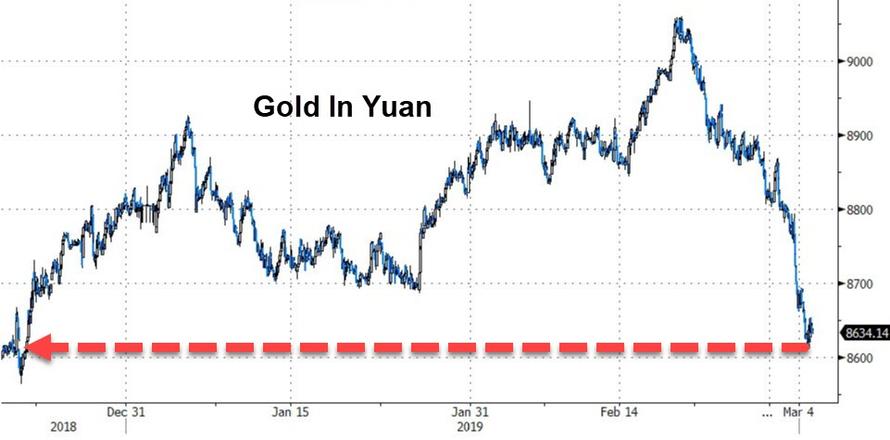

GOLD: $1285.50 DOWN $12.50 (COMEX TO COMEX CLOSING)

Silver: $15.09 DOWN 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1286.60

silver: $15.08

GOLD/SILVER EQUITY SHARES HELD TODAY SO MAYBE WE HIT THE BOTTOM OF THIS CONTINUAL RAID CYCLE.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 52 NOTICE(S) FOR 5200 OZ (0.1617 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 244 NOTICES FOR 24400 OZ (.7589 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

351 NOTICE(S) FILED TODAY FOR 1,755,000 OZ/

total number of notices filed so far this month: 4220 for 21,100,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3794:DOWN $95

Bitcoin: FINAL EVENING TRADE: $3769 D0WN 94

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/52

first time in two months

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,296.400000000 USD

INTENT DATE: 03/01/2019 DELIVERY DATE: 03/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 36

690 C ABN AMRO 23 2

737 C ADVANTAGE 14 9

800 C MAREX SPEC 14 3

878 C PHILLIP CAPITAL 1

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 52 52

MONTH TO DATE: 244

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 1641 CONTRACTS FROM 196,641 DOWN TO 195,000 WITH FRIDAY’S 38 CENTS LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 4964 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 4964 CONTRACTS. WITH THE TRANSFER OF 4964 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 14964 EFP CONTRACTS TRANSLATES INTO 24.82 MILLION OZ ACCOMPANYING:

1.THE 38 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 24.535 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

6760 CONTRACTS (FOR 2 TRADING DAYS TOTAL 6760 CONTRACTS) OR 33.800 MILLION OZ: (AVERAGE PER DAY: 3380 CONTRACTS OR 16.90 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 33.800 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.820% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 398.66 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1690 WITH THE 38 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD VERY STRONG SIZED EFP ISSUANCE OF 4964 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 3274 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4964 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1641 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 38 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.23 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.975 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 351 NOTICE(S) FOR 1,755,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 24.535 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUMONGOUS SIZED 14,721 CONTRACTS DOWN TO 475,158 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $16.90//FRIDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 11,397 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 11,397 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 475,158. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE ONLY A TINY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3324 CONTRACTS: 14,721 OI CONTRACTS DECREASED AT THE COMEX AND 11,397 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF ONLY 3324 CONTRACTS OR 332,400 = 10.34 TONNES. IT IS IMPORTANT TO NOTE THAT ALTHOUGH WE HAD A CONSIDERABLE DROP IN OPEN INTEREST AT THE COMEX, MANY DID NOT LEAVE THE GOLD ARENA..THEY JUST MORPHED INTO LONDON BASED FORWARDS. ON FRIDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $16.90.

FRIDAY, WE HAD 11,192 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 22,589 CONTRACTS OR 2,258,900 OZ OR 70.26 TONNES (2 TRADING DAYS AND THUS AVERAGING: 11,295 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 70.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 70.26/2550 x 100% TONNES = 2.75% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 945.82 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 14,721 WITH THE LOSS IN PRICING ($16.90) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11397 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,397 EFP CONTRACTS ISSUED, WE HAD A SMALL LOSS OF 3824 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,397 CONTRACTS MOVE TO LONDON AND 14,721 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE SMALL LOSS IN TOTAL OI EQUATES TO 10.34 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $16.90 IN FRIDAY’S TRADING AT THE COMEX

we had: 52 notice(s) filed upon for 5200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $12.50 TODAY

ON FRIDAY I REPORTED:

“HUGE CHANGES IN INVENTORY AT THE GLD: AS EXPECTED AS THIS GOLD WAS PROBABLY USED IN THE RAID THESE PAST FEW DAYS;

A WITHDRAWAL OF 4.11 TONNES

/GLD INVENTORY 784.22 TONNES

Inventory rests tonight: 784.22 tonnes.””

WELL THE CROOKS WERE AT IT AGAIN, AS THEY RAIDED THE COOKIE JAR BIG TIME AGAIN TODAY TO THE TUNE OF: 11.76 TONNES

THUS A WITHDRAWAL OF 11.76 TONNES

GLD INVENTORY 772.46 TONES

INVENTORY RESTS AT 772.46 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS IN PRICE TODAY:

A SMALL CHANGE IN SILVER INVENTORY AT THE SLV..///

A WITHDRAWAL OF 871,000 OZ FROM THE SLV INVENTORY

/INVENTORY RESTS AT 308,503 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 1641 CONTRACTS from 196,686 DOWN TO 195,000 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 4964 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4964 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1641 CONTRACTS TO THE 4964 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE SURPRISINGLY OBTAIN A STRONG GAIN OF 3323 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.61 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 24.535 MILLION OZ FOR MARCH.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 38 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 4964 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

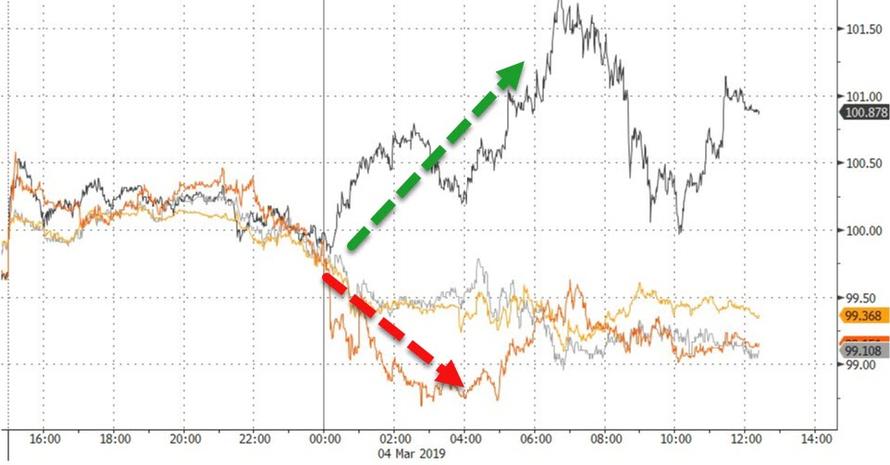

SHANGHAI CLOSED UP 33.57 POINTS OR 1.12% //Hang Sang CLOSED UP 147.42 POINTS OR 0.51% /The Nikkei closed UP 219.35 POINTS OR 1.02%/ Australia’s all ordinaires CLOSED UP 0.46%

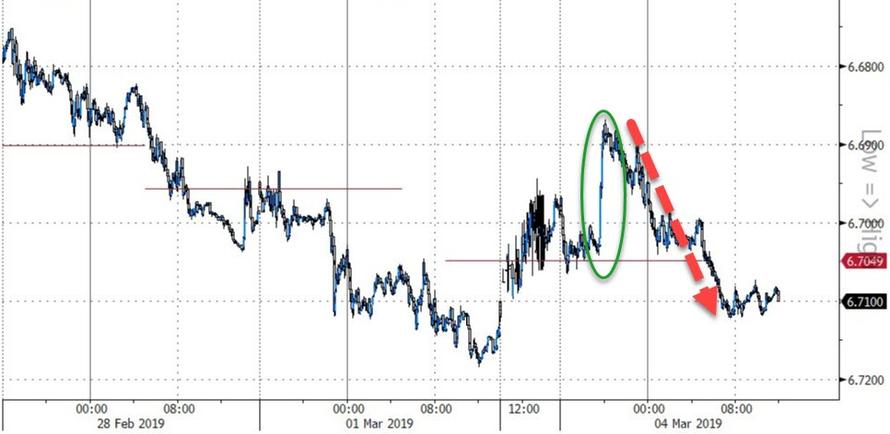

/Chinese yuan (ONSHORE) closed UP at 6.7018 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.09 dollars per barrel for WTI and 65.50 for Brent. Stocks in Europe OPENED GREEN EXCEPT SPAIN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7018 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7025: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

The battle over Huawei is getting fierce. Now Huawei fights back and sues the uSA government in a Texas court over equipment ban

( zerohedge)

ib)Getting quite nasty: Beijing threatens jailed Canadians with espionage charges in the latest retaliation for sending the Huawei case forward, i.e. the extradition of Meng

( zerohedge)

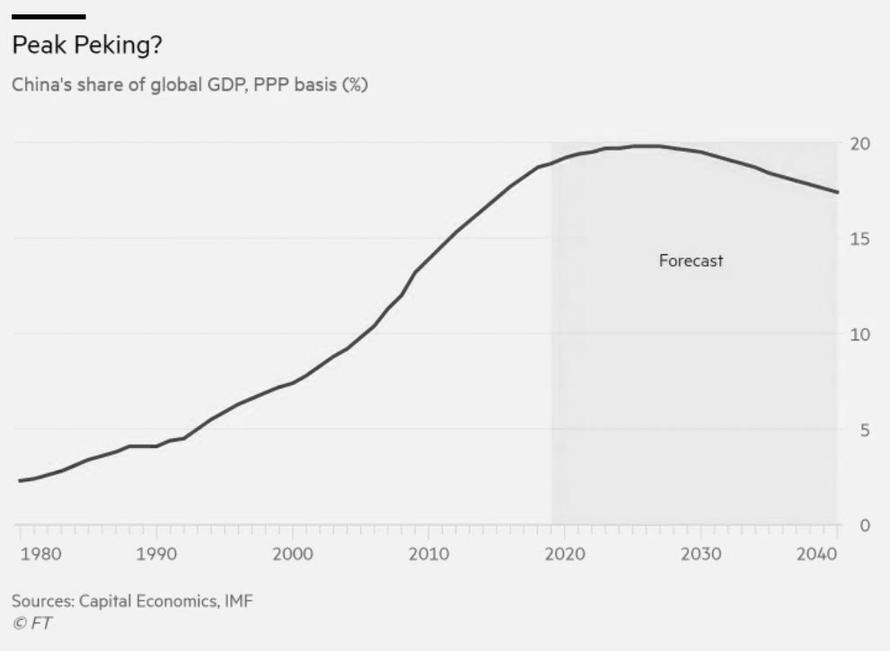

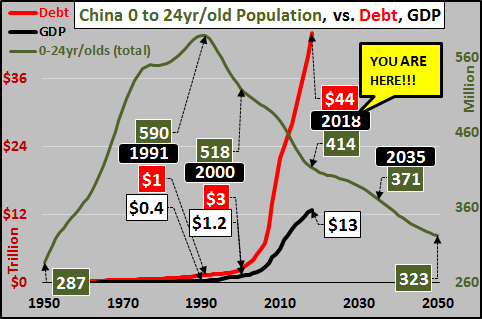

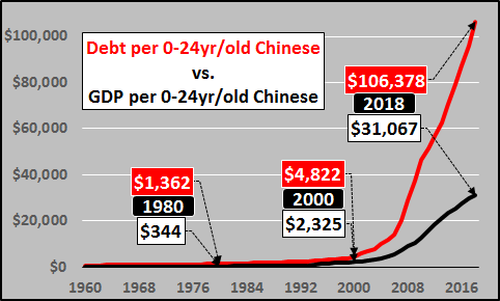

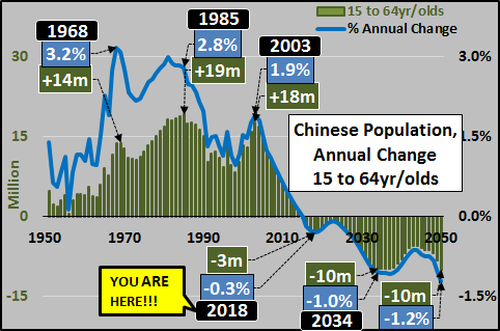

ii)The following is a very important article on how demographics are starting to eat into China’s economy. As the debt rises, the population shrinks and thus greater debt per GDP. Also the shortage of labour is causing costs to rise further hurting their economy

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

A good look at the chaos in Great Britain

( Meijer/Alexander Aston)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

Sweden

Rosengard, a notorious neighbourhood in Malmo Sweden mostly populated by Muslim migrants now have UPS drivers halting deliveries because of attacks on their trucks.

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

Guaido is set to re enter Venezuela today..if harmed the USA threatens actions. Russia and China support Maduro…good reason for gold to be hit today.

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)Par for the course: Australian central bank feeds legislators disinformation about gold/how it is stored/leased etc

( Ronan Manly/Bullionstar/gata)

ii)Barrick has now chance of taking over Newmont..they (Barrick) are a bunch of crooks

( Bloomberg/GATA)

iv)Our good friend; Hugo..Salinas Price

(courtesy Hugo..)

v)Bill Murphy is exactly correct that fundamentals are meaningless in gold.

(GATA/Goldseek/

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

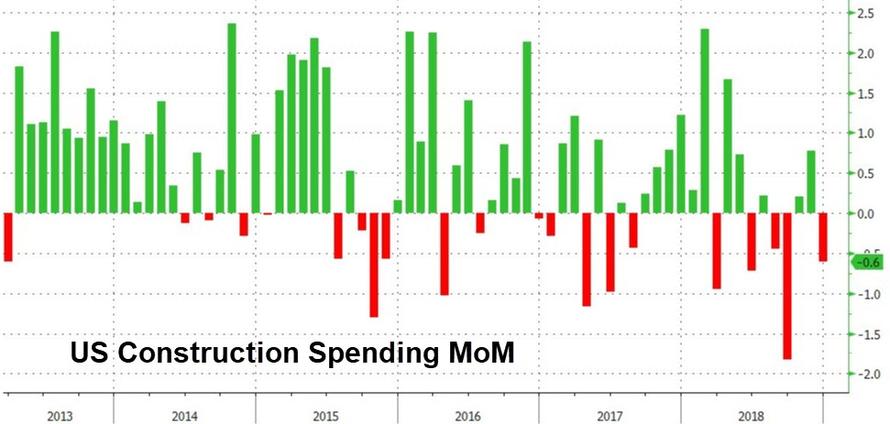

Early trading as the Dow dumps because of poor construction numbers

(courtesy/ZEROHEDGE)

ii)Market data

USA construction spending tumbles to eight year lows as today’s drop was .6% month/over..pretty large..the USA economy is crumbling

( zerohedge)

iv)SWAMP STORIES

The idiot Nadler is now ready to hit over 60 people with document requests. His main contention is that Trump obstructed justice which he did not:

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL RISES TO 772 CONTRACTS FOR A GAIN OF 1 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 1732 CONTRACTS DOWN TO 145,179 CONTRACTS.

i) out of HSBC: 44,944.828 oz

Gold Still o

Barrick chief Bristow rules out higher offer for Newmont

Submitted by cpowell on Fri, 2019-03-01 15:08. Section: Daily Dispatches

By Henny Sanderson

Financial Times, London

Friday, March 1, 2019

Barrick Gold’s boss Mark Bristow has ruled out increasing his offer for arch-rival Newmont Mining.

Mr. Bristow told the Financial Times that the $18 billion nil-premium, all-stock offer for Newmont was “logical” and would combine multiple world-class gold mines into one company.

Asked if Barrick would increase its offer for Newmont, Mr. Bristow said no.

…

What’s better than five world-class assets? Eight,” Mr. Bristow said. “We can demonstrate that it’s so logical. …” Synergies “are about whether you put two things together is better or worse. And it’s far better.”

Mr. Bristow has to convince a small group of investors who have shareholdings in both companies that the deal makes more sense than Newmont’s planned $10 billion acquisition of Vancouver-based Goldcorp, which was announced in January. …

… For the remainder of the report:

https://www.ft.com/content/2cc619d6-3c23-11e9-b72b-2c7f526ca5d0

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Par for the course: Australian central bank feeds legislators disinformation about gold/how it is stored/leased etc

(courtesy Ronan Manly/Bullionstar/gata)

Ronan Manly: Australian central bank feeds legislators disinformation about gold

Submitted by cpowell on Sat, 2019-03-02 02:43. Section: Daily Dispatches

9:43p ET Friday, March 1, 2019

Dear Friend of GATA and Gold:

Bullion Star gold analyst Ronan Manly tonight details how this week’s exchange between Australian legislators and central bankers about the country’s gold reserves was almost completely disinformation, inaccurate and misleading, never really getting to the point about what really has been done with the country’s gold.

Manly’s painstaking analysis is headlined “RBA Bosses Squirm as Aussie Politicians Throw Easy Questions about RBA Gold in London” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/rba-bosses-squirm-as-aussi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Our good friend; Hugo..

(courtesy Hugo..)

Hugo Salinas Price: The gold gambling casino

Submitted by cpowell on Sat, 2019-03-02 15:59. Section: Daily Dispatches

11a ET Saturday, March 2, 2019

Dear Friend of GATA and Gold:

Hugo Salinas Price, president of the Mexican Civic Association for Silver, writes this week that governments manipulate the gold market so much that speculators are unlikely ever to make a profit from buying and selling assets that constitute only “paper” gold.

The only promising way of coming out ahead with gold, Salinas Price writes, is to buy and hold metal for the long term.

His analysis is headlined “The Gold Gambling Casino” and it’s posted at the association’s internet site here:

http://plata.com.mx/enUS/More/371?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

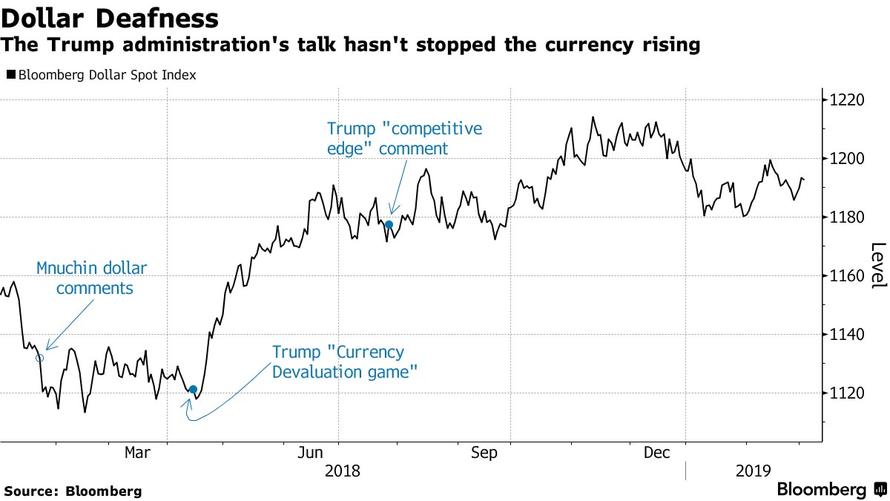

Zero hedge also discusses this in detail as Trump states that the dollar is too strong

(courtesy Bloomberg/GATA)

Trump says dollar too strong, swipes at Fed for rate hikes

Submitted by cpowell on Sun, 2019-03-03 02:56. Section: Daily Dispatches

By Alyza Sebenius

Bloomberg News

Saturday, March 2, 2019

President Donald Trump said today that the U.S. dollar is too strong, and took a swipe at Federal Reserve Chairman Jerome Powell as someone who “likes raising interest rates.”

The U.S. economy is doing well in spite of the actions of the central bank, Trump said during a wide-ranging speech at the Conservative Political Action Conference in National Harbor, Maryland.

“I want a strong dollar but I want a dollar that does great for our country, not a dollar that’s so strong that it makes it prohibitive for us to do business with other nations and take their business,” Trump said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-02/trump-says-dollar-too.

end

In expensive stores, the 1000 Swiss Franc note is now getting a new look for big purchases.

(courtesy Bloomberg/GATA)

Switzerland’s controversial thousand-franc note is getting a new look

Submitted by cpowell on Sun, 2019-03-03 16:30. Section: Daily Dispatches

By Catherine Bosley

Bloomberg News

Sunday, March 3, 2019

At jeweller Les Millionnaires, tucked away in the historic old town of Zurich, being handed a 1,000-franc bill ($1,002) to settle a purchase is no unusual event.

“It’s quite frequent that we’ve got someone who comes in looking for a present and who pays in cash because they don’t want their partner to find out,” said one of the proprietors of the shop, which sells earrings, necklaces, and bracelets made of gold with precious stones. “It’s the surprise effect.”

True to Switzerland’s penchant for discretion — one reason cash has remained popular in the generally tech-savvy country even as its use is dwindling elsewhere — she declines to give her name. “Here in our shop, we do get thousand-franc notes when it’s a very big purchase.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-03/switzerland-s-controv…

end

Bill Murphy is exactly correct that fundamentals are meaningless in gold.

a good interview

(GATA/Goldseek/)

Fundamentals are meaningless in gold, GATA chairman tells GoldSeek Radio

Submitted by cpowell on Sun, 2019-03-03 05:41. Section: Daily Dispatches

12:40p ET Sunday, March 4, 2019

Dear Friend of GATA and Gold:

Interviewed by GoldSeek Radio’s Chris Waltzek, GATA Chairman Bill Murphy says supply-and-demand fundamentals mean nothing in the gold market compared to the machinations of the gold cartel, but the gold price will fly when the cartel exhausts the metal it needs for price suppression.

Murphy adds that the seeming short supply of palladium may be foreshadowing what will happen in gold and silver.

The interview is 10 minutes long and begins at the 28-minute mark here:

http://radio.goldseek.com/shows/2019/03.01.2019/GSR-03.01.19-c.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7018/

//OFFSHORE YUAN: 6.7025 /shanghai bourse CLOSED UP 33.57 POINTS OR 1.12% /

HANG SANG CLOSED UP 147.42 POINTS OR 0.51%

2. Nikkei closed UP 219.35 POINTS OR 1.02%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 96.68/Euro FALLS TO 1.1331

3b Japan 10 year bond yield: RISES TO. –.00/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.86/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.09 and Brent: 65.50

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.17%/Italian 10 yr bond yield UP to 2.77% /SPAIN 10 YR BOND YIELD UP TO 1.20%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.67

3k Gold at $1288.80.40 silver at:15.19 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 15/100 in roubles/dollar) 65.77

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.86 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0012 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1350 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.17%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

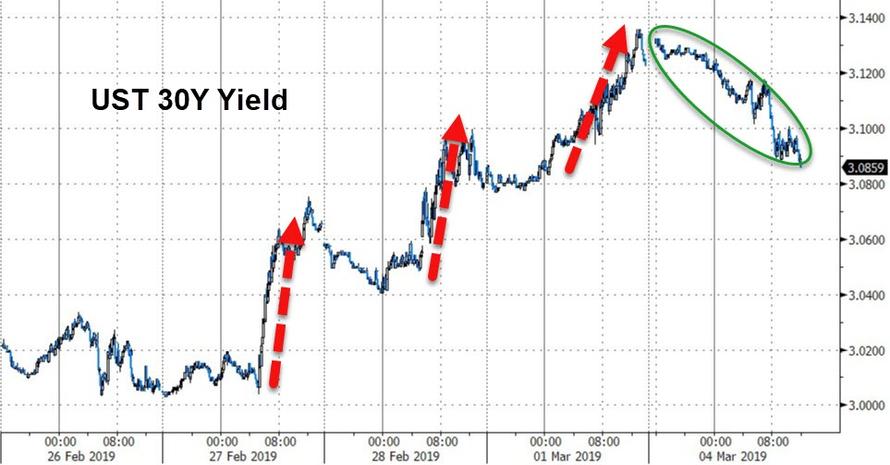

4. USA 10 year treasury bond at 2.74% early this morning. Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3853

Groundhog Day As Markets Rise On “Trade Talk Optimism”; Dollar Jumps Despite Trump Threat

It’s groundhog day again as global markets and US equity futures are once again higher on the same regurgitated “news”, this time courtesy of the WSJ, that the US and China are “In the final stages of completing a trade deal.” If Phil Connors had the distinct displeasure of covering geopolitics for the past 3 months, his report today would be that presidents Trump and Xi Jinping “might” seal a formal trade deal around March 27, as the two countries appear close to a deal that would roll back U.S. tariffs on at least $200 billion worth of Chinese goods. The proposed trade deal would require Beijing to follow through on pledges ranging from better protecting intellectual-property rights to buying a significant amount of American products, including 50 million liters of Jack Daniels whiskey.

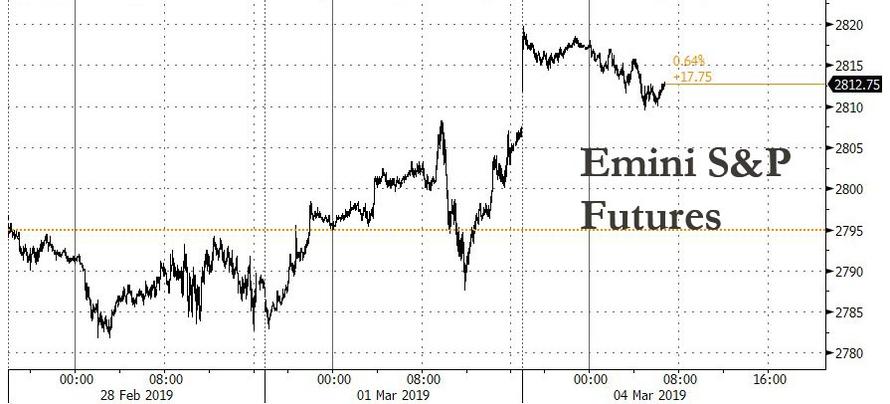

And Phil would be suicidal to see the same old market reaction as global stocks rose on the news, with European markets following their Asian counterparts higher. Asia’s MSCI ex Japan index was up 0.2%, Europe’s STOXX 600 index was up 0.4%, while the E-Mini was 0.3% higher…

… however much of the early burst higher faded with Eminis losing half of the initial euphoria …

… as even the algos appear to be growing bored with the now daily ruse, and the key outstanding question is whether all of the upcoming “trade deal” has now been priced in.

Actually, according to Lukman Otunuga, research analyst at FXTM, there was another question: “The key question is – will all tariffs will be removed instantly, or will they be gradually dialled back?” wrote “While the renewed risk appetite is seen boosting European and U.S. stocks, investors should consider how much upside is left, given that markets have been actively pricing in the possible resolution to the trade saga.”

Questions or not, the news was enough to reverse any lingering doubts about ongoing trade talk progress and MSCI’s All Country World Index was up 0.1% on the day, as the S&P500 is rapidly approaching its all time highs again.

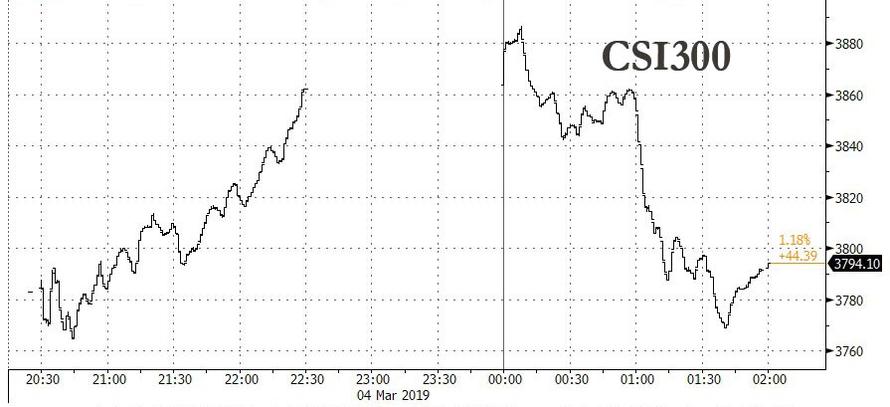

In Asia, Chinese shares were the biggest gainers, with the blue-chip index up as much as 3 percent, before however losing much of the overnight gains. The CSI300 index rallied last week after index provider MSCI quadrupled its weighting for mainland shares in its global benchmarks.

Elsewhere, Australian shares rose 0.4 percent and Hong Kong’s Hang Seng index added 0.7 percent. That left MSCI’s index of Asia-Pac shares ex Japan higher 0.2% on the day, and up almost 10% so far this year. Japan’s Nikkei strengthened more than 1 percent.

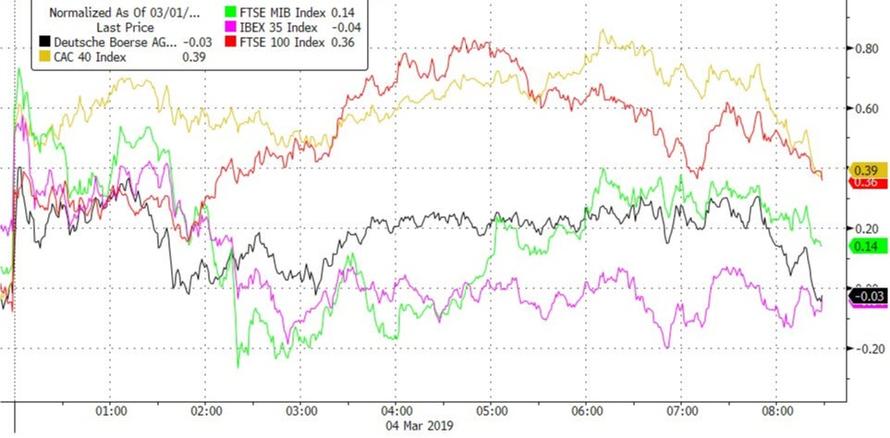

In Europe, gains in miners and media companies led the Stoxx Europe 600 Index to five-month high.

One possible reason for the fizzling euphoria is that the dollar jumped higher overnight even after U.S. President Donald Trump warned against it becoming too strong.

Despite the market’s enthusiasm, not everyone was fooled: “while we have all these great headlines about what could be achieved under a U.S.-China trade agreement, we’re still a little way away,” said Kerry Craig, JP Morgan’s global market strategist. “There could be a chance for a disappointment. It could be phased in over a number of years. There’s still questions about how and what China will actually buy to try and reduce their deficit.”

Sure, but for now, as for the past 10 consecutive weeks of upside, the algos are buying first and aksing questions later, if at all.

Meanwhile, in addition to the daily trade talk, the market will keep focused on several other key developments as well: China’s annual National People’s Congress may yield policy clues when it kicks off on Tuesday and investors will get the latest read on the U.S. economy with the monthly jobs report on Friday.

“While it will take time for economic data to stabilise from the current slowdown, policy shifts by central banks and governments, especially in the U.S. and China, should help support investor confidence for now,” said Tai Hui, Asia-Pacific chief market strategist at JPMorgan Asset Management.

In FX, the dollar recovered from an earlier slump that was fueled by President Donald Trump’s renewed criticism of Fed Chairman Jerome Powell and complaint about the greenback’s strength. The dollar reached a session high in early London trading while Treasury yields were little changed after reversing an earlier climb; the euro reversed gains on cross selling versus the yen and the pound. Earlier, turozone Sentix investor confidence rose to -2.2 in March, vs -3.1 estimate and -3.7 in February.

The pound led gains among major currencies after the Sunday Times reported that Pro- Brexit hardliners in May’s Conservative party have outlined conditions for supporting her plan; the sterling trimmed gains after construction PMI fell to 49.5 vs 50.6 in January and estimated 50.5. Meanwhile, the Aussie and kiwi retreated from early highs; poor economic Australian data over company profits and inventories sparked concern over growth data due later in the week; both currencies earlier advanced on hopes of a potential U.S.-China trade deal.

Greece’s benchmark 10-year government bond yields dropped to their lowest since 2006 on Monday after Moody’s raised its rating late last week, bolstering investor optimism towards the euro zone’s most indebted country. Moody’s on Friday lifted Greece’s issuer ratings to B1 from B3, citing the effectiveness of the country’s reform programme.

Looking ahead, March is expected to be a crucial month for global markets. Britain’s parliament will vote on an agreement to leave the European Union, the U.S. Federal Reserve will hold a policy meeting that could yield clues on its plans for interest rates and balance sheet reduction, and the European Central Bank will hold its scheduled policy meeting this week.

Elsewhere, oil prices gained on Monday with Brent (+0.7%) and WTI (+0.9%) benefitting from the positive trade sentiment following reports that US and China are in the final stages of completing a trade deal, alongside China’s spokesperson Zhang stating that substantial progress has been made. Adding to the upside is Friday’s Baker Hughes rig count where US oil rigs fell by 10 to 843, the lowest level since May 2018. Elsewhere, Russian oil output was 11.34mln BPD in February, 75k barrels below the October baseline level; according to Energy Ministry Data. Separately, Barclays have maintained their Brent price forecast, stating that prices have moved in-line with their view however Barclays does note that downside risks remain.

Gold (-0.4%) prices are weaker weighed on by the positive risk sentiment, with the yellow metal trading towards the bottom of a USD 10/oz range. Elsewhere, Vale have, on a temporary basis, removed its Chief Executive Schvartsman, along side 3 other executives following recommendations by both state and federal prosecutors. Elsewhere, nickel futures, which is used to make stainless steel, have climbed to around a 5-month peak, as the price of stainless steel continues to rise with Chinese steel mills actively replenishing their stocks in-spite of the rising prices; although some mills have been delaying purchases due to the price increase.

It’s a quiet day otherwise, with only construction spending data due, while Salesforce.com is scheduled to report earnings

Market Snapshot

- S&P 500 futures up 0.3% to 2,814.00

- MXAP up 0.4% to 159.69

- MXAPJ up 0.2% to 525.32

- Nikkei up 1% to 21,822.04

- Topix up 0.7% to 1,627.59

- Hang Seng Index up 0.5% to 28,959.59

- Shanghai Composite up 1.1% to 3,027.58

- Sensex up 0.6% to 36,063.81

- Australia S&P/ASX 200 up 0.4% to 6,217.41

- Kospi down 0.2% to 2,190.66

- STOXX Europe 600 up 0.4% to 375.83

- German 10Y yield unchanged at 0.183%

- Euro down 0.2% to $1.1345

- Brent Futures up 1% to $65.70/bbl

- Italian 10Y yield fell 1.8 bps to 2.375%

- Spanish 10Y yield rose 1.1 bps to 1.208%

- Brent Futures up 1% to $65.70/bbl

- Gold spot down 0.5% to $1,287.03

- U.S. Dollar Index unchanged at 96.53

Top Overnight News

- The U.S. and China are close to a trade deal that could lift most or all U.S. tariffs as long as Beijing follows through on pledges ranging from better protecting intellectual-property rights to buying a significant amount of American products, two people familiar with the talks said

- Substantial progress was made in the U.S. trade talks, China National People’s Congress spokesman Zhang Yesui says before legislative meetings

- Prime Minister May received a boost over the weekend as she prepares to return her Brexit deal to Parliament. Pro-Brexit hardliners in her Conservative Party outlined conditions for supporting her plan, the Sunday Times said. Theresa May is promising a 1.6b pound boost for poorer areas of the U.K. as she steps up efforts to get her Brexit deal over the line. The Stronger Towns Fund was immediately attacked as an attempt by the prime minister to “buy” the support of opposition politicians

- China’s political leaders gather this week to detail policy priorities for the year, with deliberations under added pressure from the trade standoff with the U.S. and a domestic economic slowdown.

- Hedge funds increased wagers on rising Brent crude prices for an eighth week, the longest streak since 2012, according to ICE Futures Europe data

- The House Judiciary Committee plans to issue document requests to more than 60 people on Monday as investigations begin into obstruction of justice, corruption and abuse of power related to President Trump, Chairman Jerrold Nadler said

- China is planning to cut the value-added tax rate that covers the manufacturing sector by 3 percentage points as part of measures to support the slowing economy, a person familiar with the matter said

- President Donald Trump’s attempts to blame Federal Reserve Chairman Jerome Powell for any hiccups in the U.S. economy have made a comeback — this time directed at his conservative base as he gears up for a tough 2020 re-election campaign

- House Judiciary Chairman Jerrold Nadler said he’s aggressively investigating whether there’s evidence of wrongdoing by President Donald Trump, thrusting the veteran New York City lawmaker into center of a politically risky probe

- The Swiss National Bank racked up a 14.9 billion- franc ($14.9 billion) loss for 2018 as the global stock market rout eroded the value of its foreign-currency holdings

Asian equities were higher across the board amid trade-optimism after WSJ noted that a US-Sino trade deal is reportedly being finalised and may be signed during a Trump-Xi Summit at the end of March. On Friday, US equities rose amid the overall risk appetite wherein the S&P closed above the 2800 level for the first time since November last year. The Dow closed above 26000 as Nike and Chevron led the gains, whilst Nasdaq advanced due to outperformance in heavyweight Amazon. ASX 200 (+0.4%) was led by the outperformance in the IT sector alongside a strong performance in material names, whilst Nikkei 225 (+1.0%) was lifted by its heavy China-exposed machinery sector and a marginally weaker domestic currency. Elsewhere, Shanghai Comp. (+1.2%) was the marked outperformer and breached the key 3000 level to the upside with all sectors firmly in the green ahead of the China National People’s Congress coupled with reports of optimistic trade developments. Meanwhile, Hang Seng (+0.5%) posted modest gains but initially failed to piggy-back on the same momentum as its mainland peers as the heavy-weight financial and energy names weighed on the index. Huawei are said to be preparing to sue the US government for banning federal agencies from using their products. Prior to this, Huawei CFO Meng Wanzhou has sued the Canadian government, police and border officials, claiming her legal rights were violated. Elsewhere, the UK could cap the use of Huawei equipment following the UK government’s review of the company; according to FT citing sources

Top Asian News

- South Korea, U.S. Decide to End Biggest Joint Military Exercises

- China, Malaysia Sign $891 Million of Palm Oil Purchase Deals

- China Copper Premium Falls to 22-Month Low as Stockpiles Expand

Major European indices are off best levels [Euro Stoxx 50 +0.2%], continuing from a strong overnight session where Shanghai Comp breached 3000 to the upside. Although, there is some slight underperformance in the DAX (U/C) which is weighed on by Fresenius Medical Care (-2.3%) after US President Trump’s administration have stated they are looking at value based pricing to promote home dialysis and kidney transplants, designed to spur innovation and decrease in-clinic dialysis; with the market currently dominated by the Co. and US Company DaVita, who are down by around 2% in the pre-market. Sectors are similarly in positive territory; however, the healthcare sector is largely unchanged with sentiment capped by the aforementioned performance of Fresenius Medical Care, along with Novarits (-2.5%) who in spite of their positive update regarding psoriasis are in the red as they are trading ex-dividends today. Other notable movers include, British American Tobacco (+0.5%) who opened down by just under 2% following a class action lawsuit against the Co’s Canadian unit. Elsewhere, Casino (-1.6%) are in the red after being downgraded at Societe Generale. Towards the top of the Stoxx 600 are Daily Mail (+4.9%) after the Co. stated they are offloading their GBP 900mln stake in Euromoney, with funds to be returned to shareholders. Separately, Julius Baer (+0.9%) are up after the Co. increased their stake in NSC Asesores by 30% to 70% for an undisclosed amount.

Top European News

- Ted Baker CEO Kelvin Resigns After Misconduct Allegations

- VW Straddles Old and New With Electric Buggy, Passat Face-off

- Bill Gross Sees ‘Much Less’ Alpha in Era of QE and Quant Trading

- U.K. Construction Contracts as Brexit Delays Building Projects

In FX, The Dollar is somewhat mixed vs its major counterparts, but the DXY recovered from another US President Trump set-back to revisit 96.600 and marginally eclipse tech resistance (96.594 Fib) on the way. However, latest encouraging reports on US-China trade, suggesting a deal is in the offing have hampered the Greenback to an extent, especially vs more risk-sensitive and high beta currency peers.

- GBP – The Pound has shrugged off an unexpected fall in UK construction PMI through the 50 growth/contraction threshold, and instead remains supported at the top of the G10 table on the more positive Brexit-related news in the form of growing support for PM May’s Withdrawal Agreement among the more ardent Tory leaver ranks, albeit with set conditions. Indeed, Cable remains close to 1.3250 and Eur/Gbp has retreated from highs around 0.8600, though the latter partly due to relative weakness in the single currency. Note, however, a hefty 1 bn option expiry at the 0.8500 strike looks too distant to come into play today as the cross hovers near 0.8560.

- EUR – As noted above, an underperformer amidst broadly risk-on trade at the start of the new week, with stops noted vs the Usd on a break of 1.1350 once last Friday’s low was breached taking the headline pair down to 1.1335. Similarly, sell orders are said to have been triggered in Eur/Jpy, possibly through 127.00 and in Eur/Gbp, but the single currency has pared some lost ground in wake of a more upbeat than forecast Sentix index.

- CHF/JPY – A bit of divergence between the traditional safe-havens, as the Franc remains below parity vs the Greenback on the aforementioned positive US-China paper talk, but the Jpy rebounds from worst levels circa 112.00, perhaps with the aid of those Eur cross sales, to sit just off 111.73 highs.

- NZD/AUD/CAD – The Antipodean Dollars are off best levels achieved overnight when the WSJ trade deal between Beijing and Washington near to completion report broke, but still underpinned as the Kiwi keeps its head above 0.6800 and Aussie hovers just below 0.7100. However, Aud/Nzd has slipped back towards 1.0400 in wake of some disappointing pre-RBA data in the form of Gross Company Profits and the Loonie is still underperforming circa 1.3300 lows following last Friday’s sub-consensus Canadian GDP release in the run up to the BoC.

- EM – The Lira and Peso are under pressure vs the Buck on bearish specific/independent impulses, as softer than expected Turkish CPI could prompt the CBRT to tweak its tight monetary stance on Wednesday, or even shift guidance in preparation for an ease ahead, while the Mxn is clearly feeling the adverse effects of S&P’s move to credit watch negative from stable. Note, Usd/Try is currently around 5.3850 vs almost 5.4000 at one stage and Usd/Mxn circa 19.3500 vs 19.3820 earlier, while in stark contrast the Thai Central Bank has been forced to curb excess Thb strength with a 31.75-85 range.

Brent (+0.7%) and WTI (+0.9%) are benefitting from the positive trade sentiment following reports that US and China are in the final stages of completing a trade deal, alongside China’s spokesperson Zhang stating that substantial progress has been made. Adding to the upside is Friday’s Baker Hughes rig count where US oil rigs fell by 10 to 843, the lowest level since May 2018. Elsewhere, Russian oil output was 11.34mln BPD in February, 75k barrels below the October baseline level; according to Energy Ministry Data. Separately, Barclays have maintained their Brent price forecast, stating that prices have moved in-line with their view however Barclays does note that downside risks remain. Gold (-0.4%) prices are weaker weighed on by the positive risk sentiment, with the yellow metal trading towards the bottom of a USD 10/oz range. Elsewhere, Vale have, on a temporary basis, removed its Chief Executive Schvartsman, along side 3 other executives following recommendations by both state and federal prosecutors. Elsewhere, nickel futures, which is used to make stainless steel, have climbed to around a 5-month peak, as the price of stainless steel continues to rise with Chinese steel mills actively replenishing their stocks in-spite of the rising prices; although some mills have been delaying purchases due to the price increase.

US Event Calendar

- 10am: Construction Spending MoM, est. 0.2%, prior 0.8%

DB’s Jim Reid concludes the overnight wrap

Happy Monday. I’m so dazed I hardly know what day of the week it is. I’ve had the most virulent strain of man-flu imaginable and spent a lot of the weekend in bed drained and with a hacking cough. I wasn’t very popular at home as you can imagine. Bronte the dog has been so worried that every time I go to sleep somewhere she curls up next to me. It’s fair to say that my wife hasn’t replicated this.

If I live to see it, the highlight this week is likely to be the ECB meeting on Thursday. We’ll also see the start of China’s NPC (Tuesday – 15th March) and the latest employment report in the US (Friday). The final PMI revisions (Tuesday) are also likely to be closely watched and you never know when you’re going to get the next US/China trade headline.

Speaking of which, overnight the WSJ broke a story highlighting that the US and China are close to a trade deal that could lift most or all US tariffs as long as China follows through on its pledges ranging from better protecting intellectual-property rights to buying a significant amount of US products (increasing by $1.2tn over 6 years). Specifically, its being reported that China would buy $18bn in natural gas from Houston-based Cheniere Energy Inc. Elsewhere, the WSJ reported that the likely summit between President Trump and his Chinese counterpart Xi Jinping could happen around 27th March. The WSJ report added that China is offering to lower tariffs on US farm, chemical, auto and other products while pledging to speed up the timetable for removing foreign-ownership limitations on auto ventures, and to reduce tariffs on imported vehicles to below the current rate of 15%. China’s National People’s Congress spokesman Zhang Yesui also said that substantial progress has been made in trade talks before the start of legislative meetings. Meanwhile, after extending the deadline last week of a planned tariff increase on March 1, Trump has tweeted that “I have asked China to immediately remove all Tariffs on our agricultural products (including beef, pork, etc.) based on the fact that we are moving along nicely with Trade discussions….”

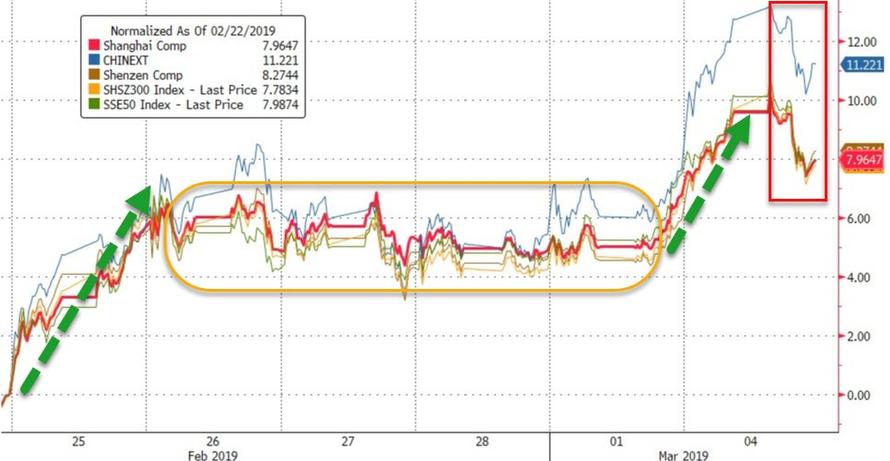

Sentiment has improved overnight on the positive trade headlines with China’s bourses leading the advance – the Shanghai Comp (+3.05%), CSI (+3.47%) and Shenzhen Comp (+3.95%) are all up. The Nikkei (+1.09%), Hang Seng (+1.22%), and Kospi (+0.09%) are also up. In the meantime, China’s onshore yuan is up +0.24%. Elsewhere, futures on the S&P 500 are +0.45% and in commodities, US futures on corn and soybeans are up +0.74% and +0.63%, respectively.

Also over the weekend, (per Bloomberg) Mr Trump commented on the Fed again saying that there is “a gentleman that likes raising interest rates in the Fed, we have a gentleman that loves quantitative tightening in the Fed, we have a gentleman that likes a very strong dollar in the Fed.” In response the dollar is (-0.11%) slightly weaker overnight and 10yr Treasuries are up +1.0bps. Sterling is also up +0.25% on incrementally more positive Brexit noises. See later for more details.

Now going back to the highlights of the week ahead. While no change in policy from the ECB is expected, we will get updated staff forecasts (which are likely to show downgraded growth forecasts) and perhaps further hints about TLTRO2. Recent ECB commentary and the accounts of the January ECB meeting clearly signal that addressing TLTRO2 maturity is on the agenda, although its not clear that a decision will come as soon as Thursday’s meeting. Nevertheless, it’s likely to be a topic of discussion. Our economists believe that at the very least, it is appropriate for the ECB to implement a TLTRO2 solution that allows net exposures to be rolled over. This would help the ECB to preserve its monetary policy stance and prevent a temporary economic slowdown from propagating through unnecessary deleveraging, especially in the periphery.

Also of significance for markets is China’s National People’s Congress which officially gets underway on Tuesday and runs through until March 15th. Premier Li will present the government’s draft working plan on Tuesday and the details of the government’s draft budget will come out on Wednesday. Throughout the 10 days we’re also expecting the PBoC and ministries to hold press conferences which may send important policy messages. Our China economists expect the Chinese government to keep the policy stance flexible at this stage without committing to aggressive loosening measures. On growth, our colleagues expect the government to lower the GDP growth target for 2019 to “above 6%” or “between 6% and 6.5%”, which would represent a downward revision from “around 6.5%”. They expect the official fiscal deficit target to be around 2.8% to 3.0% of GDP, up from 2.6% in 2018, and also for the government to announce a total of RMB 1.2-1.5tn of tax cuts. On monetary policy, the team expect the government to reiterate the “prudent” monetary policy stance and no change in policy stance to the property sector.

Meanwhile, the big data highlight next week comes on Friday when we get the February employment report in the US. The consensus is for another solid round of data. Expectations for payrolls is 185k which as a reminder follows a much stronger than expected 304k print in January. Earnings are expected to have risen +0.3% mom which if true, would likely push the annual rate up one-tenth to +3.3% yoy and so matching the highs from the end of last year. The unemployment rate is expected to fall a tenth to 3.9% and hours hold at 34.5 hours.

Away from that, other data worth flagging in the US includes the final February PMIs and ISM non-manufacturing (+0.5pts to 57.2 expected) on Tuesday, the February ADP report on Wednesday, claims on Thursday and housing starts and building permits on Friday. In Europe, the highlight is the final February PMIs on Tuesday. We’ve already had the flash readings and as a reminder that the services and composite readings for the Euro Area were 52.3 and 51.4 respectively. Expect the main focus to be with Italy and France though where both services readings are hovering below 50. Other than that, we’ll also get the final Q4 GDP reading for the Euro Area on Thursday prior to the ECB meeting. No change from the +0.2% qoq/+1.2% preliminary readings are expected. Finally in Asia we’ve got the February PMIs in Japan and China on Tuesday, and China trade data on Friday. The rest of the day by day week ahead is at the end.

Recapping last week now. On Friday, attention was dominated by trade negotiations and communications from central banks. Equities rallied with the S&P 500, DOW, and NASDAQ ending the week +0.62%, +0.57%, and +0.74% (+0.64%, +0.70%, and +0.91% on Friday), respectively. In Europe, the STOXX 600 gained +0.62% (+0.22% Friday), with the DAX outperforming, up +1.40% (+0.30% Friday). Commodities rallied as well, with Brent crude oil advancing +1.15% (-0.09% Friday) and copper posting its best week since last September to reach its highest level since last June, gaining +5.40% (+1.81% Friday). Basically markets exposed to China did well as the Shanghai Comp. climbed +6.77% on the week and 1.80% on Friday. The offshore yuan appreciated +0.91% on the week (+0.21% Friday) to reach its strongest level since last July.

One of the most important moves last week were the rising yields. 10 year Treasuries, Bunds, Gilts rose 9bp, 7.4bp and 12.3bps respectively on the week but rallied off the yield highs on Friday on disappointing US data led by the manufacturing PMI declining 2.4 points to 54.2 vs 55.8 expected. The reason Gilts rose as much as they did is that the threat of a no-deal Brexit on March 29th seems to have been reduced to close to zero. The chances of Mrs May’s deal being passed before that seem to be increasing as the weekend press disclosed the terms that the ERG would require to support the deal. It does seem that their demands suggest a desire to compromise but all depends on how legally tight any agreement between the U.K. and EU over the temporary nature of the backstop can be. Expect numerous headlines on this this week.

Quickly recapping Friday’s central bank speak. Banque de France Governor Villeroy mentioned that the ECB should “study pragmatically how to contain possible adverse effects on the bank transmission of our monetary policy”. That mirrored earlier comments from the BoJ Governor Kuroda, who said that any future easing would come via tools that have the “least side-effects”. These could be references to some alleviation of the harm from negative interest rates. In the US, many Fed speakers spoke at a conference in New York, including Vice Chair Clarida who said that yield curve control, where 10-year yields are pegged, is one potential option to fight a future recession. The Fed will conduct a thorough review of its policy framework later this year.

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 33.57 POINTS OR 1.12% //Hang Sang CLOSED UP 147.42 POINTS OR 0.51% /The Nikkei closed UP 219.35 POINTS OR 1.02%/ Australia’s all ordinaires CLOSED UP 0.46%

/Chinese yuan (ONSHORE) closed UP at 6.7018 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.09 dollars per barrel for WTI and 65.50 for Brent. Stocks in Europe OPENED GREEN EXCEPT SPAIN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7018 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7025: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/

The battle over Huawei is getting fierce. Now Huawei fights back and sues the uSA government in a Texas court over equipment ban

(courtesy zerohedge)

Huawei Sues US Government In Texas Court Over Equipment Ban

According to the latest batch of market-positive trade-deal headlines, US negotiators are scrambling to hash out a deal with their counterparts in Beijing that would enable Trump and President Xi to save face, while averting the next round of US tariffs (and possibly removing existing tariffs) – even if this means squandering the leverage Trump has accrued by backing the Chinese economy into a corner.

But amid the rush to finish a deal by the end of the month, the battle of wills between Chinese telecoms giant Huawei and the US government rages on. And in what appears to be its latest salvo, Huawei is reportedly suing the US government over its ban on federal agencies purchasing Huawei products, which it argues is illegal under US law.

According to the NYT, which was tipped off about the suit by two sources close to Huawei, the Chinese firm is planning to file in the Eastern District of Texas, where its American headquarters is based:

SHANGHAI – The Chinese electronics giant Huawei is preparing to sue the United States government for banning federal agencies from using the company’s products, according to two people familiar with the matter.

The lawsuit is due to be filed in the Eastern District of Texas, where Huawei has its American headquarters, according to the people, who requested anonymity to discuss confidential plans. The company plans to announce the suit later this week.

While the legal precedents are stacked against Huawei, reversing the ban probably isn’t the lawsuit’s ultimate goal; rather, according to the Times, the company is hoping to force the White House to “more publicly make its case against the Chinese equipment maker.” The suit is part of a multi-pronged approach by the company to defend its reputation from aspersions cast by the US.

The move could be aimed at forcing the United States government to more publicly make its case against the Chinese equipment maker. It is part of a broad push by Huawei to defend itself against a campaign led by the United States to undermine the company, which Washington sees as a security threat. Executives have spoken out strongly against America’s actions, and new marketing campaigns have been aimed at mending the company’s image among consumers.

For many years, United States officials have said that Huawei’s telecommunication equipment could be used by Beijing to spy and disrupt communication networks. The company has denied the allegations, but major wireless carriers such as AT&T and Verizon have effectively been prevented from using Huawei’s equipment as a result.

Mirroring a strategy employed by Russian security firm Kaspersky Labs after the federal government ordered agencies to uninstall Kaspersky’s software over fears it was being used to spy on the federal government, Huawei’s lawyers are expected to argue that a defense spending authorization law passed last year was tantamount to a “bill of attainder” – legislation that unfairly singles out a person or group.

The lawsuit that Huawei is preparing to file in the United States is expected to challenge a section of a defense spending authorization law that was approved last year. The provision blocks executive agencies from using telecom equipment made by Huawei and another Chinese company, ZTE.

According to one of the people familiar with the matter, Huawei’s lawsuit is likely to argue that the provision is a “bill of attainder,” or a legislative act that singles out a person or group for punishment without trial. The Constitution forbids Congress from passing such bills.

The United States Embassy in Beijing did not immediately respond to a request for comment. A call placed outside business hours to the United States Courthouse in Plano, Tex., where Huawei’s American headquarters are located, was not answered.

Huawei executives have argued that the US’s campaign to encourage its western allies to ban or put up barriers preventing Huawei technology from being used in the construction of their 5G wireless networks was motivated not by security concerns, like the US has maintained, but by commercial interests. The US wants 5G technology developed by Verizon and other US providers to form the backbone of 5G, not Huawei. However, the fact that many of the US’s allies have refused to go along with this has demonstrated that Huawei’s market leading technology is simply too valuable.

And as Huawei ramps up its legal efforts in the US (as criminal proceedings alleging IP theft have started in a Seattle courtroom), CFO Meng Wanzhou is suing the Canadian government and the officers who arrested her for violating the Canadian Charter of Rights and Freedoms, Reuters reports.

In a civil lawsuit filed in the British Columbia Supreme Court on Friday, Meng’s lawyers said the manner in which officers obtained evidence and information from Meng constituted serious violations of the Canadian Charter of Rights and Freedoms. Meng is the daughter of Huawei’s founder.

It added that Canadian Border Services Agency (CBSA) officers deliberately delayed the immediate execution of an arrest warrant and unlawfully subjected Meng to detention, search and interrogation to extract evidence from her before she was arrested.

[…]

The lawsuit further alleged that Meng was directed to surrender all her electronic devices, computers and passwords and that CBSA officers then unlawfully opened and viewed the contents of the seized devices in violation of her right to privacy.

CBSA officers also searched Meng’s luggage in violation of the right to privacy, the lawsuit said. “The CBSA Officers knew or were recklessly indifferent to the fact that they had no authority to conduct such a search, which search was performed under the false pretense of a routine customs or immigration related examination,”according to the lawsuit.

While any failure to secure a trade deal with China would certainly be embarrassing for Trump, a series of losses in Western courts to Huawei would not only be embarrassing, but seriously undermine the US’s efforts to muscle out Huawei and establish American firms as the dominant global force in 5G.

end

Getting quite nasty: Beijing threatens jailed Canadians with espionage charges in the latest retaliation for sending the Huawei case forward, i.e. the extradition of Meng

(courtesy zerohedge)

Beijing Threatens Jailed Canadians With Espionage Charges In Latest Retaliation For Huawei CFO’s Arrest

Beijing has fired off its latest threatening message to Ottawa on Monday, just days after the Canadian Justice Ministry decided to allow extradition hearings for Huawei CFO Meng Wanzhou to move forward.

With Meng set to make her first court appearance during the extradition proceedings later this week, two Chinese media reports published Monday claimed that jailed Canadian nationals Michael Kovrig – a former diplomat – and Michael Spavor – a businessman who arranged tours to North Korea – would face charges of spying on Beijing. Earlier, Chinese officials had said only that the two men faced charges related to threatening national security, which allowed Chinese authorities to immediately imprison the two men while an investigation was still underway.

The reports, which were summarized by the Financial Times, claimed that Spavor, who is being held in isolation in Liaoning, “provided intelligence to Kovrig and was an important intelligence contact of Kovrig.” One Chinese media personality said the reports suggest that Kovrig was the primary target in the crackdown, and that he was responsible for stealing state secrets.

Wei Du 杜唯@WeiDuCNA

Wei Du 杜唯@WeiDuCNAChinese state media reporting “major breakthrough” in case against Canadian @MichaelKovrig. Website linked to party law enforcement agency says Michael Spavor, the other Canadian in Chinese custody, was an informant to Kovrig.

Luna Lin@LunaLinCNStealing state secrets?

Wei Du 杜唯@WeiDuCNAThough Spavor’s work was mostly linked to North Korean, the report alleges that Kovrig stole state secrets, assumably Chinese ones. Also the way it’s written makes you think Kovrig is the main target here.

While the charges haven’t been officially filed, the message to Ottawa is clear: Kovrig and Spavor could face the death penalty if found guilty, just like a third Canadian national who late last year saw his sentence for drug trafficking modified from a 15 year prison term to the death penalty.

Unlike Spavor and Kovrig, who have been kept in solitary confinement, denied books sent by friends and allowed only a single consular visit per month, Meng has been under house arrest in her sprawling Vancouver home.

Meng’s extradition must now be decided by Canadian courts, a process that could take months or even years. Meanwhile, her lawyers have sued Canada over alleged civil-rights violations from when she was detained in Vancouver on Dec. 1.

The following is a very important article on how demographics are starting to eat into China’s economy. As the debt rises, the population shrinks and thus greater debt per GDP. Also the shortage of labour is causing costs to rise further hurting their economy

(courtesy zerohedge)

China’s Employed Population Shrinks For The First Time Ever

China’s imminent, and historic conversion from a current account surplus to deficit nation is not the only “tectonic shift” taking place in the world’s most populous nation. According to the latest census data from its National Bureau of Services, China’s employed population has shrunk for the first time ever on record, and at the end of 2018, the number of people employed fell to 776 million, a drop of 540,000 from 2017.

Meanwhile, in yet another sign that China’s population is aging rapidly, the broader working-age population, or people between the ages of 16 and 59, also shrank for the seventh consecutive year, down a total of 2.8% from 2011 to 2018 according to Caixing. Last year’s China’s total working-age population stood at 897 million, down 5 million from 902 million in 2017, according to the NBS.

Li Xiru, director of the Population and Employment Department at NBS, warned last month that the employed population would further drop in the coming years.

While China is already beset with a myriad of economic and asset price bubbles, most notably a massive corporate debt load and a still gargantuan shadow banking system both of which it has to balance against an unprecedented housing bubble to avoid a collapse in the financial system sparking a “working class insurrection“, the country’s shrinking work force creates even more headaches for officials as it pushes up labor costs, sparking inflationary pressures and placing more strains on an economy already struggling against external headwinds.

As China Daily reported recently, the shortage of workforce means labor cost will continue to increase and industrial transfer and technology will substitute workers. And since university graduates – who expect far higher wages – account for nearly half of the labor force entering the market, the market is unable to provide traditional industries with the required number of workforce and the past high-input economic development mode is unsustainable.

The futures is even bleaker: the working-age population is expected to see a sharp drop from 830 million in 2030 to 700 million in 2050 at a declining speed of 7.6 million every year, said Li Zhong, a spokesman for the Ministry of Human Resources and Social Security, in July. Meanwhile, with decreasing supply of labor force, the salary of all industries grew at a rate of 11.3 percent in 2011, 10.5 percent in 2012, and 9.7 percent in 2013, said Zeng, adding that as a result many foreign enterprises left China and shifted to Southeast China due to rising labor cost.

Adding to the warnings, back in 2015, the World bank cautioned that China’s working age population will fall more than 10% by 2040 in spite of a recent relaxation of its one child policy, heightening the risk of the world’s most populous country “getting old before getting rich”.

A further decline of 10% would equate to a net loss of 90 million Chinese workers, a number greater than the population of Germany, and is consistent with demographic pressures across East Asia. The working populations of South Korea, Thailand and Japan are also expected to fall by 10 per cent or more over the next 25 years.

“East Asia has undergone the most dramatic demographic transition we have ever seen,” said Axel van Trotsenburg, World Bank regional vice-president. “All developing countries in the region risk getting old before getting rich.”

As of 2010, almost 40% of all people on the planet aged 65 or older — some 211 million individuals — lived in East Asia, and the World Bank estimates that a least a dozen East Asian countries will see the percentage of their populations aged 65 or higher double to 14 per cent in a quarter century or less. In France and the US, the same transformation took 115 and 69 years respectively

“As [countries] get richer, fertility falls,” said Philip O’Keefe, lead author of the World Bank report. “Given China’s current fertility [rates], you may get a temporary uptick in people who wanted to have a second child having one, but we don’t see a big long-term impact there.”

O’Keefe cited surveys showing that only a quarter of Chinese people eligible to have a second child would in fact do so, however according to recent data, despite China’s relaxation of the infamous “one-child policy”, local birth rates have remained stagnant and in fact, in 2018 China’s birth rate dropped to a new record low.