GOLD: $1298.00 DOWN $16.90 (COMEX TO COMEX CLOSING)

Silver: $15.23 DOWN 38 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : xxx

silver: $xxx

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 66 NOTICE(S) FOR 6600 OZ (0.2121 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 192 NOTICES FOR 19200 OZ (.5972 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

530 NOTICE(S) FILED TODAY FOR 2,650,000 OZ/

total number of notices filed so far this month: 3869 for 19,345,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3828:UP $14

Bitcoin: FINAL EVENING TRADE: $3848 UP 35

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 29/66

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,312.800000000 USD

INTENT DATE: 02/28/2019 DELIVERY DATE: 03/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 29

685 C RJ OBRIEN 1

690 C ABN AMRO 3 4

709 C BARCLAYS 4

737 C ADVANTAGE 19 14

800 C MAREX SPEC 33 14

878 C PHILLIP CAPITAL 6 1

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 66 66

MONTH TO DATE: 192

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2414 CONTRACTS FROM 199,055 DOWN TO 196,641 WITH YESTERDAY’S 12 CENTS LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 1796 FOR APRIL, 0 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1796 CONTRACTS. WITH THE TRANSFER OF 1796 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1796 EFP CONTRACTS TRANSLATES INTO 8.98 MILLION OZ ACCOMPANYING:

1.THE 12 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 23.870 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

29,480 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1796 CONTRACTS) OR 8.98 MILLION OZ: (AVERAGE PER DAY: 1796 CONTRACTS OR 8.98 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 8.98 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.20% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 373.835 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2414 WITH THE 12 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 1796 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 618 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1796 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2414 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.61 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.995 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 530 NOTICE(S) FOR 2,650,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 23.870 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 7310 CONTRACTS DOWN TO 489,879 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $4.90//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11,182 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 11,192 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 489,879. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A CONSIDERABLE SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3882 CONTRACTS: 7310 OI CONTRACTS DECREASED AT THE COMEX AND 11,192 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN 3882 CONTRACTS OR 388,200 = 12.07 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.90.

YESTERDAY, WE HAD 6469 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 11,192 CONTRACTS OR 1,119,200 OZ OR 34.81 TONNES (1 TRADING DAYS AND THUS AVERAGING: 11,192 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 34.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 34.81/2550 x 100% TONNES = 1.36% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 910.37 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 7310 WITH THE LOSS IN PRICING ($4.90) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11192 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,192 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 3882 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,192 CONTRACTS MOVE TO LONDON AND 7310 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 12.07 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $4.90 IN YESTERDAY’S TRADING AT THE COMEX??

we had: 66 notice(s) filed upon for 6600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $16.90 TODAY

HUGE CHANGES IN INVENTORY AT THE GLD: AS EXPECTED AS THIS GOLD WAS PROBABLY USED IN THE RAID THESE PAST FEW DAYS;

A WITHDRAWAL OF 4.11 TONNES

/GLD INVENTORY 784.22 TONNES

Inventory rests tonight: 784.22 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 38 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 309.374 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2414 CONTRACTS from 199,055 DOWN TO 196,686 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1796 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1796 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2414 CONTRACTS TO THE 1796 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 618 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 3.09 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 23.870 MILLION OZ FOR MARCH.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 12 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 1796 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 53.05 POINTS OR 1.80% //Hang Sang CLOSED UP 178.99 POINTS OR 0.63% /The Nikkei closed UP 217.53 POINTS OR 1/62%/ Australia’s all ordinaires CLOSED UP 0.34%

/Chinese yuan (ONSHORE) closed UP at 6.7053 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 57.39 dollars per barrel for WTI and 66.33 for Brent. Stocks in Europe OPENED RED//.

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7053 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7058: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCE

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

The real story behind the North Korean talk breakdown

(courtesy Tom Luongo)

ii) South Korea

My goodness: shipments fell 11.1% year over year in the powerful exporting nation of South Korea. This is hard data and suggests that the world’s economy is grinding to a halt.

( zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

China’s shadow debt business has finally hit a roadblock

( zerohedge)

( zerohedge)

Canada allows the extradition of Meng to move forward. There must still be a hearing which will be on March 6 and then the Canadians can decide to send her to the uSA. Needless to say that relations between China and Canada will spiral southbound.

( zerohedge

4/EUROPEAN AFFAIRS

i)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)A good look at two nations economic outlook and both are bad:

1. the uSA

2. Germany

( John Rubino)

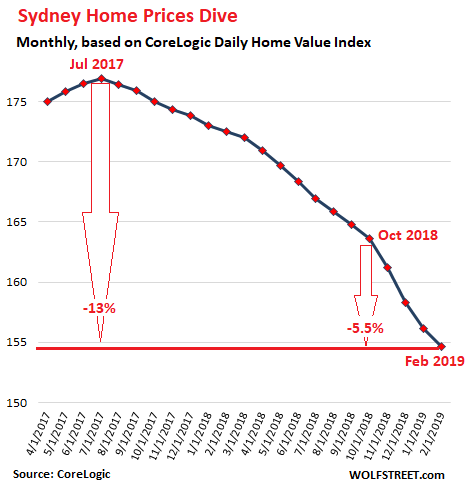

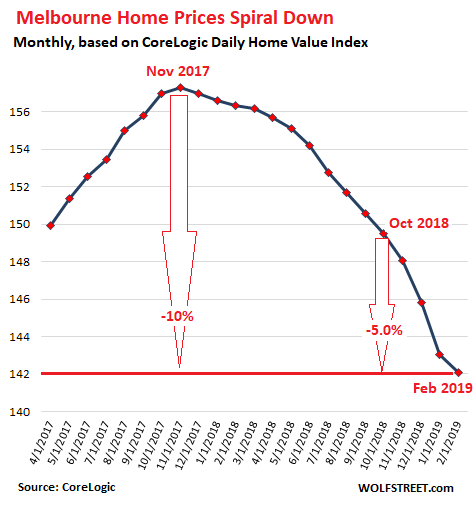

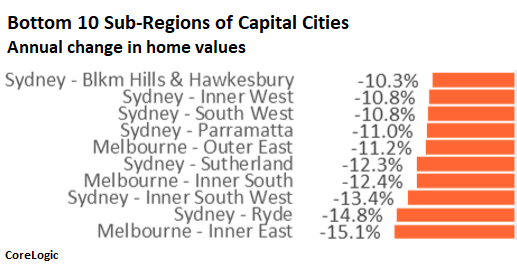

ii)Australia

Wolf Richter notes that home prices in Sydney and Melbourne are spiraling down.

( Wolf Richter)

iii)Canada

The Canadian Looney tumbles on an unexpected drop for two consecutive months in Canadian GDP

As I am stating, the entire world’s economies are grinding to a screeching halt

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

Venezuela closes it’s European offices in Lisbon Portugal and moves it to Moscow. Putin affirms his support for the former bus driver Maduro

( zero hedge)

9. PHYSICAL MARKETS

( zerohedge)

( GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

We have been highlighting to you the falling in Treasury bond prices i.e. higher yields as China adds huge stimulus to the global economy. This will end not too good

( zerohedge)

ii)Market data

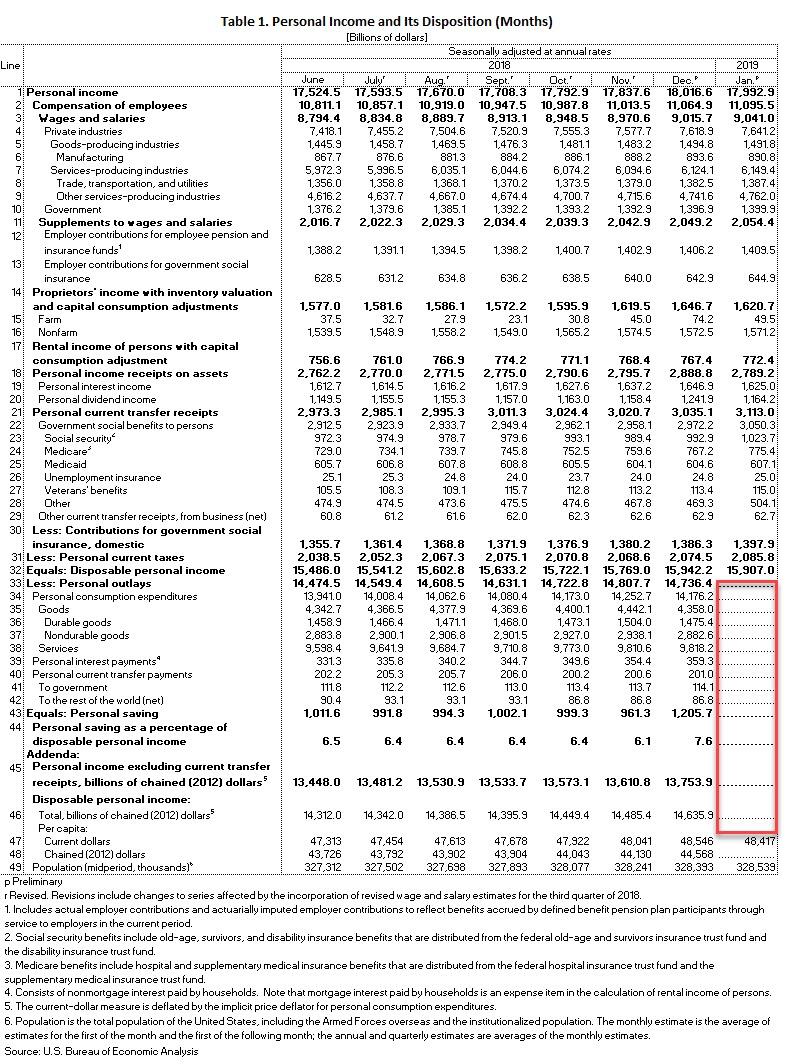

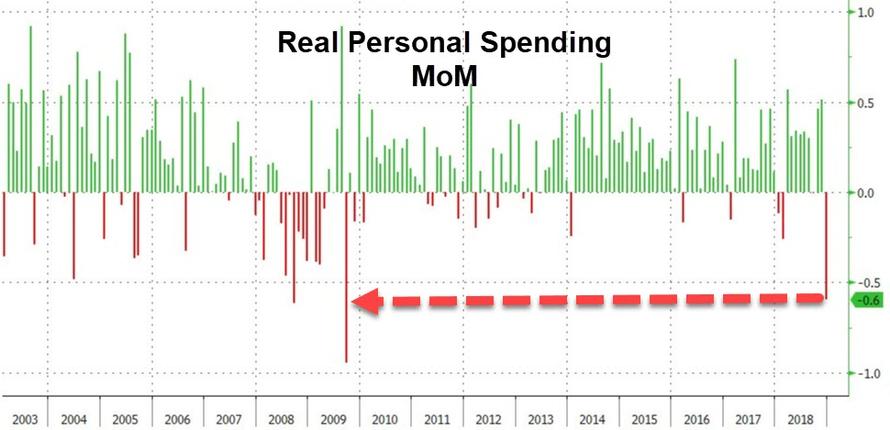

a)This is not good for GDP numbers; December personal income fell .1% month/month when the street was expecting a huge .3% rise. That put a dart into their balloon. The personal spending plunged a massive .5% month/month in January and no doubt ta small percentage was due to the government shutdown from Dec 21 onward. Interestingly enough no spending data was forthcoming from January..we only have December numbers

( zerohedge)

d)It did not take Goldman Sachs, the Atlanta Fed and the New York Fed to revise its estimate of Q1 GDP

iv)SWAMP STORIES

a)Trump comments that Congress must demand the transcript of Michael Cohen’s new book to show his lies

( zerohedge)

b)AOC gets her story all mixed up with respect to Michael Cohen’s testimony

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL FALLS TO 771 CONTRACTS FOR A LOSS OF 13 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 797 CONTRACTS UP TO 146,911 CONTRACTS.

comex gold volumes are getting extremely low as players just do not want to play in this casino.

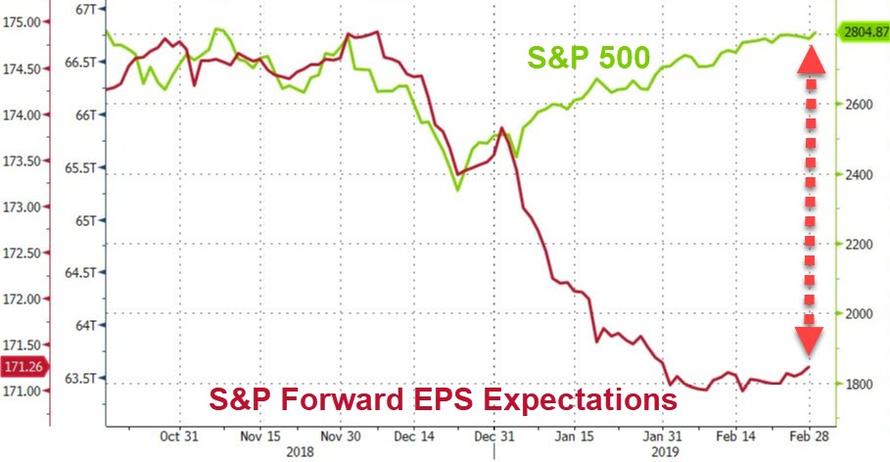

Gold Still on a Long Term Track to Reach $2,000 An Ounce

– Why gold is down for the month, but still on a long-term track to reach $2,000 an ounce

“A $22 trillion national debt and the lack of any will to rein in massive spending is making America’s creditors nervous and…the ‘risk free’ status of U.S. Treasuries will come into question” said GoldCore

– “Central bank buying is quite bullish as they are massive institutional players…and even a small allocation to gold can be quite significant in terms of additional physical demand” – GoldCore

– “Official sector gold buying … means that they are concerned regarding the outlook for the dollar and are reducing and hedging exposures in this regard…”

– Gold ‘more than likely’ to climb to a record high in 24 months

By Myra Saefong of Dow Jones Marketwatch

Gold prices have pulled back from a 10-month high in recent sessions, leaving investors wondering why the many geopolitical and economic issues plaguing the market haven’t been able to fully support the metal’s haven appeal.

Gold notched that multi month peak just over a week ago on the back of uncertainty linked to Brexit, the U.S.-China trade dispute, and global economic growth. But prices on Thursday suffered a loss for the month on the heels of four monthly gains—the longest upward streak since 2016.

“Prices have run up to the top end of the trading range they have held for the past five years,” says Rob Haworth, senior investment strategist at U.S. Bank Wealth Management, pegging the “top end” at $1,350 to $1,400. “Without further easing in financial conditions, ramping inflation or stock market volatility, gold prices are likely to struggle at the top end of this five-year trading range,” he says.

Futures prices settled at two-week low of $1,316.10 an ounce on Thursday and logged a monthly loss of about 0.7%. They had finished at $1,347.90 on Feb. 20, the highest for a most-active contract since April.

Gold still faces supply challenges and any uptick in demand would tighten inventories.

The gold mining sector has seen a spate of merger and acquisition activity, most recently with Barrick Gold Corp’s unsolicited proposal to buy Newmont Mining Corp. in a deal that values Newmont at nearly $18 billion.

“The M&A activity is reflective of the increasing difficulty [in] finding and mining gold reserves,” says Will Rhind, chief executive officer at exchange-traded fund issuer GraniteShares. “The consolidation of the gold-mining sector…highlights existing gold supply difficulties and shortages, which is supportive of gold prices,” he says.

On the demand side, central banks have been on a gold buying spree, lifting 2018 net purchases of the metal to 651.5 metric tons—their highest in more than 50 years, as geopolitical uncertainty and economic worries prompted national banks to diversify their reserves, according to the World Gold Council.

“Central bank choices about composition of their reserves send important signals to financial markets about relative safety of currency alternatives,” says Trey Reik from Sprott, which manages the Sprott Physical Gold Trust.

“Whenever gold allocations are on the rise, central bank authority is augmenting the [money-like qualities] of gold.”

Carlos Artigas, WGC director of investment research, says that on an annual basis, central banks have been net buyers of gold since 2010. A recent WGC survey also revealed that almost one-fifth of central banks signaled their intention to raise gold purchases over the next 12 months.

“Central bank buying is quite bullish as they are massive institutional players…and even a small allocation to gold can be quite significant in terms of additional physical demand,”says Mark O’Byrne, research director at precious metal brokerage GoldCore.

“Official sector gold buying does not imply necessarily that [central banks] are bullish on gold per se….It likely means that they are concerned regarding the outlook for the dollar and are reducing and hedging exposures in this regard.”

Year to date as of Thursday, the dollar, as measured by the ICE U.S. Dollar Index was little changed after a 4.4% rise in 2018. Dollar-denominated gold often trades inversely to the U.S. currency.

“Trillion-dollar deficits in the U.S. under [President Donald] Trump and growing fiscal imprudence will be making central banks with large dollar reserves increasingly nervous about the outlook for the dollar,” says O’Byrne.

“A $22 trillion national debt and the lack of any will to rein in massive spending is making America’s creditors nervous and…the ‘risk free’ status of U.S. Treasuries will come into question.” That may lead to higher demand for haven gold.

“Given the scale of the risks,” O’Byrne believes gold is “more than likely” to climb to a record high of $2,000 within the next 24 months.

News and Commentary

Gold hits two-week low as upbeat U.S. data lifts dollar (Reuters.com)

Romania Ruling Party Battles Bank Over Gold Reserves, Return 95% back (BalkanInsight.com)

Growing China downdraft chills Asia factory activity (Reuters.com)

Oil climbs amid OPEC-led supply cuts, but economic weakness drags (Reuters.com)

Stocks Post Year’s First 3-Day Slide; Dollar Gains: Markets Wrap (Bloomberg.com)

Gold’s Four-Month Winning Streak on the Line Today (GoldCore in Barrons) (Barrons.com)

Gold – here’s why it just might be different this time (MoneyWeek.com)

Trump Returns Home to Face the Mueller Music (Bloomberg.com)

Home Prices in Sydney & Melbourne Spiral Down, Bust Spreads (WolfStreet.com)

Murphy and Hemke on Silver and Palladium Manipulation (Youtube.com)

Stockman on Peak Trump, The Undrainable Swamp & the Fantasy of MAGA (Youtube.com)

Gold Prices (LBMA PM)

28 Feb: USD 1,325.45, GBP 996.21 & EUR 1,162.82 per ounce

27 Feb: USD 1,326.45, GBP 998.02 & EUR 1,164.09 per ounce

26 Feb: USD 1,327.55, GBP 1005.79 & EUR 1,168.11 per ounce

25 Feb: USD 1,329.15, GBP 1016.80 & EUR 1,170.32 per ounce

22 Feb: USD 1,322.25, GBP 1016.15 & EUR 1,166.49 per ounce

21 Feb: USD 1,335.05, GBP 1021.85 & EUR 1,177.78 per ounce

Silver Prices (LBMA)

28 Feb: USD 15.81, GBP 11.89 & EUR 13.85 per ounce

27 Feb: USD 15.86, GBP 11.91 & EUR 13.92 per ounce

26 Feb: USD 15.83, GBP 11.98 & EUR 13.93 per ounce

25 Feb: USD 15.95, GBP 12.19 & EUR 14.04 per ounce

22 Feb: USD 15.87, GBP 12.20 & EUR 14.00 per ounce

21 Feb: USD 15.91, GBP 12.19 & EUR 14.02 per ounce

Recent Market Updates

– “Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Gold Broker Has Good Sense and Prefers Gold To All That Glitters (The Times)

– The Utterly Unbelievable Scale of U.S. Debt Right Now

– The Best Time In History To Buy GOLD

– Jim Willie Interviews Mark O’Byrne – Prepare Now For Global Financial Crisis II

– 7 Major Flaws Of The Global Financial System – Excellent Infographic

– The Case for Gold In 2019 – The Economist

– Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

BMG Group’s Nick Barisheff: Canadian regulators discourage investment in gold mutual funds

Submitted by cpowell on Thu, 2019-02-28 17:30. Section: Daily Dispatches

12:30p ET Thursday, February 28, 2019

Dear Friend of GATA and Gold:

Nick Barisheff of bullion dealer and metals fund manager BMG Group in Canada writes that the country’s securities regulators have issued rules —

http://www.osc.gov.on.ca/en/SecuritiesLaw_ni_20161208_81-101-81-102_csa-…

— that discourage investors from putting money in mutual funds holding gold. The rules, Barisheff writes, assign the monetary metal a risk rating of medium to high, even though the Bank for International Settlements now classifies gold as a risk-free asset like U.S. dollars and U.S. Treasuries.

Barisheff’s commentary is headlined “Devastating Losses Are Coming” and it’s posted at the BMG Group internet site here:

http://bmg-group.com/devastating-losses-are-coming-what-is-your-advisor-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

We brought you this story last night but it is worth repeating: Parliament in Romania wants its gold stored in London back

we wish them luck

(courtesy zerohedge)

Parliament leaders want Romanian gold reserves brought home

Submitted by cpowell on Thu, 2019-02-28 23:50. Section: Daily Dispatches

By Ioana Erdei

Business Review, Bucharest, Romania

Wednesday, February 27, 2019

BUCHAREST, Romania — Chamber of Deputies President Liviu Dragnea and Socia Democratic Party Sen. Serban Nicolae have proposed a bill to force the National Bank to store 95 percent of Romania’s gold reserves in the country.

The bill is meant to change the law that establishes the National’s Bank statute. According to the document, the reason for this demand is that gold stored abroad produces only additional costs with storage. The bill also wants to eliminate the word “international” from the terminology used by the National Bank in “international gold reserves.”

Romania’s gold reserves, 103.7 tons, are stored in three countries, according to the National Bank officials. Three years ago, the institution announced that 60 percent of the gold reserves were stored abroad. The situation has not changed — 61 tons of the gold are stored at the Bank of England, more than 40 tons are kept at the Bank of Romania in Bucharest, and fewer than five tons are stored at the Bank for International Settlements in Basel, Switzerland. …

… For the remainder of the report:

http://business-review.eu/news/liviu-dragnea-demands-the-national-bank-t…

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Murphy talks with Craig Heme on palladium and silver

(courtesy GATA)

GATA Chairman Murphy, TF Metals Report’s Hemke interviewed on palladium, silver

Submitted by cpowell on Fri, 2019-03-01 01:16. Section: Daily Dispatches

8:17p ET Thursday, February 28, 2018

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report and GATA Chairman Bill Murphy were interviewed this week by Phil Kennedy of Kennedy Financial, discussing the recent explosion in palladium and whether failure of naked shorting of futures contracts in that metal could cause failure of the futures markets in gold and silver. They also discuss JPMorganChase’s domination of the silver market. The interview is 36 minutes long and can be viewed at You Tube here:

https://www.youtube.com/watch?v=SUcsne5XnyI&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7053/

//OFFSHORE YUAN: 6.7058 /shanghai bourse CLOSED UP 53.05 POINTS OR 1.80% /

HANG SANG CLOSED UP 178.99 POINTS OR 0.63%

2. Nikkei closed UP 217.53 POINTS OR 1.62%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 96.19/Euro RISES TO 1.1384

3b Japan 10 year bond yield: RISES TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.70/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.39 and Brent: 66.33

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.19%/Italian 10 yr bond yield UP to 2.75% /SPAIN 10 YR BOND YIELD UP TO 1.20%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.65

3k Gold at $1306.40 silver at:15.50 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 65.85

3m oil into the 57 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.79 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9981 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1363 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.19%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.73% early this morning. Thirty year rate at 3.10%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3582

Global Stocks Surge On Rebound In Chinese Data, MSCI Inclusion

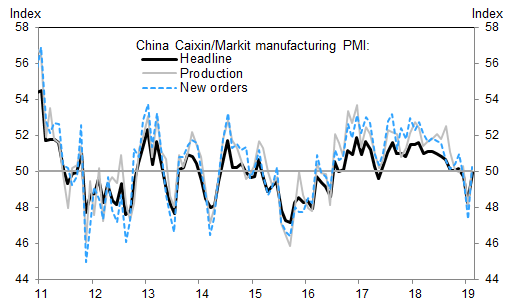

Just as the official Chinese manufacturing PMI’s disappointing Thursday print (to a three year low) pressured stocks on the last day of February, and sent both the MSCI World Index and the Dow Jones to three consecutive days of declines, the longest such stretch of 2019 yet, overnight’s Caixin PMI which unexpectedly posted a sharp rebound in February, rising to 49.9 from 48.3 in January, offered some reassurance to investors concerned about the growth outlook that the global economic drop may have troughed while “optimism” for a trade deal returned; Treasuries extended their recent decline and the dollar pushed higher for a third day before easing back. The result is a sea of green in global stocks with the S&P trading back over the critical 2,800 level.

Bullish sentiment stormed back led by China, where shares outperformed with the Shanghai Composite closing 1.8% higher following confirmation that MSCI Inc. will quadruple the weight of Chinese stocks in its global benchmarks from 5% to 20%, while in contrast to the small decline in NBS manufacturing PMI reported just one day earlier, the Caixin manufacturing PMI bounced back in February from the dip in January. It rose by 1.6pp to 49.9, although January-February combined, Caixin manufacturing PMI averaged at 49.1, lower than 49.7 in December last year. Most sub-indexes of the survey rebounded in February vs January. The fact that the index remained just barely in contraction territory was offset by a sharp increase in the forward-looking new orders index component.

According to Goldman, the Caixin manufacturing PMI showed “some early signs of better growth momentum in the manufacturing sector in February. However, the floating holiday and continued weakness shown in other indicators such as NBS manufacturing PMI added uncertainties to the above view, and for the period of January to February on average, growth momentum still likely softened from late last year. We continue to expect more policy easing to support the economy, and Jan-Feb industrial production data to be released in two weeks’ time will shed more light on the underlying growth trend early this year.”

As a result, China’s blue-chip CSI300 index surged 2.2% to land its best week since November 2015 after the MSCI announcement. It could potentially draw up to $80 billion of fresh foreign inflows to the world’s second-biggest economy.

“The news surrounding China and the Chinese economy has been better than news we’ve seen elsewhere,” Andrew Cole, head of multi asset at Pictet Asset Management Ltd., told Bloomberg TV in Hong Kong. “Clearly the central bank and the authorities are providing both fiscal and monetary stimulus.”

Elsewhere in Asia, Australia’s ASX 200 (+0.4%) extended on opening gains as IT and healthcare names led the advances, whilst heavy-exporter Nikkei 225 (+1.0%) outperformed after the yen dropped to a 10-week low against the greenback.

Later in the session, European shares opened notably higher, with the Stoxx Europe 600 Index rising to the highest in almost five months, as 18 of 19 industry sectors were in the green and car makers leading the charge, even after PMI data showed that euro-area manufacturing contracted last month, offset by the fastest rise in German retail sales since Oct 2016.

“We are seeing a fairly decent uptick in European markets,” said CMC Markets analyst David Madden, citing the combination of U.S. and China data as well as encouraging comments from the United States on China trade talks.

To be sure, the bad data in Europe continued and Spain’s manufacturing sector contracted for the first time for more than five years in February data from Madrid showed while in eastern Europe Czech manufacturing sentiment fell at its fastest rate in six years.

However, market reaction showed that “bad news can be good news” because it could well encourage the European Central Bank to hand out cheap TLTRO loans to euro zone banks in the coming months. Boosted by strong Chinese data and weak European data, futures on the S&P 500, Dow Jones and Nasdaq gained, with the EMini back over the critical 2,800 “quad top” resistance level. Emerging-market stocks snapped a three-day losing streak.

Traders will be relieved to see a strong close to the week after a 16% surge from Christmas through the start of this week, MSCI’s gauge of global equities has tread water as investors await progress in U.S.-China trade negotiations. American officials are preparing a final deal that Donald Trump and China President Xi Jinping could sign in weeks, even as a debate continues in Washington over whether to push Beijing for more concessions. Meanwhile, as Bloomberg notes, geopolitical concerns remain in the background, amid tensions between India and Pakistan and the failure of a summit between Kim Jong Un and Trump to achieve an agreement between the U.S. and North Korea on denuclearization.

U.S. President Donald Trump on Thursday fueled concerns over U.S.-China trade talks, warning that he could walk away from a trade deal with China if it were not good enough. But in subsequent comments Thursday, White House economic adviser Larry Kudlow called progress in the negotiations “fantastic” and said the countries were “heading towards a remarkable, historic deal.”

Mixed messages on trade combined with the collapse of the summit between Trump and North Korean leader Kim Jong Un on denuclearization, and data from China showing slowing factory activity to pressure U.S. stocks as Reuters notes. “News that President Trump walked out of the meeting with Supreme Leader Kim, because the two sides couldn’t reach an agreement over North Korea’s nuclear disarmament, dashed hopes for an easing in geopolitical tensions,” analysts at ANZ said in a morning note.Overnight, president Trump said he believes a good deal with North Korea will happen and added that North Korea did not want to fully denuclearise. Meanwhile, North Korea Foreign Minister said if US lifts sanctions, North Korea will denuclearise, whilst adding that Pyongyang will not change its stance even if the US seeks further talks. US Secretary of State Pompeo said that North Korea basically asked for all sanctions to be lifted.

In the latest Brexit news, UK’s Labour Party is reportedly moving towards a compromise plan which would allow PM May’s Brexit deal to pass but makes it clear that Parliament “withholds support” until the deal has been put to a public vote; according to multiple party sources.

Following a stronger than expected Q4 GDP print, Dallas Federal Reserve Bank President Robert Kaplan said on Thursday that it will take time to see how much the U.S. economy is slowing, supporting views of the Fed’s rate-hike holiday at least through to June.

In rates, long-dated government bond yields in Germany, the euro zone’s benchmark issuer, were set on Friday for their biggest weekly increase in more than year, reflecting easing concern about the global growth outlook and hopes that a no-deal Brexit will be avoided, and ignoring today’s equity euphoria. 10Y TSY yields meanwhile continued to rise, and were trading at 2.73% today after trading 10bps lower earlier in the week.

In FX, the Bloomberg Dollar Spot Index rose a third day, tracking a rise in Treasury yields; the dollar index which tracks the greenback against major rivals, was up 0.2 percent at 96.302, though it remained fractionally lower for the week overall. The yen led losses among G-10 currencies after better-than-expected China data sapped haven demand. The euro edged lower as PMIs out of the euro-zone confirmed a contraction in the manufacturing sector amid a slump in orders, while core CPI for the region slowed to 1.0% y/y, falling short of a 1.1% estimate. Britain’s pound has been the star of the week, jumping more than 1.5 percent after another set of twists in Brexit saga has cut the chances of the UK crashing out the EU at the end of the month with a transition deal. It was down a fraction on the day at $1.3250.

In commodities, iron ore extended its rally, stoking a gain in the Bloomberg Industrial Metals Subindex to the highest since early October. West Texas oil futures nudged toward $58 a barrel as strengthening economic trends in the U.S. signaled tightening supplies, and gold’s third successive drop set it up for the worst week since November. Brent and WTI are essentially flat, in-spite of trading positively overnight and initially during the European session, although they are once again trading within a fairly narrow range of less than USD 2/barrel. Elsewhere, since the imposition of US sanctions on the 28th January on Venezuelan oil, Venezuela’s oil exports have dropped by 40% for the month to around 920k BPD. Separately, Lukoil have agreed to reach the OPEC+ targets in April, and Rosneft’s VP state that they fully comply with the pact. Gold is weaker as the USD moves higher recouping recent losses, with the yellow metal hitting a two-week low and currently trading around USD 1306/oz. Elsewhere, copper weakened following China printing a 3rd month of contraction in their Caixin Manufacturing PMI, although the metal did recover as the figure was above expectations and risk sentiment remained positive. Separately, Goldman Sachs trade ideas include Long Dec’19 copper vs. Dec’19 zinc, Long jun’19 and short June’20 aluminium.

Today’s expected data include personal income and spending, as well as manufacturing PMIs. Foot Locker and Onex are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.6% to 2,802.00

- STOXX Europe 600 up 0.8% to 375.62

- MXAP up 0.2% to 159.00

- MXAPJ up 0.4% to 524.20

- Nikkei up 1% to 21,602.69

- Topix up 0.5% to 1,615.72

- Hang Seng Index up 0.6% to 28,812.17

- Shanghai Composite up 1.8% to 2,994.01

- Sensex up 0.7% to 36,108.55

- Australia S&P/ASX 200 up 0.4% to 6,192.73

- Kospi down 1.8% to 2,195.44

- German 10Y yield rose 0.4 bps to 0.187%

- Euro down 0.1% to $1.1360

- Italian 10Y yield fell 3.2 bps to 2.393%

- Spanish 10Y yield rose 0.3 bps to 1.176%

- Brent futures up 0.3% to $66.51/bbl

- Gold spot down 0.5% to $1,306.59

- U.S. Dollar Index up 0.2% to 96.34

Top Overnight News from Bloomberg

- U.S. officials are preparing a final trade deal that President Donald Trump and his Chinese counterpart Xi Jinping could sign in weeks, people familiar with the matter said. The U.S. is eyeing a summit between the two presidents as soon as mid-March, said one of the people, who spoke on condition of anonymity because the preparations are confidential

- Federal Reserve Chairman Jerome Powell repeated the central bank’s recent mantra of pledging patience in the face of conflicting economic signals and subdued inflation. signals and subdued inflation. “The Federal Open Market Committee will be patient as we determine what future adjustments to the target range for the federal funds rate may be appropriate to support our dual-mandate objectives,” Powell said in the text of a speech Thursday evening in New York

- Federal Reserve Bank of Dallas President Robert Kaplan says “global growth is decelerating” and due to potential spillovers from this headwind and other sources of uncertainty, he has been advocating that “we should pause and be patient” on monetary policy.

- MSCI Inc. will expand the weighting of China-listed shares in benchmark indexes tracked by global investors, a decision that could see billions of dollars flow into one of the world’s most volatile major stock markets

- Oil was poised to eke out a third weekly gain after Saudi Arabia defied U.S. President Donald Trump’s call for lower prices, and a drop in American crude inventories signaled supplies are tightening.

- North Korean leader Kim Jong Un vowed to meet again with President Donald Trump to continue nuclear negotiations after a two-day summit between the leaders collapsed Thursday amid discord over sanctions and conflicting accounts of Pyongyang’s demands

- Bank of England Governor Mark Carney says the drop in business investment due to Brexit uncertainty will hamper the U.K. economy

- Underlying price pressures in the euro area remain weak, according to the latest inflation figures for the region, giving European Central Bank policy makers more to digest ahead of their crucial meeting next week

Asian equities started the first trading day of the month on an optimistic note, despite a relatively downbeat session on Wall Street where the three main indices closed lower by around three-tenths of a percent. The Dow was weighed on by UnitedHealth shares which trimmed around 50 points off the index, meanwhile Nasdaq was pressured as heavyweights Facebook, Apple and Netflix all fell over 0.5%. In terms of February performance, Dow rose 3.7%, S&P gained 3.0% and Nasdaq advanced 3.4% in the month. ASX 200 (+0.4%) extended on opening gains as IT and healthcare names led the advances, whilst heavy-exporter Nikkei 225 (+1.0%) outperformed on the back of a weaker domestic currency. Elsewhere, Shanghai Comp (+1.8%) was choppy as the third straight month of contraction in China’s manufacturing sector capped upside in the index, despite MSCI quadrupling China A-share weightings in global benchmarks to 20%. Goldman Sachs estimates that the MSCI move would lead to a potential USD 70bln net buying in A-shares, skewed towards the healthcare and consumer sectors. Finally, Hang Seng (+0.6%) edged higher during the session as the index felt support from its heavy-weight financial and energy sectors.

Top Asian News

- Hong Kong Dollar Near Weak End of Band Raises Tightening Risk

- New Philippines Central Bank Chief Eyed by Dominguez This Month

- Carlyle Buys Stake in Indian Life Insurer From BNP Paribas

Major European equities are in the green [Euro Stoxx 50 +0.7%], as markets follow from the positive risk sentiment seen overnight in Asia. Dax (+1.0%) is the outperforming index with all components in the green on the positive risk sentiment following concerns over China’s economy being somewhat alleviated after Chinese Caixin manufacturing PMI came in stronger than expected; as such the Auto sector is outperforming its peers. Other notable movers include Rheinmetall (+7.3%) leading the Stoxx 600 after the Co’s FY18 revenue was in-line with expectations. WPP (+8.2%) are also firmly in the green in-spite of the Co’s outlook for 2019 being rather downbeat, particularly regarding the first half, as they reported results that marginally beat on expectations. Elsewhere, Man Group (-4.2%) are towards the bottom of the Stoxx 600 after stating that their funds under management fell in 2018.

Top European News

- Italy’s Di Maio Trusts Salvini to Stand by Him for Long Term

- Deficit Conquered, Germany Is Finally Boosting Public Spending

- WPP Dodges Another Results Shock After Year of Client Losses

- Jupiter Rises Most in Five Years as Payout Beats Expectations

In FX, although the Dollar has pared some of its post-GDP and Chicago PMI gains vs certain major counterparts, the index has rebounded further from sub-96.000 lows towards 96.400, largely at the expense of safe-haven currencies, and especially the Jpy.

- JPY – No respite for the Yen after yesterday’s slide through 111.00 and accelerated losses below the 200 DMA as US Treasury yields continue to rally and the 10 year benchmark clears 2.70% in wake of the aforementioned stronger than forecast data and survey news. Usd/Jpy is now just a whisker away from the next big figure where more offers are touted, and with key Fib resistance residing not far above at 112.08.

- CHF/GBP – Also victims of the broad Greenback revival, but the former unwinding more of its safe-haven premium as well, with the Franc back under parity vs the Buck and below 1.1350 against the Euro. Meanwhile, Cable’s pull-back from recent Brexit no deal highs has extended to 100+ pips and not far from Fib support around 1.3215, with little reaction or independent direction gleaned from a bang in line with consensus UK manufacturing PMI.

- EUR – The single currency has pulled back further from best levels too (1.1400+), but holding up relatively well amidst mixed Eurozone data and perhaps with the aid of hefty option expiry interest at the 1.1350 level for today’s NY cut (2 bn) plus M&A news that has lifted Eur/Jpy very close to a key Fib. On that note, the 30 DMA in Eur/Usd at 1.1363 could also be influential on a closing basis along with 0.8593 in Eur/Gbp.

- CAD/NZD/AUD – All on a firmer footing vs their US peer, and particularly the Loonie that has rebounded strongly from sub-1.3200 lows on Thursday ahead of Canadian GDP data and gleaning some traction from steadier oil prices. Usd/Cad is currently near the bottom of a 1.3132-77 range, and a big option expiry between 1.3140-50 may also have a bearing on trade given 1.4 bn rolling off later today. Meanwhile, the Kiwi and Aussie have both managed to regain composure and round number status after falling below 0.6800 and 0.7100, with some comfort drawn from the overnight Caixin Chinese manufacturing PMI that was sub-50 again, but not as weak as the official version.

In commodities, Brent (U/C) and WTI (+0.1%) prices are essentially flat, in-spite of trading positively overnight and initially during the European session, although they are once again trading within a fairly narrow range of less than USD 2/barrel. Elsewhere, since the imposition of US sanctions on the 28th January on Venezuelan oil, Venezuela’s oil exports have dropped by 40% for the month to around 920k BPD. Separately, Lukoil have agreed to reach the OPEC+ targets in April, and Rosneft’s VP state that they fully comply with the pact. Gold (-0.3%) is weaker as the USD moves higher recouping recent losses, with the yellow metal hitting a two-week low and currently trading around USD 1306/oz; however, analysts do highlight that the metal has strong support at the USD 1300/oz level. Elsewhere, copper weakened following China printing a 3rd month of contraction in their Caixin Manufacturing PMI, although the metal did recover as the figure was above expectations and risk sentiment remained positive. Separately, Goldman Sachs trade ideas include Long Dec’19 copper vs. Dec’19 zinc, Long jun’19 and short June’20 aluminium.

Looking at the day ahead, the big highlight in the US today meanwhile is the December PCE report which is expected to show a +0.2% mom core reading (+1.9% yoy and unchanged versus November). We’ll also get the December personal income and spending reports, January manufacturing PMI and February ISM manufacturing – the latter of which is expected to fall just under 1pt to 55.7. The final revisions to the February University of Michigan consumer sentiment survey round out the data. Away from all that, it’s the turn of the Fed’s Bostic to speak this evening.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%; Personal Spending, est. -0.3%, prior 0.4%

- 8:30am: Real Personal Spending, est. -0.3%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.0%, prior 0.1%; PCE Deflator YoY, est. 1.7%, prior 1.8%

- 8:30am: PCE Core MoM, est. 0.2%, prior 0.1%; PCE Core YoY, est. 1.9%, prior 1.9%

- 9:45am: Markit US Manufacturing PMI, est. 53.7, prior 53.7

- 10am: ISM Manufacturing, est. 55.8, prior 56.6

- 10am: U. of Mich. Sentiment, est. 95.9, prior 95.5; Current Conditions, prior 110; Expectations, prior 86.2

DB’s Jim Reid concludes the overnight wrap

With it being the first day of March, this morning Craig was up in the middle of the night publishing the February performance review as a standalone document which you should see in your inbox an hour or so before this one. You’ll find the usual charts and tables in that document too which will help show that it’s actually been one of the better starts to a year on record.

Overnight we’ve already seen China’s Caixin February manufacturing PMI. It came in at 49.9 (vs. 48.5 expected), marking the third consecutive month below 50 but obviously showing some signs of improving. Sub-index level details were more mixed with new orders returning above 50 (at 50.2) after 2 months below while new export orders slipped back ( at 49.4 vs. 50.4 last month). The accompanying statement from Markit with the release stated that the domestic manufacturing demand improved significantly in February while foreign demand was not deteriorating as quickly as last year. However, we need to be cautious on over interpreting domestic demand in February as the significant improvement could be on the back of higher spending on account of Lunar New Year holidays. Nevertheless some signs of green shots. Elsewhere, Japan’s final February manufacturing PMI came +0.4pts above the preliminary read at 48.9 (vs. 50.3 last month). In other news, MSCI has said that it will expand the weighting of China-listed shares in its benchmark indexes which is helping sentiment there.

Geo-political tensions are also showing signs of de-escalation as the week closes with Pakistan’s PM Imran Khan saying yesterday that he will return the captured Indian pilot back to India today while overnight, North Korea’s Kim Jong Un said that he will meet again with President Donald Trump to continue nuclear negotiations after a two-day summit between the leaders collapsed yesterday and expressed appreciation for Trump’s “active efforts toward results” and called the summit talks “productive.”

The better than expected China’s PMI, China’s MSCI news and de-escalation of geo-political risks has helped sentiment overnight with markets in Asia trading largely up with the Nikkei (+1.13%), Hang Seng (+0.31%) and Shanghai Comp (+0.21%) advancing while the Kospi (-1.76%) is down after the disappointing end to the summit yesterday. Elsewhere, futures on the S&P 500 are up +0.40% and the Japanese yen is weak (-0.30%) this morning.

As we start a new month, markets will do well to match the heady gains of the last two months however the last day of February proved to be a bit of a damp squib for risk assets. That being said, it’s bond markets that continue to remain (relatively speaking) lively with yields finally deciding to move against zero’s gravitational pull in the last 48 hours. Better than expected Q4 GDP and Chicago PMI readings in the US – more on those below – was as good an excuse as any yesterday and it helped Bunds (+3.5bps) climb to 0.183% and the highest since 30 January. Treasuries were also up as much as +7.2bps from the intraday lows at one stage and ultimately finished +3.6bps on the day at 2.719%. Amazingly, despite all the excitement of the last two days, on an intra-day basis the range for Treasuries in February was just 11.6bps and we’d completed that by February 5th. If we look at the period since then, the range is just 9.3bps. So it wasn’t exactly the most exciting month for Treasuries despite the mini tantrum in the last couple of days.

By contrast, there was some divergence across risk assets yesterday. The various geopolitical noise hasn’t helped sentiment this week, including talks between Trump and Kim Jong Un being cut short in Hanoi. This was offset to some degree by the more upbeat trade comments from Kudlow and Mnuchin. The S&P 500 ended -0.28%, and traded in an intraday range of just 40bps, its tightest range since last September. The STOXX 600 finished +0.06%, while there were outsized gains for the IBEX (+0.72%) and FTSE MIB (+0.78%). Banks appeared to play a role in that, with European Banks as a sector up +2.01% reflecting the bond move and Spanish and Italian Banks up +1.86% and +2.12%. Meanwhile, HY credit spreads were -4bps and -3bps tighter in the US and Europe. The euro traded close to flat versus the dollar at 1.1374, capping its narrowest three month stretch ever, with a range of just 2.9% over that period.

Back to that data yesterday, Q4 GDP in the US printed at a better-than-expected +2.6% qoq saar (vs. +2.2% expected). The breakdown was equally supportive with private domestic demand up +3.1% and consumer spending reasonable following concerns post the odd December retail sales report. Trade also subtracted less than expected from the overall headline number. Core PCE prices rose at an annualized pace of 1.7% on the quarter, a touch above expectations, which presents some upside risks to today’s December print. As for the Chicago PMI, the February reading jumped a whopping 8pts to 64.7 and far exceeded expectations for a more moderate 57.5. That is the highest reading since December 2017 and like the GDP report, the details also made for pleasant reading with new orders up over 15pts and production over 8pts higher. As you’ll see in the day ahead at the end, we’ve got the ISM manufacturing reading today which is expected to fall slightly from 56.6 to 55.8 however recent regional surveys perhaps indicate some upside risk to the headline reading now, since the Chicago, Dallas, Empire, and Richmond prints all moved higher this month, leaving the weak Philly print as an outlier.

The other data of note in the US yesterday was the latest weekly initial jobless claims print, which rose 8k and a bit more than expected to 225k. That said, the four-week average has dropped for two consecutive weeks now to 229k. As for the data in Europe, it was a busy day for inflation releases. In a nutshell, Germany (+0.5% mom vs. +0.6% expected) and France (+0.1% mom vs. +0.3% expected) missed, Spain (+0.2% mom vs. +0.1% expected) beat and Italy (-0.2% mom) was in line. Today we’ve got the broader Euro Area reading with the consensus pegged at an unchanged +1.1% yoy for the core reading. Our economists had expected it to also come in at a weak +1.1% yoy however yesterday’s country level data likely puts the risk at that coming in below market.

Turning to Fedspeak, where the most interesting comments were from Vice Chair Clarida, who noted that “market-based measures of inflation compensation have moved lower, on net, since last summer, though they have increased some recently.” This suggests that Clarida wants to see higher inflation pricing before endorsing another rate hike, which is the rationale behind one of our rates strategists’ favorite trades of being long US breakevens. The rest of Clarida’s comments conformed to recent FOMC rhetoric emphasizing patience and data dependence as a response to financial market volatility and slower global growth. Elsewhere, Philadelphia Fed President Harker reiterated his preference for one hike each this year and next. That was likely also his view as of December, so his stasis suggests reduced scope for the dots to fall at the March FOMC meeting.

Finally to the day ahead, which kicks off this morning with January retail sales data in Germany before all eyes turn to the final revisions of the February manufacturing PMIs. For what it’s worth, no change in the Euro Area reading of 49.2 is expected, while the same applies for Germany and France at 47.6 and 51.4, respectively. Italy and Spain are expected to fall slightly to 47.2 and 51.7, respectively. Away from that this morning we also get February employment data in Germany and January money and credit aggregates data in the UK, as well as the advanced February CPI reading for the Euro Area as mentioned above. The big highlight in the US today meanwhile is the December PCE report which is expected to show a +0.2% mom core reading (+1.9% yoy and unchanged versus November). We’ll also get the December personal income and spending reports, January manufacturing PMI and February ISM manufacturing – the latter of which is expected to fall just under 1pt to 55.7. The final revisions to the February University of Michigan consumer sentiment survey round out the data. Away from all that, it’s the turn of the Fed’s Bostic to speak this evening.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 53.05 POINTS OR 1.80% //Hang Sang CLOSED UP 178.99 POINTS OR 0.63% /The Nikkei closed UP 217.53 POINTS OR 1/62%/ Australia’s all ordinaires CLOSED UP 0.34%

/Chinese yuan (ONSHORE) closed UP at 6.7053 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 57.39 dollars per barrel for WTI and 66.33 for Brent. Stocks in Europe OPENED RED//.

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7053 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7058: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/

China’s shadow debt business has finally hit a roadblock

(courtesy zerohedge)

“There’s No Money” – Has China’s Shadow-Debt Reckoning Finally Arrived?

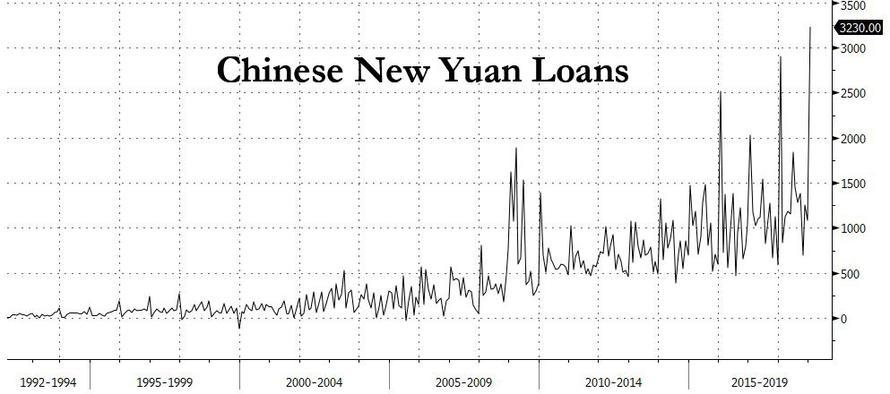

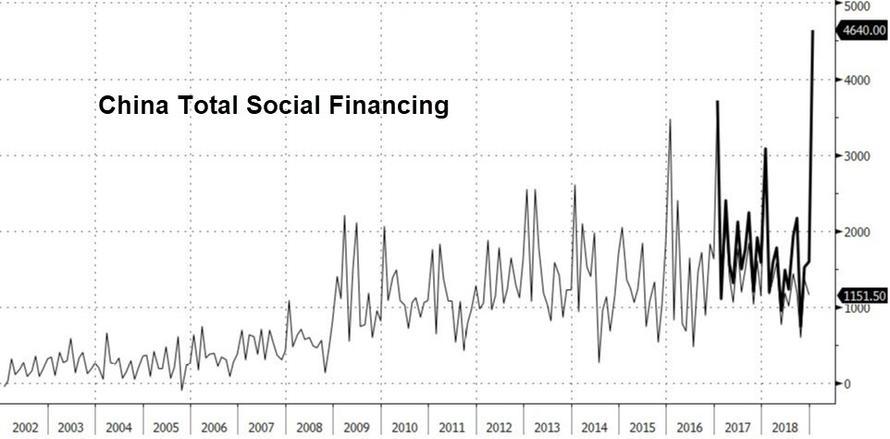

Months before Beijing abandoned its deleveraging plans and approved a gargantuan 4.64 trillion yuan credit injection (including the “shadow” credit that the government had vowed to curb) – which, as we pointed out at the time, resembled the January 2016 “Shanghai Accord” intervention (when Beijing famously intervened to stop global stock markets from careening off a cliff) – a team of S&P credit analysts warned in an October report that China’s debt burden might be much larger than previously believed.

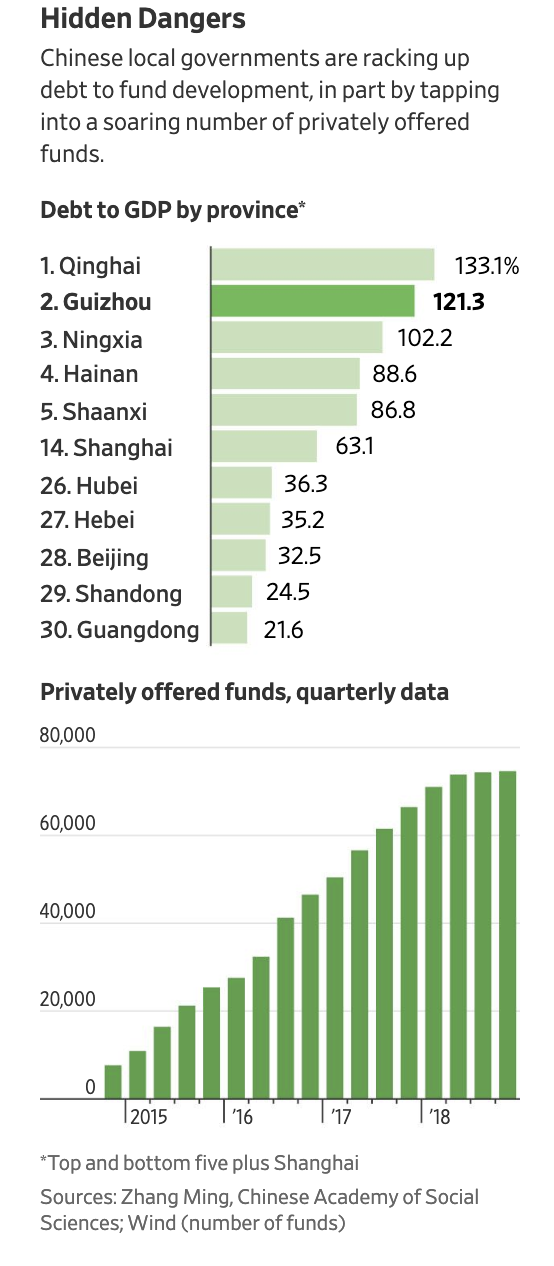

Against a backdrop of soaring corporate defaults, the team from S&P warned that investors could safely tack on another ~40% of debt/GDP to China’s total (with even more likely hidden from view) after a careful analysis of a new source of shadow debt being tapped by local governments to further their development plans. These Local Government Financing Vehicles, or LGFVs, represented “an iceberg with titanic credit risks” as local officials had increasingly turned to these sources of shadow financing to finance development projects while bureaucrats in Beijing struggled to turn off the credit taps.

Now that Beijing has reckoned with the idea that now is not the time to try and contain the country’s massive debt load, even as the percentage of bad debt balloons, it increasingly appears that these measures might be too little, too late for investors who financed these LGFVs,as the Wall Street Journal revealed in a report about how a local government in China’s impoverished Southern had caused a stir by stiffing its creditors after racking up a debt pile – largely through these LGFVs – equivalent to roughly three times the government’s annual revenue.

When a group of wealthy investors traveled to Sanhe to confront the local government, they were swiftly rebuffed, leaving them little recourse to recover their money.

Meanwhile, many of the buildings that their money helped to finance stood half-finished.

A building splurge in this impoverished pocket of rural China ended in half-finished projects and a trail of angry investors from some of the country’s wealthiest areas.

On a recent winter workday, investors and representatives from private fund companies in Shanghai and elsewhere descended on Sandu,a county in the deep south where tens of thousands of locals live on less than a dollar a day. After taxi rides from the high-speed rail station that took them past incomplete buildings and a gigantic golden statue of a man on horseback, they sat in government offices, demanding repayment.

“We sympathize with you investors,” Jian Shiwei, deputy general manager of a Sandu government-backed investment company that borrowed hundreds of millions of yuan to develop the area. “But there’s no money right now.”

Though it might be tempting to chalk this up to the mismanagement of Sanhe’s local officials, WSJ claimed that situations like this are playing out in rural areas across China.

The standoff in Sandu is a microcosm of China’s mounting debt problem. Across the country, local governments and their more than 2,000 financing companies have run up trillions of dollars of debt to borrow and build their way to prosperity, tapping into ready financing from well-off investors chasing higher returns. Now the bills are coming due, and China’s slowing economy, curbs by Beijing on risky financing—and the massive scale of borrowing—are plaguing repayment and leaving some investors in limbo.

After the confrontation with investors and just before this month’s Lunar New Year holiday, Sandu hustled out interest payments for some overdue obligations. Still, investors and brokers estimate that the government and its companies will need to deliver two billion yuan ($297.6 million) more in payments this year, nearly three times Sandu’s annual revenue.

Many regional governments are already struggling with debt piles in excess of 100% debt-to-GDP, and that’s before factoring in the shadow financing sources.

And it’s not just wealthy Chinese fund managers who are being left in the lurch; many residents opted to invest in these vehicles after being seduced with high advertised returns – only to see their savings vanish. One investor who spoke with WSJ claimed that the shortfall wasn’t the local government’s fault, but a result of mismanagement and regulatory failures impacting the entire Chinese financial system.

“Sandu has its problems, but we can’t blame it,” said Jiang Xiaqiu, a factory owner and investor who bought 1.6 million yuan of Sandu’s debt via a private fund in Beijing, with an advertised 9% annual return. “It’s the whole financial system and how poorly regulated the private fund industry has been.”

Sandu’s government debt totaled 3.73 billion yuan in 2017, according to official figures. Deputy propaganda chief Wu Maohua declined to comment on what the sum includes; some economists, analysts and experts say it doesn’t cover recent borrowings by government-backed investment companies, including off-the-book borrowing from private funds.

In Sanhe, problems first arose after the local Communist Party chief was removed in a bribery investigation last year. The region missed its first debt payment in September, but has been struggling to make up these payments.

Mr. Wu said the county is working to resolve its debts, pointing to the overdue payments given to some investors. “You can see the government is being very diligent,” he said.

For its borrowing spree, Sandu turned to funds like the one Ms. Jiang invested in. These privately offered funds have mushroomed, with more than 74,000 of them, nearly 10 times the number five years ago. Independent brokers and wealth advisers market the funds to well-off clients. Ms. Jiang said a broker connected her with fund managers.

While putting a number on the amount of shadow debt in the system is difficult due to the opacity of the Chinese financial system, one economist at a domestic think tank estimated that off-balance-sheet borrowings by local governments could be as much as 23.6 trillion yuan,(3.4 TRILLION USA DOLLARS) as of the end of 2017, meaning that total is likely higher today, as governments have been forced to tap these vehicles during Beijing’s deleveraging campaign.

The proliferation of private funds and other money-raising channels for local governments makes it difficult for economists and for Beijing to track the total amount of borrowings.Official figures pegged the sum of local and central government debt at 29.95 trillion yuan ($4.457 trillion) in 2017, roughly 36% of the economy.

[…]

Off-balance-sheet borrowings by local governments are estimated to be nearly just as much, at 23.6 trillion yuan by 2017, according to Zhang Ming, an economist at the Chinese Academy of Social Sciences, a government think tank. When this hidden debt is factored in, he said, total government debt is about 67% of the economy. But the proportion is much higher in some places, such as less-developed areas trying to catch up, and Mr. Zhang’s estimates don’t capture all borrowings, especially those involving private funds outside banking channels.

Fortunately, Beijing’s latest reversal should at least reopen the taps for on-the-books debt, allowing governments to restart some of these projects, and potentially raise money to pay back the LGFVs. But whether this could work as a long-term solution is doubtful, as most see it as just another episode of can-kicking by Beijing, in the absence of real structural reforms.

end

They are talking a final China/USA trade deal but do not buy it.

(courtesy zerohedge)

US Said To Prepare “Final China Trade Deal” But Skeptics Aren’t Buying It

Commenting on the disappointing outcome of Trump’s second Kim summit, UBS’ economist Paul Donovan writes that “the US president (like the rest of us) is subject to the economic problem – limited time, and lots of demand on that time. Time focused on Korea is time that cannot be spent tweeting about trade. The president may want a quick win on trade to offset the Korean situation. There are media reports of a mid-March summit with China and a “quick” trade deal.”

Indeed, at 1:37am ET overnight, Bloomberg reported that U.S. officials are preparing a “final trade deal” that President Trump and Chinese counterpart Xi Jinping could sign in weeks. As Bloomberg further adds, “the U.S. is eyeing a summit between the two presidents as soon as mid-March” although the planning has been complicated by Xi’s need to lead China’s annual National People’s Congress in early March, as well as make other foreign trips.

Naturally, the report goes on to say that Trump will have the final call on the U.S. side, and references what he said in Vietnam when he showed he’s willing to walk away if he doesn’t like the terms on the table, including with China.

“Speaking of China we’re very well on our way to doing something special. But we’ll see,” Trump said at a press conference in Hanoi on Thursday. “I am always prepared to walk. I’m never afraid to walk from a deal, and I would do that with China, too, if it didn’t work out.”