdown in export growth in coming months according to Nomura chief China economist Ting Lu, who notes that the rush to buy up goods in advance of possible tariff increases is now over.

4.EUROPEAN AFFAIRS

UK

UK manufacturers are beginning to sound the alarm bell on a no deal BREXIT…they catastrophic events

(courtesy zerohedge)

UK Manufacturers Deny “Scaremongering”, Fear “Catastrophic” No-Deal Brexit

While ‘Project Fear’ runs rampant through the British media – regurgitating government-sanctioned propaganda to the masses to put pressure on hardline Brexiteers – the head of the country’s main manufacturing association said on Tuesday that Britain faces the “catastrophic prospect” of a no-deal Brexit next month due to the selfishness of some politicians and chaotic parliamentary proceedings.

As Reuters reports, the strong warning from Make UK, previously known as the EEF, comes as Japanese carmaker Honda is expected to say it is preparing to shut its main UK plant with a loss of 3,500 jobs.

Nissan earlier this month canceled plans to build its X-Trail sport utility vehicle in Britain, mostly blaming “business reasons” but also citing Brexit uncertainty.

Make UK’s chair, Judith Hackitt, said in remarks ahead of the group’s annual conference…

“Let me be clear … for those hard Brexiteers who accuse us of scaremongering. This is very real and very serious,”

“The clock has almost run down and it is now essential that the pantomime in parliament ends.”

Britain’s parliament overwhelmingly rejected the transition deal that May negotiated with the EU and time is running out to avoid a disruptive no-deal Brexit on March 29 which would lead to the re-imposition of customs checks on British exports.

“Some of our politicians have put selfish political ideology ahead of the national interest and people’s livelihoods and left us facing the catastrophic prospect of leaving the EU next month with no deal,” Hackitt said.

British manufacturers are facing a global slowdown as well as Brexit uncertainty. Official data last week showed their output fell by the most in over five years in the final quarter of 2018.

“It’s a big shock,” said David Bailey, a professor of industrial strategy at Aston University.

“But it’s not a surprise. Many of us have been warning for several years of the risks to UK automotive over Brexit, that we needed to nail down the uncertainty as soon as possible.”

As The FT reports, Ford said last week it had repeatedly urged the government not to leave the EU without a deal, in response to reports it had warned Theresa May it could move production overseas.

“Such a situation would be catastrophic for the UK auto industry and Ford’s manufacturing operations in the country,” the carmaker said, adding it would take “whatever action is necessary to preserve the competitiveness of our European business”.

Some 49 percent of 429 manufacturers surveyed for Make UK said a no-deal Brexit would make Britain unattractive, compared with 28 percent who said Britain would still be an attractive location, with bigger companies more likely to express concerns.

ITALY

Wow!! this is big…Salvini is gaining big time in popularity as he forms a broad coalition of eurosceptic groups. He is set to form the second biggest party in the European parliamentary elections held in May.

(courtesy zerohedge)

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia

Very scary!! Russia is advancing in weaponry at an alarming pace. They now state that they will point weapons at the USA directly if it deploys missiles to Europe

(courtesy zerohedge)

Russia Will Target US With New Hypersonic Weapons If It Deploys Missiles To Europe

6. GLOBAL ISSUES

7 OIL ISSUES

8. EMERGING MARKETS

Venezuela/USA

Border class imminent:

(courtesy zerohedge)

Border Clash Imminent As Maduro Deploys Military To Borders To Block ‘Aid’

Venezuela has shut a key maritime border and grounded flights as the Washington-backed coup-leader Juan Guaido has said that foreign aid will enter Venezuela from neighboring countries by land and sea on Saturday.

CNN reports that a government representative confirmed Venezuela has closed its maritime border with Aruba, Curacao, and Bonaire and, in the Western state of Falcon, prevented flights leaving from or departing to those islands.President Maduro has rejected offers of foreign food and medicine, denying there are widespread shortages and accusing Guaido of using aid to undermine his government in a U.S.-orchestrated bid to oust him.

CNN reports that a government representative confirmed Venezuela has closed its maritime border with Aruba, Curacao, and Bonaire and, in the Western state of Falcon, prevented flights leaving from or departing to those islands.President Maduro has rejected offers of foreign food and medicine, denying there are widespread shortages and accusing Guaido of using aid to undermine his government in a U.S.-orchestrated bid to oust him.

In comments broadcast on state TV, Defense Minister Vladimir Padrino said the opposition would have to pass over “our dead bodies” to impose a new government. Guaido, who has invoked the constitution to assume an interim presidency, denounces Maduro as illegitimate and has received backing from some 50 countries.

Padrino said it was unacceptable for the military to receive threats from Trump, and said officers and soldiers remained “obedient and subordinate” to Maduro.

“They will never accept orders from any foreign government … they will remain deployed and alert along the borders, as our commander in chief has ordered, to avoid any violations of our territory’s integrity,” Padrino said.

“Those that attempt to be president here in Venezuela … will have to pass over our dead bodies,” he said, referring to what he called Guaido’s efforts to create a “puppet government.”

Additionally, Thomson reports that Cuba denied on Tuesday it has security forces in Venezuela (after the Trump administration made claims):

“Our government categorically and energetically rejects this slander,” Cuban Foreign Minister Bruno Rodriguez said at a Havana press conference, adding all of the some 20,000 Cubans in Venezuela were civilians, most health professionals.

Rodriguez called on the U.S. administration to produce proof.

“The accusation by the US President that Cuba maintains a private army in Venezuela is despicable. I demand that you present evidence.

“There is a big political and communications campaign underway which are usually the prelude to larger actions by this government,” Rodriguez said.

Rodriguez termed the political crisis in Venezuela “a failed imperialist coup … fabricated in Washington,” and warned plans to deliver humanitarian aid were a recipe for violence and intervention.

“We are all witnesses in the making of humanitarian pretexts. A deadline has been set for forcing the entry of humanitarian aid,” Rodriguez said.

U.S. President Donald Trump on Monday warned members of Venezuela’s military who remain loyal to Maduro that they would “find no safe harbor, no easy exit and no way out.”

“You’ll lose everything,” Trump told a crowd of Venezuelan and Cuban immigrants in

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settingsWEDNESDAY morning 7:00 AM….

Euro/USA 1.1283 DOWN .0029 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES RED

USA/JAPAN YEN 110.76 UP .169 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2914 DOWN 0.0009 (Brexit March 29/ 2017/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.3255 UP .0019 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS WEDNESDAY morning in Europe, the Euro FELL by 26 basis points, trading now ABOVE the important 1.08 level FALLING to 1.1269/ Last night Shanghai composite closed UP 5.57 POINTS OR 0.20%/

//Hang Sang CLOSED UP 285.92 POINTS OR 1.81%

/AUSTRALIA CLOSED DOWN .14% /EUROPEAN BOURSES GREEN

The NIKKEI: this WEDNESDAY morning CLOSED UP 128.84 POINTS OR 0.60%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 285,92 POINTS OR 1.81%

/SHANGHAI CLOSED UP 5.57 POINTS OR 0.20%

Australia BOURSE CLOSED DOWN 14%

Nikkei (Japan) CLOSED UP 128.84 POINTS OR 0.60%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1344.00

silver:$16.03

Early WEDNESDAY morning USA 10 year bond yield: 2.63% !!! DOWN 3 IN POINTS from TUESDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%. (POLICY FED ERROR)/

The 30 yr bond yield 2.97 DOWN 1 IN BASIS POINTS from TUESDAY night. (POLICY FED ERROR)/

USA dollar index early TUESDAY morning: 96.59 UP 7 CENT(S) from TUESDAY’s close.

This ends early morning numbers WEDNESDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing WEDNESDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.52% UP 1 in basis point(s) yield from TUESDAY/

JAPANESE BOND YIELD: -.03% DOWN 0 BASIS POINTS from TUESDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.20% DOWN 1 IN basis point yield from TUESDAY

ITALIAN 10 YR BOND YIELD: 2.86 UP 8 POINTS in basis point yield from TUESDAY/

the Italian 10 yr bond yield is trading 166 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: FALLS TO +.10% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.76% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR WEDNESDAY

Closing currency crosses for WEDNESDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1359 UP .0020 or 20 basis points

USA/Japan: 110.73 UP 0.146 OR YEN DOWN 15 basis points/

Great Britain/USA 1.3069 UP.0010( POUND UP 10 BASIS POINTS)

Canadian dollar UP 60 basis points to 1.3151

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed HOLIDAY AT 6.7213 0N SHORE

THE USA/YUAN OFFSHORE: 6.7138( YUAN UP)

TURKISH LIRA: 5.3227

the 10 yr Japanese bond yield closed at -.03%

Your closing 10 yr USA bond yield UP 2 IN basis points from TUESDAY at 2.66 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 3.00 UP 2 in basis points on the day /

THE RISE IN BOTH THE 10 YR AND THE 30 YR ARE VERY PROBLEMATIC FOR VALUATIONS

Your closing USA dollar index, 96.39 DOWN 13 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for WEDNESDAY: 12:00 PM

London: CLOSED UP 40.28 OR 0.56%

German Dax : UP 90,09 POINTS OR .80%

Paris Cac CLOSED UP 33.73 POINTS OR 0.65%

Spain IBEX CLOSED UP 41.70 POINTS OR 0.46%

Italian MIB: CLOSED UP 81.75 POINTS OR 0.40%

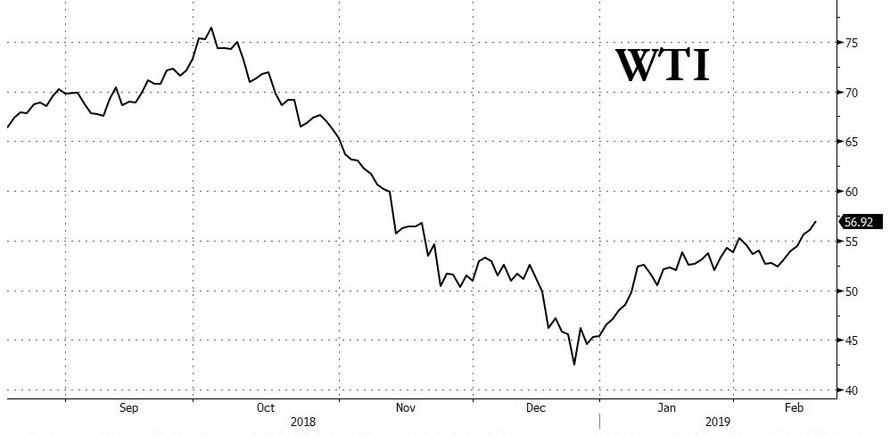

WTI Oil price; 56.92 1:00 pm;

Brent Oil: 67.24 12:00 EST

USA /RUSSIAN / ROUBLE CROSS: 65.54 THE CROSS LOWER BY 0.17 ROUBLES/DOLLAR (ROUBLE HIGHER BY 17 BASIS PTS)

TODAY THE GERMAN YIELD FALLS TO +.10 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM : 56.92

BRENT : 66.97

USA 10 YR BOND YIELD: … 2.64.. bond market did not buy the FOMC

USA 30 YR BOND YIELD: 2.99

EURO/USA DOLLAR CROSS: 1.1343 ( UP 4 BASIS POINTS)

USA/JAPANESE YEN:110.83 UP .252 (YEN DOWN 25 BASIS POINTS/..

.

USA DOLLAR INDEX: 96.51 DOWN 2 cent(s)/

The British pound at 4 pm: Great Britain Pound/USA:1.3058 DOWN 1 POINTS FROM YESTERDAY

the Turkish lira close: 5.3227