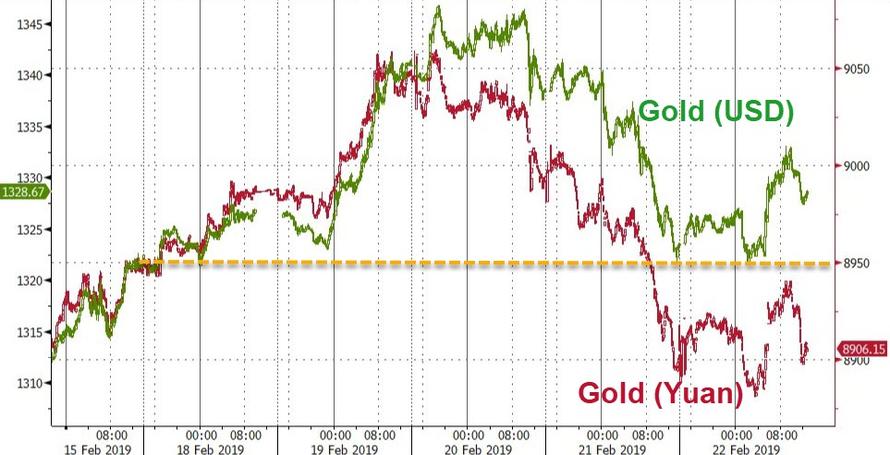

GOLD: $1330.60 UP $5.15 (COMEX TO COMEX CLOSING)

Silver: $15.96 UP 7 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1328.30

silver: $15.92

The comex options expire on Monday and the London/LBMA expires on Thursday, the 28th of February..

Expect extreme volatility until first day notice.

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 830 NOTICE(S) FOR 83000 OZ (2.5866 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 11,296 NOTICES FOR 1,129,600 OZ (35.135 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 570 for 2,850,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3964:UP $25

Bitcoin: FINAL EVENING TRADE: $3963 UP 27

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 708/830

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,323.500000000 USD

INTENT DATE: 02/21/2019 DELIVERY DATE: 02/25/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

555 H BNP PARIBAS SEC 11

657 C MORGAN STANLEY 21

661 C JP MORGAN 681

661 H JP MORGAN 27

690 C ABN AMRO 2

737 C ADVANTAGE 18 109

800 C MAREX SPEC 3 11

880 H CITIGROUP 740

905 C ADM 35 2

____________________________________________________________________________________________

TOTAL: 830 830

MONTH TO DATE: 11,296

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A HUMONGOUS SIZED 4542 CONTRACTS FROM 225,889 DOWN TO 221,347 WITH YESTERDAY’S 37 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

2260 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2644 CONTRACTS. WITH THE TRANSFER OF 2260 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2260 EFP CONTRACTS TRANSLATES INTO 11.30 MILLION OZ ACCOMPANYING:

1.THE 37 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.855 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 24,692 CONTRACTS (FOR 15 TRADING DAYS TOTAL 24,692 CONTRACTS) OR 123.46 MILLION OZ: (AVERAGE PER DAY: 1646 CONTRACTS OR 8.230 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 123.46 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.63% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 331.985 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4542 WITH THE 37 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2260 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 2282 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2260 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 4542 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 37 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.83 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.106 BILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.855 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A STRONG SIZED 6221 CONTRACTS DOWN TO 504,332 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $19.50//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6559 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 6559 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 505,070. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A CONSIDERABLE SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 338 CONTRACTS: 6221 OI CONTRACTS DECREASED AT THE COMEX AND 6559 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 338 CONTRACTS OR 107,600 OZ = 3.3468 TONNES. AND ALL OF THIS DEMAND OCCURRED DESPITE A NASTY FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $19.50.

YESTERDAY, WE HAD 6689 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 89,348 CONTRACTS OR 8,934,800 OZ OR 277.90 TONNES (15 TRADING DAYS AND THUS AVERAGING: 5,956 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAYS IN TONNES: 277.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 277.90/2550 x 100% TONNES = 10.89% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 798,03 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 6221 WITH THE LOSS IN PRICING ($19.50) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6559 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6559 EFP CONTRACTS ISSUED, WE SURPRISINGLY HAD A GOOD 1076 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6559 CONTRACTS MOVE TO LONDON AND 6221 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 1.05 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $19.50 IN YESTERDAY’S TRADING AT THE COMEX

we had: 830 notice(s) filed upon for 83000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.15 TODAY

A HUGE WITHDRAWAL OF 4.99 TONNES OF PAPER GOLD AND THIS WAS USED IN THE WHACKING OF GOLD YESTERDAY/TODAY.

/GLD INVENTORY 789.51 TONNES

Inventory rests tonight: 789.51 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 7 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV..///

THESE GUYS ARE NOTHING BUT FRAUDSTERS.

/INVENTORY RESTS AT 309.984 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUMONGOUS SIZED 4542 CONTRACTS from 225,889 DOWN TO 221,347 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2260 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2260 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 4542 CONTRACTS TO THE 2260 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 2282 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 11.41 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.855 MILLION OZ STANDING IN FEBRUARY.

RESULT: A POWERFUL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 37 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A VERY STRONG SIZED 2260 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 52.43 POINTS OR 1.91% //Hang Sang CLOSED UP 186.38 POINTS OR 0.65% /The Nikkei closed DOWN 38.72 POINTS OR 0.18%/ Australia’s all ordinaires CLOSED UP 0.44%

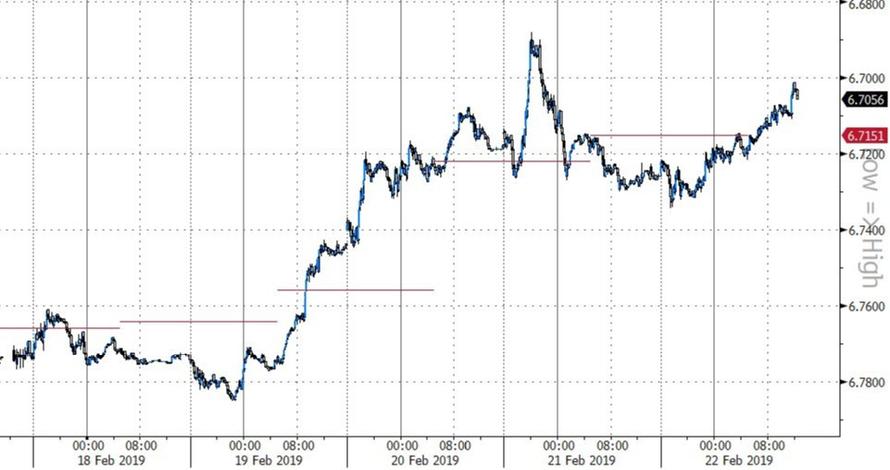

/Chinese yuan (ONSHORE) closed UP at 6.7197 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7197 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7197: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/USA//TAIWAN

4/EUROPEAN AFFAIRS

I)EU/GREAT BRITAIN

The EU expects Theresa May to request an extension of 3 months. Not sure if the crooks will agree to it

( zerohedge)

ii)FRANCE

French bank, Soc Generale is set to fire thousands of bankers. Business must be really good

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

SYRIA/ISRAEL/RUSSIA

A good explanation as to why the S 300 defense shield has not been used against Israel as their bomb Iranian warehouses

( SouthFront)

6. GLOBAL ISSUES

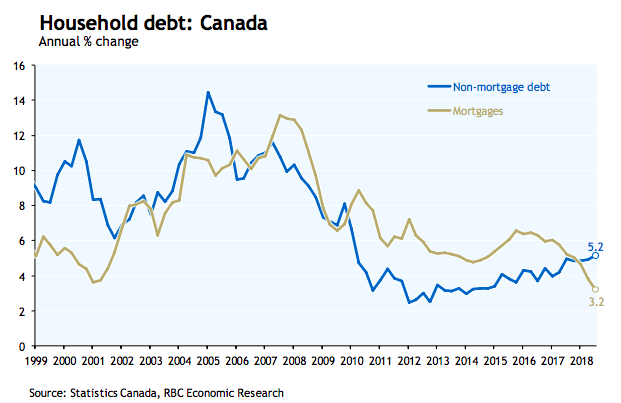

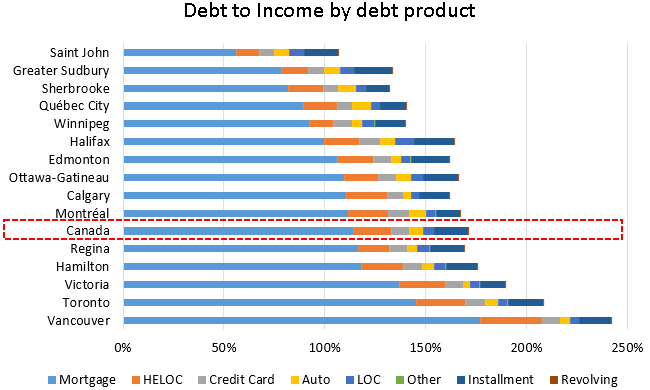

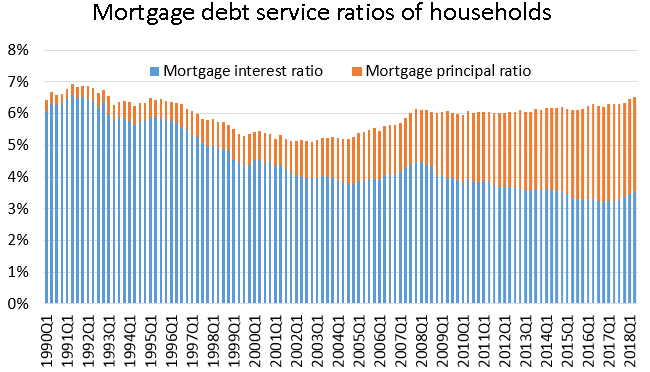

This report shows how Canadians are borrowing against the equity in the homes. An economic downturn in Canada will be deadly especially if home prices go below the net debt

( zerohedge)

ii)Most Americans and Europeans are terrified about retirement because they have not saved anything. This is what inflation will do.

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

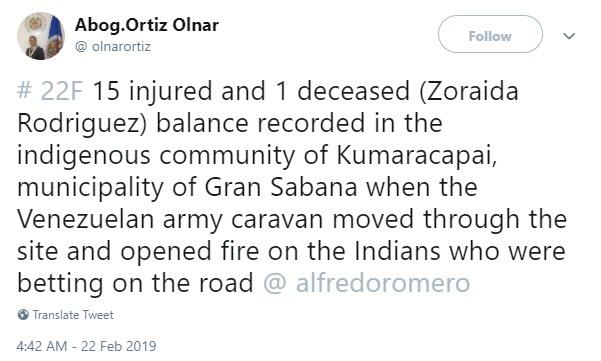

i)VENEZUELA/

Not good: 1 dead and 15 injured as Venezuelan soldiers open fire on civilians near the Brazil border according to the Washington Post. There is urgent need to get rid of former bus driver Maduro.

( zerohedge)

9. PHYSICAL MARKETS

iii)Ted Butler..on the huge short positions by our criminal banking operations

( Ted Butler/GATA)

iv)Australia reports on where it’s gold is stored:

(Wright Sydney Herald/GATA)

v)A good one@!! What happened to Australia’s 80 tonnes of stored gold?

( Manly/Bullionstar)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

iv)SWAMP STORIES

a)This is fascinating: The FBI’s top lawyer James Baker thought that Hillary Clinton should have been criminally prosecuted

( zerohedge)

b)This is going to be fun: McConnell is going to fast track AOC’s “Green New Deal”. This should show the world which democrats are supporting this crazy proposal

( zerohedge)

d) the true cost of Eliz Warren’s childcare program. It is not 70 billion dollars. It is more than 174 billion dollars

e)The following is very important as we will now enter Phase II of the Mueller /Russian election interference probe

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 17,738 CONTRACTS DOWN TO 53,083 CONTRACTS. AFTER MARCH, APRIL ADVANCES TO 515 CONTRACTS FOR A GAIN OF 162 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 12,785 CONTRACTS UP TO 124,622 CONTRACTS.

FIRST DAY NOTICE IS THURSDAY FEB 28.2019

comex gold volumes are getting extremely low as players just do not want to play in this casino.

The Utterly Unbelievable Scale of U.S. Debt Right Now

– Last week, the United States national debt ticked above US$22 trillion for the first time, an amount equivalent to $67,000 per U.S. citizen

– The U.S. federal government owes more money than any other institution in the history of human civilization and it’s just getting worse

– Below, a few factoids about just how eye-wateringly, bone-chillingly large the U.S. debt has become

– The U.S. debt is now higher than the combined market value of the Fortune 500 and just with the money it spends on interest, the U.S. could run Canada or Mexico

– Debt from one Trump term could pay for another WWII and all the gold ever mined would only pay off the debt accumulated under Obama

– All the gold in the world mined since the dawn of time adds to about 190,040 tonnes or 6.7 billion ounces. At the current per-ounce price of about $1,300, the world’s goal hoard worth over $8.5 trillion would be not enough to pay off the U.S. debt accumulated between 2009 and 2016

by Tristan Hopper in National Post

Gold bars worth a small fortune that would only cover a few hours’ worth of U.S. debt accumulation

U.S. debt is now higher than the combined market value of the Fortune 500

The Fortune 500 list includes all the recognizable titans of American business from Apple to Amazon to Exxon-Mobil to the list’s ranking 500th spot, the uniform and laundry company Cintas. Taken together, they basically constitute every major consumer, media, industrial and entertainment product in the United States. If you are the average westerner, the Fortune 500 is responsible for most of your wardrobe, your diet, your home and your leisure pursuits.

The sheer size of Amazon alone is difficult to picture: Millions of products, thousands of employees, hundreds of buildings. And yet, add up the market values of all 500 companies and it’s equivalent to just $21.7 trillion.

Thus, even if the United States nationalized the most profitable segment of its private sector and immediately auctioned them off for cash, it would still have $300 billion owing on its debt. (This would also destroy the world economy. Don’t nationalize things to pay off debts, everybody).

Every second, the U.S. national debt grows by about $46,000. In the time it takes you to look at this photo, the debt will have swelled much more than $46,000

Holding a $22 trillion pile of debt is not cheap. Although the United States benefits from ludicrously cheap interest rates on its treasury bills, in 2019 it will spend $383 billion just to service its debt. By 2023, interest payments are expected to be larger even than the U.S. defence budget. Even now, $383 billion dwarfs the entire federal budget of Canada. Even at a time of its own unprecedented government spending, Ottawa will burn through the equivalent of only US$254.35 billion in 2019. This means that, merely with the money it uses to service the debt, the United States could run the entire Canadian government and still have enough left over to run most provinces. And if the Americans don’t feel like running Canada with their debt servicing money, they could also run Mexico.

Their southern neighbour has a federal budget of only $291.5 billion for 2019.

All the gold ever mined would only pay off the debt accumulated under Obama

U.S. debt has been steadily climbing ever since the Sept. 11 attacks, but under Obama it was sent into overdrive. Not all of this was Obama’s fault; the Great Recession, ongoing Asian wars and a boom in entitlement spending on retiring Baby Boomers all helped swell the tab. But still, in eight years of the Obama presidency, the U.S. national debt jumped from $11.1 trillion to $19.85 trillion. Coincidentally, this $8.75 trillion debt surge is the same as the combined value of all the gold ever mined. Every nugget pulled out of the Klondike, every ounce plundered from the Aztecs, every gold bar leach-mined out of Australia: It all adds to about 190,040 tonnes or 6.7 billion ounces. At the current per-ounce price of about $1,300, the world’s goal hoard would be just enough to pay off the U.S. debt accumulated between 2009 and 2016.

Debt from one Trump term could pay for another WWII

President Donald Trump, meanwhile, has only accelerated the Obama-era debt accumulation. In the 25 months since Trump was inaugurated, his administration has overseen a $2 trillion increase to the debt. Given current conditions, that figure is likely to surpass $4 trillion by the end of Trump’s first term. According to the Congressional Research Service, $4 trillion also happens to be the inflation-adjusted cost of U.S. involvement in the Second World War. And let’s take a moment to remember how expensive that war was for the United States. American forces led efforts to defeat two major military powers simultaneously while spearheading the greatest military industrial buildup in history. Every single automotive factory in the United States was retooled to produce equipment for the government. Total wartime aircraft production was almost 300,000, with the Manhattan Project alone costing the modern-day equivalent of $22 billion. At the time, the U.S. contribution to World War II was the most shockingly exorbitant expenditure of resources ever seen, with government spending in some years of the war being equivalent to more than 50 per cent of GDP. But now, an extra $4 trillion in debt is simply budgetary routine.

One year of debt could pay for everything NASA has ever done

Since 1958, NASA has landed six manned missions on the moon, sent 26 probes to Mars, launched 135 shuttle missions and blasted two spacecraft into interstellar space. And that’s just its space stuff: NASA has also spent years dominating aircraft and earth science research, including some of the most critical data confirming the existence of anthropogenic climate change. Add it all up, and the combined cost for 61 years of NASA is an inflation-adjusted $1.16 trillion. For context, over just the last 12 months (from Jan. 31, 2018 to Jan. 31, 2019), the United States piled up an extra $1.5 trillion in debt.

Jeff Bezos’ fortune would cover only 34 days of debt accumulation

There’s a lot of talk lately about how rich people should pay more taxes. However, given the sheer scale of U.S. spending right now it would take an awful lot of these extra taxes to come close to running a balanced budget. For example, consider Amazon founder Jeff Bezos, the richest man in the world. His net worth is roughly $136 billion. Right now, the U.S. adds another $4 billion to its debt every day. Thus, if Bezos gave his entire fortune to the U.S. government, it would only cover 34 days of debt accumulation. And this is just new debt. If Bezos’ fortune was used to cover all U.S. federal spending, it would run out in only 11 days. Bezos is one among 26 billionaires who collectively control $1.4 trillion – a wealth equivalent to that owned by nearly four billion of the world’s poorest. Still, even that $1.4 trillion would only cover a year’s worth of U.S. debt accumulation and about four months’ worth of federal spending overall.

Free Registration (including Research Reports) for 2019 Gold Summit here

In one year, the per-household share of the debt could buy a new car

According to its most recent census figures, the United States has 118,825,921 households. This means that the $1.5 trillion in debt accumulated over just the past year is equal to about $12,605 per household. This would be just enough for every single household in the United States to buy a brand-new Nissan Versa. When accounting for the total $22 trillion debt, that per-household share jumps to $185,000, enough to buy a new Ferrari or Bentley. The per capita share of the debt is particularly dramatic when compared to the U.S.’ northern neighbour. As recently as the 1990s, Canada was so debt-ridden that it was considered one of the worst economic basketcases in the G20. Today, per-capita Canadian federal debt is equal to US$13,588.51. In the U.S., the same figure is nearly five times higher at $67,000 per American.

The U.S. just built history’s most expensive warship. It cost five days’ worth of deficit.

The USS Gerald R. Ford, an aircraft carrier commissioned in 2017, is the largest and most expensive warship ever built at US$12.9 billion. For context, HMS Dreadnought, the super-powerful 1906 battleship that revolutionized naval warfare, only cost the modern equivalent of about $273 million. For 2019, the U.S. budget deficit is expected to be $897 billion. This means that only five days’ worth of deficit would be enough to fully cover the cost of the USS Gerald Ford. And the deficit merely represents new instances of the government spending money it doesn’t have. Total debt accumulation is even higher, since the existing debt continues to balloon on its own if it’s not being paid off (and the Americans haven’t even tried to pay down their debt since 2000).

The vast majority of this is entitlement spending

It would be tempting to assume that the United States is piling up all this debt because of big, tangible budget items: Battleships, fighter jets, highways, disaster relief, etc. But the majority of U.S. spending is eaten up by cheques: Millions of relatively small-denomination cheques handed out as entitlement spending. The U.S. government will spend $4.4 trillion in 2019, of which only $3.5 trillion will be covered by tax revenues. Of that $4.4 trillion, $2.7 trillion is spent on what is known as “mandatory spending”: Social security, Medicare, Medicaid and the like. As a result, much of the expansion in U.S. spending is due to factors beyond the government’s control: Higher healthcare costs and more retired Baby Boomers collecting pension cheques.

This is all happening during good times

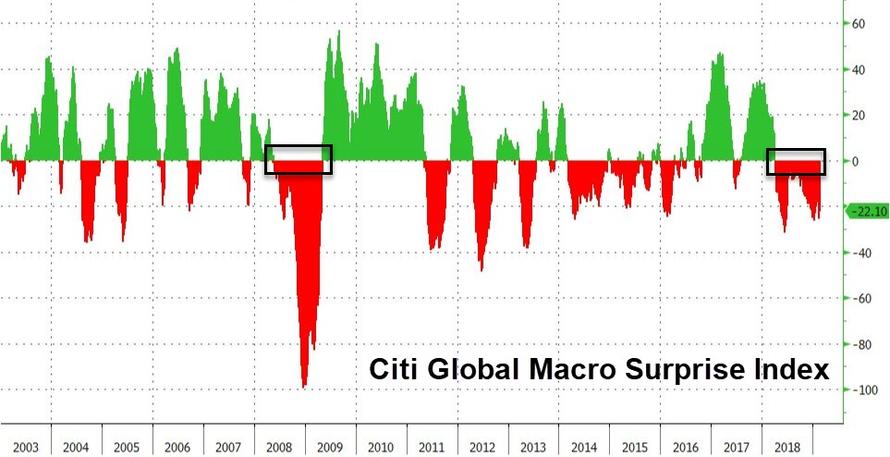

Throughout U.S. history, periods of massive debt accumulation have usually coincided with bad times: The Great Depression, the Civil War, etc. By any economic measure, however, the United States is currently doing fantastic. Major foreign wars have been stepped down. The jobless rate is at a 49-year low. Economic growth has been topping four per cent. The last time the U.S. economy was this good, the federal government was running budget surpluses to pay down the debt, rather than piling up debt faster than ever. The implication is that when the boom inevitably ends, U.S. deficits are set to explode even faster. “The economy is going well and we are looking at deficits that are four per cent of GDP going forward,” Congressional Budget Office director Keith Hall said in late January.

“That is an unusual thing.”

News and Commentary

Gold falls off 10-month peak after Fed stance; palladium retreats (Reuters.com)

Gold sinks, set to snap 3-day string of gains (MarketWatch.com)

U.S. stocks sag on poor economic outlook; oil, gold slip (Reuters.com)

Stocks fall as weak economic data overshadow trade-talk optimism (MarketWatch.com)

Australia’s Gold … Safely in the Hands of the Bank of England (SMH.com)

CFTC and Justice Dept. overlook manipulative short position in silver (Gata.org)

Gold: Will “America First” End America’s Dominance? (Gold-Eagle.com)

For The First Time Since 2000, Most Assets Are Overbought (ZeroHedge.com)

Most Americans & Europeans Are Terrified About Retirement (ZeroHedge.com)

Listen on iTunes, Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

21 Feb: USD 1,335.05, GBP 1021.85 & EUR 1,177.78 per ounce

20 Feb: USD 1,345.75, GBP 1032.86 & EUR 1,186.82 per ounce

19 Feb: USD 1,329.55, GBP 1028.81 & EUR 1,175.72 per ounce

18 Feb: USD 1,323.95, GBP 1025.13 & EUR 1,169.58 per ounce

15 Feb: USD 1,319.00, GBP 1027.64 & EUR 1,168.17 per ounce

14 Feb: USD 1,305.65, GBP 1017.49 & EUR 1,158.50 per ounce

Silver Prices (LBMA)

21 Feb: USD 15.91, GBP 12.19 & EUR 14.02 per ounce

20 Feb: USD 16.03, GBP 12.31 & EUR 14.15 per ounce

19 Feb: USD 15.78, GBP 12.22 & EUR 13.99 per ounce

18 Feb: USD 15.76, GBP 12.19 & EUR 13.91 per ounce

15 Feb: USD 15.67, GBP 12.23 & EUR 13.90 per ounce

14 Feb: USD 15.58, GBP 12.17 & EUR 13.83 per ounce

Recent Market Updates

– The Best Time In History To Buy GOLD

– Jim Willie Interviews Mark O’Byrne – Prepare Now For Global Financial Crisis II

– 7 Major Flaws Of The Global Financial System – Excellent Infographic

– The Case for Gold In 2019 – The Economist

– Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

– Valentine’s Day Record Spending Due to Gold Love Trade?

– Gold Prices In Pounds and Euros Gain More as Economic Growth Falters in the UK and EU

– Irish Investors Storing Their Gold Bullion In Ireland

– Large Gold Bullion Shipment Moves From London to Dublin Gold Vaults As Brexit Concerns Deepen

Citigroup asks Treasury what to do with $1.1 billion Maduro gold deal

Submitted by cpowell on Thu, 2019-02-21 19:21. Section: Daily Dispatches

By Patricia Laya

Bloomberg News

Thursday, February 21, 2019

Citigroup bankers have been holding talks with U.S. Treasury officials to figure out how to handle a gold deal they had arranged with Nicolas Maduro’s regime in Venezuela, people familiar with the matter said.

The deal — a $1.1 billion swaps contract backed by gold held by the Venezuelan central bank — was struck before the U.S. stepped up sanctions on Maduro’s government. But it’s due to expire early next month and Citigroup bankers are seeking to make sure they avoid making a move now that would violate the sanctions, according to Senator Marco Rubio and other U.S. and Venezuelan officials familiar with the matter.

…

The one thing, no banker, global or financial institution is going to do is run the risk of secondary sanctions,” Rubio, who’s been helping drive the U.S. push to oust Maduro, said in a telephone interview late Wednesday. “The sale of gold is another revenue source that the Maduro regime is using and I know for a fact that Citibank has had multiple meetings with Treasury seeking guidance, trying to figure out how to avoid exposure.” …

The four-year swaps contract — which handed Venezuela a loan in exchange for putting the gold up as collateral — matures on March 11. Because the cash-strapped Maduro regime is unlikely to come up with the money it had received in the deal, Citigroup could wind up getting the gold. Allies of Juan Guaido, the legislator who’s trying to take power from Maduro with the help of the U.S. and other countries, are lobbying the bank to not take possession of it as part of their effort to safeguard the nation’s dwindling assets.

“Citi hasn’t responded publicly, but they understand the situation and are willing to collaborate and we’re asking them not to execute the guarantee,” said Angel Alvarado, who’s a member of the National Assembly’s finance commission. “We’re waiting to see what mechanisms will be used. The strategy is to protect assets.”

Under the contract’s current terms, if Venezuela does not pay next month, Citi would keep the gold and only pay the central bank the difference in value since the metal’s price has increased since it was signed in 2015. In the meantime, the gold would remain inside the Bank of England’s vaults, according to one person familiar with the issue.

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-02-21/citigroup-huddles-wit…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Only a return to the gold standard can save the world’s economic system

(courtesy Alasdair Macleod/GATA)

Alasdair Macleod: The return to a gold exchange standard

Submitted by cpowell on Thu, 2019-02-21 21:17. Section: Daily Dispatches

4:17p ET Thursday, February 21, 2019

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod argues today that only reimposition of a gold standard can save Western countries from the hyperinflationary collapse made inevitable by their welfare-state model of government. The example of Germany during and just after World War I, Macleod writes, shows how quickly a fiat currency can crash once people apprehend its devaluation, though he acknowledges that through market rigging and data doctoring Western welfare states have prolonged the process of recognition.

Macleod’s commentary is headlined “The Return to a Gold Exchange Standard” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/the-return-to-a-go…

GATA does not advocate returning to a gold standard, as it’s all the organization can do simply to discern and expose what sort of systems are being operated largely surreptitiously by central banks. But we’re generally of the opinion that if the monetary metals markets are ever liberated from central bank intervention, the world will remonetize them all by itself in less than a week — which is precisely why central banks intervene so relentlessly against the monetary metals.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ted Butler..on the huge short positions by our criminal banking operations

(courtesy Ted Butler/GATA)

Ted Butler: CFTC and Justice Dept. overlook manipulative short position in silver

Submitted by cpowell on Fri, 2019-02-22 01:27. Section: Daily Dispatches

8:28p ET Thursday, February 21, 2019

Dear Friend of GATA and Gold:

At the urging of Jim Cook of Investment Rarities and with the assistance of 24hGold, silver market analyst Ted Butler’s most recent proprietary letter has been posted in the clear.

This edition examines the failure of the U.S. Commodity Futures Trading Commission and the Justice Department to investigate the concentrated and manipulative short position in the silver futures market.

…

Butler writes: “An underground mine in Peru that digs out of the earth 4 million ounces in a year was just shut down due to low silver prices. Yet at the same time and price, eight crooked banks have increased their net speculative short position to more than 100 times that mine’s annual production.

“If the Justice Department doesn’t see something drastically wrong with that, then all hope for the rule of law is lost. Remember, concentration is the one absolute requirement in any manipulation. In silver, the concentration is off the charts.”

Butler’s letter is headlined “Mr. Butler’s Silver Newsletter — Icing on the Cake” and it’s posted at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-mr-butler-s-silver-newsl…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

MR. BUTLER’S SILVER NEWSLETTER

By James Cook

Silver analyst Theodore Butler writes a twice weekly newsletter on precious metals. Only a few people get to read this important newsletter. I’ve been talking to Ted about releasing one full issue for people to read. It’s important for investors to see the scope of his analysis. Mr. Butler has been a paid consultant to my company Investment Rarities for almost 20 years. I can vouch for his absolute integrity and his cautious approach in analyzing silver and gold. He relies on evidence and facts in arriving on his conclusions. He analyzes every known fact about silver and his knowledge of the silver market is unsurpassed. It’s no exaggeration to call him a silver genius. He has agreed to release the following current newsletter which gives insight into the thoroughness of his approach.

ICING ON THE CAKE

Unbeknownst to me when I wrote last week’s article, “A New Silver Issue for the Justice Department”, was the near simultaneous news that a leading silver mining company, Hochschild, had announced the closing of one of its Peruvian silver mines due to low silver prices. The Arcata mine, first put into production 55 years ago and reported to contain over 100 million ounces in reserves, was said to produce around 4 million ounces annually. There was little doubt that the decision to put the mine on care and maintenance was the result of continued depressed silver prices, despite the ten percent increase in price since Nov 13.

https://www.reuters.com/article/hochschild-min-operations/update-1-hochschild-mining-shuts-down-arcata-mine-in-peru-idUSL3N2082KY

The news announcement resonates for a number of reasons. In attempting to convince the Department of Justice’s Antitrust Division to take up the matter of concentrated short selling on the COMEX silver futures market as being responsible for depressed silver prices, I made the point that it was absurd to conclude that the concentrated short selling was due to legitimate hedging by silver miners. Hochschild’s announcement underscores my point in that it proves silver prices are too low for legitimate producers to consider locking in by short sale on the COMEX. Instead, Hochschild took the painful but logical step of shutting down the mine until silver prices rise enough.

Since it’s clear that silver miners are not engaged in widespread bona fide hedging at current depressed silver prices to warrant their inclusion among the concentrated short sellers on the COMEX, then it’s imperative to ask then who is responsible. Thanks to unmistakably clear data from the CFTC in the form of disaggregated Commitments of Traders (COT) and Bank Participation reports, there can be little doubt that the concentrated short sellers are domestic and foreign banks – not miners.

The way it works is like this – the speculating banks (which are merely betting against the managed money speculators) pretend to be hedging and the CFTC accommodates this subterfuge by agreeing to classify the banks in the Producer/Merchant/User/Processor or Swap Dealers categories despite the obvious fact that the banks are speculating. Since there is always an ample supply of observers (not a one with hands on professional futures experience) who will glibly agree that anyone classified as a commercial is automatically engaged in legitimate hedging, regardless of clear evidence to the contrary, the con lives on.

What makes the silver manipulation con of speculative concentrated short selling so egregious is that the short sellers pretending to be legitimate commercial hedgers are hurting the very participants which should be hedging, the miners. That would likely occur if the price of silver was anywhere near where it should be in true free market conditions. Our regulated commodity futures markets were created and designed for legitimate hedgers to lay off risk through bona fide hedging. Instead, a handful of speculating banks and managed money traders have completely usurped the legitimate hedging function and have taken control of the pricing process. Not only is the price being set artificially by outsiders, the resultant price is most damaging to the market participants that futures trading was intended to benefit.

One of the reasons the matter of concentrated short selling in COMEX silver futures has gone by almost unnoticed all these years and is rarely commented on, even to this day, is because most commentators and observers don’t know how to calculate the concentration data. I believe that’s because it takes a bit of hand-calculating to derive at the concentration statistics. While the data are precise to the exact contract, the COT report doesn’t present the data in contract form, only as a percentage of total open interest; leaving it to the observer to multiply the total open interest by the percentage of concentration given. As I’ve written previously, the percentages given for the net short positions of the 4 and 8 traders are the only numbers that matter.

A reason the concentrated short position in COMEX silver futures may have escaped the notice of the Antitrust Division of the DOJ is because most price-fixing and monopolistic activities it deals with are of the variety that artificially boost prices to the detriment of the consuming public. But the reason that the statue of Lady Justice is blindfolded is because the law shouldn’t distinguish between artificial price-setting of either the higher or lower variety. The efficient functioning of free markets depends on the law of supply and demand not being distorted by artificial pricing of any kind. Any market artificially depressed in price may give users and consumers some advantage in the short term, but the eventual end to the illegal artificiality will lead to much higher prices in the long run.

In fact, it’s quite understandable that the Antitrust Division has not focused on the monopolistic pricing in COMEX silver futures. After all, there was created and exists a specific primary federal regulator, the CFTC, whose main mission is to prevent manipulation. In addition, there exists a designated self-regulating organization (SRO), the CME Group, also charged with the preventing of market manipulation. Normal protocol would suggest that matters pertaining to allegations of manipulation would be the province of the CFTC and the CME. If either regulator had fulfilled their prime responsibilities, there would be no need for Antitrust Division intervention. Sadly, that’s not the case.

In any event, it is particularly pernicious when prices are set artificially by participants not involved with or even interested in the actual production or consumption of silver. Speculating banks or managed money traders couldn’t care less about the plight of actual silver producers, consumers or investors – they are just out to make a quick buck off each other in some massive private betting game on the COMEX sanctioned by the CFTC and CME Group. The problem is the private betting game is what sets prices and that “outsiders”, not actual producers and consumers run the game.

The closing of a not insignificant silver mine that has produced for more than half a century and appears capable of producing for another 50 years due to low prices is a timely reminder and confirmation that silver prices are unreasonably depressed. That’s why it is so potentially significant that the Department of Justice has stepped into the matter with an ongoing investigation by its Criminal Division, the FBI and the US Attorneys Division of COMEX precious metals trading. The Antitrust Division has every reason to join in as well.

As if to underscore the matter, yesterday’s release of the still delayed Commitments of Traders (COT) report featured notable increases in the concentrated short positions of the 8 largest traders in both COMEX gold and silver. The increases demonstrate beyond a doubt that concentrated short selling is all that prevents sharply higher prices for both gold and, particularly silver. It’s not just that the reporting week ended Jan 29 featured managed money buying and commercial selling, which was fully expected given the sharp price rallies that took place, but it has become increasingly clear that without concentrated commercial short selling prices would have rallied much more.

As of the close of business Jan 29, the commercials increased their total net short position by 26,500 contracts to 118,600 contracts, as the price of gold traded and closed decisively above $1300 for the first time in ten months, trading as high as $1310 on the cutoff day. Considering that the reporting week’s close was up $110 from the price lows of Nov 13, the overall COMEX gold market structure was still much more bullish than I would have imagined at this stage. But the standout feature of the report was the sharp increase in concentrated short selling.

The 8 largest concentrated gold shorts, apparently all commercials, accounted for 20,000 contracts of the total commercial net selling during the reporting week. As of Jan 29, the 8 largest gold shorts hold a concentrated net short position of 187,072 contracts (18.7 million ounces) versus a total commercial net short position of 118,600 contracts. While it is certainly typical and even “normal” for the concentrated short position of the 8 largest traders to be much higher than the total commercial net short position, it is only normal in a manipulated market, which is a state the COMEX gold futures market has been in for many years. That’s because COT data prove that without the concentrated short selling by 8 speculating banks, there would be no net commercial short position at all (since away from the 8 largest traders, the commercials are net long).

One doesn’t even need to prove that these 8 big short banks have actively colluded to depress and contain gold prices – their documented short positions speak for themselves. If these 8 crooked banks hadn’t sold short 187,000 net contracts, gold prices would be much higher. That’s because all futures contracts need both a buyer and seller; so if the 8 crooked banks needed to be replaced by other sellers, unless one could find another 8 short sellers to replace them at current prices (an impossibility), then it would take many more traders for replacement. The only way to do that (conceivably) is through much higher prices. This is the central theme, but let me finish the COT report before coming back to this.

The managed money traders in gold bought far fewer net gold contracts than the commercial sold (always a good sign); 16,187 contracts to be precise, consisting of new longs of 21,109 and the new short sale of 4992 contracts. Explaining why managed money buying was less than commercial selling, was the nearly 9000 contracts of net buying by other large speculative traders. The net long position of the managed money traders of 32,000 contracts as of Jan 29, while higher by around 110,000 net contracts from the Nov 13 price lows, still leaves room for as many as 200,000 additional net contracts to reach the extremes seen in both 2016 and 2017.

In COMEX silver futures as of Jan 29, the commercials increased their total net short position by 7500 contracts to 72,500 contracts. This was in the expected range given silver’s three day price jump of as much as 60 cents into Jan 29. However, silver had yet to penetrate $16 by reporting week’s end (it would do so in the report to be published on Friday). The short position of JPMorgan appears to have increased to 21,000 to 22,000 net contracts, while the concentrated short position of the 8 largest traders (definitely now all commercials) increased by 3000 contracts to 96,278 contracts, the equivalent of more than 481 million ounces.

Please consider this. An underground mine in Peru that digs out of the earth 4 million ounces in a year was just shut down due to low silver prices; yet at the same time and price, 8 crooked banks have increased their net speculative short position to more than 100 times that mine’s annual production. If the Justice Department doesn’t see something drastically wrong with that, then all hope for the rule of law is lost. Remember, concentration is the one absolute requirement in any manipulation. In silver, the concentration is off the charts.

You have to go back to last summer to find a larger concentrated short position in silver, but even when you do, some big differences are obvious. For one, JPMorgan’s short position was larger then, while the short position of other commercial traders (swap dealers) back then was smaller than it is now. What I think this reflects is JPMorgan’s move to be done with manipulating the price of silver and it quietly passing the hot potato to the other big commercial shorts. I further believe this could prove to be the ruin of the other big commercial shorts that will soon be evident in an explosive price move higher. Dead men walking, indeed.

The managed money silver traders bought less than the commercials sold (same as in gold), in buying 4746 net contracts, consisting of 3230 new long contracts and the buy back and covering of 1516 short contracts. Even though the managed money traders in silver have bought more than 80,000 net contracts (400 million ounces) since Nov 13, much more proportionately than the 110,000 net contracts they purchase in gold, there is still room for as many as 60,000 net contracts of additional managed money buying (and, admittedly, even more room for selling to get back to Nov 13 levels).

If you hadn’t noticed, I keep referring to price and market structure levels since Nov 13. The reason is because I think the world of silver and gold may have changed because of the shocking announcement by the DOJ on Nov 6 that it was investigating precious metals manipulation on the COMEX. Let’s face it – as of today, just over three months later, gold has now rallied by as much as $150 and silver by more than $2, with nary a spoofing price take down in the interim. It’s either a remarkable coincidence or something more. Count me in the “something more” category.

I continue to believe that the fate of the 8 concentrated shorts in COMEX silver and gold holds the key to what occurs next, namely, these big manipulative traders will, yet again, succeed in knocking down prices and buying back added shorts at lower and profitable (to them) prices or they will fail spectacularly for the first time ever. While this is a clear either or circumstance, the consequences of the big shorts failing for the very first time loom larger in my opinion than ever before. The only way in which I can explain that is by my money scoreboard tabulation, which I hadn’t raised very recently because prices hadn’t done much since my calculation on Feb 2.

Just to be clear, I include JPMorgan in the calculation for how the big 8 shorts are doing in gold and silver on a combined basis, but I hope you know that JPMorgan, by virtue of its massive physical holdings of silver and gold (800 million ounces and 20 million ounces respectively), is completely immune from real losses on its short positions on an explosion in gold or silver prices. JPMorgan is in great jeopardy from Justice Department findings, just not market losses from higher gold and silver prices.

It’s a much different situation for the other big gold and silver shorts, which are completely exposed to unlimited losses on the short positions they hold. Certainly, JPMorgan is nowhere near as short as it has been in the past and that’s an indication to me that the big remaining commercial shorts are no longer the cohesive “all for one, one for all” unit that existed in the past. In fact, the only question in my mind is if these other big shorts actually realize the danger they are in or are they about to learn it ahead on a first hand basis. I think I do understand why these big shorts would have put themselves in such a dangerous situation, namely, it always worked for them before. But that was before JPMorgan abandoned ship and the DOJ began nosing around (likely one and the same). But COT data indicate clearly that the big shorts have committed themselves to the short side, wittingly or unwittingly.

So now the question is how much financial damage the big shorts, ex-JPM, can and will take before one or two (to start) break ranks and, in turn, weaken the collective death-grip on prices always held by the big 8 shorts. This is where the money scoreboard calculations come in handy. Back on Feb 2, when I resumed the calculations after a long absence, I calculated that the big 8 shorts, on a combined basis in silver and gold, were out $1.3 billion. That was based upon a 20 million ounces short position (200,000 contract) in gold and a 400 million ounces short position (80,000 contracts) in silver and using a gold price of $1322 and silver price of $15.92. I had calculated on Feb 2 that the average price (cost basis) for the big 8 short position to be $1275 in gold and $15 in silver.

Updating the variables for latest reported positions (19 million ounces in gold and 480 million ounces in silver and the slightly higher average shorting price ($1280 in gold and $15.20 in silver), at today’s prices ($1345 in gold and $16.10 in silver), the combined open loss for the big 8 traders in both gold and silver is just under $1.8 billion, up nearly a half billion dollars since Feb 2.

The previous high-water mark for the maximum dollar amount the big 8 shorts were in the hole for on an open and unrealized basis was approximately $4 billion in the summer of 2016, when gold hit $1385 and silver was over $21. That time, the big commercial shorts prevailed and just after Election Day 2016, the commercial shorts recouped all their open losses. While that possibility must be said to exist today, there are some important differences between the summer of 2016 and now. What are those differences?

For one, the current move higher is relatively young, just over three months in existence, while the move in 2016 was two or three times more mature. In addition, gold prices are not that far from its peak prices of 2016, while silver is still miles below its $21 former high. Also, the concentrated gold short position in back at the peak in 2016 was 100,000 contracts (10 million ounces) larger than it is now; I believe due to the much larger rally that took place in 2016, when gold rose around $300 to the peak (versus $150 in the current move).

However, the biggest differences today are that JPMorgan is no longer the stalwart and backbone of the concentrated short position as it was back in 2016, meaning there is a greater propensity for the remaining shorts to panic and rush to cover at some point than they were back then; plus one other thing. That “other thing,” of course, is that there was no Department of Justice ongoing investigation in place back then, as there surely is now.

I don’t think the big shorts, away from JPMorgan, have a clue as to what type of exposure they have placed themselves in by virtue of what they have shorted to date – otherwise they wouldn’t have shorted in the first place. I believe, as is customary in any DOJ investigation that subpoenas have been issued and depositions have occurred; but that those subpoenas and depositions have been confined to JPMorgan and do not include the other banks wildly speculating in COMEX gold and silver futures. Yet.

That leaves open the distinct possibility that the other big shorts might learn the hard way about what a predicament they are in. The “hard way” involves a sudden recognition that the gold and silver rally have run far enough for them to do anything but starting to buy back and cover shorts to limit losses as quickly as possible. That translates into sudden and aggressive buying in markets in which they have been the primary short sellers. That leaves open the question of who the heck might sell to the newly panicky shorts desperate to buy and at what price? Yes, I’m talking about the possibility of a price explosion and the mechanics for why it might happen.

Finally, a month ago, in the weekly review of Jan 19, I mentioned the futures market structure of a number of markets, including copper, palladium and crude oil. In copper, I mentioned that the managed money short position was likely near a record and most likely to unfold in a “hellacious” rally. Over the next week, copper prices fell anew (making me feel like a jerk for bringing it up). However, after the subsequent price low of $2.63, copper prices have rallied to over $2.92 today. I don’t know if that meets the definition of hellacious, but it is the highest price copper has seen since last July. I do know that the prime driver for the rally has most likely been managed money short covering. It sure hasn’t been economic reports indicating an uptick in actual copper consumption.

In mentioning palladium, I commented how the managed money net long position had likely hardly changed since Dec 18, since total open interest had not changed much. The COT report of Jan 29 confirms that the net and gross long position of the managed money traders has hardly budged in NYMEX palladium futures. This means that whatever drove palladium prices to new highs (up more than $250) was something other than managed money buying. The most likely “something other” was physical buying by industrial users, not speculators. I’m not predicting what palladium prices may do, just that there is scant evidence that the rally is being driven by speculative buying in futures markets.

As for crude oil, I mentioned that the managed money long position looked historically low and most likely to increase in time, driving prices higher. While crude oil prices are a few dollars higher amid some signs of managed money buying (mostly short covering), it’s far too early to conclude whether my take will be correct. But, hopefully, the Justice Department will take a strong look at what really sets the price of many commodities.

Ted Butler

February 20, 2019

https://www.butlerresearch.com/

More from Jim Cook: I was in the silver and gold business for 25 years before I ran across Mr. Butler. I’ve learned more from him than everyone else combined. If you have an interest in silver and gold, I’m certain you will learn as well. Butler’s service is like an intensive college course on silver and gold. For $35 a month, I recommend you give it a try.

Also, if you would like to hear my comments on Ted and his case for silver Google Chris Marcus interviews Jim Cook.

END

Australia reports on where it’s gold is stored:

(Wright Sydney Herald/GATA)

Australia’s central bank reports on its gold reserves …

Submitted by cpowell on Fri, 2019-02-22 04:38. Section: Daily Dispatches

… just days after Bullion Star’s Ronan Manly questions bank’s custody of them:

http://www.gata.org/node/18882

* * *

Australia’s Gold … Safely in the Hands of the Bank of England

By Shane Wright

Sydney Morning Herald, Sydney, Australia

Friday, February 22, 2019

Those looking to break into the Reserve Bank of Australia’s Sydney headquarters looking for a stash of gold are going to be disappointed.

The bank explained to a parliamentary committee today that its store of gold — all 80 tonnes of it — is 17,000 kilometres away in the Bank of England.

…

About 6,400 bars of the precious metal, which according to RBA governor Philip Lowe is worth about $4 billion, is sitting with 400,000 other bars in special vaults in the world’s gold-trading capital.

Later this year a special audit will be conducted to ensure all these bars are there and that they weigh the 80 tonnes the Reserve Bank has on its ledger. …

Last financial year about 10 tonnes of the precious metal was leased. In the early parts of the 2000s, almost all of it was being borrowed. …

… For the remainder of the report:

https://www.smh.com.au/politics/federal/australia-s-gold-safely-in-the-h…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

A good one@!! What happened to Australia’s 80 tonnes of stored gold?

(courtesy Manly/Bullionstar)

What’s Up With Australia’s 80 Tonnes Of Gold At The Bank Of England?

Submitted by Ronan Manly of BullionStar

Recently, news network RT.com asked for comments on the question of the 80 tonnes of the Reserve Bank of Australia’s (RBA) gold reserves and their supposed storage location at the Bank of England’s gold vaults in London. Based on some of those comments I made, RT has now published an article in its English language news website at www.rt.com about this Australian gold that the RBA claims is held in London.

The RT.com article, which was published on 18 February 2018, is titled “Hey UK! It’s not just Venezuela, what happened to Australia’s gold?“, and can be read in full here on the RT website.

For the commentary, RT actually asked me quite a few interesting questions on both the Australian gold and other related gold topics. Since both the extended questions and the answers might be of interest to readers, we have decided to publish below the full set of questions and answers in Q&A format, which are as follows:

1) What happened to Australia’s gold? What’s your opinion?

The Reserve Bank of Australia (RBA) claims to have 80 tonnes of gold bars stored in a bailment arrangement, in an allocated gold account, at the Bank of England vaults in London. Bailment means the Bank of England is custodian, and the RBA owns and has title to specific serial numbered gold bars.

However, there have never been any independent physical audits of this gold, which means that there is no way to verify the RBA’s claim that it has all the gold that it claims to have.

In 2013, the Bank of England allowed the RBA to do a partial audit of some of the claimed RBA gold holdings, but the results of this audit remain secret, and even after FOIA requests, the documents from this audit were blocked by both the Bank of England and the RBA and never released. This also raises a red flag.

Most importantly, the critical document to any gold holding held under bailment is a proper weight list of the gold bar holdings (including refiner serial numbers), and such a list has also never been published by the RBA. Such a weight list is fundamental to any claimed gold holding (for example, think about the gold-backed Exchange Traded Funds (ETFs) which publish their full gold bar weight lists online on a daily basis).

The RBA has not made any gold purchases or sales over the last 20 years, so apart from gold lending, the RBA gold should be the same bars that it has held over at least the last 20 years. It would therefore be a simple matter to publish in a single zipped file all of the versions of the gold bar weight list that this 80 tonnes of gold has represented over the last 20 years. The Bank of England’s gold bar accounting system has all of this information and it would be simple to extract it.

Throughout the last 20 years, the RBA also admits that a lot of its claimed gold holdings have been lent out in the secretive London Gold Lending Market, but there is no information whatsoever available on any of these lending transactions or the serial numbers of the gold bars involved. In other words, there has never even been one snapshot publication of a proper industry standard weight list for these RBA gold bars (by refiner serial numbers), let alone an updated weight list every time the RBA lent out or closed a gold lending deal.

During the years 1999 – 2004, the RBA says that almost all of it’s gold was on loan, and the RBA is still in the gold lending market to this day, for example, 10 tonnes of its claimed 80 tonnes at the Bank of England were said to be on loan during 2018. The important point here is that the gold bars that the RBA would have title to at the completion of a gold lending deal would not be the same bars that it held prior to this gold being lent to a bullion bank in London.

Independent physical audits, full and proper weight lists, details of gold lending transactions, and above all a transparent attitude, would all allow instant verification of the RBA’s claims about the sovereign Australian gold holdings. That the RBA and Bank of England refuse to do any of these things is highly suspicious. Therefore, there is no black and white way to say that the RBA has the 80 tonnes of gold it claims to have.

2) Why are countries like Australia and Canada willing to part with physical gold assets? Is that a good idea in your opinion? How much gold does Australia really have?

Up until late 1996, the Australian central bank held nearly 247 tonnes of gold, a considerable amount of gold by any measurement. However, it then went on a gold selling spree during the first half of 1997 and sold 167 tonnes, leaving it with the current claimed 80 tonnes.So why did the RBA sell this gold? At the time, the usual justifications were wheeled out by the RBA such as that the proceeds of gold sales could be better invested in financial assets, and that other countries were also selling gold at that time, including Canada, Netherlands and Belgium. But, these reasons have always stinked. Firstly, the RBA gold sales occurred just before a huge bull market run-up the gold price between 2000 and 2011, so the RBA made a huge opportunity loss on the gold sales.

Secondly, selling gold just because another central bank is doing is nonsensical and void of investment rationale. The same goes for Canada which basically sold all of its gold, about 500 tonnes, in the late 1990s and early 2000s. Again, there was no investment rationale for doing so and the Canadians seem to have been coaxed into these sales by external parties. It’s also interesting that in hindsight, no one in the Canadian Department of Finance ever wanted to talk about these gold sales later on when asked by the media or investigative journalists.

Of course, it was not a good idea for Australia to sell most of its gold and for Canada to sell all of its gold. The timing of these sales was also some of the worst ever. Beyond this, these central banks acted irresponsibly and had no accountability to the populations of their nations. Gold is the Wealth of Ages, the sovereign wealth of a nation. It is not some securitized financial asset to be sold and squandered by statist central bankers who answer to no one.

3) Some experts believe that western central banks are “covertly disposing” of their gold or otherwise leasing it to China and India through bullion banks. Do you believe in that? Do you believe there’s some grand, global gold conspiracy involving the world’s central banks?

There is a mountain of evidence that Western central banks despise the power of gold and will go to great lengths at the highest levels to contain the gold price through coordinated interventions and anti-gold policies. From the London Gold Pool of the 1960s, to the US and IMF gold sales in the 1970s, to the 1980s Gold Pool discussions at the Bank for International Settlements (BIS), to the Bank of England intervening into the London Gold Fixes in the 1980s, G10 central bank governors have often been personally involved in committing to gold market manipulation.

This continued through the 1980s and 1990s with the growth of the secretive gold lending market and central bank gold leasing, the various European central bank gold “agreements” which did the opposite of what they claimed to do, the sabotage of transparent IMF gold accounting policies by the main European central banks in 1999, and the gold price fix manipulation by bullion banks in London where regulators looked the other way. All of this evidence and more is available if anyone wants to look, such as on the GATA website and elsewhere.

As regards the Australian and Canadian gold sales, the more logical explanation for both of these was that they were coordinated gold sales by G10 central banks as part of a plan to fire-fight the physical gold market or to bail out gold short bullion banks, or that the sales were part of secretive gold re-distributions to other countries, such as to China. While this may seem far-fetched, you have to realize that central banks never tell the truth, especially when it comes to the gold market, and that the sheer numbers of central bank gold sales around that time in the 1990s and 2000s, including by the UK and Switzerland, point to something collusive about the sales rationales.

All of these sales were also secretive, with nothing revealed about the identities of the buyers. Any lists of such central bank gold sales, for example in an FOIA connected to the UK’s gold sales, have the identities of the buyers redacted. So its totally possible that a central bank, such as China, was on the receiving end of these gold sales. There is evidence that the UK Treasury gold sales in 1999 done for bullion bank bailout purposes, so this could be true with the RBA sales.

At a broader level, there seems to be collusive policy behind the scenes of western central banks offloading physical gold in a coordinated manner through secretive sales and leasing it to achieve various policy objectives. These objectives include inducing extra gold supply to dampening down the gold price, fire fighting physical shortages, at times bailing out bullion banks, and most intriguingly, redistributing some of the West’s central bank gold holdings to central banks such as the People’s Bank of China. Gold Pools (central bank syndicates) don’t have to take the form of advertised arrangements as in the 1960s. A central bank gold pool exists any time two or more central banks clandestinely use some of their gold holdings in a coordinated way.