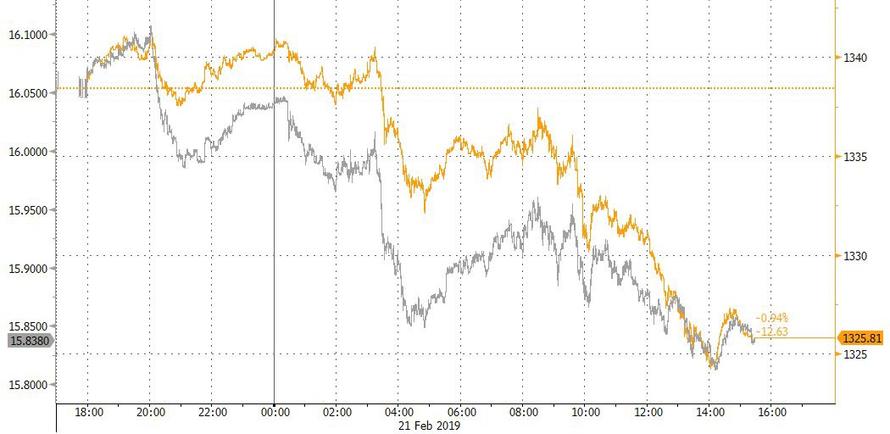

GOLD: $1325.45 DOWN $19.50 (COMEX TO COMEX CLOSING)

Silver: $15.87 DOWN 37 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1323.10

silver: $15.81

We begin options expiry week.

The comex options expire on Monday and the London/LBMA expires one week from today.

That is the reason the crooks whacked today. It is interesting that the crooks supplied a massive amount of paper silver but were rather reluctant to supply the same ratio in gold. Maybe they are afraid that too many investors are turning their paper gold into real physical gold

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 143 NOTICE(S) FOR 14300 OZ (0.4447 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10,466 NOTICES FOR 1,046600 OZ (32.5536 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

total number of notices filed so far this month: 567 for 2,835,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3942:DOWN $42

Bitcoin: FINAL EVENING TRADE: $3941 DOWN $44.

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 103/143

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,343.300000000 USD

INTENT DATE: 02/20/2019 DELIVERY DATE: 02/22/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

365 C ED&F MAN CAPITA 1

555 H BNP PARIBAS SEC 11

657 C MORGAN STANLEY 45

661 C JP MORGAN 30 103

661 H JP MORGAN 6

685 C RJ OBRIEN 25

690 C ABN AMRO 2

737 C ADVANTAGE 18 18

800 C MAREX SPEC 1 3

905 C ADM 23

____________________________________________________________________________________________

TOTAL: 143 143

MONTH TO DATE: 10,466

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUMONGOUS SIZED 5067 CONTRACTS FROM 220,822 UP TO 225,889 WITH YESTERDAY’S STRONG 19 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1924 EFP’S FOR MARCH, 120 FOR APRIL, 0 FOR MAY, 600 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2644 CONTRACTS. WITH THE TRANSFER OF 2644 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2644 EFP CONTRACTS TRANSLATES INTO 13.22 MILLION OZ ACCOMPANYING:

1.THE 19 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.840 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 22,432 CONTRACTS (FOR 14 TRADING DAYS TOTAL 22432 CONTRACTS) OR 112.16 MILLION OZ: (AVERAGE PER DAY: 1602 CONTRACTS OR 8.011 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 112.16 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 16.08% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 320.685 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5067 WITH THE 19 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2644 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GIGANTIC SIZED: 7711 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2644 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 5067 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 19 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.20 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.131 BILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.840 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 5914 CONTRACTS UP TO 510,553 WITH THE GAIN IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $3.10//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6689 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 6689 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 510,533. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,603 CONTRACTS: 5914 OI CONTRACTS INCREASED AT THE COMEX AND 6689 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 12,603 CONTRACTS OR 1,260,300 OZ = 39.20 TONNES. AND ALL OF THIS POWERFUL DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.10.

YESTERDAY, WE HAD 10,210 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 82,789 CONTRACTS OR 8,278,900 OZ OR 257.50 TONNES (14 TRADING DAYS AND THUS AVERAGING: 5,913 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAYS IN TONNES: 257.50 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 257.50/2550 x 100% TONNES = 10.00% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 777,63 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 5914 WITH THE GAIN IN PRICING ($3.10) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6689 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6689 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG 12,603 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6689 CONTRACTS MOVE TO LONDON AND 5914 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 39.20 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $3.10 IN YESTERDAY’S TRADING AT THE COMEX

we had: 143 notice(s) filed upon for 14,300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $19.50 TODAY

SURPRISE: A BIG CHANGE IN GOLD INVENTORY TODAY TO THE UPSIDE:

A DEPOSIT OF 2.05 TONNES

/GLD INVENTORY 794.50 TONNES

Inventory rests tonight: 792.50 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 37 CENTS IN PRICE TODAY:

SURPRISE: A HUGE CHANGE IN SILVER INVENTORY/ A DEPOSIT OF 1.688 MILLION OZ

THESE GUYS ARE NOTHING BUT FRAUDSTERS.

/INVENTORY RESTS AT 309.984 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 5067 CONTRACTS from 220,822 UP TO 225,889 AND CLOSER T0 THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1924 CONTRACTS FOR MARCH. 120 CONTRACTS FOR APRIL., 600 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2644 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 5067 CONTRACTS TO THE 2644 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN OF 7711 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 38.55 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.840 MILLION OZ STANDING IN FEBRUARY.

RESULT: A POWERFUL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 19 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 2644 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 9.42 POINTS OR 0.34% //Hang Sang CLOSED UP 115.87 POINTS OR 0.41% /The Nikkei closed UP 32.74 POINTS OR 0.150%/ Australia’s all ordinaires CLOSED UP 0.63%

/Chinese yuan (ONSHORE) closed UP at 6.7182 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7182 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7151: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/USA//TAIWAN

Taiwan’s leader is very worried about a Chinese invasion. The threat is ‘growing every day”

( zerohedge)

4/EUROPEAN AFFAIRS

i)DEUTSCHE BANK/GERMANY

Our good friends over at the world’s largest derivative player Deutsche bank hid a 10 yr loss from regulators. Eventually the loss mushroomed 4 x its original loss as 1.6 billion dollars was hidden.

( zerohedge)

Despite providing less than 1% of its GDP for defense, Merkel defends her gas deal for Russian gas…mainly becuase it is much cheaper than the USA. Trump is not a happy camper

( zerohedge)

iii)GERMANY/SAUDI ARABIA

This has consequences for NATO as Germany rebuffs the UK call to back off Saudi arms freeze. Germany wants to export these fighter jets to the Saudis and if rebuffed it will hurt their export markets terribly

( zerohedge)

iv)GERMANY/RUSSIA/NATO

Despite providing less than 1% of its GDP for defense, Merkel defends her gas deal for Russian gas…mainly because it is much cheaper than the USA. Trump is not a happy camper

( zerohedge)

v)HUNGARY/EU

Euroskeptic Prime Minister Orban attacked the drunkard Juncker and Soros in a billboard ad

(courtesy Mish Shedlock/Mishtalk)

vi)Europe

Europe continues to disappoint as factory orders are dragging the 27 EU economy to a near halt

( Reuters/)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/TURKEY/USA

NATO and uSA ally Turkey totally defies the Americans as they set to receive the Russian S 400 surface to air defense missile system in July. They rejected the uSA patriot system

( zerohedge)

ii)Russia continues with its rhetoric against the USA. Trump ignores Putin.

(courtesy zerohedge)

6. GLOBAL ISSUES

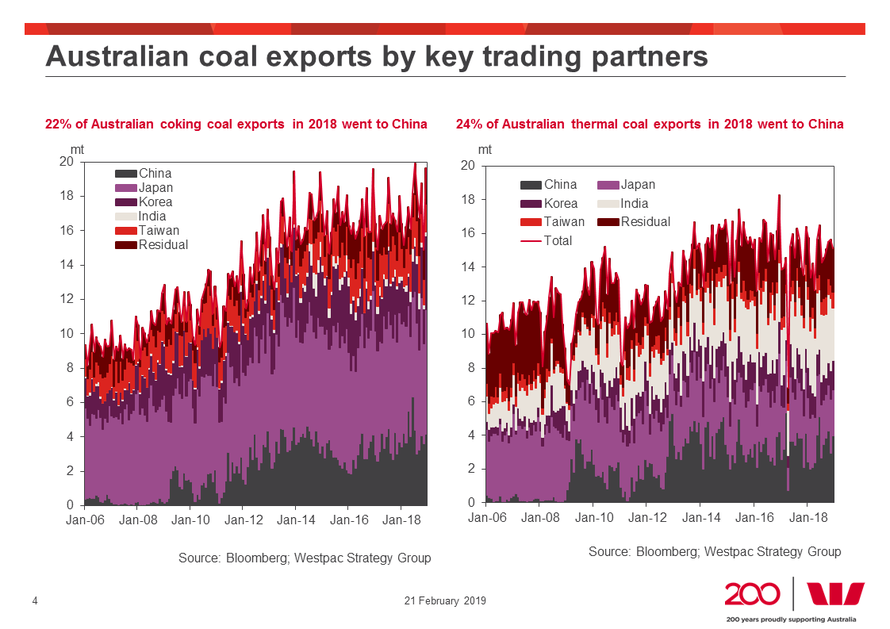

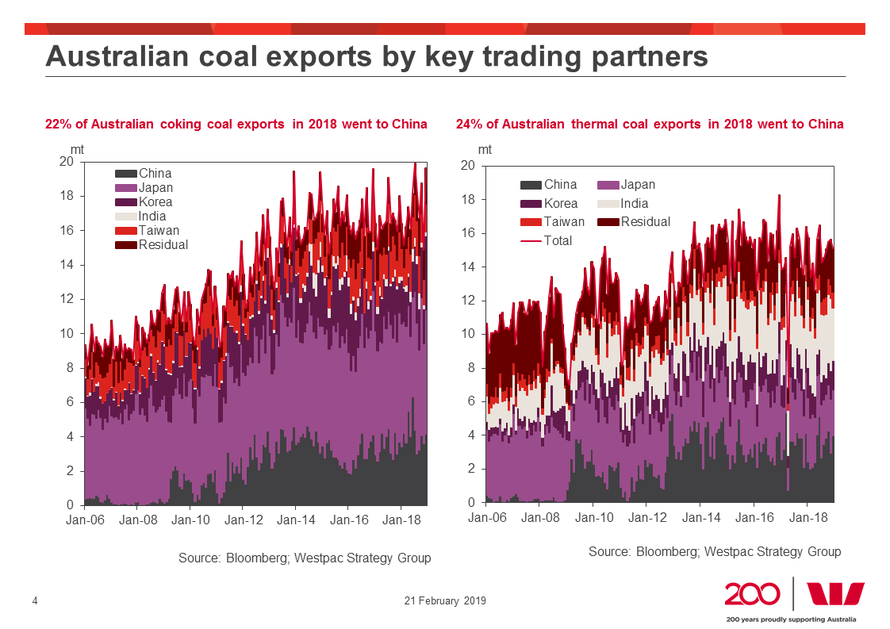

i)And they are close to a Memorandum of Understanding??? the trade war goes ballistic as China indefinitely bans the importation of Australian coal..a staple of the Australian economy

( zerohedge)

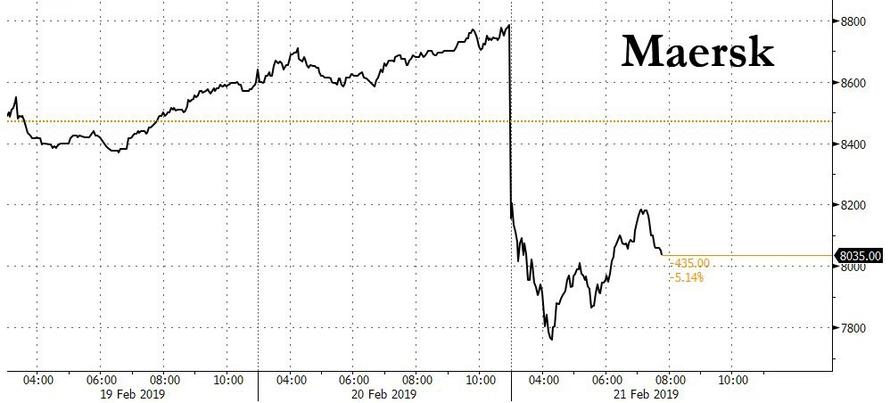

ii)Whenever these guys (Maersk) issues a warning, pay attention: They state that the 2019 global economic outlooks is worse than last year

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

Our resident expert on the Deep State explains why Venezuela may be on the verge of becoming another Syria as Russia and China will enter the scene if the USA tries to give their version of “humanitarian aid…

(courtesy Brandon Smith)

ii)Not good: Protesters executed as they protest.

( zerohedge)

iii)Maduro closes the Venezuelan border with Brazil:

( zerohedge)

9. PHYSICAL MARKETS

ii)Now Asia does a sharp turn as it seems that monetary policy is easing across the globe

( Reuters/Zaharia/GATA)

iii)Palladium has a huge short position and it’s prices are in constant backwardation. Will Palladium break the bank?

Platinum is very low and i will bet that the car manufacturers are ready to switch to Pt from Palladium

( Craig Hemke/Sprott/GATA)

iv)Barrick may be allowed to export gold dore from its subsidiary Acacia gold

(McGee/Globe and Mail/GATA

v)This will be good for the gold industry: Trump is ready to allow the controversial Alaska Pebble project to proceed

(Anchorage Daily News//GATA)

vi)We brought this story to your attention yesterday but it is worth repeating. The criminal Deutsche bank continues to defraud whenever they can. It is their destiny ….

( Wall Street Journal/GATA)

vii)A real joke: the shareholder’s gold council has no interest in finding out how gold/silver being manipulated by the bullion banks

( GATA/)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

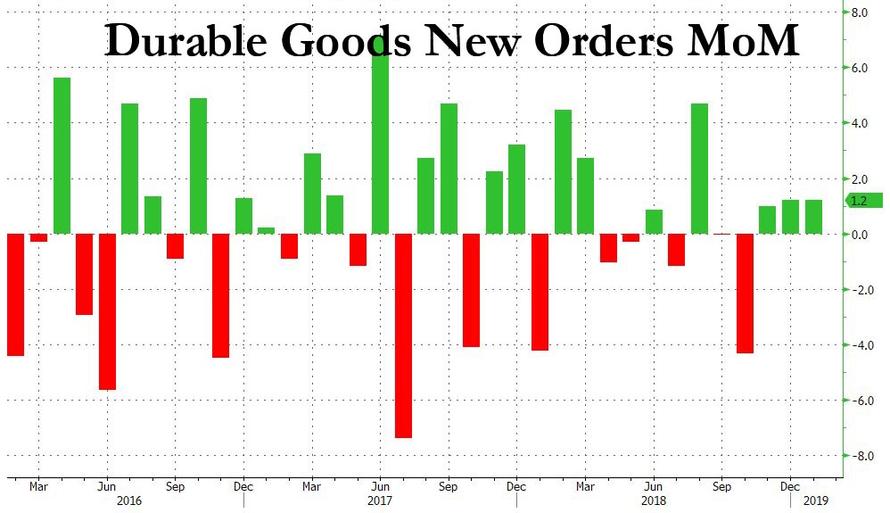

a)Durable goods rose less than expected at just 1.2% instead of 1.7% from Nov 1.2018. The report is for two months and data continues to show the USA economy contracting

( zerohedge)

b)This is quite interesting: soft data Philly Fed (Mfg) index drops big time, the largest drop since 2011 and it falls into the negative category i.e. a drop to +17.0 to – 4.1. The data continues to show that the USA economy is faltering badly.

( zerohedge)

c)A biggy!~! USA manufacturing PMI tumbles to a 17 month low..continual numbers showing that the uSA is contracting.

( zerohedge)

( zerohedge)

e)JPMorgan now estimates first quarter GDP 2019 at only 1.5%

iv)SWAMP STORIES

a)Smollet charged with felony after falsely reporting a hate crime

( zerohedge

( zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 16.563 CONTRACTS DOWN TO 70,821 CONTRACTS. AFTER MARCH, APRIL ADVANCES TO 353 CONTRACTS FOR A GAIN OF 105 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 19,548 CONTRACTS UP TO 111,837 CONTRACTS.

FIRST DAY NOTICE IS THURSDAY FEB 28.2019

comex gold volumes are getting extremely low as players just do not want to play in this casino.

Global Fina

Shuli Ren: U.S., not China, is the currency manipulator

Submitted by cpowell on Wed, 2019-02-20 15:17. Section: Daily Dispatches

The Yuan Has Been Tracking the Dollar, So Any Volatility Begins at Home in Washington.

By Shuli Ren

Bloomberg News

Wednesday, February 20, 2019

President Donald Trump should take a look in the mirror. China isn’t the currency manipulator.

The U.S. is asking Beijing to keep the value of the yuan stable as part of trade negotiations between the world’s two largest economies, Saleha Mohsin and Katherine Greifeld of Bloomberg News reported. Washington fears that China could weaken its currency to counteract the effect of higher American tariffs on imports from the nation

That perception is unfair. Despite the trade conflict, the People’s Bank of China has effectively pegged the yuan to the dollar, loyally following the greenback’s cycle. …

… For the remainder of the commentary:

https://www.bloomberg.com/opinion/articles/2019-02-20/the-u-s-not-china-…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

Now Asia does a sharp turn as it seems that monetary policy is easing across the globe

(courtesy Reuters/Zaharia/GATA)

In sharp U-turn, monetary policy easing is back in play across Asia

Submitted by cpowell on Wed, 2019-02-20 15:31. Section: Daily Dispatches

By Marius Zaharia

Reuters

Wednesday, February 20, 2019

HONG KONG — A slowing global economy and increasing strain on businesses from a year-long Sino-U.S. trade war are tilting central banks from Japan to Australia toward monetary easing in a remarkable 180-degree turn.

Late last year the debate in Japan was focused on the demerits of printing money and the Reserve Bank of Australia was adamant the next likely move in rates will be up. An emerging market currency selloff was seen forcing externally vulnerable economies such as India, Indonesia and the Philippines to keep tightening their policy rates.

But even they are now subject to rate cut bets.

A softer dollar and lower oil prices played an important role in the turnaround. But crucially for Asia, regional growth engine China is having a worse than expected start to the year and is exporting disinflation to the rest of the region. …

… For the remainder of the report:

https://www.reuters.com/article/us-asia-economy-rates/in-sharp-u-turn-mo…

* * *

END

Palladium has a huge short position and it’s prices are in constant backwardation. Will Palladium break the bank?

Platinum is very low and i will bet that the car manufacturers are ready to switch to Pt from Palladium

(courtesy Craig Hemke/Sprott/GATA)

Is palladium the magic bullet against the banking cartel, or is it about to crash?

Submitted by cpowell on Thu, 2019-02-21 02:15. Section: Daily Dispatches

9:13p ET Wednesday, February 20, 2019

Dear Friend of GATA and Gold:

Because palladium’s lease rates are high, its futures prices are uniformly in backwardation against its spot price, and its short position in Comex futures contracts is so much larger than the metal available in Comex vaults, the TF Metals Report’s Craig Hemke writes today that the metal is the best bet for breaking the banking cartel’s lid on metal prices.

Hemke’s analysis is headlined “The Magic Palladium Bullet” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-magic-palladium-bullet-craig-hemke

Meanwhile 321Gold’s Bob Moriarty disagrees, arguing — when he’s done promoting his new book — that palladium will soon crash because sentiment about the metal is way too bullish. Moriarty’s analysis is headlined “Basic Investing in Resource Stocks, or Why Palladium is about to Fall Off a Cliff” and it’s posted at 321Gold here:

http://www.321gold.com/editorials/moriarty/moriarty022019.html

Your secretary/treasurer is no investment adviser but has seen enough intervention in the markets during GATA’s 20 years to suspect that, since governments and central banks are always surreptitiously trading all futures markets —

http://www.gata.org/node/14385

http://www.gata.org/node/14411

— theirs is the only sentiment that really matters most of the time, at least until a commodity is on the verge of running out and can’t effectively be shorted anymore.

Exhaustion of supply doesn’t happen often, but it happens, as it did with gold in 1968 upon the collapse of the London Gold Pool:

https://en.wikipedia.org/wiki/London_Gold_Pool

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Barrick may be allowed to export gold dore from its subsidiary Acacia gold

(McGee/Globe and Mail/GATA)

Barrick outlines agreement with Tanzania aimed at ending Acacia gold export ban

Submitted by cpowell on Thu, 2019-02-21 02:44. Section: Daily Dispatches

By Niall McGee

The Globe and Mail, Toronto

Wednesday, February 20, 2019

https://www.theglobeandmail.com/business/article-barrick-outlines-agreem…

Barrick Gold Corp. has reached a new agreement with Tanzania that may end a punishing multiyear gold-export ban at its subsidiary Acacia Mining that has weighed heavily on the share prices of both companies.

The development comes about six weeks after skilled African operator Mark Bristow took over as the new chief executive officer of Toronto-based Barrick.

…

The latest proposal would see Acacia split “economic benefits,” including taxes and royalties from its Tanzanian mines, 50/50 with the East African country. Acacia would also pay Tanzania US$300-million to resolve a long-running tax dispute. While the agreement is similar to one announced in late 2017, the tax penalty can be paid over time, instead of up front. Barrick says it will present a proposal to Acacia in the “near future.”

Unusually, Barrick, which owns 63.9 percent of London-based Acacia, has been negotiating with the Tanzanian government on its behalf. Acacia’s management team was locked out of discussions partly because of its poor relationship with Tanzania.

“Significant amounts of real value have been destroyed by this dispute,” Mr. Bristow said in a statement today.

“This proposal will allow the business to focus on rebuilding its mining operations in partnership with their respective stakeholders, and, most importantly, long-suffering investors, including Barrick.”

In a statement today, Acacia said that an independent committee of its board of directors must review any proposal. A shareholder vote at Acacia must also take place before the agreement could take effect and the Tanzanian government would have to give its stamp of approval.

“Whilst crunching the numbers on all of this is hard to do right now, if it allows operations to return to normal, it could be a net positive for Acacia,” RBC Dominion Securities analyst James Bell wrote in a note to clients.

Shares in Barrick, which owns 63.9 percent of Acacia, rose by just more than 1 percent on the Toronto Stock Exchange, while Acacia’s stock shot up by 12.8 percent on the London Stock Exchange, the biggest increase in 16 months.

After Barrick’s US$6-billion acquisition of Randgold Resources Ltd. was announced in September, there was hope that Mr. Bristow, who joined the company as CEO, might be able to end the Acacia impasse considering his long history of operating successfully in Africa.

Over the past few years a number African countries, including Democratic Republic of the Congo and Zambia, have introduced punitive tax measures that have driven up the cost of doing business abroad for Canadian miners.

The Acacia tax fracas can be traced back to the election in 2015 of Tanzanian President John Magufuli, who promised to go after a bigger share of the mineral wealth. Tanzania historically had a relatively light tax code in place for Western miners. In 2017 Mr. Magufuli zeroed in on Acacia, accusing the company of US$200 billion in tax fraud and rolling out a crippling gold-concentrate export ban. While Acacia maintains it has paid a significant amount in taxes to Tanzania over time, both Mr. Bristow and Barrick’s executive chairman John Thornton have argued it needs to pay more.

“Despite all the promises,” Acacia hasn’t delivered real taxable profits,” Mr. Bristow said in an interview last week.

He also said that a 50/50 split in the economics between Tanzania and Acacia is “reasonable” when compared with current tax rates imposed by other African countries on Western miners.

After a tentative agreement was reached in October 2017, talks between Barrick and Tanzania hit a stalemate, with neither side revealing what had gone wrong. Late last year relations between Acacia and Tanzania deteriorated further with criminal money-laundering charges laid against three employees and one ex-employee. Three of the individuals are still being detained in Tanzania under non-bailable offences. Mr. Bristow characterized the situation as “a product of the fallout of the relationship between Acacia and the government.”

END

This will be good for the gold industry: Trump is ready to allow the controversial Alaska Pebble project to proceed

(Anchorage Daily News//GATA)

Feds advance Alaska’s Pebble gold and copper project with release of draft environmental review

Submitted by cpowell on Thu, 2019-02-21 03:33. Section: Daily Dispatches

By Alex DeMarban

Anchorage Daily News, Anchorage, Alaska

Wednesday, February 20,2019

The Trump administration today unveiled the first draft environmental review of the controversial Pebble gold and copper project.

The report is a key step in the regulatory process and will lead to a 90-day public comment period for the southwest Alaska mine that has been in the works for more than a decade, the U.S. Army Corps said.

…

The agency is expected to release a final environmental report and make a final decision in 2020 to help determine how development should proceed at the giant prospect in the Bristol Bay region. Other state and federal agencies must also weigh in before mining can begin, and the Environmental Protection Agency still holds the option to essentially veto the project, Corps officials said.

The 1,400-page report, including hundreds more pages in supporting documents, is broken down into several chapters and is available at the federal agency’s Pebble Project website, pebbleprojecteis.com.

If built, the open-pit mine would be about 200 miles southwest of Anchorage, straddling salmon-producing headwaters of the valuable Bristol Bay fishery. …

… For the remainder of the report:

https://www.adn.com/business-economy/2019/02/20/feds-release-draft-envir…

END

We brought this story to your attention yesterday but it is worth repeating. The criminal Deutsche bank continues to defraud whenever they can. It is their destiny ….

(courtesy Wall Street Journal/GATA)

Deutsche Bank lost $1.6 billion on municipal bond bet, concealed it

Submitted by cpowell on Thu, 2019-02-21 03:42. Section: Daily Dispatches

By Jenny Strasburg and Gretchen Morgenson

The Wall Street Journal

Wednesday, February 20, 2019

Deutsche Bank racked up a loss of $1.6 billion over nearly a decade on a complex municipal-bond investment that it bought in the run-up to the 2008 financial crisis and failed to confront even as markets were upended and regulations tightened.

The loss, which hasn’t previously been reported, represents one of Deutsche Bank’s largest ever from a single wager — roughly quadruple its entire 2018 profit — and ranks as one of the banking industry’s biggest soured bets in the last decade.

…

The prolonged struggle over how to handle the investment sheds light on cultural and financial challenges inside one of Europe’s biggest banks that have hampered its ability to compete with stronger U.S. rivals.

Deutsche Bank resisted for years reducing the value of those bonds and related derivatives on its books to a level that markets suggested they were worth, and it brushed aside concerns raised by the bank’s financial auditors about how it was valuing the trade, according to internal bank documents and people involved in discussions about the investment.

During that time period, the bank was telling investors its internal financial controls were sound, and it raised billions of dollars in the capital markets without any disclosure of the bond valuation issue. Behind the scenes, the badly timed bet exerted a sustained drag on the bank’s finances. …

… For the remainder of the report:

https://www.wsj.com/articles/deutsche-bank-lost-1-6-billion-on-a-bond-be…

END

A real joke: the shareholder’s gold council has no interest in finding out how gold/silver being manipulated by the bullion banks

(courtesy GATA/)

Shareholders’ Gold Council doesn’t want to hear about market rigging

Submitted by cpowell on Thu, 2019-02-21 14:57. Section: Daily Dispatches

10a ET Thursday, February 21, 2019

Dear Friend of GATA and Gold:

The Shareholders’ Gold Council, started last year by fund manager John Paulson “to conduct research reports and studies of interest to investors in the gold industry” (https://www.goldcouncil.net/), has rejected GATA’s requests for membership and to make a presentation about manipulation of the gold market by central banks and their bullion bank agents.

A representative of the council has told GATA that “our focus is on the companies themselves, not the gold market.”

Of course that’s not quite how the council’s internet site describes it, but the council is entitled to what seems to be its opinion that the manipulation of the price of the metal produced by gold-mining companies is of no interest to the companies themselves.

Shareholders in gold-mining companies might be equally entitled to some puzzlement about this.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7182/

//OFFSHORE YUAN: 6.7151 /shanghai bourse CLOSED DOWN 9.42 POINTS OR 0.34% /

HANG SANG CLOSED UP 115.87 POINTS OR 0.41%

2. Nikkei closed UP 32.74 POINTS OR 0.15%

3. Europe stocks OPENED MIXED

/USA dollar index RISES TO 96.46/Euro RISES TO 1.1353

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.24 and Brent: 66.95

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.13%/Italian 10 yr bond yield DOWN to 2.84% /SPAIN 10 YR BOND YIELD DOWN TO 1.20%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.71: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.77

3k Gold at $1335.40 silver at:15.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 19/100 in roubles/dollar) 65.74

3m oil into the 57 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.71 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0007 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1361 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.13%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.67% early this morning. Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3114

Market Rally Fizzles As New Front Breaks Out In Global Trade War Amid Dismal Econ Data

Another strong overnight market rally, built on the back of – what else – trade deal optimism, fizzled with US futures paring gains, European stocks edging lower and Asian shares rising as initial optimism was dented following more revelations that for all pompous talk, and now multiple MoUs, the trade war is actually escalating behind the scenes.

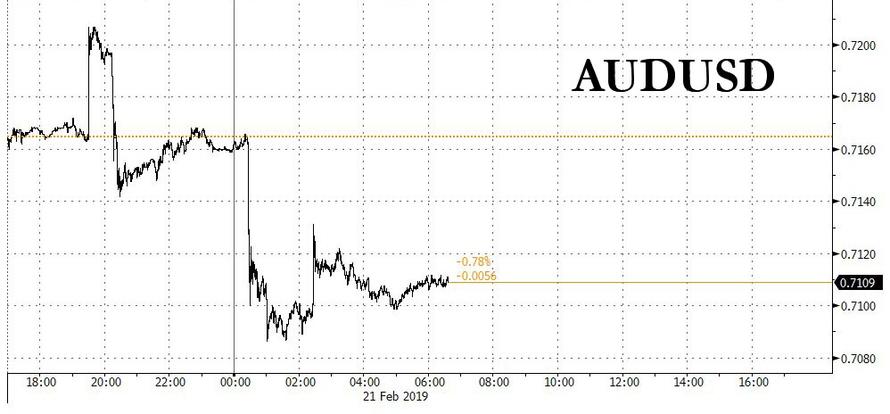

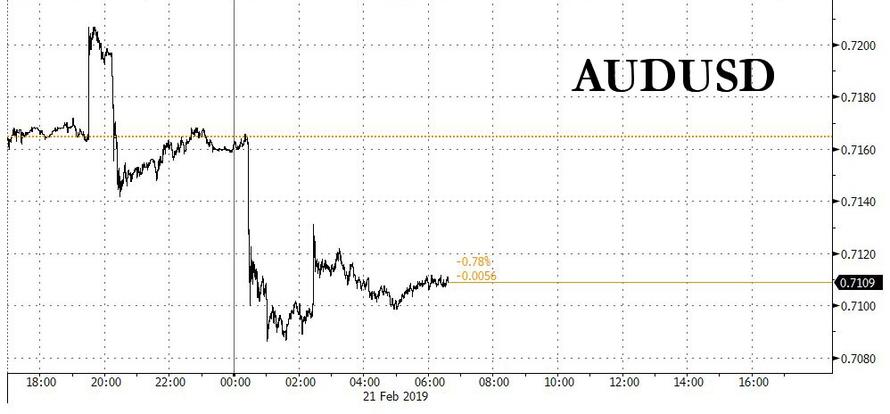

Europe’s Stoxx 600 Index drifted lower, weighed down by bank shares as individual companies including Centrica and shipping giant Maersk also underperformed after disappointing earnings. Over in the US, futures on all three main indexes levitated higher following Fed minutes that merely added to dovish sentiment, after a late Wednesday report that negotiators are working on multiple memorandums of understanding that would form the basis of a final trade deal; however the latest trade deal optimism – which has now become a daily joke as the market now prices in a successful outcome to the trade war every single day – faded, Chinese stocks dropped the yuan pared an advance and the Aussie plunged after a report that China’s Dalian port banned coal imports from Australia while Westpac, called for two RBA rate cuts this year.

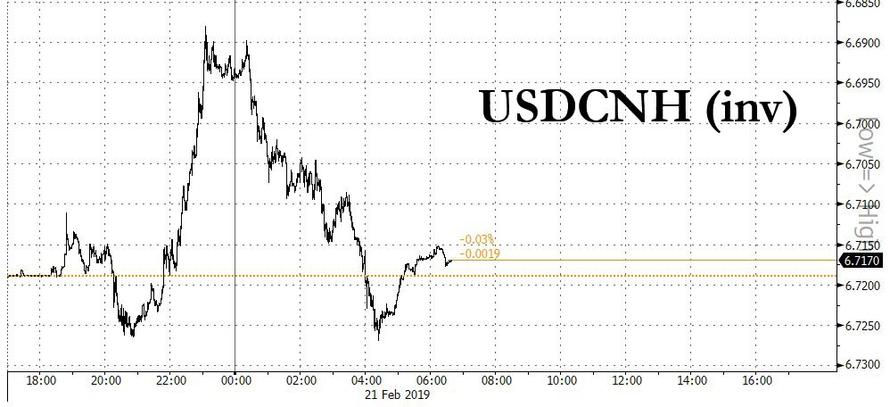

The Aussie was last trading at $0.7105, down 0.8 percent on the day but it was not the only one struggling. The Kiwi dollar got bundled down 0.5 percent and the euro had given back its early gains to stand at $1.1320. The slide in the Aussie dollar had helped its share market close at a six-month high. Japan’s Nikkei had ended 0.1% stronger too and though Chinese shares sagged, the “offshore” yuan firmed to its strongest level since July on the trade hopes.

MSCI’s main Asia-Pacific index rose to a 4-1/2 month high, lifted by the initial, more optimistic trade reports, while generally ignoring the new trade war between Australia and China.

As noted earlier, the reported banning of Australian coal imports at the Chinese port of Dalian is seen as a sign that Beijing is flexing its economic muscles and warning nations not to bar its next-generation, 5G wireless technology or Huawei for that matter. The indefinite coal restrictions started this month and are part of an overall plan to cap imports into the customs region this year, Reuters reported, citing an unnamed Dalian Port official.

How China blocking Australian exports is conducive to a trade deal is beyond any rational thinking person, however, since algos are neither, they merely digested the “optimistic” headlines and futures are still higher, but fading gains fast.

In any case, the “steady” progress toward a trade agreement between the world’s biggest economies – one which could take years sending the S&P above 3,000 on “optimism” a deal is coming any moment, could give further impetus to a risk rally with the MSCI world index up about 15 percent since Christmas Day. But the new front in the global spat, this time between China and Australia, risks denting investor sentiment before concrete progress is seen in Washington.

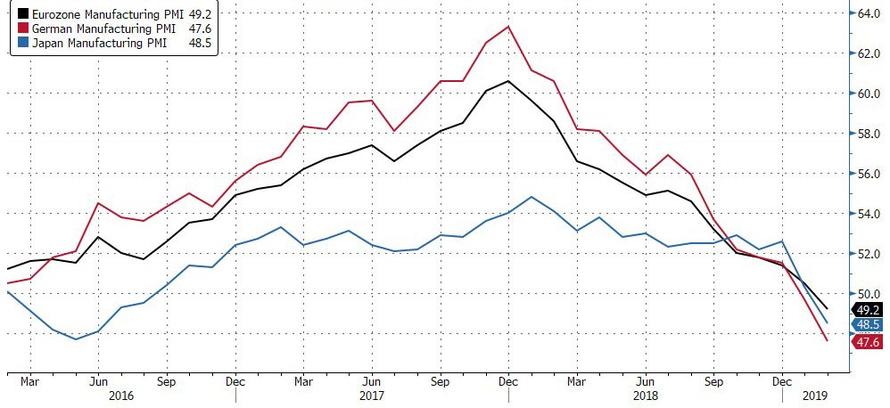

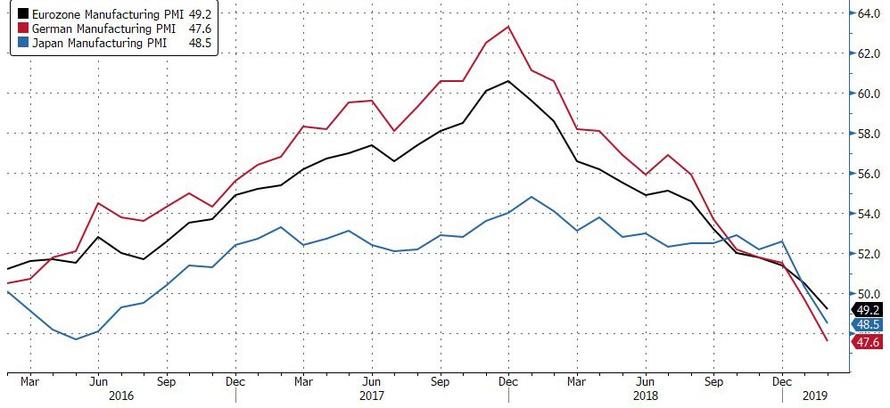

Meanwhile, the global economic picture is going from bad to abysmal, with manufacturing PMIs in Germany, Japan and the Eurozone all now officially in contraction, i.e. recession, territory.

“The euro zone economy remained close to stagnation in February. The general picture remained one of a more subdued business environment than seen throughout much of last year,” Chris Williamson, IHS Markit’s chief business economist said. Williamson said the results pointed to first-quarter euro zone growth of just 0.1 percent, below the latest Reuters poll estimate for 0.4 percent. They come soon after the European Central Bank ended its more than 2.6 trillion euro asset purchase stimulus program.

Elsewhere, Treasuries drifted lower with the 10Y yield rising 3bps to 2.67% while European bonds were mixed and the euro fluctuated.

Today’s trading session follows a muted day in the markets yesterday, following a FOMC Minutes release that had something in it for everyone: the overall tone of Fed rhetoric should “help to keep financial markets relatively steady as we head toward the weekend, all in the context of the recent risk asset roller coaster that has resulted from overly hawkish miscommunication from the Fed late last year, followed in January by an apparent overly-dovish policy U-turn,” Simon Ballard, a macro strategist at First Abu Dhabi Bank, wrote in a note.

In other FX, the dollar relinquished an Asia-session advance as the pound reversed losses amid growing Brexit optimism, only to tumble after an official said a deal was not coming. Sterling also shrugged off Fitch putting its UK credit rating on a formal downgrade warning amid uncertainty about whether the country’s parliament will be able to agree a transition deal before next month’s planned Brexit date.

Europe’s common currency swung between gains and losses and euro-area bonds traded mixed amid concerns over a slump in manufacturing in the region. Treasuries traded in the red, while European stocks were mixed and U.S. futures pointed to a higher open.

In the commodity market, crude prices rose more than 1 percent on Wednesday to their highest in 2019 on hopes that oil markets will balance later this year. U.S. crude was last up 0.3 percent, or 17 cents, at $57.33 per barrel. Brent was 0.1 percent, or 5 cents, higher at $67.13.

Initial jobless claims, durable goods orders and Markit PMI data are due. Scheduled earnings include Intuit and Hormel Foods

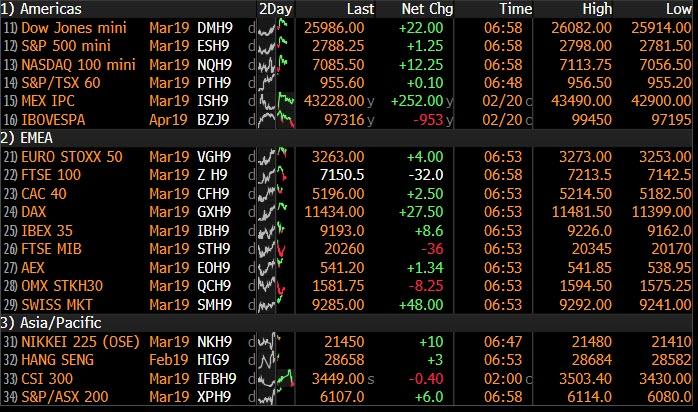

Market Snapshot

- S&P 500 futures up 0.1% to 2,790.25

- STOXX Europe 600 down 0.06% to 371.23

- MXAP up 0.2% to 159.07

- MXAPJ up 0.3% to 521.17

- Nikkei up 0.2% to 21,464.23

- Topix unchanged at 1,613.50

- Hang Seng Index up 0.4% to 28,629.92

- Shanghai Composite down 0.3% to 2,751.80

- Sensex up 0.4% to 35,908.47

- Australia S&P/ASX 200 up 0.7% to 6,139.25

- Kospi down 0.05% to 2,228.66

- German 10Y yield rose 1.0 bps to 0.11%

- Euro down 0.04% to $1.1333

- Brent Futures down 0.09% to $67.02/bbl

- Italian 10Y yield rose 7.0 bps to 2.499%

- Spanish 10Y yield fell 1.5 bps to 1.185%

- Gold spot down 0.3% to $1,334.15

- U.S. Dollar Index up 0.1% to 96.56

Top Overnight News

- The reported banning of Australian coal imports at the Chinese port of Dalian is maybe a sign that Beijing is flexing its economic muscles and warning nations not to bar its next- generation wireless technology. The indefinite coal restrictions started this month and are part of an overall plan to cap imports into the customs region this year, Reuters reported, citing an unnamed Dalian Port official.

- U.S. and Chinese negotiators are working on multiple memorandums of understanding that would form the basis of a final trade deal, according to a person briefed on the talks. The MoUs would cover areas including agriculture, non-tariff barriers, services, technology transfer and intellectual property, said the person, who asked not to be identified because the discussions are private

- Federal Reserve policy makers see 2019 marking the end of their balance sheet run-off, but not necessarily their interest-rate increases, according to minutes of the central bank’s Jan. 29-30 policy meeting released Wednesday

- Brexit Secretary Steve Barclay and Attorney General Geoffrey Cox are due in Brussels Thursday with proposed changes the U.K. is seeking to the divorce deal to make it acceptable to the House of Commons. Fitch placed the U.K.’s AA grade on rating watch negative, citing concerns over Brexit

- President Donald Trump reiterated his threat to impose tariffs on cars imported from the European Union if the U.S. can’t reach a trade deal with the EU

- Activity in Japan’s manufacturing sector contracted in February for the first time in two and a half years, as production and new orders fell, according to preliminary data that will strengthen concerns about a global economic slowdown

- Oil extended gains from a three-month high as industry data signaled a limited increase in American crude stockpiles

- U.K.’s Hammond said deadline pressure in the Brexit talks was helping officials to make progress and British lawmakers could vote on a revised deal next week. He said there were positive signs coming from Brussels that the EU is moving its position and giving ground on the Irish border backstop, and it was “significant” that the EU is now promising “guarantees” that the contentious backstop will be temporary

- In a sign of the challenge that U.K. Prime Minister Theresa May faces next week, as many as 15 government ministers are debating voting against her Brexit strategy and then challenging her to fire them in next week’s planned ballots, three people familiar with the matter said. The senior officials want to back a cross- party effort to stop Britain crashing out of the EU without a deal

Asian equity markets eventually traded mostly higher with the region supported by US-China trade hopes after reports that negotiators were drafting MOUs on key structural issues and are looking at a list of measures to address the trade imbalance. This helped the region shake off the early cautious tone brought on by another marginal performance of their US counterparts and a mixed-perceived FOMC minutes. ASX 200 (+0.7%) was underpinned by strength in Financials as well as outperformance in Consumer Discretionary after Wesfarmers shares rallied post-earnings, while the trade hopes inspired a turnaround for the Nikkei 225 (+0.2%) which was initially dampened by currency effects and after Nikkei Manufacturing PMI data slipped into contraction territory for the 1st time since August 2016. Elsewhere, the KOSPI (+0.1%) lagged with index heavyweight Samsung Electronics lacklustre after it unveiled its ground-breaking foldable smartphone which comes with an eye-watering price of nearly USD 2000, while Hang Seng (+0.4%) and Shanghai Comp. (-0.3%) were also initially choppy before the trade-related optimism provided a rising tide across the region. Finally, 10yr JGBs found support from the early cautious tone and after disappointing Nikkei Manufacturing PMI data, but then reversed course as risk sentiment improved and after weaker results in the enhanced liquidity auction for longer-dated bonds.

Top Asian News

- Top PC Maker Lenovo Gains Most in a Decade as Turnaround Sticks

- Goldman Says Asian Funds Positioned All Wrong for 2019’s Rally

- Hong Kong Monetary Authority Chief Norman Chan to Retire Oct. 1

Major European indices are mixed [Euro Stoxx 50 +0.1%] in spite of the firmer trade seen in Asia following reports that negotiators are drafting MOU’s. The FTSE 100 (-0.6%) is underperforming its peers, weighed on by BAE Systems (-7.0%) and Centrica (-11.8%) following earnings for both Co’s; additional downward pressure is applied by Anglo American (-0.1%) after earnings and Glencore (-1.5%) who are in the red following a tax demand and mine production cut. Sectors are mixed, with some mild outperformance in consumer discretionaries. Other notable movers include Bouygues (+3.4%) near the top of the Stoxx 600 as their FY profit came in above the prior. Also performing well after earnings are Barclays (+0.2%), with the Co. stating they are considering additional returns which include buybacks. Of note are Maersk (-9.6%) in the red after stating that 2019 guidance is subject to considerable uncertainty from trade risks, also the Co. and Maersk Drilling are to trade separately from April 4th.

Top European News

- Telecoms Trail in Europe as Results From Heavyweights Fall Flat

- European Banks Caught Between Nordic Contagion and Barclays Joy

- Just Eat Drops on Report Uber Eats Eyes U.K. Marketplace Service

In FX, it was a really rough night for the Antipodean Dollars, and especially the Aud that failed to glean any lasting benefit from a robust if not stellar January jobs report, as Westpac delivered an extremely dovish RBA outlook with not just one, but two rate cuts pencilled in for this year (August and November). Aud/Usd recoiled from just over 0.7200 in response and then reversed even more sharply on headlines reporting that China was blocking coal imports as several ports including the main Dalian hub, hitting lows under 0.7100. Meanwhile, Aud/Nzd fell from around 1.0490 to circa 1.0400, but is holding above the base as Nzd/Usd suffers knock-on losses towards 0.6800 vs 0.6875 at one stage.

- CAD/CHF/EUR – All on a softer footing vs the Greenback, as the DXY recovers from its post-FOMC minutes lows and with the overall take from the release not as dovish as many anticipated or were positioned for (end of balance sheet reduction by end 2019 favoured by most, but prospect of further rate normalisation this year left on the table) – index straddling 96.500 vs 96.390 at one stage. The Loonie is close to the bottom of a 1.3207-1.3163 range, while the Franc is back below parity, albeit just, and the single currency is pivoting 1.1350 amidst mixed Eurozone flash PMIs, volatile trade on stops and near term technical with some hefty option expiries also thrown in for good measure. Specifically, 1.1365, 1.1371-73 represent resistance, with the latter zone incorporating Wednesday’s high and the 30 DMA, while 1.2 bn rolls off at the 1.1300 strike and almost 3 bn at 1.1400.

- GBP/JPY – Relative G10 outperformers as Cable holds firmly above 1.3000, after a few wobbles, and not far from overnight peaks just over 1.3100 following a record UK public finance haul in January, a well received 2057 Gilt auction and comments from Chancellor Hammond suggesting the EU is showing some willingness to budge on the Irish backstop. Meanwhile, the Jpy has pared some losses within a 110.60-87 range in wake of another drop in the PBoC’s mid-point Usd/Cny fixing rate.

- NOK/SEK – The Scandi Crowns are both back under pressure, with Eur/Nok nudging above 9.7900 against the backdrop of stagnating oil prices and a somewhat disappointing Norwegian energy investment report, while Eur/Sek has rebounded to 10.6000+ from around 10.5600 following the IMF’s annual report that revealed a downward revision to Sweden’s 2019 GDP forecast and urged the Riksbank to hold off from another repo rate hike.

In commodities, Brent (+0.1%) and WTI (+0.5%) prices are largely unchanged after a mixed overnight session, with both Brent and WTI trading within a narrow USD 1/bbl range. Yesterday’s delayed API release showed a crude oil inventories build of 1.26mln barrels, although this was less than the expectation for a 3.1mln barrel build. EIA’s delayed weekly report is to be published later today where expectations are for a crude stock build of 3.1mln, which would make it the fifth consecutive week of builds. Elsewhere, reports show that Venezuela are paying large premiums for Russian and European fuel imports due to a limited number of available sellers, following US sanctions against PDVSA. Gold (-0.2%) is weaker after trading largely sideways overnight, with the yellow metal approaching the bottom of its USD 10/oz range. Elsewhere, Barrick Gold have outlined a deal reached with the Tanzania government, which features a USD 300mln payment, regarding disputes with Acacia Mining. Separately, China’s northern Dalian port bans imports of Australian coal and are to cap overall imports for the year at 12mln tonnes; this ban follows other Chinese ports taking 40 days to clear Australian coal. China’s Dalian customs bans Australian coal imports indefinitely and sets 12mln tons overall coal import quota for this year, according to sources.

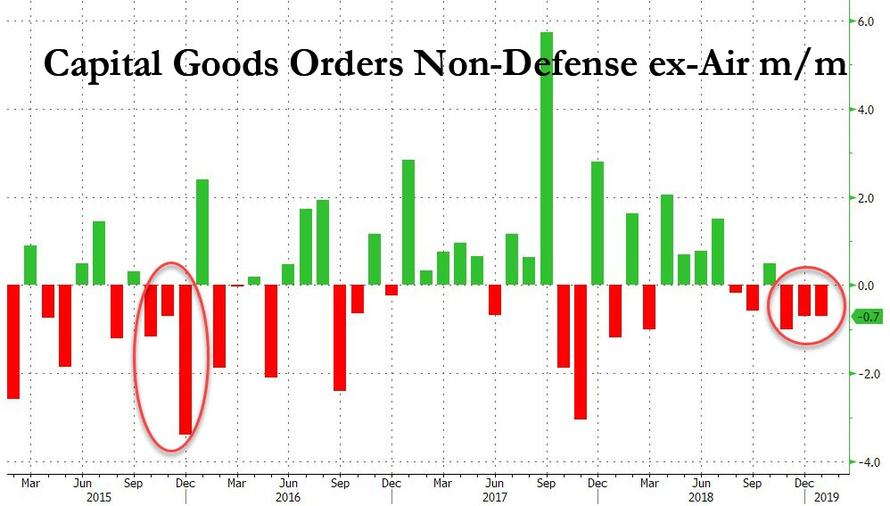

Looking at the day ahead, we get the delayed December durable and capital goods orders data which should help to further sharpen Q4 GDP expectations. The consensus expects a +0.3% mom pickup in core durable goods orders and +0.2% mom core capex orders reading. Also due out is the October Philly Fed survey which will be worth watching for a mid-quarter update on the factor sector. The consensus expects a 3pt decline to +14.0. Away from that we’ll also get the latest weekly initial jobless claims print – where the four-week moving average has ticked up in recent weeks – the flash February PMIs, January leading index and January existing home sales. Other than data, we’ll also hear from more central bank speakers with the ECB’s Praet due to speak this morning and afternoon, and the Fed’s Bostic this afternoon. The ECB is also due to publish the accounts of the January meeting while EU trade ministers are due to meet. Today also see’s China’s Vice Premier Liu He join trade talks in Washington with Lighthizer and Mnuchin.

US Event Calendar

- 8:30am: Philadelphia Fed Business Outlook, est. 14, prior 17

- 8:30am: Initial Jobless Claims, est. 228,235, prior 239,000; Continuing Claims, est. 1.74m, prior 1.77m

- 8:30am: Durable Goods Orders, est. 1.7%, prior 0.7%; Durables Ex Transportation, est. 0.25%, prior -0.4%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.2%, prior -0.6%; Cap Goods Ship Nondef Ex Air, est. 0.0%, prior -0.2%

- 9:45am: Markit US Manufacturing PMI, est. 54.8, prior 54.9; Markit US Services PMI, est. 54.3, prior 54.2

- 10am: Existing Home Sales, est. 5m, prior 4.99m; Existing Home Sales MoM, est. 0.2%, prior -6.4%

DB’s Jim Reid concludes the overnight wrap

Ahead of today’s important flash PMIs (preview later), I was in Frankfurt last night for a macro dinner and it’s fair to say that whilst nervous, most investors thought the pain trade was a further tightening of spreads and higher equity markets – in-line with my thought. In a show of hands no-one thought we’d get a hard Brexit and the vast majority thought we’d get some kind of supportive US-China trade deal in the coming weeks. So that’s the bias of views. There was less certainty beyond the next few months but some who previously were worried about the US cycle, like me, were a little less pessimistic about 2020 now due to the Fed 180 degree pivot in 2019. A lot of the conversation was taken up by the bubbling momentum of socialism in US politics. I think this could be a huge topic as we hit the primaries ahead of the 2020 election. So it’s something I’m going to write about in more depth soon.

Politics remains highly changeable at a global level and in an otherwise quiet week it’s the reshuffling of UK political lines which is proving to be the most interesting story at the moment. Yesterday’s news that three Conservative MPs had quit to join a new Independent Parliamentary Group might not have an immediate direct Brexit read-through but it does mean that May is becoming perilously close to losing her majority, especially with one of the defectors – Heidi Allen – saying that she expects more Tories to quit. This means the medium term risk of a new election is surely rising even if the gang of three made it clear that they would likely support the government outside of Brexit votes. Yesterday’s YouGov poll – while a little less meaningful at this stage and covering Feb 18-19 just before the Tory defections – put support for the Tories at 38% versus 26% for Labour. This is a remarkable collapse for the opposition party and only a small decline for the Tories. Whatever you think of Tory party tactics and handling of Brexit there is only one party that is pursuing Brexit as per the voter mandate and I think they are keeping support for them high because of this. Back to the poll and the new Independent Group scored 14%, followed by the Lib Dems at 7%. Could this be the start of a significant change in UK politics like the en Marche movement in France? The problem for them is that the U.K. has a constituency system and is “first past the post”. Indeed in the UK, winning a vote share in the low-20s has not historically been high enough to make much progress in Parliament. In 2010 the Lib Dems got 23% of the vote but fewer than 10% of the seats in Parliament. In 1983 the SDP-Liberal Alliance got 25% of the vote but didn’t even manage 5% of the seats. Indeed at a general election people usually vote tactically and unless a party can win, voters will often vote for one of the two main parties to ensure the one they don’t want to win has a better chance of losing. So a long road ahead for a centrist movement but unusual things are happening all over the world.

The pound took a roundtrip yesterday, initially depreciating -0.38% versus the dollar on the above resignations, before reversing to trade +0.36% stronger on possibly positive Brexit stories. Spain’s Foreign Minister Josep Borrell told reporters that “I think the accord is being hammered out now,” helping the pound to jump higher. His office subsequently walked back those comments, and the currency ultimately ended the session close to flat. There were also reports that the EU would want the UK Parliament to formally vote on any new agreement before the EU leaders considered it themselves. This would be new sequencing, which could indicate a subtle shift in positions that might allow a breakthrough, though it’s also an indictment of May’s inability to make promises given her fractured caucus. Elsewhere, the UK PM May and the EU President Juncker released a joint statement post their meeting saying that they discussed which guarantees could be given to underline once more the “temporary nature” of the Irish border backstop while adding that they have tasked chief Brexit negotiators of both sides – EU’s Michel Barnier and UK’s Stephen Barclay – with considering role for “alternative arrangements” in replacing backstop in future. They also discussed on any amendments that could be made to the political declaration consistent with their respective positions. In the meantime, yesterday Fitch placed the UK’s AA long term rating on a negative watch citing the “heightened uncertainty over the outcome of the Brexit process.”

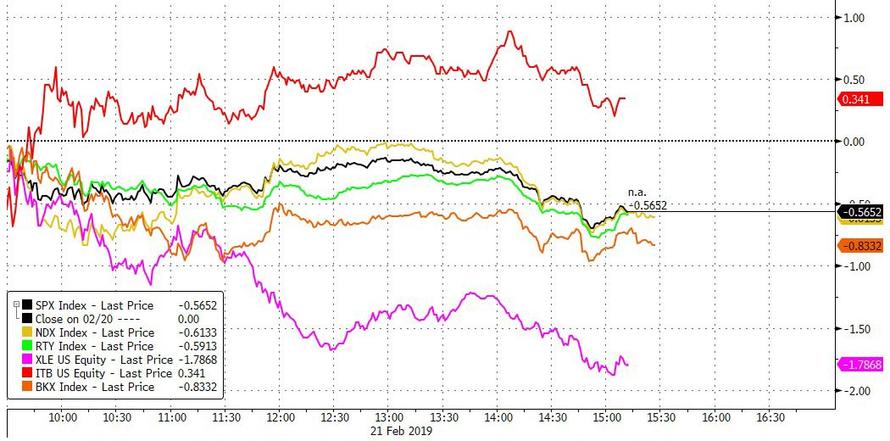

Markets are a lot less complicated than Brexit at the moment with incremental positive returns the name of the game for now. That was the case last night even after the FOMC minutes with the S&P 500, DOW and NASDAQ turning in gains of +0.19%, +0.24% and +0.03% respectively. Treasuries closed around +1bp higher across maturities and the 2s10s yield curve remains steady at 14bps. HY spreads were -4bps in the US and the dollar also closed flat on the session.

Just on the minutes, the main highlights were confirmation that the FOMC is likely to end its balance sheet runoff later this year and a reaffirmation that rate hikes remain on hold for now. Due to a snow storm in Washington, DC, reporters did not receive embargoed access to the minutes before the official release, so the details trickled out as everyone read through the details. The market reaction was somewhat more muddled than usual, with the S&P 500 dropping -0.38% in the 20 minutes after the release but subsequently fully retracing. Perhaps investors initially focused on hawkish excerpts like “participants continued to view a sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes over the next few years.” However, the minutes also said that “maintaining the current target range for the federal funds rate for a time posed few risks at this point” which suggests no imminent change in policy and “almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve’s asset holdings later this year.” That’s a very clear confirmation that we should expect a formal announcement and an end to the balance sheet runoff by year-end.

Meanwhile, overnight Bloomberg reported that the US and Chinese negotiators are working on multiple memorandums (6 in total as per Reuters) of understanding that would form the basis of a final trade deal and the MoUs are likely to cover areas including agriculture, non-tariff barriers, services, technology transfer and intellectual property. The report also added that the enforcement mechanism for the MoUs remains unclear as of now, but would likely be a threat of re-imposition of tariffs if conditions aren’t met and also indicated that China’s Vice Premier Liu He is likely to meet with President Trump on Friday. As a reminder China Vice Premier Liu He is set to meet Lighthizer and Mnuchin today. Elsewhere, President Trump reiterated his threat to impose tariffs on cars imported from the EU if the US can’t reach a trade deal with the EU. He said that “If we don’t make the deal we’ll do the tariffs. We’re trying to make a deal. They’re very tough to make a deal with, the EU.”

Asian markets pared losses on the above positive US-China trade headlines and are heading higher. The Nikkei (+0.49%), Hang Seng (+0.53%) and Shanghai Comp (+0.36%) are all up while the Kospi (-0.06%) is trading flattish. China’s onshore yuan also rose (+0.39%) on positive trade headlines to 6.6950, highest since July 2018. Elsewhere, futures on the S&P 500 are up +0.31% while 10y treasury yields are up +1.9bps this morning. In terms of overnight data releases, and a bit worrying ahead of today’s other flash numbers, Japan’s preliminary February manufacturing PMI was in contractionary territory at 48.5 (vs. 50.3 last month) for the first time since September 2016. The subindex for production fell to 47.0 (vs. 49.4 last month), indicating that actual output declined further. Joe Hayes, an economist at IHS Markit, said that “unless service sector activity can offset manufacturing weakness, the chance of Japan entering a recession in 2019 looks set to rise.”

In Europe, the STOXX 600 rallied +0.67% yesterday, closing above its 200-day moving average for the first time since September. Bunds were little changed and BTPs weakened a further +7.1bps after the ECB’s Praet confirmed that while the ECB will discuss a new TLTRO, it’s unclear that a decision will actually be made. Along with Lane and Rehn, that is 3 senior figures who have suggested that a new TLTRO might not come as soon as the next ECB meeting on March 7.

In other news from yesterday , the US Trade Representative Lighthizer is to testify about China trade matters before the House Ways and Means Committee on February 27th according to CNBC. As for the S232 report, it was interesting to note yesterday’s Politico report which suggested that there are rising calls for the White House to release the report with a source suggesting that it does find a threat and recommends tariffs of up to 25%. Despite those rumours, automaker stocks rallied +2.30% and +1.08% in Europe and the US, respectively.

Moving on. While it’s not been the most exciting of weeks in markets this week we do have the flash February PMIs to look forward to today in Europe. A reminder that we’ve seen the composite Euro Area PMI decline in 10 of the last 12 months to a five-and-a-half year low of 51.0 in January. The consensus is for a very modest pick-up to 51.1 this month. The services reading is expected to rise to 51.3 (from 51.2) however the manufacturing reading is expected to slide a little further, to 50.3 from 50.5 in January. That print has fallen in 12 of the last 13 months and last month hit the lowest since November 2014. As for the country level data, there will be plenty of focus on the data out of France given the recent slide with only a modest pick-up in the composite to 48.9 expected (from 48.2 in January). Germany’s composite reading is expected to nudge down slightly to 52.0 from 52.1.

Back to yesterday, where in EM land it was a bit of a roundabout session for South African assets following the release of the latest budget deficit forecasts. The Rand weakened as much as -2.28% at one stage and bonds blew wider with the National Treasury forecasting a budget deficit of 4.5% for the year starting April 1 which would be the widest since 2010. Growth rates were also cut, however the announcement of an operational overhaul of Eskom and discussions about privatising part of the transmission business helped assets to pretty much fully recover by the end of play. Wider EM FX was flat yesterday while the MSCI EM index finished +0.57%.

Looking at the day ahead, this morning we’ll get the final January CPI revisions in Germany and France, as well as February confidence indicators in the latter. The PMIs are out just after that before we can get a look at January public finances data in the UK. Over in the US this afternoon we’re due to get the delayed December durable and capital goods orders data which should help to further sharpen Q4 GDP expectations. The consensus expects a +0.3% mom pickup in core durable goods orders and +0.2% mom core capex orders reading. Also due out is the October Philly Fed survey which will be worth watching for a mid-quarter update on the factor sector. The consensus expects a 3pt decline to +14.0. Away from that we’ll also get the latest weekly initial jobless claims print – where the four-week moving average has ticked up in recent weeks – the flash February PMIs, January leading index and January existing home sales. Other than data, we’ll also hear from more central bank speakers with the ECB’s Praet due to speak this morning and afternoon, and the Fed’s Bostic this afternoon. The ECB is also due to publish the accounts of the January meeting while EU trade ministers are due to meet. Today also see’s China’s Vice Premier Liu He join trade talks in Washington with Lighthizer and Mnuchin.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 9.42 POINTS OR 0.34% //Hang Sang CLOSED UP 115.87 POINTS OR 0.41% /The Nikkei closed UP 32.74 POINTS OR 0.150%/ Australia’s all ordinaires CLOSED UP 0.63%

/Chinese yuan (ONSHORE) closed UP at 6.7182 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7182 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7151: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/USA//TAIWAN

Taiwan’s leader is very worried about a Chinese invasion. The threat is ‘growing every day”

(courtesy zerohedge)

Taiwan’s Leader Says Threat Of Chinese Invasion “Growing Every Day”

President Trump’s at times warm, at times contentious relationship with his Chinese counterpart has been an exercise in cognitive dissonance that’s reflective of a broader truth about the relationship between the world’s two largest economies. The veneer of economic cooperation belies deeper military tensions as China’s expansionist military aims threaten US security in the Pacific.

Just last week, the top US Navy commander in the Pacific warned that China represents the “greatest long-term strategic threat to a free and open Indo-Pacific and to the United States.” And the country’s insistence on carrying on with its military buildup in the South China Sea, one of the most vital waterways for global trade, has angered the US and nearly all of its neighbors. But while the US public labors under the illusion that a military conflict with the Chinese is only a vague possibility somewhere off in the indeterminate future, for the island of Taiwan, China’s increasing muscular military presence in the region is a daily threat that requires 24/7 vigilance, according to CNN.

As she struggles with waning poll numbers ahead of an election later this year, Taiwan’s pro-independence leader Tsai Ing-wen claimed in yet another interview with a western media organization that the world is underestimating the growing threat posed by Beijing.

After President Xi claimed during a landmark speech early this year that Taiwan would eventually be re-unified with the mainland in an arrangement similar to that of Hong Kong or Macau – something the Taiwanese people popularly oppose – and threatened any meddling foreign powers (ie the US) who dare to interfere), Tsai said that China crushing Taiwan would be a “setback for global democracy.”

In response to Xi’s threat, Tsai said earlier this year that Taiwan “would never accept” reunification with Beijing.

“If it’s Taiwan today, people should ask who’s next?” she said. “Any country in the region – if it no longer wants to submit to the will of China, they would face similar military threats.”

[…]

“If a vibrant democracy that champions universal values and follows international rules were destroyed by China, it would be a huge setback for global democracy,” she said.

[…]

“With China becoming increasingly strong and ambitious, we are faced with growing threats,” Tsai said.